Data Fusion for Joining Income and Consumption Information Using Different Donor-Recipient Distance Metrics

Abstract.

Data fusion describes the method of combining data from (at least) two initially independent data sources to allow for joint analysis of variables which are not jointly observed. The fundamental idea is to base inference on identifying assumptions, and on common variables which provide information that is jointly observed in all the data sources. A popular class of methods dealing with this particular missing-data problem is based on nearest neighbour matching. However, exact matches become unlikely with increasing common information, and the specification of the distance function can influence the results of the data fusion. In this paper we compare two different approaches of nearest neighbour hot deck matching: One, Random Hot Deck, is a variant of the covariate-based matching methods which was proposed by Eurostat, and can be considered as a ’classical’ statistical matching method, whereas the alternative approach is based on Predictive Mean Matching. We discuss results from a simulation study to investigate benefits and potential drawbacks of both variants, and our findings suggest that Predictive Mean Matching tends to outperform Random Hot Deck.

Key words and phrases:

Statistical Matching, Missing Data, Predictive Mean Matching, Nearest Neighbour Imputation, Missing-By-Design Pattern1. Introduction

Data fusion, also known as statistical matching, is a perfect example of secondary data analysis. The objective of a data fusion is to jointly analyse variables from (at least) two different data sources which were not jointly observed, and each of the data sources originally served a different purpose.

The studies of the National Statistical Institutes (NSIs) are often committed to a particular objective such as measuring, e.g. consumption expenditure of private households, in great detail. If the need arises to incorporate and combine information from several objectives, data fusion is a standard mean to provide a microdata source, where these different types of information are artificially joined on an individual or household level.

In 2009, the Stiglitz-Sen-Fitoussi commission (Stiglitz et al. 2009) published a report on welfare and its components, which led to various approaches among NSIs within the European Union to measure the dimensions ’income’, ’consumption’ and ’wealth’ (ICW) as proposed by the commission. Countries which do not measure all three dimensions within a single official statistics data source have been exploring data fusion methods in order to provide a corresponding data base (see e.g. Donatiello et al. 2014; Uçar & Betti 2016; Albayrak & Masterson 2017; Dalla Chiara et al. 2019). The proposed data fusion methods are largely based on the research conducted by the European Statistical Office (Eurostat) (Lamarche 2018)111This paper is currently under review and, therefore, unpublished yet. A preliminary and freely accessible version of this paper is Lamarche (2017). and several NSIs (see e.g. D’Orazio et al. 2018) on statistically matching data from EU-SILC with data from the Household Budget Survey (HBS). By matching EU-SILC and HBS, Eurostat and the NSIs pursue the goal to provide joint information about the household income details observed from EU-SILC and the household consumption expenditures observed from HBS. The original focus of their analyses had been on preserving marginal distributions and one of the preliminary findings is that Random Hot Deck (RHD), a classical nearest neighbour matching technique, performs very good in terms of preserving marginal distributions (Webber & Tonkin 2013; Serafino & Tonkin 2017; Lamarche 2018). However, the preservation of marginal distributions does not give any hint about whether the joint distributions of the variables not jointly observed, income and consumption expenditures in our case, is adequately reproduced in the matched data file.

Our research connects by extending the analysis objective to investigating associations between different variables, and we will explain in the following, why RHD yields good results for marginal distributions, but not necessarily for conditional or joint distributions. We investigate the properties of an imputation method called Predictive Mean Matching (PMM) (Rubin 1986) which was extended by Little (1988) to multivariate data situations (which is a typical scenario for data fusion settings). While both, RHD and PMM, are based on nearest neighbour hot deck matching, the underlying principles are very different, as RHD matches on the combined distances of the covariates, jointly observed in both studies, whereas PMM matches on the combined distances of model-based predictions of the variables which are observed in only one of the two studies. While these two methods do not exhaust the plethora of available nearest neighbour matching variants, they can be considered as archetypical for what we like to refer to as covariate-based matching and model-based matching. In order to discuss benefits and drawbacks of both data fusion archetypes, we compare the performance of Random Hot Deck and Predictive Mean Matching within a simulation study. As an extension to the research conducted by Eurostat and the NSIs, we focus on preserving joint distributions and associations between different variables, especially between the variables not jointly observed.

We focus in this paper on point estimators and descriptive statistics, and we therefore do not address incorporating uncertainty caused by the originally missing data, but extension to Multiple Imputation for multivariate PMM is straightforward (see e.g. Rubin 1986; Koller-Meinfelder 2009).

Nearest neighbour methods also spawn various other interesting research problems, such as balancing the usage of donors using constrained matching (see e.g. Rodgers 1984; Rubin 1986) or selecting donors from Nearest Neighbours (see e.g. Chen & Shao 2000; Andridge & Little 2010; Beretta & Santaniello 2016). For the sake of simplicity, we do not explicitly address these issues in the following, although the setup of our simulations could be extended accordingly.

To meet our objective of comparing the data fusion performance of RHD and PMM, we structure our paper as follows: Section 2 contains a general overview of data fusion, followed by an in-depth description of the two aforementioned algorithms in Section 3. We investigate the properties of RHD and PMM as data fusion methods within a simulation study based on Scientifc Use Files (SUFs) data from the EU-SILC study which we modify to mimic a data fusion situation. The setup of this stimulation study is described in Section 4 and we discuss the corresponding results in Section 5. We conclude the findings of our research in the final Section 6.

2. Methodological Aspects of Data Fusion Scenarios

In this section we introduce the basic notation used throughout this paper, and we introduce perspectives on data fusion from statistical literature as well as the practitioners’ perspective which often relies on the identification of ’statistical twins’ or nearest neighbours.

2.1. Theoretical Background

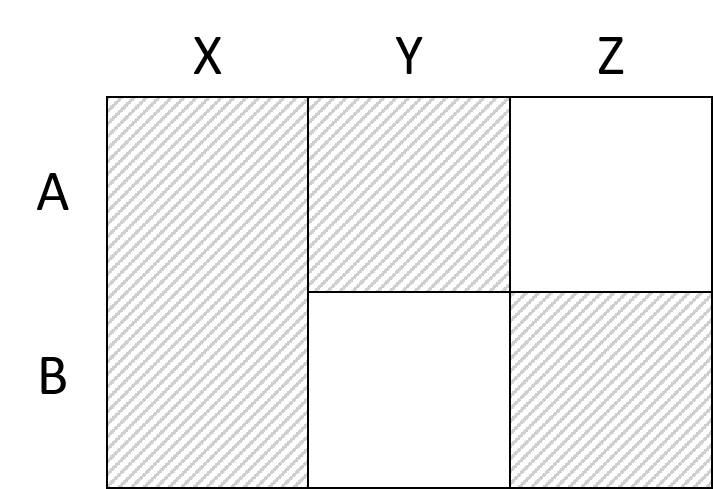

Following the suggestion by Rubin (1986) to consider data fusion as file concatenation leads to the particular missing-by-design pattern (see e.g. Rässler 2002, ch. 4), and Figure 1 displays this schematic pattern if we stack two originally independent data sources A and B. The blank parts are missing and the corresponding variables were initially not part of the particular study, i.e. variables are not observed in the first original study A (upper part of the stacked data set), and variables are not observed in the second original study B (lower part of the stacked data set). In this respect, we denote variables which are observed in both studies as in the following, and we further denote variables relevant for the analysis which are only part of study A (but unobserved in study B) as and, analogously, variables required for the analysis which are only observed in study B (but unobserved in study A) as .

A typical data fusion analysis objective is based on variables and , and from the schematic overview it is apparent that we need identifying assumptions for the joint distribution of . In most imputation variants, either fully parametric or matching-based, an implicit Conditional Independence Assumption (CIA) is made, which was first pointed out by Sims (1972) in a comment on a technical report (Okner 1972). It states that any association between and is a function of , i.e. and, analogously, . This, for instance, yields a correlation of zero between and if conditioned on . We will, however, not consider violations of distributional assumptions for as part of this research. Rodgers (1984) extensively discussed the shortcomings of the CIA within a comprehensive simulation study, but in recent years several publications have addressed this issue by proposing to introduce auxiliary information (Singh et al. 1993, see e.g.;Fosdick et al. 2016).

2.2. Implementation in Practice

Technically, we can apply any sophisticated method for handling missing data to this artificially created missing-by-design data situation, such as fully parametric multiple imputation or single imputation with variance correction, or Maximum Likelihood-based methods. The majority of empirical data fusions seem, however, to be based on some form of nearest neighbour matching (see e.g. Koschnick 1995; D’Orazio et al. 2006, ch. 2.4), and we assume that there are at least two reasons for it:

-

(1)

Nearest neighbour based imputation methods are often more robust to model misspecification than fully parametric methods (see e.g. Koller-Meinfelder 2009);

-

(2)

The synonymous term ’Statistical Matching’ already suggests matching-based methods to the practitioners as the most viable alternative.

Although the missing-data pattern displayed in Figure 1 suggests that both missing parts could be imputed within the new stacked data set, it is far more common that only one of the original studies is used for data fusion analysis. Staying true to the matching concept, this study is labeled the recipient study, whereas we refer to the study that ’donates’ data from its observations as the donor study (see e.g. Gabler 1997; van der Putten et al. 2002). This applies to the content-based aspect of this paper, where EU-SILC represents the recipient study that has to be extended by the missing consumption expenditures, while HBS donates the household consumption information and, therefore, serves as the donor study (see e.g. Serafino & Tonkin 2017). This implies that, referring to the missing-by-design pattern displayed in Figure 1, study A equals EU-SILC with the observed income variables and study B corresponds to the HBS with the observed consumption variables . The aim is to expand the EU-SILC data file by the household consumption expenditures, i.e. imputing the missing information in study A in order to provide a joint analysis of the income () and consumption () variables originally not jointly observed.

2.3. Overview of Traditional Data Fusion Algorithms

Traditionally, as already pointed out, data fusions are conducted using some form of covariate-based nearest neighbour matching methods (see e.g. Rodgers 1984; Koschnick 1995). These algorithms match data on observations that are as close as possible with regard to their common characteristics, i.e. by imputing the missing values in the recipient data file by the observed values of the most similar donor observation according to the common variables (see e.g. van der Putten et al. 2002; Kiesl & Rässler 2005). Usually, either a certain distance metric is applied that accounts for the different scale levels of , e.g. the distance proposed by Gower (1971), or all variables will be categorised such that (alleged exact) matches can be identified in both data files (D’Orazio et al. 2006, ch. 2.4). In the latter case, only zero distances between the variables are considered. In addition, however, there also exist fully parametric approaches. Such methods are based on regressions of on within the donor file and subsequently estimate the missing values in the recipient file by means of the computed regression parameters (see e.g. D’Orazio et al. 2006, ch. 2.2; Gilula et al. 2006).

While coviarate-based methods are non-parametric as they are not subject to distributional assumptions, PMM can be considered as mixed (or semi-parametric) methods between coviarate-based algorithms and fully parametric approaches. Note that Eurostat discusses different data fusion methods in previous working papers as well, and refers to semi-parametric algorithms as mixed methods between non-parametric and parametric approaches (Leulescu & Agafitei 2013; Webber & Tonkin 2013; Serafino & Tonkin 2017). However, their ’mixed methods’ are slightly different to the multivariate variant of PMM proposed by Little (1988), as they consider ranks to identify suitable matches.

Nearest neighbour methods, in general, can be applied as either ’unconstrained’ or ’constrained’ matching (Rodgers 1984; Rubin 1986). Unconstrained matching allows a donor observation to be matched with a recipient record multiple times, whereas constrained matching limits the use of a donor observation to a predefined integer, for example to one. We focus on the unconstrained version for both, RHD and PMM, in the following, as there are many other sources discussing and comparing the two alternatives (see e.g. Rässler 2002, p. 53-63; Kiesl & Rässler 2005).

3. Random Hot Deck and Predictive Mean Matching

In this section we will provide some details on the two methods, RHD and PMM, we want to compare within the subsequent Monte Carlo study, before we focus on describing the aforementioned differences of both methods in detail, and how these differences might affect the analysis results of our MC study.

3.1. Random Hot Deck (RHD)

In general, RHD randomly assigns observations from the donor file to observations of the recipient file. The missing values for each recipient record are then imputed by the corresponding values of its assigned donor observation. However, the random allocation between recipient and donor observations is usually carried out within homogeneous subgroups, for example only within the same gender category. Thus, in this example, female (male) donor observations can only be assigned to female (male) recipient observations (D’Orazio et al. 2006, ch. 2.4.1).

We also apply RHD within homogeneous subgroups analogously to Eurostat (2018) and Lamarche (2018). For any specific variable (with ) of stemming from the donor data file, the detailed fusion algorithm can be described as follows: First, in order to identify relevant matching classes that serve as homogeneous subgroups, all common variables that have a metric scale level are categorised. For example, age is transferred to rough age groups or income to income quintiles. Thus, all variables are at most ordinal scaled and only zero distances between the recipient and the donor observations are allowed. Subsequently, a stepwise selection based on OLS regression of on in the donor file is implemented in order to select common variables that have an acceptable explanatory power for . Along the stepwise-selected variables, an auxiliary variable is created that concatenates the respective values of for each observation in the recipient and the donor file. This results in a stratum characteristic for each donor and recipient record that form the homogeneous subgroups. The random assignment between the donor and the recipient observations is only conducted within the same stratum, i.e. every donor record is only permitted to be matched with a recipient record that has exactly the same (categorical) characteristics with respect to the stepwise-selected variables (Eurostat 2018; Lamarche 2018).

In order to ensure enough donor observations () compared to recipient records () for each stratum level , the following threshold is set:

where the constant is set as a rule of thumb to (see Lamarche 2018, p. 13). As long as 90% of the sample do not exceed this threshold,222In the case of equal sample sizes of the recipient and the donor data file, the threshold means that a maximum of three recipients can be assigned to one donor – for a maximum of 10 % of the recipients, a deviation from this threshold is allowed. the stepwise-selected variables are retained and the Random Hot Deck within each subgroup is performed. Otherwise, the process will be reiterated, with the maximum subset of the variables to be selected by the stepwise selection333The maximum subset of variables is controlled by the nvmax argument within the regsubsets() function from the leaps package (Lumley & Miller 2020). being reduced by 1 for each iteration step. If there are still recipients left who cannot be assigned to a donor, a second round of allocation is conducted with and without a tolerance specification (Eurostat 2018; Lamarche 2018).

3.2. Predictive Mean Matching (PMM)

Predictive Mean Matching is not frequently discussed as a dedicated data fusion method, but it has become popular as an imputation method in general, and is the default method for metric-scale variables in the R package mice (van Buuren 2020). The method was first introduced by Rubin (1986) and Little (1988) for the simultaneous imputation of continuous variables. The basic idea is that for each missing value its ’predictive mean’ (Little 1988, p. 291) based on regression (e.g. OLS) is compared with the predictive means of all observed values, and the predictive mean among the observed values with minimum distance serves as donor record, and its actually observed values is imputed (Rubin 1986; Little 1988).

The PMM algorithm for any specific variable () of is as follows: First, as with RHD, relevant variables are selected using a stepwise selection based on OLS regression of on . In contrast to RHD, all variables can remain on their original scale level, i.e. metric variables are not categorised (Meinfelder & Schnapp 2015). By means of the regression equation, which includes the stepwise-selected variables, the predictive mean is then calculated for each observation in the recipient and the donor file. The search for corresponding donor observations is now performed using the Mahalanobis distance function as proposed by Little (1988):

, where corresponds to the predictive mean of the -th observation from the recipient file and corresponds to the predictive mean of the -th observation from the donor file. denotes the inverse variance-covariance matrix of the residuals from the regression of on the stepwise selection subset of , by which the distance is weighted.

3.3. Conceptual Differences of the two Algorithms

Traditional co-variate-based nearest neighbour methods like Random Hot Deck assign per default equal weights to all variables, without taking into account the explanatory power or any other definition of relevance regarding the specific variables. Sometimes, as is the case with the considered implementation of the RHD algorithm, a regression-based stepwise selection of relevant variables precedes the distance computation. While the variables selected via the stepwise algorithm might be adequate predictors for the and variables to be matched, their explanatory power is unlikely to be equally high. Technically, any variable selection to identify ’suitable’ variables equates a weighting process, where weights for variables are either or . Although covariate-based methods like Random Hot Deck are widely used, the issue of unequal explanatory power of the common variables results in an optimization problem for identifying the ’best’ matches. PMM, on the other hand, addresses this optimization problem by weighting the distance computation with , i.e. the variance-covariance matrix of the residuals from . Therefore, the main difference of PMM compared to RHD is in the distance processing: Within RHD, every stepwise-selected variable has the same weight in finding those ’best’ matches within the recipient and donor files. The reasonable possibility that there exist selected variables that have a better explanatory power for than other common variables is ignored by RHD. PMM takes the unequal explanatory power of the selected variables into account, as the predictive means depend on the estimated regression parameters. Additionally, distances between predictive means are weighted with the inverse of the residual covariance matrix from the regressions of on . This means that the better some variable can be explained by the covariates , the more distances between predictive means of potential donors and recipients are penalized. This may indicate a more sophisticated distance processing in favour of PMM and, consequently, we expect PMM to result in a better fusion performance than the RHD method. Therefore we formulate the following hypothesis: Since Predictive Mean Matching provides a more precise distance processing, PMM leads to a better fusion result than RHD. The upcoming simulation study is designed to provide a differentiated and detailed scrutiny of this underlying hypothesis.

4. Simulation Design

Since the motivation for the present analysis is derived from the findings published by Eurostat (Webber & Tonkin 2013; Serafino & Tonkin 2017; Lamarche 2018), our aim for the data basis of the simulation study is to stay as close as possible to the relevant official statistics data sources.

With respect to the analysis objective of our comparison between RHD and PMM, we deviate from the focus of the previous studies, where emphasis was mainly put on preserving marginal distributions of the donor study within the fused data source. Instead, we concentrate on bivariate associations between common variables and fused variables as well as on the primary objective of any data fusion, the joint distribution of the not jointly observed variables and . As stated above, we expect PMM to preserve the correlations between the variables and as well as between and better than RHD, since correlations suffer more from non-exact matches than marginal distributions. Therefore, our simulation study focuses on evaluating the performance of both algorithms with respect to associations among different variables.

4.1. Database

We conduct a Monte Carlo (MC) study based on Scientific Usefiles (SUFs) of EU-SILC from 2015.444Eurostat and the NSIs also focus on matching of the EU-SILC and HBS data files from 2015. In order to ensure a sufficiently large surrogate population, we combine EU-SILC data for Germany () and France (). This leads to a total number of observations from which we draw random samples that we subsequently split into two data files which serve as substitutes for EU-SILC as recipient and HBS as donor file. For our simulation purposes, all data are based on EU-SILC due to the necessity of knowing the ’true’ joint distribution of the simulated and variables and their correlations.

As common variables we select seven variables that represent those variables Eurostat had selected for their analyses (Leulescu & Agafitei 2013; Lamarche 2018). Table 1 shows an overview of the variables used in the upcoming simulation study as well as the respective value range and measurement level. It can be seen that for RHD we have to categorise all variables, whereas for PMM the variables age () and income () keep their original metric scale level.

| Common Variables | Range / Measurement Level | |

|---|---|---|

| RHD | PMM | |

| : Activity Status of RP | 1 to 5 / categorical | 1 to 5 / categorical |

| : Age of RP | 1 to 8 / categorical | acc. / metric |

| : Population Density Level | 1 to 3 / categorical | 1 to 3 / categorical |

| : Dwelling Type | 1 to 4 / categorical | 1 to 4 / categorical |

| : Tenure Status | 1 to 5 / categorical | 1 to 5 / categorical |

| : Main Source of Income | 1 to 2 / categorical | 1 to 2 / categorical |

| : Income | 1 to 5 / categorical | acc. / metric |

| RP: ’Reference person’ (interviewed person of the household); | ||

| Actual range 1 to 5, category 5 is empty. | ||

| Here, the missing values also form a category (coded as 9); | ||

| Source: EU-SILC 2015 SUF: DE, FR.555EU-SILC 2015 SUF DE: European Union Statistics on Income and Living Conditions, 2015. Scientific Usefile Germany. EU-SILC 2015 SUF FR: European Union Statistics on Income and Living Conditions, 2015. Scientific Usefile France. | ||

The variable activity status () contains information about the types of employment (self-employed or non-self-employed, pensioner, unemployed, etc.) (Eurostat 2016, p. 285). Details concerning the generation and recoding of this variable can be found in the Appendix. The population density level () indicates the population density of the current residential area. For the German EU-SILC SUF, this variable is empty (probably due to confidentiality reasons). Therefore, we generated the respective values randomly for German data but under consideration of the univariate distribution of the original 2015 EU-SILC data for Germany (see Eurostat 2020). The generation is documented in the Appendix. Dwelling type (Eurostat 2016, p. 173) reflects the type of accommodation (residential building, flat, etc.) (Eurostat 2016, p. 173). The tenure status () combines information about the ownership status of the housing unit (sole owner, tenant, etc.) and on the (classified) rental costs incurred in case of a rental contract (Eurostat 2016, p. 174, 181). The binary variable main source of income () distinguishes between (1) income from self-employment or non-self-employment, property, ownership and assets and (2) income from pensions, social benefits and other transfers (Eurostat 2013, p. 20, 27-28; Eurostat 2016, p. 7, 313-316, 322-336). Its generation and recoding is documented in the Appendix. Income reflects the ’total disposable household income’ (Eurostat 2016, p. 209) and, for RHD, is recoded into five income quintiles.

For the specific variables and , which represent the income variables of EU-SILC () and the consumption variables of HBS () that are actually not jointly observed, we select substitutes each, i.e. and , from the database. This underlines the possibility that the univariate data fusion (imputing only one HBS variable) can also be performed in a multivariate setting with more than one specific HBS characteristic. It becomes obvious that an exact coverage of the specific variables and is only possible for the income variables from EU-SILC, because the database itself consists of EU-SILC. However, since both, statistical and methodological conclusions, are of interest, it is more important to ensure the same measurement level for the respective income and expenditure substitutes and, therefore, it is essential to select metric variables.

For we choose the variable ’total disposable household income before social transfers including old-age and survivor’s benefits’ (Eurostat 2016, p. 209) and for the variable ’interest, dividends, profit from capital investments in unincorporated business’ (Eurostat 2016, p. 214). The variables ’total household gross income’ (Eurostat 2016, p. 207) and ’total disposable household income before social transfers other than old-age and survivor’s benefits’ (Eurostat 2016, p. 209) are selected for and . Table 2 displays an overview of the specific and variables used for the simulation study and the corresponding measurement level.

| Specific EU-SILC Substitute Variables () | Measurement Level |

| : Total disposable household income before social | metric |

| transfers including old-age and survivor’s benefits | |

| : Interest, dividends, profit from capital investments in | metric |

| unincorporated business | |

| Specific HBS Substitute Variables () | Measurement Level |

| : Total household gross income | metric |

| : Total disposable household income before social | metric |

| transfers other than old-age and survivor’s benefits | |

| Source: EU-SILC 2015 SUF: DE, FR. | |

4.2. Monte Carlo Study

Our MC study is structured as follows: First, we draw random samples without replacement (Jackknife) from the data specified above. Subsequently, for each random draw we generate the specific missing data pattern underlying data fusion scenarios (see Fig. 1) and impute the missing and values in the simulated data files via RHD on the one hand and PMM on the other hand.

More specifically, each random draw leads to a simulated data file that represents EU-SILC with the observed variables and without information on the variables as well as to a simulated data file that represents HBS with the observed variables and that in turn contains no information about the variables. ’Stacking’ both data sources results in the specific missing data pattern displayed in Figure 1. We impute the missing and values in the simulated EU-SILC data file using the two proposed data fusion algorithms, RHD and PMM. Thus, the imputed values in the matched data file reflect an artificial distribution . After the imputation step the correlations between and as well as between the metric variables (: age and : income) and are then calculated and compared to the true correlations known from the surrogate population with individuals as described in Section 4.1. We apply single imputation (), resulting in point estimates for the correlations. This process, from sampling to imputation to the computation of correlations is performed with simulation draws.

In order to get a rough understanding of how sensitive the performance of RHD and PMM could be with regard to the sample sizes of the recipient data file () and the donor data file (), we vary the sample size . Of particular interest is the extent to which an excessive number of donors () compared to an equal recipient and donor ratio () has an effect on the performance of both data fusion algorithms. Therefore, the MC simulation is performed twice using different sample sizes and . For both simulation scenarios we consider observations for EU-SILC. In the first simulation scenario we also assign units to the HBS. However, in the second scenario we choose a significantly higher number of donor observations, namely for the HBS data. This leads to a sample size of with for the first scenario as well as to a sample size of with and for the second scenario.

5. Results

Since we start out with complete samples, where parts of the data are removed to mimic a data fusions scenario, we know the true parameter values even for those parameters pertaining to , but the fusion algorithms implicitly rely on the CIA, and the theoretically correct values under this assumption are displayed as additional benchmarks in the results. Note, however, that while data fusion requires assumptions regarding the joint distribution of and , the identification problem and the natural uncertainty arising from it are not the primary focus of our work, but has been covered by many other authors (see e.g. Kiesl & Rässler 2006; Conti et al. 2012; Fosdick et al. 2016; Endres et al. 2019).

5.1. Correlations Between and

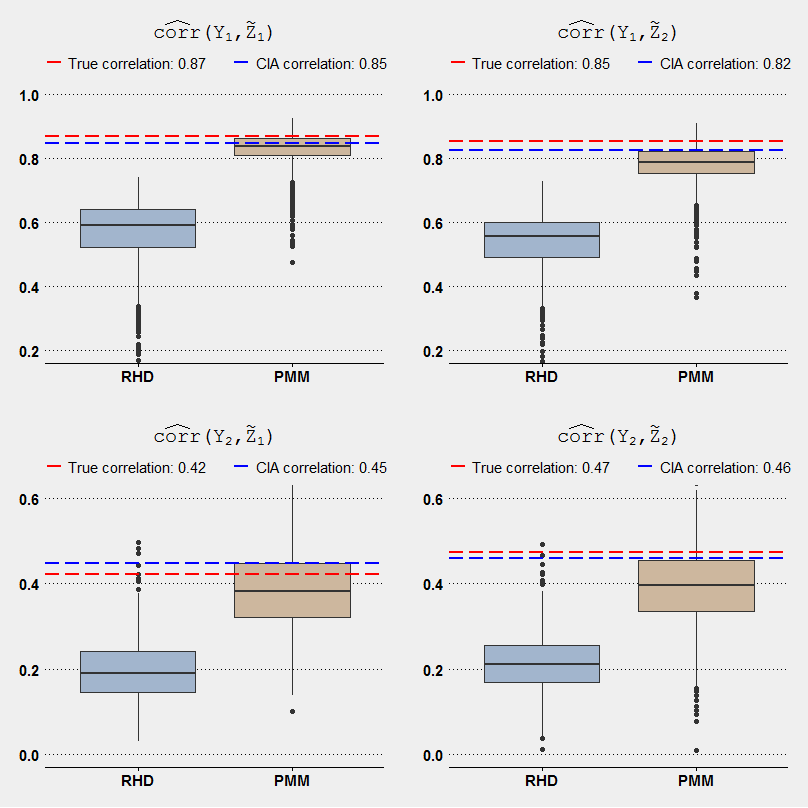

As stated in Section 3.3, we expect PMM to outperform RHD for bivariate associations. Hence, PMM should be able to reproduce the unobserved correlations between and more accurately than RHD. Table 3 displays the correlations between the specific variables and , resulting from the artificial population consisting of observations. These population correlations are used as true parameters for graphical diagnostics throughout this section and for Bias and MSE. The correlations between and as well as the correlations between and (0.87 and 0.85) are relatively high, whereas for and as well as for and we observe moderate correlations (0.42 and 0.47).

| 0.8665 | 0.8515 | 0.4211 | 0.4734 |

| Source: EU-SILC 2015 SUF: DE, FR. | |||

Figure 2 displays the MC distributions of the estimated correlations over all MC simulation draws with equal number of recipients and donors (). For high original correlations of 0.87 and 0.85, we find convincing evidence that PMM is able to reproduce the true parameter values more accurately than RHD. While RHD never covers the immediate area around the true correlations of 0.87 and 0.85 – the respective maximum for RHD amounts to 0.74 for and 0.73 for – the distributions of the estimated correlations resulting from PMM for and are considerably close to the original parameter values. This also becomes clear by looking at the respective means: PMM produces mean correlations for of 0.83 and for of 0.78 and thus comes on average very close to the original values of 0.87 and 0.85, respectively. RHD generates mean correlations of 0.57 for and 0.54 for that deviate more strongly from the observed original parameter values. Furthermore, PMM reproduces the correlation between and more accurately than the respective relationship between and . For moderate original correlations between and of 0.42 and 0.47 it can be seen that the superior performance in favour of PMM is slightly lower but still present. The MC distributions over all simulation draws illustrated in Figure 2 show for and that the estimated PMM correlations cover the area around the true parameters more frequently while RHD tends to underestimate them. Consequently, the mean of the estimated correlations for and resulting from RHD are negatively biased with 0.20 and 0.21, respectively, while PMM produces almost unbiased estimators with MC mean correlations of 0.38 and 0.40.

Source: EU-SILC 2015 SUF: DE, FR.

Source: EU-SILC 2015 SUF: DE, FR.

The second scenario of the MC study contains an excessive number of donors in order to investigate mitigating effects on the results, if the proposed matching methods can choose from a larger donor pool, i.e. the overall sample size consists of donors versus recipients. In general, no substantial change can be observed for the RHD results as we can see in the respective MC distributions illustrated in Figure 3. The correlations resulting from PMM with indicate, compared to the PMM correlations with in the first scenario, in terms of and slightly improved results, since the bulk of MC distribution of the PMM correlations is even closer to the true values of 0.87 and 0.85. Accordingly, the mean correlations computed with PMM under increase marginally to 0.84 for and 0.80 for . In contrast, with respect to and a slightly smaller number of the PMM correlation estimates covers the area around the moderate true correlations of 0.42 and 0.47, while again the mean values marginally increase to 0.39 and 0.41 due to a higher outlier rate towards 1 that goes along with a somewhat higher variance. However, it should be noted that only small changes between and can be observed that should be treated with caution due to random fluctuations.

In addition to the true correlations of and , we marked the respective correlations under CIA in Figures 2 and 3, i.e. the theoretical correlations of and , assuming independence if conditioned on . This scenario underpins the relative advantage of PMM over RHD, as the PMM correlations are close to the correct values, whereas RHD fails to accurately reproduce the correlation structure of and , even though correlations under CIA are in this case close to the true correlations.

Consequently, the PMM correlation estimates have a smaller bias compared to the RHD estimates, as displayed in Table 4. While PMM yielded more outlier results within the MC simulation study, the MSE for PMM is still much lower than RHD’s with respect to all four correlations of interest over both scenarios (see Tab. 5).

| RHD | 0.2973 | 0.3163 | 0.2250 | 0.2606 | |

|---|---|---|---|---|---|

| PMM | 0.0405 | 0.0731 | 0.0367 | 0.0773 | |

| RHD | 0.2878 | 0.3224 | 0.2332 | 0.2583 | |

| PMM | 0.0245 | 0.0563 | 0.0319 | 0.0632 | |

| Source: EU-SILC 2015 SUF: DE, FR. | |||||

| RHD | 0.0987 | 0.1089 | 0.0557 | 0.0728 | |

|---|---|---|---|---|---|

| PMM | 0.0050 | 0.0096 | 0.0109 | 0.0152 | |

| RHD | 0.0913 | 0.1113 | 0.0587 | 0.0719 | |

| PMM | 0.0040 | 0.0071 | 0.0133 | 0.0147 | |

| Source: EU-SILC 2015 SUF: DE, FR. | |||||

5.2. Correlations Between and

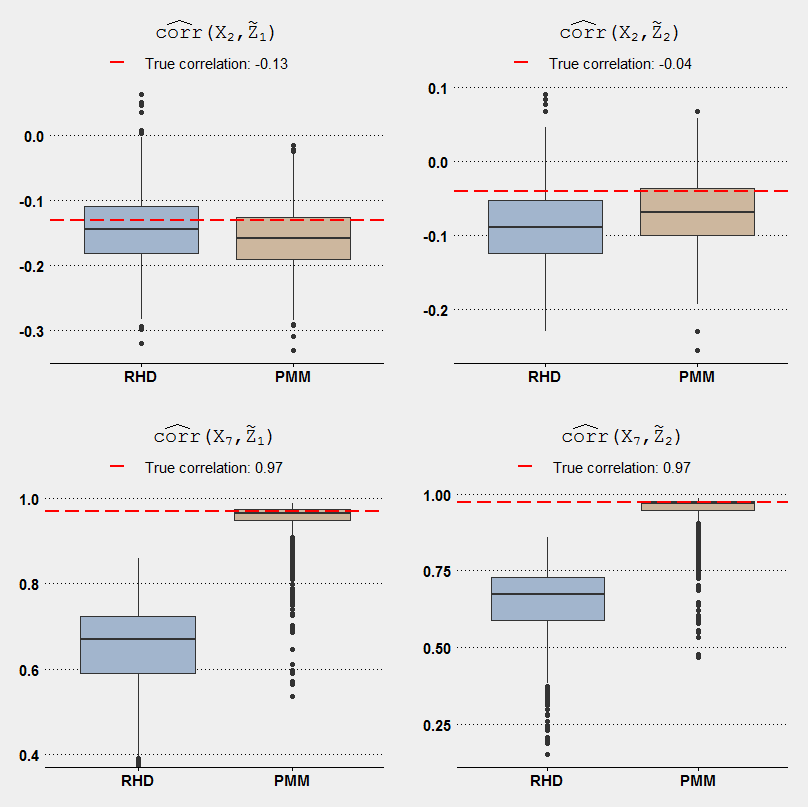

Apart from the reproduction of the joint information between the variables not jointly observed, the preservation of the distribution between the common variables and the specific variables can be regarded as a minimum requirement, as it does not rely on any identifying assumptions. Table 6 shows the true correlations resulting from the data base that represents our artificial population specified in Section 4.1. For we consider the metric variables and . Here, correlations between and as well as between and are relatively low with and , respectively, while correlations for and as well as for and are rather high with 0.97 each.

| 0.9695 | 0.9735 | ||

| Source: EU-SILC 2015 SUF: DE, FR. | |||

As can be seen in the respective MC distributions displayed in Figure 4, both methods struggle with preserving the low correlations between and both specific variables. One possible explanation is that variable was not included in the backward-deletion selected matching model, as variable explains variables and almost perfectly, thus accidentally creating an uncongeniality issue (Meng 1994). For the scenario with excessive donors this phenomenon vanishes which can be seen in Figure 5, because the larger sample size increased the probability of to remain in the underlying model.

As expected, PMM does once again much better in preserving high correlations, as the respective correlation estimates for and come very close to the true parameter values and amount on average to 0.95 under and approximately to the real parameter value of 0.97 under . RHD produces mean correlations of 0.64 () and 0.65 () for as well as 0.65 () and 0.64 () for , respectively, that fall far behind the real observed parameter values. Investigating the bias and the MSE underlines these findings in favour of PMM, as displayed in Tables 7 and 8.

Source: EU-SILC 2015 SUF: DE, FR.

Source: EU-SILC 2015 SUF: DE, FR.

| RHD | 0.0124 | 0.0474 | 0.3263 | 0.3263 | |

|---|---|---|---|---|---|

| PMM | 0.0264 | 0.0275 | 0.0224 | 0.0284 | |

| RHD | 0.0138 | 0.0132 | 0.3235 | 0.3313 | |

| PMM | 0.0111 | 0.0103 | 0.0022 | 0.0042 | |

| Source: EU-SILC 2015 SUF: DE, FR. | |||||

| RHD | 0.0032 | 0.0049 | 0.1197 | 0.1192 | |

|---|---|---|---|---|---|

| PMM | 0.0030 | 0.0029 | 0.0033 | 0.0051 | |

| RHD | 0.0025 | 0.0022 | 0.1158 | 0.1210 | |

| PMM | 0.0022 | 0.0021 | 0.0004 | 0.0007 | |

| Source: EU-SILC 2015 SUF: DE, FR. | |||||

6. Conclusion

The objective of our research was to compare two types of data fusion methods, Random Hot Deck as a representative of classical nearest neighbour hot deck methods as well as the alternative Predictive Mean Matching algorithm. Covariate-based variants like RHD are wide-spread for data fusion in practice, whereas Predictive Mean Matching is a popular method for conditional univariate sequential regression imputation algorithms (van Buuren & Groothuis-Oudshoorn 2011), but is far less common as a data fusion alternative. In general, PMM can be classified as a semi-parametric method (Rubin 1987), since it requires an underlying parametric model for predicting the (conditional) means of missing and observed cases, which distinguishes it from the purely covariate-based statistical matching methods. This can be perceived as a drawback, as the ’non-parametric’ covariate-based methods do not require this step. However, we still make implicit assumptions for covariate-based algorithms about the association between the common and the specific variables by deciding to use a particular distance metric. Since our goal is the joint analysis of these variables, we assume a particular data generating process (including identifying assumptions), and we implicitly assume the imputation method to be congenial to the analysis model, i.e. associations among variables which are part of the analysis have to be accounted for by the imputation model as well (for details see Meng 1994; Xie & Meng 2017). To some extent this drawback therefore can be viewed as advantageous, as PMM requires us to think about the nature of the relationship between the common variables and the specific variables to be fused.

The already mentioned benefit of PMM is the implicit weighting of the common variables with respect to the specific variables. Since exact matches are rare in purely discrete settings and impossible in continuous settings, distances between recipients and potential donors play a crucial role. And some variables usually turn out to be more relevant for the distance processing in order to find the ’nearest’ donor observation and, therefore, we have to account for the unequal explanatory power of the common variables with regard to the specific variables to be matched. Classical covariate-based methods assign weights to the variables, and these are either 1 or 0, depending on whether a particular variable is included in the distance measure. There is no straightforward procedure that decides which variables should be included, but, using all potential common variables can lead to very inefficient matches. PMM, on the other hand, reverses the weighting to the specific variables using the Mahalanobis distance of the residuals. As stated in Section 3 in order to keep our research close to applied problems, we additionally included a variable selection scheme via backward-deletion for both algorithms to reduce the potentially high number of common variables to a more sensible subset of matching covariates. However, this does not invalidate the general perspective on the differences between PMM and RHD.

Moreover, adequate distance processing is even more important if the number of variables included in the data fusion process is relatively high. Additionally, the lower the number of potential donors, the higher, on average, the distances between recipients and matched donors (Andridge & Little 2010). Subsequently, the probability for exact matches decreases and the way we are dealing with non-exact matches becomes more relevant.

The RHD algorithm as implemented by Eurostat requires a categorisation of metric variables which may cause a loss of information. The effect is similar to the above mentioned problem of increasing distances between recipients and matched donors, as the categorisation might lead to matches which are not the best possible ones under the original metric scale. Findings from additional simulations using Gower distance (without categorisation) suggest, however, that PMM is still superior to covariate-based matching, although the gap becomes slightly closer in the excessive donor scenario.

We did not consider constrained matching (see e.g. Rodgers 1984; Rubin 1986) in this paper which typically aims at a balanced usage of donors. We feel, however, that taking this approach to the extreme ’forces’ the marginal distribution of from the donor study upon the recipient study, irrespective of different sample properties, indicated by deviating distributions in . Under these circumstances it would be plausible that the fused distribution of in the recipient study should be different to the corresponding distribution in the donor study.

Besides, the primary objective of any data fusion is the preservation of the joint distribution of and (Kiesl & Rässler 2005) which might clash with the objective of preserving the marginal distribution of at all costs. In our simulation studies PMM outperformed the covariate-based RHD method with respect to preserving . While Predictive Mean Matching can only be applied to metric-scale variables, we believe we have demonstrated that the method is a very useful addition to the toolbox of data fusion methods and, thus, should be taken into consideration for general application.

7. Appendix

Recoding Details of Certain Variables

Activity Status ()

Variable PL031 ’Self-defined current economic status’ (Eurostat 2016, p. 285) with the following levels:

1: Employee working full-time

2: Employee working part-time

3: Self-employed working full-time (including family worker)

4: Self-employed working part-time (including family worker)

5: Unemployed

6: Pupil, student, further training, unpaid work experience

7: In retirement or in early retirement or has given up business

8: Permanently disabled or/and unfit to work

9: In compulsory military community or service

10: Fulfilling domestic tasks and care responsibilities

11: Other inactive person

Grouping to activity status:

Original category Activity status

: Working

: Unemployed

: In retirement or early retirement

: Fulfilling domestic tasks

: Permanently disabled

: Not specified (NA)

The categories coded as 9 (NA) within the activity status had a too small number of cases which causes problems in some MC samples.

Population Density Level ()

Random variable generation for Germany due to completely missing information in the German EU-SILC Scientific Usefile. We randomly generated the variable with a sampling probability that is analogue to the published distribution which can retrieved by the online Data Explorer (Eurostat 2020).

Variable DB100 ’Degree of urbanisation’ (Eurostat 2016, p. 112) with the following levels and its sampling probability:

1: Densely-populated area (35.8%)

2: Intermediate area (41.8%)

3: Thinly-populated area (22.4%)

Main Source of Income ()

The generated variable is based on six main sources of income that reflect for each individual the maximum total value of the following variables:

PY010G: ’Employee cash or near cash income’ (Eurostat 2016, p. 313)

PY020G: ’Non-cash employee income’ (Eurostat 2016, p. 315)

PY050G: ’Cash benefits or losses from self-employment’ (Eurostat 2016, p. 322)

PY080G: ’Pension from individual private plans’ (Eurostat 2016, p. 327)

PY090G: ’Unemployment benefits’ (Eurostat 2016, p. 328)

PY100G: ’Old-age benefits’ (Eurostat 2016, p. 328)

PY110G: ’Survivor’ benefits’ (Eurostat 2016, p. 328)

PY120G: ’Sickness benefits’ (Eurostat 2016, p. 328)

PY130G: ’Disability benefits’ (Eurostat 2016, p. 328)

PY140G: ’Education-related allowances’ (Eurostat 2016, p. 328)

The variables are all metric scaled and the highest total value in each case leads to the following auxiliary categories:

Maximum for

As long as all total values for the variables PY010G to PY140G amounts to zero, we code this as a missing value (NA). In this case, we included the missing values (NAs) and code it as 9.

Finally, the auxiliary categories are grouped into two categories that build the final variable main source of income ():

Auxiliary category Main source of income

References

- (1)

- Albayrak & Masterson (2017) Albayrak, O. & Masterson, T. (2017), ‘Quality of statistical match of household budget survey and SILC for Turkey’, Levy Economics Institute, Working Paper (885).

- Andridge & Little (2010) Andridge, R. R. & Little, R. J. (2010), ‘A review of hot deck imputation for survey non-response’, International statistical review 78(1), 40–64.

- Beretta & Santaniello (2016) Beretta, L. & Santaniello, A. (2016), ‘Nearest neighbor imputation algorithms: a critical evaluation’, BMC medical informatics and decision making 16 Suppl 3, 74.

- Chen & Shao (2000) Chen, J. & Shao, J. (2000), ‘Nearest neighbor imputation for survey data’, Journal of official statistics 16(2), 113.

- Conti et al. (2012) Conti, P. L., Marella, D. & Scanu, M. (2012), ‘Uncertainty analysis in statistical matching’, Journal of Official Statistics 28(1), 69–88.

- Dalla Chiara et al. (2019) Dalla Chiara, E., Menon, M. & Perali, F. (2019), ‘An integrated database to measure living standards’, Journal of Official Statistics 35(3), 531–576.

- Donatiello et al. (2014) Donatiello, G., D’Orazio, M., Frattarola, D., Rizzi, A., Scanu, M. & Spaziani, M. (2014), ‘Statistical matching of income and consumption expenditures’, International Journal of Economic Sciences 3(3), 50.

-

D’Orazio (2019)

D’Orazio, M. (2019), ‘Statmatch: Statistical

matching or data fusion: R-package’.

https://cran.r-project.org/web/packages/StatMatch/StatMatch.pdf -

D’Orazio et al. (2006)

D’Orazio, M., Di Zio, M. & Scanu, M. (2006), Statistical Matching: Theory and Practice,

Wiley series in survey methodology, John Wiley, Chichester.

http://site.ebrary.com/lib/alltitles/docDetail.action?docID=10301727 -

D’Orazio et al. (2018)

D’Orazio, M., Frattarola, D., Rizzi, A., Scanu, M. & Spaziani, M.

(2018), ‘The statistical matching of

EU-SILC and HBS at ISTAT: where do we stand for the production of official

statistics’.

https://www.istat.it/it/files//2018/11/Scanu_original-paper.pdf - Endres et al. (2019) Endres, E., Fink, P. & Augustin, T. (2019), ‘Imprecise imputation: A nonparametric micro approach reflecting the natural uncertainty of statistical matching with categorical data’, Journal of Official Statistics 35(3), 599–624.

-

Eurostat (2013)

Eurostat (2013), ‘European household income

by groups of households’, 2013 Edition.

https://ec.europa.eu/eurostat/documents/3888793/5858173/KS-RA-13-023-EN.PDF/7e1dcfb2-2735-4334-9b0a-5a95af934b1d - Eurostat (2016) Eurostat (2016), ‘Methodological Guidelines and Description of EU-SILC Target Variables: DocSILC065, 2015 Operation (Version August 2016)’.

- Eurostat (2018) Eurostat (2018), ‘R code to match EU-SILC and HBS’.

-

Eurostat (2020)

Eurostat (2020), ‘Eurostat - data explorer’.

https://appsso.eurostat.ec.europa.eu/nui/submitViewTableAction.do - Fosdick et al. (2016) Fosdick, B. K., DeYoreo, M. & Reiter, J. P. (2016), ‘Categorical data fusion using auxiliary information’, The Annals of Applied Statistics 10(4), 1907–1929.

- Gabler (1997) Gabler, S. (1997), ‘Datenfusion’, ZUMA-Nachrichten 21(40), 81–92.

- Gilula et al. (2006) Gilula, Z., McCulloch, R. E. & Rossi, P. E. (2006), ‘A direct approach to data fusion’, Journal of Marketing Research 43(1), 73–83.

-

Gower (1971)

Gower, J. C. (1971), ‘A general coefficient

of similarity and some of its properties’, Biometrics 27(4), 857.

www.jstor.org/stable/2528823 - Kiesl & Rässler (2005) Kiesl, H. & Rässler, S. (2005), Techniken und Einsatzgebiete von Datenintegration und Datenfusion, in C. König, M. Stahl & E. Wiegand, eds, ‘Datenfusion und Datenintegration: 6. Wissenschaftliche Tagung’, Tagungsberichte, Bonn, pp. 17–32.

-

Kiesl & Rässler (2006)

Kiesl, H. & Rässler, S. (2006), ‘How valid can data fusion be?’.

http://doku.iab.de/discussionpapers/2006/dp1506.pdf - Koller-Meinfelder (2009) Koller-Meinfelder, F. (2009), Analysis of Incomplete Survey Data - Multiple Imputation via Bayesian Bootstrap Predictive Mean Matching, PhD thesis, Bamberg.

- Koschnick (1995) Koschnick, W. J. (1995), Standard-Lexikon für Mediaplanung und Mediaforschung in Deutschland: Bd. 1.2, 2., überarb. aufl. edn, Saur, München.

- Lamarche (2017) Lamarche, P. (2017), ‘Measuring Income, Consumption and Wealth jointly at the Micro-Level: Preliminary Version June 2017’.

- Lamarche (2018) Lamarche, P. (2018), ‘Measuring Income, Consumption and Wealth jointly at the micro-level, Version August 19, 2018’.

-

Leulescu & Agafitei (2013)

Leulescu, A. & Agafitei, M. (2013), ‘Statistical matching: A model based approach for data integration’, 2013 Edition.

http://ec.europa.eu/eurostat/documents/3888793/5855821/KS-RA-13-020-EN.PDF/477dd541-92ee-4259-95d4-1c42fcf2ef34?version=1.0 - Little (1988) Little, R. J. A. (1988), ‘Missing-data adjustments in large surveys’, Journal of Business & Economic Statistics 6(3), 287–296.

-

Lumley & Miller (2020)

Lumley, T. & Miller, A. (2020),

‘leaps: Regression subset selection: R-package’.

https://cran.r-project.org/web/packages/leaps/leaps.pdf -

Meinfelder & Schnapp (2015)

Meinfelder, F. & Schnapp, T. (2015), ‘Baboon: Bayesian bootstrap predictive mean matching – multiple and single

imputation for discrete data: R-package’.

https://cran.r-project.org/web/packages/BaBooN/BaBooN.pdf - Meng (1994) Meng, X.-L. (1994), ‘Multiple-imputation inferences with uncongenial sources of input (with discussion).’, Statistical Science 9(4), 538–558.

- Okner (1972) Okner, B. (1972), Constructing a new data base from existing microdata sets: The 1966 merge file, in ‘Annals of Economic and Social Measurement, Volume 1, Number 3’, National Bureau of Economic Research, Inc, pp. 325–362.

-

R Core Team (2019)

R Core Team (2019), ‘R: A language and

environment for statistical computing’.

https://www.R-project.org/ - Rässler (2002) Rässler, S. (2002), Statistical matching: A frequentist theory, practical applications, and alternative Bayesian approaches, Vol. 168 of Lecture notes in statistics, Springer, New York.

- Rodgers (1984) Rodgers, W. L. (1984), ‘An evaluation of statistical matching’, Journal of Business & Economic Statistics 2, 91–102.

- Rubin (1986) Rubin, D. B. (1986), ‘Statistical matching using file concatenation with adjusted weights and multiple imputations’, Journal of Business & Economic Statistics 4(1), 87.

- Rubin (1987) Rubin, D. B. (1987), Multiple Imputation for Nonresponse in Surveys, Wiley, New York.

- Serafino & Tonkin (2017) Serafino, P. & Tonkin, R. (2017), ‘Statistical Matching of European Union Statistics on Income and Living Conditions (EU-SILC) and the Household Budget Survey’, 2017 Edition.

- Sims (1972) Sims, C. A. (1972), ‘Comments (on Okner 1972)’, Annals of Economic and Social Measurement 1, 343–345.

- Singh et al. (1993) Singh, A. C., Mantel, H. J., Kinack M. D. & Rowe, G. (1993), ‘Statistical matching: Use of auxiliary information as an alternative to the conditional independence assumption’, Survey Methodology 19(1), 59–79.

- Stiglitz et al. (2009) Stiglitz, J., Sen, A. & Fitoussi, J. (2009), ‘Report of the Commission on the Measurement of Economic Performance and Social Progress (CMEPSP)’.

- Uçar & Betti (2016) Uçar, B. & Betti, G. (2016), ‘Longitudinal statistical matching: transferring consumption expenditure from HBS to SILC panel survey’.

-

van Buuren (2020)

van Buuren, S. (2020), ‘mice: Multivariate

imputation by chained equations: R-package’.

https://cran.r-project.org/web/packages/mice/mice.pdf -

van Buuren & Groothuis-Oudshoorn (2011)

van Buuren, S. & Groothuis-Oudshoorn, K. (2011), ‘mice: Multivariate imputation by chained equations

in r’, Journal of Statistical Software 45(3), 1–67.

http://www.jstatsoft.org/v45/i03/ - van der Putten et al. (2002) van der Putten, P., Kok, J. N. & Gupta, A. (2002), ‘Data fusion through statistical matching: Working paper 4342-02’, MIT Sloan School of Management .

-

Webber & Tonkin (2013)

Webber, D. & Tonkin, R. (2013),

‘Statistical Matching of EU-SILC and the Household Budget Survey to Compare

Poverty Estimates Using Income, Expenditures and Material Deprivation’,

2013 Edition.

https://ec.europa.eu/eurostat/documents/3888793/5857145/KS-RA-13-007-EN.PDF/37d4ffcc-e9fc-42bc-8d4f-fc89c65ff6b1 - Xie & Meng (2017) Xie, X. & Meng, X.-L. (2017), ‘Dissecting multiple imputation from a multi-phase inference perspective: What happens when god’s, imputer’s and analyst’s models are uncongenial?’, Statistica Sinica pp. 1485–1545.