Powerful Knockoffs via Minimizing Reconstructability

Abstract

Model-X knockoffs (Candès et al.,, 2018) allows analysts to perform feature selection using almost any machine learning algorithm while still provably controlling the expected proportion of false discoveries. To apply model-X knockoffs, one must construct synthetic variables, called knockoffs, which effectively act as controls during feature selection. The gold standard for constructing knockoffs has been to minimize the mean absolute correlation (MAC) between features and their knockoffs, but, surprisingly, we prove this procedure can be powerless in extremely easy settings, including Gaussian linear models with correlated exchangeable features. The key problem is that minimizing the MAC creates strong joint dependencies between the features and knockoffs, which allow machine learning algorithms to partially or fully reconstruct the effect of the features on the response using the knockoffs. To improve the power of knockoffs, we propose generating knockoffs which minimize the reconstructability (MRC) of the features, and we demonstrate our proposal for Gaussian features by showing it is computationally efficient, robust, and powerful. We also prove that certain MRC knockoffs minimize a natural definition of estimation error in Gaussian linear models. Furthermore, in an extensive set of simulations, we find many settings with correlated features in which MRC knockoffs dramatically outperform MAC-minimizing knockoffs and no settings in which MAC-minimizing knockoffs outperform MRC knockoffs by more than a very slight margin. We implement our methods and a host of others from the knockoffs literature in a new open source python package knockpy.111See https://github.com/amspector100/knockpy.

1 Introduction

Model-X (MX) knockoffs (Candès et al.,, 2018) has recently emerged as a powerful and flexible method to perform controlled variable selection. Informally, given a set of features and an outcome of interest , knockoffs allows one to leverage almost any regression method to discover relationships between the features and the outcome. Notably, knockoffs exactly control the expected proportion of false positives in finite samples provided that the distribution of the features is known, while assuming nothing about the conditional distribution .

The knockoffs framework accomplishes this task by constructing synthetic variables, called knockoffs, which mimic the correlation structure of the original features. In principle, there are many possible ways to construct valid knockoff variables. However, the knockoffs literature has largely converged to a single measure of knockoff quality, namely that one should minimize the mean absolute correlation (MAC) between features and their knockoffs in order to maximize statistical power. Such knockoffs can be constructed via semidefinite programming (SDP) when the features are multivariate Gaussian, and almost the entire knockoffs literature has treated them as the “gold standard” of knockoff quality (see, e.g., Barber and Candès, (2015); Candès et al., (2018); Li and Maathuis, (2019); Bates et al., (2020); Askari et al., (2020)).

1.1 Contribution

This paper describes an improved heuristic for generating powerful knockoffs. With this goal in mind, our work makes two key contributions.

Identifying the reconstruction effect. We prove that existing knockoff generators often create strong joint dependencies between the features and knockoffs. This allows predictive algorithms like the lasso to reconstruct the effect of non-null features on the response using the knockoffs, which can substantially reduce statistical power.

-

•

We prove that in a very simple setting—an exchangeable Gaussian design with correlation and a Gaussian linear model for the response—almost every feature statistic has asymptotically zero power when used with knockoffs that minimize the MAC.

-

•

We argue via both theory and simulations that minimizing the MAC frequently causes the reconstruction effect for correlated designs, and that this phenomenon will reduce power. We also identify several examples of the reconstruction effect in the previous knockoffs literature.

More powerful knockoffs via minimizing reconstructability (MRC). We introduce a novel framework which generates powerful knockoffs by minimizing one’s ability to reconstruct a feature using the other features and the knockoffs. We consider two concrete instantiations of this framework based on two measures of reconstructability: minimum variance-based reconstructability (MVR) knockoffs and maximum entropy (ME) knockoffs. These methods are well-defined for all design distributions, although they are particularly easy to analyze in the case when the features are Gaussian.

-

•

We prove that when the features and response jointly follow a multivariate Gaussian distribution, MVR knockoffs exactly minimize the estimation error when using ordinary least squares (OLS) coefficients as feature importances. This means that even if MAC-minimizing knockoffs are perturbed to prevent the features from being exactly reconstructable, we still expect MVR knockoffs to have higher power.

-

•

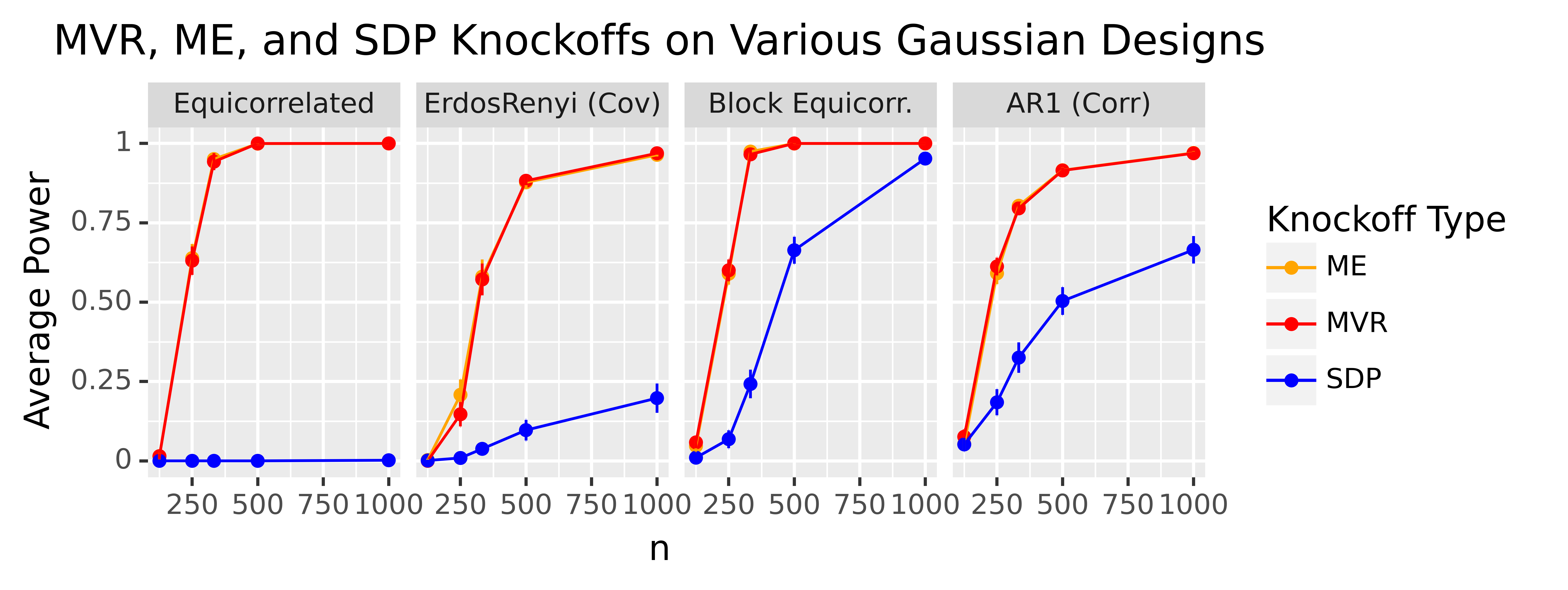

We demonstrate via simulations that MVR and ME knockoffs often have dramatically higher power than MAC-minimizing knockoffs for correlated Gaussian features. As the features become less dependent, the performances of all three methods equalize, but crucially, we have not observed any examples where SDP knockoffs dramatically outperform either MVR or ME knockoffs. We provide simulation results in both high and low dimensions for a wide variety of design distributions, response distributions, and feature statistics. Notably, this same conclusion holds even in our simulations with highly non-linear responses and feature statistics.

-

•

We also apply the MRC framework in a variety of simulation settings beyond the Gaussian model-X case. We demonstrate MRC knockoffs can increase the power of fixed-X knockoffs (Barber and Candès,, 2015), second-order knockoffs (Candès et al.,, 2018), and the general Metropolized knockoff sampler for non-Gaussian features (Bates et al.,, 2020).

Figure 1 encapsulates both of these contributions, namely that when the features are correlated, minimizing the MAC (via SDP when the features are Gaussian) often produces much-lower-power knockoffs than the MVR and ME knockoffs considered in this paper.

1.2 Notation

Let be the set of features and let be the response. We stack i.i.d. observations of the features and response into the design matrix and the response vector . We use the non-bolded notation to refer to an arbitrary single observation. For , let denote the set . For any subset , we will denote as the matrix of columns of whose indices belong to . denotes all of the columns of whose indices do not belong to . denotes the th column of , and denotes all of the columns of except column . We let refer to the identity. For a pair of square matrices , we say that if and only if is positive semi-definite. We will let and denote the minimum and maximum eigenvalues of a square matrix , respectively, and denotes the th smallest eigenvalue of . For two vectors with , we let denote their concatenation. For two matrices , we will define to represent the column-wise concatenation of and . For , we will let denote the concatenation of and except that the th column of has been swapped with the th column of . For , refers to the concatenation of and except with all columns swapped. For any permutation and any matrix , let denote the same matrix as but with the columns permuted according to the permutation . E.g., if , then the first column of becomes the third column of . For , we let refer to the vector such that for and when . For a scalar , we let represent the vector of all ones in . For a vector , represents the diagonal matrix with diagonal . If are square matrices, denotes the square block-diagonal matrix with blocks through .

1.3 Review of model-X knockoffs

MX knockoffs aims to simultaneously test the hypotheses , for . If is the set of null hypotheses, the knockoffs procedure selects a set of features and provably controls the false discovery rate (FDR) when the distribution of is known:

for some prespecified . Note that when , we use the convention that . The knockoffs procedure consists of three steps: constructing knockoffs, computing feature importances and feature statistics, and applying a data-dependent threshold.

Step 1: Constructing knockoffs. First, given a feature vector , we define knockoffs as random variables satisfying

| (1) |

for all . This pairwise exchangeability condition implies that

| (2) |

for some diagonal matrix such that , where . Note in the case where , Candès et al., (2018) proved that when , are valid knockoffs for for any , as long as . If one chooses to generate such that are multivariate Gaussian, then the choice of uniquely determines any valid knockoff-generation mechanism.

Step 2: Feature importances and feature statistics. The next step is to compute feature importances where for , and measure the importances of and its knockoff , respectively. We can use any function of the data to generate under the restriction that swapping a feature with its knockoff also swaps the feature importances . This allows one to use almost any feature importance measure to create , from cross-validated lasso coefficients to neural networks (Lu et al.,, 2018).

We combine into a feature statistic , where is an antisymmetric function such that . For example, if are absolute lasso coefficients, we might set . Here, represents the lasso (absolute) coefficient difference (LCD), where a high value of indicates that feature is more important than its knockoff in predicting . The antisymmetric property of implies that swapping with its knockoff flips the sign of . We let be the vector of feature statistics. Note are random variables, and are functions.

Step 3: The data-dependent threshold. Finally, we define the data-dependent threshold

| (3) |

Formally, to ensure this minimum is well-defined, the minimum is only over By convention, if that set is empty. Selecting features guarantees FDR control at level .

1.4 Related literature

The MX knockoffs framework (Candès et al.,, 2018) has received significant attention recently because it guarantees exact FDR control in feature selection even when the response is nonlinear and the features are arbitrarily correlated. In particular, knockoffs has been applied successfully in genome-wide association studies (GWAS), with promising empirical performance (Sesia et al., (2018, 2019, 2020)). Although the model-X framework does assume that the distribution of is known, prior work has shown through both theory (Barber et al.,, 2020) and simulations (for example, Sesia et al., (2018)) that knockoffs is fairly robust to misspecification of the distribution of . Additionally, a new line of research has relaxed the assumptions of knockoffs, such that knockoffs can control the false discovery rate as long as the distribution of is known up to a parametric model (Huang and Janson,, 2020). Since a main advantage of knockoffs is that they control the false discovery rate under feature dependence, the main goal of our paper is to improve the power of knockoffs under feature dependence. We pause to briefly compare our contribution in this respect to two relevant strands of the wider knockoffs literature.

First, our work draws heavily from the literature on sampling model-X knockoffs. Initially, Barber and Candès, (2015) introduced the fixed-X knockoff framework and suggested creating knockoffs which minimize the MAC. Candès et al., (2018) built on Barber and Candès, (2015) to introduce the model-X knockoffs filter, demonstrate how to sample knockoffs for Gaussian designs, and prove the existence of nontrivial knockoffs for general designs. Notably, Candès et al., (2018) also suggested generating knockoffs which minimize the MAC metric, although in their discussion they note the possibility of increased power from alternate knockoff constructions. Since then, several works have developed techniques to sample knockoffs for non-Gaussian designs. Sesia et al., (2018) developed a method to sample knockoffs for discrete Markov chains, and Gimenez et al., (2019) demonstrated how to sample knockoffs for some Bayesian networks. When the true model is unknown, Romano et al., (2018); Jordon et al., (2019) showed how to use deep generative networks and generative adversarial networks (GANs), respectively, to generate approximate knockoff constructions. Most recently, Bates et al., (2020) characterized all knockoff distributions and developed efficient algorithms to sample exact knockoffs in great generality, using tools from Markov Chain Monte Carlo (MCMC). However, very little of the existing literature has discussed which knockoffs to generate, and most works have assumed implicitly that weaker feature-knockoff correlations improve power. Indeed, Bates et al., (2020) did not even simulate the power of their general knockoff sampler—instead, they reported the MAC as a proxy for knockoff quality. The point of our paper is to demonstrate that the MAC heuristic can fail spectacularly and to propose a solution to this problem.

Second, four recent papers (Chen et al., (2019); Gimenez and Zou, (2019); Liu and Rigollet, (2019); Ke et al., (2020)) have observed that knockoffs can sometimes lose power in correlated settings, and Fan et al., (2020) prove the consistency of lasso-based knockoffs under certain conditions on the feature-knockoff distribution. Our work differs substantially from these, but we will be better able to explain why after we have formally introduced the reconstruction effect. See Section 2.5 for detailed comparisons to each of these works.

1.5 Outline

The outline of the rest of the paper is as follows. In Section 2, we describe how minimizing the MAC causes the reconstruction effect for general Gaussian designs. We also demonstrate that reconstructability reduces the power of knockoffs for all designs. In Section 3, we define two types of MRC knockoffs: MVR knockoffs and ME knockoffs. We prove that MVR knockoffs are optimal in a sense for OLS coefficients in Gaussian linear models, and we further prove that MVR knockoffs are consistent in low dimensions, unlike SDP knockoffs. We also give intuition as to why MRC knockoffs are likely to improve power for nonlinear responses and discuss efficient algorithms for computing MRC knockoffs when the features are Gaussian. Finally, in Section 4, we present an extensive set of simulations comparing the power of MRC and MAC-minimizing knockoffs.

2 The reconstruction effect reduces knockoffs’ power

The MAC heuristic applied in correlated settings can lead to significant power loss due to the reconstruction effect we identify in this section.

2.1 Minimizing the MAC results in reconstructability for Gaussian designs

In this section, we demonstrate that minimizing the MAC often ensures that many can be reconstructed from when is Gaussian and correlated. To begin with, note that when , choosing a type of knockoffs to generate is equivalent to choosing the -matrix from equation (2). When is Gaussian, we will refer to MAC-minimizing knockoffs as SDP knockoffs, as in the literature. When , we will also assume is scaled such that for .

Definition 2.1 (SDP Knockoffs).

Set where is the solution to the semidefinite program

A more computationally-efficient version of this procedure, called the equicorrelated method, minimizes the same objective under the constraint that is a constant vector.

This SDP formulation will continue to increase the diagonal values of until it hits the boundary condition or attains the optimal . Since the eigenvalues of are those of and , will be low rank whenever .

Lemma 2.1.

Suppose and . Then . Furthermore, if is block-diagonal with blocks, each with an eigenvalue below , then .

As a running example throughout this section, we will often analyze the simple case where is “equicorrelated” to enable more explicit analysis of the power of SDP knockoffs. This means where if and only if and otherwise, which implies is exchangeable.

Lemma 2.2.

In the equicorrelated case when , let be generated according to the SDP procedure. Then has rank , and for all .

2.2 Reconstructability and power

Why does the rank of affect power? As an intuitive example, consider the equicorrelated case, where Lemma 2.2 tells us that one could reconstruct all information contained in the features simply by looking at and one other feature. This makes it difficult to assign feature importances to versus . For example, suppose follows a single-index model, meaning we can represent for some deterministic function and independent of . Then Lemma 2.2 implies that for any , we can write

| (4) |

To see why this is a problem, initially assume , which guarantees that . In this setting, the feature importances will have difficulty distinguishing between two different models, the correct model where and an incorrect model where . Note that in the correct model, we would expect to be large and to be near zero, leading to large positive , but in the incorrect model, we would expect the opposite, leading to highly negative . Since both models fit the data equally well and the models differ only in some of the signs of their coefficients, is equally likely to be positive or negative unless the feature statistic function incorporates prior information about the signs of . For example, one could constrain the lasso to only assign nonnegative coefficient values to each feature. With enough data, the lasso would then correctly assign high feature importances to the set of features . On the other hand, it would also ensure that the lasso would assign zero importance to features in the set and high importances to their knockoff counterparts, precluding the discovery of those features.

When , the incorrect model becomes

In this case, regularized feature statistics like the lasso, with enough data, may eventually identify the correct model, whose coefficients have smaller norm than the coefficients in the incorrect model. However, when the norms of both options are similar, it will take a very large amount of data for the lasso to identify the true model (see Theorem 2.4). This exemplifies a broader theme, which is that the power of common sparsity-inducing feature statistics will decline further when it is possible to reconstruct features using a sparse subset of the other features and knockoffs. We refer to this phenomenon as sparse reconstructability, and in the general Gaussian case, it will occur when many eigenvalues of are close to zero.

Gaussian equicorrelated designs with a single-index response are only an example of the broader reconstruction effect, which occurs quite generally: whenever can be reconstructed from , feature importances such as those derived from a random forest are likely to confuse the contribution of a non-null with other features or knockoffs. In the worst case, however, Theorem 2.3 indicates that if depends on through a statistic which can be reconstructed using some function of , no feature statistic will be able to use the data to distinguish between and . This theorem does not assume to be Gaussian, nor does it assume to follow a single-index model.

Theorem 2.3.

Suppose we can represent for some set , functions and , and independent noise . Equivalently, this means . Suppose a function exists such that

| (5) |

holds almost surely. If , then

| (6) |

Furthermore, if we set , and , then for all ,

| (7) |

For instance, in the equicorrelated case when is single-index, SDP knockoffs satisfy the assumption when . In this setting, equation (7) says that SDP knockoffs produce a no free lunch situation, where no feature statistic can have non-trivial power to select any for both and . Indeed, equation (6) tells us that even a limitless amount of data gives us no way to distinguish between the features and the knockoffs in , since any statistic which consistently selects over when the response comes from faces exactly the opposite choice when the response comes from . Therefore, any feature statistic which has nontrivial power to select when the response follows will have “negative” power (less power than if all features in were null) when the response follows . For example, any feature statistic which uses to predict (using ) can do equally well using to predict (using ). If we have no a priori bias towards or , then we will be equally likely to select the features or their knockoffs , making us powerless to detect any of , no matter the signal-to-noise ratio. Alternatively, a feature statistic which a priori biases towards (for example) over may gain power when the true model uses , but as equation (7) indicates, it will correspondingly lose power when the true model uses . Furthermore, a preference for sparsity will not help in general. For example, when , both models have the same sparsity.

To gain intuition about when equation (5) might hold, it may again be helpful to let for . This includes (but is not limited to) the set of models where is partially linear in . In this case, equation (5) would be satisfied if a exists such that holds almost surely. Although this condition may initially seem pathological, several remarks are in order here. First, even if this relation only holds approximately, reconstructability will still reduce the power of knockoffs in finite samples. For example, if one perturbed SDP knockoffs to prevent from being exactly low rank, we can still have as long as some of the eigenvalues of are small. Second, as the approximate rank of decreases, the approximate null space of will grow larger, which makes it more likely that for any , there may be some such that . This corresponds to the sparse reconstructability phenomenon we identified earlier, where it is possible to reconstruct each feature using a small subset of the other features and knockoffs. Third, note that (5) does not require to be reconstructable from alone—for example, in the equicorrelated case, is not reconstructable from , but anyway when . In general, certain classes of statistics can be reconstructable from even when reconstructing requires joint information from . For this reason, it is important to prevent from being reconstructable from any of . Lastly, as grows larger, there are many more subsets for which (5) can hold, especially when the distribution of does not have any special structure. As a result, we expect this phenomenon to be more frequent in higher dimensions.

To briefly summarize, so far, we have shown that the MAC heuristic often causes the diagonal entries of the matrix to become so large that many eigenvalues of the joint covariance matrix become quite small. Unfortunately, this creates strong joint dependencies in the distribution of . In practice, this means that many features can largely be reconstructed from the knockoffs and the other features in spite of low marginal correlations between and . As a result, knockoff feature importances (such as lasso coefficients) may ignore a non-null feature and instead use to reconstruct its effect on , dramatically reducing the power of knockoffs. In Section 2.3, we show that the reconstruction effect can actually render knockoffs powerless in some settings, and as we will see in Section 4, this phenomenon occurs quite broadly, even when is not Gaussian.

2.3 Main result for equicorrelated Gaussian designs

Our main result for equicorrelated Gaussian designs and single-index response models largely follows from the intuition that as , there will often be a very large number of subsets such that , unless has very special structure. Theorem 2.3 tells us that when is equicorrelated, the presence of many such will dramatically reduce the power of knockoffs unless the feature statistic function encodes specific information about each of the signs of the non-null coefficients. To exclude this case, we impose a mild condition on which prevents it from treating any of the features of differently based on their position, and therefore prevents from incorporating different a priori information about features with positive and negative signs. In particular, we define a knockoff feature statistic function to be permutation invariant if and only if for any permutation ,

| (8) |

Since some feature statistics are randomized functions, our proofs also allow for equation (8) to hold in distribution conditional on the data. Note almost all feature statistics in the knockoffs literature, including those derived from lasso coefficients and even neural networks, satisfy this property. To quickly define notation, we denote the average power by:

where the expectation above is over the data for a fixed feature statistic function and a fixed vector of coefficients . As a reminder, is the set of selected features.

Theorem 2.4.

Let be an equicorrelated Gaussian design with correlation . Assume we can represent for and independent of the data. Let be the class of all permutation invariant feature statistic functions and suppose we aim to control the FDR at level using SDP knockoffs.

Sample uniformly from a -dimensional hypercube centered at with a fixed side-length. Let be the number of data points and suppose there exists some such that . Then as ,

Theorem 2.4 follows from a more general statement which applies to block-diagonal whose blocks are equicorrelated, which we prove in Appendix A. Note that neither the precise distribution of nor the assumption that are essential, as we discuss in Appendix A.5.

This theorem tells us that even in low-dimensional regimes, SDP knockoffs may have asymptotically zero average power, even when the feature statistic is chosen with oracle knowledge of the response model . This theorem applies to a variety of familiar single-index models, including Gaussian linear models and probit regression, which satisfy the assumption that . Furthermore, since can be arbitrarily small, we expect this conclusion to hold for most single-index and generalized linear models, which take the form .

Of course, real datasets will rarely be exactly equicorrelated. The point of Theorem 2.4 is to show that the reconstruction effect can prevent SDP knockoffs from discovering many non-null features, no matter the signal size or feature statistic. However, as we discuss at length in Section 2.2, the reconstruction effect can occur without equicorrelated features, and indeed, our empirical results in Section 4 show that SDP knockoffs lose power in a variety of practical settings.

2.4 SDP knockoffs infer signal magnitudes but not signs

To help understand why SDP knockoffs fail in the equicorrelated setting, we briefly analyze what SDP knockoffs do right. In particular, SDP knockoffs can easily be used to detect that either or has an effect on , but not to choose between them. This means that when using SDP knockoffs, non-null will often have the “right” magnitude but a negative sign.

Proposition 2.1.

Assume is equicorrelated and with and correlation . Suppose we generate knockoffs such that the feature-knockoff correlation is constant and the MAC equals . If are OLS coefficients fit on , then the mean squared error of as an estimator of is increasing in .

This theorem proves that for OLS coefficients, the differences proxy better as the marginal correlations between and get smaller, apparently in support of the MAC heuristic. Unfortunately, setting is a poor feature statistic when may be negative, since will likely be negative when is negative, preventing the selection of features with negative coefficients. On the other hand, if we set to fix this problem, knockoffs will still have extremely low power as the MAC gets smaller because and individually will have high variance, making (approximately) equally likely to be positive or negative.

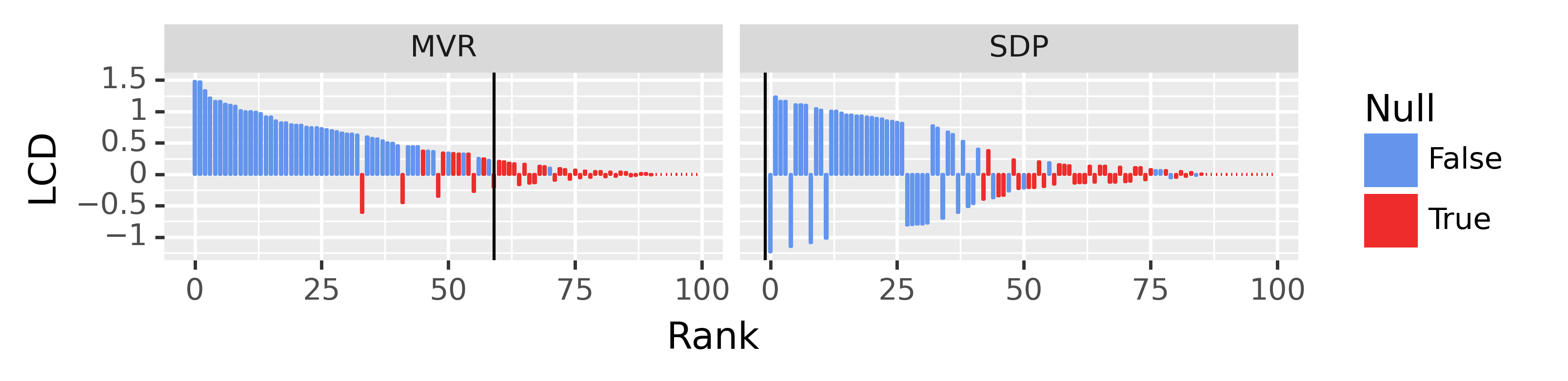

Penalized regressions like lasso coefficients exhibit the same behavior. Consider how the lasso assigns coefficient values to a pair of features and their knockoffs when . As , the lasso will have to choose between at least two options: setting and , or alternatively setting and . When using SDP knockoffs, both options deterministically have the same empirical mean-squared error as well as the same norm, so the lasso genuinely cannot choose between these two options. Moreover, this applies to every such that . Note that since are symmetric but have large magnitudes, they actually make it more difficult to discover other features, since knockoffs can only make discoveries when the with large magnitudes have consistently positive signs (see equation (3) or Figure 2 for an illustration of this).

2.5 Relationship with the literature

At this point, we pause to put our results on the reconstruction effect in context with the rest of the literature. To start, we note that the reconstruction effect appears to differ fundamentally from the “alternating sign effect” introduced by Chen et al., (2019), who give heuristic evidence that lasso-path statistics may lose power when two features are positively correlated and their coefficients have opposite or “alternating” signs. For instance, the alternating sign effect only plagues certain feature statistics such as lasso-path statistics, and the initial version of Chen et al., (2019) shows that simple statistics like OLS statistics do not suffer from this effect. In contrast, Theorem 2.4 shows that minimizing the MAC creates an unidentifiability problem which makes nearly every feature statistic asymptotically powerless in the equicorrelated case. Second, the reconstruction effect does not even rely on the presence of alternating signs in —for example, we have shown in Theorem 2.3 that it can occur outside of single-index models, where no coefficient vector exists.

Furthermore, Theorem 2.4 may seem to contradict Theorem of Fan et al., (2020), which proves that when is Gaussian with a Gaussian linear response , the power of lasso-based knockoffs approaches one asymptotically. However, that theorem assumes the regularity condition that and must be bounded away from zero. Yet Lemma 2.1 demonstrates that for SDP knockoffs, and therefore its Schur complement will often be low rank, meaning the regularity conditions used by Fan et al., (2020) will not hold. This suggests that we ought to use a different heuristic than minimizing the MAC, one that will automatically ensure is full rank whenever is. In the next section, we will define two heuristics which satisfy this property. Furthermore, we will prove that one of these heuristics is consistent under only the assumption that is bounded away from zero. This result parallels Theorem of Fan et al., (2020), except we use different technical tools to avoid requiring the problematic assumption that is bounded above zero.

Like Fan et al., (2020), Liu and Rigollet, (2019) observed that the consistency of knockoffs may depend on properties of the joint covariance matrix . Although Liu and Rigollet, (2019) did not analyze the power of SDP knockoffs, they proposed generating “conditional independence” (CI) knockoffs such that , and they proved that some lasso-based feature statistics applied to CI knockoffs are consistent in Gaussian linear models. Unfortunately, the CI condition says little about whether is (approximately) reconstructable using joint information from , and as a result, we show in Appendix F.2 that CI knockoffs actually can suffer from the same reconstructability problems that SDP knockoffs suffer from. This means that CI knockoffs may have low power in finite samples even if they are consistent asymptotically. Furthermore, CI knockoffs only exist for a restricted set of Gaussian designs, outside of which they violate the pairwise exchangeability condition (1). While Ke et al., (2020) recently suggested an extension of CI knockoffs to the general Gaussian case, their method involves computing without constraining and then performing a binary search to find the maximum such that . Unfortunately, this new matrix lacks any conditional independence properties, and furthermore, can be extremely small in practice, substantially reducing power. We discuss this more in Appendix F.2.

Lastly, Theorem of Ke et al., (2020) proves that SDP (fixed-X) knockoffs match the power of an “oracle” procedure for a positive, block-equicorrelated correlation structure. However, Ke et al., (2020) assume a fixed block-size of and vanishing sparsity, meaning that asymptotically, a vanishing proportion of the non-nulls lie in the same equicorrelated block as other non-nulls. Since the reconstruction effect for block-equicorrelated designs only occurs when multiple non-null features are correlated, it will asymptotically not occur in this regime.

3 Minimum reconstructability knockoffs

In Section 2, we demonstrated that SDP knockoffs lack power in the equicorrelated case because they make it possible to “reconstruct” a feature using . To fix this problem, we suggest constructing in order to minimize the reconstructability (MRC) of each feature given the other features and the knockoffs . In this section, we describe two instantiations of this framework which can be efficiently computed when is Gaussian and perform well in a variety of settings.

3.1 Minimum variance-based reconstructability (MVR) knockoffs

One intuitive way to minimize “reconstructability” is to maximize the conditional variance for each . This motivates the minimum variance-based reconstructability (MVR) knockoff construction.

Definition 3.1 (Minimum Variance-Based Reconstructability (MVR) Knockoffs).

To sample MVR knockoffs, sample so as to minimize

| (9) |

MVR knockoffs minimize the inverse expected conditional variances in order to harshly penalize high levels of reconstructability and ensure for all . This is important because high levels of reconstructability often cause some feature statistics to have large magnitudes but negative signs, which dramatically reduces the power of knockoffs. For example, if is non-null and highly reconstructable, then feature statistics can easily reconstruct the effect of on using , especially when the number of data points is small. When this happens, will likely be assigned a low feature importance and, more importantly, a knockoff variable such as or may be assigned a high feature importance corresponding to the effect of on . This implies that the feature statistic (resp. ) may have a large magnitude but a negative sign. Ultimately, the knockoff filter can only make rejections if there exists some such that approximately of the feature statistics with the largest absolute values have positive signs. Thus, when even a few feature statistics have large magnitudes but negative signs, knockoffs may have very low power. We illustrate this effect in Figure 2 for equicorrelated designs. We discuss this phenomenon more in Appendix C.3, where we also show that the same phenomenon occurs for a diverse range of design matrices, including Gaussian Markov chains and Gaussian designs where the covariance matrix is sparse.

In the Gaussian case when , we can write as a simple and convex function of the -matrix. In particular, , as for Gaussian features (see Anderson, (2009), Section ). See Appendix D.1 for a proof of convexity. This convenient formulation allows us to prove two appealing properties of MVR knockoffs when , , and we use the absolute value of OLS coefficients as feature importances.

First, we prove a type of optimality result for MVR knockoffs. Although we would like to know which -matrix maximizes power to detect non-nulls, the exact answer depends on the unknown coefficients . As a proxy for this, however, we note that the power of knockoffs almost entirely depends on the accuracy of the OLS coefficients . As , we hope that will converge to and the knockoff feature importances will converge to . In finite samples, it turns out that for any and , MVR knockoffs minimize the mean-squared error between and its target.

Proposition 3.1.

Suppose for any and . Let be the concatenation of with zeros. Suppose are OLS coefficients fit on and . Then

Second, we prove that the MVR knockoff filter is consistent in low-dimensions for OLS feature statistics. This result would not be surprising except that we showed in Section 2 that in some low-dimensional settings, SDP knockoffs is inconsistent for every feature statistic.

Theorem 3.1.

Suppose , , and is generated using . Suppose are OLS coefficients fit on , and set .

Let such that and consider a sequence of covariance matrices such that the minimum eigenvalue of is bounded above a fixed constant . Suppose we sample a sequence of random as follows. Let all but a uniformly drawn subset of entries of equal zero, for a fixed constant , and then sample the remaining (non-null) entries of from a -dimensional hypercube centered at with any fixed side-length. Then

Note that the equicorrelated case discussed in Section 2 satisfies these regularity conditions on , since its eigenvalues are bounded uniformly above . As noted in Section 2.5, this theorem proves a similar consistency result to Fan et al., (2020), except our proof uses properties of MVR knockoffs to avoid assumptions about the minimum eigenvalue of .

This result should also make intuitive sense in the context of Liu and Rigollet, (2019), who show that knockoffs are consistent if and only if (informally) the diagonals of converge to . Technically, Liu and Rigollet, (2019)’s theory does not directly apply to our setting, as it assumes a different asymptotic regime and relies on regularity conditions which the authors themselves admit are “highly nontrivial” to verify unless is block-diagonal. We use different technical tools to avoid these assumptions. Conceptually, however, the key novelty of Theorem 3.1 is that it shows for the first time that a concrete method—MVR knockoffs—can achieve Liu and Rigollet, (2019)’s condition with minimal assumptions on . To summarize, Liu and Rigollet, (2019)’s theory established the importance of making the diagonals of small, and MVR knockoffs explicitly follows this principle by minimizing , allowing us to prove its consistency in more generality than has been established for any other knockoff generation method.

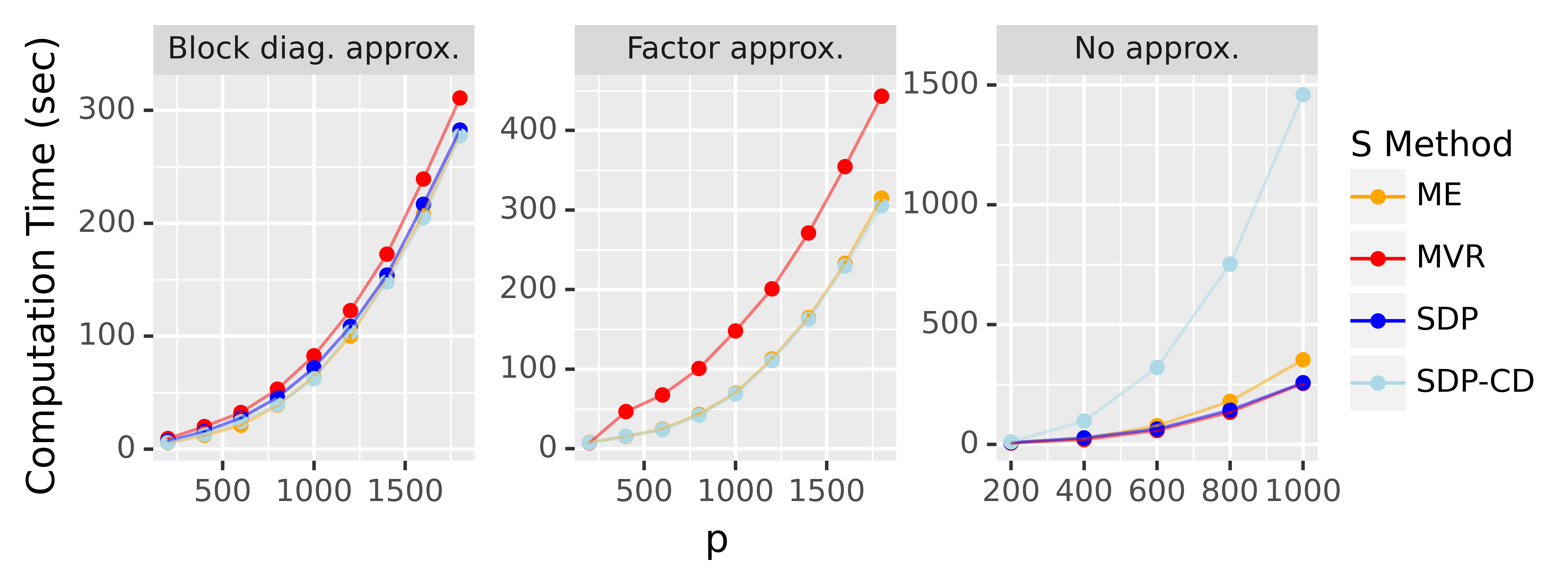

Lastly, we note that the convexity of in the Gaussian case allows us to develop an algorithm to compute in , which is the same time complexity or faster than the methods used to compute SDP knockoffs Askari et al., (2020). Our method is inspired by Askari et al., (2020), who introduced a coordinate-descent algorithm to compute efficiently. The key idea is to use rank-one updates to maintain a running Cholesky decomposition of . Our algorithm uses this same strategy, although extending their ideas to the MVR loss requires some nontrivial additional analysis. For brevity, we defer the details to Appendix D. Since the algorithms used to compute MVR and SDP knockoffs are extremely similar, we show in simulations in Appendix D.6 that not only do they have the same computational complexity, but they have very similar runtimes in practice. Additionally, like the SDP formulation (2.1), our algorithm can take advantage of block-diagonal approximations (Candès et al.,, 2018) or low-rank factor structure in (Askari et al.,, 2020) to dramatically speed up computations to be linear in —see Appendix D.5 for additional details. The overall point is that there is no computational reason to prefer either MVR or SDP knockoffs.

3.2 Maximum entropy (ME) knockoffs

An information-theoretic alternative to MVR knockoffs is to minimize the mutual information between and ; as we shall see in a moment, this is equivalent to maximizing the entropy of . Gimenez and Zou, (2019) have previously considered ME knockoffs, but only in the Gaussian case, and they introduce this method for a very different reason than we do. In particular, the authors motivate ME knockoffs by observing that the SDP knockoff construction can induce sparsity in the diagonal of , meaning that some values of the diagonal of become too small to distinguish between features and knockoffs. Although they demonstrate that ME knockoffs will not suffer from this problem, they only compare the power of the two methods in a single case where the distributions of both and are chosen adversarially against SDP knockoffs. In contrast, we advocate the use of ME knockoffs to solve almost exactly the opposite problem: that the values of are frequently too large. Indeed, our most dramatic empirical results come in the equicorrelated case, where for as large as . Clearly, in this case, the diagonal of is not sparse at all.

Definition 3.2 (Maximum Entropy (ME) Knockoffs).

Suppose is absolutely continuous on with respect to a base measure with density . To sample ME knockoffs, sample so as to minimize

| (10) |

where is the support of , and is the joint density of . Note corresponds to the negative entropy of . If admits no joint density with respect to the product measure , we adopt the convention that .

Given this definition, it is not immediately obvious that ME knockoffs minimize any notion of reconstructability. Of course, the entropy of equals twice the entropy of minus the mutual information between and , so ME knockoffs also minimize the mutual information between and . Since mutual information can account for joint dependencies between and , we might expect it to perform better than the MAC metric, which only looks marginally at dependencies between and . However, mutual information still may not necessarily capture the right notion of reconstructability. To perform feature selection with knockoffs, one must assign a feature importance to each individual feature and knockoff. To do this powerfully, we have argued that each non-null feature must contain information that cannot be reconstructed using and . Although mutual information captures some notion of the aggregate dependencies between and , it is not clear it coincides with this feature-level definition of reconstructability.

To better connect ME knockoffs with reconstructability, we turn to the setting where is Gaussian, where has a simple formulation. In particular, we can take to be jointly Gaussian with , and then the entropy of equals up to a constant. Thus, maximizing the entropy of corresponds to minimizing . This loss is actually quite similar to the MVR loss for Gaussian , as both losses are convex, elementwise-decreasing functions of the eigenvalues of . In particular,

| (11) |

where we express the loss up to an additive constant. As a result, and are quite similar in the Gaussian case, suggesting that captures a similar notion of reconstructability in this setting. This also indicates that ME and MVR knockoffs will have very similar power in the Gaussian setting, which we confirm in Section 4. In Appendix D.3, we modify the algorithm which computes to compute in the same time complexity.

Outside the Gaussian case, we cannot write so simply, but we do prove in Lemma 3.2 that when has finite support, ME knockoffs will not allow any feature to be perfectly reconstructable as long as any knockoff procedure can accomplish this. Intuitively, this result holds because if is nearly a deterministic function of , then almost all of the probability density of will lie along a dimensional subset of . To ensure the density integrates to one over , the average log value of must become larger than is optimal. See Appendix E for a more detailed discussion of the discrete case as well as a proof of Lemma 3.2.

Lemma 3.2.

Let have finite support . For any and any , ME knockoffs satisfy , so long as this property does not contradict the definition of valid knockoffs.

At this point, one might wonder whether there are clear grounds to prefer MVR knockoffs over ME knockoffs or vice versa. Our empirical results in Section 4 suggest MVR and ME knockoffs perform very similarly in the Gaussian case. There is more theoretical work to be done to better understand their relationship in general, but we can make two comments summarizing what we know (and do not know) so far. First, ME knockoffs seem to minimize some notion of reconstructability in all examples we can tractably analyze, but it is not clear that our arguments generalize beyond the Gaussian case. We include ME knockoffs in this section for the reader’s consideration because they seem promising and they perform well empirically in Section 4. Second, MVR knockoffs are appealing because they enjoy exact optimality properties with OLS feature importances and are more readily proved to be consistent, as shown in Section 3.1. Note that since ME knockoffs are not identical to MVR knockoffs, they do not enjoy this exact optimality, and it is difficult to prove the consistency of ME knockoffs for general sequences of . That said, the solutions to MVR and ME knockoffs are asymptotically identical in the case where is equicorrelated, so consistency and (approximate) optimality do hold for ME knockoffs for exchangeable Gaussian designs—see Appendix D.4 for a precise statement.

4 Empirical results

In this section, we run an extensive set of simulations to demonstrate the power of MVR and ME knockoffs. To do this, we developed a new open source python package knockpy, which implements a host of methods from the knockoffs literature, including a wide variety of feature statistics and knockoff sampling mechanisms for both fixed-X and model-X knockoffs. For example, knockpy includes a fully general Metropolized knockoff sampler (Bates et al.,, 2020) which can be multiple orders of magnitude faster than previous implementations. Most importantly, knockpy is written to be modular, so researchers can easily tweak its functionality or add other features on top of it. We discuss knockpy further in Appendix G. All additional code for our simulations is available at https://github.com/amspector100/mrcrep.

We aim to demonstrate that the MRC framework offers real advantages over MAC-minimizing knockoffs in very practical settings, even when minimizing the MAC does not result in exact reconstructability. At the outset, we highlight some key conclusions.

Power for linear responses: Both MVR and ME knockoffs generally outperform SDP knockoffs in the setting where the design is Gaussian and is linear. This result holds for a range of highly correlated covariance matrices and feature statistics, although as the features become less correlated, the performances of all three methods tend to equalize. We note further that MRC knockoffs frequently outperform their SDP counterparts by very large margins (as much as percentage points). Although there are examples where SDP knockoffs outperform MVR and ME knockoffs, these are rare, and even in such cases, SDP knockoffs usually outperform MVR and ME knockoffs by only a small margin.

Power for nonlinear responses: The preceding paragraph’s conclusions also hold when the conditional distribution is highly nonlinear, even in cases where does not follow a single-index model and linear feature statistics such as the lasso have zero power. Even very complex feature statistics like random forests with swap importances (Gimenez et al.,, 2019) or DeepPINK (Lu et al.,, 2018) perform better with MVR and ME knockoffs.

MVR vs. ME knockoffs: As our theory predicts, MVR and ME knockoffs perform similarly in the Gaussian setting, although there are a few cases where ME knockoffs slightly outperform MVR knockoffs. From now on, we use “MRC knockoffs” to refer to both MVR and ME knockoffs at once.

Robustness: Although we did not study robustness theoretically, we found empirically that MRC knockoffs can be both powerful and robust in the setting where is Gaussian but the covariance matrix is unknown and estimated using the data. In particular, in the high-dimensional setting where is estimated with a shrinkage estimator, MRC knockoffs appear to violate FDR control less severely than SDP knockoffs, although we have no theoretical reason to believe that MRC knockoffs are in general more robust than SDP knockoffs.

Power for fixed-X (FX) knockoffs: It is straightforward to define MRC knockoffs for the fixed-X knockoff filter of Barber and Candès, (2015). We demonstrate that MRC FX knockoffs are generally more powerful than their SDP counterparts.

Power for non-Gaussian designs: MRC-inspired knockoffs even perform well in the setting where the features are not Gaussian, both for second-order knockoffs and as a guide for the Metropolized knockoff sampler. We will carefully define these generalizations in Section 4.6.

In general, we will only plot average power, since knockoffs provably control the FDR. The exception to this, of course, is when we discuss the robustness of the knockoffs procedure. Unless otherwise specified, we use knockoffs to control the FDR at level . In all examples, we use Algorithms 1 and 2, detailed in Appendix D, to compute MVR and ME knockoffs. In all instances, our plots include two standard deviation error bars, although in some cases the error bars are so small they are difficult to see. We also always plot both MVR and ME knockoffs, although often the two methods have nearly identical performance, causing their power curves to entirely overlap.

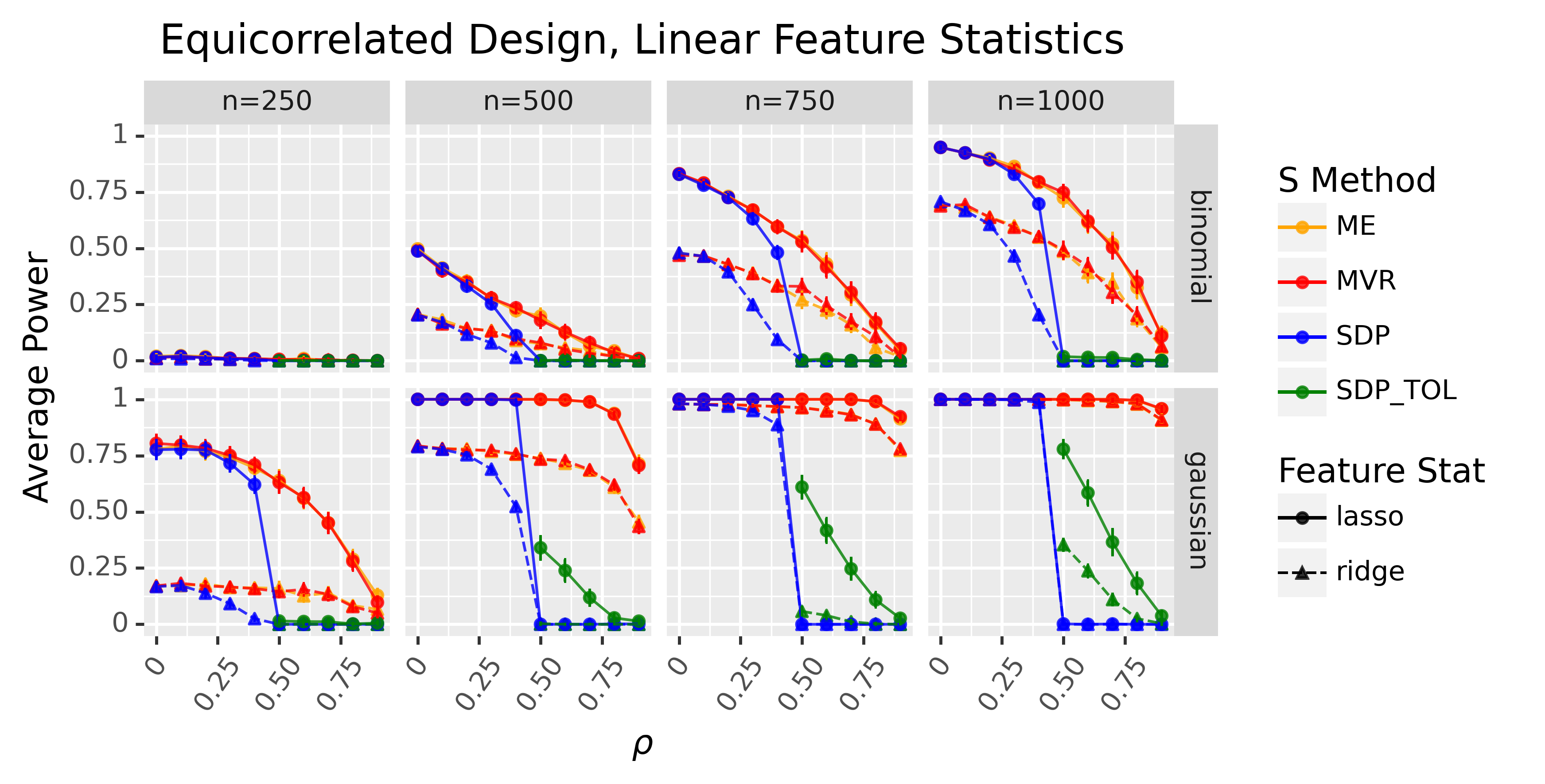

4.1 Simulations on equicorrelated designs

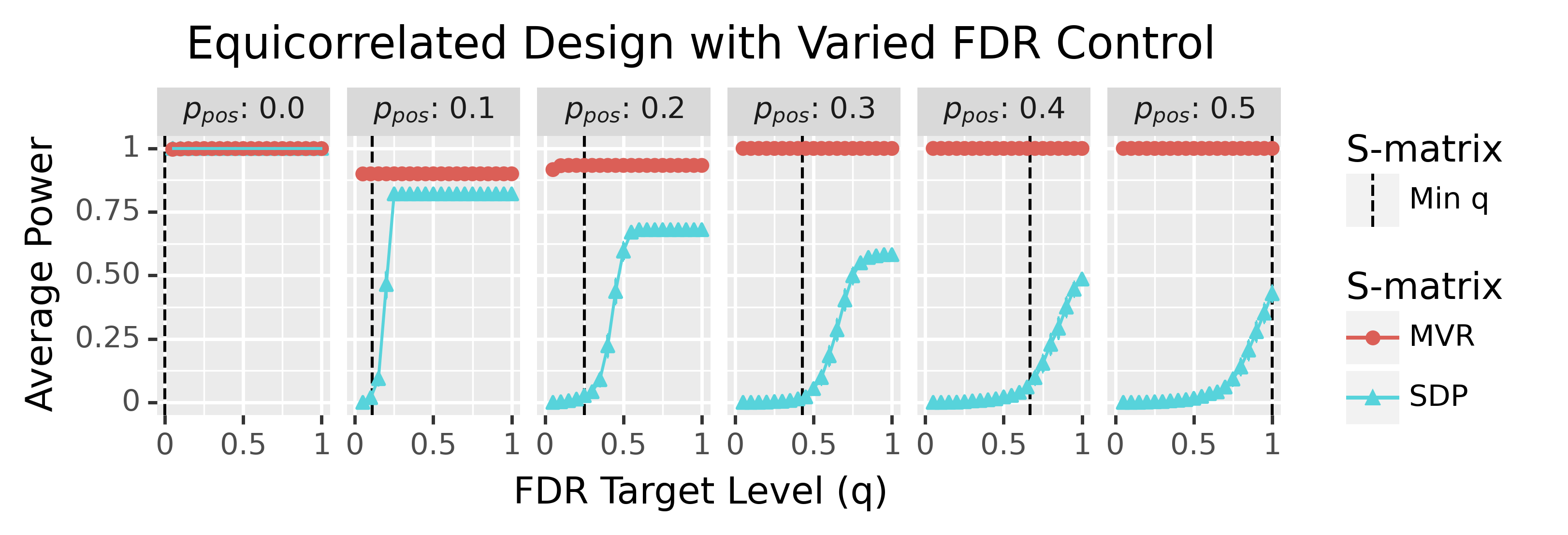

In this subsection, we investigate the performance of MRC and SDP knockoffs in the equicorrelated setting studied in Section 2. In Figure 3, we run simulations where with equicorrelated and varied between and for both a Gaussian and logistic linear response (see the caption for details). We compare four types of knockoffs: MVR, ME, SDP, and a perturbed version of SDP knockoffs where we set

| (12) |

We refer to this version as the “sdp_tol” option because it ensures that the minimum eigenvalue of is above a tolerance . When , we set to ensure that . We only do this in the case where , since otherwise will be full rank anyway. As our feature statistics, we use cross-validated lasso and ridge absolute coefficient differences of the form , where refers to the th estimated lasso or ridge coefficient, respectively, for .

Figure 3 demonstrates that MRC knockoffs substantially outperform SDP knockoffs, even when is not low rank. First, both MRC knockoff types uniformly outperform the perturbed SDP knockoffs, even though the perturbed SDP knockoffs outperform the exact SDP knockoffs. Moreover, even when and is full rank, MRC knockoffs can have much more power than SDP knockoffs: for example, when and , logistic ridge has over twice the power when applied to MRC knockoffs versus SDP knockoffs. We note that this power gain in highly correlated settings does not come at the cost of power in settings with weaker correlations, since MRC knockoffs outperform or match the power of SDP knockoffs for every value of .

Note that MVR and ME knockoffs provably yield the same solution asymptotically in this setting (see Appendix D.4), which is why their power curves almost entirely overlap in Figure 3.

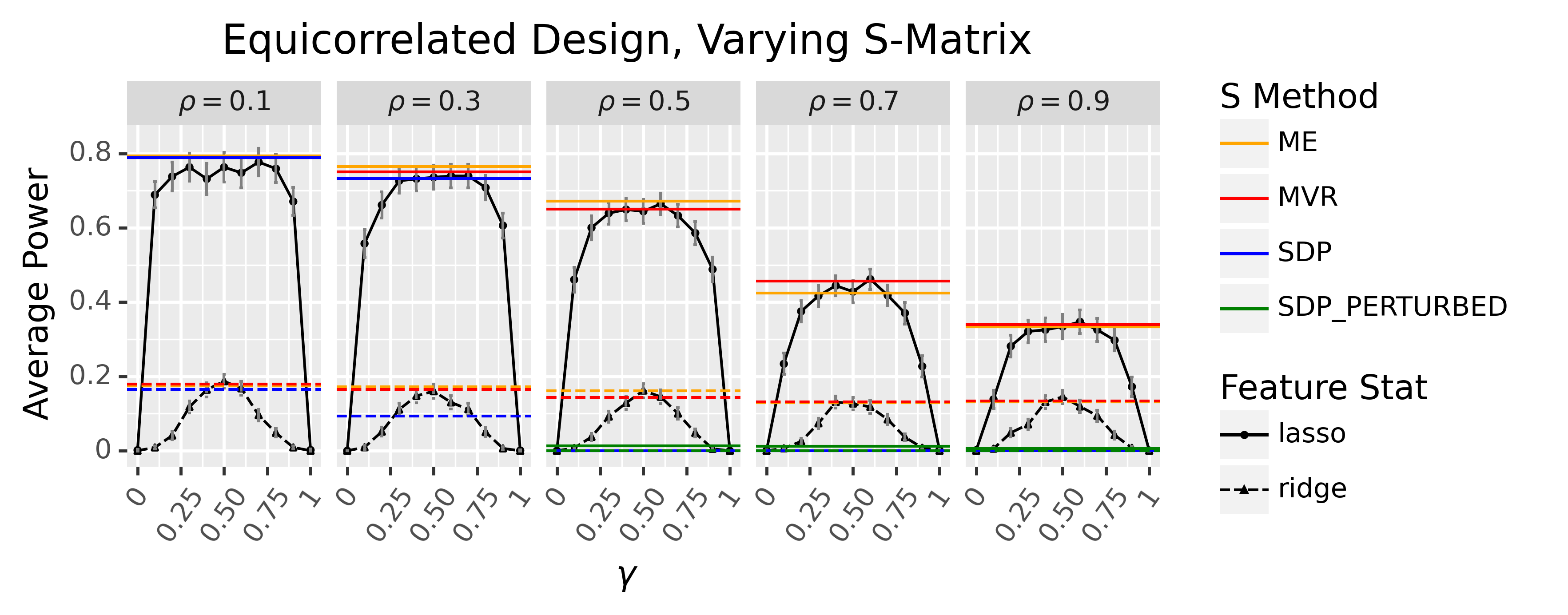

Since the perturbed SDP knockoffs outperform the SDP knockoffs, one might wonder how the choice of affects power. To analyze this question, we perform a line search over all -matrices which can be represented as a scaled identity matrix. In particular, we set

| (13) |

Here, we can think of as interpolating between the minimum possible -matrix where and the “maximum” -matrix, where . The results indicate that up to Monte Carlo error, MVR and ME knockoffs have the highest power among all such -matrices in this setting for both lasso and ridge feature statistics. Notably, this result holds for all , whereas SDP knockoffs lose power compared to MVR knockoffs for all except , where all methods have nearly the same performance. For brevity, we present these results in Appendix F.1.

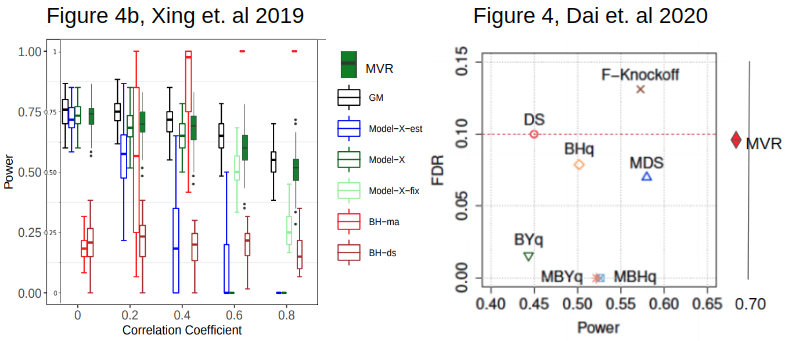

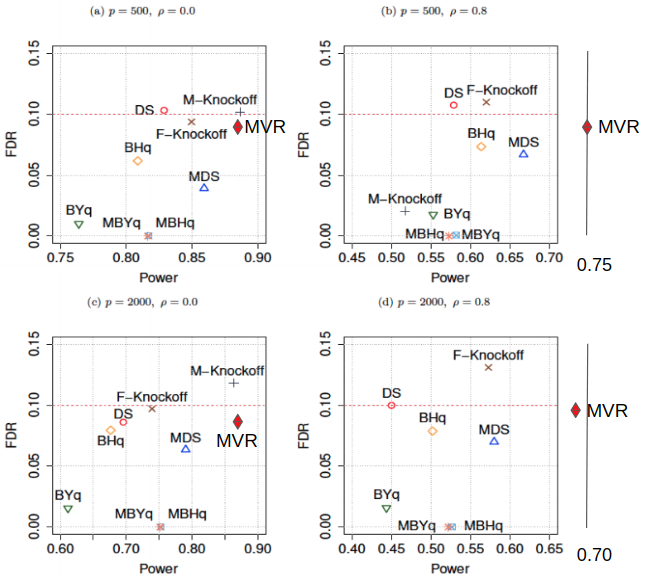

Lastly, we note that two previous papers (Xing et al.,, 2019; Dai et al.,, 2020) have observed that in the equicorrelated case, knockoffs have surprisingly low power when compared to other feature selection methods. Since these papers used the SDP formulation, in Appendix F.3, we exactly replicate these simulations but use MRC knockoffs instead. Our results show that MRC knockoffs have comparable or higher power than all of the other methods used in these papers.

4.2 Simulations on Gaussian designs

In the previous section, we investigated the performance of MRC and SDP knockoffs on equicorrelated Gaussian designs with linear responses. In this section, we let but vary extensively. Furthermore, we allow the conditional distribution to be highly nonlinear.

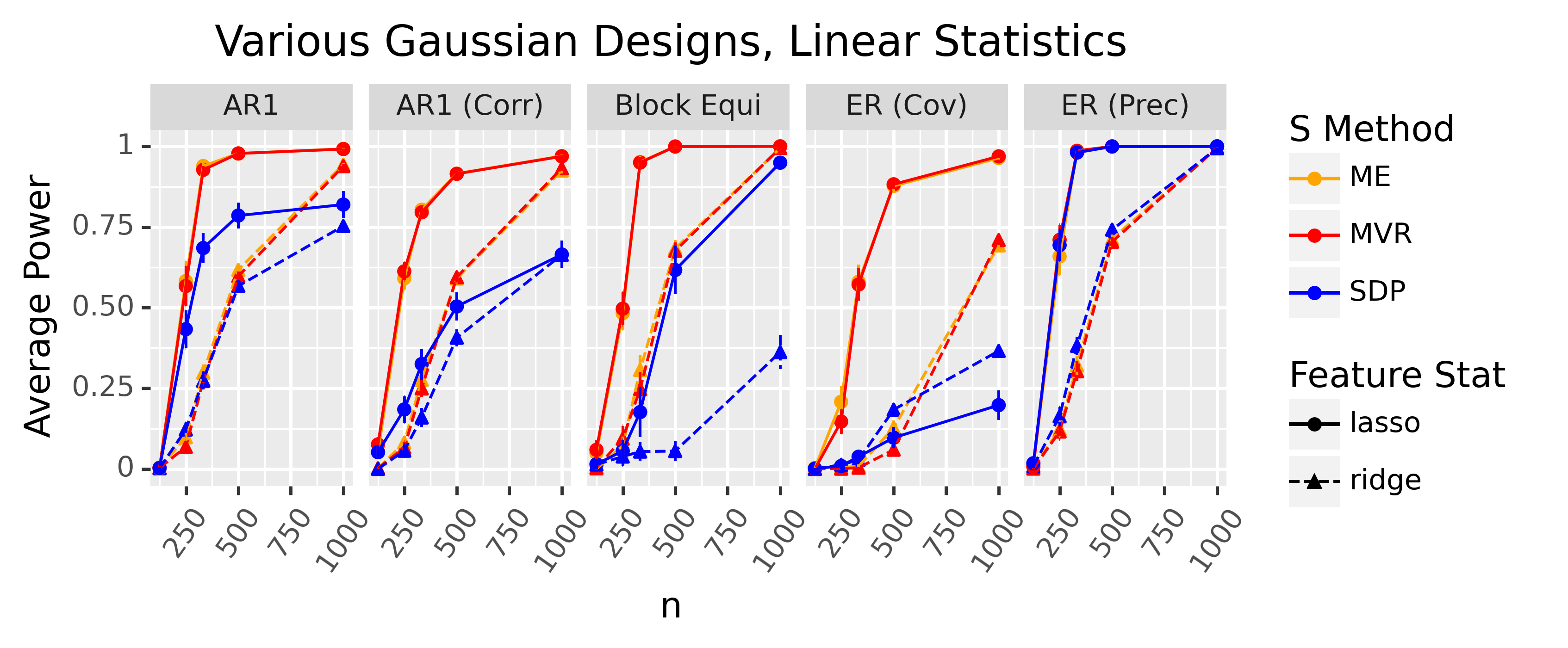

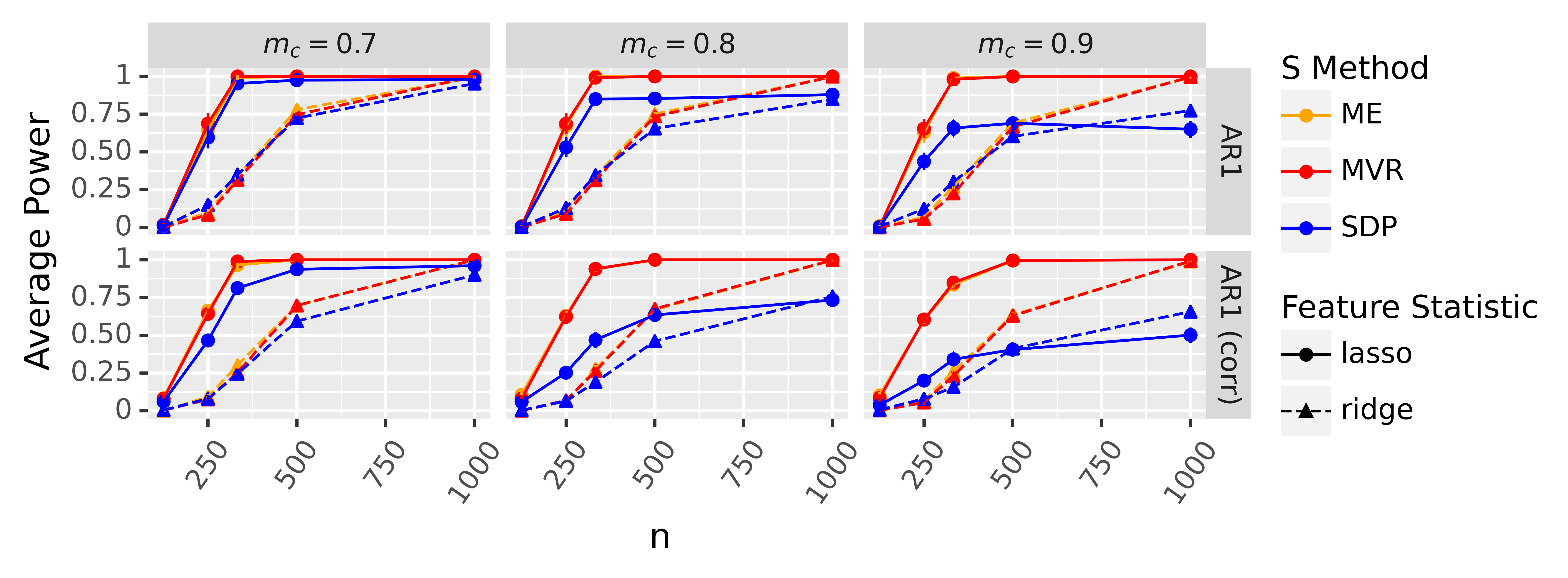

We defer a precise description of the covariance matrices in our simulations to Appendix F.4. However, we will give a brief overview of the types of in order to emphasize that these differ substantially from the equicorrelated case. In the “AR1” setting, for example, is a standardized Gaussian Markov chain with correlations sampled from . The “AR1 (Corr)” is the same setting except we cluster the non-nulls together along the chain, as we might expect in, e.g., genetic studies. Then, in the “ER (Cov)” and “ER (Precision)” settings, the covariance and precision matrices (respectively) are sparse, where the nonzero entries are chosen uniformly at random, in accordance with an ErdosRenyi (ER) procedure. Lastly, we include simulations when is block-equicorrelated with a block size of and within-block correlations of .

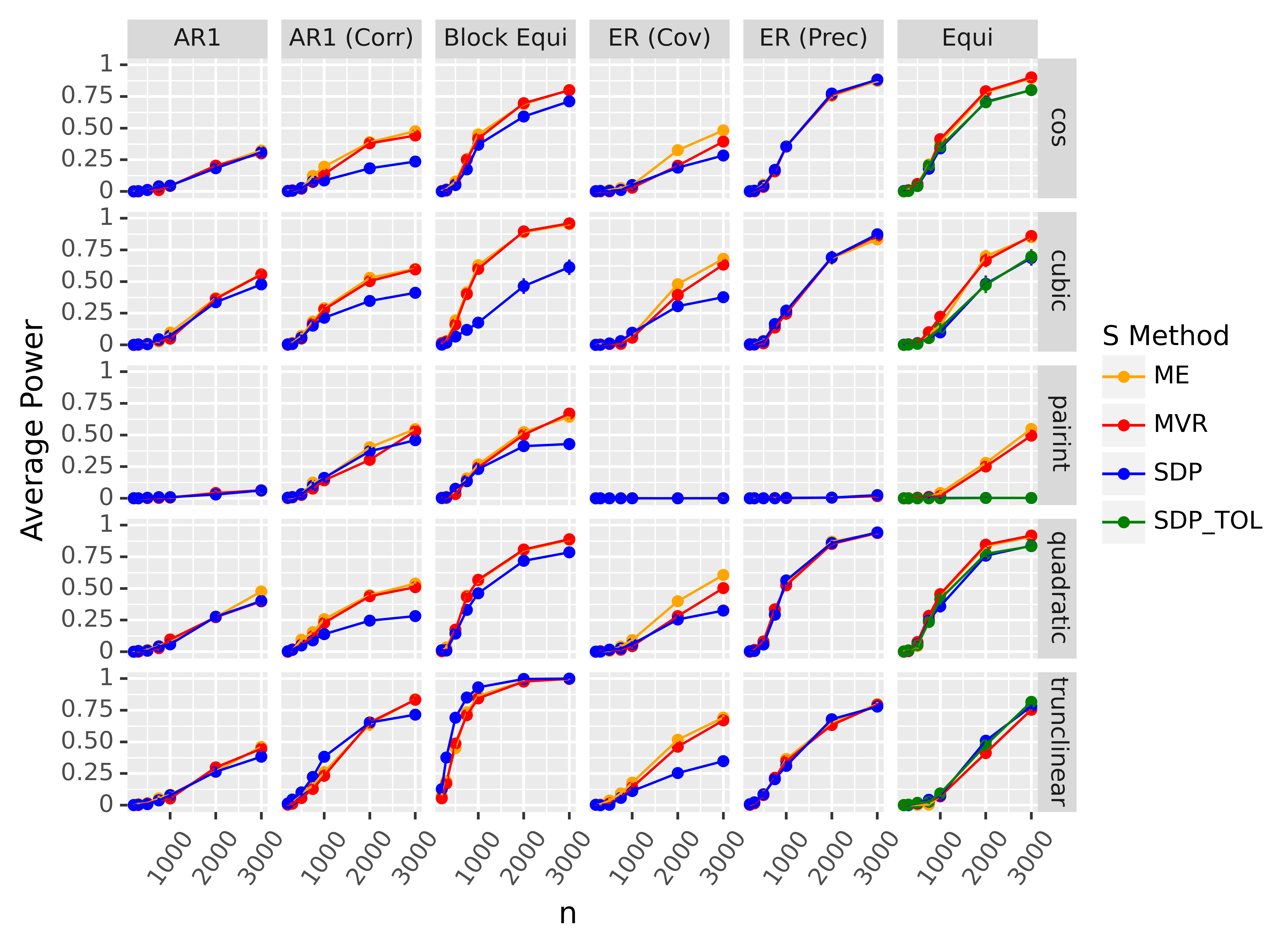

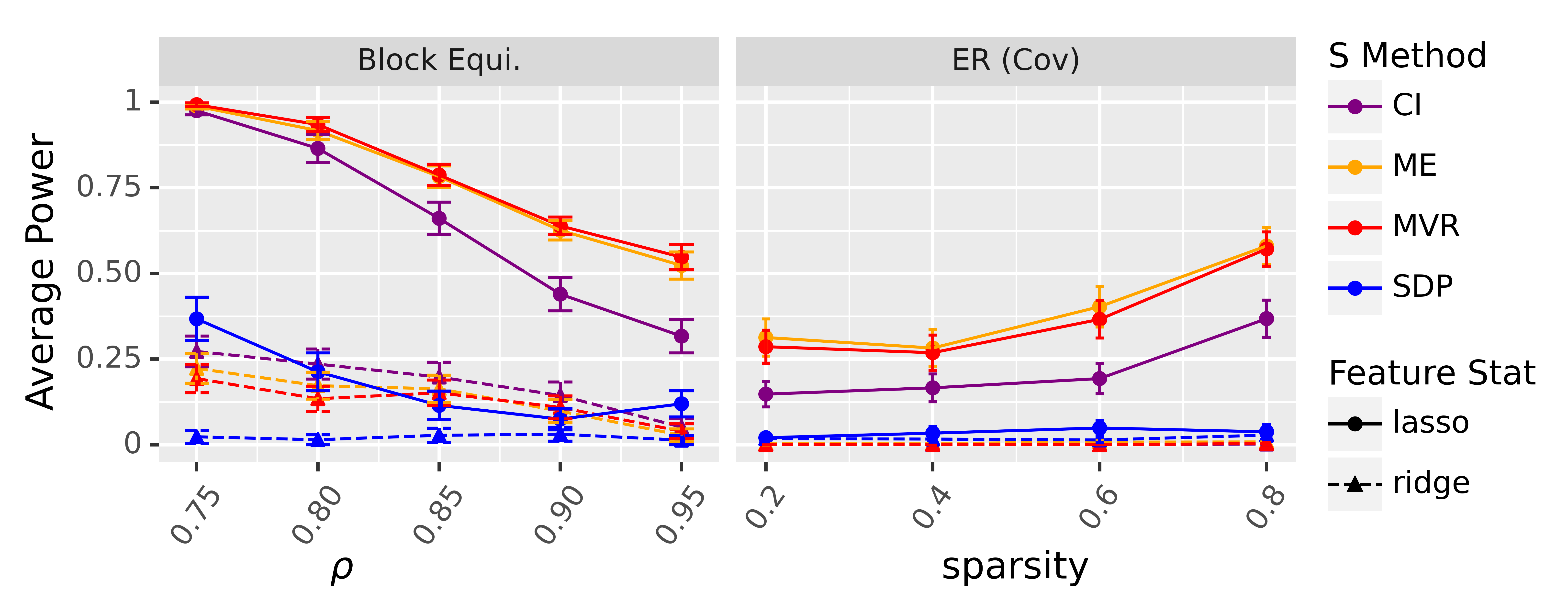

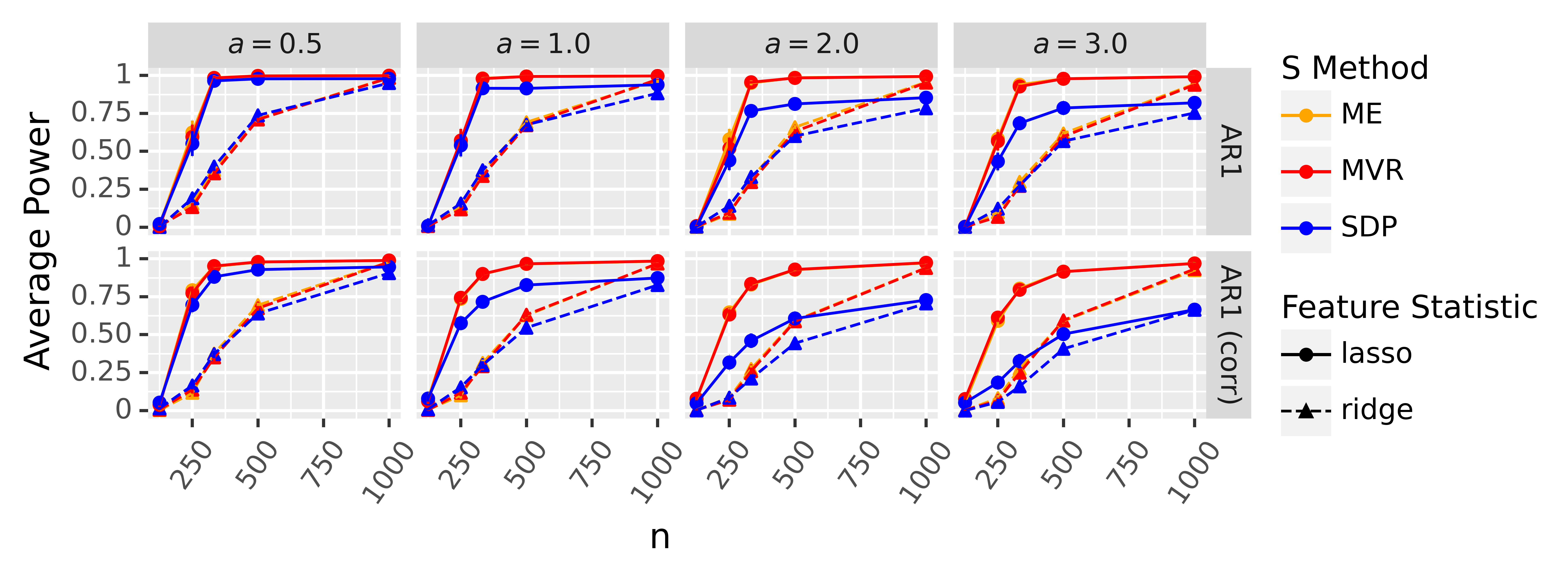

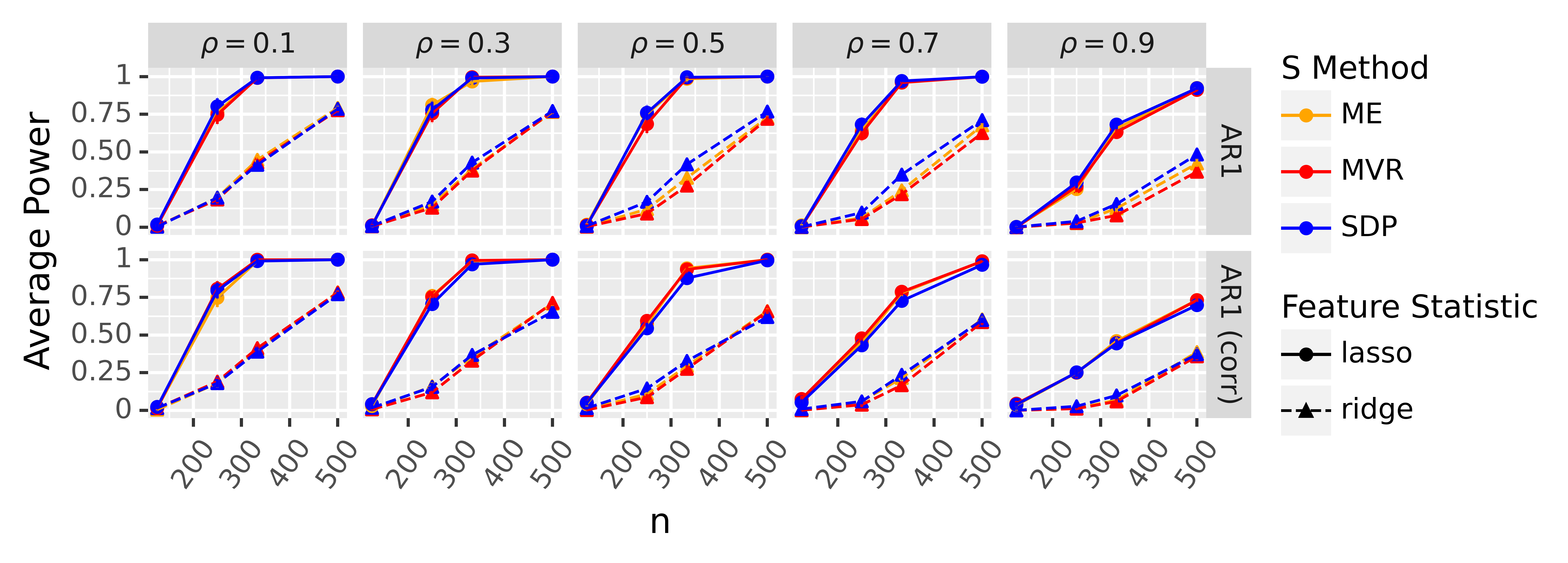

First, in Figure 4, we compare the power of MVR, ME, and SDP knockoffs when for sparse (see the caption for details). We use cross-validated lasso and ridge coefficient differences as feature statistics, and once again, we find that both MVR and ME knockoffs tend to substantially outperform SDP knockoffs.

In Appendix F.5, we also explore the effect of varying the between-feature correlations in the AR1 setting. As expected, higher correlations improve the performance of MRC knockoffs relative to SDP knockoffs, although interestingly, when the correlation is constant over all , the performances of all methods are quite similar. This result is broadly consistent with our theory, although we defer discussion to Appendix F.5.

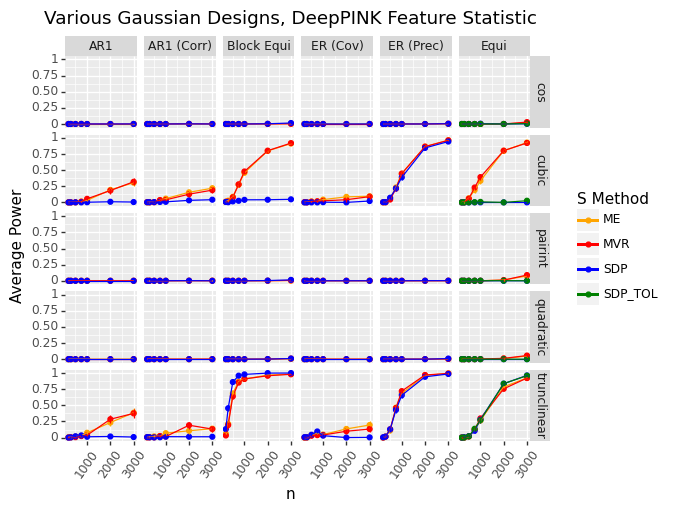

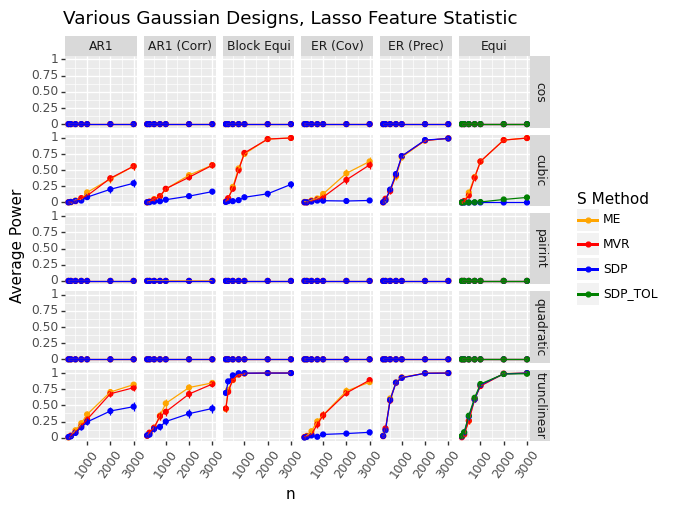

Next, we consider the case where where is a nonlinear sparse model. We defer precise descriptions of these to Appendix F.4, but we emphasize that they are highly nonlinear and never follows a single-index model. For example, in the “pairint” setting, for a sparse . Similarly, in the “cos” setting, , and since is an even function, this ensures the features have no linear effect on . For this reason, linear feature statistics like the lasso frequently have zero power even when is as large as , as demonstrated in Appendix F.6.

Since the conditional distribution is very complicated, knockoffs will not have much power except in fairly low-dimensional settings. For example, when is a linear response to pairwise interactions among the features, even a parametric feature statistic that searches explicitly for pairwise interactions must estimate coefficients. In contrast, a single-index model only requires estimation of parameters. As a result, we set with non-null values and vary between and .

We consider three feature statistics: a random forest feature statistic using the swap importance suggested by Gimenez et al., (2019), the DeepPINK feature statistic from Lu et al., (2018), and, as a baseline, the lasso coefficient difference. We report results for the random forest statistic in Figure 5. Results for the DeepPINK feature statistic and the lasso feature statistic are in Appendix F.6. In all three cases, MVR and ME knockoffs consistently outperform SDP knockoffs (although there are again a few exceptions to this, such as the truncated linear conditional mean on equicorrelated designs).

4.3 Robustness on Gaussian designs

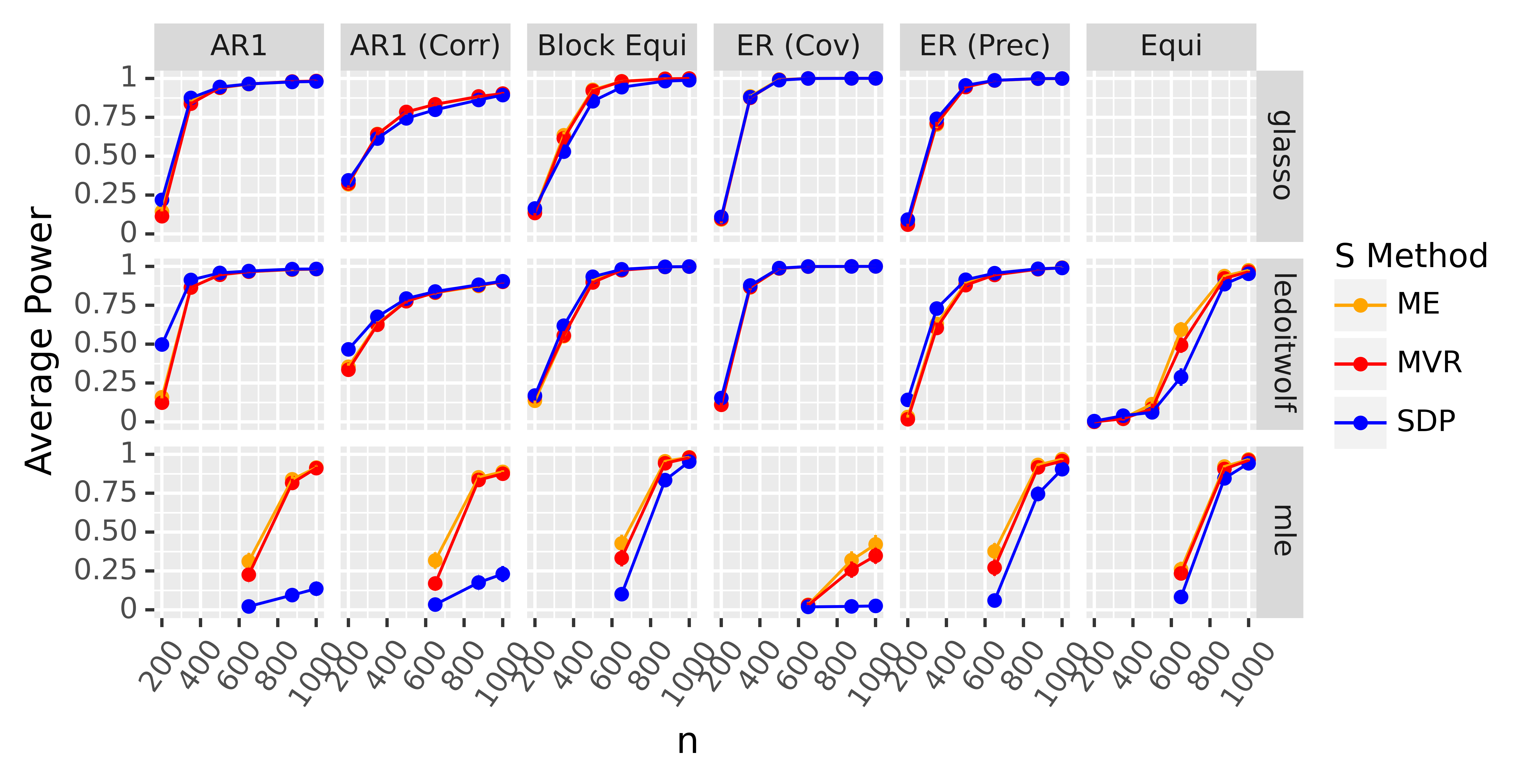

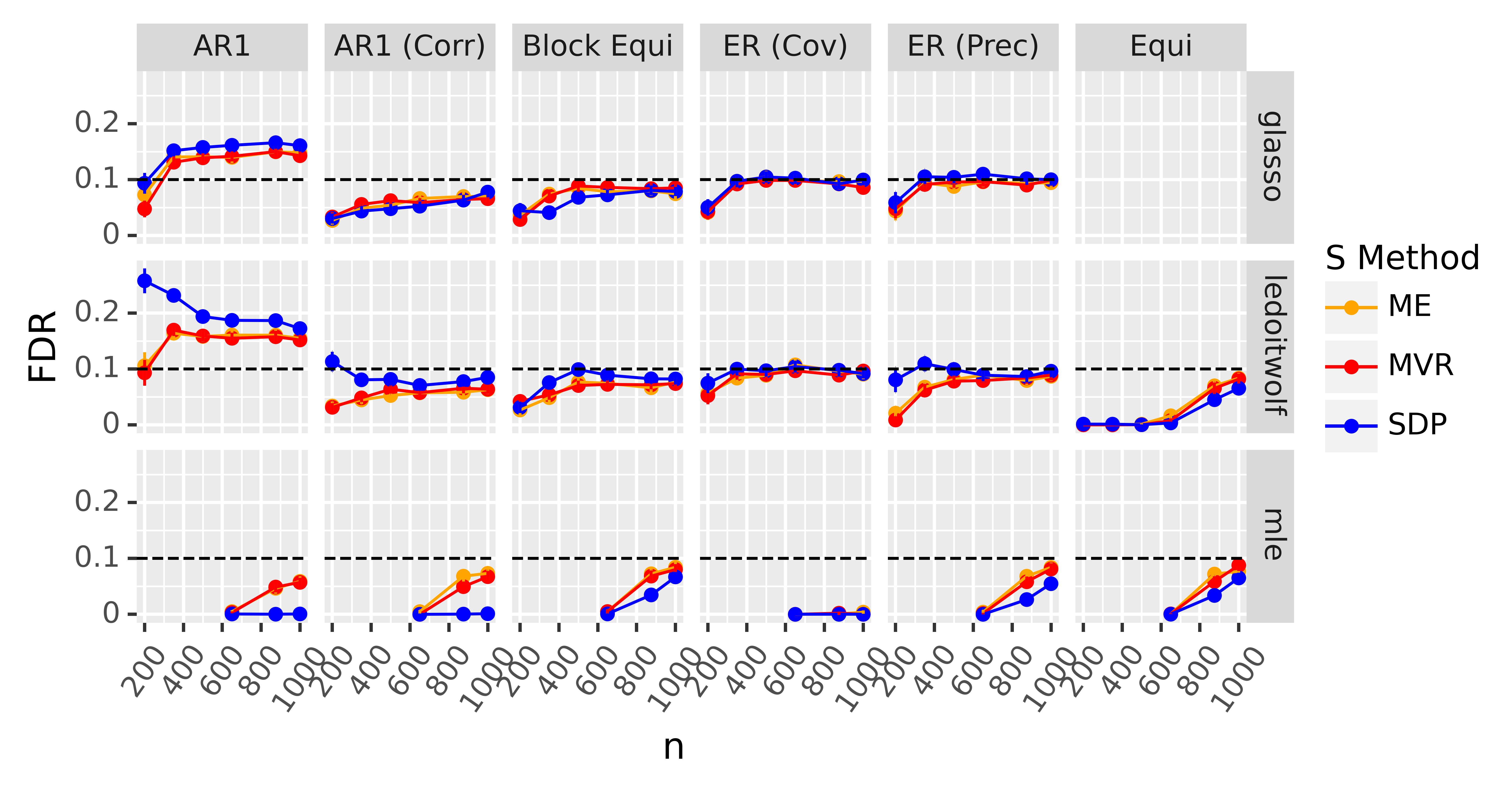

In Sections 2 through 4.2, we have assumed that we know the true covariance matrix . In this section, we analyze the robustness of MVR, ME, and SDP knockoffs when is not known and is estimated using the same data used to run knockoffs, using one of three methods: Ledoit–Wolf estimation (Ledoit and Wolf,, 2004), the graphical lasso algorithm (Friedman et al.,, 2007), and the maximum likelihood estimate of when . We let , and we use lasso coefficient difference statistics. Figures 6 (power) and 7 (FDR) show that MVR and ME knockoffs control the FDR better than SDP knockoffs, especially in high-dimensional settings where the covariance has been estimated using shrinkage methods. None of our theory predicted this, but it at least indicates that the power improvement of MVR/ME knockoffs over SDP knockoffs does not come at the expense of robustness. See the figure caption for more simulation details.

4.4 Application to fixed-X knockoffs

So far, we have worked with the MX knockoffs framework, where we assume we know the distribution of and we control the FDR in expectation over the distribution of . However, the idea behind MVR and ME knockoffs extends straightforwardly to the fixed-X (FX) knockoff filter, which treats the features as fixed and controls the FDR when follows a Gaussian linear model. In the fixed-X setting, we assume the Gram matrix has diagonals equal to and construct knockoffs such that

| (14) |

where as previously, is a diagonal matrix such that and . can be efficiently constructed when as outlined in Barber and Candès, (2015). From here on, the FX-knockoffs procedure is quite similar to the MX-knockoffs procedure, except that the feature statistics must obey a sufficiency constraint that they only depend on the matrix and the empirical covariances . Then, when , the FX knockoff filter provably controls the FDR in finite samples.

Although the features do not have conditional variances or entropy in this setting since they are treated as fixed, the MVR and ME losses in terms of naturally generalize to this setting. In particular, we set

| (15) |

Proposition 3.1 naturally extends to the FX setting, where the matrix minimizes the estimation error of OLS feature importances, except this time conditional on . See the proof of Proposition 3.1 for details.

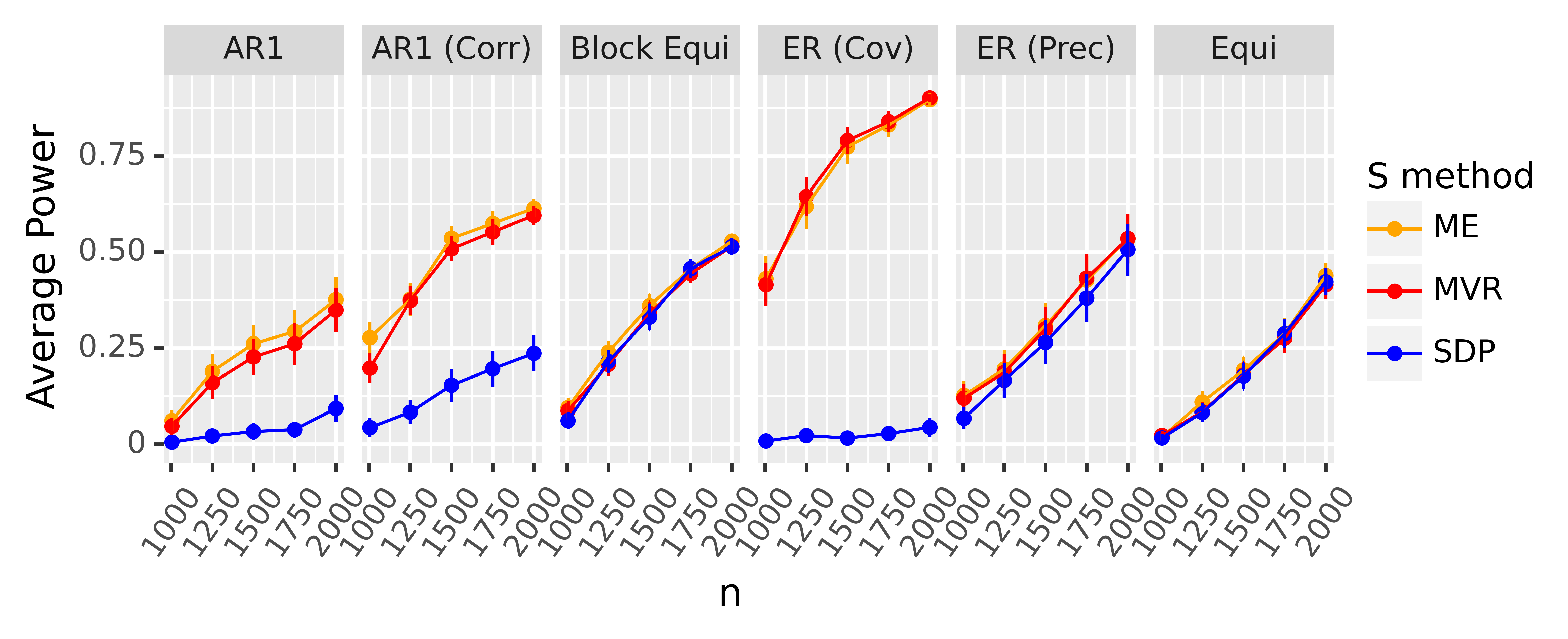

To study the power of MVR and ME FX knockoffs, we simulate for the same covariance matrices as in Section 4.2 and let for sparse (see the caption of Figure 8 for details). In order to obey the sufficiency property, FX feature statistics cannot use cross-validation, so we use the lasso signed max (LSM) statistic introduced in Barber and Candès, (2015) instead of cross-validated lasso and ridge coefficient differences. Figure 8 shows that MRC knockoffs generally outperform SDP knockoffs, although the power differential can be lower than in the MX case.

4.5 Application to group knockoffs

In this section, we show that the MRC framework can increase the power of group knockoffs Dai and Barber, (2016). In settings with highly correlated features, such as GWAS, some previous work has suggested partitioning the features into disjoint groups . After clustering the features such that the between-group correlations are suitably low, Dai and Barber, (2016) showed how to construct “group knockoffs” which test the group-level hypotheses . Such group knockoffs need only satisfy a relaxed pairwise-exchangeability constraint, where the distribution of is invariant to swaps of entire groups, but not necessarily swaps of individual features. Although grouping the features can reduce correlations between the groups, it generally will not remove all dependence from the data (see Candès et al., (2018); Dai and Barber, (2016)), motivating the construction of MRC group knockoffs. One can construct MRC group knockoffs by minimizing the MRC loss functions and subject to this relaxed constraint.

Figure 9 compares the powers of MRC and SDP group knockoffs in the AR1 settings studied in Section 4.2. To partition the features, we hierarchically cluster the features using correlations as a similarity measure and a single-linkage cutoff of , where we vary between , which recovers the ungrouped procedure, and . The results show that MRC group knockoffs consistently outperform SDP group knockoffs.

4.6 Application to non-Gaussian designs

So far, we have focused on the case where . Now, we consider the non-Gaussian case. To do this, we first review two general methods of constructing knockoffs for non-Gaussian features.

First, Candès et al., (2018) proposed an approximate second-order knockoff construction for the non-Gaussian case. In particular, if has mean zero and , the authors considered picking an -matrix and sampling

| (16) |

This guarantees that the first two moments of and match, and moreover that as in the Gaussian case. These are not valid knockoffs and do not guarantee FDR control, but they may be fairly robust in practice. Furthermore, second-order knockoffs only require knowledge of the first two moments of , as opposed to the joint density function. Candès et al., (2018) suggested setting in equation (16). We will demonstrate below that and are more powerful alternatives.

Second, the Metropolized knockoff sampler introduced in Bates et al., (2020) allows one to sample exact, valid knockoffs for arbitrary distributions of under the assumption that the unnormalized density of is known. Given an ordering of the features , the key idea is to sample by taking a step along a time-reversible Markov chain starting from , such that is the stationary distribution of the chain. To accomplish this, Bates et al., (2020) employ a Metropolis–Hastings style proposal and acceptance scheme to ensure the exact validity of the knockoffs. The authors suggested using Gaussian covariance-guided proposals, where the Metropolis–Hastings proposals are sampled as second-order knockoffs according to equation (16). In the following simulations, we will generate second-order proposals using the MVR, ME, and SDP -matrices and then compare their power.

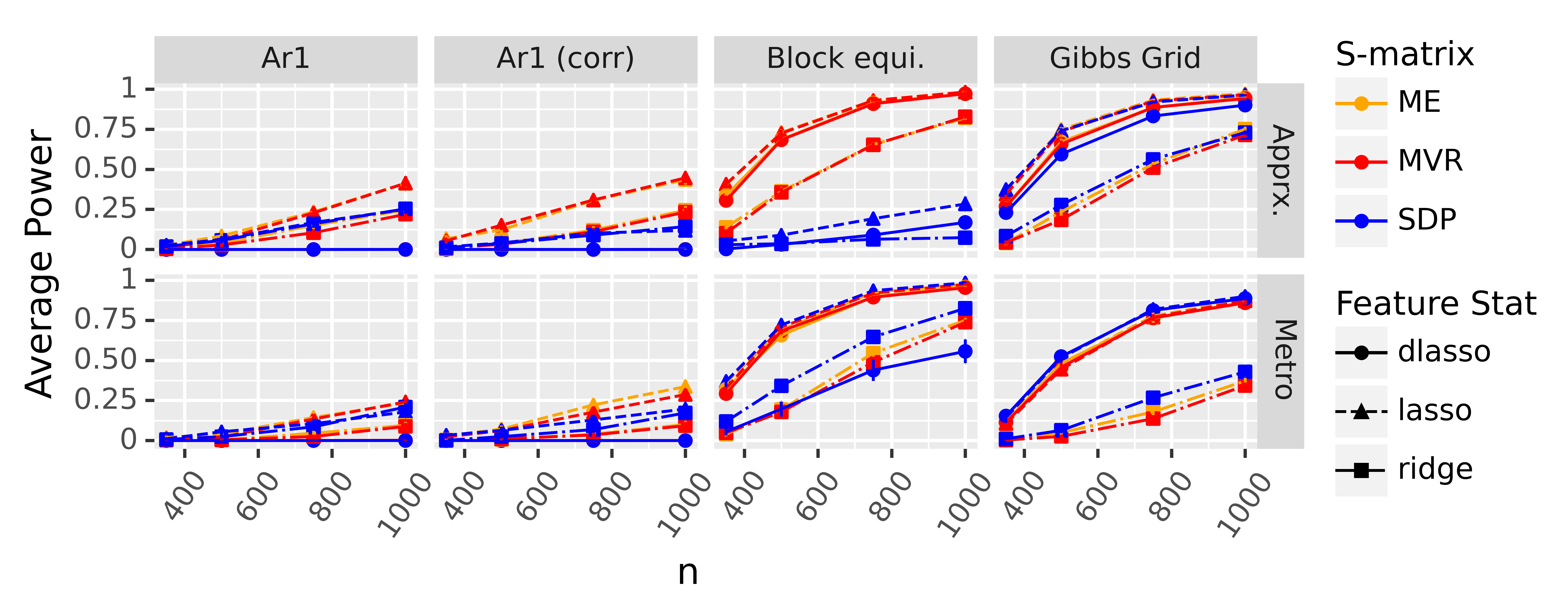

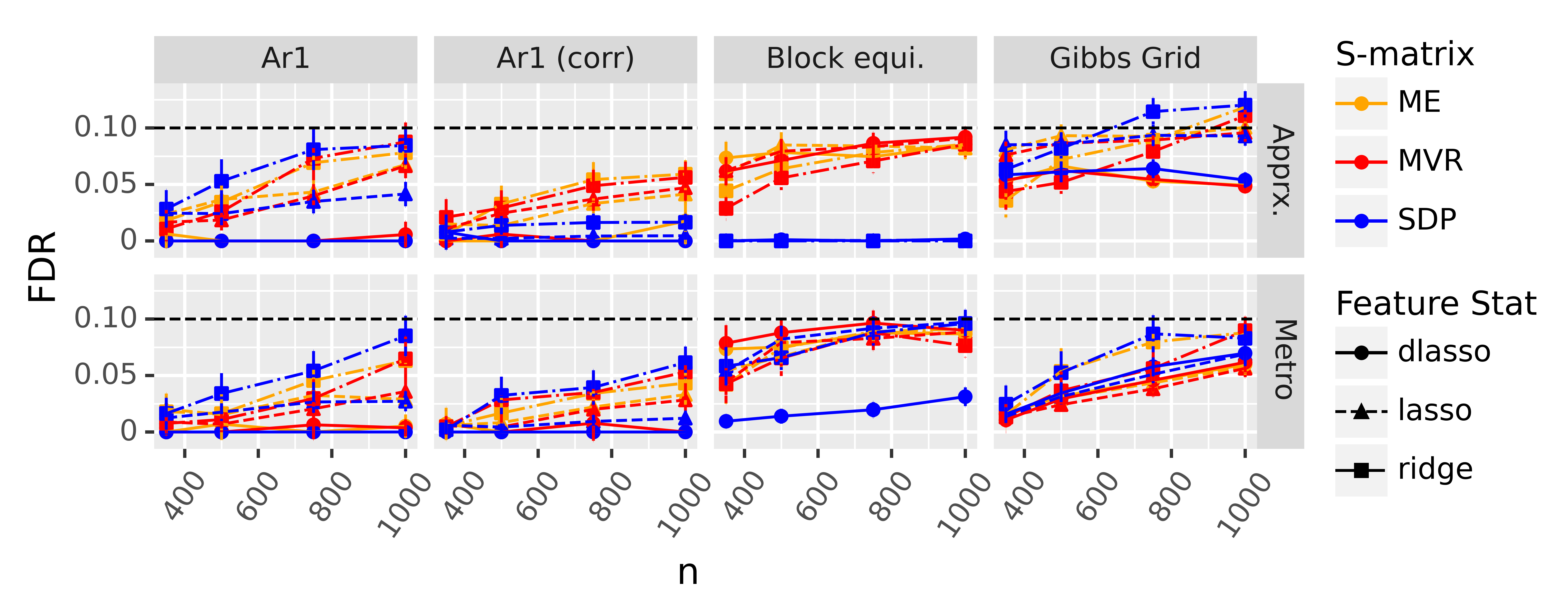

We consider three types of non-Gaussian designs: a -tailed Markov chain discussed in Bates et al., (2020) with and without correlated signals, a “block-equicorrelated” design where each block is independently -distributed with an equicorrelated covariance matrix, and a Gibbs measure on a grid. In all cases, the features differ substantially from the Gaussian case: for example, in the first two settings, we let our distributions have degrees of freedom. See Appendix F.7 for more details on the precise design distributions as well as our knockoff generation mechanism for the “discrete grid” model.

In Figure 10, we let with similar as before (see the captions for details). We test three types of feature statistics: lasso coefficient differences, ridge coefficient differences, and debiased lasso (dlasso) coefficient differences (Javanmard and Montanari,, 2014).

We make two observations about these plots. First, the only difference between the second-order and Metropolized knockoff procedures is that the Metropolized sampling procedure takes the second-order knockoffs as proposals and sometimes rejects these knockoffs, setting in the case of a rejection. These rejections increase the marginal correlations between and , but outside of the Gibbs grid model, the SDP-guided Metropolized knockoffs have more power than their second-order counterparts. We interpret this as evidence that the reconstruction effect can still occur for non-Gaussian designs, and the Metropolis rejections (inadvertently) correct for this effect by increasing the marginal feature-knockoff correlations. Second, we observe that the MRC second-order knockoffs are substantially more powerful than their SDP counterparts. For the Metropolized knockoff sampler, the MVR and ME proposals increase the power of debiased lasso statistics while decreasing the power of the ridge statistics. The lasso power is fairly similar between all three methods throughout. We present the corresponding FDR plot in Appendix F.7.

Lastly, a few other works have introduced methods to sample approximate knockoffs when the distribution of is unknown, using tools from the machine learning literature Romano et al., (2018); Jordon et al., (2019). These constructions generally use pairwise dependency measures such as the MAC as part of their optimization criteria, but we expect it to be straightforward to “plug in” the MRC objective criteria in place of the MAC. For example, one could repeatedly resample to estimate , although we leave such details to future work.

5 Discussion

This paper identifies an important flaw in previous knockoff generation mechanisms, which reduces power by allowing regression test statistics like the lasso to reconstruct non-null features using the other features and knockoffs. To solve this problem, we introduced minimum reconstructability knockoffs, which substantially increase the power of knockoffs for correlated designs. However, our work leaves several questions open for future research.

One immediate question is how to construct exact MRC knockoffs for non-Gaussian designs. Our technique in Section 4.6 minimizes the reconstructability of the proposal knockoffs in the Metropolized knockoff sampling framework, but the actual knockoffs may have different properties due to the complex acceptance scheme of the sampler. Additionally, Huang and Janson, (2020) introduced the idea of conditional knockoffs, which enable FDR control when the distribution of is only known up to a parametric model. Constructing conditional MRC knockoffs may be practically useful, but it is not obvious even how to define conditional MRC knockoffs, with the exception of the Gaussian case, where conditional MRC knockoffs can be defined analagously to fixed-X MRC knockoffs (see Section 4.4).

Interestingly, for discrete designs with finite support, computing the distribution of ME knockoffs corresponds to a maximum entropy problem with linear constraints (see Appendix E for details). Such problems are convex and well studied (Persson and Clarke,, 1986; Boyd and Vandenberghe,, 2004), but the number of optimization variables and constraints grow exponentially with , making the problem intractable. We discuss three potential ways around this in Appendix E, including using conditional independence properties of , restricting the class of feasible knockoff distributions, or finding approximate solutions, but further study is needed.

Another interesting future direction would be to better understand the notion of reconstructability. For example, we observed in Section 2 that the reconstruction effect gets worse when feature statistics can reconstruct non-null features using sparse subsets of the other features and knockoffs. This can occur when is particularly low rank, but it can also occur when the eigenvectors of corresponding to small eigenvalues are (approximately) sparse. It may therefore be fruitful to incorporate the structure of the eigenvectors of into knockoff generation mechanisms. Alternatively, we have advocated minimizing two specific measures of reconstructability, but we have not thoroughly investigated other possibilities. Further analysis on this front may turn out to further improve power.

Acknowledgements

The authors would like to thank Chenguang Dai, Buyu Lin, Jun Liu, Wenshuo Wang, and Xin Xing for valuable discussions and suggestions. The authors are also grateful to the anonymous referees for helpful comments. L. J. was partially supported by the William F. Milton Fund.

References

- Anderson, (2009) Anderson, T. (2009). An Introduction to Multivariate Statistical Analysis. Wiley india pvt. limited. edition.

- Arratia and Gordon, (1989) Arratia, R. and Gordon, L. (1989). Tutorial on large deviations for the binomial distribution. Bulletin of Mathematical Biology, 51(1):125–131.

- Askari et al., (2020) Askari, A., Rebjock, Q., d’Aspremont, A., and Ghaoui, L. E. (2020). Fanok: Knockoffs in linear time. arXiv preprint arXiv:2006.08790.

- Barber and Candès, (2015) Barber, R. F. and Candès, E. J. (2015). Controlling the false discovery rate via knockoffs. Ann. Statist., 43(5):2055–2085.

- Barber and Candès, (2019) Barber, R. F. and Candès, E. J. (2019). A knockoff filter for high-dimensional selective inference. Ann. Statist., 47(5):2504–2537.

- Barber et al., (2020) Barber, R. F., Candès, E. J., and Samworth, R. J. (2020). Robust inference with knockoffs. Ann. Statist., 48(3):1409–1431.

- Bates et al., (2020) Bates, S., Candès, E., Janson, L., and Wang, W. (2020). Metropolized knockoff sampling. Journal of the American Statistical Association, 0(0):1–15.

- Boyd and Vandenberghe, (2004) Boyd, S. and Vandenberghe, L. (2004). Convex Optimization. Cambridge University Press, USA.

- Candès et al., (2018) Candès, E., Fan, Y., Janson, L., and Lv, J. (2018). Panning for gold: ‘model-x’ knockoffs for high dimensional controlled variable selection. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(3):551–577.

- Chen et al., (2019) Chen, J., Hou, A., and Hou, T. Y. (2019). A prototype knockoff filter for group selection with FDR control. Information and Inference: A Journal of the IMA, 9(2):271–288.

- Dai et al., (2020) Dai, C., Lin, B., Xing, X., and Liu, J. S. (2020). False discovery rate control via data splitting. arXiv preprint arXiv:2002.08542.

- Dai and Barber, (2016) Dai, R. and Barber, R. (2016). The knockoff filter for fdr control in group-sparse and multitask regression. volume 48 of Proceedings of Machine Learning Research, pages 1851–1859, New York, New York, USA. PMLR.

- Devroye et al., (2018) Devroye, L., Mehrabian, A., and Reddad, T. (2018). The total variation distance between high-dimensional gaussians. arXiv preprint arXiv:1810.08693.

- Fan et al., (2020) Fan, Y., Demirkaya, E., Li, G., and Lv, J. (2020). Rank: Large-scale inference with graphical nonlinear knockoffs. Journal of the American Statistical Association, 115(529):362–379. PMID: 32742045.

- Friedman et al., (2007) Friedman, J., Hastie, T., and Tibshirani, R. (2007). Sparse inverse covariance estimation with the graphical lasso. Biostatistics, 9(3):432–441.

- Gimenez et al., (2019) Gimenez, J. R., Ghorbani, A., and Zou, J. Y. (2019). Knockoffs for the mass: New feature importance statistics with false discovery guarantees. In Chaudhuri, K. and Sugiyama, M., editors, The 22nd International Conference on Artificial Intelligence and Statistics, AISTATS 2019, 16-18 April 2019, Naha, Okinawa, Japan, volume 89 of Proceedings of Machine Learning Research, pages 2125–2133. PMLR.

- Gimenez and Zou, (2019) Gimenez, J. R. and Zou, J. (2019). Improving the stability of the knockoff procedure: Multiple simultaneous knockoffs and entropy maximization. In Chaudhuri, K. and Sugiyama, M., editors, Proceedings of Machine Learning Research, volume 89, pages 2184–2192. PMLR.

- Huang and Janson, (2020) Huang, D. and Janson, L. (2020). Relaxing the assumptions of knockoffs by conditioning. Ann. Statist., 48(5):3021–3042.

- Ising, (1925) Ising, E. (1925). Beitrag zur Theorie des Ferromagnetismus. Zeitschrift fur Physik, 31(1):253–258.

- Javanmard and Montanari, (2014) Javanmard, A. and Montanari, A. (2014). Confidence intervals and hypothesis testing for high-dimensional regression. J. Mach. Learn. Res., 15(1):2869–2909.

- Jordon et al., (2019) Jordon, J., Yoon, J., and van der Schaar, M. (2019). KnockoffGAN: Generating knockoffs for feature selection using generative adversarial networks. In International Conference on Learning Representations.

- Ke et al., (2020) Ke, Z. T., Liu, J. S., and Ma, Y. (2020). Power of fdr control methods: The impact of ranking algorithm, tampered design, and symmetric statistic. arXiv preprint: arXiv:2010.08132.

- Ledoit and Wolf, (2004) Ledoit, O. and Wolf, M. (2004). A well-conditioned estimator for large-dimensional covariance matrices. J. Multivar. Anal., 88(2):365–411.

- Li and Maathuis, (2019) Li, J. and Maathuis, M. H. (2019). Ggm knockoff filter: False discovery rate control for gaussian graphical models.

- Liu and Rigollet, (2019) Liu, J. and Rigollet, P. (2019). Power analysis of knockoff filters for correlated designs. In Wallach, H., Larochelle, H., Beygelzimer, A., d'Alché-Buc, F., Fox, E., and Garnett, R., editors, Advances in Neural Information Processing Systems 32, pages 15446–15455. Curran Associates, Inc.

- Lu et al., (2018) Lu, Y. Y., Fan, Y., Lv, J., and Noble, W. S. (2018). Deeppink: reproducible feature selection in deep neural networks. In Bengio, S., Wallach, H. M., Larochelle, H., Grauman, K., Cesa-Bianchi, N., and Garnett, R., editors, Advances in Neural Information Processing Systems 31: Annual Conference on Neural Information Processing Systems 2018, NeurIPS 2018, 3-8 December 2018, Montréal, Canada, pages 8690–8700.

- Nakkiran et al., (2020) Nakkiran, P., Kaplun, G., Bansal, Y., Yang, T., Barak, B., and Sutskever, I. (2020). Deep double descent: Where bigger models and more data hurt. In 8th International Conference on Learning Representations, ICLR 2020, Addis Ababa, Ethiopia, April 26-30, 2020. OpenReview.net.

- Oikonomou and Grünwald, (2016) Oikonomou, K. N. and Grünwald, P. D. (2016). Explicit bounds for entropy concentration under linear constraints. IEEE Transactions on Information Theory, 62(3):1206–1230.

- Pedregosa et al., (2011) Pedregosa, F., Varoquaux, G., Gramfort, A., Michel, V., Thirion, B., Grisel, O., Blondel, M., Prettenhofer, P., Weiss, R., Dubourg, V., Vanderplas, J., Passos, A., Cournapeau, D., Brucher, M., Perrot, M., and Duchesnay, E. (2011). Scikit-learn: Machine learning in Python. Journal of Machine Learning Research, 12:2825–2830.

- Persson and Clarke, (1986) Persson, H. and Clarke, R. M. (1986). Algorithm 12: Solving the entropy maximization problem with equality and inequality constraints. Environment and Planning A: Economy and Space, 18(12):1665–1676.

- Pipeleers and Vandenberghe, (2011) Pipeleers, G. and Vandenberghe, L. (2011). Generalized KYP lemma with real data. IEEE Trans. Autom. Control., 56(12):2942–2946.

- Romano et al., (2018) Romano, Y., Sesia, M., and Candès, E. J. (2018). Deep knockoffs.

- Sesia et al., (2020) Sesia, M., Bates, S., Candès, E., Marchini, J., and Sabatti, C. (2020). Controlling the false discovery rate in gwas with population structure. bioRxiv.

- Sesia et al., (2019) Sesia, M., Katsevich, E., Bates, S., Candès, E., and Sabatti, C. (2019). Multi-resolution localization of causal variants across the genome. bioRxiv.

- Sesia et al., (2018) Sesia, M., Sabatti, C., and Candès, E. J. (2018). Gene hunting with hidden Markov model knockoffs. Biometrika, 106(1):1–18.

- Vandenberghe et al., (1998) Vandenberghe, L., Boyd, S., and Wu, S.-P. (1998). Determinant maximization with linear matrix inequality constraints. SIAM J. Matrix Anal. Appl., 19(2):499–533.

- Xing et al., (2019) Xing, X., Zhao, Z., and Liu, J. S. (2019). Controlling false discovery rate using gaussian mirrors.

Appendix A Proofs for Section 2

A.1 Proofs for the general reconstruction effect

In this section, we prove some general facts about the reconstruction effect, which we will apply to the equicorrelated case in the following section. To start, we prove Lemma 2.1, which shows that when is Gaussian, minimizing the MAC will often cause to be low rank.

Lemma 2.1.

Suppose and . Then . Furthermore, if is block-diagonal with blocks, each with an eigenvalue below , then .

Proof.

The eigenvalues of are the eigenvalues of and . The case where is trivial, as we can set , which implies will have at least one eigenvalue that equals .

When , assume for sake of contradiction that is full rank, and thus . This implies as well. Represent and denote , where the minimum is taken element-wise over the vector.

By the previous argument, is a feasible -matrix with lower mean absolute correlation than . Therefore, cannot be the solution to the SDP. This is a contradiction and completes the proof of the non-block-diagonal statement. The block-diagonal statement follows because when is block-diagonal, the solution to the SDP is the SDP solution to each of the blocks (Barber and Candès,, 2015). ∎

Next we prove Theorem 2.3, which we very slightly restate to make it easier to apply in our later proofs. We use to denote elementwise multiplication.

Theorem 2.3.

Suppose we can represent for some set , functions and , and independent noise . Equivalently, this means . Suppose a function exists such that holds almost surely. If , then

In particular, this implies

| (17) |

which ensures .

Proof.

Note that since , also implies . Thus, we can rewrite

This means that . Since marginally , this implies

The former equality holds for each i.i.d. row and therefore holds for the matrix versions . Since is a function of and must obey the knockoff antisymmetry property, we obtain that

For each , this proves . ∎

A.2 Simple proofs for block-equicorrelated Gaussian designs

In this section, we will prove Lemma 2.2 and apply Theorem 2.3 to the equicorrelated case. These will be important tools for our later proof of Theorem 2.4.

Lemma 2.2.

In the equicorrelated case when , let be generated according to the SDP procedure. Then has rank , and for all .

Proof.

To find the solution for the SDP, we simply verify that by checking the KKT conditions in Lemma B.1. Then, we have

First, we note that the eigenvalues of are those of and . Note, however, that , so , which has a rank of . Since has full rank, this implies that has rank .

To show that remains constant over all , denote the th column of as . Simple arithmetic shows that . This implies that if is the vector of all zeros except and , then . If is a symmetric square root of , this implies .

Now, let . We may represent . Using this representation, we conclude

∎

Corollary A.1.

Suppose and is equicorrelated with correlation at least , for . Let be the set of indices corresponding to block . Then for all , if are SDP knockoffs.

Proof.

This follows directly from Lemma 2.2 since the solution to the SDP for a block-diagonal matrix is simply the diagonal matrix composed of the solutions to the blocks . ∎

Corollary A.1 allows us to apply Theorem 2.3 to the block-equicorrelated case. We define some notation before doing this.

Definition A.1 (Negation Notation).

For coefficients and , define . For the response variable , define , where denotes elementwise multiplication.

Note that in the follow Corollary, corresponds to in the Theorem 2.3.

Corollary A.2.