Bayesian Bootstrap Spike-and-Slab LASSO

Abstract

The impracticality of posterior sampling has prevented the widespread adoption of spike-and-slab priors in high-dimensional applications. To alleviate the computational burden, optimization strategies have been proposed that quickly find local posterior modes. Trading off uncertainty quantification for computational speed, these strategies have enabled spike-and-slab deployments at scales that would be previously unfeasible. We build on one recent development in this strand of work: the Spike-and-Slab LASSO procedure of Ročková and George (2018). Instead of optimization, however, we explore multiple avenues for posterior sampling, some traditional and some new. Intrigued by the speed of Spike-and-Slab LASSO mode detection, we explore the possibility of sampling from an approximate posterior by performing MAP optimization on many independently perturbed datasets. To this end, we explore Bayesian bootstrap ideas and introduce a new class of jittered Spike-and-Slab LASSO priors with random shrinkage targets. These priors are a key constituent of the Bayesian Bootstrap Spike-and-Slab LASSO (BB-SSL) method proposed here. BB-SSL turns fast optimization into approximate posterior sampling. Beyond its scalability, we show that BB-SSL has a strong theoretical support. Indeed, we find that the induced pseudo-posteriors contract around the truth at a near-optimal rate in sparse normal-means and in high-dimensional regression. We compare our algorithm to the traditional Stochastic Search Variable Selection (under Laplace priors) as well as many state-of-the-art methods for shrinkage priors. We show, both in simulations and on real data, that our method fares very well in these comparisons, often providing substantial computational gains.

Keywords: Bayesian Bootstrap, Posterior Contraction, Spike-and-Slab LASSO, Weighted Likelihood Bootstrap.

1 Posterior Sampling under Shrinkage Priors

Variable selection is arguably one of the most widely used dimension reduction techniques in modern statistics. The default Bayesian approach to variable selection assigns a probabilistic blanket over models via spike-and-slab priors Mitchell and Beauchamp (1988); George and McCulloch (1993). The major conceptual appeal of the spike-and-slab approach is the availability of uncertainty quantification for both model parameters as well as models themselves (Madigan and Raftery (1994)). However, practical costs of posterior sampling can be formidable given the immense scope of modern analyses. The main thrust of this work is to extend the reach of existing posterior sampling algorithms in new faster directions.

This paper focuses on the canonical linear regression model, where a vector of responses is stochastically linked to fixed predictors through

| (1) |

where and where is a possibly sparse vector of regression coefficients. In this work, we assume that is known and we refer to Moran et al. (2019) for elaborations with an unknown variance. We assume that the vector and the regressors have been centered and, thereby, we omit the intercept. In the presence of uncertainty about which subset of is in fact nonzero, one can assign a prior distribution over the regression coefficients as well as the pattern of nonzeroes where for whether or not the effect is active. This formalism can be condensed into the usual spike-and-slab prior form

| (2) |

where are scale parameters and where is a highly concentrated prior density around zero (the spike) and is a diffuse density (the slab). The dual purpose of the spike-and-slab prior is to (a) shrink small signals towards zero and (b) keep large signals intact. The most popular incarnations of the spike-and-slab prior include: the point-mass spike (Mitchell and Beauchamp (1988)), the non-local slab priors (Johnson and Rossell (2012)), the Gaussian mixture (George and McCulloch (1993)), the Student mixture (Ishwaran and Rao (2005)). More recently, Ročková (2018a) proposed the Spike-and-Slab LASSO (SSL) prior, a mixture of two Laplace distributions and where , which forms a continuum between the point-mass mixture prior and the LASSO prior (Park and Casella (2008)).

Posterior sampling under spike-and-slab priors is notoriously difficult. Dating back to at least 1993 (George and McCulloch, 1993), multiple advances have been made to speed up spike-and-slab posterior simulation (George and McCulloch (1997), Bottolo and Richardson (2010), Clyde et al. (2011), Hans (2009), Johndrow et al. (2020), Welling and Teh (2011), Xu et al. (2014)). More recently, several clever computational tricks have been suggested that avoid costly matrix inversions by using linear solvers (Bhattacharya et al., 2016) or by disregarding correlations between active and inactive coefficients (Narisetty et al., 2019). Neuronized priors have been proposed (Shin and Liu (2018)) that offer computational benefits by using close approximations to spike-and-slab priors without latent binary indicators. Modern applications have nevertheless challenged MCMC algorithms and new computational strategies are desperately needed to keep pace with big data.

Optimization strategies have shown great promise and enabled deployment of spike-and-slab priors at scales that would be previously unfeasible (Ročková and George (2014), Ročková and George (2018), Carbonetto and Stephens (2012)). Fast posterior mode detection is effective in structure discovery and data exploration, a little less so for inference. In this paper, we review and propose new strategies for posterior sampling under the Spike-and-Slab LASSO priors, filling the gap between exploratory data analysis and proper statistical inference.

We capitalize on the latest MAP optimization and MCMC developments to provide several posterior sampling implementations for the Spike-and-Slab LASSO method of Ročková and George (2018). The first one (presented in Algorithm 1) is exact and conventional, following in the footsteps of Stochastic Search Variable Selection (George and McCulloch, 1993)). The second one is approximate and new. The cornerstone of this strategy is the Weighted Likelihood Bootstrap (WLB) of Newton and Raftery (1994) which was recently resurrected in the context of posterior sampling with sparsity priors by Newton et al. (2020), Fong et al. (2019) and Ng and Newton (2020). The main idea behind WLB is to perform approximate sampling by independently optimizing randomly perturbed likelihood functions. We extend the WLB framework by incorporating perturbations both in the likelihood and in the prior. The main contributions of this work are two-fold. First, we introduce BB-SSL (Bayesian Bootstrap Spike-and-Slab LASSO), a novel algorithm for approximate posterior sampling in high-dimensional regression under Spike-and-Slab LASSO priors. Second, we show that suitable “perturbations” lead to approximate posteriors that contract around the truth at the same speed (rate) as the actual posterior. These theoretical results have nontrivial practical implications as they offer guidance on the choice of the distribution for perturbing weights. Up until now, theoretical properties of WLB have largely concentrated on consistency statements in low dimensions for iid data (Newton and Raftery (1994)). More recently, Ng and Newton (2020) established conditional consistency (asymptotic normality) in the context of LASSO regression for a fixed dimensionality and model selection consistency for a growing dimensionality. Our theoretical results also allow the dimensionality to increase with the sample size and go beyond mere consistency by showing that BB-SSL leads to rate-optimal estimation in sparse normal-means and high-dimensional regression under standard assumptions. Last but not least, we make thorough comparisons with the gold standard (i.e. exact MCMC sampling) on multiple simulated and real datasets, concluding that the proposed algorithm is scalable and reliable in practice. BB-SSL is (a) unapologetically parallelisable, and (b) it does not require costly matrix inversions (due to its coordinate-wise optimization nature), thereby having the potential to meet the demands of large datasets.

The structure of this paper is as follows. Section 1.1 introduces the notation. Section 2 revisits Spike-and-Slab LASSO and presents a traditional algorithm for posterior sampling. Section 3 investigates performance of weighted Bayesian bootstrap, the building block of this work, in high dimensions. In Section 4, we introduce BB-SSL and present our theoretical study showing rate-optimality as well as its connection with other bootstrap methods. Section 5 shows simulated examples and Section 6 shows performance on real data. We conclude the paper with a discussion in Section 7.

1.1 Notation

With we denote the Gaussian density with a mean and a variance . We use to denote convergence in distribution. We write if for any , there exist finite and such that for any . We write if for any , . We also write as . We use if and . We use to denote and to denote . We denote with a sub-matrix consisting of columns of ’s indexed by a subset and with the orthogonal projection to the range of (Zhang and Zhang, 2012), i.e., where is the Moore-Penrose inverse of . We denote with the matrix operator norm of .

2 Spike-and-Slab LASSO Revisited

The Spike-and-Slab LASSO (SSL) procedure of Ročková and George (2018) recently emerged as one of the more successful non-convex penalized likelihood methods. Various SSL incarnations have spawned since its introduction, including a version for group shrinkage (Bai et al. (2020), Tang et al. (2018)), survival analysis (Tang et al. (2017)), varying coefficient models (Bai et al. (2020)) and/or Gaussian graphical models (Deshpande et al. (2019), Li et al. (2019)). The original procedure proposed for Gaussian regression targets a posterior mode

| (3) |

where is obtained from (2) by integrating out the missing indicator and by deploying and with . Ročková and George (2018) develop a coordinate-ascent strategy which targets and which quickly finds (at least a local) mode of the posterior landscape. This strategy (summarized in Theorem 3.1 of Ročková and George (2018)) iteratively updates each using an implicit equation333Here we are not necessarily assuming that and the above formula is hence slightly different from Theorem 3.1 of Ročková and George (2018).

| (4) |

where , and with where

| (5) |

Ročková and George (2018) also provide fast updating schemes for and . In this work, we are interested in sampling from the posterior as opposed to mode hunting.

One immediate strategy for sampling from the Spike-and-Slab LASSO posterior is the Stochastic Search Variable Selection (SSVS) algorithm of George and McCulloch (1993). One can regard the Laplace distribution (with a penalty ) as a scale mixture of Gaussians with an exponential mixing distribution (with a rate as in Park and Casella (2008)) and rewrite the SSL prior using the following hierarchical form:

where is the vector of variances. The conditional conjugacy of the SSL prior enables direct Gibbs sampling for (see Algorithm 1 below). However, as with any other Gibbs sampler for Bayesian shrinkage models (Bhattacharya et al., 2015), this algorithm involves costly matrix inversions and can be quite slow when both and are large. In order to improve the MCMC computational efficiency when , Bhattacharya et al. (2016) proposed a clever trick. By recasting the sampling step as a solution to a linear system, one can circumvent a Cholesky factorization which would otherwise have a complexity per iteration. Building on this development, Johndrow et al. (2020) developed a blocked Metropolis-within-Gibbs algorithm to sample from horseshoe posteriors (Carvalho et al., 2010) and designed an approximate algorithm which thresholds small effects based on the sparse structure of the target. The exact method has a per-step complexity while the approximate one has only . In similar vein, the Skinny Gibbs MCMC method of Narisetty et al. (2019) also bypasses large matrix inversions by independently sampling from active and inactive ’s. While the method is only approximate, it has a rather favorable computational complexity . A referee suggested another Gibbs sampler implementation with a complexity which can be obtained by updating one at a time while conditioning on the remaining ’s (Geweke, 1991). While this implementation is very fast for point-mass spikes, the Spike-and-Slab LASSO prior requires sampling from a half-normal distribution which can be inefficient in practice. One-site Gibbs samplers also generally lead to slower mixing due to increased autocorrelation. In simulations, we find the performance of this method to be comparable with SSVS using Bhattacharya et al. (2016)’s trick. The detailed description of this algorithm is included in the Appendix (Section C).

The impressive speed of the Spike-and-Slab LASSO mode detection makes one wonder whether performing many independent optimizations on randomly perturbed datasets will lead to posterior simulation that is more economical. Moreover, one may wonder whether the induced approximate posterior is sufficiently close to the actual posterior and/or whether it can be used for meaningful estimation/uncertainty quantification. We attempt to address these intriguing questions in the next sections.

3 Likelihood Reweighting and Bayesian Bootstrap

The jumping-off point of our methodology is the weighted likelihood bootstrap (WLB) method introduced by Newton and Raftery (1994). The premise of WLB is to draw approximate samples from the posterior by independently maximizing randomly reweighted likelihood functions. Such a sampling strategy is computationally beneficial when, for instance, maximization is easier than Gibbs sampling from conditionals.

In the context of linear regression (1), the WLB method of Newton and Raftery (1994) will produce a series of draws by first sampling random weights from some weight distribution and then maximizing a reweighted likelihood

| (6) |

where

Newton and Raftery (1994) argue that for certain weight distributions , the conditional distribution of ’s given the data can provide a good approximation to the posterior distribution of . Moreover, WLB was shown to have nice theoretical guarantees when the number of parameters does not grow. Namely, under uniform Dirichlet weights (more below) and iid data samples, WLB is consistent (i.e. concentrating on any arbitrarily small neighborhood around an MLE estimator) and asymptotically first-order correct (normal with the same centering) for almost every realization of the data. The WLB method, however, is only approximate and it does not naturally accommodate a prior. Uniform Dirichlet weights provide a higher-order asymptotic equivalence when one chooses the squared Jeffrey’s prior. However, for more general prior distributions (such as shrinkage priors considered here), the correspondence between the prior and is unknown. Newton and Raftery (1994) suggest post-processing the posterior samples with importance sampling to leverage prior information. This pertains to Efron (2012), who proposes a posterior sampling method for exponential family models with importance sampling on parametric bootstrap distributions.

Alternatively, Newton et al. (2020) suggested blending the prior directly into WLB by including a weighted prior term, i.e. replacing (6) with

where 444Note that if , then which brings us back to the uniform Dirichlet distribution.. This so called Weighted Bayesian Bootstrap (WBB) method treats the prior weight as either fixed (and equal to one) or as one of the random data weights arising from the exponential distribution. We explore these two strategies in the next section within the context of the Spike-and-Slab LASSO where is the SSL shrinkage prior implied by (2).

3.1 WBB meets Spike-and-Slab LASSO

Since SSL is a thresholding procedure (see (4)), WBB will ultimately create samples from pseudo-posteriors that have a point mass at zero. This is misleading since the posterior under the Gaussian likelihood and a single Laplace prior is half-normal (Hans (2009), Park and Casella (2008)). Deploying the WBB method thus does not guarantee that uncertainty be propertly captured for the zero (negligible) effects since their posterior samples may very often be exactly zero. We formalize this intuition below. We want to understand the extent to which the WBB (or WLB) pseudo-posteriors correspond to the actual posteriors. To this end, we focus on the canonical Gaussian sequence model

| (7) |

Under the separable SSL prior (i.e. fixed), the true posterior is a mixture

| (8) |

where and . From Hans (2009), we know that and are orthant truncated Gaussians and thus is a mixture of orthant truncated Gaussians.

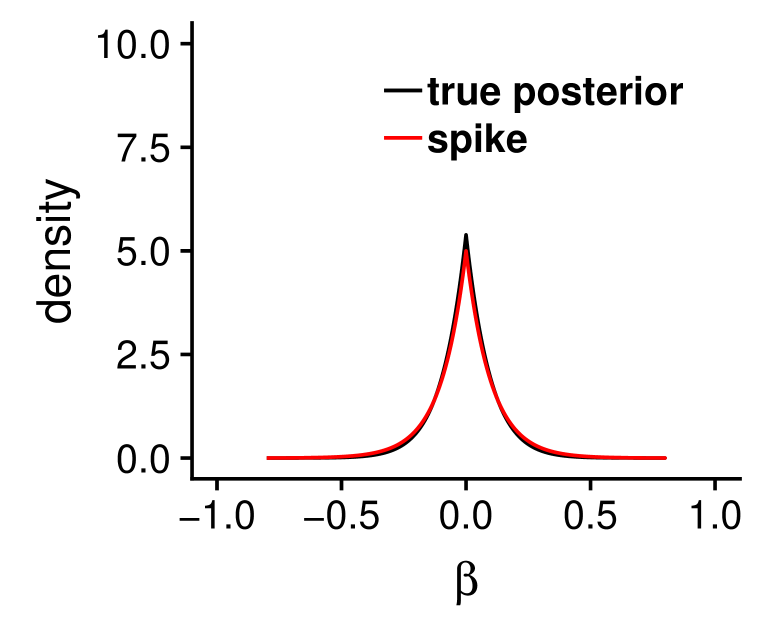

We start by examining the posterior distribution of active coordinates such that (this event happens with high probability when is sufficiently large). For the true posterior, we show in the Appendix (Proposition 1) that and . The true posterior is hence dominated by the component , which takes the following form

where

| (9) | ||||

| (10) |

Intuitively, vanishes when is large, so both and will be close to . This intuition is proved rigorously in the Appendix (Section A.6.2), where we show that the density of the transformed variable converges pointwise to the standard normal density and thereby the posterior converges to in total variation (Scheffé (1947)).

We now investigate the limiting shape of the pseudo-distribution obtained from WBB. For a given weight , the WBB estimator equals

| (11) |

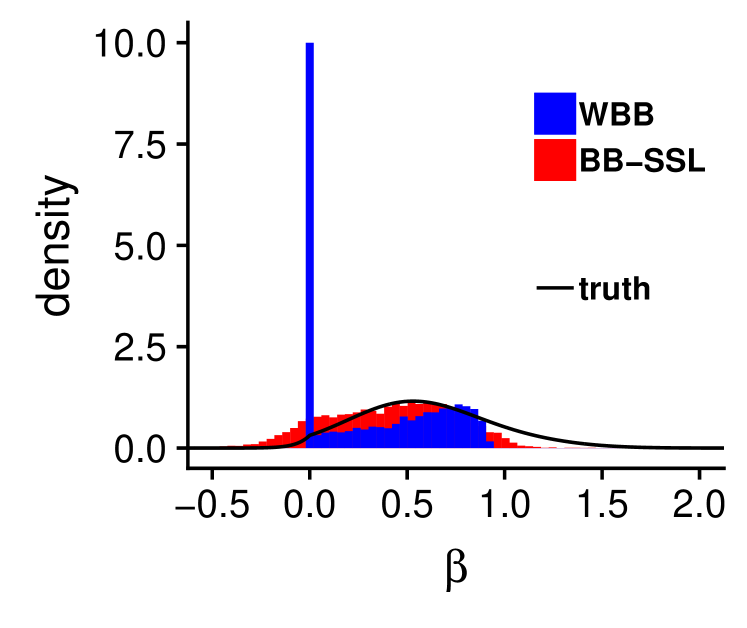

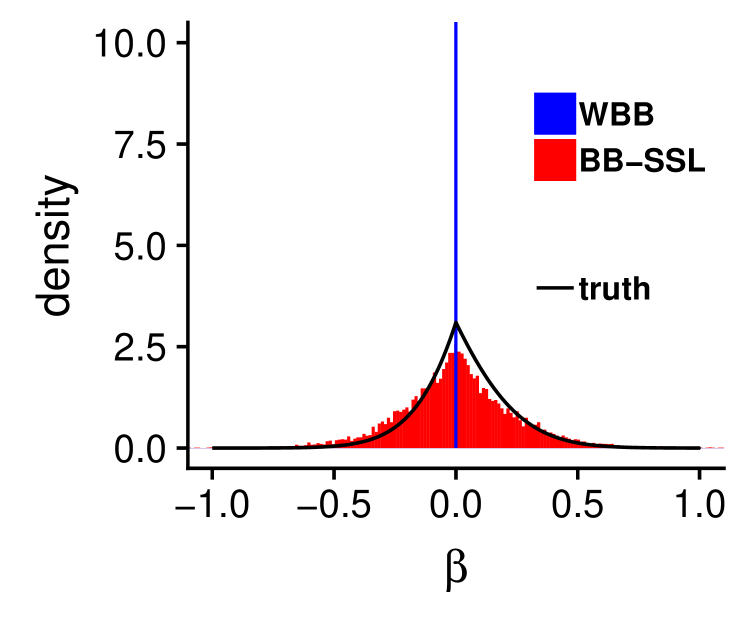

where is the analogue of defined below (4) for the regression model and where was also defined below (4). When , we show in the Appendix (Section A.6.2) that . Under the condition , it can be shown (Section A.6.2) that . For active coordinates, the distribution of the WBB samples is thus purely determined by that of . The shape of this posterior can be very different from the standard normal one, as can be seen from Figure 1. In particular, Figure 1(a) shows how WBB (a) assigns a non-negligible prior mass to zero (in spite of evidence of signal) (b) incurs bias in estimation and (c) underestimates variance with a skewed misrepresentation of the posterior distribution. This last aspect is particularly pronounced when the signal is even stronger.555 In fact, under the uniform Dirichlet distribution, the marginal distribution becomes . Since , the distribution of converges to Inverse-Gamma(1,1) which exhibits a skewed shape, which is in sharp contrast to the symmetric Gaussian distribution of the true posterior.

The approximability of WBB does not get any better for inactive coordinates such that and thereby from (7). The following arguments will be under the assumption . One can show (Section A.6.3 in the Appendix) that the true posterior is dominated by the component since and . When is sufficiently large, one can then approximate this distribution with the Laplace spike, indeed converges to in total variation (Section A.6.3 in the Appendix). When the signal is weak, the posterior thus closely resembles the spike Laplace distribution, as can be seen from Figure 1(c). For the fixed (and also random) WBB pseudo-posteriors, we show (in Section A.6.3 in the Appendix) that the posterior converges to a point mass at 0, i.e. This is a misleading approximation of the actual posterior (Figure 1(b)). To conclude, since SSL is always shrinking the estimates towards , WBB samples will often be zero. The true posterior, however, follows roughly a spike Laplace distribution when the signal is weak. Motivated by Papandreou and Yuille (2010), one possible solution is to introduce randomness in the shrinkage target of the prior.

4 Introducing BB-SSL

Similarly as Newton et al. (2020), we argue that the random perturbation should affect both the prior and the data. Instead of inflating the prior contribution by a fixed or random weight, we perturb the prior mean for each coordinate. This creates a random shift in the centering of the prior so that the posterior can shrink to a random location as opposed to zero. Instead of the prior in (2) which is centered around zero, we consider a variant that uses hierarchical jittered Laplace distributions.

Definition 4.1.

For , a location shift vector and a prior inclusion weight , the jittered Spike-and-Slab LASSO prior is defined as

| (12) |

and where , and .

The Bayesian Bootstrap Spike-and-Slab LASSO (which we abbreviate as BB-SSL) is obtained by maximizing a pseudo-posterior obtained by reweighting the likelihood and recentering the prior. Namely, one first samples weights , one for each observation, from for some (we discuss choices in the next section). Second, one samples the location shifts from the spike distribution as in (12). Lastly, a draw from the BB-SSL posterior is obtained as a pseudo-MAP estimator

| (13) |

BB-SSL can be implemented by directly applying the SSL algorithm we described in the previous section on randomly perturbed data. In particular, denote with . We can first calculate

and then get through a post-processing step

4.1 Theory for BB-SSL

For the uniform Dirichlet weights, Newton and Raftery (1994) (Theorem 1 and 2) show first-order correctness, i.e. consistency and asymptotic normality, of WLB in low dimensional settings (a fixed number of parameters) and iid observations. Their result can be generalized to WBB (Newton et al., 2020; Ng and Newton, 2020) as well as BB-SSL. While the uniform Dirichlet weight distribution is a natural choice, Newton and Raftery (1994) point out that it is doubtful that such weights would yield good higher-order approximation properties. The authors leave open the question of relating the weighting distribution to the model itself and to a more general prior. A more recent theoretical development in this direction is the work of Ng and Newton (2020) who find that WBB first-order correctness holds for a wide class of random weight distributions in low-dimensional LASSO regressions. They also theoretically assess the influence of assigning random weights to the penalty term. Here, we address this question by looking into asymptotics for guidance about the weight distribution. We focus on high-dimensional scenarios where the number of parameters ultimately increases with the sample size.

In particular, we provide sufficient conditions for the weight distribution so that the pseudo-posterior concentrates at the same rate as the actual posterior under the same prior settings. After stating the result for general weight distributions, we particularize our considerations to Dirichlet and gamma distributions and provide specific guidance for implementation. Our first result is obtained for the canonical high-dimensional normal-means problem, where is observed as a noisy version of a sparse mean vector , i.e.

| (14) |

Theorem 4.1 (Normal Means).

Consider the normal means model (14) with such that as . Assume the SSL prior with and with such that . Assume that are non-negative and arise from such that

-

(1)

for each ,

-

(2)

such that and for each ,

-

(3)

such that for each

Then, for any , the BB-SSL posterior concentrates at the minimax rate, i.e.

| (15) |

Proof.

See Section A.1.2 in the Appendix.

In Theorem 4.1, denotes the BB-SSL sample whose distribution, for each given , is induced by random weights arising from and random recentering arising from . Despite the approximate nature of BB-SSL, the concentration rate (15) is minimax optimal and it is the same rate achieved by the actual posterior distribution under the same prior assumptions (Ročková (2018a)). Condition (1) in Theorem 4.1 is not surprising and aligns with considerations in Newton et al. (2020). Conditions (2) and (3) can be viewed as regularizing the tail behavior of ’s (left and right, respectively). While Newton et al. (2020) only showed consistency for iid models in finite-dimensional settings, Theorem 4.1 is far stronger as it shows optimal convergence rate in a high-dimensional scenario. The following Corollary discusses specific choices of .

Corollary 4.1.

Proof.

See the Appendix (Section A.2).

Theorem 4.1 and Corollary 4.1 give insights into what weight distributions are appropriate for sparse normal means. In parametric models, the uniform Dirichlet distribution would be enough to achieve consistency (Newton and Raftery, 1994). It is interesting to note, however, that in the non-parametric normal means model, the assumption for yields risk (for active coordinates) that can be arbitrarily large (as we show in Section A.3 in the Appendix). The requirement is thus necessary for controlling the risk of active coordinates and the plain uniform Dirichlet prior (with ) would not be appropriate.

In the following theorems, we study the high-dimensional regression model (1) with rescaled columns for all .

Theorem 4.2 (Regression Model Size).

Consider the regression model (1) with , (unknown). Assume the SSL prior with and where . Assume that are non-negative and arise from such that

-

(1)

for each ,

-

(2)

,

-

(3)

,

-

(4)

for any ,

-

(5)

, and satisfies

-

(6)

for some , where , , is a sequence s.t. , and .

Then the BB-SSL posterior satisfies

where . The definition of is in the Appendix, Section A.4.1.

Proof.

Section A.4.6 in the Appendix.

Theorem 4.3 (Regression model).

Proof.

Section A.4.7 in the Appendix.

It follows from Ročková and George (2018) and from (16) that the BB-SSL posterior achieves the same rate of posterior concentration as the actual posterior. In Theorem 4.2, Conditions (1)-(4) regulate the distribution while Conditions (5) and (6) impose requirements on , and . Conditions (2) and (3) are counterparts of (2) and (3) in Theorem 4.1 and control the left and right tail of ’s, respectively. The larger (or the smaller ) is, the larger and will become and the larger the bound on will be. Compared with the normal means model, we have one additional Condition (4) which requires that each becomes more and more concentrated around its mean and that ’s are asymptotically uncorrelated. It is interesting to note that distributions in Corollary 4.1 both satisfy Condition (4). Moreover, the Dirichlet distribution in Corollary 4.1 achieves both upper bounds tightly. Finally, Condition (5) ensures that identifiability holds with high probability (Zhang and Zhang (2012)) and Condition (6) ensures that our bound is meaningful.666 In order for to be a bounded real number smaller than 1, we would need . For example when , for random matrix where each element is generated independently by Gaussian distribution, we have (Vivo et al. (2007)). So in order for such a sequence (s.t. ) to exist, we need . We can choose and under such settings. In practice, many distributions will satisfy Conditions (1)-(4), e.g. bounded distributions with a proper covariance structure or distributions from Corollary 4.1.

Remark 4.1.

4.2 Connections to Other Bootstrap Approaches

Our approach bears a resemblance to Bayesian non-parametric learning (NPL) introduced by Lyddon et al. (2018) and Fong et al. (2019) which generates exact posterior samples under a Bayesian non-parametric model that assumes less about the underlying model structure. Under a prior on the sampling distribution function , one can use WBB (and also WLB) to draw samples from a posterior of by optimizing a randomly weighted loss function based on an enlarged sample (observed plus pseudo-samples) with weights following a Dirichlet distribution (see Algorithm 3 which follows from Fong et al. (2019)). Despite the fact that these two procedures have different objectives, there are many interesting connections. In particular, the idea of randomly perturbing the prior has an effect similar to adding pseudo-samples from the prior defined through

where is the Dirac measure, is the Spike, and where satisfies . A motivation for this prior is derived in the Appendix (Section B). Under this prior, the NPL posterior samples generated by Algorithm 3 approximately follow the distribution (see Section B in the Appendix)

| (17) |

where , each coordinate of independently follows the spike distribution, and where represents the strength of our belief in and can be interpreted as the effective sample size from . In comparison with the BB-SSL estimate

| (18) |

where , both (17) and (18) are shrinking towards a random location and both are using Dirichlet weights. The main difference is in the choice of the concentration parameter . When , (17) reduces to WBB (with a fixed weight on the prior) which reflects less confidence in the prior and thus less prior perturbation (location shift). When is large, (17) becomes more similar to (18) where the prior is stronger and thereby more prior perturbation is induced. Another difference is that (17), although shrinking towards a random location , adds the location back which results in less variance (see Figures in Section B in the Appendix).

| Algorithm | Complexity |

|---|---|

| SSVS1 | |

| SSVS2 | |

| Skinny Gibbs | |

| WLB | when , not applicable when |

| BB-SSL | for a single value |

5 Simulations

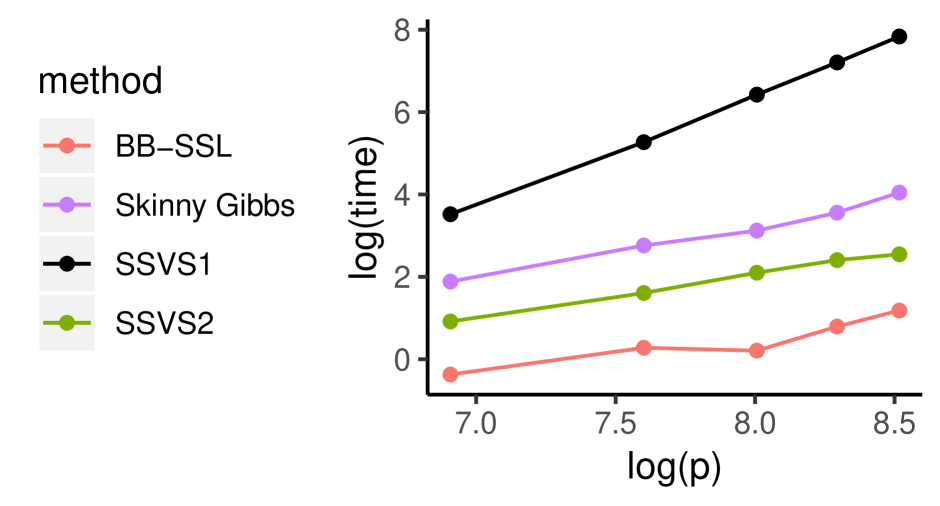

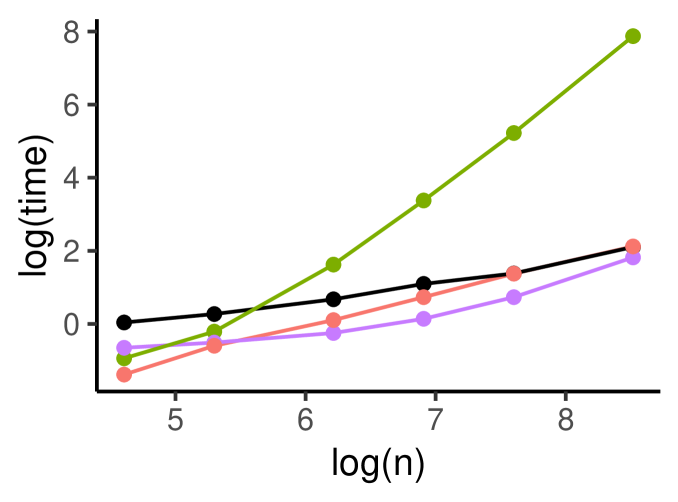

We compare the empirical performance of our BB-SSL with several existing posterior sampling methods including WBB (Newton et al. (2020)), SSVS (George and McCulloch (1993)), and Skinny Gibbs (Narisetty et al. (2019)). We implement two versions of WBB: WBB1 (with a fixed prior weight) and WBB2 (with a random prior weight). We also implement the original SSVS algorithm (Algorithm 1 further referred to as SSVS1) and compare its complexity and running times with its faster version (further referred to as SSVS2) which uses the trick from Bhattacharya et al. (2016). Comparisons are based on the marginal posterior distributions for ’s, marginal inclusion probabilities (MIP) as well as the joint posterior distribution . As the benchmark gold standard for comparisons, we run SSVS initialized at the truth for a sufficiently large number of iterations and discard the first samples as a burn-in. We use the same and for Skinny Gibbs except that we initialize at the origin. For BB-SSL, we draw weights where depends on . When solving the optimization problem (13) using coordinate-ascent, the default initialization for in the SSLASSO R package (Ročková and Moran, 2017) is at the origin. In high-dimensional correlated settings when , however, the performance of BB-SSL can be further enhanced by using a warm start re-initialization strategy for a sequence of increasing ’s where the last value is the target value (as recommended by Ročková (2018a) and Ročková and Moran (2017)). It is computationally more economical to perform such annealing only once on the original data and then use the output (for the target value ) for each BB-SSL iteration. We apply this strategy using an output obtained from the R package SSLASSO using an equispaced sequence of ’s of length , starting at and ending at . We then run WWB1, WBB2 and BB-SSL for iterations. Throughout the simulations we set and assume the prior . Computational complexity of each algorithm is summarized in Table 1 with actual running times reported (for varying and ) in Figure 2.

5.1 The Low-dimensional Case

Similarly to the experimental setting in Ročková (2018b), we generate observations on predictors with , where the predictors have been grouped into blocks. Within each block, predictors have an equal correlation and there is only one active predictor. All the other correlations are set to 0. We choose a single value for and generate Dirichlet weights assuming (for WBB1, WBB2 and BB-SSL).

Uncorrelated Designs

Assuming and we run SSVS1 and Skinny Gibbs for iterations with a burn-in . For WBB1, WBB2 and BB-SSL we use iterations. All methods perform very well under various metrics in this setting. We refer the reader to Section E.1 in the Appendix for details.

Correlated Designs

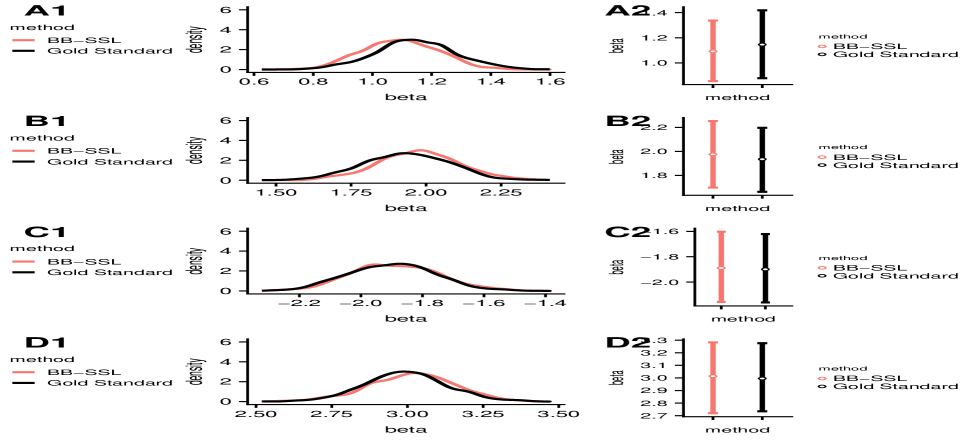

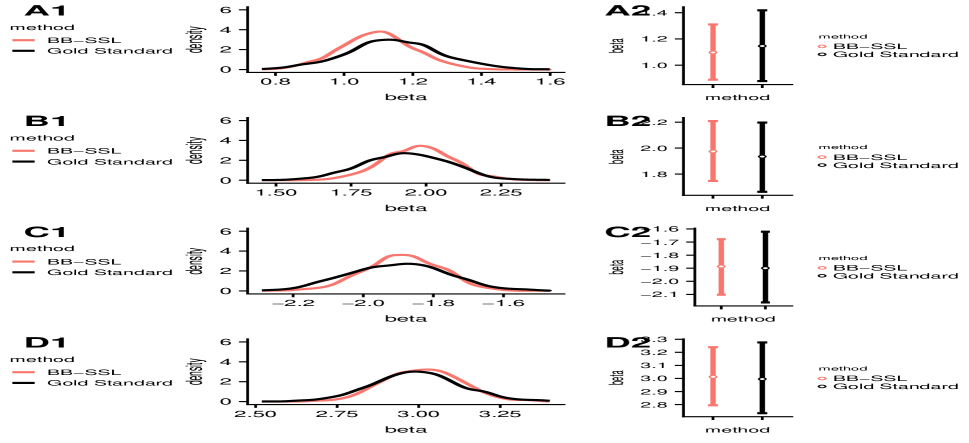

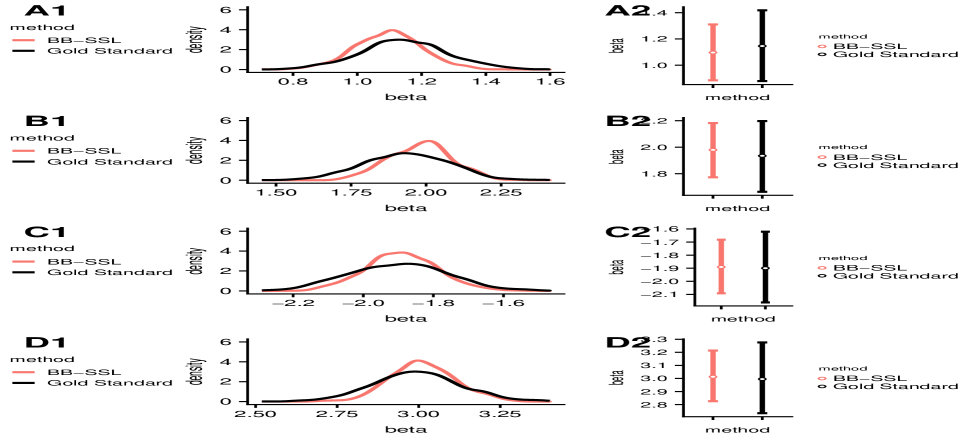

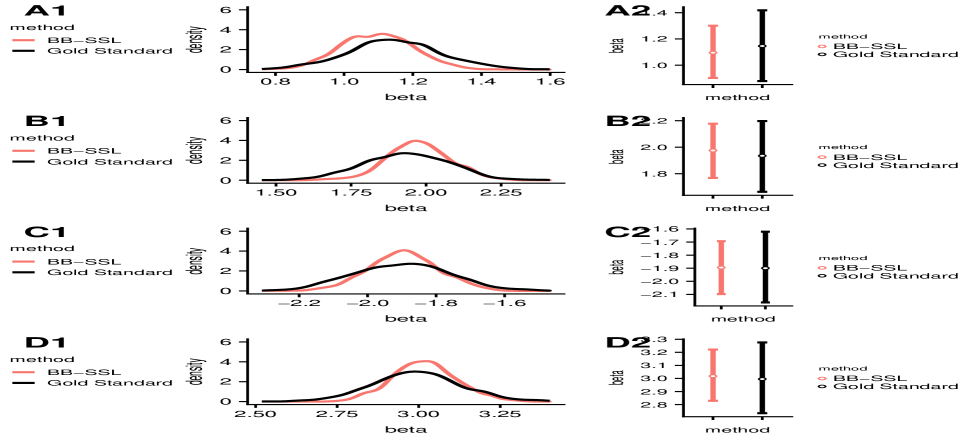

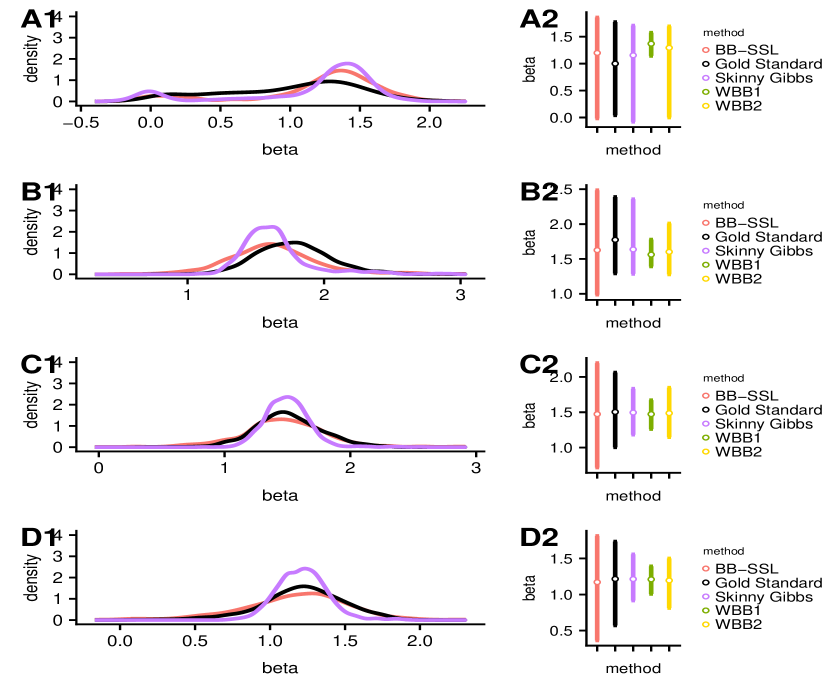

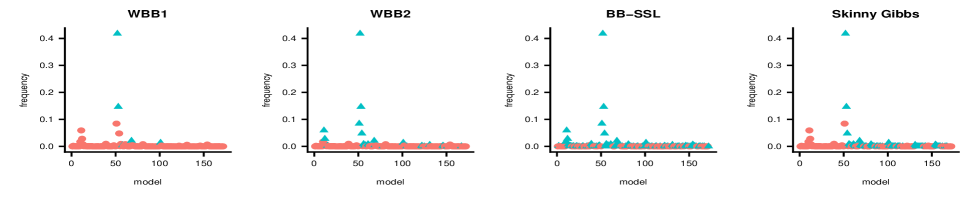

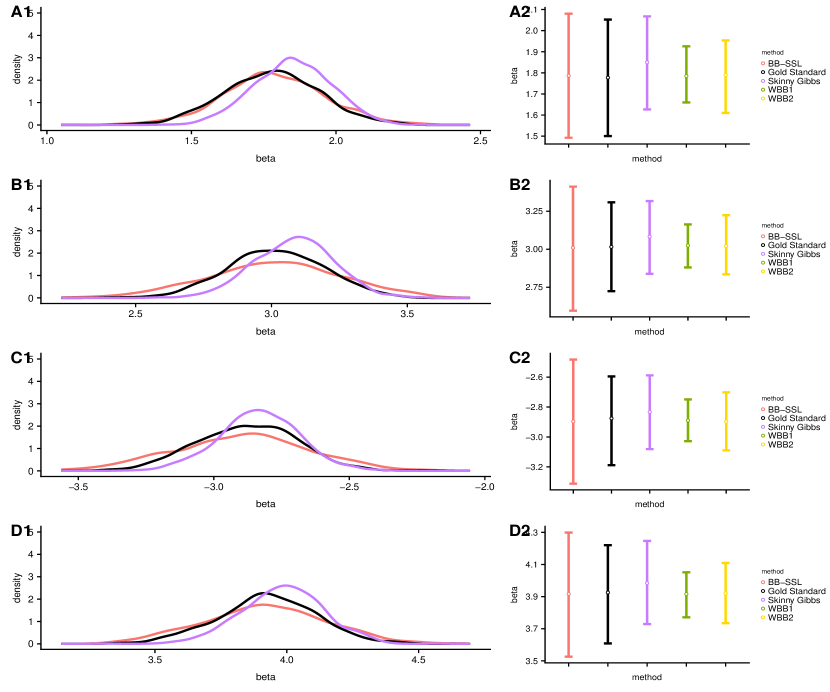

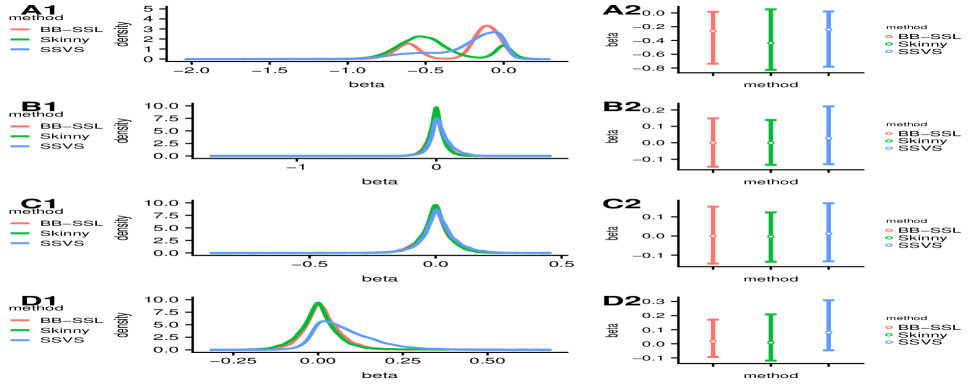

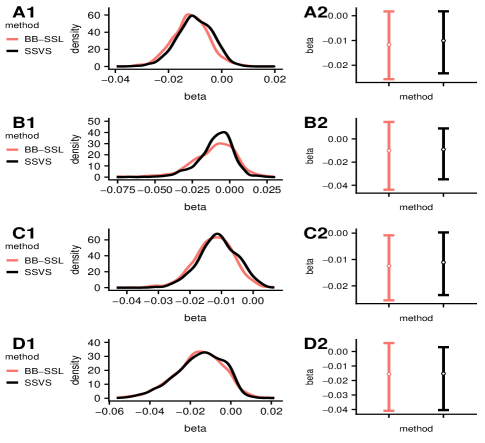

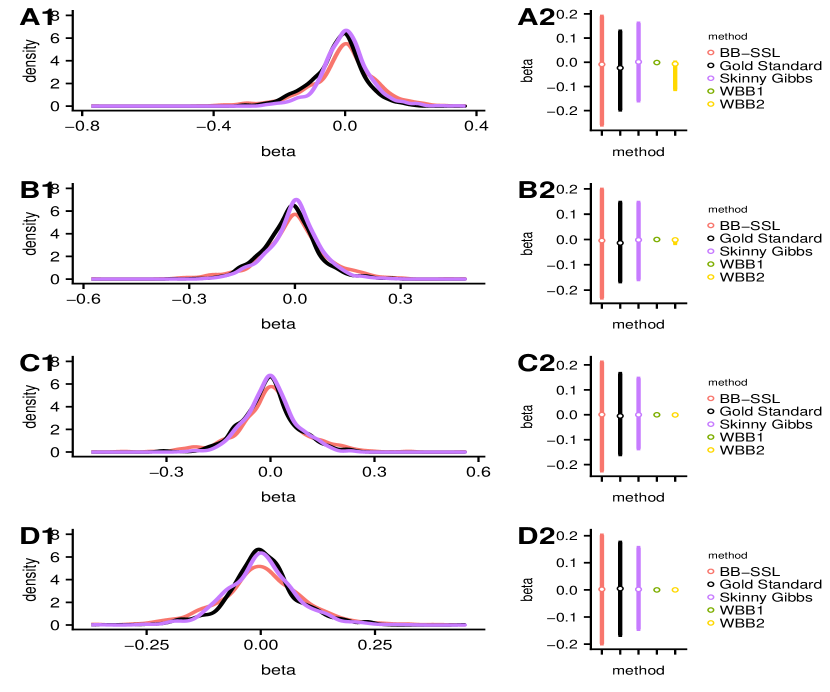

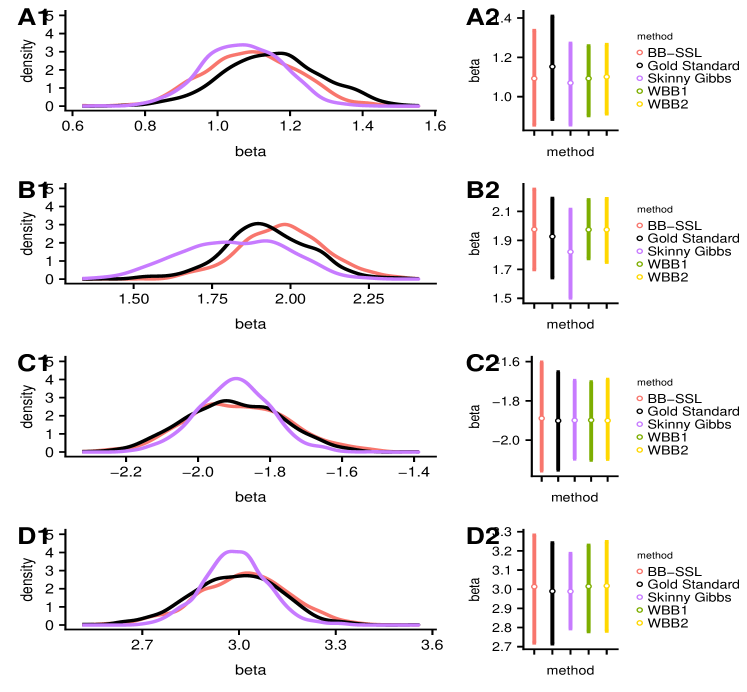

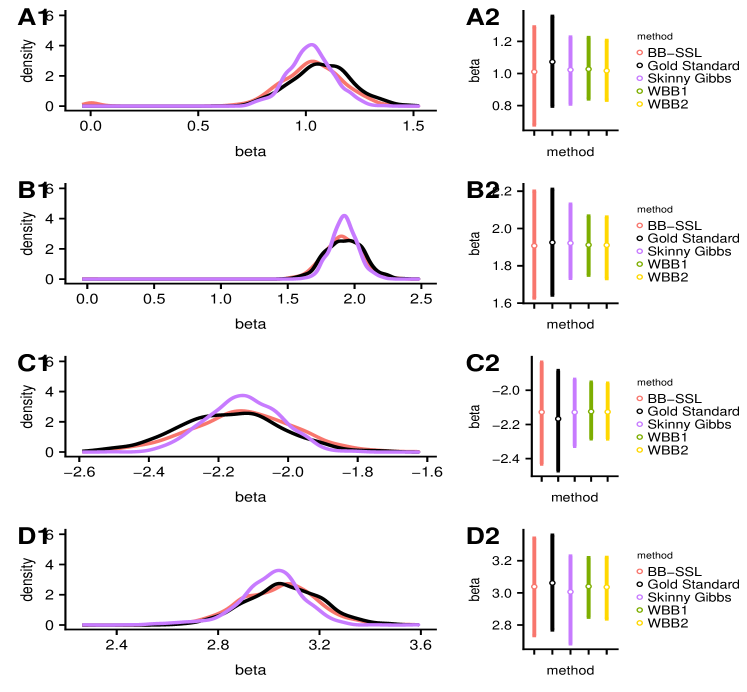

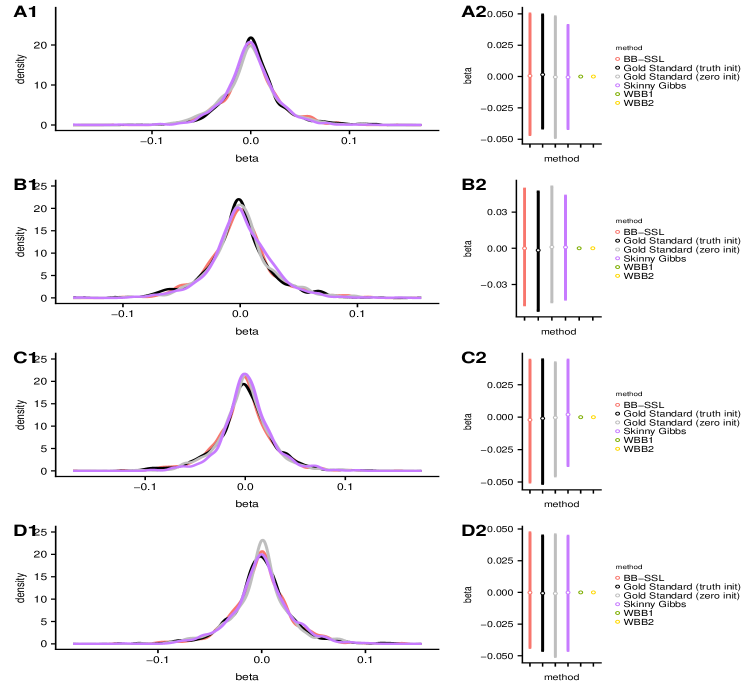

Correlated designs are far more interesting for comparisons. We choose and to deliberately encourage multimodality in the model posterior (see Figure 4(b)). For SSVS1 and Skinny Gibbs, we set and . For WBB1, WBB2 and BB-SSL we set .

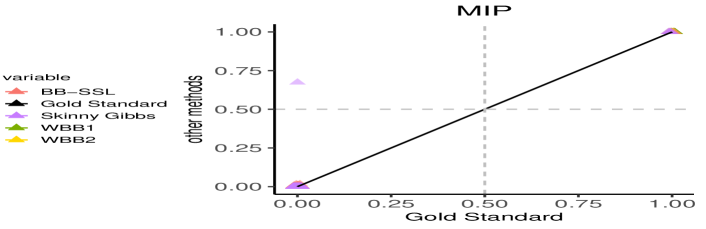

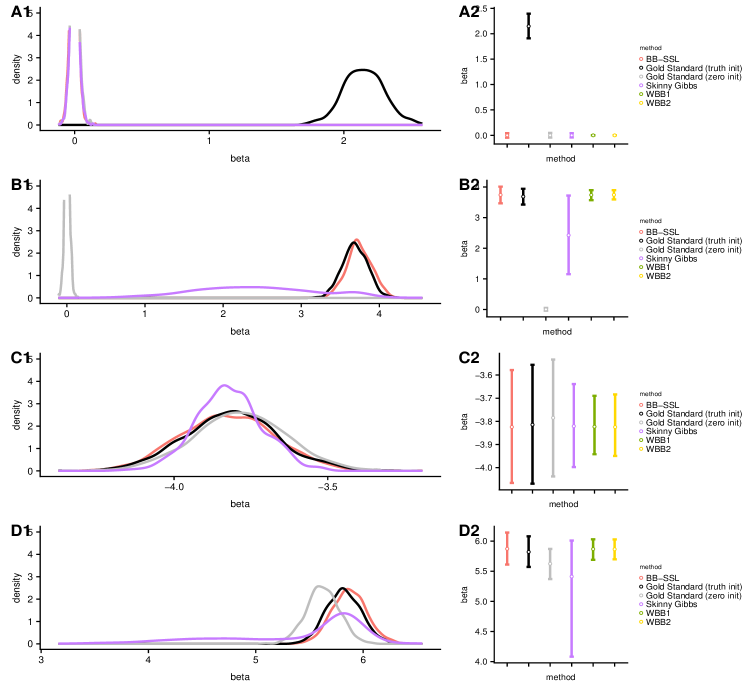

In terms of the marginal densities of ’s, Figure 3 shows that BB-SSL tracks SSVS1 very closely. All methods can cope with multi-collinearity where BB-SSL tends to have slightly longer credible intervals with the opposite being true for Skinny Gibbs, WBB1 and WWB2. In terms of the marginal means of (Figure 4(a)) all methods perform well, where the median probability model rule (truncating the marginal means at 0.5) yields the true model. In terms of the overall posterior , we identify over 60 unique models using SSVS1 where the true model accounts for most of the posterior mass. In Figure 4(b), we show the visited (blue triangle) and not visited (red dots) among these models, where -axis represents the estimated posterior probability for each model (calculated from SSVS1). All methods can detect the dominating model. BB-SSL tracked down 99% of the posterior probability, followed by WBB1 (92%), WBB2 (91%) and Skinny Gibbs (73%). The average times (reported in seconds and ordered from fastest to slowest) spent on generating effective samples for ’s are WBB2 (0.68 s) WBB1 (0.72 s) BB-SSL (0.74 s) SSVS2 (0.82 s) SSVS1 (0.85 s) Skinny Gibbs (1.19 s).

5.2 The High-dimensional Case

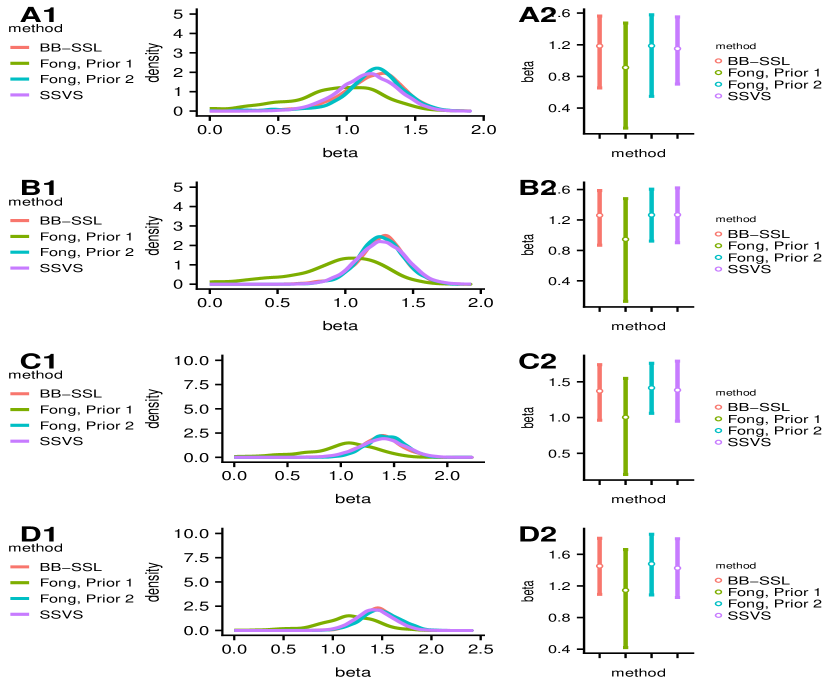

We now consider a higher-dimensional case with and , assuming and for BB-SSL. For SSVS1 and Skinny Gibbs we set and while for WBB1, WBB2 and BB-SSL we set .

We consider two correlation structures: (a) block-wise correlation, and (b) equi-correlation. In the setting (a), the active predictors have regression coefficients and all predictors are grouped into blocks of size , where each group has exactly one active coordinate and where predictors have a within-group correlation . We consider and an extreme case with a larger signal . For the equi-correlation setting (with a correlation coefficient ), active predictors have regression coefficients . We consider .

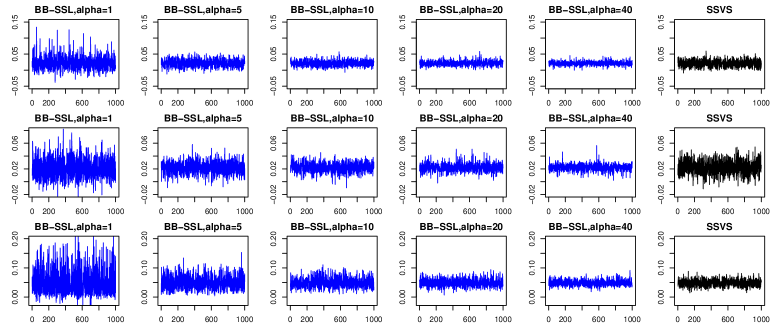

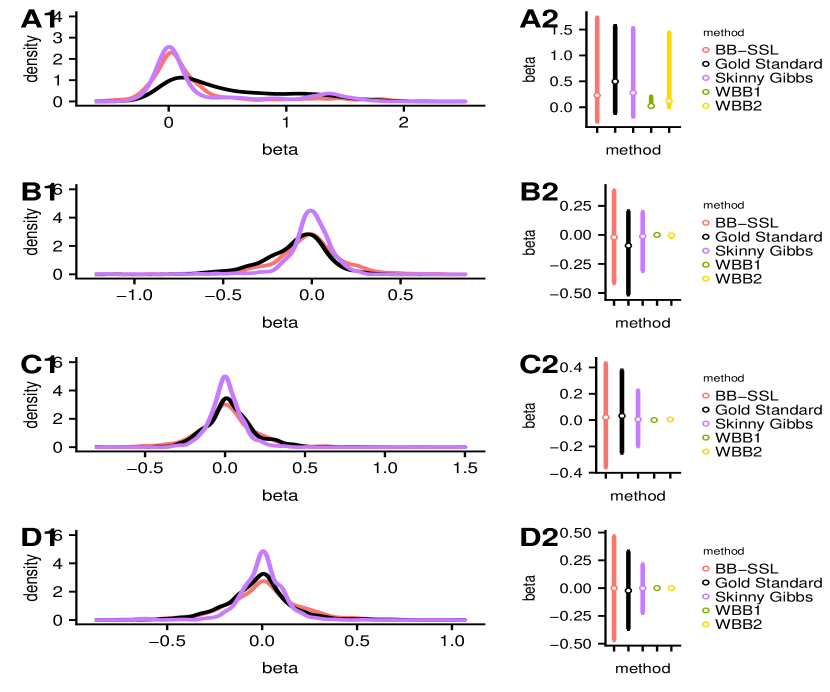

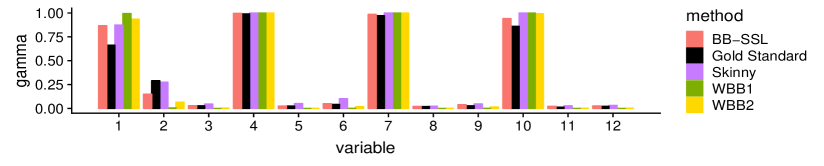

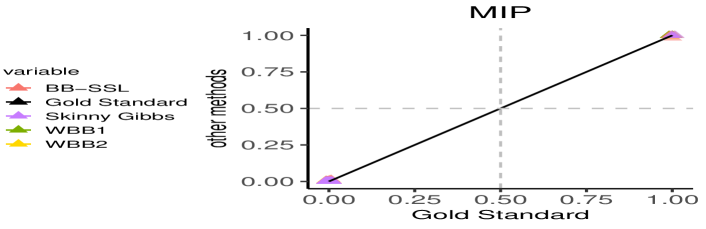

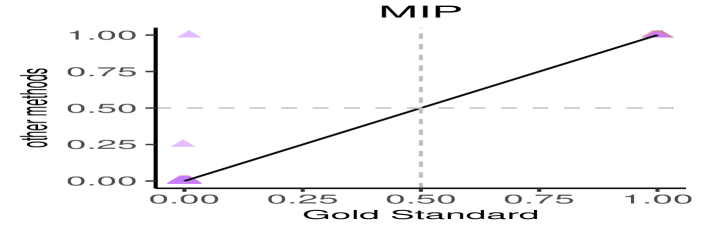

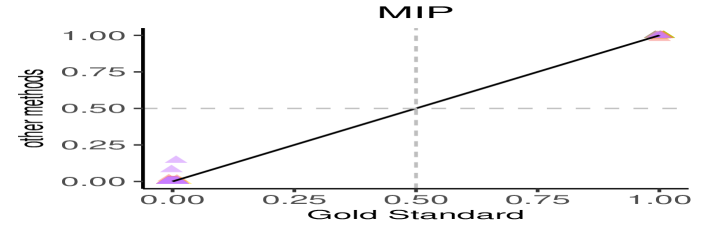

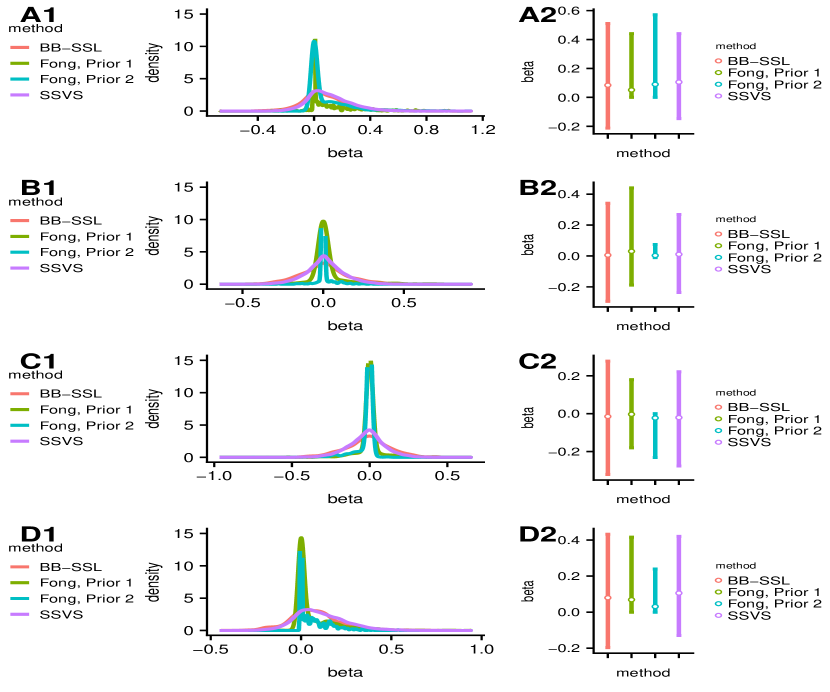

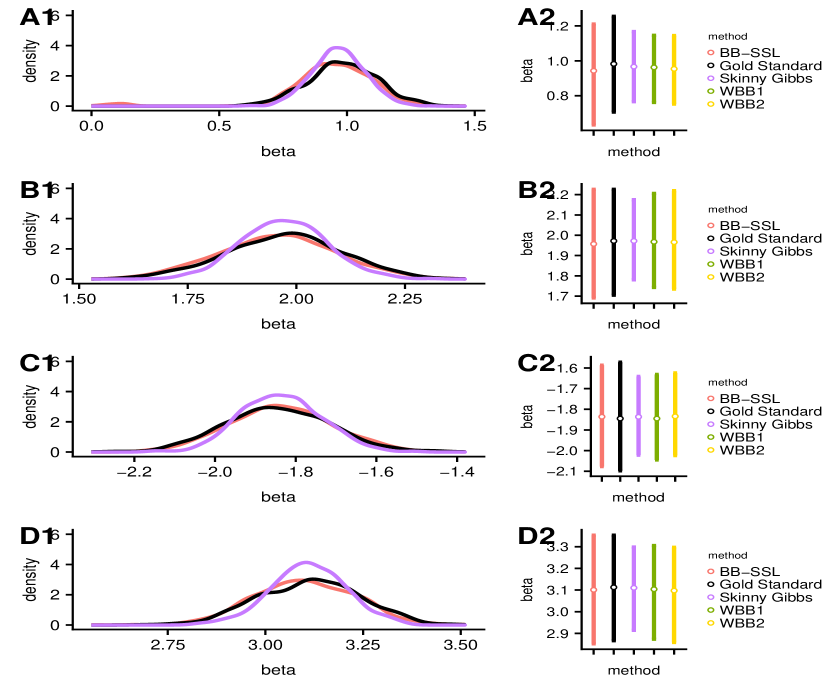

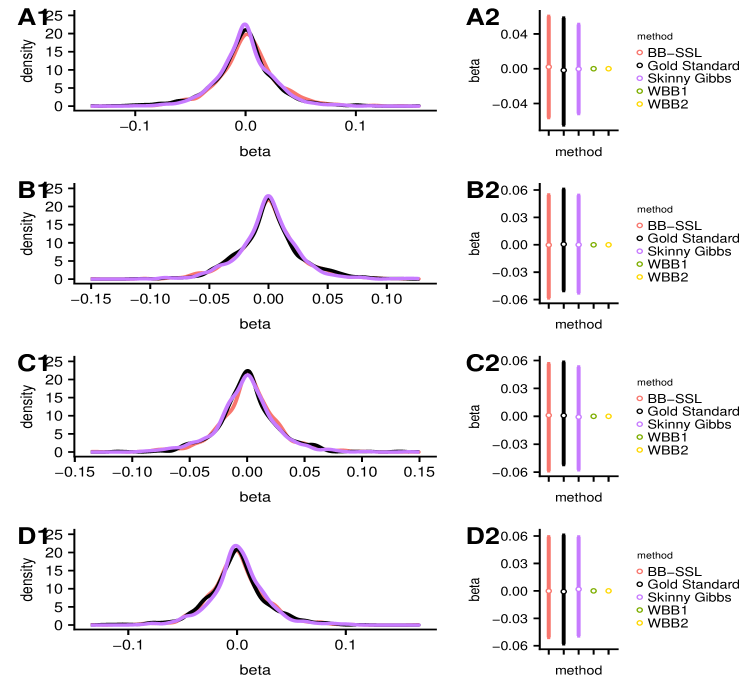

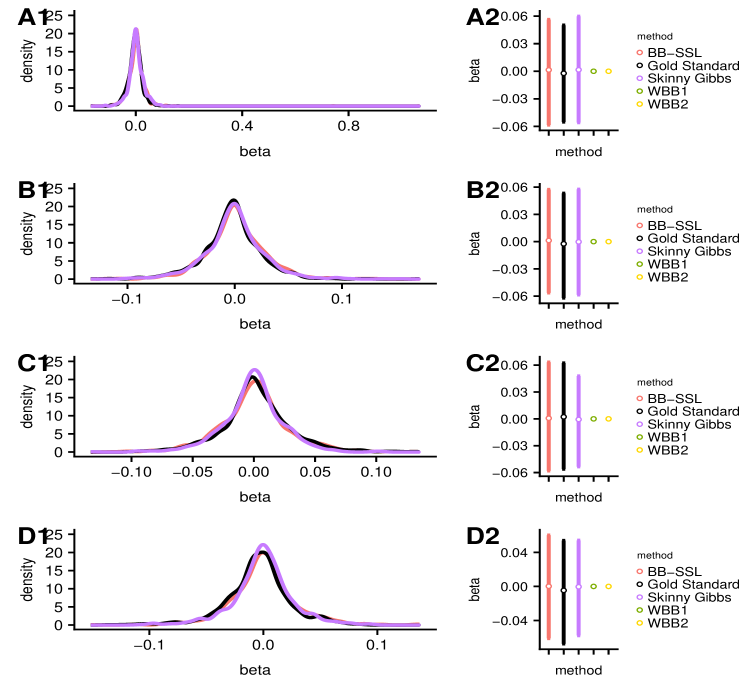

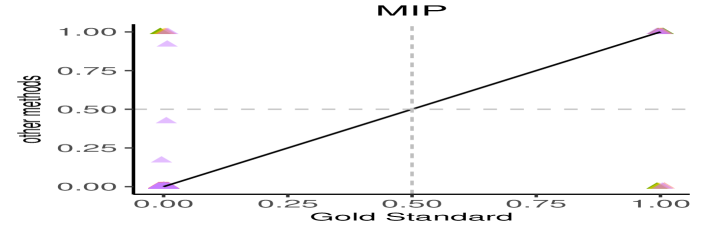

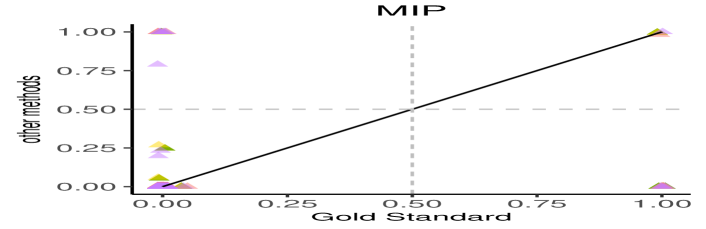

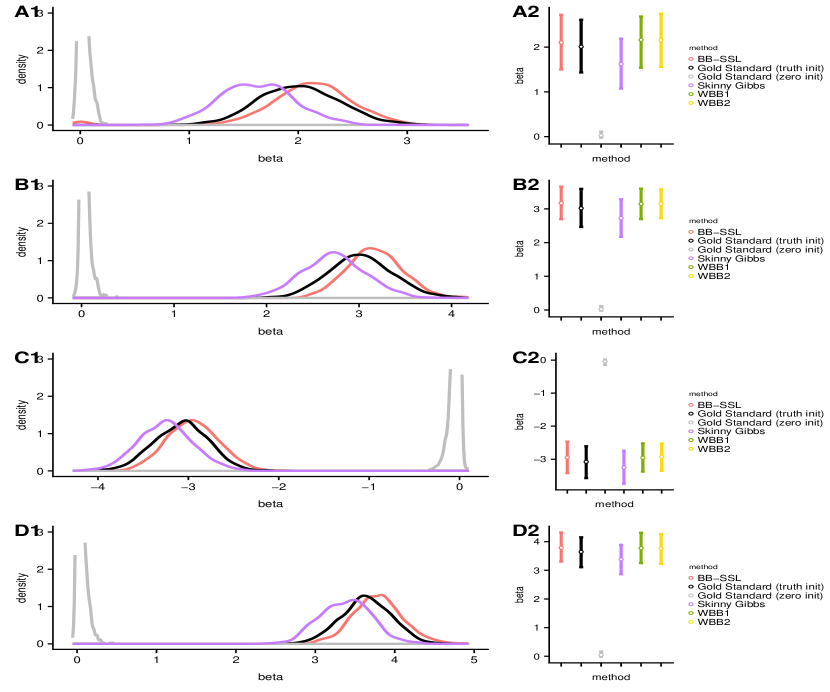

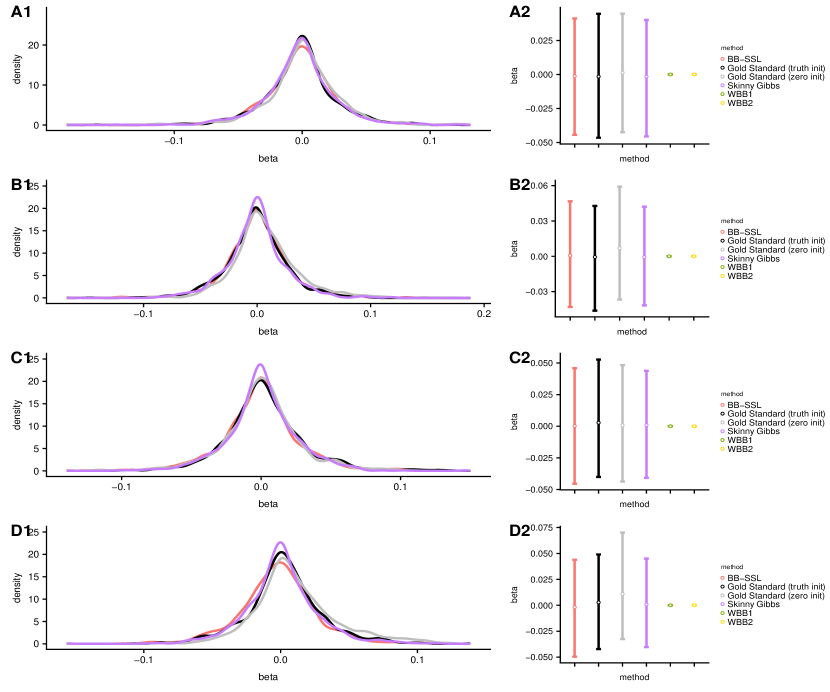

For brevity, we only show results for in the equi-correlation setting with the rest postponed until the Appendix (Section E). In the setting (b) with , in terms of the marginal density of ’s (shown in Figure 6), Skinny Gibbs tends to underestimate the variance for active coordinates and WBB1 and WBB2 produce a point mass at for inactive coordinates. BB-SSL, on the other hand, fares very well. Figure 5 shows that BB-SSL, WBB1 and WBB2 accurately reproduce the MIPs, while Skinny Gibbs tends to slightly overestimate the MIP as increases.

| Setting | Block-wise , | Block-wise , | ||||||||||||||||

| Metric | ’s | ’s | Model | ’s | ’s | Model | ||||||||||||

| Metric | KL | JD of 90% CI | ‘Bias’ | ‘Bias’ | HD | KL | JD of 90% CI | ‘Bias’ | ‘Bias’ | HD | ||||||||

| all | all | |||||||||||||||||

| Skinny Gibbs | 0.19 | 0.009 | 0.30 | 0.10 | 0.04 | 0.003 | * | * | 0 | 2.00 | 0.02 | 0.62 | 0.10 | 0.68 | 0.005 | 0.15 | 0.002 | 2.2 |

| WBB1 | 0.41 | 3.09 | 0.45 | 1 | 0.03 | 0.003 | * | * | 0 | 1.89 | 3.09 | 0.51 | 1 | 0.74 | 0.006 | 0.25 | 0.001 | 2 |

| WBB2 | 0.21 | 3.09 | 0.37 | 1 | 0.03 | 0.003 | * | * | 0 | 1.89 | 3.09 | 0.52 | 1 | 0.74 | 0.006 | 0.25 | 0.001 | 2 |

| BB-SSL | 0.02 | 0.003 | 0.14 | 0.10 | 0.04 | 0.003 | * | * | 0 | 1.73 | 0.01 | 0.37 | 0.10 | 0.74 | 0.006 | 0.25 | 0.001 | 2 |

| Setting | Equi-correlation , | Equi-correlation , | ||||||||||||||||

| Metric | ’s | ’s | Model | ’s | ’s | Model | ||||||||||||

| Metric | KL | JD of 90% CI | ‘Bias’ | ‘Bias’ | HD | KL | JD of 90% CI | ‘Bias’ | ‘Bias’ | HD | ||||||||

| all | all | |||||||||||||||||

| Skinny Gibbs | 0.13 | 0.01 | 0.23 | 0.11 | 0.05 | 0.003 | 0.0008 | * | 1 | 0.30 | 0.02 | 0.33 | 0.09 | 0.23 | 0.004 | 0.001 | * | 2 |

| WBB1 | 0.12 | 3.09 | 0.30 | 1 | 0.03 | 0.003 | * | * | 0 | 0.14 | 3.08 | 0.23 | 1 | 0.13 | 0.002 | * | * | 0 |

| WBB2 | 0.13 | 3.09 | 0.30 | 1 | 0.03 | 0.003 | * | * | 0 | 0.15 | 3.08 | 0.23 | 1 | 0.13 | 0.002 | * | * | 0 |

| BB-SSL | 0.06 | 0.003 | 0.20 | 0.03 | 0.003 | * | * | 0 | 0.11 | -0.003 | 0.23 | 0.08 | 0.12 | 0.002 | * | * | 0 | |

To better quantify the performance of each method, we gauge the quality of the posterior approximation using various metrics in Table 2. The KL divergence is calculated using an R package “FNN” (Beygelzimer et al. (2013)), where all parameters are set to their default values. We also report the Jaccard distance of credible intervals relative to the SSVS benchmark. The Jaccard distance (Jaccard, 1912) of two intervals and is defined as where and denotes the length. The Hamming distance is calculated using an R package “e1071” (Meyer et al. (2014)). We also compare the norm of posterior means (i.e. “bias” relative to the SSVS standard) for ’s as well as ’s. All methods do well in terms of MIP and the selected model (based on the median probability model rule). For ’s, all methods estimate the mean accurately. Taking into account the shape of the posterior for ’s, the performance is divided among coordinates and methods. For all methods, the approximability of active coordinates is less accurate than for the inactive ones. In the settings we tried, we rank the performance of various methods as follows: . The average times (in seconds (s) when in the equi-correlated design) spent on generating effective samples for each are: BB-SSL (0.69 s) SSVS2 (2.58 s) Skinny Gibbs (6.61 s) WBB2 (13.53 s) WBB1 (17.25 s) SSVS1 (34.67 s).

Conclusion

We found that BB-SSL is a reliable approximate method for posterior sampling that achieves a close-to-exact (SSVS) performance but is computationally cheaper. Additional speedups can be obtained with parallelization. The most expensive step in BB-SSL is solving the optimization problem (13) at each iteration. This could be potentially circumvented by using the Generative Bootstrap Sampler (GBS) (Shin et al., 2020) which constructs a generator function that can transform weights into samples from the posterior distribution. This strategy could be particularly beneficial when both and are large and when many posterior samples are needed. While MCMC-based methods are sensitive to the initialization and can fall into a local trap (e.g. when predictors are highly correlated), we have seen BB-SSL to be less susceptible to this problem. BB-SSL, in some sense, relies on the optimization procedure not finding the global mode at all times. Indeed, we want to provide a representation of the entire posterior distribution consisting of both local and global modes. However, we anticipate that the global mode will be found more often, correctly reflecting the amount of posterior mass assigned to it. This issue was also discussed in Section 2.5.1 in Fong et al. (2019), who point out that not necessarily finding the global mode will result in assigning more posterior density to local modes. We have found BB-SSL (initialized at the SS-LASSO solution after annealing) perform similarly as SSVS initialized at the truth in very highly correlated cases.

6 Data Analysis

6.1 Life Cycle Savings Data

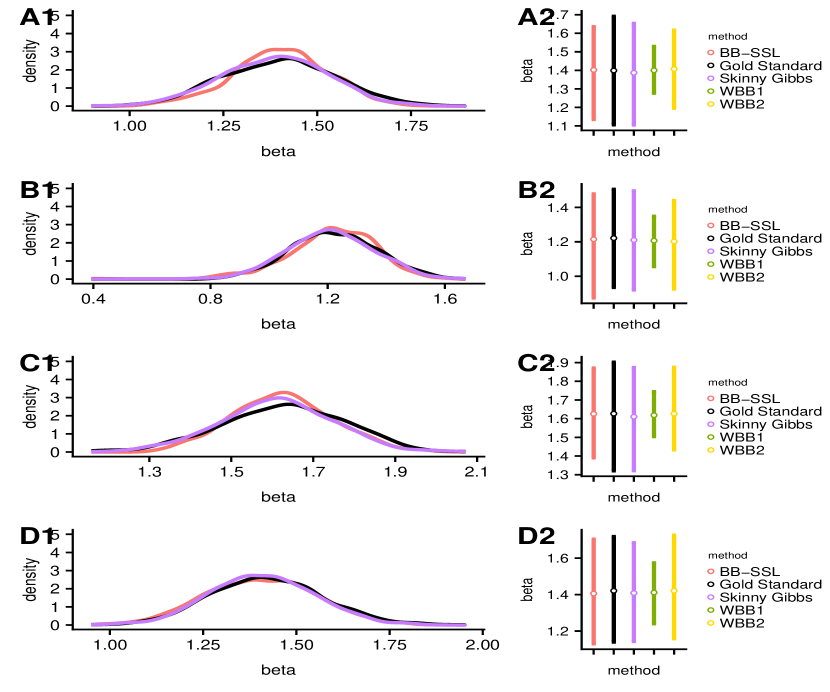

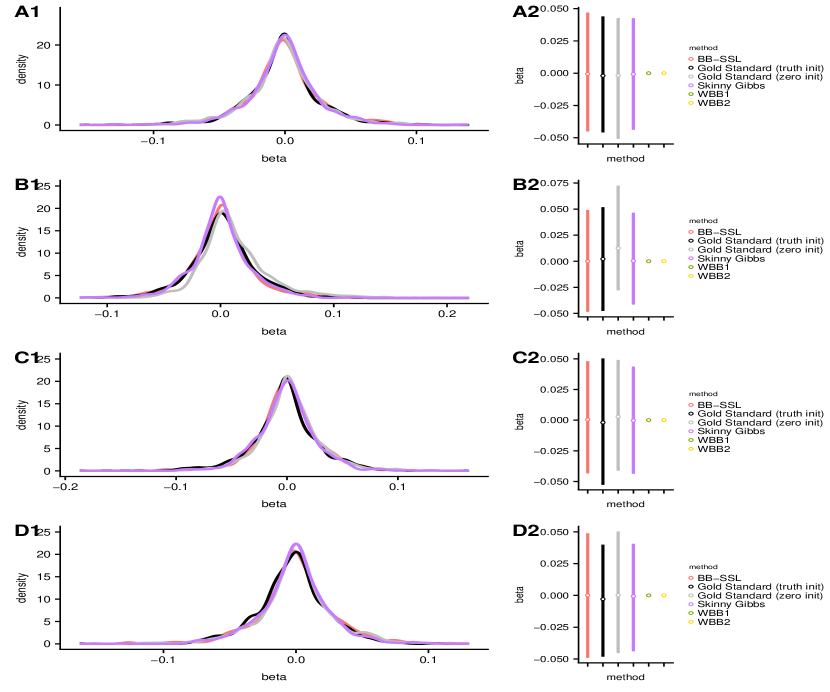

The Life Cycle Savings data (Belsley et al., 2005) consists of observations on highly correlated predictors: “pop15” (percentage of population under 15 years old), “pop75” (percentage of population over 75 years old), “dpi” (per-capita disposable income), “ddpi” (percentage of growth rate of dpi). According to the life-cycle savings hypothesis proposed by Ando and Modigliani (1963), the savings ratio () can be explained by these four predictors and a linear model can be used to model their relationship.

We preprocess the data in the following way. First, we standardize predictors so that each column of is centered and rescaled so that . Next, we estimate the noise variance using an ordinary least squares regression. We then divide by the estimated noise standard deviation and estimate by fitting SSL with . For BB-SSL we set and set , . We run SSVS1 and Skinny Gibbs for and BB-SSL for .

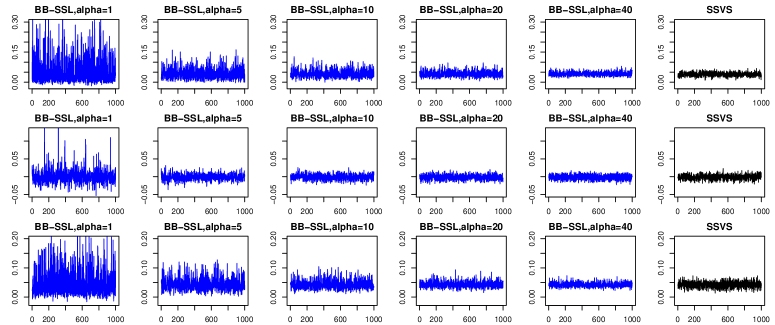

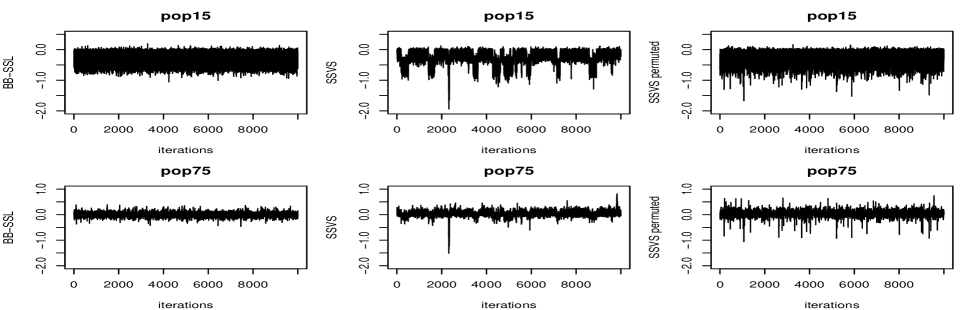

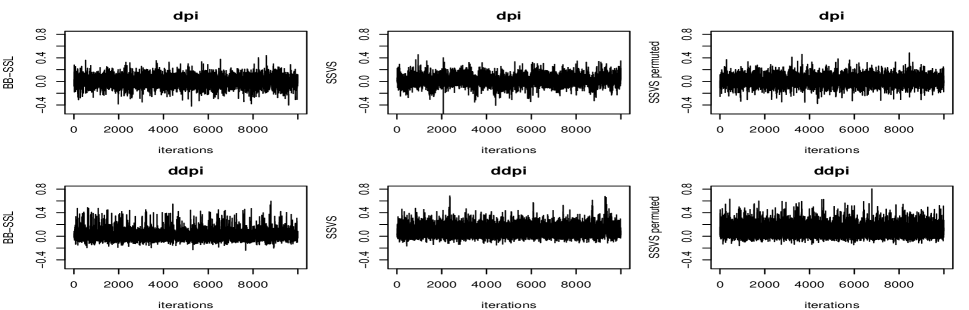

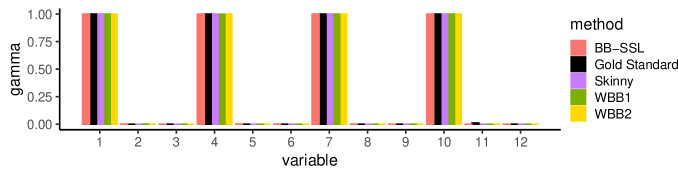

Figure 7 shows the trace plots on the four predictors. BB-SSL (first column) has the same mean and spread as SSVS (third column). We also observe that raw samples from SSVS (second column) are correlated, so more iterations are needed in order to fully explore the posterior. In contrast, each sample from BB-SSL is independent and thereby fewer samples will be needed in practice. See Table 3 for effective sample size comparisons. Figure 8(a) shows the marginal density of ’s and 8(b) shows the marginal mean of ’s. In both figures BB-SSL achieves good performance.

| SSVS | Skinny Gibbs | BB-SSL | |

|---|---|---|---|

| Effective sample size | 2716 | 11188 | 15000 |

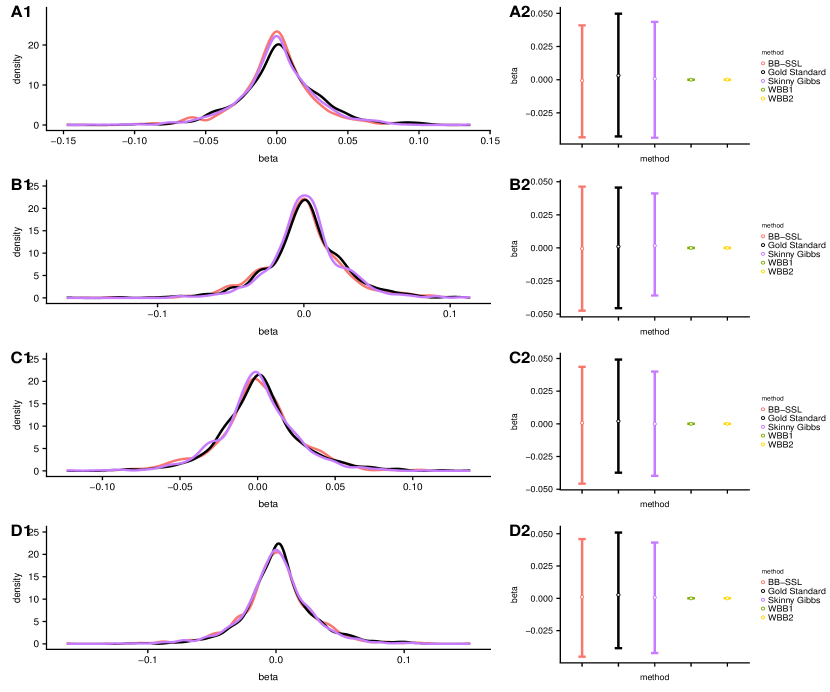

6.2 Durable Goods Marketing Data Set

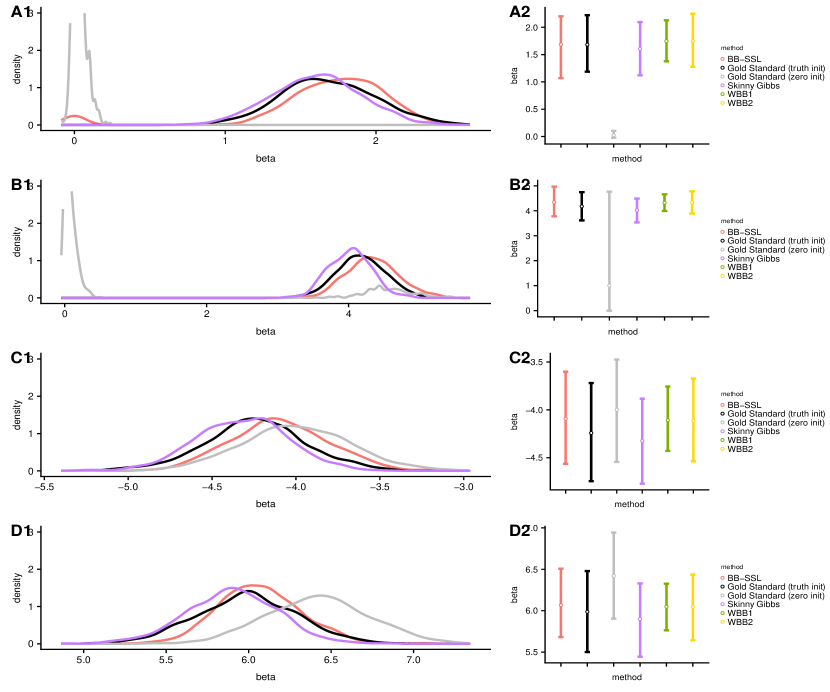

Our second application examines a cross-sectional dataset from Ni et al. (2012) (ISMS Durable Goods Dataset 2) consisting of durable goods sales data from a major anonymous U.S. consumer electronics retailer. The dataset features the results of a direct-mail promotion campaign in November 2003 where roughly half of the households received a promotional mailer with off their purchase during the promotion time period (December 4-15). The treatment assignment () was random. The data contains descriptors of all customers including prior purchase history, purchase of warranties etc. We will investigate the effect of the promotional campaign (as well as other covariates) on December sales. In addition, we will interact the promotion mail indicator with customer characteristics to identify the “mail-deal-prone” customers. To be more specific, we adopt the following model

| (19) |

where refers to the 146 covariates, is the treatment assignment, and the noise is iid normally distributed. And our aim is to (1) estimate the coefficients ; (2) identify those customers with .

For preprocessing, we first remove all variables that contain missing values or that are all ’s. We also create new predictors by interacting the treatment effect with the descriptor variables. After that the total number of predictors becomes . We standardize such that each column has a zero mean and a standard deviation and we use the maximum likelihood estimate of the standard deviation to rescale the outcome. We run BB-SSL for iterations and SSVS1 for iterations with a burnin period, initializing MCMC at the origin. We set . Estimating by fitting the Spike-and-Slab LASSO, we then set .

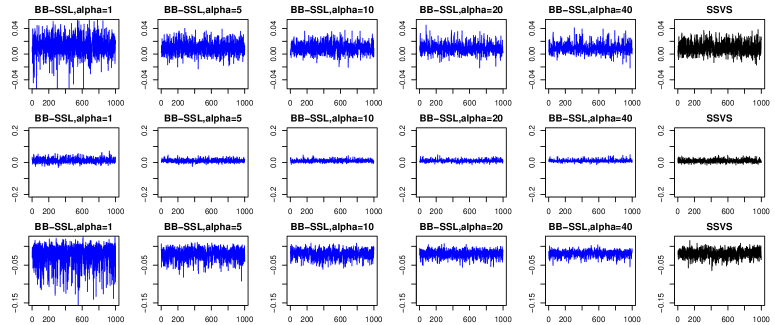

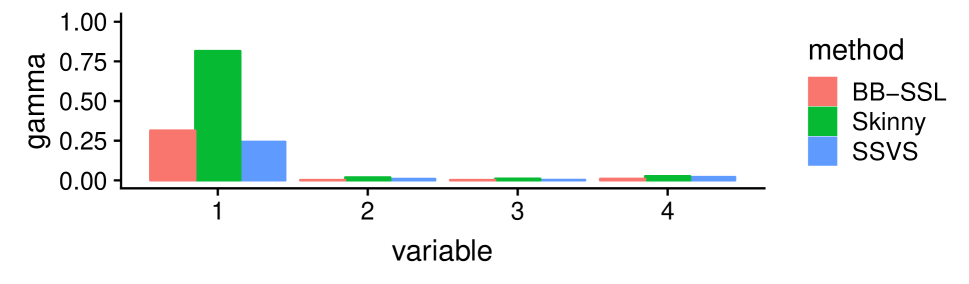

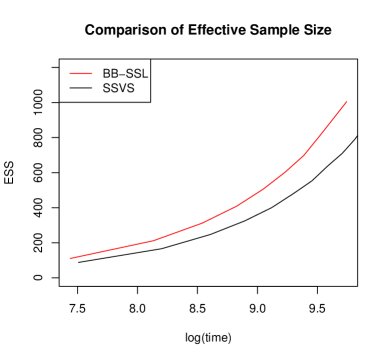

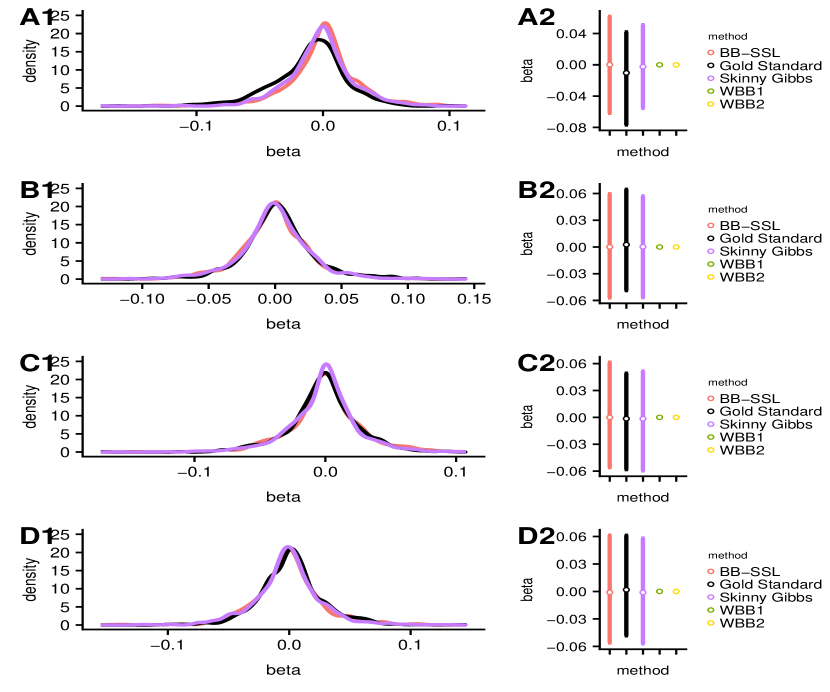

Figure 10 depicts estimated posterior density of selected coefficients in the model (19), showing that BB-SSL estimation is very close to the gold standard (SSVS). Further, BB-SSL identified of customers as “mail-deal-prone”, reaching accuracy and a false positive rate (treating SSVS estimation as the truth). Despite the comparable performance to SSVS, BB-SSL is advantageous in terms of computational efficiency. As shown in Figure 9, within the same amount of time, BB-SSL obtains more effective samples compared with SSVS and its advantage becomes even more significant as time increases. This experiment confirms our hypothesis that BB-SSL has a great potential as an approximate method for large datasets.

7 Discussion

In this paper we developed BB-SSL, a computational approach for approximate posterior sampling under Spike-and-Slab LASSO priors based on Bayesian bootstrap ideas. The fundamental premise of BB-SSL is the following: replace sampling from conditionals (which can be costly when either or are large) with fast optimization of randomly perturbed (reweigthed) posterior densities. We have explored various ways of performing the perturbation and looked into asymptotics for guidance about perturbing (weighting) distributions. We have concluded that with suitable conditions on the weights distribution, the pseudo-posterior distribution attains the same rate as the actual posterior in high-dimensional estimation problems (sparse normal means and high-dimensional regression). These theoretical results are reassuring and significantly extend existing knowledge about Weighted Likelihood Bootstrap (Newton et al. (2020)), which was shown to be consistent for iid data in finite-dimensional problems. We have shown in simulations and on real data that BB-SSL can approximate the true posterior well and can be computationally beneficial. The GBS method of Shin et al. (2020) could potentially greatly improve the scalability of BB-SSL. We leave this direction for future research.

References

- Ando and Modigliani (1963) Ando, A. and Modigliani, F. (1963). The “life cycle” hypothesis of saving: Aggregate implications and tests. The American Economic Review, 53(1):55–84.

- Bai et al. (2020) Bai, R., Moran, G. E., Antonelli, J. L., Chen, Y., and Boland, M. R. (2020). Spike-and-slab group lassos for grouped regression and sparse generalized additive models. Journal of the American Statistical Association (to appear).

- Belsley et al. (2005) Belsley, D. A., Kuh, E., and Welsch, R. E. (2005). Regression diagnostics: Identifying influential data and sources of collinearity, volume 571. John Wiley & Sons.

- Beygelzimer et al. (2013) Beygelzimer, A., Kakadet, S., Langford, J., Arya, S., Mount, D., and Li, S. (2013). FNN: fast nearest neighbor search algorithms and applications. R package version, 1(1).

- Bhattacharya et al. (2016) Bhattacharya, A., Chakraborty, A., and Mallick, B. K. (2016). Fast sampling with Gaussian scale mixture priors in high-dimensional regression. Biometrika, 103(4):985.

- Bhattacharya et al. (2015) Bhattacharya, A., Pati, D., Pillai, N. S., and Dunson, D. B. (2015). Dirichlet–Laplace priors for optimal shrinkage. Journal of the American Statistical Association, 110(512):1479–1490.

- Bottolo and Richardson (2010) Bottolo, L. and Richardson, S. (2010). Evolutionary stochastic search for Bayesian model exploration. Bayesian Analysis, 5(3):583–618.

- Carbonetto and Stephens (2012) Carbonetto, P. and Stephens, M. (2012). Scalable variational inference for Bayesian variable selection in regression, and its accuracy in genetic association studies. Bayesian Analysis, 7(1):73–108.

- Carvalho et al. (2010) Carvalho, C. M., Polson, N. G., and Scott, J. G. (2010). The horseshoe estimator for sparse signals. Biometrika, 97(2):465–480.

- Clyde et al. (2011) Clyde, M. A., Ghosh, J., and Littman, M. L. (2011). Bayesian adaptive sampling for variable selection and model averaging. Journal of Computational and Graphical Statistics, 20(1):80–101.

- Deshpande et al. (2019) Deshpande, S. K., Ročková, V., and George, E. I. (2019). Simultaneous variable and covariance selection with the multivariate spike-and-slab lasso. Journal of Computational and Graphical Statistics, 28(4):921–931.

- Efron (2012) Efron, B. (2012). Bayesian inference and the parametric bootstrap. The Annals of Applied Statistics, 6(4):1971.

- Fong et al. (2019) Fong, E., Lyddon, S., and Holmes, C. (2019). Scalable nonparametric sampling from multimodal posteriors with the posterior bootstrap. In International Conference on Machine Learning, pages 1952–1962.

- George and McCulloch (1993) George, E. I. and McCulloch, R. E. (1993). Variable selection via Gibbs sampling. Journal of the American Statistical Association, 88(423):881–889.

- George and McCulloch (1997) George, E. I. and McCulloch, R. E. (1997). Approaches for Bayesian variable selection. Statistica Sinica, 7(2):339–373.

- Geweke (1991) Geweke, J. (1991). Efficient simulation from the multivariate normal and student-t distributions subject to linear constraints and the evaluation of constraint probabilities. In Computing science and statistics: Proceedings of the 23rd symposium on the interface, pages 571–578.

- Geweke (1996) Geweke, J. (1996). Variable selection and model comparison in regression. In Bayesian Statistics 5.

- Hans (2009) Hans, C. (2009). Bayesian lasso regression. Biometrika, 96(4):835–845.

- Ishwaran and Rao (2005) Ishwaran, H. and Rao, J. S. (2005). Spike and slab gene selection for multigroup microarray data. Journal of the American Statistical Association, 100(471):764–780.

- Jaccard (1912) Jaccard, P. (1912). The distribution of the flora in the alpine zone. 1. New Phytologist, 11(2):37–50.

- Johndrow et al. (2020) Johndrow, J. E., Orenstein, P., and Bhattacharya, A. (2020). Bayes shrinkage at GWAS scale: Convergence and approximation theory of a scalable MCMC algorithm for the horseshoe prior. Journal of Machine Learning Research (to appear).

- Johnson and Rossell (2012) Johnson, V. E. and Rossell, D. (2012). Bayesian model selection in high-dimensional settings. Journal of the American Statistical Association, 107(498):649–660.

- Li et al. (2019) Li, Z., Mccormick, T., and Clark, S. (2019). Bayesian joint spike-and-slab graphical lasso. In International Conference on Machine Learning, pages 3877–3885.

- Lyddon et al. (2018) Lyddon, S., Walker, S., and Holmes, C. C. (2018). Nonparametric learning from Bayesian models with randomized objective functions. In Advances in Neural Information Processing Systems, pages 2071–2081.

- Madigan and Raftery (1994) Madigan, D. and Raftery, A. E. (1994). Model selection and accounting for model uncertainty in graphical models using Occam’s window. Journal of the American Statistical Association, 89(428):1535–1546.

- Martin and Walker (2014) Martin, R. and Walker, S. G. (2014). Asymptotically minimax empirical Bayes estimation of a sparse normal mean vector. Electronic Journal of Statistics, 8(2):2188–2206.

- Meyer et al. (2014) Meyer, D., Dimitriadou, E., Hornik, K., Weingessel, A., Leisch, F., Chang, C., and Lin, C. (2014). e1071: Misc functions of the department of statistics (e1071), TU Wien. R package version, 1(3).

- Mitchell and Beauchamp (1988) Mitchell, T. J. and Beauchamp, J. J. (1988). Bayesian variable selection in linear regression. Journal of the American Statistical Association, 83(404):1023–1032.

- Moran et al. (2019) Moran, G. E., Ročková, V., George, E. I., et al. (2019). Variance prior forms for high-dimensional Bayesian variable selection. Bayesian Analysis, 14(4):1091–1119.

- Narisetty et al. (2019) Narisetty, N. N., Shen, J., and He, X. (2019). Skinny Gibbs: A consistent and scalable Gibbs sampler for model selection. Journal of the American Statistical Association, 114(527):1205–1217.

- Newton et al. (2020) Newton, M. A., Polson, N. G., and Xu, J. (2020). Weighted Bayesian bootstrap for scalable posterior distributions. Canadian Journal of Statistics (In Press).

- Newton and Raftery (1994) Newton, M. A. and Raftery, A. E. (1994). Approximate Bayesian inference with the weighted likelihood bootstrap. Journal of the Royal Statistical Society: Series B (Methodological), 56(1):3–26.

- Ng and Newton (2020) Ng, T. L. and Newton, M. A. (2020). Random weighting to approximate posterior inference in lasso regression. arXiv e-prints, arXiv:2002.02629.

- Ni et al. (2012) Ni, J., Neslin, S. A., and Sun, B. (2012). Database submission—The ISMS durable goods data sets. Marketing Science, 31(6):1008–1013.

- Papandreou and Yuille (2010) Papandreou, G. and Yuille, A. L. (2010). Gaussian sampling by local perturbations. In Advances in Neural Information Processing Systems, pages 1858–1866.

- Park and Casella (2008) Park, T. and Casella, G. (2008). The Bayesian Lasso. Journal of the American Statistical Association, 103(482):681–686.

- Plummer et al. (2006) Plummer, M., Best, N., Cowles, K., and Vines, K. (2006). CODA: convergence diagnosis and output analysis for MCMC. R News, 6(1):7–11.

- Ročková (2018a) Ročková, V. (2018a). Bayesian estimation of sparse signals with a continuous spike-and-slab prior. The Annals of Statistics, 46(1):401–437.

- Ročková (2018b) Ročková, V. (2018b). Particle EM for variable selection. Journal of the American Statistical Association, 113(524):1684–1697.

- Ročková and George (2014) Ročková, V. and George, E. I. (2014). EMVS: The EM approach to Bayesian variable selection. Journal of the American Statistical Association, 109(506):828–846.

- Ročková and George (2018) Ročková, V. and George, E. I. (2018). The spike-and-slab lasso. Journal of the American Statistical Association, 113(521):431–444.

- Ročková and Moran (2017) Ročková, V. and Moran, G. (2017). SSLASSO: The Spike-and-Slab LASSO. URL https://cran.r-project.org/package=SSLASSO, 1:25.

- Scheffé (1947) Scheffé, H. (1947). A useful convergence theorem for probability distributions. The Annals of Mathematical Statistics, 18(3):434–438.

- Shin and Liu (2018) Shin, M. and Liu, J. S. (2018). Neuronized priors for Bayesian sparse linear regression. arXiv:1810.00141.

- Shin et al. (2020) Shin, M., Wang, L., and Liu, J. S. (2020). Scalable uncertainty quantification via generative bootstrap sampler. arXiv:2006.00767.

- Tang et al. (2018) Tang, Z., Shen, Y., Li, Y., Zhang, X., Wen, J., Qian, C., Zhuang, W., Shi, X., and Yi, N. (2018). Group spike-and-slab lasso generalized linear models for disease prediction and associated genes detection by incorporating pathway information. Bioinformatics, 34(6):901–910.

- Tang et al. (2017) Tang, Z., Shen, Y., Zhang, X., and Yi, N. (2017). The spike-and-slab lasso Cox model for survival prediction and associated genes detection. Bioinformatics, 33(18):2799–2807.

- Trautmann et al. (2015) Trautmann, H., Steuer, D., Mersmann, O., Bornkamp, B., and Mersmann, M. O. (2015). Package ‘truncnorm’.

- Vivo et al. (2007) Vivo, P., Majumdar, S. N., and Bohigas, O. (2007). Large deviations of the maximum eigenvalue in Wishart random matrices. Journal of Physics A: Mathematical and Theoretical, 40(16):4317.

- Welling and Teh (2011) Welling, M. and Teh, Y. W. (2011). Bayesian learning via stochastic gradient Langevin dynamics. In Proceedings of the 28th international conference on machine learning (ICML-11), pages 681–688.

- Xu et al. (2014) Xu, M., Lakshminarayanan, B., Teh, Y. W., Zhu, J., and Zhang, B. (2014). Distributed Bayesian posterior sampling via moment sharing. In Advances in Neural Information Processing Systems, pages 3356–3364.

- Zhang and Zhang (2012) Zhang, C.-H. and Zhang, T. (2012). A general theory of concave regularization for high-dimensional sparse estimation problems. Statistical Science, 27(4):576–593.

Appendix A Proofs

This section presents proofs of the main theoretical statements: Section A.1 shows the proof of Theorem 4.1. Section A.2 presents the proof of Corollary 4.1. Section A.3 shows an example for the remark under Theorem 4.1. Section A.4 proves Theorem 4.2 and Theorem 4.3. Section A.5 proves Corollary 4.1. Section A.6 introduces a motivation for Section 3.1.

A.1 Proof of Theorem 4.1

A.1.1 Definitions and Lemmas used in the proof of Theorem 4.1

Denote constants

and

With slight abuse of notation, we denote the marginal prior (after integrating out ) by

Similarly as in Ročková (2018a), the conditional mixing weight between the spike and the slab will be denoted with

| (20) |

and the weighted penalty with

The quantities and are analogues of and defined in (5) (main manuscript). Here, we have emphasized the dependence on and and suppressed the dependence on since this parameter is treated as fixed in our theory. Finally, we denote

and (similarly as in Ročková (2018a))

The following Lemma (a version of Theorem 3.1 in Ročková (2018a)) will be useful for characterizing the BB-SSL posterior properties.

Lemma A.1.

Notice that is the normal-means analogue of (defined below (4) in the main manuscript) where we have added to emphasize its dependence on and . Next, we will need an upper and lower bound for . When and , has two modes and Ročková (2018a) shows that can also be written as

where is the local mode (not the global mode) of . It follows from Theorem 3.1 in Ročková (2018a) and Lemma 1.2 in the Appendix of Ročková (2018a) that

| (22) |

where

Based on these facts, we then obtain the following simple Lemma.

Lemma A.2.

Proof.

Since and , from Lemma A.1 (the discussion below) and the fact that , we have

The other inequality is obtained similarly.∎

Lemma A.3.

For any fixed constant , and a random variable , we have

where and are the standard normal distribution and density functions.

Proof.

Denote a truncated normal random variable with and recall that

Then we have

A.1.2 Proof of Theorem 4.1

First assume that . Throughout this section, we will simply denote . We want to obtain the expression for BB-SSL estimate . Notice that the objective function (13) for BB-SSL can be written as

| (24) |

where , , and . So from (21), the mode estimator for satisfies

The BB-SSL estimate can then be calculated via . Equation (3.2) in Ročková (2018a) says that

From the chain rule and the fact that

we know

Thus,

| (25) |

From the Markov’s inequality, we know that for any ,

Thus, in order to prove the desired statement, we only need to bound . Notice that for the separable SSL prior (i.e. with a fixed value of ), the posterior is separable and we obtain

We will bound the risk separately for active and inactive coordinates.

Active coordinates

For active coordinates, we have

| (26) |

where

Now we bound and separately. First,

| (27) |

where utilizes the observation from Equation (25). Deploying Lemma A.2 in equation (27), we get (when is sufficiently large)

| (28) |

where uses the fact that , , and we denote , and follows from the Markov’s inequality.

For , we have

| (29) |

where utilizes the fact that from Equation (25), and we abbreviate . In order to bound (29), we bound separately.

-

•

To bound : When and , following the proof of Theorem 4.1 in Ročková (2018a), we know that and thus . This implies , so we have

where follows from the fact that

and

In view that , we have

-

•

To bound : When , we have

So in view that , we have

-

•

To bound : When , we have , thus when is sufficiently large,

So plugging the above bounds into Equation (29), we obtain

| (30) |

Inactive coordinates

For inactive coordinates, we have

| (31) |

where uses the fact that when and when in view of Equation (25), and we denote

Now we bound separately.

For the first term in (31), when is sufficiently large, we have

| (32) |

where follows from the fact that when is sufficiently large, , which ensures that Lemma A.2 holds, uses Lemma A.3, follows from the fact that for all , and here always holds when is sufficiently large.

For the third term in (31), utilizing condition (3), when is sufficiently large, we have

In (31), combining the bound on , the risk for inactive coordinates will be bounded

Combining the risk for active and inactive coordinates, we obtain

Then from the Markov’s inequality, for any ,

where . This means when , for any ,

For a general fixed value , notice that we can always rescale the model so that it becomes

And thus all previous analysis holds for the rescaled model. Thus, for any ,

A.2 Proof of Corollary 4.1

The condition (1) of Theorem 4.1 is satisfied. With , the condition (2) also holds because when , and when , . Both of them satisfy condition (2). So we only need to check condition (3).

When , the following equation holds for any ,

where (a) uses the fact for any . Inequality (b) uses . Inequality (c) uses Chernoff bound and we need for the above inequality to hold. Notice that when , we can directly get

Setting and , we have

| (33) |

Setting , we notice that when is sufficiently large and thus condition (3) always holds when is sufficiently large. We can get Lemma 4.1 by applying Theorem 4.1.

Now let us consider the case when depends on . From the proof of Theorem 4.1, we know that for any fixed ,

where follows from the fact that the dominating term in the upper bound for risk comes from . When we have . Thus

An ideal choice of should thus satisfy . We thereby suggest choosing when , observing that and thus

A.3 Explanation of Remarks below Corollary 4.1

We utilize the notation introduced in Section A.1.1. Here we want to show that for where is a fixed constant, the risk for BB-SSL arising from (14) can be arbitrarily large.

From the proof of Theorem 4.1, we know that for active coordinate , when is sufficiently large,

| (34) |

where follows from Equation (25), follows from Lemma A.2, and we denote

Notice that and as ,

where is integrable. Thus, direct application of the Dominated Convergence Theorem shows that as ,

Plugging into Equation (34), we know that when is sufficiently large,

For all constants which satisfy , we have

We set

Then, suppose , when is sufficiently large, we have

where

Notice that is always satisfied when is sufficiently large, so we know that when is sufficiently large,

where the lower bound depends on through . For any fixed, sufficiently large , when becomes larger and larger, becomes smaller and smaller, and as , , and the lower bound goes to infinity, which implies that as .

Thus, we conclude that the risk depends on the truth and for any fixed, sufficiently large , when one of the coordinates becomes arbitrarily large, the risk can also be arbitrarily large.

A.4 Proof of Theorem 4.2 and Theorem 4.3

A.4.1 Definitions and Lemmas used in Theorem 4.2 and Theorem 4.3

We rewrite model (1) in a matrix form and denote

where is a vector of all 0’s. We write and denote with

and with

| (35) |

Notice that the BB-SSL solution satisfies . The matrix norm is defined as where is the vector -norm. Write . We use to denote the vector 1-norm. We define

| (36) |

with defined as

where is equal to the defined in Equation (20). We fix in and thus simply write . Notice that

The proofs below use similar ideas and techniques as Ročková and George (2018). We first outline auxiliary Lemmas and then prove them later in this section.

Definition A.1.

Let . We say that satisfies the -null consistency (-NC) condition with a penalty function if

Lemma A.4.

Under Condition (5) in Theorem 4.2, we have

i.e. satisfies the -NC condition with probability approaching 1.

Lemma A.5.

Under Conditions (1)-(5) in Theorem 4.2, given that and satisfies -NC condition, we have

where and is any sequence that satisfies .

Lemma A.6.

If, for ,

| (37) |

then defined in (35) lies inside a cone

with high probability, where is the active set of ’s, and

with the -th dimension of .

Lemma A.7.

Definition A.2.

The minimal restricted eigenvalue is defined as

Definition A.3.

The compatibility number of vectors in cone is defined as

A.4.2 Proof of Lemma A.4

This Lemma is a direct consequence of Proposition 3 of Zhang and Zhang (2012). This Proposition says the following. In a regression model (1), suppose and , and

| (38) |

Then, the -NC condition is satisfied with probability at least , provided that

| (39) |

From the Condition (5), we know that (A.4.2) holds with . Thus, we only need to show (38) holds. Denote

Notice that from Proposition 5 in Moran et al. (2019) and (38) holds trivially when . Thus, in order to show (38), we only need to show that

Notice that

where follows from L’Hopital’s rule. It implies that there exists a positive constant such that, for all , and thus we have

where follows from L’Hopital’s rule. Thus, for all , when is sufficiently large. For ,

is always satisfied when is sufficiently large. Combining the above, we know that (when is sufficiently large)

Recall that Proposition 5 of Moran et al. (2019) implies that

Thus, if , when is sufficiently large, we know that . To sum up, if then (for is sufficiently large)

and thus

A.4.3 Proof of Lemma A.5

On the event , since , we have

where (a) uses the assumption (4) in Theorem 4.2, the fact and Spike. The inequality (b) follows from and the Cauchy-Schwarz inequality . The inequality (d) follows from the fact that where , and . Thus, from the Markov’s inequality, on the event that , we have for any ,

Set where , we have

| (40) |

When , we have

| (41) |

Notice that

where (e) follows from . Plugging this into (41), we have

| (42) |

Since the -NC condition holds, we have

| (43) |

Thus, on condition that , if we choose , we have ,

| (44) |

where (f) follows from Equation (42), (g) follows from the definition of and the fact that for any . We set if and if . The last inequality directly follows from the -NC condition (43).

Previous analysis implies that under conditions (1), (4) and (5) in Theorem 4.2 (and assuming , and that the -NC condition holds), whenever holds, (44) holds. Thus, when and satisfies -NC condition,

Notice that the conditions (2) and (3) in Theorem 4.2 say

Thus, as ,

So given that and that satisfies -NC condition, we have

Combined with Equation (40), we know (given that and satisfies -NC condition), the following holds

which is equivalent to the conclusion in Lemma A.5.

A.4.4 Proof of Lemma A.6

A.4.5 Proof of Lemma A.7

The proof follows from the proof of Lemma 1 in the Appendix of Zhang and Zhang (2012). For any , denote with the vector where the -th element is 1 and all the other elements are 0. Denote

Notice that . For any , leads to

where follows from the fact that . Thus, for any ,

Again, from the definition of (36) and Proposition 5 in Moran et al. (2019), we have

A.4.6 Proof of Theorem 4.2

The proof follows from the proof of Theorem 7 in Ročková and George (2018). First, we assume that (i) ; (ii) , (iii) , (iv) and (v) holds. Then, from Lemma A.7, we know that

where is defined in Lemma A.7. Following Ročková and George (2018), we denote . Notice that is the inflection point of in the -th direction while keeping the other coordinates fixed. Since when is sufficiently large, is well-defined when is sufficiently large. Denote and . From the basic inequality , we get

| (47) |

where follows from the fact that when and we denote , uses Holder inequality. So, from Equation (47) and Lemma A.6, we have

where (a) follows from the definition of . This is equivalent to

and consequently,

where follows from . Thus,

where

For simplicity assume that with . Then , so

Thus, the desired conclusion holds when conditions (i)-(v) hold. Now, we only need to verify that . Notice that (i) implies (v) from Lemma A.6 and

Combined with Lemma A.4 and Lemma A.5, we have

This means . In addition, assumptions (2) and (3) in Theorem 4.2 say that

Thereby, from the union bound, . Since

We have

A.4.7 Proof of Theorem 4.3

The proof follows from the proof of Theorem 8 in Ročková and George (2018). Notice that

First, we prove the high probability bound for . Since , we know if (i) ; (ii) , then

| (48) |

where follows from and Holder Inequality, follows from Lemma A.7. From Theorem 4.2, , and using , we have

Plugging into (48), we know (i), (ii), plus (iii) and (iv) implies the following:

Thus, whenever (i)-(iv) holds, in view that , we have

Thus, whenever (i)-(iv) holds,

It follows from definition of that

Notice that the difference between and only depends on and satisfies

Set , then when . Thus, from triangle inequality,

where the right hand side goes to zero as goes to infinity. Thus, we have

A.5 Proof of Corollary 4.1

We notice that if , we have , , . So we only need to prove the two high probability bounds for the order statistics for . Let , from the union bound we have

Since , we know . From the proof of Corollary 4.1 and the union bound, for any ,

Set when is sufficiently large, then . If , we have , , . Using the fact that , we can prove

Thus, conditions (1)-(4) hold for both and where .

A.6 Derivation of Observations in Section 3.1

In this section, we theoretically justify our statements from Section 3.1.

A.6.1 Notation

Define

Next, define

where is the Gaussian density with mean and variance . The quantities are defined in a similar way in Section 3.1 in the main paper, with replaced by . Throughout this section, we assume that the parameters and satisfy , where and with some constant .

A.6.2 Active Coordinates

Proposition 1.

Assume the true posterior defined in (8) with an active coordinate. Conditioning on the event , we have

Proof.

Without loss of generality, we assume .

| (49) |

We consider the four terms in the denominator separately. It is helpful to divide each of them by . Regarding the first term, we have

| (50) |

Regarding the second term in the denominator, from the Mills ratio we have

where . Thus,

| (51) |

For the third term in the denominator, we write

| (52) |

For the fourth term, we then have

where . Thus,

| (53) |

Proposition 2.

For the true posterior defined in (8), we have

Proof.

Setting , we have

| (54) |

Notice that both

For any , only one of and holds, and the denominator in (54) does not depend on , so . ∎

Proposition 3.

Consider the fixed WBB estimator . Conditioning on and , when and , we have

Proof.

Fixed WBB estimate satisfies equation (11) in the main text. Without loss of generality, we assume . Conditioning on , when ,

Proposition 4.

Consider the fixed WBB estimator . Conditioning on the event that , we have

Proof.

The fixed WBB estimator satisfies Equation (11). When is sufficiently large, from Proposition 5 in Moran et al. (2019), we have

| (55) |

Thus, from the Markov’s inequality, we find

| (56) |

where (a) follows from Equation (11), (b) follows from the condition and (55). Notice that

In order to bound , notice that

Thus, following the same analysis as that for Equation (29), (30) in Section A.1.2, we know that

and thus, the right hand size of (56) satisfies

Thus holds. ∎

A.6.3 Inactive Coordinates

Proposition 5.

For and defined in (8), when conditioning on , we have and .

Proof.

The expression for is given in (49). Again, we consider the four terms in the denominator separately and divide each one of them by . For the first term, we write

| (57) |

For the second term, for any fixed , we have

where . Since the right-hand size term

because we know

| (58) |

Regarding the third term in denominator, we obtain

| (59) |

Finally, for the fourth term, for any fixed , we have

where . Since the right hand side term satisfies

we know

| (60) |

Combining (57), (58), (59) and (60), we know that in (49), the and thus the . Thus and . ∎

We denote

which is the total variation distance between two probability measures and on a sigma-algebra of subsets of the sample space. We have the following result:

Proposition 6.

When is sufficiently large, conditioning on the event , we have

where is the Laplace distribution whose density is .

Proof.

Notice that

Thus, letting , since with we have for any fixed

which implies that

From Scheffé (1947), we know that converges in total variation to Laplace(1). ∎

Proposition 7.

Consider the fixed WBB estimator . Conditioning on , we have

Proof.

The definition of the fixed WBB sample is in (11). Notice that

Then, when is sufficiently large,

where the right-hand size

since and . Thus,

Remark A.1.

The random WBB is equivalent to the fixed WBB by setting weights to be where is the weight assigned to the prior term. Thus, using exactly the same arguments as fixed WBB, we can prove: .

Appendix B Details of Connection to NPL in Section 4.2

In Algorithm 3, we define the loss function as

| (61) |

Motivation for the Prior.

For paired data , Fong et al. (2019) uses independent prior which assumes that does not depend on :

However, this choice of might be problematic when the sample size is small. When is small, a well-specified prior can help us better estimate but this independent prior shrinks all coeffcients towards zero and will result in bias (see Figure 11).

One possible solution is to use where is the MAP of under SSL penalty. This choice of has an Empirical Bayes flavor (Martin and Walker (2014)). However, it includes information only from the posterior mode, ignoring shape information contained in the posterior variance. We could consider incorporating such information by adding noise to . We would want to be centered at the origin but not too far away from the origin. One choice that comes to mind is the spike distribution. So the prior becomes

where . If is close enough to the truth, we have . Since and , we can set where satisfies . Then the above prior becomes

Derivation for Equation (17)

When choosing in Algorithm 3, the NPL posterior of Fong et al. (2019) using Prior 2 becomes

where . Since and follow the same distribution, define and

where and thus .

Appendix C Another Gibbs Sampler with Complexity

A referee suggested a one-site Gibbs sampler which can be implemented with our continuous Spike-and-Slab LASSO prior and which can potentially improve computational efficiency. The sampler is reminiscent of Geweke (1996) who proposed a variant for point mass spikes to avoid getting stuck after generating . However, although George and McCulloch (1997) mentioned that this implementation might also be useful under continuous spike-and-slab priors (where the variance ratio of slab to spike is large), we find this implementation to be rarely used for continuous priors. One-site Gibbs samplers are expected to converge slower and yield higher autocorrelation, which is one of the reasons why block-Gibbs samplers have been preferred. We nevertheless explore this Gibbs sampler further.

The algorithm to implement Geweke (1996)’s Gibbs sampler for the Spike-and-Slab LASSO prior is outlined in Algorithm 4 and we further refer to it as Gibbs II. We calculate the vector through and is calculated once before running MCMC and updated after each update on . When , Algorithm 4 has complexity compared to for SSVS1 and for SSVS2. However, generating from the Truncated Normal distribution typically requires an accept-reject algorithm (Geweke, 1991) which creates some computational bottlenecks. We utilize the R package ‘truncnorm’ (Trautmann et al., 2015) which implements this accept-reject algorithm in C. The performance of Algorithm 4 against other methods is summarized in Table 4. We see that the per-iteration running time of Gibbs II is similar to SSVS2 (using the trick in Bhattacharya et al. (2016)), yet the serial correlation is higher than for both implementations of SSVS. Thus, contrary to the point-mass spike, Algorithm 4 (which is based on Geweke (1996)) trades computational efficiency for serial correlation. In general, the time used for generating the same number of effective samples is slightly longer than SSVS2, but improves significantly over SSVS1. From this observation, we believe Gibbs II is yet another useful method to speed up the standard SSVS1 under the Spike-and-Slab LASSO prior.

| method | time per 100 iter (sec) | ESS per 100 iter | lag-one auto correlation on ’s | time per 100 ESS (sec) |

| BB-SSL | 0.7 | 100 | -0.002 | 0.7 |

| SSVS1 | 40 | 98 | 0.006 | 40.82 |

| SSVS2 | 3.2 | 98 | 0.006 | 3.27 |

| Gibbs II | 3.1 | 83 | 0.100 | 3.73 |

A less relevant, but perhaps interesting, observation is that since the Spike-and-Slab LASSO prior is a mixture of Laplace distributions, SSVS1 (which augments the data with ’s) can be seen as a generalization of the MCMC algorithm in Park and Casella (2008) while Gibbs II can be seen as a spike-and-slab version of the MCMC algorithm in Hans (2009). Our conclusion from this exercise is that, for the Spike-and-Slab LASSO prior, BB-SSL is actually doing better (both in terms of serial correlation and timing) compared with Gibbs II.

Appendix D Details on Computational Complexity Analysis

Below are details for the computational complexity analysis as shown in Table 1 of the main text.

BB-SSL, WBB1, WBB2.

BB-SSL uses R package SSLASSO (Ročková and Moran (2017)) to implement the coordinate-descent algorithm in Ročková and George (2018). It iteratively updates until convergence. At each iteration, we first update the active coordinates, then the candidate coordinates, and finally the inactive coordinates. The total number of iterations is limited to a pre-defined number. There are two ways to update each coordinate, one way is to keep track of a residual vector and for each coordinate we compute the inner product between the residual vector and – this takes ; another way is to pre-compute the Gram matrix and for each coordinate, we calculate the inner product between and – this takes . For both ways, we update every iterations where each update is . So for a single value of , SSLASSO is . For a sequence of ’s, complexity is where is the length of ’s. Usually if the biggest is large enough, we would expect that the larger ’s can reach convergence quickly using the estimated from previous ’s, so usually it takes less than .

SSVS1.

The computational complexity for Algorithm 1 is per iteration when . Under this setting, we use the Woodbury matrix identity to simplify the matrix multiplication , whose complexity is .

SSVS2.

Using Bhattacharya et al. (2016)’s matrix inversion formula to generate the -dimensional multivatiate Gaussian takes .

Skinny Gibbs.