acks

Acknowledgments and Disclosure of Funding

Risk-Monotonicity in Statistical Learning

Abstract

Acquisition of data is a difficult task in many applications of machine learning, and it is only natural that one hopes and expects the population risk to decrease (better performance) monotonically with increasing data points. It turns out, somewhat surprisingly, that this is not the case even for the most standard algorithms that minimize the empirical risk. Non-monotonic behavior of the risk and instability in training have manifested and appeared in the popular deep learning paradigm under the description of double descent. These problems highlight the current lack of understanding of learning algorithms and generalization. It is, therefore, crucial to pursue this concern and provide a characterization of such behavior. In this paper, we derive the first consistent and risk-monotonic (in high probability) algorithms for a general statistical learning setting under weak assumptions, consequently answering some questions posed by (viering2019open, ) on how to avoid non-monotonic behavior of risk curves. We further show that risk monotonicity need not necessarily come at the price of worse excess risk rates. To achieve this, we derive new empirical Bernstein-like concentration inequalities of independent interest that hold for certain non-i.i.d. processes such as Martingale Difference Sequences.

1 Introduction

Guarantees on the performance of machine learning algorithms are desirable, especially given the widespread deployment. A traditional performance guarantee often takes the form of a generalization bound, where the expected risk associated with hypotheses returned by an algorithm is bounded in terms of the corresponding empirical risk plus an additive error which typically converges to zero as the sample size increases. However, interpreting such bounds is not always straight forward and can be somewhat ambiguous. In particular, given that the error term in these bounds goes to zero, it is tempting to conclude that more data would monotonically decrease the expected risk of an algorithm such as the Empirical Risk Minimizer (ERM). However, this is not always the case; for example, loog2019minimizers showed that increasing the sample size by one, can sometimes make the test performance worse in expectation for commonly used algorithms such as ERM in popular settings including linear regression. This type of non-monotonic behavior is still poorly understood and indeed not a desirable feature of an algorithm since it is expensive to acquire more data in many applications.

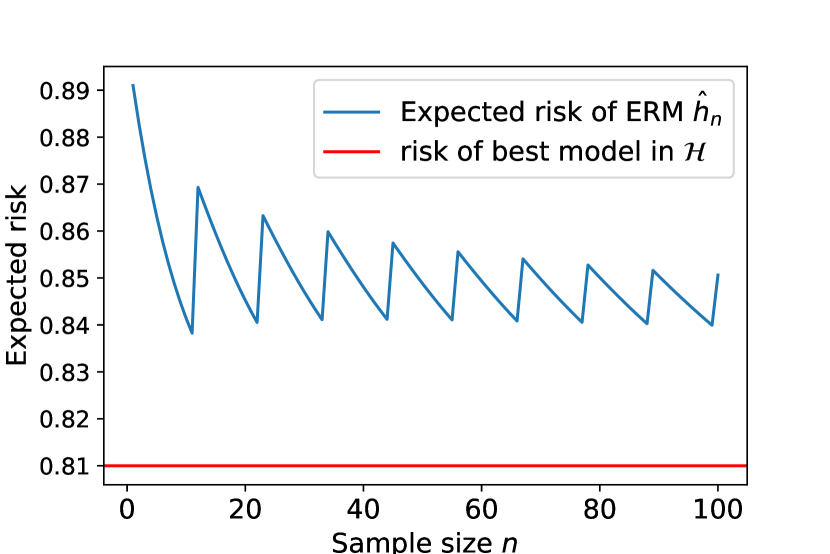

Non-monotonic behavior of risk curves (shalev2014understanding, )—the curve of the expected risk as a function of the sample size—has been observed in many previous works (duin1995, ; opper1996statistical, ; smola2000advances, ; Opper2001, ) (see also (loog2019minimizers, ; viering2021shape, ) for nice accounts of the literature). At least two phenomena have been identified as being the cause behind such behavior. The first one, coined peaking (kramer2009peaking, ; duin2000classifiers, ), or double descent according to more recent literature (belkin2018reconciling, ; spigler2018jamming, ; belkin2019two, ; dereziski2019exact, ; deng2019model, ; mei2019generalization, ; nakkiran2019more, ; nakkiran2020deep, ; derezinski2020exact, ; chen2020multiple, ; cheema2020geometric, ; d2020triple, ; nakkiran2020optimal, ), is the phenomenon where the risk curve peaks at a certain sample size . This sample size typically represents the cross-over point from an over-parameterized to under-parameterized model. For example, when the number of data points is less than the number of parameters of a model (over-parameterized model), such as Neural Networks, the expected risk can typically increase until the number of data points exceeds the number of parameters (under-parameterized model). The second phenomenon is known as dipping (loog2012dipping, ; loog2015contrastive, ), where the risk curve reaches a minimum at a certain sample size and increases after that—never reaching the minimum again even for very large . This phenomenon typically happens when the algorithm is trained on a surrogate loss that differs from the one used to evaluate the risk (ben2012minimizing, ).

It is becoming more apparent that the two phenomena just mentioned (double descent and dipping) do not fully characterize when non-monotonic risk behavior occurs (Loog10625, ). loog2019minimizers showed that non-monotonic risk behavior could happen outside these settings and formally prove that the risk curve of ERM is non-monotonic in linear regression with prevalent losses. The most striking aspect of their findings is that the risk curves in some of the cases they study can display a perpetual “oscillating” behavior; there is no sample size beyond which the risk curve becomes monotone—see Figure 1. In such cases, the risk’s non-monotonicity cannot be attributed to the peaking/double descent phenomenon. Moreover, they rule out the dipping phenomenon by studying the ERM on the actual loss (not a surrogate loss).

The findings of loog2019minimizers stress our current lack of understanding of generalization. This was echoed more particularly by viering2019open , who posed the following question as part of a COLT open problem:

| How can we provably avoid non-monotonic behavior? |

While excess risk bounds are typically monotonic, this does not guarantee the monotonicity of the actual risk. In this work, we study under which assumptions on the learning problem there exist consistent and risk monotonic algorithms. We also aim to quantify the price to pay, in terms of corresponding excess risk rates, for achieving risk monotonicity.

Contributions.

In this work, we answer some questions posed by viering2019open by presenting an algorithm that is both consistent and risk-monotonic in high probability under weak assumptions on the learning problem. Our algorithm is technically a “wrapper” that takes as input any base learning algorithm and makes up a new algorithm that is risk monotonic in high probability and enjoys essentially the same excess risk rate as . Crucially, our results show that risk monotonicity need not come at the expense of worse excess risk rates. In fact, we show that fast rates are achievable under a Bernstein condition (Definition 3).

Our results hold under the general statistical learning setting with a bounded loss. We even go beyond the standard i.i.d. assumption on the loss process. Our relaxed technical condition on the loss process, which is formalized in Assumption 1 below, is reminiscent of the condition characterizing Martingale Difference Sequences (MDS). In a nutshell, we will assume a setting where the instance random variables and the loss satisfy, for all hypotheses , , for some risk function . This is trivially satisfied in the i.i.d. case, where corresponds to the standard risk function. In general, this condition may be satisfied even if are dependent or have different marginal distributions. We argue that our relaxed assumption on the loss process is the weakest assumption under which studying risk-monotonicity still makes sense.

To achieve risk monotonicity under our loss process assumption, we derive a new concentration inequality/generalization bound of PAC-Bayesian flavor for MDS (see Proposition 5). This concentration inequality may be thought of as an empirical Freedman’s inequality freedman1975tail or as an extension of the empirical Bernstein inequality maurer2009empirical to MDS. Our concentration inequalities also have the advantage of being time-uniform with the optimal dependence on the number of samples. Here, time-uniform means that the inequalities hold for all sample sizes simultaneously. While standard concentration inequalities can be turned into time-uniform ones using a union bound over the number of samples , the resulting bounds will have a sub-optimal factor instead of the optimal111One can not improve on the factor by the law of iterated logarithm darling1967iterated . that we are able to get. Finally, our concentration bounds are easily derived using the guarantee of a recent parameter-free online learning algorithm—FreeGrad(MhammediK20, ). Our approach opens up the door for obtaining new concentration inequalities through the design of online learning algorithms.

Approach Overview.

Our approach to deriving the new concentration inequalities is based on the guarantee of the recent FreeGrad algorithm. The algorithm operates in rounds, where at each round , FreeGrad outputs in some convex set , say , then observes a vector , typically the sub-gradient of a loss function at the iterate . The algorithm guarantees a regret bound of the form , for all , where . What is more, FreeGrad’s outputs ensure the following (see (MhammediK20, , Theorem 5)):

| (1) |

where , , and , for any . Instantiating this guarantee in 1d with set to an MDS and taking (conditional) expectation in (1) shows that is a non-negative supermartingale, from which concentration results can be obtained via Ville’s inequality (a generalization of Markov’s inequality—see Lemma 18). Our proof technique is similar to the one introduced in (jun2019parameter, ),with the difference that we use the specific shape of FreeGrad’s potential function to build our supermartingale, which leads to a desirable empirical variance term in the final concentration bound.

On the side of risk monotonicity, given samples, the key idea behind our approach is to iteratively generate a sequence of distributions leading up to over hypotheses, where we only allow consecutive distributions, say and to differ if we can guarantee (with high enough confidence) that the risk associated with is lower than that of . To test for this, we compare the average empirical losses of hypotheses sampled from versus ones sampled from , taking into account the potential gap between empirical and population expectations. Applying our new concentration bounds to quantify this gap not only allows us to achieve risk monotonicity under a non-i.i.d. loss process but also enables us to achieve fast excess risk rates under the Bernstein condition. For the latter, it was crucial to have an empirical loss variance term in the concentration inequality.

Related Works.

Much work has already been done in efforts to mitigate the non-monotonic behavior of risk curves (viering2019making, ; nakkiran2020optimal, ; loog2019minimizers, ). For example, in the supervised learning setting with the zero-one loss, ben2011universal introduced the “memorize” algorithm that predicts the majority label on any test instance that was observed during training; otherwise, a default label is predicted. ben2011universal showed that this algorithm is risk-monotonic. However, it is unclear how their result could generalize beyond the particular setting they considered. Risk-monotonic algorithms are also known for the case where the model is correctly specified (see loog2019minimizers for an overview); in this paper, we do not make such an assumption.

Closer to our work is that of viering2019making who, like us, also used the idea of only updating the current predictor for sample size if it has a lower risk than the predictor for sample size . They determine whether this is the case by performing statistical tests on a validation set (or through cross-validation). They introduce algorithm wrappers that ensure that the risk curves of the final algorithms are monotonic with high probability. However, their results are specialized to the 0-1 loss and they do not answer the question by viering2019open on the existence of learners that guarantee a monotonic risk in expectation.

On the side of concentration bounds for non-i.i.d. processes, our results are somewhat similar to those found in e.g. howard2020time ; howard2021time . However, our technique for deriving them, which relies on the guarantee of a parameter-free online learning algorithm, is entirely different. The theoretical link between online regret and concentration inequalities was previously drawn—see e.g. rakhlin2017equivalence ; Foster2018 . However, our approach is slightly different as we use the monotonicity of an online algorithm’s potential function to get our concentration results. Thus, new concentration inequalities may be derived similarly by modifying the explicit potential function directly. Our approach is more similar to that of jun2019parameter who also derived concentration inequalities using guarantees of online betting algorithms that bet fractions smaller than one of their wealth at each round.

We allow for a parameter in our concentration bounds to make the results useful in the statistical learning setting. These bounds are of PAC-Bayesian type and are somewhat reminiscent of those in TolstikhinS13 ; mhammedi2019pac . We refer the reader to guedj2019primer for an overview of existing PAC-Bayesian bounds.

Outline.

In Section 2, we introduce the setting, notation, and relevant definitions. In Section 3, we present our new concentration inequalities for Martingale Difference Sequences and loss processes we are interested in (those that satisfy Assumption 1 below). In Section 4, we present our risk-monotonic algorithm wrapper and show that it achieves risk monotonicity in high probability. We conclude with a discussion in Section 5. The proofs of the new concentration inequalities and risk monotonicity are differed to Appendices B and C, respectively. Appendix A presents existing and new technical results needed in some of our proofs.

2 Preliminaries

In this section, we present the setting, notation, and relevant definitions for the rest of the paper.

Setting and Notation.

Throughout, we will assume an underlying probability space . Let [resp. ] be an arbitrary feature [resp. hypothesis] space, and let be a bounded loss function. We denote by the set of probability measures on . Data is represented by random variables that we assume are accessible to a learning algorithm in a sequential fashion. We use the concise notation for the tuple and denote by the -algebra generated by the random variables , with the convention that . We will write , for .

We will not assume that the random variables are independent and identically distributed. Instead, we will make the following weaker assumption on the loss process :

Assumption 1 (Process Assumption).

There exists a risk function such that the sequence of random variables satisfy , for all and .

When the random variables are i.i.d. and , , then Assumption 1 trivially holds with the standard risk function . In Assumption 1, the conditional distribution of given may be arbitrary as long as the corresponding conditional expectation of the loss of a given hypothesis is the same (equal to ) for all . Arguably, Assumption 1 represents the weakest condition under which studying risk monotonicity in the statistical learning setting still makes sense. We touch more on this point after defining risk monotonicity below. To simplify notation for the rest of this paper, we let

where is as in Assumption 1.

A learning algorithm is a map from to ; given data , the output of the algorithm is a distribution over hypotheses in . This definition includes deterministic algorithms for which the distribution is a Dirac at some . We will use the notation .

Throughout, we will make use of a fixed “prior” distribution over hypotheses in . In Section 4, we will present an algorithm wrapper that takes any base algorithm as input and makes a risk-monotonic algorithm out of it with essentially the same excess risk rate. The results of this paper are useful for base algorithms that output distributions that are absolutely continuous w.r.t. our choice of prior ; that is , for all 222We inherit this restriction from the PAC-Bayesian approach that we use to quantify generalization. In Appendix D, we show how this restriction can be removed in the i.i.d. setting (see also Remark 7).. In practice, if , may be a multivariate Gaussian around the origin and may also be a multivariate Gaussian around the ERM , in which case holds for all . We now define the notion of risk monotonicity we will work with:

Definition 1 (Risk Monotonicity).

For and , we say that a learning algorithm is -risk-monotonic if, with probability at least ,

| (2) |

Note that since the loss is positive, Fubini’s theorem implies that , for all . Thus, the condition in (2) requires the expected loss of algorithm on the next sample, conditioned on the past data, to decrease with the size of the data. We note that if Assumption 1 does not hold and depends on in an arbitrary fashion, then requiring (2) would be too strong. Thus, we will restrict our attention to processes that satisfy Assumption 1. We stress that the condition in this assumption is weaker than i.i.d., and allows the random variables to have different (conditional) distributions as long as the moment constraint is satisfied for all and .

The notion of monotonicity presented in loog2019minimizers ; viering2019open concerned only i.i.d. random variables, and requires the risk to be monotonic in expectation as opposed to in high probability. In particular, the strongest notation of monotonicity in loog2019minimizers , which they refer to as global -monotonicity, can be expressed as

| (3) |

where and . We will show that achieving risk-monotonicity in expectation up to a small fast rate term is as easy as achieving -risk-monotonicity—at least for bounded losses. In fact, we will show how our risk-monotonic (in the sense of Def. 1) algorithm can easily be turned into one that satisfies (3) up to a fast rate term.

Monotonicity alone is rather easy to achieve; it suffices to output a fixed hypothesis regardless of the training dataset. In this case, the risk would be constant, and so risk monotonicity is achieved by definition. In practice, it is important to generate hypotheses with low risk, and so a fixed hypothesis that does not dependent on data is likely to be useless. Formally, we want algorithms that are risk monotonic and consistent:

Definition 2 (Consistency).

Under Assumption 1, we say that algorithm is consistent if for any , .

We will go beyond the notation of consistency and study the rate of convergence of the risk of our algorithm to the optimal risk. We do this under the assumption that the loss process satisfies the Bernstein condition for :

Definition 3 (Bernstein Condition).

For and , the -Bernstein condition holds if the random variables and the loss satisfy, for all and all ,

for .

The Bernstein condition (audibert2004pac, ; bartlett2006convexity, ; bartlett2006empirical, ; erven2015fast, ; koolen2016combining, ) essentially characterizes the easiness of the learning problem. In particular, it implies that the conditional variance of the excess-loss random variable vanishes when the risk associated with the hypothesis gets closer to the -optimal risk . For bounded loss functions, the Bernstein condition with always holds, and so the results of this paper are always true for . The Bernstein condition with corresponds to the easiest learning setting. The case where interpolates naturally between these two extremes, where intermediate excess-risk rates are achievable. We refer the reader to (koolen2016combining, , Section 3) for examples of learning settings where a Bernstein condition holds.

Additional useful definitions.

For and , we define

| (4) | |||

| (5) |

Note that is not too large as a function of . In fact, the definitions of and imply that . In the next section, we present some new concentration inequalities of independent interest that will be useful in achieving risk-monotonicity under Assumption 1 while maintaining good excess risk rates.

3 New (PAC-Bayesian) Concentration Inequalities

In this section, we present some new concentration inequalities of PAC-Bayesian flavor that will be crucial to deriving our risk monotonic algorithm wrapper under Assumption 1. These concentration inequalities hold for non-i.i.d. data (which we require to accommodate Assumption 1), and are so-called time-uniform; the inequalities hold for all sample sizes simultaneously given a fixed confidence level. We explain below the advantage that this has in our setting.

We start by a new concentration inequality for Martingale Difference Sequences, from which we derive the bound we need under Assumption 1. First, we give the formal definition of an MDS:

Definition 4.

Let be a filtration w.r.t. the underlying probability space , i.e. is a sequence of non-decreasing sub--algebras of . A sequence of random variables is an MDS w.r.t. , if for all , is -measurable; ; and a.s.

With this in hand, we present our first concentration inequality:

Proposition 5 (PAC-Bayes for MDS).

Let and be as in (4). Further, let be a family of random variables taking values in and be a filtration such that is an MDS w.r.t to , for all . Then, for any distribution on and all , we have

| (6) |

where and .

The proof of the theorem is in Appendix B. The bound in Proposition 5 does not look like the typical PAC-Bayesian bound. However, simple algebra reveals that for any ,

Combining this with the fact that (by Jensen’s inequality), and (6), we obtain, under the same conditions as Proposition 5 that

| (7) |

where . When is a singleton, the concentration inequality in (7) can be viewed as an empirical version of Freedman’s inequality freedman1975tail for MDS. The inequality is also reminiscent of the PAC-Bayesian empirical Bernstein inequality due to TolstikhinS13 . In addition to it holding for MDS, another advantage of (7) is that it is time-uniform—it holds for all sample sizes , simultaneously. While standard concentration inequalities that hold for a fixed sample size can be turned into time-uniform ones by applying a union bound over sample sizes, the resulting inequalities will have sub-optimal factors under the main square-root error term. In contrast, the concentration inequality in (7) has a term, which matches the optimal dependence in according to the law of iterated logarithm darling1967iterated . MDS is a central concept in probability theory pena2008self and machine learning cesa06 , and so our result in Proposition 5 is of independent interest.

Interestingly, the concentration inequality in Proposition 5 is derived using the guarantee of a parameter-free online algorithm—FreeGrad. This opens the door for new ways of deriving such concentration inequalities through online learning algorithms, adding to existing results due to rakhlin2017equivalence ; Foster2018 ; jun2019parameter .

Using the result of Proposition 5, we are now going to derive a time-uniform “Empirical Bernstein” concentration inequality that holds under Assumption 1:

Theorem 6.

The restriction that in the theorem merely ensures that the denominator in the concentration bound remains positive. The set is guaranteed to be non-empty for all . In this case, is in whenever , which is a fairly weak condition on the distribution ; even for large models such as Neural Networks the -divergence does not typically grow superlinearly with the size of the sample used to generate the posterior ZhouVAAO19 . Nevertheless, we note that if one only cares about the i.i.d. setting then other concentration inequalities may be used to achieve risk monotonicity without restrictions on the posterior (see Appendix D).

The concentration inequality in Theorem 6 can be viewed as an extension of the empirical Bernstein inequality in maurer2009empirical ; TolstikhinS13 that holds under the non-i.i.d. condition described in Assumption 1. Our new bound is also time-uniform with the optimal dependence in the sample size . As mentioned before, simply applying a union bound to a standard (non-time-uniform) concentration inequalities to obtain its time-uniform version will lead to a sub-optimal dependence in . When is a singleton (i.e. no learning), the concentration inequality becomes reminiscent of an existing one due to howard2021time . However, the latter has a term that looks like, but is different than, the empirical variance, and so it is not directly comparable to ours. The proof of Theorem 6 is postponed to Appendix B.

Finally, we note that for any sample size the value of in Theorem 6 that minimizes the bound would typically fall within the interval . One can tune as a function of the data by treating as an extra “hypothesis” parameter. In the case of a finite grid of ’s, the result of Theorem 6 would hold for all inside the probability event as long as any instance is replaced by .

We now move on to describing our risk monotonic procedure that makes use of our new concentration inequality.

4 Risk Monotonicity in Statistical Learning

In this section, we combine the concentration inequality from Theorem 6 with a novel “greedy” procedure for selecting distributions over hypotheses to derive a risk monotonic algorithm in the statistical learning setting. With the right choice of gap sequence , the procedure we present in Algorithm 1 takes as input a base learning algorithm together with samples whose generating process satisfies Assumption 1, and returns a distribution over that has a monotonic risk as a function of with high probability. By leveraging our new concentration inequality in Theorem 6 to specify the gap sequence , we further show that achieving risk monotonicity need not deteriorate rates of convergence to the optimal risk . In fact, we show that it is possible to attain fast rates under the Bernstein condition (Definition 3). To arrive at this result, it was crucial for our concentration inequality to have an empirical variance term.

To simplify our analysis, we will focus our attention on base algorithms that are restricted in the following way:

Assumption 2 (Base Algorithm Restriction).

We assume access to a base algorithm such that for , prior distribution on , and all ,

| (8) |

In other words, we are restricting our attention to algorithms whose posteriors given samples of size do not have a divergence to the prior that grow too quickly with . We make this assumption to satisfy the technical conditions needed for the concentration bound in Theorem 6 to be non-vacuous. Assumption 2 is reasonable even for large Neural Network models ZhouVAAO19 333Besides, when the KL divergence is very large, it is often very hard to infer non-vacuous generalization bounds (which one may view as a prerequisite to achieving risk monotonicity) using a PAC-Bayesian approach..

In practice, if is , an option for is the algorithm that outputs a multivariate Gaussian distribution around a regularized ERM. The -divergence between the outputs of and can be controlled by tuning the regularisation parameter(s) and/or the co-variance matrix of the multivariate Gaussian.

Remark 7.

If one only cares about i.i.d. loss processes, Assumption 2 can be removed by using generalization bounds based on the standard Bernstein concentration inequality, e.g. (TolstikhinS13, ; MaurerP09, ), which would also enable our risk decomposition in Theorem 9 below (and thus fast rates). We make Assumption 2 only to bound the denominator in our (non-i.i.d) concentration in Theorem 6 away from zero, which is not needed for other concentration bounds in the i.i.d. setting such as those in (TolstikhinS13, ; MaurerP09, ) (see Appendix D for more detail).

To specify the sequence of gaps that our wrapper Algorithm 1 requires, we will use our concentration bound in Theorem 6. We recall that using this concentration bound instead of other existing ones allows us to I) achieve risk monotonicity under a weaker condition than i.i.d. on the loss process (Assumption 1 in this case); and II) to achieve potentially fast excess risk rates under the Bernstein condition. The latter is made possible by the fact that the concentration bound in Theorem 6 has an empirical loss variance term that allows a particularly useful decomposition of the excess risk under the Bernstein condition (see Theorem 9 below).

To give a concise expression of the gaps , we let , where are the intermediate distributions generated internally by Algorithm 1. With this, and the convention that , we define

| (9) | |||

We note that our Assumption 2 ensures that (which in turn ensures that the gaps are not too large), for all , where is as in (5). This follows from the fact that , and that there exists such that (by definition of in Algorithm 1). Furthermore, for all .

Before presenting our results for this section, we also note that Algorithm 1 assumes we can evaluate expectations over the output distributions of . Such expectations can be approximated via Monte Carlo sampling, and any approximation errors need be added to the gaps to maintain the guarantees we present. Alternatively, one can avoid estimating expectations by applying recent derandomization techniques, see e.g. rivasplata2020pac ; viallard2021general , or by using other, non PAC-Bayesian generalization bounds (see Appendix D).

We now state the guarantees of Algorithm 1. We start by the statement of risk-monotonicity (the proof is postponed to Appendix C):

Theorem 8 (Risk Monotonicity).

We now show that risk monotonicity need not come at a worse excess risk rate. Under the Bernstein condition, we have the following excess risk decomposition for the output of Algorithm 1:

Theorem 9 (Risk Decomposition).

We stress that this risk decomposition was only made possible by the fact that our concentration bound in Theorem 6 has an empirical loss variance term.

Theorem 9 shows that the excess risk of Algorithm 1 is at most a constant times the excess risk of the base algorithm , plus a potentially lower-order term . To appreciate what this additional term is doing, consider the case of a finite hypothesis class . In this case, the definition of in (9) implies that . Thus, interpolates between the fast rate under the best Bernstein condition with and the standard (up to log-log-factors) rate under the Bernstein condition with , which we recall always holds for bounded losses. What is more, if is finite and algorithm is the ERM, i.e. if is a Dirac at , then we have the following explicit excess risk rate for Algorithm 1:

Proposition 10.

The story is not much different for a continuous set . The standard excess risk rate one would expect from algorithm is , which can dominate the right-most term in our risk decomposition (10) since444We note that it is typical that , for .

Together, the above inequality and Theorem 9 show that fast rates for algorithm 1 are achievable whenever the Bernstein condition holds with and the base algorithm itself achieves a fast rate (when is finite and is the ERM, Proposition 10 shows that it is sufficient that ). Thus, risk monotonicity need not come at the price of a worse rate of convergence to the optimal risk. Finally, we note that the factor 3 in our risk decomposition (10) is just an artifact of our analysis. In fact, by slightly modifying our proof of Theorem 9, one can show that any factor in the interval is achievable at the cost of a larger lower-order term in (10).

Risk monotonicity in expectation.

The original open problem due to viering2019open was around risk monotonicity in expectation—as in (3). Our algorithm wrapper also allows us to almost555We thank Olivier Bousquet and his collaborators for pointing out a mistake in the original proof of Theorem 11. The theorem originally claimed that Algorithm 1 achieves risk-monotonicity in expection without the additive term in (12), which turns out not to be correct. achieve this notion of monotonicity with a slight modification of the sequence in (9); we essentially set the confidence level as a function of . In fact, the next result shows that risk monotonicity in expectation is achievable up to an additive fast-rate term:

Theorem 11.

We note that need not be too large since . However, while taking large will make the additive term in (12) small, it will increase the sample size beyond which (12) holds. Ignoring the additive term, the notion of risk-monotonicity in theorem 11 corresponds to the notion of weak -monotonicity in loog2019minimizers —one of their strongest notions of risk monotonicity since it holds for all data generating distributions (granted Assumption 1 holds, or the data is i.i.d.). We can modify Algorithm 1 to make it globally -monotonic, where (12) would hold for all (instead of ), by forcing the outputs of the algorithm to be for all .

5 Discussion and Future Work

The primary goal of this paper was to answer the fundamental question around the existence of a consistent, risk-monotonic algorithm in the general statistical learning setting. We answer this in the affirmative for a notation of monotonicity that holds with high probability and further show that there is virtually no cost for achieving this when it comes to excess-risk rates. We believe this is an important milestone in the search for risk-monotonic algorithms. It remains to see if risk-monotonicity in expectation is achievable; i.e. achieving (12) without the additive term.

From a computational perspective, the main setback of Algorithm 1 is that returning the distribution requires -calls to the base algorithm . This implies that 1 may run times slower than in the worst case. However, when the base algorithm outputs distributions centered at ERMs, it may be possible to efficiently generate the sequence of distributions by leveraging the fact that ERM solutions for sample sizes and can be close to each other.

When the loss is convex in the first argument, there is no need for a randomized algorithm666Randomization is also not needed if one is only interested in i.i.d. processes (see Appendix D). (i.e. we do not need ), and it is possible to efficiently generate a sequence of predictors with monotonic risk using an online convex optimization algorithm as the base algorithm . However, in general, it is unclear whether risk-monotonicity can be achieved without the (greedy) for-loop procedure of Algorithm 1. We note also that if one only wants a decreasing risk after some sample size , then computing the distributions is unnecessary. In this case, the for-loop in Algorithm 1 need only start at ; the resulting hypotheses would satisfy the monotonicity condition in Definition 1 for all .

Through Theorem 9, we showed that the excess risk of Algorithm 1 is at most three times that of the base algorithm plus a lower-order term. It remains to evaluate the empirical performance of the algorithm to identify for which applications the additional cost in the excess risk is worth it to achieve risk monotonicity.

Some important questions remain open along the axes of assumptions. In particular, can we remove the boundedness condition on the loss while retaining risk-monotonicity? It might be possible to achieve this for unbounded convex losses using the non-exponential weighted aggregation techniques recently suggested by alquier2020non . Lifting the boundedness assumption may be key in resolving another COLT open problem (grunwald2011bounds, ) regarding achievable risk rates of log-loss Bayesian predictors. Our results build foundations for these avenues, which are promising subjects for future work.

Finally, it would be interesting to explore what other concentration inequalities for non-i.i.d. processes can be derived using other parameter-free online learning algorithms. An obvious starting point is to look at Matrix-FreeGrad MhammediK20 .

Acknowledgments and Disclosure of Funding

We would like to thank Hisham Husain for instrumental discussions during the early phases of the project. We thank Olivier Bousquet and his collaborators for pointing out a mistake in the original proof of Theorem 11. We also thank anonymous reviewers for their valuable feedback. This work was supported by the Australian Research Council and Data61.

References

- (1) Amir Ahmadi-Javid. Entropic value-at-risk: A new coherent risk measure. Journal of Optimization Theory and Applications, 155(3):1105–1123, 2012.

- (2) Pierre Alquier. Non-exponentially weighted aggregation: regret bounds for unbounded loss functions. arXiv preprint arXiv:2009.03017, 2020.

- (3) Jean-Yves Audibert. PAC-Bayesian statistical learning theory. These de doctorat de l’Université Paris, 6:29, 2004.

- (4) Peter L. Bartlett, Michael I. Jordan, and Jon D. McAuliffe. Convexity, classification, and risk bounds. Journal of the American Statistical Association, 101(473):138–156, 2006.

- (5) Peter L. Bartlett and Shahar Mendelson. Empirical minimization. Probability Theory and Related Fields, 135(3):311–334, 2006.

- (6) Mikhail Belkin, Daniel Hsu, Siyuan Ma, and Soumik Mandal. Reconciling modern machine learning and the bias-variance trade-off. arXiv preprint arXiv:1812.11118, 2018.

- (7) Mikhail Belkin, Daniel Hsu, and Ji Xu. Two models of double descent for weak features. arXiv preprint arXiv:1903.07571, 2019.

- (8) Shai Ben-David, David Loker, Nathan Srebro, and Karthik Sridharan. Minimizing the misclassification error rate using a surrogate convex loss. In Proceedings of the 29th International Coference on International Conference on Machine Learning, pages 83–90, 2012.

- (9) Shai Ben-David, Nathan Srebro, and Ruth Urner. Universal learning vs. no free lunch results. In Philosophy and Machine Learning Workshop NIPS, 2011.

- (10) Nicolo Cesa-Bianchi and Gábor Lugosi. Prediction, learning, and games. Cambridge university press, 2006.

- (11) Prasad Cheema and Mahito Sugiyama. A geometric look at double descent risk: Volumes, singularities, and distinguishabilities. arXiv preprint arXiv:2006.04366, 2020.

- (12) Lin Chen, Yifei Min, Mikhail Belkin, and Amin Karbasi. Multiple descent: Design your own generalization curve. arXiv preprint arXiv:2008.01036, 2020.

- (13) DA Darling and Herbert Robbins. Iterated logarithm inequalities. Proceedings of the National Academy of Sciences of the United States of America, 57(5):1188, 1967.

- (14) Stéphane d’Ascoli, Levent Sagun, and Giulio Biroli. Triple descent and the two kinds of overfitting: Where & why do they appear? arXiv preprint arXiv:2006.03509, 2020.

- (15) Zeyu Deng, Abla Kammoun, and Christos Thrampoulidis. A model of double descent for high-dimensional binary linear classification. arXiv preprint arXiv:1911.05822, 2019.

- (16) Michal Derezinski, Feynman T Liang, and Michael W Mahoney. Exact expressions for double descent and implicit regularization via surrogate random design. Advances in Neural Information Processing Systems, 33, 2020.

- (17) Michał Dereziński, Feynman Liang, and Michael W. Mahoney. Exact expressions for double descent and implicit regularization via surrogate random design, 2019.

- (18) Robert P.W. Duin. Small sample size generalization. In Proceedings of the Scandinavian Conference on Image Analysis, volume 2, pages 957–964, 1995.

- (19) Robert P.W. Duin. Classifiers in almost empty spaces. In Proceedings 15th International Conference on Pattern Recognition. ICPR-2000, volume 2, pages 1–7. IEEE, 2000.

- (20) Robert P.W. Duin. Learning to generalize. Frontiers of Life, 3(part 2):763–775, 2001.

- (21) Tim Van Erven, Nishant A. Mehta, Mark D. Reid, and Robert C. Williamson. Fast rates in statistical and online learning. Journal of Machine Learning Research, 16:1793–1861, 2015.

- (22) Dylan J. Foster, Alexander Rakhlin, and Karthik Sridharan. Online learning: Sufficient statistics and the Burkholder method. In Conference On Learning Theory, COLT 2018, Stockholm, Sweden, 6-9 July 2018., pages 3028–3064, 2018.

- (23) David A Freedman. On tail probabilities for martingales. the Annals of Probability, pages 100–118, 1975.

- (24) Peter D Grünwald and Wojciech Kotłowski. Bounds on individual risk for log-loss predictors. In Proceedings of the 24th Annual Conference on Learning Theory, pages 813–816, 2011.

- (25) Benjamin Guedj. A primer on pac-bayesian learning. arXiv preprint arXiv:1901.05353, 2019.

- (26) Steven R Howard, Aaditya Ramdas, Jon McAuliffe, and Jasjeet Sekhon. Time-uniform, nonparametric, nonasymptotic confidence sequences. The Annals of Statistics, 49(2):1055–1080, 2021.

- (27) Steven R Howard, Aaditya Ramdas, Jon McAuliffe, Jasjeet Sekhon, et al. Time-uniform chernoff bounds via nonnegative supermartingales. Probability Surveys, 17:257–317, 2020.

- (28) Kwang-Sung Jun and Francesco Orabona. Parameter-free online convex optimization with sub-exponential noise. In Conference on Learning Theory, pages 1802–1823, 2019.

- (29) Wouter M. Koolen, Peter D. Grünwald, and Tim Van Erven. Combining adversarial guarantees and stochastic fast rates in online learning. In Advances in Neural Information Processing Systems, pages 4457–4465, 2016.

- (30) Nicole Krämer. On the peaking phenomenon of the lasso in model selection. arXiv preprint arXiv:0904.4416, 2009.

- (31) Marco Loog. Contrastive pessimistic likelihood estimation for semi-supervised classification. IEEE transactions on pattern analysis and machine intelligence, 38(3):462–475, 2015.

- (32) Marco Loog and Robert P.W. Duin. The dipping phenomenon. In Joint IAPR International Workshops on Statistical Techniques in Pattern Recognition (SPR) and Structural and Syntactic Pattern Recognition (SSPR), pages 310–317. Springer, 2012.

- (33) Marco Loog, Tom Viering, and Alexander Mey. Minimizers of the empirical risk and risk monotonicity. In Advances in Neural Information Processing Systems, pages 7476–7485, 2019.

- (34) Marco Loog, Tom Viering, Alexander Mey, Jesse H. Krijthe, and David M. J. Tax. A brief prehistory of double descent. Proceedings of the National Academy of Sciences, 117(20):10625–10626, 2020.

- (35) Andreas Maurer and Massimiliano Pontil. Empirical bernstein bounds and sample variance penalization. arXiv preprint arXiv:0907.3740, 2009.

- (36) Andreas Maurer and Massimiliano Pontil. Empirical bernstein bounds and sample-variance penalization. In COLT 2009 - The 22nd Conference on Learning Theory, Montreal, Quebec, Canada, June 18-21, 2009, 2009.

- (37) Song Mei and Andrea Montanari. The generalization error of random features regression: Precise asymptotics and double descent curve. arXiv preprint arXiv:1908.05355, 2019.

- (38) Zakaria Mhammedi, Peter Grünwald, and Benjamin Guedj. Pac-bayes un-expected bernstein inequality. In Advances in Neural Information Processing Systems, pages 12202–12213, 2019.

- (39) Zakaria Mhammedi and Wouter M. Koolen. Lipschitz and comparator-norm adaptivity in online learning. In Conference on Learning Theory, COLT 2020, 9-12 July 2020, Virtual Event [Graz, Austria], volume 125 of Proceedings of Machine Learning Research, pages 2858–2887. PMLR, 2020.

- (40) Preetum Nakkiran. More data can hurt for linear regression: Sample-wise double descent. arXiv preprint arXiv:1912.07242, 2019.

- (41) Preetum Nakkiran, Gal Kaplun, Yamini Bansal, Tristan Yang, Boaz Barak, and Ilya Sutskever. Deep double descent: Where bigger models and more data hurt. In International Conference on Learning Representations, 2020.

- (42) Preetum Nakkiran, Prayaag Venkat, Sham Kakade, and Tengyu Ma. Optimal regularization can mitigate double descent. arXiv preprint arXiv:2003.01897, 2020.

- (43) Manfred Opper and Wolfgang Kinzel. Statistical mechanics of generalization. In Models of neural networks III, pages 151–209. Springer, 1996.

- (44) V.H. Peña, T.L. Lai, and Q.M. Shao. Self-Normalized Processes: Limit Theory and Statistical Applications. Probability and Its Applications. Springer Berlin Heidelberg, 2008.

- (45) Alexander Rakhlin and Karthik Sridharan. On equivalence of martingale tail bounds and deterministic regret inequalities. In Conference on Learning Theory, pages 1704–1722. PMLR, 2017.

- (46) Omar Rivasplata, Ilja Kuzborskij, Csaba Szepesvári, and John Shawe-Taylor. Pac-bayes analysis beyond the usual bounds. In NeurIPS, 2020.

- (47) Shai Shalev-Shwartz and Shai Ben-David. Understanding machine learning: From theory to algorithms. Cambridge university press, 2014.

- (48) Alexander J. Smola, Peter J. Bartlett, Dale Schuurmans, and Bernhard Schölkopf. Advances in large margin classifiers. MIT press, 2000.

- (49) Stefano Spigler, Mario Geiger, Stéphane d’Ascoli, Levent Sagun, Giulio Biroli, and Matthieu Wyart. A jamming transition from under-to over-parametrization affects loss landscape and generalization. arXiv preprint arXiv:1810.09665, 2018.

- (50) Ilya O. Tolstikhin and Yevgeny Seldin. Pac-bayes-empirical-bernstein inequality. In Advances in Neural Information Processing Systems 26: 27th Annual Conference on Neural Information Processing Systems 2013. Proceedings of a meeting held December 5-8, 2013, Lake Tahoe, Nevada, United States, pages 109–117, 2013.

- (51) Paul Viallard, Pascal Germain, Amaury Habrard, and Emilie Morvant. A general framework for the disintegration of pac-bayesian bounds, 2021.

- (52) Tom Viering and Marco Loog. The shape of learning curves: a review. arXiv preprint arXiv:2103.10948, 2021.

- (53) Tom Viering, Alexander Mey, and Marco Loog. Open problem: Monotonicity of learning. In Conference on Learning Theory, pages 3198–3201, 2019.

- (54) Tom J. Viering, Alexander Mey, and Marco Loog. Making learners (more) monotone, 2019.

- (55) Wenda Zhou, Victor Veitch, Morgane Austern, Ryan P. Adams, and Peter Orbanz. Non-vacuous generalization bounds at the imagenet scale: a pac-bayesian compression approach. In 7th International Conference on Learning Representations, ICLR 2019, New Orleans, LA, USA, May 6-9, 2019, 2019.

Appendix A Technical Results

In this section, it will be convenient to adopt the ESI notation [29]:

Definition 12 (Exponential Stochastic Inequality (ESI) notation).

Let be a probability space. Further, let , be any two random variables and be a sub--algebra of . For , we define

For , we simply write instead of . In what follows, given random variables and loss satisfying Assumption 1, we denote by

the excess-loss random variable, where (with as in Assumption 1). Let

| (13) |

be the (conditional) normalized cumulant generating function of . We note that since the loss takes values in the interval , we have

We now present some existing results pertaining to the excess-loss random variable and its normalized cumulant generating function, which will be useful in our proofs:

Lemma 13 ([29]).

Let and . Further, let , and be as above. Then, for all ,

and is the -algebra generated by .

Lemma 14 ([29]).

Lemma 16 ([10]).

For and , the excess-loss random variable satisfies

where is the -algebra generated by and .

The following useful proposition is imported from [38] with minor modifications:

Proposition 17.

[ESI Transitivity] Let be a probability space and be a sub--algebra of . Further, let be random variables such that for , , for all . Then

To prove our time-uniform concentration inequality in Section 3, we will require the following generalization of Markov’s inequality (we state the version found in [27]):

Lemma 18 (Ville’s inequality).

If is a non-negative supermartingale, then for any ,

The upcoming lemmas will help us bound the sequence of gaps in (9) under the Bernstein condition.

Lemma 19.

Let , and , and suppose that the -Bernstein condition holds. Then, under Assumption 1, for any and , with probability at least ,

| (14) |

for all , where and .

Proof of Lemma 19.

Let and define . We recall that is the -algebra generated by , and . Note that under Assumption 1, , for all and . For any and our strategy is to show that, under the -Bernstein condition,

| (15) |

is a non-negative supermartingale, for all . After that, invoking Ville’s inequality (Lemma 18) and applying a change of measure argument (Lemma 21), we get the desired result.

Under the -Bernstein condition, Lemmas 13-15 imply, for all and ,

| (16) |

where we used the fact that , for all ( is involved in Lemma 13). Now, due to the Bernstein inequality (Lemma 16), we have for all and ,

| (17) |

The last inequality follows by the fact that , for (in our case, we set to get to (17)). By chaining (16) with (17) using Proposition 17, we get:

| (18) |

This implies that in (15) is a non-negative supermartingale. This in turn implies that for any distribution , is also a supermartingale. Thus, by Ville’s inequality (Lemma 18), we have, for any ,

| (19) |

On the other hand, by the -change of measure lemma (Lemma 21), we have for all

Combining this with (19), we get the desired result. ∎

Lemma 20.

For , we have

| (20) |

Proof.

We need one more classical change of measure result (see e.g. [1]):

Lemma 21 (-change of measure).

For all distributions and such that , it holds that

Appendix B Proofs of the New Concentration Inequalities

To prove our first concentration inequality for MDS in Proposition 5, we start by constructing a non-negative supermartingale with the help of the recent FreeGrad algorithm [39]. As mentioned in the introduction, our proof technique is similar to the one introduced in [28] with the difference that we use the specific shape of FreeGrad’s potential function to build our supermartingale. Using the latter leads to a desirable empirical variance term in our final concentration bound.

To express the FreeGrad supermartingale, we define

| (23) |

Proposition 22.

Let and be a filtration. For any random variables s.t. is -measurable and , for all , the process , where and is a non-negative supermartingale w.r.t. ; that is,

As mentioned above, the proof of the proposition is based on the guarantee of the parameter-free online learning algorithm FreeGrad. The algorithm operates in rounds, where at each round , FreeGrad outputs (that is a deterministic function of the past) in some convex set , say , then observes a vector , typically the sub-gradient of a loss function at round . The algorithm guarantees a regret bound of the form , for all , where . What is more, FreeGrad’s outputs ensure the following (see [39, Theorem 5]):

| (24) |

where and . In the proof of Proposition 22, we will reason about the outputs of FreeGrad in one dimension (i.e. ) in response to the inputs .

One way to prove Proposition 22 is to show that FreeGrad is a betting algorithm that bets fractions smaller than one of its current wealth at each round. In this case, Proposition 22 would follow from existing results due to, for example, [28]. However, for the sake of simplicity, we decided to present a proof that does not explicitly refer to bets.

Proof of Proposition 22.

By [39, Theorem 5 and proof of Theorem 20], FreeGrad’s outputs in response to and parameter (playing the role of in their Theorem 20) guarantee777Technically, FreeGrad also requires a sequence of hints that provides upper bounds on . Since , these hints can all be set to .,

Re-arranging this inequality and taking the expectation yields

where the penultimate equality follows by the fact that is a deterministic function of the history up to round , and so it is -measurable. Finally, the last equality follows by the assumption that . ∎

Next, using standard tools from PAC-Bayesian analyses, we extend the result of Proposition 22 by allowing the random variables to depend on . We will also “mix” over the free parameter to obtain the optimal (doubly-logarithmic) dependence in in our final concentration bounds.

Proposition 23.

Let be a filtration and be a family of random variables in s.t. is -measurable and , for all and . Further, let and be prior distributions on and , respectively. Then, for any , we have

where and .

Proof of Proposition 23.

By the KL-change of measure lemma (Lemma 21), we have

| (25) |

for all and . On the other hand, by Proposition 22, we know that the process is a supermartingale for any . This in turn implies that is also a non-negative supermartingale, since a mixture of supermartingales is also a supermartingale. Now, by Ville’s inequality (Lemma 18), we have, for all ,

By combining this inequality with (25), we obtain the desired result. ∎

We now use Proposition 23 to prove Proposition 5 (some of the steps in the next proof are similar to ones found in [28]):

Proof of Proposition 5.

Let and . We will apply Proposition 23 with a specific choice of prior . In particular, we let be a prior on , such that for ,

where is as in (4). For and , let be such that

| (26) |

Note that is guaranteed to exist and (26) implies that . Let . With our choice of , we have, for all ,

| (27) | ||||

| (28) | ||||

| (29) |

where in (27) we used (26) and in (28) we used the fact that . Now, by an application of Jensen’s inequality, we get from (29) that

Thus, we have only if

Combining this fact with Proposition 23 implies the desired result. ∎

Proof of Theorem 6.

We will apply Proposition 5 with , where the last equality follows by Assumption 1. As before, we let and . By the classical bias-variance decomposition, we have

| (30) |

where is as in the theorem’s statement. Thus,

| (31) | |||

| holds only if, | |||

| (32) | |||

where we used the bias-variance decomposition in (30) together with the facts that (Jensen’s inequality) and that the function is increasing on for all . On the other hand, (32) is true for , only if,

| (33) |

Thus, (31) holds only if (33) is true, and so we obtain the desired result by Proposition 5. ∎

Appendix C Proofs of Monotonicity and Excess Risk Rates

To simplify notation in this section, we define

We start by presenting a sequence of intermediate results needed in the proofs of Theorems 8 and 9.

C.1 Intermediate Results

We now present a bound on the risk difference , for any , using our new time-uniform empirical Bernstein inequality in Theorem 6. For , and , we recall the definitions

| (34) |

where are the outputs of Algorithm 1 and is as in Proposition 5.

Lemma 24.

Proof of Lemma 24.

The proof follows by our new time-uniform concentration inequality in Theorem 6 with the function defined by

Theorem 6 implies that, for any , with probability at least ,

| (36) |

for all and , where and is given by:

Plugging this into (36) and multiplying the resulting inequality by 2, leads to the desired inequality. ∎

Lemma 24 leads to the following corollary that will be useful for our excess risk rates:

Corollary 25.

Proof of Corollary 25.

The next lemma provides a way of bounding the square-root term in the previous corollary under the Bernstein condition (Definition 3):

Lemma 26.

Proof of Lemma 26.

Applying the fact that , for all , to the LHS of (37) with

which leads to, for all , and ,

| (38) |

Now, let By combining (38) and Lemma 19, we get, for any and , with probability at least ,

| (39) |

Now, minimizing the RHS of (39) over and invoking Lemma 20, we get, for any , with probability at least ,

| (40) |

Combining (40) with the fact that is bounded in , we get the desired result. ∎

We now move on to the proofs of the main results of Section 4.

C.2 Proofs of Theorems 8 and 9

Let and be as in (9) and (34), respectively. Further, it will be useful to define the event

| (41) |

where and are as in Algorithm 1 with the choice of in (9). Observe that by Lemma 24, we have , under Assumptions 1 and 2. We begin by the proof of risk-monotonicity:

Proof of Theorem 8.

Proof of Theorem 9.

Let and be as in Algorithm 1 with the choice of in (9). Further, we let be as in (9) and

| (44) |

It will be convenient to also consider the events:

where and are as in Lemma 26. We note that by Corollary 25 and Lemma 26, we have

| (45) |

For the rest of this proof, we will assume the event holds, and let throughout. We consider two cases pertaining to the condition in Line 6 of Algorithm 1.

Case 1.

Case 2.

Now suppose the condition in Line 6 does not hold for . This means that , and so

| (47) |

where the last inequality follows by the fact that , for all under Assumption 2. Thus, by the assumption that is true, we have,

| ( is true) | |||||

| (by (47)) | |||||

| (48) | |||||

where to obtain the last inequality, we used the fact that and for all . Now, by (48), the fact that holds, and Assumption 2 (which implies that for ), we have

| which, after re-arranging, becomes | |||

| (49) | |||

Multiplying on both sides by 2 and using (45) with a union bound leads to the desired result. ∎

C.3 Additional Results and Proofs

Using the lemmas in Section C.1, we derive the excess-risk rate of ERM under the Bernstein condition:

Lemma 27.

Proof of Lemma 27.

Let be as in (34) and define

Further, consider the events

where is as in Lemma 26. By Corollary 25 and Lemma 26, instantiated with equal to the uniform prior over and [resp. ] equal to the Dirac at [resp. ], we have

| (51) |

For the rest of this proof, we will assume that the event holds, and let . By the assumption that holds, we have

| ( is the ERM) | |||||

| (52) | |||||

Now by the assumption that holds, we can bound the middle term on the RHS of (52), leading to

| (53) |

for all , where in the last inequality we used the definition of . Combining (53) with (51), and applying a union bound, we obtain the desired result. ∎

Proof of Theorem 11.

First, note that by linearity of the expectation it suffices to show that

where the expectation is over the randomness of the samples . Moving forward, we let , and for , define the event

| (54) |

where and as in Algorithm 1 with the choice of in the theorem’s statement. Observe that by Lemma 24, we have for all , under Assumptions 1 and 2.

Now, by the law of the total expectation, we have

where the last inequality follows by the fact that the loss takes values in and that . By applying the law of the total expectation again, we obtain

| (55) |

where the last inequality follows by the fact that if , then . Now, if , then by Line 6 of Algorithm 1, we have

| (56) |

Under the event , we have

This, in combination with (56), implies that under the event ,

As a result, we have

| (57) |

Appendix D Risk Monotonicity without PAC-Bayes

In this section, we show how risk monotonicity can be achieved in the i.i.d. setting without Assumption 2. For this, we will use a concentration inequality due to [35] that has an empirical variance term under the square root just like ours in Theorem 6. To present this inequality, we first present some new notation. For any , we let . Further, for any subset and , we let be the cardinality of smallest subset such that is contained in the union of -balls of radii centered at points in . Finally, we consider the following complexity measure:

| (58) |

With this, we state the concentration inequality due to [35] that we will need:

Theorem 28.

Let be a random variable with values in a set with distribution , and let be a set of hypotheses. Further, let , , and set

Then, with probability at least in the random vector , we have

where .

Using Theorem 28 and following the same steps in the proof of Theorem 11, it follows that Algorithm 2 is risk monotonic in expectation (up to an additive term) for all sample sizes. Furthermore, since the concentration inequality in Theorem 28 has an empirical variance term under the square-root (just like ours in Theorem 6), the risk decomposition in our Theorem 9 also holds for Algorithm 2, albeit with probability at least for sample size .