Simultaneous inference for time-varying models

Abstract

A general class of non-stationary time series is considered in this paper. We estimate the time-varying coefficients by using local linear M-estimation. For these estimators, weak Bahadur representations are obtained and are used to construct simultaneous confidence bands. For practical implementation, we propose a bootstrap based method to circumvent the slow logarithmic convergence of the theoretical simultaneous bands. Our results substantially generalize and unify the treatments for several time-varying regression and auto-regression models. The performance for tvARCH and tvGARCH models is studied in simulations and a few real-life applications of our study are presented through the analysis of some popular financial datasets.

keywords:

arXiv:0000.0000 \startlocaldefs \endlocaldefs

, and

1 Introduction

Time-varying dynamical systems have been studied extensively in the literature of statistics, economics and related fields. For stochastic processes observed over a long time horizon, stationarity is often an over-simplified assumption that ignores systematic deviations of parameters from constancy. For example, in the context of financial datasets, empirical evidence shows that external factors such as war, terrorist attacks, economic crisis, some political event etc. introduce such parameter inconstancy. As Bai [3] points out, ‘failure to take into account parameter changes, given their presence, may lead to incorrect policy implications and predictions’. Thus functional estimation of unknown parameter curves using time-varying models has become an important research topic recently. In this paper, we propose a general setting for simultaneous inference of local linear M-estimators in semi-parametric time-varying models. Our formulation is general enough to allow unifying time-varying models from the usual linear regression, generalized regression and several auto-regression type models together. Before discussing our new contributions in this paper, we provide a brief overview of some previous works in these areas.

In the regression context, time-varying models are discussed over the past two decades to describe non-constant relationships between the response and the predictors; see, for instance, Fan and Zhang [17], Fan and Zhang [18], Hoover et al. [24], Huang, Wu and Zhou [25], Lin and Ying [35], Ramsay and Silverman [42], Zhang, Lee and Song [54] among others. Consider the following two regression models

where () are the covariates, is the transpose, and are the regression coefficients. Here, is a constant parameter and is a smooth function. Estimation of has been considered by Hoover et al. [24], Cai [8]) and Zhou and Wu [59] among others. Hypothesis testing is widely used to choose between model I and model II, see, for instance, Zhang and Wu [55], Zhang and Wu [56], Chow [10], Brown, Durbin and Evans [6], Nabeya and Tanaka [38], Leybourne and McCabe [32], Nyblom [39], Ploberger, Krämer and Kontrus [41], Andrews [2] and Lin and Teräsvirta [33]. Zhou and Wu [59] discussed obtaining simultaneous confidence bands (SCB) in model I, i.e. with additive errors. However their treatment is heavily based on the closed-form solution and it does not extend to processes defined by a more general recursion. Little has been known for time-varying models in this direction previously.

The results from time-varying linear regression can be naturally extended to time-varying AR, MA or ARMA processes. However, such an extension is not obvious for conditional heteroscedastic (CH) models. These are difficult to estimate but also often more useful in analyzing and predicting financial datasets. Since Engle [15] introduced the classical ARCH model and Bollerslev [5] extended it to a more general GARCH model, these have remained primary tools for analyzing and forecasting certain trends for stock market datasets. As the market is vulnerable to frequent changes, non-uniformity across time is a natural phenomenon. The necessity of extending these classical models to a set-up where the parameters can change across time has been pointed out in several references; for example Stărică and Granger [47], Engle and Rangel [16] and Fryzlewicz, Sapatinas and Subba Rao [20]. Towards time-varying parameter models in the CH setting, numerous works discussed the CUSUM-type procedure, for instance, Kim, Cho and Lee [29] for testing for changes in the parameters of a GARCH(1,1) time series. Kulperger et al. [31] studied the high moment partial sum process based on residuals and applied it to residual CUSUM tests in GARCH models. Interested readers can find some more change–point detection results in the context of CH models in James Chu [26], Chen and Gupta [9], Lin et al. [34], Kokoszka et al. [30] or Andreou and Ghysels [1].

Historically in the analysis of financial datasets, the common practice to account for the time-varying nature of the parameter curves was to transfer a stationary tool/method in some ad hoc way. For example, in Mikosch and Stărică [37], the authors analyzed S&P500 data from 1953-1990 and suggested that time-varying parameters are more suitable due to such a long time-horizon. They re-estimated the parameters for every block of 100 sample points and to account for the abrupt fluctuation of the coefficients, they generated re-estimates of parameters for samples of size This treatment suffers from different degree of reliability of the estimators at different parts of the time horizon. There are examples outside the analysis of economic datasets, where similar approach of splitting the time-horizon has been adapted to fit CH type models. For example, in Giacometti et al. [22], the authors analyzed Italian mortality rates from 1960-2003 using an AR(1)-ARCH(1) model and observed abrupt behavior of yearwise coefficients. Our framework can simultaneously capture these models and provide significant improvements over such heuristic treatments.

A time-varying framework and a pointwise curve estimation using M-estimators for locally stationary ARCH models was provided by Dahlhaus and Subba Rao [14]. Since then, while several pointwise approaches were discussed in the tvARMA and tvARCH case (cf. Dahlhaus and Polonik [12], Dahlhaus and Subba Rao [14], Fryzlewicz, Sapatinas and Subba Rao [20]), pointwise theoretical results for estimation in tvGARCH processes were discussed in Rohan and Ramanathan [45] and Rohan [44] for GARCH(1,1) and GARCH(,) models. Even though the conditional heteroscedastic model remained widely popular in analyzing many different types of econometric data, the topic of simultaneous inference in this field remains relatively untouched. Consider the simple tvARCH(1) model

Typically, it is considered that for large number of realizations, the corresponding parameters vary smoothly over time and can be modeled as smooth functions . Pointwise confidence bands for these functions do not help to infer about their overall pattern (like testing for constancy or some specific parametric form). While one remedy could be to subjectively assume a certain class of functions for such as linear or polynomial and perform a hypothesis test, this can be problematic for many real life datasets. See for example the intercept function for the USGBP analysis in Section 5. We rather take an objective approach where we do not assume any parametric form as such and wish to establish valid simultaneous inference. In this paper, we therefore derive simultaneous confidence bands which cover over the whole time interval with a given confidence. After construction, one can perform many hypothesis tests such as time-constancy, linearity etc. in one go. To the best of our knowledge, no theoretical results for simultaneous confidence intervals for nonstationary time series were derived before this work.

We next summarize our contributions in this paper. We use Bahadur representations, a Gaussian approximation theorem from Zhou and Wu [58] and extreme value theory for Gaussian processes to obtain simultaneous confidence bands for contrasts of parameter curves in very general time-varying models. These intervals provide a generalization from testing parameter constancy to testing any particular parametric form such as linear, quadratic, exponential etc. To deal with bias expansions, we use a theory for locally stationary processes which was recently formalized in Dahlhaus, Richter and Wu [13].

Moving on to some practical applicability of our results, we show how our result applies to time-varying ARCH and GARCH models. For tv(G)ARCH models, we improve the existing conditions in [21] (we only need that the innovation process has moments for some compared to 8 moments needed therein) for constructing confidence intervals and provide simultaneous instead of pointwise confidence intervals. We provide an empirical justification of how the coverage can be significantly improved by a wild bootstrap technique and use Gaussian approximation theory to theoretically establish it. Finally we also provide some data analysis and volatility forecasting. First we show for numerous real-life datasets that the time-varying fit does better than the time-constant ones in short-range forecasts. This underlines the importance to decide whether a constant or a time-varying model should be used. One interesting find from our analysis is that simultaneous inference can lead to models where a subset is time-varying and these semi-time varying model can sometimes achieve both statistical confidence and better forecasting ability.

The rest of the article is organized as follows. In Section 2, we state two specific classes of time series models and the related assumptions. For the sake of better focus and readability, we decided to narrow down the scope of the paper to these specific models. However our theoretical results of M-estimation and the SCBs allow to treat much more general models. The more general assumptions are given in the Appendix (cf. Assumption A.1 therein). In Section 3 we provide our main results, namely a Bahadur representation of the estimators of the parameter functions and a SCB result for the related contrasts. Section 4 is dedicated to practical issues which arise when using the SCBs, like estimation of the dispersion matrix of the estimator, bandwidth selection and a wild Bootstrap procedure to overcome the slow logarithmic convergence from the theoretical SCB. Some summarized simulation studies and real data applications can be found in Section 5. The proofs of the main results are deferred to Appendix, while the proof of several more elementary lemmata and a more general assumption set for tvGARCH processes can be found in the Supplementary material.

2 Model assumptions and estimators

2.1 The model

Suppose that , is a sequence of i.i.d. random variables. We consider the following two time series models. In both cases, denotes a parameter space specified below in Section 2.3.

-

•

Case 1: Recursively defined time series. Suppose that for ,

(2.1) where and

with some functions , . Put .

This model covers, for instance, tvARMA and tvARCH models.

-

•

Case 2: tvGARCH. For , consider the recursion

where . Put .

Case 1 does not directly cover the tvGARCH model, we therefore operate with it separately as Case 2 throughout the paper. In either case, our goal is to estimate from the observations , .

2.2 The estimator

In this paper, we focus on local M-estimation: Let , where is the family of non-negative symmetric kernels with support which are continuously differentiable on such that . We consider as objective function the negative conditional Gaussian likelihood. This reads

-

•

in Case 1:

-

•

in Case 2:

where here, is recursively defined via and .

For some bandwidth , define the local linear likelihood function

| (2.2) |

where . Let with some . A local linear estimator of , is given by

| (2.3) |

Remark 2.1.

As defined above, we consider a quite specific form of the objective function . In the Appendix, we allow to be much more general. Basically, it has to be twice continuously differentiable and ’compatible’ with the time series model. A referee asked if also the differentiability assumption on might be relaxed. A relaxation might be possible by using sharper and more recent Gaussian approximation results from [28] and empirical process results for dependent data. However, this would significantly increase the complexity on the assumptions on , since its smoothness is used for several completely different key steps in the proofs, such as Bahadur representations, a bias expansion and the quantification of the underlying dependence.

2.3 Assumptions

For our main results, we need the following assumptions on our time series models.

Assumption 2.2 (Case 1).

Assume that

-

1.

are i.i.d. with , and for some , . Here, . In the special case , one can choose .

-

2.

For all , the sets

are (separately) linearly independent in .

-

3.

There exist , such that for all :

(2.4) Let be some constant such that for all , . With some , choose such that for all ,

(2.5) -

4.

is compact and for all , lies in the interior of . Each component of is in .

For the tvAR() model (cf. [43], Example 4.1), one may choose , , …, , , , leading to the rather strong condition in (2.5). However, as it can be seen in the proof of Proposition E.6 in the appendix, the condition (2.5) is only needed to guarantee the existence of the process and corresponding moments. By using techniques which are more specific to the model, one can obtain much less strict assumptions such as being a compact subset of

cf. [43], Example 4.1. In the tvARCH case, the above Assumption 2.2 asks for with some .

In the following, we consider Case 2, the tvGARCH model. In this specific model, the moment conditions can be relaxed to . The tvGARCH model was for instance studied in the stationary case in Francq and Zakoïan [19]. More recently, pointwise asymptotic results were obtained in Rohan and Ramanathan [45]. For a matrix , we define as a component-wise application of . For matrices , let denote the Kronecker product and

| (2.6) |

denote the -fold Kronecker product. Let denote the spectral norm of .

Assumption 2.3 (Case 2).

Let and let be the unit column vector with th element being 1, . Define . Let and such that for all ,

| (2.7) |

Suppose that

-

(i)

is compact and for all , lies in the interior of . Each component of is in ,

-

(ii)

are i.i.d. with , and with some .

In the important GARCH(1,1) case, a straightforward calculation shows that the condition (2.7) can be translated to

| (2.8) |

If , it holds that . Bollerslev [5] proved that stationary GARCH(1,1) processes have 4th moments under the exact same condition (2.8). In Section 4, Remark 4.4 therein, we further talk about the applicability of (2.8).

We conjecture that also for general GARCH() models, (2.7) is equivalent to the condition

which would then exactly meet the condition from [5]. Note that estimation and the true curve lie in which is has to be a compact subset of . Therefore, we automatically ask that all parameters of the GARCH process are nonzero. Again, this condition could in principle be relaxed which would add a significant amount of technicalities.

3 Main results

We discuss the theoretical confidence band result in this section. We directly start with a weak Bahadur representation which plays a key role for introducing simultaneity. For , define

We now have to define some quantities which are needed to provide the theoretical results. They correspond to the so-called (miss-specified) Fisher information matrices which occur naturally as variance of the M-estimators. These quantities need not to be known in practice because they are estimated. They depend on the so-called stationary approximation of the considered time-varying process . In case 1 and case 2, this is given as follows: For ,

-

•

is the solution of

-

•

is the solution of

For , let denote the infinite vector containing the stationary approximations. We now define

| (3.1) | |||||

| (3.2) | |||||

| (3.3) |

In our theoretical models, these quantities can be related to each other. The following lemma (a direct implication of Propositions E.6 and E.9 in the appendix) summarizes these forms.

Lemma 3.1.

-

•

Case 1: It holds that .

If additionally (i) , or (ii) or (iii) and , thenwhere denotes the -dimensional identity matrix.

-

•

Case 2: It holds that .

3.1 A weak Bahadur representation for

In the following, we obtain a weak Bahadur representation of which will be used to construct simultaneous confidence bands. The first part of Theorem 3.2 shows that can be approximated by the expression as expected due to a standard Taylor argument. The second part of Theorem 3.2 deals with approximating this term by a weighted sum of -free terms, namely

which is necessary to apply some earlier results from Zhou and Wu [59]. Let . For some vector or matrix , let denote its Euclidean or Frobenius norm, respectively.

3.2 Simultaneous confidence bands for

Based on the weak Bahadur result, we use results from Wu and Zhou [53] to obtain a Gaussian analogue of

for some . For a positive semidefinite matrix with eigendecomposition , where is orthonormal and is a diagonal matrix, define , where is the elementwise root of . Then the following asymptotic statement for simultaneous confidence bands for holds.

Theorem 3.3 (Simultaneous confidence bands for ).

Let be a fixed matrix with rank . Define and , , .

Remark 3.4.

The conditions on are fulfilled for bandwidths , where satisfies

The bandwidths are covered in both cases.

Note that for practical use of the SCB in (3.6), one needs to estimate the bias term, choose a proper bandwidth and estimate . Furthermore, the theoretical SCB only has slow logarithmic convergence, thus one requires huge to achieve the desired coverage probability. To tackle these type of problems, we discuss practical issues in the next Section 4.

4 Implementational issues

In this section, we discuss some issues which arise by implementing the procedure from Theorem 3.3. We focus on estimation of and optimization of the corresponding SCBs.

4.1 Bias correction

There are several possible ways to eliminate the bias term in Theorem 3.3. A natural way is to estimate by using a local quadratic estimation routine with some bandwidth . However the estimation of may be unstable due to the convergence condition which may be hard to realize together with from Theorem 3.3 in practice. Here instead we propose a bias correction via the a jack-knife method inspired from [23]. We define

| (4.1) |

Since the weak Bahadur representation from Theorem 3.2 holds both for and , we obtain

where . Note that the bias term of order is eliminated by construction. This shows that Theorem 3.3 still holds true for with kernel replaced by the fourth-order kernel and with no bias term of order .

4.2 Estimation of the covariance matrix

In this subsection, we discuss the estimation of since this term is generally unknown but arises in the SCB in Theorem 3.3. By Lemma 3.1, one has in both cases that , which shows that

| (4.2) |

As pointed out by a referee, is of the well-known ’sandwich’-form (cf. [bollerslevwooldridge1992]). Even if the distribution of the innovations is misspecified by the likelihood, one can typically simplify the representation (4.2). If the distribution of is correctly specified, one has and thus

| (4.3) |

If the distribution of is misspecified by the likelihood, Lemma 3.1 shows that with some constant matrix which only depends on the fourth moment of . Then one has

| (4.4) |

This also means that the representation (4.3) is stable under misspecification of the innovation distribution as long as one corrects the expression with the factor . To do so, one needs a possibility to estimate from the data. A possibility how to do this for linear processes was discussed in [bootstrap4cumulant].

In summary, the representation (4.2) holds always true, the simpler representations (4.3) and (4.4) can be used under additional assumptions or if stable estimators of are available.

To cover all possible situations above, we discuss both estimation of and . We propose the (boundary-corrected) estimators

| (4.5) | |||||

where . The convergence of these estimators is given in the next Proposition. Note that the following Proposition also holds if in (4.5) and (4.2) is replaced by .

This shows uniform consistency of , if . Note that in (ii), we need more moments to discuss (). In many special cases, this may be relaxed.

4.3 Bandwidth selection

Based on the asymptotic squared error decomposition

which can be read off the weak Bahadur representation (3.6), the squared error global optimal bandwidth choice reads

| (4.7) |

In practice, is not available due to the unknown quantities on the right hand side, in particular . We therefore adapt a model-based cross validation method from Richter and Dahlhaus [43], which was shown to work even if the underlying parameter curve is only Hölder continuous and is uncorrelated. Here, we reformulate this selection procedure for the local linear setting. For , define the leave-one-out local linear likelihood

| (4.8) |

and the corresponding leave-one-out estimator

The bandwidth is chosen via minimizing

| (4.9) |

where is some weight function to exclude boundary effects. A possible choice is with some fixed . Note that it is important to use the modified local linear approach due to the different bias terms. In Richter and Dahlhaus [43], it was shown that the local constant version of this procedure selects asymptotically optimal bandwidths and works even if a model misspecification is present, i.e. if the function leads to estimators which are not consistent. This motivates that a similar behavior should hold for the local constant version.

4.4 Bootstrap method

The SCB for obtained in Theorem 3.3 provides a slow logarithmic rate of convergence to the Gumbel distribution. Thus, even for moderately large values of sample size , it is practically infeasible to use such a theoretical SCB as the coverage will possibly be lower than the specified nominal level. First we show an empirical coverage comparison of how far the theoretical confidence intervals lag behind in achieving their nominal coverage. We use the same simulation setting (cf. Section 5.1) for the tvGARCH case:

where , and , is i.i.d. standard normal distributed. For estimation, we choose to be the Epanechnikov kernel, for several different . From Table 1 one can see that the simultaneous coverage is never even positive for the SCB specified in Theorem 3.3. The individual coverages are very low for small bandwidth and with higher bandwidth they over-compensate. The performance for observations is slightly better, hinting at the logarithmic rate of convergence in Theorem 3.3.

| 2000 | Gumbel | 0.778 | 0.405 | 0.638 | 0 | 0.629 | 0.215 | 0.42 | 0 |

| Bootstrap | 0.944 | 0.822 | 0.924 | 0.869 | 0.967 | 0.89 | 0.961 | 0.92 | |

| Gumbel | 0.954 | 0.891 | 0.94 | 0 | 0.871 | 0.714 | 0.818 | 0 | |

| Bootstrap | 0.941 | 0.843 | 0.923 | 0.864 | 0.967 | 0.908 | 0.945 | 0.913 | |

| 5000 | Gumbel | 0.6 | 0.248 | 0.481 | 0 | 0.481 | 0.126 | 0.298 | 0 |

| Bootstrap | 0.955 | 0.855 | 0.936 | 0.886 | 0.974 | 0.903 | 0.959 | 0.929 | |

| Gumbel | 0.756 | 0.461 | 0.642 | 0 | 0.643 | 0.261 | 0.432 | 0 | |

| Bootstrap | 0.941 | 0.889 | 0.939 | 0.904 | 0.974 | 0.931 | 0.967 | 0.949 | |

| Gumbel | 0.96 | 0.917 | 0.957 | 0 | 0.878 | 0.701 | 0.84 | 0 | |

| Bootstrap | 0.949 | 0.903 | 0.941 | 0.903 | 0.972 | 0.95 | 0.975 | 0.946 | |

We circumvent this convergence issue in this subsection by proposing a wild bootstrap algorithm. Recall the jackknife-based bias corrected estimator from (4.1). Let . We have the following proposition as the key idea behind the bootstrap method.

Proposition 4.2.

Suppose that Assumption 2.2 or Assumption 2.3 holds. Furthermore, assume that with . Then on a richer probability space, there are i.i.d. such that

| (4.10) |

where and

The proof of Proposition 4.2 is immediate from the approximation rates (B.13), (B.14), (B.16) and (B.18) in the appendix which, ignoring the terms, are of the form with

where is arbitrarily large and .

One can interpret (4.10) in the sense that approximates the stochastic variation in uniformly over . Thus it can be used as a margin for the noise to construct confidence bands, provided one can consistently estimate .

4.4.1 Boundary considerations

The results shown above only hold for . For inference of some time series models like ARCH or GARCH, large bandwidths are needed to get sufficiently smooth and stable estimators even for a large number of observations. It seems hard to generalize the SCB result Theorem 3.3 to the whole interval . However it is possible to generalize the bootstrap procedure which may be more important in practice:

Proposition 4.3.

Suppose that the conditions on of Proposition 4.2 hold. Then on a richer probability space, there exist i.i.d. such that

where

| (4.11) |

and , ,

Note that the additional term in (4.11) reduces to for .

To eliminate the bias inside , it is still recommended to use the jack-knife estimator . From Proposition 4.3 we obtain

| (4.12) |

where

| (4.13) |

The additional factor in (4.12) serves as an indicator how near is to the boundary. For , this factor is 1 while for , may be very small, inducing large diameters of the band near the boundary. Note that the bias correction of the jack-knife estimator may be useless in since . However it is necessary from a theoretical point of view to use the same estimator for the whole region to get a uniform band based on the approximation (4.12).

In practice, the result (4.12) can be used as follows: We can create a large number of i.i.d. copies of by creating i.i.d. copies

| (4.14) | |||

where are i.i.d. -distributed random variables, and computing according to (4.13). Quantiles of then can be determined by using the corresponding empirical quantile of the copies . Then one can use (4.12) to construct the confidence band for . For convenience of the readers, we provide a summarized algorithm of the above discussion.

Algorithm for constructing SCBs of :

- •

- •

-

•

Compute , the empirical th quantile of .

-

•

Calculate with the estimators proposed in Subsection 4.2. As mentioned there, can often be simplified.

-

•

The SCB for is , where is the unit ball in .

Remark 4.4.

(Discussion of the tvGARCH parameter restriction) A very valid question was asked by a reviewer about the applicability of the assumption (2.8). We would like to point out that this assumption is necessary under the fourth moment assumption of the GARCH process. Investigating the proof of Proposition E.9 very minutely, it seems that it might be possible to relax the existence of moments for the GARCH process to only moments which could potentially improve the condition (2.8) to

However, the entire bias expansion arguments in the proof of Theorem 3.3 would change based on this relaxed moment assumption and it would require a different notion of local-stationarity that allows more approximating terms. To keep the general theme of the paper, we decided against proving a separate result for just GARCH(1,1). Moreover, from a practical point of view, when we estimate , we use from section 4 which is only consistent under at least 4th moment existence of the GARCH process. We also found that, for some very popular stock market datasets (one such example is given in Section 5) one can reasonably assume that the condition (2.8) is satisfied.

5 Simulation results and applications

This section consists of some summarized simulations and some real data applications related to our theoretical results. Because of the generality of our theoretical framework, it is impossible to report simulation performance even for the most prominent examples in these different classes. Therefore we restrict ourselves to conditional heteroscedasticity (CH) models for simulations and real data applications. For the time-varying simultaneous band, to the best of our knowledge, there is no or little simulation results reported. For the tvAR, tvMA and tvARMA processes we obtained quite satisfactory results, but they are omitted here to keep this discussion concise.

5.1 Simulations

In this section, we study the finite sample coverage probabilities of our SCBs for theoretical coverage and in the following tvARCH(1) and tvGARCH(1,1) models:

-

(a)

, where , ,

-

(b)

, , where , and ,

where is i.i.d. standard normal distributed. For estimation, we choose to be the Epanechnikov kernel, for several different (the optimal bandwidths (4.7) are also reported for model (a) and model (b)). For each situation, replications are performed and it is checked if the obtained SCB based on (4.12) contains the true curves in . In both models we have and therefore estimate via replacing by from (4.2). We obtained the results given in Tables 2 and 3. The estimation, for smaller sample sizes , sometimes may lead to difficulties since the optimization routine (optim in programming language R) may not converge. We decided to discard these pathological cases for simplicity. It can be seen that the empirical coverage probabilities are reasonably close to the nominal level for bandwidths close to the optimal ones and they do not differ too much for other bandwidths as well.

| 500 | 0.45 | 0.859 | 0.839 | 0.833 | 0.948 | 0.912 | 0.900 |

| 0.5 | 0.869 | 0.864 | 0.842 | 0.937 | 0.914 | 0.895 | |

| 0.55 | 0.864 | 0.849 | 0.832 | 0.930 | 0.901 | 0.898 | |

| 1000 | 0.4 | 0.873 | 0.846 | 0.845 | 0.937 | 0.906 | 0.900 |

| 0.45 | 0.885 | 0.875 | 0.879 | 0.941 | 0.925 | 0.927 | |

| 0.5 | 0.887 | 0.876 | 0.864 | 0.948 | 0.926 | 0.931 | |

| 0.55 | 0.871 | 0.870 | 0.866 | 0.931 | 0.925 | 0.921 | |

| 2000 | 0.893 | 0.861 | 0.868 | 0.946 | 0.924 | 0.930 | |

| 0.35 | 0.886 | 0.872 | 0.866 | 0.938 | 0.928 | 0.921 | |

| 0.4 | 0.891 | 0.878 | 0.874 | 0.937 | 0.926 | 0.933 | |

| 0.45 | 0.874 | 0.873 | 0.883 | 0.940 | 0.937 | 0.937 | |

| 5000 | 0.25 | 0.885 | 0.883 | 0.882 | 0.941 | 0.931 | 0.936 |

| 0.3 | 0.892 | 0.883 | 0.889 | 0.949 | 0.938 | 0.941 | |

| 0.35 | 0.900 | 0.891 | 0.894 | 0.948 | 0.945 | 0.938 | |

| 0.4 | 0.900 | 0.899 | 0.894 | 0.953 | 0.947 | 0.937 | |

| 0.45 | 0.878 | 0.880 | 0.881 | 0.934 | 0.937 | 0.930 | |

| 500 | 0.943 | 0.778 | 0.902 | 0.793 | 0.962 | 0.851 | 0.939 | 0.854 | |

|---|---|---|---|---|---|---|---|---|---|

| 0.946 | 0.815 | 0.922 | 0.837 | 0.962 | 0.875 | 0.961 | 0.89 | ||

| 0.947 | 0.828 | 0.92 | 0.841 | 0.966 | 0.884 | 0.956 | 0.899 | ||

| 0.939 | 0.849 | 0.922 | 0.853 | 0.962 | 0.897 | 0.957 | 0.903 | ||

| 1000 | 0.943 | 0.857 | 0.936 | 0.864 | 0.974 | 0.913 | 0.966 | 0.914 | |

| 0.947 | 0.869 | 0.926 | 0.891 | 0.97 | 0.929 | 0.954 | 0.937 | ||

| 0.946 | 0.884 | 0.943 | 0.908 | 0.971 | 0.937 | 0.966 | 0.948 | ||

| 0.944 | 0.873 | 0.921 | 0.889 | 0.965 | 0.921 | 0.951 | 0.934 | ||

| 2000 | 0.944 | 0.822 | 0.924 | 0.869 | 0.967 | 0.89 | 0.961 | 0.92 | |

| 0.941 | 0.843 | 0.923 | 0.864 | 0.967 | 0.908 | 0.945 | 0.913 | ||

| 0.958 | 0.846 | 0.92 | 0.894 | 0.972 | 0.91 | 0.96 | 0.943 | ||

| 0.957 | 0.875 | 0.931 | 0.897 | 0.98 | 0.928 | 0.965 | 0.942 | ||

| 0.946 | 0.887 | 0.952 | 0.911 | 0.978 | 0.938 | 0.979 | 0.952 | ||

| 5000 | 0.955 | 0.855 | 0.936 | 0.886 | 0.974 | 0.903 | 0.959 | 0.929 | |

| 0.941 | 0.889 | 0.939 | 0.904 | 0.974 | 0.931 | 0.967 | 0.949 | ||

| 0.949 | 0.903 | 0.941 | 0.903 | 0.972 | 0.95 | 0.975 | 0.946 | ||

| 0.954 | 0.882 | 0.94 | 0.92 | 0.968 | 0.94 | 0.969 | 0.959 | ||

| 0.966 | 0.892 | 0.956 | 0.909 | 0.98 | 0.946 | 0.98 | 0.96 | ||

| 0.948 | 0.886 | 0.932 | 0.896 | 0.976 | 0.937 | 0.976 | 0.957 | ||

5.2 Applications

In this section, we consider a few real-data applications of our procedure. As mentioned in Section 1, there are abundant results in the literature about time-varying regression but the results for time-varying autoregressive conditional heteroscedastic models are scarce. Thus it is important to evaluate the performance of our constructed SCBs for these type of models in both theoretical and real data scenarios. Among the popular heteroscedastic models, usually GARCH type models are most difficult to estimate due to the recursion of the variance term.

We consider two examples from the class of conditional heteroscedastic models with two types of financial datasets: one foreign exchange and one stock market daily pricing dataset. As Fryzlewicz, Sapatinas and Subba Rao [20] found out, ARCH models have good forecasting ability for currency exchange type data whereas for data coming from the stock market, GARCH models are preferred. Typically, these daily closing price datasets show unit root behavior and thus instead of using the daily price data, we model the log-return data. The log-return is defined as follows and is close to the relative return

where is the closing price on the day. Because of the apparent time-varying nature of volatility these log-return data typically show, conditional heteroscedastic models are used for analysis and forecasting.

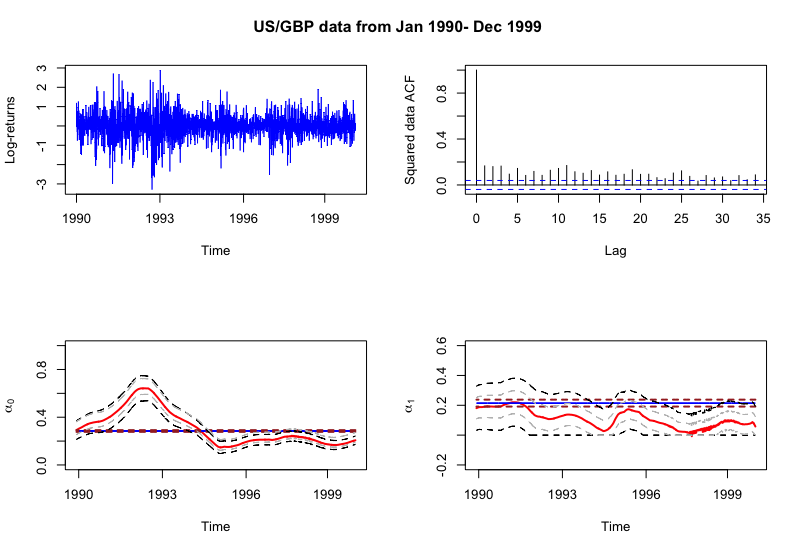

5.2.1 Real data application I: USD/GBP rates

For the first application, we consider a tvARCH() model with . It has the following form

Many different exchange rates from 1990-1999 for USD with other currencies were analyzed in [20] using tvARCH() models with . We collect the data for USD-GBP exchange rates from www.federalreserve.gov/releases/h10/Hist/default1999.htm. The authors suggested choosing for USD-GBP exchange rates and we also decided to restrict ourselves to fitting a tvARCH(1) model only. Note that in principle, our simultaneous bands can be used to decide whether the additional parameter in a tvARCH(2) model is needed or not. The dataset has sample size 2514 and we use a cross-validated bandwidth of . We also provide the plots for the log-returns and an ACF plot of the squared time series that shows the evidence of conditional heteroscedasticity.

Based on Figure 1, time-constancy for the parameter curve is rejected at 5% level of significance. For , the estimate generally stays below the stationary fit. This can be explained by the geometry of the parameter space of the GARCH model, cf. [hillebrand_garch]. Also, one can see from the plot of actual log-returns that there are large shocks from 1990 to 1993 compared to those seen in 1993-1999. This can be explained through the high (low) values shown for the estimated curve for the time-period 1990-1993 (1993-1999).

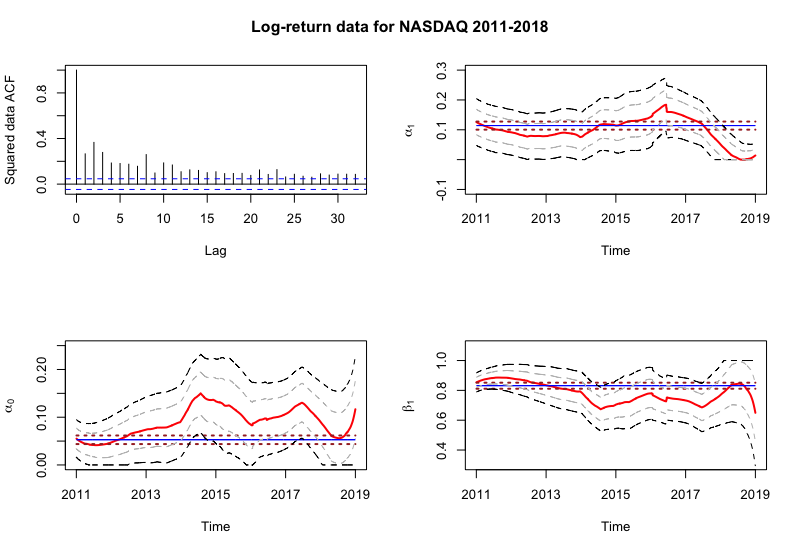

5.2.2 Real data application II: NASDAQ index data

In the empirical analysis of log-returns for stock market data, Palm [40] and others have found that lower order GARCH models account sufficiently for conditional heteroscedasticity. Moreover, GARCH(1,1) and in a very few cases GARCH(1,2) and GARCH(2,1) models are used and higher order GARCH models are typically not necessary. Another advantage of using GARCH(1,1) over ARCH() models is that one does not need to worry about choosing a proper lag as GARCH(1,1) can be thought as an ARCH model with . In this subsection, we implement a time-varying version of GARCH(1,1) and obtain the bootstrapped SCB. A tvGARCH(1,1) model has the following form:

As our second example, we choose to analyze the log returns of NASDAQ from January 2011 to December 2018. This is an important index in the US stock market. We collect this one and all other stock index datasets in later analysis from www.investing.com. Our cross-validated bandwidth is for this dataset of size . Since our simulations show excellent performance for sample sizes around and the estimated parameter functions satisfy the parameter restriction , it is reasonable to say our simultaneous confidence bands would also be valid here. As one can see from Figure 2, the time series shows significant lags in its ACF plot after squaring; indicating conditional heteroscedasticity.

One can see that the estimates for is mostly above the corresponding time-constant fit. As mentioned in the caption is time-varying since the SCB does not contain a horizontal line. The fit fluctuates around the time-constant fit. For , the time-varying fit is below the corresponding time-constant fit. Overall, since is deemed time-varying through this analysis the time-constant hypothesis can be rejected at 5% level of significance.

5.3 Forecasting volatility

It is a legitimate question whether time-varying models in forecasting econometric time-series are more useful compared to their time-constant analogue. Note that the main goal of this paper is not to build better forecasting models. The extension to predictive intervals from confidence intervals for conditional heteroscedastic models is not very straight-forward. Moreover, it is unclear how in-fill asymptotics discussed in this paper would extend to forecasting future trends or estimate time-varying functions with time arguments in the future. Any asymptotic theory would need to consider the rescaling mechanism rigorously, keeping in mind the data observed up to a certain point. In this subsection we show empirically that time-varying models can indeed lead to better forecasts compared to time-constant analogues.

5.3.1 Short-range forecasts

Following [46] and [21], we show for a wide range of econometric datasets that time-varying models can provide better short range forecasts. We also allow multiple windows of forecasting and multiple start points to highlight why most of these datasets call for a time-varying fit. In the following Tables 4 and 5, we use ARCH(1) models for the forex datsets and GARCH(1,1) for the stock market indices. Our POOS (pseudo-out-of-sample) evaluation of forecasting is chalked out as follows:

Define, for a step ahead forecasting scheme, where are the step ahead forecasts of time-constant or time-varying fit at time . We compare this with the ‘realized’ volatility . We then compute the aggregated measure for a start point as following:

For the forecasting horizon values, we choose and start points . Our forecasting method is the same as the one implemented in the fGARCH R-package. For the time-constant fit at time we use the data from 1 to to predict the -step ahead forecast. For the time-varying fit however, it is unclear what the time-varying projection will be. Following [21], we assume the last points to be stationary for a small and use that to obtain the future forecasts. Since is a tuning parameter, we choose the value that produces the minimum over .

| ahead=25 | ahead=50 | ahead=75 | ahead=100 | ahead=150 | ahead=200 | |||||||

| TC | TV | TC | TV | TC | TV | TC | TV | TC | TV | TC | TV | |

| USGBP | 0.101 | 0.07 | 0.085 | 0.057 | 0.078 | 0.053 | 0.075 | 0.052 | 0.07 | 0.048 | 0.067 | 0.046 |

| USCHF | 2.968 | 2.775 | 1.702 | 1.528 | 1.269 | 1.115 | 1.048 | 0.099 | 0.803 | 0.601 | 0.646 | 0.524 |

| USCAD | 0.029 | 0.026 | 0.024 | 0.024 | 0.022 | 0.023 | 0.02 | 0.021 | 0.017 | 0.018 | 0.015 | 0.017 |

| EURGBP | 0.083 | 0.074 | 0.057 | 0.048 | 0.044 | 0.036 | 0.039 | 0.032 | 0.034 | 0.029 | 0.028 | 0.025 |

| EURUSD | 0.052 | 0.033 | 0.044 | 0.028 | 0.041 | 0.027 | 0.042 | 0.028 | 0.038 | 0.032 | 0.036 | 0.038 |

| SP Merval | 7.722 | 7.094 | 6.632 | 4.679 | 5.317 | 4.376 | 5.763 | 4.514 | 5.372 | 4.529 | 5.086 | 4.620 |

| BSE | 3219 | 3038 | 2916 | 1901 | 2313 | 2040 | 2259 | 1321 | 2000 | 1106 | 1897 | 1038 |

| SP500 old | 5.475 | 5.346 | 8.752 | 7.511 | 4.265 | 4.048 | 3.339 | 2.344 | 2.092 | 1.079 | 1.768 | 0.939 |

| SP500 | 0.319 | 0.042 | 0.379 | 0.372 | 0.249 | 0.324 | 0.304 | 0.306 | 0.277 | 0.280 | 0.269 | 0.274 |

| Dow Jones | 0.037 | 0.0365 | 0.316 | 0.277 | 0.223 | 0.231 | 0.215 | 0.200 | 0.185 | 0.183 | 0.169 | 0.176 |

| FTSE | 0.470 | 0.461 | 0.456 | 0.283 | 0.322 | 0.279 | 0.346 | 0.206 | 0.336 | 0.240 | 0.319 | 0.278 |

| NASDAQ | 0.424 | 0.399 | 0.498 | 0.237 | 0.283 | 0.233 | 0.404 | 0.175 | 0.388 | 0.200 | 0.364 | 0.218 |

| Smallcap | 0.448 | 0.292 | 1.035 | 0.189 | 0.398 | 0.157 | 0.981 | 0.143 | 0.979 | 0.144 | 0.970 | 0.143 |

| NYSE | 0.318 | 0.245 | 0.470 | 0.144 | 0.277 | 0.148 | 0.418 | 0.107 | 0.413 | 0.121 | 0.404 | 0.136 |

| DAX | 0.903 | 0.800 | 1.142 | 0.559 | 0.639 | 0.552 | 0.992 | 0.501 | 0.961 | 0.580 | 0.920 | 0.697 |

| Apple | 3.736 | 3.535 | 1.853 | 2.100 | 2.069 | 1.816 | 1.380 | 1.787 | 1.305 | 1.818 | 1.280 | 1.749 |

| Microsoft | 2.729 | 3.388 | 1.600 | 1.999 | 1.156 | 1.898 | 0.981 | 1.335 | 0.766 | 1.084 | 0.664 | 0.973 |

| AXP | 2.350 | 2.13 | 2.142 | 1.500 | 1.456 | 1.264 | 1.726 | 1.065 | 1.759 | 0.984 | 1.625 | 0.928 |

| ahead=25 | ahead=50 | ahead=75 | ahead=100 | ahead=150 | ahead=200 | |||||||

| TC | TV | TC | TV | TC | TV | TC | TV | TC | TV | TC | TV | |

| USGBP | 0.068 | 0.019 | 0.064 | 0.017 | 0.062 | 0.015 | 0.061 | 0.014 | 0.059 | 0.013 | 0.058 | 0.014 |

| USCHF | 4.344 | 4.009 | 1.796 | 1.584 | 1.074 | 0.891 | 0.799 | 0.624 | 0.559 | 0.392 | 0.419 | 0.278 |

| USCAD | 0.029 | 0.028 | 0.024 | 0.027 | 0.022 | 0.024 | 0.019 | 0.023 | 0.017 | 0.021 | 0.015 | 0.020 |

| EURGBP | 0.019 | 0.012 | 0.017 | 0.011 | 0.016 | 0.010 | 0.015 | 0.009 | 0.015 | 0.010 | 0.014 | 0.011 |

| EURUSD | 0.039 | 0.028 | 0.034 | 0.029 | 0.032 | 0.031 | 0.032 | 0.034 | 0.029 | 0.040 | 0.027 | 0.045 |

| SP Merval | 10.39 | 8.714 | 9.432 | 6.12 | 7.666 | 6.029 | 8,522 | 5.883 | 7.908 | 5.857 | 7.052 | 5.739 |

| BSE | 2478 | 2126 | 2798 | 1437 | 1506 | 949 | 2288 | 783 | 2263 | 771 | 2362 | 945.9 |

| SP500 OlD | 8.104 | 7.964 | 12.57 | 11.26 | 6.242 | 5.949 | 4.292 | 3.469 | 2.307 | 1.463 | 1.741 | 1.216 |

| SP500 | 0.371 | 0.503 | 0.328 | 0.276 | 0.259 | 0.236 | 0.231 | 0.196 | 0.183 | 0.166 | 0.155 | 0.152 |

| DowJones | 0.484 | 0.509 | 0.351 | 0.400 | 0.263 | 0.335 | 0.210 | 0.292 | 0.167 | 0.267 | 0.145 | 0.238 |

| FTSE | 0.644 | 0.639 | 0.514 | 0.378 | 0.409 | 0.394 | 0.358 | 0.270 | 0.347 | 0.353 | 0.314 | 0.419 |

| NASDAQ | 0.519 | 0.505 | 0.482 | 0.345 | 0.332 | 0.377 | 0.340 | 0.267 | 0.312 | 0.338 | 0.284 | 0.365 |

| Smallcap | 0.457 | 0.374 | 0.671 | 0.243 | 0.338 | 0.243 | 0.558 | 0.229 | 0.488 | 0.232 | 0.433 | 0.206 |

| NYSE | 0.375 | 0.329 | 0.374 | 0.207 | 0.271 | 0.212 | 0.287 | 0.153 | 0.260 | 0.194 | 0.237 | 0.228 |

| DAX | 1.245 | 1.123 | 1.130 | 0.755 | 0.842 | 0.708 | 0.925 | 0.762 | 0.897 | 0.896 | 0.832 | 1.102 |

| Apple | 2.465 | 2.275 | 1.799 | 1.279 | 1.530 | 1.206 | 1.374 | 0.871 | 1.276 | 1.036 | 1.237 | 1.052 |

| Microsoft | 2.868 | 3.668 | 1.720 | 2.295 | 1.214 | 2.147 | 1.057 | 1.596 | 0.851 | 1.335 | 0.770 | 1.232 |

| AXP | 2.837 | 2.668 | 1.749 | 1.462 | 1.395 | 1.347 | 1.151 | 0.825 | 0.982 | 0.681 | 0.834 | 0.581 |

One can see from Table 4 and 5 how for a wide range of datasets, starting points and forecasting horizons the AMSE of the time-varying forecast is considerably smaller than the one for the time-constant version. We believe, even if prediction and forecasting is more important from an economist’s perspective, this POOS analysis provides a strong motivation to choose a time-varying model over a time-constant one.

5.3.2 One-step ahead forecasting and semi-timevarying models from inference

We use the following one-step ahead , inspired from [45] to validate our models:

.

Here, are the log-returns and refers to the fitted model using ARCH(1) for foreign exchange datasets, and GARCH(1,1) for stock market indices. In each row we exhibit the best model in bold.

| Index (opt ) | Time-varying | Time-constant | Time-constant coefficients | Semi-timevarying model |

|---|---|---|---|---|

| USGBP (0.26) | 0.5701109 | 0.5956046 | 0.5697231 | |

| USCHF (0.24) | 45.42274 | 45.61378 | None | NA |

| USCAD (0.22) | 0.1604907 | 0.1672808 | 0.1616965 | |

| EURGBP (0.34) | 0.778459 | 0.789287 | 0.7837281 | |

| EURUSD (0.23) | 0.3234517 | 0.3399221 | None | NA |

| SP Merval (0.36) | 60.62419 | 62.02226 | 61.58843 | |

| SP500 old (0.29) | 26.48272 | 26.12195 | None | NA |

| SP500 recent (0.22) | 3.54 | 3.527918 | 3.529355 | |

| Wilshire 5k (0.35) | 1.943517 | 1.964926 | 1.972347 | |

| FTSE (0.45) | 3.650331 | 3.687818 | None | NA |

| NASDAQ (0.405) | 5.4258546 | 5.446805 | 5.611163 | |

| Smallcap (0.35) | 12.36647 | 12.56344 | 12.53796 | |

| NYSE (0.24) | 4.830424 | 4.841198 | 5.287622 | |

| DAX (0.44) | 9.908042 | 9.987583 | None | NA |

| Apple (0.27) | 48.06839 | 46.4968 | None | NA |

| Microsoft (0.39) | 38.08752 | 38.33715 | None | NA |

| AXP (0.28) | 37.39755 | 37.90381 | 38.1988 |

Note that the examples exhibited here show that often the time-constant model has poor one-step ahead forecasting quality compared to their time-varying analogue. However, from Table 6, one can see that in some of these time-varying models, we have a subset of parameters not rejecting the hypothesis of time-constancy. We suspect that setting a subset of parameters to be time-constant and allowing the rest to vary over time can improve forecasting over both models. One finding of this analysis is that for some of the datasets such as USGBP, the semi-time-varying model may outperform the time-constant model in terms of forecasting. Note that it is easy to tailor and find time-constant fits that allow for even better forecasts, but those models do not have proper confidence (in terms of closeness to the true model) for the already observed data. For the numbers in the above table on the semi-time-varying column, we kept the time-varying coefficients as they are and searched for the best (in terms of ) constant for the time-constant coefficients among the horizontal lines that fit within the bands entirely. Here we would like also to put a word of caution: Note that the semi-time-varying analysis is somewhat adhoc. In principle, one can also re-run the optimization by fitting only a proper subset as time-varying and the rest as time-constant. We have checked this with multiple of the above datasets and the AMSE were not too different from that reported above. The major takeaway from this analysis remains that our time-varying fit, albeit not meant for prediction and constructed only for building simultaneous confidence intervals, can achieve better forecasts than the corresponding time-constant fits. Additionally, our theory can also lead to new models which have only a subset of coefficients time-varying.

6 Acknowledgement

We are grateful to the editor, associate editor and two anonymous referees for their valuable comments and feedback in different rounds which has helped in significantly improving this paper. This research was partially supported by NSF/DMS 1405410.

Appendix A Technical tools and more general assumptions

A.1 The functional dependence measure

To state the structure of dependence we use throughout the appendix, we introduce a functional dependence measure on the underlying process using the idea of coupling as done in Wu [50]. Let and let , a stationary process which admits the causal representation

| (A.1) |

Suppose that is an independent copy of . For some random variable , let denote the -norm of . For , define the functional dependence measure

| (A.2) |

where with

| (A.3) |

a coupled version of with in replaced by an independent copy . Note that measures the dependence of on in terms of the th moment. The tail cumulative dependence measure for is defined as

| (A.4) |

Let . We define the adjusted dependence measure as follows (cf. [57]): For a stationary process , let

A.2 The class for Case 1

To prove uniform convergence of and its derivatives w.r.t. , we require the objective function introduced in Section 2.2 to be Lipschitz continuous in the direction of and to grow at most polynomially in the direction of , where the degree is measured by real numbers . We will therefore ask and its derivatives to be in the class which is now defined.

Let be a sequence of nonnegative real numbers with , and be some constant. Let , and put . Put .

A function is in if ,

and

If is vector- or matrix-valued, means that every component of is in .

A.3 A more general set of assumptions

We show the main theorems under a more general set of assumptions which contain more ‘high-level’ properties of the process and the objective function . These assumptions can therefore be seen as an ‘intermediate step’ in our proofs: We first derive these high-level properties of the processes which hold under the more specific Assumptions 2.2 and 2.3. These high-level assumptions are given in Assumption A.1 and E.8. In Section E at the end of the supplementary material we show that Assumption 2.2 implies Assumption A.1 and Assumption 2.3 implies Assumption E.8. To keep the presentation concise, we only state Assumption A.1 here in the main part of the paper.

For each , let with some measurable function . This process serves as a stationary approximation of the observed process (cf. the introduction in Section 3). The necessary properties are made rigorous in Assumption A.1 (for Case 1) or Assumption E.8 (for Case 2) below. Recall that and , and , .

Assumption A.1.

Suppose that for some and some ,

-

(A1)

(Smoothness in -direction) is twice continuously differentiable w.r.t. . It holds that for some , and with .

-

(A2)

(Assumptions on unknown parameter curve) is compact and for all , lies in the interior of . Each component of is in .

-

(A3)

(Correct model specification) For all , the function is uniquely minimized by .

- (A4)

-

(A5)

(Stationary approximation) There exist such that for all , , :

(A.5) -

(A6)

(Weak dependence) .

Appendix B Proofs of the theorems

In this section, we show the validity of the theorems stated in the paper under the more general Assumption A.1 or Assumption E.8, respectively. We make use of the elementary lemmas derived in Section D. Let us introduce some notation. For , define

and , similarly as but with replaced by or , respectively. Furthermore, put

is estimated by

B.1 Proof of Theorem 3.2

Proof B.1 (Proof of Theorem 3.2).

By Proposition E.6, Assumption A.1 is fulfilled with some . By Proposition E.9, Assumption E.8 is fulfilled with some . In the following, we will only use the more general Assumptions A.1 or E.8, respectively.

By Lemma D.3(i),(iii)(a) and Lemma D.5(a) (in case Assumption A.1 holds) or Lemma D.3(i),(iii)(c) and Lemma D.5(a) (if Assumption E.8 holds) applied to , we have that

where

That is, converges to uniformly in if and . By Lemma D.7, is Lipschitz continuous in both components. Since is the unique minimizer of , we have that is the unique minimizer of . Since is a minimizer of , standard arguments yield

Since , we have

| (B.1) |

Thus for large enough, is in the interior of uniformly in . By a Taylor expansion, we obtain for each :

| (B.2) |

where

with some satisfying , and

| (B.3) |

By Lemma D.3(i),(iii)(a) and Lemma D.5(a) (if Assumption A.1 holds) or Lemma D.3(i),(iii)(c) and Lemma D.5(b) (if Assumption E.8 holds) applied to and , or , respectively, we have for some fixed :

| (B.4) |

where

| (B.5) |

For the moment, let . Note that by Assumption A.1(A3), (A1) (or Assumption E.8(A3’), (A1’)).

By Lemma D.13(i) (if Assumption A.1 holds) or Lemma D.15(i) (if Assumption E.8 holds), we have for each . Using Lemma D.7 (if Assumption A.1 holds) or Lemma D.11 (if Assumption E.8 holds), we see that the conditions of Lemma B.4 are fulfilled and thus, applied to ,

| (B.6) |

With Lemma C.7, we obtain

Since , we obtain with Lemma C.3 (a bias expansion result) and Lemma D.3(i):

| (B.7) |

where . Since is Lipschitz continuous (apply Lemma D.7 in case of Assumption A.1 or Lemma D.11 in case of Assumption E.8 to ), the same holds for . We conclude that with some constant ,

| (B.8) |

Inserting (B.7), (B.8) and (B.1) into (B.2), we obtain

| (B.9) |

where . Inserting (B.9), (B.4) into (B.8), we get . Together with

and (B.7) we obtain the assertion (3.4). The other result (3.5) follows from Lemma D.3(i), Lemma C.7 and Lemma C.3.

B.2 Proof of Theorem 3.3

In this section, we prove Theorem 3.3 by proving its assertion under the morel general Assumption A.1 or E.8, respectively. We first cite some auxiliary results: Lemma B.2 is a confidence band result for i.i.d. Gaussian vectors, Lemma B.4 extends this result to sums of dependent variables by using a Gaussian approximation result (Theorem B.3, cf. [53]). Theorem 3.3 is then proven by applying Lemma B.4 to a Bahadur representation of from Theorem 3.2.

From Lemma 1 in [59], we adopt the following SCB result for Gaussian random vectors:

For the following results, let us assume that there exists some measurable function such that for each , is well-defined. Put .

Theorem B.3 (Theorem 1 and Corollary 2 from Wu and Zhou [53]).

Assume that for each component :

-

(a)

,

-

(b)

,

-

(c)

with some .

for some . Then on a richer probability space, there are i.i.d. and a process such that and

where

| (B.11) |

and

The following lemma is an analogue of Lemma 2 in [59]. Since we use other Gaussian approximation rates from Theorem B.3, we shortly state the proof for completeness.

Lemma B.4.

Let the assumptions and notations from Theorem B.3 hold. Define

Assume that is Lipschitz-continuous and that its smallest eigenvalue is bounded away from 0 uniformly on . Assume that and . Then

| (B.12) |

Proof B.5 (Proof of Lemma B.4).

By Theorem B.3 and summation-by-parts, there exist i.i.d. such that

| (B.13) |

where . Here, (B.13) is due to

Since is Lipschitz continuous by Assumption (b), we can use a standard chaining argument in (as it was done in Lemma C.7 for ) and the fact that , with for some constant to obtain

| (B.14) | |||||

which is due to . So the result follows from Lemma B.2 in view of (B.13) and (B.14).

Proof B.6 (Proof of Theorem 3.3).

By Proposition E.6, Assumption 2.2 implies Assumption A.1 with arbitrarily large . By Proposition E.9, Assumption 2.3 implies Assumption E.8 with arbitrarily large . We now prove the statement under the more general Assumptions A.1 or E.8, respectively.

Choose large enough such that . We therefore have

| (B.15) |

by assumption.

References

- Andreou and Ghysels [2006] {barticle}[author] \bauthor\bsnmAndreou, \bfnmElena\binitsE. and \bauthor\bsnmGhysels, \bfnmEric\binitsE. (\byear2006). \btitleMonitoring disruptions in financial markets. \bjournalJ. Econometrics \bvolume135 \bpages77–124. \bdoi10.1016/j.jeconom.2005.07.023 \bmrnumber2328397 \endbibitem

- Andrews [1993] {barticle}[author] \bauthor\bsnmAndrews, \bfnmDonald W. K.\binitsD. W. K. (\byear1993). \btitleTests for parameter instability and structural change with unknown change point. \bjournalEconometrica \bvolume61 \bpages821–856. \bdoi10.2307/2951764 \bmrnumber1231678 \endbibitem

- Bai [1997] {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. (\byear1997). \btitleEstimation of a change point in multiple regression models. \bjournalThe Review of Economics and Statistics \bvolume79 \bpages551–563. \endbibitem

- Billingsley [1999] {bbook}[author] \bauthor\bsnmBillingsley, \bfnmPatrick\binitsP. (\byear1999). \btitleConvergence of probability measures, \beditionsecond ed. \bseriesWiley Series in Probability and Statistics: Probability and Statistics. \bpublisherJohn Wiley & Sons, Inc., New York \bnoteA Wiley-Interscience Publication. \bdoi10.1002/9780470316962 \bmrnumber1700749 \endbibitem

- Bollerslev [1986] {barticle}[author] \bauthor\bsnmBollerslev, \bfnmTim\binitsT. (\byear1986). \btitleGeneralized autoregressive conditional heteroskedasticity. \bjournalJ. Econometrics \bvolume31 \bpages307–327. \bdoi10.1016/0304-4076(86)90063-1 \bmrnumber853051 \endbibitem

- Brown, Durbin and Evans [1975] {barticle}[author] \bauthor\bsnmBrown, \bfnmR. L.\binitsR. L., \bauthor\bsnmDurbin, \bfnmJames\binitsJ. and \bauthor\bsnmEvans, \bfnmJ. M.\binitsJ. M. (\byear1975). \btitleTechniques for testing the constancy of regression relationships over time. \bjournalJ. Roy. Statist. Soc. Ser. B \bvolume37 \bpages149–192. \bnoteWith discussion by D. R. Cox, P. R. Fisk, Maurice Kendall, M. B. Priestley, Peter C. Young, G. Phillips, T. W. Anderson, A. F. M. Smith, M. R. B. Clarke, A. C. Harvey, Agnes M. Herzberg, M. C. Hutchison, Mohsin S. Khan, J. A. Nelder, Richard E. Quant, T. Subba Rao, H. Tong and W. G. Gilchrist and with reply by J. Durbin and J. M. Evans. \bmrnumber0378310 \endbibitem

- Burkholder [1988] {barticle}[author] \bauthor\bsnmBurkholder, \bfnmDonald L.\binitsD. L. (\byear1988). \btitleSharp inequalities for martingales and stochastic integrals. \bjournalAstérisque \bvolume157-158 \bpages75–94. \bnoteColloque Paul Lévy sur les Processus Stochastiques (Palaiseau, 1987). \bmrnumber976214 \endbibitem

- Cai [2007] {barticle}[author] \bauthor\bsnmCai, \bfnmZongwu\binitsZ. (\byear2007). \btitleTrending time-varying coefficient time series models with serially correlated errors. \bjournalJ. Econometrics \bvolume136 \bpages163–188. \bdoi10.1016/j.jeconom.2005.08.004 \bmrnumber2328589 \endbibitem

- Chen and Gupta [1997] {barticle}[author] \bauthor\bsnmChen, \bfnmJie\binitsJ. and \bauthor\bsnmGupta, \bfnmArjun K\binitsA. K. (\byear1997). \btitleTesting and locating variance changepoints with application to stock prices. \bjournalJournal of the American Statistical association \bvolume92 \bpages739–747. \endbibitem

- Chow [1960] {barticle}[author] \bauthor\bsnmChow, \bfnmGregory C.\binitsG. C. (\byear1960). \btitleTests of equality between sets of coefficients in two linear regressions. \bjournalEconometrica \bvolume28 \bpages591–605. \bdoi10.2307/1910133 \bmrnumber0141193 \endbibitem

- Dahlhaus [2011] {barticle}[author] \bauthor\bsnmDahlhaus, \bfnmR.\binitsR. (\byear2011). \btitleLocally Stationary Processes. \bjournalHandbook of Statistics. \endbibitem

- Dahlhaus and Polonik [2009] {barticle}[author] \bauthor\bsnmDahlhaus, \bfnmRainer\binitsR. and \bauthor\bsnmPolonik, \bfnmWolfgang\binitsW. (\byear2009). \btitleEmpirical spectral processes for locally stationary time series. \bjournalBernoulli \bvolume15 \bpages1–39. \bdoi10.3150/08-BEJ137 \bmrnumber2546797 \endbibitem

- Dahlhaus, Richter and Wu [2017] {barticle}[author] \bauthor\bsnmDahlhaus, \bfnmR.\binitsR., \bauthor\bsnmRichter, \bfnmS.\binitsS. and \bauthor\bsnmWu, \bfnmW. B.\binitsW. B. (\byear2017). \btitleTowards a general theory for non-linear locally stationary processes. \bjournalArXiv e-prints: 1704.02860. \endbibitem

- Dahlhaus and Subba Rao [2006] {barticle}[author] \bauthor\bsnmDahlhaus, \bfnmRainer\binitsR. and \bauthor\bsnmSubba Rao, \bfnmSuhasini\binitsS. (\byear2006). \btitleStatistical inference for time-varying ARCH processes. \bjournalAnn. Statist. \bvolume34 \bpages1075–1114. \bdoi10.1214/009053606000000227 \bmrnumber2278352 \endbibitem

- Engle [1982] {barticle}[author] \bauthor\bsnmEngle, \bfnmRobert F.\binitsR. F. (\byear1982). \btitleAutoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. \bjournalEconometrica \bvolume50 \bpages987–1007. \bdoi10.2307/1912773 \bmrnumber666121 \endbibitem

- Engle and Rangel [2005] {barticle}[author] \bauthor\bsnmEngle, \bfnmRobert F\binitsR. F. and \bauthor\bsnmRangel, \bfnmJ Gonzalo\binitsJ. G. (\byear2005). \btitleThe spline garch model for unconditional volatility and its global macroeconomic causes. \endbibitem

- Fan and Zhang [1999] {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmZhang, \bfnmWenyang\binitsW. (\byear1999). \btitleStatistical estimation in varying coefficient models. \bjournalAnn. Statist. \bvolume27 \bpages1491–1518. \bdoi10.1214/aos/1017939139 \bmrnumber1742497 \endbibitem

- Fan and Zhang [2000] {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmZhang, \bfnmWenyang\binitsW. (\byear2000). \btitleSimultaneous Confidence Bands and Hypothesis Testing in Varying-coefficient Models. \bjournalScandinavian Journal of Statistics \bvolume27 \bpages715–731. \endbibitem

- Francq and Zakoïan [2004] {barticle}[author] \bauthor\bsnmFrancq, \bfnmChristian\binitsC. and \bauthor\bsnmZakoïan, \bfnmJean-Michel\binitsJ.-M. (\byear2004). \btitleMaximum likelihood estimation of pure GARCH and ARMA-GARCH processes. \bjournalBernoulli \bvolume10 \bpages605–637. \bdoi10.3150/bj/1093265632 \bmrnumber2076065 \endbibitem

- Fryzlewicz, Sapatinas and Subba Rao [2008a] {barticle}[author] \bauthor\bsnmFryzlewicz, \bfnmPiotr\binitsP., \bauthor\bsnmSapatinas, \bfnmTheofanis\binitsT. and \bauthor\bsnmSubba Rao, \bfnmSuhasini\binitsS. (\byear2008a). \btitleNormalized least-squares estimation in time-varying ARCH models. \bjournalAnn. Statist. \bvolume36 \bpages742–786. \bdoi10.1214/07-AOS510 \bmrnumber2396814 \endbibitem

- Fryzlewicz, Sapatinas and Subba Rao [2008b] {barticle}[author] \bauthor\bsnmFryzlewicz, \bfnmPiotr\binitsP., \bauthor\bsnmSapatinas, \bfnmTheofanis\binitsT. and \bauthor\bsnmSubba Rao, \bfnmSuhasini\binitsS. (\byear2008b). \btitleNormalized least-squares estimation in time-varying ARCH models. \bjournalAnn. Statist. \bvolume36 \bpages742–786. \bdoi10.1214/07-AOS510 \bmrnumber2396814 \endbibitem

- Giacometti et al. [2012] {barticle}[author] \bauthor\bsnmGiacometti, \bfnmRosella\binitsR., \bauthor\bsnmBertocchi, \bfnmMarida\binitsM., \bauthor\bsnmRachev, \bfnmSvetlozar T\binitsS. T. and \bauthor\bsnmFabozzi, \bfnmFrank J\binitsF. J. (\byear2012). \btitleA comparison of the Lee–Carter model and AR–ARCH model for forecasting mortality rates. \bjournalInsurance: Mathematics and Economics \bvolume50 \bpages85–93. \endbibitem

- Hardle [1986] {barticle}[author] \bauthor\bsnmHardle, \bfnmWOLFGANG\binitsW. (\byear1986). \btitleA note on jackknifing kernel regression function estimators (corresp.). \bjournalIEEE transactions on information theory \bvolume32 \bpages298–300. \endbibitem

- Hoover et al. [1998] {barticle}[author] \bauthor\bsnmHoover, \bfnmDonald R.\binitsD. R., \bauthor\bsnmRice, \bfnmJohn A.\binitsJ. A., \bauthor\bsnmWu, \bfnmColin O.\binitsC. O. and \bauthor\bsnmYang, \bfnmLi-Ping\binitsL.-P. (\byear1998). \btitleNonparametric smoothing estimates of time-varying coefficient models with longitudinal data. \bjournalBiometrika \bvolume85 \bpages809–822. \bdoi10.1093/biomet/85.4.809 \bmrnumber1666699 \endbibitem

- Huang, Wu and Zhou [2004] {barticle}[author] \bauthor\bsnmHuang, \bfnmJianhua Z.\binitsJ. Z., \bauthor\bsnmWu, \bfnmColin O.\binitsC. O. and \bauthor\bsnmZhou, \bfnmLan\binitsL. (\byear2004). \btitlePolynomial spline estimation and inference for varying coefficient models with longitudinal data. \bjournalStatist. Sinica \bvolume14 \bpages763–788. \bmrnumber2087972 \endbibitem

- James Chu [1995] {barticle}[author] \bauthor\bsnmJames Chu, \bfnmChia-Shang\binitsC.-S. (\byear1995). \btitleDetecting parameter shift in GARCH models. \bjournalEconometric Reviews \bvolume14 \bpages241–266. \endbibitem

- Karmakar [2018] {btechreport}[author] \bauthor\bsnmKarmakar, \bfnmSayar\binitsS. (\byear2018). \btitleAsymptotic Theory for Simultaneous Inference Under Dependence \btypeTechnical Report, \bpublisherUniversity of Chicago. \endbibitem

- Karmakar and Wu [2020] {barticle}[author] \bauthor\bsnmKarmakar, \bfnmSayar\binitsS. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2020). \btitleOptimal gaussian approximation for multiple time series. \bjournalTo appear in Statistica Sinica arXiv preprint arXiv:2001.10164. \endbibitem

- Kim, Cho and Lee [2000] {barticle}[author] \bauthor\bsnmKim, \bfnmSoohwa\binitsS., \bauthor\bsnmCho, \bfnmSinsup\binitsS. and \bauthor\bsnmLee, \bfnmSangyeol\binitsS. (\byear2000). \btitleOn the cusum test for parameter changes in GARCH (1, 1) models. \bjournalCommunications in Statistics-Theory and Methods \bvolume29 \bpages445–462. \endbibitem

- Kokoszka et al. [2000] {barticle}[author] \bauthor\bsnmKokoszka, \bfnmPiotr\binitsP., \bauthor\bsnmLeipus, \bfnmRemigijus\binitsR. \betalet al. (\byear2000). \btitleChange-point estimation in ARCH models. \bjournalBernoulli \bvolume6 \bpages513–539. \endbibitem

- Kulperger et al. [2005] {barticle}[author] \bauthor\bsnmKulperger, \bfnmReg\binitsR., \bauthor\bsnmYu, \bfnmHao\binitsH. \betalet al. (\byear2005). \btitleHigh moment partial sum processes of residuals in GARCH models and their applications. \bjournalThe Annals of Statistics \bvolume33 \bpages2395–2422. \endbibitem

- Leybourne and McCabe [1989] {barticle}[author] \bauthor\bsnmLeybourne, \bfnmS. J.\binitsS. J. and \bauthor\bsnmMcCabe, \bfnmB. P. M.\binitsB. P. M. (\byear1989). \btitleOn the distribution of some test statistics for coefficient constancy. \bjournalBiometrika \bvolume76 \bpages169–177. \bdoi10.1093/biomet/76.1.169 \bmrnumber991435 \endbibitem

- Lin and Teräsvirta [1999] {barticle}[author] \bauthor\bsnmLin, \bfnmChien-Fu Jeff\binitsC.-F. J. and \bauthor\bsnmTeräsvirta, \bfnmTimo\binitsT. (\byear1999). \btitleTesting parameter constancy in linear models against stochastic stationary parameters. \bjournalJ. Econometrics \bvolume90 \bpages193–213. \bdoi10.1016/S0304-4076(98)00041-4 \bmrnumber1703341 \endbibitem

- [34] {bbook}[author] \bauthor\bsnmLin, \bfnmShinn-Juh\binitsS.-J., \bauthor\bsnmYang, \bfnmJian\binitsJ. \betalet al. \btitleTesting shifts in financial models with conditional heteroskedasticity: an empirical distribution function approach. \endbibitem

- Lin and Ying [2001] {barticle}[author] \bauthor\bsnmLin, \bfnmD. Y.\binitsD. Y. and \bauthor\bsnmYing, \bfnmZ.\binitsZ. (\byear2001). \btitleSemiparametric and nonparametric regression analysis of longitudinal data. \bjournalJ. Amer. Statist. Assoc. \bvolume96 \bpages103–126. \bnoteWith comments and a rejoinder by the authors. \bdoi10.1198/016214501750333018 \bmrnumber1952726 \endbibitem

- Ling and McAleer [2002] {barticle}[author] \bauthor\bsnmLing, \bfnmShiqing\binitsS. and \bauthor\bsnmMcAleer, \bfnmMichael\binitsM. (\byear2002). \btitleNecessary and sufficient moment conditions for the and asymmetric power models. \bjournalEconometric Theory \bvolume18 \bpages722–729. \bdoi10.1017/S0266466602183071 \bmrnumber1906332 \endbibitem

- Mikosch and Stărică [2004] {barticle}[author] \bauthor\bsnmMikosch, \bfnmThomas\binitsT. and \bauthor\bsnmStărică, \bfnmCătălin\binitsC. (\byear2004). \btitleNonstationarities in financial time series, the long-range dependence, and the IGARCH effects. \bjournalThe Review of Economics and Statistics \bvolume86 \bpages378–390. \endbibitem

- Nabeya and Tanaka [1988] {barticle}[author] \bauthor\bsnmNabeya, \bfnmSeiji\binitsS. and \bauthor\bsnmTanaka, \bfnmKatsuto\binitsK. (\byear1988). \btitleAsymptotic theory of a test for the constancy of regression coefficients against the random walk alternative. \bjournalAnn. Statist. \bvolume16 \bpages218–235. \bdoi10.1214/aos/1176350701 \bmrnumber924867 \endbibitem

- Nyblom [1989] {barticle}[author] \bauthor\bsnmNyblom, \bfnmJukka\binitsJ. (\byear1989). \btitleTesting for the constancy of parameters over time. \bjournalJ. Amer. Statist. Assoc. \bvolume84 \bpages223–230. \bmrnumber999682 \endbibitem

- Palm [1996] {bincollection}[author] \bauthor\bsnmPalm, \bfnmF. C.\binitsF. C. (\byear1996). \btitleGARCH models of volatility. In \bbooktitleStatistical methods in finance. \bseriesHandbook of Statist. \bvolume14 \bpages209–240. \bpublisherNorth-Holland, Amsterdam. \bdoi10.1016/S0169-7161(96)14009-8 \bmrnumber1602132 \endbibitem

- Ploberger, Krämer and Kontrus [1989] {barticle}[author] \bauthor\bsnmPloberger, \bfnmWerner\binitsW., \bauthor\bsnmKrämer, \bfnmWalter\binitsW. and \bauthor\bsnmKontrus, \bfnmKarl\binitsK. (\byear1989). \btitleA new test for structural stability in the linear regression model. \bjournalJ. Econometrics \bvolume40 \bpages307–318. \bdoi10.1016/0304-4076(89)90087-0 \bmrnumber994952 \endbibitem

- Ramsay and Silverman [2005] {bbook}[author] \bauthor\bsnmRamsay, \bfnmJ. O.\binitsJ. O. and \bauthor\bsnmSilverman, \bfnmB. W.\binitsB. W. (\byear2005). \btitleFunctional data analysis, \beditionsecond ed. \bseriesSpringer Series in Statistics. \bpublisherSpringer, New York. \bmrnumber2168993 \endbibitem

- Richter and Dahlhaus [2017] {barticle}[author] \bauthor\bsnmRichter, \bfnmS.\binitsS. and \bauthor\bsnmDahlhaus, \bfnmR.\binitsR. (\byear2017). \btitleCross validation for locally stationary processes. \bjournalArXiv e-prints: 1705.10046. \endbibitem

- Rohan [2013] {barticle}[author] \bauthor\bsnmRohan, \bfnmNeelabh\binitsN. (\byear2013). \btitleA time varying GARCH (p, q) model and related statistical inference. \bjournalStatistics & Probability Letters \bvolume83 \bpages1983–1990. \endbibitem

- Rohan and Ramanathan [2013] {barticle}[author] \bauthor\bsnmRohan, \bfnmNeelabh\binitsN. and \bauthor\bsnmRamanathan, \bfnmT. V.\binitsT. V. (\byear2013). \btitleNonparametric estimation of a time-varying GARCH model. \bjournalJ. Nonparametr. Stat. \bvolume25 \bpages33–52. \bdoi10.1080/10485252.2012.728600 \bmrnumber3039969 \endbibitem

- Starica [2003] {barticle}[author] \bauthor\bsnmStarica, \bfnmCatalin\binitsC. (\byear2003). \btitleIs GARCH (1, 1) as good a model as the accolades of the Nobel prize would imply? \bjournalAvailable at SSRN 637322. \endbibitem

- Stărică and Granger [2005] {barticle}[author] \bauthor\bsnmStărică, \bfnmCătălin\binitsC. and \bauthor\bsnmGranger, \bfnmClive\binitsC. (\byear2005). \btitleNonstationarities in stock returns. \bjournalThe Review of Economics and Statistics \bvolume87 \bpages503–522. \endbibitem

- Vogt et al. [2012] {barticle}[author] \bauthor\bsnmVogt, \bfnmMichael\binitsM. \betalet al. (\byear2012). \btitleNonparametric regression for locally stationary time series. \bjournalThe Annals of Statistics \bvolume40 \bpages2601–2633. \endbibitem

- Witting and Müller-Funk [1995] {bbook}[author] \bauthor\bsnmWitting, \bfnmHermann\binitsH. and \bauthor\bsnmMüller-Funk, \bfnmUlrich\binitsU. (\byear1995). \btitleMathematische Statistik. II. \bpublisherB. G. Teubner, Stuttgart \bnoteAsymptotische Statistik: parametrische Modelle und nichtparametrische Funktionale. [Asymptotic statistics: parametric models and nonparametric functionals]. \bmrnumber1363716 \endbibitem

- Wu [2005] {barticle}[author] \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2005). \btitleNonlinear system theory: another look at dependence. \bjournalProc. Natl. Acad. Sci. USA \bvolume102 \bpages14150–14154 (electronic). \bdoi10.1073/pnas.0506715102 \bmrnumber2172215 \endbibitem

- Wu and Min [2005] {barticle}[author] \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. and \bauthor\bsnmMin, \bfnmWanli\binitsW. (\byear2005). \btitleOn linear processes with dependent innovations. \bjournalStochastic Processes and their Applications \bvolume115 \bpages939 - 958. \bdoihttp://dx.doi.org/10.1016/j.spa.2005.01.001 \endbibitem

- Wu and Shao [2004] {barticle}[author] \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. and \bauthor\bsnmShao, \bfnmXiaofeng\binitsX. (\byear2004). \btitleLimit theorems for iterated random functions. \bjournalJ. Appl. Probab. \bvolume41 \bpages425–436. \bmrnumber2052582 \endbibitem

- Wu and Zhou [2011] {barticle}[author] \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. and \bauthor\bsnmZhou, \bfnmZhou\binitsZ. (\byear2011). \btitleGaussian approximations for non-stationary multiple time series. \bjournalStatist. Sinica \bvolume21 \bpages1397–1413. \bdoi10.5705/ss.2008.223 \bmrnumber2827528 \endbibitem

- Zhang, Lee and Song [2002] {barticle}[author] \bauthor\bsnmZhang, \bfnmWenyang\binitsW., \bauthor\bsnmLee, \bfnmSik-Yum\binitsS.-Y. and \bauthor\bsnmSong, \bfnmXinyuan\binitsX. (\byear2002). \btitleLocal polynomial fitting in semivarying coefficient model. \bjournalJ. Multivariate Anal. \bvolume82 \bpages166–188. \bdoi10.1006/jmva.2001.2012 \bmrnumber1918619 \endbibitem

- Zhang and Wu [2012] {barticle}[author] \bauthor\bsnmZhang, \bfnmTing\binitsT. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2012). \btitleInference of time-varying regression models. \bjournalAnn. Statist. \bvolume40 \bpages1376–1402. \bdoi10.1214/12-AOS1010 \bmrnumber3015029 \endbibitem

- Zhang and Wu [2015] {barticle}[author] \bauthor\bsnmZhang, \bfnmTing\binitsT. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2015). \btitleTime-varying nonlinear regression models: nonparametric estimation and model selection. \bjournalAnn. Statist. \bvolume43 \bpages741–768. \bdoi10.1214/14-AOS1299 \bmrnumber3319142 \endbibitem

- Zhang and Wu [2017] {barticle}[author] \bauthor\bsnmZhang, \bfnmD.\binitsD. and \bauthor\bsnmWu, \bfnmW. B.\binitsW. B. (\byear2017). \btitleGaussian Approximation for High Dimensional Time Series. \bjournalAnn. Statist. \bvolume45 \bpages1895–1919. \endbibitem

- Zhou and Wu [2009] {barticle}[author] \bauthor\bsnmZhou, \bfnmZhou\binitsZ. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2009). \btitleLocal linear quantile estimation for nonstationary time series. \bjournalAnn. Statist. \bvolume37 \bpages2696–2729. \bdoi10.1214/08-AOS636 \bmrnumber2541444 \endbibitem

- Zhou and Wu [2010] {barticle}[author] \bauthor\bsnmZhou, \bfnmZhou\binitsZ. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2010). \btitleSimultaneous inference of linear models with time varying coefficients. \bjournalJ. R. Stat. Soc. Ser. B Stat. Methodol. \bvolume72 \bpages513–531. \bdoi10.1111/j.1467-9868.2010.00743.x \bmrnumber2758526 \endbibitem

Supplement: This material contains the remaining proofs of the results in the paper.

Appendix C Remaining proofs and intermediate lemmata for the proofs of the main theorems

In this section, we give the proofs for the Propositions 4.1 and 4.3 in Section 4. Moreover, we provide the remaining high-level lemmas for the proofs of the main results Theorem 3.2 and Theorem 3.3 of the paper in Section C.1 below.

Proof C.1 (Proof of Proposition 4.1).

(i) Lemma D.3(i),(iii), Lemma D.5 and the notation therein applied to imply

| (C.1) | |||||

We obtain similar as in the proof of Theorem 3.2((B.9) therein) that

Since is Lipschitz continuous by Lemma D.7, the result follows from (C.1) and .

(ii) follows similarly due to with some .

Proof C.2 (Proof of Proposition 4.3).

We proceed similar as in the proof of Theorem 3.2. Now we use the explicit result of Lemma D.5(a) applied to (both for Assumption A.1 and E.8), we obtain

where . By optimality of ,

This implies

| (C.2) |

Assume that for some , . Then there exists such that either (c1)

and thus , or (c2)

and thus .

In case (c1), we have for , thus with some ,

since is continuous and attains its unique minimum at .

In case (c2), we have for , thus with some ,

In both cases, (C.2) becomes a contradiction. Therefore,

Using summation-by-parts and Gaussian approximation similar to that presented in Theorem B.3 for the process , there exists i.i.d. on a richer probability space such that, for as in (B.11)

| (C.3) |

Thus one can replace by in (B.6). A careful examination of the rest of the proof of Theorem 3.2 (with Lemma C.3(C.7) replaced by Lemma C.3(C.8)) now yields the result

| (C.4) |

where (we shortly write )

C.1 Intermediate Lemmas for

In this section, we show some lemmas for which are needed to prove the main results. To do so, we make use of the elementary lemmas derived in Section D. Lemma C.3 derives a bias expansion of , Lemma C.7 shows an approximation of by a localized sum of , that is, the lemma justifies the replacement of the locally stationary process in by with a certain convergence rate. Lemma C.5 discusses Lipschitz properties of a quantity which occurs in the proof of Lemma C.7.

Lemma C.3.

Proof C.4 (Proof of Lemma C.3).

Let . By a Taylor expansion of around , we have

where and is between and . We conclude that

| (C.9) | |||||

Using (if Assumption A.1 holds) or with small enough (if Assumption E.8 holds), we obtain with Lemma D.7 for :

| (C.10) |

Using (C.9), (which follows from Assumption A.1(A1),(A3) or Assumption E.8(A1’), (A3’)) and (C.10), we obtain

| (C.11) | |||||

which shows (C.8). Equation (C.7) follows since and symmetry of imply

Lemma C.5 (Lipschitz properties of ).

Define

where

and . Then there exist come constants such that

Proof C.6 (Proof of Lemma C.5).

We have

If Assumption A.1 holds, we have . Elementary calculations show that

As long as and is small enough, we obtain . So in the case that either or , Lipschitz continuity of implies that there exists some constant such that , .

Proof C.8.

Note that by Assumption A.1(A1),(A3) or Assumption E.8(A1’),(A3’). Put

We have to prove that ). Define and . By a Taylor expansion of w.r.t. , we have

We now apply a similar technique as in the proof of Lemma D.3(iii), namely we use a chaining argument similar to (D.5) to prove

for some large enough. Define the discretization with . By Lemma C.5, we have with Markov’s inequality for :

which converges to 0. Choose . By Lemma D.13(iii) or Lemma D.15(iii) applied with ( small enough), we obtain that . Thus

| (C.13) | |||||

(the constant being independent of ) and

| (C.14) | |||||

(the constant being independent of ). We now apply Theorem 6.2 of [57] (the proof therein also works for the uniform functional dependence measure) with , to , where . For large enough, we obtain with some constant :

which finishes the proof.