Reinforced optimal control

Abstract.

Least squares Monte Carlo methods are a popular numerical approximation method for solving stochastic control problems. Based on dynamic programming, their key feature is the approximation of the conditional expectation of future rewards by linear least squares regression. Hence, the choice of basis functions is crucial for the accuracy of the method. Earlier work by some of us [Belomestny, Schoenmakers, Spokoiny, Zharkynbay. Commun. Math. Sci., 18(1):109–121, 2020] proposes to reinforce the basis functions in the case of optimal stopping problems by already computed value functions for later times, thereby considerably improving the accuracy with limited additional computational cost. We extend the reinforced regression method to a general class of stochastic control problems, while considerably improving the method’s efficiency, as demonstrated by substantial numerical examples as well as theoretical analysis.

Key words and phrases:

Reinforced regression, least squares Monte Carlo, stochastic optimal control2020 Mathematics Subject Classification:

91G20,93E241. Introduction

Stochastic control problems form an important class of stochastic optimization problems that find applications in a wide variety of fields, see [Pha09] for an overview. The general problem can be formulated as follows: How should a decision-maker control a system with a stochastic component to maximize the expected reward? In the theory of stochastic control, one distinguishes between problems with continuous and discrete sets of possible control values. While the first class of control problems contains, for example, energy storage problems, the second one includes stopping and multiple stopping problems. Furthermore one differentiates between discrete-time and continuous-time optimal control problems. (Neither of these distinctions is fundamental: for instance, many numerical methods will replace optimal control problems with a continuous set of control values in continuous time by a surrogate problem with discrete control values in discrete time. Moreover, many discrete optimal control problems may well be analyzed as continuous ones, if the number of possible control values or time-steps is finite but very high).

The range of applications of stochastic control problems is very wide. Originally, optimal stochastic continuous control problems were inspired by engineering problems in the continuous control of a dynamic system in the presence of random noise, see [Åst12] and references therein. In the last decades, problems in mathematical finance (portfolio optimization, options with variable exercise possibilities) and economics inspired many new developments, see [BR11] for some recent developments. Let us also mention a closely connected area of reinforcement learning with plethora of applications in robotics, data science, and engineering, see [SB18].

As a canonical general approach for solving a discrete-time optimal control problem one may consider all possible future evolutions of the process at each time that a control choice is to be made, see [Åst12]. This method is well developed and may be effective in some special cases but for more general problems such as optimal control of diffusion in high dimensions, this approach is impractical. In [BKS09] a generic Monte Carlo approach combined with linear regression was proposed and studied, see also [BS18] for an overview. However, as an important disadvantage, there may be not enough flexibility when modeling highly non-linear behavior of optimal value functions. For instance, a regression based on higher-degree polynomials or local polynomials (splines) may contain too many parameters and, therefore, may over-fit the Monte Carlo sample or even prohibit parameter estimation because the number of parameters is too large. As an alternative to the polynomial bases, nonlinear approximation structures (e.g., artificial neural networks) can be used instead (see, e.g. [HE16],[BCJ19] and [BCJW21]).

In [BSSZ20] a Monte Carlo based reinforced regression approach is developed for building sparse regression models at each backward step of the dynamic programming algorithm in the case of optimal stopping problems. In a nutshell, the idea is to start with a generic set of basis functions, which is systematically enlarged with highly problem-dependent additional functions. The additional basis functions are constructed for the optimal stopping problem at hand without using a fixed predefined finite dictionary. The new basis functions are learned during the backward induction via incorporating information from the preceding backward induction step. More specifically, the (computed, hence approximate) value function at time is used as an additional basis function at time . Thereby, basis functions highly specific to the problem at hand are constructed in a completely automatic way. Indeed, the continuation function at time can often be observed to be very close to the value function at time , especially when the time-step is small – alluding to continuity in time of the solution to some continuous time version of the optimal stopping problem. [BSSZ20] report that the reinforced basis leads to increased precision over the starting set of basis functions, comparable to the standard regression algorithm based on a substantially increased set of basis functions. This improvement is obtained with a limited increase of the computational cost.

In this work, we carry over the approach of [BSSZ20] to a general class of discrete-time optimal control problems including multiple stopping problems (thus allowing pricing of swing options) and a gas storage problem. This generalization turns out to be rather challenging as the complexity of using the previously constructed value function in regression basis at each step of the backward procedure becomes prohibitive when applying the original approach of [BSSZ20]. We overcome this computational bottleneck by introducing a novel version of the original reinforced regression algorithm where one uses a hierarchy of fixed time-depth approximation of the optimal value function instead of a full-depth approximation employed in [BSSZ20]. As a result, we regain efficiency and are able to improve upon the standard linear regression algorithm in terms of achievable precision for a given computational budget.

More precisely, we construct a hierarchy , , of (approximate) value functions with depth . Here, denotes the value functions obtained from the classical Monte Carlo regression algorithm. The higher levels are computed by regression based on a set of basis functions reinforced by the value function one level lower. This way, the added computational cost incurred from reinforcing the basis can be further decreased with minimal sacrifices of accuracy already for small values of . In fact, we propose two versions of the algorithm. In the first version, the levels of the hierarchy of value functions are trained consecutively, allowing for an adaptive choice of the depth of the hierarchy. In the second version, all the levels are trained concurrently, thereby improving the accuracy at each individual level. As a consequence, needs to be fixed in advance and cannot be chosen adaptively in the second variant.

Outline of the paper

In Section 2 we describe a rather general setting for discrete stochastic control problems which we are going to use in this paper. The setting is based on [GHW11]. We recall the reinforced regression algorithm for optimal stopping problems by [BSSZ20] in detail in Section 3. There we also motivate the hierarchical construction of the new reinforced regression algorithm as restricted to the optimal stopping problem. The full algorithm – including both variants – is introduced in Section 4. A detailed analysis of computational costs is provided in Section 5. The next Section 6 provides a detailed convergence analysis for the standard and reinforced regression algorithms in the current setting. Extensive numerical examples including optimal stopping problems, multiple stopping problems and a gas storage optimization problem are provided in Section 7.

2. Setting

First, we present a proper setting for the construction and analysis of reinforced regression algorithms. The setting will be largely based on [GHW11]. We will consider stochastic control problems in discrete time with finite action sets. We note that extensions to continuous action sets are certainly possible, but are left to future research.

We consider a filtration , , which is extended by , for convenience. Let be a Markov process with values in adapted to . Note that we assume that the dynamics of the underlying process does not depend on the control.

At time we are given a control , which is -measurable, and an -measurable cash-flow for some deterministic, measurable function , where is an action that we may choose at time in some finite action space . Note that cash-flows may be positive or negative. We assume that the control takes values in a finite set .

Remark 2.1.

The assumption that actions and controls take values in finite sets and , respectively, is a weaker assumption than it may seem at first sight. Many important control problems naturally fall into this class, see examples below. Even more importantly, it is a well-known fact that many optimal control problems with genuinely continuous action and control spaces have solutions of bang-bang type, i.e., all optimal controls consist of actions taken from a finite set, usually at the boundaries of the (continuous) action sets. Hence, such control problems can effectively be reduced to control problems with finite actions sets. Extensions of the reinforced regression algorithm to infinite action spaces will be studied in future work.

For a given value of the control and a given value of the underlying process , we are given a set of admissible actions

| (2.1) |

i.e., is admissible iff . Finally, if we apply , then the control is updated by

| (2.2) |

Suppose that the control and the underlying state process take values and at time , respectively. For and , we define

| (2.3) |

noting that only depends on . Additionally, we define to be the set of -adapted processes taking values in indexed by . Clearly, if and , then the process is previsible. The set of admissible strategies or admissible policies is defined as follows:

| (2.4) |

Now the central issue is the optimal control problem

| (2.5) |

at a generic time where denotes the conditional expectation w.r.t. .

Taking advantage of the Markov property, we introduce the notation where denotes the Markov process conditioned on , and is defined for . We may then define the value function as

| (2.6) |

which satisfies the dynamic programming principle:

| (2.7) |

for (with ).

Let us now give a few examples for classical stopping and control problems which fall into the above setup.

Example 2.2.

For a single optimal stopping problem with payoff at time , the set of possible control values is , where a control state denotes the number of remaining exercise opportunities. The action takes the value if we stop at the current time and otherwise. Hence, we have

implying that . The cash-flow is defined by

independent of the value of the control . Finally, the update function of the control is defined by Note that the value function , and, hence, the optimal stopping literature usually only considers .

Example 2.3.

Let us now suppose that we have a multiple stopping problem with exercise rights. Again, the control state signifies the remaining exercise opportunities, leading to . The admissible action set is now defined as

Again, . The cash-flow and the update function are defined as in Example 2.2.

Example 2.4.

Consider a simple gas storage problem: given and , we assume that the volume of gas in a storage can only be increased and decreased by a fraction over a given time increment. Let the control denote the status (fill level) of the storage at time . Hence, we define At time , we may either sell (volume of gas; ), buy () – at the current market price – or do nothing (). Hence, the admissible policy set is

with , while the cash-flow is given by

The update function in given by

Remark 2.5.

While we do not allow the actions to have an effect on the dynamics of the state process , a large class of more general control problems could be incorporated by a simple modification of our setting. If we allow updates of the control variable to depend on the state as well as on the previous control and the action, i.e., , then our theoretical analysis remains intact. However, it now becomes possible to control the dynamics of the state process , provided that the law of the controlled process remains absolutely continuous w.r.t. the law of the original process . We refer to the discussion of the optimal liquidation example in [GHW11, Section 2] for more details. Note, however, allowing to depend on in such a way might require us to use regression in rather than just for most practical problems.

3. Reinforced regression for optimal stopping

In this section, we recall the standard regression algorithm as well as the reinforced regression algorithm introduced in [BSSZ20] for optimal stopping problems. We will point out the drawbacks of the latter algorithm for more general control problems, and propose and motivate several modifications. However, for the purpose of a clear illustration, we will restrict ourselves in this section to the optimal stopping case.

Let us recall the optimal stopping setup from Example 2.2 and denote by the value function at evaluated in and . Further recall that the dynamic programming principle is given by

where the continuation function is given by . Fix a set of basis function with , , and sample trajectories from the underlying Markov chain, i.e., are i.i.d. samples from the distribution of , . Then the regression method due to Tsitsiklis-van Roy [TVR01], which we will refer to as the standard regression method, inductively constructs an approximation to the value function as follows: For initialize . For set

| (3.1) |

where the regression coefficients are given by the solution to the least squares problem

| (3.2) |

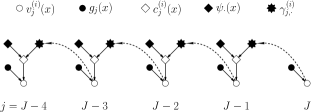

The procedure is illustrated in Figure 1. Note that the costs of this algorithm are of the order (see, e.g., [BSSZ20] or Section 5).

One problem of the standard regression algorithm is that its performance strongly depends on the choice of basis functions. Indeed, while standard classes such as polynomials or splines usually form the backbone of the construction of basis functions, practitioners usually add customized basis functions, for instance the payoff function and some functionals applied to it.

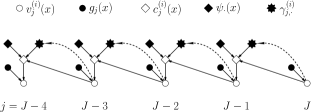

As a more systematic approach, the authors of [BSSZ20] proposed a reinforced regression algorithm. In this procedure the regression basis at each step of the backward induction is reinforced with the approximate value function from the previous step of the induction. The approximate continuation function at is then given by

where the regression coefficient are the solution to the least squares problem

Note that this procedure induces a recursion whenever an approximate value function is evaluated: in order to evaluate we need to evaluate , which in turn requires an evaluation of and so forth, until terminates the recursion. Figure 2 illustrates this procedure. The costs of the reinforced regression method are proportional to (see [BSSZ20]).

Despite the increased computational cost compared to the standard regression algorithm with the same set of basis functions , the reinforced regression algorithm can improve the overall computational cost for a fixed error tolerance drastically. As a rule of thumb, [BSSZ20] report that the reinforced regression algorithm with a standard basis consisting of polynomials of a given degree leads to similar accuracy as the standard regression algorithm based on polynomials of one degree higher. In particular, the reinforced regression algorithm already outperforms the standard regression algorithm for small dimensions , as long as the number of time-steps is not too large.

A direct generalization of the reinforced regression algorithm to more general control problems is certainly possible. The main difference to the optimal stopping problem is that for fixed time we have to choose from many potential candidates to reinforce with, namely any is a candidate. Additionally, the dynamic programming principle (2.7) now entails a possibly non-trivial optimization problem in terms of the policy . Especially the second point makes the recursion at the heart of the reinforced regression algorithm untenable for general control problems.

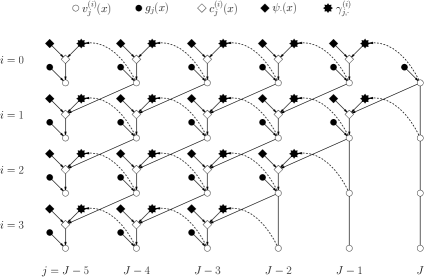

One solutions immediately comes to mind: If performing the recursion all the way to terminal time is too costly, why not truncate at a certain recursion depth? This idea is, in principle, sound, and is the basis of the adaptations suggested below. However, some care is needed in the implementation of this idea. Indeed, if “truncation” simply were to mean “replace the reinforcing basis functions by after a certain truncation step”, this would introduce a structural error in the procedure, as regression coefficients formerly computed in the presence of these basis functions would suddenly be incorrect. Instead, we propose to compute a hierarchy of reinforced regression solutions, corresponding to different “cut-off depths” of the recursion. This way, we can make sure that the coefficients are always consistent, that is, an error as mentioned above can be avoided. We introduce two versions, which both adhere to the same general idea, but differ in an important implementation detail.

The hierarchical reinforced regression algorithm A iteratively constructs approximations to the true value function as follows: For we construct using the standard regression method described above. Then for any , given that is already constructed for , define with the usual backwards induction, where the regression basis at step is reinforced with . The approximate continuation function of the iteration is given by

| (3.3) |

where the regression coefficients are the solutions to the least squares problem

The procedure may be stopped after a fixed number of iterations, or using an adaptive criterion. An illustration of the method can be found in Figure 3. Note that the recursion that is started when evaluating always terminates after at most steps in the evaluation of for or in for .

For a fixed number of iterations we can modify the structure of the previous method so that the primary iteration is the backwards induction over and the secondary iteration is over . In this case we can further modify the algorithm by using as the regression target for the continuation functions for all . We name the resulting algorithm the hierarchical reinforced regression algorithm B. The approximate continuation function at step and iteration is then still given by (3.3) and the least squares problem is given by

Also in this algorithm, the recursion that is started when evaluating stops after at most steps. The costs of the algorithm are discussed in Section 5.

4. Iterated reinforced regression for optimal control

Following the ideas and motivations of Section 3 we now present hierarchical reinforced regression algorithms for optimal control based on the Bellman equation (2.7). The algorithms are based on sample trajectories from the underlying Markov chain . and some initial set of basis functions . For each we will define a subset of cardinality and reinforce the basis by . The respective algorithms iteratively construct sequences of approximations to the value function

for until the iteration is terminated.

4.1. Hierarchical reinforced regression algorithm A

For construct using the standard regression method inductively as follows: At the terminal time initialize where

| (4.1) |

For a , assume that is already constructed for all . Then for each define the regression coefficients by solving the following least squares problem

| (4.2) |

Next define the continuation function by

| (4.3) |

and the approximate value function through the dynamic programming principle

| (4.4) |

Given the approximation for some we construct a new approximation using reinforced regression inductively as follows: Initialize at the terminal time . For assume that is already constructed for . Then for each define the regression coefficients by solving the following least squares problem

| (4.5) |

where , and define the continuation function by

| (4.6) |

for all and . Finally define the approximation through the dynamic programming principle by

| (4.7) |

for all and .

The iteration over can be terminated after steps, yielding as an approximation to the true value function. Alternatively one can introduce an adaptive termination criterion, for example by comparing the relative change in the error of the least squares problem (4.5), terminating after the change falls under a given threshold.

Remark 4.1.

Recall that in the initialization we have for all . It then follows inductively that

| (4.8) |

This identity can be used to reduce the costs of the algorithm, since the regression problem only needs to be solved for all with and .

Remark 4.2.

More general or other forms of reinforced basis functions are certainly possible. The essential point is that they are based on the regression result from the preceding step in the backwards induction and the preceding iteration. Our specific choice may be seen as a natural primal choice. We left flexibility in the choice of the sets , for which depending on the cardinality of the set , possible choices are the trivial and , or for some set independent of , or more elaborately for some . Note that the use of a step dependent set in the above method is straightforward.

4.2. Hierarchical reinforced regression algorithm B

Note that (4.2) and (4.5) are based on the approximate value functions and , respectively, even though the more accurate approximation is already available at this point. Hence, we can potentially improve the algorithm’s accuracy by always considering the most accurate approximation of the value function in the Bellman equation.

Fix a number of iterations and initialize the approximate value functions at the terminal time by for all , where is given by (4.1). The approximate value functions at times previous to are defined inductively as follows:

Let and assume that is already defined for all and . For and each determine the coefficients for the regression basis by solving the least squares problem

| (4.9) |

and define the approximate continuation function by (4.3). For and each determine the regression coefficients by solving the least squares problem

| (4.10) |

where , and define the continuation function by (4.6).

Finally, define the approximation to the value function for all by (4.7). After ending the backwards induction use as an approximation to the true value function.

Remark 4.3.

Note that the identity (4.8) also holds for the above algorithm. Moreover, since we are only interested in , we can discard the computation of and for all , since they do not contribute to the construction of . The least squares problem then only needs to be solved for with and

Remark 4.4.

Choosing the number of iterations we then have from the previous remark that only the value functions on the diagonal need to be constructed. In this case, denote , etc., and observe that the least squares problem which is solved in each step of the backwards induction is given by

where . Hence, for the above algorithm represents a direct extension of the reinforced regression algorithm in [BSSZ20] from optimal stopping to optimal control problems.

5. Computational cost

We study the computational work of the modified reinforced regression algorithm of Section 4.2. In what follows, the following operations are considered to be performed at constant cost:

-

•

Multiplications, additions and other primitive operations at cost ;

-

•

Simulation from the distribution of the Markov process at cost ;

-

•

Evaluation of the standard basis functions or of the payoff at cost ;

We furthermore introduce the following notations:

-

•

We set .

-

•

The cost of evaluating other non-trivial, but known functions (think of the value function when all the required regression coefficients are already known) will be denoted by .

If an expression involves several such operations, then only the most expensive constant is reported. (E.g., evaluating a basis function and multiplying the value by a scalar constant is considered to incur a cost .) We may also use constants which do not depend on the specifics of the algorithm. We now go through the individual stages of the algorithm.

-

(1)

Simulating trajectories at cost .

-

(2)

Computing the terminal value function as in (4.1) for a given and all at cost .

-

(3)

For fixed and set up the least squares problem (4.9) at cost .

-

(4)

For fixed and , we solve the least squares problem (4.9) at cost . The total cost is .

-

(5)

For fixed , , and set up the least squares problem (4.10) at cost .

-

(6)

For fixed , , and solve the least squares problem (4.10) at cost , leading to a total cost of .

For simplicity of the presentation, we shall only consider the following scenario:

Assumption 5.1.

The total set of reinforced basis functions contains all available value functions, i.e.,

For fixed and let

| (5.1) |

The key step of the cost analysis is understanding the cost of evaluating the reinforced basis functions, which are, in turn, given in terms of reinforced basis functions at later time steps. We note that it is essential to analyze the cost of evaluating the full set of reinforced basis functions rather than individual ones , as the latter method would show us an apparent explosion of basis functions as we increase time.111Suppose that each reinforced basis function depends on two reinforced basis functions and . If we follow this recursion for steps, we arrive at a total set of basis functions. The catch is that many, if not all, of these basis functions overlap with basis functions for other reinforced basis functions . By (4.7), evaluating requires evaluating the payoff functions for all combinations of controls and policies , then evaluating , and taking the corresponding maxima. In total, this means

On the other hand, by (4.6) evaluating requires evaluations of standard basis functions, elementary operations for summing them, one evaluation of , and elementary operations for their summation. In total, this means that

This implies the cost estimate

| (5.2) |

Lemma 5.2.

The cost of evaluating , , can be bounded by

Proof.

For , consider the cost recursion

Assuming that the recursion hits before , i.e., , the cost satisfies the recursion with , and, hence, we obtain

This gives the first expression in the statement of the lemma with .

On the other hand, if , we hit before . In this case, satisfies the same recursion, but with initial value . ∎

In order to shorten notation, we introduce

so that the estimate of Lemma 5.2 shortens to

We next estimate the cost of setting up the regression problem (4.9), which is proved similarly.

Lemma 5.3.

The cost of setting up the regression problem for , , , can be bounded by

The cost for setting up the least squares problem (4.10) is computed in a similar way.

Lemma 5.4.

The cost of setting up the regression problem for , , , , can be bounded by

Proof.

A closer look at (4.10) reveals that the total cost of setting up all these least squares problems can be bounded by

| (5.3) |

taking into account that was already evaluated during the set-up of the least squares problem (4.9) and, hence, does not need to be evaluated again. Using Lemma 5.2, we obtain

Evaluating the double sums gives the estimate from the statement of the lemma. ∎

Abandoning the difference between and using the trivial bounds , , we obtain

Theorem 5.5.

The computational cost of the algorithm presented in Section 4.2 can be bounded by

where is a positive number independent of , , , , and .

Remark 5.6.

Recall that Remark 4.4 introduced a significantly cheaper variant of algorithm B for the case . It is easy to see that the computational cost of this variant is bounded by

i.e., the total cost is proportional to rather than . Indeed, the main difference in the cost analysis as compared to the full modified algorithm is that (5.3) can be replaced by

Note that this essentially corresponds to the algorithm of [BSSZ20] directly generalized to optimal control problems.

6. Convergence analysis

In this section we analyze the convergence properties of the standard and reinforced regression algorithms introduced in the previous sections. For related convergence analysis in the case of optimal stopping problems we refer the interested reader to [Zan13], [Zan18], and [BS20], see also [BRS21]. Henceforth we assume that

| (6.1) |

then all the value functions

are uniformly bounded by Fix a sequence of spaces of functions defined on We stress that these spaces are not necessarily linear at this point. Construct the corresponding sequence of estimates via

| (6.2) | ||||

where stands for the empirical projection of the conditional expectation on based on a sample

| (6.3) |

from the joint distribution of that is,

In (6.2) is a truncation operator at level defined by

Due to Theorem 11.5 in [GKKW02], one has for all with and all that

| (6.4) |

where is the Vapnik-Chervonenkis dimension of (see Definition 9.6 in [GKKW02] is the distribution of and is an absolute constant. In order to keep the analysis tractable, we assume that the sets are independent for different , see Remark 6.5 below. More specifically, we consider an algorithmic framework based on (6.2), where for every exercise date the samples (6.3) are simulated independently, and consider the information sets

Let us define for

| (6.5) |

and for a generic (exact) dummy trajectory independent of let

| (6.6) |

Note that is a -measurable random function while the estimate is a -measurable one. We further define

| (6.7) |

The following lemma holds.

Lemma 6.1.

We have that,

| (6.8) |

Proof.

Let be a generic (exact) dummy trajectory independent of Then from (6.6), and (6.7) we see that for

| (6.9) |

Next, by (2.7), (6.2), (6.5), and (6.7) we have that

| (6.10) | |||||

Hence, by (6.9) one has that

Finally, by taking the “all-in expectation” w.r.t. the law , we observe that

by Jensen’s inequality and the tower property. ∎

In fact, Lemma 6.1 is the key to the next proposition.

Proposition 6.2.

Set

with being the law of the sample Then it holds

| (6.11) |

for all with by definition.

Proof.

Corollary 6.4.

By inserting the estimate

in Proposition 6.2, we get the alternative recursion

and under the alternative assumption

for some and we obtain for the bounds

Remark 6.5.

In [Zan13] the convergence of an “independent sample version” of the Longstaff-Schwartz algorithm was studied based on an assumption similar to the independence for different here. However, in a later paper [Zan18] it was shown (by more involved analysis) that the convergence rates based on one and the same sample are basically the same as in [Zan13] up to certain constants. One therefore may naturally expect that similar conclusions apply in our context. Therefore the numerical examples in Section 7 are based on a single sample of trajectories.

The proposed reinforced regression algorithm with uses linear approximation spaces of the form

| (6.15) |

for where are some fixed basis functions (e.g. polynomials) on In this case In order to see the advantage of adding additional basis functions more clearly, we prove the following proposition.

Proposition 6.6.

Assume additionally that

| (6.16) |

for all and

| (6.17) |

for some constants Then it holds for reinforced spaces from (6.15)

Proof.

The above proposition implies that if stays bounded for (for example if scales as ), then the approximation error becomes small as Note that the latter property can not be guaranteed when using fixed (nonadaptive) linear spaces Of course, the exponential in factor in (6.14) will lead to explosion of the overall error as but the above observation still indicates that the inclusion of the functions into can significantly improve the quality of the estimates especially in the case of large . Concerning the dependence of the bound (6.14) on , we note that this estimate is likely to be too pessimistic, see also a discussion in [Zan13].

7. Numerical examples

We now present various numerical examples which demonstrate the accuracy of the reinforced regression algorithm in practice. To allow for a direct comparison with the reinforced regression algorithm of [BSSZ20], we first consider a (single) optimal stopping problem, more particularly a Bermudan max-call option. Our second example is a multiple stopping problem, for which the hyperparameters already become crucial. Finally, our last example is an optimal control of a gas storage.

We have tested both algorithms A and B for the HRR (hierarchical reinforced regression) method, however, the latter version always gave slightly better results and therefore we have only included the value obtained with the algorithm B. Intuitively this is to be expected, as the algorithm B uses more accurate regression targets in the backwards induction. The algorithm A may be of use in situations where one is interested in improving the approximation until a certain accuracy threshold is reached, however, properly done this approach should also include a calculation of upper bounds, which we do not discuss in our paper.

Before, let us also mention how a lower biased estimate to the value of a control problem in a Markovian setting is calculated using the result of a regression procedure. Let be an approximation to the function given by

with by convention. Using the hierarchical reinforced regression method, such an approximation is given by defined in (4.6). Further let be sample trajectories from the underlying Markov chain, generated independently from the samples used in the regression procedure. Then we can iteratively define a sequence of polices with by

or all and , where and . It then follows from the definition, that each is an admissible sequence of policies, i.e. . Therefore, a lower estimate to the value is given by

Lower bounds allow a direct comparison of the performance of different methods, in the sense that the method yielding the highest lower bound (up to Monte Carlo errors) performed best, since this value must be closest to the true value of the control problem. This direct comparison is, however, not possible for the approximate value which may lie above or below the true value. Our main premise in the following is that the HRR algorithm is a more efficient way to improve the performance of the regression algorithm as compared with increasing the complexity of the regression basis. Hence, for this relative comparison it is also sufficient to study lower bounds.

7.1. Bermudan max-call option

In this section we evaluate the performance of the hierarchical reinforced regression (HRR) method from Section 4 on the valuation of a Bermudan max-call option. Let be a filtered probability space on which a -dimensional Brownian motion is defined. Further let be the geometric Brownian motion defined by

where . Option rights can be exercised on a predefined set of possible exercise dates , where at most one right can be exercised on any given date. Assume that the exercise dates are equidistant for all with and define the underlying Markov chain by . Recall from Example 2.3 that in order to model a multiple stopping problem in the optimal control framework we define the set of policies by and the set of controls by , where is the number of exercise rights. Further, we define

for all , and , where is the max-call pay-off function defined by

where is the option strike. Then the value function defined in (2.6) yields the value of the Bermudan max-call option with underlying and data .

7.1.1. Single exercise right

We will first consider the case of a single exercise right . This is a standard example in the literature, see for example [BG04, Rog02, AB04] and more recently [BCJ19]. The performance of the reinforced regression method for this example was already analyzed in [BSSZ20]. We revisit this example in order to demonstrate that even in the optimal stopping case our novel HRR method allows for improvements in computational costs without sacrificing the quality of the estimations.

| Basis | Lower bounds | CI from [BCJ19] | |||

|---|---|---|---|---|---|

| Regression | HRR | Reinf. Reg. | |||

| 2 | 13.015 (0.022) | 13.772 (0.015) | 13.794 (0.015) | [13.880,13.910] | |

| 13.679 (0.019) | - | - | |||

| 13.775 (0.016) | 13.871 (0.015) | 13.882 (0.014) | |||

| 13.874 (0.016) | - | - | |||

| 3 | 17.764 (0.029) | 18.526 (0.017) | 18.540 (0.018) | [18.673,18.699] | |

| 18.404 (0.022) | - | - | |||

| 18.519 (0.020) | 18.639 (0.017) | 18.653 (0.017) | |||

| 18.655 (0.021) | - | - | |||

| 5 | 25.463 (0.024) | 25.998 (0.021) | 25.990 (0.019) | [26.138, 26.174] | |

| 25.823 (0.026) | - | - | |||

| 25.990 (0.023) | 26.097 (0.019) | 26.109 (0.020) | |||

| 26.111 (0.022) | - | - | |||

| 10 | 38.022 (0.025) | 38.234 (0.022) | 38.225 (0.024) | [38.300,38.367] | |

| 38.058 (0.024) | - | - | |||

| 38.299 (0.023) | 38.316 (0.020) | 38.331 (0.021) | |||

| 38.349 (0.021) | - | - | |||

Define the functions , , the th largest entry of , for and consider the following three sets of regression basis functions:

Note that the cardinalities of these sets are given by , , , and , respectively. Regarding the HRR method, we use the algorithm of the second type described in Section 4.2. Further note that in the optimal stopping case there is only one choice for the set of reinforced value function for the HRR method since and therefore we always set .

We considered two different set-ups for the comparison of the different methods:

-

•

First we keep the number of exercises dates fixed and vary the number of underlying assets ;

-

•

Second we keep fixed and vary (while also keeping fixed).

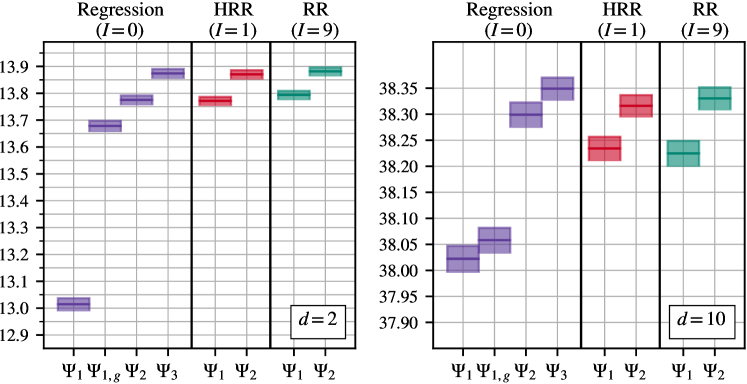

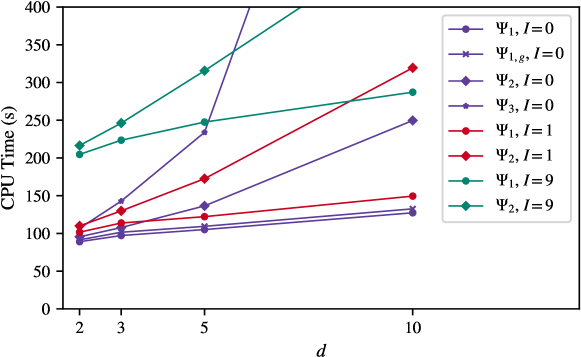

In Table 1 we present lower estimates to the value of a Bermudan max-call option with a single exercise right for and . In the corresponding Figure 4 we have visualized the lower bounds for the comparison between the different regression methods. For each of the considered methods we used simulated training samples paths to determine the regression coefficients and paths for calculating the lower bounds.

In order to give the reader an easy reference point, in Table 1 we have also included the confidence intervals for the value of the Bermudan max-call option from [BCJ19]. Note however that we do not aim for an improvement of the latter values in terms of benchmarking. In fact the method used in [BCJ19] is quite different from ours, as it uses deep neural networks for approximating the optimal stopping policies at each time step, and a direct comparison would require the usage of higher order polynomials for our method.

We first observe that across all numbers of assets the HRR method with the set of basis functions performs significantly better then the standard regression method with the basis and . The same holds true when comparing the methods using the regression basis . More importantly however, we observe that for the HRR method with basis yields lower bounds of the same quality as obtained with the standard method and the larger basis . The same holds true when comparing the HRR method with basis against the standard method with the basis . In the case assets, the lower bounds obtained with the HRR method and basis lie just slightly below the values of the lower bounds obtained with standard method and the basis , however one has to keep in mind that in this case and . Moreover, we see that the HRR method with a recursion depth performs just as well as the (full depth) reinforced regression method ().

Furthermore, in Figure 5 we have visualized the corresponding elapsed CPU times during the backwards induction and the calculation of the lower bounds. As foreshadowed in Section 5, we see that the computational costs of the HRR method are significantly reduced by choosing a small recursion depth . In particular, we are able to state that for sufficiently large ( respectively ) the HRR method with recursions depth and the basis respectively is more efficient then the standard method with the basis respectively .

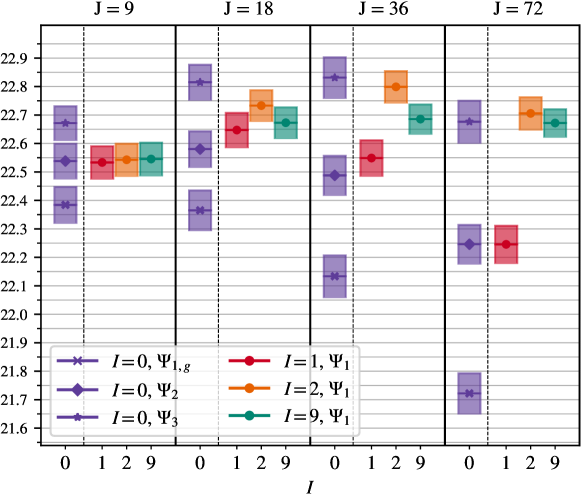

The results of the second set-up are visualized in Figure 6. In this case, we have approximated the value of Bermudan max-call options with a fixed number of assets and different numbers of exercise dates , while also keeping fixed. When keeping all other parameters fixed, the value of the option clearly is non-decreasing in the number of exercise dates . Our first observation is that for all considered methods there exists a threshold for at which the performance worsens. Indeed, Corollary 6.3 shows that the approximation error depends exponentially on .

However, in practice, some methods are less vulnerable to the error explosion in than others. In this example, we see that the standard regression method with the basis and , respectively, starts to perform worse for . The lower bounds calculated with the HRR method with the basis and stay approximately on the same level as the lower bounds calculated with the standard method and the basis , for all numbers of exercise dates. The lower bounds calculated with the standard method and the basis first increase when moving from to exercise dates and decrease at last when moving from to exercise dates.

The main observation is that when we increase , the HRR methods with and come closer to the lower bounds calculated with the standard method and the basis . This underlines the theoretical discussion for from Section 6. Moreover, we see that the HRR method performs at least as well with as with . Regarding CPU time, the HRR method with is more efficient than then the standard regression method with the basis for . Comparing the HRR methods with and , we see that choosing the parameter small is necessary to in order to obtain desirable efficiency. Since on the other hand, the HRR method with performed significantly worse then with , we also see that in this case it was necessary to choose . These observations underline the relevance of the HRR in its full complexity even in the case of optimal stopping problems.

7.1.2. Multiple exercise rights

Next we consider a Bermudan max-call option with exercise rights. In this case the HRR method allows for different possibilities of reinforced value functions depending on the choice of the sets (recall Remark 4.2). Since is small, we choose for simplicity.

| Basis | Regression | Hierarchical Reinforced Regression | |||

|---|---|---|---|---|---|

| 90.863 (0.072) | 92.038 (0.070) | 92.287 (0.070) | 92.311 (0.067) | 92.357 (0.061) | |

| 91.837 (0.082) | - | - | - | - | |

| 92.140 (0.070) | 92.418 (0.064) | 92.548 (0.060) | 92.631 (0.061) | 92.625 (0.061) | |

| 92.571 (0.069) | - | - | - | - | |

In Table 3 we present lower bounds to the value of a Bermuda max-call option with exercises rights, obtained with the standard regression method and HRR method for different choices of regression basis functions and the parameter , with the implementation of the second type described in Section 4.2. We first observe that for a fixed set of basis functions or increasing the parameter yields increased, and thus improved, lower bounds. This improvement is most significant when moving from (standard regression) to and from to and becomes less significant when further increasing . Moreover, we observe that the HRR method with and basis functions yields better lower bounds then the standard regression method with the larger set of basis functions and more importantly, for the HRR with basis functions method yields better lower bounds than the standard regression method with the even larger set of basis functions . This observation prevails when comparing the standard regression method with the basis against the HRR method with the basis . We can therefore conclude that the HRR method yields results of better quality than standard regression using fewer regression basis functions. Moreover, we realize that up to changes that are insignificant with respect to the Monte Carlo error, the HRR reaches its best performance already for , thus further increasing is not necessary.

7.2. A gas storage problem

In this subsection we consider a gas-storage problem of the kind introduced in Example 2.4. In contrast to the example in the previous subsection, this optimal control problem is not of a multiple stopping type, which is a consequence of the anti-symmetry in the policy set: injection of gas into the facility , no action and production of gas .

For the gas price we use a similar but slightly more elaborate model to the one proposed in [TDR09] (and also used in [GHW11]). More specifically, we use the following joint dynamics to model the price of crude oil and the price of natural gas

| (7.1) |

for , where for , and are Brownian motions with correlation , is a Poisson process with intensity and are i.i.d. normal distributed random vectors with , and . Moreover we assume that , and are independent. Note that both and are mean reverting processes with jump contributions. The oil price process reverts to the long-term constant mean and the gas price process reverts towards the oil price , which is aiming to model the well known strong correlation between crude oil and natural gas prices. Note also that we have assumed for simplicity that the jump signal, which has the purpose of modeling price peaks, is the same Poisson process for both oil and gas prices, however the magnitude of the jumps is given by different (but correlated) normal distributed random variables.

Denote by the 2-dimensional Markov chain that is obtained by discretizing the above SDE (7.1) with an Euler-scheme on the time interval interval . We assume that the manager of the gas storage facility has the possibility to buy and sell gas on a predefined set of dates in the year with and some such that . The 2-dimensional Markov chain underlying the optimal control problem is then given by with .

Recall from Example 2.4 that we assume that the volume of gas in the storage can only be increased or decreased by a fraction for some over the time interval of days. The state space of the control variable is then given by . Also recall the definition of the space of policies , the constraint sets and the function from Example 2.4. We assume that there is no trading at hence . The cash-flow underlying to the optimal control problem only depends on the second component of the Markov chain and is given by

where is the interest rate.

We do not pay attention to the physical units of the parameters quantifying the gas storage capacity and the quotation of the gas price, since the linearity of the pay-off with respect to the parameter and the gas price allows to properly scale the resulting value of the optimal control problem. The following specific choice of the price model parameters are oriented at the values in [TDR09]

| (7.2) |

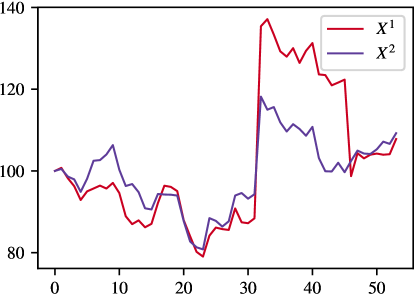

Figure 7 shows a sample trajectory of the Markov chain with the above parameters.

Further we define the following sets of polynomial regression basis functions

| (7.3) |

| I | Basis | Lower bounds | |

|---|---|---|---|

| 0 | 78.381 | 70.489 (0.066) | |

| 78.575 | 70.635 (0.068) | ||

| 73.072 | 71.253 (0.068) | ||

| 73.207 | 71.402 (0.068) | ||

| 72.929 | 71.333 (0.081) | ||

| 72.595 | 71.498 (0.068) | ||

| 1 | 71.991 | 71.579 (0.070) |

The quantities were obtained with the standard regression method () and the HRR method (), the different sets of basis functions (7.3), training sample paths and paths for calculating the lower bounds.

We have approximated the value of the gas storage problem with the following parameters

| (7.4) |

In this configuration the gas storage facility is initially loaded with half its capacity and the gas storage manager has the possibility to trade gas every seven days, and the amount by which the manager can inject or produce gas is one height of the total capacity. In Table 3 we present the numerical results that were obtained with the standard regression method and the HRR method.

We used training sample paths and sample paths for the calculation of the lower bounds. For the set of reinforced basis functions in the HRR method we have chosen , i.e. in each step of the backwards induction, the regression basis was reinforced with only one function.

We observe at first, that the lower bounds obtained with the standard regression method are improved when using polynomials in both variables instead of just in the second variable (gas price) and are also improved when using polynomials of increasing order (with the only exception of the third degree polynomials). Moreover, we observe that the lower bound obtained with the HRR method, using the set of basis functions and , lies above all lower bounds that were obtained with the standard regression, in particular the bound obtained with the regression basis (up to Monte Carlo errors). Hence the HRR method based on polynomials of degree one performed at least as well as the standard method with polynomials of degree four.

7.3. Conclusions

Let us summarize the findings of the numerical experiments. We observe that the hierarchical reinforced regression algorithm (HRR) based on polynomial basis functions of a certain degree tend to produce results comparable to standard regression (SR) based on polynomial basis functions of degree or even higher, see Figures 4, 6, Tables 2, and, most impressively, 3.

The numerical results also indicate that, indeed, HRR with low depth of the hierarchy already performs very well, even if , see Figures 4, 6 and Table 2. Hence, HRR performs with similar accuracy to the reinforced regression algorithm (RR) of [BSSZ20], but at much improved cost. Additionally, when comparing HRR with SR at fixed accuracy, the computational cost of HRR is usually much smaller, especially for large, see Figure 5.

References

- [AB04] L. Andersen and M. Broadie. A Primal-Dual Simulation Algorithm for Pricing Multi-Dimensional American Options. Management Science, 50(9):1222–1234, 2004.

- [Åst12] Karl J Åström. Introduction to stochastic control theory. Courier Corporation, 2012.

- [BCJ19] Sebastian Becker, Patrick Cheridito, and Arnulf Jentzen. Deep optimal stopping. Journal of Machine Learning Research, 20:74, 2019.

- [BCJW21] Sebastian Becker, Patrick Cheridito, Arnulf Jentzen, and Timo Welti. Solving high-dimensional optimal stopping problems using deep learning. European Journal of Applied Mathematics, 32(3):470–514, 2021.

- [BG04] Mark Broadie and Paul Glasserman. A stochastic mesh method for pricing high-dimensional American options. Journal of Computational Finance, 7:35–72, 2004.

- [BKS09] D. Belomestny, A. Kolodko, and J. Schoenmakers. Regression methods for stochastic control problems and their convergence analysis. SIAM Journal on Control and Optimization, 48:3562–3588, 01 2009.

- [BR11] Nicole Bäuerle and Ulrich Rieder. Markov decision processes with applications to finance. Springer Science & Business Media, 2011.

- [BRS21] Christian Bayer, Martin Redmann, and John Schoenmakers. Dynamic programming for optimal stopping via pseudo-regression. Quantitative Finance, 21(1):29–44, 2021.

- [BS18] Denis Belomestny and John Schoenmakers. Advanced simulation-based methods for optimal stopping and control. Palgrave Macmillan, London, 2018. With applications in finance.

- [BS20] Denis Belomestny and John Schoenmakers. Optimal stopping of McKean–Vlasov diffusions via regression on particle systems. SIAM Journal on Control and Optimization, 58(1):529–550, 2020.

- [BSSZ20] Denis Belomestny, John Schoenmakers, Vladimir Spokoiny, and Bakhyt Zharkynbay. Optimal stopping via reinforced regression. Communications in Mathematical Sciences, 16(1):109–121, 2020.

- [BSZ15] Christian Bender, John Schoenmakers, and Jianing Zhang. Dual representations for general multiple stopping problems. Math. Finance, 25(2):339–370, 2015.

- [GHW11] Lajos Gyurko, B. Hambly, and Jan Witte. Monte Carlo methods via a dual approach for some discrete time stochastic control problems. Mathematical Methods of Operations Research, 81, 12 2011.

- [GKKW02] László Györfi, Michael Kohler, Adam Krzyżak, and Harro Walk. A distribution-free theory of nonparametric regression. Springer Series in Statistics. Springer-Verlag, New York, 2002.

- [HE16] Jiequn Han and Weinan E. Deep learning approximation for stochastic control problems, 2016.

- [Pha09] Huyên Pham. Continuous-time stochastic control and optimization with financial applications, volume 61. Springer Science & Business Media, 2009.

- [Rog02] L. C. G. Rogers. Monte Carlo valuation of American options. Math. Finance, 12(3):271–286, 2002.

- [SB18] Richard S Sutton and Andrew G Barto. Reinforcement learning: An introduction. MIT press, 2018.

- [Sch12] J. Schoenmakers. A pure martingale dual for multiple stopping. Finance Stoch., 16:319–334, 2012.

- [TDR09] Matt Thompson, Matt Davison, and Henning Rasmussen. Natural gas storage valuation and optimization: A real options application. Naval Research Logistics (NRL), 56(3):226–238, 2009.

- [TVR01] John Tsitsiklis and Benjamin Van Roy. Regression methods for pricing complex American style options. IEEE transactions on neural networks / a publication of the IEEE Neural Networks Council, 12:694–703, 02 2001.

- [Zan13] Daniel Z. Zanger. Quantitative error estimates for a least-squares Monte Carlo algorithm for American option pricing. Finance Stoch., 17(3):503–534, 2013.

- [Zan18] Daniel Z. Zanger. Convergence of a least-squares Monte Carlo algorithm for American option pricing with dependent sample data. Math. Finance, 28(1):447–479, 2018.