Online Orthogonal Matching Pursuit

Abstract

Greedy algorithms for feature selection are widely used for recovering sparse high-dimensional vectors in linear models. In classical procedures, the main emphasis was put on the sample complexity, with little or no consideration of the computation resources required. We present a novel online algorithm: Online Orthogonal Matching Pursuit (OOMP) for online support recovery in the random design setting of sparse linear regression. Our procedure selects features sequentially, with one pass over data, alternating between allocation of samples only as needed to candidate features, and optimization over the selected set of variables to estimate the regression coefficients. Theoretical guarantees about the output of this algorithm are proven and its computational complexity is analysed.

1 Introduction

In the context of large scale machine learning, one often deals with massive data-sets and a considerable number of features. While processing such large data-sets, one is often faced with scarce computing resources. The adaptability of online learning algorithms to such constraints made them very popular in the machine learning community.

In the current work we address the problem of online feature selection, i.e support recovery algorithms restricted to a single training pass over the available data. This setting is particularly relevant when the system cannot afford several passes throughout the training set: for example, when dealing with massive amounts of data or when memory or processing resources are restricted, or when data is not stored but presented in a stream.

Suppose that there exists a vector with such that the response variable is generated according to the linear model , where satisfies , let . Throughout the article, we consider that the feature vector is random, and we assume that and almost surely for a known constant . The straightforward formulation of sparse regression using a pseudo-norm constraint is computationally intractable. This challenge motivated the rise of many computationally tractable procedures whose statistical validity has been established under additional assumptions such as the Irrepresentable Condition (IC) and Restricted Isometry Property (RIP).

Many algorithms have been proposed for support recovery, the most popular procedures use a convex relaxation with the norm (LASSO based algorithms, Tibshirani (1996)), and greedy procedures such as Orthogonal Matching Pursuit algorithm (OMP, Mallat and Zhang (1993)), where features are selected sequentially. In this paper, we develop a novel online variant of OMP. Theoretical guarantees about OMP on support recovery were developed by Zhang (2011), under the IC+RIP assumption, and many variants have been developed Blumensath and Davies (2008); Combettes and Pokutta (2019), where different optimization procedures are used instead of ordinary least squares. However, the computational complexity remains of the order for one variable selection step and for total support recovery, with a sample size satisfying for exact support recovery with a high probability guarantee. A drawback of these procedures, besides the need to perform multiple passes over the training set, is that the sample size, hence the computational complexity of every step, depends on . Intuition suggests that recovery of the larger coefficients of should be possible with less data and hence less computational complexity. We propose a feature selection procedure that is consistent with this intuition.

If the support size is known, the proposed algorithm (OOMP) halts after recovering all features in . Otherwise, it relies on some external criterion (such as a runtime budget), whenever halted, the procedure returns a set of features guarantees to belong to with high probability. Moreover, we show that support recovery is achieved in finite time and provide a control on the computational complexity necessary to attain this goal.

1.1 Main contributions

This paper is about the design and analysis of support recovery for linear models in the online setting. We make the following contributions:

-

•

We design a general modular procedure, where the learner can use any black-box optimization algorithm combined with an approximate best arm identification approach, provided those procedures come with suitable guarantees. We show that at any interruption time, it is guaranteed with high probability that the set of selected features satisfies: .

-

•

We instantiate the general design using a variant of the stochastic gradient descent for the optimization and a LUCB-type (Lower Upper Confidence Bound) procedure for approximate best arm selection. The proposed algorithm has the advantage of being adapted to the streaming setting (i.e. requiring only one pass over data).

-

•

A prior knowledge on the support size or the magnitude of the smallest coefficient: , is not necessary to run the procedure. We show that OOMP recovers the support in finite time and provide a control on the runtime necessary to achieve this objective.

-

•

We compare the runtime required for support recovery using OOMP () with the corresponding runtime using batch version OMP (). We show that when , it always holds , and when the coefficients of have a different order of magnitude, can be much smaller than . We provide some examples (such as polynomially decaying coefficients) to illustrate the gain in computational complexity of OOMP with respect to OMP.

-

•

OMP was shown to require less data than Lasso for support recovery (Zhang (2009)). We consider the streaming sparse regression algorithm (SSR) presented in Steinhardt et al. (2014), which is conceptually related to Lasso, as a benchmark to compare OOMP with -regularization type algorithms. We prove that when , OOMP outperforms SSR in terms of computational complexity.

Organization

In section 2, we present high level ideas and key properties which underpin greedy feature selection principles such as the Orthogonal Matching Pursuit algorithm (in the batch as well as in the online setting). We then extend this idea and design a general Online OMP procedure which is built using two black-box procedures (namely Optim and Try-Select) in Section 3. Then, we instantiate this general procedure using Algorithms 5 for Optim and 6 for Try-Select in Section 4. Finally, we state theoretical guarantees about the output of the presented algorithm and provide a control on its runtime complexity. The last section presents simulations using synthetic data.

1.2 Notations used

Throughout the paper, we use the notation . We denote by the total input space dimension (total number of features), and denotes the cardinality of the set of features to be recovered. For a vector and , we denote the coordinate of corresponding to the -th element of ranked in increasing order, and the vector of such that . Similarly, for a matrix we denote the matrix in obtained by restricting the matrix to the lines and columns with indices in . For a random vector , a random variable and we denote the vector in defined by . We denote the covariance matrix of . For let us denote the (population) squared risk function.

The prefix S refers to results presented in the supplementary material.

2 Batch OMP and oracle version

We start with recalling the standard batch OMP (Algorithm 1) for reference. Then we will introduce an “oracle” version when the data is random, which will serve as a guide for constructing the online algorithm.

2.1 Batch OMP

Given a batch measurement matrix and a response vector , at each iteration, OMP picks a variable that has the highest empirical correlation (in absolute value) with the ordinary linear least squares regression residue of the response variable with respect to features selected in the previous iterations. The algorithm stops when the maximum correlation is below a given threshold .

Each iteration of Algorithm 1 comprises a selection procedure, where one selects a feature based on its correlation with the current residuals, and an optimization procedure, in this case the ordinary least squares, where one optimizes the squared loss function over the space spanned by the set of selected features, and determines the new residuals for the next iteration.

2.2 Oracle OMP

To understand why OMP works, we consider the setting where the data is random and present an “oracle” (or population) version of OMP in order to give an insight about the core principle of its selection strategy, which we will adapt to the streaming setting. Throughout this work we assume the following on the generating distribution of feature vector and noise:

Assumption 1.

, , and the noise variable satisfies .

Let us introduce the following classical assumption in support recovery literature, which appears in Tropp (2004); Zhao and Yu (2006) and Zhang (2009) as the irrepresentable condition (IC). Consider a subset and denote

Assumption 2 (Irrepresentable condition, IC).

For all such that ,

Remark: The assumption is often used for exact support recovery, it was shown in Zhang (2009) that it is a necessary condition for the consistency of batch OMP feature selection.

Consider for a subset :

We define the covariance between the oracle residuals with each feature as:

| (1) |

The selection criterion used in oracle OMP relies on the quantities , thanks to the following lemma:

Algorithm 2 presents the resulting procedure, called Oracle version of OMP. In order to ease notations will use instead of in the remainder of this paper.

Remarks:

A similar result was used in Zhang (2009)

for the case of fixed design with random noise, where it was shown that either the empirical counterparts of are small, or they satisfy an inequality analogous to (2).

The right-hand side of (2) can be written as , since for all .

This lemma shows in particular that under Assumptions 1-2, if and , then . Hence, unless , picking the feature with the largest population correlation guarantees that this feature belongs to .

In the oracle setting, the algorithm stops as soon as , since Lemma 2.1

guarantees that then. In the batch setting with a finite amount of available data, the algorihm stops

when the maximum empirical correlation is too small and and cannot guarantee due to

estimation error. The threshold for stopping then depends on estimation error, hence on , see Zhang (2009).

3 Online OMP

3.1 Settings

In a computation-resources-constrained setting, one aims at using the least possible queries of data points and features in order to gain in computational and memory efficiency. For a data point , define by: and .

In this paper, we focus on the the streaming data setting were one-pass over data is performed, as summarized above:

The algorithm queries quantities through: query-new, which takes as input and outputs the partial observation of a fresh data point independent from all previously queried quantities. One call to query-new has a time complexity of .

In what follows, we will split algorithms into subroutines and assume that the input of each subroutine only depends on the result of past queries. This ensures that all the new data accessed by a subroutine can be considered as i.i.d. conditionally to its input. More formally, let us denote by the -algebra generated by all queried quantities up to the query-new query, and let be the (possibly random) number of queries made before the call to the current subroutine. Mathematically, is a stopping time; and, conditional to the next calls to query-new produce an i.i.d. sequence of (possibly partially observed) data points. We always assume that the input to each subroutine is -measurable. Below we will analyse each subroutine for a fixed input and derive probabilities with respect to the queried (i.i.d.) data; in the global flow of the algorithm, under the above assumption the same probabilistic bounds will hold conditional to .

3.2 Algorithm

Online OMP (Algorithm 3) selects variables sequentially. In its general form, Algorithm 4 (Select) consists of two sub-routines: Optim and Try-Select. The first provides an approximation of the regression coefficients for features in . The latter is an approximate best arm identification strategy which uses the output of Optim and queries data points in order to try to select feature , such that is large enough (Lemma 2.1 shows that such a feature is in ). We now describe how Optim and Try-Select operate:

Optim sub-routine:

is assumed to be a black-box optimization procedure such that for any fixed subset , positive number and , queries fresh data points through query-new and outputs an approximation for . We say that Optim satisfies the optimization confidence property if

| (3) |

where the probability is with respect respect to the data queried during the procedure, for any fixed input .

Try-Select sub-routine:

Given a set of selected features , an (approximate) regression coefficients vector and a confidence bound (on ), queries fresh data points to approximate defined by (1) for and either returns Success=False, or Success=True along with a set of new selected features.

We say that Try-Select satisfies the selection property if for any (fixed) input , it holds for the (random) output :

| (4) |

where the probability is with respect to all data queries made by Try-Select for fixed input. This implies in particular that with probability , by Lemma 2.1 (and in particular, with the convention , the probability of returning when is less than ).

If Try-Select returns , this suggests that the bound is not tight enough, i.e. that the prescribed precision for the optimization part is insufficient to find a feature with the guarantee (4) holding with the required probability. In this case, using the doubling trick principle, Select is called recursively with the input . Algorithm 4 presents the general form of the procedure Select.

If the cardinality is not known in advance, there is no stopping criterion and the procedure is run indefinitely. We assume that Online OMP will be interrupted externally by the user based on some arbitrary criterion, for example a limit on total computation time or other resource. In this case the current set of selected features is returned. The next lemma ensures that at any interruption time, it is guaranteed with high probability that .

Lemma 3.1.

Suppose that Assumptions 2 and 1 hold. Consider Algorithm 3 with the procedure Select given in Algorithm 4, assume that Optim satisfies the optimization confidence property (3) and that Try-Select satisfies the selection property (4). Then when OOMP() (Algorithm 3) is terminated, the variable satisfies with probability at least : .

Remark: The above result only guarantees that the recovered features belong to the true support. We will see later in Lemma 5.1 that for the instantiations of Try-Select and Optim considered in the next section, unless the support is completely recovered, the procedure Select finishes in finite time. Together with the previous lemma, this guarantees that the support will be recovered in finite time with high probability, at which point Select will enter an infinite loop of recursive calls until interruption. In Section 5, we will derive quantitative bounds on the complexity for recovering the full support.

About the stopping rule: OOMP has access to a virtually infinite stream of data points, so unless it is halted externally by the user, the algorithm can (in principle) continue querying more data to search for potentially extremely small coefficients (in contrast to the batch setting where the amount of available data is limited). However it is possible, in every call of the procedure Try-Select, to communicate to the user an upper bound on the maximal magnitude of the remaining coefficients of variables in (as shown in Section F). Therefore, the user can halt the procedure whenever that bound is small enough (alternatively, a threshold can be passed as an input to the algorithm and a corresponding stopping rule can be derived). We advocate an agnostic point of view where the user can decide for themselves when to halt the algorithm (based on the information on the magnitude of the remaining coefficients, but also possibly on limitations of the size of available data or computation time). Our recovery result guarantees that stopping at any time, the set of selected variables is (with high probability) a subset of .

4 Instantiation of the Optimization procedure and Selection Strategy

In this section we provide an instantiation of Try-Select and Optim procedures.

4.1 Assumptions

In addition to the Irrepresentable Condition (IC) (Assumption 2 ) we will make an assumption of Restricted Isometry Property (RIP) Tropp (2004); Zhang (2009); Wainwright (2009) for the distribution of . Denote and the lowest and largest eigenvalue of respectively.

Assumption 3.

[RIP] For all such that , it holds

We also make the following assumption:

Assumption 4.

Assume that and (a.s.).

4.2 Instantiation of Optim and Try-Select

Recall that one call of the procedure Select results in successive calls of Optim and Try-Select until (at least) a feature is selected. Moreover, the quantities queried in a sub-routine call (either Try-Select or Optim) are independent from quantities queried during the execution of previous functions.

Optimization procedure:

We opted for the averaged stochastic gradient descent (Algorithm 5). High probability bounds on the output of this procedure were given in Harvey et al. (2019b). We use this finding to build an optimization procedure satisfying the optimization confidence property (3) for an input .

Proposition 4.1.

Try-Select Strategy:

Different approximate best arm identification strategies were developed in the literature. In this work, we opt for a LUCB-type strategy were we use some ideas from Mason et al. (2020). We approximate by (i) replacing by an approximation assumed to satisfy the condition ; (ii) replacing the expectation by an empirical counterpart using queried quantities. Given an i.i.d sequence , we define and for , using written in matrix and vector form as , by:

Note that represents a thresholded version of the empirical variance . Proposition 4.2 gives a concentration inequality for , using empirical Bernstein bounds maurer2009empirical. For and , define and:

| (5) |

Proposition 4.2.

Proposition 4.2 entails the following: conditionally to , for all , with probability at least : for all , the condition implies

| (7) |

Provided inequality (7) holds true, and let , then, if satisfies the following condition:

| (8) |

then it holds that (see Lemma G.1 for a proof). Thus, in view of Proposition 4.2, under the above conditions, an algorithm selecting features satisfying (8) satisfies the selection property.

Using this observation, we build Algorithm 6 as follows: the procedure repeatedly queries fresh data points and updates the quantities simultaneously for all . After each iteration, we pick and we eliminate features for which we are certain that (i.e suboptimal features) with high probability through the test:

Moreover, we select features satisfying the condition (8). The procedure halts when the condition:

is no longer satisfied. The algorithm then returns the set of selected features . Lemma 5.1 shows that unless the support is completely recovered, and the procedure halts in finite time almost surely. A concise version of Try-Select is given in Algorithm 6 (the detailed version is in Algorithm 8).

5 Theoretical Guarantees and Computational Complexity Analysis

Consider one call of , for a fixed . Lemma 5.1 below shows that, unless the support of is totally recovered, the procedure halts in finite time and updates with a non-empty set of features.

Lemma 5.1.

Suppose Assumptions 1,2,3 and 4 hold. Consider one call of where Try-Select is given by Algorithm 6, and Optim is given by Algorithm 5. Denote by the stopping time where updates with the set of selected features (i.e the subroutine Try-Select returns and ), then :

If : .

If : .

Let be a fixed subset and denote . Recall that running results in executing Optim and Try-Select alternatively (see Algorithm 4). Let us denote by the cumulative computational complexity of Optim when running and by the cumulative computational complexity of Try-Select when running .

Theorem 5.2.

Suppose Assumptions 1, 2, 3 and 4 hold. Consider the procedure Select given by Algorithm 4, Try-Select given by Algorithm 6, and Optim as in Algorithm 5. Assume that and denote . Then selects a non-empty set of additional features such that:

Moreover, the computational complexity of subroutines Optim and Try-Select satisfy with probability at least :

where ; ; and is a constant depending only on and .

Theorem 5.2 provides high probability bounds on the computational complexity for a call to the procedure Select. A crucial point is that the complexity of the -th step depends on the largest correlation over the remaining (yet unselected) features, which in turn can be related to the average of the corresponding coefficients of (see Lemma J.1). By contrast, due to the batch nature of OMP, its complexity is driven by the minimum coefficient of , which determines the minimum amount of needed data for full recovery.

Let us introduce the following notation: let be the coefficients of ordered in decreasing sequence of magnitude. Let denote the average of the square of the smallest non-zero coefficients of : .

Corollary 5.3.

Under the same assumptions as theorem 5.2. The computational complexity of subroutines Optim and Try-Select satisfy with probability at least :

where is a constant depending only on , and .

We use bounds of corollary 5.3 to compare the computational complexity of OOMP with the computational complexity of OMP using the sample size prescribed by Zhang (2009) for full support recovery. Then, we compare OOMP with the SSR algorithm presented in Steinhardt et al. (2014) for streaming sparse regression, as a Lasso-type procedure. We use Theorem 8.2 in Steinhardt et al. (2014) to derive a sufficient sample size to achieve full support recovery.

We denote by the total runtime necessary for OOMP in order to recover the support completely, and denote by and the corresponding quantities for OMP and SSR respectively.

Corollary 5.4.

Under the same assumptions as theorem 5.2. If , we have with probability at least :

where is a constant depending only on and .

Recall that we have . Hence: , with equality only if all the square of the coefficients are equal. The SSR complexity bound have and additional factor , the same factor appears when comparing the sample size used by OMP for support recovery in Zhang (2009), with the corresponding quantity for Lasso in Zhao and Yu (2006): . Since our objective is support recovery, we will focus on the comparison between OOMP and OMP in the remainder of this paper.

In order to illustrate the advantage of OOMP over OMP, we consider the specific situation where the coefficients of decay polynomially as: , for and for ; with and we assume that . Then we have, with probability at least :

| (9) |

where is a constant depending only on and . See section K for a proof of the results above. Thus, in a typical scenario of coefficient decay (), OOMP reduces the complexity of OMP by a large factor (observe that the worst case in this scenario is , i.e. when all coefficients all are of the same order, which is not the typical case in practice).

6 Simulations

In this section, we aim at comparing the computational complexities of OOMP and OMP. We denote the sample size prescribed by- Zhang (2011) (recalled as Theorem K.2) to fully recover the support using OMP. We consider as a proxy for the computational complexity of OMP. For OOMP, we use Lemma I.4 and evaluate as a function of the quantity of data points queried.

From a practical point of view, the number of iterations theoretically prescribed in the optimization procedure (the number in Algorithm 5), and coming from Harvey et al. (2019b) is very pessimistic, due to the large numerical constant up to which the confidence bounds of the averaged stochastic gradient descent were developed. Taking this theoretical prescription to the letter resulted in the Optim step demanding an inordinate amount of data compared to Try-Select, while we expect the latter step to carry the larger part of the complexity burden due to the influence of the dimension . For this reason, in our simulation we opted to significantly reduce this numerical constant, while ascertaining (since we know the ground truth) that the optimization confidence property (3) was still satisfied in practice in all simulations.

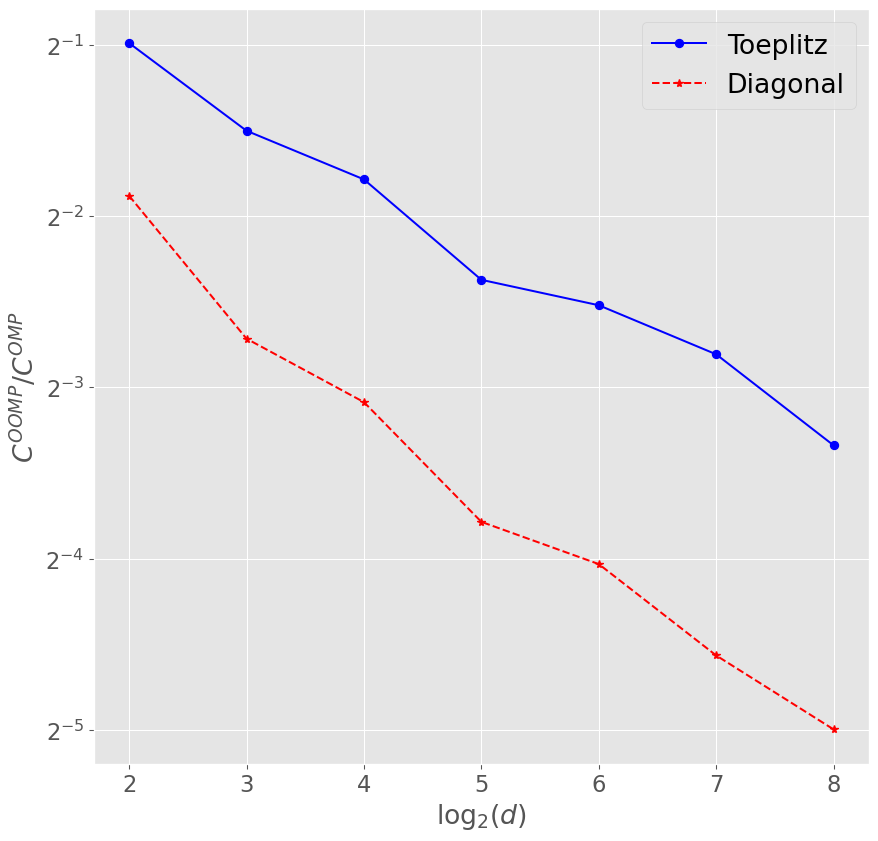

We generate samples with each coordinate of distributed as with and . We pick to be a sparse vector with non zero coordinates and , where . We consider the case where the coefficients of decay linearly: for and if . We consider two scenarios for the structure of the correlation matrix : the orthogonal design and the power decay Toeplitz design, with parameter :

We run OOMP for , we average the number of queried quantities over 20 runs and plot the ratio in the logarithmic scale with base 2 as a function of (Figure 1). We set . In all our simulation runs, the support was correctly recovered. The results reported in Figure 1 show a significant reduction of the complexity between OOMP and OMP.

References

- Blumensath and Davies [2008] Thomas Blumensath and Mike E Davies. Gradient pursuits. IEEE Transactions on Signal Processing, 56(6):2370–2382, 2008.

- Combettes and Pokutta [2019] Cyrille Combettes and Sebastian Pokutta. Blended matching pursuit. In Advances in Neural Information Processing Systems, pages 2042–2052, 2019.

- Harvey et al. [2019a] Nicholas JA Harvey, Christopher Liaw, Yaniv Plan, and Sikander Randhawa. Tight analyses for non-smooth stochastic gradient descent. In Conference on Learning Theory, pages 1579–1613. PMLR, 2019a.

- Harvey et al. [2019b] Nicholas JA Harvey, Christopher Liaw, and Sikander Randhawa. Simple and optimal high-probability bounds for strongly-convex stochastic gradient descent. arXiv preprint arXiv:1909.00843, 2019b.

- Mallat and Zhang [1993] Stéphane G Mallat and Zhifeng Zhang. Matching pursuits with time-frequency dictionaries. IEEE Transactions on signal processing, 41(12):3397–3415, 1993.

- Mason et al. [2020] Blake Mason, Lalit Jain, Ardhendu Tripathy, and Robert Nowak. Finding all -good arms in stochastic bandits. Advances in Neural Information Processing Systems, 33, 2020.

- Maurer and Pontil [2009] Andreas Maurer and Massimiliano Pontil. Empirical bernstein bounds and sample-variance penalization. In COLT 2009 - The 22nd Conference on Learning Theory, Montreal, Quebec, Canada, June 18-21, 2009, 2009. URL http://www.cs.mcgill.ca/%7Ecolt2009/papers/012.pdf#page=1.

- Steinhardt et al. [2014] Jacob Steinhardt, Stefan Wager, and Percy Liang. The statistics of streaming sparse regression. arXiv preprint arXiv:1412.4182, 2014.

- Tibshirani [1996] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58(1):267–288, 1996.

- Tropp [2004] Joel A Tropp. Greed is good: Algorithmic results for sparse approximation. IEEE Transactions on Information theory, 50(10):2231–2242, 2004.

- Wainwright [2009] Martin J Wainwright. Sharp thresholds for high-dimensional and noisy sparsity recovery using -constrained quadratic programming (lasso). IEEE transactions on information theory, 55(5):2183–2202, 2009.

- Zhang [2009] Tong Zhang. On the consistency of feature selection using greedy least squares regression. Journal of Machine Learning Research, 10(Mar):555–568, 2009.

- Zhang [2011] Tong Zhang. Sparse recovery with orthogonal matching pursuit under rip. IEEE Transactions on Information Theory, 57(9):6215–6221, 2011.

- Zhao and Yu [2006] Peng Zhao and Bin Yu. On model selection consistency of lasso. Journal of Machine learning research, 7(Nov):2541–2563, 2006.

Appendix A Proof of Lemma 2.1

Let us fix , recall that ; at first we only use the fact that the support of is a subset of . We have, if :

(The above remains true for with the convention ). Recall that , hence the support of is included in . Moreover by definition of , its support is in . Therefore, we have:

Let , and assume (the case is trivial). By definition of , we have for any , using Assumption 2 and the previous display:

We now use the actual definition of , namely , with . Since , we must have for all . We conclude that (including in the case where the latter right-hand side is 0 by convention), yielding the desired conclusion in conjunction with the last display.

Appendix B Technical Results

In this section we collect some technical results we will need for the proofs below. Recall that we assume the exact linear model:

with . In the result to come we restrict our attention to vectors having support included in for a fixed and denote . Consequently we can with some abuse of notation assume that the ambient dimension is reduced to (i.e , ); let us denote by the loss function defined by: , the gradient function defined by and for a sample define: . Denote by the closed ball centred at the origin with radius in .

Lemma B.1.

Proof.

Recall that from Assumption 3, then the eigenvalues of the matrix belong to .

-

1.

Since , and , we have for any :

By definition of , it holds , together with the above it gives:

In particular for , we have: . By the triangle inequality, for an arbitrary :

-

2.

Let , we have:

where we used: , and the assumptions , .

-

3.

Let , we have:

using the estimate of the previous point.

-

4.

Recall that is twice differentiable and its Hessian is given by , therefore is -strongly convex.

∎

Appendix C Proof of Lemma 3.1

Let us start by restating Lemma 3.1.

Lemma C.1.

Suppose that Assumptions 2 and 1 hold. Consider Algorithm 3 with the procedure Select given in Algorithm 4, assume that Optim satisfies the optimization confidence property and that Try-Select satisfies the selection property. Then when the OOMP() (Algorithm 3) is terminated, the variable satisfies with probability at least : .

Proof.

First consider an idealized setting where the algorithm runs indefinitely. Let denote the set of selected features at the -th iteration of the main while loop of Algorithm 3. It can happen that the call to Select never terminates (this is actually the expected behaviour if all relevant features have been already discovered), so if denotes the (random) last terminating iteration, we formally define if (this is of course irrelevant in practice but is just needed to always have a formally well defined for all integers ). Denoting , we see that with this definition, for any integer :

The event implies that all iterations including the one have terminated. Furthermore, the th selection iteration then consisted in calling repeatedly the Try-Select with allowed error probability at the -th call, until it returned Success=true (indicating termination of the -th main selection iteration). Let us denote the event “the -th call to Optim during the -th selection iteration, if it took place, returned such that the optimization confidence property (3) holds”, and the event “the -th call to Try-Select during the -th selection iteration, if it took place, returned Success=true and a subset of features .” It holds by the optimization confidence property, and by the selection property, so we have

Now, the algorithm may be interrupted at a completely arbitrary time, and returns the last active set for some . We then have

∎

Appendix D Proof of Proposition 4.1

In this section we give high probability bounds on the output of the averaged stochastic gradient descent (ASGD, Algorithm 7). Theorem D.1 below is a slight modification of the main result in Harvey et al. [2019a], which consists in assuming that the error on the stochastic sub-gradients is bounded by a constant instead of . We denote by the projection operator on .

We use the same notations as in Section B, we assume with some abuse of notation that the ambient dimension is reduced to (i.e , ). We recall that we denote by the loss function defined by: , the gradient function defined by ; in addition we consider defined by , where are the output of the call of query-new during Algorithm 5. Denote by the closed ball centred at the origin with radius in .

Lemma B.1 shows that (under Assumptions 3-4), we have via the triangle inequality:

| (10) |

Where are the iterates of Algorithm 5. We denote by the upper bound in equation (10).

Theorem D.1.

The following corollary results by simply choosing large enough such that the optimization confidence property is satisfied by Algorithm 7.

Appendix E Proof of Proposition 4.2

E.1 Technical Results

The following result is a straightforward modification of the empirical Bernstein inequality from Maurer and Pontil [2009], which consists in assuming that the random variables belong to for a , instead of .

Lemma E.1.

Maurer and Pontil [2009] Let be i.i.d. random variables with values in and let . Then with probability at least we have:

where:

We are interested in applying the Lemma above to the quantities . Let be a queried sample, the following claim shows that the random variable for , where is the feature , satisfies the conditions of Lemma E.1.

Claim E.2.

Suppose Assumption 4 holds. Let be a sample, of support and such that . Fix and define . Then it holds almost surely:

Proof.

Using the Cauchy-Schwartz inequality, we have:

∎

Moreover, a straightforward calculation yields the result below.

Claim E.3.

Suppose Assumption 4 holds. Let be a sample, of support . Fix and define . Then it holds

Proof.

We have:

∎

E.2 Proof of Proposition 4.2

Consider an i.i.d sequence . Let and denote in matrix and vector form as: .

Let us first fix a set , a feature and a vector . Denote for all : , where is the feature of the sample . Recall that and . We have:

Let us denote , and . Since are i.i.d and belong to (Claim E.3, following from Assumption 3 and Lemma B.1 (i)), we have using Lemma E.1: for any , with probability at least :

| (11) |

Now we apply a union bound over the sample size and features , we obtain: with probability at least , bound (11) holds for all and . To conclude, we choose and we use the risk bound (3) to have: with probability at least :

Recall:

Using the fact that , combining with the above inequality we get the announced claim.

Appendix F Detailed algorithms for Try-Select

Algorithm 8 is a detailed version of Algorithm 6 (the shortened version in the main body of the paper).

On the upper bound of the mean of the non-recovered coefficients:

Appendix G Proof of the selection property

The proof that the proposed Algorithm 6 satisfies the selection property hinges on the following lemma:

Lemma G.1.

Let be fixed. Let be given. Assume there exists , and positive numbers are such that:

| (12) | ||||

| (13) | ||||

| (14) |

Then it holds .

Proof.

First assume . Let . We have:

In the case , we have that for all , Therefore the claimed conclusion holds. ∎

Appendix H Proof of Lemma 5.1

Lemma 5.1 shows that the procedure Select given in Algorithm 4, where Try-Select is given by Algorithm 6 in the Data Stream setting and Optim given by Algorithm 5, finishes in finite time if and with high probability doesn’t select any feature if .

We start by stating the two following technical claim.

Consider a set of i.i.d samples , recall the following notation:

| (15) | ||||

| (16) | ||||

| (17) | ||||

| (18) | ||||

| (19) | ||||

| (20) |

Proof of Lemma 5.1.

For the situation , the argument is a repetition of the proof of Lemma 3.1 (only considered at the particular selection iteration where ).

We now deal with the situation . We assume to be fixed, denote . As explained in the main body of the paper, the argument to follow, for fixed , can be transposed directly as a reasoning conditional to , being the number of data used before starting the -th selection step, with a random assumed to be -measurable.

Let (a deterministic quantity). Proceeding by proof via contradiction, suppose that with positive probability, during the execution of Select , Try-Select either never finishes, or always returns . Assume for the rest of the argument that this event is satisfied. We can rule out the fact Try-Select never stops, since there is a stopping condition of the type , which is eventually met since during Try-Select, so that the left-hand side goes to zero and the right-hand-side constant is positive. Therefore, for all representing the number of recursive calls, Try-Select returns , after having queried a (random) number of data points, satisfying (see Algorithms 4 and 6) that

| (21) |

This implies that for some factor , and in particular that .

Now Claim E.2 shows that defined by (18) is bounded almost surely by a constant independent of . Hence, from the definition (20):

We use the second inequality of (21) to conclude that . By the contradiction hypothesis we assumed that this happens on an event of positive probability. On the other hand, since the variables are averages of i.i.d. variables , and is a stopping time that is lower bounded by , Lemma H.2 implies that the variance of goes to 0 as grows, hence converges in probability to . Finally, we have , hence , so that converges in probability to as well. Therefore , which contradicts the fact that (see Claim H.1).

We used the following result:

Lemma H.2.

Let be a martingale with respect to the filtration and be a stopping time. Let , for (putting ). Assume for all , and that a.s. Then:

Proof.

Assume without loss of generality that . We have, using the fact that the event is -measurable since is a stopping time:

∎

Finally, the set of selected features is not empty since the condition: implies that the condition: is satisfied. Therefore, contains at least .

Appendix I Proof of Theorem 5.2

Theorem 5.2 states that Select is guaranteed to select a feature in with high probability if the support is not totally recovered. This part is directly implied by Lemma 3.1 and the fact that the proposed Optim and Try-Select subroutines satisfy the optimization confidence property and the selection property, respectively, as established previously.

More importantly, the theorem gives an upper bound on the cumulative computational complexity of the sub-routines Try-Select and Optim.

In what follows, following the same approach as in the rest of the paper, we concentrate on a specific selection iteration (call to Select) and consider to be fixed. We start by stating some technical lemmas useful for the proof of this theorem.

I.1 Technical Result

The following concentration inequality is a simple modification of the inequality presented in Maurer and Pontil [2009] Theorem 10, which consists in assuming that variables defined below belong to instead of .

Lemma I.1.

Consider a fixed . Suppose Assumption 4 holds with and being centred random variables. Consider a set of i.i.d. data points . Let such that and .

Define for a sample : , where is the feature of . Finally we define as:

| (22) |

We have in the samples :

where .

We refer to Maurer and Pontil [2009] Theorem 10, for a proof; recall that Claim E.2 shows that almost surely.

Claim I.2.

Let . Under the same assumptions as in Lemma I.1, we have:

where the expectation is taken with respect to the sample .

Proof.

∎

Claim I.3.

Let and such that:

| (24) |

Then:

Proof.

Inequality (24) implies

and further

since it can be easily checked that for all . Solving and plugging back into the previous display leads to the claim. ∎

I.2 Proof of Theorem 5.2

It has already been established based on Lemma 3.1 that under Assumptions 1,2, 3 and 4, the set of features selected by belongs to with high probability, and based on Lemma 5.1 that .We therefore now focus on the control of the computational complexity.

Let be a fixed subset and denote . Recall that running results in executing Optim and Try-Select alternatively until a condition is verified, implying that at least one feature was selected (see Algorithm 4). We use the same notations as in Section 5 to denote the computational complexities of Select, Try-Select and Optim.

Lemma 5.1 shows that, unless interrupted, terminates in finite time. Therefore, the number of calls to Optim and Try-Select is finite. Let denote this (random) number.

Let us adopt the following additional notations: For , let denote the number of samples queried during the execution of Optim. Let, for , denote the sample size used to compute in the execution of Try-Select.

The following lemma provides upper bounds for and .

Lemma I.4.

Proof.

-

1.

Optim was instantiated using the averaged stochastic gradient descent (Algorithm 5), hence the computational complexity of the call of Optim is upper bounded by (up to a numerical constant). Therefore:

-

2.

Consider the procedure Try-Select given in Algorithm 6. In one iteration, calling costs . Once a sample is obtained, computing the residual costs and updating and for all costs . Finally, selecting the feature with the maximum costs . The cost of the last two tests is . Let denote the active set of features for the -th iteration of Try-Select during its -th call. We therefore have

∎

In order to provide a control on the computational complexity of , we need to derive a control on the (random) quantities , and for and . In the remainder of this proof, will refer to a constant depending only on and . The value of may change from line to line.

Recall the definition:

| (25) |

where and is given by (22). Since is a data-dependent function, the claim below provides a deterministic upper bound.

Claim I.5.

Suppose Assumption 4 holds with and being centered random variables. Let and define:

| (26) |

Then, for all , with probability at least we have: , :

Proof.

Let us denote . At each iteration of OOMP (Algorithm 3), the procedure Select is called with inputs . Then Select is run following Algorithm 4 recursively until a condition, implying that at least an additional feature was selected, is verified. Thus, the inputs of the call to Select are .

Computational complexity bounds:

We define the following key quantities: for , for , let:

| (27) |

and

| (28) |

where .

The following argument proves the existence of : By assumption , Claim H.1 shows that , thus as well. Definition 26 shows that is strictly decreasing and converges to when , which guarantees that exists.

The technical result below gives an upper bound for :

Lemma I.6.

where depends only on , and , and .

Proof.

For the rest of the proof, we upper bound the complexities of Try-Select and Optim using . The lemma below relates the quantities and .

Lemma I.7.

Under the assumptions of Theorem 5.2:

Proof.

Let us fix and . We consider the iteration during the -th call of Try-Select, and let denote the active set of features for this iteration.

Let . We have by design of Algorithm 6 (since ):

hence:

We therefore have (by definition of ):

| (30) |

As in the proof of Lemma 3.1, let us denote the event “the -th call to Optim during the -th selection iteration, if it took place, returned such that (3) holds” and recall that the optimization confidence property guarantees . Provided this control holds, recall that Proposition 4.2 shows that

| (31) |

Let us denote by the event:

| (32) |

Recall that at iteration , we must have:

thus (31) implies

| (33) |

Using (30), we have:

| (34) |

Using Claim I.5, it holds:

| (35) |

therefore, (34) gives:

| (36) |

Let . Suppose that event is true. Let us show that . In fact, if , we have by design of the procedure Try-Select: and such that:

By definition of event in (32). We conclude that:

which contradicts the definition of . We therefore have: if is true then .

Moreover, by design of Try-Select:

Therefore:

Since event is true, we upper bound the quantity : , and lower bound the quantity: . We obtain:

As a conclusion, we have:

which leads to:

Finally, we use (35) to upper bound and using :

| (37) |

We obtain, using (37) and (36):

| (38) |

furthermore by definition of (see (28)):

| (39) |

Denoting the event appearing above, we use together with a union bound over to get

The result follows from the fact that the function is decreasing for all . ∎

In order to get an upper bound for the computational complexity of Select, we now develop a high probability bound on (the total number of calls of Try-Select and Optim during one call of ).

Lemma I.8.

Suppose . Under the assumptions of Theorem 5.2, satisfies the following inequality:

where only depends on .

Proof.

By definition of , the procedure Try-Select returns in its call number . Then (see Algorithm 6) such that:

Using Definition 25 for conf, we deduce:

Recall that by definition of , it holds

therefore

and finally

for an absolute numerical constant.

Using Lemma I.7 along with the fact that the function is non-decreasing for , we have:

Recall from (29) that there is a numerical constant such that:

Finally, it is elementary to check that :

Hence, taking above, we get . As a conclusion, there exists a constant depending only on and such that:

∎

Recall that we have: (Lemma I.4). Therefore, using Lemmas I.6, I.7 and I.8 above, we have with probability at least :

In particular, Lemma I.8 shows that:

Hence, with probability at least :

We conclude after some elementary bounding that, with probability at least :

where is a constant depending only on and .

Appendix J Lower bound on the scores :

Let us denote the reordered coefficients of : . Lemma J.1 provides a lower bound for .

In this section we prove Lemma J.1, we begin by presenting the following technical lemmas adapted from Zhang [2009] to fit the random design.

Claim J.2 is a direct consequence of Assumption 3 stating that the eigenvalues of are lower bounded by and upper bounded by , and the observation that are the diagonal terms of .

Lemma J.3.

Let and be real valued bounded and centered random variables, such that . We have:

Proof.

The proof follows from simple algebra, the minimum is attained for . ∎

Lemma J.4.

Proof.

Let , we have:

Recall that optimality of implies that for all : . Hence:

Therefore:

Optimizing over we obtain:

Observe that: . Moreover, . We plug in this inequality into the above and obtain the announced conclusion. ∎

Appendix K Computational Complexity Comparisons

K.1 Proof of Corollary 5.3:

Suppose Assumptions 1, 2, 3 and 4 hold. Consider the procedure Select given by Algorithm 4, Try-Select given by Algorithm 6, and Optim as in Algorithm 5. Assume that and denote . Using the result of theorem 5.2 we have with probability at least :

where , and is a constant depending on and (for which the value may vary from line to line).

We plug-in the inequality of lemma J.1 and obtain:

Hence, using the fact that and the definition of :

The following claim concludes the proof:

Claim K.1.

Under the assumptions of theorem 5.2:

Proof.

We have by definition of :

∎

K.2 Computational complexity of the Orthogonal Matching Pursuit

We consider OMP (Algorithm 1) as a benchmark and show that OOMP is more efficient in time complexity. OMP was initially derived under the fixed design setting presented below:

Let an data matrix and a response vector generated according to the sparse model:

Where is a zero mean random noise vector and . Define the following quantities:

and let be the least eigenvalue of the empirical covariance matrix .

OMP theoretical guarantees

Assumption 5.

Assume that:

-

•

and .

-

•

, for are i.i.d random variables bounded by .

OMP computational complexity:

We derive the computational complexity of OMP. Consider one iteration of Algorithm 1 and denote . We assimilate the command:

| (43) |

to Try-Select and denote its computational complexity. Moreover, we assimilate the command:

| (44) |

to Optim and denote its computational complexity.We assume the OMP is run with prescribed by Theorem K.2 for exact support recovery. We introduce the following additional notation: if there exists numerical constants and such that: and .

Lemma K.3.

Proof.

Hence, the computational complexity for full support recovery using OMP satisfies:

| (45) |

K.3 SSR computational complexity

SSR (Streaming Sparse Regression) is an online procedure guaranteed to perform well under similar conditions to the Lasso Steinhardt et al. [2014]. Theoretical guarantees show that if the number of iterations is large enough the support recovery is achieved with high probability.

Theorem 8.2 in Steinhardt et al. [2014] states that, the output vector satisfies with probability at least , and:

| (46) |

where we used the bound . Hence, a sufficient condition to achieve the full support recovery is : . Using (46) leads to the following bound on the number of iterations to recover all the support of :

One iteration of Algorithm 2 in Steinhardt et al. [2014] has a computational complexity of . Hence, the total computational complexity for full support recovery satisfies:

| (47) |

K.4 Proof of Corollary 5.4

Assuming that , we have for every : . Hence, using corollary 5.3, we have:

| (48) |

Recall that:

We conclude that:

where is a constant depending only on and .

K.5 A specific scenario: Polynomially decaying coefficients

We consider the case where the coefficients of are given by

| (52) |

with . We omit the superscript to ease notations, in the remainder of this section, all the inequalities and equalities are up to factors depending only only on and .

The following lemma provides a bound on the computational complexity of OOMP, OMP and SSR.

Lemma K.4.

Proof.

Recall that .

If :

If :

which gives the result.

∎

Using the lemma above, we conclude that, if :