Continuous-Time Risk Contribution of the Terminal Variance and its Related Risk Budgeting Problem

Abstract

To achieve robustness of risk across different assets, risk parity investing rules, a particular state of risk contributions, have grown in popularity over the previous few decades. To generalize the concept of risk contribution from the single-period case to the continuous-time case, we characterize the terminal variance’s marginal risk contribution as a process through the Gâteaux differential and Doléans measure. Meanwhile, the risk contributions we extend here have the aggregation property. Total risk can be represented as the aggregation of individual risk contributions among different assets and . Subsequently, as an inverse target — allocating risk, the risk budgeting problem of how to obtain policies whose risk contributions coincide with pre-given risk budgets in the continuous-time case is also explored in this paper. These risk-budgeted policies are related to stochastic convex optimizations parametrized by associated risk budgets. We also give the economic interpretations on this optimization objective. On the application side, we put three examples to state the connections with other strategies regarding risk contribution/budgeting.

1 Background

Since the first ten years of this century, risk budgeting models have gotten much attention from academics and practitioners. These portfolio construction methods do not require expected returns as inputs and calculate asset positions by appointing risk contributions under a predefined risk measure.

Just as Pearson stated in [Pearson, 2002], risk budgeting acts as a

‘process of measuring and decomposing risk, using the measures in asset-allocation decisions, assigning portfolio managers risk budgets defined in terms of these measures, and using these risk budgets in monitoring the asset allocations and portfolio managers’.

Specifically, we need to explain the term risk contribution before considering the term budget. This concept implies how we decompose the total risk into individual ones in some manners. The contributions to risk can be classified into two types: risk contributions to the individual assets in the portfolio or specified risk factors. In the second type, the returns of assets are often expressed in a linear model by factors such as market, momentum and etc. However, this linear structure has significant limitations, and there is no definite conclusion as to which factors are recognized as effective. We are studying the first type in this paper, which focuses only on the assets. For a specific asset, the risk contribution is the quantity times the marginal growth of risk. The quantity is the weights or shares on this asset. The marginal growth of risk is calculated as the derivative of total risk with respect to the position of this asset. When the predefined risk measure is positive homogeneous, the total risk coincides with the aggregation of individual risk contributions. So we can use this tool, risk contribution, to calculate how much the asset contributes to the total risk. In this heuristic manner, people can construct a risk-budgeted portfolio in terms of risk, not weights, to avoid concentration on the risk. Among those budget-based models, risk parity is one of the most common cases, equalizing individual risk contributions. We will give a formal description of related concepts such as risk contribution in Section 2. The following example will be helpful to understand these concepts quickly.

Example 1.

Suppose there are assets with their -valued random returns and the positive definite covariance matrix is denoted as . We use to denote the weights on the assets, which describes how the total capital is allocated. To state the risk contribution of each asset, we set the standard error as the risk measure to quantify the total risk. The measure satisfies the Euler property

| (1) |

Then the marginal risk contribution of the -th assets is defined as and the risk contribution is defined as . Given a risk budget vector which represents the pre-determined relative risk level of the underlying assets, the -budgeted portfolio should satisfy for arbitrary . As a special case, the risk contribution of risk parity portfolio is equally distributed, namely for arbitrary . One can find the optimal solution through some algorithms to minimize the heuristic cost function

| (2) |

or some other similar functions.

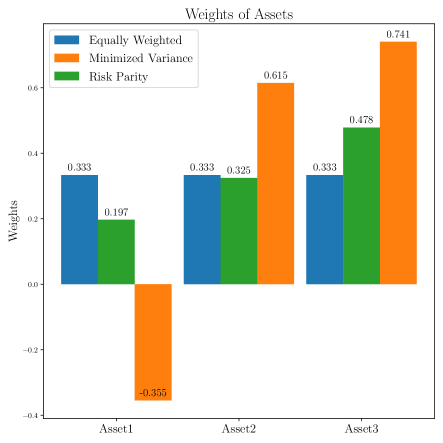

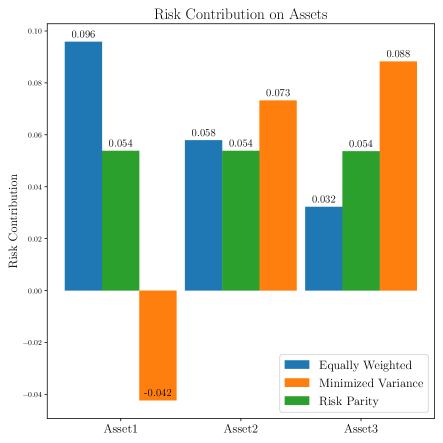

Here is a concrete calculation with the covariance matrix . Figure 1 gives the comparison on the weights and the risk contributions among equally weighted, risk parity, and minimized variance portfolios. It shows that the minimized variance portfolio is aggressive with a negative weight on the first asset and implies the concentration in terms of risk contribution on the latter two assets. However, because of the existence of correlation, the equally weighted strategy also shows the risk concentration on the first asset. Compared with the other two strategies, the risk parity strategy behaves more robust both on the weight term and the risk contribution term.

As a risk-based strategy, the idea of risk budgeting can date back to Markowitz’s Nobel-prize-winning result, which quantifies the risk and gives the optimal solution of the mean-variance tradeoff framework. Along with Markowitz’s pioneering work, Merton’s analytic answer to the efficient frontier [Merton, 1972] is regarded as the essential foundation for portfolio design in a single period. After this, kinds of literature on multi-period portfolio selections were dominated for years by the maximizing expected utility framework, and we recommend these works [Samuelson, 1975, Merton, 1992]. Similar to the expectation-utility framework, the continuous-time mean-variance problem was obtained by [Li and Ng, 2000, Zhou and Li, 2000] using the stochastic linear-quadratic framework with an embedding technique. These works are more about maximizing utility or balancing return and risk. Sensitivity analyses were performed [Best and Grauer, 1991a, Best and Grauer, 1991b] on mean-variance portfolio selections that were substantially quadratic programming, meaning a loss of robustness when meeting non-stable inputs. However, the minimization of the total risk always implies the concentration on weights. Based on the market features and underlying assets, [Fernholz, 2002] shows that portfolios with diversification can beat the market portfolio in the stochastic language. In light of policy constraints, one may seek a compromise between diversification and variance minimization objectives. -weighted, namely the equally weighted portfolios, can be considered an absolute diversification policy without knowledge on risk; and Markowitz’s global variance minimized portfolio based on its covariance matrix is verified to take concentrations on those low-correlation assets. Mixtures, such as portfolios with maximal diversification, equal risk contribution, and inverse-volatility weights, come between these two extremes. The term risk parity was coined by [Qian, 2005], and the analytical properties of risk parity portfolios were explored in [Maillard et al., 2010]. They showed that the long-only risk parity portfolio is unique and lies between the minimized variance and equally weighted portfolios. Risk parity and risk-budgeted portfolios are also widespread in practice. Bridgewater Associates were the first to launch a risk parity fund on the asset management side. Equal risk contributions indices are also available (EURO iSTOXX 50 Equal Risk, for example).

The reasons for using risk budgeting strategies are diverse. Paying more attention to the total risk, portfolio construction techniques based on decreasing risk often give results concentrating on low-risk assets. Consequently, the mean-variance framework of Markowitz is not robust when the inputs are unstable. Given this situation, people prefer to give regular constraints on the positions. The second reason is the low-risk anomaly. Empirical literature states that stocks with the lowest risks have higher returns than stocks with the sub-lowest risks. This phenomenon occurs in the cross-section and in the time axis. Risk parity strategies may be motivated through the low-risk anomaly. The last reason can be attributed to the information capacity. Forecasting the future returns is not easy, and no expectation of future returns is needed in the risk budgeting world. Equal distribution on risk can give true diversification and thus should prevent the portfolio from losing better than other portfolios.

As the result of single-period investments, the concept risk contribution acts as a tool to detect if the portfolio is concentrated in risk. Respectively, continuous-time investments should also have this tool to measure the concentration on their risk. Unlike the single-period case, the concept of risk contribution may depend not only on assets but also on the stochastic intervals, i.e., the subsets of . For example, the single-period case can not answer this question: how much does the -th asset contribute to the total risk when values in with ? Respectively, the risk budgets are supposed to be allocated over . In other words, the changes in the measurability of assets’ dynamics, risk contributions, and risk budgets are essential to risk contribution/budgeting problems, and these changes do not appear in the single-period case. We notice that the concentration occurs in the cross-section and on the time axis. We think continuous-time risk budgeted investments are attractive to catch the extra benefits from the low-risk anomaly phenomenon. As far as we know, there is no such technique to define the risk contribution in the continuous-time case. It is interesting to generalize (marginal) risk contribution in the framework of stochastic analysis.

Inspired by the work of [Zhou and Li, 2000], where the continuous-time mean-variance strategy is studied in a stochastic control framework, and that of [Maillard et al., 2010], where the single-period risk budgeting problem can be solved by a variance optimization with some constraints within the covariance matrix, we want to develop the risk budgeting theory in the continuous-time case. As a prerequisite, the concept of continuous-time (marginal) risk contribution should be adequately defined. As the echo of how single-period risk contribution/budgeting works, this paper addresses the following points:

-

•

(Defining Risk Contribution) Without the structure of terminal wealth in the form of a covariance matrix, how can the risk contribution of policies be quantified? Additionally, does the risk aggregation property hold in the continuous-time case in which the policy is no longer a constant?

-

•

(Posing Risk Budgeting) Assuming that risk contributions and budgets are stochastic processes, can we formulate and solve the inverse problem of how to align the desired policy with the pre-determined risk budget?

-

•

(Connecting) What is the relationship between continuous-time and single-period solutions?

Also, we put three examples to show how the risk contribution/budget is linked to some known results in the continuous-time case.

The remainder of this paper is structured as follows. In Section 2, we will give some necessary axiomatic introduction to these concepts appearing in Example 1. Then we use the Gâteaux derivative of the terminal variance to derive a continuous process and define it as the marginal risk contribution. Immediately afterward, the risk contribution was also appropriately defined. In Section 3, we provide a convex stochastic optimization problem similar to the result [Maillard et al., 2010] presented in the single-period case, and the optimal policy to the problem happens to match the pre-given risk budget process. In addition, we give some explanations for this optimization. Moreover, classic single-period solutions are interpreted here as the solutions to those optimizations associated with the projection of the original risk budget process onto the naive -algebra. We build a policy congruent with the work in [Moreira and Muir, 2017] using regularised risk-parity optimization in Subsection 4.1 to demonstrate how the risk budgeting strategy behaves on the time axis. Their volatility-timing strategy, motivated by the factor Sharpe ratio, reflects the robustness of the risk basket on the time axis and essentially is a risk parity strategy in our risk budgeting view. To illustrate, we will cover risk contributions, risk-parity budgeting, and naive projections for the SABR model as an example in Subsection 4.2. Coefficients in the SABR model setup can essentially influence the risk contribution of investment policies. The influence of the coefficients states the connection between risk contribution and options of the underlying assets. In Subsection 4.3, we will give the risk contribution of continuous-time mean-variance strategies admitted by [Zhou and Li, 2000] and the result shows that there are concentrations in terms of risk contribution for these mean-variance strategies. Finally, in Section 5, we conclude with a discussion of the enhancements from the classic case and suggest several potential limitations as open problems.

2 Characterize Risk Contribution

2.1 A Formal Revisiting of Single-Period Risk Contribution/Budgeting

This section extends the concept of risk contribution for the terminal variance to the continuous-time case, in which the risk contribution is characterized as a continuous process. In order to address fundamental questions regarding both the single-period case and the continuous-time case, it is imperative to have a prior and formal understanding of the tenets of risk contribution. To this goal, we address three concepts: risk measure, marginal risk contribution, and risk contribution.

Let be the risk measure of the random variable on the probability space , which is the position of the investment. Throughout this paper, we consider the variance, or standard deviation, as the risk measure. In order to be acceptable in terms of a risk allocation principle, we give the axiomatic definition of the deviation risk measure, of which standard deviation is a particular case.

Definition 2 (Deviation Risk Measure,[Rockafellar et al., 2006]).

A deviation risk measure is a functional satisfying:

-

D1

for all ;

-

D2

for ;

-

D3

for and ;

-

D4

for an arbitrary constant, and for any non-constant random variable.

Suppose that there are assets in the market with the -valued random vector acting as the value of those assets and with the shares -valued investors hold. Then we have the random variable as the associated investment outcoming. Hence we can talk about the sensitivity analysis of the risk measure. This idea is based on marginal analysis and was proposed by [Litterman, 1996]. Indeed, for a differentiable risk measure , the marginal growth with respect to the -th asset is calculated as and implies an infinitesimal property

| (3) |

If the risk measure is positive homogeneous, then the function is also positive homogeneous and implies the Euler homogeneity principle

| (4) |

[Kalkbrener, 2005] shows that this Euler allocation principle is the only risk allocation method in an axiom system for capital allocation. Realizing these things, we can show the definition of risk contribution.

Definition 3 (Risk Contribution/Budgeting - Single Period).

Let the function be a continuously differentiable risk measure(not necessary a deviation risk measure).

-

•

Marginal risk contribution of portfolio in a vector style is defined by

where the -th element is the marginal risk contribution on -th asset.

-

•

Risk contribution of portfolio in a vector style is333We denote as the -th element of the vector . With -valued and , vector is defined by .

of which the -th element is the risk contribution on the -th asset.

Particularly, a policy is called risk-parity if with notation for some . In other words, the risk contributions on these assets are equal

| (5) |

When exogenously given a budget , the risk budgeting problem aims to find a suitable policy satisfying

Obviously, from the above point of view, the variance does not meet those properties deviation risk measures. However, Euler’s aggregation principle, together with the marginal contribution, still holds and is similar to standard deviations. Standard deviation is a deviation risk measure, and we can see

and

The risk contribution of variance is the scaled one of the standard deviation measure with the coefficient and the proportion of -th varaince contribution to the standard deviation contribution is identical to that of -th asset

Euler’s principle is also valid for the variance with the scaled coefficient . In this sense, it is equivalent to considering the risk contribution of the variance. For convenience, we can set the marginal risk contribution of the variance as and will talk about the continuous-time risk contribution of the terminal variance in the following sections.

2.2 Technical Preliminaries

We will characterize the associated risk contribution and marginal risk contribution of the terminal variance acting as the risk measure. The marginal risk contribution of a given policy will be firstly derived in a signed measure form whom the integral of the policy with respect to is the terminal variance. Then the Radon-Nikodým derivative of this signed measure is proved to be a continuous process meaning that total risk is continuously aggregated. Some preliminary settings are listed below.

With the time horizon , we let be the random basis equipped with a filtration and is an -dim Brownian motion on this space. We also assume that is the natural filtration generated by the Brownian motion and completed by the collection of -null sets , i.e.,

with . The processes we discussed in this paper are assumed to be -adapted. We also denote the predictable -algebra and the stochastic integral. We use the notation for the space of random variables.

Assets

The value processes of assets are characterized as a sequence of continuous special semi-martingales in

to make sure that the value of assets admits a finite variance. Without the loss of generality, the dynamics of assets value are assumed to be in the following form

where the instantaneous diffusion is a multi-dim process , the -th row of . We shall denote the -valued process as the assets for short.

Policy/Control

The policy is assumed to be a -valued predictable process with where

For every , the random variable is the shares we buy at time , and process implies that we cannot afford to hold infinitely many shares in any case.

Investment Process

The Itô-type integral of the policy with respect to the assets is defined as the value of investment where

| (6) |

is the value of investment at time with its initial wealth . By the way, the investment is called a self-financing portfolio in addition if

| (7) |

for each . With and , it’s easy to check is in , and we can say that the investment is still variance-finite.

Terminal Variance as the Risk Measure

Here we consider the terminal variance of the portfolio as its risk measure where

It’s easy to check that is a convex functional. Moreover, the space ensures that the investment process has a second-order moment implying a finite terminal variance.

Definition 4 (Non-Degeneration).

The market is non-degenerate if we always have

for arbitrary policy .

With the slope mapping at the point in the direction , this non-degeneration condition above ensures that the functional is strictly convex.

2.3 Marginal Risk Measure

At the first of this subsection, we put , i.e., there is only one risky asset in our sight. The result of the -dim case can help us understand how risk contribution behaves on the time axis. As an application, volatility-managed portfolios in Subsection 4.1 can be derived in this risk contribution view. With the help of the differential technique in this subsection, the multi-dimensional result will not be lengthy when it meets the cross-section risk contributions of various assets.

By Itô’s formula, we can rewrite the terminal variance of our investment process and divide it into three parts,

For the (I) part, we give an operator

whose image is a random variable. We can also define the operator for the (II) and (III) parts respectively:

The images of these three operators are equipped with the -norm.

Lemma 5 (Gâteaux differential).

Under -norm, the Gâteaux differentials of and are

Proof.

With arbitrary and , we take the variation of . For (I) part, we have

by the linearity of stochastic integral. Let . Obviously, the linear operator satisfies

Hence the linear operator is the Gâteaux differential of . Considering that is associated with , we denote it by in the fashion of directional derivative.

Similarly, for the (II)part we have the convex variation of

and the Gâteaux differential of

As for part (III), we can get

And we take

Then we get

since

Finally the Gâteaux differential of at is . ∎

Definition 6 (Doléans measure, [Cohen and Elliott, 2015]).

Given a non-decreasing integrable process , there is a non-negative measure defined on as

for each set . The measure is the Doléans measure associated with the process .

We will propose a signed measure to ensure that the terminal risk is distributed appropriately on .

Theorem 7 (Marginal Risk Measure - -dim).

Given , the terminal variance of the investment can be represented as an integral

| (8) |

where . is called the marginal risk measure444Measure is actually induced by , therefore we use the notation . Without causing ambiguity, we prefer omitting . of at .

Moreover, in the non-degenerate market, the signed measure introduced by the mapping above is unique on the support .

Proof.

When we take the direction policy in the form of where is a -measurable set, the Gâteaux differentials in the Lemma 5 give us three set functions with the common domain

We want to show that are signed measures so that we can get the result on representation by integrating our policy with respect to the summation of these measures . For the measures , it is easy to check the following properties:

-

•

;

-

•

;

-

•

(Finite Additivity). For arbitrary disjoint , we have

And it is left us to seek the countably additivity property of .

For part, we should notice that

where is the part of finite variation in the canonical decomposition of . With the positive-negative decomposition of and , we can rewrite the first term

By Definition 6, is a combination of Doléans measures induced by four increasing process, hence a signed measure. And the decomposition of the second term(denoted by ) shows

Noticing that is a non-decreasing sequence for disjoint set sequence , we take , then is also a non-decreasing sequence and respectively non-decreasing . Applying monotone convergence theorem, we can get the countably additivity of . Consequently is a signed measure on .

As for , it can be considered the difference of two Doléans measures induced by two respected processes and since

Hence is a signed measure. Through the decomposition technique we treat with, we can see that

Then is a signed measure on . Finally we take , and the integral of with respect to shows us

If there is an another signed measure also representing the integral above, then we straightly have a singular property

for arbitrary . We can take in the form for with , then the singular proprty implies for any arbitrary predictable set . Hence and must agree on unless with some special policies . This singular result together with the non-degenerate condition in Definition 4 ensures the uniqueness of mapping . ∎

Remark 8.

The concept of marginal risk measure we put here has several meanings. Given any -continuous positive homogeneous function of order , we have the Euler’s homogeneity theorem

where is the gradient of at . The same is true for the marginal risk contribution in Definition 3. Compared with the property above, Theorem 7 inherits that in the case . Further, this marginal risk measure is given by the Gâteaux differential which characterize the marginal growth of the terminal variance. That is the reason why we stress the word marginal.

We should also notice that for arbitrary the linear mapping

leads to a Riesz representation in the dual space of , and hence the marginal risk measure is identical to this Riesz representation.

2.4 The Flow Representation of Marginal Risk Measure

The risk associated with an investment process, specifically the terminal variance in our model, is supposed to be accumulated over the time interval and sample space where the investment process behaves differently. The terminal variance of our investment process should take the following suspected form

where the measurable process can be considered the instantaneous marginal risk contribution to the total risk. The terminal variance has already been represented as the integral in Theorem 7. What we are going to do is the show the relation between and .

Theorem 9 (Flow Representation - -dim).

Given a non-degenerate market, the signed measure on obtained in Theorem 7 can be uniquely represented as

| (9) |

where the measurable set is taken in and the process is continuous in . As the instantaneous marginal risk contribution, the process is the Radon-Nikodým derivative of with respect to .

Proof.

The predictable -algebra is generated by the simple left-continuous processes in the form where and . We can just take the simple form into consideration. The measure of in the form above can be split as

We can take a sequence of set functions parametrized by as

where is defined on the -algebra for each .

We claim that is a signed measure absolutely continuous with respect to since it is induced by the signed . It’s left to show the absolute continuity of for every fixed index . For the -null sets , we take . Those three parts of in Theorem 7 satisfies the following properties.

-

•

For part, we have

since is -measurable.

-

•

In a same manner, part gives

-

•

As for part, noticing , we have

Consequently, for each and -null set we have

hence .

For every index , we denote as the Radon-Nikodým derivative of with respect to . For every -measurable set , we have

since the finiteness of and the Hahn-Jordan decomposition of , and hence

where the supremum is taken over the possible partitions of . Consequently, the process is an integrable process of finite variation. To see that is right-continuous, we should notice

Let with (hence ), and then we have

The process has a right-continuous version since is handled in a same manner. Living in the natural filtration generalized by Brownian motion , for any arbitrary set , we have a representation

where is a sequence of countable points with and with given by . Here we let be the projection of in head-most coordinates , and we have with and . The process is left-continuous since

by the continuity of from above for . Consequently, we can say that is an integrable continuous process of finite variation. We can see that

If there is another process satisfying the equation (9), is distinguishable from since the measure introduced by is identical to .

With and as the Radon-Nikodým derivative of with respect to Lebesgue measure, we complete the proof. ∎

2.5 Multi-Dimension Case: Separation of the Terminal Variation

When it comes to a generalized multi-asset situation, we should stress the benefits of why we consider investment value processes in equation (6) instead of a self-financing portfolio usually characterized by a linear stochastic differential equation. Here are the reasons:

-

•

With , the self-financing portfolio acts only in the form where the policy is a constant determined by the investor’s initial wealth, instead of the generalized form . Due to money limits, it is difficult to examine the evolution of risk contribution in this constant policy situation using the method described in Theorem 7 and Theorem 9.

-

•

With , people often prefer a controlled linear stochastic differential equation to character the value process of the self-financing portfolio where control is usually a -dim process. But as one may expect, the (marginal) risk contribution should be a -dim process instead of -dim. And the Riesz representation mentioned in Remark 8 can be viewed as macro description of this point.

A particular case where there is one zero-interest risk-free asset and stocks is of particular interest. We should notice that these total assets and the stocks have the same risk. It sounds weird, but that is true in the view of risk. We cannot assign a risk budget to this coupon with no risk. However, when we throw light on the risk of these stocks, the risk budgets on the stocks imply the allocation of money that comes from the zero-interest coupon. In practice, it is proper to do this when facing the risk allocation of risky assets. The volatility-managed portfolio in [Moreira and Muir, 2017] is constructed in this manner where they only focus on the risk of risky assets. We will give an interpretation to it in the view of the risk budget in Subsection 4.1.

Compared to the classical single-period case, risk contribution is expected to be similar to the covariance matrix structure where the off-diagonal elements make sense. The following result can be considered an extension of Theorem 7 regarding the interaction of assets, as it also provides a characterization of the covariance-like structure.

Theorem 10 (Risk Gradient Measure - Generalized Version).

For the multi-assets investing case, its terminal variance can be uniquely expressed as

| (10) |

where is the marginal risk measure of -th asset mentioned in Theorem 7 and is a new signed measure related to mutual effect between -th and -th assets for each , or briefly

where is the multi-dim measure defined by

Proof.

Noticing , we can write

by the Itô’s formula and Theorem 7. Firstly for convenience, we give some notations of those parts by taking these operators

Hence we can give their related set functions induced by the Gâteaux differential manner where we use the notation with to treat multi-dim case.

Comparing the result above to the single-period case in Definition 3 where

gives the structure of the single-period marginal risk contribution, we can say that the -dim measure represent the properties of somehow. Respectively, is associated to . Actually, whenever is a multi-dim martingale, the associated product measure can be calculated as

for any predictable set .

Corollary 11 (Covariance).

The terminal covariance of two portfolios and can be calculated as

Proof.

Corollary 12 (Linearity of Marginal Contribution).

The marginal risk measure induced by policy in Theorem 10 is linear in .

Proof.

Only noticing the oprators and are both linear to the policy for arbitrary directions , we can get the assertion above. ∎

Corollary 13.

With the notation , the marginal risk measure in Theorem 10 can be uniquely represented as the vector integration

by a continuous adapted process . And is the Radon-Nikodým derivative of with respect to Lebesgue measure .

Proof.

Taking , the section set of , we can check that

is a signed measure over absolutely continuous with respect to . Hence we can write the Radon-Nikodým derivative of . Varying over time interval , we can get a process by what we have done in Theorem 9. Similarly for are calculated in a same manner. Finally we put them together

and get our result. ∎

The significance of the formula above is that it enables us to investigate the structure of terminal variance and the aggregated nature of instantaneous risk contributions. Corollary 13 gives the density of the marginal risk measure in the multi-asset case. Finally, with the help of this corollary, we can formalize the concept of continuous-time risk contribution, which is the focus of this section.

Definition 14 ((Marginal) Risk Contribution - Continuous-time).

Given a -valued policy within the associated density process in Corollary 13, we can define as the marginal risk contribution of -th asset at time in the case . And is defined as the risk contribution.

Particularly, the policy is said to be risk-parity if the associated risk distribution satisfies

| (11) |

In other words, is a constant vector valued process with some constant .

The risk marginal risk contribution is derived from the Gâteaux differential of the terminal variance. The definition of the marginal risk contribution here is identical to the definition in [Cherny and Orlov, 2011], where it goes by the name of directional risk contribution. The risk of an investment can be represented as

| (12) |

implying that the total risk is accumulated continuously on the support of . Clearly, this accumulation of risk contributions is described uniquely by Euler’s homogeneous decomposition, which appears in the statement (4) as a continuous version.

Remark 15.

The critical point of this theorem is the existence of a density process for the marginal risk measure . That means the total risk is continuously accumulated over within the density . Another critical point of this flow representation is that the transition from marginal risk measure to the continuous process can make the risk contribution we shall define in Definition 14 predictable. If we focus on the existence some satisfying

one may be confused with this theorem because the process can be easily get from

| (13) |

by Itô’s formula. Of course, this result of marginal contribution is correct in this situation, but we also need to be alert to the dangers this manner poses. When there are some jumps in the dynamics of assets, the marginal process can not be given by Itô’s formula in equation (13). To be able to understand this point better, we can consider the variance in the single-period case

If we look only at the results, both the terms and can be considered as the marginal risk contribution. It is not hard to check where is a zero-mean random variable also meets the equation above. Taking the marginal risk measure can avoid this disagreement in the expression. The first one is accepted for its predictable property. So it is necessary and reasonable to take the marginal risk measure and the associated density process in Theorem 9. In particular, when dealing with risk budgeting problems in Section 3, an ideal form of risk contribution should coincide with a given predictable risk budget. Hence, this flow representation appears to be of importance.

Corollary 16 (Continuity of the Marginal Risk Contribution on Policy).

Suppose we have two policies and with the notation . Then we have an estimation of the difference between two marginal risk contributions

for arbitrary predictable sets .

Proof.

For convenience, we provide the proof here for the case , and the left part for the multi-dim case can be easily derived in the same manner. Starting with three Gâteaux differential originally appearing in Lemma 5, we have

Finally replacing by and by , with the representation in Theorem 10 we get the result

∎

Corollary 17 (Risk Contributions of Self-financing Portfolios).

Given that the dynamic of assets processes are characterized by a multi-dim SDE

we can give the marginal risk contribution

Moreover, working on the self-financing case, i.e., the portfolio with properties (6) and (7), the related risk contribution of the policy is given by

-

•

(in a general share manner)

-

•

(in a money manner where policies are specified by the money allocated on each assets)

-

•

(in a weight manner where policies are specified by the weights allocated on each assets)

3 Risk Budgeting Problem

Compared to the classical result in Example 1, the risk contribution and marginal risk contribution in the continuous-time case depends not only on the assets but also on the time and the sample points . These latter two newly appearing terms are of our interest for risk allocation over . Having depicted the structure of terminal variance in Section 2, we are facing the risk budgeting problem. We write the collection of risk distributions induced by all feasible policies in under the assets in a fixed market. Within fixed assets, we write the collection of risk distributions induced by all possible policies in . The elements in can be obtained through the implementation of some policies.

Problem 18 (Risk Budgeting - Continuous-time).

With the terminal variance acting as the risk measure of investments and a continuous -valued process , the modelers seek to find suitable policies satisfying

for each .

To obtain the policy associated with the risk budget, we can design some ‘loss’ functions. To budget the standard deviation or the variance in the single-period case, one can take the loss function like

| (14) |

to make the risk contribution near enough to the budget . However the loss functions in a penalty form (for example ) can not work well in the continuous-time case, because it spends too much on the calculation of the marginal term -pointwisely. The result of [Maillard et al., 2010] gives an optimization to obtain the long-only risk parity policy of the variance where the marginal risk contribution does not need to appear explicitly. The optimization is a minimization of the variance with the constraints on the weights given by

| to minimize | (15) | |||

| s.t. |

Then the risk parity weight is given by the regularization of , i.e., . We adopt the loss function in this form where the minimization of the variance and the constants of the shares/weight are concerned and develope it in the continuous-time case.

Inspired by the tradeoff between the diversification of policies and the minimization of risk, we modify the loss function in (15) as

| (16) |

where is the exogenously risk budget. Here the vector is the share of assets and the matrix is the covariance matrix of the prices instead of returns. Hence the risk budget should be understood as the budget according to the price rather than the yield rate.

3.1 Relations between Risk-based Policy and Terminal Variation in Continuous-time Case

As a generalization of the optimization in the equation (16) the connection between the continuous-time policy with risk budget process and the optimization problem

| (17) |

over possible policies remains to be explored.

Theorem 19 (Continuous-time Risk Budgeting).

Proof.

The positive process ensures the strict convexity of the first term . As for the terminal variance, it is naturally convex as a risk measure. Hence is a convex functional. To reach the minimum, we need to check the closedness and the recession direction of . The closedness is guaranteed by the space of assets and the space of policies. To see the recession functioanl of , we notice the slope function of satisfies

for any point . On the directions with , the recession . But on the directions with , the recession functional may be less equal to zero(depends on ). The non-degenerate condition in Definition 4 guarantees for any direction . Hence what left us to see is the local minimum of .

By the slope function above and Corollary 11, we can see the first order condition of the functional at the local minimum which satisfies555For two non-zero vectors and , .

for arbitrary policies . Hence we have

and the equation above also implies

The level sets are certain bounded closed convex sets and also for . Now suppose and are two differnet policies in the minimum set . We can take and the policies are also in the minimum set. The slope function between and shows

which implies a contradiction. Hence the optimal solution is unique. ∎

Now we want to make an interpretation of the term . Actually, the result of [Maillard et al., 2010] takes the optimization 15 as alternative to the residual sum of squares in 14. The risk parity portfolio is similar to a minimum variance portfolio subject to a diversification constraint on the weights of its components. Here we want to give the economic interpretation of the diversification term. The derivation of the term is given step by step.

First, we can consider a basic single-period optimization with constants on shares, namely

| to minimize | (18) | |||

| s.t. |

The aim of the area is to prevent the shares from concentrating. We can appoint linear constraints for . The optimal policy of this linear constraint has a constant marginal risk contribution by a simple calculation. The boundary is exogenously given and usually follows the varying trend of the prices. In other words, the boundary may have an exponential growth which implies an exponential boundary of shares. To avoid this, one can take logarithmic constraints of the shares, i.e.,

| (19) |

It is easy to check that the risk contribution of the optimal policy happens to be the Lagrangian multipliers of the optimization with the logarithmic constraints. As a special case, the optimal policy with the constraint , also the constraint in [Maillard et al., 2010], shows an equal risk distribution. Having noticed the connection between the Lagrangian multipliers of the log-constrained optimization and the risk contribution of the associated solution, we can generalize the Lagrangian to the function

where the multipliers are replaced by the budget . The optimization solution above can give the policy with the risk budget . Finally, with the help of the results in Section 2, we put it in a continuous-times style and get the optimization (17).

In perspective on the constraints, the continuous-time optimization problem (17) can also be considered as a constrained convex minimization of terminal variance, i.e.,

where convex constraint area is given by

This convex constraint area may be thought of as a regulatory mechanism that prevents the concentration of the shares from nearing zero -pointwisely. When changing the shares for each pair , the Lagrangian multiplier can be regarded as the tolerance of the exponential growth in the level of .

Now that the risk has a distribution over , we can also think about the constraint term in the way of distribution. To see this, we can consider the Doléans measures and introduced by the multi-dim processes and the process over by

for each and predictable set . is the distribution of the undetermined shares and is the distribution of risk budget. And then the Kullback-Leibler divergence—also known as the relative entropy—from to implies

which measures the divergence between and . Thus, given a positive risk budget process , the objective of reducing both the K-L divergence and the terminal variance is identical to that in (17). As a particular example, taking a naive risk budget for some positive constant and a.a. , this implies the K-L divergence from undetermined to a uniform distributed over . Overall, the risk budgeting optimization is equal to balancing the diversification of the policy and the minimization of the total risk .

Remark 20.

Theorem 19 discusses the continuous-time risk parity/budgeting cases within a positive share setting in order to establish the connection between admissible set and possible budget processes . Those risk budgeting problems with negative supports where the policies are negative-valued remain interesting. In light of the regulation of the shares, we can divide the constraint area into two sections

Then we can deduce a generalized optimization

where the risk budget can be negative on and -valued sign process coinciding with is also negative on . Additionally, we can observe that the policy and its inverse have the same risk distribution.

The behavior of the optimal policy is also of interest when there is no constraint on some area or the risk budget satisfies on the area . In this case, the optimization 19 still has an optimal solution and the associated policy also meets the budget for a.a. ., i.e.,

The equation above implies that the risk contribution of is zero on and also implies the marginal risk contribution or the share itself is zero on that zero-risk-budget area. The policy is one of the policies with risk contribution identical to on the complement of , and is also the minimized total variance of these policies. The zero-valued marginal risk contribution and the share on make sure that is true.

3.2 Ramifications

In simple terms, both the policy and the exogenous risk budget depend on the information, and the information is equal to the measurability of the processes in the stochastic language. The critical point here is how the risk budgeted policy behaves when given rough information. When dealing with less information, it can be challenging to establish a policy whose risk contribution is the same as the budget . Suppose we can only make a choice at the start of and can not change it. Given the budget , how to determine the best policy in this case? The corollary following gives the relation between the risk budget and the optimal policy with less information.

Corollary 21 (Projection).

Given an integrable positive risk budget and the admissible policy set where is a sub -algebra of , the solution of the optimization

gives a policy of which the associated risk distribution is the projection of onto .

Proof.

The assertion can be quickly get from the first-order condition

with arbitrary -mesurable set , and hence

where is the projection from to within measure . ∎

The projection corollary above also shows that the single-period risk budgeting problem is the degenerate case of continuous-time risk budgeting problems where the risk budgets are constants and the policy is constrained in the naive -algebra.

The optimization (17), unlike the well-known expected utility problems, is not a pure stochastic control problem. The embedding lemma is typically employed to solve the continuous-time mean-variance frontier problem where the mean-variance object is converted to a stochastic control problem. The lemma following gives a similar method to solve the risk budgeting problem in a stochastic control framework.

Lemma 22 (Embedding, original version in [Zhou and Li, 2000]).

Proof.

We can define a function

which is a concave function with

If is not optimal for , there will be a optimal for satisfying

On the one hand, the convexity of implies

which induces a contradiction to the original problem, and hence we get the result . ∎

Lemma 22 implies that risk budgeting problems can be accomplished by solving a family of parameterized stochastic control problems. The optimal solution of optimization 17 is embedded in the parameterized solutions of those auxiliary problems. Usually, these auxiliary problems can be solved identically. To find the optimal solution, we can check .

Additionally, the item appearing in the auxiliary functional can give a parameterized signed measure

This parameterized measure can be considered as a guess of established in Theorem 7. And when we get the right guess , the related meets true . Actually, in the language of risk contribution, this embedding technique in [Zhou and Li, 2000] gives a modification of the marginal risk contribution.

4 Examples

It is natural to extend the risk contribution idea from the classical covariance matrix structure to the continuous-time setting. This section will provide three examples to demonstrate the concepts of risk contribution and risk budgeting.

-

•

In the first subsection, we derive a strategy based on a concrete risk budget. This derived strategy is identical to the volatility-managed portfolio in [Moreira and Muir, 2017] where the portfolio is based on the volatility anomaly in the time axis. We will derive this strategy in a risk budget manner without the tenet of risk anomaly and give the average return at long-term growth.

-

•

The risk contributions of policies depend on the concrete model of the dynamics. As for the second example, we will relate the risk contribution to the coefficients in the SABR model, which is commonly used for option modeling. The risk contribution can be derived through the options of the underlying assets.

-

•

As a tool to detect the concentration of the risk, the final example gives the risk contribution of the continuous-time mean-variance portfolio in [Zhou and Li, 2000].

4.1 Volatility-Managed Portfolios

Unlike consensus that higher risk always brings a higher return, low-risk anomaly states that the stocks with low risks have higher returns than the stocks with higher risk. This smile risk-return curve happens not only in the cross-section but also in the time axis. The volatility-managed portfolio in [Moreira and Muir, 2017] suggests enlarging the investment on the risky assets when their risk is at a lower level. To be more specific, they investigate the relationship between the lagged volatility factor and the current return of stocks. Empirical results show that

-

•

the current month’s average returns have a weak relationship with the lagged realized volatility;

-

•

whereas the current month’s volatility has a strong relationship with lagged realized volatility.

Consequently, the return-volatility ratio has a negative correlation with the volatility because of the volatility clustering. In other words, the efficiency of the assets is higher when the volatility is at a lower level. The difference in the return-volatility ratio in the time axis implies different risk budgets at different times. The agents can time volatility by shorting risky assets during periods of high volatility and accepting risk during periods of low volatility to gain from the mean-variance trade-off.

How does the volatility-managed portfolio work? In [Moreira and Muir, 2017], volatility-managed portfolios are designed by scaling monthly returns by the inverse of the previous month’s realized variance, therefore reducing risk exposure when the realized variance was at a high level and vice versa. This managed strategy can be summarized as

| (20) |

where is the buy-and-hold portfolio return of current month, represents the proxy for portfolio’s instantaneous variance and constant controls the average risk exposure of this managed strategy. The buy-and-hold portfolio can be a capital-weighted market index or a simple stock. The investor can borrow money from a bank account (risk-free assets) to scale this buy-and-hold portfolio. Through this simple scheme, though volatility does not forecast returns, the efficiency of the investment is improved by time-selected volatility.

This scheme implies the idea of the risk budget in the time axis: the risk budget can be taken at a high level when the volatility is lower. We will give a continuous-time risk budgeting interpretation of this scheme. In this subsection, we assume that the dynamic of the underlying asset is in a linear form

where is a -dim Brownian motion under the physical probability measure . The coefficients return rate , volatility rate are locally bounded processes such that this Lipschitz SDE can be well-posed in and satisfies the non-degenerate condition in Definition 4. The solution to this SDE can be considered the price of a single stock or the market portfolio, e.g., market stock indices.

The reference probability measure appearing in budgeting optimization can be identified as the risk-neutral measure constructed by a Doléans-Dade exponential martingale

| (21) |

under which is a martingale and is called the market price of risk. Hence under this reference probability , the terminal variance can be calculated as

| (22) |

Since is in exponential growth and the terminal variance is homogeneous of order , the parity risk budget we will take should be in a regularized form

for each . Without the loss of generality, we can take

where this positive proportion coefficient plays the same role in the formula (20) to control the total risk level.

Given this regularized risk parity budget, the optimal condition of the associated convex risk budgeting optimization

is given by

The optimal policy can be straightly calculated by

which is identical to the core equation (20) in [Moreira and Muir, 2017] and derives the optimal investment process

| (23) | ||||

We can rewrite this investment process in the form

| (24) |

Having been back to our physical world , our optimal investment captures the gain from the market price of risk under a unit noise with square-rooted risk budget as the amplifier. Notice that the market price of risk is high when the volatility is low and the budget is high at the same time. Hence we call the term as an amplifier to make the investment more efficient.

We also care about the long-term return of and have the proposition following.

Proposition 23.

Suppose that has the semi-martingale decomposition where is the continuous martingale part. Then bounded volatility together with can ensure that , the martingale part of , satisfies

and implies the long-term behaviour of

The limitation above is a straight result of the strong law of large numbers for Brownian motions and martingales. Readers can refer to Lemma 1.3.2 in [Fernholz, 2002] for the martingale case. This proposition states that the long-term average return of depends on the time-averaged signal .

4.2 Volatility Budgeting: SABR Model

In this subsection, we demonstrate the relationship between the smile of volatility and the continuous-time risk contribution established Definition 14 by using a risk-budgeted forward interest rate example. In light of the smile of the implied volatility, we choose the SABR model to describe the dynamics of this future interest rate.

The SABR model, a stochastic volatility model, is frequently used in the financial industry, particularly in interest rate derivative markets. It was first proposed in [Hagan et al., 2002] to capture the volatility smile for Markovian local volatility model improvement. Just as the name ’stochastic, alpha, beta, rho’ implies, we consider a single forward interest rate with the stochastic-volatile underlying dynamic

where . Controlling the implied at-the-money volatilities of European options, the parameter acts as the volatility of volatility for the underlying . The power coefficient characterizes the curvature of implied at-the-money volatilities. And the remained constant reflects the correlation of two risk sources and . For convenience, a -dim equivalent Brownian motion is defined by

The risk contribution of the specified hedging policy is now investigated. The associated terminal variance is given by

| (25) |

from which we can get the related marginal risk contribution

| (26) |

Then we can also give the risk contribution

| (27) |

where represents the Doléans-Dade exponential martingale of processes. The parameters in the SABR model are primarily used to calibrate the volatility smile; nevertheless, they can have an impact on our risk contribution in a variety of ways:

-

•

The fundamental level of stochastic volatility has a positive correlation with the contribution of marginal risk;

-

•

The stochastic exponential yields a log-normal distribution of volatility changing through with a scale factor of ;

-

•

The correlation reconciles the volatility produced by the rewritten risk resources and ;

-

•

Naturally, the price of the underlying has the right to assert that a higher price implies a greater risk contribution;

-

•

Controlling the curvature of implied skewness when confronted with the calibration of options, the parameter also distributes the influence of across different price levels in an exponential way.

Risk-budgeted policies within different information are also of interest, particularly in the case mentioned in Corollary 21, where we are restricted to some sub--algebras. Suppose that we are dealing with the policy limited to a fixed risk level , i.e.,

Assume that and a shrinkage filtration generated by . The following four cases are projected with less information one-by-one.

-

1.

(Purely Risk-Parity) In the view of Theorem 19, we can indicate the optimal policy associated to risk-parity budget for almost all in by

Then purely risk-parity policy with total risk is given by

-

2.

(-Projection) Considering that stochastic volatility of underlying is not easy to perceive, we have a second-best solution restricted on by Corollary 21

where is the associated projection of the underlying asset. Comparing this solution to , we cannot distinguish the policy among different namely the volatility rate and is substituted by its expectation in the formula above. This projected policy is substantially equivalent to that of the Black-Scholes model, where the volatility rate is assumed constant.

-

3.

(Non-stochastic Time-varying) Furthermore another shrunk -algebra gives a non-stochastic time-varying policy by

for each .

-

4.

(Naive Single-Period) Finally, a buy-and-hold policy can give the degenerated single-period solution by the equation

These four policies illustrate the distinctions between the single-period case and the continuous-time one. Similar to the extended mean value theorem of integrals, single-period policies act like a low-resolution version of continuous-time ones. This risk budgeting technique implies that adjusting the position of the underlying, continuous-time risk budgeting can produce more exquisite -pointwise policies associated with more robust targeted risk distributions.

4.3 Risk Contribution of Continuous-Time Mean-Variance Policy

Mean-variance investors are facing a Markowitz’s mean-variance minimization target

with the coefficient representing the risk tolerance to make a balance between the return and the risk . Having found the approach to get the risk contribution of a policy in Section 2, we are also interested in how the related risk contribution of continuous-time mean-variance policy behaves.

For simplicity, here we assume the dynamics of two assets are

Then the wealth process of the self-financing portfolio is specified as

where is the amount of money allocated on . According to [Zhou and Li, 2000], the optimal policy of object is given in a linear feedback manner by

For convenience, we denote in a vector style where is the money on the bond . One can also derive the expected return of terminal wealth

With the help of Corollary 17, we can give the related (marginal) risk contribution of the continuous-time mean-variance policy

where we denote and for convenience.

Hence the risk contribution of two assets has the elements

and

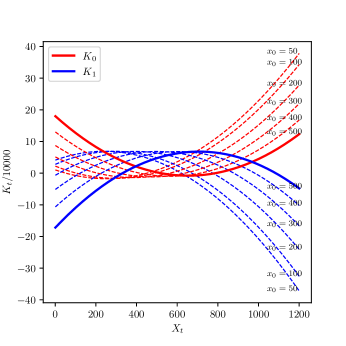

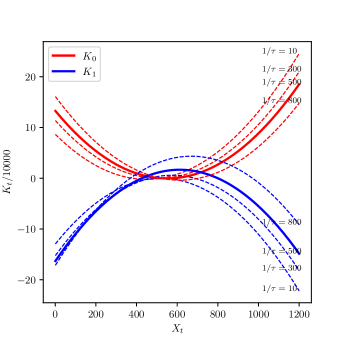

In order to have a better understanding on , we illustrate the impact of the exogenous parameters and in Fig. 2.

We can summarize:

-

•

The risk contributions on each asset are quadratically distributed with respect to the spot price . The recession directions of and are different and specified by the market parameters instead of the tolerance . As the deviation risk measure suggests, risk contributions of the terminal variance are at a low level around the average of the spot price and a high level far away from the average price.

-

•

In the central area of the spot price , has a positive risk contribution and vice versa with . In the extreme circumstances on the spot price , however, it shows that the risk contribution on the stock is negative, which exceeds our expectation that risky assets are supposed to contribute more in extreme circumstances. This conflict is due to shorting the stock when the spot price is high, or in other words, negative shares on the stock with a positive marginal contribution lead to the negative cases of .

-

•

When the spot price is varied, the risk tolerance does not affect the second-order state. Indeed, when placed in the same position as , can merely contribute to the shift of . One can expect that a higher initial wealth parameter brings us a whole lift of risk level without changing the structure of risk contribution, and does the same.

-

•

It appears that policies in the affine feedback form of , as well as the mean-variance policy as a specific case, cannot prevent the concentration of risk.

5 Concluding Remarks

We have generalized the concept of risk contribution to the continuous-time case in a differential manner. The primary purpose of this paper is to give a proper definition of the continuous-time risk contribution for the terminal variance. The marginal risk contribution is defined from the Gâteaux derivative of terminal variance. The non-degeneration condition ensures the uniqueness of the marginal risk contribution.

The continuous-time risk budget problem is then raised. Different from the single-period case, the risk budget together with the risk contribution depends not only on the assets but also on . The risk-budgeted investment is related to an optimization object, a tradeoff between the minimization of risk and the diversification of shares. We give an economic interpretation of this optimization in the view of constraints.

We also put three examples to stress the application prospect of the continuous-time risk contribution/budgeting.

-

•

A price-regularized risk-parity strategy reproduces the volatility-managed portfolios in [Moreira and Muir, 2017]. With the help of this risk-budgeted strategy, we give the long-term averaged return of this strategy.

-

•

The risk contribution depends on the concrete dynamics of the assets. We give the risk contribution of SABR dynamics in the second example to describe how the risk contribution is related to the coefficients, which can also be implied by the options.

-

•

As a tool to measure the risk concentration, the risk contribution of the continuous-time mean-variance portfolio is calculated in the last example. The result shows that the continuous-time mean-variance policy has a concentration indeed.

6 Acknowledgements

The authors would like to thank the referees for their helpful comments.

References

- [Best and Grauer, 1991a] Best, M. J. and Grauer, R. R. (1991a). On the sensitivity of mean-variance-efficient portfolios to changes in asset means: some analytical and computational results. The review of financial studies, 4(2):315–342.

- [Best and Grauer, 1991b] Best, M. J. and Grauer, R. R. (1991b). Sensitivity analysis for mean-variance portfolio problems. Management Science, 37(8):980–989.

- [Cherny and Orlov, 2011] Cherny, A. and Orlov, D. (2011). On two approaches to coherent risk contribution. Mathematical Finance, 21(3):557–571.

- [Cohen and Elliott, 2015] Cohen, S. N. and Elliott, R. J. (2015). Stochastic calculus and applications. Springer.

- [Fernholz, 2002] Fernholz, E. R. (2002). Stochastic Portfolio Theory. Springer New York, New York, NY.

- [Hagan et al., 2002] Hagan, P. S., Kumar, D., Lesniewski, A. S., and Woodward, D. E. (2002). Managing smile risk. The Best of Wilmott, 1:249–296.

- [Kalkbrener, 2005] Kalkbrener, M. (2005). An Axiomatic Approach to Capital Allocation. Mathematical Finance, 15(3):425–437.

- [Li and Ng, 2000] Li, D. and Ng, W.-L. (2000). Optimal Dynamic Portfolio Selection: Multiperiod Mean-Variance Formulation. Mathematical Finance, 10(3):387–406.

- [Litterman, 1996] Litterman, R. (1996). Hot spots and hedges. Journal of Portfolio Management, page 52.

- [Maillard et al., 2010] Maillard, S., Roncalli, T., and Teïletche, J. (2010). The properties of equally weighted risk contribution portfolios. The Journal of Portfolio Management, 36(4):60–70.

- [Merton, 1972] Merton, R. C. (1972). An analytic derivation of the efficient portfolio frontier. Journal of financial and quantitative analysis, 7(4):1851–1872.

- [Merton, 1992] Merton, R. C. (1992). Continuous-time finance. Journal of Finance, 52(4).

- [Moreira and Muir, 2017] Moreira, A. and Muir, T. (2017). Volatility-managed portfolios. The Journal of Finance, 72(4):1611–1644.

- [Pearson, 2002] Pearson, N. D. (2002). Risk budgeting: portfolio problem solving with Value-at-risk. Wiley finance series. J. Wiley, New York.

- [Qian, 2005] Qian, E. E. (2005). Risk parity portfolios: Efficient portfolios through true diversification. Panagora Asset Management.

- [Rockafellar et al., 2006] Rockafellar, R. T., Uryasev, S., and Zabarankin, M. (2006). Generalized deviations in risk analysis. Finance and Stochastics, 10(1):51–74.

- [Samuelson, 1975] Samuelson, P. A. (1975). Lifetime portfolio selection by dynamic stochastic programming. In Stochastic Optimization Models in Finance, pages 517–524. Elsevier.

- [Zhou and Li, 2000] Zhou, X. Y. and Li, D. (2000). Continuous-time mean-variance portfolio selection: A stochastic LQ framework. Applied Mathematics and Optimization, 42(1):19–33.