A Worrying Analysis of Probabilistic Time-series Models for Sales Forecasting

Abstract

Probabilistic time-series models become popular in the forecasting field as they help to make optimal decisions under uncertainty. Despite the growing interest, a lack of thorough analysis hinders choosing what is worth applying for the desired task. In this paper, we analyze the performance of three prominent probabilistic time-series models for sales forecasting. To remove the role of random chance in architecture’s performance, we make two experimental principles; 1) Large-scale dataset with various cross-validation sets. 2) A standardized training and hyperparameter selection. The experimental results show that a simple Multi-layer Perceptron and Linear Regression outperform the probabilistic models on RMSE without any feature engineering. Overall, the probabilistic models fail to achieve better performance on point estimation, such as RMSE and MAPE, than comparably simple baselines. We analyze and discuss the performances of probabilistic time-series models.

1 Introduction

Sales forecasting is an essential task in logistic companies as well as retail business concerning resource optimization. Probabilistic time-series models are becoming increasingly important in sales forecasting as it helps automate optimal decision making under uncertainty. There have been many studies on the probabilistic time-series models [1, 2], and big IT companies have already commercialized basic models through cloud services [3, 4]. They are being applied to various kinds of sequential data such as images [5], traffic, and finance [6, 7].

Despite their tremendous studies and usages, it is hard to precisely evaluate the progress being made due to the lack of rigorous empirical evaluation procedures. Researchers often evaluate their models with different training procedures; such factors, including dataset split, data normalization, model hyperparameters, evaluation metrics, and a choice of baselines, can affect the performance of learning architecture, which may unfairly benefit the new model [8]. As such, we also empirically experienced that prominent probabilistic time-series models do not work effectively especially for other datasets not used in the original papers.

In this paper, we carefully study those concerns with the following main research question: To what extent the publicly used probabilistic time-series models are better than simple baselines in forecasting performance? To answer the question, we choose three probabilistic time-series models such as DeepAR, DeepState, and Prophet, after scanning the widely used cloud services and referenced reproducible papers [6, 9, 10]. Moreover, the paper aims to thoroughly discuss the potential factors that can undermine the performance of probabilistic models in other datasets as well.

To eliminate the possibility of changes in performance due to external factors, we make following experimental principles. 1) Large-scale dataset with various cross-validation splits. We construct a real-world sales dataset named EC dataset consisting of 6,032 time-series of 1,725 time steps, each representing daily sales for a shop on an e-commerce website. We use ten cross-validation splits. Spectral entropy density analysis [11] shows that the entropy density distribution of EC dataset is much more balanced than that of publicly available datasets, preventing learning architecture from biasing toward a specific time-series property. 2) A standardized training and hyperparameter selection procedure for all models including four baselines. In such setting, the differences in performance can be attributed to architectures, not other factors. For each split, all comparative models search hyperparameter space using 72 randomized trials or heuristic trials guided by an ablation study. Section 3.3 describes the experimental settings in more detail.

The experimental results show that a simple Multi-layer Perceptron (MLP) comfortably beats all competitive probabilistic models on RMSE and MAPE metrics. A Linear Regression follows the MLP on RMSE metric. Overall, the probabilistic models fail to achieve better performance on point estimation than simple non-probabilistic baselines. We include further analysis and discussion in Section 4 and 5. We would like to make a disclaimer that point estimation such as RMSE and MAPE are not the only way to judge the performance of probabilistic time-series models. Learning and representing a probability distribution of output is an important research direction of the field. However, rigorous empirical evaluation of the models is critical to understanding the model’s strengths and weaknesses to use them in both commerce and academia.

2 Time-series Models

Let a set of univariate time series, where and represents the value of the -th time series at time 111The time series of variable length can be applied without loss of generality, but this paper fixed the length for the sake of simplicity of the implementation.. Additionally, consider a set of corresponding covariates (i.e., feature vectors), where and . The goal of probabilistic sales forecasting problem is to predict the conditional probability distribution of future time series, , given the past observation and covariates:

| (1) |

Following subsections briefly describe prominent sales forecasting models and how they predict the future time series. Please refer to supplementary materials for more details.

2.1 DeepAR

DeepAR [6] is one of the most prominent forecasting model that is based on the auto-regressive recurrent network architecture [12, 13]. DeepAR approximates the conditional distribution using a neural network as follows:

| (2) | ||||

where is a likelihood function parameterized by and is an output of the recurrent network, .

2.2 DeepState

Deep State Space Models (DeepState) [9] is a probabilistic forecasting model that fuses state space models and deep neural network. State space model introduces a latent Markovian state encoding temporal features, and models the time-series observation via transition and observation model . In particular, DeepState adopts linear Gaussian models:

| (3) | |||||

where and are initial state parameters, while are time-varying parameters of the model. DeepState estimates model parameters for each time series by using recurrent neural network which takes covariates as input:

| (4) |

where is a function mapping the output vector of the recurrent neural network to the parameters. Unlike the auto-regressive models, DeepState uses the observation values to compute the posterior distribution of latent state, , by integrating Kalman filtering [14, 15]. DeepState estimate the joint distribution of future time series from the estimated posterior and state space models.

2.3 Prophet

Prophet[10] is a modular regression model with interpretable parameters. It is a sum of trend , seasonality , and holidays components as follows: , where is a normally distributed error term. Prophet incorporates trend changepoints in the trend model that the analysts can manually configure or the model automatically finds. The seasonality model is a general Fourier series with a regular period that we manually set.

3 Experiments

3.1 Dataset

To create a testbed, we construct a large-scale real-world sales dataset named EC dataset from our e-commerce website. As most shops in the e-commerce site tend to have sparse sales records, i.e., many zeros in the daily sales history, the models tend to rely on other features instead of time series information. We seek to make our dataset as predictable as possible and let models to learn nature of time-series data. To select shops with steady sales performance, we filter out shops containing zeros in the daily sales records from 2019-01-01 to 2020-09-20. As a result, the EC dataset contains daily sales records from 6,032 different shops for 1,725 days from 2016-01-01 to 2020-09-20. Figure 1 shows the comparison of widely used public datasets and the EC dataset in terms of forecastability. Our dataset is more trickier than traffic and electricity but easier than Wikipedia. Figure 2 describes the comparison of spectral entropy density [11] for the EC dataset and others. The entropy of our dataset is much more distributed than that of others, meaning that ours is much more balanced. The length of test and validation sets are all seven days, and remaining past days are training set. We make ten cross validation splits with no intersection in the test sets.

![[Uncaptioned image]](/html/2011.10715/assets/figures/comparison.png)

![[Uncaptioned image]](/html/2011.10715/assets/figures/ec_histogram.png)

3.2 Baselines

In addition, we consider four baseline models: MA (Moving Average), LR (Linear Regression), MLP (Multi-layer Perceptron) and SARIMA (Seasonal ARIMA). MA is a simple unweighted mean of past few days. The historical value of the time series is solely used as an input feature for all the baselines. We try various historical length for MA, LR, and MLP. We test all combination of for SARIMA models and fix seasonal length to seven. The SARIMA show better performance than ARIMA, so we omit the results of ARIMA.

3.3 Experimental Setups

For neural or hybrid architectures such as DeepAR, DeepState, LR, and MLP, we define a standard set of hyperparameters. We use the same weight initialization (PyTorch [16] default initialization), same optimization method (Adam with default parameters), and search multiple learning rates (value between 0.0001 and 0.01). We try randomly sampled 72 different hyperparameters for prophet and baselines with the same early stopping strategy (loss value as early stopping criteria and five as the number of patience). Simiarly, we conduct the ablation studies of DeepAR and DeepState with 72 heuristically selected points. We describe below detailed architecture configuration with tunable hyperparameter set.

DeepAR: We select GRU as RNN architecture for DeepAR since it slightly outperforms LSTM. We test the model with 72 different hyperparameters: the number of RNN layers (3 and 5) context length (7, 14, 28, 56, 84, and 112) 3 different scaling strategy (mean, median or no scaling) output distributions (negative binomial and Gaussian). For features, we feed lagged values, normalized day-of-the-week, normalized day-of-the-month, and age (i.e., the distance to the first observation).

DeepState: First of all, we adopt the same RNN architecture as in the setups of DeepAR for the sake of unity. Same as in DeepAR experiments, we explore the model with two different RNN layers, six different context lengths, and three different scaling methods. We further test two different state space model (SSM) architectures in Eq. 3: fully-learnable (FL) SSM and partially-learnable (PL) SSM. The total number of runs are 72 as in the experiments for DeepAR. For PL SSM, we apply widely-used level-trend and day-of-the-week seasonality models, that are widely used approaches in the sales dataset as well as the default settings from GluonTS implementation [17]. In this case, the only learnable parameters are and . To achieve a fair comparison, we use the same latent dimension for the FL SSM (i.e., ). We use shop index, normalized day-of-the-week, and normalized day-of-the-month features as covariates.

Prophet: It is hard to identify all kinds of events in the EC dataset, so we omit holidays functions. There are two kinds of trend models: linear and nonlinear saturating trend models. We choose former one since saturating patterns are rare in the EC dataset. In the official Prophet API, it recommends three effective hyperparameters: changepoint prior scale, seasonality prior scale, and seasonality mode. The prior scales determines the flexibility of the trend and seasonality. A large value is more likely to overfit on the training dataset. The two options of seasonality mode are ‘additive’ and ‘multiplicative’ where the multiplicative seasonality multiplies the seasonality function by the trend model.

We report the results of best setups for each model.

3.4 Metrics and Evaluation

In practice, the costs are not scale-free since the prediction errors in the large shops would cause more financial damage. We use RMSE (Root Mean Squared Error) to consider such aspects. We also measure MAPE (Mean Absolute Percentage Error) for a scale-free metric:

| (5) |

where is the total number of the prediction targets and is a prediction value. In order to evaluate probabilistic prediction, we use NQL[6]222Note that NQL is the same metric as -risk in [6]. (Normalized Quantile Loss) that quantify the accuracy of a -quantile of the predictive distribution as follows:

| (6) |

Specifically, we compute mean of NQL(0.1) and NQL(0.9).

4 Results and Analysis

| Model | RMSE | MAPE | Mean NQL[0.1, 0.9] |

|---|---|---|---|

| MA | 79.2813.79 | 0.3480.015 | - |

| MLP | 72.2312.60 | 0.2670.015 | - |

| LR | 73.2013.60 | 0.3000.010 | - |

| SARIMA | 79.0917.50 | 0.3180.017 | 0.1650.033 |

| DeepAR | 76.6917.86 | 0.2840.022 | 0.1320.026 |

| DeepState | 79.1015.83 | 0.3140.030 | 0.1520.020 |

| Prophet | 82.2117.64 | 0.4150.018 | 0.1940.027 |

We report the prediction results of prominent probabilistic models and baseline models on the EC dataset in the following sections. The paper shows the negative results and their causes that degrade the performance of each model. The ablation study illustrating hyperparameter’s effect on each model is described in Section C of the Appendix with details.

4.1 DeepAR

As reported in Table 1, DeepAR shows the best result on mean NQL compared to other probabilistic models. Still, DeepAR performs worse than a simple MLP model on RMSE and MAPE metrics. The result indicates that although DeepAR is a decent probabilistic model as widely known, it is not a remarkable point estimator, unlike our expectation. The paper would like to address the point that autoregressive architecture such as RNN, is not the sole approach to dealing with time-series data. As shown in the results, simple MLPs could capture richer latent time-series characteristics when the length of lagged values are appropriately adjusted. We observe empirically that DeepAR’s performance is affected unstably by which lagged value is selected; an autoregressive architecture may not effectively convey information from the distant past well over time, unlike ideal.

As mentioned in the reference paper [6], we confirm that scaling method is a critical factor that hugely affects the results. There is relatively little difference between the mean and median scaling, but there is a noticeable gap in performance depending on whether the scaling is applied or not, as shown in Table 2. The scaling method not only helps the stability of the learning procedure by adjusting the range of values fed into the model, but prevents the over or under-fitting to a specific data instance by balancing the scale between time series. The consistent results are shown in the experiments with DeepState.

4.2 DeepState

Primarily, DeepState fails to outperform competing models including DeepAR on any of three evaluation metrics. The paper regard above results are mainly due to the inherent lack of representation power of DeepState. The only factors that govern the system parameters in DeepState are the covariates as illustrated in Eq. 4, while the real-world tasks often do not provide a sufficient set of covariates. For example, in sales data, ordinary information such as day-of-the-week and season is accessible, but latent features such as sales trend and promotion for each shop are generally not provided. As such, if the system parameters are estimated only through indistinct features (i.e., without observation sequences), the inferred models are highly likely to be inaccurate. Taken together, DeepState may function properly only when the target system is assumed to be fairly known and less volatile, like the traffic and electricity dataset reported in the reference paper [9].

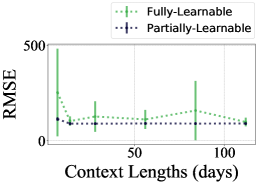

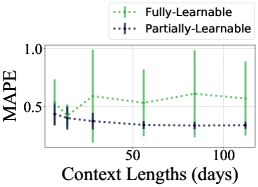

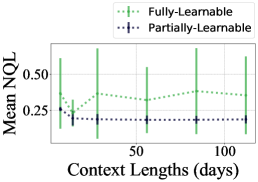

We further compare the DeepState with the FL SSMs to PL SSMs to evaluate the effect of SSM architectures to the performance. Our initial hypothesis is that FL model would give much higher performance compare to the PL due to its flexibility; remark that the only learnable parts in PL model were about the uncertainty estimators, while FL offers the flexibility in indetifying the transition and observation models. FL mode, however, shows significantly dropped performance to the one with PL SSMs as described in Table 5. Moreover, the value of standard deviation calculated over hyperparmeter samples for FL model is noticeably large (i.e., the robustness of the model and the prevalent advantage of using probabilistic model are not guaranteed.). We reason that the SSMs’ extreme flexibility causes the non-identifiability problem [18, 19] as well as the overfitting.

4.3 Prophet

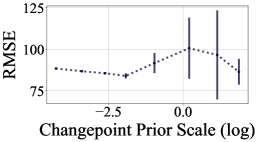

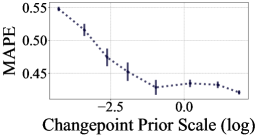

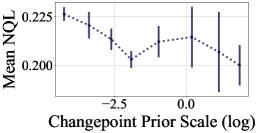

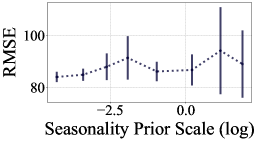

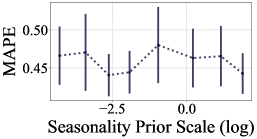

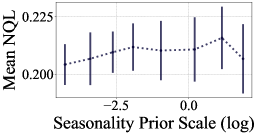

The patterns of the time series are complicated and change dynamically over time, but Prophet follows such changes only with the trend changing. The seasonality prior scale is not effective, while higher trend prior scale shows better performance. There exist some seasonality patterns in the EC dataset, but these patterns are not consistent neither smooth. Since Prophet does not directly consider the recent data points unlike other models, this can severely hurts performance when prior assumptions do not fit. The detailed results are shown in Appendix.

5 Discussion and Conclusion

This paper analyzes the performance and negative results of three prominent probabilistic time-series models such as DeepAR, DeepState, and Prophet, for sales forecasting by comparing them with simple baselines including Linear Regression and Multi-layer Perceptron. For experiment, we construct a large-scale real-world benchmark dataset containing 6,032 time series of 1,725 time-steps with ten cross-validation splits. We use the standardized training and hyperparameter selection procedure to remove the role of random chance in model’s performance.

Prior to our experiment, we observe that the spectral entropy densities of widely used public datasets such as traffic, electricity, and Wikipedia are biased towards a specific point. If a researcher tests his or her idea on only these datasets, specifically traffic or electricity, with a small number of baselines, it may unfairly benefit the new model. However, which has often been the case.

Another observation is that, surprisingly, a simple MLP and LR outperform all the competing probabilistic models on RMSE and MAPE metrics. Previous studies on probabilistic forecasting report their model performances based on the quantile loss while making a small effort to compare the point estimation performance to baselines. Contrary to the researcher’s interest, point estimation performance is essential in industries that require specific numbers, such as the number of delivery people in a logistics company. When this practice is combined with other aspects, i.e., not reporting on hyperparameter selection in the original paper, it is difficult to precisely assess the progress of the field.

Moreover, this paper points out that the belief that probabilistic models are considered robust is not always guaranteed. In our experiments, for instance, DeepState with fully learnable SSMs shows high variance results, which is inconsistent with the statement from the original paper: DeepState is robust to noise. In the case of the SSM-based model, in particular, this paper advises the future research papers to conduct research developing models that can further increase the stability of well-known probabilistic models by resolving the related issue such as non-identifiability.

Lastly, the paper suggests the future works to further consider the selection of the probability distribution of output that time-series model assumes. Despite the wide variety of recent studies on probabilistic time-series models that combine neural networks, research about choosing proper probability distribution that fits a given dataset has not been sufficiently studied while previous works often assumed a Gaussian distribution [20, 21, 22, 23, 9, 24]. By choosing the appropriate probability distribution, the bias in the objective function such as likelihood, become further reduced, and the prediction accuracy, especially the point estimation performance, can be improved.

References

- [1] Raphaël Dang-Nhu, Gagandeep Singh, Pavol Bielik, and Martin Vechev. Adversarial attacks on probabilistic autoregressive forecasting models. In Proceedings of International Conference on Machine Learning (ICML), 2020.

- [2] David Salinasa, Michael Bohlke-Schneider, Laurent Callot, Roberto Medico, and Jan Gasthaus. High-dimensional multivariate forecasting with low-rank gaussian copula processes. In Advances in neural information processing systems, 2019.

- [3] Amazon web services (aws) - cloud computing services. https://aws.amazon.com.

- [4] Oracle retail demand forecasting cloud service. https://www.oracle.com/industries/retail/products/supply-chain-planning/demand-forecasting/.

- [5] H. Kim, A. Mnih, J. Schwarz, M. Garnelo, A. Eslami, D. Rosenbaum, O. Vinyals, and Y.W. Teh. Attentive neural processes. In Proceedings of International Conference on Learning Representations, 2019.

- [6] David Salinas, Valentin Flunkert, Jan Gasthaus, and Tim Januschowski. Deepar: Probabilistic forecasting with autoregressive recurrent networks. International Journal of Forecasting, 36(3):1181–1191, 2020.

- [7] Ye-Sheen Lim and Denise Gorse. Deep probabilistic modelling of price movements for high-frequency trading. arXiv preprint arXiv:2004.01498, 2020.

- [8] Zachary C. Lipton and Jacob Steinhardt. Troubling trends in machine learning scholarship. arXiv preprint arXiv:1807.03341, 2018.

- [9] Syama Sundar Rangapuram, Matthias W Seeger, Jan Gasthaus, Lorenzo Stella, Yuyang Wang, and Tim Januschowski. Deep state space models for time series forecasting. In Advances in neural information processing systems, pages 7785–7794, 2018.

- [10] Sean J Taylor and Benjamin Letham. Forecasting at scale. The American Statistician, 72(1):37–45, 2018.

- [11] Georg M. Goerg. Forecastable component analysis. In Proceedings of the 30th International Conference on Machine Learning, 2013.

- [12] Alex Graves. Generating sequences with recurrent neural networks. arXiv preprint arXiv:1308.0850, 2013.

- [13] Ilya Sutskever, Oriol Vinyals, and Quoc V Le. Sequence to sequence learning with neural networks. In Advances in neural information processing systems, pages 3104–3112, 2014.

- [14] Rudolph Emil Kalman. A new approach to linear filtering and prediction problems. Journal of basic Engineering, 82(1):35–45, 1960.

- [15] Greg Welch, Gary Bishop, et al. An introduction to the kalman filter, 1995.

- [16] Adam Paszke, Sam Gross, Francisco Massa, Adam Lerer, James Bradbury, Gregory Chanan, Trevor Killeen, Zeming Lin, Natalia Gimelshein, Luca Antiga, Alban Desmaison, Andreas Kopf, Edward Yang, Zachary DeVito, Martin Raison, Alykhan Tejani, Sasank Chilamkurthy, Benoit Steiner, Lu Fang, Junjie Bai, and Soumith Chintala. Pytorch: An imperative style, high-performance deep learning library. In Advances in Neural Information Processing Systems 32, pages 8026–8037. Curran Associates, Inc., 2019.

- [17] Alexander Alexandrov, Konstantinos Benidis, Michael Bohlke-Schneider, Valentin Flunkert, Jan Gasthaus, Tim Januschowski, Danielle C Maddix, Syama Rangapuram, David Salinas, Jasper Schulz, et al. Gluonts: Probabilistic time series models in python. arXiv preprint arXiv:1906.05264, 2019.

- [18] Andreas Doerr, Christian Daniel, Martin Schiegg, Duy Nguyen-Tuong, Stefan Schaal, Marc Toussaint, and Sebastian Trimpe. Probabilistic recurrent state-space models. arXiv preprint arXiv:1801.10395, 2018.

- [19] Roger Frigola, Yutian Chen, and Carl Edward Rasmussen. Variational gaussian process state-space models. In Advances in neural information processing systems, pages 3680–3688, 2014.

- [20] Rahul G Krishnan, Uri Shalit, and David Sontag. Deep kalman filters. arXiv preprint arXiv:1511.05121, 2015.

- [21] Maximilian Karl, Maximilian Soelch, Justin Bayer, and Patrick Van der Smagt. Deep variational bayes filters: Unsupervised learning of state space models from raw data. arXiv preprint arXiv:1605.06432, 2016.

- [22] Rahul G Krishnan, Uri Shalit, and David Sontag. Structured inference networks for nonlinear state space models. arXiv preprint arXiv:1609.09869, 2016.

- [23] Jung-Su Ha, Young-Jin Park, Hyeok-Joo Chae, Soon-Seo Park, and Han-Lim Choi. Adaptive path-integral autoencoders: Representation learning and planning for dynamical systems. In Advances in Neural Information Processing Systems, pages 8927–8938, 2018.

- [24] Yuyang Wang, Alex Smola, Danielle C Maddix, Jan Gasthaus, Dean Foster, and Tim Januschowski. Deep factors for forecasting. arXiv preprint arXiv:1905.12417, 2019.

Appendix

Appendix A Parameterizaion of likelihood function for DeepAR

This paper follows the parameterization methods described in the references [6, 17] for of DeepAR. To be specific, we parameterize the model for a Gaussian likelihood distribution by using two affine functions:

| (7) | |||

where is a likelihood function of normal distribution. The negative binomial distribution is parameterized as follows:

| (8) | |||

Appendix B Estimation of joint distribution of future time series for DeepState

Unlike the auto-regressive models such as DeepAR, DeepState uses the observation values to compute the posterior distribution of latent state at each time step. Especially, DeepState integrates Kalman filtering [14, 15] into the model to estimate the analytical solution for the posterior: . From the estimated posterior, DeepState predict the conditional joint distribution of future time series as follows:

| (9) |

Although the joint distribution is analytically tractable, it is evaluated by Monte Carlo approaches for the sake of implementation convenience following the reference paper.

Appendix C Additional Results

The mean and standard deviation value reported in following tables and figures are calculated over hyperparameter samples.

C.1 DeepAR

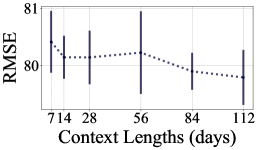

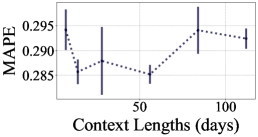

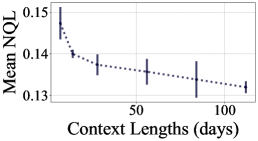

To illsutrate the effect of important hyperparameters to the performance of DeepAR, we report the result with different scaling methods, output distribution, context length, and number of RNN layers. As reported in Section 4.1, applying scaling method is essential to achieve desirable performance. The longer the context length is, the better the RMSE and the mean NQL are. The output distribution and number of RNN layers slightly varies the performance: negative binomial distribution is shown to be better fits to our EC dataset, and the performance drops as the number of layers increases probably due to the overfitting.

C.2 DeepState

Primarily, we address the performance of DeepState with fully-learnable (FL) SSMs and partially-learnable (PL) SSMs. We perform experiments with different context lengths and report each metrics’s best mean score in Table 5 and Fig. 4. The performance of both models approximately converges after 56 days of context lengths. The model with FL SSMs shows inaccurate and imprecise performance, and this appears to be a problem of the inherent lack of representation power in the model and non-identifiability problem [18, 19] caused by SSMs’ extreme flexibility.

Secondly, we compare the DeepState with different scaling methods: mean and median scalers. The performance degrades significantly when the scaler is not used. Empirically found that the model without scaler occasionally raise error when it calls Cholesky decomposition operator in Kalman filtering.

| Model | RMSE | MAPE | Mean NQL[0.1, 0.9] |

|---|---|---|---|

| DeepAR w/ mean scaler | 81.372.60 | 0.3030.013 | 0.1400.008 |

| DeepAR w/ median scaler | 81.061.07 | 0.3000.008 | 0.1390.006 |

| DeepAR w/o scaler | 94.081.59 | 0.3080.005 | 0.1620.007 |

| DeepState w/ mean Scaler | 87.88 11.00 | 0.342 0.022 | 0.169 0.028 |

| DeepState w/ median scaler | 114.68 124.45 | 0.365 0.118 | 0.211 0.140 |

| DeepState w/o scaler | 150.91 101.84 | 0.671 0.297 | 0.427 0.238 |

| Model | RMSE | MAPE | Mean NQL[0.1, 0.9] |

|---|---|---|---|

| DeepAR w/ 3-layer GRU | 80.21 0.34 | 0.288 0.002 | 0.135 0.002 |

| DeepAR w/ 5-layer GRU | 79.91 0.40 | 0.294 0.007 | 0.136 0.001 |

| DeepState w/ 3-layer GRU | 120.45 89.05 | 0.467 0.268 | 0.271 0.210 |

| DeepState w/ 5-layer GRU | 115.20 103.49 | 0.450 0.203 | 0.266 0.182 |

| Model | RMSE | MAPE | Mean NQL[0.1, 0.9] |

|---|---|---|---|

| DeepAR w/ Gaussian output | 80.500.87 | 0.2970.004 | 0.1400.006 |

| DeepAR w/ Negative Binomial output | 80.871.27 | 0.2960.008 | 0.1380.006 |

| Model | RMSE | MAPE | Mean NQL[0.1, 0.9] |

|---|---|---|---|

| DeepState w/ partially-learnable SSMs | 93.83 11.51 | 0.373 0.077 | 0.200 0.042 |

| DeepState w/ fully-learnable SSMs | 141.82 131.80 | 0.545 0.304 | 0.338 0.256 |

| Model | RMSE | MAPE | Mean NQL[0.1, 0.9] |

|---|---|---|---|

| Prophet w/ additive seasonality | 83.891.98 | 0.4610.038 | 0.2020.009 |

| Prophet w/ multiplicative seasonality | 97.0216.85 | 0.4600.044 | 0.2220.010 |