Policy Gradient Methods for the Noisy Linear Quadratic Regulator over a Finite Horizon

Abstract

We explore reinforcement learning methods for finding the optimal policy in the linear quadratic regulator (LQR) problem. In particular we consider the convergence of policy gradient methods in the setting of known and unknown parameters. We are able to produce a global linear convergence guarantee for this approach in the setting of finite time horizon and stochastic state dynamics under weak assumptions. The convergence of a projected policy gradient method is also established in order to handle problems with constraints. We illustrate the performance of the algorithm with two examples. The first example is the optimal liquidation of a holding in an asset. We show results for the case where we assume a model for the underlying dynamics and where we apply the method to the data directly. The empirical evidence suggests that the policy gradient method can learn the global optimal solution for a larger class of stochastic systems containing the LQR framework and that it is more robust with respect to model mis-specification when compared to a model-based approach. The second example is an LQR system in a higher dimensional setting with synthetic data.

1 Introduction

The Linear Quadratic Regulator (LQR) problem is one of the most fundamental in optimal control theory. Its aim is to find a control for a linear dynamical system, that is the dynamics of the state of the system is described by a linear function of the current state and input, subject to a quadratic cost. It is an important problem for a number of reasons: (1) the LQR problem is one of the few optimal control problems for which there exists a closed-form analytical representation of the optimal feedback control; (2) when the dynamics are nonlinear and hard to analyze, a LQR approximation may be obtained as a local expansion and provide an approximation that is provably close to the original problem; (3) the LQR has been used in a wide variety of applications. In particular, in the set-up of fixed time horizon and stochastic dynamics, applications include portfolio optimization [3] and optimal liquidation [7] in finance, resource allocation in energy markets [40, 45], and biological movement systems [34].

Until recently much of the work on the LQR problem has focused on solving for the optimal controls under the assumption that the model parameters are fully known. See the book of Anderson and Moore [9] for an introduction to the LQR problem with known parameters. However, assuming that the controller has access to all the model parameters is not realistic for many applications, and this has lead to the exploration of learning approaches to the problem. We consider reinforcement learning (RL), one of the three basic machine learning paradigms (alongside supervised learning and unsupervised learning). Unlike the situation with full information on the model parameters, RL is learning to make decisions via trial and error, through interactions with the (partially) unknown environment. In RL, an agent takes an action and receives a reinforcement signal in terms of a numerical reward, which encodes the outcome of her action. In order to maximize the accumulated reward over time, the agent learns to select her actions based on her past experiences (exploitation) and/or by making new choices (exploration). There are two popular approaches in RL to handle the LQR with unknown parameters: the model-based approach and the model-free approach.

In the paradigm of the model-based approach, the controller estimates the unknown model parameters and then constructs a control policy based on the estimated parameters. The classical approach is the certainty equivalence principle [10]: the unknown parameters are estimated using observations (or samples), and a control policy is then designed by treating the estimated parameters as the truth. In the first step, the unknown model parameters can be estimated by standard statistical methods such as least-square minimization [20]. The second step is to show that when the estimated parameters are accurate enough, the policy using the “plug-in” estimates enjoys good theoretical guarantees of being close to optimal. See [20] and [24] for the optimal gap and sample complexities along this line and see [22] for the sample complexity with distributed robust learning. Another line of work in the model-based regime focuses on uncertainty quantification. The controller updates their posterior belief or the confidence bounds on the unknown model parameters and then makes decisions in an online manner, see [1, 2, 21, 31, 39].

Another recently developed approach is the model-free approach, where the controller learns the optimal policy directly via interacting with the system, without inferring the model parameters. As the optimal policy in the LQR problem is a linear function of the state, the aim is to determine this linear function. This is equivalent to learning a set of parameters in matrix form, called the policy matrix. One natural way to achieve this goal is to apply the gradient descent method in the parameter space of the policy matrix, also referred to as the policy gradient method. In particular, the policy gradient method computes the gradient of the cost function with respect to the policy matrix and then updates the policy in the steepest decent direction to find the optimal policy. The paper [23] was the first to show that policy gradients converge to the global optimal solution with polynomial (in the relevant quantities) sample complexity. However, [23] focuses on the case where the only noise in the system is in the initial state, and the rest of the state transitions are deterministic. There are other methods that fall into the category of the model-free approach, including the Actor-Critic method [46] and least-squares temporal difference learning [43].

If the true system is indeed linear-quadratic, the model-based approaches (may) outperform the model-free approaches by fully utilizing the linear-quadratic structure. For example in the setting that the system transition matrices are unknown and the parameters in the cost function are known, [42] and [44] showed that model-based methods are (asymptotically) more sample-efficient than some popular model-free methods. However, we are often uncertain about whether the actual system is linear-quadratic in the learning setting; for instance there might be some small nonlinear terms in the system dynamics. Therefore, compared to the model-based approach, which strongly relies on the assumption that the stochastic system lies within the LQR framework and may, in practice, suffer from model mis-specification, the execution of the model-free algorithm does not rely on the assumptions of the model. It has been shown that the policy gradient method can learn the global optimal solution, not only for the LQR framework, but also for a more general class of deterministic systems in the setting of an infinite time horizon [13]. Thus the advantage of the model-free approach is that it is more robust against model mis-specification compared to the model-based approach.

Our Contributions.

We now summarize our contributions. Motivated by many real-word decision-making problems with a fixed deadline and uncertainty in the underlying dynamics, such as the optimal liquidation problem that we discuss in Section 2, we extend the framework of [23] by incorporating a finite time horizon and sub-Gaussian noise (which includes Gaussian noise as a special case). In particular, we provide a global linear convergence guarantee and a polynomial sample complexity guarantee for the policy gradient method in this setting with both known parameters (Theorem 3.3) and unknown parameters (Theorem 4.4). The analysis with known parameters paves the way for learning LQR with unknown parameters. In addition, numerically solving the Riccati equation with known parameters in high dimensions may suffer from computational inaccuracy. The policy gradient method provides a direct way of searching for the optimal solution with known parameters in this case, which may be of separate interest. Note that the optimal policy is time-invariant for the LQR with infinite time horizon, whereas the optimal policy is time-dependent with finite time horizon and hence harder to learn in general. With noise in the dynamics, we need more careful choices of the hyper-parameters to retrieve compatible sample complexities with noisy observations. In addition, when optimal polices need to satisfy certain constraints, we provide a global convergence result for the projected policy gradient method in Theorem 4.5. This is required in the context of our application to the optimal liquidation problem.

We will formulate the optimal liquidation problem over a fixed horizon as a noisy LQR problem which is essentially the classical Almgren-Chriss formulation [7]. The performance of the algorithm on NASDAQ ITCH data is assessed. As well as using the method within this modelling approach, we also consider the performance of the policy gradient method when applied directly to the data with an appropriate cost function. This improves the performance of the LQR/Almgren-Chriss solution and shows promising results for the use of the policy gradient method for problems that are ‘close’ to the LQR framework.

1.1 Related Work

Policy Gradient Methods for LQR Problems.

Since the policy gradient method is the main focus of our paper, here we provide a review of the previous theoretical work on this method in various LQR settings and extensions. The first global convergence result for the policy gradient method to learn the optimal policy for LQR problems was developed in [23] in the setting of infinite horizon and deterministic dynamics. The work of [23] was extended in [13] to give global optimality guarantees of policy gradient methods for a larger class of control problem that includes the linear-quadratic case. In particular, this class of control problem satisfies a closure condition under policy improvement and convexity of policy improvement steps. The paper [14] considers policy gradient methods for LQR problems in terms of optimizing a real valued matrix function over the set of feedback gains. The extension of the policy gradient method to continuous-time can be found in [15]. All of these methods are in the infinite horizon setting and without the addition of noise in the dynamics.

There has been some work on the case of noisy dynamics, but all in the setting of infinite horizon. In [27] the problem with a multiplicative noise was discussed, using a relatively straightforward extension of the deterministic dynamics considered in the original framework. In the case of additive noise [32] studies the global convergence of policy gradient and other learning algorithms for the LQR over an infinite time-horizon and with Gaussian noise. In particular, the policy considered in [32] is a randomized policy with Gaussian distribution. There is also [35] which studies derivative-free (zeroth-order) policy optimization methods for the LQR with bounded additive noise. Finally some other contributions can be found in [16, 47] for zero-sum LQR games and [17, 29] for mean-field LQR games.

Compared to [23], our technical difficulties are three-fold. First due to the time-dependent nature of the admissible policies over a finite-horizon and randomness from the system noise, we need additional conditions and analysis to guarantee the well-definedness of the state process, i.e., the non-degeneracy of the controlled state-covariance matrices. This holds almost for free in the infinite horizon case with deterministic dynamics. Second, we need to take care of the additional randomness from the sub-Gaussian noise when developing the perturbation analysis and the gradient dominant condition. Third, we need more advanced concentration inequalities and tighter upper bounds to provide compatible sample complexity analysis in the unknown parameter case. See the more detailed discussion in Remark 4.12.

Optimal Liquidation.

An early mathematical framework for the optimal liquidation problem is due to Almgren and Chriss [7]. In this problem a trader is required to liquidate a portfolio of shares over a fixed horizon. The selling of a large number of shares at once has both temporary and permanent impacts on the share price causing it to decrease. The trader therefore wishes to find a trading strategy which maximizes their return from, or alternatively, minimizes the cost of, the liquidation of the portfolio subject to a given level of risk.

This problem has been considered in many papers and extended in many directions. See for instance [5], [6] and [26]. We will cast this as an LQR problem and show how the policy gradient method is a powerful tool for solving this problem even without assumptions on the model.

More recently techniques from reinforcement learning have been applied to the optimal liquidation problem. The first paper to do this was [37] where the authors showed promising results for this approach by designing a Q-learning based algorithm to optimally select price levels and passively place limit orders. This was further developed in [30] which designed a Q-learning based algorithm for liquidation within the standard Almgren-Chriss framework. For recent work incorporating deep learning see for example [11], [33], [38], and [48]. See [18] for a detailed review on reinforcement learning with applications in finance and economics, and the references therein. However, all these works focus on the model-free setting without taking advantage of even weak modelling assumptions on the market dynamics. In addition, the performances of these proposed algorithms are validated only through empirical studies and no theoretical guarantee of convergence is provided.

Organization and Notation.

For any matrix with (), denote the transpose of , denotes the spectral norm of a matrix ; denotes the trace of a square matrix ; denotes the Frobenius norm of a matrix ; denotes the minimal singular value of a square matrix ; and denote the vectorized version of a matrix . For a sequence of matrices , we define a new norm as , where . Further denote as the Gaussian distribution with mean and covariance matrix .

The rest of the paper is organized as follows. We introduce the mathematical framework and problem set-up in Section 2. The first step in our convergence analysis of the policy gradient method is to consider the case of known model parameters in Section 3. When parameters are unknown, the convergence results for the sample-based policy gradient method and projected policy gradient method are obtained in Section 4. Finally, the algorithm is applied to liquidation problem. See Sections 2.1 and 5 for the corresponding set-up and algorithm performance, respectively.

2 Problem Set-up

We consider the following LQR problem over a finite time horizon ,

| (2.1) |

such that for ,

| (2.2) |

Here is the state of the system with the initial state drawn from a distribution , is the control at time and are zero-mean IID noises which are independent from . At this moment, we only assume and have finite second moments. That is, and exist. The system parameters and are referred to as system (transition) matrices; ) and ) are matrices that parameterize the quadratic costs. Note that the expectation in (2.1) is taken with respect to both and (). We further denote by , , , , and , the profile over the decision period .

To solve the LQR problem (2.1)-(2.2), let us start with some conditions on the model parameters to assure the well-definedness of the problem.

Assumption 2.1 (Cost Parameter).

Assume , for , and , for , are positive definite matrices.

Under Assumption 2.1, we can properly define a sequence of matrices as the solution to the following dynamic Riccati equation [12]:

| (2.3) |

with terminal condition The matrices can be found by solving the Riccati equations iteratively backwards in time. In particular with a slight modification of the initial state distribution in [12, Chapter 4.1], we have the following result.

Lemma 2.2 (Well-definedness and the Optimal Solution [12]).

To find the optimal solution in the linear feedback form (2.4), we only need to focus on the following class of linear admissible policies in feedback form

| (2.6) |

which can be fully characterized by .

2.1 Application: The Optimal Liquidation Problem

One application of the LQR framework (2.1)-(2.2) is the optimal liquidation problem. We give a slight variant of the setup of Almgren-Chriss [7]. Our aim is to liquidate an amount of an asset, with price at time 0, over the time period with trading decisions made at discrete time points . At each time our decision is to liquidate an amount of the asset. Any residual holding is then liquidated at time . This will have two types of price impact. There will be a temporary price impact, caused when the order ‘walks the book’ and a permanent price impact as traders rearrange their positions in the light of the sell order. We will assume the impacts are linear in the number of traded shares.

We write for the asset price at time . This evolves according to a Bachelier model with a linear permanent price impact in that

where, for each , is an independent standard normal random variable, is the volatility and is the permanent price impact parameter. The inventory process records the current holding in the asset at time . Thus we have

Therefore, the two-dimensional state process is

| (2.7) |

When selling shares we incur a temporary price impact, parameter , in that if, at time , we trade of our asset then we obtain per share. Therefore the total revenue is , and , the total cost of execution over , is the book value at time 0 minus the revenue:

In a similar way to [7], after summation by parts, we have

The mean and variance of the total cost of execution are given by

where summarizes the impact and is assumed positive.

Following Almgren-Chriss [7], we minimize the following cost function

| (2.8) |

where is a parameter balancing risk versus return. For our LQR framework we take the cost function to be

| (2.9) |

Note that the term , with some small , serves as a regularization term to guarantee Assumption 2.1 holds. In practice, we can show that the optimal solution with small is close to the Almgren-Chriss solution (when ). In addition, the algorithm will still converge with . See more discussion in Section 5. Thus, in the LQR formulation we have , , and and the objective function has , and . It is easy to see that , for and for are positive definite, hence Assumption 2.1 is satisfied.

We will show that the problem is well-defined and can be solved using the methods of this paper with rigorous convergence guarantees.

3 Exact Gradient Methods with Known Parameters

In this section we assume all the parameters in the model, , , , , are known. The analysis of exact gradient methods with known parameters paves the way for learning LQR with unknown parameters in Section 4. In addition, the policy gradient method provides an alternative way to solve the LQR problem when the parameters are fully known. In this setting the Riccati equation (2.3) is just solved backward in time. However this operation involves inverting large matrices when the problem is in high dimensions, which may lead to high computational cost and accumulation of computational errors.

Since an admissible policy can be fully characterized by , the cost of a policy can be correspondingly defined as

| (3.1) |

where and are the dynamics and controls induced by following , starting with . Recall that is the optimal policy for the problem, in that

| (3.2) |

subject to the dynamics (2.2).

Well-definedness of the State Process.

To prove the global convergence of policy gradient methods, the essential idea is to show the gradient dominance condition, which states that can be bounded by for any admissible policy . One of the key steps to guarantee this gradient dominance condition is the well-definedness of the state covariance matrix. That is, is positive definite for . This condition holds almost for free for LQR problems with infinite time horizon and deterministic dynamics. The only condition needed there is the positive definiteness of (See [23]). However, some effort needs to be made to ensure that the state covariance matrix is well-defined for LQR problems with finite horizon and stochastic dynamics. We show that this condition holds under moderate conditions.

Assumption 3.1 (Initial State and Noise Process).

We assume that

-

1.

Initial state: such that is positive definite;

-

2.

Noise: are IID and independent from such that , and is positive definite, .

Define as the lower bound over all the minimum singular values of :

| (3.3) |

then we have the following result and the proof can be found in Appendix C.1.

Lemma 3.2 (Well-definedness of the State Covariance Matrix).

Under Assumption 3.1, we have is positive definite for under any control policy . Therefore, .

Lemma 3.2 implies that if the initial state and the noise driving the dynamics are non-degenerate, the covariance matrices of the state dynamics are positive definite for any policy . However, the covariance matrix may be degenerate in many applications, especially when inventory processes are involved. (See, for example, the liquidation problem (2.7).) In this case, some problem-dependent conditions are needed to guarantee that holds. See more discussion on the condition for the liquidation problem in Section 5.1. In the light of this we will assume in the analysis of the convergence of the algorithm in Sections 3 and 4.

Similarly, we define and to be the smallest values of all the minimum singular values of and :

| (3.4) | |||||

| (3.5) |

Under Assumption 2.1, we have and .

We write and when there are other dependencies. The model parameters are in terms of , , , , , , , , , , , , , , and .

Exact Gradient Descent.

We consider the following exact gradient descent updating rule to find the optimal solution (3.2),

| (3.6) |

where is the number of iterations, is the gradient of with respect to , and is the step size. We further denote .

Let us define the state covariance matrix

| (3.7) |

where is a state trajectory generated by . Further define a matrix as the sum of ,

| (3.8) |

Then, the main result for this setting is the following.

Theorem 3.3 (Global Convergence of Gradient Methods).

The proof of Theorem 3.3 relies on the regularity of the LQR problem, some properties of the gradient descent dynamics, and the perturbation analysis of the covariance matrix of the controlled dynamics.

3.1 Regularity of the LQR Problem and Properties of the Gradient Descent Dynamics

Let us start with the analysis of some properties of the LQR problem (2.1)-(2.2).

To start, Proposition 3.4 focuses on the well-definedness of the Ricatti system induced by a control ; Lemma 3.5 gives a representation of the gradient term; Lemma 3.6 and Lemma 3.7 provide the gradient dominance condition and a smoothness condition on the cost function with respect to policy , respectively; and finally, Lemma 3.8 gives two useful upper bounds on Ricatti system and state covariance matrices.

In the finite time horizon setting, define as the solution to

| (3.9) |

with terminal condition

Note that (3.9) is equivalent to the Riccati equation (2.3) with optimal as given by (2.5). We have the following result on the well-definedness of and the proof can be found in Appendix C.1.

To ease the exposition, we write as when there is no confusion. Then the cost of can be rewritten as

where, for ,

| (3.10) |

with . To see this,

In addition, define

| (3.11) |

Then we have the following representation of the gradient term.

Lemma 3.5.

The policy gradient has the following representation, for ,

Proof.

Since

we have

Similarly, ,

where the expectation is taken with respect to both initial distribution and noises . ∎

In classical optimization theory [23], gradient domination and smoothness of the objective function are two key conditions to guarantee the global convergence of the gradient descent methods. To prove that is gradient dominated, we first prove Lemma 3.6, which indicates that for a policy , the distance between and the optimal cost is bounded by the sum of the magnitude of the gradient for .

Lemma 3.6.

We defer the proof of Lemma 3.6 to Appendix C.1. Lemma 3.6 implies that when the gradient becomes small, the value of the objective function is close to . Now we consider the smoothness condition of the objective function. Recall that a function is said to be smooth if

for some finite constant . In general, it is difficult to characterize the smoothness of , since it may blow up when is large. Here we will prove that is “almost” smooth, in the sense that when is sufficiently close to , is bounded by the sum of the first and second order terms in .

Lemma 3.7 (“Almost Smoothness”).

Let be the sequence of states for a single trajectory generated by starting from . Then, satisfies

| (3.12) |

where .

We defer the proof of Lemma 3.7 to Appendix C.1. To see why Lemma 3.7 is related to the smoothness, observe that when is sufficiently close to , in the sense that

the first term in (3.12) will behave as by Lemma 3.5, and the second term in (3.12) will be of second order in .

3.2 Perturbation Analysis of

First, let us define two linear operators on symmetric matrices. For we set

If we write , then

| (3.13) | |||||

| (3.14) |

We first show the relationship between the operator and the quantity . The proof can be found in Appendix C.1.

Proposition 3.9.

For , we have that

| (3.15) |

where with (for ), and .

Let

| (3.16) |

for some small constant . Then we have the following result on perturbations of .

Lemma 3.10 (Perturbation Analysis of ).

Assume Assumption 2.1 holds. Then

Remark 3.11.

By the definition of in (3.16), we have . This regularization term is defined for ease of exposition. Alternatively, if we define , a similar analysis can still be carried out by considering the different cases: , and . Note that for the infinite horizon problem, the spectral radius of needs to be smaller than 1 to guarantee the stability of the system (see [23]). In our setting with finite horizon, instability is not an issue and we do not need a condition on the boundedness of . However, we will show later that does appear in the sample complexity results. The smaller the , the smaller the sample complexity.

The proof of Lemma 3.10 is based on the following Lemmas 3.12 and 3.13, which establish the Lipschitz property for the operators and , respectively.

Lemma 3.12.

It holds that, ,

| (3.17) |

Recall the definition of in (3.13) associated with , similarly let us define for policy . Then we have the following perturbation analysis for .

Lemma 3.13 (Perturbation Analysis for ).

For any symmetric matrix , we have that

| (3.18) |

We defer the proof of Lemma 3.13 to Appendix C.2. The following perturbation analysis on follows immediately from Lemma 3.13.

Corollary 3.14.

Now we are ready for the proof of Lemma 3.10.

3.3 Convergence and Complexity Analysis

We now provide the proof of Theorem 3.3 after two preliminary Lemmas.

Lemma 3.15.

Lemma 3.16.

Proof.

Proof of Theorem 3.3.

In order to show the existence of a positive such that (3.23) holds, it suffices to show there exists a positive lower bound on the RHS of (3.23). By Lemma 3.16 and the Cauchy-Schwarz inequality,

| (3.26) |

Note that if for some , and , then . Also for and . Therefore, based on (3.24) and (3.26), is bounded below by polynomials in , , , , , , , , and .

Now we aim to show that is bounded below by some polynomials in the parameters. To see this, let us first show that is bounded above by polynomials in , , , , and . Since holds under the assumptions in Lemma 3.15, we have

| (3.27) |

Given the bound on by Lemma 3.16 and by Lemma 3.8, is bounded above by polynomials in , , , , and , or a constant . Therefore is bounded below by polynomials in , , , , and , or a constant . Hence, by choosing to be an appropriate polynomial in , , , , , , , , , , and , (3.23) is satisfied, since by performing gradient descent, . Therefore, by Lemma 3.15, we have

which implies that the cost decreases at . Suppose that , then the stepsize condition in (3.23) is still satisfied by Lemma 3.16. Thus, Lemma 3.15 can again be applied for the update at round to obtain:

For , provided , we have

∎

4 Sample-based Policy Gradient Method with Unknown Parameters

In the setting with unknown parameters, the controller has only simulation access to the model; the model parameters, , , , , are unknown. By using a zeroth-order optimization method to approximate the gradient, this section proves the policy gradient method with unknown parameters also leads to a global optimal policy, with both polynomial computational and sample complexities.

Note that in this section, when bounding the Frobenius norm of a matrix, we usually treat the matrix as a stacked vector. Therefore we denote by the dimension of the corresponding vector formed from the matrix for convenience in the proofs. Therefore in each iteration , we can update the policy as, for ,

| (4.1) |

where is the estimate of . We analyze the following Algorithm 1.

| (4.2) |

Remark 4.1.

[Zeroth-order Optimization Approach in the Sub-routine (4.2)] In the estimation of the gradient term (4.2), we adopt a zeroth-order optimization method, using only query access to a sample of the reward function at input points , without querying the gradients and higher order derivatives of . In a similar way to the observation in [23], the objective may not be finite for every policy when Gaussian smoothing is applied, therefore may not be well-defined. This is avoidable by smoothing over the surface of a ball. The step (4.2) (in Algorithm 1) provides a procedure to find an (bounded bias) estimate of .

The idea in (4.2) is to approximate the gradient of a function by only using the function values (see e.g. Lemma 2.1 in [25]). Observe that by a Taylor expansion to first order when and is uniform over the surface of the ball of radius in . Thus the gradient of the function at can be estimated by averaging over the samples .

Note that in Algorithm 1, we require samples to perform the policy gradient method times.

To guarantee the global convergence of the sample-based algorithm (Algorithm 1), we propose some conditions on the distribution of and , in addition to the finite second moment condition specified in Section 2.

Definition 4.2.

A zero-mean random variable

-

1.

is said to be sub-Gaussian with variance proxy and we write if its moment generating function satisfies for all .

-

2.

is said to be sub-exponential with parameters and we write , if for any such that .

We assume the initial distribution and the noise in the state process dynamics satisfy the following assumptions.

Assumption 4.3 (Initial State and Noise Process (II)).

-

1.

Initial state: where

is a random vector with independent components which are sub-Gaussian, mean-zero, and have sub-Gaussian parameter ; is an unknown and deterministic matrix. -

2.

Noise process: where are IID and independent from . has independent components which are sub-Gaussian, mean-zero, and have sub-Gaussian parameter , . is an unknown and deterministic matrix.

Note that Assumptions 3.1 and 4.3 serve different purposes in this paper. Assumption 3.1 provides one sufficient condition to assure . Assumption 4.3 is used to guarantee the convergence of the sample based algorithm (Algorithm 1).

In addition to the model parameters specified in Section 3, here we assume includes polynomials that are also functions of , , , , , ,, , , , and .

Theorem 4.4.

Note that is quadratic in (when the logarithmic order is omitted) and cubic in dimension . The proof of Theorem 4.4 is based on a perturbation analysis of and , smoothing and the gradient descent analysis of the procedures in Algorithm 1. We provide the perturbation analysis and the smoothing analysis in Sections 4.1 and 4.2, respectively. We defer the proof of Theorem 4.4 to Section 4.3.

Projected Policy Gradient Method.

In many situations constrained optimization problems arise and the projected gradient descent method is one popular approach to solve such problems. Recall the projection of a point with () onto a set is defined as

| (4.3) |

Then the projected policy gradient (PPG) updating rule can be defined as

| (4.4) |

where denotes the estimate of .

If the projection set is convex and closed, the projection onto is non-expansive, that is,

with and . Given any policy matrix and learning rate , define the gradient mapping for the projection operator

| (4.5) |

with . Note that the gradient mapping has been commonly adopted in the analysis of projected gradient descent methods in constrained optimization [36, 47]. A policy matrix is called a stationary point of if

| (4.6) |

It is well-known in the optimization literature that (4.6) holds if and only if . We have the following sub-linear convergence result for the PPG version.

Theorem 4.5.

Assume Assumptions 2.1 and 4.3 hold, and the projection set of policies, denoted by , is convex and closed. Further assume , , and is finite. At every step the policy is updated as in (4.4), that is

with and is computed with hyper-parameters such that and with some fixed polynomials and . Then the projected policy gradient method has a global sublinear convergence rate, that is, converges to 0 at rate , where is defined in (4.5).

Remark 4.6.

We assume the projection step is perform accurately and the associated computational cost is of a separate interest and hence omitted here. The convergence result in Theorem 4.5 is described in terms of the sample complexity and to perform the projection step does not need extra samples.

4.1 Perturbation analysis of and

This section shows that the objective function and its gradient are stable with respect to small perturbations. The proofs of the following Lemmas can be found in Appendix C.4.

Lemma 4.7 ( Perturbation).

Lemma 4.8 ( Perturbation).

Under the same assumptions as in Lemma 4.7, there exists a polynomial such that

4.2 Smoothing and the Gradient Descent Analysis

In this section, Lemma 4.9 provides the formula for the perturbed gradient term, Lemma 4.10 provides the concentration inequality for finite samples, and Lemma 4.11 provides the guarantees for the gradient approximation.

Recall that . Let represent the uniform distribution over the points with norm in dimension , and represent the uniform distribution over all points with norm at most in dimension . For each , the algorithm performs gradient descent on the following function:

| (4.8) |

where and .

Lemma 4.9.

Assume is finite,

| (4.9) |

We first state two facts on sub-Gaussian and sub-exponential random variables. Firstly, if and are zero-mean independent random variables such that and , then . Secondly, if are zero-mean independent random variables such that , then

Using the above two facts, we have the following.

Lemma 4.10.

Proof.

We first observe that, by direct calculation,

| (4.10) |

Define

as the average of perturbed cost functions across scenarios which is an empirical approximation of (4.9). Similarly, define

| (4.13) |

as the average of perturbed and single-trajectory-based cost functions across scenarios, which is the same as (4.2) in Algorithm 1. Note that in order to calculate , we require access to , which involves the calculation of expectations with respect to unknown initial states and state noises. This may be restrictive in some settings. On the other hand, the calculation of only involves single-trajectory-based cost functions.

Lemma 4.11.

Assume Assumptions 2.1 and 4.3 hold, and . Given any , there are fixed polynomials and such that when , with samples of for each ,

holds with high probability (at least ). In addition, there is a polynomial such that when , with samples of for each ,

holds with high probability (at least ). Here, for each , and are the dynamics and controls for a single path sampled using policy .

Proof.

For the first term, choose ( is chosen later), where is defined in Lemma 4.8. By Lemma 4.8 when , for where , we have

| (4.14) |

Since , we have

by (4.14) and the continuity of . Therefore

| (4.15) |

holds by triangle inequality. We choose such that for any , we have that . By Lemma 4.7, we can pick , then .

For the second term, by Lemma 4.9, , and each individual sample is bounded by , so by the Operator-Bernstein inequality [28, Theorem 12] with

we have

| (4.16) |

Note that since . Adding these two terms together and applying the triangle inequality gives the result.

For the second part, note that

| (4.17) |

By Lemma 4.10,

is sub-exponential with parameters . Therefore,

is sub-exponential matrix with parameters . Then by Operator-Berinstein inequality [28, Theorem 12],

when . That is, there exists a polynomial where

such that when ,

| (4.18) |

Combining (4.18) with (4.15) and (4.16), we arrive at the desired result. ∎

4.3 Proof of Theorem 4.4

Proof of Theorem 4.4.

By Lemma 3.15 and by choosing such that the step size condition (3.23) is satisfied,

Recall the definition of in (4.13) and let be the iterate that uses the approximate gradient. We will show later that given enough samples, the gradient can be estimated with enough accuracy that makes sure

| (4.19) |

That means as long as , we have

Then the same proof as that of Theorem 3.3 gives the convergence guarantee.

Now let us prove (4.19). First note that is bounded. By Lemma 4.7, if , where is the polynomial in Lemma 4.7, then (4.19) holds. To get this bound, recall in (3.22) and writing for ease of exposition, observe that , therefore it suffices to make sure

By Lemma 4.11, it is enough to pick

, and

This gives the desired upper bound on with high probability (at least ).

Since the number of steps is a polynomial, we have . By the union bound with probability at least

we have , . Therefore,

| (4.20) |

This implies . To guarantee that (4.20) holds at each iteration , it suffices to pick and . The rest of the proof is the same as that of Theorem 3.3. Note again that in the smoothing, because the function value is monotonically decreasing, and by the choice of radius, all the function values encountered are bounded by , so the polynomials are indeed bounded throughout the algorithm. ∎

4.4 Discussion

Remark 4.12 (Comparison with [23]).

The proofs of our main results, Theorems 3.3 and 4.4, are different to those from [23]. Firstly, to prove the gradient dominant condition, [23] only required conditions on the distribution of the initial position. However, we need conditions to guarantee the non-degeneracy of the state covariance matrix at any time. Secondly, the extra randomness from the sub-Gaussian noise needs to be taken care of in the perturbation analysis of . Finally, we need more advanced concentration inequalities to provide the number of samples and number of simulation trajectories that leads to the theoretical guarantee in the case with unknown parameters.

Remark 4.13 (Non-stationary Dynamics).

Note that our framework can be generalized to non-stationary dynamics, that is, for ,

| (4.21) |

with and time-dependent state parameters.

Remark 4.14 (Other Policy Gradient Methods).

Our convergence and sample complexity analysis could be applied to other policy gradient methods, including the Natural policy gradient method and the Gauss-Newton method, in the framework of the LQR with stochastic dynamics and finite horizons.

5 Numerical Experiments

The performance of the PPG algorithm (4.4) is demonstrated for the optimal liquidation problem with single asset and the empirical analysis of the policy gradient method (4.1) in higher dimensions is also provided with synthetic data. We will specifically focus on the following questions.

-

•

In practice, how fast do the policy gradient algorithm and the PPG algorithm with known and unknown parameters converge to the true solution?

-

•

How does the deadline (the finite horizon) influence the optimal policy?

-

•

When the real-word system does not exactly follow the LQR framework, does the policy-gradient method outperform mis-specified LQR models?

This section is organized as follows. We demonstrate the performance of the PPG algorithms for the optimal liquidation problem with a single asset in the LQR framework in Section 5.1. We then show that without the LQR model specification, the learned policy from the policy gradient algorithm improves the Almgren-Chriss solution in Section 5.2. Finally, we test the performance of the algorithm with unknown parameters in high dimensions in Section 5.3.

Note the policy gradient method outperforms the Q-learning algorithm, a popular model-free method, in terms of both sample complexity and accuracy in our setting. An illustration in a one-dimensional example can be found in the Appendix B.

5.1 Optimal Liquidation within the LQR Framework

Recall the set up of the optimal liquidation problem in (2.1). By convention, we write the control in the feedback form as . Writing , we have , the state equation becomes

In the liquidation problem, we assume . That is, and .

Assumption 5.1 (Assumptions for the Optimal Liquidation Problems).

We assume

-

(1)

;

-

(2)

.

Justification of the Assumption.

Assumption 5.1-(1) is essential to ensure that the liquidation problem is well defined. First, makes sure that the stock price process is well-behaved:

If , then since . Second, guarantees that inventory will not be negative. Note that

If and , then . Assumption 5.1-(2) implies that the temporary market impact is “bigger” than one half of the permanent market impact, which is consistent with the empirical evidence [8] and assumptions in [7].

Learning to Liquidate.

In practice, traders may not know the market impact parameter . But one can always take some based on some basic understandings of the market and perform a PPG algorithm to the closed convex set :

| (5.1) |

with some small parameter .

In practice is usually on the order of (See Table 3 in Appendix A) and hence a universal upper bound in (5.1) is not a strong assumption for a given portfolio of stocks to liquidate.

Proposition 5.2.

The proof of Proposition 5.2 is deferred to Appendix C.5. It is easy to check that the projection set defined in (5.1) is convex and closed. Along with Proposition 5.2, the convergence result in Theorem 4.5 holds for the liquidation problem (2.7) and (2.9) as long as the conditions in Proposition 5.2 are satisfied.

We test the performance of the PPG algorithm with projection set on Apple (AAPL) and Facebook (FB) stocks. The market simulator of the associated LQR framework is constructed with NASDAQ ITCH data and the details can be found in Appendix A.

Performance Measure.

We use the following normalized error to quantify the performance of a given policy ,

where is the optimal policy defined in (2.5).

Set-up.

(1) Parameters: (for both AAPL and FB), , ; smoothing parameter , number of trajectories ; initial policy with for all , , for both algorithms with known and unknown parameters; step sizes are indicated in the figures; , for the projection set. (2) Initialization: Assume the initial inventory follows . The small variance of the initial inventory distribution is used to guarantee the initial state covariance matrix is positive definite. In practice, the algorithm converges with deterministic initial inventories.

Convergence.

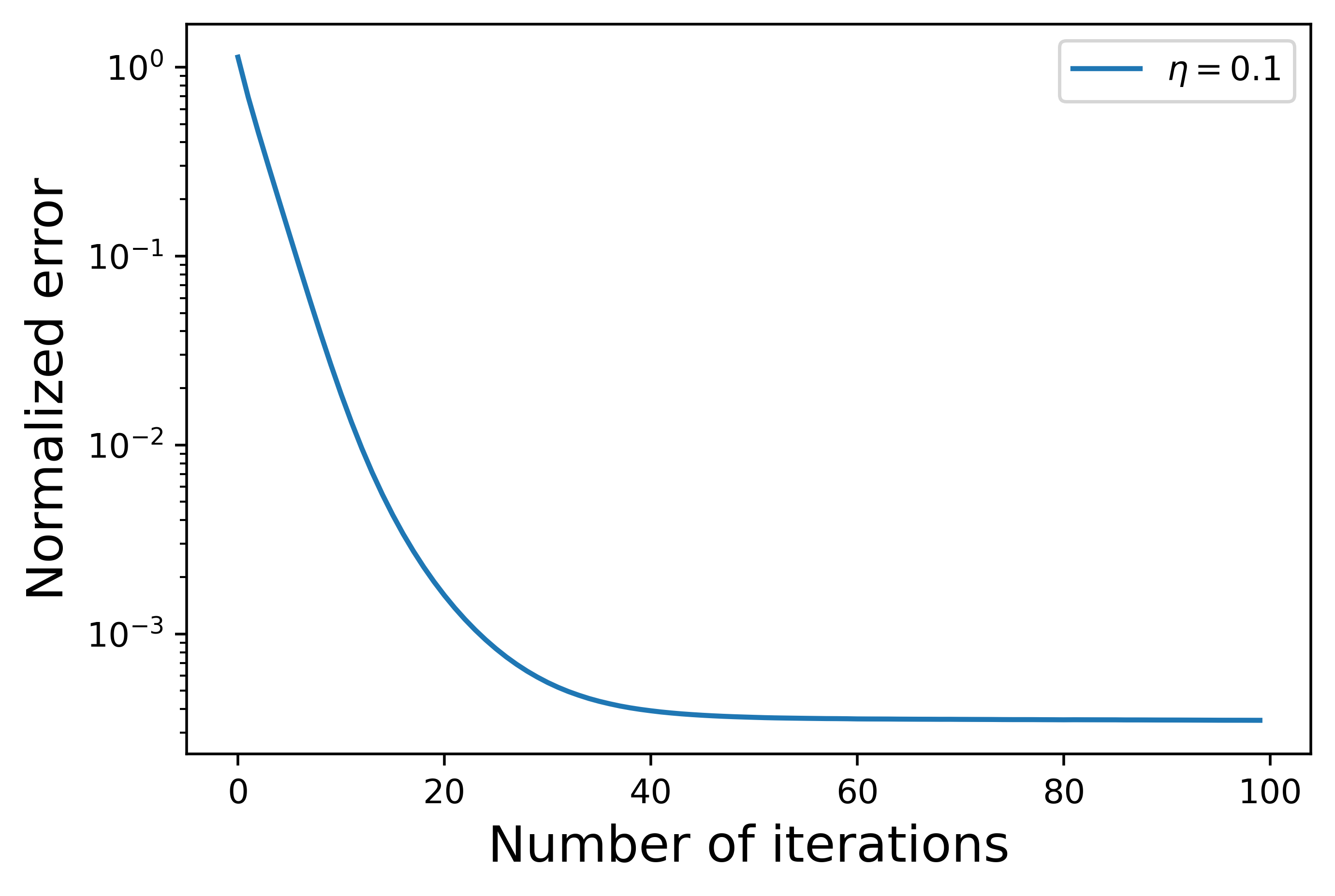

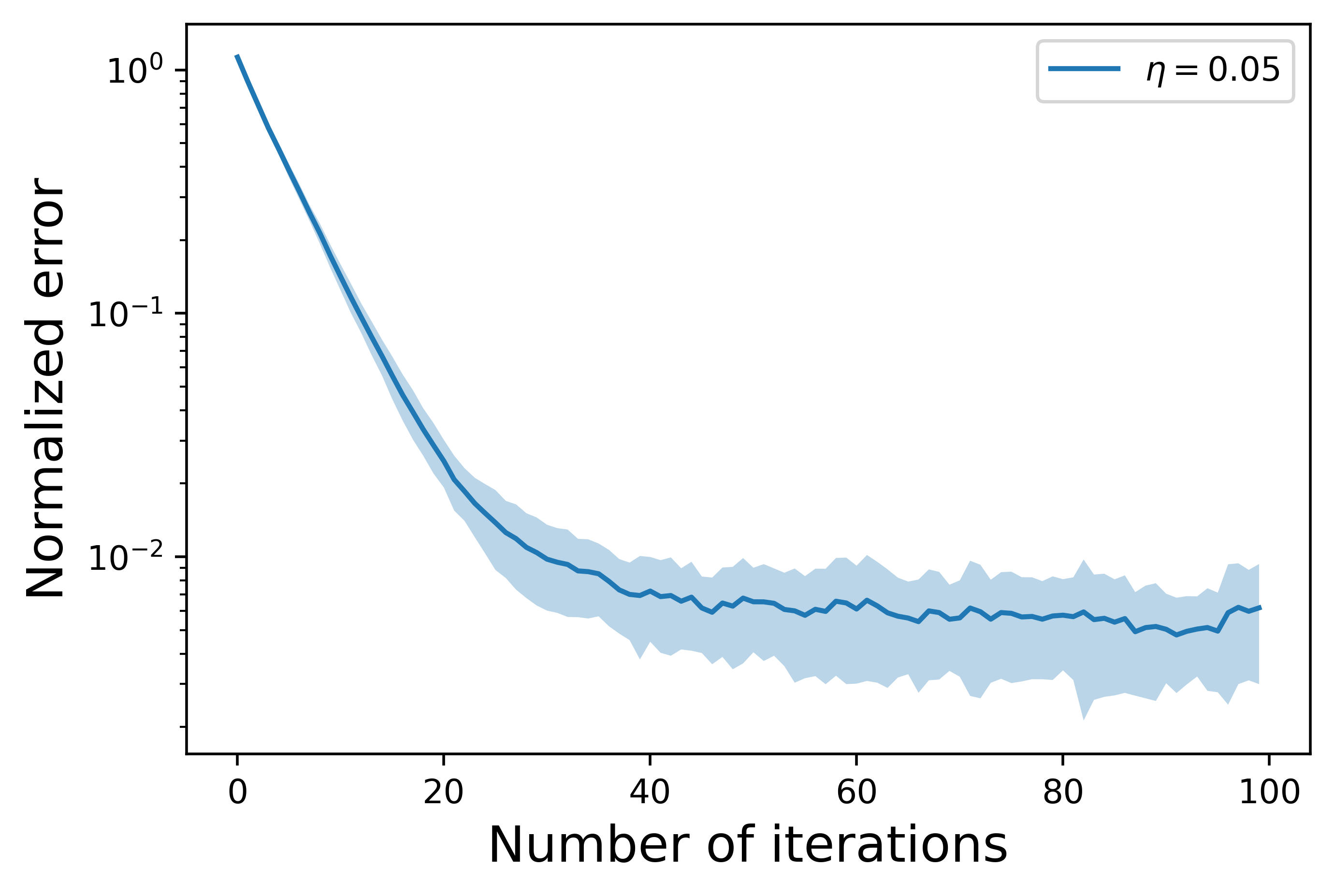

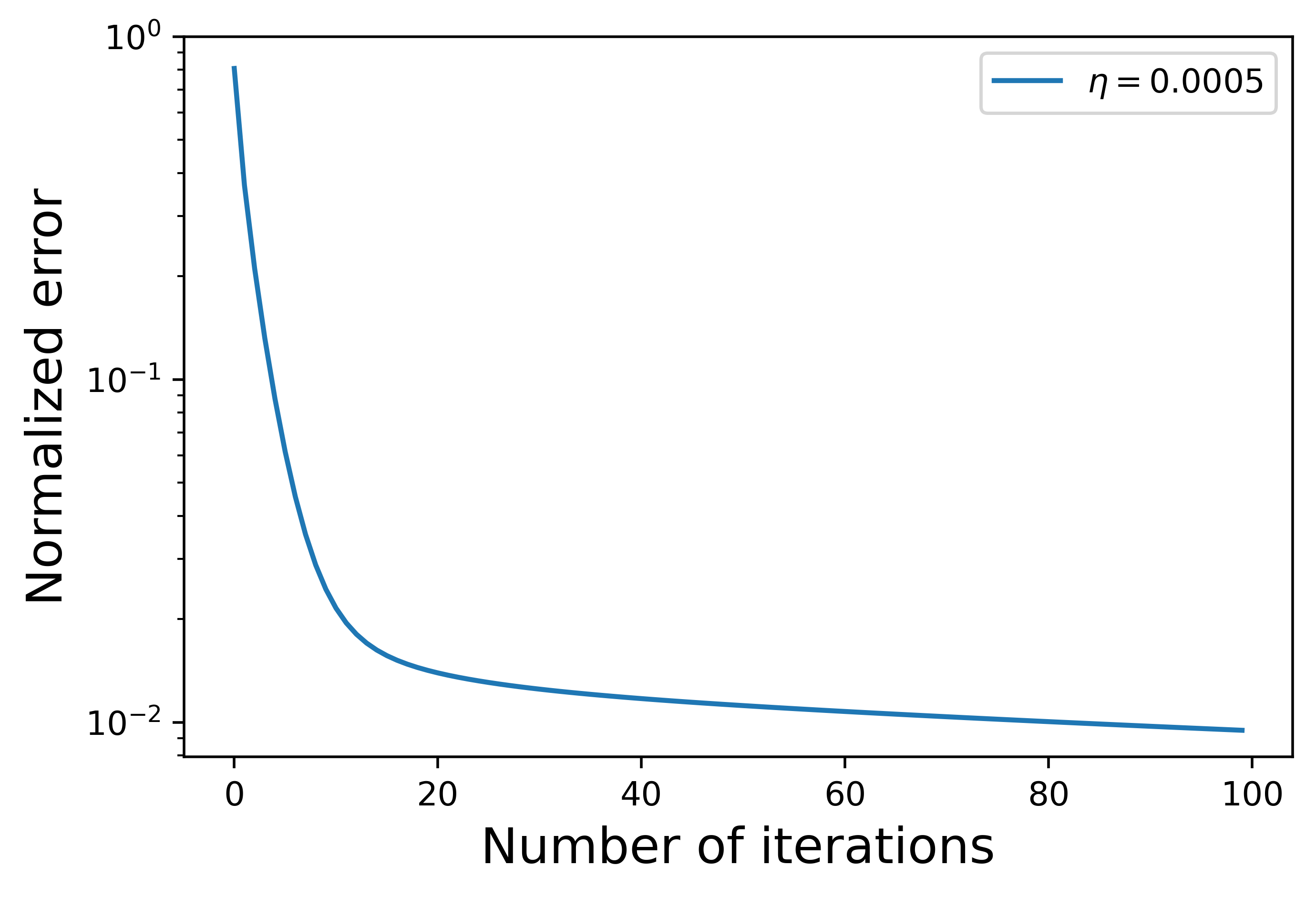

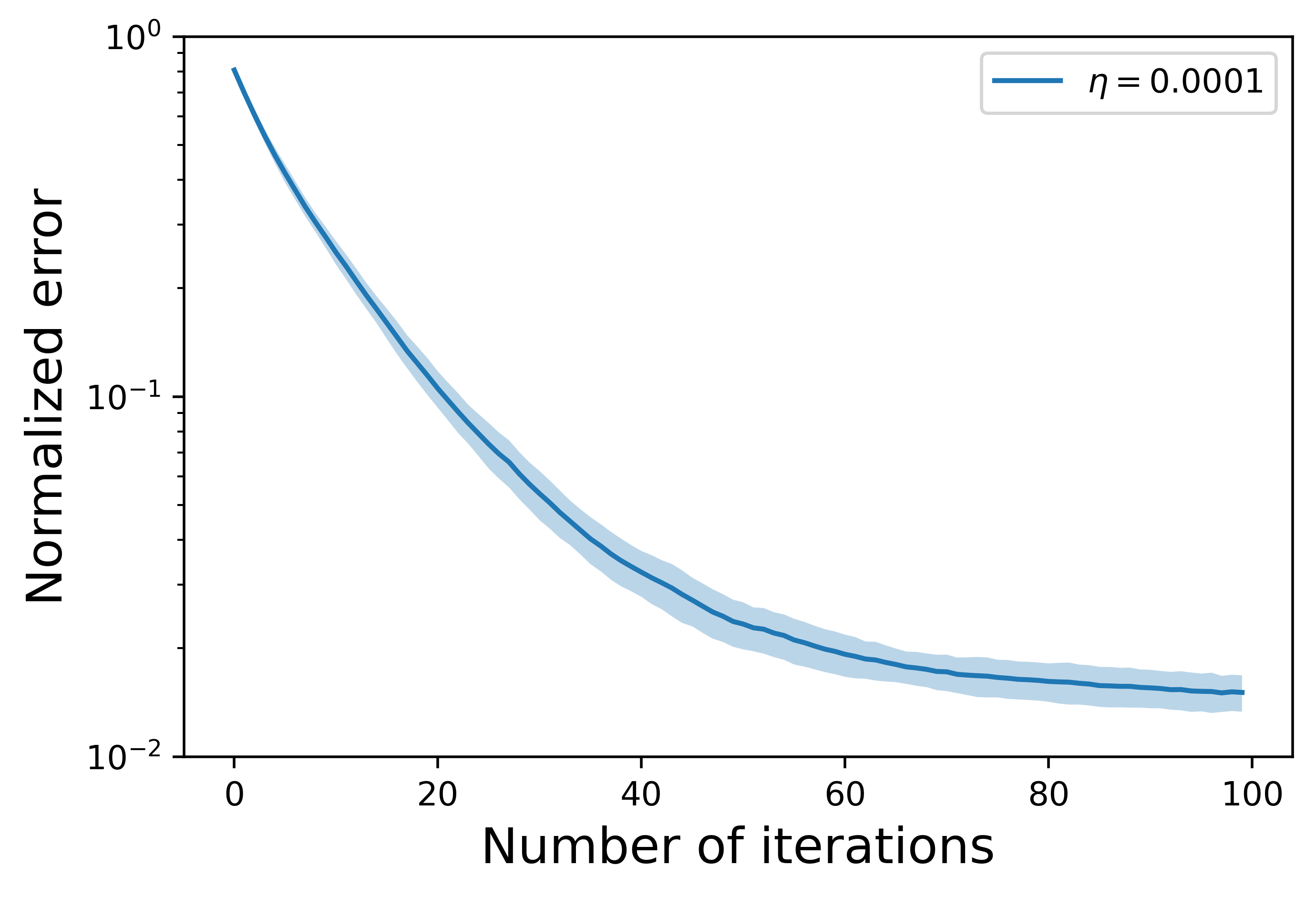

Both PPG algorithms with known parameters and unknown parameters show a reasonable level of accuracy within 50 iterations (that is the normalized error is less than ). The PPG algorithm with known parameters has almost no fluctuations across the 50 scenarios. By choosing , the performance of the PPG algorithm with unknown parameters is stable with relatively small fluctuations (see the blue area in Figure 1(b)) across the 50 scenarios.

Impact of the Deadline.

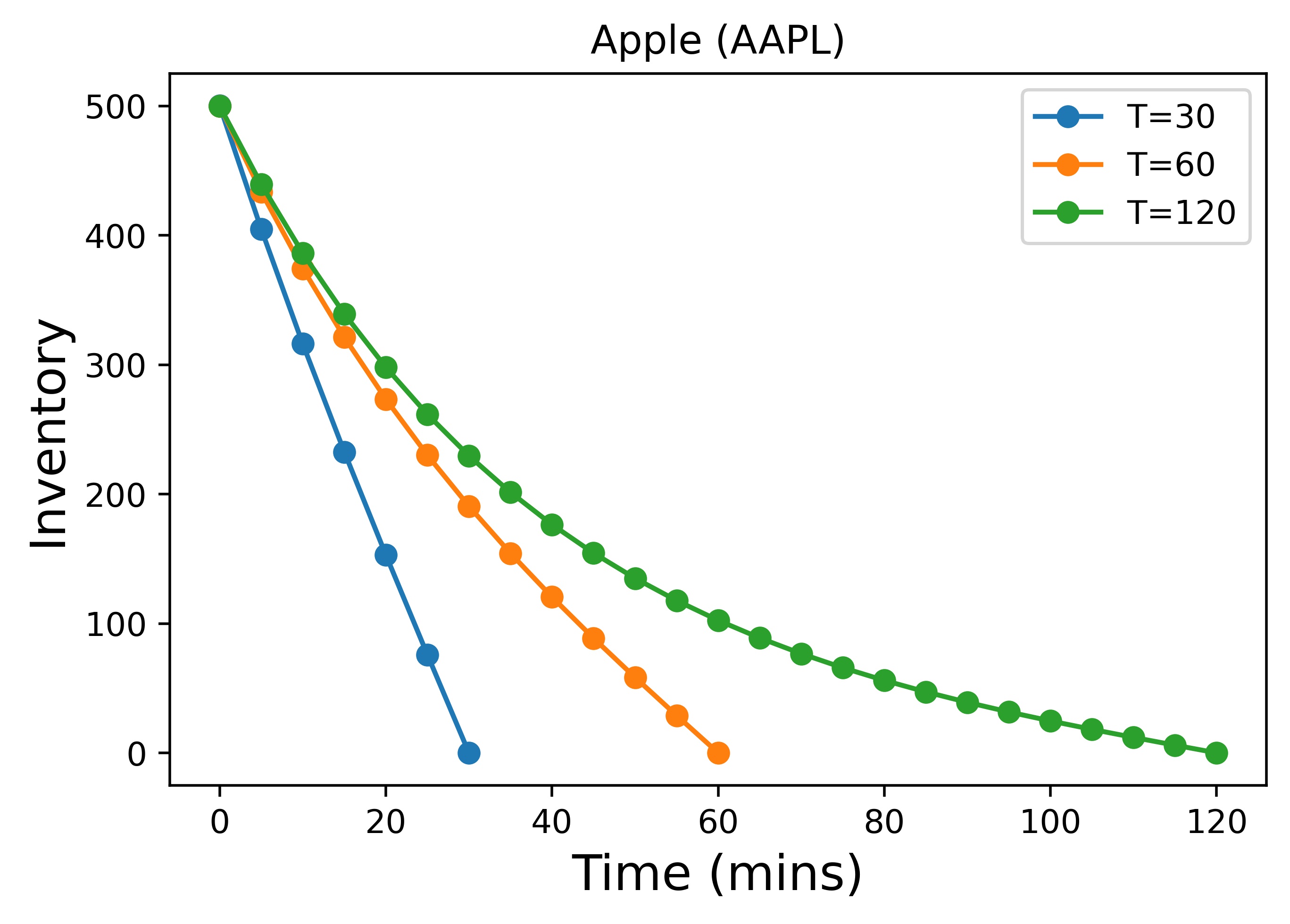

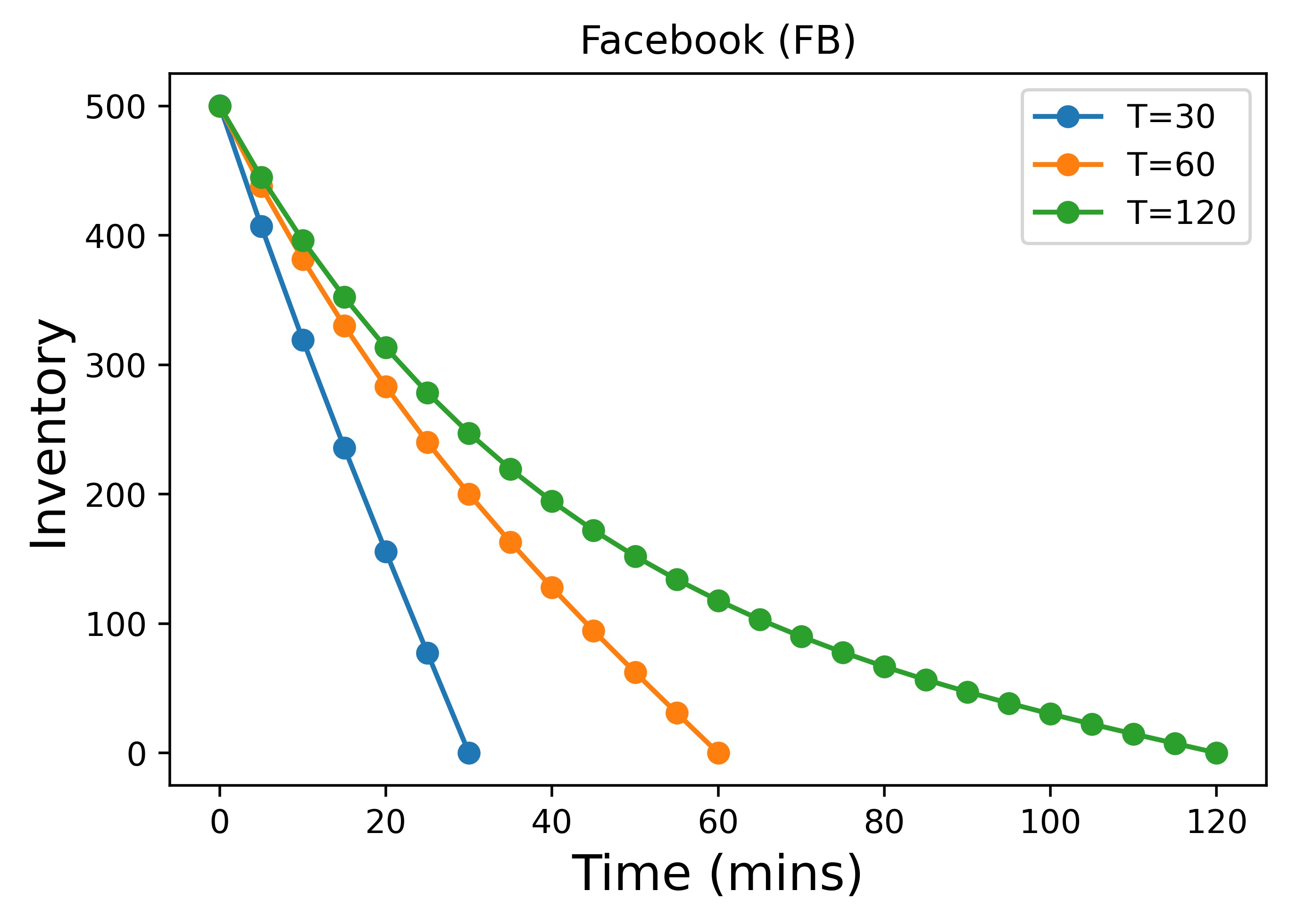

The optimal policy is sensitive to the deadline in that the shapes of the optimal inventory trajectories are different with different deadlines. See Figure 2 for both AAPL and FB with and minutes. The liquidation speed is almost linear when is small; and it is faster in the initial trading phase and slower at the end when is relatively large.

Impact of the Parameter .

Recall that in (2.9) the parameter is used to balance the expected terminal wealth and the variance of the terminal wealth . To show the impact of , we set to be , , , and and show the corresponding inventory trajectories in Figure 4. The optimal liquidation speed is almost linear when is small, while it is faster in the initial trading phase and slower at the end when is relatively large.

Impact of the Parameter .

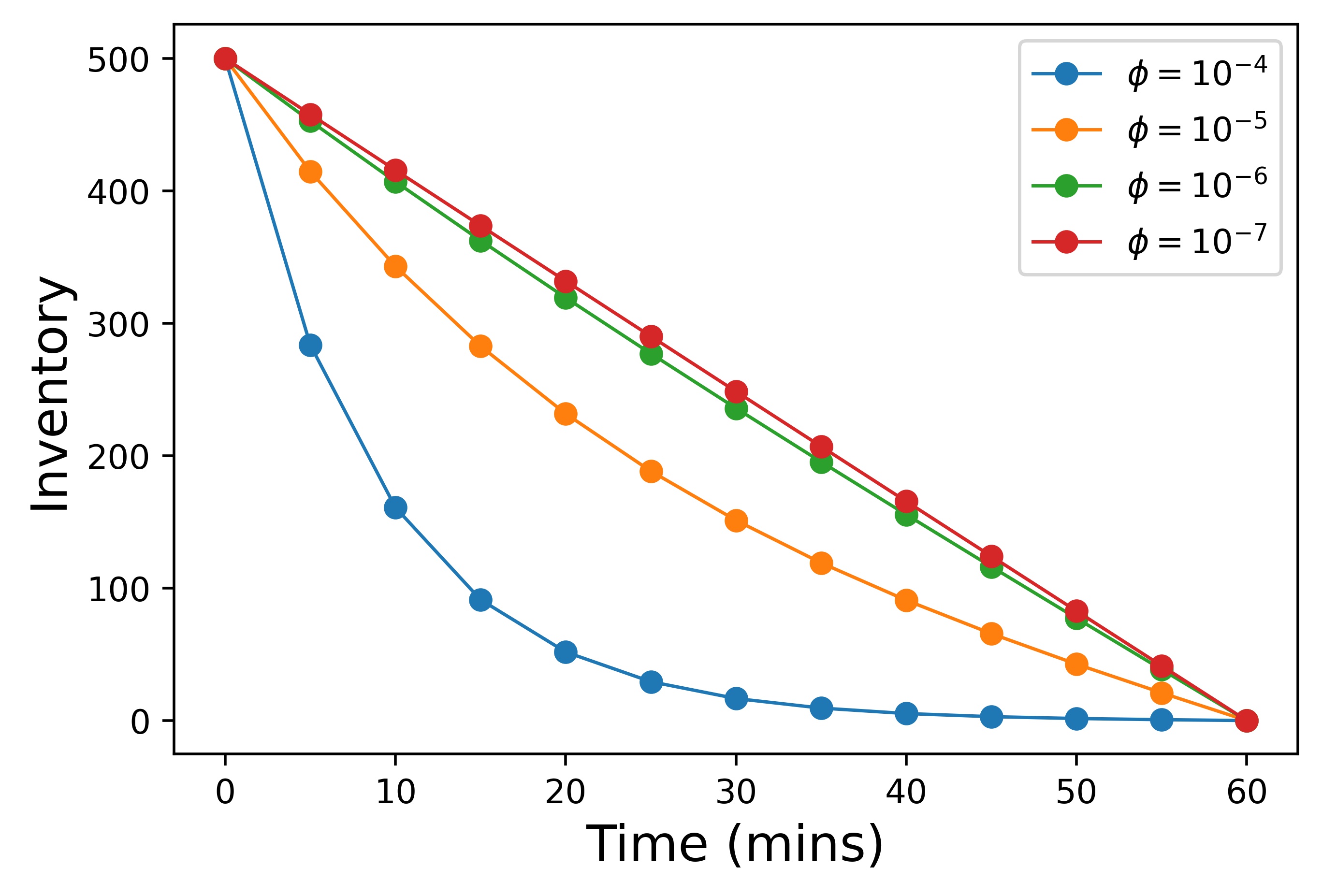

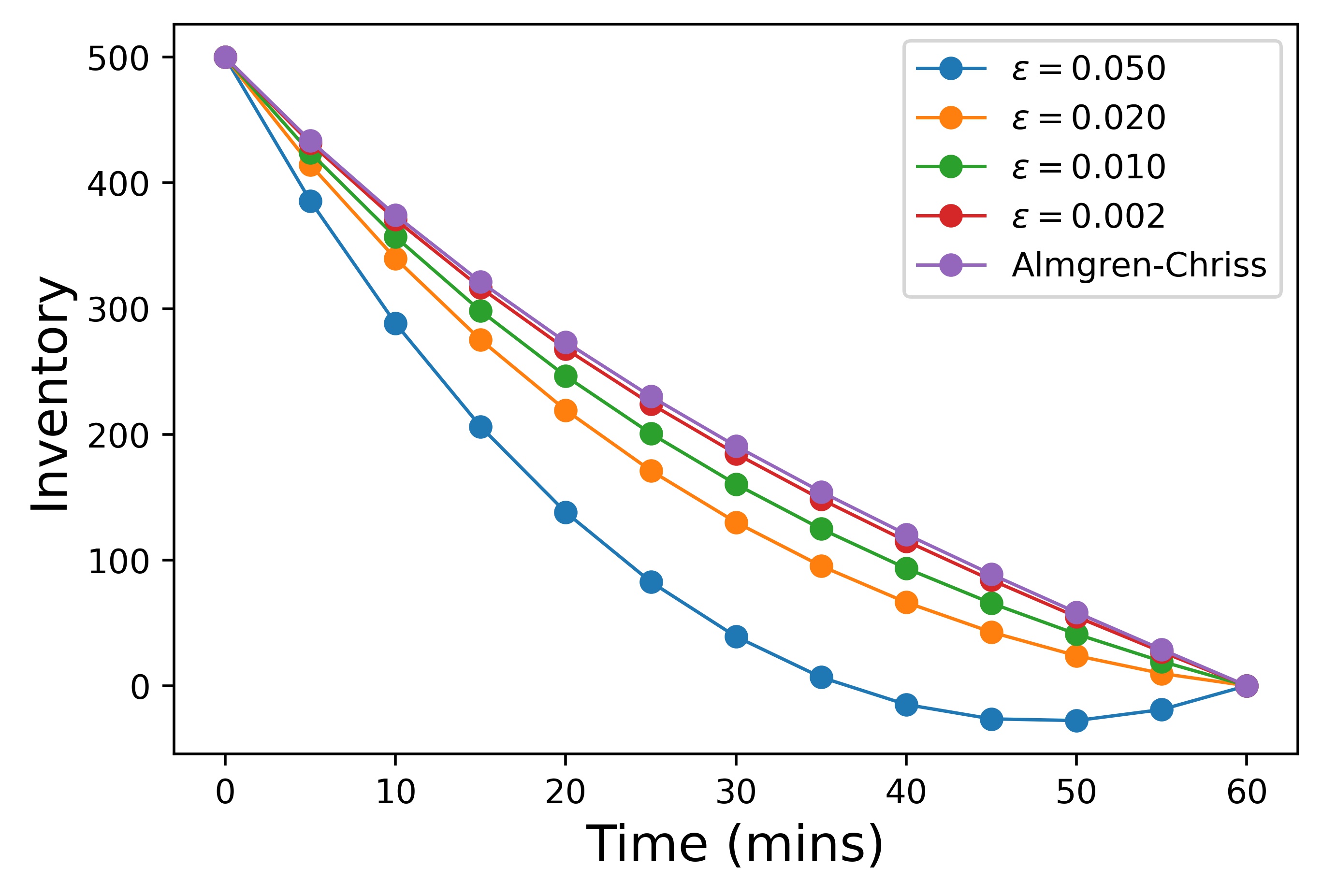

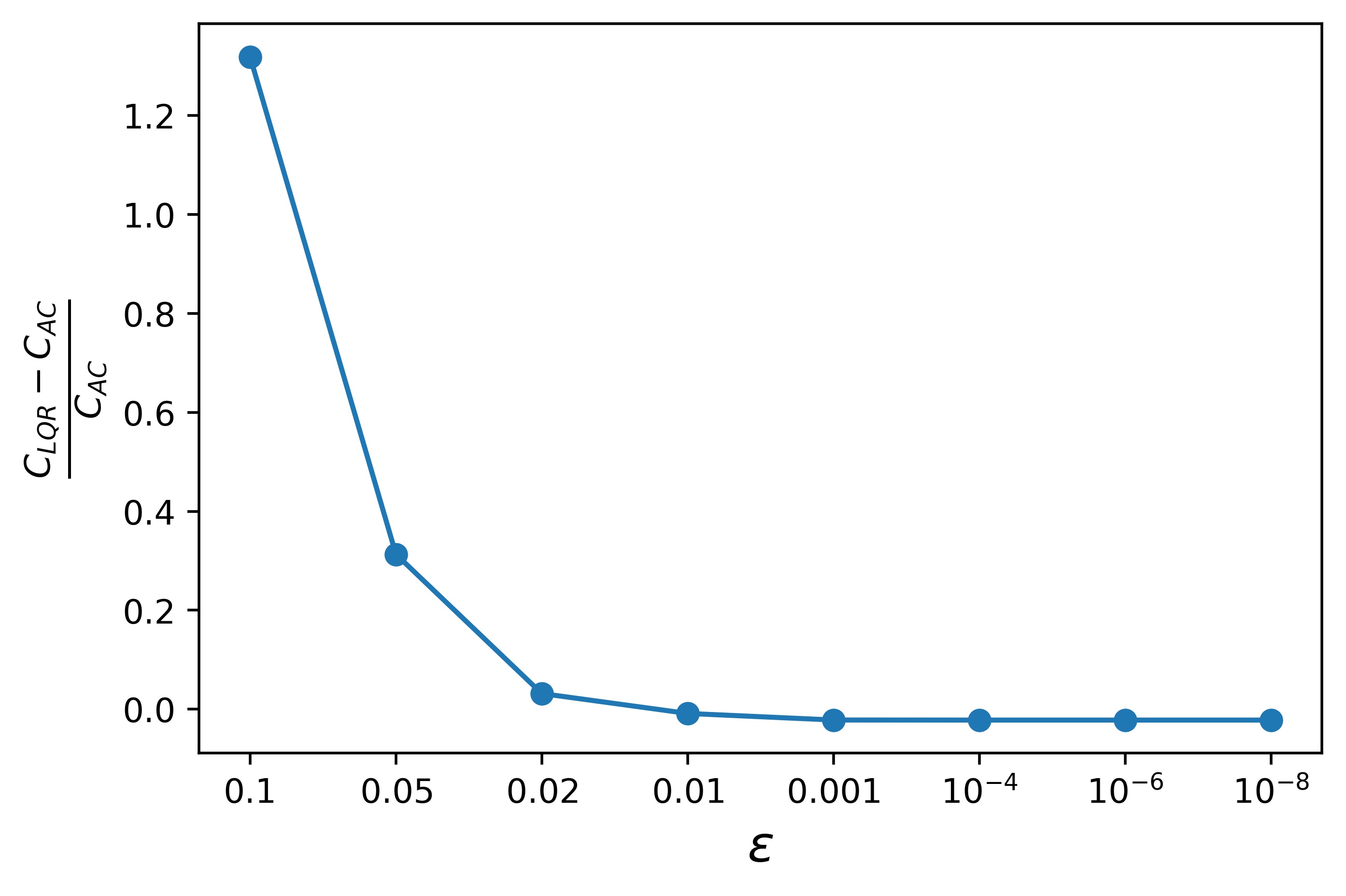

Recall that our liquidation formulation (2.9) differs from the Almgren-Chriss formulation (2.8) by an additional regularization term . The role of this term is to enable the problem to be cast in the LQR framework and to guarantee the well-definedness of the Ricatti equation. From Figure 4(a), the optimal policies and inventory trajectories are close to the Almgren-Chriss solution when . However, when , the optimal policy is far away from the Almgren-Chriss solution. We show the difference between , defined in (2.8), and , defined in (2.9), in Figure 4(b). We see that is close to when and is markedly different from when . It is worth noticing that when , the algorithm does converge to the Almgren-Chriss solution in our setting although the convergence of the algorithm in this case is not guaranteed by our theoretical results.

5.2 Learning to Liquidate without Model Specification

In practice, the dynamics of the trading system may not be exactly those assumed in the LQR framework but we might expect that the policy gradient method could still perform well when the system is “nearly” linear quadratic as the execution of the policy gradient method does not rely on the model specification. In this section, we consider liquidation problems in the Limit Order Book (LOB) setting. A LOB is a list of orders that a trading venue, for example the NASDAQ exchange, uses to record the interest of buyers and sellers in a particular financial instrument. There are two types of orders the buyers (sellers) can submit: a limit buy (sell) order with a preferred price for a given volume or a market buy (sell) order with a given volume which will be immediately executed with the best available limit sell (buy) orders. Here we perform the policy gradient method to learn the optimal strategies to liquidate using market orders in the LOB.

We denote by the mid-price of the asset at time , that is the average of the best-bid price and best-ask price. At each time , the decision is to liquidate an amount of the asset. The action will have an impact on the market, with possibly both temporary and permanent impacts. Unlike the LQR framework or the classical Almgren-Chriss model, where dynamics are assumed to follow some stochastic model, here we run the policy gradient method directly on the LOB without any assumption on how the mid-price moves and what are the forms of the market impacts. Denote by the inventory at time . We restrict the admissible controls to be of the linear feedback form with some .

The cost at time consists of two parts. The first part is the holding cost of the inventory weighted by a parameter . The quantity is the amount we receive by liquidating shares at time . Note that may depend on and other market observables. For example, if we liquidate shares of the asset with the market conditions given in Table 1, then the amount received would be

This transaction moves the best bid price two levels down. This is commonly referred to as the temporary impact of a market order.

| Bid level | One | Two | Three | Four | Five | |

|---|---|---|---|---|---|---|

| Bid price (USD) | 200.1 | 200.0 | 199.9 | 199.8 | 199.7 | |

| Volume available | 397 | 412 | 502 | 442 | 529 |

Performance Metric: Implementation Shortfall [41].

| (5.2) |

The first term of (5.2) is the cost of implementing policy over the horizon . The second term is the cost when liquidating market orders at time . If we expect is better than liquidating everything at time , then . A smaller implementation shortfall implies the strategy is more profitable.

We use the following relative performance (evaluated on a single trajectory) to compare the performance of two policies and ,

Experiment Set-up.

We consider the LOB data consisting of the best levels and we assume the trading frequency minute and the trading horizon minutes. We perform a numerical analysis for five different stocks, Apple (AAPL), Facebook (FB), International Business Machines Corporation (IBM), American Airlines (AAL) and JP Morgan (JPM), during the period from 01/01/2019 to 12/31/2019. The data is divided into two sets, a training set with data between 10:00AM-12:00AM 01/01/2019-08/31/2019 and a test set with data between 10:00AM-12:00AM 09/01/2019-12/31/2019.

We take ; ; smoothing parameter ; number of trajectories ; initial policy with for all ; and step size . We assume the initial inventory follows . We compare the performance of the policy gradient method with the Almgren-Chriss solution with fitted parameters given in Table 3 in the Appendix. In the Almgren-Chriss model, we set to ensure a reasonable comparison.

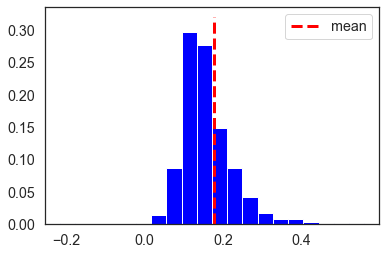

Results.

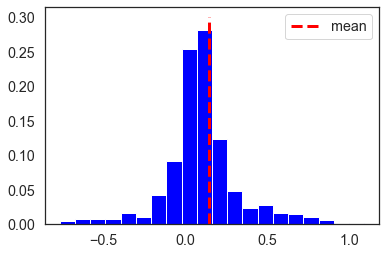

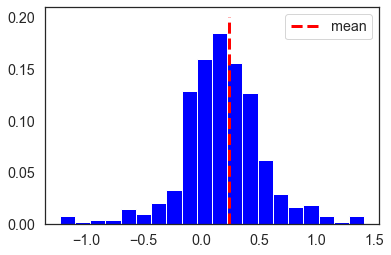

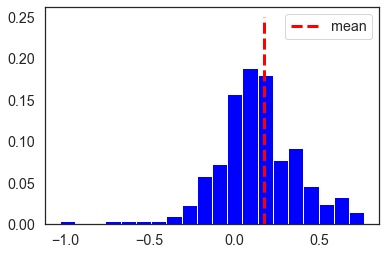

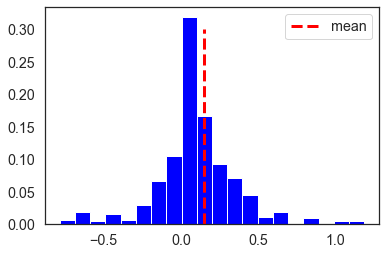

From Table 2 and Figure 5, the policy gradient method improves on the Almgren-Chriss solution by around on five different stocks from different financial sectors. Note that the goal of the policy gradient method is to learn the global minimizer of the expected cost function, hence it is expected that the Almgren-Chriss solution could perform better than the policy gradient method for some sample trajectories, as shown in Figure 5. This result is compatible with the performance of the Q-learning algorithms [30]. The drawback of Q-learning algorithms is that the computational complexity is highly dependent on the size of the set of (discrete) states and actions, where as the policy gradient method can handle continuous states and actions.

We conjecture that the policy gradient method may be capable of learning the global “optimal” solution for a larger class of models that are “similar” to the LQR framework with stochastic dynamics and finite time horizon. In addition, as the policy gradient method is a model-free algorithm, it is more robust with respect to model mis-specification as compared to the Almgren-Chriss framework.

| Asset | IBM | AAL | JPM | FB | AAPL |

|---|---|---|---|---|---|

| In sample | 0.173 | 0.152 | 0.251 | 0.181 | 0.165 |

| (std) | (0.09) | (0.27) | (0.31) | (0.32) | (0.31) |

| Out of sample | 0.178 | 0.146 | 0.245 | 0.175 | 0.163 |

| (std) | (0.08) | (0.29) | (0.36) | (0.24) | (0.37) |

5.3 Learning LQR in Higher Dimensions

In practice we can perform the policy gradient method for the optimal liquidation problem with multiple assets. However it is difficult to capture the cross impact and permanent impact with historical LOB data. Therefore we test the performance of the policy gradient method in higher dimensions on synthetic data consisting of a four-dimensional state variable and a two-dimensional control variable. The parameters are randomly picked such that the conditions for our LQR framework are satisfied.

Set-up.

(1) Parameters:

, ; smoothing parameter , number of trajectories ; initial policy with for all , , for both known and unknown parameters;

(2) Initialization: We assume and are independent. , and are sampled from , , , .

Convergence.

For the high-dimensional case, the normalized error falls below the threshold within 80 iterations for the policy gradient algorithm with known parameters. It takes substantially more iterations for the policy gradient algorithm with unknown parameters to have an error near such a threshold, which is as expected.

().

().

(50 simulation scenarios)

Outcomes from Varying the Parameter .

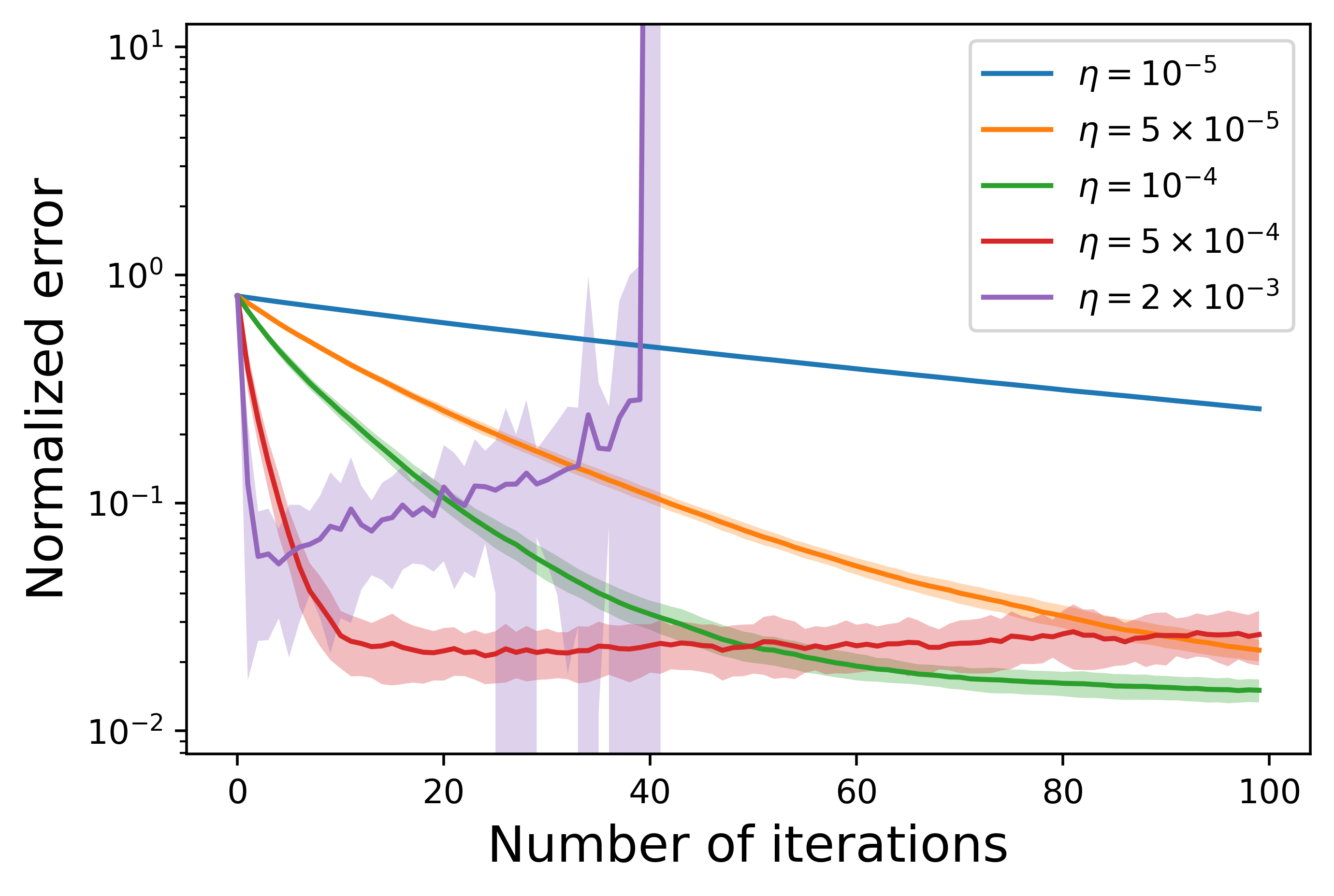

The performance of the policy gradient algorithm also depends on the values of the step size . We show how the values of the step size affect the convergence of the policy gradient algorithm with unknown parameters in Figure 7. A tiny step size leads to slow convergence (see the blue line when ) and a larger step size may cause divergence (see the purple line when ).

References

- [1] Yasin Abbasi-Yadkori and Csaba Szepesvári. Regret bounds for the adaptive control of linear quadratic systems. In Proceedings of the 24th Annual Conference on Learning Theory, pages 1–26, 2011.

- [2] Marc Abeille and Alessandro Lazaric. Thompson sampling for linear-quadratic control problems. AISTATS 2017 - 20th International Conference on Artificial Intelligence and Statistics, 2017.

- [3] Marc Abeille, Alessandro Lazaric, Xavier Brokmann, et al. LQG for portfolio optimization. Available at SSRN 2863925, 2016.

- [4] Radoslaw Adamczak. A note on the Hanson-Wright inequality for random vectors with dependencies. Electronic Communications in Probability, 20, 2015.

- [5] Aurélien Alfonsi, Antje Fruth, and Alexander Schied. Optimal execution strategies in limit order books with general shape functions. Quantitative Finance, 10(2):143–157, 2010.

- [6] Robert Almgren. Optimal execution with nonlinear impact functions and trading-enhanced risk. Applied Mathematical Finance, 10(1):1–18, 2003.

- [7] Robert Almgren and Neil Chriss. Optimal execution of portfolio transactions. Journal of Risk, 3:5–40, 2001.

- [8] Robert Almgren, Chee Thum, Emmanuel Hauptmann, and Hong Li. Direct estimation of equity market impact. Risk, 18(7):58–62, 2005.

- [9] Brian D. O. Anderson and John B Moore. Optimal Control: Linear Quadratic Methods. Courier Corporation, 2007.

- [10] Karl J Åström and Björn Wittenmark. Adaptive control. Courier Corporation, 2013.

- [11] Wenhang Bao and Xiao-yang Liu. Multi-agent deep reinforcement learning for liquidation strategy analysis. arXiv preprint arXiv:1906.11046, 2019.

- [12] Dimitri Bertsekas. Dynamic Programming And Optimal Control, volume 1. Athena Scientific, 3rd edition, 2005.

- [13] Jalaj Bhandari and Daniel Russo. Global optimality guarantees for policy gradient methods. arXiv preprint arXiv:1906.01786, 2019.

- [14] Jingjing Bu, Afshin Mesbahi, Maryam Fazel, and Mehran Mesbahi. LQR through the lens of first order methods: discrete-time case. arXiv preprint arXiv:1907.08921, 2019.

- [15] Jingjing Bu, Afshin Mesbahi, and Mehran Mesbahi. Policy gradient-based algorithms for continuous-time linear quadratic control. arXiv preprint arXiv:2006.09178, 2020.

- [16] Jingjing Bu, Lillian J Ratliff, and Mehran Mesbahi. Global convergence of policy gradient for sequential zero-sum linear quadratic dynamic games. arXiv preprint arXiv:1911.04672, 2019.

- [17] René Carmona, Mathieu Laurière, and Zongjun Tan. Linear-quadratic mean-field reinforcement learning: convergence of policy gradient methods. arXiv preprint arXiv:1910.04295, 2019.

- [18] Arthur Charpentier, Romuald Elie, and Carl Remlinger. Reinforcement learning in economics and finance. arXiv preprint arXiv:2003.10014, 2020.

- [19] Rama Cont, Arseniy Kukanov, and Sasha Stoikov. The price impact of order book events. Journal of Financial Econometrics, 12(1):47–88, 2014.

- [20] Sarah Dean, Horia Mania, Nikolai Matni, Benjamin Recht, and Stephen Tu. On the sample complexity of the linear quadratic regulator. Foundations of Computational Mathematics, pages 1–47, 2019.

- [21] Mohamad Kazem Shirani Faradonbeh, Ambuj Tewari, and George Michailidis. Optimism-based adaptive regulation of linear-quadratic systems. IEEE Transactions on Automatic Control, 2020.

- [22] Salar Fattahi, Nikolai Matni, and Somayeh Sojoudi. Efficient learning of distributed linear-quadratic control policies. SIAM Journal on Control and Optimization, 58(5):2927–2951, 2020.

- [23] Maryam Fazel, Rong Ge, Sham M Kakade, and Mehran Mesbahi. Global convergence of policy gradient methods for the linear quadratic regulator. Proceedings of the 35th International Conference on Machine Learning, pages 1467–1476, 2018.

- [24] Claude-Nicolas Fiechter. PAC adaptive control of linear systems. In Proceedings of the Tenth Annual Conference on Computational Learning Theory, pages 72–80, 1997.

- [25] Abraham D. Flaxman, Adam Tauman Kalai, and H. Brendan McMahan. Online convex optimization in the bandit setting: Gradient descent without a gradient. In Society for Industrial and Applied Mathematics, SODA ’05, pages 385–394, USA, 2005.

- [26] Jim Gatheral and Alexander Schied. Optimal trade execution under geometric Brownian motion in the Almgren and Chriss framework. International Journal of Theoretical and Applied Finance, 14(03):353–368, 2011.

- [27] Benjamin Gravell, Peyman Mohajerin Esfahani, and Tyler Summers. Learning robust controllers for linear quadratic systems with multiplicative noise via policy gradient. arXiv preprint arXiv:1905.13547, 2019.

- [28] David Gross. Recovering low-rank matrices from few coefficients in any basis. IEEE Transactions on Information Theory, 57(3):1548–1566, 2011.

- [29] Xin Guo, Renyuan Xu, and Thaleia Zariphopoulou. Entropy regularization for mean field games with learning. arXiv preprint arXiv:2010.00145, 2020.

- [30] Dieter Hendricks and Diane Wilcox. A reinforcement learning extension to the Almgren-Chriss framework for optimal trade execution. In 2014 IEEE Conference on Computational Intelligence for Financial Engineering & Economics (CIFEr), pages 457–464. IEEE, 2014.

- [31] Morteza Ibrahimi, Adel Javanmard, and Benjamin V Roy. Efficient reinforcement learning for high dimensional linear quadratic systems. In Advances in Neural Information Processing Systems, pages 2636–2644, 2012.

- [32] Zeyu Jin, Johann Michael Schmitt, and Zaiwen Wen. On the analysis of model-free methods for the linear quadratic regulator. arXiv preprint arXiv:2007.03861, 2020.

- [33] Laura Leal, Mathieu Laurière, and Charles-Albert Lehalle. Learning a functional control for high-frequency finance. arXiv preprint arXiv:2006.09611, 2020.

- [34] Weiwei Li and Emanuel Todorov. Iterative linear quadratic regulator design for nonlinear biological movement systems. In ICINCO, pages 222–229, 2004.

- [35] Dhruv Malik, Ashwin Pananjady, Kush Bhatia, Koulik Khamaru, Peter Bartlett, and Martin Wainwright. Derivative-free methods for policy optimization: guarantees for linear quadratic systems. In The 22nd International Conference on Artificial Intelligence and Statistics, pages 2916–2925. PMLR, 2019.

- [36] Yurii Nesterov. Introductory lectures on convex optimization: A basic course, volume 87. Springer Science & Business Media, 2003.

- [37] Yuriy Nevmyvaka, Yi Feng, and Michael Kearns. Reinforcement learning for optimized trade execution. In Proceedings of the 23rd International Conference on Machine Learning, pages 673–680, 2006.

- [38] Brian Ning, Franco Ho Ting Ling, and Sebastian Jaimungal. Double deep Q-learning for optimal execution. arXiv preprint arXiv:1812.06600, 2018.

- [39] Yi Ouyang, Mukul Gagrani, and Rahul Jain. Control of unknown linear systems with Thompson sampling. In 2017 55th Annual Allerton Conference on Communication, Control, and Computing (Allerton), pages 1198–1205. IEEE, 2017.

- [40] Panagiotis Patrinos, Sergio Trimboli, and Alberto Bemporad. Stochastic MPC for real-time market-based optimal power dispatch. In 2011 50th IEEE Conference on Decision and Control and European Control Conference, pages 7111–7116. IEEE, 2011.

- [41] Andre F Perold. The implementation shortfall: Paper versus reality. Journal of Portfolio Management, 14(3):4, 1988.

- [42] Benjamin Recht. A tour of reinforcement learning: The view from continuous control. Annual Review of Control, Robotics, and Autonomous Systems, 2(1):253–279, 2019.

- [43] Stephen Tu and Benjamin Recht. Least-squares temporal difference learning for the linear quadratic regulator. In International Conference on Machine Learning, pages 5005–5014, 2018.

- [44] Stephen Tu and Benjamin Recht. The gap between model-based and model-free methods on the linear quadratic regulator: An asymptotic viewpoint. In Conference on Learning Theory, pages 3036–3083, 2019.

- [45] Yasuaki Wasa, Kengo Sakata, Kenji Hirata, and Kenko Uchida. Differential game-based load frequency control for power networks and its integration with electricity market mechanisms. In 2017 IEEE Conference on Control Technology and Applications (CCTA), pages 1044–1049. IEEE, 2017.

- [46] Zhuoran Yang, Yongxin Chen, Mingyi Hong, and Zhaoran Wang. On the global convergence of actor-critic: a case for linear quadratic regulator with ergodic cost. arXiv preprint arXiv:1907.06246, 2019.

- [47] Kaiqing Zhang, Zhuoran Yang, and Tamer Basar. Policy optimization provably converges to Nash equilibria in zero-sum linear quadratic games. In Advances in Neural Information Processing Systems, pages 11602–11614, 2019.

- [48] Zihao Zhang, Stefan Zohren, and Stephen Roberts. Deep reinforcement learning for trading. The Journal of Financial Data Science, 2(2):25–40, 2020.

Appendix A Market Simulator for Linear Price Dynamics

We estimate the parameters for the LQR model using NASDAQ ITCH data taken from Lobster111https://lobsterdata.com/.

Permanent Price Impact and Volatility.

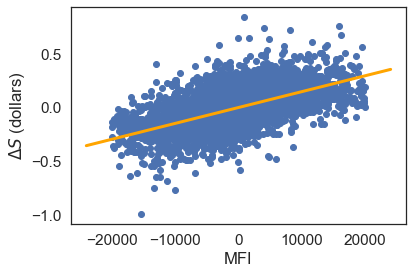

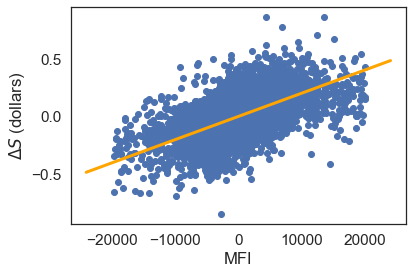

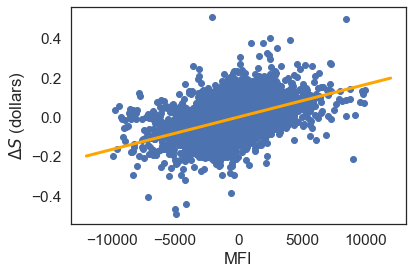

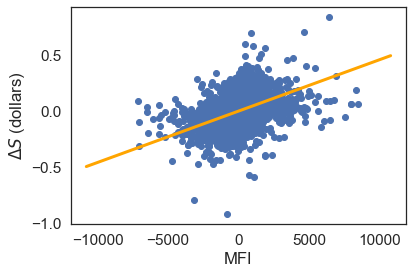

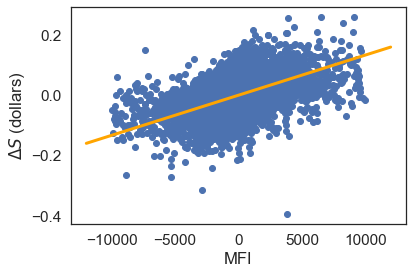

The model in (2.7) implies that prices changes are proportional to the market-order flow imbalances (MFI). We adopt the framework from [19], namely that the price change is given by

| (A.1) |

with where and are the volumes of market sell orders and market buy orders respectively during a time interval mins and . We then estimate and from the data.

Temporary Price Impact.

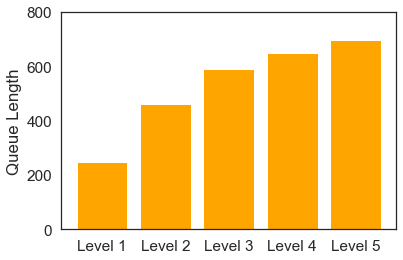

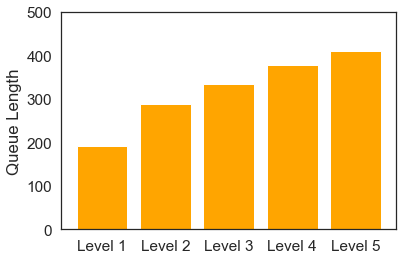

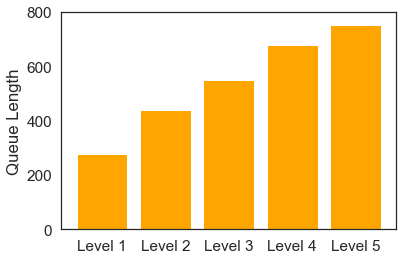

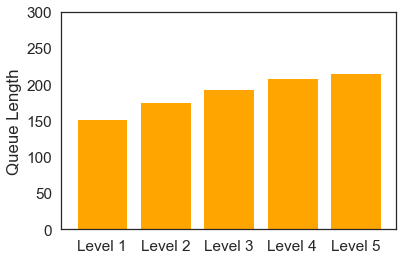

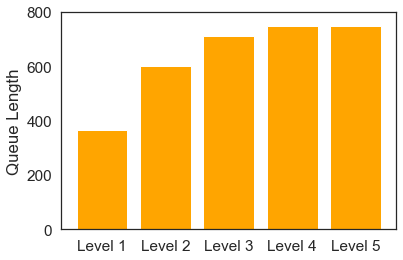

We assume the LOB has a flat shape with constant queue length for the first few levels. Figure 9 shows the average queue lengths for the first 5 levels so that our assumption is not too unreasonable. Therefore the following equation, on the amount received when we liquidate shares with best bid price , holds

Therefore we have , where is the tick size and is the average queue length.

Parameter Estimation.

See the estimates for AAPL, FB, IBM, JPM, and AAL in Table 3.

| Paramters/Stock | AAPL | FB | IBM | JPM | AAL |

|---|---|---|---|---|---|

Appendix B Comparison between the Policy Gradient Method and Q-learning

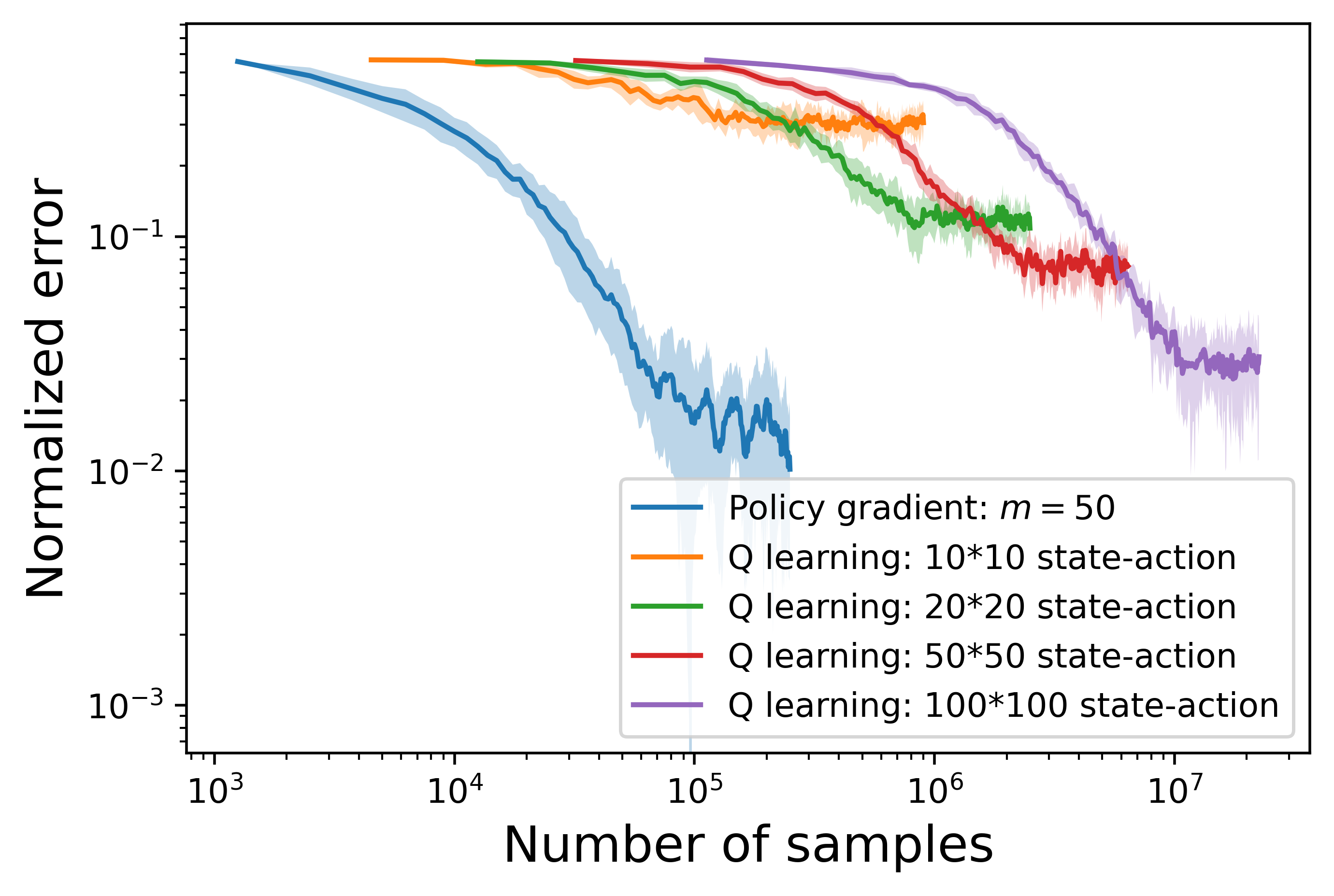

The computational complexity of Q-learning is highly dependent on the size of the set of the (discrete) states and actions. Therefore Q-learning is typically less suited to problems with continuous and unbounded states and actions. In order to apply Q-learning for such problems, we need to discretize the continuous state and action space. Intuitively speaking, Q-learning suffers from low accuracy when the discretization scheme is less refined (see Figures 10 and 12). On the other hand, the computational complexity grows quadratically when increasing the level of granularity of discretization (see Figures 11 and 12).

To demonstrate this view point, we compare the performance of the Q-learning algorithm with the policy gradient method on a one-dimensional LQR problem with finite horizon as suggested by the reviewer. (We would expect the deep Q-learning algorithm and the deep policy gradient method to have similar comparison results.)

Q learning update.

We initialize the Q table with all zeros. In the -th iteration, we update the Q table for ,

| (B.1) |

with terminal condition . Here is the instantaneous cost at time ; is the next state simulated from the system when the agent takes an action in state at time ; and is the learning rate.

Model set-up.

We set , , , , for , , for , , and .

Parameter set-up.

To perform Q-learning, we uniformly partition the states and actions in . We set the learning rate for Q-learning as . For the policy gradient method, we set the learning rate and the number of trajectories in the zero-th optimization as .

Conclusion.

From Figure 12, we observe that

-

•

For LQR with finite horizon, the policy gradient method outperforms Q-learning algorithms (with the size of actions and states varying from 10 to 100) in terms of both sample efficiency and accuracy.

-

•

When increasing the size of the states and actions from 10 to 100, the accuracy of the Q-learning algorithm improves, however, it requires many more samples to converge.

To conclude, Q-learning is less suited to handling decision-making problems with continuous and unbounded states and actions. More advanced approximation techniques may be needed in this case [43].

Appendix C Proofs of Technical Results

We now give the proofs that were omitted in the text.

C.1 Proofs in Section 3.1

Proof of Lemma 3.2.

Denote by the state trajectory induced by an arbitrary control . By Assumption 3.1 the matrix is positive definite. For , we have

Now is positive semi-definite and is positive definite. Hence is positive definite and as a result . In this case, we can simply take

.

∎

Proof of Proposition 3.4.

This can be proved by backward induction. For , is positive definite since is positive definite. Assume is positive definite for some , then take any such that ,

The last inequality holds since , and By backward induction, we have positive definite, . ∎

To prove Lemma 3.6, let us start with a useful result for the value function. Define the value function for , as

with terminal condition

where is defined in (3.10). We then define the function, for as

and the advantage function

Note that . Then we can write the difference of value functions between and in terms of advantage functions.

Lemma C.1.

Assume and have finite costs. Denote and as the state and control sequences of a single trajectory generated by starting from , then

| (C.1) |

and where is defined in (3.11).

Proof.

Denote by the cost generated by with a single trajectory starting from . That is, and with

Therefore,

where the third equality holds since with the same single trajectory. For ,

| (C.2) |

∎

Proof of Lemma 3.6.

Proof of Lemma 3.8.

C.2 Proofs in Section 3.2

C.3 Proofs in Section 3.3

Proof of Lemma 3.15.

Given (3.22) and condition (3.23), we have Therefore,

| (C.8) |

The last inequality holds since given by Lemma 3.8. Therefore, by Lemma 3.12,

| (C.9) |

| (C.10) |

C.4 Proofs in Section 4

Before proceeding to the proof of Theorem 4.5, we show two important Lemmas which provide the intermediate steps. We first show the optimality condition for the projection operator in Lemma C.2. We then show the one-step convergence result in Lemma C.3.

Lemma C.2 (Optimality Condition).

Fix a policy matrix and write . Then for any , we have

| (C.15) |

Proof of Lemma C.2.

We show condition (C.15) by contradiction. Assume condition (C.15) does not hold, then there exist some and some constant such that

| (C.16) |

Let

and take

By the convexity of , we have . Hence from definition (4.3), we have

| (C.17) |

On the other hand,

| (C.18) | |||||

By the definition of we have,

Thus substituting this in (C.18) contradicts (C.17) which completes the proof.

∎

Lemma C.3.

Assume Assumption 2.1 holds, , and that

| (C.19) |

| (C.20) |

| (C.21) |

| (C.22) |

Take

| (C.23) |

with and defined in (C.19) . Then we have

Proof.

By definition of , and as , we have

| (C.24) |

Take and in Lemma C.2, we have

| (C.25) |

Combining (C.24) and (C.25) leads to

| (C.26) |

Given the definition (C.23), we have and . By Lemmas 3.5 and 3.7,

| (C.27) |

with and is the trajectory under policy .

Second given (C.19) and condition (C.21), we have

Therefore,

The second inequality holds by (C.26) and the last inequality holds since given by Lemma 3.8. By (3.21),

| (C.28) |

where the last inequality holds by step size condition . Hence

where the third inequality holds by (C.4) and the fourth inequality holds by Cauchy-Schwarz inequality. By (C.26) we have and thus and

Thus . Therefore when , we have

∎

Proof of Theorem 4.5.

The key step in this proof is Lemma C.3 and it suffices to show that the projected policy gradient method enjoys sublinear convergence rate in the setting of known paramaters. This is because moving from the analysis for the case of known parameters to that for the case of unknown parameters follows the same procedure of policy gradient descent (without projection). In particular, the zeroth order estimation of the gradient term in (C.19) is the same for policy gradient method and projected policy gradient method.

We now show that the projected policy gradient method with known parameters enjoys a sublinear convergence rate. Since the step size conditions (C.20)-(C.22) are independent of the term , the existence of follows the analysis in Theorem 3.3. Hence when is an appropriate polynomial in and model parameters, by Lemma C.3, we have for any ,

| (C.29) |

Therefore converges at rate , which thus completes the proof for the case of known parameters. ∎

Proof of Lemma 4.7.

Under Assumption 4.3, we have and With the sub-Gaussian distributed noise, then we have .

Denote , . Thus, for ,

The last equality holds by (C.5). Therefore,

For the first term, For the second term , since

we have,

We denote , then

| (C.30) |

where the second inequality holds by Lemma 3.13 and (C.9), and the third inequality holds by (C.6). For the first term in , we have

where the last step holds by (3.20). The second term in is bounded by

Similarly, by (3.20) and (C.9), is bounded by

Now we bound the term , which appears several times in previous inequalities:

The last step holds since by assumption.

Proof of Lemma 4.8.

Recall and . We have,

| (C.32) |

For the second term, by Lemma 3.6 and Cauchy-Schwarz inequality,

| (C.33) |

By (C.7) and direct calculation, we have

Next we bound the first term in (C.32). Similar to (C.14), . For , we first need a bound on . Since , by (C.30), we have

| (C.35) |

Thus,

Given the bound on in Lemma 3.16 and the bound on in Lemma 3.8, all the terms in (C.32) can be bounded by polynomials of related parameters multiplied by and . Similarly to the proof of Lemma 4.7, we have and

for some polynomial .

∎

C.5 Proofs in Section 5

Proof of Proposition 5.2.

Denote . Since has two eigenvalues and , is positive definite when ().

Then let us show the first claim by induction. Assume is positive definite for all , then

Hence is positive definite since is positive definite and is positive definite. Therefore .

The second claim can be proved by backward induction. For , is positive definite since is positive definite. Assume is positive definite for some , then take any such that ,

Note that is positive definite when and . The last inequality holds since and are positive definite, and is positive semi-definite. Hence we have positive definite for all . ∎