Canonical Regression Quantiles

with application to CEO compensation

and predicting company performance

Abstract

In using multiple regression methods for prediction, one often considers the linear combination of explanatory variables as an index. Seeking a single such index when here are multiple responses is rather more complicated. One classical approach is to use the coefficients from the leading canonical correlation. However, methods based on variances are unable to disaggregate responses by quantile effects, lack robustness, and rely on normal assumptions for inference. We develop here an alternative regression quantile approach and apply it to an empirical study of the performance of large publicly held companies and CEO compensation. The initial results are very promising.

company performance, canonical correlation

11footnotetext: Professor, Department of Statistics, University of Illinois at Urbana-Champaign

corresponding email: sportnoy@illinois.edu

22footnotetext: Portland State University, Mark O. Hatfield School of Government

1 Introduction.

We develop a novel approach for using the explanatory -variables to find an index that predicts future outcomes given by -variables in a quantile regression setting. The approach is motivated by a specific financial data set listing various measures of the behavior and performance of some large U.S. companies. The aim is to use prior company data to predict future performance, and seeks to define an index (in terms of past data) with better predictive power than CEO total compensation for regression quantile methods. A classical approach might be to use the leading Canonical Correlation, which provides a linear combination of -variables that is most highly correlated with some linear combination of the -variables. However, the inability of correlation methods to disaggregate responses by quantile effects, their inherent lack of robustness, and their need for normal assumptions strongly motivates the search for an alternative regression quantile approach.

The empirical data set concerns research into the relationship between CEO compensation and corporate performance. Much previous financial analysis had failed to yield meaningful results and suggests decoupling of CEO compensation from corporate performance. Recent work by Barton et al (2017) suggested a predictive model where public corporations that adopt operational and financial long-termism will achieve superior financial and market results. The suggested predictive power of long-termism could provide a quantitative measure of future corporate performance that are tied to current CEO’s actions. If true, such models could be used to set current CEO compensation. Corporate ownership structure can influence CEO compensation to reflect ownership powers rather than corporate performance. Therefore, we limited our research to non-controlled public corporations – those with a single class of shares and without blockholders (defined as stock ownership exceeding 10%).

The analysis here develops an index with noticeably better predictive properties than CEO compensation. We focus on predicting two years into the future based on 5 years of past data (which accords with a long-term view). While the results are preliminary, they strongly support the potential value of the “canonical” regression quantile approach. A more complete analysis of the data together with a careful consideration of the financial issues appears in Haimberg and Portnoy (2020).

2 Data.

The study assembled a database by extracting financial information on publicly traded companies on the S&P500 index with continuous operations from 2009 to 2018. Data sources include SEC Form DEF 14A (also refer to as Proxy Statement) and SEC 10K (Annual Report) that are filed annually with the Securities and Exchange Commission (SEC).

Our data includes only companies without any blockholders and to companies with a single class of shareholders to prevent potential bias due to controlling shareholders. We also excluded companies that either went through a merger or new companies that have been in existence for less than 10 years to remove longitudinal data gaps. We identified 100 companies satisfying these criteria.

In a attempt to model long-termism, Barton (2017) suggested a set of independent variables to predict the dependent variables that measure future performance. We used the same set of variables with the exception of one of the independent variables that measure external input based on analysts’ earnings target. We restrict our data to the period from 2009 to 2018 in order to analyze a rather stable economic environment without any major financial shocks.

The explanatory -variables and performance response -variables are defined in the Tables 1 and 2. To include technical definitions, “Accruals” means Operating Net Income minus Operating Cash Flow, “True Earnings” means Operating Cash Flow divided by Diluted Number of Shares, and “opportunity cost” means the Total Invested Capital times the Weighted Average Cost of Capital, and “Shares” means Diluted Number of Shares.

| variable | abbr. | definition |

|---|---|---|

| Investment Ratio | IR | Ratio of capital expenditures to Depreciation |

| Earning Quality Ratio | EQ | Accruals as share of the revenues |

| Margin Growth Ratio | MG | Earning growth divided by revenue growth |

| Earnings per Share | EPS | EPS Growth less True Earnings Growth |

| CEO Total Package | CEOtot | Salary, bonus, stock, stock options and other pay |

| variable | abbr. | definition |

|---|---|---|

| Revenues | REV | Gross sales – returns – discounts revenues |

| Earnings | Earn | Earnings available to shareholders |

| Economic Profits | Eprof | Net Income – opportunity cost |

| Market Capitalization | MCap | Share Price at year-end times Shares |

| Total Shareholder Return | TSR | Capital gain on shares plus dividends |

As described below, the CEOtot variable is used both in developing the predictive index and compared to the index in predicting future performance. In addition, there is a categorical variable with 6 levels giving the type of company: industrial, health, consumer, energy, tech, and utility. See Haimberg and Portnoy (2021) for further discussion of the issues involved in analyzing this data,

3 Statistical Methodology.

The method of Canonical Regression Quantiles seeks to find a linear combination of the response variables that is best predicted by a linear combination of the explanatory variables in terms of regression quantile objective functions. The basic idea is as follows: let be the quantile objective function so that the th quantile, of a sample satisfies

| (1) |

Given a data matrix, , of explanatory variables (generally including a constant intercept column) and a data matrix of response variables, we would like to define the first canonical regression quantile as the pair of coefficient vectors, achieving

| (2) |

where and denote the th rows of and respectively. Unfortunately, this won’t define unique solutions since the objective function in (2) is invariant under scale changes. In the case of canonical correlations, this problem is resolved by imposing orthogonality (or, more generally, a quadratic norm identity). However, to reflect the quantile setting and to avoid the lack of robustness of quadratic measures, it would be preferable to impose the following identity:

| (3) |

where are the coordinates of . Minimizing (2) subject to (4) can be expressed as a linear programming problem, and one could stop here. However, settings like the application here suggest the need for an additional element.

In many (most) applications, the response variables measure related outcomes, and so we expect them to be positively correlated and to be monotonic in the predictors. This suggests imposing the side conditions:

| (4) |

Minimizing (2) subject to this constraint is a constrained regression quantile problem. The solution to (2) is well defined, and easily computable since the linear constraints perfectly match the linear programming form of the regression quantile problem (see Koenker (2005), p. 213). Thus, letting solve (2) subject to (4), we consider and to define predictive and response indices (respectively), and call and the observed predictive and response indices corresponding to the -th observation (that is, the -th row of and ).

If (for all ), it is possible in theory to reduce to a standard regression quantile problem. From the side condition (4), we can write and substitute into the objective function (2) to get

The solution to this minimization problem provides and (with ) as standard regression quantile coefficients. Furthermore, if all , the estimates will all be positive with probability tending to 1 asymptotically. The coefficient estimates will satisfy all known results for regression quantiles (finite sample, asymptotic, and computational; see Koenker (2005)).

Unfortunately, the presence of constraints can seriously affect theoretical properties if some are negative or are on the boundary. This can occur with positive probability for finite samples even when all are positive. In such cases, the constrained solution will be a projection into the constraint set, and the asymptotic theory becomes rather complicated. See Chernoff (1954) for an early description of such asymptotics.

Specifically, if the -constraints fail, the estimates will lie on the boundary with non-vanishing probability (asymptotically). In this case, Andrews (2000) showed that standard bootstrap methods fail, but that a subsample bootstrap whose subsample size tends to infinity more slowly than will provide appropriate inferences for certain constrained maximum likelihood estimators. Later work extended these results in various directions, and the Andrews bootstrap should work here.

Thus, the focus here will use a weighted version of the Andrews’ bootstrap that is informed by recent research in this area. One complication is that the rank of the -matrix is not a small fraction of the sample size, . Thus, repeated observations in bootstrap samples can lead to singular (or nearly singular) design matrices. To avoid this problem, weighted resampling methods will be used here. Specifically, a weighted version of a subsample bootstrap of size (proportional to ) will be used here. A subsample of size will be given independent negative exponential weights, and the remaining observations will be given times independent uniform weights; and this subsampling process will be repeated times to provide a “bootstrap” sample. In theory, this should be asymptotically equivalent to Andrews’ bootstrap procedure, and this was used for all results reported here.

The problem of estimates potentially falling on the boundary might be addressed by an alternative approach. Cavaliere and Georgiev (2019) suggest that the main problem generating bootstrap inconsistency in such cases occurs when the probability that a parameter falls on the bounder differs substantially between the bootstrap distribution and the distribution of the estimator under the model. To keep the difference between the bootstrap and empirical probabilities small, a weighted version of a delete- jackknife might be used successfully. Portnoy (2013) provides evidence that such a procedure is appropriate for censored regression quantiles, where it is also important to keep the resampling distribution close to the empirical distribution. This method was tried for most of the runs described below. It provided roughly similar estimates of standard deviations, though often somewhat smaller. We also computed standard errors for predictions using CEOtot and the Index using the bootstrap method internal to rq. That is, we computed standard errors conditional on the Index, ignoring variability in the data used to construct the index. The observed differences were sufficiently small that our conclusions would not be affected.

4 Results of the data analysis

.

For the data described above, a “long-term” perspective suggests using several years of data to predict a small number of years ahead. Given only 10 years of data, we focus on using 5 years data to predict 2 years ahead. Past values of both X and Y variables will be used, perhaps suggestive of “Granger Causality” (Granger, 1980). In addition, we will include CEO total compensation (CEOtot) in the variables to define the index and also as a predictor for the response two years ahead. Assuming we have observed 7 years, we use the canonical regression quantile method above and, as an alternative, classical canonical correlations to predict the 5 Y-variables in the current year. As described in detail below, we use the -coefficients for the first 5 years data to produce a prediction index; and then use this index to predict 2 years into the future.

With only 100 companies, it is not reasonable to use all the and data over 5 years. From the long-term perspective, we may consider replacing each variable by simple aggregates of the 5 years of data. Specifically, we consider two such aggregates: a discounted average, discounting 5% each year into the past (essentially an exponential smoothing); and the minimum of the 4 differences between successive years. The first measures overall performance while the second measures some form of stability. This leads to 2 measurements for each of the 4 variables, the 5 response variables, and CEOtot: a total of 20 variables. In addition, we introduce an indicator variable for each of the 6 industry types (implicitly including an intercept). This creates a 100 by 26 matrix of explanatory variables (for each time period), that we denote by . Letting denote the response variables 2 years ahead of the data for (that is, two years ahead of the “current” year), we apply two “canonical” analyses to develop predictor () and response () indices. The first is the canonical regression quantile method described above and the second used the vectors corresponding to the leading (classical) canonical correlation. We then use these indices applied to the data from the current year and the previous 4 years to predict each of the 5 -values two years ahead. To be consistent with the basic formulations, we use Least Squares to predict 2 years ahead for classical canonical correlation index, and we use median () regression to predict for the canonical regression quantile index here. We then compare the predictions with the observed -values (2 years ahead).

To be precise, for example, we use the and data from years 2009 to 2013 to predict data in 2015 in order to create the index coefficients, and then apply these coefficients to data from years 2011 to 2015 to predict variables in year 2017 (by a regression quantile estimator with proportion ). We then repeat this process for data from 2010 to 2014 to create an index for predicting variables in year 2018. Of course, other spans of years can be used, both for creating the predictor indices and for predicting into the future. As remarked after presenting the statistical results below, runs using other choices were done. Though the details of the alternative analyses differed, there were no substantive differences in conclusions.

As a final remark concerning the data set-up, note that, like typical economic measurements, the variables were expected to be generally positive values but with clear non-normal variability. Thus, we followed common economic practice and took logs. Unfortunately, some values were actually negative, especially for the variables “Economic Profits” and “Total Shareholder Returns”. Based on the rather large variability in the negative values for these variables, we decided to use a signed log-transformation: sign(y) Some runs with the more usual transformation were done, and they showed almost no difference (often in the third significant figure or smaller).

To analyze the results, we consider three predictors: the index predictors using each of the two canonical methods and also predictions based on total CEO compensation, CEOtot. To allow consistent comparisons, we use both Least Squares and Median regression to predict performance (2 years ahead) based on CEOtot. To elucidate the canonical regression quantile method, we will look at the and coefficients and their standard errors based on the weighted version of Andrews’ bootstrap described above. Numerical comparisons were made in terms of root-mean-squared-error (RMSE) and the mean-absolute-error (MAE) combining results for years 2017 and 2018. However, only the MAE results are reported here, as MAE is more robust and less sensitive to non-normality. We assess statistical variation in these values using the same weighted version of the Andrews’ bootstrap. We also look at some graphical presentations to get a more intuitive idea of the issues, focussing on the canonical regression quantile and the CEOtot predictors. Among the plots considered, we present here scatter plots of predictor index (from the canonical regression quantile approach) and CEOtot versus the canonical regression quantile response index 2 years ahead. We also present scatter plots of the index and CEOtot versus each of the response variables separately, and plots of vs. in terms of Q-Q plots. Finally, we provide an alternative comparison of predictability of future economic performance by presenting median regressions based on using the current Index and CEOtot together to predict the response variables 2 years ahead.

All computer work was done in R (R core team, 2015). Median regression used the function rq from the R-package, quantreg, while Least Squares regression used the base function lm. The results are as follows.

The coefficients for the “best” predicted combination of response variables given in Table 3:

| year | logRev | logEarn | logEprof | logMarCap | logTSR |

|---|---|---|---|---|---|

| 2017 | .884 | .003 | 0 | .113 | 0 |

| 2918 | .998 | 0 | 0 | 0 | .002 |

Clearly, is controlled almost entirely by log Revenue, and it would likely be adequate to base on the regression of log Revenue alone on . This was done as a check on the canonical regression quantile approach, since standard bootstrap inference for conditional quantile analysis is legitimate. As expected, the differences between using log Revenue alone and the canonical regression quantile index were very small, often in the third significant figure or smaller.

The coefficients and their t-statistics (using the weighted bootstrap standard errors) are in Table 4:

| 2017 | t-stat | 2018 | t-stat | |

|---|---|---|---|---|

| intercept | ||||

| indust | ||||

| health | ||||

| consum | ||||

| energy | ||||

| tech | ||||

| IRwt | - | - | - | - |

| IRminD | - | - | - | - |

| EQwt | - | - | ||

| EQminD | - | - | - | - |

| MGwt | - | - | - | - |

| MGminD | - | - | ||

| EPSGwt | - | - | - | - |

| EPSGminD | - | - | ||

| CEOtwt | - | - | ||

| CEOtminD | - | - | - | - |

| logRevwt | ||||

| logRevminD | ||||

| logEarnwt | - | - | - | - |

| logEarnminD | ||||

| logEprofwt | ||||

| logEprofminD | - | - | - | - |

| logMCapwt | - | - | ||

| logMCapminD | - | - | - | - |

| logTSRwt | ||||

| logTSRminD | - | - |

It is somewhat surprising that many of these coefficients are significantly negative, but gratifying that many are significantly non-zero (or nearly so). Most also seemed somewhat consistent from 2017 to 2018. These results suggest strongly that there is a signal. This is confirmed by Table 5, which gives values of the mean absolute error (MAE) averaged over the 2 years of prediction.

| Method | logRev | logEarn | logEprof | logMCap | logTSR |

|---|---|---|---|---|---|

| cancor | 0.190 (.049) | 1.878 (.271) | 6.050 (.209) | 0.498 (.042) | 7.036 (.192) |

| Index | 0.162 (.028) | 1.413 (.020) | 4.940 (.065) | 0.529 (.027) | 6.262 (.162) |

| CEOrq | 0.776 (.012) | 1.610 (.015) | 5.081 (.142) | 0.658 (.014) | 6.327 (.170) |

Clearly, the canonical regression quantile provides better predictions than CEOtot for all response variables under the more robust MAE criterion. The plots below show that the moderately large number of negative values for log Economic Profits and Total Shareholder Return make these variables somewhat anomalous, and this point will be discussed further below. It was true that the canonical correlation index outperformed the canonical rq index in terms of RMSE (Root Mean Squared Error), but the difference was not large, and CEOtot was never the better predictor. The differences between MAE and RMSE seem mainly a result of the bimodality and outliers.

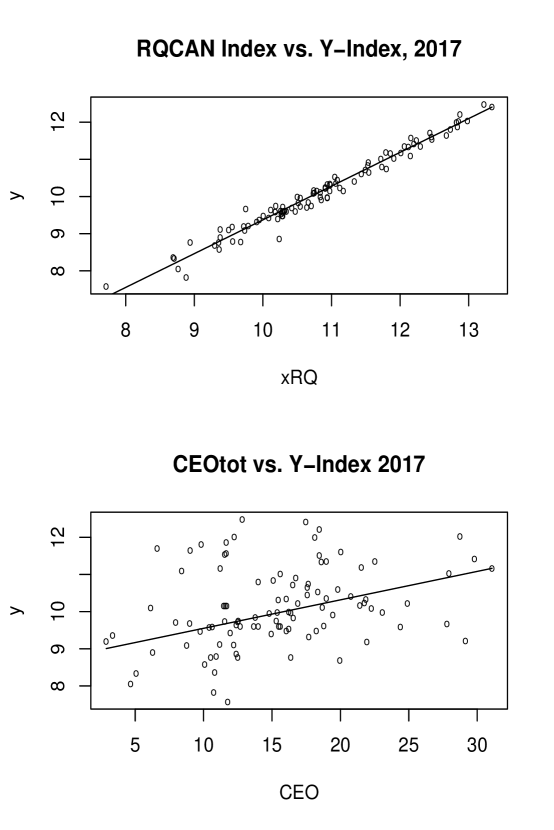

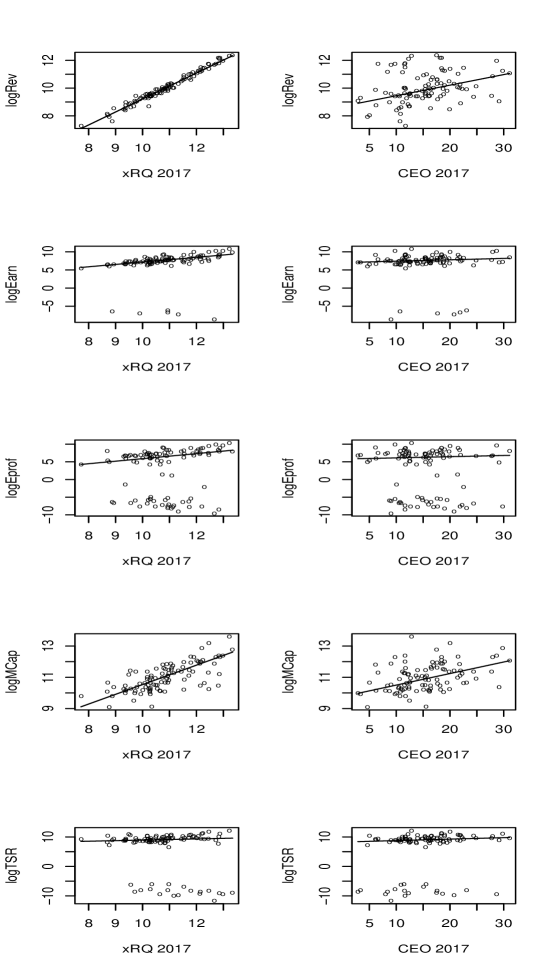

Finally, some plots for the 2017 predicted responses may clarify the nature of the data. Plots for 2018 are quite similar. Figures 1 and 2 present scatter plots of the canonical regression quantile index and CEOtot on the -axis against the canonical regression quantile -index (, see Figure 1) and against each of the 5 variables (Figure 2). The median regression lines are also plotted.

It is clear that the canonical regression quantile index is predicting its -index much better than CEOtot. In fact, if the -index is fit using both the canonical regression quantile index and CEOtot, the coefficient of CEOtot is not significantly different from zero, while the coefficient of the index is highly significant. Regressions of each of the Y-responses on the Index and CEOtot together is discussed below.

Considering the plot for logEprof and logTSR, clearly the negative values are well-separated from positive ones, and are remarkably large in absolute value and rather variable. Both predictors predict the more numerous positive values quite well (as would be expected for a median predictor), but the CEOtot predictions seem pulled down more toward the negative values and thus tend to underestimate the positive ones. There are only a few negative responses for other variables, and so these act more like outliers.

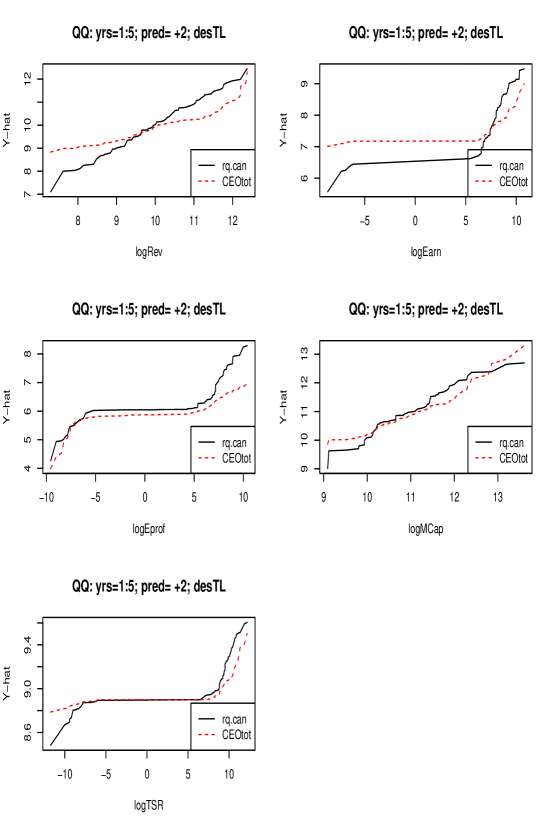

Figure 3 gives Q-Q plots of the observed -response vs. the predicted response from each of the two methods. The separation of negative and positive responses is clear again, as is the tendency of CEOtot to overestimate smaller responses and underestimate larger ones.

To provide an alternative numerical measure of how much better the index does as compared to CEOtot in predicting the -variables, we consider predicting each variable from both CEOtot and the index together (in terms of median regression). That is, we use the the Index and CEOtot in 2015 to predict 2017 responses, and the Index and CEOtot in 2016 to predict 2018 responses. We use median regression with standard errors computed using the Andrews bootstrap (that is, the Indices are recomputed for each bootstrap replication). The resulting t-statistics are summarized in Table 6. Note that the -statistic for the Index tends to be much larger than the statistic for CEOtot, strongly indicating that the index is a much better predictor. In fact, the CEOtot coefficient is negative for three responses in 2017.

| 2017 | logRev | logEarn | logEprof | logMCap | logTSR |

|---|---|---|---|---|---|

| Index15 | |||||

| CEO15 | - | - | - | ||

| 2018 | |||||

| Index16 | |||||

| CEO16 |

Finally, since a fundamental advantage of regression quantile methods is their ability to provide information about the entire response distribution (nonparametrically), some runs were done using the canonical regression quantile to construct indices. As expected, the .75 canonical regression quantile indices were not as good as the median () for both RMSE and MAE. When was used as a measure of accuracy, the .75-quantile showed a relatively similar improvement over CEOtot except for logEprof and logTSR. This is not surprising in view of the bimodality of this variable shown in the plots. Note that the metric weights positive residuals exactly 3 time more than negative ones, thus exaggerating the cost of underestimation. The numerical results for MAE and for the .75-quantile loss are given in Tables 7 and 8.

| logRev | logEarn | logEprof | logMCap | logTSR | |

|---|---|---|---|---|---|

| cancor | 0.190 (.049) | 1.878 (.271) | 6.050 (.209) | 0.498 (.042) | 7.036 (.192) |

| rq.can | 0.192 (.040) | 1.540 (.061) | 5.144 (.064) | 0.625 (.050) | 6.670 (.120) |

| CEOrq | 0.972 (.097) | 1.791 (.081) | 5.265 (.104) | 0.827 (.069) | 6.673 (.118) |

| CEOls | 0.784 (.018) | 2.012 (.232) | 6.004 (.207) | 0.661 (.011) | 7.069 (.198) |

| logRev | logEarn | logEprof | logMCap | logTSR | |

|---|---|---|---|---|---|

| cancor | 0.095 (.024) | 0.930 (.055) | 3.004 (.042) | 0.248 (.026) | 3.515 (.123) |

| rq.can | 0.126 (.028) | 1.104 (.057) | 3.779 (.061) | 0.421 (.045) | 4.878 (.121) |

| CEOrq | 0.637 (.092) | 1.248 (.078) | 3.827 (.100) | 0.548 (.068) | 4.873 (.128) |

| CEOls | 0.395 (.035) | 1.002 (.054) | 2.985 (.051) | 0.331 (.026) | 3.522 (.114) |

Remarks: A number of particular specifications were employed in the analysis summarized above. In fact, many of these specifications were generalized in trials not reported here. Several runs considered using 4 years of prior data to predict 1, 2, and 3 years ahead. The results differed in detail, but were qualitatively the same.

Notice that the standard errors for the for logEprof and logTSR are somewhat larger than other standard errors, reflecting the bimodality of this data. Nonetheless, the standard error estimates above seem reliable. As noted, using a weighted delete- jackknife gave similar results, as did the standard bootstrap using total revenue alone to develop the index. Using a larger resampling size (R = 600 rather than R = 200) also gave similar standard error estimates, with the same cases of larger standard errors.

The original idea was to use only the -data to develop the indices. Some runs were carried out using only the X-data (all the -data and not just the 2 summary aggregates) from 2 to 4 earlier years. This approach did not produce very good predictors. Some attempts at variable selection were also tried. In almost all cases, the variable selection methods suggested that all variables were needed, and so differed very little (or not at all) from the results presented here.

5 Conclusions.

The Canonical Regression Quantile method has been developed in analogy with Canonical Correlations. Basically, we seek linear combinations of explanatory and response variables with the normalization of Canonical Correlations replaced by an normalization and with mean squared error replaced by the regression quantile objective function. We have focussed on only the most predictive linear combinations (analogous to the leading canonical correlation). It is conceptually clear that canonical regression quantiles can be extended by seeking the most predictive indices subject to the constraint that they be orthogonal to the leading indices. Since the condition for orthogonality is linear in the new linear coefficients, the computations are essentially the same application of constrained regression quantiles as for the leading indices. The process could clearly be continued to provide a dimension reduction method entirely analogous to Canonical Correlations. The main conceptual problem is the imposition of orthogonality: outside normal models, the resulting indices will not be independent, and it seems clear that specific applications may suggest alternative conditions, both for canonical quantile regression as well as for traditional canonical correlations. Some preliminary explorations are promising.

The application to financial data show that Canonical Regression Quantiles can provide useful information for the scientist. Additional analysis and financial development in Haimberg and Portnoy (2021) indicate that, at least when economic conditions are stable, there is information available that might provide better ways to set CEO compensation so as to improve company performance.

References

- [1] Andrews, D. (2000). Inconsistency of the Bootstrap When a Parameter is on the Boundary of the Parameter Space. Econometrica, 68(2), 399-405.

- [2] Barton, D., Manyika, J., Koller, T., Palter, R., Godsall, J., and Zoffer, J. (2017) Measuring the economic impact of short-termism, McKinsey Global Institute.

- [3] Cavaliere, G and Georgiev, I (2019). Inference under random limit bootstrap measures, arXiv:1911.12779, arxiv.org

- [4] Chernoff, H.(1954). On the distribution of the likelihood ratio, Annals of Mathematical Statistics, 25, 573-578.

- [5] Granger, CWJ (1980). Testing for causality: A personal viewpoint, Journal of Economic Dynamics and Control, 2 329-352.

- [6] Haimberg, J. and Portnoy, S. (2021). Long-Termism as a CEO Compensation Predictor in Non-Controlled Public Corporations, preprint.

- [7] Koenker, Roger (2005). Quantile Regression, Cambridge University Press.

- [8] Portnoy, S. 2013). The Jackknkfe’s Edge: Inference for censored regression quantiles, Comp. Statist. Data Analysis, 72, 273-281.

- [9] R Core Team(2019). R: A Language and Environment for Statistical Computing, R Foundation for Statistical Computing, Vienna, Austria. www.R-project.org.