Sun, Wang, and Zhou \RUNTITLENear-Optimal Primal-Dual Algorithms for NRM

Near-Optimal Primal-Dual Algorithms for Quantity-Based Network Revenue Management

We study the canonical quantity-based network revenue management (NRM) problem where the decision-maker must irrevocably accept or reject each arriving customer request with the goal of maximizing the total revenue given limited resources. The exact solution to the problem by dynamic programming is computationally intractable due to the well-known curse of dimensionality. Existing works in the literature make use of the solution to the deterministic linear program (DLP) to design asymptotically optimal algorithms. Those algorithms rely on repeatedly solving DLPs to achieve near-optimal regret bounds. It is, however, time-consuming to repeatedly compute the DLP solutions in real time, especially in large-scale problems.

In this paper, we propose innovative algorithms for the NRM problem that are easy to implement and do not require solving any DLPs. Our algorithm achieves a regret bound of , where is the system size. To the best of our knowledge, this is the first NRM algorithm that (i) has an asymptotic regret bound, and (ii) does not require solving any DLPs.

Rui Sun\AFFAlibaba Group US, Bellevue, WA, 98004, \EMAILsunruimit@gmail.com \AUTHORXinshang Wang\AFFAlibaba Group US, Bellevue, WA, 98004, \EMAILxinshang.w@alibaba-inc.com \AUTHORZijie Zhou\AFFOperations Research Center, Massachusetts Institute of Technology, Cambridge, MA, 02139, \EMAILzhou98@mit.edu

1 Introduction

In this paper, we consider the canonical network revenue management (NRM) problem (Williamson 1992, Talluri and Van Ryzin 1998), which finds applications in airline, retail, advertising, and hospitality (Talluri and Van Ryzin 2004). The NRM problem is stated as follows: there is a set of resources with limited capacities that are available over a finite time horizon. Customers of different types arrive sequentially over time. The type of a customer is defined by the customer’s consumption of resources and the price she pays. Each type of customer requests a certain amount of each resource. Upon a customer’s arrival, the decision-maker needs to decide whether to accept or reject the customer. Accepting the customer generates a certain amount of revenue, which equals the price the customer pays, and also consumes certain units of each resource associated with the customer’s type. Rejecting the customer generates no revenue and uses no resources. The objective is to maximize the total expected revenue during the entire horizon under the capacity constraints of all the resources.

The model we focus on in this paper is known as the “quantity-based” NRM model. There exists another well-known NRM model called the “price-based” model. In the price-based NRM problem, the decision-maker chooses product prices rather than admission (accept/reject) decisions. These two models are different but are equivalent in certain special cases, such as the single resource multi-product model suggested in Maglaras and Meissner (2006).

A classic example of the NRM problem is airline seat allocation. In this problem, resources correspond to flight legs and the capacity of a resource corresponds to the number of seats on the flight. Each customer requests a flight itinerary that consists of a single or multiple flight legs (thus a network structure) and pays the ticket price of the itinerary. Arriving customers are sorted into different classes based on combinations of itinerary and price. This allows the airline to maximize the expected revenue by allocating seats on different flights to different customer classes.

In theory, the NRM problem can be solved by dynamic programming. The state is described jointly by time and the remaining capacities of all the resources. The optimal admission policy compares the revenue of each arriving customer with the marginal value of the requested resources and accepts the customer if the former is larger. However, the time complexity of this optimal algorithm grows exponentially with the number of resources, and is thus computationally intractable. In this paper, we study approximate algorithms that are easy to implement and have provable performance guarantees.

One of the most used mathematical tools for designing and analyzing approximate algorithms in the NRM literature is the deterministic linear program (DLP) formulation. See Section 1.2 for a detailed review of algorithms based on solutions of the DLP. Typically, the DLP is formulated by replacing random variables in the model with their distributional information (e.g., replacing random demand variables with their expectations).

The DLP formulation is essential in the following two aspects. First, an optimal solution to the DLP is a guideline for making online decisions. Specifically, the primal solution of the DLP can be used to design booking limit heuristics, nesting strategies (Talluri and Van Ryzin 2004), and probabilistic assignment policies (Reiman and Wang 2008, Jasin and Kumar 2012, Bumpensanti and Wang 2020). In addition, the dual solution of the DLP serve as bid prices in bid-price control heuristics (Talluri and Van Ryzin 1998). Second, the DLP provides an upper bound on the optimal revenue since the capacity constraints in the DLP are only satisfied in expectation. The DLP upper bound (and its variants) is considered the benchmark performance in the analysis of many algorithms.

In the literature of quantity-based NRM, Reiman and Wang (2008), Jasin and Kumar (2012), and Bumpensanti and Wang (2020) show much better regret bounds compared to preceding results by (re-)solving DLPs multiple times. More precisely, Reiman and Wang (2008) show that strategically resolving the DLP once achieves a regret bound of , where is the system size, improving upon the classic bounds (Talluri and Van Ryzin 2004). Jasin and Kumar (2012) show that resolving the DLP in every time period achieves a regret bound of . Bumpensanti and Wang (2020) prove a uniform regret bound of that does not depend on any numerical values in the solutions of the DLP.

Despite the theoretical developments for the NRM problem, there are challenges in implementing those algorithms that require solving DLPs in an online manner. First, direct linear system solvers, which are necessary for solving DLPs, are time consuming for large-scale problems. Second, consider e-commerce platforms that must deal with more than hundreds of customer visits per second 111For example, 62 million monthly visits took place on Expedia in 2018 (Medium (2018)), and 193 million bookings on Airbnb in 2020 (Airbnb (2020)). In a typical implementation of online algorithms on such e-commerce platforms, DLPs are solved on dedicated computational servers, which sync with an online streaming database at a much lower rate. In such cases, algorithms handling the online customer traffic are not able to acquire DLP solutions to real-time models.

To overcome these difficulties, we propose primal-dual algorithms that are amenable to online platforms. Our algorithm does not require solving any linear programs or performing any matrix factorization, and still achieves an regret bound.

Similar motivations for such fast online algorithms that do not require solving any linear programs are also considered in Li et al. (2020). Specifically, Li et al. (2020) study the online linear programming model, which is a generalization of the quantity-based NRM model studied in this paper. We show that our algorithm achieves a regret bound of , while the algorithm in Li et al. (2020) for the generalized problem achieves a regret bound of . We will discuss more differences between our work and Li et al. (2020) in Section 1.2.

1.1 Overview of main results

Table 1 summarizes the related regret bounds proved in the literature, and our results in this paper. In the table, stands for the scaling factor, namely the size of the system.

The algorithms proposed in Reiman and Wang (2008), Jasin and Kumar (2012), Bumpensanti and Wang (2020) are re-solving algorithms for the NRM problem. The regret bound proved in Reiman and Wang (2008) grows slower than , and the regret bounds proved in Jasin and Kumar (2012), Bumpensanti and Wang (2020) are . The main intuition behind their algorithms is as follows: if the algorithm makes a mistake of accepting too many customers of a certain type in an earlier stage, then after re-solving the DLP, the algorithm is able to correct the mistake by accepting fewer customers of that type in later periods. Li and Ye (2019) also prove an regret bound but for a more general online linear programming model. All those algorithms that obtain regret bounds require solving the DLP at least twice. In particular, at least one of the DLPs has to be solved online. That is, the algorithms need to wait for the DLP solution before making any further online decisions.

In this paper, we propose three two algorithms that do not require solving any DLPs for the NRM problem. Both algorithms are based on primal-dual frameworks, and they apply online convex optimization (Hazan 2019) techniques to learn the optimal dual values (or bid prices) of the resources. We introduce our first algorithm (Algorithm 2) in Section 3. We show that Algorithm 2 has a regret bound of . This algorithm is a warm up for our subsequent main results. It can also be viewed as a direct adaptation of the existing algorithms, such as Li and Ye (2019), Li et al. (2020), Balseiro et al. (2020a), Balseiro et al. (2020b), Agrawal and Devanur (2014) and Agrawal and Devanur (2016).

In Section 4, we introduce a new algorithm (Algorithm 3). It builds on Algorithm 2 and uses a “thresholding” technique for making admission decisions. The algorithms in Bumpensanti and Wang (2020) use a similar thresholding technique. Their algorithm relies on repeatedly solving DLPs to calculate the threshold values. By contrast, in our algorithm, the threshold values are adaptively computed based on a novel statistical property of the admission decisions. We show that Algorithm 3 has a regret bound of . To the best of our knowledge, Algorithm 3 is the first algorithm, for any dynamic multi-resource allocation problem, that (i) has an asymptotic regret bound and (ii) does not require solving any DLPs (or equivalently time-consuming problems).

In Section 5, we provide results from numerical experiments to demonstrate the performance of all these algorithms.

| Previous work | Arrival assumptions | Regret bound | Number of times solving LPs |

|---|---|---|---|

| Reiman and Wang (2008) | known i.i.d. | ||

| Jasin and Kumar (2012) | known i.i.d. | ||

| Bumpensanti and Wang (2020) | known i.i.d. | ||

| Agrawal and Devanur (2014) | unknown i.i.d. | 1 | |

| Li and Ye (2019) | unknown i.i.d. | ||

| Li and Ye (2019) | unknown i.i.d. | ||

| Li et al. (2020) | unknown i.i.d. & random permutation | ||

| Balseiro et al. (2020a, b) | unknown i.i.d. |

1.2 Other related work

We study in this paper a canonical network revenue management problem that has a quantity-based formulation. Compared with a price-based formulation as studied in Gallego and Van Ryzin (1994, 1997), both formulations can be solved using dynamic programming (DP). However, the curse of dimensionality renders the DP computationally intractable even for moderate size problems. Therefore, this has motivated studies in the literature to find approximate algorithms for both formulations.

In the price-based formulation, the decision-maker chooses posted prices of different products. In this stream of literature, Gallego and Van Ryzin (1997) show that a static fixed-price policy is asymptotically optimal on the fluid scale (see the definitions of fluid scale optimality and diffusion scale optimality in Section 2.1). It achieves a regret bound of given system size . Maglaras and Meissner (2006) and Chen and Farias (2013) study the potential benefit of re-optimization to improve the static control policy. Jasin and Kumar (2012) and Atar and Reiman (2013) propose policies that are optimal on the diffusion scale.

For the quantity-based formulation, a review of DLP-based algorithms can be found in the book by Talluri and Van Ryzin (2004). Here, we briefly review a few commonly used control policies: booking limit control, nesting and bid-price control.

Booking limit control sets a fixed quota for each customer type and accepts customers in a first-come-first-serve (FCFS) fashion. The booking limits are given by DLP solutions, as proposed in Williamson (1992). Later, many variants of the DLP are proposed, e.g., Wollmer (1992) and Li and Yao (2004), to improve the practical performance of the booking limit control policy.

Nesting is a remedy strategy for booking limit control. The nesting policy ranks different customer types based on their revenue and resource usage, and allows high-ranking types to use the quota of the low-ranking types. The nesting policy is shown to be effective for single-resource problems. However, when there exist multiple resources, Talluri and Van Ryzin (1998) show that the advantage of nesting is less clear due to the ambiguity in ranking different customer types.

Bid-price control uses dual variables of DLPs to decide admissions. Bid prices are defined as the Lagrangian multipliers associated with the capacity constraints. A customer is accepted if the price she pays is higher than the estimated value of the requested resource. Talluri and Van Ryzin (1998) provide a comprehensive analysis on the asymptotic optimality of bid-price control, and a comparison of different methods to estimate bid prices.

The quantity-based NRM model in this paper is also related to the online knapsack/secretary problems in Arlotto and Xie (2018) and Arlotto and Gurvich (2019), the packing/matching problems in Vera and Banerjee (2020), and the online linear programming (OLP) problems in Agrawal et al. (2014), Li and Ye (2019), and Li et al. (2020).

Arlotto and Gurvich (2019) study a multi-secretary problem, where the decision-maker selects from a sequence of i.i.d. random variables with known distribution to maximize the expected value of the sum of the selected variables under a given budget constraint. Arlotto and Gurvich (2019) develop an adaptive algorithm that makes accept/reject decisions by comparing the ratio between the residual budget and the remaining number of arrivals to certain thresholds, and prove that the algorithm achieves a uniformly bounded regret compared to the optimal offline policy.

Vera and Banerjee (2020) study an online allocation problem that generalizes a wide range of online problems including multi-secretary, online packing/matching and NRM. They propose an algorithm that resolves the DLP upon each customer arrival and accepts a customer if the acceptance probability suggested by the DLP is greater than . Vera and Banerjee (2020) show that their algorithm achieves regret under mild assumptions on the customer arrival process. The analysis is based on an innovative “compensated coupling” technique. The design of their algorithm and their proof idea are generally different from what we present in this paper.

The OLP problem studied in Li and Ye (2019) and Li et al. (2020) generalizes the NRM problem as the OLP model does not impose any parametric structure on the distribution of customer types. In addition, the OLP model assumes the revenue and resource units associated with each arriving customer are i.i.d. sampled from an unknown distribution. Li and Ye (2019) propose an algorithm that solves approximate dual problems of the DLP at geometric time intervals, and show the algorithm achieves a regret bound of . They also propose a resolving heuristic that updates the solution of the dual problem for each customer arrival, and show the resolving algorithm achieves a regret bound of . Later, Li et al. (2020) further the study aiming to relax the assumptions about the input data proposed in Li and Ye (2019). Li et al. (2020) provide an algorithm that does not require solving any LPs, and show that their algorithm achieves a regret bound of without assumptions that ensure a strong convexity of the dual problem.

It is also worth mentioning that Agrawal and Devanur (2014) study fast algorithms for a class of online convex programming problems. The algorithms in Agrawal and Devanur (2014) require solving a DLP once in order to estimate an upper bound on the norm of dual variables. Note that in both our model and the model in Li et al. (2020), constant upper bounds on the norm of dual variables can be derived due to a convenient assumption that the constraint capacities are non-negative and scale with the size of the time horizon.

2 Problem Formulation

Consider a finite time horizon of periods. There are types of customers, indexed by . (Throughout the paper, we use to denote the set for any positive integer .) In each period, one customer arrives, and the type of the customer is with probability . We must have . Let denote the number of arrivals of type- customers during periods , for , and the number of arrivals of type- customers during periods for and . There are resources, indexed by . Resource has initial capacity . Let be the vector of initial capacities. Upon the arrival of each customer, we need to make an irrevocable decision on whether to accept or reject the customer. Accepting a customer of type generates revenue and consumes units of each resource . Let denote the vector of revenues, the column vector of resource consumption associated with customer type , and the bill-of-materials (BoM) matrix. Rejecting a customer generates no reward and consumes no resource. Remaining resources at the end of the horizon have no salvage value. The objective is to maximize the total expected revenue during the entire horizon by deciding whether or not to accept each arriving customer while satisfying all the capacity constraints of the resources.

For an online algorithm ALG, let denote the number of type- customers accepted during periods under the algorithm, for all , and . An online algorithm is feasible if it is non-anticipating and satisfies

The total revenue of ALG is given by

Hindsight optimum. To characterize how close ALG is to the “best” algorithm, we compare with the hindsight optimal revenue. The hindsight optimal revenue is defined as the revenue of an optimal algorithm that knows the arrival information of all customer types a priori. Let denote the hindsight optimal revenue. Formally, we have

| (1) | ||||

Let denote an optimal solution to (1). Then is given by . It is straightforward that because for is always a feasible solution to (1). Note that and for are random variables that depend on . The hindsight optimum is defined as the expectation of the optimal hindsight revenue, i.e., .

In this paper, we define the regret of an algorithm ALG as

| (2) |

namely the gap between the expected total revenue of ALG and the hindsight optimum. We focus on analyzing asymptotic upper bounds on the regret of online algorithms. We will define the asymptotic regime of our model in Section 2.1.

Deterministic linear program (DLP). The DLP formulation is a useful mathematical tool for analyzing regret bounds, and it is obtained by replacing all random variables with their expectations:

| (3) | ||||

Let for be an optimal solution to (3). We have .

The constraints in (3) are weaker than those of the hindsight problem since the capacity constraints in (3) only need to be satisfied in expectation. In addition, observe that the expectation of the hindsight optimal solution is a feasible solution to (3). It is thus easy to verify that

| (4) |

We refer the reader to Talluri and Van Ryzin (1998) for a detailed proof of this result.

Equivalently, we can reformulate (3) as

| (5) | ||||

where the decision variable stands for the (fractional) number of type- customers accepted per period.

2.1 Asymptotic regime

Define , as the unscaled horizon length and capacity levels, respectively. Let denote the scaling factor. In the asymptotic regime, we have , and for all . By the definition in Reiman and Wang (2008), an algorithm ALG is optimal on the fluid scale if its regret grows slower than , namely

and an algorithm ALG is optimal on the diffusion scale if its regret grows slower than , namely

We are interested in analyzing the regret bounds of algorithms as increases. In the rest of the paper, we express the regret bounds in terms of , with the understanding that is proportional to .

3 Optimal Algorithm on the Fluid Scale

In this section, we propose an algorithm that is optimal on the fluid scale (Algorithm 2). The algorithm is a bid-price control heuristic that uses online gradient descent (OGD) to update the bid prices of the resources.

3.1 Preliminaries in online convex optimization

We first introduce the online gradient descent (OGD) algorithm (see Hazan (2019) for a review). In an online convex optimization (OCO) problem, we need to make a sequence of decisions from a fixed feasible set . After each decision is chosen in period , it encounters a convex cost function . The objective is to minimize the sum of the sequence of convex cost functions. In each period , OGD takes a step of size from the current point in the negative (sub)gradient direction of the cost function to obtain , and then project the point to the convex set to obtain . We outline the detailed procedure of OGD in Algorithm 1. The algorithm’s performance is measured by a special notion of regret that is defined as

| (6) |

Note that the definition of regret in (6) for the online convex optimization problem is different from the definition of regret in (2) for the NRM problem.

Let denote the norm. Let denote an upper bound of the diameter of the convex set such that . Let be an upper bound of the maximum gradient of the convex functions at each point such that . The following proposition is well-established in the literature.

Proposition 3.1

3.2 Connection Between OCO and NRM

In this section, we discuss how to apply OGD to our revenue management model. The connection between the OCO problem and the NRM problem is a specialized bid-price heuristic. Consider the Lagrangian relaxation of DLP (5)

| (8) | ||||

We view , namely the Lagrangian multiplier for capacity constraint , as the bid price for resource . Let denote the bid price for resource at the beginning of period . Let denote the type of customer arriving in period . The customer in period is accepted if and only if is larger than the aggregated cost .

In the corresponding OCO problem, the bid-price vector is the decision in period . Once the bid-price vector is chosen for period , the realized cost function is

| (9) |

where denotes the indicator that represents the accept/reject action for the customer in period . To be more precise, we have

3.3 Primal-dual algorithm

We provide in Algorithm 2 the detailed procedure of our first primal-dual algorithm. Algorithm 2 takes as input a start time , an end time , and a vector of capacities at time . These input values are used by the algorithm in the next section, which uses Algorithm 2 as a subroutine. In particular, the end-of-execution time can be earlier than the end of the horizon .

For convenience, we denote as the length of the remaining time horizon that scales with . With capacity and time length , the definition of (9) can be written as

| (10) |

For the OGD steps in Algorithm 2, we set to be the convex feasible set of the bid prices (i.e., the convex set used in Algorithm 1), where is defined as follows. We first define , which is an upper bound on the revenue that can be achieved from one unit of resource . Let and be the maximum and minimum resource capacity, respectively. Then we define as

| (11) |

Throughout all of our algorithms, we will ensure that . The definition of is constructed so that serves as an upper bound on the optimal dual variables, which we formally state in Lemma 7.8 in the appendix.

In order to apply Proposition 3.1, we calculate and as follows. For any two vectors of bid prices , by the Cauchy-Schwarz inequality, we have Thus, we use

| (12) |

as the upper bound on the diameter of region .

Recall that is the upper bound of the gradient of function . Let

| (13) |

denote the maximum consumption of any resource from any customer type. Starting from the definition of (10), we have

where the last two inequalities follow from the triangle inequality and the Cauchy-Schwarz inequality, respectively. Thus, we use

| (14) |

We stress that , and depend on either or . Both of the ratios and become constants when we execute Algorithm 2 alone over the entire horizon (i.e., when and ), because the values of and are proportional to the system size (see Section 2.1).

Algorithm 2 maintains a vector of remaining resources. It terminates at the end of period , or when any resource is not sufficient at the beginning of a period.

3.4 Regret analysis

In this section, we sketch the key ideas in proving the regret bound of Algorithm 2. For ease of presentation, we use , and in this section, and defer rigorous proofs to the appendix.

Let denote the revenue of Algorithm 2 from the periods. The regret of Algorithm 2 can be upper-bounded as

where the inequality is due to (4). It thus suffices to prove an upper bound on .

We present in Proposition 3.2 a high probability bound for the gap .

Proposition 3.2

With probability at least , we have

| (15) |

where , and do not depend on .

This bound is more informative than many regret bounds in the literature that are shown in expectations, e.g., in Agrawal and Devanur (2016). We need this high probability bound to prove further properties in the next section. Similar high probability bounds are also derived in Agrawal and Devanur (2014).

Our analysis is based on an elegant construction of a martingale that incorporates the Lagrangian relaxation (8) and the cost function (9) in the OGD procedure. Specifically, we show that the stochastic process

is a martingale, and apply Azuma’s inequality to obtain a high-probability upper bound of .

The intuition behind the construction of is as follows:

-

•

The first term in the brackets is related to the DLP by weak duality .

-

•

The second term is the revenue of Algorithm 2 in period .

- •

Theorem 3.3

The regret bound of Algorithm 2 is .

Proof 3.4

Therefore, Algorithm 2 is optimal on the fluid scale.

4 Optimal Algorithm on the Diffusion Scale

In this section, we present Algorithm 3 that is optimal on the diffusion scale. The algorithm calls Algorithm 2 as subroutines and furthermore applies a thresholding technique that divides customers into three classes. Algorithm 3 then uses a different online decision rule for each customer class.

Compared to the thresholding algorithms in Bumpensanti and Wang (2020), the design of the threshold values in Algorithm 3 addresses two additional challenges. First, since DLP solutions are not available, we device a statistical method to calculate the threshold values based on past online information. Second, while the threshold values are based on primal information (i.e., the number of customers accepted), the bid-price vector is a dual solution. In the presence of degeneracy, the primal and dual information may not be complementary. To overcome this difficulty, we make a mild assumption on the DLP’s degeneracy, and prove in the next section a proposition that guarantees that the DLP has a unique optimal primal solution (but possibly multiple optimal dual solutions).

4.1 An Additional High Probability Bound for Algorithm 2

In this section, we present another high probability bound in Proposition4.3 for Algorithm 2. This bound results from Lemma 4.2 and guarantees that the allocation made by Algorithm 2 is close to the unique optimal primal solution of the DLP.

We show Proposition 4.3 based on a mild assumption, which is the same as assumption 3 in Agrawal et al. (2014). Consider the following LP in the standard form. Given capacity vector , upper bound vector , decision variables and , we define

| (17) | ||||

Note that the hindsight LP shown in (1) and the DLP shown in (3) are both special instances of . Specifically, when and for , is equivalent to (3).

Let denote the columns of the capacity constraints in , and the coefficients in the objective.

The problem inputs in (17) are in general position. Namely, for any bid price vector , there can be at most columns among such that .

Remark 4.1

Assumption 4.1 is not necessarily true for all inputs. However, as discussed in Agrawal et al. (2014) and Devanur and Hayes (2009), one can always randomly perturb the revenue vector by adding to a random variable that follows a uniform distribution over a small interval . In this way, with probability one, no bid-price vector can satisfy equations simultaneously among . The effect of this perturbation on the objective can be made arbitrarily small.

Lemma 4.2

Recall is an optimal solution to DLP (3). Let be the number of type- customers accepted by Algorithm 2 with start time , end time and initial capacity . By Lemma 4.2, we show the following proposition.

Proposition 4.3

4.2 Algorithm

We present Algorithm 3 with three technical parameters , and that satisfy , and . In the technical theorems, we will choose special values of , and for proving regret bounds.

The algorithm defines two special time points and that divide the horizon into three intervals. Here, the values of and are defined by the input parameters and .

For instance, if we run Algorithm 3 using and , then we have , (by Line 2 of Algorithm 3), and Algorithm 3 divides the horizon into three intervals: (i) from period to period , (ii) from period to period and (iii) from period to period .

Algorithm 3 uses a different strategy in each of the three intervals, and thus we call each of the three intervals as a different “phase” of Algorithm 3.

-

•

In phase I, Algorithm 3 runs Algorithm 2 as a subroutine. Let denote the number of type- customers accepted in phase I. At the end of phase I, customer types are divided into three classes based on . In particular, if exceeds a certain threshold, then we add type into an “accept” class , or if is below another threshold, then we add type into a “reject” class . The thresholds are given by the technical parameters and .

The purpose of thresholding is to exclude customer types for which concentration inequalities are not effective. Intuitively, when very few customers are accepted (i.e., is small), there is very large (relative) estimation error on the chance of accepting a customer. Similarly, when very few customers are rejected (i.e., is large), there is very large (relative) estimation error on the chance of rejecting a customer. When we are estimating the DLP solution, the thresholding technique helps us focus on the customer types for which concentration inequalities lead to small relative uncertainty intervals.

-

•

At the beginning of phase II, Algorithm 3 sets initial capacity where denotes the time length of phase I, and denotes the vector of remaining resources at the beginning of period . Algorithm 3 also creates a virtual copy of vector , denoted as , and initiates a subroutine of Algorithm 2 that updates .

In each period of phase II, if both and are sufficient, i.e., and for all and , then when a customer of type arrives, the subroutine calculates according to the definition of Algorithm 2, namely

and Algorithm 3 makes admission decision

The algorithm then updates capacity vectors

and bid prices according to the subroutine based on (see Line 23 of Algorithm 3).

If is sufficient, but is not sufficient, i.e., there exists such that is violated, then the subroutine of Algorithm 2 stops, and Algorithm 3 makes admission decision:

and then updates .

If is not sufficient, phase II stops.

The reason we construct the virtual copy of capacity vector is because we can then easily apply previous results of Algorithm 2 to the decisions made by the subroutine. Notice that the difference between and the real decision is only caused by the customer types in and . We will separately analyze those customer types in order to characterize .

-

•

In phase III, Algorithm 3 runs Algorithm 2 over the rest of the time horizon. For this phase, the main challenge is that the remaining capacity values are no longer proportional to the number of time periods left. As a result, we cannot simply use Proposition 3.2 (which assumes that both the capacity values and the length of the time horizon are proportional to the system size) to obtain the regret bound for phase III. To overcome this difficulty, we show a more general capacity-dependent regret bound for Algorithm 2. In addition, we create a new virtual copy of capacity vector for phase III, in which the ratio between the maximum and minimum resource capacities is related to the length of phase III.

Specifically, for each resource , we set the initial virtual capacity for phase III towhere is the real remaining capacity at the beginning of phase III and is the length of phase III. Note that the upper bound is essentially the maximum amount of any resource that can be allocated in phase III.

The subroutine of Algorithm 2 runs on the new virtual capacity values. Algorithm3 copies the decisions of the subroutine whenever the decision is feasible (i.e., when is enough for the decision).

4.3 Regret analysis

In the following theorem, we provide the regret bound of Algorithm 3 for the original NRM problem. The detailed analysis is provided in Appendix 8.

Theorem 4.4

If we let the parameters be

The algorithm is optimal on the diffusion scale. Specifically, we have

We outline the key idea of the proof here. Let HO denote the hindsight LP for periods from to . Formally, HO is given by

| (19) | ||||

Let for denote an optimal solution to . We have .

Let be the starting time period of phase II, the starting time period of phase III, where , are the lengths of phase I and phase II, respectively.

To analyze the performance of Algorithm 3, we define an auxiliary algorithm -I that follows Algorithm 3 in phase I, and then uses the hindsight optimal decisions, namely the optimal solution to , in the remaining time periods. Similarly, we define an auxiliary algorithm -II that follows Algorithm 3 in phase I and phase II, and then uses the hindsight optimal decisions, namely, the optimal solution to , in the remaining time periods. Let , denote the revenue of the auxiliary algorithms -I and -II, respectively. By definition, we decompose the regret of Algorithm 3 as

| (20) |

Our proof of Theorem 4.4 depends on the following proposition, which is proved in Appendix 8.

Proposition 4.5

Consider Algorithm 3 with parameters that satisfy , and . The algorithm calculates , , .

Under Assumption 4.1, given such that , and , we have

In fact, each item in Proposition 4.5 describes a regret bound of Algorithm 3 relative to the hindsight optimum HO, and in each phase. Intuitively, for phase I, is upper bounded by , which is of order .

Let denote the DLP for periods from to , given by

| (21) | ||||

Let for denote an optimal solution to , and for the optimal solution to the DLP in (5). By definition of Algorithm 3 (Line 12), we have , and hence is also an optimal solution to (5). Under Assumption 4.1, we know by Lemma 4.2 that is unique (since (5) is a special case of ). Thus, we have for all .

Let denote the number of type customers accepted by Algorithm 3 during periods . By Proposition 4.3, we know for is close to with high probability, since the admission decision for customer types follows that of Algorithm 2.

In addition, we know for , and for . We show in Lemma 8.3 that the hindsight optimal solution is close to with high probability. Combining these results with the thresholding conditions with respect to , we show in Lemma 8.6 that satisfies

| (22) |

for all customer types with high probability. This implies that the decision-maker is able to achieve the hindsight optimum of if she follows the decision of Algorithm 3 during period , and then accepts type- customers during periods . Thus, the regret for phase II is small.

The result for phase III follows from a more general version of Proposition 3.2. In particular, phase III corresponds to an NRM problem with initial capacity and horizon length . It differs from the original NRM model in that the capacity values are not proportional to the length of the time horizon. Thus, we must prove a capacity-dependent regret bound of Algorithm 2. The result for phase III directly follows from that capacity-dependent regret bound.

Now we complete the proof of Theorem 4.4 by setting the technical parameters in Algorithm 3 as follows:

Note that the parameters , , satisfy the condition , and when is large enough, e.g., when . Given , we apply Proposition 4.5 and get

5 Numerical Experiments

In this section, we show the numerical performance of Algorithm 2 and Algorithm 3. In addition, we introduce several practical algorithms based on the structure of Algorithm 2 and Algorithm 3. We first introduce the new algorithms.

We propose a new algorithm (Algorithm 4) that restarts Algorithm 3 at a sequence of specific time points of the horizon. As an extension of Algorithm 4, we propose a hybrid algorithm (Algorithm 6) that is allowed to solve DLPs for a limited number of times. We analyze the performance of Algorithm 6 to demonstrate how solving DLPs helps further reduce the regret bound. The pseudocode and detailed description of Algorithm 4 and Algorithm 6 can be found in Appendix 9.

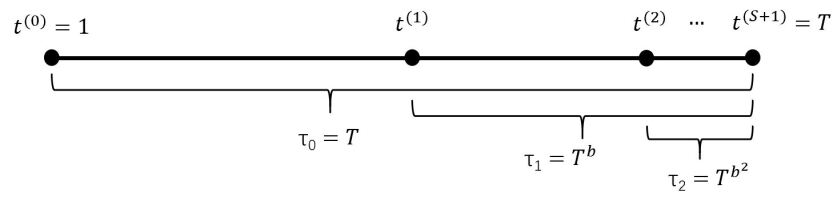

We also consider variants of Algorithm 4 and Algorithm 6. Both algorithms include a total of epochs. Each epoch , where , starts from period and ends at period , where is the time length between the starting period of epoch and period . Next, we introduce Algorithm 7 and Algorithm 8 that warm-start each epoch by reusing the bid prices of epoch for . Algorithm 7 and Algorithm 8 are variants of Algorithm 4 and Algorithm 6, respectively.

For Algorithm 3, we use the input parameters as shown in Theorem 4.4. For Algorithm 6, we experiment with different values of , namely the number of epochs that require solving DLPs. For the remaining algorithms, we tune the input parameters to achieve a good algorithm performance.

5.1 Single Resource

We first consider an NRM problem with a single resource (i.e., ), and two types of customers (i.e., ). Let be the system size. In the experiment, we set horizon length . The number of arrivals for each customer type follows an independent binomial distribution with mean given horizon length (i.e., ). Both types of customers consume one unit of the resource if accepted (i.e., for and ). Customers of type generate revenue if accepted, and customers of type generate revenue if accepted.

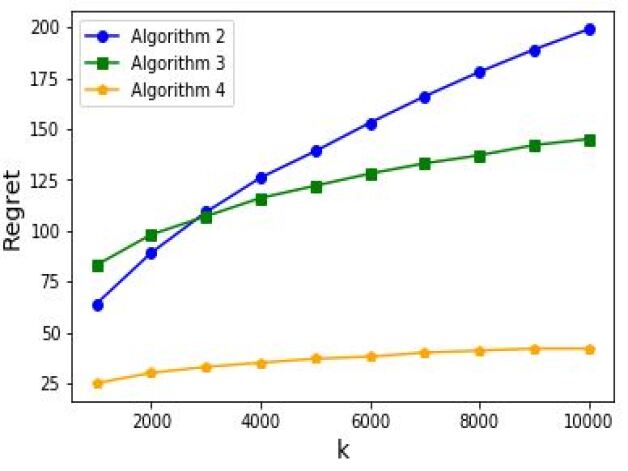

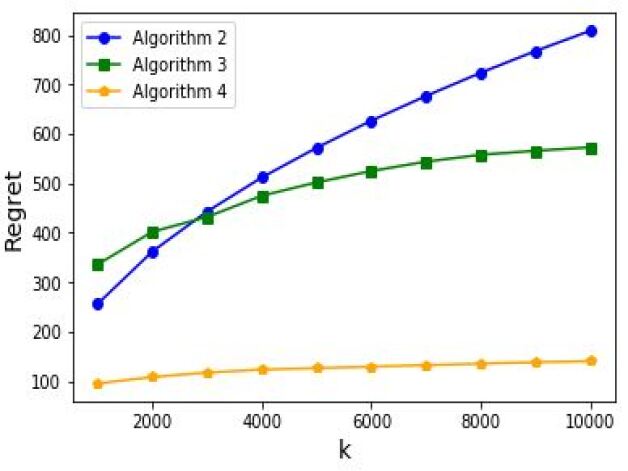

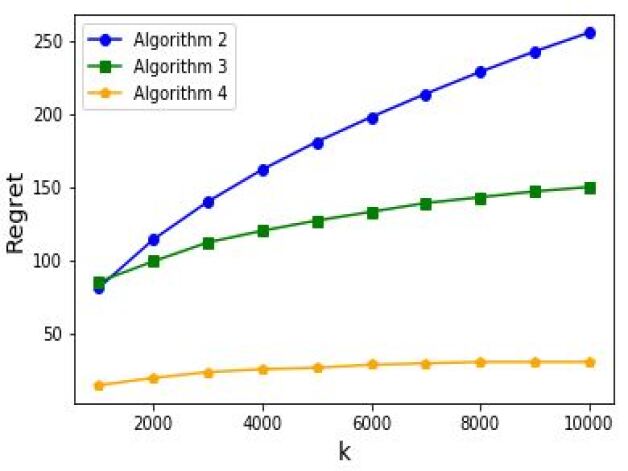

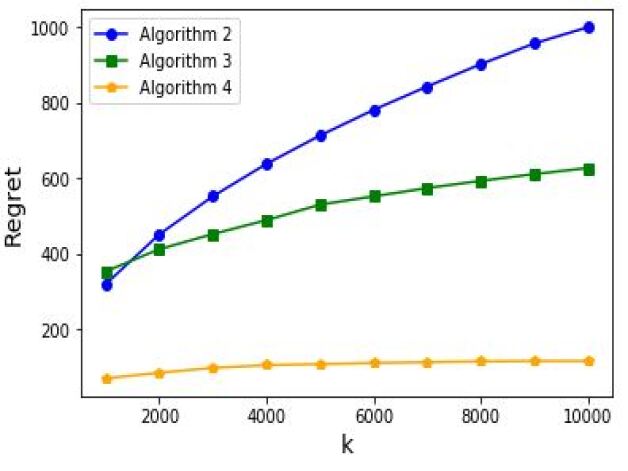

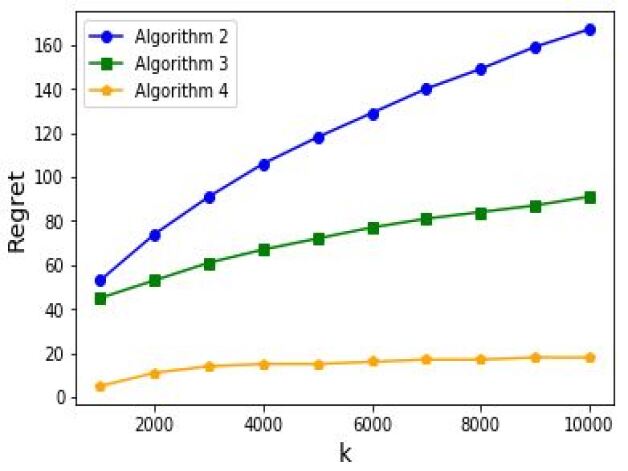

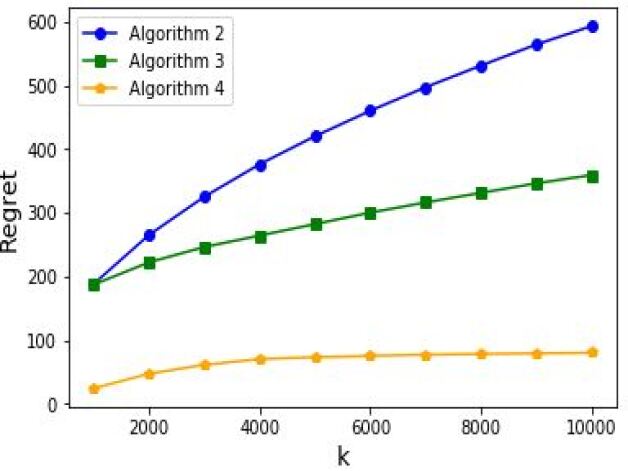

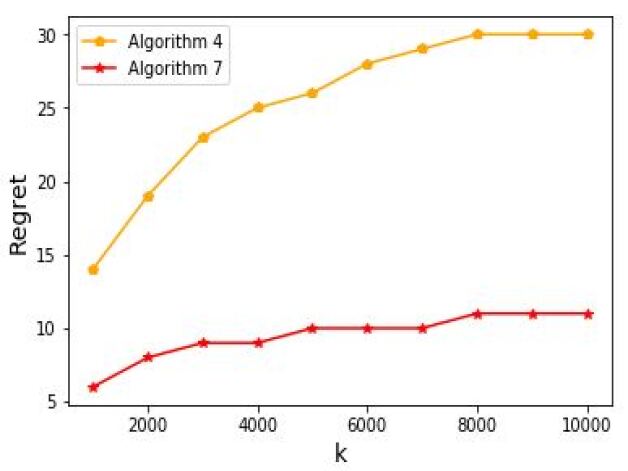

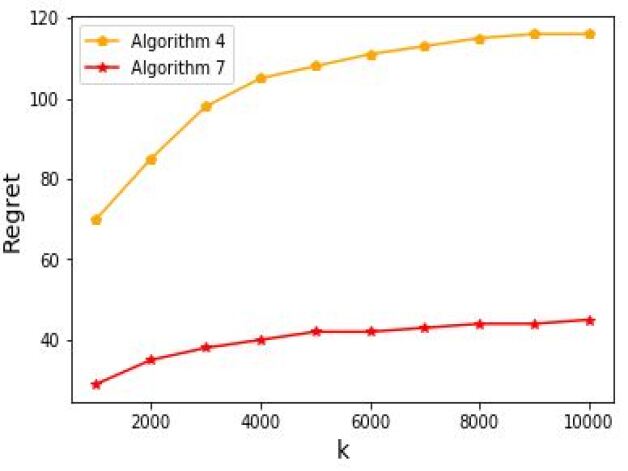

Following the setting in Bumpensanti and Wang (2020), we test two cases: 1) , and 2) , . We experiment with capacities for , and horizon length , for each case, respectively.

(a) , and (b) , and

(c) , and (d) , and

(e) , and (f) , and

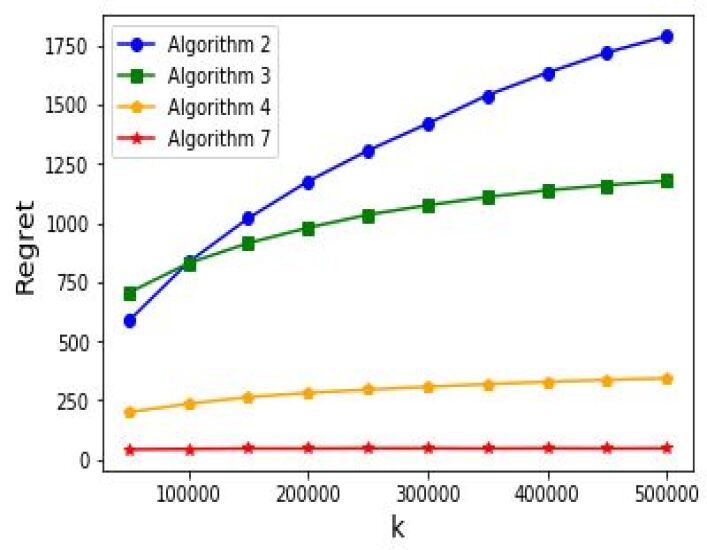

Figure 1 shows the regret of Algorithm 2, Algorithm 3 and Algorithm 4, namely the average gap between the algorithm’s total revenue and the hindsight optimum, under different settings. The first row shows the case where , , and , , . The second row shows the case where , , and , , . The third row shows the case where , , and , , . We observe that in all three cases, algorithm Algorithm 4 performs the best among all three algorithms, and Algorithm 2 performs the worst. This comparison result is aligned with our theoretical regret bounds shown in (16) and Theorem 4.4.

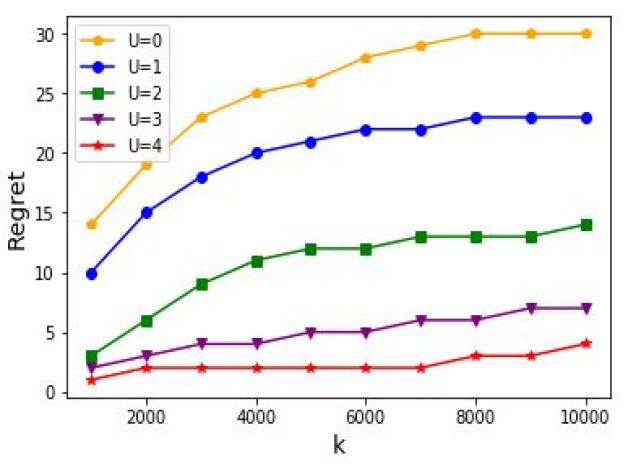

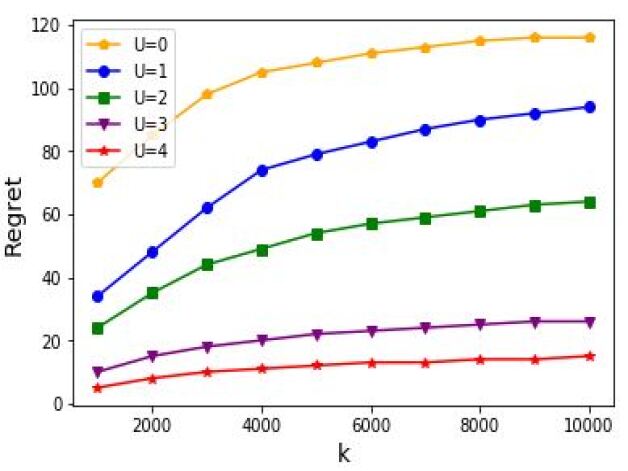

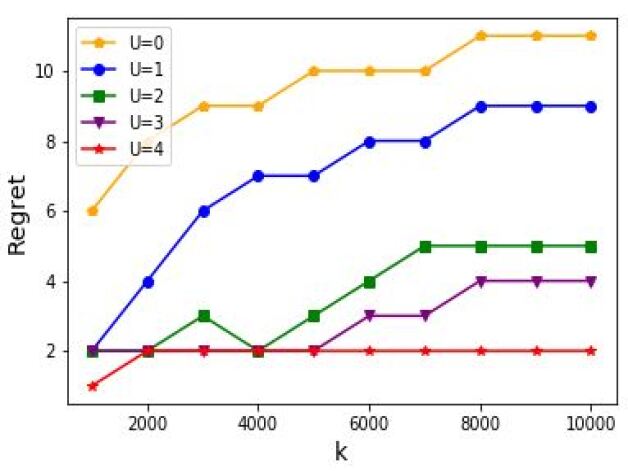

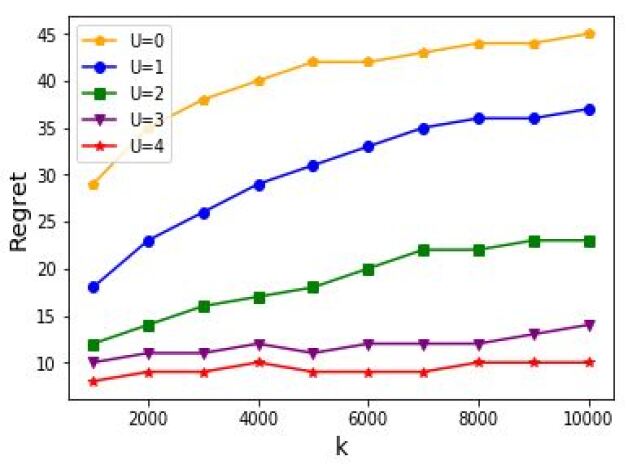

We next investigate the benefit of solving DLPs by examining the performance of Algorithm 6 under different LP-resolving times. Recall that Algorithm 6 runs Algorithm 5 as subroutines in the first epochs, and then runs Algorithm 3 as subroutines in the remaining epochs. We test the performance of Algorithm 6 for under two cases: 1) , , 2) , . We set capacity and horizon length . In both cases, we observe that the regret decreases significantly if we resolves DLPs in the first four epochs. The benefit of resolving DLPs becomes less significant as the value of increases.

(a) , and (b) , and

Next, we test the performance of Algorithm 7 and Algorithm 8, and compare their performance to that of Algorithm 4 and Algorithm 6 to show the effect of reusing bid prices. We test Algorithm 7 under two cases: 1) , , 2) , , and we set capacity . In both cases, we observe a significant improvement in regret by warm-starting each epoch with the bid prices from the last epoch.

We test the performance of Algorithm 8 using the same setting as that of Algorithm 7 where 1) , , 2) , ; capacity ; horizon length . We set parameter under both cases. By comparing the results in Figure 2 and Figure 4, we observe that the warm-starting technique is effective in improving the algorithm’s performance. In addition, we observe that the value of resolving DLPs in the case of Algorithm 8 is not as significant as that in the case of Algorithm 6.

(a) , and (b) , and

(a) , and (b) , and

5.2 Multiple Resources

Now we consider a NRM problem with multiple resources. Suppose that there are a thousand types of customers and a thousand types of resources. The total number of arrivals of each customer type follows an independent binomial distribution with mean , i.e., the arrival rate is for . Each type- customer pays price if accepted. We generate by randomly sampling a value from the set under a uniform distribution. We generate the bill-of-material matrix by setting each element

for all , . We then fix revenue vector and the bill-of-material matrix in the experiments. We set , and test our Algorithm 2, Algorithm 3 and Algorithm 4 under horizon length .

Figure 5 shows the average regret of Algorithm 2, Algorithm 3, Algorithm 4, Algorithm 7 over experiments with the fixed revenue vector and the fixed bill-of-material matrix . The regret results of different algorithms are aligned with those in the single-resource case: 1) all algorithms show convergence in regret as ; 2) among Algorithm 2, Algorithm 3 and Algorithm 4, Algorithm 4 performs the best and Algorithm 2 performs the worst; 3) Algorithm 7 improves the performance of Algorithm 4 by warm-starting each epoch with the bid prices from the last epoch.

6 Conclusion

In this paper, we study the quantity-based network revenue management problem and propose near-optimal algorithms with provable performance guarantees. In particular, our algorithm is the first to achieve regret bound among all the algorithms that do not solve any deterministic linear programs. Moreover, our algorithms are amenable to implementations in online platforms as the algorithms do not perform matrix inversions, and their memory consumption does not scale with the online traffic.

References

- Agrawal and Devanur (2016) Agrawal S, Devanur N (2016) Linear contextual bandits with knapsacks. Advances in Neural Information Processing Systems, 3450–3458.

- Agrawal and Devanur (2014) Agrawal S, Devanur NR (2014) Fast algorithms for online stochastic convex programming. Proceedings of the twenty-sixth annual ACM-SIAM symposium on Discrete algorithms, 1405–1424 (SIAM).

- Agrawal et al. (2014) Agrawal S, Wang Z, Ye Y (2014) A dynamic near-optimal algorithm for online linear programming. Operations Research 62(4):876–890.

- Airbnb (2020) Airbnb (2020) Airbnb q4 2020 shareholder letter. https://investors.airbnb.com/financials/default.aspx#quarterly, accessed: 2020-12-31.

- Arlotto and Gurvich (2019) Arlotto A, Gurvich I (2019) Uniformly bounded regret in the multisecretary problem. Stochastic Systems 9(3):231–260.

- Arlotto and Xie (2018) Arlotto A, Xie X (2018) Logarithmic regret in the dynamic and stochastic knapsack problem. arXiv preprint arXiv:1809.02016 .

- Atar and Reiman (2013) Atar R, Reiman MI (2013) Asymptotically optimal dynamic pricing for network revenue management. Stochastic Systems 2(2):232–276.

- Balseiro et al. (2020a) Balseiro S, Lu H, Mirrokni V (2020a) The best of many worlds: Dual mirror descent for online allocation problems. arXiv preprint arXiv:2011.10124 .

- Balseiro et al. (2020b) Balseiro S, Lu H, Mirrokni V (2020b) Dual mirror descent for online allocation problems. International Conference on Machine Learning, 613–628 (PMLR).

- Bumpensanti and Wang (2020) Bumpensanti P, Wang H (2020) A re-solving heuristic with uniformly bounded loss for network revenue management. Management Science .

- Chen and Farias (2013) Chen Y, Farias VF (2013) Simple policies for dynamic pricing with imperfect forecasts. Operations Research 61(3):612–624.

- Devanur and Hayes (2009) Devanur NR, Hayes TP (2009) The adwords problem: online keyword matching with budgeted bidders under random permutations. Proceedings of the 10th ACM conference on Electronic commerce, 71–78.

- Gallego and Van Ryzin (1994) Gallego G, Van Ryzin G (1994) Optimal dynamic pricing of inventories with stochastic demand over finite horizons. Management Science 40(8):999–1020.

- Gallego and Van Ryzin (1997) Gallego G, Van Ryzin G (1997) A multiproduct dynamic pricing problem and its applications to network yield management. Operations research 45(1):24–41.

- Hazan (2019) Hazan E (2019) Introduction to online convex optimization. arXiv preprint arXiv:1909.05207 .

- Jasin and Kumar (2012) Jasin S, Kumar S (2012) A re-solving heuristic with bounded revenue loss for network revenue management with customer choice. Mathematics of Operations Research 37(2):313–345.

- Li et al. (2020) Li X, Sun C, Ye Y (2020) Simple and fast algorithm for binary integer and online linear programming. arXiv preprint arXiv:2003.02513 .

- Li and Yao (2004) Li X, Yao DD (2004) Control and pricing in stochastic networks with concurrent resource occupancy. ACM SIGMETRICS Performance Evaluation Review 32(2):50–52.

- Li and Ye (2019) Li X, Ye Y (2019) Online linear programming: Dual convergence, new algorithms, and regret bounds. arXiv preprint arXiv:1909.05499 .

- Maglaras and Meissner (2006) Maglaras C, Meissner J (2006) Dynamic pricing strategies for multiproduct revenue management problems. Manufacturing & Service Operations Management 8(2):136–148.

- Medium (2018) Medium (2018) Online travel metrics: Traffic, marketing, channels, mobile. , accessed: 2020-12-31.

- Reiman and Wang (2008) Reiman MI, Wang Q (2008) An asymptotically optimal policy for a quantity-based network revenue management problem. Mathematics of Operations Research 33(2):257–282.

- Talluri and Van Ryzin (1998) Talluri K, Van Ryzin G (1998) An analysis of bid-price controls for network revenue management. Management Science 44(11-part-1):1577–1593.

- Talluri and Van Ryzin (2004) Talluri K, Van Ryzin G (2004) Revenue management under a general discrete choice model of consumer behavior. Management Science 50(1):15–33.

- Vera and Banerjee (2020) Vera A, Banerjee S (2020) The bayesian prophet: A low-regret framework for online decision making. Management Science .

- Williamson (1992) Williamson EL (1992) Airline network seat inventory control: Methodologies and revenue impacts. Ph.D. thesis, Massachusetts Institute of Technology.

- Wollmer (1992) Wollmer RD (1992) An airline seat management model for a single leg route when lower fare classes book first. Operations research 40(1):26–37.

7 Proofs for Algorithm 2

Without loss of generality, we prove lemmas, propositions and theorems with respect to Algorithm 2 with

and initial capacity , for any . Let and be the maximum and minimum of the initial capacity values, respectively. Then other notations in Algorithm 2 become

| (23) |

| (24) |

| (25) |

and

Suppose Algorithm 2 stops at the beginning of period . In particular, when the algorithm stops due to insufficient remaining resources at the beginning of period , namely due to some that violates , we have . Otherwise, we have .

7.1 Lemma 7.1

Lemma 7.1

There exists some random variable such that

almost surely, for any , where is defined in (13), and do not depend on , or .

Proof 7.2

Proof of Lemma 7.1.

Consider the following two cases.

-

•

Case 1: . Let denote a unit vector with the -th component being one. For any , since , we use (26) to obtain

(27) for all .

Conditioned on , since some resource has been depleted before the end of the horizon, we have , and

(28) where the first equality is by definition of , the first inequality is because resource is depleted by time , and the last inequality follows since .

-

•

Case 2: . Again, we use (26) to obtain

Finally, from (24) and (25), it is easy to derive

where and only depend on , the coefficients in , and .

This completes the proof. \halmos

7.2 Lemma 7.3

Lemma 7.3

The stochastic process as defined in (30) is a martingale for .

Proof 7.4

Proof of Lemma 7.3. Let denote all the information in periods where .

For the first term, since , we have

| (31) |

For the second term, let for denote an optimal solution to (29). The structure of (29) is simple enough that we can calculate for all :

-

•

given , we have ;

-

•

given , we have .

By definition, we know . Therefore, we have .

Notice that , since the value of has been determined at the end of period . Thus, by taking expectation over all customer types for , we have

| (32) |

| (33) |

Hence, we have

| (35) |

7.3 Lemma 7.5

Lemma 7.5 (Azuma’s Inequality)

Suppose is a martingale, and

| (37) |

almost surely, then for any positive integer and any positive , we have

| (38) |

7.4 Lemma 7.6

Lemma 7.6

Consider as defined in (30). With probability at least , we have

for all , where and do not depend on , or .

Proof 7.7

Proof of Lemma 7.6. We apply Azuma’s inequality to obtain

| (39) |

where satisfies . We next find the proper values of , and .

Let for denote an optimal solution to in (29). We have .

By definition of , we know

Recall and . We remove the non-positive terms in the above equation to obtain

| (40) |

On the other hand, we remove the non-negative terms to obtain

| (41) |

In sum, we have

| (42) |

for all .

This completes the proof. \halmos

7.5 Lemma 7.8

Lemma 7.8

Given the definition of in (23), we have

Proof 7.9

Proof of Lemma 7.8. Consider as defined in (29). By weak duality, we have for any . Recall that and By definition, we know

Now let for and let denote an optimal solution to (29). We can derive

The last inequality follows since 1) the first term on the left hand side is non-positive, and 2) for all by definition. Divide both sides by , and we obtain the result. \halmos

7.6 Proposition 3.2

Now we prove the following proposition, which is more general than Proposition 3.2. Let denote the revenue of Algorithm 2 with start time , end time and initial capacity .

Proposition 7.10

With probability at least where , we have

| (43) |

where do not depend on , , or .

Proof 7.11

Proof of Proposition 7.10.

By Proposition 7.6 and definition of , we have with probability at least that

| (44) |

By Lemma 7.1, we know there exists some random variable such that

| (45) |

almost surely, for any .

Recall that is the Lagrangian relaxation defined in Equation (29). By weak duality, we have for all . Combining this with (44) and (45), we can derive that with probability at least that

for any . Now we set . By Lemma 7.8, we know . We continue to derive

Finally, we set to obtain

which completes the proof.

7.7 Lemma 4.2

Proof 7.12

Proof of Lemma 4.2. Let be an optimal solution to where for .

First, suppose is a basic feasible solution (BFS). Let be the set of indices for the basic variables, and the set of indexes for the non-basic variables. By definition, we know given there exists constraints in (17). In addition, the reduced cost of the basic variables is zero, i.e., we have

Consider moving from along the -th basic direction where . By definition, , which implies . In particular, we have two types of basic feasible directions.

-

•

where corresponds to the index of non-basic variable or . In this case, , and moving one unit along results in a change of revenue ;

-

•

where corresponds to the index of non-basic variable . In this case, , and moving one unit along results in a change of revenue .

Define bid price vector . Under Assumption 4.1, we know there are at most columns such that . Since we already have for and , we know for all . In addition, since is the optimal solution, we know all basic directions are strict gradient descent directions, namely,

In particular, we have for , and for . Thus, we know is unique.

Second, suppose is not a BFS. Then following the same argument, we know there exists a BFS optimal solution that is unique, which results in a violation.

Given any selection of basis index and , define , i.e., the maximum value of for . Since there are finitely many selections of basis, we know there exists a constant such that for any price vector .

Now consider any feasible solution of (17), and direction . Given the basic direction for associated with optimal solution , we know can be written as a convex combination of , namely, there exist constants for such that

We have

which is guaranteed to be smaller than a fixed constant.

7.8 Proposition 4.3

Now we prove a lemma and a proposition that generalize the results of Proposition 4.3.

Let denote the number of type- customers accepted by Algorithm 2 with start time , end time and initial capacity .

Let denote an optimal solution to

Let , and .

Lemma 7.13

Proof 7.14

Proof of Lemma 7.13.

Consider with capacity vector and upper bound vector where for . Define for , and . By definition, we know is an optimal solution to . By Lemma 4.2, we know is unique, and is a BFS of the LP.

If , we define , where for . We know is a feasible solution to . Now define direction . By Lemma 4.2, we know is guaranteed to be smaller than a fixed constant, denoted as .

Since , we know

Since , we know there exist constants and such that for all , we have . This implies , and hence

By definition, we know . Therefore,

Proposition 7.15

Under Assumption 4.1, with probability at least where , we have

| (46) |

for all , where does not depend on , or .

Proof 7.16

Proof of Proposition 7.15.

Given , define . Let denote the event . Since is a binomial random variable with mean . By Hoeffding’s inequality, we have

Define . Let denote the event . By Proposition 7.10, we know that . Therefore, the joint event happens with probability at least

where the inequality follows by the union bound.

Consequently, it suffices to prove Proposition 7.15 conditional on . We consider two cases:

where we define .

In case 1) where , we have conditioned on event . By Lemma 7.13, we know immediately .

In case 2) where , we first project onto . Let be the projection of onto . Since , where denotes a vector of ones in , by the definition of projection, we know

| (47) |

which then implies

| (48) |

where the second inequality is due to the Cauchy-Schwartz inequality.

Conditioned on , we have , which in combination with (48) shows . Since , by Lemma 7.13, we have . By the triangle inequality, we have

To summarize, in both cases, we have . Proposition 7.15 follows since for any .

8 Proof for Algorithm 3

8.1 Theorem 4.4

Proof 8.1

Proof of Theorem 4.4.

Consider Algorithm 3 with technical parameters

Let be the starting time period of phase II, and the starting time period of phase III, where , denote the lengths of phase I and phase II, respectively.

Let , denote the revenue of the auxiliary algorithms -I and -II, respectively. By definition, we have

| (49) |

Therefore, the regret bound of the algorithm is . \halmos

8.2 Proposition 4.5

Recall Algorithm 3 with technical parameters , , that satisfy , and . The algorithm calculates , and . Let be the starting time period of phase II, and the starting time period of phase III, where , denote the lengths of phase I and phase II, respectively.

Proof 8.2

Proof of Proposition 4.5.

We first show (1) .

By definition of the algorithm, we have , where denotes the value of the hindsight LP over periods to as shown in (19).

Since for is a binomial random variable with mean , we apply Hoeffding’s inequality to obtain

We then have

We next show (2) given , and .

Consider a variant of Algorithm 3 that does not include the thresholding conditions (Line 5 to Line 11). We refer to this algorithm as Algorithm 3’. In other words, Algorithm 3’ simply runs the Algorithm 2 as a subroutine in Phase II. Let and denote the number of type- customers accepted by Algorithm 3 and Algorithm 3’, respectively, during .

Observe that the virtual capacity vector defined in phase II describes the capacity updating procedure of Algorithm 3’. In addition, Algorithm 3 and Algorithm 3’ have identical dual updates until the subroutine of Algorithm 2 in Algorithm 3’ stops. Since customer types uses an additional amount of capacities in the case of Algorithm 3, we have

| (50) |

Let denote the number of type customers accepted by Algorithm 3 during if we were allowed to go over capacity limits . We then have

| (51) |

| (52) |

Recall that is the hindsight optimal solution to , defined in (19). Define events

| (53) |

The definition of these events is similar to that in Bumpensanti and Wang (2020).

Observe that under event , we have for all , and thus

Combining (50), (51) and (52), we have

| (54) |

which means Algorithm 3 will not stop before time due to insufficient capacity . Therefore, conditioned on event , we have for all , and hence

| (55) |

This means the decision-maker would still be able to achieve the hindsight optimum of if she follows the decision of Algorithm 3 in periods and then accepts type- customers during periods .

Apply Hoeffding’s inequality to bound . We have

Thus, we have

By Lemma 8.6, we have , and therefore,

| (56) |

We last show (3) given , and .

Observe that Algorithm 3 runs Algorithm 2 as a subroutine using a virtual copy of initial capacity . In particular, the virtual capacity inflates any resource with small capacity to , and truncates any resource with large capacity to . By definition of , we know is an upper bound on the units of resource consumption over the length of phase III. Define

| (57) | ||||

Compare with as defined in (21). We know

| (58) |

Now consider those resources with inflated virtual capacities. Recall that denotes the upper bound on the revenue that can be achieved from one unit of resource . Let denote the actual revenue of Algorithm 3 in phase III, namely and the revenue of the Algorithm 2 subroutine based on virtual capacity , namely . We have

| (59) |

Combining (58) and (59), we have

| (60) |

Notice that is the regret of Algorithm 2 in phase III based on the virtual capacity , and we can apply Proposition 7.10 to upper bound this regret. In particular, the notations in Proposition 7.10 become , , and thus . Now take . We have . Given , we know .

For simplicity of exposition, let and .

Define event . By definition of auxiliary algorithm -II, we have

| (62) |

In particular, we have

where the second term is due to the following

Additionally, conditioned on event , by (60) and (8.2), we have

| (63) |

where . The equality follows given that and by definition.

Combining the results above, we have

This completes the proof. \halmos

8.3 Lemma 8.3

Lemma 8.3

Remark 8.4

More specifically, is the maximum absolute value of the elements in the inverses of all invertible submatrices of the BOM matrix . In a special case when all entries of are either or , we have .

Proof 8.5

Proof of Lemma 8.3. The Lemma follows theorem 4.2 in Reiman and Wang (2008).

8.4 Lemma 8.6

Recall Algorithm 3 with start time , end time , initial capacity vector , and technical parameters , , that satisfy , and . The algorithm calculates , and . Let be the starting time period of phase II, and the starting time period of phase III, where , denote the lengths of phase I and phase II, respectively.

Recall that is the number of type customers accepted by Algorithm 3 over periods if we were allowed to go over the real capacity limits , for is the hindsight optimal solution to , and for is the optimal solution to the DLP in (5). Under Assumption 4.1, by Lemma 4.2, we know (5) has a unique optimal solution, which is equivalent to the optimal solution of , and thus we know for .

Lemma 8.6

Proof 8.7

Proof.

By union bound, we have . Thus, it suffices to show

| (66) |

Define events

| (67) |

| (68) |

Thus, we have for all .

Let denote the number of type- customers accepted by Algorithm 3 during periods . Recall that . Apply Proposition 7.15 to bound given , and we obtain

| (69) |

with probability at least .

In addition, by definition, we know for are decisions of the Algorithm 2 subroutine in phase II. Apply Proposition 7.15 to bound given , and we obtain

| (70) |

with probability at least .

Given and , set . We then have and .

In the following proof, we will show (66) in three cases:

First, we consider case 1) .

By Proposition 7.15, we know

with probability at least , where the last inequality follows since . This implies .

Conditioned on , we have , and thus .

Now consider event . Define variables

| (71) |

We know by (65) in Lemma 8.3 that . Thus, we have

where the second inequality follows since , and the last inequality follows by union bound and the observation that when happens, at least one of the following two events

must happen.

Let . By definition,

| (72) |

By Hoeffding’s inequality, we have

| (73) |

Thus, we obtain

| (74) |

In addition, by Hoeffding’s inequality, we have

| (75) |

Therefore, in case 1), we have

| (77) |

where the last line follows since .

Next, we consider case 2) .

By Proposition 7.15, we know with probability at least that

where the last equality follows since . This implies .

Conditioned on , we have , and . Thus, .

Now consider event . We know by (65) in Lemma 8.3 that . Thus, we have

where the last line follows because

| (78) |

| (79) |

Therefore, in case 2), we have,

| (80) |

Last, we consider case 3) . We have

| (81) |

We first show that and .

By Proposition 7.15, we know with probability at least that

where the last inequality follows since . This implies

| (82) |

In addition, we know with probability at least that

where the last inequality follows since and . This implies

| (83) |

Now consider event conditioned on .

Observe that the event is equivalent to

| (85) |

Therefore, when happens, at least one of the following three events must happen:

| (86) |

| (87) |

| (88) |

By Proposition 7.15, we know that with probability at least ,

where the last inequality follows since and .

Since given , we know

and therefore, we have

| (89) |

In addition, we know with probability at least that

Thus, we have

| (90) |

By Hoeffding’s inequality, we have

| (91) |

where the last inequality follows since .

Now consider event conditioned on .

We know by (65) that . Thus, we have

| (93) | ||||

| (94) |

Observe that the event is equivalent to

| (95) |

Therefore, when happens, at least one of the following four events must happen:

| (96) |

| (97) |

| (98) |

| (99) |

By Proposition 7.15, we know with probability at least that

Since given , we know , and hence

Therefore, we have

| (100) |

In addition, we know with probability at least that

Thus, we have

| (101) |

By Hoeffding’s inequality, we have

| (102) |

In addition, we have

| (103) |

9 Variants of Algorithms

9.1 Primal-dual restart algorithm

Algorithm 4 shows the detailed procedure of our restart algorithm that does not require solving any LPs. The algorithm includes a total of epochs. Each epoch , where , starts from period and ends at period , where is the time length between the starting period of epoch and period . At the beginning of each epoch, Algorithm 4 restarts Algorithm 3. The restart schedule is shown in Figure 6.

9.2 Hybrid restart algorithm

In the following, we first introduce the LP-based thresholding algorithm in Algorithm 5, which is called as subroutines in Algorithm 6.

Algorithm 5 takes as inputs a start time , an end time , initial capacity at the start time, and technical parameters and that satisfy and .

At the beginning of the time horizon, Algorithm 5 solves a DLP, and uses its optimal solution to calculates the thresholding conditions. The entire horizon is then divided in two “phases”: in phase I, Algorithm 5 makes probabilistic allocation decisions; in phase II, Algorithm 5 runs the primal-dual algorithm in Algorithm 2.

Now we introduce Algorithm 6, which is a hybrid of Algorithm 5 and Algorithm 3 under a similar restart schedule shown in Figure 6.

Algorithm 6 includes a total of epochs. Each epoch , where , starts from period and ends at period , where is the time length between the starting period of epoch and period . At the beginning of the first epochs, Algorithm 6 runs (restarts) Algorithm 5 as a a subroutine, and at the beginning of the remaining epochs, Algorithm 6 runs (restarts) Algorithm 3 as a subroutine.