A Computationally Efficient Classification Algorithm in Posterior Drift Model: Phase Transition and Minimax Adaptivity

Abstract

In massive data analysis, training and testing data often come from very different sources, and their probability distributions are not necessarily identical. A feature example is nonparametric classification in posterior drift model where the conditional distributions of the label given the covariates are possibly different. In this paper, we derive minimax rate of the excess risk for nonparametric classification in posterior drift model in the setting that both training and testing data have smooth distributions, extending a recent work by Cai and Wei, (2019) who only impose smoothness condition on the distribution of testing data. The minimax rate demonstrates a phase transition characterized by the mutual relationship between the smoothness orders of the training and testing data distributions. We also propose a computationally efficient and data-driven nearest neighbor classifier which achieves the minimax excess risk (up to a logarithm factor). Simulation studies and a real-world application are conducted to demonstrate our approach.

Keywords: Transfer Learning, Domain Adaptation, Computational advantage, Adaptive Rate-Optimal

1 Introduction

Despite the significant successes of conventional classification algorithms, one of their unavoidable limitations is to assume that the source (training) data and target (testing) data are identically distributed. In real-world scenarios, it could be difficult and expensive to obtain source data that has the same distribution as the target data (Weiss et al.,, 2016). Thus, an algorithm which can overcome such discrepancy would be highly valuable. Transfer learning is a promising tool to build models for the target domain by transferring data information from the related source domain. In comparison with traditional machine learning algorithms, transfer learning has demonstrated advantages in many aspects such as image classification (Zhu et al.,, 2011; Han et al.,, 2018; Hussain et al.,, 2018), autonomous driving (Kim and Park,, 2017), recommendation system (Zhao et al.,, 2013; Zhang et al.,, 2017), etc. An important transfer learning technique is the so-called domain adaptation (Weiss et al.,, 2016), in which the information or knowledge is adapted from one or more source domains to the target domain. Empirical successes of domain adaptation have attracted increasing attention to the study of its theoretical properties. For example, Ben-David et al., (2007) derive a bound on the generalization error of the classifiers trained from data in the source domain, later extended by Blitzer et al., (2008), Zhang et al., (2012) and Zhao et al., (2018) to the case where the classifiers are trained from both source and target domains. Researchers have also proposed additional structural relationships between the source and target domains, e.g., the covariate shift model with different marginal distributions and the posterior drift model with different conditional distributions, under which the generalization error bounds are successfully established. To name a few, see Shimodaira, (2000); Huang et al., (2007); Sugiyama et al., (2008); Mansour et al., (2012); Hoffman et al., (2018); Kpotufe and Martinet, (2018); Scott et al., (2013); Natarajan et al., (2013); Manwani and Sastry, (2013); Gao et al., (2016); Natarajan et al., (2017); Cannings et al., (2020); Cai and Wei, (2019).

A notable work is Cai and Wei, (2019) who propose a -nearest neighbor (NN) classifier based on the posterior drift model and derive minimax optimality. The -nearest neighbors are detected over the entire source and target data which could be computationally expensive when data size is large. Meanwhile, the theoretical results only involve the smoothness of the target distribution but the impact of the smoothness of the source distributions remains unknown. The aim of this work is to further strengthen the two aspects. Specifically, we propose a more computationally efficient NN classifier that requires detecting the nearest neighbors for local data only. We discover a phase transition phenomenon for the minimax excess risk characterized by the mutual relationship between the smoothness orders of the source and target distributions, which degenerate to Cai and Wei, (2019) in the special case when the smoothness order of the source distributions vanishes. Such a phenomenon provides a more complete understanding on the impact of smooth data distributions in transfer learning. In the following subsection, we describe our contributions in more details. Before that, let us introduce some terminologies and notation.

Terminologies and Notation: Let denote the Euclidean norm of the vector . For two sequences and , we say if for some constant and all sufficiently large . For , let be the largest integer that less than or equal to . Let and be probability distributions over . For , the -dimensional is regarded as covariates or features, and is the binary label of . For drawn from (or ), let (or ) denote the marginal probability distribution of . Define and as the conditional distributions of given for any . For positive sequences and , we say () if () for some and all large enough . We say if and . We use to denote the support of the a probability measure .

1.1 Nonparametric classification in posterior drift model

Suppose that are i.i.d. observations from , and are i.i.d. observations from . Moreover, we assume these observations from and are mutually independent. For simplicity, we call the -data and the -data. Given future covariates from , we are interested in predicting its unknown binary label based on the full training data , where

| (1.1) |

We adopt the posterior drift model proposed by Scott, (2019), in which and have common supports, whereas the conditional distributions of given under , namely and , are possibly different. In this model, is the source distribution and is the target distribution. This model has been recently adopted by Cai and Wei, (2019) in nonparametric classification who proposed an optimal adaptive NN classifier. Since their method requires identifying the nearest covariates among all covariates in , which requires attempts and might be computationally expensive. The computational cost easily scales up when the training data consists of observations from multiple distributions. Hence, it is interesting to design a more efficient algorithm that can achieve the same optimality.

1.2 Our Contributions

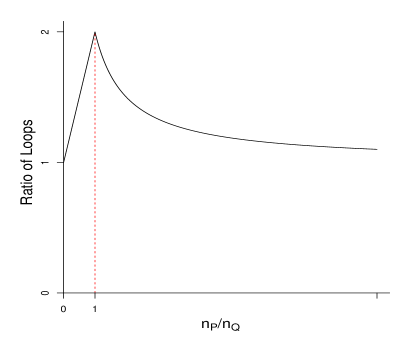

Our first contribution is to propose a more computationally efficient adaptive -NN classifier, i.e., Algorithm 1 in Section 2. Notably, our method requires attempts to identify the nearest covariates. Consequently, the ratio of attempts required by Cai and Wei, (2019) and Algorithm 1 is , which is nearly 2 if (see Figure 1). In other words, when -data and -data have equal amount of data points, Algorithm 1 only requires nearly half computational cost of Cai and Wei, (2019). The ratio of attempts further increases if more source distributions are involved, hence, the computational cost of our method, compared to Cai and Wei, (2019), will be further reduced. See discussions in Section 3.3.

Our second contribution is in theoretical aspect. We establish exact orders for the minimax excess risk when are -Hölder smooth (see Assumption A2). In contrast, Cai and Wei, (2019) established exact orders for the minimax excess risk in the special case . It turns out that when , the minimax rate has a faster order, demonstrating the advantage of utilizing smooth source distributions. To describe our findings, consider for simplicity. Below is a summary of the results in which the orders for the minimax excess risk demonstrate a phase transition characterized by a mutual relationship between and :

| (1.2) |

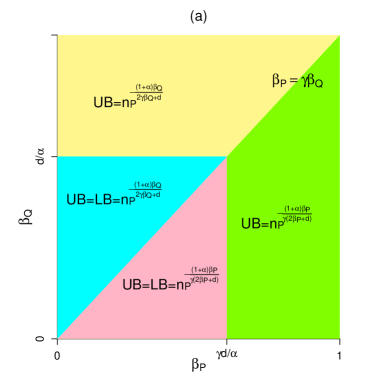

where quantifies the Tsybakov noise level (see Assumption A3) and measures the relative signal strength of and (see Assumption A5). See Figure 2(a) for an illustration of (1.2). Note that (1.2) excludes the regions and in which only upper bounds on the minimax excess risk are available. Interestingly, the upper bounds are super fast , see Figure 2(b), which is consistent to the findings of Audibert and Tsybakov, (2007). The orders of the minimax excess risk are fast or in a nonparametric rate () in other domains of . The results are further extended to general in Section 3.2, and to multiple source distributions in Section 3.3.

2 A Computationally Efficient Adaptive NN Classifier

In this section, we propose a computationally efficient adaptive NN classifier. For any , and , let denote the th nearest covariate of among , and let denote the label of . One can similarly define and . Let

| (2.1) |

Here () is the NN estimator of () based on the -data (-data). Inspired from Cai and Wei, (2019), we can aggregate and into a weighted NN estimator:

where are positive weights. The corresponding NN classifier is then defined as

| (2.2) |

A limitation of is that it requires predetermined . To address this, we propose Algorithm 1 in which the parameters are data-driven.

To ease presentation, Algorithm 1 has only considered . When , by flipping and we can set during the loops until the same stopping rule is met. Below we discuss the intuition why Algorithm 1 performs optimal. Let , so we can rewrite as , whose “signal,” defined as the absolute deviation from random guess, and “standard deviation” are given as and , respectively. During each loop, Algorithm 1 finds the “optimal” that minimizes the “signal-to-noise” ratio:

| (2.3) |

By direct calculations, the minimal value of (2.3) is which is achieved at . Therefore, Algorithm 1 scans the first such that the minimal “signal-to-noise” ratio is greater than a threshold . The choice of such threshold is inspired from Cai and Wei, (2019), under which it can be shown that, with high probability, and have the same sign. Here is the collection of all covariates. Under assumptions in Section 3, is can be shown that has the same sign as , so is asymptotically optimal.

To conclude this section, we briefly discuss the computing advantage of our method. In Algorithm 1, is selected over which requires attempts. In contrast, Cai and Wei, (2019) selects over a set of cardinality , hence, requires attempts. Therefore, Algorithm 1 is computationally more feasible than Cai and Wei, (2019).

3 Asymptotic Theory

In this section, we explore the asymptotic properties of in (2.2) and provided in Algorithm 1. We start from the easier case , and proceed to the general case .

3.1 Minimax Rate for the Excess Risk when

When , we have , where is given in (2.1). Meanwhile, by (2.3) we have . Thus, Algorithm 1 becomes the following Algorithm 2.

Before investigating the asymptotic properties of the above classifiers, we introduce some technical assumptions. Throughout, let denote the Lebesgue measure on .

Assumption A1.

(Common Support and Strong Density) There exist an and constants such that

-

(a)

is the common support of the marginal distributions and ;

-

(b)

for all and ;

-

(c)

and , for all .

Assumption A2.

(Hölder Smoothness) There exist constants and with such that are -Hölder smooth, i.e., and for all .

Assumption A3.

(Tsybakov’s Noise Condition) There exist constants and such that, for all , .

Assumption A4.

(Relative Signal Exponent Condition) For all , it holds that

-

(a)

;

-

(b)

for some constants .

Assumption A1 consists of three aspects. Assumption A1(a) requires supp()supp() which can be relaxed to supp() supp() with a slight modification in the proof. The latter is necessary since otherwise there will be a covariate in supp() supp() which is unpredictable by the -data. Assumptions A1(b) and A1(c) are the so-called Strong Density Assumption commonly used in literature (see Audibert and Tsybakov,, 2007). Assumption A1(b) regularizes the feature space . Assumption A1(c) assumes that the densities of and are bounded away from zero and infinity.

Assumption A2 requires that and are Hölder smooth with orders and , which includes the special case in Cai and Wei, (2019). Assumption A3 is the so-called Tsybakov noise condition with a noise exponent (see Mammen et al.,, 1999; Audibert and Tsybakov,, 2007). Assumption A4, firstly introduced by Cai and Wei, (2019), consists of two parts. Assumption A4(a) requires that the Bayes classifiers and are essentially the same. Assumption A4(b) measures the relative signal strength of and . Similar assumption is also proposed by Hanneke and Kpotufe, (2019).

Recall that the excess risk of under is defined as

where is the classification risk of classifier under , and is the Bayes classifier defined as . Let be the collection of satisfying Assumptions A1-A4, where is the collection of constants in the statements of the above assumptions. Based on the above assumptions and notation, the following theorem provides upper bounds for the excess risk of and in the special case .

Theorem 1.

The following statements hold when :

-

(a)

If and , then ;

-

(b)

If and , then .

Moreover, the following holds for the classifier proposed in Algorithm 2:

-

(a)

If , then ;

-

(b)

If , then .

Theorem 1 provides upper bounds for the excess risk of and over in two smoothness scenarios: and . Up to logarithmic sacrifice, performs equally well as . When is small, all upper bounds become smaller, indicating that more information has been transferred from to to boost the classification performance.

Under certain circumstances, the excess risk has a very fast convergence rate. For instance, the excess risk is faster than if and , or and ; it is faster than if and , or and . It is easy to see that these results degenerate to Audibert and Tsybakov, (2007) in the conventional setting and . Our findings are summarized in Figure 2(b).

The following theorem provides the minimax lower bounds for the excess risk.

Theorem 2.

If , then the following statements hold:

-

(a)

If and , then ;

-

(b)

If and , then ,

where is a positive constant relying on , and the infimum is taken over classifiers constructed on the -data.

We emphasize that the conditions and are necessary to obtain minimax lower bounds. In fact, in the special case , we have and , so both conditions reduce to , which was used by Audibert and Tsybakov, (2007) to establish the minimax lower bounds for the excess risk. Without assuming , the minimax lower bound remains unknown (see Andrea and Samory,, 2017).

Combining Theorem 1 and Theorem 2, we immediately have the following conclusion:

-

(a)

If and , then ;

-

(b)

If and , then .

Consequently, and both achieve the minimax optimal convergence rate. The optimal rate does not change when , while it tends to zero faster when . The above conclusions are summarized in Figure 2(a) in which a phase transition phenomenon is observed.

3.2 Extensions to General

We extend the results in Section 3.1 to general . We need the following assumption, a stronger version of Assumption A4.

Assumption A5.

(Mutual Relative Signal Exponent Condition) For all , it holds that

-

(a)

;

-

(b)

for some constants .

Assumption A5 requires an additional upper bound in comparison with Assumption A4. After rewriting this bound as , we can see the additional condition essentially requires being the relative signal exponent of with respective to , which assesses the information that can be transferred from to (see the discussion right after Theorem 1). Therefore, it is reasonable to view as the mutual relative signal exponent.

Let be the collection of satisfying Assumptions A1, A2, A3 and A5, where is the collection of constants involved in the corresponding assumptions. Clearly, is a subset of . The following theorem extends the results in Theorem 1 to general .

Theorem 3.

Suppose that either or . Then the following statements hold:

-

(a)

If , , , and , where , then

(3.1) -

(b)

If , , and , where , then

(3.2)

Moreover, the adaptive classifier proposed in Algorithm 1 has the following properties:

-

(a)

If , then

-

(b)

If , then

Theorem 3 implies that the excess risks of and have the same upper bounds under general . The bounds under are derived over , which is a subset of , so it is interesting to explore the upper bounds over as well. A reexmination of the proof reveals that, if , then

| (3.3) |

When , (3.2) and (3.3) degenerate to Theorem 1 both being optimal thanks to Theorem 2. For general , (3.2) is optimal thanks to Theorem 4 (b), whereas (3.3) is substantially slower than the lower bound stated in Theorem 4 (a).

Theorem 4.

The following statements hold:

-

(a)

If and , then

-

(b)

If and , then

where is a constant depending on , and the infimum is taken over the classifiers constructed based on the entire data described in (1.1).

Theorem 4 provides lower bounds for the minimax excess risk under and . Combining Theorem 3 and Theorem 4, we get that

-

(a)

if and , then ;

-

(b)

if and , then .

In view of Theorems 1-4 and (3.3), we summarize the (sub)optimality of convergence rate for the minimax excess risk in the following Table 1.

| rate for | Optimal | Optimal | |

|---|---|---|---|

| rate for | Optimal | Optimal | |

| rate for | Optimal | Optimal | |

| rate for | Optimal | Suboptimal |

3.3 Extensions to Multiple Sources

In this section, we extend the previous results to the scenario where the data come from multiple sources. Multi-source scenario is common in big data research (Zhang et al.,, 2015; Shang and Cheng,, 2017). Suppose that, for , the observations are generated from a source distribution . Without loss of generality, assume . Let be the target distribution. For simplicity, assume , though the results are extendable to general . Similar to Section 3.1, define the NN classifier as follows:

where , is the NN estimator of based on the nearest covariates in -data, and is the corresponding weight. We also propose an adaptive classifier in Algorithm 3 in which the parameters ’s and ’s are data-driven. Note that Algorithm 3 selects the tuple over , which requires attempts. In contrast, Cai and Wei, (2019) requires attempts to select the tuple, hence, the ratio of attempts for Cai and Wei, (2019) and Algorithm 3 is which is nearly if .

We extend the theoretical results in Sections 3.1 and 3.2 to multi-source scenario. For that, let and be the collection of tuples such that for .

Theorem 5.

Let , . If and for all , then the following holds:

| (3.4) | |||

Furthermore, there exists a constant depending on such that

where the infimum is taken over the classifiers based on the entire data , , .

4 Monte Carlo Experiments

In this section, we investigate the finite-sample performance of the proposed algorithms through Monte Carlo experiments. We chose , the source and target distributions, to be uniform on . The data generating process (DGP) proceeds by first generating features and then generating label . Various choices of are summarized below.

-

DGP 1:

For , , ,

and

-

DGP 2:

For , , ,

and

We will comment both DGPs satisfy Assumptions A1, A2, A3, A5 are all satisfied. Since is uniformly distributed on under both and , Assumption A1 holds. Obviously, we have and which implies Assumption A2. We can verify Assumption A3 with in both DPGs, and show that Assumption A5 is satisfied for both DGPs with

and

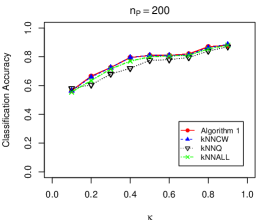

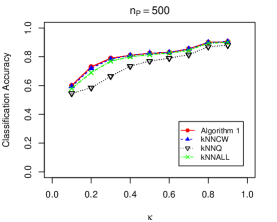

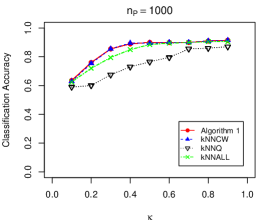

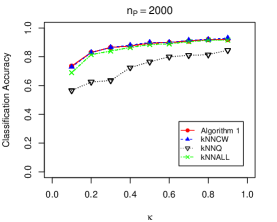

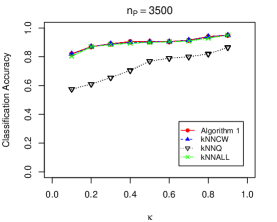

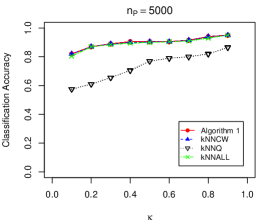

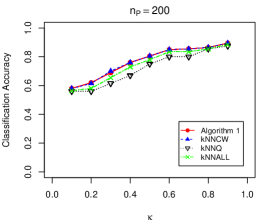

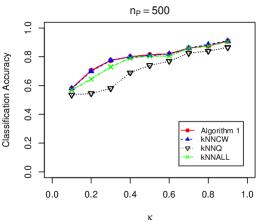

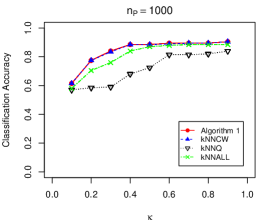

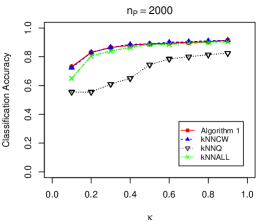

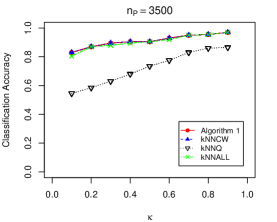

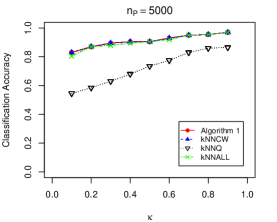

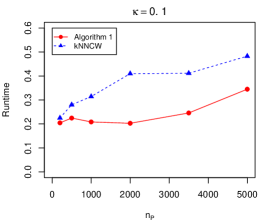

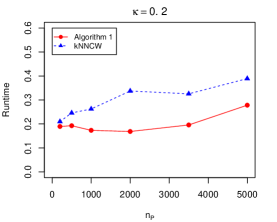

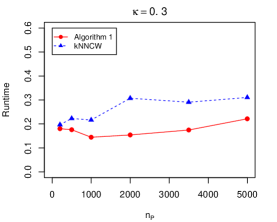

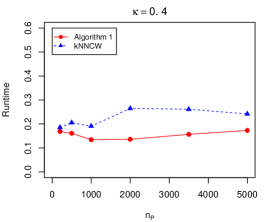

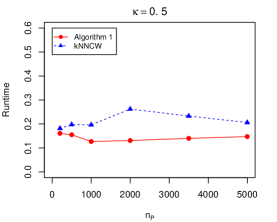

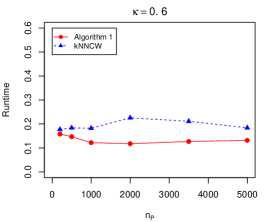

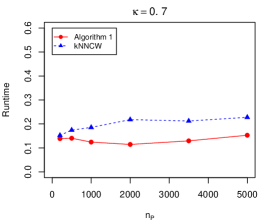

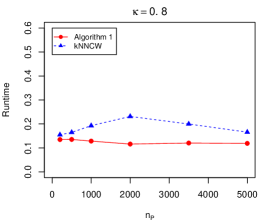

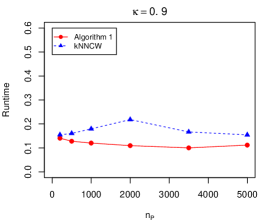

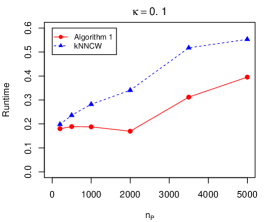

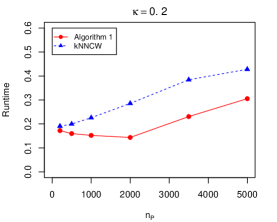

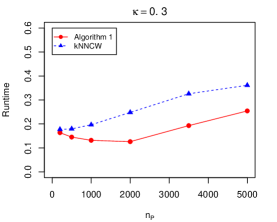

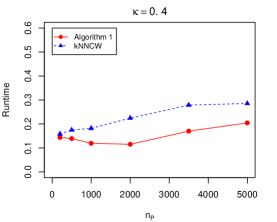

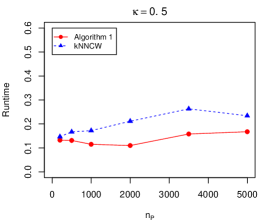

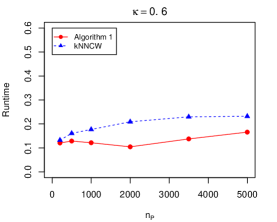

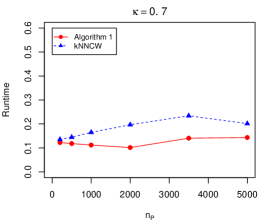

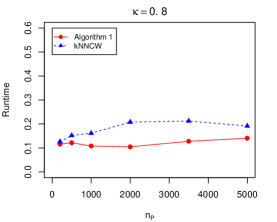

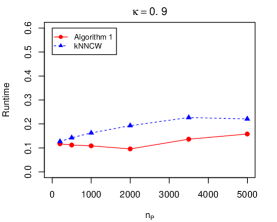

Heuristically, with a larger , both and become stronger, which makes the classification problem easier. In both DGPs, we chose , and , . We considered three competitors: (NNCW) the adaptive algorithm proposed in Cai and Wei, (2019); (NNQ) naive NN on -data only; (NNALL) naive NN on the entire data (recall that is the collection of both -data and -data). To approximate the classification accuracy, we generated new features and calculated their predicted label based on Bayes classifier, and the classification accuracy of the proposed algorithms is approximated by the percentage of producing the same prediction as over replicated trials. Moreover, we compare the runtime of Algorithm 1 and NNCW in different settings.

Numerical results are summarized in Figures 3-6, in which several interesting findings can be observed. First, under different combinations of and , the performance of Algorithm 1 is almost identical to NNCW in both DGPs, which meets the theoretical results of Theorem 3. Second, when increasing , the performance of NNQ, which is only relying on -data, becomes much poorer in comparison with the other three classifiers.

Third, in terms of classification accuracy, NNALL is comparable with Algorithm 1 and NNCW when ether is relatively large or relatively small in comparison with . However, the difference becomes significant when and . Last, according to Figures 5 and 6, our algorithm is faster than NNCW. In particular, the computational advantage of Algorithm 1 is notable when .

5 Empirical Application

We apply the proposed adaptive algorithm to the Australian Credit Approval dataset (Quinlan,, 1987) downloaded from UCI machine learning repository (Dua and Graff,, 2017). After removing missing values, we keep four continuous explanatory variables and normalize them into , whose descriptive statistics are summarized in Table 2. The response variable indicates approval or disapproval status. Based on the binary explanatory variable , we further divide the observations into two datasets: -data consists of observations and -data consists of observations. We randomly selected observations from -data with , and combined them with -data to train the four classifiers: Algorithm 1, NNCW, NNQ, and NNALL. The rest observations are treated as the testing dataset. The classification accuracy is calculated based on independent replications. Results are summarized in Table 3 which indicate that our proposed algorithm leads to a slightly better classification accuracy.

| V1 | y | |||||||

|---|---|---|---|---|---|---|---|---|

| 1st Qu. | 0.134 | 0.036 | 0.006 | 0.040 | class 0 | 222 | 383 | |

| Median | 0.224 | 0.098 | 0.035 | 0.080 | class 1 | 468 | 307 | |

| Mean | 0.268 | 0.170 | 0.078 | 0.092 | ||||

| 3rd Qu. | 0.360 | 0.257 | 0.092 | 0.136 |

| Algorithm 1 | KNNCW | KNNQ | KNNALL | |

|---|---|---|---|---|

| 100 | 57.52 | 56.61 | 52.36 | 56.16 |

| 120 | 57.33 | 56.43 | 52.79 | 56.01 |

| 140 | 56.53 | 56.04 | 53.26 | 55.72 |

References

- Andrea and Samory, (2017) Andrea, C. A. L. and Samory, K. (2017). Adaptivity to noise parameters in nonparametric active learning. volume 65 of Proceedings of Machine Learning Research, pages 1383–1416, Amsterdam, Netherlands. PMLR.

- Audibert and Tsybakov, (2007) Audibert, J.-Y. and Tsybakov, A. B. (2007). Fast learning rates for plug-in classifiers. The Annals of Statistics, 35(2):608–633.

- Ben-David et al., (2007) Ben-David, S., Blitzer, J., Crammer, K., and Pereira, F. (2007). Analysis of representations for domain adaptation. In Schölkopf, B., Platt, J. C., and Hoffman, T., editors, Advances in Neural Information Processing Systems, pages 137–144. MIT Press.

- Blitzer et al., (2008) Blitzer, J., Crammer, K., Kulesza, A., Pereira, F., and Wortman, J. (2008). Learning bounds for domain adaptation. In Platt, J. C., Koller, D., Singer, Y., and Roweis, S. T., editors, Advances in Neural Information Processing Systems, pages 129–136. Curran Associates, Inc.

- Cai and Wei, (2019) Cai, T. T. and Wei, H. (2019). Transfer learning for nonparametric classification: Minimax rate and adaptive classifier. The Annals of Statistics. To appear.

- Cannings et al., (2020) Cannings, T. I., Fan, Y., and Samworth, R. J. (2020). Classification with imperfect training labels. Biometrika, 107(2):311–330.

- Dua and Graff, (2017) Dua, D. and Graff, C. (2017). UCI machine learning repository.

- Gao et al., (2016) Gao, W., Wang, L., Li, Y.-F., and Zhou, Z.-H. (2016). Risk minimization in the presence of label noise. In AAAI, pages 1575–1581.

- Han et al., (2018) Han, D., Liu, Q., and Fan, W. (2018). A new image classification method using cnn transfer learning and web data augmentation. Expert Systems with Applications, 95:43–56.

- Hanneke and Kpotufe, (2019) Hanneke, S. and Kpotufe, S. (2019). On the value of target data in transfer learning. In Advances in Neural Information Processing Systems, pages 9871–9881.

- Hoffman et al., (2018) Hoffman, J., Mohri, M., and Zhang, N. (2018). Algorithms and theory for multiple-source adaptation. In Advances in Neural Information Processing Systems, pages 8246–8256.

- Huang et al., (2007) Huang, J., Gretton, A., Borgwardt, K., Schölkopf, B., and Smola, A. J. (2007). Correcting sample selection bias by unlabeled data. In Advances in Neural Information Processing Systems, pages 601–608.

- Hussain et al., (2018) Hussain, M., Bird, J. J., and Faria, D. R. (2018). A study on cnn transfer learning for image classification. In UK Workshop on Computational Intelligence, pages 191–202. Springer.

- Kim and Park, (2017) Kim, J. and Park, C. (2017). End-to-end ego lane estimation based on sequential transfer learning for self-driving cars. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition (CVPR) Workshops.

- Kpotufe and Martinet, (2018) Kpotufe, S. and Martinet, G. (2018). Marginal singularity, and the benefits of labels in covariate-shift. arXiv preprint arXiv:1803.01833.

- Mammen et al., (1999) Mammen, E., Tsybakov, A. B., et al. (1999). Smooth discrimination analysis. The Annals of Statistics, 27(6):1808–1829.

- Mansour et al., (2012) Mansour, Y., Mohri, M., and Rostamizadeh, A. (2012). Multiple source adaptation and the rényi divergence. arXiv preprint arXiv:1205.2628.

- Manwani and Sastry, (2013) Manwani, N. and Sastry, P. (2013). Noise tolerance under risk minimization. IEEE transactions on cybernetics, 43(3):1146–1151.

- Natarajan et al., (2017) Natarajan, N., Dhillon, I. S., Ravikumar, P., and Tewari, A. (2017). Cost-sensitive learning with noisy labels. The Journal of Machine Learning Research, 18(1):5666–5698.

- Natarajan et al., (2013) Natarajan, N., Dhillon, I. S., Ravikumar, P. K., and Tewari, A. (2013). Learning with noisy labels. In Advances in Neural Information Processing Systems, pages 1196–1204.

- Quinlan, (1987) Quinlan, J. R. (1987). Simplifying decision trees. International journal of man-machine studies, 27(3):221–234.

- Scott, (2019) Scott, C. (2019). A generalized neyman-pearson criterion for optimal domain adaptation. In Algorithmic Learning Theory, pages 738–761.

- Scott et al., (2013) Scott, C., Blanchard, G., and Handy, G. (2013). Classification with asymmetric label noise: Consistency and maximal denoising. In Conference On Learning Theory, pages 489–511.

- Shang and Cheng, (2017) Shang, Z. and Cheng, G. (2017). Computational limits of a distributed algorithm for smoothing spline. The Journal of Machine Learning Research, 18(1):3809–3845.

- Shimodaira, (2000) Shimodaira, H. (2000). Improving predictive inference under covariate shift by weighting the log-likelihood function. Journal of statistical planning and inference, 90(2):227–244.

- Sugiyama et al., (2008) Sugiyama, M., Nakajima, S., Kashima, H., Buenau, P. V., and Kawanabe, M. (2008). Direct importance estimation with model selection and its application to covariate shift adaptation. In Advances in Neural Information Processing Systems, pages 1433–1440.

- Weiss et al., (2016) Weiss, K., Khoshgoftaar, T. M., and Wang, D. (2016). A survey of transfer learning. Journal of Big data, 3(1):9.

- Zhang et al., (2012) Zhang, C., Zhang, L., and Ye, J. (2012). Generalization bounds for domain adaptation. In Advances in Neural Information Processing Systems, pages 3320–3328.

- Zhang et al., (2017) Zhang, Q., Wu, D., Lu, J., Liu, F., and Zhang, G. (2017). A cross-domain recommender system with consistent information transfer. Decision Support Systems, 104:49–63.

- Zhang et al., (2015) Zhang, Y., Duchi, J., and Wainwright, M. (2015). Divide and conquer kernel ridge regression: A distributed algorithm with minimax optimal rates. The Journal of Machine Learning Research, 16(1):3299–3340.

- Zhao et al., (2018) Zhao, H., Zhang, S., Wu, G., Moura, J. M., Costeira, J. P., and Gordon, G. J. (2018). Adversarial multiple source domain adaptation. In Advances in Neural Information Processing Systems, pages 8559–8570.

- Zhao et al., (2013) Zhao, L., Pan, S. J., Xiang, E. W., Zhong, E., Lu, Z., and Yang, Q. (2013). Active transfer learning for cross-system recommendation. In AAAI. Citeseer.

- Zhu et al., (2011) Zhu, Y., Chen, Y., Lu, Z., Pan, S. J., Xue, G.-R., Yu, Y., and Yang, Q. (2011). Heterogeneous transfer learning for image classification. In AAAI, volume 11, pages 1304–1309.