No-regret Learning in Price Competitions under Consumer Reference Effects

Negin Golrezaei \AFFSloan School of Management, Massachusetts Institute of Technology \EMAILgolrezaei@mit.edu, \AUTHORPatrick Jaillet \AFFDepartment of Electrical Engineering and Computer Science, Massachusetts Institute of Technology \EMAILjaillet@mit.edu, \AUTHORJason Cheuk Nam Liang \AFFOperations Research Center, Massachusetts Institute of Technology \EMAILjcnliang@mit.edu,

We study long-run market stability for repeated price competitions between two firms, where consumer demand depends on firms’ posted prices and consumers’ price expectations called reference prices. Consumers’ reference prices vary over time according to a memory-based dynamic, which is a weighted average of all historical prices. We focus on the setting where firms are not aware of demand functions and how reference prices are formed but have access to an oracle that provides a measure of consumers’ responsiveness to the current posted prices. We show that if the firms run no-regret algorithms, in particular, online mirror descent (OMD), with decreasing step sizes, the market stabilizes in the sense that firms’ prices and reference prices converge to a stable Nash Equilibrium (SNE). Interestingly, we also show that there exist constant step sizes under which the market stabilizes. We further characterize the rate of convergence to the SNE for both decreasing and constant OMD step sizes.

price competition, consumer reference effect, no-regret learning, convergence in games

1 Introduction

In markets with repeated consumer-seller interactions, consumers develop price expectations (or reference prices) based on past observed prices. Such price memories would influence consumers’ willingness-to-pay and hence their purchasing decisions, eventually impacting the overall aggregate market demand. Due to such memory dependent reference price effects, developing pricing strategies is challenging because firms may not necessarily know how consumers form and adjust price expectations. The complexity of pricing is further increased with competition, as competitors’ pricing decisions impact not only a firm’s immediate demand but also consumers’ reference prices. Such challenges in pricing under competition and reference price effects make market stability particularly attractive to firms: under stable markets, long-term organizational planning and business strategy development can be conducted more effectively (see Caves and Porter (1978)). Inspired by this, in this paper, we study the impact of consumer reference prices on the long-term stability of competitive markets.

We examine a simplified market scenario where two firms sequentially set prices to sell goods over an infinite time horizon, and demand of each firm’s goods are influenced by both firms’ current prices and the current consumers’ reference price, which is a weighted average of all past price trajectories. Also, the repeated price competitions occur in an opaque environment, where firms are not aware of any demand or reference price characteristics, and only have access to an oracle that returns consumers’ responsiveness to posted prices.111We consider a linear demand model, but firms are not aware of the functional form of the demand. In such a market scenario, we consider that both firms run a general online mirror descent (OMD) algorithm.222OMD algorithms are closely related to the regularized learning paradigm, which includes algorithms such as follow the regularized leader (FTRL), EXP3, Hedge, etc (see Hoi et al. (2018) for a comprehensive survey). Despite its simplicity, OMD algorithms have been theoretically shown to have good performance guaranties in both purely stochastic and adversarial environments (see Bubeck and Slivkins (2012), Zimmert and Seldin (2018), Zimmert et al. (2019)), and hence would be a plausible option for firms in this opaque environment of interest.

Our goal is to investigate whether firms’ prices and consumer reference prices eventually stabilize in the long-run if firms run OMD. The notion of stability that we consider is represented by the convergence of firms’ price profiles and reference prices such that there is no incentive for firms to deviate, eliminating the possibility for long-run price cycles and fluctuations. Similar notions of stability under dynamic competition has been studied under various equilibrium frameworks, and most relevant to this work are Markov perfect equilibrium and stationary equilibrium (see for example Hopenhayn (1992), Escobar (2007), Doraszelski and Satterthwaite (2010), Weintraub et al. (2011), Adlakha et al. (2015)). Nevertheless, these frameworks assume firms have complete information or optimize pricing decisions according to some prior on their competitors (or their aggregate) and the market. In contrast, our work focuses on competition in an opaque environment where firms post prices using no-regret learning algorithms like OMD. Here, we point out that our objective is not to present dynamic pricing polices that maximize firms’ cumulative revenue. Instead, we seek to shed light on whether simple pricing polices like OMD that do not require a large amount of information eventually achieve market stability. Our contributions are summarized as follows.

-

•

We characterize stability for dynamic competitive markets under consumers’ reference price effects by defining the notion of Stable Nash Equilibrium (SNE). We theoretically demonstrate its existence and shed light on its structural properties; see Theorem 3.1.

-

•

We transform the two-firm game with a dynamic state (reference price) that varies in time according to firms’ posted prices to a three-firm game without a state. The added virtual firm, which is referred to as nature, runs OMD with a constant step size (i.e. has a fast learning rate), and models how reference prices are affected by firms’ past pricing decisions.

-

•

We show that prices and reference prices converge to an SNE and achieve stable markets when the two (real) firms adopt decreasing step sizes that go to zero at a moderate rate; see Theorem 5.1 for details. We further show that with decreasing step sizes, the market stabilizes at a linear rate. We highlight that obtaining these convergence results is challenging because in our three-firm game, there is a firm (nature) who adopts a constant step size and learns at a fast rate. Our results show that despite the need to deal with such an inflexible virtual firm, the real firms can stabilize the market by adopting decreasing step sizes. In fact, the existence of the inflexible virtual firm in our game does not allow us to use the results in the literature on multi-agent online learning, where multiple interacting agents make sequential decisions via running the OMD algorithm to maximize individual rewards (see Mertikopoulos and Staudigl (2017), Bravo et al. (2018), Mertikopoulos and Zhou (2019)). More specifically, in the multi-agent online learning literature, agents in the system of interest typically use step sizes of the same order (i.e. homogeneously decreasing or constant). In contrast, in our setting, firms are unaware of reference price update dynamics, and may possibly take decreasing step sizes while nature’s step sizes remain constant.

-

•

Interestingly, we also show that there exist constant step sizes under which markets will converge to an SNE at much faster rates compared to adopting decreasing step sizes. Additionally, we show through an example that not every constant step size results in a stable market. Roughly speaking, if the firms’ constant step size is compatible with nature’s constant step size, the market stabilizes at a faster rate compared to decreasing step sizes; see Corollary 5.3.1 and Theorem 5.4 for details.

We refer the readers to Appendix 6 for an expanded literature review.

2 Preliminaries

Consumer Demand and Reference Price Update Dynamics.

We study a dynamic system where two firms simultaneously set prices in each period over an infinite time horizon to sell goods to consumers whose willingness-to-pay is affected by their price expectations, referred to as reference prices. We assume that the number of consumers is large so that demand for each firm is governed by the aggregate behavior of all consumers. Specifically, the demand of firm in time period with posted prices and consumers’ reference price is given by

| (1) |

where is the price of firm and is the price of the other firm. To simplify notation, we may denote with . We assume prices and reference prices are bounded, i.e., for , for some , and for any . The boundedness of prices corresponds to real-world price floors or price caps and is not unnatural. In Equation (1), and , where . Later in this section, we will provide an interpretation for these parameters that characterize our linear demand model. We note that linear demand models, which are widely used in the literature (see Huang et al. (2013) for a comprehensive survey), can be viewed as a first-order approximation to more complex models.

After firms post prices, reference prices update according to the following dynamics:

| (2) |

where and . Here, , which is independent of prices, represents how visible firm is to consumers: the larger the , the more visible firm is, and the more it influences consumers’ price expectations. The reference price update dynamics can be viewed as a memory-based process that characterizes how consumers adjust price expectations for goods over time as they observe new prices. Reference prices are formed by a weighted average of historical prices, where more recent prices are assigned larger weights. The specific exponential weighting scheme adopted in this paper has been motivated and empirically validated in the literature of behavioral economics (see, for example Winer (1986), Sorger (1988), Greenleaf (1995)). The parameter in the reference price update model characterizes to what extent consumers’ reference price depends on past prices: As increases, the reference prices depend less on recently observed prices. Empirical estimates of typically range from to (see Greenleaf (1995), Briesch et al. (1997)) depending on the type of goods sold.

We now provide an economic interpretation for our linear demand model by rearranging terms:

| (3) |

When the posted price is greater than the reference price, i.e., , the value can be viewed as the consumers’ perceived price surcharge w.r.t. the reference price, and when , the value is consumers’ perceived price discount. Observe that in this rearrangement, demand increases when consumers’ perceived price discount increases, and decreases as price surcharge increases, which is a conventional representation of how reference prices affect consumer decisions in the related literature, see, for example, Popescu and Wu (2007), Nasiry and Popescu (2011). Furthermore, the coefficients , and measure the demand sensitivity of firm to its own prices , its competitor’s prices , and price surcharge/discount respectively.333The dependency of demand on price surcharges and discounts are of the same order , which corresponds to so-called risk-neutral consumers. Related literature have also studied asymmetric demand dependencies on surcharges and discounts; see Popescu and Wu (2007), Nasiry and Popescu (2011), Hu et al. (2016). With these interpretations, parameter in the condition of can be viewed as a sensitivity margin that represents to what extent demand is more sensitive to a firm’s own prices relative to competitor’s prices and surcharge/discount. Take for example the case where : we have , which means the impact of firm ’s price on its demand is greater than the aggregate impact of its price on the competitor’s demand and the competitor’s price on firm ’s demand (see Equation (3)). Additionally, for , we have , which represents the fact that reference effects in the market due to surcharge/discounts are generally less influential than any firm’s price on its own demand.

We point out that the aforementioned relationships between model parameters lead to a diagonally dominant Jacobian matrix w.r.t. some mapping that characterizes the linear system consisting of firms and reference prices (particularly linearity in demand and reference price updates). We will provide further details on this particular mapping and its relevance with variational inequalities in Section 5.3.

Market Stability. In this work, our goal is to present simple pricing policies for the firms that stabilize the market even when firms do not have complete information on market conditions. Define as the single-period firm ’s revenue when prices are and the reference price is . We say the market is stable at point if the following two conditions hold:

-

1.

Best-response Conditions. for , we have for any in the feasible set ; that is, firm cannot increase its revenue by posting another price when the other firm posts a price of and the reference price is .

-

2.

Stability Condition. ; that is, the reference price does not change if the firm keeps posting price ; see Equation (2).

Throughout the paper, we may refer to a point that satisfies the aforementioned conditions as a Stable Nash Equilibrium (SNE).

Firms’ Information Structure.

We present pricing policies under a partial information setting.

In this setting, a firm does not know , , reference price update dynamics, and does not observe any of historical competing prices nor the current reference price. To be more specific, in this setting, firms do not know the specific form of the demand functions and reference update dynamics, which in our case are linear. Nevertheless, we assume that after firms post prices under reference price , they can access a first-order oracle that outputs , which intuitively represents consumers’ responsiveness to a firm’s prices under current market conditions.444We note that such information can be obtained by a slight perturbation of the posted price. Furthermore, the assumption of having access to the first-order oracle is very common in the literature; see, for example, a comprehensive introduction to convex optimization in Nesterov (2013). We note that the partial information setting models real-world opaque environments where firms do not possess information of the market or its competitors. In this setting, firms set prices simultaneously, so a firm does not observe its competitor’s pricing decision in the current period before setting its own price.

3 Existence and Structural Properties of SNE

In this section, we show that an SNE exists. Recall that for any SNE, each firm best responds to its competitor as well as consumers’ reference price with no incentive for unilateral deviation. Let , 555Here, the revenue function is quadratic, so is a singleton. be firm ’s best-response to the reference price and the price of the other firm . Further, for any reference price , define set as follows

| (4) |

As we will show in Theorem 3.1 below, is non-empty and when it is not a singleton, it is an ordered set with total ordering.666A set is an ordered set with total ordering if for any , either or where the relationship and between two vectors is component-wise. To show the existence of an SNE, we consider a simple pricing strategy that works as follows: in each period, firms set the largest best response profiles w.r.t. reference price , i.e., (because is an ordered set, is well-defined). We show that for any initial reference price , converges monotonically to an SNE. Of course, this pricing strategy is only possible under the complete information setting, where each firm knows its own demand function , its competitor’s demand function , and the current reference price. That is, the described pricing strategy cannot be implemented in our partial information setting. Nevertheless, the convergence under this policy confirms the existence of an SNE.

Theorem 3.1 (Existence of an SNE)

Let , defined in Equation (4), be the set of best-response profiles w.r.t. reference price . Then, for a fixed reference price , is non-empty, and when is not a singleton, it is an ordered set with total ordering. Furthermore, assume that in each period , firms set the largest best response prices w.r.t. reference price , i.e., . Then, for any initial reference price , converges monotonically to an SNE.

The proof of the first half of the result regarding the structural properties of the set of best response profiles is inspired by that of Tarski’s fixed point theorem (e.g., see Echenique et al. (2005)). The proof of the second half regarding the convergence of the pricing policy builds on that of Theorem 6 in Milgrom and Roberts (1990). (This theorem shows the monotonocity of pure-strategy Nash Equilibrium for paramtererized games.) Detailed proofs can be found in Appendix 7. Theorem 3.1 illustrates structural properties of SNEs: since is an ordered set with total ordering, if there are multiple SNE’s, any two SNE’s and must either satisfy or under component-wise comparisons.

Due to the decision set boundaries, there may exist multiple SNE’s. However, to simplify our analyses, in the rest of the paper we assume that there exists an SNE that lies within the interior of the action set . Under this assumption, Lemma 3.2 shows that the interior SNE is unique.

Assumption 1

There exists an SNE such that .

Lemma 3.2 (Uniqueness of SNE)

Under Assumption 1, there is a unique SNE .

4 No-regret Pricing Policies under Partial Information Setting

Recall that under partial information, firms are unaware of the consumer demand function (they do not know the demand function is linear), reference prices, and reference price update dynamics. Hence, a natural approach for firms to increase revenue is to employ so-called no-regret online learning algorithms that adjusts prices in a dynamic fashion. We study the regime in which firms adopt the general OMD algorithm. We start by the following standard definition.

Definition 4.1 (Strong convexity)

Let be a convex set. A function is said to be -strongly convex if for any , we have .

In the OMD algorithm, each firm chooses a continuously differentiable and strongly convex regularizer associated with strong-convexity parameter , a sequence of step sizes , and, for our convenience, minimizes the cost function (i.e. inverse of revenue) , which is convex in . Here, we assume each regularizer also satisfies a standard reciprocity condition used in optimization and online learning literature Chen and Teboulle (1993), Kiwiel (1997), Alvarez et al. (2004), i.e. whenever for we have where is the Bregman divergence w.r.t. .777The Bregman divergence associated with convex and continuously differentiable regularizer function and convex set is defined as . In OMD, each firm maintains a proxy variable over time, and in each period , conducts pricing according to the following three steps:

-

1.

Project the proxy variable back to the decision interval : , where is the projection operator such that .

-

2.

Access the first-order oracle defined by , where

(5) This oracle can be viewed as a feedback mechanism that outputs the payoff gradient evaluated at a given price profile and reference price . We note that the first-order feedback is very common in the optimization and learning literature as discussed in Section 2. Here, we point out that after a firm posts prices according to the OMD algorithm, it only obtains , and does not necessarily observe the prices of its competitor nor the reference price.888Firms do not know the linear form of demand, and hence cannot learn parameters and then best respond given parameter estimates.

- 3.

We summarize the two-firm OMD pricing scheme in Algorithm 1.

One can think of this sequential price competition with reference prices as a state-based dynamic game model where the reference price plays the role of an underlying state: each player (i.e., firm) has a continuous action space and payoff function that depends on all players’ actions as well as an underlying state variable that undergoes deterministic transitions. However, the view that we will adopt in the rest of the paper perceives reference prices as price decisions posted by a virtual firm which we refer to as nature and denote it by . This is possible if, for any (), we are able to construct a universal nature cost function , strongly convex regularizer , and step size sequence , such that when firms 1, 2 and nature independently run the OMD algorithm with their respective regularizers and step sizes (as summarized in Algorithm 2), the resulting price profiles recover the respective prices of Algorithm 1. Here, note that . The following Proposition 4.1 formalizes this view and shows that such , and indeed exist. The proof is provided in Appendix 8, and we will refer to the dynamic game characterized in Algorithm 2 as the induced 3-firm dynamic game.

Proposition 4.1 (Induced 3-firm dynamic game)

We note that the choices for nature’s cost function , regularizer and step sizes may not be unique, and in Proposition 4.1, we simply choose the most straightforward feasible candidate. Nonetheless, by this lemma, the nature takes constant step sizes , which implies that we have an inflexible (virtual) firm whose learning rate is always very fast.

By viewing reference prices as prices posted by nature, the induced 3-firm game is also associated with the static game that involves 3 players with respective payoffs and common action set . It turns out that the pure strategy Nash Equilibrium (PSNE) of this static game is unique and is identical to the SNE of Lemma 3.2:

Proposition 4.2 (PSNE of induced 3-firm static game)

5 Convergence Results

The key challenge in showing convergence for the induced 3-firm OMD game play in Algorithm 2 lies in the fact that the step size sequence for nature is the constant , unlike previously studied multi-agent learning settings where step size sequences are typically identical across agents (see for example Scutari et al. (2010), Nagurney and Zhang (2012), Bravo et al. (2018), Tampubolon and Boche (2019), Mertikopoulos and Zhou (2019)). This highlights the fundamental issue in our problem of interest: will convergence still occur if one of the players takes a constant (fixed) step size?

In Section 5.1, we show that prices and reference prices converge to the unique interior SNE when the two firms adopt decreasing step sizes and characterize the corresponding convergence rate. In Section 5.2, we show that there exist constant step sizes for the two firms with which prices convergence to the SNE at faster rates compared to decreasing step sizes.

5.1 Decreasing Step Sizes

The first key result in this section is the following theorem, which states that if the two firms run the OMD algorithm with decreasing step sizes that do not go to zero too fast, then convergence to the SNE is guarantied.

Theorem 5.1 (Convergence under Decreasing Step Sizes)

Suppose that Assumption 1 holds and firm adopts regularizer that is -strongly convex, constinuosly differentiable, and satisfies the reciprocity condition (see Section 4). Then, when the sequence is nonincreasing with , we have . Furthermore, if , and the sensitivity margin , then converges to the unique interior SNE .

The first part of Theorem 5.1 shows that prices stabilize when the firms’ step sizes go to zero eventually. This is an interesting result because in the induced 3-firm dynamic game presented in Algorithm 2, nature adopts a constant step size and learns quickly, while the two other firms are learning slowly through decreasing step sizes. However, firms’ prices may not necessarily converge, and even if they do, firms may have the incentive to deviate, leading to an volatile market.101010 An example is the extreme case where firms 1 and 2 adopt step sizes . This obviously guaranties convergence because prices are fixed at the initial prices, which are likely not the SNE, encouraging the firms to unilaterally deviate. The second part of the theorem addresses this concern and shows that when and , the market becomes stable as the prices converge to the SNE. In fact, these conditions admit a large range of step sizes, e.g. for . The proof is provided in Appendix 9. Here, we provide some examples to solidify the aforementioned ideas.

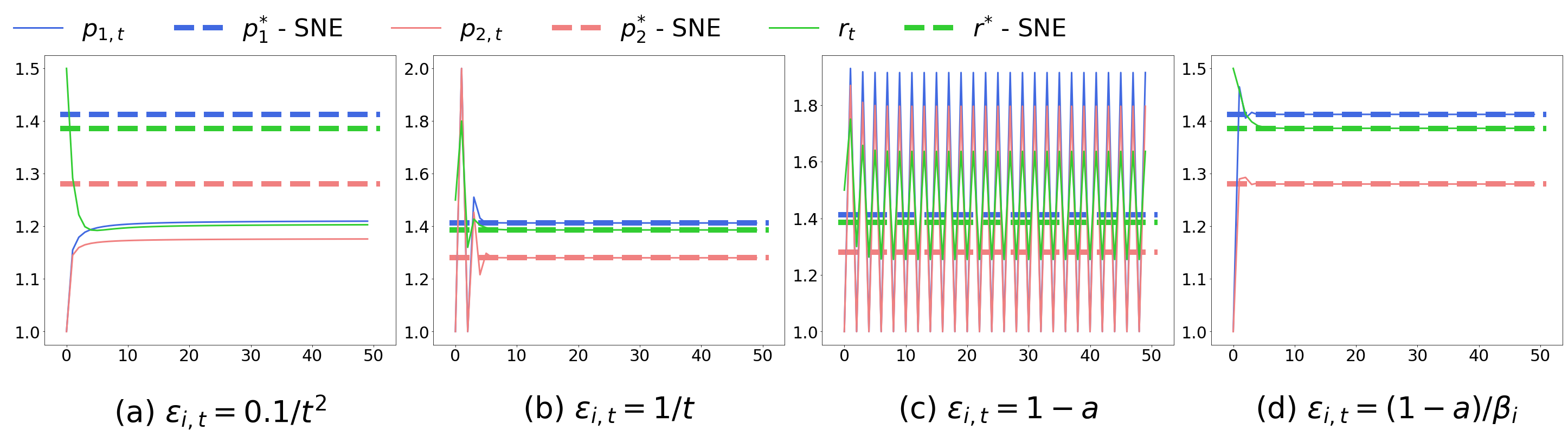

Example 1 (Decreasing Step Sizes)

Consider the following demand and reference update model parameters: , , , , , , , and initial prices . These parameters admit the unique SNE given by . We consider two different decreasing step size sequences when both firms use the quadratic regularizer, i.e. :

-

•

With , the price profile eventually converges to the point which is not the SNE (see Figure 1a) and firms are incentivized to deviate, e.g., the best response for firm 1 w.r.t. and is .111111Here, we choose because the gap between the convergence point and the SNE is more visible. For the more natural choice , we obtain similar results. Hence, under this step size sequence, firms may go through different epochs in the long run, in which firms converge in an epoch, and may decide to deviate and start over.

-

•

With , we have and . Thus, per Theorem 5.1, prices and reference prices converge to the unique SNE; see Figure 1b. Moreover, we observe that (i) convergence occurs very quickly (for ), and (ii) prices do not converge monotonically. The latter is in contrast with the pricing policy presented in Theorem 3.1.

In Example 1, we observe fast convergence to the SNE when firms choose decreasing step sizes. Inspired by this, we also characterize convergence rates for such step sizes:

Theorem 5.2 (Convergence Rate under Decreasing Step Sizes)

Assume Assumption 1 holds. For any sensitivity margin , if both firms adopt regularizer , there exists step sizes and an absolute constant , which depends on and , such that for any .

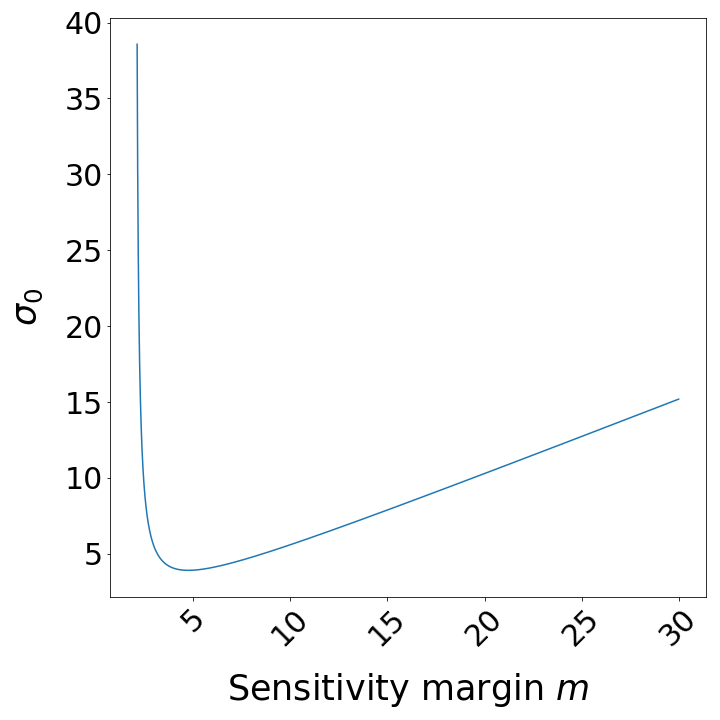

The proof of this theorem constructs a sufficiently large absolute constant and shows via induction. The main procedure involves bounding with and , and developing a tight bound for . Bounding helps us bound because the deviations of prices w.r.t. the interior SNE will cumulatively propagate into due to reference price update dynamics. The detailed proof is provided in Appendix 9. We also remark that the condition is a rather practical regime because this condition, as discussed in Section 2, implies a firm’s demand is more sensitive to its own prices compared to competitor’s prices and surcharge (or discounts) relative to reference prices. Finally, we remark that the constant scales reasonably w.r.t. and as long as they are bounded away from ; see Figure 2(b) in Appendix 9.7 for an illustration for and .

5.2 Constant Step Sizes

We start by revisiting Example 1 and adopt constant step sizes.

Example 2 (Constant Step Sizes)

Given this example, we present the first main result for this section in the following theorem (see proof in Appendix 9) which shows that under some conditions, there exists constant step size proportional to under which pricing profiles and reference price convergence to the unique interior SNE.

Theorem 5.3 (Sufficient Conditions for Convergence under Constant Step Sizes)

Suppose that firm adopts regularizer that is -strongly convex and continuously differentiable. For strong-convexity parameters and sensitivity margin , define the set , where

| (6) |

Then, under Assumption 1, if , the step size sequence ( for any guarantees converges to the unique interior SNE .

This theorem indicates that under some conditions on , and , there exist constant step sizes with which convergence to the unique interior SNE is guaranteed. The desired step size is proportional to . This, roughly speaking, implies that prices converge to the SNE if firms adjust prices at a pace similar to that of nature. Recall that can be considered as the step size of nature, and by demand model in Equation (1), is firm ’s price sensitivity parameter. The conditions on , and in Theorem 5.3 are, in fact, quite mild: the following Corollary 5.3.1 provides an example where for any , we can find sufficiently large that guaranties convergence to an SNE.

Corollary 5.3.1 (Convergence under Constant Step Sizes)

For any sensitivity margin , assume both firms adopt continuously differentiable regularizer that is -strongly convex where and . Then there exists constant dependent on and so if firm adopts step size , converges to the unique interior SNE.

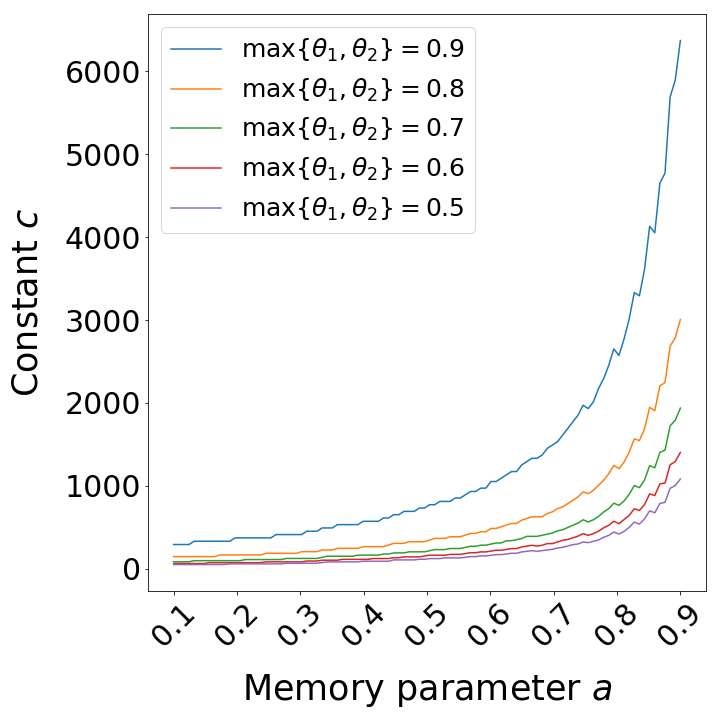

This corollary provides sufficient conditions for the existence of constant step sizes that guarantee convergence to the SNE for any sensitivity margin . In fact, for suitable , we can possibly find relatively small values of and such that the conditions are satisfied (e.g., for ). Note that for large , which means firms generally need to take larger strong-convexity parameters as increases. (See Figure 2(a) in Appendix 9.7 for illustration of as a function of .) Having everything else fixed, the larger , the slower price movements happens. 121212For example, taking in step 5 of Algorithm 1, we get , which implies the gap between and is small with large . This is so because for large , a firm’s demand is very sensitive to its own prices, encouraging the firm to adjust prices slowly via large .

Moreover, we also characterize the convergence rate when firms adopt suitable constant step sizes via the following Theorem 5.4, and highlight that such fast learning rates give us much faster convergence to the SNE, compared to slow learning rates from decreasing step sizes.

5.3 Comparison with Multi-agent Online Learning

In light of Proposition 4.2, we can characterize the 3-player game consisting of firms and nature with the mapping s.t. , where we slightly abuse the notation and write , and . Note that the corresponding Jacobian of is

which is not necessarily positive definite,131313Square matrix is positive definite if for any , . Note that does not need to be symmetric. despite being diagonally dominant141414A square matrix is diagonally dominant if . due to our assumptions on model parameters as illustrated in Section 2. Also note that is linear in , and Corollary 1.4 in Nagurney (2013) implies is monotone if and only if is positive definite. Hence, in our setting, the mapping may not be monotone, which prohibits us from naively applying arguments in the variational inequality (VI) framework to conclude convergence of the system as agents run OMD (see Scutari et al. (2010), Nagurney and Zhang (2012) for a detailed introduction on convergence to Nash Equilibrium under the VI framework).

Consequently, our proof techniques for Theorems 5.1,5.2, 5.3, and 5.4 are not standard since the aforementioned mapping does not necessarily satisfy monotonicity or other favorable properties that allow direct applications of the VI methodology. Even if we assume is monotonic, we still face technical issues that arise from heterogeneous step sizes, which provides another motivation to develop new techniques to show convergence as firms run general OMD algorithms. To briefly illustrate such challenges, assume is monotonic, meaning for , where the equality follows from Assumption 1 and first order conditions. If one can enforce for , showing the convergence results in this line of work boils down to verifying the following inequalities (e.g. see Bravo et al. (2018), Tampubolon and Boche (2019), Mertikopoulos and Zhou (2019)):

where can be viewed as some absolute constant, and is Bregman divergence w.r.t. strongly convex regularizer . At a high level, the above equations show that the distance between and becomes smaller over time and hence implies convergence to the SNE. The inequality (a) follows from classical mirror descent proofs; and inequality (b) utilizes the variational stability condition by choosing suitable (for example ). However, this procedure will not be applicable in our setting as nature is inflexible in the sense that it always takes the constant step size sequence , while the two firms are unaware of how nature updates, and may independently use different step sizes (e.g. decreasing step sizes).

References

- Adida and Perakis (2010) Adida E, Perakis G (2010) Dynamic pricing and inventory control: Uncertainty and competition. Operations Research 58(2):289–302.

- Adlakha et al. (2015) Adlakha S, Johari R, Weintraub GY (2015) Equilibria of dynamic games with many players: Existence, approximation, and market structure. Journal of Economic Theory 156:269–316.

- Ahn et al. (2007) Ahn Hs, Gümüş M, Kaminsky P (2007) Pricing and manufacturing decisions when demand is a function of prices in multiple periods. Operations Research 55(6):1039–1057.

- Aksoy-Pierson et al. (2013) Aksoy-Pierson M, Allon G, Federgruen A (2013) Price competition under mixed multinomial logit demand functions. Management Science 59(8):1817–1835.

- Alvarez et al. (2004) Alvarez F, Bolte J, Brahic O (2004) Hessian riemannian gradient flows in convex programming. SIAM journal on control and optimization 43(2):477–501.

- Balseiro and Gur (2019) Balseiro SR, Gur Y (2019) Learning in repeated auctions with budgets: Regret minimization and equilibrium. Management Science 65(9):3952–3968.

- Baron et al. (2019) Baron O, Deng C, He S, Yuan H (2019) Data driven forecasting and revenue management with exposure dependent reference prices. Available at SSRN 3388941 .

- Bernstein and Federgruen (2004) Bernstein F, Federgruen A (2004) A general equilibrium model for industries with price and service competition. Operations research 52(6):868–886.

- Boyd et al. (2004) Boyd S, Boyd SP, Vandenberghe L (2004) Convex optimization (Cambridge university press).

- Bravo et al. (2018) Bravo M, Leslie D, Mertikopoulos P (2018) Bandit learning in concave n-person games. Advances in Neural Information Processing Systems, 5661–5671.

- Briesch et al. (1997) Briesch RA, Krishnamurthi L, Mazumdar T, Raj SP (1997) A comparative analysis of reference price models. Journal of Consumer Research 24(2):202–214.

- Bubeck (2011) Bubeck S (2011) Introduction to online optimization. Lecture Notes 2.

- Bubeck and Slivkins (2012) Bubeck S, Slivkins A (2012) The best of both worlds: Stochastic and adversarial bandits. Conference on Learning Theory, 42–1.

- Caves and Porter (1978) Caves RE, Porter ME (1978) Market structure, oligopoly, and stability of market shares. The Journal of Industrial Economics 289–313.

- Chen and Teboulle (1993) Chen G, Teboulle M (1993) Convergence analysis of a proximal-like minimization algorithm using bregman functions. SIAM Journal on Optimization 3(3):538–543.

- Coulter and Krishnamoorthy (2014) Coulter B, Krishnamoorthy S (2014) Pricing strategies with reference effects in competitive industries. International transactions in operational Research 21(2):263–274.

- den Boer and Keskin (2019) den Boer A, Keskin NB (2019) Dynamic pricing with demand learning and reference effects. Available at SSRN 3092745 .

- Doraszelski and Satterthwaite (2010) Doraszelski U, Satterthwaite M (2010) Computable markov-perfect industry dynamics. The RAND Journal of Economics 41(2):215–243.

- Echenique et al. (2005) Echenique F, et al. (2005) A short and constructive proof of tarski’s fixed-point theorem. International Journal of Game Theory 33(2):215–218.

- Escobar (2007) Escobar JF (2007) Existence of pure and behavior strategy stationary markov equilibrium in dynamic stochastic games. Available at SSRN 936745 .

- Federgruen and Lu (2016) Federgruen A, Lu L (2016) Price competition based on relative prices. Columbia Business School Research Paper .

- Fibich et al. (2003) Fibich G, Gavious A, Lowengart O (2003) Explicit solutions of optimization models and differential games with nonsmooth (asymmetric) reference-price effects. Operations Research 51(5):721–734.

- Gallego and Hu (2014) Gallego G, Hu M (2014) Dynamic pricing of perishable assets under competition. Management Science 60(5):1241–1259.

- Gallego et al. (2006) Gallego G, Huh WT, Kang W, Phillips R (2006) Price competition with the attraction demand model: Existence of unique equilibrium and its stability. Manufacturing & Service Operations Management 8(4):359–375.

- Greenleaf (1995) Greenleaf EA (1995) The impact of reference price effects on the profitability of price promotions. Marketing science 14(1):82–104.

- Hoi et al. (2018) Hoi SC, Sahoo D, Lu J, Zhao P (2018) Online learning: A comprehensive survey. arXiv preprint arXiv:1802.02871 .

- Hopenhayn (1992) Hopenhayn HA (1992) Entry, exit, and firm dynamics in long run equilibrium. Econometrica: Journal of the Econometric Society 1127–1150.

- Hu et al. (2016) Hu Z, Chen X, Hu P (2016) Dynamic pricing with gain-seeking reference price effects. Operations Research 64(1):150–157.

- Huang et al. (2013) Huang J, Leng M, Parlar M (2013) Demand functions in decision modeling: A comprehensive survey and research directions. Decision Sciences 44(3):557–609.

- Kalyanaram and Winer (1995) Kalyanaram G, Winer RS (1995) Empirical generalizations from reference price research. Marketing science 14(3_supplement):G161–G169.

- Kiwiel (1997) Kiwiel KC (1997) Free-steering relaxation methods for problems with strictly convex costs and linear constraints. Mathematics of Operations Research 22(2):326–349.

- Kopalle et al. (1996) Kopalle PK, Rao AG, Assuncao JL (1996) Asymmetric reference price effects and dynamic pricing policies. Marketing Science 15(1):60–85.

- Levin et al. (2009) Levin Y, McGill J, Nediak M (2009) Dynamic pricing in the presence of strategic consumers and oligopolistic competition. Management science 55(1):32–46.

- Mertikopoulos and Staudigl (2017) Mertikopoulos P, Staudigl M (2017) Convergence to nash equilibrium in continuous games with noisy first-order feedback. 2017 IEEE 56th Annual Conference on Decision and Control (CDC), 5609–5614 (IEEE).

- Mertikopoulos and Zhou (2019) Mertikopoulos P, Zhou Z (2019) Learning in games with continuous action sets and unknown payoff functions. Mathematical Programming 173(1-2):465–507.

- Milgrom and Roberts (1990) Milgrom P, Roberts J (1990) Rationalizability, learning, and equilibrium in games with strategic complementarities. Econometrica: Journal of the Econometric Society 1255–1277.

- Nagurney (2013) Nagurney A (2013) Network economics: A variational inequality approach, volume 10 (Springer Science & Business Media).

- Nagurney and Zhang (2012) Nagurney A, Zhang D (2012) Projected dynamical systems and variational inequalities with applications, volume 2 (Springer Science & Business Media).

- Nasiry and Popescu (2011) Nasiry J, Popescu I (2011) Dynamic pricing with loss-averse consumers and peak-end anchoring. Operations research 59(6):1361–1368.

- Nedic and Ozdaglar (2009) Nedic A, Ozdaglar A (2009) Distributed subgradient methods for multi-agent optimization. IEEE Transactions on Automatic Control 54(1):48–61.

- Nesterov (2013) Nesterov Y (2013) Introductory lectures on convex optimization: A basic course, volume 87 (Springer Science & Business Media).

- Popescu and Wu (2007) Popescu I, Wu Y (2007) Dynamic pricing strategies with reference effects. Operations research 55(3):413–429.

- Rosen (1965) Rosen JB (1965) Existence and uniqueness of equilibrium points for concave n-person games. Econometrica: Journal of the Econometric Society 520–534.

- Scutari et al. (2010) Scutari G, Palomar DP, Facchinei F, Pang JS (2010) Convex optimization, game theory, and variational inequality theory. IEEE Signal Processing Magazine 27(3):35–49.

- Sorger (1988) Sorger G (1988) Reference price formation and optimal marketing strategies. Optimal control theory and economic analysis 3(3):97–120.

- Tampubolon and Boche (2019) Tampubolon E, Boche H (2019) Pricing mechanism for resource sustainability in competitive online learning multi-agent systems. arXiv preprint arXiv:1910.09314 .

- Tversky and Kahneman (1979) Tversky A, Kahneman D (1979) Prospect theory: An analysis of decision under risk. Econometrica 47(2):263–291.

- Tversky and Kahneman (1992) Tversky A, Kahneman D (1992) Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and uncertainty 5(4):297–323.

- Weintraub et al. (2011) Weintraub GY, Benkard CL, Van Roy B (2011) Industry dynamics: Foundations for models with an infinite number of firms. Journal of Economic Theory 146(5):1965–1994.

- Winer (1986) Winer RS (1986) A reference price model of brand choice for frequently purchased products. Journal of consumer research 13(2):250–256.

- Zimmert et al. (2019) Zimmert J, Luo H, Wei CY (2019) Beating stochastic and adversarial semi-bandits optimally and simultaneously. arXiv preprint arXiv:1901.08779 .

- Zimmert and Seldin (2018) Zimmert J, Seldin Y (2018) An optimal algorithm for stochastic and adversarial bandits. arXiv preprint arXiv:1807.07623 .

Appendices for

No-regret Learning in Price Competitions under Consumer Reference Effects

6 Expanded Literature Review

Reference Price Effects and Monopolist Pricing. Consumer reference effects have been validated empirically in many works including Tversky and Kahneman (1979, 1992), Kalyanaram and Winer (1995), Baron et al. (2019). This motivated a wide range of research including Kopalle et al. (1996), Fibich et al. (2003), Popescu and Wu (2007), Ahn et al. (2007), Nasiry and Popescu (2011) that studies optimal dynamic monopolistic pricing under different demand and reference price update models, where the single firm has complete information on consumer demand as well as how reference prices update. There are also very recent works that address the dynamic pricing problem with consumer reference effects under uncertain demand. Baron et al. (2019) utilizes real retail data and concludes the inclusion of exposure effects to sales or number of consumers151515Exposure effects in reference price formation refer to considering reference prices as a weighted average of all historical prices, where weights depend on factors such as sales or number of consumers. when considering reference price formations leads to more accurate forecasts in demand, and proposes a pricing policy using dynamic programming. den Boer and Keskin (2019) couples the problem of monopolistic dynamic pricing with reference effects and online demand learning. In our work, similar to Baron et al. (2019), den Boer and Keskin (2019), firms do not know the demand functions and how the reference prices are formed. But, while in Baron et al. (2019), den Boer and Keskin (2019), the form of demand model is known to the firm (monopolist) that aims to estimate model parameters, our work assumes competition between firms that do not know the form of demand and hence run OMD algorithms to increase revenue. Additionally, the algorithms proposed in Baron et al. (2019) and den Boer and Keskin (2019) aim to increase revenue from the firm’s perspective, while our work focuses on analyzing market stability for long-run competitions under reference effects.

Pricing in Competitive Markets without Reference Effects. A large stream of work studies static price competitions and characterizes structural properties of corresponding equilibria (for example, see Bernstein and Federgruen (2004), Gallego et al. (2006), Aksoy-Pierson et al. (2013)). Other works such as Adida and Perakis (2010), Levin et al. (2009), Gallego and Hu (2014) study oligopolistic dynamic pricing under various inventory, market, or product characteristics. Nevertheless, these two lines of works are oblivious to consumer reference effects. In this work, we jointly tackle the dynamic pricing problems in competitive markets with reference price effects when the firms lack the knowledge of demand functions and reference price dynamics.

Pricing in Competitive Markets with Reference Effects. Similar to our work, the works of Coulter and Krishnamoorthy (2014) and Federgruen and Lu (2016) also consider price competitions under reference effects. Coulter and Krishnamoorthy (2014) considers a similar linear demand model and an identical reference price update dynamic, but the work only provides theoretical analysis on the two-firm, two-period price competition setting, for which they characterize the unique sub-game perfect Nash Equilibrium. On the other hand, Federgruen and Lu (2016) studies multiple-firm single-period price competition equipped with different reference price effects in consumers’ demand (e.g. the reference price is specified by the lowest posted price). Additionally, both of these works study the complete information setting. In contrast to these two papers, our work studies price competitions over an infinite time horizon where reference prices adjust over time, and provides theoretical guarantees for the convergence of pricing strategies under the partial information setting. Finally, our work is the first study that provides theoretical analyses on long-term market stability of repeated price competitions in the presence of consumer reference effects.

Convergence in Games with Descent Methods. In addition to Mertikopoulos and Staudigl (2017), Bravo et al. (2018), Mertikopoulos and Zhou (2019) that we discussed in Section 1, here we also review related literature that study convergence in games where multiple agents adopt descent methods. Rosen (1965) studies finding a Nash Equilibrium of concave games via having each agent run projected gradient descent under complete information, i.e., agents know each others’ payoff functions and decision constraints. Nedic and Ozdaglar (2009) studies a distributed network optimization problem to optimize a sum of convex objective functions corresponding to multiple agents. Our paper distinguishes itself from this line of work from two aspects: unlike the two aforementioned works, (i) our model involves a varying underlying state (i.e., reference prices) dependent on all agents’ historical decisions, and can be modeled as a sequence of decisions made by an inflexible virtual agent that adopts descent methods with a constant step size; (ii) the agents (i.e., firms) in our model do not have any information on one another’s revenue function or how reference prices update. Finally, Balseiro and Gur (2019) considers multiple budget-constrained bidders participating in repeated second price auctions by adopting so-called adaptive pacing strategies, which is equivalent to the subgradient descent method. In their setting, the subgradient for each bidder’s objective is a function of all bidders’ decisions as well as its budget rate (i.e. total fixed budget divided by a given time horizon), which can be thought of as an underlying model state that remains constant over time.161616Note to run OMD algorithms in Balseiro and Gur (2019), agents need to know the length of the time horizon. Such knowledge is not required in our setting. In contrast, in our setting, the gradient oracle each firm receives is not only a function of all firms’ decisions, but also of the reference price which varies over time according to firms’ past decisions, making our analysis more challenging.

7 Appendix for Section 3

Additional Definitions.

We define the best-response mapping as such that . Then, we can rewrite the set of best-response profiles w.r.t. reference price , defined in Equation (4), as . Note that for any SNE , we must have , and is a fixed point of the mapping .

7.1 Proof of Theorem 3.1

(i) By first order conditions, we know that

Hence, due to boundary constraints on the decision set and the revenue function being quadratic, we have

where is the projection operator such that . Hence, is a nondecreasing function in and , which further implies is nondecreasing in and . Again, recall for any , the relationships and are component-wise comparisons.

We now follow a similar proof to that of Tarski’s fixed point theorem: consider the set . It is apparent that this set is nonempty because . Fix any . Then, we have which further implies since is nondecreasing in . Hence . By taking (this is possible since all are bounded), we have so . This further implies because is the least upper bound of , and thus . This allows us to conclude and hence , which means is a fixed point of the mapping . Thus, belongs in the set of best-response profiles , confirming is not empty.

Next, we show that is an ordered set with total ordering if it is not a singleton. To do so, consider any and without loss of generality assume . Since and , by monotonicity of we have . Thus, and is an ordered set with total ordering.

(ii) In the proof of (i), we showed that is a fixed point of the best-response mapping for any which allows us to conclude is the largest best-response profile, i.e., , and hence . Furthermore, since is increasing in , we know that is also an increasing function. In the following, we will argue that the reference prices is monotonically increasing or decreasing, which implies is also monotonic, and hence converges since prices and reference prices are bounded.

We write . At , if , then the reference price at satisfies the following equation

By the monotonicity of , we have for . Thus,

A simple induction argument thus shows is a nondecreasing sequence. Since for any , we know that converges to some number when . Furthermore, we observe that by the definition of . Also, from (i) we have and because is a fixed point of for any . Hence, , which implies converges to . Note that convergence is monotonic because is nondecreasing. Therefore,

which implies is an SNE. We can thus conclude that if , firms’ prices and reference prices converge monotonically to an SNE .

Following a symmetric argument, if , we can show that is a nonincreasing sequence. Since for any , we know that converges to some number . Similar to the previous arguments, we can conclude that prices and reference prices converge monotonically to an SNE .

7.2 Proof of Lemma 3.2

Let be an interior SNE, whose existence is guarantied by Assumption 1. Since revenue functions are quadratic, first order conditions at the interior best-response profiles should hold, which means the derivative of revenue functions at the interior best-responses and should be 0:

which leads to the relationship . Solving for the best-response equations, we get

| (7) |

Finally, the definition of an SNE guaranties . Thus, solving for , we obtain the unique solution

| (8) |

This implies that under Assumption 1, the interior SNE is unique. We remark that for any , because and we have . Hence, .

8 Appendix for Section 4

8.1 Proof of Proposition 4.1

First of all, it is easy to see prices at the first period are identical between Algorithm 1 and 2: for and . We now use induction to show price trajectories of the two algorithms are identical via considering the induction hypothesis that prices and reference prices are the same up to period .

Note that implies . Then, the proxy variable update step for nature is

Since the projection step for nature is trivial, which means . Furthermore, it is not difficult to see that prices and are identical between the two algorithms under the induction hypothesis. This implies that Algorithm 2 indeed recovers the prices and reference prices produced by Algorithm 1.

8.2 Proof of Proposition 4.2

Directly considering first order conditions for the cost functions , we have the system of equations

Solving these equations results in a unique solution that is identical to that in Equation (LABEL:eq:SNE), which is the unique interior SNE according to Lemma 3.2. Since the SNE is an interior point of , it is the unique PSNE of the induced static 3-firm game.

9 Appendix for Section 5

9.1 Additional Definitions

Definition 9.1 (Bregman Divergence)

The Bregman divergence associated with convex set , and convex and continuously differentiable function is defined as

where the inequality follows from convexity of . Furthermore, if is -strongly convex, then .

Note that is the Bregman divergence associated with regularizer used by firm , and is Bregman divergence associated with regularizer used by nature.

Definition 9.2

Let be the partial derivative of the cost function w.r.t. evaluated at the interior SNE , i.e. for

9.2 Proof for Theorem 5.1

The proof of this theorem is divided into two parts. In the first part, we show that the price profiles converge as under the condition , . In the second part, under the additional conditions and , we show that the price profiles converge to the unique interior SNE.

First part: Convergence of prices and reference prices.

Recall that , and and are both bounded. Hence, because for , and is nonincreasing, we have for any small there exist such that for all . Our goal is to show that for , is small.

For ,

| (9) |

To see why inequality (a) holds recall that is the proxy variable in Step 5 of Algorithm 1 such that . Hence,

which implies that , as desired. Here, the first inequality holds because:

where (a) follows from summing up and due to strong convexity.

By Equation (9), for ,

| (10) |

where the equality holds because under the event , no projection occurs and hence, . In the first of the proof, we bound the first two terms in the right hand side, i.e., and .

To bound , similar to Equation (9) we use for which implies . Thus,

| (11) |

where (a) holds because for any . On the other hand, under the event , projection occurs and therefore we have .

Using a similar argument as above to bound , we have under the event .

Second part: Convergence to the SNE.

The proof of this part is inspired by the proof of Theorem 4.6 in Mertikopoulos and Zhou (2019). However, in that proof, they rely on the Nash Equilibria of the game being variationally stable, or more strictly speaking, the gradient of the virtual 3-player game (consisting of firms and nature) s.t. to be a monotone mapping. In this proof, we do not rely on such structural assumption for the virtual 3-player game (see discussion in Section 5.3).

The proof of this theorem is split into two steps. First, we show that for any , the price profile must enter an -neigborhood of the SNE prices infinitely many times. In the second step, we show that when enters the -neigborhood with small enough step sizes, it must remain their forever.

Before we begin, we first introduce a lemma that would be used in both steps:

Lemma 9.1

Assume for any , for as described in Section 2. Consider the 2-by-2 matrix

| (17) |

Then, for any , . Furthermore, for any , define an -neighborhood around where is the Bregman divergence w.r.t. . Assuming the regularizers satisfy the reciprocity condition, i.e. whenever for we have , there exists some absolute constant such that

| (18) |

Proof.

Since, for , the sum of the first row of . Similarly, the sum of the second row of is also strictly greater than 0, and hence is a symmetric strict diagonally dominant matrix, and hence positive definite.171717A symmetric square matrix has real eigenvalues, and a diagonally dominant square matrix has eigenvalues whose real parts are positive. Hence has positive eigenvalues, and is thus positive definite. Therefore, for any and , we have . Since , this implies our desired result

We now show Equation (18). The reciprocity condition implies there exists some such that when , it holds that . Hence, for any , it must be the case that . So, for , we have

where is the minimum eigenvalue of the matrix (which is positive due to the fact that is positive definite). ∎

Now, returning to the proof for Theorem 5.1.

Step 1: show must enter an -neigborhood of the SNE prices infinitely many times. We use a contradiction argument. Fix any and let be the absolute constant defined in Lemma 9.1. Assume by contradiction that only visits finitely many times, i.e. there exists some s.t. for all . Further, in the first part of this theorem we showed that , so without loss of generality (by taking large enough), we can also assume for some small such that (where ), we have for all .

We start by deducing a recurrence relationship between and as followed:

| (19) |

where in (a) we directly evoked Corollary 10.1.1; and in (b) we used the fact that according to the definition of the SNE, and for . Summing the above over and recalling we have

| (20) |

where in (a) we take some finite for all by recalling Equation (5) which states , and that are bounded within for all ; in (b) we applied Lemma 9.1 since for all .

Telescoping Equation (LABEL:eq:OMD:standardAnalysis1) from some large time period down to we get

| (21) |

Rearranging terms in Equation (9.2) and dividing both sides by we get the following:

Since and are finite, the condition implies that , and the condition implies that . Hence, as . Finally, because due to our definition of , as , the above left hand side goes to zero and the right hand side goes to . This is a contradiction, implying that must enter an infinitely many times.

Step 2: show when enters an -neigborhood of the SNE prices for large (small step size), it must stay in the neighborhood. Here, we will show that for any , if for some large , then for all . In fact, we only need to show that implies for large , and the rest follows from an induction argument.

Consider two scenarios, namely and .

Scenario 1: If , consider some such that when , we have for some small that satisfies . Following the same deduction as in Equation (LABEL:eq:OMD:standardAnalysis1), we have

| (22) |

In (a) we used Lemma 9.1 such that , and the fact that so by definition of an -neighborhood (see Lemma 9.1) . In (b), we considered large such that and used the definition of such that .

Scenario 2: If , let be defined as in Lemma 9.1. Consider some such that when , we have for some small that satisfies . Following the same deduction as in Equation (LABEL:eq:OMD:standardAnalysis1), we have

where the final inequality follows from . Taking large such that we get .

Combining the above two scenarios, we showed that for any such that and , implies and hence for all large enough (by induction).

9.3 Proof of Theorem 5.2

Following the same deduction in Equation (LABEL:eq:OMD:standardAnalysis0) we have

where in (a) we used the basic inequality for and .

Now, consider the step-size sequences that satisfy

| (23) |

Equation (23) holds due to the fact that and , which further implies . This leads to

where in (a) we take some for all by using the fact that . Summing across , we have

where in inequality (a) we applied for , and .

When , we have . Therefore, denoting for and , the equation above yields

| (24) |

We will show via induction that for some and any . The proof is constructive and will rely on the following definitions, whose motivations will later be clear.

Fix , , and take any such that . Here, for any . Note that is bounded as is bounded away from 1.

Next, define

| (25) | |||

| (26) |

Note that is bounded because is bounded away from one. Further, since and are constant, and , it is easy to see that exists. Furthermore, define

Note that must exist because the left hand side is quadratic in , while the right hand side is exponential in for . We provide an illustration for the size of w.r.t. memory parameter and in Figure 2(b) of Appendix 9.7.

Note that the definition of and implies that the following three equations hold

| (27) | |||

| (28) | |||

| (29) |

Here, Equation (27) is due to the following: plugging the definition of into that of we get , and since for any , we have

where (a) follows from the definition of . Equation (28) directly follows from the definition of . Equation (29) follows because and hence . Hence, this implies that for any , where we recall .

Consider . We will now show via induction that using our induction hypothesis that holds for all . Note that the base case for any is trivially true as we just discussed. Then, multiplying on both sides of the recurrence relation in Equation (24) and telescoping from to , we have

| (30) |

We will now bound for all . Using the definition , we get

By convexity, we further have for any ,

where (a) follows from the induction hypothesis, i.e., holds for all . Using a telescoping argument, we then have for any ,

Here, (a) follows from the definition of in Equation (26); (b) follows from Equation (27); and (c) follows from Lemma 10.3 since . Applying this upper bound on in Equation (9.3) we have

where (a) follows from since . Dividing both sides of the above equation by , and using the fact that for any , we have

Here, (a) follows from the fact that , so ; (b) follows from so that according to Equation (25); finally, (c) follows from Equation (28).

9.4 Proof of Theorem 5.3

Here, we first provide a roadmap for the proof. Evoking Corollary 10.1.1, we get

| (31) |

By bounding the first order term and the second order term , we achieve a recursive relation in the form of

where we recall the definition for as in the proof of Theorem 5.2, and is some constant that takes negative values if the conditions in the theorem’s statement are satisfied. We then argue if does not converge to the SNE, will be greater than some positive constant for all large enough . Combining this with the above recursive relationship, this further implies that the distance between the price profile and the SNE decreases by a positive constant for each period. This will eventually contradict the fact that Bregman divergence is positive.

We start our proof by recalling Equation (5) which states . Hence,

Furthermore, for , we have

| (32) |

where we used for , , and . Hence, we have

| (33) |

In the inequality (a), we used the basic inequality twice, and the last inequality is obtained by invoking Equation (32). Furthermore, we have . Thus,

where (a) follows from and convexity. By applying the above inequality in Equation (31) with , we have

| (34) |

where in the second inequality, we again use the inequality .

Summing up Equations (9.4) (over ) and (9.4), and collecting terms yields

| (35) |

where the coefficient for is

| (36) |

Now, for , consider taking step size , for some constant that will be determined later, and denote the corresponding as (we drop the dependence on time as step sizes are constant), where for ,

| (37) |

Here, in (a) we substitute for ; in (b) we use the fact that (wich implies ) and .

We follow a similar argument as above and obtain

| (38) |

where in (a) we substitute for ; in (b) we used the fact that and for any .

Now, recall the definition . Then, if we have , taking any yields for . Hence, Equation (35) now becomes

| (39) |

Therefore, we know that

| (40) |

Furthermore, by strong convexity,

Hence, for any small , if there exists some such that , then by Equation (40), for all , which further implies for all . Hence .

Thus, it remains to show that for any small , there exists such that . We will prove this by contradiction. If this is not the case, there exists , and for all . Define for any , and slightly abuse the notation to define as the Bregman divergence with respect to . In the rest of this proof for simplicity we also write and . A simple analysis shows .

Since is continuously differentiable (by definition of Bregman divergence), is also continuously differentiable, and hence it is easy to see for any there exists such that

Since we assumed for all , the above implies for all . Hence following Equation (39),

where (a) follows because for and for all ; (b) follows from a telescoping argument. Finally, implies the right hand side in the above inequality goes to negative infinity as goes to infinity. This implies that , which contradicts nonnegativity of Bregman divergence. Hence, for any small , there exists such that , concluding the proof.

9.5 Proof of Corollary 5.3.1

When , Equation (6) becomes

Since in this case the function and are identical, we only consider . Note that the function has two distinct zero roots if and only if its discriminant is strictly greater than 0, i.e., which is equivalent to . Therefore, when has two distinct zero roots, the smaller one is given by

| (41) |

Similarly, the discriminant of (i.e., ) is always positive, so always has two zero roots. The larger one is given by

| (42) |

For any , the two roots of are both positive, while always has one positive root and one negative root. Hence, using a simple geometric argument regarding two quadratic functions, it is easy to see that if , any satisfies .

Now, consider . Since we observe is decreasing in and is increasing in , we have is increasing in . By direct calculations, we see that when , (i.e., ). Therefore because is increasing in , we conclude for any

which implies for any .

In sum, we conclude for any , if , there exists that depends on and such that for , and by Theorem 5.3, this implies that there exist constant step sizes under which prices and reference prices converge to the unique interior SNE.

9.6 Proof of Theorem 5.4

When for , we have , and Equation (6) becomes

We define for and , i.e.

| (43) |

Note that for any , if and only if . Hence, according to Corollary 5.3.1, we know that when and , for any (defined in Equations (9.5) and (42)) we have for , which implies for . Furthermore, via a simple geometric argument, the quadratic functions (with two positive zero roots) and (with two zero roots, one positive and one negative) have a unique intersection point . Define . Furthermore, since , we have

Now, note that when , . Also recall , so . Hence, , where we define and as in the proof of Theorem 5.3. Hence, by taking , and continuing from Equation (39), we get

Here, (a) follows from upper bounding with for any and in Equations (9.4) and (9.4) within the proof of Theorem 5.3; (b) follows from the definition of in Equation (43); (c) follows from the definition of for and .

Using a telescoping argument, we have

where the final inequality follows from since . Finally, because and , we have

9.7 Supplementary Figures for Section 5

10 Supplementary Lemmas of Section 5

Lemma 10.1

For and any , we have for any ,

| (44) |

Proof.

In the projection step of Algorithm 1, we have . Since we are working with one-dimensional decision sets, it is easy to see that due to convexity of . Recalling the definition , we have

Here (a) follows from the proxy update step in Algorithm 1. Now, evoking Lemma 10.2 (ii) by taking , , , , we have

It then follows that

where (a) follows from strong convexity of . ∎

Corollary 10.1.1

Under Assumption 1, let be the unique interior SNE as illustrated in Lemma 3.2, then for ,

| (45) |

and for any

| (46) |

Proof.

Similar to the proof of Lemma 3.2 and Proposition 4.2, the SNE must satisfy first order conditions w.r.t. quadratic cost function , respectively, due to the fact that it lies in the interior of the decision set. So for .

Furthermore, Evoking Lemma 10.1 by replacing with and combining yields the second part of the proof. ∎

Lemma 10.2 (Lemma 3.1 and 3.2 of Chen and Teboulle (1993))

Let be the Bregman divergence associated with convex function on the convex set : Then,

-

(i)

For any , .

-

(ii)

Let be any convex function and . If , then for any , we have

The proofs for the above lemma are very standard and we will omit them in this paper.

Lemma 10.3

Let , , and . Then, for any , we have

Proof of Lemma 10.3.

We adopt an induction argument with hypothesis . For the base case, consider . We can easily see . Now assume that the induction hypothesis holds for some some . We will show . We start with

Furthermore,

where (a) follows from and the fact that

Therefore, we can conclude that

which is the desired result. ∎