Bias correction for quantile regression estimators111This paper supersedes “Conditional quantile estimators: A small sample theory”.

Abstract

We study the bias of classical quantile regression and instrumental variable quantile regression estimators. While being asymptotically first-order unbiased, these estimators can have non-negligible second-order biases. We derive a higher-order stochastic expansion of these estimators using empirical process theory. Based on this expansion, we derive an explicit formula for the second-order bias and propose a feasible bias correction procedure that uses finite-difference estimators of the bias components. The proposed bias correction method performs well in simulations. We provide an empirical illustration using Engel’s classical data on household expenditure.

JEL Classification: C21, C26.

Keywords: instrumental variables, higher-order stochastic expansion, Bahadur-Kiefer expansion, finite-difference estimators, mixed integer linear programming (MILP).

1 Introduction

Many interesting empirical applications of classical quantile regression (QR) (Koenker and Bassett, 1978) and instrumental variable quantile regression (IVQR) (Chernozhukov and Hansen, 2005, 2006) feature small sample sizes, which can arise either as a result of a limited number of observations or when estimating tail quantiles, or both (e.g., Chernozhukov, 2005; Elsner et al., 2008; Chernozhukov and Fernández-Val, 2011; Adrian and Brunnermeier, 2016; Adrian et al., 2019). QR and IVQR estimators are nonlinear and can thus exhibit substantial biases in small samples. In this paper, we theoretically characterize these biases and develop a feasible bias correction procedure.

To study the biases, we start by deriving a higher-order stochastic expansion of the classical QR and exact IVQR estimators.222We define exact IVQR estimators as estimators that exactly minimize a norm of the sample moment conditions. Such estimators can be obtained using mixed-integer programming (MIP) methods (e.g., Chen and Lee, 2018; Zhu, 2019). See Appendix D. Such an expansion is needed because the higher-order terms contribute nonzero biases while the first-order term does not. We derive explicit expressions and uniform (in the quantile level) rates for the components in the expansion, building on the empirical process arguments of Ota et al. (2019). This expansion can be thought of as a refined Bahadur-Kiefer (BK) representation of the estimator that decomposes the nonlinear component into terms up to the order and a remainder.333In Appendix E, we also derive a uniform BK representation for generic IVQR estimators after a feasible 1-step Newton correction.

Using the stochastic expansion, we study the bias of QR and exact IVQR estimators. We derive a bias formula based on the leading terms up to order in the expansion, which we refer to as the second-order (asymptotic) bias. This approach of focusing on the moments of the leading terms in the stochastic expansions is standard in the literature.444See, for example, Nagar (1959); Newey and Smith (2004); Kato et al. (2012); Galvao and Kato (2016); Kaplan and Sun (2017); Hahn et al. (2023), among others. The second-order bias formula provides an approximation of the actual bias that yields a feasible correction. Our results explicitly account for the (up to a logarithmic factor) bias due to nonzero sample moments at the estimator. Our proof strategy is different from the generalized function heuristic used in the existing literature (Phillips, 1991; Lee et al., 2017, 2018), which does not account for all the leading terms up to in the bias.555See Section 3.2 and Appendix C for further discussion and examples. The missing terms can be important bias contributors in practice, as we document in the empirical application in Section 5.

A feasible bias correction procedure then follows from the second-order bias formula. We propose finite-difference estimators of all the components in the formula. These estimators admit higher-order expansions that allow us to select bandwidth rates.666In particular, our finite-difference estimator for the Jacobian coincides with Powell (1986)’s classical estimator, and the bandwidth rate we derive coincides with the AMSE optimal bandwidth choice in Kato (2012). We show that the resulting bias-corrected estimator has zero second-order bias.

We evaluate the performance of our bias correction procedure in a Monte Carlo simulation study. The simulations show that the theoretical (infeasible) bias formula describes well the second-order bias of classical QR and exact IVQR. We find that the proposed feasible bias correction can effectively reduce the bias in many cases, even in samples as small as . However, strong asymmetry and, especially, heavy tails in the conditional distribution of the outcome may reduce the effectiveness of bias correction. The impact of the feasible bias correction on the root MSE (RMSE) is rather small and ambiguous.

We illustrate the bias correction approach by revisiting the relationship between food expenditure and income based on the original Engel (1857) data (e.g., Koenker and Bassett, 1982; Koenker and Hallock, 2001). Our results highlight the importance of bias correction in empirical applications with small sample sizes. Specifically, we find that the second-order bias of classical QR is non-negligible, especially at the upper tail, leading QR to underestimate the effect heterogeneity across quantiles.

Roadmap.

The remainder of the paper is organized as follows. Section 2 describes the model and the estimators. Section 3 provides our main theoretical results. Section 4 presents the Monte Carlo simulation results. Section 5 contains the empirical application. Section 6 concludes. All the proofs and some additional details are given in the Appendix.

2 Model and estimators

Consider a setting with a continuous outcome variable , a vector of covariates , and a vector of instruments . We assume throughout that is fixed. Every observation , , is jointly drawn from a distribution . We assume that is i.i.d., and we will sometimes suppress the index to lighten up the notation. The parameter of interest is defined as a solution to the following unconditional quantile moment restrictions,

| (1) |

We consider two cases: (i) classical QR, where (Koenker and Bassett, 1978), and (ii) linear IVQR, where in general (Chernozhukov and Hansen, 2006, 2008).

The classical QR estimator of is a solution to the following convex minimization problem,

| (2) |

where is the check function (Koenker, 2005) and denotes the sample average, i.e., the expectation with respect to the empirical measure. For IVQR, we consider estimators that exactly minimize the -norm of the sample moments,

| (3) |

where and . This class of exact IVQR estimators includes GMM, which corresponds to as in Chen and Lee (2018) for just-identified models, and the estimator proposed by Zhu (2019), which corresponds to . The cases and have computationally convenient mixed integer linear programming (MILP) representations, while the MILP formulation for has many more decision variables. In our Monte Carlo simulations, we use for computational convenience (see Appendix D).

We use the notation for the unconditional moment restrictions as a function of , and write for its derivative. We maintain the following standard identification assumptions.

Assumption 1 (Identification).

-

1.

is the unique solution to over a compact set , and is in the interior of for all for some .

-

2.

The Jacobian has full rank for all .

As noted by Chernozhukov and Hansen (2006, p.502), compactness of the parameter space “is not restrictive in micro-econometric applications.” Throughout the paper, we use the short notation for whenever it does not lead to ambiguity.

We impose the following smoothness assumptions on the conditional density and its derivatives. Such assumptions are standard in the literature on higher-order properties of quantile estimators (e.g., Ota et al., 2019).

Assumption 2 (Conditional density).

The conditional density of given , , exists, is a.s. three times continuously differentiable on , and there exists a constant such that for all , where and is the -th derivative of .

In our theoretical analysis of the bias, we will often work with a related object, the conditional density of the quantile residual .

Finally, we assume that the regressors and the instruments have bounded higher-order moments.

Assumption 3 (Regressors and instruments).

There exists constants and such that and for all .

Assumption 3 guarantees the existence of all relevant moments of the terms involving and in the higher-order derivatives of the moment conditions and the bias correction (e.g., ). The power parameter (as we show below) determines the upper bound on the rate at which the norm of the sample moment functions converge to zero — higher implies faster convergence to zero.

3 Asymptotic theory for bias correction

To derive a bias correction procedure, we follow the approach of Nagar (1959) and focus on the bias of the leading terms in an asymptotic stochastic expansion of the estimator.

3.1 Stochastic expansion of quantile regression estimators

The classical first-order asymptotic theory for quantile regression estimators (e.g., Koenker and Bassett, 1978; Angrist et al., 2006; Chernozhukov and Hansen, 2006; Kaplan and Sun, 2017; Kaido and Wüthrich, 2021) is based on the following leading term,

| (4) |

For correctly specified models, is an infeasible unbiased estimator of . However, because feasible quantile estimators are nonlinear, they generally have a nonzero higher-order bias. The following theorem provides a characterization of the terms in a stochastic expansion of up to order (ignoring logarithmic terms).

To state the result, we introduce some additional notation. For , define the auxiliary functions , , and .777Processes and take values in the space of bounded functions on . Also, denote the Hessian of the -th moment function by . Finally, for any , denote by the vector with components , .

Theorem 1.

The proof of Theorem 1 builds on the empirical process arguments in Lemma 3 of Ota et al. (2019) and uses the maximal inequality in Corollary 5.1 of Chernozhukov et al. (2014).

The rates in Theorem 1 are uniform in the quantile level . Uniformity is important in theory and practice because QR and IVQR methods are particularly powerful when used to analyze the entire quantile process.

Classical QR and linear IVQR are motivated by the linearity of the true conditional quantile function. In practice, linearity may be restrictive, especially when it is imposed at each . While the result in Theorem 1 remains valid if linearity fails, the interpretation is more complicated in this case. Specifically, if the true conditional quantiles are nonlinear, then the expansion in Theorem 1 applies to the pseudo-true value defined via moment condition (1). For classical QR, this pseudo-true value can be interpreted as the minimizer of a weighted mean-squared error loss function (Angrist et al., 2006). Note further that the result in Theorem 1 holds for every fixed . Thus, if linearity holds at a given , we can interpret the expansion at this under the correct specification without requiring linearity at the other quantile levels.

The expansion in Theorem 1 can be thought of as a refined Bahadur-Kiefer (BK) expansion. Different from standard BK expansions, we do not bundle together all the higher-order terms (as opposed to, for example, Zhou and Portnoy, 1996; Ota et al., 2019). Notice that the dominant nonlinear term in the BK expansion, , has order (Equation (6)). Theorem 3 in Knight (2002) shows that for classical QR with discrete covariates, this term converges in distribution to a zero mean random process. Therefore, we explicitly extract the higher-order terms up to order (ignoring logarithmic terms) from the BK remainder. As we will show in the following sections, these higher-order terms admit feasible counterparts.

Remark 1 (Alternative approach for deriving stochastic expansions).

Portnoy (2012) proposed an alternative approach for deriving a stochastic expansion of classical QR estimators. This approach yields bounds on the precision of a nonlinear Gaussian approximation of order . As we will show, the expansion in Theorem 1 yields a bias formula for both QR and IVQR estimators that admits a feasible implementation. The results in Portnoy (2012) are specific to classical QR, and it is not clear to us whether these results can be used for bias correction using a Nagar-style approach. ∎

3.2 Bias formula for exact estimators

Following common practice (e.g., Nagar, 1959; Kaplan and Sun, 2017), for a generic estimator , we define the second-order bias as the bias of the leading terms in the stochastic expansion of up to the order . This second-order bias can be interpreted as an approximation of the actual bias that works with arbitrarily high probability in large samples.

Before stating the result, we observe that under our Assumption 2, the moment condition (1) is equivalent to

Thus, we can characterize the QR and IVQR estimators using the moment function with sample analog . The following theorem characterizes the second-order bias in terms of and . As in Section 3.1, we define for all .

Theorem 2.

The second-order bias formula (8) has three components.

The first component, , captures the bias from the sample moments not being zero at the estimator. This term is not equal to zero in general. By Theorem 1 and Assumption 3, this term has bias of order at most .

The second component, , appears because of the discontinuity in the sample moment functions. The term reflects the dependence between the sample moments and the linear influence of a single observation on . Notice that the first two components combined correspond to the second order bias of the terms in Theorem 1.

The last component, , stems from the non-uniformity of the conditional distribution of given . This term correspond to the term in Theorem 1. Similar terms are typically present in most nonlinear estimators with nonzero Hessian of the score function (see, for example, Rilstone et al., 1996).

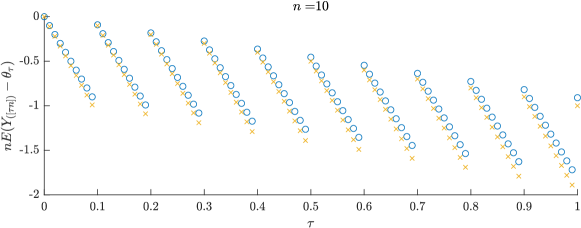

To illustrate the approximate bias formula, consider an order statistic of (corresponding to our framework with ), for which an exact bias formula is available (e.g., Ahsanullah et al., 2013). We show in Appendix C that the precision of the second-order bias formula in this case is , which is smaller than the order of the remainder term in the stochastic expansion of Theorem 1. Figure 1 illustrates the precision of the asymptotic formula by comparing it to the actual bias of the order statistic.

It is interesting to compare our results to the higher-order bias analysis of non-smooth estimators based on the generalized functions heuristic (e.g., Phillips, 1991). In recent work, Lee et al. (2017, 2018) derived a second-order bias formula for classical QR and IVQR under the assumption that the sample moments are zero at the estimator so that the first term of the bias formula vanishes. We show in Appendix C that this term is non-negligible even in simple cases (see also Figure 5 in Section 5).

3.3 Feasible bias correction

The bias formula suggests the following feasible bias-corrected estimator,

where , , , and are estimators of , , , and , respectively, satisfying the following consistency requirement.

Assumption 4 (Consistency of component estimators).

The estimators , , , and are consistent for , , , and , respectively. Moreover, .

In Section 3.4, we propose finite-difference estimators for which Assumption 4 holds under Assumptions 1–3. Assumption 4 could also be verified for other nonparametric estimators of the bias components.

The next theorem shows that the second-order bias of the bias-corrected estimator is zero.

Theorem 3.

Note that the requirement that in Assumption 4 is necessary to ensure that the contribution of the product of the sample moments, which are with (as required by Assumption 3) by Theorem 1, and the estimation error in can be omitted in computing the second-order bias. This condition is only required for IVQR estimators. For classical QR estimators, the sample moments are of order , so that consistency of at any rate of convergence suffices for Theorem 3.

3.4 Finite difference estimators of bias components

To implement the bias correction, we need estimators of , , , and that satisfy Assumption 4. The variance matrix can be estimated using the analogy principle,

All other bias components take the form of derivatives. Therefore, we leverage our theoretical results on the properties of the sample moments to develop a unified finite-difference framework for estimating these components.

Under Assumptions 1 and 2, the Jacobian is and the Hessian consists of gradients of the components of , i.e. , where This suggests the following analog estimators.

The -th component of can be estimated using Powell (1986)’s estimator

| (9) |

where is a bandwidth. Denote by the -th unit vector in , where . The derivative of the -th component of in the direction (i.e. the second partial derivative of ) can be estimated as the symmetric first difference of (9),

where is a (potentially different) bandwidth. For , the finite difference sample analog is

where is a bandwidth. Finally, can be estimated by the sample analog matrix with columns

where is the matrix with elements for .

The next lemma establishes the consistency of the estimators of the bias components. It implies that these estimators satisfy the high-level conditions in Assumption 4. Moreover, it provides nearly remainder-optimal bandwidth rates, i.e., the rates that yield the fastest convergence rates of the stochastic remainder terms of the corresponding stochastic expansions (up to logarithmic terms).

Lemma 1.

Proposition 1 in Kato (2012) shows that the remainder rate for in Lemma 1, , is the AMSE-optimal rate.888 We conjecture that analogous AMSE-optimality results could be established for estimators and , but leave this extension for future work. To implement the finite difference estimators in practice, one needs to choose constants in addition to the bandwidth rates. We discuss the choice of these constants in Sections 4 and 5.

4 Simulation evidence

In this section, we evaluate the performance of our feasible bias correction procedure in a Monte Carlo simulation study. We consider data-generating processes (DGPs) inspired by the simulations in Andrews and Mikusheva (2016). The outcome is generated according to the following location-scale model

where , , , , , , and is the standard normal CDF. Hence, in all the designs, both the regressors and the instruments are . We consider four DGPs that differ with respect to the error distribution and whether or not is exogenous.

| DGP1 (Uniform, exogenous) | , | |

|---|---|---|

| DGP2 (Triangular, exogenous) | , | |

| DGP3 (Cauchy, exogenous) | , | |

| DGP4 (Uniform, endogenous) | , |

An important practical issue is the choice of the bandwidths , , and . We choose the nearly remainder-optimal rates for the bandwidths from Lemma 1: , , , where are constants that are independent of the sample size. We report results for both our baseline choice and the choice of that minimizes the -distance between the residual biases after infeasible and feasible correction for the intercept and the slope parameter over the grid

| (10) |

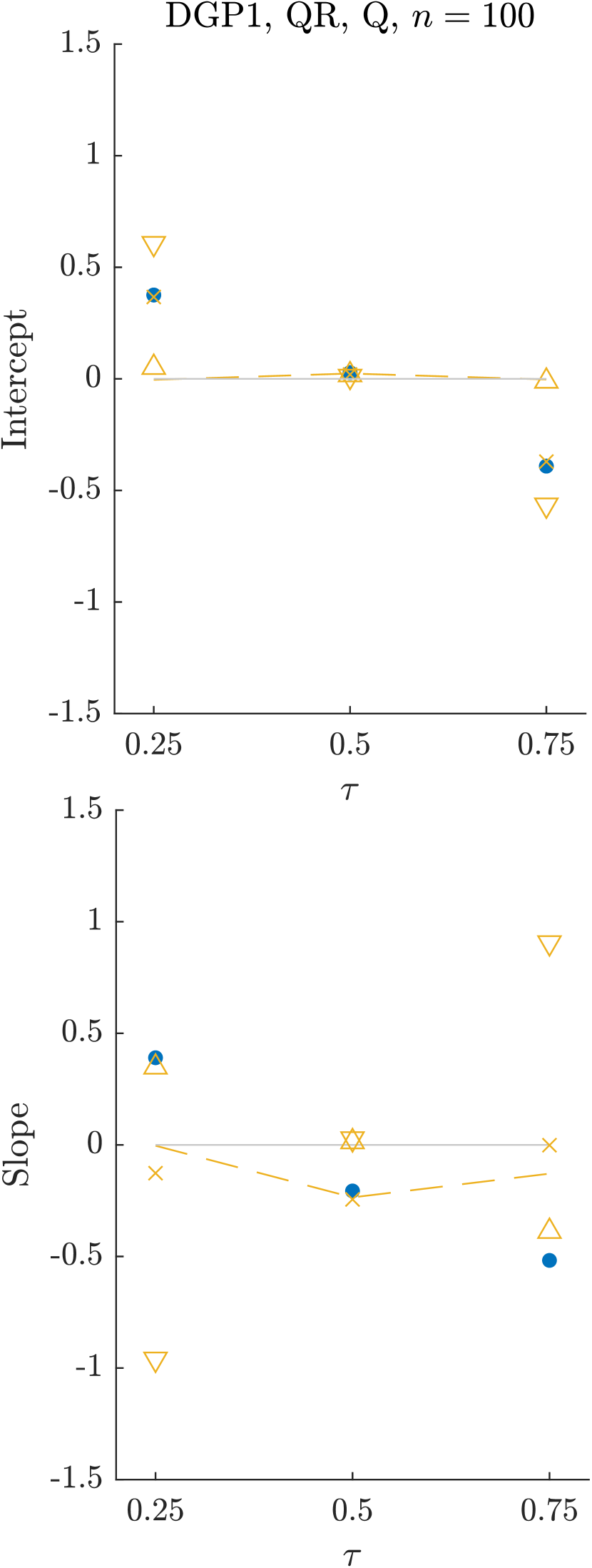

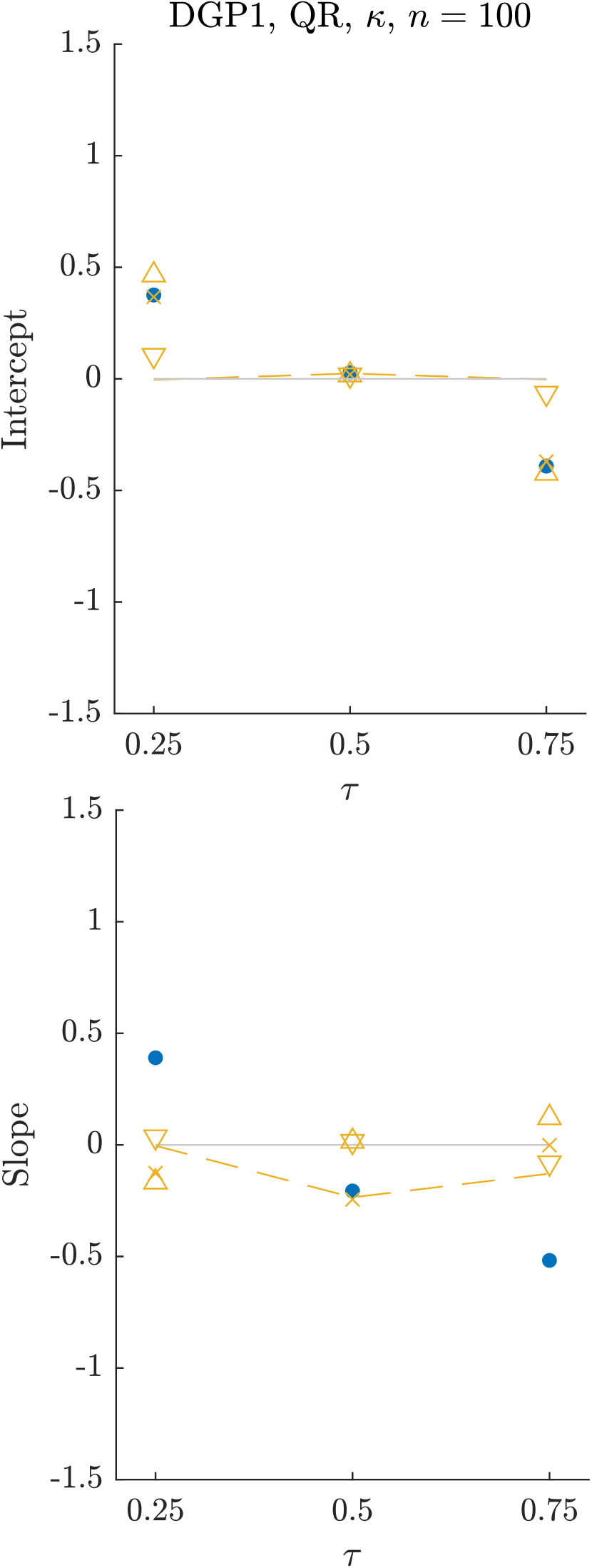

Figure 6 in Appendix F shows how the results change if we increase/decrease each element of , one at a time.

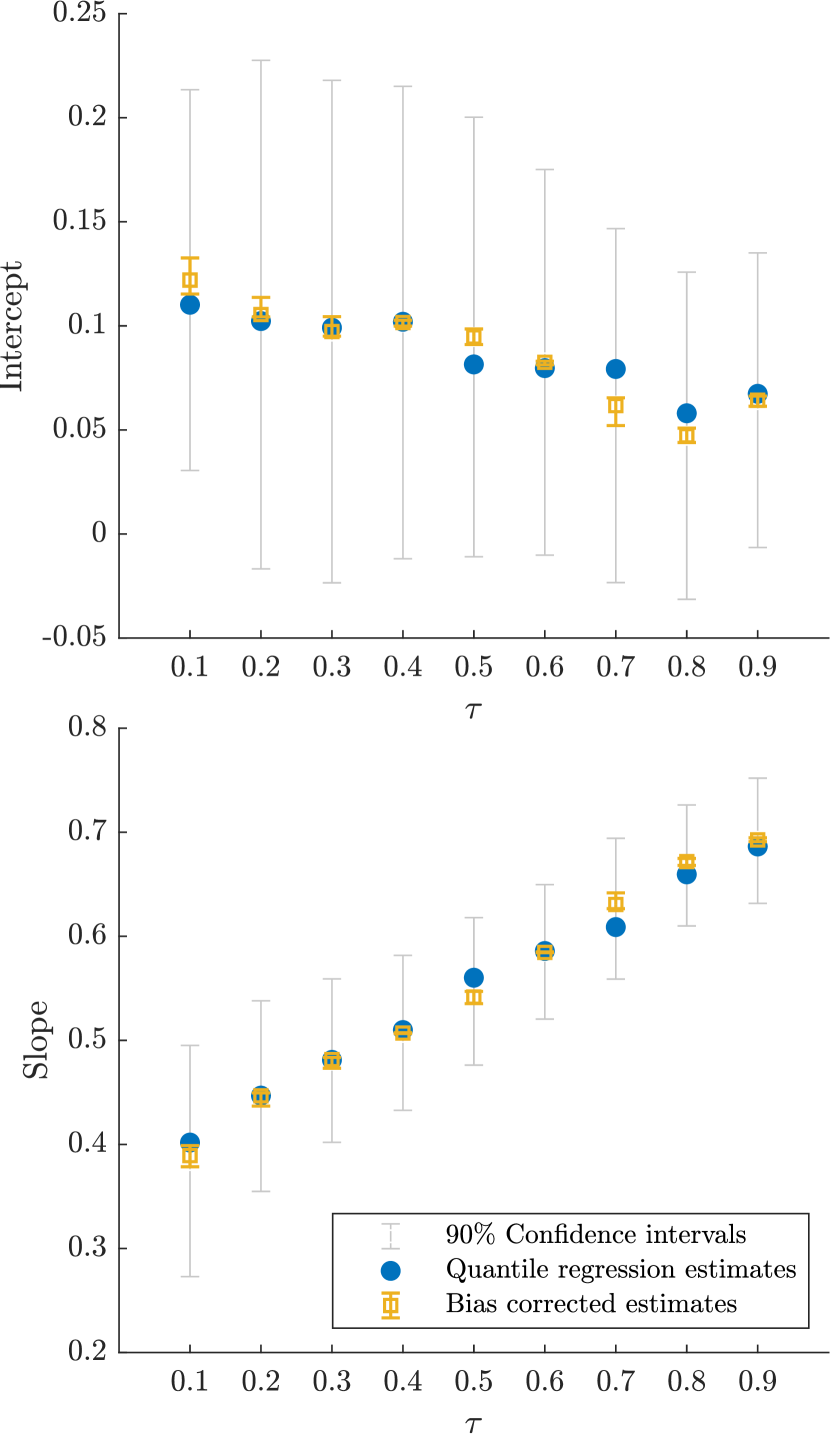

We focus on the performance of bias correction for . To evaluate the precision of the Monte Carlo integration, we compute the Monte Carlo standard error (MCSE). We report MCSE to account for the joint testing of six hypotheses (two hypotheses per each of three levels of ). For comparison, we also display the infeasible bias correction based on the true , , and .

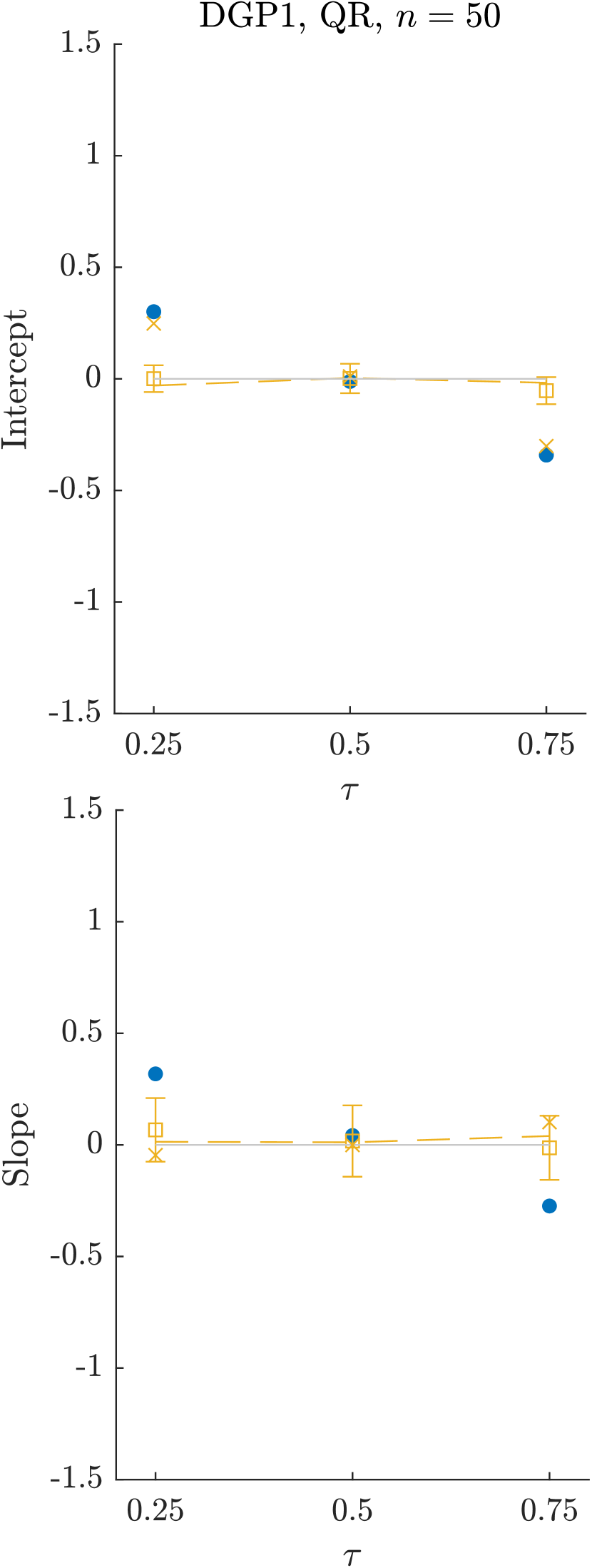

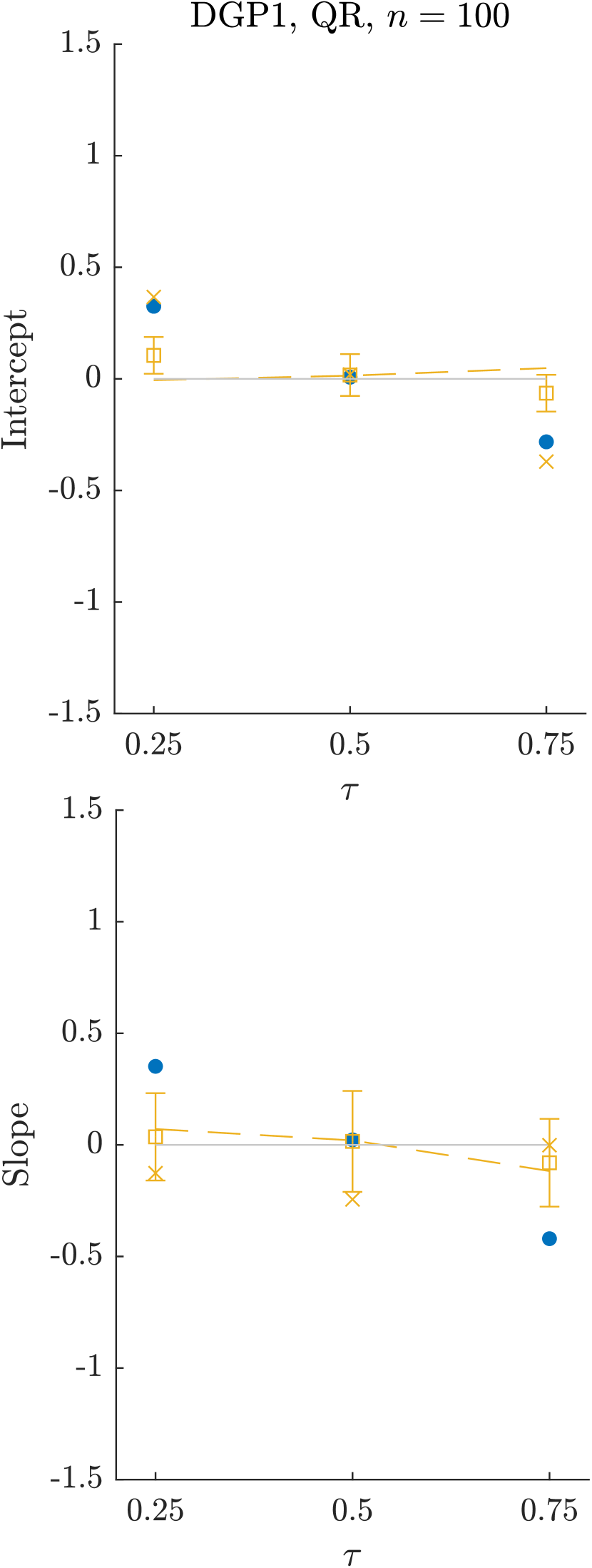

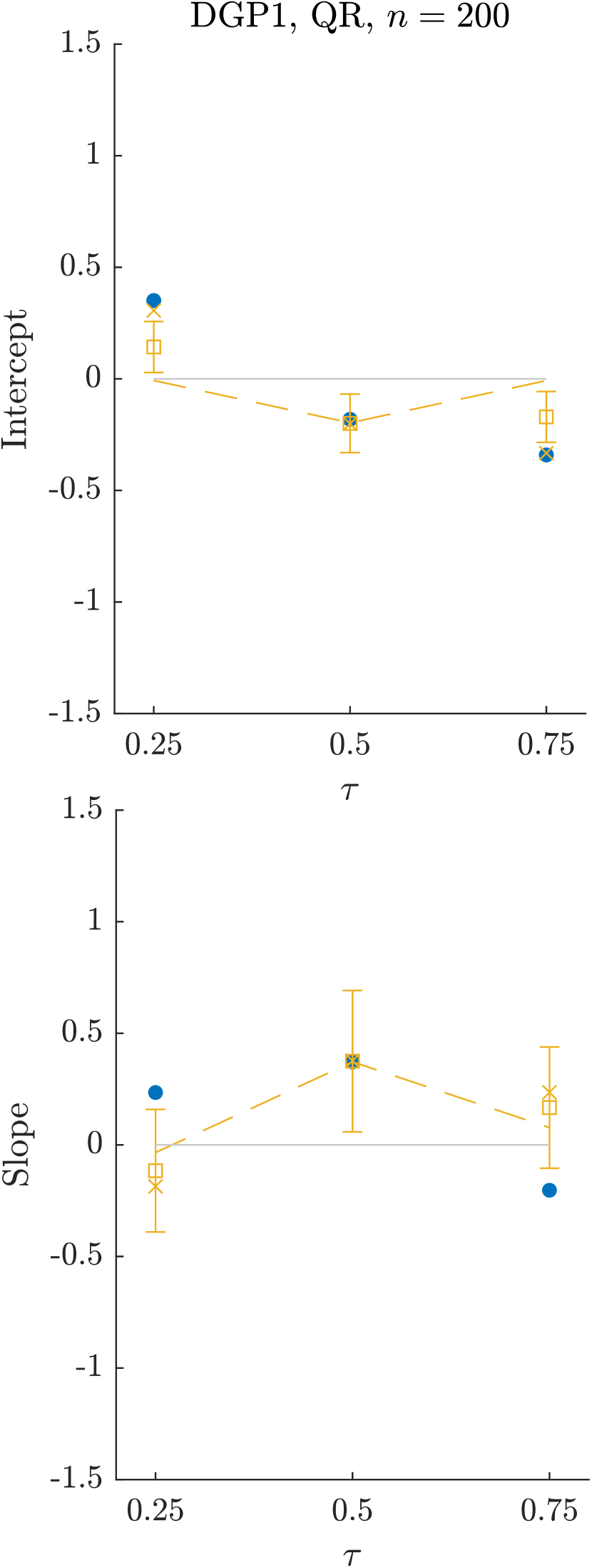

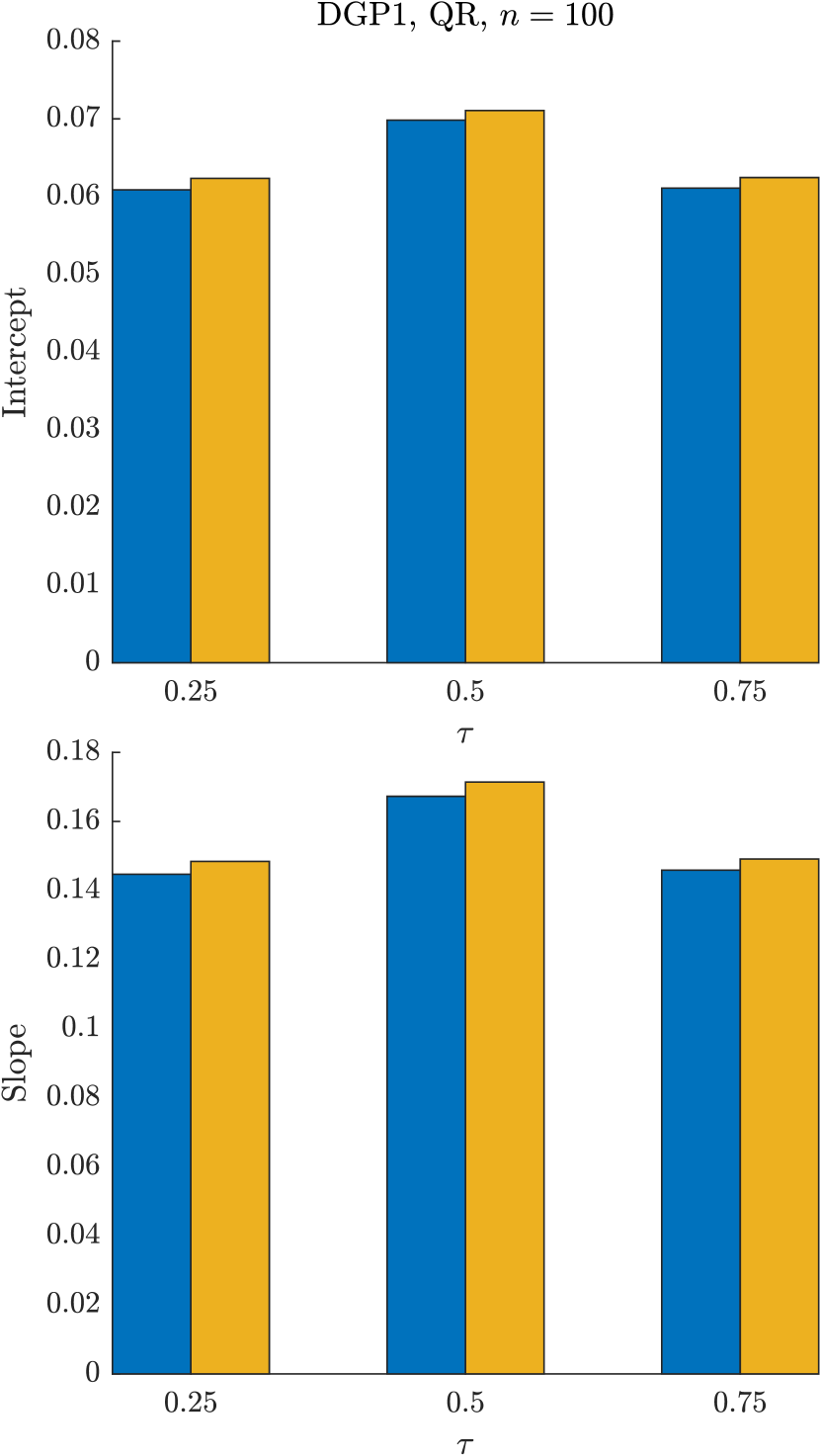

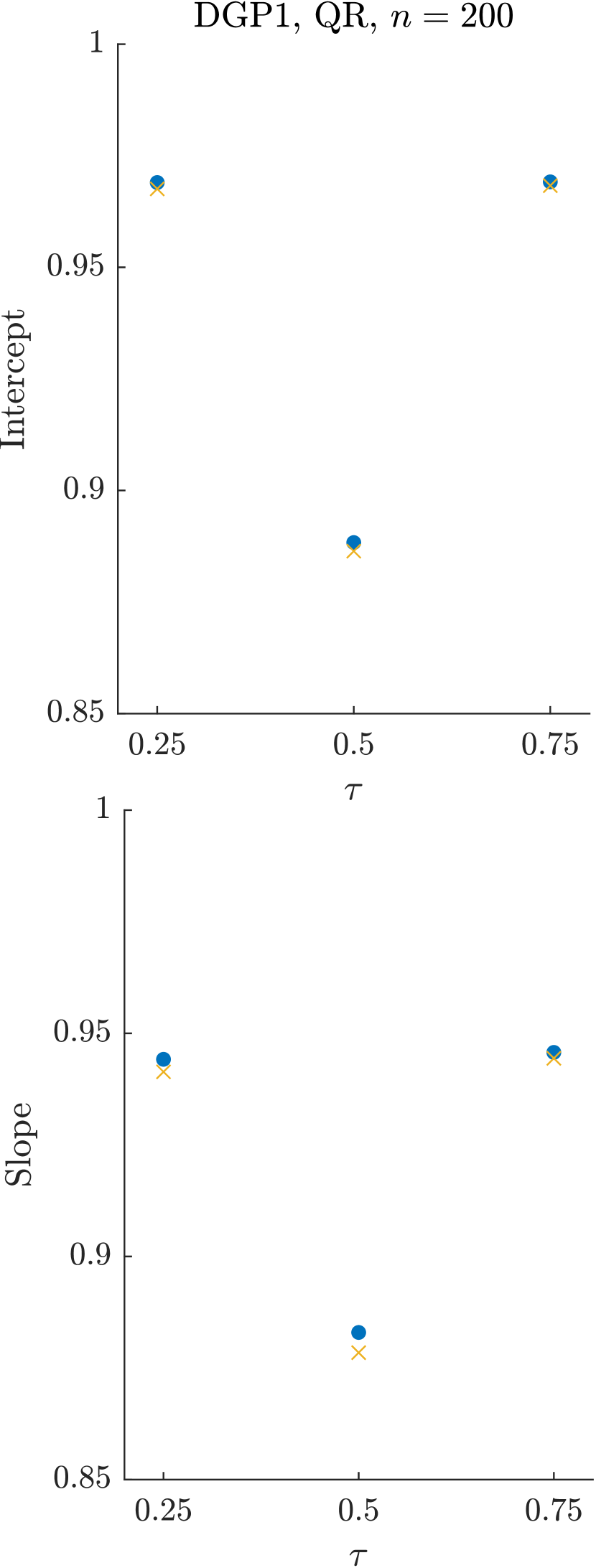

Figure 2 shows the results for the exogenous DGP1 with based on classical QR of on , implemented via linear programming (see Appendix D). Notice that the scaled bias of the QR estimator, , (blue dots) has the same range across the different sample sizes. This illustrates that we are estimating terms in the asymptotic bias expansion, which should be approximately constant after scaling by . One can see that the infeasible bias correction (gold dashed lines) reduces the bias at most quantile levels. The correction does not result in zero bias due to the finite precision of the simulation (the sample moment term does not have an explicit bias formula) and the presence of the higher-order bias terms. Notice that the MCSE grows with the sample size for a fixed number of simulations due to the rescaling, which helps explain the seemingly better performance for .

We find that the feasible bias correction (gold squares and crosses) typically reduces the bias at , where the bias of classical QR is largest, and can get very close to the infeasible bias correction. At , the bias of classical QR is small so that the feasible bias correction has a negligible impact. The feasible bias correction with the baseline bandwidth choice results in comparable deviations from the infeasible one across the different sample sizes. This is consistent with Lemma 1 since, otherwise, different sample sizes would require different constants .

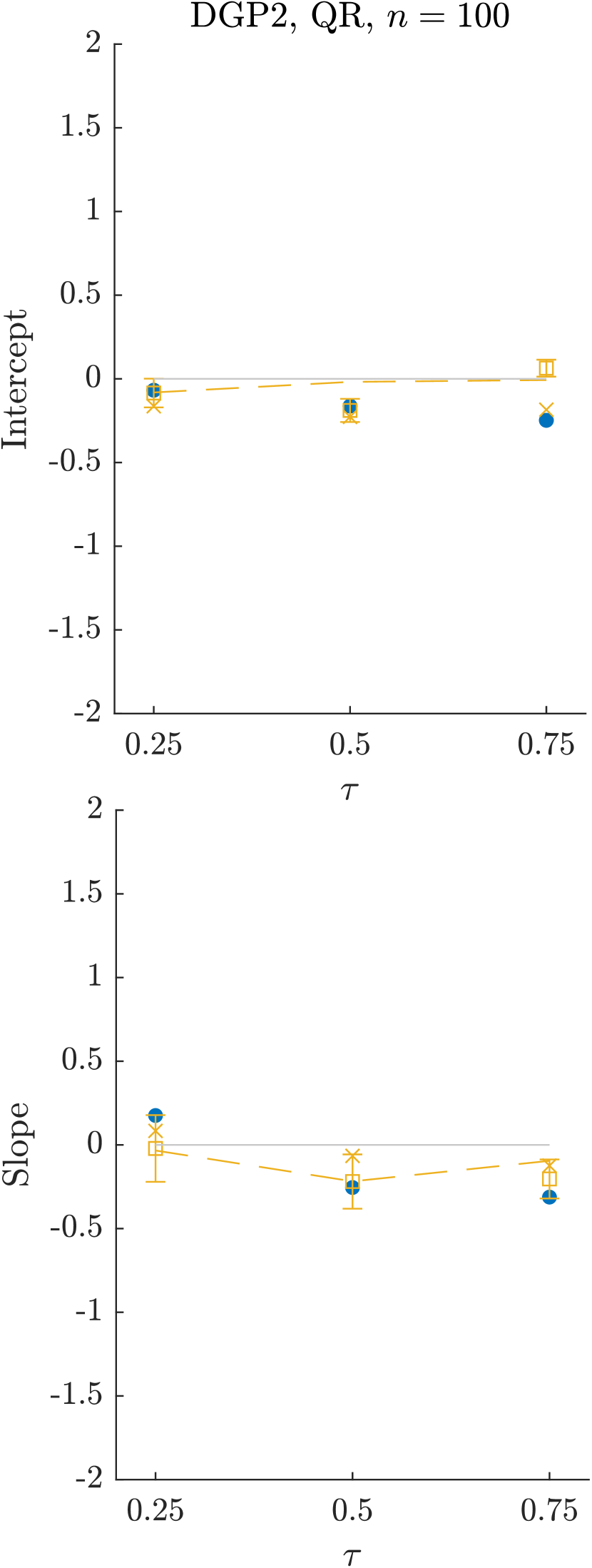

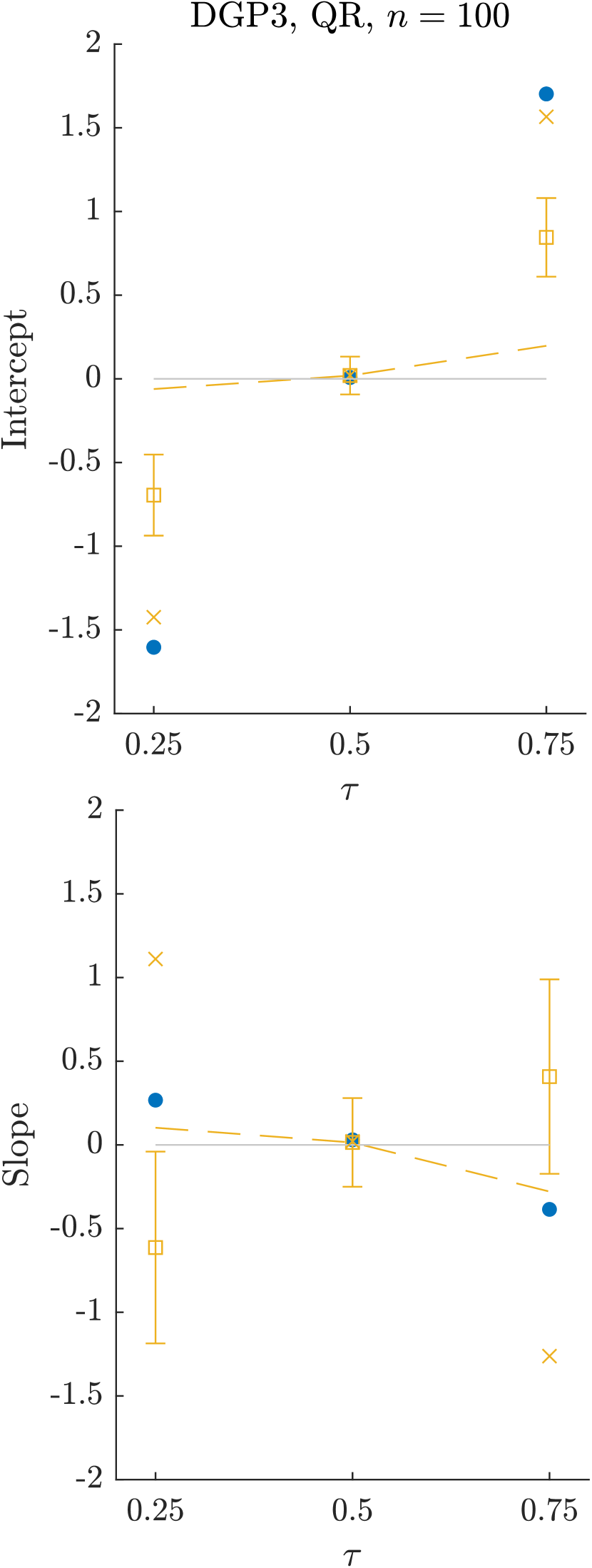

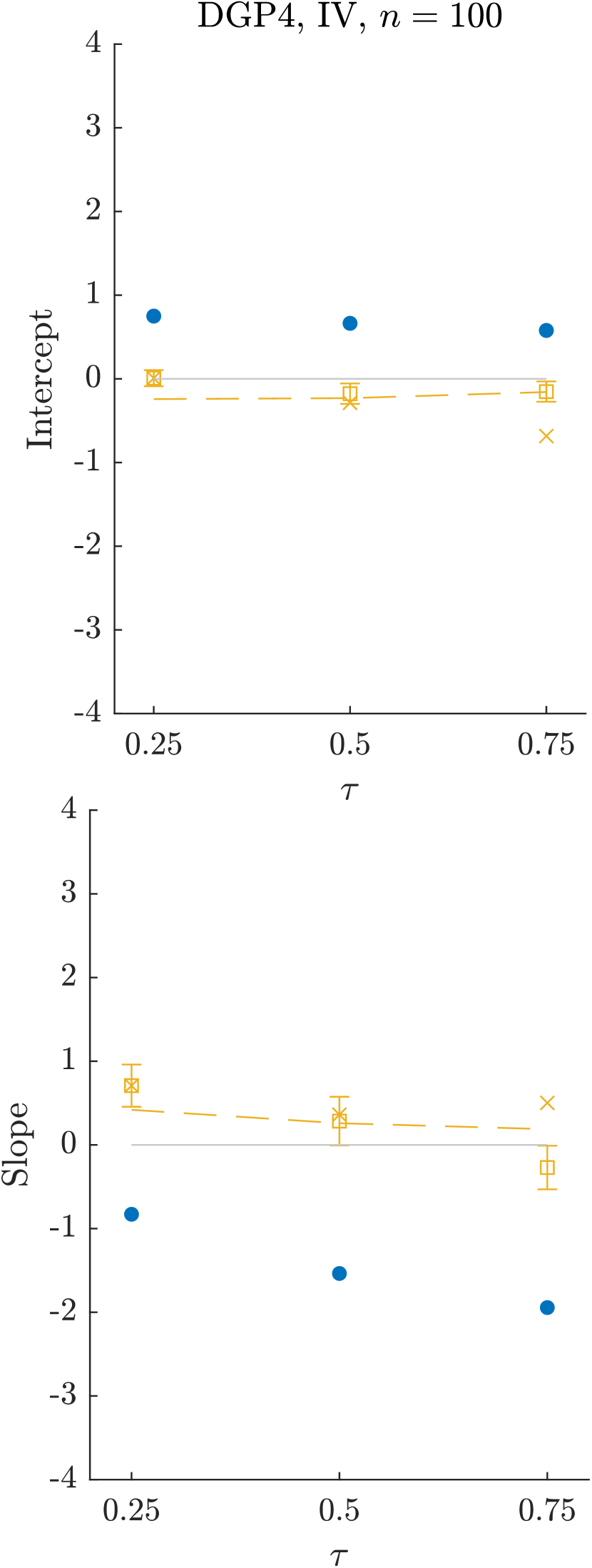

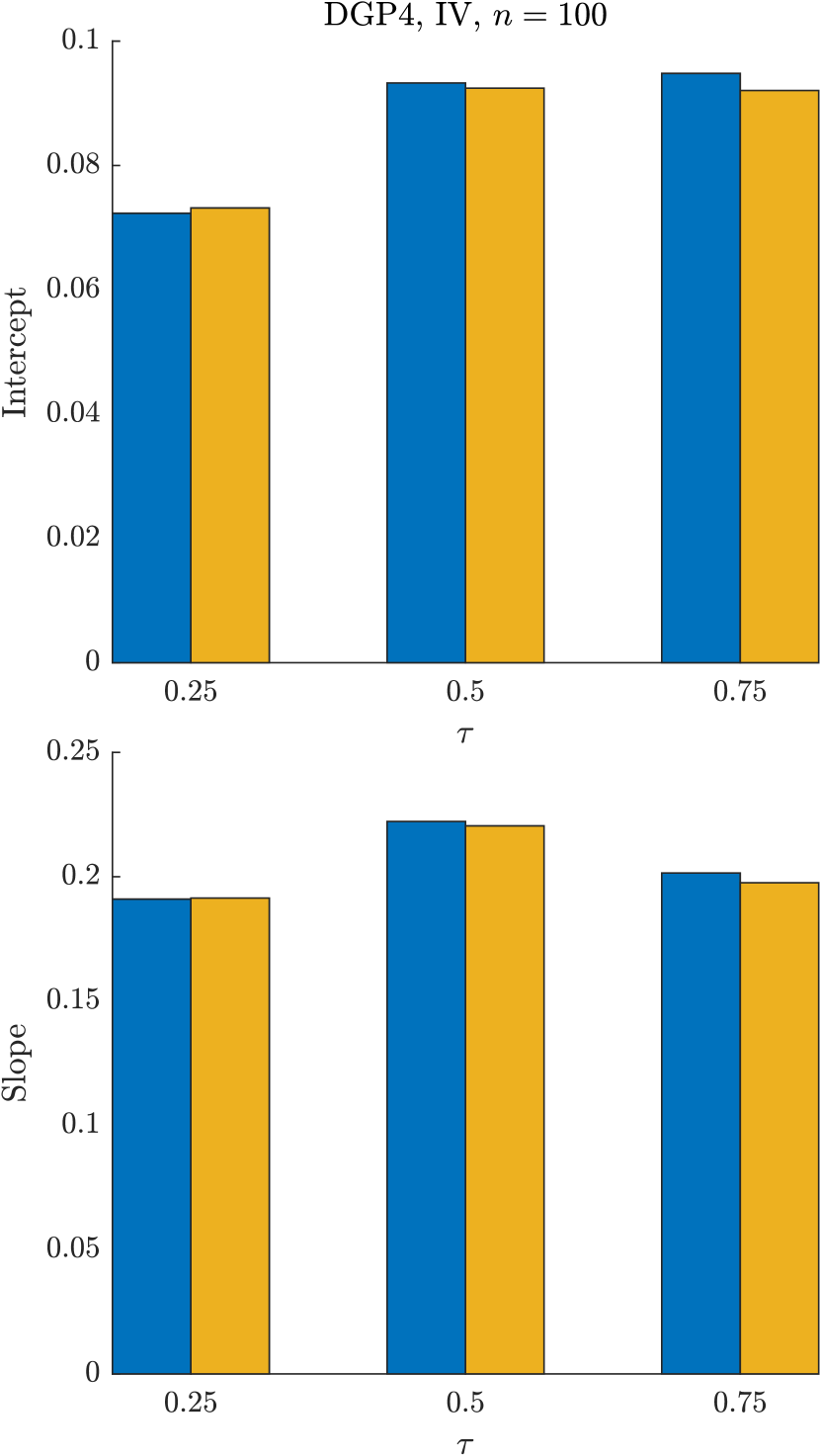

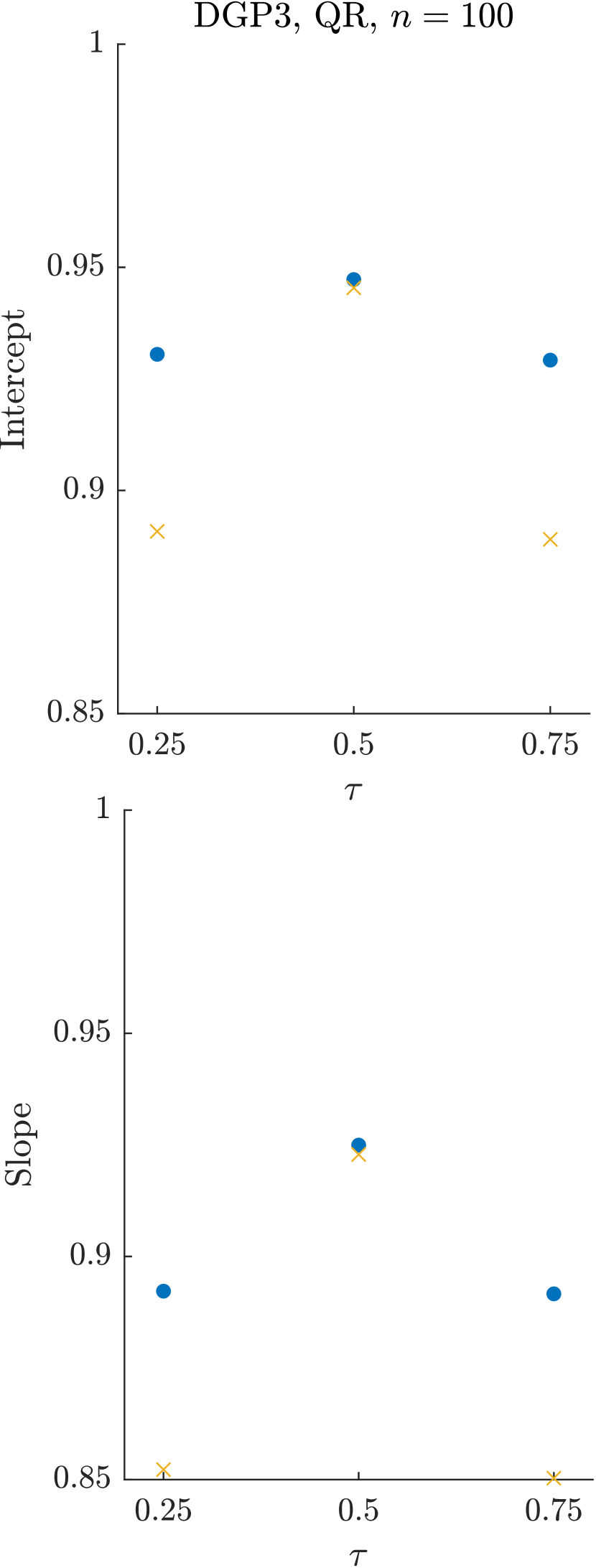

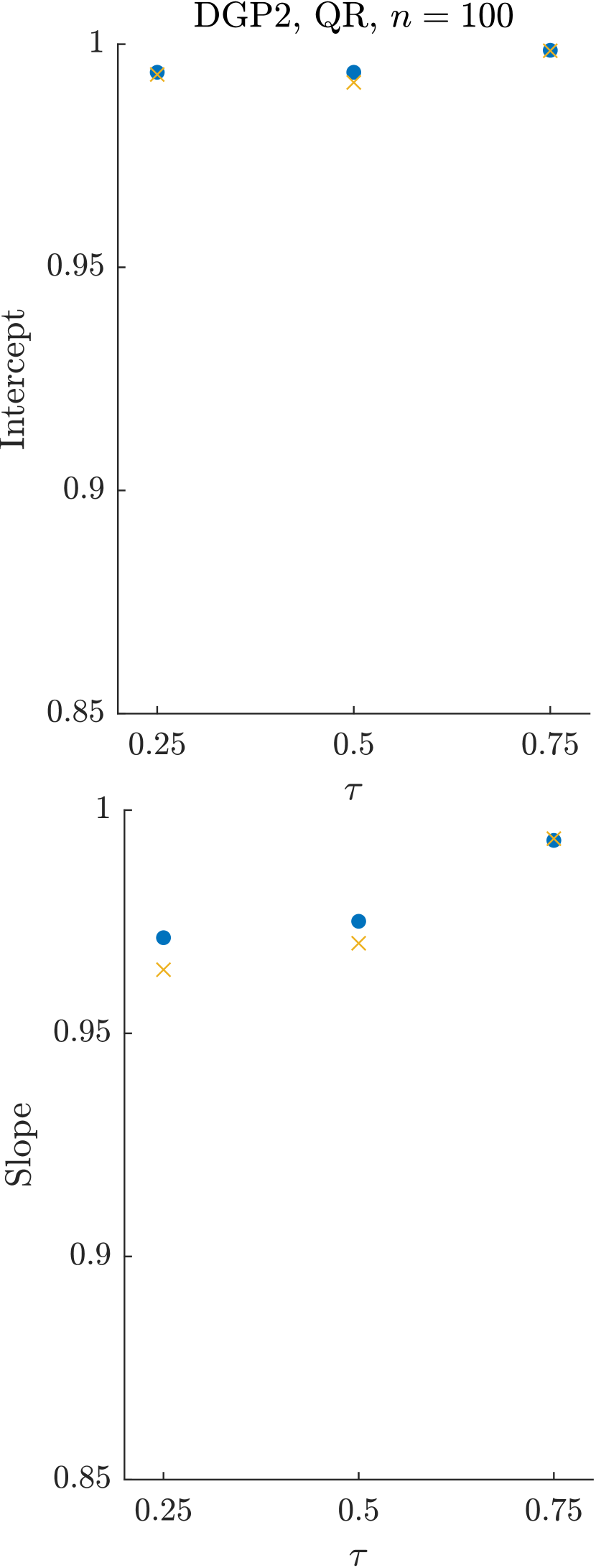

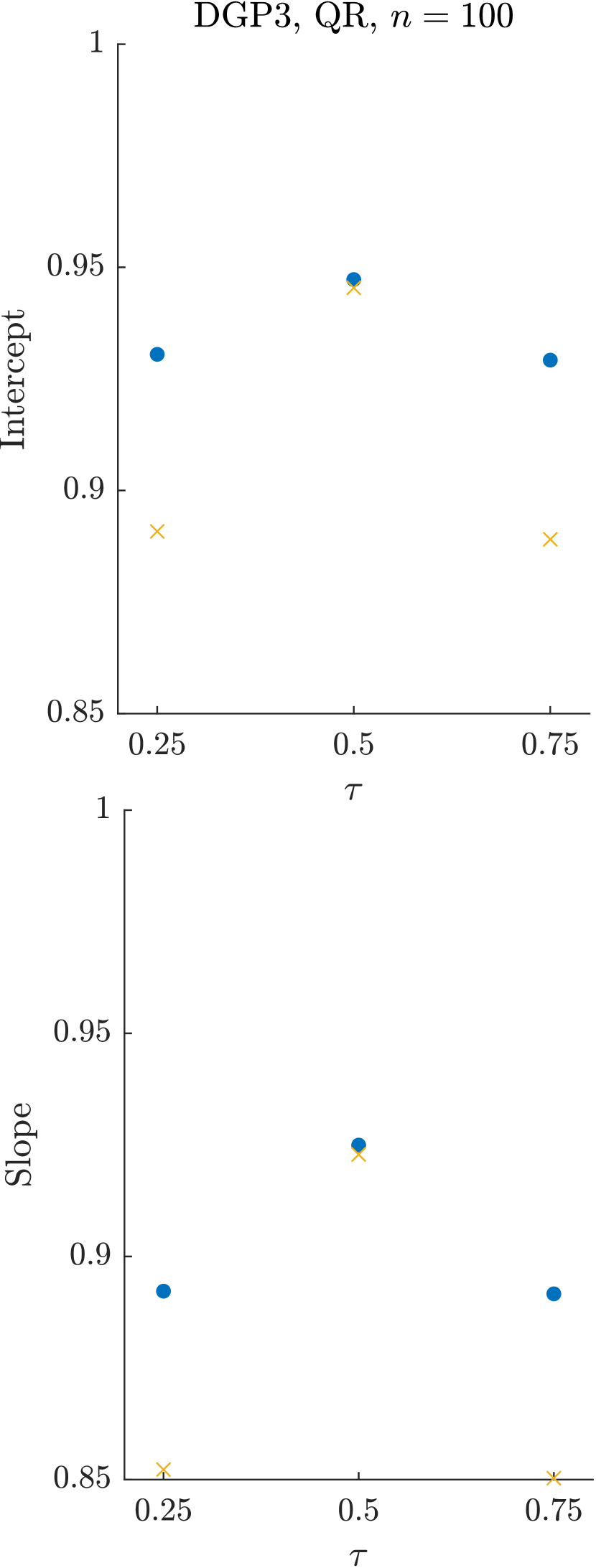

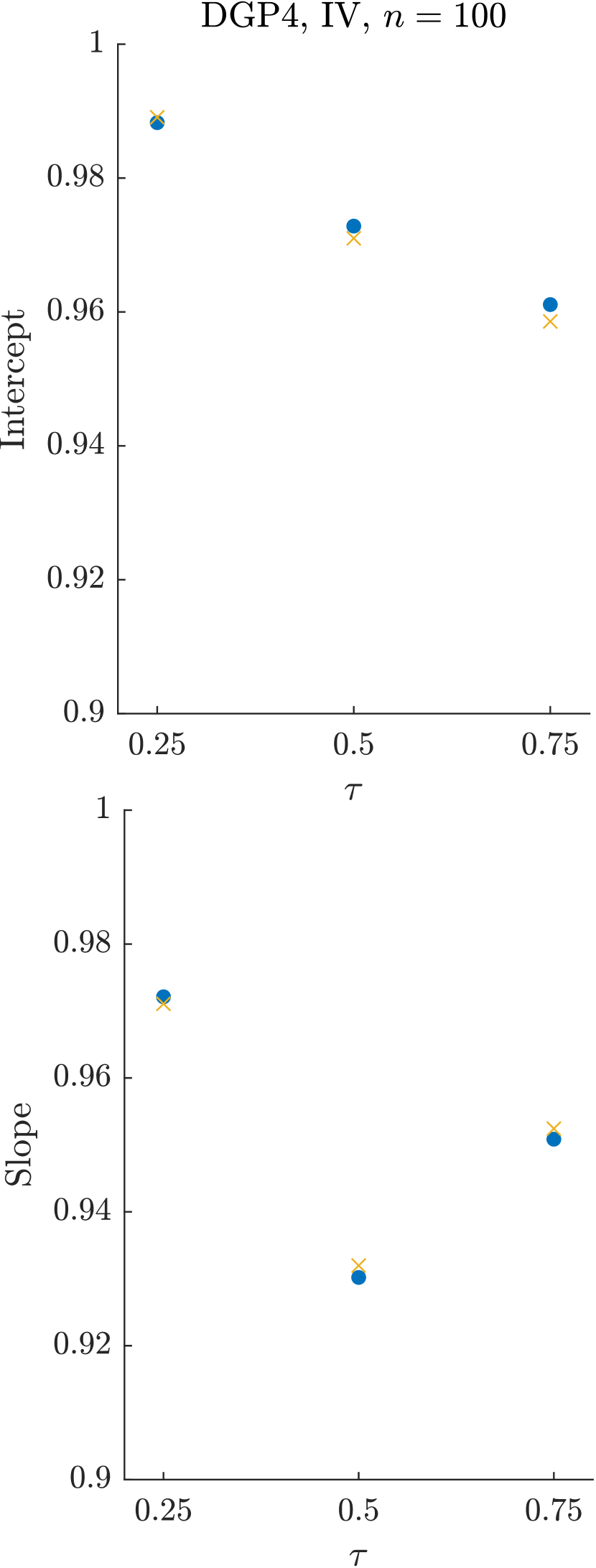

In Figure 3, we study the role of the error distribution and endogeneity. The infeasible bias correction reduces the bias across all the DGPs. Panels (a) and (b) document two cases that present challenges for the feasible bias correction procedure in small samples: strong asymmetry in DGP2, which may affect the performance at the median, and, especially, heavy tails in DGP3, which may affect the performance at tail quantiles. Panel (c) demonstrates that the bias correction performs well when combined with IVQR implemented using the MILP formulation in Appendix D. While the scaled second-order bias of IVQR can be substantial, especially for the slope parameter, the feasible bias correction effectively reduces that bias across all quantile levels considered.

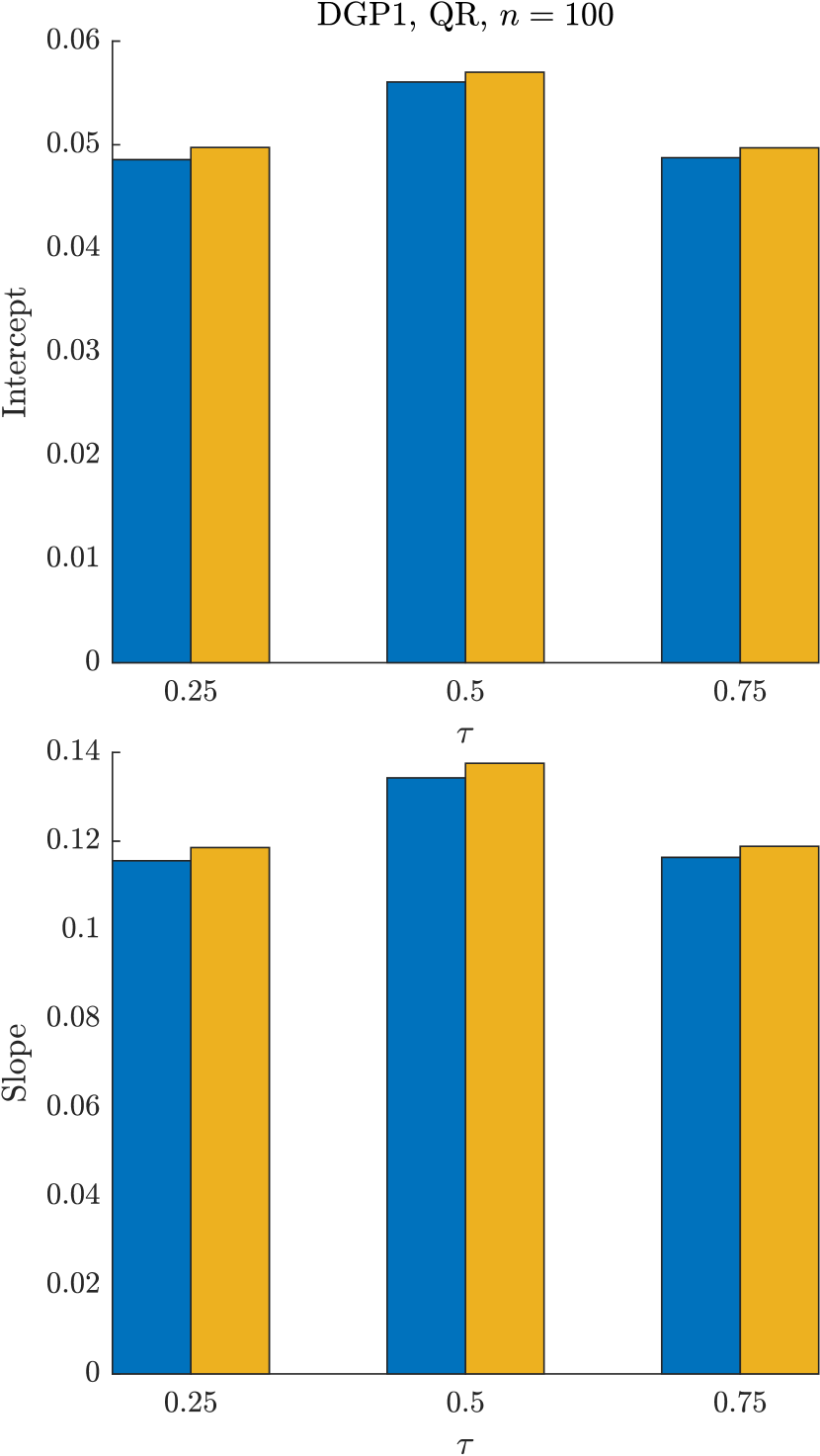

We investigate the impact of bias correction on the RMSE of the estimators in Figure 4. We report the results for QR based on the exogenous DGP1 and IVQR based on the endogenous DGP4 with . Overall, the impact of bias correction on the RMSE is small. While it slightly increases the RMSE for DGP1, it sometimes decreases the RMSE for DGP4. The alternative measure of dispersion, mean absolute deviation, shows similar performance. See Figure 7 in the Appendix.

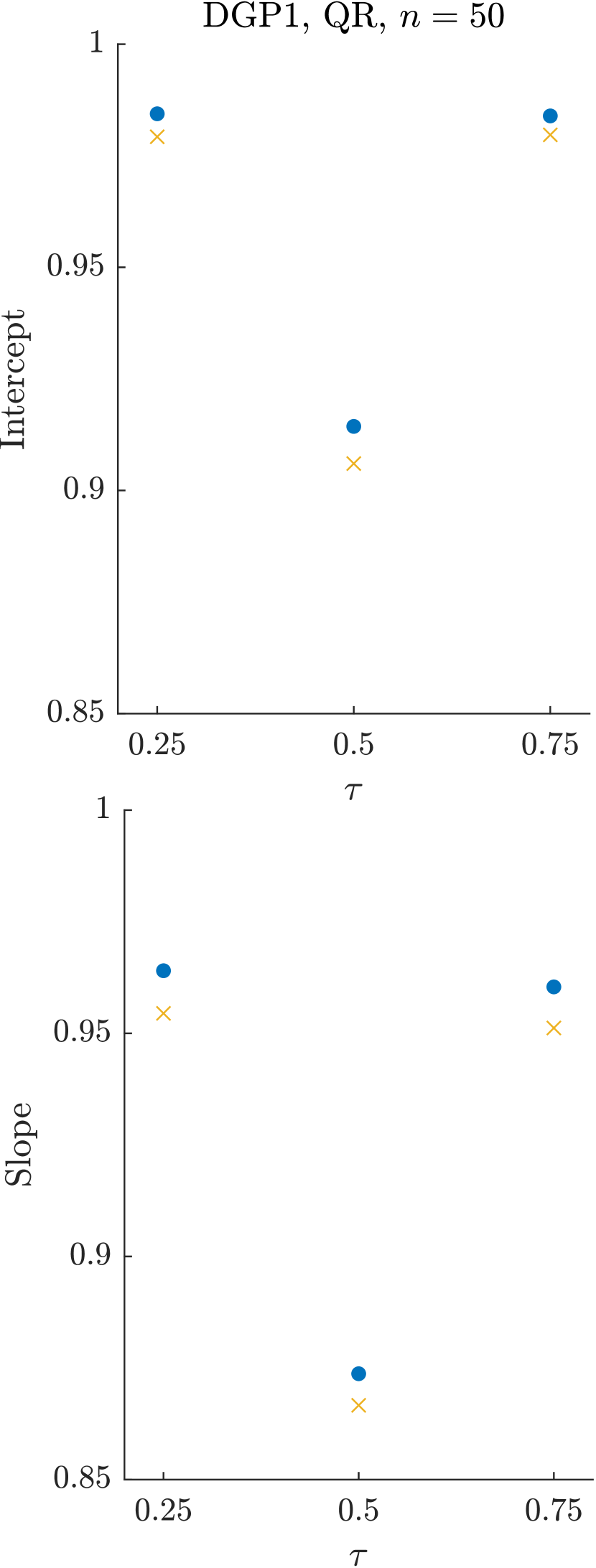

Finally, we study the impact of the bias correction on the coverage probability of the standard confidence intervals. We use the same asymptotic variance estimator of , , as in Section 3.3, for both original and bias-corrected estimator. As a result, by construction, the bias correction does not impact the length of the confidence intervals. Figures 8 and 9 in the Appendix show coverage before and after the bias correction. The bias correction brings the empirical coverage closer to the nominal coverage in many but not all cases. This impact is small for all the DGPs, except for extreme quantiles in DGP3 with heavy tails where the feasible bias correction would require larger sample sizes. (The infeasible formula still results in bias improvement in that case, see Panel (b) in Figure 3.)

Notes: The panels display the bias (multiplied by ) of the intercept and the slope for classical QR without bias correction (blue dots), QR with the best feasible bias correction (gold squares), QR with the baseline feasible bias correction (gold crosses), and QR with infeasible bias correction (gold dashed line) for DGP1 with . The error bands (gold bars) correspond to MCSE to account for the joint testing of 6 hypotheses. (Notice that the scaled MCSE of the estimator grows with .) All results are based on 40,000 simulation repetitions.

Notes: The panels display the bias (multiplied by ) of the intercept and the slope for classical QR without bias correction (blue dots), QR with the best feasible bias correction (gold squares), QR with the baseline feasible bias correction (gold crosses), and QR with infeasible bias correction (gold dashed line) for DGP2–DGP4 with . We use classical QR for DGP2 and DGP3 and exact IVQR (implemented via the MILP formulation in Appendix D) for DGP4. The error bands (gold bars) correspond to MCSE to account for the joint testing of 6 hypotheses. The DGP2 and DGP3 results are based on 40,000 simulation repetitions; the DGP4 results are based on 10,000 repetitions. For DGP4, the infeasible bias correction is based on the feasible formula applied to a simulated sample of 10,000,000 observations.

Notes: Panel (a) compares the RSME for classical QR without (blue) and with (gold) bias correction. Panel (b) compares the RMSE for exact IVQR (implemented via the MILP formulation in Appendix D) without (blue) and with (gold) bias correction. The results are based on 40,000 simulation repetitions.

5 Empirical application

The second-order bias matters most in applications with small sample sizes. We therefore illustrate our bias correction approach using the classical dataset of Engel (1857), analyzed by Koenker and Bassett (1982) and Koenker and Hallock (2001), among others. The data contain information on annual income and food expenditure (in Belgian francs) for Belgian working-class households and are obtained from the R package quantreg (Koenker, 2022). One feature of these data is the growing dispersion of the outcome variable (food expenditure) as a function of the regressor (income) (Koenker and Hallock, 2001), which is similar to our Monte Carlo designs. We divide the values of income and food expenditure by so that the unit of measurement becomes a thousand Belgian francs. This makes the scale of the variables comparable to that in our Monte Carlo simulations, allowing us to use the same baseline bandwidth choices.

We estimate classical QRs of food expenditure () on income () and a constant (blue dots). The bias-corrected estimators (gold squares) are obtained using the baseline bandwidth choice , , and with .

Figure 5 presents the results. Panel (a) shows the impact of bias correction. The results suggest that bias correction is more important at the upper tail, where we find differences between the classical QR and the bias-corrected estimates. After the bias correction, we observe more heterogeneity across quantile levels, suggesting that the second-order bias leads classical QR to underestimate this heterogeneity. Notice that there is a second-order bias even at the median (i.e., least absolute deviation) regression.

To investigate the sensitivity of our results to the choice of the three bandwidths, we also report the minimum and maximum bias-corrected estimates when varies over the set in equation (10). Our results suggest that bias-corrected estimates are insensitive to the bandwidth choice.

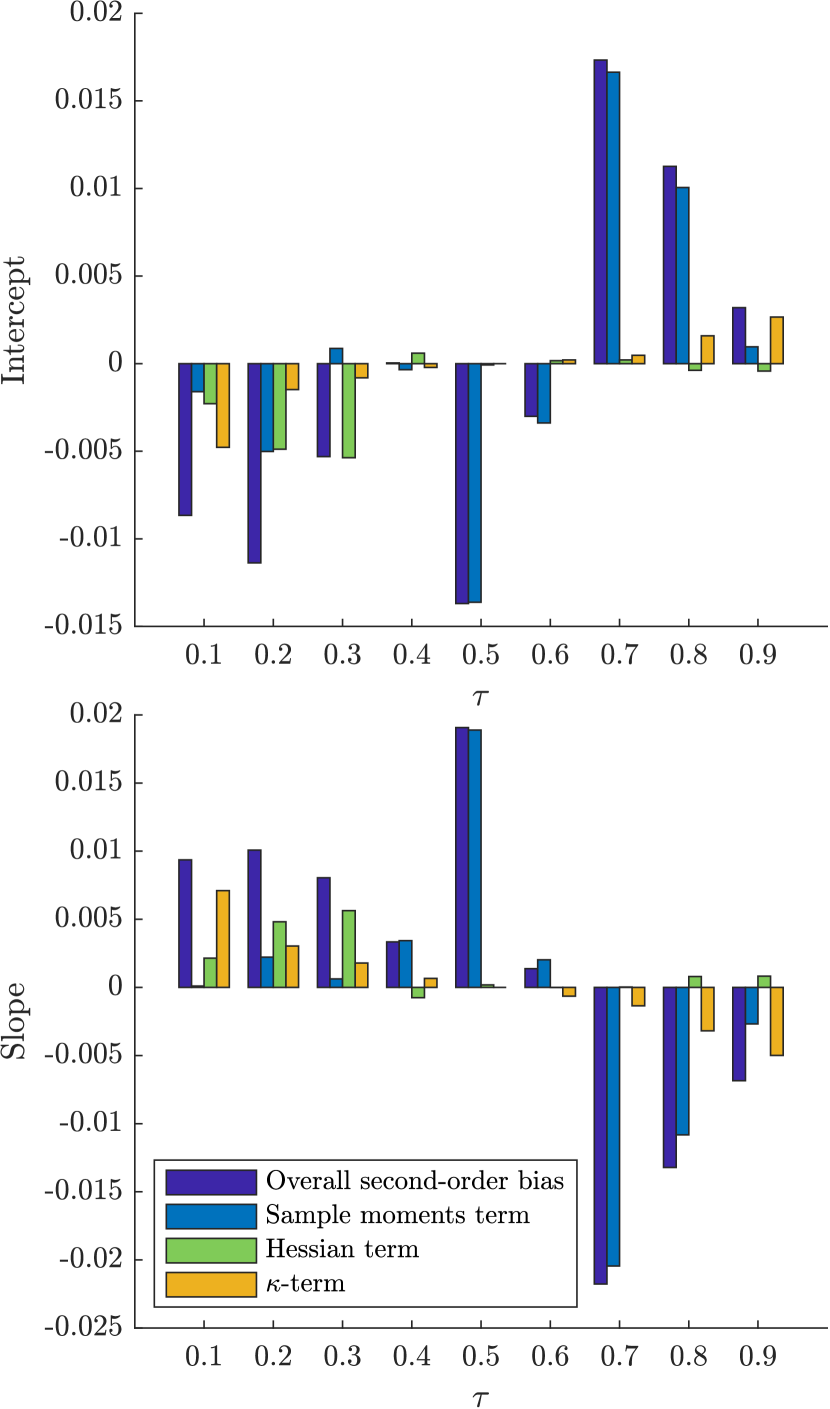

Panel (b) shows the individual contributions of the different components to the overall second-order bias. We can decompose the bias correction term as follows:

The main takeaway from the bias decomposition is that while all three components play a role, the sample moments term (i) can be very large and accounts for most of the bias at the upper tail quantiles. The QR estimates with the highest overall second-order bias have the largest contribution from the sample moments term (). These results suggest that one could reduce the worst-case bias substantially by only correcting the sample moment term, which is akin to a 1-step Newton correction (see Appendix E).

Notes: Panel (a) compares the classical QR estimates with (blue dots) and without (gold squares) bias correction, where . The bars indicate the minimum and the maximum of the estimates when varying over the grid defined in (10). Panel (b) shows the contributions of different bias components to the overall second-order bias.

6 Conclusion

We demonstrate that QR and IVQR estimators can exhibit a non-negligible second-order bias. We theoretically characterize this bias and use our results to derive a novel feasible bias correction method. Our method can effectively reduce the second-order bias at a very low computational cost and without substantially increasing RMSE.

Acknowledgements

We are grateful to the Editor (Xiaohong Chen), the Associate Editor, and three anonymous referees, as well as Victor Chernozhukov, Zheng Fang, Dalia Ghanem, Jiaying Gu, Marc Henry, Keisuke Hirano, Nail Kashaev, Roger Koenker, Vladimir Koltchinskii, Michal Kolesar, Simon Lee, Blaise Melly, Hyungsik Roger Moon, Hashem Pesaran, Joris Pinkse, Wolfgang Polonik, Stephen Portnoy, Geert Ridder, Andres Santos, Davide Viviano, Yuanyuan Wan, and seminar participants at UC Berkeley, UC Davis, University of Toronto, and USC for valuable comments. All errors and omissions are our own.

References

- Abramowitz and Stegun (1972) Abramowitz, M. and I. A. Stegun (1972): Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables, National Bureau of Standards Applied Mathematics Series 55. Tenth Printing.

- Adrian et al. (2019) Adrian, T., N. Boyarchenko, and D. Giannone (2019): “Vulnerable Growth,” American Economic Review, 109, 1263–89.

- Adrian and Brunnermeier (2016) Adrian, T. and M. K. Brunnermeier (2016): “CoVaR,” American Economic Review, 106, 1705–41.

- Ahsanullah et al. (2013) Ahsanullah, M., V. B. Nevzorov, and M. Shakil (2013): An introduction to order statistics, vol. 8, Springer.

- Andrews and Mikusheva (2016) Andrews, I. and A. Mikusheva (2016): “Conditional inference with a functional nuisance parameter,” Econometrica, 84, 1571–1612.

- Angrist et al. (2006) Angrist, J., V. Chernozhukov, and I. Fernández-Val (2006): “Quantile regression under misspecification, with an application to the US wage structure,” Econometrica, 74, 539–563.

- Chen and Lee (2018) Chen, L.-Y. and S. Lee (2018): “Exact computation of GMM estimators for instrumental variable quantile regression models,” Journal of Applied Econometrics, 33, 553–567.

- Chernozhukov (2005) Chernozhukov, V. (2005): “Extremal quantile regression,” The Annals of Statistics, 33, 806 – 839.

- Chernozhukov et al. (2014) Chernozhukov, V., D. Chetverikov, and K. Kato (2014): “Gaussian approximation of suprema of empirical processes,” The Annals of Statistics, 42, 1564–1597.

- Chernozhukov and Fernández-Val (2011) Chernozhukov, V. and I. Fernández-Val (2011): “Inference for extremal conditional quantile models, with an application to market and birthweight risks,” The Review of Economic Studies, 78, 559–589.

- Chernozhukov and Hansen (2005) Chernozhukov, V. and C. Hansen (2005): “An IV model of quantile treatment effects,” Econometrica, 73, 245–261.

- Chernozhukov and Hansen (2006) ——— (2006): “Instrumental quantile regression inference for structural and treatment effect models,” Journal of Econometrics, 132, 491–525.

- Chernozhukov and Hansen (2008) ——— (2008): “Instrumental variable quantile regression: A robust inference approach,” Journal of Econometrics, 142, 379–398.

- Elsner et al. (2008) Elsner, J. B., J. P. Kossin, and T. H. Jagger (2008): “The increasing intensity of the strongest tropical cyclones,” Nature, 455, 92–95.

- Engel (1857) Engel, E. (1857): “Die Produktions- und Konsumptionsverhältnisse des Königreichs Sachsen.” Zeitschrift des Statistischen Bureaus des Königlich Sächsischen Ministeriums des Innern, 8, 1–54.

- Galvao and Kato (2016) Galvao, A. F. and K. Kato (2016): “Smoothed quantile regression for panel data,” Journal of Econometrics, 193, 92–112.

- Hahn et al. (2023) Hahn, J., D. W. Hughes, G. Kuersteiner, and W. K. Newey (2023): “Efficient Bias Correction for Cross-section and Panel Data,” arXiv:2207.09943.

- Kaido and Wüthrich (2021) Kaido, H. and K. Wüthrich (2021): “Decentralization estimators for instrumental variable quantile regression models,” Quantitative Economics, 12, 443–475.

- Kallenberg (2006) Kallenberg, O. (2006): Foundations of modern probability, Springer Science & Business Media.

- Kaplan and Sun (2017) Kaplan, D. M. and Y. Sun (2017): “Smoothed estimating equations for instrumental variables quantile regression,” Econometric Theory, 33, 105–157.

- Kato (2012) Kato, K. (2012): “Asymptotic normality of Powell’s kernel estimator,” Annals of the Institute of Statistical Mathematics, 64, 255–273.

- Kato et al. (2012) Kato, K., A. F. Galvao Jr, and G. V. Montes-Rojas (2012): “Asymptotics for panel quantile regression models with individual effects,” Journal of Econometrics, 170, 76–91.

- Knight (2002) Knight, K. (2002): “Comparing conditional quantile estimators: first and second order considerations,” Working Paper.

- Koenker (2005) Koenker (2005): Quantile Regression, Cambridge University Press.

- Koenker (2022) Koenker, R. (2022): quantreg: Quantile Regression, R package version 5.94.

- Koenker and Bassett (1978) Koenker, R. and G. Bassett (1978): “Regression Quantiles,” Econometrica, 46, 33–50.

- Koenker and Bassett (1982) ——— (1982): “Robust Tests for Heteroscedasticity Based on Regression Quantiles,” Econometrica, 50, 43–61.

- Koenker and Hallock (2001) Koenker, R. and K. F. Hallock (2001): “Quantile Regression,” Journal of Economic Perspectives, 15, 143–156.

- Lee et al. (2017) Lee, T.-H., A. Ullah, and H. Wang (2017): “The Second-order Bias and MSE of Quantile Estimators,” Unpublished manuscript.

- Lee et al. (2018) ——— (2018): “The second-order bias of quantile estimators,” Economics Letters, 173, 143–147.

- Nagar (1959) Nagar, A. L. (1959): “The Bias and Moment Matrix of the General k-Class Estimators of the Parameters in Simultaneous Equations,” Econometrica, 27, 575–595.

- Newey and McFadden (1994) Newey, K. and D. McFadden (1994): “Large sample estimation and hypothesis,” Handbook of Econometrics, IV, Edited by RF Engle and DL McFadden, 2112–2245.

- Newey and Smith (2004) Newey, W. K. and R. J. Smith (2004): “Higher order properties of GMM and generalized empirical likelihood estimators,” Econometrica, 72, 219–255.

- Olver (2014) Olver, P. J. (2014): Introduction to partial differential equations, Springer.

- Ota et al. (2019) Ota, H., K. Kato, and S. Hara (2019): “Quantile regression approach to conditional mode estimation,” Electronic Journal of Statistics, 13, 3120–3160.

- Phillips (1991) Phillips, P. C. B. (1991): “A shortcut to LAD estimator asymptotics,” Econometric Theory, 450–463.

- Portnoy (2012) Portnoy, S. (2012): “Nearly root- approximation for regression quantile processes,” The Annals of Statistics, 40, 1714–1736.

- Powell (1986) Powell, J. L. (1986): “Censored regression quantiles,” Journal of Econometrics, 32, 143–155.

- Rilstone et al. (1996) Rilstone, P., V. Srivastava, and A. Ullah (1996): “The second-order bias and mean squared error of nonlinear estimators,” Journal of Econometrics, 75, 369 – 395.

- van der Vaart and Wellner (1996) van der Vaart, A. W. and J. A. Wellner (1996): Weak Convergence and Empirical Processes: With Applications to Statistics, Springer Science & Business Media.

- Vapnik and Chervonenkis (1971) Vapnik, V. N. and A. Y. Chervonenkis (1971): “On uniform convergence of the frequencies of events to their probabilities,” Teoriya Veroyatnostei i ee Primeneniya, 16, 264–279.

- Zhou and Portnoy (1996) Zhou, K. Q. and S. L. Portnoy (1996): “Direct use of regression quantiles to construct confidence sets in linear models,” The Annals of Statistics, 24, 287–306.

- Zhu (2019) Zhu, Y. (2019): “Learning non-smooth models: instrumental variable quantile regressions and related problems,” arXiv preprint arXiv:1805.06855.

Online appendix

Appendix A Bahadur-Kiefer representation, proofs

A.1 Auxiliary results for generic IVQR estimators

Proof.

By definition, . The result then follows from the dominated convergence theorem. ∎

Lemma A.2.

Proof.

By definition,

By Lemma A.1, is three times continuously differentiable. Since is restricted to a compact set , the norm of the third derivative is bounded on . The Taylor theorem implies that there exist a neighborhood of such that for any in the neighborhood,

where uniformly in . Then (11) follows immediately because is a uniformly consistent estimator. ∎

Now let us study the large sample behavior of the term in (11).

Lemma A.3.

Proof.

The proof relies on the arguments in Ota et al. (2019, Lemma 3) adapted to our setting. The idea is to verify the conditions of Lemma 1 of Ota et al. (2019), which follows from Corollary 5.1 in Chernozhukov et al. (2014) and use this corollary to prove the desired result.

Since , we have for any sequence . Consider the functions

that constitute the function class

where is a sequence such that and . Let be the standard empirical process operator on with the data , . By Assumption 3, admits an envelope .

Let us now verify the conditions in Lemma 1 of Ota et al. (2019). First, since

we obtain

where we used Assumptions 2 and the inequality

in conjunction with Assumption 3.

Therefore, the variance parameter of the process is

Second, using Lemma 2 in Ota et al. (2019), we have

Third, because the function class is a VC class (Vapnik and Chervonenkis, 1971) with the envelope , there exist constants and independent of such that the standard entropy bound

holds (e.g., van der Vaart and Wellner, 1996, Section 2.6). Here the supremum is taken over all finitely discrete measures and is the norm.

Finally, applying Lemma 1 in Ota et al. (2019), we obtain

| (12) |

where the last equality holds by choosing sufficiently slowly. Note that the right-hand side of this equation does not depend on . Consequently, by the definition of the norm and equation (12),

where the last equality holds by Markov’s inequality.

∎

A.2 Auxiliary results for exact estimators

Proof.

We give the proof for . Uniform consistency for the case of was established by Angrist et al. (2006, Theorem 3).

Lemma A.5.

Proof.

The exact QR estimators yield exact zeros of the subgradient

where the multi-valued function is defined as for and for . The subgradient function differs from sample moment functions by the fraction of observations with . Note that under Assumption 2, has density with respect to the Lebesgue measure conditional on . Thus the observations are in general position with probability 1 (see Definition 2.1 and the subsequent discussion in Koenker, 2005). Because the observations are in general position with probability 1, there are at most terms like that, and so . ∎

Lemma A.6.

Proof.

The proof proceeds in four steps.

Step 1. Under the assumptions of the lemma, the empirical process is Donsker (see proof of Lemma A.3 above) and thus asymptotically stochastically equicontinuous (see discussion in van der Vaart and Wellner, 1996, Section 2.1.2; also Theorem 1.5.7 and Problem 2.1.5 in the same book).

Step 2. By definition, can be written as

| (17) |

where and are well-defined by Assumption 1 . This class of functions indexed by is Donsker by similar arguments as in Lemma A.3 (note that the parameter enters this class only through and through the linear term ). The Donsker property implies

| (18) |

By Lemma A.2 applied to ,

Then after substituting the first equation in (18) into the term , we have

So by Step 1, .

Since is defined as the estimator attaining the minimal -norm,

Step 3. Consider . By equation (18), is uniformly consistent, and hence uniformly in since is stochastically equicontinuous (Step 1). Then by the stochastic equicontinuity of (Step 1) and Lemma A.2 applied to , uniformly in ,

This implies

which establishes (16).

By Assumption 1.2, we can multiply the last equation by and obtain

which implies we can take by a fixed point argument, which is discussed in detail in Step 3 of the proof of Lemma A.7 below. This implies (14).

By uniform consistency of and Step 1,

The results of the previous lemma can be further refined.

Proof.

The proof proceeds in four steps.

Step 2. Consider the estimator

where, by Step 1, .

Define to be a sequence satisfying (Lemma A.6 implies uniform consistency of and that can be taken to be at least ).

By Lemma A.3,

By Lemma A.2 applied to and the definition of ,

So by (20) and the definition of , we get

which implies we can take as the rate of .

Step 3. By definition of , . Then from (22), we obtain

On the right-hand side of this inequality, suppose that the first term dominates the second term. Then we have

or, equivalently,

By Step 2, it implies the statement of the lemma.

Suppose, instead, that the second term dominates the first term. Then by Step 2, . The statement of the lemma follows.

∎

A.3 Proof of Theorem 1

Step 1 (Uniform consistency). The estimators under consideration are uniformly consistent, . Specifically, the QR estimator is analyzed in Lemma A.5; the exact IVQR estimator is analyzed in Lemma A.6.

Step 2 (Generic stochastic expansion). By Step 1, we can apply Lemma A.2 with to obtain

Step 3 (Bounds on remainder in asymptotic linear expansion). Now we can use the remaining lemmas to bound the orders of the terms in the expansion. The result in equation (6) follows from Lemma A.3 with and . The first equation in (5) is stated in Lemma A.5. Similarly, Lemma A.7 yields the second equation in (5). As a result, we have

| (23) |

which is a uniform Bahadur-Kiefer expansion for both QR and exact IVQR estimators.

Step 4 (Analysis of quadratic term). The empirical process indexed by is Donsker (see Step 2 of Lemma A.6), which implies (7), i.e.,

| (24) |

Then by Step 3, we have, uniformly in ,

Hence, the expansion in Step 2 becomes

with .

∎

Appendix B Second-order bias correction, proofs

B.1 Auxiliary results

Lemma B.1.

Consider any random sequence a.s. Under Assumption 3, the following expectations exist,

| (25) | |||

| (26) |

Proof.

By the triangular inequality,

| (27) |

Therefore, Since the right-hand side does not depend on , equation (25) holds.

By definition, we have

| (28) |

We can bound using a maximal inequality for an appropriately chosen empirical process. Consider the functions

and the corresponding function class

Note that , where with 1 in -th position. By Assumption 3, admits an envelope .

We use the maximal inequality in Lemma 1 of Ota et al. (2019) to establish (26). To do so, we verify the three conditions of this lemma. First,

Therefore, the variance parameter of the process is

Second, using Lemma 2 in Ota et al. (2019) we have

Third, because the function class is a VC class with the envelope , there exist constants and independent of such that the standard entropy bound

holds (e.g., van der Vaart and Wellner, 1996, Section 2.6). Here the supremum is taken with respect to all finitely discrete measures and is the norm.

Finally, applying Lemma 1 in Ota et al. (2019), we obtain

| (29) |

It follows that

which implies

∎

Lemma B.2.

Consider such that and . Then for any .

Proof.

Notice that

Hence the sequence is uniformly integrable. By Proposition 4.12 from Kallenberg (2006), .

∎

Lemma B.3.

Proof.

The proof proceeds in six steps.

Step 1. By Lemma B.1, exists. Note that

| (30) |

Theorem 1 implies

| (31) |

where . Since by construction, is restricted to a compact set , it is bounded. The term has bounded moments up to order by Assumption 3. As a result, the remainder term has bounded moments up to order .

Step 2. Define and split the first term in equation (30) as follows:

| (32) |

We can use (31) to isolate an influence of observation , . Without loss of generality for i.i.d. data, we consider . The indicator can be rewritten as where

is equal to without the linear influence of the observation .

Note also that the first term in the Taylor expansion can be rewritten as

The following argument justifies the use of Taylor’s theorem here. The function is measurable as a limit of measurable functions (increments of conditional CDF).

Therefore, for any non-negative measurable function with finite expectation, the integral

exists (but may take infinite values).

By the law of iterated expectations,

(see Step 5 below for a detailed justification based on Fubini-Tonelli theorem). By Assumption 2, is uniformly bounded and

| (33) |

The same is true for the derivative of the density in place of , by Assumption 2. Therefore, and , which justifies the Taylor expansion of the expectations of the conditional PDF above. By this property (a.s. smoothness of ) and equation (31),

where is some random variable that takes values between and . By the boundedness of , Assumption 3, the bound on the derivative of the density in Assumption 2, and the fact that , these expectations exist and the second term denoted as

is of order .

By the definition of , the first term can be rewritten as

Step 3. Now consider , the second term in (30). Let be a copy of , which is independent of the sample . Also, define

which satisfies . Then

| (35) | ||||

where by the mean value theorem and

The rate is derived by an argument similar to the one below equation (33). Note that the term in line (35) is equal to zero since by the i.i.d. data assumption. Combining this equality with (34) yields

| (36) |

Step 4. Let us simplify the first two terms of equation (36). Define

so that has zero mean and is independent of and .

Denote . Apply Taylor’s theorem (as in Step 2) to obtain

| (37) |

where is a random scalar that takes values between and . By Step 1, has a finite second moment. Therefore, the last term in (37) is finite.

For the second term in (37), note that

where is a random scalar that takes values between and . The last equality follows since by Step 1 and . As before, let us introduce

By the boundedness of -moments of (Assumption 3), exists. Hence, (37) becomes

Step 5. Let us study the last term in equation (38). For any , consider an auxiliary function

By definition, for every ,

By the existence of the corresponding conditional PDF (possibly taking infinite values),

By the Fubini-Tonelli theorem for product measures, we can exchange the order of integration,

Hence, by the main theorem of calculus, for all ,

Since the function , we have

Therefore, equation (38) becomes

| (39) |

where

Step 6. Let us simplify the second and the third terms in equation (39). The latter can be rewritten as

| (40) | |||

| (41) | |||

| (42) |

where , is the analog of corresponding to the moment condition for , , and , and the last equality uses (39). Notice that it follows from equations (40) and (41) that

| (43) |

Using the definition of and Fubini-Tonelli theorem as in Step 5,

Since has conditional density by Assumption 2, the same argument can be applied to show that . Hence, equations (39) and (42) imply

Finally, equations (39) and (43) yield

where . By construction, and is uniformly integrable as the sum of uniformly integrable components. The proof is complete. ∎

Lemma B.4.

Suppose that a function is four times continuously differentiable in a neighborhood of x. Then for sufficiently small ,

B.2 Proofs of main results on bias correction

Proof of Theorem 2.

Proof of Theorem 3.

Theorem 1 implies the following asymptotic expansion for the bias-corrected estimator,

| (44) | ||||

| (45) | ||||

| (46) | ||||

| (47) | ||||

| (48) |

By Theorem 2, the expectation of the sum of the terms in (44) and (45) is zero. By Theorem 1, Assumption 4, and the Mann-Wald and Delta theorems, the first term in (46) is

since . The same rate is true for the second term in (46) and the terms in (47) The last line, expression (48), has zero mean by Assumption 3. Therefore, . ∎

Proof of Lemma 1.

Notice that by the same arguments as in Lemma A.3, for any ,

Then using Lemma B.4 for and the Delta theorem, we obtain

The overall rate is . By Lemmas A.3, A.5, A.7, and Assumption 2, this remainder rate is uniform in . Ignoring a logarithmic factor, we see that the bandwidth delivers an optimal overall remainder rate that is uniform in .

Notice that

By an argument similar to the above,

Since, under the optimal step size for the estimator , we have , the overall rate is

The optimal bandwidth is with

By the CLT and the equicontinuity of the relevant sample moment functions implied by Lemma A.3,

∎

Appendix C Illustration of approximate bias formula in univariate case

Suppose we are interested in estimating the -quantile of a uniformly distributed outcome variable . This is a special case of the general framework with , .

Note that, under the maintained assumptions, the true parameter has an equivalent alternative definition as a solution to

As a result, there are two ways of defining an estimator: as a minimizer of or as a minimizer of , where

The derivatives of the population moment conditions are , and , , respectively. In either case, the closure of the argmin set will be , where . If the fractional part , a minimizer of () is the order statistic (, respectively); if , a minimizer of () is (, respectively). Of course, on the real line , all norms , coincide with the absolute value .

In this simple example, formula (8) yields asymptotic bias expansions

| (49) | |||

| (50) |

The exact bias formulas are given by (e.g., Ahsanullah et al., 2013)

Comparing these formulas with the asymptotic formulas (49) and (50), we see that they indeed coincide up to . Figure 1 in the main text illustrates the exact and the second-order bias formula (scaled by ) for .

Appendix D Exact QR and IVQR algorithms

First consider a linear programming (LP) implementation of the QR regression (2) (Koenker, 2005, Section 6.2):

Here is an vector of ones. This formulation allows us to apply LP solvers like Gurobi to obtain the exact minimum in (2).

Next consider the exact estimator for the IVQR case,

The underlying optimization problem can be equivalently reformulated as a mixed integer linear program (MILP) with special ordered set (SOS) constraints,

where is an vector of realizations of instrument . All constraints except the last one coincide with the ones derived by Chen and Lee (2018) in Appendix C.1 (we also omit the redundant constraint , which is implied by the two constraints). The last constraint ensures that the objective function is the norm of the just identifying moment conditions.

Remark 3.

We also considered the “big-M” formulation while performing the Monte Carlo analyses. The big-M formulation has certain computational advantages, although the arbitrary choice of tuning parameters may result in sub-optimal solutions. This problem is more prominent for tail quantiles. Since the big-M formulation does not guarantee exact solutions, consistent with our theory, the choice of tuning parameters may affect the asymptotic bias. We prefer the above SOS formulation because it does not depend on tuning parameters as the big-M MILP/MIQP formulations in Chen and Lee (2018) and Zhu (2019).999These papers pick the value of the tuning parameter as a solution to a linear program that in turn depends on the choice of an arbitrary box around a linear IV estimate. This is problematic if there is a lot of heterogeneity in the coefficients across quantiles. Moreover, in linear models with heavy tailed residuals, the linear IV estimator is not consistent. ∎

Appendix E Stochastic expansion of 1-step corrected IVQR estimators

In the main text, we focus in classical QR and exact IVQR estimators. As shown in the following corollary, the results in Theorem 1 can be used to obtain a uniform BK expansion for general IVQR estimators after a feasible 1-step correction.

Corollary 1.

Proof.

By Lemma A.2 applied to , uniformly in ,

Under the maintained assumptions, Lemma 1 implies

By Lemma A.1, is bounded uniformly over . Then, by Assumption 1.2 and continuity of the minimal eigenvalue function, the eigenvalues of are bounded away from zero on . Therefore, the derivative of the inverse matrix function, , is uniformly bounded over for . Hence, by the element-wise Taylor expansion of at ,

By Lemma A.3,

| (51) |

By Donsker’s theorem,

so, by the triangular inequality and (51),

Then

which concludes the proof. ∎

Appendix F Additional figures

Notes: The panels display the bias (multiplied by ) of the intercept and the slope for classical QR without bias correction (blue dots), QR with feasible bias correction using the baseline bandwidth choice (gold crosses), QR with feasible bias correction using deviation in one bandwidth at a time (up-pointing triangles for , down-pointing triangles for ), and QR with infeasible bias correction (gold dashed line) for DGP1. In Panel (a), we vary , in Panel (b), we vary , and in Panel (c), we vary . All results are based on 40,000 simulation repetitions.

Notes: Panel (a) compares the MAD for classical QR without (blue) and with (gold) bias correction. Panel (b) compares the MAD for exact IVQR (implemented via the MILP formulation in Appendix D) without (blue) and with (gold) bias correction. The results for both DGPs are based on 40,000 simulation repetitions.

Notes: The panels display the coverage probability of the confidence intervals for the intercept and the slope for classical QR without bias correction (blue dots) and QR with the best feasible bias correction (gold crosses) for DGP1 with . All results are based on 40,000 simulation repetitions.

Notes: The panels display the coverage probability of the confidence intervals for the intercept and the slope for classical QR without bias correction (blue dots) and QR with the best feasible bias correction (gold crosses) for DGP2–DGP4 with . All results are based on 40,000 simulation repetitions.