Nonparametric Estimation of Functional Dynamic Factor Model

Israel Martínez-Hernández111

Mathematics and Statistics,

Lancaster University, Lancaster,

United Kingdom

E-mail: i.martinezhernandez@lancaster.ac.uk∗, Jesús Gonzalo222

Universidad Carlos III de Madrid, Spain,

and Graciela González-Farías333

Centro de Investigación en Matemáticas, A.C. CIMAT, Mexico

This research was partially supported by 1) CONACYT, Mexico, scholarship as visiting research student, 2) CONACYT, Mexico, CB-2015-01-252996 and 3) Centro de Investigación en Matemáticas (CIMAT).

Abstract

Data can be assumed to be continuous functions defined on an infinite-dimensional space for many phenomena. However, the infinite-dimensional data might be driven by a small number of latent variables. Hence, factor models are relevant for functional data. In this paper, we study functional factor models for time-dependent functional data. We propose nonparametric estimators under stationary and nonstationary processes. We obtain estimators that consider the time-dependence property. Specifically, we use the information contained in the covariances at different lags. We show that the proposed estimators are consistent. Through Monte Carlo simulations, we find that our methodology outperforms estimators based on functional principal components. We also apply our methodology to monthly yield curves. In general, the suitable integration of time-dependent information improves the estimation of the latent factors.

Some key words: Functional cointegration; Functional dynamic factor model; Functional time series; functional process; Long-run covariance operator.

Short title: Functional Dynamic Factor Model

1 Introduction

Functional data analysis (FDA) has attracted interest in recent years in different areas in statistics, where data can be collected almost continuously, e.g., in finance, economics, climatology, medicine, and engineering. FDA is a new methodology and an interesting approach to deal with large-scale, high-dimensional and high-frequency data. Unlike the multivariate approach, which depends on the points at which data are taken, FDA can extract additional information about the continuous underlying stochastic process since each curve is treated as a unit (Ramsay and Silverman, 2005). In many real applications, functional data, , are time-dependent, e.g., yield curves (Diebold and Li, 2006), mortality curves (Hyndman and Ullah, 2007), electricity consumption curves (Liebl, 2013), and intraday price curves (Kokoszka et al., 2015). When the functional data are time-dependent, they are called functional time series (see Horváth and Kokoszka, 2012, for a survey on functional time series). A way to construct a functional time series is to partition a continuous-time stochastic process into consecutive segments of length , that is, , where depends on the dataset application (daily, monthly, annual, etc.). Some functional time series are naturally modeled by using factor models, e.g., yield curves (Diebold and Li, 2006), electricity consumption curves (Liebl, 2013), and intraday price curves (Kokoszka et al., 2015). In this paper, we consider factor models for functional time series. We propose a new methodology to obtain an estimator of the functional dynamic factor (FDF) model.

Factor models represent a large number of dependent variables from a dataset in terms of a small number of latent variables. When the data are time-dependent, attention is focused on dynamic factor models. A dynamic factor model can explain a large fraction of the variance in many macroeconomic series (Giannone et al., 2005), and it is also consistent with broad applications to various phenomena; see Stock and Watson (1988), Bai and Ng (2002), Bai (2003), Diebold and Li (2006), Friguet et al. (2009), Härdle and Trück (2010) and Desai and Storey (2012). Dynamic factor models have been studied for multivariate time series in both stationary and nonstationary cases. Bai and Ng (2002), Bai (2003), Forni et al. (2005), and Lam et al. (2011) considered the stationary case. Stock and Watson (1988) studied factors in a cointegrated time series, Gonzalo and Granger (1995) proposed a method to estimate the factors in a cointegrated time series, Bai and Ng (2004) studied the factor structure of large dimensional panels in nonstationarity data, and Peña and Poncela (2006) presented a procedure to obtain dynamic factor models for a vector of time series. Here, we also study both cases of functional time series, stationary and nonstationary.

Specifically, we assumed that the functional time series is driven by latent factor loadings curves and latent factor time series , i.e., . This FDF model was studied previously by other authors. Hays et al. (2012) assumed that , with , is observed in a sample of discrete points, , and that the factors, , follow an AR model. In that paper, the factor loading and the components of the AR model are estimated jointly via maximum likelihood and using the EM algorithm. However, the EM algorithm becomes increasingly complicated when the sample size grows or when the number of point observations of each curve grows. Here, we assume that is given in functional form instead of discrete observations of each, and we propose a nonparametric estimator for the latent variables and . Liebl (2013) used the FDF model to forecast electricity spot prices, where the factor loading curves, , are defined as eigenfunctions of the covariance operator of , and the factor process is defined as the corresponding score. One disadvantage is that functional principal component analysis (PCA) operates in a static way. That is, if the functional data are time-dependent, then the dynamics are not accurately represented by the principal components, as noted in Hörmann et al. (2015). In Jungbacker et al. (2014), the factor loading curves are proposed as cubic splines and rely on hypothesis tests to select the number of knots and their locations. This is inefficient when the sample size increases. Kokoszka et al. (2015) assumed that the factor loading curves are known and depend on time. Then, they propose the use of least square estimators to obtain the factors.

In this paper, we propose a nonparametric estimator of the FDF model, considering time-dependent functional data that are either stationary or nonstationary. The factor processes are assumed to be scalar processes, and they described the dynamics of the data (by dynamics, we mean the dependence structure over time). The factor loadings are assumed to be continuous functions. The subspace generated by the proposed estimators for the factor loading curves represents the dynamics of the functional time series. Thus, our interest is in estimating the trajectory of the factor processes without assuming any model in such a way that each trajectory accurately represents the dependency over time. To take into account the temporal dependency, we consider a specific long-run covariance operator.

The remainder of our paper is organized as follows: In Section 2, we introduce mathematical concepts for functional time series. In Section 3, we describe the methodology to obtain the estimators in both cases: stationary and nonstationary models. Additionally, we present algorithms and examples to illustrate the methodology. In Section 4, we study the properties and consistency of the proposed estimators. In Section 5, we evaluate the performance of the proposed estimators under different simulation settings, comparing our results with functional PCA estimators. In Section 7, we apply our methodology to the yield curves. Finally, Section 8 presents a discussion. The proofs are provided in the Appendix.

2 Preliminaries

To describe our methodology, we first introduce some concepts for functional time series. Let be the separable real Hilbert space of square integrable functions defined on compact subset , with inner product , and the corresponding norm denoted by . A functional random variable is defined as a random variable in , i.e., . Let be the set of random variables in with finite moments of order . The expected value of is defined as a unique element of , denoted by , such that for all . In the rest of the paper, we write instead of to refer to the expected value of .

A functional time series is a sequence of functional random variables in . The covariance operator at lag of is defined by for all . This covariance operator can be written as where is called the kernel of . A functional time series is said to be stationary if (i) and (ii) for all , , and . In this case, we use the notation instead of . If is a stationary functional time series with and for all , then it is called functional white noise and strong functional white noise if it is a sequence of i.i.d. functional random variables. In the rest of the paper, we refer to strong functional white noise as an i.i.d. sequence in . The reader can consult Bosq (2000) and Horváth and Kokoszka (2012) for more details on functional time series.

Let be a stationary functional time series, and the long-run covariance operator of is defined as

| (1) |

where the corresponding kernel is , and . We should note that the assumption of stationarity on does not guarantee the existence of . For that, we need an additional weak dependence condition stated in Section 4.

Let be the set of all continuous linear operators from to , with an operator norm denoted by . Let ; an eigenfunction of is defined as a nonzero element of such that where is a scalar number and is the associated eigenvalue.

Let be an i.i.d. sequence in , and let . A functional linear process with innovations is defined as

If the functional linear process is stationary, and if its covariance long-run covariance operator exists, then this long-run covariance operator can be written as (see Appendix)

| (2) |

where is the covariance operator of , and is the adjoint operator of .

Now, we introduce the functional process. We use the approach proposed by Beare et al. (2017), where the notion of cointegration for multivariate time series is extended to an inifinite-dimensional space. Let be a functional time series such that the first difference admits the representation , where is an i.i.d. sequence in , and coefficient operators satisfying . Then, can be written as , where , and is a stationary functional time series. The functional time series is called an functional process if and only if the long-run covariance operator of is different from zero.

3 Methodology

In this paper, we assume that the functional time series are given in the functional form. In a real application, functional data are observed on a grid of points, and thus, the continuous curve should be estimated (see Ramsay and Silverman, 2005, Chapter 3-7).

3.1 Model setting

Assume that we observe functional data . We assume that the functional data follow the model

| (3) |

where , , are factor loading curves, are scalar factor time series, is the number of factors, and is a sequence of centered, independent and identically distributed innovations in with covariance operator . We refer to model as the functional dynamic factor model or FDF model. The factors are assumed to be time-dependent, and then is time-dependent. The factor processes drive the dynamics of the functional data . Factors and factor loadings are latent functions and latent random variables, respectively.

For model identifiability, we assume orthonormality of the factor loading curves, that is,

| (4) |

for , where takes the value if and zero otherwise. In some scenarios, the factor processes can be known, and then, condition (4) can be omitted (Kokoszka et al., 2018).

Since factors and factor loadings are unobserved, and are not uniquely determined in model (3), even with the constraint (4). However, the linear space generated by the factor loadings, called the factor loading space, is uniquely defined. Thus, any orthonormal rotation of the orthonormal basis system can be a solution to model (3) as well. Therefore, our goal is to estimate . To do so, we assume the following conditions.

Assumption 1.

The functional white noise is uncorrelated with the functional process , that is, , .

Assumption 2.

There exists such that , for some .

Assumptions 1 is the usual conditions assumed for the FDF model. Assumption 2 requires time-dependent functional data and ensures not being an empty set. To motivate our methodology, let us assume that the functional data are stationary and follow model 3 (we will use similar ideas for the nonstationary case in Section 3.3). Thus, under Assumption 1, the covariance operator of satisfies

where denotes the tensor product. Therefore, for any , with . Moreover, if and is invertible, then . Hence, is the orthogonal complement of the linear space spanned by the eigenfunctions of (or ) corresponding to the zero eigenvalues, with . Thus, our methodology uses the operator , and we consider the summation over all possible lags , that is,

| (5) |

where is the long-run covariance of defined in (1). We notice that, under Assumption 2, .

We observe that for any as well. Consequently, we propose to estimate the space using the eigenfunctions of the operator corresponding to nonzero eigenvalues. Additionally, these eigenfunctions are defined as estimators of the factor loadings , .

In general, is unbounded (Bosq, 2000; Martínez-Hernández et al., 2019). The method typically employed to address this problem is to truncate the spectral representation of and then compute the inverse from this representation. We adopt this method, and we describe it in Section 3.2.

Remark 1.

The consideration of the term in (5) is equivalent to assuming that the data have identity as the covariance operator. The latter case requires transforming the data to . Thus, is the covariance operator at lag of the transformed data.

3.2 Estimation for stationary FDF model

Without loss of generality, we assume that . To estimate , we compute the eigenfunctions of , where is the estimator of . To obtain , we use a smooth periodogram-type estimator (Rice and Shang, 2017). Let be the kernel estimator of defined as

Now, we define as

where is a continuous, symmetric weight function and satisfies , if for some . In this paper, we use , where is a bandwidth parameter. To obtain a consistent estimator, the bandwidth must satisfy as and (Horváth et al., 2013). However, in practice, the selection of should be done carefully, since this can affect the performance of the estimator in finite samples. Here, we select similarly as described in Rice and Shang (2017), that is, minimizing the mean-squared error , where denotes the usual norm in . We use the notation to denote with the optimal value of the bandwidth .

Then, the estimator of the operator is defined by , . To obtain a bounded estimator of , we only consider the first eigenfunctions corresponding to the largest eigenvalues of . Thus, the inverse is approximated by , where , , are such that . We select the parameter using the scree plot.

Finally, we obtain an estimator of as , and consecutively, we estimate the eigenfunctions of corresponding to the first largest nonzero eigenvalues , with a positive number. That is, for each , satisfies

As mentioned above, we have that is the number of nonzero eigenvalues of . In practice, the number of eigenfunctions of with nonzero eigenvalues is not exactly , since the zero-eigenvalues of are unlikely to be zero exactly. Here, we estimate the number of factors similarly as in Lam and Yao (2012), using a ratio-based estimator. Explicitly, we define as

| (6) |

where should be large enough that . Although we do not study the theoretical properties of , thorough empirical investigations suggest it works well in practice.

Once we have estimated the eigenfunctions of and the number of factors, we define , and , . The estimated trajectories of the factor processes are obtained as

Algorithm 1 presents a summary of the steps to obtain the estimators of model (3) under the stationary assumption.

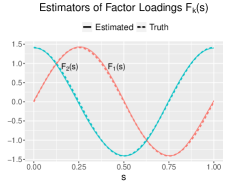

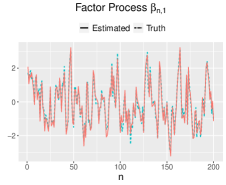

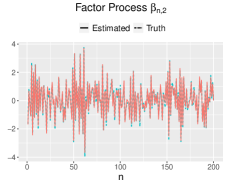

Example 3.1.

We simulate from an model with and sample size . The factors are AR processes with coefficients and . The factor loadings are defined by and with . Figure 1 shows the estimators obtained from Algorithm 1. The left panel shows the factor loadings and their corresponding estimators, while the center and right panels show the estimated trajectory for the factors. We observe that is close to the original factor loadings and that the estimated trajectories of the factor processes successfully approximately the original factor processes. Thus, the proposed estimators have good performance in this example. A more exhaustive simulation study is performed in Section 5.

3.3 Estimation for the nonstationary FDF model

In real data applications, the factor processes can be nonstationary. Here, we assume that at least one of the factor processes , , is an scalar process. Let be the number of factor processes that are processes. We consider two cases: (i) all factor processes are processes, i.e., , and (ii) there are factor processes, with , and the remaining factor processes are stationary processes. Thus, the factor loading space can be written as , where is the linear space generated by the stationary factor processes and is the linear space generated by the nonstationary factor processes. We have that if , then the scalar time series is stationary, and if , the scalar time series is nonstationary. Case (ii) is related to the concept of cointegrating in a Hilbert space (Beare et al., 2017). Here, we describe estimators for and .

Let be the operator defined in (5) for the functional process . In the following, we describe the two cases for the factor processes.

Case (i): In this case, , and is a stationary FDF model. We estimate the space as the linear space generated by the eigenfunctions of the operator , where is estimated as described in Section 3.2 using instead of . The number of factors is estimated as in (6) with the corresponding eigenvalues of . Finally, we define , , where are the eigenfunctions of . This approach guarantees that is an process for (Proposition 4.3).

Case (ii): We have that with . First, we estimate the space ; then, we subtract the estimated space from the entire space . Then, we estimate . We propose to estimate as the linear space generated by the eigenfunctions of , and then we define , where is the eigenfunction of , for . Here, we obtain using criteria (6), with being eigenvalues of . Then, we obtain the estimated trajectories of the factor processes as , for . Given , we estimate as follows. We define a new functional time series as

| (7) |

Let be the corresponding operator defined in (5) for the functional process . The functional process should be a stationary functional process. Thus, we estimate similarly as in Section 3.2, with as in (6) using the corresponding eigenvalues of . Let be the eigenfunctions of corresponding to the -th largest eigenvalues. Then, we define , with , as the estimators of the factor loadings corresponding to the stationary dynamic and , for , as the estimated trajectories of the factor processes.

In real applications, we do not know whether or . To overcome this problem, we propose to apply a test for independence for the functional process , such as a test proposed in Horváth et al. (2013). If the independency hypothesis is not rejected, then we conclude that . Otherwise, , and we can proceed to estimate the corresponding stationary loading space .

In Algorithm 2, we present a summary of the steps to obtain the estimators of model (3) with nonstationary factor processes and stationary factor processes.

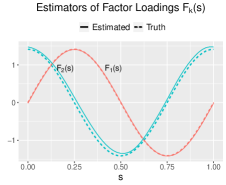

Example 3.2.

We simulate from the FDF model with , , and sample size , where , , , and , with . Figure 2 shows the estimators obtained from Algorithm 2. The left panel shows the factor loadings and their corresponding estimators, while the center and the right panels show the trajectory estimated for the factors. Similar to Example 3.1, we observe that the proposed estimators have good performance in this nonstationary example. A more exhaustive simulation study is performed in Section 5.

Remark 2.

As we mentioned before, the estimators of the FDF model are not unique, but the subspace generated by the factor loadings is unique. Here, we defined as the eigenfunctions of the corresponding long-run covariance operator. However, users can choose an appropriate orthonormal rotation to obtain factors that allow a meaningful-interpretation. For example, one possible rotation is the well-known VARIMAX rotation.

The dynamic modeling for the FDF model is attained by modeling the factor processes and using the relationship .

In general, the operator defined in (5) represents the loading space and the dynamic of the functional time series. Moreover, if the functional time series is an functional process, then the operator classifies the space of common trends and the cointegrating space. We conclude that the dynamics of the FDF model over time are accurately described by using the space generated by this operator.

4 Estimation properties

In this section, we study the properties of the estimators described in Section 3. For this, we assume that has a functional linear representation in . Without loss of generality, we assume that the curves are defined on the unit interval and .

Assumption 3.

The functional time series has a linear representation , with , and .

Assumption 4.

and where , and for each , is an independent copy of .

Assumption 3 does not impose any restrictions on the model 3. For example, if the factors processes are (scalar) linear processes, with an i.i.d. sequence, then . This latter expression can be rewritten as , with and . In this case, the condition is equivalent to . This latter condition is a common assumption on scalar time series in order to obtain basic results.

Proposition 4.1.

Proof: See Appendix.

Assumption 3 implies that is a stationary functional time series. Thus, Proposition 4.1 corresponds to the stationary case of model (3).

As we noted above, the factors and factor loadings are not uniquely determined in the FDF model. However, the factor loading space is uniquely determined. We only study the theoretical properties of the factor loading space under the assumption that is known. Here, we say that a subspace converges to a subspace if , where and are the orthonormal projectors on and , respectively, and an operator norm. We use the notation to indicate this convergence of a subspace.

Corollary 4.2.

To study the nonstationary case, we assume that admits a functional linear representation as well.

Assumption 5.

Assumption 5 does not impose any restrictions on the model (3). If any factor process is an process, then the functional time series that follows model (3) can always be written as (8), with compact and self-adjoint operators. The condition for some guarantees that is not a functional white noise. Consequently, admits a solution of the form , where is a stationary functional time series, is an i.i.d. sequence, and .

From Proposition 4.1, we have that is a consistent estimator of .

Proposition 4.3.

Proof: See Appendix.

Proposition 4.3 shows that the dynamics of the factors are recovered in the subspace generated by nonzero elements of .

Corollary 4.4.

Let be invertible, and and known. If the assumptions in Proposition 4.3 hold, then and .

Corollary 4.5.

5 Simulation study

We study the performance of our proposed estimators for the FDF model. We compare our results with estimators obtained from functional PCA. To obtain the functional PCA estimators, we replace with in Algorithm 1, where denotes the th eigenfunction of corresponding to the th largest eigenvalue (Liebl, 2013). Similarly, in Algorithm 2, we consider the covariance operators at lag zero of and instead of and . The PCA estimators are known to perform well when observations are uncorrelated.

5.1 Simulation setting

We simulate from the FDF model with four different models defined as follows:

-

1.

Model 1: , , and .

-

2.

Model 2: , , , , and .

-

3.

Model 3: , , , and .

-

4.

Model 4: , , , , , and .

The processes are scalar white noises. In all cases, the functional white noise in model 3 is simulated as , where is a Brownian motion in . Models 1 and 2 represent stationary FDF models, while Models 3 and 4 represent nonstationary FDF models.

We evaluate the performance by computing the Integrated Squared Error (ISE) value defined as:

We consider sample sizes , and . We simulate replications for each model. For each replication, we estimate the factor loadings and factor processes. Then, we compute the error value , both for our proposed estimators and for PCA estimators.

Additionally, we report the estimated factor number for each simulation using (6).

5.2 Simulation results

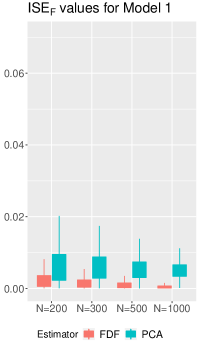

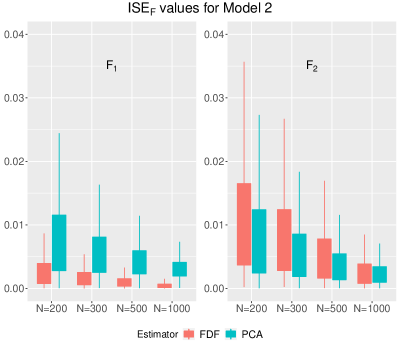

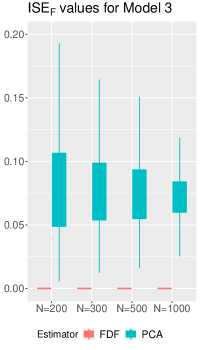

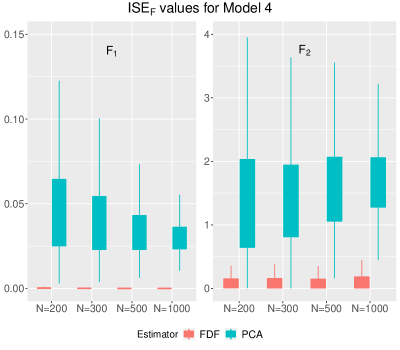

We denote by FDF the simulation results when considering our nonparametric estimators. First, we describe the results for values. In doing so, we assume that the true number of factors is known. Figure 3 shows boxplots of the results. Each plot presents the values for a specific with different sample sizes. For Models 1 and 3, we have only one loading factor, and for Models 2 and 4, we have two loading factors, and .

For Model 1 (Figure 3 top left), we observe that our proposed estimator is highly accurate and presents lower error values than the PCA estimator. These error values decrease when the sample size increases. For Model 2, we observe that for the first loading factor (Figure 3 top center), the results are similar to the results of Model 1. Our method outperforms the PCA estimator. For (Figure 3 top right), we see that the PCA method performs as well as our method. Thus, we conclude that, in general, our method outperforms the PCA estimator for the stationary Models 1 and 2.

Now, we analyze the nonstationary models (Models 3 and 4). We observe that in all cases, our method has the lowest error values. The values for our method remain as accurate as in the stationary cases. However, the values for the PCA method become significantly larger. We conclude that our proposed method performs well in all simulated cases and outperforms the PCA method.

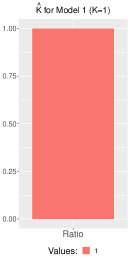

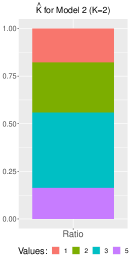

Finally, we show the results corresponding to the estimation of the number of factors. For each replication, we estimate the number of factors using (6). We only present the results from sample size , since the results from the sample sizes and are similar. Figure 4 shows the estimated values over the 1000 replications. Each bar uses colors to represent the proportion of replications.

For Model 1, we observe that with the ratio method, we obtain for all replications. For this Model 1, we conclude that the ratio method correctly estimates the value of . For Model 2, takes values in , resulting in and with a large proportion. For Model 3, the ratio method successfully estimates the value of . For Model 4, we need to estimate and , where is the number of nonstationary factor processes and is the number of stationary factor processes. In this case, we observe that the ratio method provides the correct values of and .

In general, the ratio method correctly estimates the number of factors with the exception of Model 2.

We conclude that our proposed methodology performs well and is superior to the PCA method under time dependence.

6 Data application

7 Data application

We fit the FDF model with our proposed nonparametric estimators to analyze the Federal Reserve interest rates. Then, we study the estimated factor loadings and the trajectories of the factor processes.

7.1 Yield curve

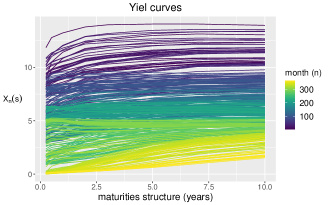

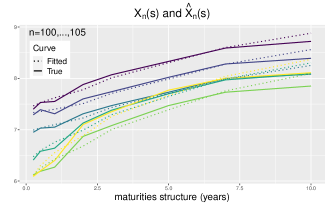

The interest rate data from the Federal Reserve are available in the R package YieldCurve. The dataset represents monthly yield data from June to May at different maturities: months, months, year, years, years, years, years and years (see Figure 5). Yield curves are important in economics and finance and can help to determine the current and future position of the economy. The Nelson-Siegel parametrization is commonly used to describe yield curves (see Nelson and Siegel, 1987; Diebold and Li, 2006; Koopman et al., 2010). Our proposal is a nonparametric estimator and can be considered as alternative modeling to the Nelson-Siegel modeling. To justify the functional approach, we assume that the dataset is continuous on maturities. That is, a curve represents interest rates in month with time to maturity . To estimate the continuous curves, we fit cubic B-spline basis functions for each monthly observation, i.e., , where is the B-spline basis function, with .

Yield curves were analyzed with a nonparametric approach and with a functional approach. Hays et al. (2012) used a functional approach combined with an EM algorithm to jointly estimate the factor loading curves and the factors. Their approach is difficult to apply if more data are observed at different maturities and almost impossible to apply if the functional data are observed in a dense set. In contrast, our estimators are easy to implement and can be applied to either dense or sparse observations and for stationary and nonstationary functional time series.

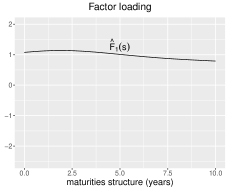

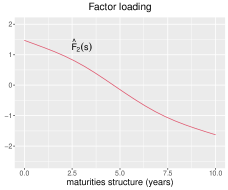

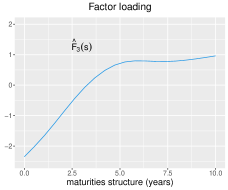

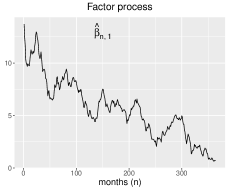

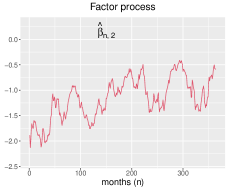

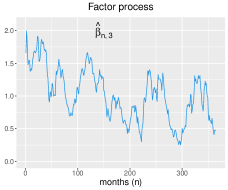

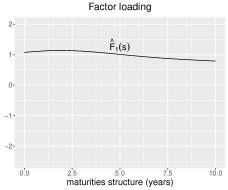

We are interested in studying the factor loading curves and the factor processes that drive the interest rates at different maturities by taking into account the dependence structure of the functional time series. To infer the stationarity of the functional time series, we apply a test proposed by Horváth et al. (2014). The -value of the test, with basis functions, is equal to , and the smaller the -value, the more evidence there is against stationarity. Therefore, we follow Algorithm 2 with three factors, and .

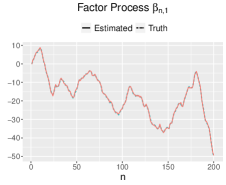

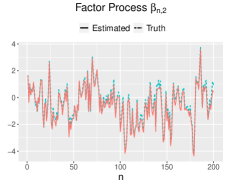

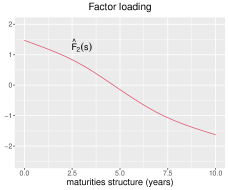

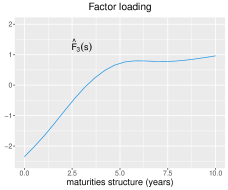

Figure 6 shows the results. In the first row, we plot the estimator of factor loading curves, and , and in the second row, we plot the trajectories of the factor processes estimated, . Since the factor loading curves are time-invariant, they represent the common properties of the yield curves, while the factor processes represent the dynamics over time. Our estimators agree with the level, slope and curvature functions of the Nelson-Siegel parameterization described by Diebold and Li (2006), which is interesting since we do not assume any specific model (see Appendix for a plot of Nelson-Siegel curves). Therefore, the first factor loading curve is the level, and it is associated with the long-term factor; these dynamics are described by . The factor loading is the slope, and it is associated with the short-term factor that is represented by the process . Finally, the factor loading is the curvature that corresponds to the medium-term factor, and the factor describes such dynamics.

Figure 5 (right) shows six consecutive yield curves from the dataset with the corresponding six yield curves obtained from the FDF model with the estimators, that is, . These six curves correspond to the months of October, November, December, January, February, and March of and , respectively. We observe that the yield curves seem to be accurately represented by the FDF model.

8 Discussion

We propose new nonparametric estimators of the functional dynamic factor model, taking into account the time dependence of the functional data. We use the long-run covariance operator to define a subspace of the continuous functions where the dynamics of the functional data are properly described by the factor processes. We have showed that the proposed estimators of the factor loading curves represent a subspace where factor processes describe the dependence of the functional time series, under both the stationarity and nonstationarity assumptions. We compared our proposed estimators with eigenfunctions of the covariance operator. From the simulation study, we conclude that our proposed estimators have better performance than PCA-based estimators.

From a mathematical point of view, factor loading curves can be considered part of basis functions for the Hilbert space. In principle, factor loading curves could be, for example, eigenfunctions, but eigenvalues do not take into account the time-dependent structure and therefore do not represent the dynamics over time. The ideas developed here can be extended to multivariate functional time series for studying the common factors among the different functional time series and the factors of each functional time series that are not shared. The extended model might be relevant in many applications, such as multi-economy yield curves.

References

- Bai (2003) Bai, J. (2003). Inferential theory for factor models of large dimensions. Econometrica, 71, 135–171.

- Bai and Ng (2002) Bai, J. and Ng, S. (2002). Determining the Number of Factors in Approximate Factor Models. Econometrica, 70, 191–221.

- Bai and Ng (2004) Bai, J. and Ng, S. (2004). A PANIC attack on unit roots and cointegration. Econometrica, 72, 1127–1177.

- Beare et al. (2017) Beare, B. K., Seo, J., and Seo, W.-K. (2017). Cointegrated linear processes in Hilbert space. Journal of Time Series Analysis, 38, 1010–1027.

- Bosq (2000) Bosq, D. (2000). Linear processes in function spaces, volume 149 of Lecture Notes in Statistics. Springer-Verlag, New York. Theory and applications.

- Desai and Storey (2012) Desai, K. H. and Storey, J. D. (2012). Cross-dimensional inference of dependent high-dimensional data. Journal of the American Statistical Association, 107, 135–151.

- Diebold and Li (2006) Diebold, F. X. and Li, C. (2006). Forecasting the term structure of government bond yields. Journal of Econometrics, 130, 337–364.

- Forni et al. (2005) Forni, M., Hallin, M., Lippi, M., and Reichlin, L. (2005). The generalized dynamic factor model: One-sided estimation and forecasting. Journal of the American Statistical Association, 100, 830–840.

- Friguet et al. (2009) Friguet, C., Kloareg, M., and Causeur, D. (2009). A factor model approach to multiple testing under dependence. Journal of the American Statistical Association, 104, 1406–1415.

- Giannone et al. (2005) Giannone, D., Reichlin, L., and Sala, L. (2005). Monetary policy in real time. In NBER Macroeconomics Annual 2004, Volume 19, pages 161–224. National Bureau of Economic Research, Inc.

- Gonzalo and Granger (1995) Gonzalo, J. and Granger, C. (1995). Estimation of common long-memory components in cointegrated systems. Journal of Business & Economic Statistics, 13, 27–35.

- Härdle and Trück (2010) Härdle, W. K. and Trück, S. (2010). The dynamics of hourly electricity prices. SFB 649 Discussion Paper 2010-013 .

- Hays et al. (2012) Hays, S., Shen, H., and Huang, J. Z. (2012). Functional dynamic factor models with application to yield curve forecasting. The Annals of Applied Statistics, 6, 870–894.

- Hörmann et al. (2015) Hörmann, S., Kidziński, L. u., and Hallin, M. (2015). Dynamic functional principal components. Journal of the Royal Statistical Society: Series B Statistical Methodology, 77, 319–348.

- Horváth et al. (2013) Horváth, L., Hušková, M., and Rice, G. (2013). Test of independence for functional data. Journal of Multivariate Analysis, 117, 100–119.

- Horváth and Kokoszka (2012) Horváth, L. and Kokoszka, P. (2012). Inference for functional data with applications. Springer Series in Statistics. Springer, New York.

- Horváth et al. (2013) Horváth, L., Kokoszka, P., and Reeder, R. (2013). Estimation of the mean of functional time series and a two-sample problem. Journal of the Royal Statistical Society: Series B Statistical Methodology, 75, 103–122.

- Horváth et al. (2014) Horváth, L., Kokoszka, P., and Rice, G. (2014). Testing stationarity of functional time series. Journal of Econometrics, 179, 66–82.

- Hyndman and Ullah (2007) Hyndman, R. J. and Ullah, M. S. (2007). Robust forecasting of mortality and fertility rates: a functional data approach. Computational Statistics & Data Analysis, 51, 4942–4956.

- Jungbacker et al. (2014) Jungbacker, B., Koopman, S. J., and van der Wel, M. (2014). Smooth dynamic factor analysis with application to the US term structure of interest rates. Journal of Applied Econometrics, 29, 65–90.

- Kokoszka et al. (2018) Kokoszka, P., Miao, H., Reimherr, M., and Taoufik, B. (2018). Dynamic functional regression with application to the cross-section of returns. Journal of Financial Econometrics, 16, 461–485.

- Kokoszka et al. (2015) Kokoszka, P., Miao, H., and Zhang, X. (2015). Functional dynamic factor model for intraday price curves. Journal of Financial Econometrics, 13, 456–477.

- Koopman et al. (2010) Koopman, S. J., Mallee, M. I. P., and der Wel, M. V. (2010). Analyzing the term structure of interest rates using the dynamic Nelson-Siegel model with time-varying parameters. Journal of Business & Economic Statistics, 28, 329–343.

- Lam and Yao (2012) Lam, C. and Yao, Q. (2012). Factor modeling for high-dimensional time series: inference for the number of factors. The Annals of Statistics, 40, 694–726.

- Lam et al. (2011) Lam, C., Yao, Q., and Bathia, N. (2011). Estimation of latent factors for high-dimensional time series. Biometrika, 98, 901–918.

- Liebl (2013) Liebl, D. (2013). Modeling and forecasting electricity spot prices: a functional data perspective. The Annals of Applied Statistics, 7, 1562–1592.

- Martínez-Hernández et al. (2019) Martínez-Hernández, I., Genton, M. G., and González-Farías, G. (2019). Robust depth-based estimation of the functional autoregressive model. Computational Statistics & Data Analysis, 131, 66–79.

- Nelson and Siegel (1987) Nelson, C. and Siegel, A. F. (1987). Parsimonious modeling of yield curves. The Journal of Business, 60, 473–89.

- Peña and Poncela (2006) Peña, D. and Poncela, P. (2006). Nonstationary dynamic factor analysis. Journal of Statistical Planning and Inference, 136, 1237–1257.

- Ramsay and Silverman (2005) Ramsay, J. O. and Silverman, B. W. (2005). Functional data analysis. Springer Series in Statistics. Springer, New York, second edition.

- Rice and Shang (2017) Rice, G. and Shang, H. L. (2017). A plug-in bandwidth selection procedure for long-run covariance estimation with stationary functional time series. Journal of Time Series Analysis, 38, 591–609.

- Stock and Watson (1988) Stock, J. and Watson, M. (1988). Testing for common trends. Journal of the American Statistical Association, 83, 1097–1107.

Appendix A. Proofs

Derivation of equation (2): Let be a stationary functional linear process, with . Let . First, we observe that for all , the covariance operator at lag holds

We note that . Since are i.i.d., we have that if . Thus, . Substituting this into the above expression, we have

Now, we compute the long-run covariance operator . For all , we have

since for all , and changing the variable to , we obtain that . That is, . This implies that the long-run covariance operator is .

All operators involved in the proof are integral operators, i.e., each operator is represented by a kernel function in . Thus, the operator norm is defined as the usual norm in , e.g., .

Proof of Proposition 4.1: Let us first observe that under Assumptions 3 and 4, the estimator is a consistent estimator of . Explicitly, we have that This is because with Assumptions 3 and 4 the functional time series is an -approximable (and hence sttaionary). The reader is referred to Horváth et al. (2013) for the details of this proof.

Similarly, we have that That is, . Thus,

Therefore, .

We now turn to the operator. We observe that is an integral operator with kernel .

For , we use the notation . Then, we observe that

with being the kernel with the true values and . Thus,

The first component on the right-hand side of the above inequality is bounded by . If is invertible or if is finite dimensional, then we have that is bounded, and as a consequence . Then,

Similarly, for the second component we have that

with . Therefore, we conclude that

that is, .

In the case where is infinite dimension, one can obtain similar result following similar ideas as in (Bosq, 2000, Ch. 8.3). We omit the proof of this case.

Proof of Corollary 4.2: Let and be the orthonormal projectors on and , respectively. Then, for any with , we have that

with , , , and , . Since we obtain with . Thus, , and then .

Proof of Proposition 4.3: We need only consider the case in which is . We have that the long-run covariance operator of the functional process is , where , with compact and self-adjoint operators. Thus, under Assumption 5, can be written as

where is a stationary functional time series. Let be an eigenfunction of ; then, . From this, we can show that and (see Beare et al. (2017) for more details).

Proof of Corollary 4.5: For , an eigenfunction of , we have that

where , , and . That is, has a random walk component since . Thus, for each eigenfunction of , the process is an process, and replacing with their corresponding estimator , we obtain that is also an process. In contrast, if , then is stationary. This completes the proof.

Appendix B. Comparison of factors

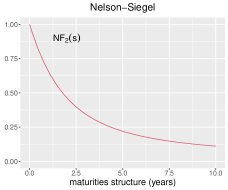

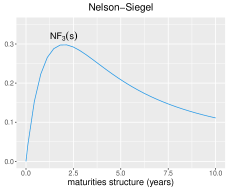

Here we present the Nelson-Siegel curves corresponding to the three factors (see, e.g., Diebold and Li, 2006). Also, we present our estimators of the Yield curve data (Section 7).

The Nelson-Siegel curves are defined as

Figure 7 presents the three Nelson-Siegel curves (second row) and our estimators (first row). In the Nelson-Siegel curves, we fix the parameter .