Non-Equilibrium Skewness, Market Crises, and Option Pricing:

Non-Linear Langevin Model of Markets with Supersymmetry

Igor Halperin111Fidelity Investments. E-mail: igor.halperin@fmr.com. Opinions expressed here are author’s own, and do not represent views of his employer. A standard disclaimer applies. E-mail for communications on the paper: ighalp@gmail.com

First version: November 8, 2020

This version:

Abstract:

This paper presents a tractable model of non-linear dynamics of market returns using a Langevin approach. Due to non-linearity of an interaction potential, the model admits regimes of both small and large return fluctuations. Langevin dynamics are mapped onto an equivalent quantum mechanical (QM) system. Borrowing ideas from supersymmetric quantum mechanics (SUSY QM), a parameterized ground state wave function (WF) of this QM system is used as a direct input to the model, which also fixes a non-linear Langevin potential. Using a two-component Gaussian mixture as a ground state WF with an asymmetric double well potential produces a tractable low-parametric model with interpretable parameters, referred to as the NES (Non-Equilibrium Skew) model. Supersymmetry (SUSY) is then used to find time-dependent solutions of the model in an analytically tractable way. Additional approximations give rise to a final practical version of the NES model, where real-measure and risk-neutral return distributions are given by three component Gaussian mixtures. This produces a closed-form approximation for option pricing in the NES model by a mixture of three Black-Scholes prices, providing accurate calibration to option prices for either benign or distressed market environments, while using only a single volatility parameter. These results stand in stark contrast to the most of other option pricing models such as local, stochastic, or rough volatility models that need more complex specifications of noise to fit the market data.

1 Introduction

This paper presents an analytically tractable model of non-linear dynamics of market returns using a Langevin approach, with five free parameters. Market returns are driven by a combination of a non-linear drift potential (a function of returns) controlled by four parameter , and a Gaussian white noise, whose strength is given by a volatility parameter . Due to a non-linear potential, the model admits regimes of both small and large return fluctuations. A stationary distribution of the model is given by a function that only involves the first four parameters , while the volatility parameter controls pre-equilibrium, time-dependent effects. Both the stationary distribution and a time-dependent transition probability density are analytically tractable and available in closed form or in quadratures. The model produces closed-form approximations for option pricing and market crash or crises probabilities. In contrast to a vast majority of the option pricing literature that resort to complex models of the noise such as local, stochastic, or rough volatility models, the model presented in this paper achieves an accurate fit to market option prices using only a single volatility parameter . Mutatis mudandis, the model can also be applied to individual stocks.

The return distribution obtained with the model can be represented as a sum of a stationary distribution and a time-varying component. The stationary distribution is a direct input to the model, in contrast to more traditional approaches where a stationary distribution is normally an output, rather than an input to a model. In this paper, the stationary distribution is given by the square of a two-component Gaussian mixture (which produces a three-component Gaussian mixture), defined using four parameters .

While a stationary return distribution is an input to our model, the output is given by a time-varying, dynamic component of the return distribution obtained with the model. The dynamic component is driven by both the first four parameters and the fifth parameter . The latter controls probabilities of large market drops or crises within a certain time horizon, e.g. a year, and hence drives the market skewness (and other moments) in a non-equilibrium setting. We will therefore refer to the model presented below as the Non-Equilibrium Skew (NES) model.

A decomposition of the return distribution into a stationary and a time-varying component is very convenient because it allows one, among other things, to also decompose moments of the distribution such as variance or skewness into a constant and time-varying components. While substantial time variations of moments of return distributions in financial markets are well documented phenomena, models that try to fit or explain such variations usually do not introduce such a structural separation. Instead, they follow purely statistical or CAPM-based regression-based approaches (see e.g. [19]), or use option pricing models to try to infer market views on future variance or skewness from option quotes, see e.g. [29]. Option-based approaches usually infer moments of a risk-neutral (option-price implied) return distribution rather than a real return distribution, and additional modeling steps are required to relate the two distributions.

The model presented in this paper constructs a direct link between deep out-of-the-money (OTM) options and moments of future returns under both risk-neutral and real-measure probability measures. By calibration to option data, the model can identify both a constant and time-varying contributions to the skew and variance of market returns. The empirical finance literature established contemporaneous correlations between a state of economy (e.g. proxied by the S&P 500 returns) and the returns’ skewness, as well as explored ways to use the historical or option-implied market skewness or variance as predictors of future returns, see e.g. [15, 29]. This paper offers a theoretical framework to pursue both sorts of analysis, with a clear separation between a static and dynamic components of the problem.

The NES model can be easily calibrated to market data for European vanilla options using a simple analytical approximation. Remarkably, while the development of the model involves some advanced concepts from quantum mechanics as will be explained below, its final version recommended for a practical use is very simple, and is given by two three-component Gaussian mixtures as models for the risk-neutral and real-measure return distributions, where parameters for both mixtures are fixed in terms of the original model parameters . Respectively, the NES model produces options prices as mixtures of three Black-Scholes prices. Numerical experiments show that the model is flexible enough to both calibrate to option data and match typical levels of market volatility and skewness across different market regimes.

The model developed here is based on a Langevin approach where we directly model non-linear stochastic dynamics of market log-returns, denoted in this paper. With the Langevin approach, dynamics are defined in terms of an interaction potential function and a noise term. For the latter, we use a simplest assumption of a constant Gaussian noise with volatility , though other more complex specifications (e.g. a state-dependent Gaussian noise, a non-Gaussian noise, or various multivariate extensions) could also be considered. For the former, we choose a potential function for which a stationary distribution of log-returns has a known and fixed functional form, and is given by a three-component Gaussian mixture mentioned above. In other words, a potential in this paper is constructed in such a way that the problem becomes quasi-exactly solvable. Here the word ’quasi’ refers to the fact that while the stationary distribution is an analytical expression, and is actually an input to our model, the model output amounts to computing the dynamic behavior - and this requires some computational efforts, and relies on certain approximations.

To develop an analytically tractable formulation, with easily computable approximations that could also be improved to any required precision, we borrow ideas from physics. First, we use a hidden supersymmetry of Langevin dynamics that was discovered in the 1980s [14]. The Langevin dynamics are mapped onto an equivalent quantum mechanical (QM) system, where the role of the Planck constant is played by the square of the volatility parameter (which explains our choice for this variable). In such an equivalent QM system, the hidden supersymmetry (SUSY) of the original Langevin dynamics becomes manifest, see e.g. [21]. The resulting equivalent QM system is mathematically identical to an Euclidean version of supersymmetric quantum mechanics (SUSY QM) developed by Witten [33] in 1981. While SUSY QM was originally proposed as a toy model to study supersymmetry in quantum field theory and string theory, since then it has become a topic of research on its own. In particular, researchers in SUSY QM found that SUSY can be used to develop very efficient computational schemes for computing wave functions or energies of different QM systems, that are often both simpler and more efficient than more traditional methods of computing in quantum mechanics, see e.g. [8] or [21]. This paper proposes to use this machinery to model non-linear stochastic dynamics of market returns.

Further using ideas from SUSY QM [8], we use a parameterized ground state wave function (WF) of this QM system as a direct input to the model, which also fixes a non-linear Langevin potential . A stationary distribution of the original Langevin model is given by the square of this WF, and thus is also a direct input to the model. This ensures that the model is quasi-exactly solvable. We use a two-component Gaussian mixture with parameters as a model of a ground state WF with an asymmetric double well potential, one of the most canonical examples in physics [23, 34]. This parametrization produces a tractable low-parametric model with intuitive and interpretable parameters, where supersymmetry (SUSY) is used to find time-dependent solutions of the model in an analytically tractable way.

Note that while a Langevin model with a non-linear potential could be introduced based on phenomenological grounds, the approach of this paper is motivated by previous work in [17] and [18] that developed a non-linear Langevin model of stock price dynamics.222Langevin dynamics with a cubic potential was previously considered by Bouchaud and Cont [4], however for a different dependent variable (the speed of a market price), and applied to modeling of market bubbles and crashes. Related ideas were also discussed by Sornette [30]. A model developed in [17, 18], called the QED (“Quantum Equilibrium-Disequilibrium”) model, explains non-linearities of price dynamics as a combined effect of capital inflows or outflows in the market, and their impact on asset returns, modeled as a linear or quadratic function of capital inflows. While the approach of [17, 18] provides a theoretical motivation for considering non-linear Langevin dynamics, here we present a different formulation that operates with similar non-linear potentials to those presented in [17, 18]333in the sense that both specifications may produce either a single well or a double well potential, depending on the parameters., but is more tractable analytically. More specifically, the potential used in this paper is ’semi-phenomenological’, and is inspired by a double-well potential, one of the most famous potentials in quantum and statistical mechanics and quantum field theory, that serves there as a prime model for describing quantum tunneling and thermally induced barrier transitions [23, 34].444The approach of this paper can also be viewed as partially inspired by machine learning paradigms, because it relies on a Gaussian mixture parametrization of a prime modeling objective - which in our case is given by a ground state wave function . A similar approach to the one developed in this paper can also be applied to other dynamical systems.

Theoretical links notwithstanding, non-linear Langevin models for market returns can also be considered on purely phenomenological grounds. Note that squares of market returns are sometimes used in the literature as additional cross-sectional predictors of stock returns in quadratic extensions of the CAPM model [28], also referred to as ’quadratic CAPM’ models, see e.g. [6] and references therein.

In this paper, squares and higher powers of market returns are used for time-series modeling. The main novelty of our Non-Equilibrium Skew (NES) model is that non-linearities of return dynamics give rise to certain solutions that are simply impossible to obtain starting with a linear model, or even with a non-linear model but treated using methods of perturbation theory. Other, non-perturbative (i.e. not traceable within a perturbation theory) saddle-point solutions of the dynamics called instantons become important to capture the right dynamics of the model. While instantons are encountered in many problems in statistical physics and quantum field theory (see e.g. [34]), the QED model of [17, 18] suggest that instantons might also be relevant for modeling of market prices and returns. This paper offers further insights into the importance of instantons (and, in general, of a non-linear and non-perturbative analysis) for modeling dynamics producing both small and large market fluctuations - with the latter interpreted as events of a severe market downturn or a crisis. More specifically, instantons and other non-linear effects induce both market crises and market skewness, enabling a theoretical link between them.

The paper is organized as follows. Sect. 2 presents the Langevin model along with its Fokker-Plank and Schrödinger representations that produce an equivalent quantum mechanical (QM) system. Sect. 2.2 introduces supersymmetry (SUSY) as a tool to solve the QM system, and Sect. 2.3 presents a quasi-exactly solvable NES model for a Langevin potential motivated by a double well potential in QM. Instantons and their role in dynamics are discussed in Sect. 2.4. Sect. 3 applies SUSY to compute pre-asymptotic corrections to a stationary distribution of the model.555This section can be skipped at the first reading, as the next Sect. 4 can be read largely independently of Sect. 3. Sect. 4 presents a simplified practical implementation of the NES model, and then applies it to explore time variations in return moments, and to option pricing out of equilibrium. Sects. 4.2 and 4.3 show that pricing of European options in the NES model reduces to a three-component mixture of Black-Scholes option prices, where all parameters are fixed in terms of the original model parameters. The following Sect. 4.4 presents examples of calibration to SPX options. The final Section 5 concludes. Additional materials are presented in Appendices A to D.

2 Langevin dynamics, double well potential, SUSY and the NES

2.1 Langevin dynamics: the Fokker-Planck and Schrödinger pictures

Let be the value of a market index at time . A period- log-return is defined as follows

| (1) |

In this paper, we focus on modeling dynamic distributions of rather than distributions of market value (or a stock price) . The reason is that unlike price dynamics which are non-stationary due to a market or stock drift, returns dynamics can be either stationary or non-stationary. If we define dynamics in terms of log-returns instead of prices , we can differentiate between regimes of stationary vs non-stationary returns, which would be impossible if a model is formulated in terms of prices . As an interplay between these regimes is a key ingredient of analysis in this paper, we explore dynamics of log-returns rather than prices . On the other hand, as , knowing a time- distribution of also gives a distribution of .

We use the Langevin approach to describe continuous-time stochastic dynamics of market returns , where dynamics are determined by an (overdamped) Langevin equation [24]:

| (2) |

where is a volatility parameter, is a standard Brownian motion, and is an interaction potential. In general, is a non-linear function whose structure is either deduced from underlying microscopic dynamics, or alternatively postulated based on phenomenological grounds. In particular, a quadratic potential gives rise to a linear drift , producing a familiar Ornstein-Uhlenbeck (OU) process as a special choice for the Langevin dynamics (2). While a different specification of the interaction potential with higher-order non-linearities will be presented below, for now we will proceed with a general development applicable for an arbitrary potential . The only assumptions used in this section is that a minimum value of the potential is zero, i.e. where stands for a minimum point of , and that the potential rises as at least as fast as . The last assumption is needed to ensure the existence of a stationary solution to the dynamics.

Transition probabilities to be at a certain state at time starting with an initial position at time satisfy a Fokker-Planck equation (FPE) corresponding to the Langevin equation (2)

| (3) |

Alongside the transition probability density that satisfies the FPE (3), it proves useful to consider a related transition density obtained if we used an inverted potential in the Langevin equation (2). Denoting such transition density and using the notation for the solution of the original FPE (3), the pair satisfies a pair of Fokker-Plank equations that can be compactly written as follows:

| (4) |

with the initial condition . We use the following ansatz to solve Eqs.(4) (see e.g. [32]):

| (5) |

Using this in Eq.(4) produces two imaginary time Schrödinger equations (SE) for :

| (6) |

where serves as a Planck constant , and are the Hamiltonians

| (7) |

Note that the Hamiltonian transforms into the partner Hamiltonian if we flip the sign of the potential . Further properties of the pair of Hamiltonians will be explored in the next section, while here we focus on the ’prime’ Hamiltonian corresponding to the initial FPE (3).

Let be a complete set of eigenstates of the Hamiltonian with eigenvalues :

| (8) |

We assume here a discrete spectrum corresponding to a motion in a bounded domain, so that the set of values is enumerable by integer values . We can now expand the wave function of the time dependent SE (6) in stationary states (quantum-mechanical wave functions, or WF’s) :

| (9) |

where coefficients should be found from the initial condition on which can be read off the initial condition and Eq.(5):

| (10) |

Combining Eqs.(5), (9) and (10), we obtain the spectral decomposition of the original FPE (see e.g. [32]):

| (11) |

When , only one term with the lowest energy survives in the sum in Eq.(11). As the potential is bounded below by zero, the lowest state, if it exists, would be a state with zero energy . In our setting, we assume that a potential is such that a normalizable zero energy state does exist. Retaining only two leading terms in the expansion (11) and defining as an energy splitting between the lowest and the first excited states, we can write it in the following form:

| (12) |

The last expression produces both time-dependent and stationary probability densities for the original problem corresponding to the Langevin equation (2) and the FPE (3).666If a lowest energy state has a positive energy , this would modify Eq.(12) by a time-decay factor , indicating a a metastability of an initial state that would decay with the decay rate . In particular, a stationary distribution is obtained by taking a limit , where only the first term survives.777An apparent remaining dependence on the initial position in the limit of Eq.(12) is spurious and will be shown to cancel out in the next section. On the other hand, for finite values , Eq.(12) describes a pre-asymptotic behavior en route to a stationary state, where a time-dependent correction is given by the second term in (12). At yet shorter times, higher-order corrections omitted in (12) may become important.

The spectral representation (11) (or its approximation (12)) that gives a decomposition of the solution of the FPE (3) in terms of eigenvalues of the SE (6) is well known in the literature. With a conventional approach, one starts with defining a potential , which is then used to find a Schrödinger Hamiltonian , and then the latter is used to compute eigenvalues . In the next section, we will present an alternative approach that provides a more direct link between the FPE transition density and wave functions . As will be shown next, the quantum-mechanical wave functions serve as ’half-probabilities’, in the sense that the FP density is related to squares of , in a close analogy to how a square of a wave function in the conventional quantum mechanics is interpreted as a probability density of a quantum mechanical particle.

2.2 Dynamics from statics: SUSY and half-probability distributions

To obtain a different representation of an approximate spectral decomposition (12), we return to the analysis of the pair of Hamiltonians (7). The first observation is that a special form of the potentials in the Schrödinger Hamiltonians enables their factorization into two first-order operators as follows:

| (13) |

where

| (14) |

The factorization properties (13) are well known within supersymmetric quantum mechanics (SUSY QM) of Witten [33]. The reason that the same mathematical construction arises in our problem is that the Schrödinger equation (6) for the FPE possesses hidden supersymmetry (SUSY) [5], that makes it mathematically identical to the Euclidean supersymmetric quantum mechanics (SUSY QM), with playing the role of the Planck constant . Using the standard nomenclature in the literature, we will refer to as the superpotential.

The factorization property (13) comes very handy to find a zero-energy eigenstate of with , as it enables replacing a second-order ODE by a first order equation , or more explicitly,

| (15) |

The conventional use of this equation is to integrate it to obtain an expression of the zero-energy state in terms of the superpotential :

| (16) |

where is a normalization constant. On the other hand, Eq.(15) can also be used in reverse in order to express the superpotential in terms of :

| (17) |

Therefore, if a zero-energy wave function of is known, the superpotential is fixed in terms of this function. Moreover, as , we also have an expression for the FPE potential in terms of :

| (18) |

where a constant is chosen such that the minimum value of is zero: . As in quantum mechanics a ground state wave function is always strictly positive [23], Eq.(18) is well-defined as long as is a valid ground state function of a quantum mechanical system. The representation (17) is well known in the literature on SUSY QM, see e.g. [11].

In our problem, the utility of the representation (18) can be immediately seen by substituting this expression into Eq.(12). This produces the following relation

| (19) |

This relation is also well-known in the literature, see e.g. [32]. It shows that the stationary distribution of as is given by the square of the ground-state wave function : , in a very similar way to a probabilistic interpretation of quantum mechanics. The stationary density is normalized to one as long as the is squared-normalized. Moreover, due to orthogonality of wave functions and , the transition density defined by Eq.(19) is automatically normalized to one for arbitrary times .

Traditionally, Eq.(19) is used from the left to the right, implying that a solution of the FPE equation (3) can be represented as in (19), where the wave functions have to be computed by solving the Schrödinger equation with a given Hamiltonian . In contrast, here we want to use it by reading from the right to the left, by defining the FPE transition density in terms of a given ground-state wave function viewed as a main modeling primitive, with higher-energy wave functions etc. derived from the same as will be explained in details below.

This implies, in particular, that if our only goal is to model a stationary distribution of as , it can be achieved by directly specifying a quantum mechanical ground state wave function . A trial ground state wave function can be constructed as a parametric function , with a functional form and parameters chosen such that has certain desired properties (such as a shape, symmetries, the local and global behavior at , etc.). Once a parametric function is specified, as , defining a stationary distribution thus requires zero extra parameters or calculations.

Note that when viewed on its own, the idea of using the relation as a way to model a stationary distribution of the FPE dynamics may appear a kind of trivial, as any stationary probability density can be represented as a square of another function. The real value of using the ground state wave function as a prime modeling primitive becomes apparent when it is used jointly with the relation (18) that defines the potential in terms of . Therefore, a parametric specification translates into a parametric choice for according to Eq.(18). Once the potential or the superpotential are defined, the first excited state (and higher states) can now be obtained as a solution of the the Schrödinger equation (6). In this equation, the Hamiltonian , with given by Eq.(14) where the superpotential is defined by Eq.(17). This procedure fixes all time-dependent terms in Eq.(19) in terms of the only model input .

This suggests a way of constructing dynamic probability distributions with desirable properties, whose parameters could be interpreted in terms of parameters that specify the ground-state wave function . Note that while defining a superpotential in terms of a properly chosen parameterized ground state wave function was previously used to compute tunneling rates with bistable potentials in the context of SUSY QM, see e.g. [11], here we propose a similar idea to model non-linear stochastic processes in a tractable way, by specifying them in terms of a parametrized ground state wave function (or a ’half-probability distribution’) . As suggested by Eq.(19), if our only objective is a limiting stationary distribution of as , no further work is needed, and .

To summarize, the representation (19) of a time-dependent transition density of the FPE (3) provides a new tractable way to model non-linear Langevin dynamics (2), where the interaction potential is defined as in Eq.(18). With this approach, calculation of a stationary density requires no calculation at all, as . This can be directly computed once a parametrized trial function is specified. To compute a time-dependent pre-asymptotic behavior due to the second term in (19), the only additional step needed is a calculation of the first excited state and the energy of the Hamiltonian . In the next section, we will consider a simple model of a ground-state wave function where such calculations become quite tractable.

2.3 NES: A Log-Gaussian Mixture double well potential

To produce an interesting and tractable formulation, we consider a two-component Gaussian mixture (GM) as a model of , with means and and a mixture coefficient , with a normalization parameter chosen such that is squared-integrable with :

| (20) |

Such a combination of Gaussian densities often provides a good representation of a ground state wave function of a particle in a double well potential. Double well potentials play a special role in statistical physics and quantum mechanics, and are often used to model tunneling phenomena, see e.g. [23] or [34]. In particular, a symmetric double well is described by a symmetric version of (20) with and . For other choices of model parameters, the GM model (20) can fit a variety of shapes including both a unimodal and bimodal shapes. For a later use, it is convenient to represent the WF (20) as a Gaussian pdf multiplied by a factor that asymptotically approaches a constant:

| (21) |

where function is defined as follows:

| (22) |

Viewing (20) as an exact, rather than an approximate ground state wave function, we can plug it into Eq.(18) to find the explicit form of the Langevin potential :

| (23) |

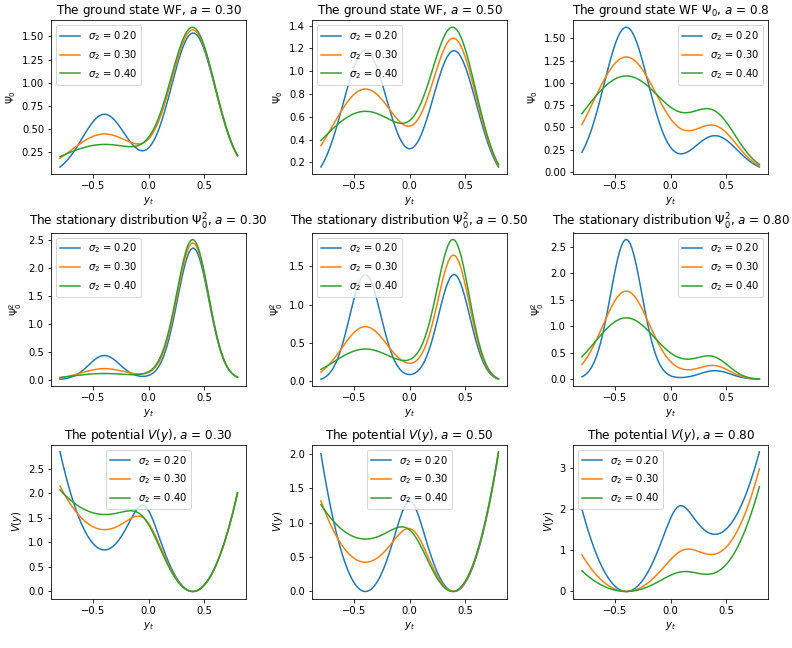

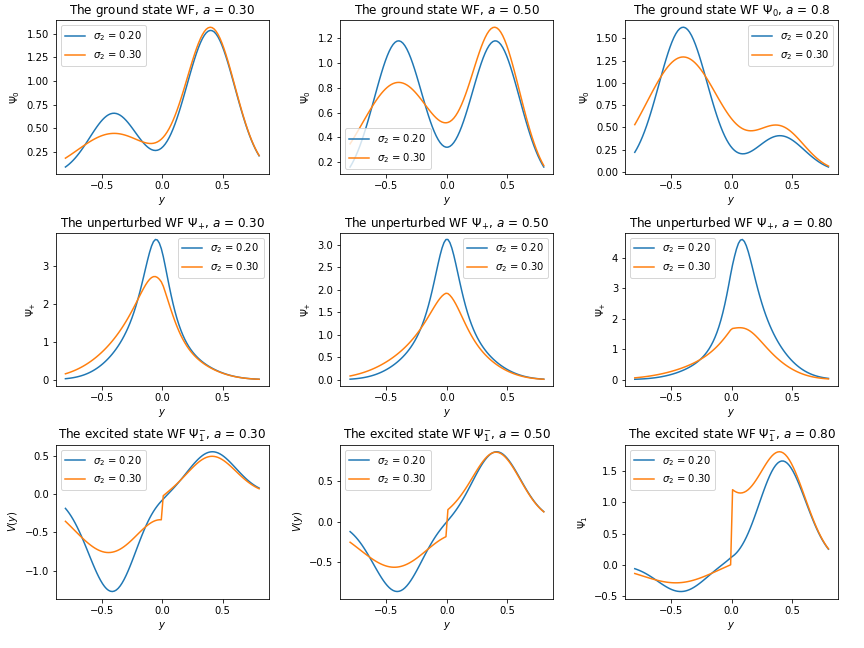

where again is a constant chosen such that the minimum value of is zero. Examples of trial ground state WFs and resulting potentials are shown in Fig. 1.

While this expression produces a non-linear behavior for small positive or negative values of , its limiting behavior at is rather simple and coincides with a harmonic (quadratic) potential:

| (24) |

The fact that the limiting behavior of the potential coincides with a harmonic potential as means that in this asymptotic regime the model behavior is described by a harmonic oscillator, and thus is fully analytically tractable.

As Gaussian mixtures are known to be universal approximations for an arbitrary non-negative functions given enough components, this implies that an arbitrary potential that asymptotically coincides with a harmonic oscillator potential can be represented as a negative logarithm of a Gaussian mixture. We can refer to such class of potentials as Log-Gaussian Mixture (LGM) potentials. In our particular case, we restrict ourselves to a two-component LGM potential.888A requirement of an asymptotic harmonic oscillator behavior could be seen as a potential limitation for the LGM class of potentials, as many interesting potentials have a different asymptotic behavior. To this point, we can note that an onset of such a quadratic regime can always be pushed further away by a proper rescaling of the coordinate, while for small or moderate values of a new rescaled argument, the dynamics can still be arbitrarily non-linear, and driven by the number of Gaussian components and their parameters.

Note that while is proportional to a two-component Gaussian mixture, its square is proportional to a three-component Gaussian mixture:

| (25) | |||||

where the additional third Gaussian component has the following mean and variance:

| (26) |

The normalization condition thus fixes the value of the constant as follows:

| (27) |

Recalling the relation and introducing weights

| (28) |

we obtain the following three-component Gaussian mixture model for the stationary distribution :

| (29) |

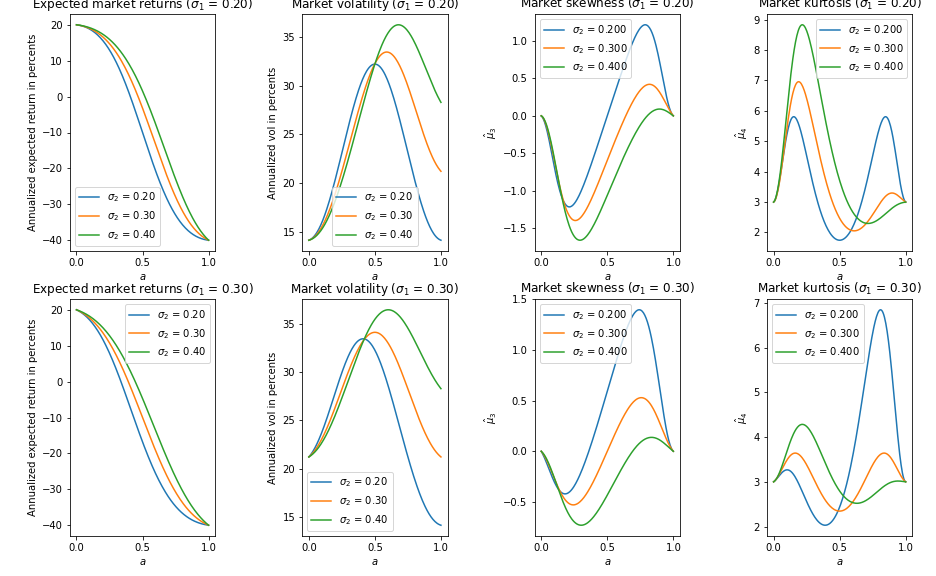

Note that while a priori defining a three-component Gaussian mixture model requires eight parameters, our approach fixes all parameters of the Gaussian mixture (29) in terms of only five original model parameters , or rather four parameters if we set as we will do in most of examples below. Interestingly, the fifth model parameter drops off in the expression for the stationary density , and only appears when treating non-stationary effects due to the second term in Eq.(19). In addition, as we will show next, this parameter also controls intensity of transitions between minima of the potential (23). The behavior of moments of the equilibrium distribution is shown in Fig. 2.

2.4 Dynamics with a bistable potential: metastability and instantons

As illustrated in Fig. 1, the NES model may produce a variety of equilibrium distributions including both unimodal and bimodal shapes, where transitions between different shapes are controlled by model parameters. Informally, one can expect that unimodal distributions would be typical for benign markets, while bimodal distributions may arise when a market is distressed or in a crisis. In this section, we focus on a model regime when parameters are such that a ground state is a bimodal function, corresponding to the market in a crisis or a severe distress. However, the final formulae that we will carry to a final model formulation will be applicable for any choice of , whether it is unimodal or bimodal, or equivalently for any specification a LGM potential, whether it has a single minimum or two local minima. Formulas that specifically assume a particular choice of the potential will be separately mentioned below.

Assume now that the market is in a regime when has two maxima separated by a local minimum, see Fig. 1. As the logarithmic function is monotonic, Eq.(18) then implies a bimodal Langevin potential , with a local maximum at separating two local minima and (the latter coincide with maxima of ). Here we assume that , and that , so that and are the global and local minima, respectively. The height of a potential barrier faced by a particle initially located at (i.e. in a local minimum) is . Such potentials lead to metastability, where a particle initially located near a local minimum hopes over the barrier as a result of thermal fluctuations. Following physics conventions, we will occasionally refer to states and as the true and metastable vacua, respectively. Using this nomenclature, a situation with a potential with a single minimum can be described as a theory with a single stable vacuum.

Using the FPE approach, an escape rate from a metastable minimum of a potential can be found as the inverse of a mean passage time to exit the interval , viewed as a function of the backward (time-zero) variable , assuming that . In our case, we can set and , with , so that and . For a time-homogeneous process, the mean passage time satisfies the following backward PDE (see e.g. [12]):

| (30) |

with boundary conditions and . This equation can be solved by multiplying by an integrating factor , and then twice integrating the resulting expression using the boundary conditions. This produces the following well-known relation for the mean passage time :

| (31) |

This is a general expression valid for any potential that is sufficiently well-behaved at . In particular, it applies to both cases of a potential with a single minimum or a potential with two local minima separated by a maximum. For the former case, is not a position of a global minimum of the potential, but rather a threshold value of log-return that signals a crisis regime of the market. For the latter case, Eq.(31) assumes that the ’particle’ is initially placed in the right well corresponding to a local minimum , and eventually escapes to the left well with a global minimum of the potential at .

For a potential with two minima, the mean passage time can be calculated using quadratic expansions of , where the first and second integrals in Eq.(31) are computed using a saddle point approximation with quadratic expansions around, respectively, a maximum and the local minimum . Such an approximation is justified when , i.e. when the barrier is high, while the initial position is near the local minimum . This produces the celebrated Kramers escape rate formula for the escape intensity (see e.g. [12] or [16]):

| (32) |

The same result (32) can also be obtained using alternative methods. In particular, with the Schrödinger equation (6), the Kramers escape rate can be calculated as where is the energy splitting between a ground state and a first excited state [5]. Within a path integral approach, the energy splitting can be obtained as a contribution to the path integral due to instantons - saddle-point solutions of dynamics obtained in a weak noise (quasi-classical) limit of the Langevin equation (2), where the potential is inverted. The instanton equation reads (see Appendix A for more details)

| (33) |

While instantons produce the exponential term in (32), the pre-exponential factor is obtained from thermal (or quantum) corrections to an instanton contribution to a transition probability for a bimodal or metastable potential , see e.g. [17]. Note that the Kramers escape rate (32) is non-analytic in the ’Planck constant’ , i.e. it does not have a Taylor expansion around the value . Instantons arising in statistical and quantum mechanics or in quantum field theory produce a similar non-analyticity of transition amplitudes in the Planck constant or in coupling constants driving non-linearities, see e.g. [7]. This means that instantons are non-perturbative solutions that can not be found to any order of a perturbation theory in . On the other hand, using methods of supersymmetry for analysis of metastability in the Fokker-Planck dynamics with a bistable potential, the same results as obtained from instanton calculus can also be obtained using a pure quantum mechanical approach, as was shown in [5].

With our approach where the ground state wave function is the main modeling primitive, we can express in Eq.(31) by substituting there Eq.(18). This gives

| (34) |

Note that unlike Eq.(32) which only applies for a bistable potential, the last expression (34) is applicable for either a bistable potential or a potential with a single minimum. In addition, numerical integration in Eq.(34) can be done with arbitrary precision, unlike the Kramers relation (32) which is based on the saddle point approximation and the presence of two minima of the potential. Therefore, we will use Eq.(34) instead of (32) in a practical implementation of the model to be presented below.

Interestingly, the last relation (34) suggests that when is provided as an input that does not depend explicitly on parameter , then the whole expression depends on as , which means that the escape rate is proportional to the ’Planck constant’ . We will return to this remark below.

While Eq.(34) is general and applies for any ground state WF , it can be approximately calculated analytically for a bistable potential, producing corrections to the Kramers relation (32). To show this, we use the expression for given for the trial function (20) by Eq.(29), and compute the inner integral in (34) explicitly:

| (35) |

where stands for the cumulative normal distribution. We approximate the outer integral in (34) by reverting to its previous expression in Eq.(31), and expanding the integrand around its maximum at , while simultaneously replacing the integration limits by infinities. This gives

| (36) |

where

| (37) |

Here we replaced the exact expression (27) for the normalization constant by its Gaussian approximation obtained using a quadratic expansion of around its local minimum . Using Eq.(35), the integral in Eq.(36) can be computed analytically using the formula999See e.g. https://en.wikipedia.org/wiki/ListofintegralsofGaussianfunctions#CITEREFOwen1980.

| (38) |

This produces the final analytical approximation for the mean passage time, which applies when an initial position is near the local minimum :

| (39) |

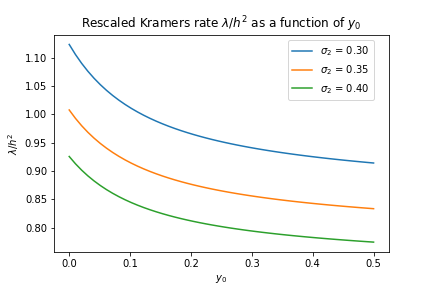

When the arguments of cumulative normal functions in this relation can be approximated by infinities (which is formally obtained in the limit the limit or alternatively ), this expression produces the same formula (32) for the escape rate . Note that a dependence on the initial position is neglected in Eq.(39) within the saddle-point approximation. A direct numerical integration in Eq.(34) (which is used for a practical implementation, as was mentioned above) shows that the saddle-point approximation becomes less accurate for smaller initial values , see Fig. 3.

It is instructive to check how the mean passage time (39) depends on the ’Planck constant’ . Note that defined in Eq.(37) is actually independent of as implied by (18). As other parameters entering the sum do not depend on while (see Eq.(23)), we have . As was mentioned above, the same parametric dependence can also be seen directly from Eq.(34).

Therefore, parameter controls the escape rate to a stable vacuum starting with a metastable vacuum. On the other hand, note that does not appear in the trial wave function (20) or the stationary distribution (29). This does not mean, of course, that properties of a stationary state are not affected by the volatility parameter , but rather means that with our method of a direct parameterization of the trial wave function (20), its impact on an equilibrium distribution is already incorporated in other model parameters.101010This can be also be simply seen in the original FPE equation (3): if we re-define the potential where is another potential, and then look for a stationary solution, the constant drops out in the resulting stationary distribution formula when expressed in terms of . It does not imply, of course, that magically disappears from the problem, but simply means that for a stationary distribution, it can be formally absorbed into parameters defining the new potential . With this parametrization, the Kramers escape rate is equal to times a fixed function of other model parameters, which is illustrated in Fig. 3. As will be shown in the next section, parameter also appears in pre-asymptotic corrections to the asymptotic (stationary) behavior of the model, and is therefore related to the speed of a relaxation to such an equilibrium state.

3 Computing dynamic corrections with SUSY

3.1 Supersymmetry and dynamics

So far, our discussion was centered around properties of a stationary distribution (20) that corresponds to an asymptotic (at time ) behavior of the FP transition density in the Langevin model with the potential given in terms of a ground state WF in Eq.(23). As was discussed above, using a parametric model (where in our case stands for all parameters entering Eq.(20)) is very convenient as it provides a direct answer to the problem of finding the asymptotic behavior of the model (assuming all parameters are kept fixed) as . As can be seen from Eq.(19), the equilibrium distribution that describes this limit is given by , so that no further work is needed to find it.

Therefore, when the stationary distribution is an input, rather than an output in a model, the burden of computing the dynamics is considerably reduced - all we need to find according to Eq.(19) are higher-energy states with , and their energies They should be computed as solution of the the Schrödinger equation (6). In this equation, the Hamiltonian , with given by Eq.(14) where the superpotential is defined by Eq.(17).

This procedure fixes all time-dependent terms in Eq.(19) in terms of the only model input . The challenging part is to actually compute these higher-energy states WFs with . For some potential, the energy split can be very small, that may give rise to substantial challenges when computing it, along with computing WFs of excited states using various approximation methods. Furthermore, while many approximate methods of quantum mechanics work well for a ground state of a QM system, they become harder to use (or not usable at all) for higher states.

Supersymmetry (SUSY) is known to offer very efficient computational methods to solve such problem, which were applied to various problems in SUSY QM and classical stochastic systems, see e.g. [8] and [21], respectively. Supersymmetry of the Hamiltonians implies that all eigenstates of should be degenerate in energy with eigenstates of the SUSY partner Hamiltonian , except possibly for a ’vacuum’ state with energy [33]. Such zero-energy ground state would be unpaired, while all higher states would be doubly degenerate between the SUSY partner Hamiltonians according to the following relations (see e.g. [8] or [21], or Appendix B for a short summary):

| (40) | |||

These relations assume that a zero-energy state exists. In certain models, Hamiltonians can be supersymmetric, while a ground state has a non-zero energy . Such scenarios correspond to a spontaneous breakdown of SUSY [33]. For such models, supersymmetry is a symmetry of a Hamiltonian but not of a ground state of that Hamiltonian. On the other hand, an unbroken SUSY is characterized by the existence of a normalizable ground state with strictly zero energy . For SUSY to be unbroken, the derivative of the superpotential should have different signs at , which means that that it should have an odd number of zeros at real values of [33]. In our problem, SUSY is not spontaneously broken by design, as the ground state WF defined in (20) has a zero energy by construction, and the superpotential in Eq.(17) does have different signs at .

Therefore, we can use the SUSY relations to compute (and other higher states, if needed) as described above. The reason SUSY is helpful in practice is that it allows one to replace a hard problem of computing a first excited state for the Hamiltonian by a simpler problem of computing a ground state WF for its SUSY partner . Once the ground state WF of the Hamiltonian is computed using some approximation (e.g. a variational or a perturbation method), the first excited state of can be obtained according to the SUSY relations (3.1) by applying the SUSY generator to , where the superpotential is defined by Eq.(17).

3.2 The ground state of the SUSY partner Hamiltonian

The first task is therefore to compute (approximately) the ground state WF of the SUSY partner Hamiltonian . To this end, note that a candidate ground-state solution of is easy to compute from the equation , whose solution can be obtained by flipping the sign of in Eq.(16):

| (41) |

However, this cannot be a right zero energy solution because it diverges as , and thus is not normalizable. The divergence can be removed if we consider the following ansatz [8, 21]:

| (42) |

where

| (43) |

The ansatz (42) can now be computed in closed form using the ground state WF (20). Using Eq.(29), we obtain

| (44) |

with

| (45) |

These relations imply that . Note as as it stands, Eq.(44) is not very convenient for numerical implementation, as it can produce numerical overflows. A more convenient representation is obtained by using the representation of given in Eq.(21), and expressing (44) in terms of the complimentary error function and the scaled complementary error function :

| (46) |

where

As for while , this produces the following asymptotic behavior at (assuming that ):

| (47) |

For numerical integration of that would be needed below, multiple calls for function can be time-consuming. As an alternative, one can rely on approximate expressions for , see e.g. [27]. Other ways to simplify calculations will be discussed below.

Note that Eqs.(47) imply that is square-integrable, as it decays as a Gaussian multiplied by . The last relation is actually independent of a particular choice of the potential , as the same functional form of a Gaussian times can also be found if the integrals in (42) are evaluated using a saddle-point approximation around a minimum of a general potential . Assuming that a potential has a local minimum at point with a value and a second derivative at this point, a saddle-point calculation of integrals entering Eq.(42) produces the following result for (here ):

| (48) |

where is a normalization constant whose specific expression will not be needed below, and is the scaled complementary error function. For negative values , one obtains the same expression with a flipped sign of the argument of , with substituted by a local minimum for the region . Assuming that local minima of are well-separated for the ground state WF (20), their positions are well approximated by values and for and , respectively, with and , respectively.

Most of the calculation in this section do not however use the explicit form (44) and proceed with a general definition in Eq.(42), while only relying on the asymptotic behavior (47).

One can easily check that defined in Eq.(42) is continuous at with , and that for . For example, by taking , we obtain

| (49) | |||||

However, its derivative has a discontinuity at :

| (50) |

Therefore, defined in Eq.(42) is not an eigenstate of . Instead, is a zero-energy ground state WF of a singular Hamiltonian given by

| (51) |

that differs from by the -function term . Indeed, with this Hamiltonian we obtain

| (52) |

as a result of the fact that for , while finite contributions coming from the discontinuity of the first derivative (50) and the additional -function term cancel each other:

| (53) |

Equivalently, we can express in terms of :

| (54) |

3.3 Logarithmic Perturbation Theory for the log-wave function

Given the structure of the Hamiltonian in Eq.(54), its ground-state eigenvalue and the eigenfunction can be found using quantum mechanical perturbation theory (see e.g. [23]). To this end, we treat the additional term as a perturbation around the exactly solvable singular Hamiltonian . Following the literature on SUSY QM (see e.g. [20, 11]), we use the Logarithmic Perturbation Theory (LPT), instead of a more conventional Rayleigh-Schrödinger (RS) perturbation theory. For a one-dimensional Schrödinger equation, the LPT yields quadrature formulas for energies and wave functions to any given order in the perturbation theory, in a hierarchical scheme. The LPT becomes especially simple for a ground state which is nodeless, and thus can be represented in the form where is some continuous function. By inversion of this formula, we have , therefore function can be referred to as a log-wave function (log-WF). The perturbation scheme is then constructed for . While the LPT can be shown to be equivalent to the RS perturbation theory [1], it is far more convenient in practice due to its recursive quadrature form and the absence of a need to compute matrix elements of a perturbation potential. Details of the LPT method are provided in Appendix C.

To the first order in perturbation , the ground-state energy is given by Eq.(C.7) where we have to substitute , and . This gives the same result as the conventional RS perturbation theory (see e.g. [23]):

| (55) | |||

Here the last approximate equality is obtained by assuming that the barrier is high, and therefore the ground state wave function is concentrated around the minimum of where the exact form of is replaced by its approximation around this minimum. In other words, tunneling is neglected when we compute the energy splitting formula (55), similarly to how tunneling is computed in quantum mechanics ([23], Sect. 50). With such assumption, can be approximated as follows: , where can be approximated by its quadratic expansion around it maximum. The first integral in the denominator in the last expression in (55) comes due to the square of the normalization factor . As the inverse of expression given in (55) is proportional to defined in Eq.(31), such a Gaussian approximation produces the same relation (32) for the escape rate . Therefore, the classical Kramers escape rate relation can also be obtained using methods of SUSY [5, 21].

For the ground-state wave function of the Hamiltonian , the LPT produces a perturbative expansion of a ’log-WF’ in powers of perturbation parameter . To the first order in , the WF has the following form:

| (56) |

where is a normalization factor to be determined later, is the unperturbed WF defined in (42), and stands for the log-WF of the unperturbed Hamiltonian .

While a specific expression for the first-order correction will be given momentarily, one should note that within perturbation theory, a first-order approximation of the form (56) is only justified when a first correction is smaller than an unperturbed log-WF :

| (57) |

As implied by Eq.(47), function grows quadratically in the asymptotics: when . On the other hand, as the perturbation potential in our problem is given by a Dirac delta-function centered at , the function that incorporates its effect is expected to decay as . Therefore, using perturbation theory is justified in our problem.

The first-order correction log-WF is determined by the following relations, see Eqs.(C.2) and (C.9):

| (58) |

We omit here an additive constant that can re-absorbed into the normalization constant in (56). Using the constraint (55), Eq.(58) can be written in a different form:

| (59) |

Due to Eq.(55), is continuous at in Eq.(58), as can also be seen in Eq.(59). For the derivative , we find

| (60) |

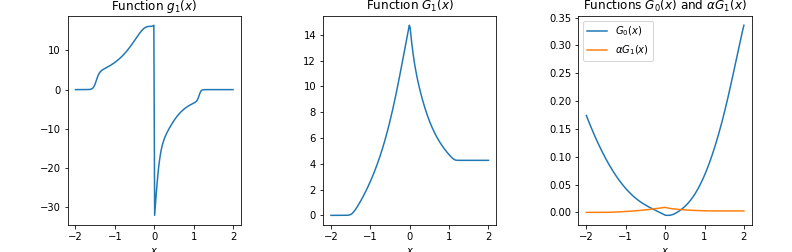

The derivative is positive for and negative for , see Fig. 4. Therefore has a maximum at with the value

| (61) |

Note that while is continuous at , its second derivative has a jump: for a small value , we obtain

| (62) |

3.4 The first excited state of

When the ground state WF of the SUSY partner Hamiltonian is computed to the first order of LPT in Eq.(56), we can now use SUSY relations (3.1) to obtain excited states of . For the first excited state of , we have the following relation in terms of the ground state of :

| (63) |

Substituting here Eqs.(3.1) and.(56), we obtain

| (64) |

We can check that this WF is orthogonal to the ground state WF :

| (65) |

One can also check that the first state is squared-normalized provided is square-normalized, while the coefficient takes care of a proper normalization of .

Shapes of obtained in our model are illustrated in Fig. 5, along with a ground state WF , and an unperturbed ground state WF of the partner SUSY Hamiltonian . As could be expected, the WF of the first excited state resembles the well known WF of the first excited state of the quantum mechanical harmonic oscillator [23].

Once the first state is computed using SUSY, we are done in terms of computing the leading pre-asymptotic correction to a stationary distribution. It is given by Eq.(19) which we repeat here for convenience:

| (66) |

This means that the non-stationary component of the return distribution is given, at a leading pre-asymptotic order, by the product . This immediately translates into non-stationary corrections to the variance and skewness of the return distribution, as will be discussed in the next section.

4 Practical implementation and applications to option pricing

4.1 NES: Practical implementation

Formulas presented above provide an accurate theoretical scheme of computing the first excited state WF in Eq.(64), and hence give an explicit solution for a time-dependent component in the non-stationary return distribution (66). In practice, computing this WF involves a numerical computation of a double integral that defines function , see Eq.(58), which may be time-consuming for model calibration when such computations should be done many times. One way to handle such potential challenges that was mentioned above was to use fast numerical approximations to evaluate the scaled complimentary error function , however this still requires a double numerical integration.

An alternative that might be preferred in practice would be to directly approximate the WF . As was mentioned above, it resembles, not accidentally, the first excited state WF of a quantum mechanical harmonic oscillator. This suggests that a simple approximation would be given by the following expression:

| (67) |

where and are the mean and standard deviation of the Gaussian mixture defined by :

| (68) |

Substituting (67) into Eq.(66) produces the following simplified form that can be used for practical applications of the model:

| (69) |

where we used the definition of the Kramers escape rate, where the energy splitting is computed according to Eq.(55). Note that the density defined by this relation can formally become negative for large negative values of . However, this is an artifact of a reliance on the first-order perturbation theory that was used to derive Eq.(69). As long as perturbation theory is applicable, we have , and can thus replace under the same assumptions. Therefore, we can replace (69) by even a simpler form

| (70) |

where the factor is absorbed into a normalization constant . When perturbation theory applies, differences between Eqs.(70) and (69) would be negligible as long as all integrals defining observable quantities using the definition (70) are dominated by a region of small where . In this case, using (70) instead of (69) would simplify calculations, while any differences could be re-absorbed in slight modifications of model parameters relative to their values in the original equation (69).

While Eq.(70) will be used below for option pricing, it is more illuminating to use the original form (69) to approximate time-dependent contributions to moments of the return distribution. For the mean, variance and skewness of the time-dependent distribution (69), we obtain

| (71) | |||

Here and are centered moments computed from the three-component Gaussian mixture according to formulas in Appendix D:

| (72) |

Equations.(4.1) are applicable as long as corrections are smaller than the first terms in these formulae. Interestingly, the model predicts that a time-dependent correction to the -th moment of a stationary distribution is approximately proportional to the -th moment, where the coefficient of proportionality has the same time dependence for all moments. This observation could shed some light on some open questions in financial modeling. In particular, [22] suggests that risk premia in equity returns are in fact premia for the skewness, rather than variance of returns. This goes contrary to the traditional financial theory such as CAPM [28] that claims that risk premia are premia for the variance. Our Eqs.(4.1) show that the variance and skewness of a stationary distribution are mixed in a time-dependent way in a non-equilibrium, pre-asymptotic distribution, thus suggesting that both views may be partially correct, and be in fact parts of the same time-dependent analysis. A more detailed look into implications for risk premia is left here for a future research.

4.2 Non-equilibrium option pricing: construction of the pricing measure

In addition to providing explicit formulae for time-dependent moments of returns, the analytical approach of this paper can also be applied to option pricing in a non-equilibrium, pre-asymptotic setting. To this end, we use the simplified form (70) of a finite horizon transition density. To use it for option pricing, recall that is defined as a time- log-return computed over the time period :

| (73) |

so that . Using Eq.(70), the transition density for can be written as follows:

| (74) |

where is a normalization constant, and we write to lighten the notation. Eq.(74) approximates pre-asymptotic effects in the time- distribution of log-return , where such effects are controlled by parameter . We can write it as another GM distribution with different weights and means:

| (75) |

where we omitted the dependence on for brevity, and defined the adjusted parameters as follows:

| (76) |

The stationary distribution can be formally obtained from this expression by taking the limit .

The non-equilibrium density (74) refers to a statistical (real-world) measure. Distributions needed for option pricing are risk-neutral distributions where by definition the expected return of a stock paying dividend is given by where stands for a risk-free rate. By Itô’s lemma, the expectation value of log-price under the risk-neutral measure should then be equal to . A simple approach to construct a risk-neutralized distribution starting with a real-measure distribution is to apply the Minimum Cross Entropy method. With this method, is found by minimization of the following Lagrangian function:

| (77) |

where is a Lagrange multiplier, and the second term is the constraint ensuring that the expected value of is equal to . This expression should be minimized with respect to , and maximized with respect to . Notice that such a procedure would induce a dependence of the optimal value of on the parameter .

Minimization of this Lagrangian with respect to produces the following expression for :

| (78) |

where is another normalization factor that is re-absorbed into the new normalization factor in the second equation. Such an exponential tilt of the real-world measure to produce a risk-neutral measure is also known as the Esscher transform. Notice that depends on only via the combination , which will be used below.

Plugging the solution (78) back into the Lagrangian (77) and flipping the overall sign, the problem of finding the Lagrange multiplier amounts to minimization of the following objective function:

| (79) |

with respect to . Equivalently but more conveniently, in the second equality in Eq.(79), we write the objective function as a function of a combination , plus an unessential constant term equal to ). Given that both and the loss function (79) depend on only via the combination , we can equivalently, but more conveniently, replace optimization with respect to in Eq.(79) by optimization with respect to . As it is easy to see, setting the derivative of to zero produces the constraint for the expected value of

| (80) |

Furthermore, the second derivative is non-negative as it is equal to the variance of , therefore the minimization problem in Eq.(79) is convex and has a unique solution for .

The risk-neutral distribution in Eq.(78) can now be re-written as a three-component Gaussian mixture similar to the real-measure density (75), but with different means and weights:

| (81) |

with

| (82) |

so that and . The constraint (80) can now be written as follows:

| (83) |

Re-grouping terms, this equation can also be written as follows:

| (84) |

This equation could be used to solve for by iterations, which could be considered an alternative to finding the optimal value of by a direct numerical minimization of the Lagrangian (79). The limiting behavior at is

| (85) |

Note again that the risk-neutral distribution in Eq.(81) only depends on via the combination . On the other hand, the latter combination is fixed in terms of the original model parameters by Eq.(84). This fact implies, in particular, that while parameter quantifies the amount of non-equilibrium in the system, for the purpose of finding the risk-neutral distribution , its exact value is irrelevant as it gets re-absorbed into the only relevant parameter combination . It is only the real-measure distribution in Eq.(75) that explicitly depends on parameter , and hence is sensitive to the amount of non-equilibrium in the dynamics.

4.3 European option pricing and model calibration

Now consider a European call option on with maturity and strike and a terminal payoff . The option value is defined as a discounted expected value of its payoff function with respect to the risk-neutral measure (81):

| (86) |

Plugging here Eq.(81) and performing integration, we obtain a closed-form expression for the option price in a non-equilibrium setting:

| (87) |

where

| (88) |

where parameter is found by the numerical minimization of Eq.(79), or alternatively by iterations in Eq.(84). Each component in the sum in Eq.(87) is given by the classical Black-Scholes formula [3] for the price of a dividend-paying stock with dividend . To differentiate them from real dividends paid on stocks, in what follows we will refer to parameters as the NES dividends.

It should be noted here that mixtures of lognormal price distributions, or equivalently normal mixtures for returns were previously suggested in the literature on empirical grounds as a flexible way to incorporate volatility smiles in option prices, see e.g. [2].111111 Two-component Gaussian mixtures were also proposed for portfolio optimization in [25] as a phenomenological way to incorporate skewness of equity returns. The novelty of the approach presented in this paper is in providing a theoretical foundation to such mixture models, while simultaneously providing a parsimonious representation of a three-component Gaussian mixture in terms of only 5 model parameters . Note that the option price depends on the value of parameter only through its dependence on the NES dividends , which in their turn depend on . Furthermore, once parameters are found from calibration to option prices, they produce both the risk-neutral and real-measure return distributions.

The availability of the closed form solution (87) for European call options (and a similar relation for puts) enables a straightforward calibration of model parameters to market option data.121212In addition to option pricing data, one can use other types of data for model calibration, as will be discussed below. To this end, one should optimize a loss function penalizing the difference between market option prices and their theoretical expressions given for calls options by Eq.(87) as functions of , with an additional regularization as described in more details in the next section. As the effective dividend parameters in Eq.(4.3) depends on the parameter combination which is defined in terms of the original model parameters according to Eq.(84), a new value of parameter should be computed at each iteration of optimization of the model parameter .

The procedure just outlined allows one to calibrate the risk-neutral distribution (81) by fitting the model parameter . As was discussed above, this distribution is also a function of fixed in terms of parameters by Eq.(84). The actual value of parameter is irrelevant for the risk-neutral distribution (81) as it gets re-absorbed into the adjusted parameter .

While the risk-neutral distribution is insensitive to variations of parameter , the real-measure distribution does depend on it as indicated in Eqs.(76). On the other hand, the value of is driven, in addition to the current value of log-return and the model parameters , by the value of the Kramers escape rate . From a viewpoint of the final expression (75), the only role of the machinery developed in the previous sections is to compute non-equilibrium corrections to the real-measure return distribution by computing the Kramers escape rate in terms of the original model parameters. This can be done by using either Eq.(34) along with the definition , or the SUSY QM relation (55), along with the formula . In the practical implementation, we compute using Eq.(34).

4.4 Examples of calibration to SPX options

We consider three sets of examples of calibration to market quotes on European options on SPX (the S&P 500 index). In each set, we separately calibrate the model to calls and puts. Note here that a common approach in the literature is to construct a single risk-neutral implied distribution by assuming the put-call parity and using both call and put option quotes jointly. While such a procedure would also be possible with the NES model, we prefer to calibrate to calls and puts separately, so that we are able to compare the resulting distributions implied separately by the calls or the puts. One advantage of this approach is that by not enforcing the put-call parity, we leave some room for a possible predictable component in returns, see e.g. [10]. Furthermore, a separate calibration of the model to either call or put options is useful as it allows one to separately quantify views of future returns from different segments of the market.

Calibration for all examples considered below is performed using the regularized weighted quadratic loss function:

| (89) |

Here are the quoted prices of SPX options, NES option prices are computed using Eq.(87) for call options and a corresponding relation for put options, and are calibration weights. The second term in Eq.(89) adds Eq.(83) as a convex regularization, with the regularization weight . While the first term in the loss function (89) is non-convex in the model parameters , by increasing the value of the regularization , the loss (89) can be made convex. We choose the calibration weights using BS deltas computed using implied volatilities to improve calibration to deep out-of-the money (OTM) options, but in addition also multiply the weight for ATM strikes by a factor of 2 or 3 to retain an accurate calibration to ATM option quotes.

In all three sets of experiments conducted below, for a given option tenor and given pricing date, we calibrate to market quotes on 10 call options and 10 put options.

The strikes are chosen among available market quotes to cover the the range of option deltas between 0.02 and 0.5, in absolute terms, so that we calibrate

to both ATM strikes and deep OTM strikes. Optimization of the loss function (89) is done using the shgo algorithm available in the Python scientific computing package scipy.

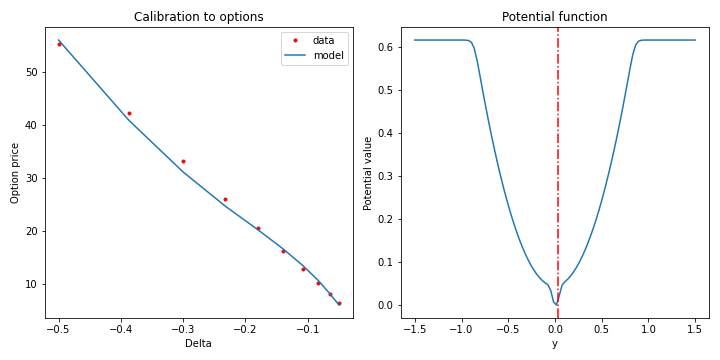

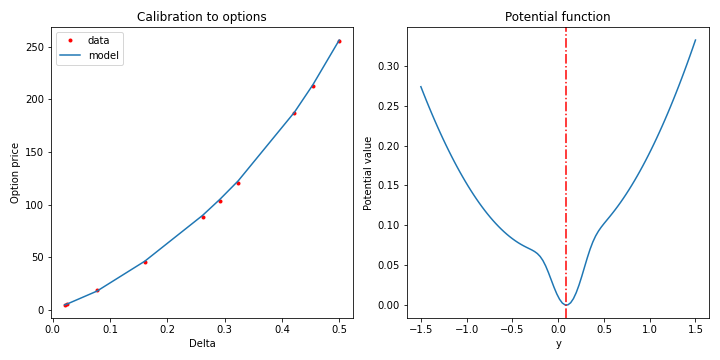

In the first example, we consider SPX 1M options on 07/12/2021 with maturity on 08/09/2021. The results of calibration are presented in Table 1 and Figs. 6 and 7. Note the difference in implied potentials for puts and calls, as well as different values of inferred model parameters. For both potentials, the current value of the log-return , as shown by the vertical red lines, is located near the bottom of the potential well. This suggests that the price dynamics on this date correspond to an equilibrium regime of small fluctuations around a stable minimum.

| MAPE | ||||||

|---|---|---|---|---|---|---|

| Puts | ||||||

| Calls |

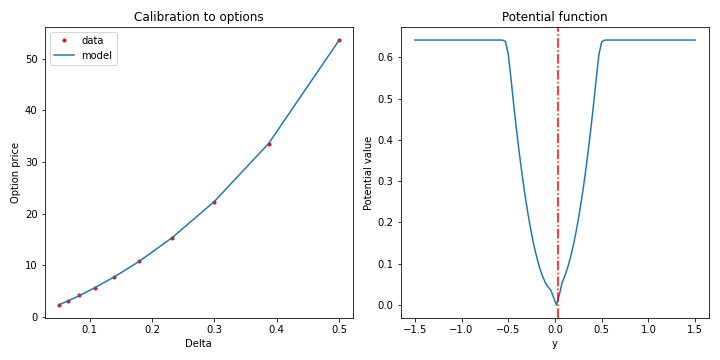

In the second example, we look at longer option tenors, and consider SPX 1Y options on 11/06/2020 with maturity on 09/21/2021. The results of calibration are presented in Table 2 and Figs. 8 and 9. Again, we note the difference in implied potentials for puts and calls, as well as different values of inferred model parameters. Also as in the previous example, for both potentials, the current value of the log-return is located near the bottom of the potential well, suggesting an equilibrium regime of small price fluctuations on this date.

| MAPE | ||||||

|---|---|---|---|---|---|---|

| Puts | ||||||

| Calls |

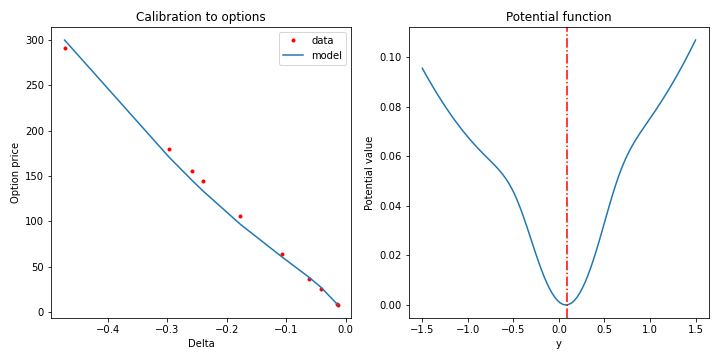

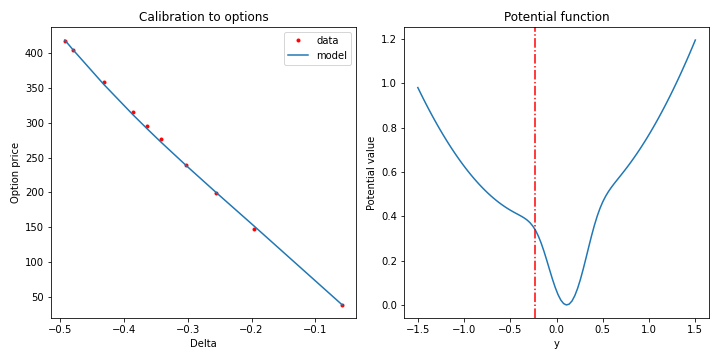

Finally, we consider an example of a severely distressed market. To this end, we analyze option quotes on 03/16/2020, at the peak of Covid-19 crisis where the SPX index had the largest drop. We consider 6M options with the expiry on 09/18/2020. The results of calibration are presented in Table 3 and Figs. 10 and 11. As in the previous examples, we again note the difference in implied potentials for puts and calls, as well as different values of inferred model parameters.

| MAPE | ||||||

|---|---|---|---|---|---|---|

| Puts | ||||||

| Calls |

Unlike the previous examples, for the present case of a distressed market, we note a very different pattern for the current value of the log-return . The current log-return is now located far away from the global minimum of the potential, suggesting strongly non-equilibrium dynamics on that date. Both sets of put and call market quotes indicate that the value of log-return observed on 03/16/2020 is a strongly non-equilibrium initial state, consistently with a prevailing market sentiment on that date.

Interestingly, while both implied potentials suggest that the current value is far from the global minimum of the potential and hence describes a non-equilibrium scenario, they differ in the character of a subsequent relaxation mechanism for this initial state. The implied potential for puts in Fig. 10 is a single-well potential, therefore the current state is an unstable state. If the potential itself remains constant through time, this initial state would eventually relax into its global minimum. This would happen even in the limit of zero volatility (zero noise). When the noise is present with , it produces both small fluctuations around this minimum, and uncertainty regarding the time needed to reach this minimum.

Differently from the puts, the call options seem to suggest a different type of relaxation dynamics. This is because unlike a single-well potential observed for the puts, the implied potential for the calls in Fig. 11 is a double well potential quite similar to the one shown in the left column in Fig. 1. The initial location is in the vicinity of the local minimum corresponding to the left well, while the right well corresponds to the global minimum. As they are separated by the barrrier, the potential in Fig. 11 describes a scenario of metastability. The relaxation to the global minimum (the true ground state) proceeds via instanton transitions as described in Sect. 2.4. This suggests that double well potentials implying metastable dynamics may occur when markets are in distress or during periods of a high market uncertainty, e.g. due to general elections. In particular, [13] found a bimodal implied distribution during British elections of 1987 (though not through other British elections in 1992), and suggested that option prices can be used to monitor the market sentiment during elections.

4.5 Discussion

Gaussian mixtures are frequently used for modeling non-Gaussian market returns on phenomenological grounds, with an objective to fit higher moments of returns such as skewness and kurtosis, see e.g. [25]. This paper shows that with a more theoretically motivated approach, a Gaussian mixture model for returns can instead be imposed as a model of a stationary distribution, which also fixes a non-linear potential in the Langevin dynamics. Using practical simplifications of the NES model presented in this section, the initial two-component Gaussian mixture that defines a square root of the stationary distribution in Eq.(20) is transformed into non-stationary three-component Gaussian mixtures (75) and (81) for the real-world and risk-neutral measures, respectively. The stationary component is parameterized in terms of parameters . A time-varying, pre-asymptotic component of a fixed-horizon distribution of market returns, is additionally driven by the volatility parameter .

Experiments show that the model is flexible and can provide accurate calibration to prices of put and call options on the SPX index for either a benign or stressed market regime. While for the former the implied potentials are typically of a single-well type, for a stressed market market environment we observe either a unstable or metastable initial state, as in Figs. 10 and 11. Due to flexibility of the Gaussian mixture model as a model of the ground state m the NES model is able to smoothly shift between stable dynamics with a single minimum, and metastable dynamics obtained when the potential has two local minima separated by a barrier. As illustrated in Fig. 2, the model can adapt to different values of skewness and kurtosis of market returns.

A particularly interesting observation is that when analyzed separately and not jointly as is done in most of related research in the literature, market quotes on the call and put options seem to produce generally different distributions and hence tell different stories about future market dynamics. As was mentioned above, this may be explained by a market segmentation between option buyers for calls and puts, and their reliance on possibly different quantitative or internal (mental) models of the world. Because we do not assume put-call parity and do not enforce a joint calibration to puts and calls, our framework is less restrictive as it does not assume that returns are not predictable [10]. Clearly, if the model is to be used to actually predict future returns from option data, it may benefit from not assuming that returns are not predictable in the first place. For such a task, an interesting practical question would be what type of option data (calls or puts) is better to use. We leave this question for a future work.

5 Summary and outlook

McCauley in his insightful and provocative book [26] pointed out various problems with traditional equilibrium approaches of classical financial models such as e.g. the CAPM model [28] or the Black-Scholes model [3]. In particular, he argued that fat tails in financial data, which is a matter of everyday concerns of practitioners and academics alike, may be simply the result of applying an unjustified binning process to non-stationary data. McCauley argued against a neoclassical economic doctrine based on the concept of a market-clearing equilibrium, and showed that among about five different definitions of a market equilibrium commonly used in the mathematical financial modeling literature, none makes sense from the physics’ perspective (see also [18] for related arguments). He also issued a challenge to econophysics as an emerging rival of the classical finance, where research often explicitly or implicitly assumes an equilibrium, potentially suffering from the same problem of a potential data distortion leading to the above-mentioned problem with problematically measured fat tails.

The Non-Equilibrium Skew (NES) model developed in this paper, as suggested by its name, provides a principled non-equilibrium view of market dynamics. It follows well defined definitions of equilibrium versus non-equilibrium dynamics as commonly accepted in the mathematical and physical literature. Equilibrium Langevin dynamics are obtained when a corresponding Langevin potential has a single stable minimum. Metastable or unstable dynamics are obtained if the potential has multiple minima. Using a two-component Gaussian mixture as the model of a ground state of a quantum mechanical system with a double well potential, we applied methods developed in supersymmetric quantum mechanics (SUSY QM) to find an analytical solution for non-equilibrium, pre-stationary dynamics.

As non-linear models rarely admit analytical solutions, they usually have much higher computational costs, which is often viewed as a main obstacle preventing their wider adaptation by practitioners. Therefore, availability of an analytical solution for non-linear non-equilibrium market dynamics may be considered a highly desirable property of a model.

Even though the first, SUSY QM-based formulation of the model is already analytically tractable, upon further simplifications, we produced a more practical version of the NES model based on insights derived from the previous analysis. The analytical approach further reduces the computational complexity to a very affordable mixture of three Gaussian distributions, where all parameters are fixed in terms of the original five parameters of the model. The amount of non-stationarity is directly encoded in these Gaussian mixture parameters, and thus can be directly estimated from the model fit to available data, assuming that a data-generating distribution is a non-equilibrium distribution. Note that while we only constructed the leading pre-asymptotic corrections to a stationary distribution, higher-order corrections can be computed along the same lines.