Coresets for Regressions with Panel Data

Abstract

This paper introduces the problem of coresets for regression problems to panel data settings. We first define coresets for several variants of regression problems with panel data and then present efficient algorithms to construct coresets of size that depend polynomially on (where is the error parameter) and the number of regression parameters – independent of the number of individuals in the panel data or the time units each individual is observed for. Our approach is based on the Feldman-Langberg framework in which a key step is to upper bound the “total sensitivity” that is roughly the sum of maximum influences of all individual-time pairs taken over all possible choices of regression parameters. Empirically, we assess our approach with synthetic and real-world datasets; the coreset sizes constructed using our approach are much smaller than the full dataset and coresets indeed accelerate the running time of computing the regression objective.

1 Introduction

Panel data, represented as and where is the number of entities/individuals, is the number of time periods and is the number of features is widely used in statistics and applied machine learning. Such data track features of a cross-section of entities (e.g., customers) longitudinally over time. Such data are widely preferred in supervised machine learning for more accurate prediction and unbiased inference of relationships between variables relative to cross-sectional data (where each entity is observed only once) [28, 6].

The most common method for inferring relationships between variables using observational data involves solving regression problems on panel data. The main difference between regression on panel data when compared to cross-sectional data is that there may exist correlations within observations associated with entities over time periods. Consequently, the regression problem for panel data is the following optimization problem over regression variables and the covariance matrix that is induced by the abovementioned correlations: Here denotes the observation matrix of entity whose -th row is and is constrained to have largest eigenvalue at most 1 where represents the correlation between time periods and . This regression model is motivated by the random effects model (Eq. (1) and Appendix A), common in the panel data literature [27, 24, 23]. A common way to define the correlation between observations is an autocorrelation structure [25, 35] whose covariance matrix is induced by a vector (integer ). This type of correlation results in the generalized least-squares estimator (GLSE), where the parameter space is .

As the ability to track entities on various features in real-time has grown, panel datasets have grown massively in size. However, the size of these datasets limits the ability to apply standard learning algorithms due to space and time constraints. Further, organizations owning data may want to share only a subset of data with others seeking to gain insights to mitigate privacy or intellectual property related risks. Hence, a question arises: can we construct a smaller subset of the panel data on which we can solve the regression problems with performance guarantees that are close enough to those obtained when working with the complete dataset?

One approach to this problem is to appeal to the theory of “coresets.” Coresets, proposed in [1], are weighted subsets of the data that allow for fast approximate inference for a large dataset by solving the problem on the smaller coreset. Coresets have been developed for a variety of unsupervised and supervised learning problems; for a survey, see [43]. But, thus, far coresets have been developed only for -regression cross-sectional data [18, 36, 8, 15, 33]; no coresets have been developed for regressions on panel data – an important limitation, given their widespread use and advantages.

Roughly, a coreset for cross-sectional data is a weighted subset of observations associated with entities that approximates the regression objective for every possible choice of regression parameters. An idea, thus, is to construct a coreset for each time period (cross-section) and output their union as a coreset for panel data. However, this union contains at least observations which is undesirable since can be large. Further, due to the covariance matrix , it is not obvious how to use this union to approximately compute regression objectives. With panel data, one needs to consider both how to sample entities, and within each entity how to sample observations across time. Moreover, we also need to define how to compute regression objectives on such a coreset consisting of entity-time pairs.

Our contributions. We initiate the study of coresets for versions of -regression with panel data, including the ordinary least-squares estimator (OLSE; Definition 2.2), the generalized least-squares estimator (GLSE; Definition 2.3), and a clustering extension of GLSE (GLSEk; Definition 2.4) in which all entities are partitioned into clusters and each cluster shares the same regression parameters.

Overall, we formulate the definitions of coresets and propose efficient construction of -coresets of sizes independent of and . Our key contributions are:

-

1.

We give a novel formulation of coresets for GLSE (Definition 3.3) and GLSEk (Definition 3.4). We represent the regression objective of GLSE as the sum of sub-functions w.r.t. entity-time pairs, which enables us to define coresets similar to the case of cross-sectional data. For GLSEk, the regression objective cannot be similarly decomposed due to the operations in Definition 2.4. To deal with this issue, we define the regression objective on a coreset by including operations.

- 2.

-

3.

Our coreset for GLSE consists of at most points (Theorem 4.1), independent of and as desired.

-

4.

Our coreset for GLSEk is of size (Theorem 5.2) where upper bounds the gap between the maximum individual regression objective of OLSE and the minimum one (Definition 5.1). We provide a matching lower bound (Theorem 5.4) for , indicating that the coreset size should contain additional factors than , justifying the -bounded assumption.

Our coresets for GLSE/GLSEk leverage the Feldman-Langberg (FL) framework [21] (Algorithms 1 and 2). The variables make the objective function of GLSE non-convex in contrast to the cross-sectional data setting where objective functions are convex. Thus, bounding the “sensitivity” (Lemma 4.4) of each entity-time pair for GLSE, which is a key step in coreset construction using the FL framework, becomes significantly difficult. We handle this by upper-bounding the maximum effect of , based on the observation that the gap between the regression objectives of GLSE and OLSE with respect to the same is always constant, which enables us to reduce the problem to the cross-sectional setting. For GLSEk, a key difficulty is that the clustering centers are subspaces induced by regression vectors, instead of points as in Gaussian mixture models or -means. Hence, it is unclear how GLSEk can be reduced to projective clustering used in Gaussian mixture models; see [20]. To bypass this, we consider observation vectors of an individual as one entity and design a two-staged framework in which the first stage selects a subset of individuals that captures the operations in the objective function and the second stage applies our coreset construction for GLSE on each selected individuals. As in the case of GLSE, bounding the “sensitivity” (Lemma 5.8) of each entity for GLSEk is a key step at the first stage. Towards this, we relate the total sensitivity of entities to a certain “flexibility” (Lemma 5.7) of each individual regression objective which is, in turn, shown to be controlled by the -bounded assumption (Definition 5.1).

We implement our GLSE coreset construction algorithm and test it on synthetic and real-world datasets while varying . Our coresets perform well relative to uniform samples on multiple datasets with different generative distributions. Importanty, the relative performance is robust and better on datasets with outliers. The maximum empirical error of our coresets is always below the guaranteed unlike with uniform samples. Further, for comparable levels of empircal error, our coresets perform much better than uniform sampling in terms of sample size and coreset construction speed.

1.1 Related work

With panel data, depending on different generative models, there exist several ways to define -regression [27, 24, 23], including the pooled model, the fixed effects model, the random effects model, and the random parameters model. In this paper, we consider the random effects model (Equation (1)) since the number of parameters is independent of and (see Section A for more discussion).

For cross-sectional data, there is more than a decade of extensive work on coresets for regression; e.g., -regression [18, 36, 8, 15, 33], -regression [11, 47, 12], generalized linear models [31, 40] and logistic regression [44, 31, 42, 49]. The most relevant for our paper is -regression (least-squares regression), which admits an -coreset of size [8] and an accurate coreset of size [33].

With cross-sectional data, coresets have been developed for a large family of problems in machine learning and statistics, including clustering [21, 22, 30], mixture model [37], low rank approximation [16], kernel regression [53] and logistic regression [42]. We refer interested readers to recent surveys [41, 19]. It is interesting to investigate whether these results can be generalized to panel data.

There exist other variants of regression sketches beyond coreset, including weighted low rank approximation [13], row sampling [17], and subspace embedding [47, 39]. These methods mainly focus on the cross-sectional setting. It is interesting to investigate whether they can be adapted to the panel data setting that with an additional covariance matrix.

2 -regression with panel data

We consider the following generative model of -regression: for ,

| (1) |

where and is the error term drawn from a normal distribution. Sometimes, we may include an additional entity or individual specified effect so that the outcome can be represented by . This is equivalent to Equation (1) by appending an additional constant feature to each observation .

Remark 2.1

Sometimes, we may not observe individuals for all time periods, i.e., some observation vectors and their corresponding outcomes are missing. One way to handle this is to regard those missing individual-time pairs as . Then, for any vector , we have for each missing individual-time pairs.

As in the case of cross-sectional data, we assume there is no correlation between individuals. Using this assumption, the -regression function can be represented as follows: for any regression parameters ( is the parameter space), where is the individual regression function. Depending on whether there is correlation within individuals and whether is unique, there are several variants of . The simplest setting is when all s are the same, say , and there is no correlation within individuals. This setting results in the ordinary least-squares estimator (OLSE); summarized in the following definition.

Definition 2.2 (Ordinary least-squares estimator (OLSE))

For an ordinary least-squares estimator (OLSE), the parameter space is and for any the individual objective function is

Consider the case when are the same but there may be correlations between time periods within individuals. A common way to define the correlation is called autocorrelation [25, 35], in which there exists , where is an integer and , such that

| (2) |

This autocorrelation results in the generalized least-squares estimator (GLSE).

Definition 2.3 (Generalized least-squares estimator (GLSE))

For a generalized least-squares estimator (GLSE) with (integer ), the parameter space is and for any the individual objective function is equal to

The main difference from OLSE is that a sub-function is not only determined by a single observation ; instead, the objective of may be decided by up to contiguous observations .

Motivated by -means clustering [48], we also consider a generalized setting of GLSE, called GLSEk ( is an integer), in which all individuals are partitioned into clusters and each cluster corresponds to the same regression parameters with respect to some GLSE.

Definition 2.4 (GLSEk: an extention of GLSE)

Let be integers. For a GLSEk, the parameter space is and for any the individual objective function is

GLSEk is a basic problem with applications in many real-world fields; as accounting for unobserved heterogeneity in panel regressions is critical for unbiased estimates [3, 26]. Note that each individual selects regression parameters () that minimizes its individual regression objective for GLSE. Note that GLSE1 is exactly GLSE. Also note that GLSEk can be regarded as a generalized version of clustered linear regression [4], in which there is no correlation within individuals.

3 Our coreset definitions for panel data

In this section, we show how to define coresets for regression on panel data, including OLSE and GLSE. Due to the additional autocorrelation parameters, it is not straightforward to define coresets for GLSE as in the cross-sectional setting. One way is to consider all observations of an individual as an indivisible group and select a collection of individuals as a coreset. However, this construction results in a coreset of size depending on , which violates the expectation that the coreset size should be independent of and . To avoid a large coreset size, we introduce a generalized definition: coresets of a query space, which captures the coreset definition for OLSE and GLSE.

Definition 3.1 (Query space [21, 9])

Let be a index set together with a weight function . Let be a set called queries, and be a given loss function w.r.t. . The total cost of with respect to a query is The tuple is called a query space. Specifically, if for all , we use for simplicity.

Intuitively, represents a linear combination of weighted functions indexed by , and represents the ground set of . Due to the separability of , we have the following coreset definition.

Definition 3.2 (Coresets of a query space [21, 9])

Let be a query space and be an error parameter. An -coreset of is a weighted set together with a weight function such that for any ,

Here, is a computation function over the coreset that is used to estimate the total cost of . By Definitions 2.2 and 2.3, the regression objectives of OLSE and GLSE can be decomposed into sub-functions. Thus, we can apply the above definition to define coresets for OLSE and GLSE. Note that OLSE is a special case of GLSE for . Thus, we only need to provide the coreset definition for GLSE. We let and . The index set of GLSE has the following form:

where each element consists of at most observations. Also, for every and , the cost function is: if , and if , Thus, is a query space of GLSE.111Here, we slightly abuse the notation by using instead of . Then by Definition 3.2, we have the following coreset definition for GLSE.

Definition 3.3 (Coresets for GLSE)

Given a panel dataset and , a constant , integer , and parameter space , an -coreset for GLSE is a weighted set together with a weight function such that for any ,

The weighted set is exactly an -coreset of the query space . Note that the number of points in this coreset is at most . Specifically, for OLSE, the parameter space is since , and the corresponding index set is Consequently, the query space of OLSE is .

Coresets for GLSEk

Due to the operation in Definition 2.4, the objective function can only be decomposed into sub-functions instead of individual-time pairs. Then let , , and We can regard as a query space of GLSEk. By Definition 3.2, an -coreset of is a subset together with a weight function such that for any ,

| (3) |

However, each consists of observations, and hence, the number of points in this coreset is . To avoid the size dependence of , we propose a new coreset definition for GLSEk. The intuition is to further select a subset of time periods to estimate .

Given , we denote as the collection of individuals that appear in . Moreover, for each , we denote to be the collection of observations for individual in .

Definition 3.4 (Coresets for GLSEk)

Given a panel dataset and , constant , integer , and parameter space , an -coreset for GLSEk is a weighted set together with a weight function such that for any ,

The key is to incorporate operations in the computation function over the coreset. Similar to GLSE, the number of points in such a coreset is at most .

4 Coresets for GLSE

In this section, we show how to construct coresets for GLSE. We let the parameter space be for some constant where . The assumption of the parameter space for is based on the fact that () is a stationary condition for [35].

Theorem 4.1 (Coresets for GLSE)

There exists a randomized algorithm that, for a given panel dataset and , constants and integer , with probability at least , constructs an -coreset for GLSE of size

and runs in time .

Note that the coreset in the above theorem contains at most points , which is independent of both and . Also note that if both and are away from 0, e.g., the number of points in the coreset can be further simplified:

4.1 Algorithm for Theorem 4.1

We summarize the algorithm of Theorem 4.1 in Algorithm 1, which takes a panel dataset as input and outputs a coreset of individual-time pairs. The main idea is to use importance sampling (Lines 6-7) leveraging the Feldman-Langberg (FL) framework [21, 9]. The key new step appears in Line 5, which computes a sensitivity function for GLSE that defines the sampling distribution. Also note that the construction of is based on another function (Line 4), which is actually a sensitivity function for OLSE that has been studied in the literature [8].

4.2 Useful notations and useful facts for Theorem 4.1

Feldman and Langberg [21] show how to construct coresets by importance sampling and the coreset size has been improved by [9].

Theorem 4.2 (FL framework [21, 9])

Let . Let be an upper bound of the pseudo-dimension. Suppose is a sensitivity function satisfying that for any , and . Let be constructed by taking

samples, where each sample is selected with probability and has weight . Then, with probability at least , is an -coreset for GLSE.

Here, the sensitivity function measures the maximum influence for each .

Note that the above is an importance sampling framework that takes samples from a distribution proportional to sensitivities. The sample complexity is controlled by the total sensitivity and the pseudo-dimension . Hence, to apply the FL framework, we need to upper bound the pseudo-dimension and construct a sensitivity function.

4.3 Proof of Theorem 4.1

Algorithm 1 applies the FL framework (Feldman and Langberg [21]) that constructs coresets by importance sampling and the coreset size has been improved by [9]. The key is to verify the “pseudo-dimension” (Lemma 4.3) and “sensitivities” (Lemma 4.4) separately; summarized as follows.

Upper bounding the pseudo-dimension.

We have the following lemma that upper bounds the pseudo-dimension of .

Lemma 4.3 (Pseudo-dimension of GLSE)

The pseudo-dimension of any query space over weight functions is at most .

The proof can be found in Section 4.4. The main idea is to apply the prior results [2, 52] which shows that the pseudo-dimension is polynomially dependent on the number of regression parameters ( for GLSE) and the number of operations of individual regression objectives ( for GLSE). Consequently, we obtain the bound in Lemma 4.3.

Constructing a sensitivity function.

Next, we show that the function constructed in Line 5 of Algorithm 1 is indeed a sensitivity function of GLSE that measures the maximum influence for each ; summarized by the following lemma.

Lemma 4.4 (Total sensitivity of GLSE)

Function of Algorithm 1 satisfies that for any , and . Moreover, the construction time of function is .

Intuitively, if the sensitivity is large, e.g., close to 1, must contribute significantly to the objective with respect to some parameter . The sampling ensures that we are likely to include such pair in the coreset for estimating . Due to the fact that the objective function of GLSE is non-convex which is different from OLSE, bounding the sensitivity of each individual-time pair for GLSE becomes significantly difficult. To handle this difficulty, we develop a reduction of sensitivities from GLSE to OLSE (Line 5 of Algorithm 1), based on the relations between and , i.e., for any we prove that The first inequality follows from the fact that the smallest eigenvalue of (the inverse covariance matrix induced by ) is at least . The intuition of the second inequality is from the form of function , which relates to individual-time pairs, say . Combining these two inequalities, we obtain a relation between the sensitivity function for GLSE and the sensitivity function for OLSE, based on the following observation: for any ,

which leads to the construction of in Line 5 of Algorithm 1. Then it suffices to construct (Lines 2-4 of Algorithm 1), which reduces to the cross-sectional data setting and has total sensitivity at most (Lemma 4.7). Consequently, we conclude that the total sensitivity of GLSE is by the definition of .

Now we are ready to prove Theorem 4.1.

Proof:

[Proof of Theorem 4.1] By Lemma 4.4, the total sensitivity is . By Lemma 4.3, we let . Pluging the values of and in the FL framework [21, 9], we prove for the coreset size. For the running time, it costs time to compute the sensitivity function by Lemma 4.4, and time to construct an -coreset. This completes the proof.

4.4 Proof of Lemma 4.3: Upper bounding the pseudo-dimension

Our proof idea is similar to that in [37]. For preparation, we need the following lemma which is proposed to bound the pseudo-dimension of feed-forward neural networks.

Lemma 4.5 (Restatement of Theorem 8.14 of [2])

Let be a given query space where for any and , and . Suppose that can be computed by an algorithm that takes as input the pair and returns after no more than of the following operations:

-

•

the arithmetic operations , and on real numbers.

-

•

jumps conditioned on , and comparisons of real numbers, and

-

•

output 0,1.

Then the pseudo-dimension of is at most .

Note that the above lemma requires that the range of functions is . We have the following lemma which can help extend this range to .

Lemma 4.6 (Restatement of Lemma 4.1 of [52])

Let be a given query space. Let be the indicator function satisfying that for any , and ,

Then the pseudo-dimension of is precisely the pseudo-dimension of the query space .

Now we are ready to prove Lemma 4.3.

Proof:

[Proof of Lemma 4.3] Fix a weight function . For every , let be the indicator function satisfying that for any and ,

We consider the query space . By the definition of , the dimension of is . By the definition of , can be calculated using operations, including arithmetic operations and a jump. Pluging the values of and in Lemma 4.5, the pseudo-dimension of is . Then by Lemma 4.6, we complete the proof.

4.5 Proof of Lemma 4.4: Bounding the total sensitivity

We prove Lemma 4.4 by relating sensitivities between GLSE and OLSE. For preparation, we give the following lemma that upper bounds the total sensitivity of OLSE. Given two integers , denote to be the computation time of a column basis of a matrix in . For instance, a column basis of a matrix in can be obtained by computing its SVD decomposition, which costs time by [14].

Lemma 4.7 (Total sensitivity of OLSE)

Function of Algorithm 1 satisfies that for any ,

| (4) |

and satisfying . Moreover, the construction time of function is .

Proof:

The proof idea comes from [51]. By Line 3 of Algorithm 1, is a matrix whose columns form a unit basis of the column space of . We have and hence . Moreover, for any and , we have

Then by Cauchy-Schwarz and orthonormality of , we have that for any and ,

| (5) |

where is the -th row of .

For each , we let . Then . Note that constructing costs time and computing all costs time.

Thus, it remains to verify that satisfies Inequality (4). For any and , letting , we have

This completes the proof.

Now we are ready to prove Lemma 4.4.

Proof:

[Proof of Lemma 4.4] For any , recall that is defined by

We have that

Hence, the total sensitivity . By Lemma 4.7, it costs time to construct . We also know that it costs time to compute function . Since , this completes the proof for the running time.

Thus, it remains to verify that satisfies that

Since always holds, we only need to consider the case that

We first show that for any ,

| (6) |

Given an autocorrelation vector , the induced covariance matrix satisfies that where

| (7) |

Then by Equation (7), the smallest eigenvalue of satisfies that

| (8) |

Also we have

which proves Inequality (6). We also claim that for any ,

| (9) |

This trivially holds for . For , this is because

Now combining Inequalities (6) and (9), we have that for any ,

This completes the proof.

5 Coresets for GLSEk

Following from Section 4, we assume that the parameter space is for some given constant . Given a panel dataset and , let denote a matrix whose -th row is for all (). Assume there exists constant such that the input dataset satisfies the following property.

Definition 5.1 (-bounded dataset)

Given , we say a panel dataset and is -bounded if for any , the condition number of matrix is at most , i.e.,

If there exists and such that , we let . Specifically, if all are identity matrix whose eigenvalues are all 1, i.e., for any , , we can set . Another example is that if and all elements of are independently and identically distributed standard normal random variables, then the condition number of matrix is upper bounded by some constant with high probability (and constant in expectation) [10, 46], which may also imply . The main theorem is as follows.

Theorem 5.2 (Coresets for GLSEk)

There exists a randomized algorithm that given an -bounded () panel dataset and , constant and integers , with probability at least 0.9, constructs an -coreset for GLSEk of size

and runs in time .

Similar to GLSE, this coreset for GLSEk () contains at most

points , which is independent of both and when is constant. Note that the size contains an addtional factor which can be unbounded. Our algorithm is summarized in Algorithm 2 and we outline Algorithm 2 and discuss the novelty in the following.

Remark 5.3

Algorithm 2 is a two-staged framework, which captures the operations in GLSEk.

First stage.

We construct an -coreset together with a weight function of the query space , i.e., for any

The idea is similar to Algorithm 1 except that we consider sub-functions instead of . In Lines 2-4 of Algorithm 2, we first construct a sensitivity function of OLSEk. The definition of captures the impact of operations in the objective function of OLSEk and the total sensitivity of is guaranteed to be upper bounded by Definition 5.1. The key is showing that the maximum influence of individual is at most (Lemma 5.7), which implies that the total sensitivity of is at most . Then in Line 5, we construct a sensitivity function of GLSEk, based on a reduction from (Lemma 5.8).

Second stage.

In Line 8, for each , apply ) and construct a subset together with a weight function . Output together with a weight function defined as follows: for any , .

We also provide a lower bound theorem which shows that the size of a coreset for GLSEk can be up to . It indicates that the coreset size should contain additional factors than , which reflects the reasonability of the -bounded assumption.

Theorem 5.4 (Size lower bound of GLSEk)

Let and and . There exists and such that any 0.5-coreset for GLSEk should have size .

5.1 Proof overview

We first give a proof overview for summarization.

Proof overview of Theorem 5.2.

For GLSEk, we propose a two-staged framework (Algorithm 2): first sample a collection of individuals and then run on every selected individuals. By Theorem 4.1, each subset at the second stage is of size . Hence, we only need to upper bound the size of at the first stage. By a similar argument as that for GLSE, we can define the pseudo-dimension of GLSEk and upper bound it by , and hence, the main difficulty is to upper bound the total sensitivity of GLSEk. We show that the gap between the individual regression objectives of GLSEk and OLSEk (GLSEk with ) with respect to the same is at most , which relies on and an observation that for any , Thus, it suffices to provide an upper bound of the total sensitivity for OLSEk. We claim that the maximum influence of individual is at most where is the largest eigenvalue of and is the smallest eigenvalue of . This fact comes from the following observation: and results in an upper bound of the total sensitivity for OLSEk since

Proof overview of Theorem 5.4.

For GLSEk, we provide a lower bound of the coreset size by constructing an instance in which any 0.5-coreset should contain observations from all individuals. Note that we consider which reduces to an instance with cross-sectional data. Our instance is to let and for all . Then letting where , and , we observe that . Hence, all individuals should be contained in the coreset such that regression objectives with respect to all are approximately preserved.

5.2 Proof of Theorem 5.2: Upper bound for GLSEk

The proof of Theorem 5.2 relies on the following two theorems. The first theorem shows that of Algorithm 2 is an -coreset of . The second one is a reduction theorem that for each individual in constructs an -coreset .

Theorem 5.5 (Coresets of )

For any given -bounded observation matrix and outcome matrix , constant and integers , with probability at least 0.95, the weighted subset of Algorithm 2 is an -coreset of the query space , i.e., for any ,

| (10) |

Moreover, the construction time of is

We defer the proof of Theorem 5.5 later.

Theorem 5.6 (Reduction from coresets of to coresets for GLSEk)

Proof:

Proof:

Proof of Theorem 5.5: is a coreset of .

It remains to prove Theorem 5.5. Note that the construction of applies the Feldman-Langberg framework. The analysis is similar to Section 4 in which we provide upper bounds for both the total sensitivity and the pseudo-dimension.

We first discuss how to bound the total sensitivity of . Similar to Section 4.5, the idea is to first bound the total sensitivity of – we call it the query space of OLSEk whose covariance matrices of all individuals are identity matrices.

Lemma 5.7 (Total sensitivity of OLSEk)

Function of Algorithm 2 satisfies that for any ,

| (11) |

and satisfying that . Moreover, the construction time of function is

Proof:

For every , recall that is the matrix whose -th row is for all . By definition, we have that for any ,

Thus, by the same argument as in Lemma 4.7, it suffices to prove that for any matrix sequences ,

| (12) |

For any and any , letting , we have

Thus, we directly conclude that

Hence, Inequality (12) holds. Moreover, since the input dataset is -bounded, we have

which completes the proof of correctness.

For the running time, it costs to compute SVD decompositions for all . Then it costs time to compute all and , and hence costs time to compute sensitivity functions . Thus, we complete the proof.

Note that by the above argument, we can also assume

which leads to the same upper bound for the total sensitivity . Now we are ready to upper bound the total sensitivity of .

Lemma 5.8 (Total sensitivity of GLSEk)

Function of Algorithm 2 satisfies that for any ,

| (13) |

and satisfying that . Moreover, the construction time of function is

Proof:

Since it only costs time to construct function if we have , we prove the construction time by Lemma 5.7.

Fix . If in Line 4 of Algorithm 2, then Inequality (13) trivally holds. Then we assume that . We first have that for any and any ,

which directly implies that

| (14) |

We also note that for any and any ,

Hence, we have that

| (15) |

This implies that

| (16) |

Thus, we have that for any and ,

which proves Inequality (13). Moreover, we have that

where the last inequality is from Lemma 5.7. We complete the proof.

Next, we upper bound the pseudo-dimension of GLSEk. The proof is similar to that of GLSE by applying Lemmas 4.5 and 4.6.

Lemma 5.9 (Pseudo-dimension of GLSEk)

The pseudo-dimension of any query space over weight functions is at most

Proof:

The proof idea is similar to that of Lemma 4.3. Fix a weight function . For every , let be the indicator function satisfying that for any and ,

We consider the query space . By the definition of , the dimension of is . Also note that for any , can be represented as a multivariant polynomial that consists of terms where , and . Thus, can be calculated using operations, including arithmetic operations and jumps. Pluging the values of and in Lemma 4.5, the pseudo-dimension of is . Then by Lemma 4.6, we complete the proof.

Proof:

[Proof of Theorem 5.5] By Lemma 5.8, the total sensitivity of is . By Lemma 5.9, we can let which is an upper bound of the pseudo-dimension of every query space over weight functions . Pluging the values of and in Theorem 4.2, we prove for the coreset size.

For the running time, it costs time to compute the sensitivity function by Lemma 5.8, and time to construct . This completes the proof.

5.3 Proof of Theorem 5.4: Lower bound for GLSEk

Actually, we prove a stronger version of Theorem 5.4 in the following. We show that both the coreset size and the total sensitivity of the query space may be , even for the simple case that and .

Theorem 5.10 (Size and sensitivity lower bound of GLSEk)

Let and and . There exists an instance and such that the total sensitivity

and any 0.5-coreset of the query space should have size .

Proof:

We construct the same instance as in [49]. Concretely, for , let and . We claim that for any ,

| (17) |

If the claim is true, then we complete the proof of the total sensitivity by summing up the above inequality over all . Fix and consider the following where , and . If , we have

Similarly, if , we have

By the above equations, we have

| (18) |

Combining with the fact that , we prove Inequality (17).

For the coreset size, suppose together with a weight function is a 0.5-coreset of the query space . We only need to prove that . Suppose there exists some with . Letting where , and , we have that

which contradicts with the assumption of . Thus, we have that for any , . Next, by contradiction assume that . Again, letting where , and , we have that

which contradicts with the assumption of . This completes the proof.

6 Empirical results

We implement our coreset algorithms for GLSE, and compare the performance with uniform sampling on synthetic datasets and a real-world dataset. The experiments are conducted by PyCharm on a 4-Core desktop CPU with 8GB RAM.222Codes are in https://github.com/huanglx12/Coresets-for-regressions-with-panel-data.

Datasets. We experiment using synthetic datasets with ( observations), , and . For each individual , we first generate a mean vector by first uniformly sampling a unit vector , and a length , and then letting . Then for each time period , we generate observation from a multivariate normal distribution [50].333The assumption that the covariance of each individual is proportional to is common in econometrics. We also fix the last coordinate of to be 1 to capture individual specific fixed effects. Next, we generate outcomes . First, we generate a regression vector from distribution . Then we generate an autoregression vector by first uniformly sampling a unit vector and a length , and then letting . Based on , we generate error terms as in Equation (2). To assess performance robustness in the presence of outliers, we simulate another dataset replacing in Equation (2) with the heavy tailed Cauchy(0,2) distribution [38]. Finally, the outcome is the same as Equation (1).

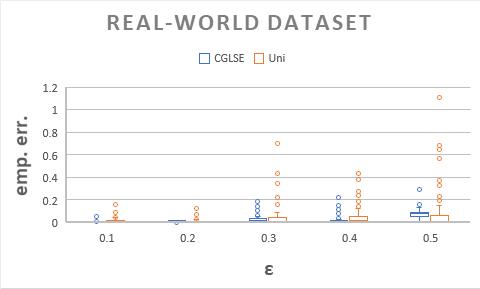

We also experiment on a real-world dataset involving the prediction of monthly profits from customers for a credit card issuer as a function of demographics, past behaviors, and current balances and fees. The panel dataset consisted of 250k observations: 50 months of data () from 5000 customers () with 11 features (). We set and .

Baseline and metrics. As a baseline coreset, we use uniform sampling (Uni), perhaps the simplest approach to construct coresets: Given an integer , uniformly sample individual-time pairs with weight for each.

Given regression parameters and a subset , we define the empirical error as . We summarize the empirical errors by maximum, average, standard deviation (std) and root mean square error (RMSE), where RMSE. By penalizing larger errors, RMSE combines information in both average and standard deviation as a performance metric,. The running time for solving GLSE on dataset and our coreset are and respectively. is the running time for coreset construction .

Simulation setup. We vary and generate 100 independent random tuples (the same as described in the generation of the synthetic dataset). For each , we run our algorithm and Uni to generate coresets. We guarantee that the total number of sampled individual-time pairs of and Uni are the same. We also implement IRLS [32] for solving GLSE. We run IRLS on both the full dataset and coresets and record the runtime.

Results. Table 1 summarizes the accuracy-size trade-off of our coresets for GLSE for different error guarantees . The maximum empirical error of Uni is always larger than that of our coresets (1.16-793x). Further, there is no error guarantee with Uni, but errors are always below the error guarantee with our coresets. The speed-up with our coresets relative to full data () in solving GLSE is 1.2x-108x. To achieve the maximum empirical error of .294 for GLSE in the real-world data, only 1534 individual-time pairs (0.6%) are necessary for . With Uni, to get the closest maximum empirical error of 0.438, at least 2734 individual-time pairs) (1.1%) is needed; i.e.., achieves a smaller empirical error with a smaller sized coreset. Though Uni may sometimes provide lower average error than , it always has higher RMSE, say 1.2-745x of . When there are outliers as with Cauchy, our coresets perform even better on all metrics relative to Uni. This is because captures tails/outliers in the coreset, while Uni does not. Figure 1 presents the boxplots of the empirical errors.

| max. emp. err. | avg./std./RMSE of emp. err. | size | (s) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Uni | Uni | ||||||||

| synthetic (G) | 0.1 | .005 | .015 | .001/.001/.002 | .007/.004/.008 | 116481 | 2 | 372 | 458 |

| 0.2 | .018 | .029 | .006/.004/.008 | .010/.007/.013 | 23043 | 2 | 80 | 458 | |

| 0.3 | .036 | .041 | .011/.008/.014 | .014/.010/.017 | 7217 | 2 | 29 | 458 | |

| 0.4 | .055 | .086 | .016/.012/.021 | .026/.020/.032 | 3095 | 2 | 18 | 458 | |

| 0.5 | .064 | .130 | .019/.015/.024 | .068/.032/.075 | 1590 | 2 | 9 | 458 | |

| synthetic (C) | 0.1 | .001 | .793 | .000/.000/.001 | .744/.029/.745 | 106385 | 2 | 1716 | 4430 |

| 0.2 | .018 | .939 | .013/.003/.014 | .927/.007/.927 | 21047 | 2 | 346 | 4430 | |

| 0.3 | .102 | .937 | .072/.021/.075 | .860/.055/.862 | 6597 | 2 | 169 | 4430 | |

| 0.4 | .070 | .962 | .051/.011/.053 | .961/.001/.961 | 2851 | 2 | 54 | 4430 | |

| 0.5 | .096 | .998 | .060/.026/.065 | .992/.004/.992 | 472 | 2 | 41 | 4430 | |

| real-world | 0.1 | .029 | .162 | .005/.008/.009 | .016/.026/.031 | 50777 | 3 | 383 | 2488 |

| 0.2 | .054 | .154 | .017/.004/.017 | .012/.024/.026 | 13062 | 3 | 85 | 2488 | |

| 0.3 | .187 | .698 | .039/.038/.054 | .052/.106/.118 | 5393 | 3 | 24 | 2488 | |

| 0.4 | .220 | .438 | .019/.033/.038 | .050/.081/.095 | 2734 | 3 | 20 | 2488 | |

| 0.5 | .294 | 1.107 | .075/.038/.084 | .074/.017/.183 | 1534 | 3 | 16 | 2488 | |

7 Conclusion, limitations, and future work

This paper initiates a theoretical study of coreset construction for regression problems with panel data. We formulate the definitions of coresets for several variants of -regression, including OLSE, GLSE, and GLSEk. For each variant, we propose efficient algorithms that construct a coreset of size independent of both and , based on the FL framework. Our empirical results indicate that our algorithms can accelerate the evaluation time and perform significantly better than uniform sampling.

For GLSEk, our coreset size contains a factor , which may be unbounded and result in a coreset of size in the worst case. In practice, if is large, each sensitivity in Line 5 of Algorithm 2 will be close or even equal to 1. In this case, is drawn from all individuals via uniform sampling which weakens the performance of Algorithm 2 relative to Uni. Future research should investigate whether a different assumption than the -bound can generate a coreset of a smaller size.

There are several directions for future work. Currenly, and have a relatively large impact on coreset size; future work needs to reduce this effect. This will advance the use of coresets for machine learning, where is typically large, and is large in high frequency data. This paper focused on coreset construction for panel data with -regression. The natural next steps would be to construct coresets with panel data for other regression problems, e.g., -regression, generalized linear models and logistic regression, and beyond regression to other supervised machine learning algorithms.

Broader impact.

In terms of broader impact on practice, many organizations have to routinely outsource data processing to external consultants and statisticians. But a major practical challenge for organizations in doing this is to minimize issues of data security in terms of exposure of their data for potential abuse. Further, minimization of such exposure is considered as necessary due diligence by laws such as GDPR and CCPA which mandates firms to minimize security breaches that violate the privacy rights of the data owner [45, 34]. Coreset based approaches to sharing data for processing can be very valuable for firms in addressing data security and to be in compliance with privacy regulations like GDPR and CCPA.

Further, for policy and managerial decision making in economics, social sciences and management, obtaining unbiased estimates of the regression relationships from observational data is critical. Panel data is a critical ingredient for obtaining such unbiased estimates. As ML methods are being adopted by many social scientists [5], ML scholars are becoming sensitive to these issues and our work in using coreset methods for panel data can have significant impact for these scholars.

A practical concern is that coresets constructed and shared for one purpose or model may be used by the data processor for other kinds of models, which may lead to erroneous conclusions. Further, there is also the potential for issues of fairness to arise as different groups may not be adequately represented in the coreset without incorporating fairness constraints [29]. These issues need to be explored in future research.

Acknowledgements

This research was conducted when LH was at Yale and was supported in part by an NSF CCF-1908347 grant.

References

- [1] Pankaj K Agarwal, Sariel Har-Peled, and Kasturi R Varadarajan. Approximating extent measures of points. Journal of the ACM (JACM), 51(4):606–635, 2004.

- [2] Martin Anthony and Peter L Bartlett. Neural network learning: Theoretical foundations. Cambridge University press, 2009.

- [3] Manuel Arellano. Panel Data Econometrics. 2002.

- [4] Bertan Ari and H Altay Güvenir. Clustered linear regression. Knowledge-Based Systems, 15(3):169–175, 2002.

- [5] Susan Athey. Machine learning and causal inference for policy evaluation. In Proceedings of the 21th ACM SIGKDD international conference on knowledge discovery and data mining, pages 5–6, 2015.

- [6] Badi Baltagi. Econometric analysis of panel data. John Wiley & Sons, 2008.

- [7] Joshua Batson, Daniel A Spielman, and Nikhil Srivastava. Twice-ramanujan sparsifiers. SIAM Journal on Computing, 41(6):1704–1721, 2012.

- [8] Christos Boutsidis, Petros Drineas, and Malik Magdon-Ismail. Near-optimal coresets for least-squares regression. IEEE transactions on information theory, 59(10):6880–6892, 2013.

- [9] Vladimir Braverman, Dan Feldman, and Harry Lang. New frameworks for offline and streaming coreset constructions. CoRR, abs/1612.00889, 2016.

- [10] Zizhong Chen and Jack J. Dongarra. Condition numbers of gaussian random matrices. SIAM Journal on Matrix Analysis and Applications, 27(3):603–620, 2005.

- [11] Kenneth L Clarkson. Subgradient and sampling algorithms for regression. In Proceedings of the sixteenth annual ACM-SIAM symposium on Discrete algorithms, pages 257–266. Society for Industrial and Applied Mathematics, 2005.

- [12] Kenneth L Clarkson, Petros Drineas, Malik Magdon-Ismail, Michael W Mahoney, Xiangrui Meng, and David P Woodruff. The fast cauchy transform and faster robust linear regression. SIAM Journal on Computing, 45(3):763–810, 2016.

- [13] Kenneth L. Clarkson and David P. Woodruff. Low-rank approximation and regression in input sparsity time. Journal of the ACM (JACM), 63:1 – 45, 2017.

- [14] Alan Kaylor Cline and Inderjit S Dhillon. Computation of the singular value decomposition. Citeseer, 2006.

- [15] Michael B Cohen, Yin Tat Lee, Cameron Musco, Christopher Musco, Richard Peng, and Aaron Sidford. Uniform sampling for matrix approximation. In Proceedings of the 2015 Conference on Innovations in Theoretical Computer Science, pages 181–190. ACM, 2015.

- [16] Michael B Cohen, Cameron Musco, and Christopher Musco. Input sparsity time low-rank approximation via ridge leverage score sampling. In Proceedings of the Twenty-Eighth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1758–1777. SIAM, 2017.

- [17] Michael B. Cohen and Richard Peng. L row sampling by lewis weights. In Proceedings of the Forty-Seventh Annual ACM on Symposium on Theory of Computing, STOC 2015, Portland, OR, USA, June 14-17, 2015, pages 183–192, 2015.

- [18] Petros Drineas, Michael W Mahoney, and Shan Muthukrishnan. Sampling algorithms for regression and applications. In Proceedings of the seventeenth annual ACM-SIAM symposium on Discrete algorithm, pages 1127–1136. Society for Industrial and Applied Mathematics, 2006.

- [19] Dan Feldman. Core-sets: An updated survey. Wiley Interdiscip. Rev. Data Min. Knowl. Discov., 10(1), 2020.

- [20] Dan Feldman, Zahi Kfir, and Xuan Wu. Coresets for gaussian mixture models of any shape. arXiv preprint arXiv:1906.04895, 2019.

- [21] Dan Feldman and Michael Langberg. A unified framework for approximating and clustering data. In Proceedings of the forty-third annual ACM symposium on Theory of computing, pages 569–578. ACM, 2011. https://arxiv.org/abs/1106.1379.

- [22] Dan Feldman, Melanie Schmidt, and Christian Sohler. Turning big data into tiny data: Constant-size coresets for -means, PCA and projective clustering. In Proceedings of the Twenty-Fourth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1434–1453. SIAM, 2013.

- [23] Edward W Frees et al. Longitudinal and panel data: analysis and applications in the social sciences. Cambridge University Press, 2004.

- [24] William E Griffiths, George G Judge, R Carter Hill, Helmut Lütkepohl, and Tsoung-Chao Lee. The Theory and Practice of Econometrics. Wiley, 1985.

- [25] John N Haddad. A simple method for computing the covariance matrix and its inverse of a stationary autoregressive process. Communications in Statistics-Simulation and Computation, 27(3):617–623, 1998.

- [26] Charles N. Halaby. Panel models in sociological research: Theory into practice. Review of Sociology, 30(1):507–544, 2004.

- [27] Daniel Hoechle. Robust standard errors for panel regressions with cross-sectional dependence. The stata journal, 7(3):281–312, 2007.

- [28] Cheng Hsiao. Analysis of panel data. Analysis of Panel Data, by Cheng Hsiao, pp. 382. ISBN 0521818559. Cambridge, UK: Cambridge University Press, February 2003., page 382, 2003.

- [29] Lingxiao Huang, Shaofeng Jiang, and Nisheeth K. Vishnoi. Coresets for clustering with fairness constraints. In Advances in Neural Information Processing Systems, pages 7587–7598, 2019.

- [30] Lingxiao Huang and Nisheeth K. Vishnoi. Coresets for clustering in euclidean spaces: Importance sampling is nearly optimal. In STOC 2020: 52nd Annual ACM Symposium on Theory of Computing, pages 1416–1429, 2020.

- [31] Jonathan Huggins, Trevor Campbell, and Tamara Broderick. Coresets for scalable Bayesian logistic regression. In Advances in Neural Information Processing Systems, pages 4080–4088, 2016.

- [32] Murray Jorgensen. Iteratively reweighted least squares. Encyclopedia of Environmetrics, 3, 2006.

- [33] Ibrahim Jubran, Alaa Maalouf, and Dan Feldman. Fast and accurate least-mean-squares solvers. In Advances in Neural Information Processing Systems, pages 8305–8316, 2019.

- [34] T Tony Ke and K Sudhir. Privacy rights and data security: Gdpr and personal data driven markets. Available at SSRN 3643979, 2020.

- [35] James P LeSage. The theory and practice of spatial econometrics. University of Toledo. Toledo, Ohio, 28(11), 1999.

- [36] Mu Li, Gary L Miller, and Richard Peng. Iterative row sampling. In 2013 IEEE 54th Annual Symposium on Foundations of Computer Science, pages 127–136. IEEE, 2013.

- [37] Mario Lucic, Matthew Faulkner, Andreas Krause, and Dan Feldman. Training Gaussian mixture models at scale via coresets. The Journal of Machine Learning Research, 18(1):5885–5909, 2017.

- [38] Ping Ma, Michael W. Mahoney, and Bin Yu. A statistical perspective on algorithmic leveraging. In Proceedings of the 31th International Conference on Machine Learning, ICML 2014, Beijing, China, 21-26 June 2014, pages 91–99, 2014.

- [39] Xiangrui Meng and Michael W. Mahoney. Low-distortion subspace embeddings in input-sparsity time and applications to robust linear regression. In Symposium on Theory of Computing Conference, STOC’13, Palo Alto, CA, USA, June 1-4, 2013, pages 91–100, 2013.

- [40] Alejandro Molina, Alexander Munteanu, and Kristian Kersting. Core dependency networks. In Thirty-Second AAAI Conference on Artificial Intelligence, 2018.

- [41] Alexander Munteanu and Chris Schwiegelshohn. Coresets-methods and history: A theoreticians design pattern for approximation and streaming algorithms. Künstliche Intell., 32(1):37–53, 2018.

- [42] Alexander Munteanu, Chris Schwiegelshohn, Christian Sohler, and David Woodruff. On coresets for logistic regression. In Advances in Neural Information Processing Systems, pages 6561–6570, 2018.

- [43] Jeff M Phillips. Coresets and sketches. arXiv preprint arXiv:1601.00617, 2016.

- [44] Sashank J Reddi, Barnabás Póczos, and Alexander J Smola. Communication efficient coresets for empirical loss minimization. In UAI, pages 752–761, 2015.

- [45] Supreeth Shastri, Melissa Wasserman, and Vijay Chidambaram. The seven sins of personal-data processing systems under GDPR. In 11th USENIX Workshop on Hot Topics in Cloud Computing (HotCloud 19), 2019.

- [46] Lin Shi, Taibin Gan, Hong Zhu, and Xianming Gu. The exact distribution of the condition number of complex random matrices. The Scientific World Journal, 2013(2013):729839–729839, 2013.

- [47] Christian Sohler and David P. Woodruff. Subspace embeddings for the l-norm with applications. In Proceedings of the 43rd ACM Symposium on Theory of Computing, STOC 2011, San Jose, CA, USA, 6-8 June 2011, pages 755–764, 2011.

- [48] Pang-Ning Tan, Michael Steinbach, Vipin Kumar, et al. Cluster analysis: basic concepts and algorithms. Introduction to data mining, 8:487–568, 2006.

- [49] Elad Tolochinsky and Dan Feldman. Generic coreset for scalable learning of monotonic kernels: Logistic regression, sigmoid and more. arXiv: Learning, 2018.

- [50] Yung Liang Tong. The multivariate normal distribution. Springer Science & Business Media, 2012.

- [51] Kasturi Varadarajan and Xin Xiao. On the sensitivity of shape fitting problems. In 32nd International Conference on Foundations of Software Technology and Theoretical Computer Science, page 486, 2012.

- [52] Mathukumalli Vidyasagar. A theory of learning and generalization. Springer-Verlag, 2002.

- [53] Yan Zheng and Jeff M Phillips. Coresets for kernel regression. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 645–654. ACM, 2017.

Appendix A Discussion of the generative model (1)

In this section, we discuss the equivalence between the generative model (1) and the random effects estimator. In random effects estimators, there exist additional individual specific effects , i.e.,

| (19) |

and we assume that all individual effects are drawn from a normal distribution, i.e.,

where is the mean and is the covariance of an unknown normal distribution. By Equation (19), for any , we let where . Then Equation (19) can be rewritten as

Let denote the covariance matrix among error terms . Next, we simplify by . Consequently, error terms satisfy that

By this assumption, a random effects estimator can be defined by the following:

Thus, we verify that the random effects estimator is equivalent to the generative model (1).

Appendix B Existing results and approaches for OLSE

We note that finding an -coreset of for OLSE can be reduced to finding an -coreset for least-squares regression with cross-sectional data. For completeness, we summarize the following theorems for OLSE whose proofs mainly follow from the literature.

Theorem B.1 (-Coresets for OLSE [8])

There exists a deterministic algorithm that for any given observation matrix , outcome matrix , a collection and constant , constructs an -coreset of size of OLSE, with running time where is the time needed to compute the left singular vectors of a matrix in .

Theorem B.2 (Accurate coresets for OLSE [33])

There exists a deterministic algorithm that for any given observation matrix , outcome matrix , a collection , constructs an accurate coreset of size of OLSE, with running time .

B.1 Proof of Theorem B.1

We first prove Theorem B.1 and propose the corresponding algorithm that constructs an -coreset. Recall that denotes the domain of possible vectors .

Proof:

[Proof of Theorem B.1] Construct a matrix by letting the -th row of be for . Similarly, construct a vector by letting . Then for any , we have

Thus, finding an -coreset of of OLSE is equivalent to finding a row-sampling matrix whose rows are basis vectors and a rescaling matrix that is a diagonal matrix such that for any ,

By Theorem 1 of [8], we only need which completes the proof of correctness. Note that Theorem 1 of [8] only provides a theoretical guarantee of a weak-coreset which only approximately preserves the optimal least-squares value. However, by the proof of Theorem 1 of [8], their coreset indeed holds for any .

The running time also follows from Theorem 1 of [8], which can be directly obtained by the algorithm stated below.

Algorithm in [8].

We then introduce the approach of [8] as follows. Suppose we have inputs and .

-

1.

Compute the SVD of . Let where and .

- 2.

-

3.

Output and .

B.2 Proof of Theorem B.2

Next, we prove Theorem B.2 and propose the corresponding algorithm that constructs an accurate coreset.

Proof:

[Proof of Theorem B.2] The proof idea is similar to that of Theorem B.1. Again, we construct a matrix by letting the -th row of be for . Similarly, construct a vector by letting . Then for any , we have

Thus, finding an -coreset of of OLSE is equivalent to finding a row-sampling matrix whose rows are basis vectors and a rescaling matrix that is a diagonal matrix such that for any ,

By Theorem 3.2 of [33], we only need . Moreover, we can construct matrices and in time by applying , and in Theorem 3.2 of [33].

Main approach in [33].

Suppose we have inputs and . Let For any , we let and have that

The main idea of [33] is to construct a sub-matrix of whose rows are of the form for some and , such that . Then we have for any ,

By the definition of , there exists a row-sampling matrix and a rescaling matrix such that .

We then discuss why such a sub-matrix exists. The main observation is that and

Thus, is inside the convex hull of matrices . By the Caratheodory’s Theorem, there must exist at most matrices whose convex hull also contains . Then can be represented as a linear combination of these matrices, and hence, the sub-matrix exists.

Algorithm 1 of [33] shows how to directly construct such a matrix . However, the running time is which is undesirable. To accelerate the running time, Jubran et al. [33] apply the following idea.

-

1.

For each , set as the concatenation of the entries of . Let be the collection of these points . Then our objective is reduced to finding a subset of size such that the convex hull of contains .

-

2.

Compute a balanced partition of into clusters of roughly the same size. By the Caratheodory’s Theorem, there must exist at most partitions such that the convex hull of their union contains . The main issue is how to these partitions efficiently.

-

3.

To address this issue, Jubran et al. [33] compute a sketch for each partition including its size and the weighted mean

The construction of sketches costs time. The key observation is that there exists a set of at most points such that the convex hull of their union contains by the Caratheodory’s Theorem. Moreover, the corresponding partitions of these are what we need – the convex hull of contains . Note that the construction of costs time. Overall, it costs time to obtain the collection whose convex hull contains .

-

4.

We repeat the above procedure over until obtaining an accurate coreset of size . By the value of , we note that

i.e., we half the size of the input set by an iteration. Thus, there are at most iterations and the overall running time is