Experimental Design for Regret Minimization in Linear Bandits

Andrew Wagenmaker∗ Julian Katz-Samuels∗ Kevin Jamieson

University of Washington ajwagen@cs.washington.edu University of Washington jkatzsam@cs.washington.edu University of Washington jamieson@cs.washington.edu

Abstract

In this paper we propose a novel experimental design-based algorithm to minimize regret in online stochastic linear and combinatorial bandits. While existing literature tends to focus on optimism-based algorithms–which have been shown to be suboptimal in many cases–our approach carefully plans which action to take by balancing the tradeoff between information gain and reward, overcoming the failures of optimism. In addition, we leverage tools from the theory of suprema of empirical processes to obtain regret guarantees that scale with the Gaussian width of the action set, avoiding wasteful union bounds. We provide state-of-the-art finite time regret guarantees and show that our algorithm can be applied in both the bandit and semi-bandit feedback regime. In the combinatorial semi-bandit setting, we show that our algorithm is computationally efficient and relies only on calls to a linear maximization oracle. In addition, we show that with slight modification our algorithm can be used for pure exploration, obtaining state-of-the-art pure exploration guarantees in the semi-bandit setting. Finally, we provide, to the best of our knowledge, the first example where optimism fails in the semi-bandit regime, and show that in this setting our algorithm succeeds.

1 INTRODUCTION

Multi-armed bandits have received much attention in recent years as they serve as an excellent model for developing algorithms that adeptly deal with the exploration-exploitation tradeoff. In this paper, we consider the stochastic linear bandit problem in which there is a set of arms and an unknown parameter . An agent plays a sequential game where at each round she chooses an arm and receives a noisy reward whose mean is . The goal is to maximize the reward over a given time horizon . An important special case of stochastic linear bandits is the combinatorial setting where , which can be used to model problems such as finding a shortest path in a graph or the best weighted matching in a bipartite graph. We consider both the bandit feedback setting, where the agent receives a noisy observation of , and the semi-bandit feedback setting, where the agent receives a noisy observation of for each with .

Existing regret minimization algorithms for linear bandits suffer from several important shortcomings. First, they typically rely on naive union bounds, which yield regret guarantees scaling as either or . Such union bounds ignore the geometry present in the problem and, as such, can be very wasteful. As the union bound often appears in the confidence interval within the algorithm, this is not simply an analysis issue—it can also affect real performance. Second, in the moderate, non-asymptotic time regime, existing algorithms tend to rely on the principle of optimism—pulling only the arms they believe may be optimal. Algorithms relying on this principle are very myopic, foregoing initial exploration which could lead to better long-term reward and instead focusing on obtaining short-term reward, leading to suboptimal long-term performance. This is a well-known effect in the bandit setting but, as we show, is also present in the semi-bandit setting.

In this paper, we develop an algorithm overcoming both of these shortcomings. Rather than employing a naive union bound, we appeal to tools from empirical process theory for controlling the suprema of a Gaussian process, allowing us to obtain confidence bounds that are geometry-dependent and potentially much tighter. In addition, our algorithm relies on careful planning to balance the exploration-exploitation tradeoff, taking into account both the potential information gain as well as the reward obtained when pulling an arm. This planning allows us to collect sufficient information for good long-term performance without incurring too much initial regret and, to the best of our knowledge, is the first planning-based algorithm in the linear bandit setting that provides finite-time guarantees.

We emphasize that we are interested in the non-asymptotic regime and aim to optimize the whole regret bound, including lower-order terms. While several recent works achieve instance-optimal regret, they suffer from loose lower-order terms which dominate the regret for small to moderate . Our results aim to minimize such terms through employing tighter union bounds. We summarize our contributions:

-

•

We develop a single, general algorithm that achieves a state-of-the-art finite-time regret bound in stochastic linear bandits, in combinatorial bandits with bandit feedback, and in combinatorial bandits with semi-bandit feedback. In addition, our framework is general enough to extend to settings as diverse as partial monitoring and graph bandits.

-

•

We show that in the combinatorial semi-bandit regime, our algorithm is computationally efficient, relying only on calls to a linear maximization oracle, and state-of-the-art, yielding a significant improvement on existing works in the non-asymptotic time horizon regime.

-

•

We give the first example for combinatorial bandits with semi-bandit feedback that shows that optimistic strategies such as UCB and Thompson Sampling can do arbitrarily worse than the asymptotic lower bound, and show that our algorithm improves on optimism in this setting by an arbitrarily large factor.

-

•

As a corollary, we obtain the first computationally efficient algorithm for pure exploration in combinatorial bandits with semi-bandit feedback, and achieve a state-of-the-art sample complexity.

This work can be seen as obtaining problem-dependent minimax bounds—minimax bounds that depend on the arm set but hold for all values of the reward vector—and are similar in spirit to the bounds on regret minimization in MDPs given by Zanette and Brunskill (2019). For some favorable arm sets , our bounds are tighter than prior -independent minimax bounds by large dimension factors. To the best of our knowledge, we are the first to obtain such geometry-dependent minimax bounds for linear bandits.

2 PRELIMINARIES

Let denote the diameter of . will refer to the operator which sets all elements in a matrix not on the diagonal to 0. hides logarithmic terms. denotes the simplex over . We use to refer to probability distributions over and to denote the probability on . We let refer to allocations over and, similarly, to denote the weight on . We will somewhat interchangeably use to refer to the vector in and the sum of its elements, , but it will always be clear from context which we are referring to. If , we will often write for and for . Throughout, we will let denote the dimension of the ambient space and .

We are interested primarily in regret minimization in linear bandits. Given some set , at every timestep we choose and receive reward , for some unknown . We will define regret as:

Throughout, we assume that . We consider two observation models: semi-bandit feedback and bandit feedback. In the bandit feedback setting, at every timestep we observe:

where . In the semi-bandit feedback setting, we assume that our bandit instance is combinatorial, , and at every timestep we observe:

where . Note that, while we assume Gaussian noise for simplicity, all our results will hold with sub-Gaussian noise (Katz-Samuels et al., 2020).

In the bandit setting, after observations, our estimate of will be the standard least squares estimate:

In the semi-bandit setting, we will estimate coordinate-wise, forming the estimate:

where is the number of times . We denote:

For convenience we assume the optimal arm is unique and denote it by . As is standard, we denote the gap of arm by . We denote the minimum gap as and the maximum gap by .

In the combinatorial setting, can often be exponentially large in the dimension, making computational efficiency non-trivial since cannot be efficiently enumerated. As such, much of the literature on combinatorial bandits has focused on obtaining algorithms that rely only on an argmax oracle:

Efficient argmax oracles are available in many settings, for instance finding the minimum weighted matching in a bipartite graph and finding the shortest path in a directed acyclic graph.

3 MOTIVATING EXAMPLES

Before presenting our algorithm and main results, we present several examples that motivate the necessity of planning and the wastefulness of naive union bounds, and illustrate how our algorithm is able to make improvements in both these aspects.

First, we show that an optimistic strategy cannot be optimal for combinatorial bandits with semi-bandit feedback. Consider a generic optimistic algorithm that maintains an estimate of at round and selects the maximizer of an upper confidence bound, . We make two assumptions on the confidence bound . First, we assume that . Second, we assume that the confidence bound is at least as good as a confidence bound formed from taking the least squares estimate

where is a universal constant. We call this algorithm the generic optimistic algorithm and let denote its regret. Then we have the following.

Proposition 1.

Fix any and . Then there exists a -dimensional combinatorial bandit problem with semi-bandit feedback where:

and Algorithm 1 has expected regret bounded as, for any :

Thus, treating as a constant, the asymptotic regret of the generic optimistic algorithm is loose by a square root dimension factor, and Algorithm 1 in the current paper improves over optimism by an arbitrarily large factor. As it also relies on the principle of optimism, albeit in a randomized fashion, Thompson Sampling will be suboptimal by this same factor on this instance. A similar instance can also be found in the bandit feedback setting. The improvement in Algorithm 1 is due to its ability to pull informative but suboptimal arms if the information gain outweighs the regret incurred, reducing the cumulative regret. Optimistic algorithms, in contrast, will only pull arms they believe may be optimal, and so do not effectively take into account the information gain which, in some cases, causes them to be very suboptimal.

To illustrate the improvement we gain by applying a less naive union bound, we will consider the following combinatorial class:

where . This class corresponds to the Cartesian product of a Top- problem on dimension and a Top- problem on dimension . As we will show, the minimax regret of Algorithm 1 scales with , a measure of the Gaussian width of , as defined below in (1). In contrast, algorithms that apply naive union bounds have regret that scales either with or . The following proposition illustrates the improvement in scaling we are able to obtain, as well as the subtle dependence of minimax regret on the geometry of .

Proposition 2.

For , on the product of Top- instances described above, we have:

This implies there exist settings of , and such that the regret of Algorithm 1 with either bandit feedback or semi-bandit feedback will be bounded:

while algorithms employing naive union bounds will achieve regret bounds scaling at best as:

In the appendix we discuss in more detail how the regret scales for specific algorithms in this setting. The regret bound we present for our algorithm in Proposition 2 is in fact state-of-the-art—all other existing algorithms will incur the larger dimension dependence.

4 EXPERIMENTAL DESIGN FOR REGRET MINIMIZATION

4.1 Gaussian Width

Before introducing our algorithm, we present a final concept critical to our results. For a fixed , let , then, for :

| (1) |

Intuitively, is the largest Gaussian width of any subset of formed by taking all with gap bounded by . The following results are helpful in giving some sense of the scaling of .

Proposition 3.

For any and , we have:

Proposition 4.

If , , and , then, for :

Note that these upper bounds are often loose. The following results shows that, in some cases, we pay a instead of .

Proposition 5.

There exists a combinatorial bandit instance in with where:

The Gaussian width is critical in avoiding wasteful union bounds, allowing instead for geometry-dependent confidence intervals. The following confidence interval will form a key piece in our analysis.

Proposition 6 (Tsirelson-Ibragimov-Sudakov Inequality (Katz-Samuels et al., 2020; Tsirelson et al., 1976)).

Consider playing arm times, where is an allocation chosen deterministically. Assume is set to correspond to the type of feedback received and let be the least squares estimate of from these observations. Then, simultaneously for all , with probability at least :

4.2 Algorithm Overview

| (2) | ||||

We next present our algorithm, RegretMED, in Algorithm 1. Inspired by several recent algorithms achieving asymptotically optimal regret (Lattimore and Szepesvari, 2017), at every epoch our algorithm finds a new allocation by solving an experimental design problem (2). This minimizes an upper bound on the regret incurred in the epoch while ensuring the allocation produced will explore enough to improve the estimates of the gaps for each arm, thereby balancing exploration and exploitation and allowing us to obtain a tight bound on finite-time regret. We apply the TIS inequality to bound the estimation error of our gaps, which motivates the constraint in (2). Critically, this yields a regret bound scaling with the Gaussian width of the action set.

We define SPARSE to be a function taking as input an allocation and returning a new allocation that is sparse and approximating the solution to (2). So long as in the semi-bandit setting and in the bandit setting, it is possible to find a distribution that is sparse and will achieve the same value of the constraint and objective of (2), see Lemma 1. MINGAP takes as input an estimate of and returns the gap between the best and second best arms in with respect to this . It is possible to compute this quantity efficiently with only calls to a linear maximization oracle (see Appendix C).

While Algorithm 1 takes as input , we require this only to simplify the analysis. In practice, we can use an upper bound instead without changing the final regret of our algorithm by more than a logarithmic factor. Since , an upper bound can be obtained without knowledge of .

Key Theoretical Tools: We briefly describe the key theoretical tools employed by RegretMED. First, we note that an experimental design based algorithm is novel in the setting of regret minimization. As we have shown, this approach allows us to perform properly on challenging instances by explicitly balancing the information gain and reward, while also yielding a computationally feasible solution in the semi-bandit regime. Our second innovation is the use of the TIS inequality to obtain tight concentration bounds. While we are not the first to utilize this in the linear bandit setting (Katz-Samuels et al., 2020), it previously was only utilized in the best arm identification setting, and our work therefore shows how it can be applied in the regret minimization setting as well. The use of the TIS inequality yields two important improvements over more naive union bounds. First, it provides tighter confidence intervals in the non-asymptotic time regime and therefore yields improved regret bounds. Second, as we will see, it allows us to write the constraint for our experiment design problem (2) in a form that is linear in the the decision variable. This allows us to reduce solving the optimization to calls of a linear maximization oracle, and is a key piece in showing our algorithm is computationally efficient.

4.3 Main Regret Bound

We now state our main regret bound. Define

and . Let .

Theorem 1.

With set to correspond to the type of feedback received, Algorithm 1 will have gap-dependent regret bounded, with probability , as:

and minimax regret bounded as:

for absolute constants and .

The proof of this result is deferred to Appendix B. See Section 6 and Table 1 for a summary of how this bound scales in particular settings of interest. As a brief comparison, in the semi-bandit feedback setting, considering expected regret, we obtain a leading term of order , which matches the lower bound (Degenne and Perchet, 2016), while the previous state-of-the-art scaled as (Perrault et al., 2020a). Algorithm 1 is then the first algorithm to achieve the lower bound for arbitrary combinatorial structures. In the bandit feedback setting our minimax regret scales as while LinUCB obtains regret scaling as (Abbasi-Yadkori et al., 2011). Proposition 3 shows that we are never worse than the LinUCB regret and, as Proposition 2 shows, we can sometimes be much better. In Appendix A, we present a modified algorithm which avoids the factors of on the leading term of the minimax regret, although it suffers from several other shortcomings.

4.4 Computationally Efficient Algorithm

While Algorithm 1 can be run in settings where is enumerable, it becomes computationally infeasible for very large , as (2) cannot be solved via a linear maximization oracle. In place of (2), consider instead solving:

| (3) | |||

As we show in Theorem 4, we can solve this problem with a computationally feasible algorithm in the semi-bandit feedback regime. Running this modified version of Algorithm 1, we obtain the following regret bound.

Theorem 2.

4.5 Pure Exploration with Semi-Bandit Feedback

Although our algorithm is designed to minimize regret, a slight modification gives a computationally efficient algorithm for best arm identification in the semi-bandit feedback setting. In particular, instead of (2) consider solving:

| (4) | |||

Then we have the following.

Theorem 3.

We state and prove a lower bound for this problem in the appendix, Theorem 6, which shows that this sample complexity is near-optimal. To the best of our knowledge, this is the first general, computationally efficient, and near optimal algorithm for pure exploration with semi-bandit feedback.

4.6 Optimization

In this section, we provide a polynomial-time algorithm for solving (3) in the semi-bandit feedback setting. The generic optimization problem can be written as follows for a fixed , , , and :

| (5) | |||

The following result shows that there exists a polynomial-time algorithm that finds an approximately optimal solution, i.e., it is within a constant approximation factor of the optimal solution.

Theorem 4.

Let opt be the optimal value of (5). There exists an Algorithm that returns such that , , and, with probability at least :

Furthermore, the number linear maximization oracle calls is polynomial in .

We briefly sketch the algorithmic approach. We recast (5) as a series of feasibility problems and employ the Plotkin-Shmoys-Tardos reduction of convex feasibility programs to online learning to solve each of these feasibility programs using the multiplicative weights update algorithm. To employ this reduction, we fix and develop a solver for the Lagrangian of (5), , which we show to be convex and strongly-smooth in over a carefully constructed subset of the simplex . We solve by employing stochastic Frank-Wolfe, which maintains sparse iterates to overcome the challenge posed by the exponential number of variables in . Evaluating the gradient requires computing for

which can be solved using only linear maximization oracle calls via the binary search procedure from Katz-Samuels et al. (2020). The proof of this result and full algorithm is given in Section D.

Rounding: The allocation is not integer, so must be rounded. Naive rounding could incur problematically large regret, so we instead seek a sparse allocation, which will allow us to round without incurring significant regret. Recalling that , we have:

Lemma 1.

We prove this result and state how this rounded distribution can be computed in Appendix E.

5 EXPERIMENTAL RESULTS

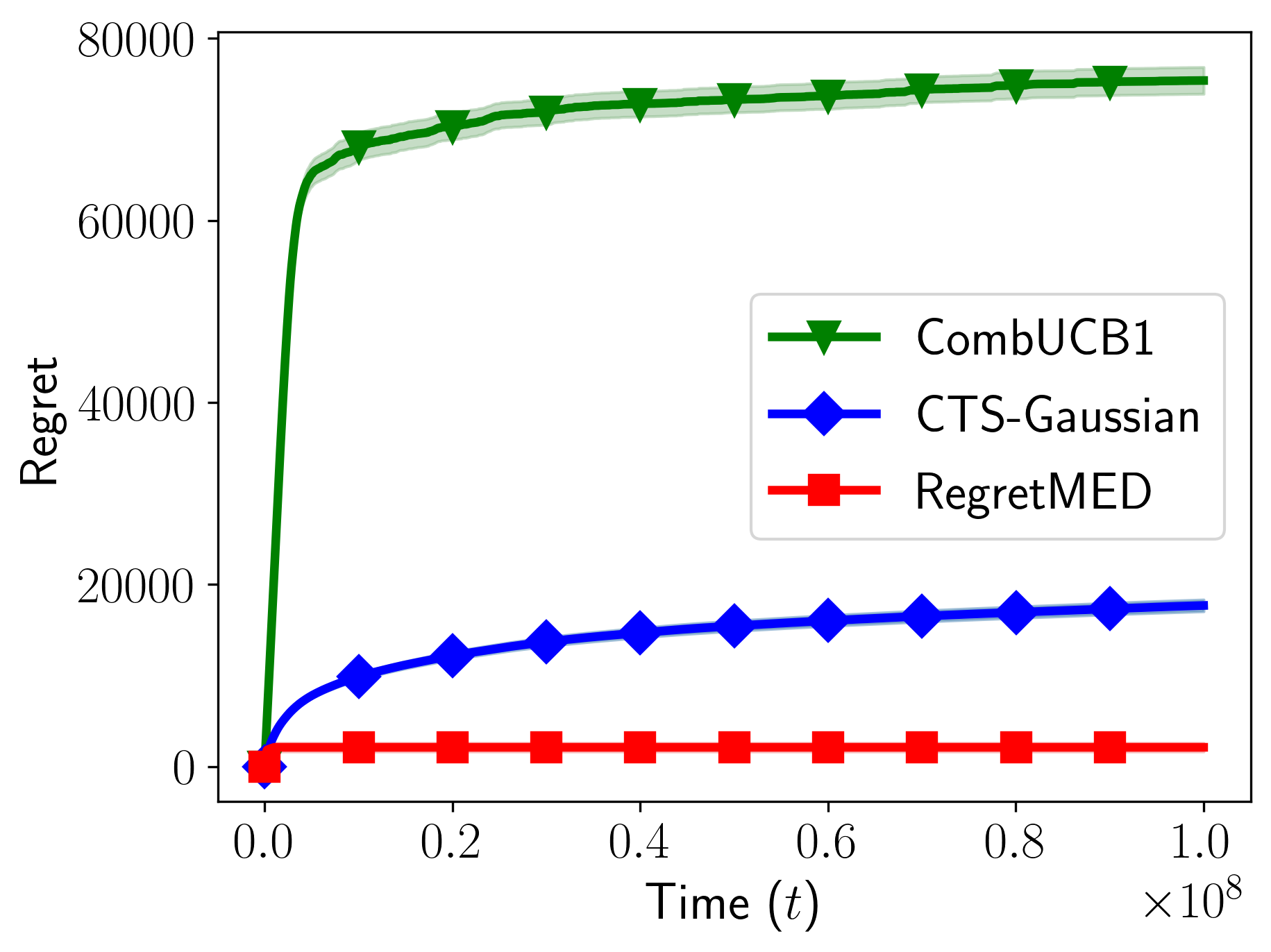

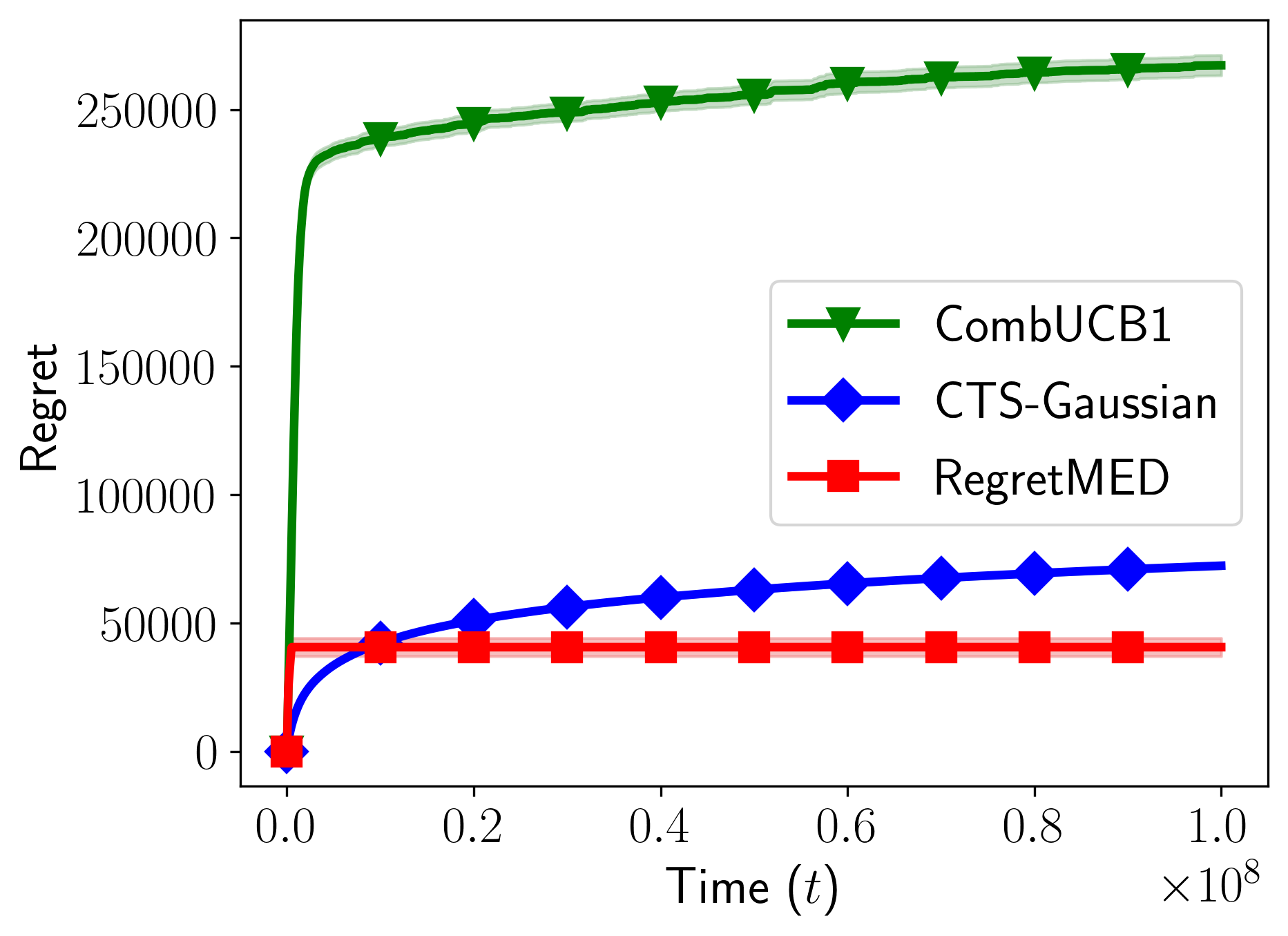

We next present experimental results for RegretMED in both the semi-bandit and bandit feedback settings. Every point in each plot is the average of 50 trials. The error bars indicate one standard error.

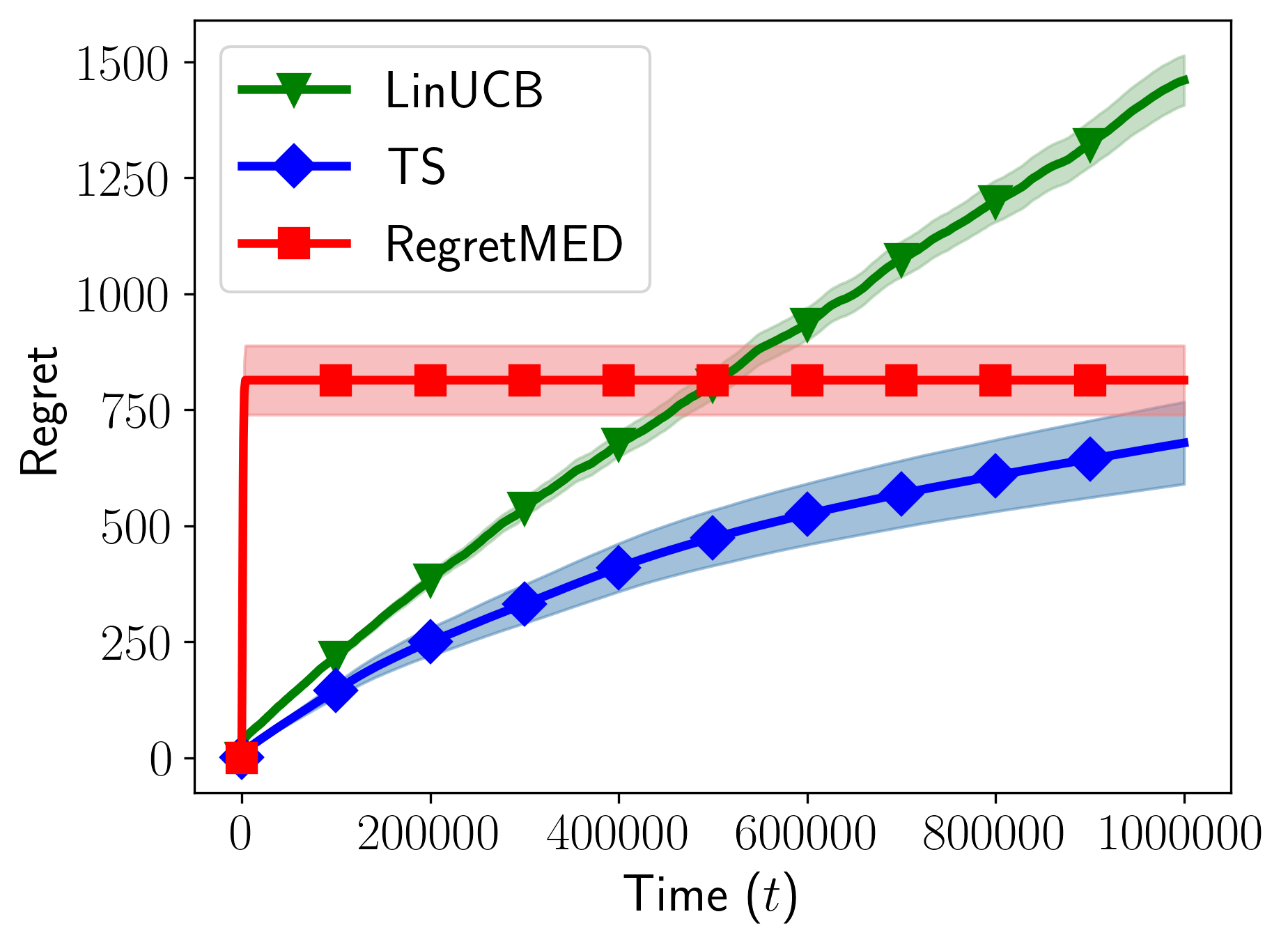

Semi-Bandit Feedback: We compare the computationally efficient version of RegretMED against CombUCB1 (Kveton et al., 2015) and CTS-Gaussian (Perrault et al., 2020a), a formulation of Thompson Sampling in the semi-bandit setting. As a test instance, we consider a resource allocation problem where an agent is tasked with maximizing profit subject to production cost. In particular, assume there are buyers, each offering a different price for a good. At each timestep the agent can sell to any number of them, but incurs an additional production cost for each item they sell. The agent observes a noisy realization of the price the buyer they sold to is willing to pay and of the production cost. In particular, if at time we sell to buyers , we will pay production costs , where is the production cost of producing the th good. We can model this problem with , corresponding to the prices each buyer will pay, and corresponding to the costs, .

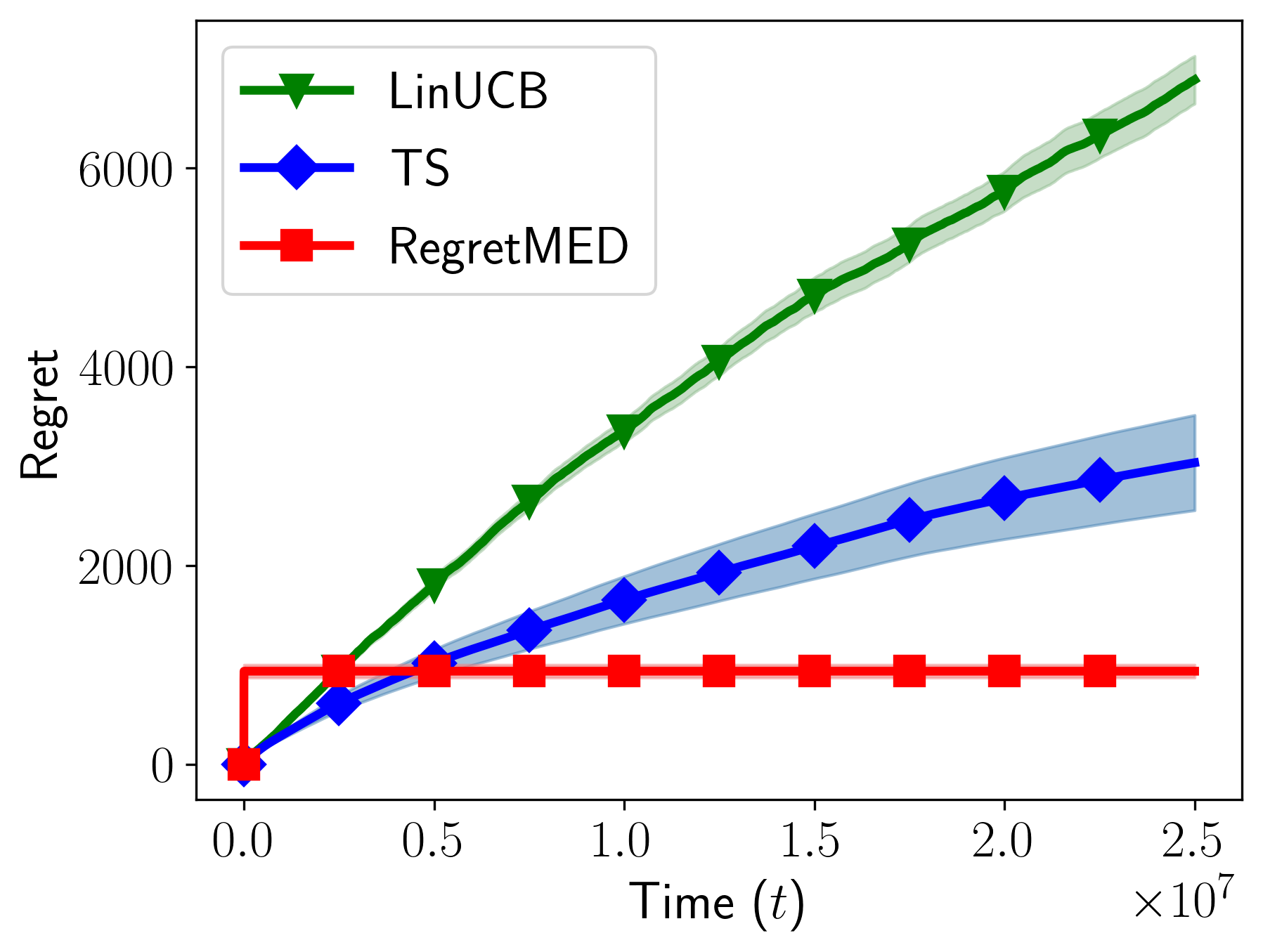

We illustrate the result in Figures 3 and 3 for different values of . In both cases, RegretMED yields a significant improvement over CTS-Gaussian and CombUCB1. Note that is growing exponentially in and for we have . In all experiments we set .

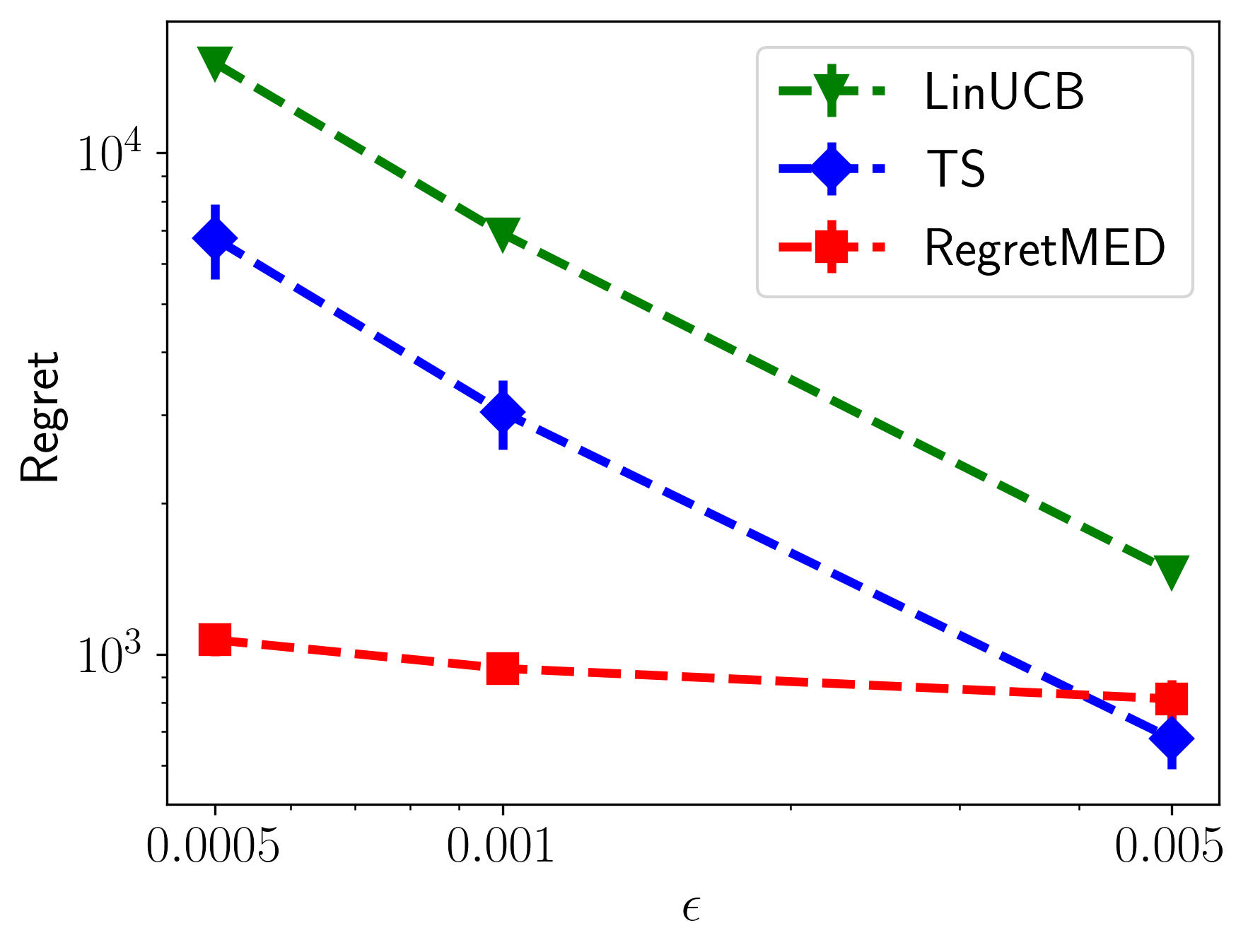

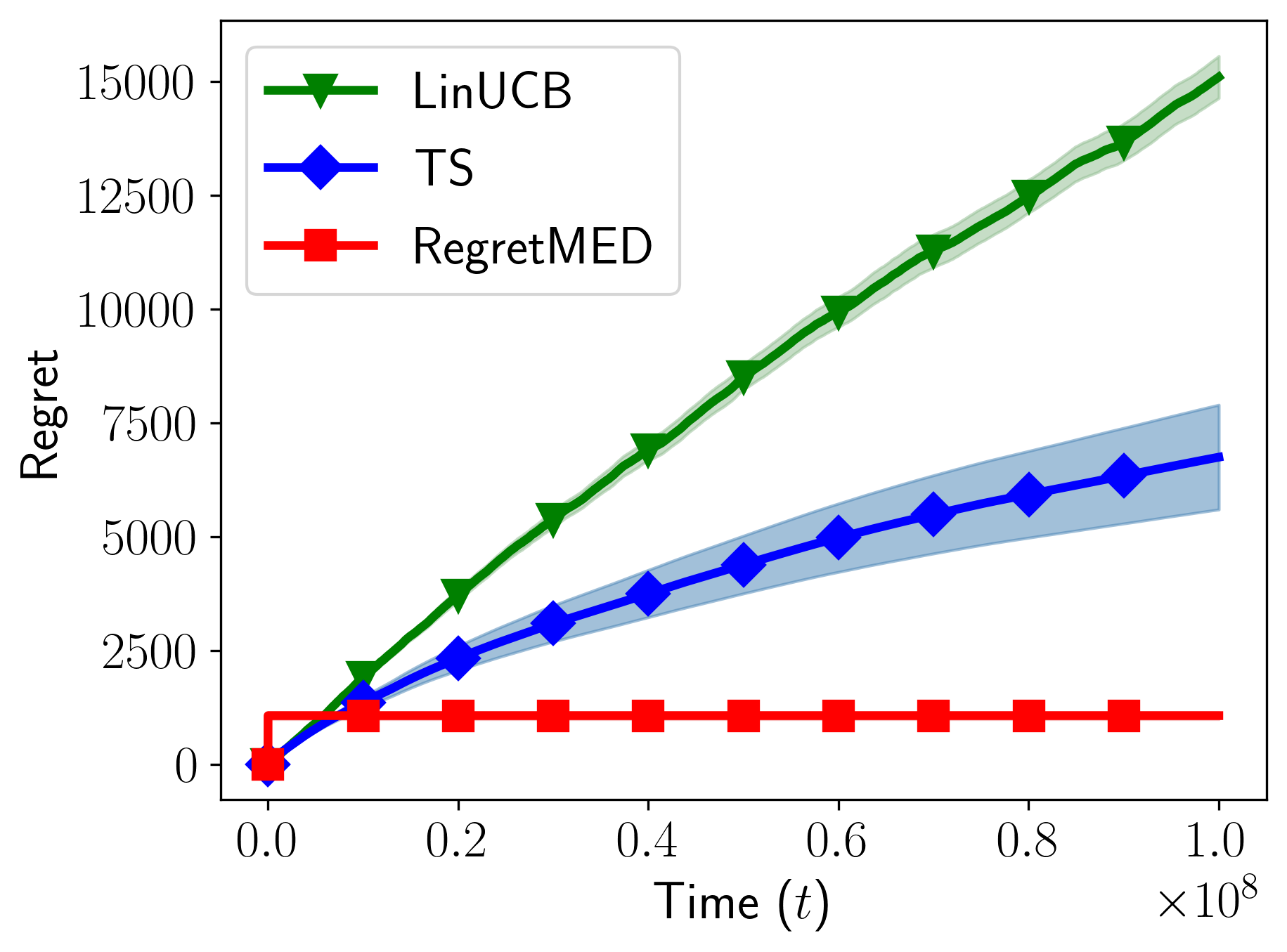

Bandit Feedback: In the bandit setting, we compare against LinUCB (Abbasi-Yadkori et al., 2011) and Thompson Sampling. For Thompson Sampling we use the Bayesian version. We run on the instance described in Lattimore and Szepesvari (2017). In particular, in this instance and where . We set and, for each experiment, use , which is the natural scaling for the problem since, as shown in Lattimore and Szepesvari (2017), optimistic algorithms will require on order pulls to determine is suboptimal. For completeness, in Appendix H we include the plots of regret against time for each point in this figure.

As Figure 3 illustrates, the performance of RegretMED is almost unaffected by the choice of , while the performance of both TS and LinUCB degrades significantly. Optimistic algorithms are suboptimal on this instance as they do not pull the suboptimal but informative arm, . Our results indicate that RegretMED is able to overcome this difficulty by continuing to pull even when it has been determined suboptimal, recognizing the information gain outweighs the regret incurred.

6 DISCUSSION AND PRIOR ART

Linear Bandits with Bandit Feedback: Several of the most well-studied algorithms for regret minimization in stochastic linear bandits with bandit feedback are LinUCB (Abbasi-Yadkori et al., 2011), action elimination, and LinTS (Lattimore and Szepesvári, 2020). LinUCB achieves regret of , action elimination has regret bounded as , and Thompson Sampling has (frequentist) regret of . Both LinUCB and action elimination rely on wasteful union bounds—LinUCB union bounds over every direction in , incurring an extra factor of , while action elimination union bounds over every arm without regard to geometry, incurring an extra . By leveraging tools from empirical process theory, we develop bounds that depend on the fine-grained geometry of . Indeed, as already stated, our algorithm achieves an expected regret of which, by Proposition 3, is at least as good as, and in some cases much better than the bounds of LinUCB and action elimination (see Proposition 2). Our bound can be seen as similar in spirit to the problem-dependent minimax bound for regret minimization in MDPs given in Zanette and Brunskill (2019).

Combinatorial Bandits with Semi-Bandit Feedback: Significant attention has been given to the combinatorial semi-bandit problem. Kveton et al. (2015) handles the case where noise is correlated between coordinates, and provides a computationally efficient algorithm with a regret bound of . Degenne and Perchet (2016) builds on this, showing that if the noise is assumed to be uncorrelated between coordinates, the on the leading term can be improved to a . Although their algorithm is not computationally efficient, several subsequent works proposed efficient procedures that achieved similar regret bounds (Wang and Chen, 2018; Perrault et al., 2020a; Cuvelier et al., 2020).

We give the first upper bound on regret (Theorem 1) that matches the lower bound on the leading term. Prior works are loose by a factor of and, moreover, have large additive terms that dominate until , making their bounds essentially vacuous for all practical time regimes. Although our analysis of the computationally efficient algorithm does not match the lower bound, its leading term is in the worst case, and, due to our smaller additive terms, our regret bound improves on the state of the art until . Furthermore, Proposition 5 implies that there exist instances where Theorem 2 matches the state-of-the-art in the leading term, up to a single factor. While we have assumed the noise between coordinates is uncorrelated, RegretMED extends to the case where it is correlated by using for an upper bound on the noise covariance and denoting element-wise multiplication.

While prior algorithms have tended to be based on the principle of optimism (Kveton et al., 2015; Combes et al., 2015; Degenne and Perchet, 2016; Wang and Chen, 2018; Perrault et al., 2020a), we have shown that optimistic strategies are asymptotically suboptimal (see Proposition 1), motivating our planning-based algorithm. Additional work includes (Chen et al., 2016; Talebi and Proutiere, 2016; Perrault et al., 2020b). We summarize our results in Table 1.

Asymptotically Optimal Regret in Linear Bandits: Another related line of work focuses on asymptotic performance (Lattimore and Szepesvari, 2017; Combes et al., 2017; Hao et al., 2020; Degenne et al., 2020; Cuvelier et al., 2020). In the bandit setting asymptotic lower bounds have been shown to scale as:

While we do not claim RegretMED is asymptotically optimal, we note that the optimization we are solving (2) closely resembles the above optimization. Indeed, at the final epoch of RegretMED, our estimates of the gaps will be sufficiently accurate so as to ensure we are playing approximately the asymptotically optimal distribution. Furthermore, as Proposition 1 and Figure 3 show, RegretMED appears to be playing the asymptotically optimal strategy in situations where optimism fails. We leave a rigorous proof of the asymptotic qualities of RegretMED to future work.

Concurrent to this work, several works appeared which simultaneously achieve asymptotically optimal and sub- regret (Tirinzoni et al., 2020; Kirschner et al., 2020b). In particular, Tirinzoni et al. (2020) achieves instance-optimal regret in finite time. We remark that their regret bound contains large additive terms which will dominate the leading term for moderate time horizons. Our primary concern is in this non-asymptotic regime, where the union bound applied is still significant, and we therefore see our work as complementary, addressing issues they do not address.

Asymptotically optimal regret has been relatively unexplored in the semi-bandit setting. Following the acceptance of this work, a very recent work (Cuvelier et al., 2021) proposed a computationally efficient asymptotically optimal algorithm in the semi-bandit setting, which was the first of its kind. As with the bandit setting, our concern is with the non-asymptotic time regime, so this result is complementary to ours.

Stochastic Multi-Armed Bandits with Side Observations: In the stochastic multi-armed bandits with side observations problem, the agent is given a graph of nodes where each node is associated with an independent distribution. When the agent pulls a node , she observes and suffers its stochastic reward and she also observes the stochastic reward of any node with an edge connected to node . Caron et al. (2012) proposed a UCB-like algorithm and Buccapatnam et al. (2014) used a linear programming solution to show that the regret scales with the minimum dominating set.

Using the design matrix , where denotes the edges in the graph, our algorithmic approach offers an explicit and natural way to model the tradeoff between estimated regret and information gain in this setting. In addition, our work suggests an algorithm for a novel extension of this problem where each node is associated with a feature vector and the expected reward of is , that is, stochastic linear bandits with side observations.

Partial Monitoring: The partial monitoring problem (Cesa-Bianchi and Lugosi, 2006; Cesa-Bianchi et al., 2006; Bartók et al., 2011) is a generalization of the multi-armed bandit problem where now the learner is no longer able to directly observe the loss incurred, but only some function of it. The linear partial monitoring problem (Lin et al., 2014; Kirschner et al., 2020a) is a special case where the learner observes , for some known , but receives reward , which is not observed. RegretMED directly generalizes to this setting if we employ the design matrix . We leave a full investigation of this application to future work.

Pure Exploration in Multi-Armed Bandits: There has not been a significant amount of previous work on pure exploration combinatorial bandits with semi-bandit feedback. Chen et al. (2020) provide a general framework that subsumes combinatorial bandits with semi-bandit feedback but their algorithm is non-adaptive and suboptimal. Several special cases of pure exploration combinatorial bandits with semi-bandit feedback have been studied. Best arm identification (where ) has received much attention (Even-Dar et al., 2006; Jamieson et al., 2014; Karnin et al., 2013; Kaufmann et al., 2016; Chen and Li, 2015). The setting in Jun et al. (2016) subsumes the top-K problem, but their approach does not generalize to other combinatorial problem instances. Concurrent to this work, Jourdan et al. (2021) derived an asymptotically optimal best arm identification algorithm for the semi-bandit setting. We note that our result focuses on optimality in the finite-time regime, so our results our complementary.

Our work is also related to transductive linear bandits (Fiez et al., 2019). In this problem, there are measurement vectors , item vectors , and the agent at each round chooses and observes the realization of a noisy random variable with mean with the goal to identify as quickly as possible. Our work on combinatorial bandits with semi-bandit feedback can be straightforwardly extended to a generalization of transductive linear bandits that allows for multiple measurements at each round. More concretely, in this setting, the agent is given a collection of subsets of , , and at each round, she chooses a set of linear measurements where , and observes the realization of a noisy random variable with mean for each . This generalization subsumes the work of Wu et al. (2015), which studies a version of this problem where .

Our algorithmic technique bridging empirical process theory and experimental design is inspired by the work on pure exploration combinatorial bandits in Katz-Samuels et al. (2020). The semi-bandit feedback setting in the present paper poses a new and non-trivial computational challenge since, unlike in Katz-Samuels et al. (2020), the number of variables in the optimization is potentially exponential in the dimension.

Acknowledgements

AW is supported by an NSF GFRP Fellowship DGE-1762114. JKS is supported by an Amazon Research Award. The work of KJ is supported in part by grants NSF RI 1907907 and NSF CCF 2007036.

References

- Abbasi-Yadkori et al. [2011] Yasin Abbasi-Yadkori, Dávid Pál, and Csaba Szepesvári. Improved algorithms for linear stochastic bandits. In Advances in Neural Information Processing Systems, pages 2312–2320, 2011.

- Allen-Zhu et al. [2020] Zeyuan Allen-Zhu, Yuanzhi Li, Aarti Singh, and Yining Wang. Near-optimal discrete optimization for experimental design: A regret minimization approach. Mathematical Programming, pages 1–40, 2020.

- Arora et al. [2012] Sanjeev Arora, Elad Hazan, and Satyen Kale. The multiplicative weights update method: a meta-algorithm and applications. Theory of Computing, 8(1):121–164, 2012.

- Bartók et al. [2011] Gábor Bartók, Dávid Pál, and Csaba Szepesvári. Minimax regret of finite partial-monitoring games in stochastic environments. In Proceedings of the 24th Annual Conference on Learning Theory, pages 133–154, 2011.

- Bubeck [2014] Sébastien Bubeck. Convex optimization: Algorithms and complexity. arXiv preprint arXiv:1405.4980, 2014.

- Buccapatnam et al. [2014] Swapna Buccapatnam, Atilla Eryilmaz, and Ness B Shroff. Stochastic bandits with side observations on networks. In The 2014 ACM international conference on Measurement and modeling of computer systems, pages 289–300, 2014.

- Caron et al. [2012] Stéphane Caron, Branislav Kveton, Marc Lelarge, and Smriti Bhagat. Leveraging side observations in stochastic bandits. arXiv preprint arXiv:1210.4839, 2012.

- Cesa-Bianchi and Lugosi [2006] Nicolo Cesa-Bianchi and Gábor Lugosi. Prediction, learning, and games. Cambridge university press, 2006.

- Cesa-Bianchi et al. [2006] Nicolo Cesa-Bianchi, Gábor Lugosi, and Gilles Stoltz. Regret minimization under partial monitoring. Mathematics of Operations Research, 31(3):562–580, 2006.

- Chen and Li [2015] Lijie Chen and Jian Li. On the optimal sample complexity for best arm identification. arXiv preprint arXiv:1511.03774, 2015.

- Chen et al. [2017] Lijie Chen, Anupam Gupta, Jian Li, Mingda Qiao, and Ruosong Wang. Nearly optimal sampling algorithms for combinatorial pure exploration. In Conference on Learning Theory, pages 482–534, 2017.

- Chen et al. [2016] Wei Chen, Yajun Wang, Yang Yuan, and Qinshi Wang. Combinatorial multi-armed bandit and its extension to probabilistically triggered arms. The Journal of Machine Learning Research, 17(1):1746–1778, 2016.

- Chen et al. [2020] Wei Chen, Yihan Du, and Yuko Kuroki. Combinatorial pure exploration with partial or full-bandit linear feedback. arxiv Preprint arXiv:2006.07905v1, 2020.

- Combes et al. [2015] Richard Combes, Mohammad Sadegh Talebi Mazraeh Shahi, Alexandre Proutiere, et al. Combinatorial bandits revisited. In Advances in Neural Information Processing Systems, pages 2116–2124, 2015.

- Combes et al. [2017] Richard Combes, Stefan Magureanu, and Alexandre Proutiere. Minimal exploration in structured stochastic bandits. In Advances in Neural Information Processing Systems, pages 1763–1771, 2017.

- Cuvelier et al. [2020] Thibaut Cuvelier, Richard Combes, and Eric Gourdin. Statistically efficient, polynomial time algorithms for combinatorial semi bandits. arXiv preprint arXiv:2002.07258, 2020.

- Cuvelier et al. [2021] Thibaut Cuvelier, Richard Combes, and Eric Gourdin. Asymptotically optimal strategies for combinatorial semi-bandits in polynomial time. arXiv preprint arXiv:2102.07254, 2021.

- Degenne and Perchet [2016] Rémy Degenne and Vianney Perchet. Combinatorial semi-bandit with known covariance. In Advances in Neural Information Processing Systems, pages 2972–2980, 2016.

- Degenne et al. [2020] Rémy Degenne, Han Shao, and Wouter M Koolen. Structure adaptive algorithms for stochastic bandits. arXiv preprint arXiv:2007.00969, 2020.

- Eggleston [1958] Harold Gordon Eggleston. Convexity. Number 47. CUP Archive, 1958.

- Even-Dar et al. [2006] Eyal Even-Dar, Shie Mannor, and Yishay Mansour. Action elimination and stopping conditions for the multi-armed bandit and reinforcement learning problems. Journal of machine learning research, 7(Jun):1079–1105, 2006.

- Fiez et al. [2019] Tanner Fiez, Lalit Jain, Kevin G Jamieson, and Lillian Ratliff. Sequential experimental design for transductive linear bandits. In Advances in Neural Information Processing Systems, pages 10667–10677, 2019.

- Hao et al. [2020] Botao Hao, Tor Lattimore, and Csaba Szepesvári. Adaptive exploration in linear contextual bandit. In International Conference on Artificial Intelligence and Statistics, pages 3536–3545. PMLR, 2020.

- Hazan and Luo [2016] Elad Hazan and Haipeng Luo. Variance-reduced and projection-free stochastic optimization. In International Conference on Machine Learning, pages 1263–1271, 2016.

- [25] Kevin Jamieson. Some notes on multi-armed bandits. https://courses.cs.washington.edu/courses/cse599i/20wi/resources/bandit_notes.pdf. Accessed: October 14, 2020.

- Jamieson et al. [2014] Kevin Jamieson, Matthew Malloy, Robert Nowak, and Sébastien Bubeck. lil’ucb: An optimal exploration algorithm for multi-armed bandits. In Conference on Learning Theory, pages 423–439, 2014.

- Jourdan et al. [2021] Marc Jourdan, Mojmír Mutnỳ, Johannes Kirschner, and Andreas Krause. Efficient pure exploration for combinatorial bandits with semi-bandit feedback. arXiv preprint arXiv:2101.08534, 2021.

- Jun et al. [2016] Kwang-Sung Jun, Kevin Jamieson, Robert Nowak, and Xiaojin Zhu. Top arm identification in multi-armed bandits with batch arm pulls. In Artificial Intelligence and Statistics, pages 139–148, 2016.

- Karnin et al. [2013] Zohar Karnin, Tomer Koren, and Oren Somekh. Almost optimal exploration in multi-armed bandits. In Sanjoy Dasgupta and David Mcallester, editors, Proceedings of the 30th International Conference on Machine Learning (ICML-13), volume 28, pages 1238–1246. JMLR Workshop and Conference Proceedings, May 2013.

- Katz-Samuels et al. [2020] Julian Katz-Samuels, Lalit Jain, Zohar Karnin, and Kevin Jamieson. An empirical process approach to the union bound: Practical algorithms for combinatorial and linear bandits. arXiv preprint arXiv:2006.11685, 2020.

- Kaufmann et al. [2016] Emilie Kaufmann, Olivier Cappé, and Aurélien Garivier. On the complexity of best-arm identification in multi-armed bandit models. The Journal of Machine Learning Research, 17(1):1–42, 2016.

- Kirschner et al. [2020a] Johannes Kirschner, Tor Lattimore, and Andreas Krause. Information directed sampling for linear partial monitoring. arXiv preprint arXiv:2002.11182, 2020a.

- Kirschner et al. [2020b] Johannes Kirschner, Tor Lattimore, Claire Vernade, and Csaba Szepesvári. Asymptotically optimal information-directed sampling. arXiv preprint arXiv:2011.05944, 2020b.

- Kveton et al. [2015] Branislav Kveton, Zheng Wen, Azin Ashkan, and Csaba Szepesvari. Tight regret bounds for stochastic combinatorial semi-bandits. In Artificial Intelligence and Statistics, pages 535–543, 2015.

- Lattimore and Szepesvari [2017] Tor Lattimore and Csaba Szepesvari. The end of optimism? an asymptotic analysis of finite-armed linear bandits. In Artificial Intelligence and Statistics, pages 728–737. PMLR, 2017.

- Lattimore and Szepesvári [2020] Tor Lattimore and Csaba Szepesvári. Bandit algorithms. Cambridge University Press, 2020.

- Lin et al. [2014] Tian Lin, Bruno Abrahao, Robert Kleinberg, John Lui, and Wei Chen. Combinatorial partial monitoring game with linear feedback and its applications. In International Conference on Machine Learning, pages 901–909, 2014.

- Maalouf et al. [2019] Alaa Maalouf, Ibrahim Jubran, and Dan Feldman. Fast and accurate least-mean-squares solvers. In Advances in Neural Information Processing Systems, pages 8307–8318, 2019.

- Munkres [2018] James R Munkres. Analysis on manifolds. CRC Press, 2018.

- Perrault et al. [2020a] Pierre Perrault, Etienne Boursier, Vianney Perchet, and Michal Valko. Statistical efficiency of thompson sampling for combinatorial semi-bandits. arXiv preprint arXiv:2006.06613, 2020a.

- Perrault et al. [2020b] Pierre Perrault, Michal Valko, and Vianney Perchet. Covariance-adapting algorithm for semi-bandits with application to sparse outcomes. volume 125 of Proceedings of Machine Learning Research, pages 3152–3184. PMLR, 09–12 Jul 2020b.

- Talebi and Proutiere [2016] Mohammad Sadegh Talebi and Alexandre Proutiere. An optimal algorithm for stochastic matroid bandit optimization. In Proceedings of the 2016 International Conference on Autonomous Agents & Multiagent Systems, pages 548–556, 2016.

- Tirinzoni et al. [2020] Andrea Tirinzoni, Matteo Pirotta, Marcello Restelli, and Alessandro Lazaric. An asymptotically optimal primal-dual incremental algorithm for contextual linear bandits. arXiv preprint arXiv:2010.12247, 2020.

- Tsirelson et al. [1976] Boris S Tsirelson, Ildar A Ibragimov, and VN Sudakov. Norms of gaussian sample functions. In Proceedings of the Third Japan—USSR Symposium on Probability Theory, pages 20–41. Springer, 1976.

- Vershynin [2018] Roman Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- Wang and Chen [2018] Siwei Wang and Wei Chen. Thompson sampling for combinatorial semi-bandits. In International Conference on Machine Learning, pages 5114–5122, 2018.

- Wu et al. [2015] Yifan Wu, Andras Gyorgy, and Csaba Szepesvari. On identifying good options under combinatorially structured feedback in finite noisy environments. In International Conference on Machine Learning, pages 1283–1291, 2015.

- Zanette and Brunskill [2019] Andrea Zanette and Emma Brunskill. Tighter problem-dependent regret bounds in reinforcement learning without domain knowledge using value function bounds. In International Conference on Machine Learning, pages 7304–7312. PMLR, 2019.

Appendix A Action Elimination with Gaussian Width

We first state an algorithm inspired by Lattimore and Szepesvári [2020] and prove a regret bound. This algorithm, while naive, incorporates the TIS inequality to obtain regret scaling with the Gaussian width. Furthermore, the analysis is simple and helps aid in the intuition of the proof of our main theorems.

For , denote:

Here ROUND is a rounding procedure which takes as input , , and and outputs an allocation such that:

and , so long as . From Katz-Samuels et al. [2020] and Allen-Zhu et al. [2020], we know such a rounding procedure exists and can be computed efficiently, and that it suffices to choose .

Denote:

where .

Theorem 5.

For , the absolute regret of GW-AE is bounded as:

with probability at least and minimax regret as:

with probability at least . Here are absolute constants.

If desired, noting that which implies that we will have at most rounds, the could be replaced with a term , as in Theorem 1.

While this result closely resembles Theorem 1, there are several major shortcomings. First, this algorithm does not plan as effectively as it only pulling arms with gap less than , which could cause it to forego pulling informative yet suboptimal arms, something Algorithm 1 improves on. In particular, the regret bound stated for Algorithm 1 in Proposition 1 will not hold for this algorithm. In a sense, this algorithm can be thought of as being optimistic. Second, it is always the case that . The parameter could be tightened by altering the constant factors in Algorithm 2 so as to guarantee that, on the good event all arms with gap less than , for some , are in . However, even with this tightening we will always have . Finally, Algorithm 2 does not seem to admit a computationally feasible solution in the combinatorial bandit setting.

Proof.

From Proposition 6, we will have that:

for all simultaneously with probability . The second inequality holds by our choice of and Kiefer-Wolfowitz and Proposition 9. Let:

where is computed assuming is the active set in the above algorithm. Then using the following calculation from Jamieson :

so the good event, that all the arm rewards are well estimated for all rounds, holds with high probability. Assume henceforth that the good event holds. Following identically the argument from Jamieson , we will have that and for all . We assume the good event holds for the remainder of the proof.

We can now follow the same argument as Lemma 12 of Katz-Samuels et al. [2020]. Take for some and let be the distribution that minimizes:

and the distribution that minimizes:

Let . Then we will have that:

From this it immediately follows that:

where the last inequality holds by Kiefer-Wolfowitz and Proposition 9. Also:

Since will always contain only arms with gap less than for some , we then have that:

Using these bounds and noting that upper bounds the number of rounds, we can upper bound the regret as:

Optimizing this over gives the final regret of:

and choosing gives the absolute regret bound. ∎

Appendix B Regret Bound Proofs

Proof of Theorem 2.

Throughout we will let denote the regret incurred in round , and the regret incurred from rounds 1 through . We assume corresponds to the type of feedback received. The first part of this proof closely mirrors the proof of Theorem 5 of Katz-Samuels et al. [2020]. We will prove this result for being a -optimal solution to (3), where we calll a solution to (3) -optimal if , where is the value of the objective attained by the approximate solution, and opt the value attained by the optimal solution.

Good event: We will define as the following:

Let and define the events:

Proposition 6 gives that with probability at least :

where follows by Lemma 11 of Katz-Samuels et al. [2020]. It follows then that , which implies that:

Estimation error: Henceforth we assume holds. We proceed by induction to show that the gaps are always well-estimated. First we prove the base case. Let and consider any . Then:

where follows by Proposition 7.5.2 of Vershynin [2018] and follows since is a feasible solution to (3).

For the inductive step, assume that, for all :

and for all :

Consider round and take . There then exists some such that . Then:

where follows by Proposition 7.5.2 of Vershynin [2018], follows since by virtue of the fact that , so , follows since and for any , we will have theta , so , holds by the inductive hypothesis and Lemma 1 of Katz-Samuels et al. [2020] and taking to be the estimate of at round , and holds since is a feasible solution to (3). We can perform a similar calculation to get the same thing for , allowing us to conclude that, for all :

and for all :

From this and Lemma 1 of Katz-Samuels et al. [2020], it follows that for all and :

and for :

So the objective of (3) upper bounds the real regret. Further, on the good event, using Lemma 1 from Katz-Samuels et al. [2020], for any and , we have:

| (6) |

This implies that if we remove arm from :

So, on the good event, if , we will have identified the best arm correctly.

Bounding the Round Regret: From the previous section, we know that on the good event all our gaps will be well-estimated. From (6), it follows that the constraint in (3) is tighter than the following constraint:

| (7) |

so any satisfying this inequality is also a feasible solution to (3).

Consider drawing some and let be the point that achieves the maximum above (if the solution is not unique, break ties by choose randomly from the for which the maximum is attained). If we assume that , then it follows that:

where follows since we will always have:

since for by Lemma 1 of Katz-Samuels et al. [2020]. Assume that . Then:

where uses the fact that for all , , and the last inequality follows as above. We therefore have that:

Let be the solution to:

Let and . Then:

Given this:

where holds by the Sudakov-Fernique inequality (Theorem 7.2.11 of Vershynin [2018]). Thus, satisfies (7) and so is a feasible solution to (3). Let be the optimal solution to (3), then:

The first term can be bounded by the regret bounded given in Lemma 2:

By construction we’ll have that:

so:

Recalling that is a -optimal solution to (3), the above implies that:

| (8) |

We in fact play , as this will attain the same objective value and so the same regret bound. However, may not be integer, so we will pull every arm times. Note that the rounded solution still meets the constraint from (3). Assume we are playing the rounded solution given by Lemma 1, then rounding the solution will incur additional regret of at most . Since upper bounds the real regret of playing , we’ll have:

We can then bound the regret incurred after stages as:

| (9) | ||||

Minimax Regret: Denote the objective to (3) at round evaluated at by:

By (8) we can upper bound:

| (10) | ||||

Let be the first round for which:

Note that, if solves this with equality, then:

is the only non-negative solution. It follows then that:

Since is the largest such solution, it follows that doesn’t satisfy this inequality so:

so in particular:

Assume that for all . Using the monotonicity of , for , we’ll have:

Furthermore, by (9), we’ll have that the total regret up to round will be bounded as:

So in this case, since by Lemma 3 there are at most rounds, and since upper bounds the regret of round , we’ll have that the total regret will be bounded as:

Now assume there is some round such that and denote this round as . By construction, it will be the case that the MLE at this point has gap at most , so the total regret incurred from playing the MLE for the remainder of time will be bounded as . Further, note that by (10):

By definition is the first round where , so it follows that . We can then upper bound the total regret incurred as:

From (9), as above, we can bound:

Since by definition we’ll have that for , the second term can be bounded as:

Finally:

Combining this, we have that:

Absolute Regret: Assume:

then we’ll have that , so the algorithm will exit before reaching round . In this case, since there are at most stages by Lemma 3 and since, as noted above, on the good event, once , we will have identified the best arm and so will incur 0 regret for the rest of time, (9) gives:

By definition, it will always be the case that , if it exists, as we would have otherwise exited the algorithm already. By (9), we’ll then have:

where holds by the definition of . If round is never reached, then the upper bound above still holds, as we can still bound , the regret we would have incurred had we reached .

Finally, by Theorem 4 we can choose , , and we will be able to compute the solution efficiently. ∎

Proof of Theorem 1.

The proof of this result is very similar to the proof of Theorem 2 but we include the points where it differs for the sake of completeness. Unless otherwise noted, all notation is defined as in the proof of Theorem 2.

Estimation error: Henceforth we assume holds. We proceed by induction to show that the gaps are always well-estimated. First we prove the base case. Let and consider any . Then:

where follows by Proposition 7.5.2 of Vershynin [2018] and follows since is a feasible solution to (2). For the inductive step, assume that, for all :

and for all :

Consider round and take . There then exists some such that . Then:

where follows by Proposition 7.5.2 of Vershynin [2018], follows since by virtue of the fact that , so , follows since and for any , we will have theta , so , holds by the inductive hypothesis and Lemma 1 of Katz-Samuels et al. [2020] and taking to be the estimate of at round , and holds since is a feasible solution to (3). We can perform a similar calculation to get the same thing for , allowing us to conclude that, for all :

and for all :

From here the remaining calculations on the gap estimates performed in the proof of Theorem 2 hold almost identically.

Bounding the Round Regret: From (6), it follows that the constraint in (2) is tighter than the following constraint:

| (11) |

so any satisfying this inequality is also a feasible solution to (2).

From here we follow the same pattern as in the proof of Theorem 2. We handle each term in the constraint separately. For the second term, note that we can upper bound:

We now choose , where is the distribution minimizing . By the same argument as in the proof of Theorem 2, effectively ignoring the second term, we will have:

For the second term, by the Kiefer-Wolfowitz Theorem in the bandit case, and Proposition 9 in the semi-bandit case, we’ll have:

So:

From this it follows is a feasible solution to (2). Furthermore, by Lemma 2, the total regret incurred by playing is bounded by:

and the total regret incurred playing is bounded as:

Following the same argument as in Theorem 2, it follows that:

From here the argument follows identically to the proof of Theorem 4, so we omit the remainder of the proof. ∎

Lemma 2.

Given an such that , let be any distribution supported on and for any set:

Play the distributions ROUND for , where ROUND is defined as in Section A. Then the total gap-dependent regret incurred by this procedure is bounded by:

Proof.

Lemma 3.

Proof.

Note that must satisfy:

However:

where follows by Proposition 7.5.2 of Vershynin [2018], follows since for any :

and follows by (6). Thus:

where the final equality holds since . If round is the last round the algorithm completes before terminating, we’ll have that , so:

The first conclusion follows by Lemma 4.

For the second conclusion, note that, as we showed above, on the good event we will have that for all , . Thus, once , we can guarantee that for any , which implies that is the optimal arm so and the algorithm will have terminated. It follows that:

∎

Lemma 4.

Proof.

∎

Appendix C Pure Exploration Proofs

For the sake of clarity, we rewrite the pure exploration algorithm (see Algorithm 3).

| (12) | ||||

Theorem (2) shows that we can solve (12) in polynomial-time, but note that it is easier to solve (12) approximately by calling stochastic Frank-Wolfe to solve

and the convergence rate shown in Lemma 5 applies.

The MINGAP subroutine (Algorithm 4), originally provided in Chen et al. [2017], is a computationally scalable method to compute the empirical gap between the empirically best arm and the empirically second best arm. It uses at most calls to the linear maximization oracle.

We note that the correctness and sample complexity proofs are quite similar to the proof of Theorem in Katz-Samuels et al. [2020], but we include it for the sake of completeness. The main contribution of our paper for the pure exploration problem is a computational method to solve (12) even when the number of variables is exponential in the dimension.

Proof of Theorem 3.

Step 1: A good event and well-estimated gaps Using the identical argument to the first two steps of the proof of Theorem 2, we have that with probability at least at every round , for all :

| (13) |

and for all :

| (14) |

For the remainder of the proof we suppose that this good event holds.

Step 2: Correctness. It is enough to show at round , if , then the Unique returns false. Inspecting Unique, a sufficient condition is to show that . By (13) and (14), we have that

proving correctness.

Step 3: Bound the Sample Complexity. Letting , Unique at round checks whether is at least , and terminates if it is. Thus, (13) and (14), the algorithm terminates and outputs once .

Thus, the sample complexity is upper bounded by

| (15) |

where we used the fact that the rounding procedure can use points in the semi-bandit case. Thus, it suffices to upper bound the second term in the above expression. Fix . Then,

Fix . The first term is bounded as follows.

| (16) | ||||

| (17) |

where we obtained line (16) using exercise 7.6.9 in Vershynin [2018].

We also have that

| (18) | ||||

| (19) |

where line (18) follows since (13), (14), and Lemma 1 in Katz-Samuels et al. [2020] imply that .

∎

C.1 Lower Bound

In this section, we prove a lower bound for the combinatorial bandit setting with semi-bandit feedback. Fix a model and let denote the distribution of the observations when arm is pulled. In this setting, at each round , is drawn and

Definition 1.

We say that an Algorithm is -PAC if for any instance , it returns with the largest mean with probability at least .

Theorem 6.

Fix an instance such that and is unique. Let be a -PAC algorithm and let be its total number of pulls on . Then,

The proof is quite similar to the proof of Theorem 1 in Fiez et al. [2019].

Proof.

For simplicity, label and . Define the set of alternative instances . Let denote the random number of times that is pulled during the game. Then, noting that the standard transportation Lemma from Kaufmann et al. [2016] easily generalizes to semi-bandit feedback, we have that for any ,

By a standard argument (see for example Theorem 1 Fiez et al. [2019]), this implies that

Let . For each , define

Note that

showing that . Note that using the identity for the KL-divergence for a multivariate Gaussian, we have that

Then, we have that

Since was arbitrary, we may let , obtaining the result. ∎

Next, we state and prove a lower bound for the non-interactive MLE: it chooses an allocation prior to the game, then observes where , and forms the MLE and outputs . Since the non-interactive MLE may use knowledge of in choosing its allocation and the estimator and recommendation rules are very natural, we view the sample complexity of the non-interactive MLE as a good benchmark to measure the sample complexity of algorithms against. The following lower bound for the non-interactive MLE resembles Theorem 3 in Katz-Samuels et al. [2020].

Theorem 7.

Fix and . Let . There exists a universal constant such that if the non-interactive MLE uses less than samples, it makes a mistake with probability at least .

The proof is quite similar to the proof of Theorem 3 in Katz-Samuels et al. [2020], so we merely sketch it here.

Proof.

Consider the combinatorial bandit protocol with as the collection of sets: at each round , the agent picks and observes (see Katz-Samuels et al. [2020] for a more precise definition). Let and fix an allocation . Define

Theorem 3 in Katz-Samuels et al. [2020] shows that there exists a universal constant such that if or , the with probability at least , the oracle MLE makes a mistake.

Now, consider the semi-bandit problem and wlog suppose that . Now, fix an allocation for the semi-bandit problem. Define . Suppose that . Then,

where

Now, rearranging the above inequality,we have that

Note that the allocation for the semi-bandit problem specifies an allocation for the combinatorial bandit problem and the stochastic process (and non-interactive MLE algorithm) is the same on both problems. Thus, can be interpreted as in the combinatorial bandit protocol for some allocation , and we may apply the proof of Theorem 3 to obtain that with probability at least , the oracle MLE makes a mistake.

∎

Appendix D Computational Complexity Results

D.1 Algorithmic Approach

In this section, we present the main computational algorithms and results in the paper, culiminating in the proof of Theorem 8, which immediately implies Theorem 4. For simplicity label . We can always find such that in linear maximization oracle calls. For each , create a cost vector:

and set . Thus, by reordering we may suppose that . Now, define

where . We optimize over due to its computational benefits,e.g., controlling the second partial order derivatives of the Lagrangian of (5).

Algorithm 5 is the main algorithm (see Theorem 8 for its guarantee); it essentially does a grid search over the time horizon variable, . Note that for a fixed , we have that for all

and thus we can ignore the term . Thus, Algorithm 5 calls Algorithm 6 to solve for a fixed the following optimization problem.

| (20) | ||||

To solve the above optimization problem, we convert it into a series of convex feasibility programs of the following form: such that

and perform binary search over . To solve each of these convex feasibility programs, we employ the Plotkin-Shmoys-Tardos reduction to online learning and apply Algorithm 7, a multiplicative weights update style algorithm. Lemmas 6 and 7 provide the guarantees for the multiplicative weights update algorithm and for the binary search procedure, respectively.

The Plotkin-Shmoys-Tardos reduction requires a method for solving for arbitrary :

To solve the above optimization problem, we use stochastic Frank-Wolfe (see Algorithm 8). Defining for a fixed ,

we see that

See Lemma 5 for our convergence result on stochastic Frank-Wolfe.

Finally, we note that each of our algorithms uses a global variable tol, which for the theory we set to . We note that scales as and thus a polynomial dependence on results in a polynomial dependence on .

D.1.1 Subroutines

Algorithm 9, originally provided in Katz-Samuels et al. [2020], uses binary search and calls to the linear maximization oracle to compute

Algorithm 10 estimates

D.2 Main Optimization Proofs

For the sake of simplicity, we assume that is a power of , and that the optimization problem is feasible. If the optimization problem is infeasible, we can determine this by applying stochastic Frank-Wolfe (see Lemma 5). For simplicity, we also assume that since typically it is assumed that and whp at every round . Further, note that whenever the algorithm is applied , and we assume this henceforth. We introduce the following functions to bound the number of linear maximization oracle calls:

Note these are polynomial in . Our algorithms share a global parameter tol; it suffices to set . Define

We say a random variable is sub-Gaussian with parameter and write if for all

The following Lemma provides the convergence guarantee for stochastic Frank-Wolfe in the semi-bandit setting (see Algorithm 8).

Lemma 5.

Let , , . With probability at least Algorithm 8 returns such that

Furthermore, with probability at least , the number of oracle calls is bounded by

Proof.

For simplicity, we focus on the case where (the other cases are similar). We write and as abbreviations for and .

Step 1: Bound the number of iterations of stochastic Frank-Wolfe. is convex in by Proposition 7. Furthermore, . Thus, by Proposition 8, it suffices to show

-

1.

Smoothness: for an appropriate choice of

-

2.

Small deviation with high probability: is chosen sufficiently large to ensure that with probability at least

Step 1.1: Smoothness. Let and fix . It suffices to show that

For the sake of abbreviation, define . By Lemma 13, we have that is twice differentiable and that

where

For any ,

where we used Jensen’s inequality and is a universal constant.

Now, by the mean value theorem, there exists such that

where the second inequality follows by Holder’s Inequality. Thus,

For the sake of brevity, we write for the remainder of the proof.

Step 1.2: Small deviation with high probability. Now, we show that is chosen sufficiently large to ensure that with probability at least

| (21) |

Recall that

where

Note that

Since

we then have that by Lemma 2.6.8 in Vershynin [2018],

Therefore, since and since for an appropriately chosen universal constant, by a standard sub-Gaussian tail bound (21) follows.

Step 2: Bound the number of linear maximization oracle calls. Next, we bound the number of linear maximization oracle calls. At each round , there is one linear maximization oracle call from finding the minimizing direction wrt the gradient over , but the dominant source of linear maximization oracles at each round is due to applying Algorithm 9 several times. Thus, it suffices to bound the number of linear maximization oracle calls due to Algorithm 9. Define the following event

Then, we have that

where we used the independence of each draw of a multivariate Gaussian in the algorithm and Lemma 9. The number of calls of Algorithm 9 at each iteration is upper bounded by and, thus, the total number of oracle calls is upper bounded by

∎

The following Lemma shows that the Multiplicative Weight Update algorithm (Algorithm 7) either finds an approximately feasible solution or if there is no approximately feasible solution, determines infeasibility.

Lemma 6.

Fix and let . Define

With probability at least , if MW() does not declare infeasibility, then MW() returns and if MW() declares infeasibility, then is infeasible. Furthermore, on the same event, MW() uses at most linear maximization oracle calls.

Proof.

The algorithm uses the Plotkin-Shmoys-Tardos reduction to online learning and essentially runs the multiplicative weights update algorithm (see Arora et al. [2012]) where there is an expert for each constraint. Define

At each round , the algorithm chooses a distribution, and , over the constraints and the adversary uses the stochastic Frank-Wolfe algorithm to find such that

The reward for expert/constraint 1 is and the reward for expert/constraint 2 is .

Let denote the event that satisfies

uses at most linear maximization oracle calls. Define Further, define the following events

By Lemmas 5 and 8 applied with and the law of total probability, we have that

Now, for the remainder of the proof we assume that occurs.

Suppose that at some round Algorithm 8 returns such that . Then, since implies that

we have that on

Therefore, it follows that for every ,

Thus, the algorithm correctly declares infeasibility of the convex feasibility program.

Next, suppose that the Algorithm 8 returns such that at every round . Then, we show that the algorithm returns . To apply Theorem 9, a standard result for the multiplicative weights update algorithm, we must show that for any returned during the execution of the Algorithm

| (22) |

where is defined in Algorithm 7. We have that

since , , and we assume that . Furthermore,

for a suitably chosen constant where we used that fact that .

Thus, we have shown (22) and therefore may apply Theorem 9, which implies on that

Now, finally, applying Lemma 7, we have that

This shows that approximately satisfies one of the constraints; showing approximate satisfaction of the other constraint follows by a similar argument. Thus, we conclude that . ∎

Lemma 7.

Proof.

Algorithm 6 applies Algorithm 7 at most times on a using a predetermined set of values for , which we denote . Define the event

where is defined in Lemma 6. Then, by the union bound, we have that . Suppose occurs for the remainder of the proof.

First, consider the case that for all ,

Then, on the event , we have that the Algorithm 6 declares infeasibility of the program.

Now, suppose there exists such that

The following Theorem establishes that Algorithm 5 approximately solves the main optimization problem (5). It directly implies Theorem 4.

Theorem 8.

Proof.

Step 0. Let be the value of

and let be the value of

Let denote the event that if for all ,

then declares the program infeasible and if

then returns that satisfies

Further, define . By Lemma 7 and a union bound, we have that . We suppose holds for the rest of the proof.

Step 1. First, we show that Algorithm 5 returns such that

By assumption the optimization problem in (5) is feasible and, hence, and thus by the event , the algorithm finds at least one nearly feasible solution, i.e., is not False for all . Let attain the optimal value in the optimization problem (5). Let such that . By event finds such that

Algorithm 5 outputs , which satisfies by Lemma 7 and by construction,

| (24) | ||||

| (25) |

where in the last line we used , which bounds the objective value of .

Next, we show feasiblity of . Observe that

| (26) |

where we used the fact that and .

Step 2: Relate to . Next, we show that

Define the function

Recall that we let attain the optimal value in the optimization problem (5). Let such that . Note that

Thus,

| (27) |

where we used the fact that

This proves the claim.

Step 3: Relate to opt. Next, we show that

Define

and

By the hypothesis, we have that and, thus, is a convex combination of and .

Next, we show that are a feasible solution to (23) and show that it is approximately optimal. Note that

which implies that

Then, by Sudakov-Fernique, we have that

showing feasibility . Furthermore, we have that

| (28) |

where in the last line we used .

Step 4: Putting it together. Putting together (26), (25), (27), and (28), we have that Algorithm 5 returns such that , , and

∎

D.3 Miscellaneous Optimization Lemmas

Lemma 8.

Let . With probability at least , Algorithm 10 returns such that

and the number of linear maximization oracle calls is bounded above by

Proof.

The following Lemma shows that the binary search procedure in Algorithm 9 is efficient with very high probability and it follows immediately from the proof of Lemma 2 of Katz-Samuels et al. [2020].

Lemma 9.

Draw and consider the optimization problem

With probability at least , Algorithm 9 returns using at most oracle calls.

Next, we describe a result on the multiplicative weights update algorithm that follows immediately from Corollary 4 in Arora et al. [2012]. Consider the experts problem. The set of events is denoted by . Suppose there are experts. At each round , the agent picks an expert and the adversary picks an outcome and the agent obtains reward . The multiplicative weights update algorithm mains a distribution over the experts and chooses an expert randomly from (see Arora et al. [2012] for details on how this distribution is chosen). The adversary may have knowledge of the when choosing . The following provides a lower bound on the expected reward obtained by the multiplicative weights update algorithm.

Theorem 9.

Let denote an error parameter. Suppose there are experts and . If the multiplicative weights algorithm sets the learning rate as , after , then the multiplicative weights algorithm achieves the following bound on its average expected reward: for any expert ,

D.4 Convergence Lemmas

The objective in semi-feedback is convex (by a similar argument to the proof in Katz-Samuels et al. [2020]).

Proposition 7.

Fix .

is convex.

Proof.

Fix and . By matrix convexity,

Furthermore, since the above matrices are diagonal,

Then, by Sudakov-Fernique inequality (Theorem 7.2.11 in Vershynin [2018]),

∎

Next, we turn to analyzing stochastic Frank-Wolfe. Although a convergence result for stochastic frank wolfe is provided in Hazan and Luo [2016], our setup is slightly different, so we include a convergence analysis for our setting for the sake of completeness. The proof is quite similar to the proof in Hazan and Luo [2016].

Proposition 8.

Let and . Define and define

Suppose that . Suppose that is convex, , and in Algorithm 11 is chosen such that with probability at least

where . Then, with probability at least ,

Proof.

The proof follows closely the analysis of SFW in Hazan and Luo [2016] but uses smoothness wrt . We have that

| (29) | ||||

| (30) | ||||

| (31) |

where line (29) uses smoothness (Lemma 11), line (30) uses the optimality of , and line (31) uses the definition of the dual norm. Now, define the event

By hypothesis, is chosen such that with probability at least , . Therefore, we have that

Now, suppose occurs. Then, we have that for all ,

The proof is concluded by simple induction. ∎

The following Lemma shows that Algorithm 8 is an instantiation of stochastic Frank-Wolfe over .

Lemma 10.

Fix . Let

Define

Then, .

Proof.

This follows by a straightforward case by case analysis. ∎

The following is standard smoothness Lemma from convex optimization.

Lemma 11.

Let satisfy . Then,

Proof.

This is standard (see Bubeck [2014]). ∎

D.5 Differentiability Lemmas

In this section, we show that is twice-differentiable wrt . We set for simplicity and write instead of for the sake of brevity. The following Lemma shows that is differentiable wrt .

Lemma 12.

Fix , and . Fix such there exists a neighborhood of such that

Then,

Furthermore, is differentiable at every and

where

Proof.

The calculation of follows by the chain rule.

Fix . Since , we have that is full rank.

Step 1: First, we show that is Lipschitz with an absolutely integrable Lipschitz constant. Define

and note that

Let . Thus, by the mean value theorem, we have that for all ,

Since and the maximum of -Lipschitz functions is -Lipschitz, we have that

Step 2: Now, we show that the partial derivatives exist. Define the event

Since is full rank and each

is distinct, if , then with probability holds and is differentiable at .

Since is -Lipschitz (because , we have

Since in addition , by the dominated convergence theorem,

where the last equality follows since on and , exists. Thus, the partial derivative exists at every point and

Step 3: We claim that the partial derivative is continuous in , which would show that that is differentiable at every Munkres [2018]. Let be a sequence in such that . Note that since , we have that

for an appropriate universal constant , which has finite expectation. Further, since , the calculation showing that is Lipschitz in implies that is Lipschitz in , so can be made arbitrarily close to . If , this implies that:

for some , the unique value the argmax is attained at, and . As we can make arbitrarily close to , it follows that for large enough , we can guarantee:

so the maximizer will be unique. As this is true for all , it follows that . An identical argument implies , so . Then, by the dominated convergence theorem,

where in the last line we used the continuity of in on for a fixed . Thus, the partial derivatives are continuous, proving differentiability at every .

∎

The following Lemma shows that is twice-differentiable wrt .

Lemma 13.

is twice-differentiable at every and

where

Proof.

Step 0: Setup. From Lemma 12, is differentiable at every . Therefore, it suffices to show that is differentiable at every . It suffices to show that the 2nd order partial derivatives exist and are continuous. For the sake of abbreviation, define and . Note that we have that

| (32) | ||||

| (33) |

To begin, we show that the 2nd order partial derivatives exist using a truncation argument. Let . Fix . Define

Define

Note that

Step 1. First, we show that

| (34) |

Define

for . Note that since for any fixed , is Lipschitz in on , there exists depending on such that for all

Let . Let . Let such that it satisfies and let . Let . Then,

which implies that . Thus, on , for all , is the same and hence for all and is thus differentiable for all . Thus, by the mean value theorem, we have that

for some . Inspection of (33) shows that using

Thus, we may apply the dominating convergence theorem to obtain

Step 2. Now, we show that

| (35) |

Define

Note that for every

and . Therefore, by the dominating convergence theorem,

Step 3. Now, we show that

| (36) |

By step 1, for every ,

for some constant . Therefore, by the bounded convergence theorem for limits, we have that

More formally, consider some sequence such that as and as . Let . If then the result is proven. Let and . Note that for finite , is uniformly bounded for all . Then the Bounded Convergence Theorem applied to the counting measure gives that:

However, , so the above implies:

By construction, we have , which proves the result.

Fix . Define

Note that for every

and . Thus, by the dominating convergence theorem,

This completes the step.

Thus, we have that that the second order partial derivatives exist and derived an expression for them. Showing that the second order partial derivatives are continuous proceeds as in the proof of Lemma 12 (apply the dominating convergence theorem).

∎

Appendix E Rounding

Theorem 10 (Caratheodory’s Theorem).

For any point in the convex hull of a set , can be written as a convex combination of at most points in .

Proof.

This is a standard result in convex geometry, see for instance Eggleston [1958]. ∎

Lemma 14.

Given any , in the bandit setting, there exists a distribution that is -sparse and:

In the semi-bandit setting, when , there exists a distribution that is -sparse and:

Proof.

This is a direct corollary of Caratheodory’s Theorem. Take and let , which we define as:

Define the set:

For any , we see that lies in the convex hull of . Caratheodory’s Theorem then immediately implies the result in the bandit case, since uniquely determines .

In the semi-bandit case, we note that the diagonal of is equal to . Thus, we only need to consider a -dimensional space, so Caratheodory implies we can find a sparse distribution. ∎

Proof of Lemma 1.

Given some allocation , let the corresponding distribution, and (so ).

Since we only care about the sparsity of , consider fixed. Then, given a solution to (2) or (3), the value of the constraint and objective the solution achieves achieves are fully specified by and . To see the latter, note that . Lemma 14 then implies that there exists a distribution that is -sparse in the bandit case and -sparse in the semi-bandit case that achieves the same value of the constraint and objective of (2) or (3).

To see the second part of the result, note that if we run the procedure of Theorem 4, we will run stochastic Frank Wolfe for a polynomial number of steps, each increasing the support of our distribution by at most 1, so we will obtain an approximate solution that has at most non-zero entries. By Theorem 6 in Maalouf et al. [2019], it then follows that we can compute the -sparse distribution achieving the same value of the constraint and objective in time . ∎

Appendix F Gaussian Width Results

Proposition 9.

| (37) |

Proof.