Discrimination in the Venture Capital Industry:

Evidence from Field Experiments

Abstract

This paper examines discrimination by early-stage investors based on startup founders’ gender and race using two complementary field experiments with real U.S. venture capitalists. Results show the following. (i) Discrimination varies depending on the context. Investors implicitly discriminate against female and Asian founders when evaluating attractive startups, but they favor female and Asian founders when evaluating struggling startups. This helps to reconcile the contradictory results in the extant literature and confirms the theoretical predictions of “discrimination reversion” and “pro-cyclical discrimination” phenomena. (ii) Among multiple coexisting sources of discrimination identified, statistical discrimination and implicit discrimination are important reasons for investors’ “anti-minority” behaviors. A consistent estimator is developed to measure the polarization of investors’ discrimination behaviors and their separate driving forces. (iii) Homophily exists when investors provide anonymous encouragement to startups in a non-investment setting. (iv) There was temporary, stronger discrimination against Asian founders during the COVID-19 outbreak.

Keywords: Discrimination, Field Experiments, Venture Capital, Entrepreneurship

JEL Classification: C93, D83, G24, G40, J15, J16, J71.

1 Introduction

The persistent gender gap and racial disparities (Bertrand et al. (2010), Bertrand and Hallock (2001), Chetty et al. (2020)) at the top of the earnings distribution often raise the question of whether explicit or implicit discrimination creates a glass ceiling for women and nonwhites in modern U.S. society (Bertrand et al. (2005a)).222Hegde et al. (2021) document the “glass ceiling” phenomenon by analyzing detailed administrative records for the universe of patent examiners at the U.S. Patent and Trademark Office. They find that minority examiners are less likely to be promoted to the most senior grades. Therefore, a significant amount of attention and debate about discrimination concentrate on top-level, high-skilled labor markets and relevant financial markets.333“Having A Glass Ceiling To Break Through Is Privilege. Here’s Why.” May 13, 2021, Forbes Despite the existence of a large body of academic literature on empirically testing discrimination in various markets,444For a recent summary, see Lang and Kahn-Lang Spitzer (2020), Lang and Lehmann (2012), and Bertrand and Duflo (2017). most prior work mainly focuses on the entry-level and low-skilled labor market and product market (Bertrand and Mullainathan (2004), Giuliano et al. (2009), Kessler et al. (2019), List (2004)). For the few papers studying discrimination in the high-skilled labor market, such as the entrepreneurial finance market, previous literature has provided conflicting empirical findings due to a lack of natural experimental settings.

In this paper, I re-examine discrimination issues in the U.S. entrepreneurial finance market, which generates huge amounts of wealth and produces many business leaders. Through two complementary field experiments with real U.S. venture capitalists (VC), this paper first identifies the existence of gender and racial discrimination by early-stage investors as well as the nature of this discrimination. Moreover, the paper also investigates how the direction and magnitude of the discovered discrimination vary across the distribution of startups’ attractiveness and in different market conditions.555Based on Gompers and Wang (2017a), 87% of U.S. venture capitalists are white, and investors may have an unconscious bias against minority founders. Given the uniqueness of the entrepreneurial financing setting, this paper mainly studies racial discrimination faced by Asians, who are the largest minority group in the U.S. entrepreneurial community. “Asians” in this paper primarily stand for “East Asian” groups who originate mainly from China, Korea, Vietnam, etc. According to Gompers and Wang (2017a), Asians account for 18% of new U.S. venture capitalists and 15% of new entrepreneurs entering the market. Studying discrimination against African Americans and other under-represented minorities is an important question. However, this paper’s experimental design would need to be adjusted for future researchers to study these important questions. The documented distributional effect and dynamic changes of discrimination not only empirically confirm the theoretical predictions of the “discrimination reversion” and “pro-cyclical discrimination” phenomena in Morgan and Várdy (2009), but also enable the reconciliation of the contradictory results of previous empirical papers. Since the VC industry plays an important role in fostering innovative and successful companies (Bernstein et al. (2016)), rigorously identifying such discrimination and its nature is of critical importance not only for maintaining social fairness (Fang and Moro (2011)) and assessing the efficiency of capital allocation (Bertrand (2020)), but also for explaining the persistent gender and racial gap at the top level.

While the stark gender funding gap and the less favorable treatment received by nonwhite founders in the fundraising process has been well-documented (Ewens and Townsend (2020), Guzman and Kacperczyk (2019), Henderson et al. (2015), Hebert (2020)),666Gompers and Wang (2017b) demonstrate that from 1990-2016, women have made up less than 10% of the entrepreneurial and venture capital labor pool despite an increase in female labor market participation during this period. Based on Gornall and Strebulaev (2020), venture capitalists only invested 1 dollar in startups with female founding teams for every 35 dollars invested in startups with male founding teams in 2017. Also, Guzman and Kacperczyk (2019) document that female-led ventures are 63 percent less likely than male-led ventures to have obtained external funding (i.e., venture capital) from 1995-2001, even though women and men are equally likely to achieve exit outcomes through IPOs or acquisitions. causally identifying discrimination and its nature in this setting poses new challenges for the commonly used empirical methods.777According to List (2004), empirically testing for marketplace discrimination has taken two quite distinct paths in economic research: regression-based methods and field experiments. For more discussion on field experiments, see List and Rasul (2010), List (2007), Levitt and List (2009), List et al. (2011), etc. Moreover, extant literature provides seemingly conflicting results. On the one hand, papers exploiting regression-based methods (Ewens and Townsend (2020), Guzman and Kacperczyk (2019), Henderson et al. (2015)) often show that women-led and minority-led startups are associated with a lower likelihood of raising external funding, suggesting the existence of gender and racial discrimination. These non-experimental studies potentially suffer from omitted variable bias due to a lack of exogenous variations.888Since most venture capital funds and startup companies are private firms, some startups’ unique comparative advantages are usually only observable to investors rather than to researchers. Also, most databases only observe the match outcomes between investors and startups, making it difficult to separate investors’ preferences from founders’ preferences. However, natural experimental settings are rarely available to solve various endogeneity concerns. On the other hand, Gornall and Strebulaev (2020) implement the first correspondence test, a widely used field experimental method, in the U.S. VC industry. They find that early-stage investors are biased towards female and Asian founders because surprisingly, investors reply more frequently to fictitious cold call, pitch emails sent by female and Asian names compared to male and white names. The major concern with this field experiment is that sending cold call emails is not a mainstream fundraising method used by high-quality startups. Hence, results mainly capture how investors evaluate struggling startup teams and might not be generalizable to the situation of evaluating top startups. Also, the “low-response-rate” problem is more severe in this setting compared with other markets,999According to Gornall and Strebulaev (2020), the response rate to cold call pitch emails with attractive startup characteristics is about 6.5% in 2018, an economic boom period. This paper shows that the email response rate to pitch emails with quality variations (i.e., including both attractive and average startup characteristics) is roughly 1% in 2021, an economic recession period. The difference in email response rates in these two papers comes from both the pro-cyclical nature of early-stage VC investment and the additional quality variations introduced in this study. Bertrand and Duflo (2017) discuss other standard limitations of the correspondence test method. making it difficult for researchers to introduce variations in startup quality and test the nature of discrimination.101010Disentangling the nature of discrimination requires researchers to separate various belief-based mechanisms (i.e., “statistical discrimination”) (Bertrand and Duflo (2017), Altonji and Blank (1999), Phelps (1972), Arrow et al. (1973)) from different taste-based mechanisms (i.e., “animus”) (Becker (2010)). This disentanglement is difficult to accomplish in discrimination literature (Gneezy et al. (2012)) despite its importance in both welfare analysis and policy-making (Bohren et al. (2019a), Neumark (2012)).

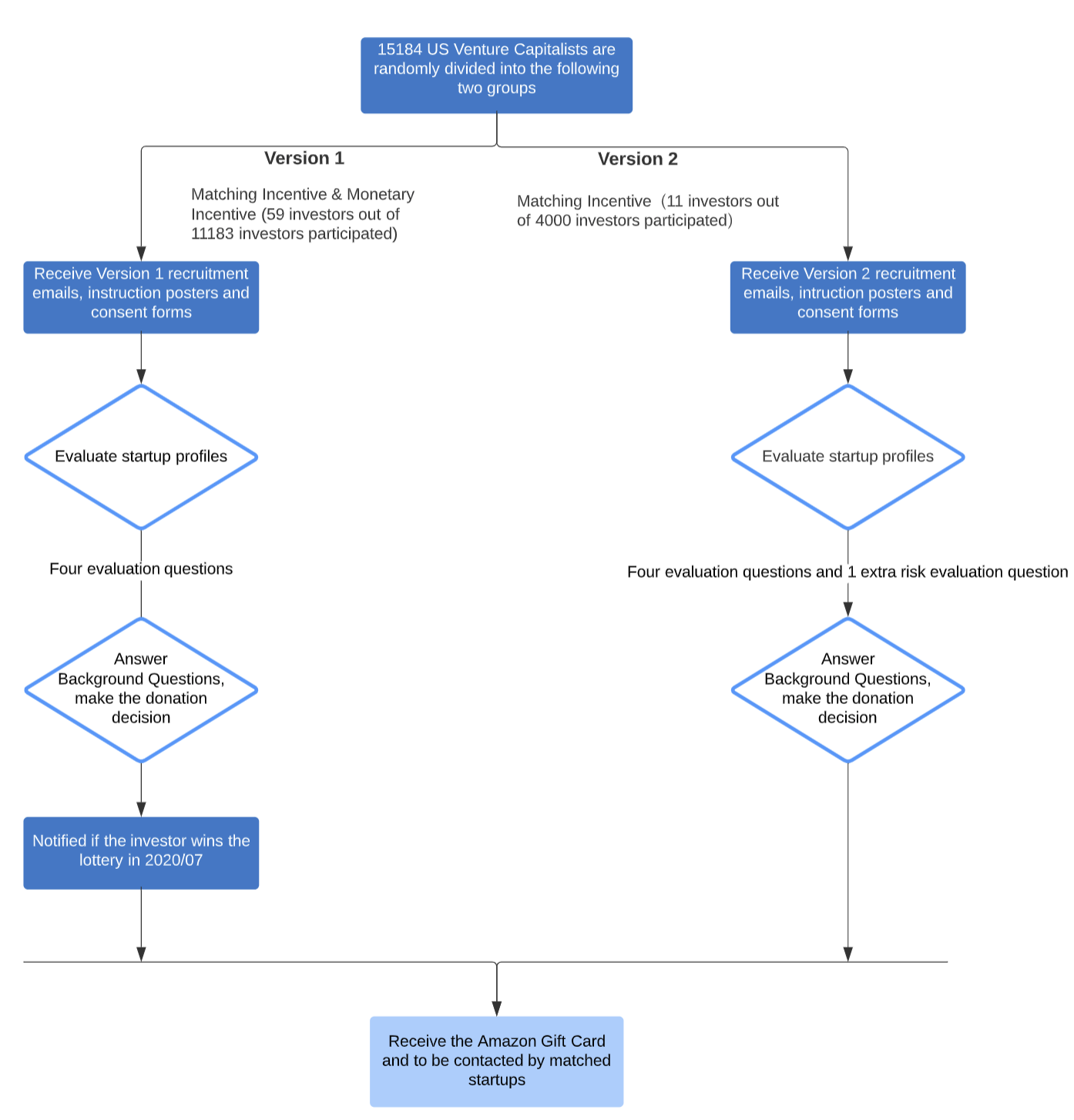

To overcome the identification challenges mentioned above and reconcile the mixed results in the literature, this study implements two complementary field experiments in the U.S. entrepreneurial finance market, referred to as Experiment A and Experiment B in this paper. Experiment A combines two preference elicitation techniques: an “incentivized resume rating (IRR)” experiment (Kessler et al. (2019)) and a “donation game” (Carpenter et al. (2008)). To implement it, I collaborate with several accelerators and build a “Nano-Search Financing Tool,” a machine learning matching tool that facilitates VCs’ deal sourcing process. In the first part of this matching tool, investors need to evaluate multiple dimensions of randomly generated startup profiles. Investors know the profiles are hypothetical, but truthful evaluations help the algorithm to better match investors with their preferred startups. Hence, the IRR experiment uses real investment opportunities to reveal VCs’ investment preferences and directly identify the nature of discrimination.111111To increase the sample size, some randomly selected investors also receive a “monetary incentive” following Armona et al. (2019) so that the more accurate investors’ evaluation results are, the larger the monetary award the lottery winners will receive. Although the “monetary incentive” elicits slightly different sources of investors’ beliefs compared to the “matching incentive”, Section 3 justifies its usage by showing that investors’ profitability judgements elicited by these two incentives do not differ quantitatively. Besides investment, VCs also add value to startups by providing non-investment support. To test whether discrimination also exists in a non-investment setting, in the second part of this matching tool, investors can anonymously donate a portion of a provided unexpected $15 Amazon Gift Card to randomly displayed startup teams. The researcher will use the donated money to purchase small gifts for the corresponding startup teams in the collaborative incubators and provide founders with anonymous encouragement from investors during the COVID-19 pandemic recession.

Experiment A yields the following findings. First, although Experiment A does not discover aggregate-level discrimination against minority founders, it does identify significant implicit discrimination against female founders. After investors become fatigued from evaluating multiple profiles, their ratings of women-led startups begin to decline. At the end of the IRR experiment, women-led startups are 16.67% less likely to be contacted by investors and also receive 19.4% less funding compared to similar men-led startups. Second, results from quantile regressions demonstrate a distributional effect in the initial contact stage, suggesting that the direction and magnitude of implicit discrimination can vary across the spectrum of startups’ attractiveness. Significant and strong implicit gender, racial, and age discrimination mainly exists when investors evaluate top startups, especially in the tech sector. Hence, results that capture the fundraising situation of struggling startups are not generalizable to that of attractive startups. Third, as predicted by Morgan and Várdy (2009), implicit discrimination is pro-cyclical. Discrimination becomes more severe when investors’ internal thresholds increase and their startup investment criteria become more selective. However, discrimination might reverse when investors are sufficiently unselective. Fourth, homophily exists in a non-investment setting.121212“Homophily effect” refers to the tendency for people to seek out or be attracted to those who are similar to themselves. Compared to male founders, male investors on average donate $3.20 less to female founders and are also 77% less likely to donate all money to female founders. Similar homophily exists within the white male group and within the other group.

Experiment A shows that some investors exhibit implicit discrimination against female and Asian founders. However, there are also some impact funds that support minority founders in the sample. So, how divided is the investment community in terms of their attitude towards minority founders, and what separates us? To answer this question in Experiment A, I develop a consistent “decision-based heterogeneous effect” estimator by using the “leave-one-out” technique and exploiting both the rich data and the exogeneous “within-individual” randomization of the IRR experiment.131313Junlong Feng has provided crucial help and discussions for developing this estimator. Standard heterogeneous effects rely on participants’ pre-determined demographic information. However, since each investor evaluates multiple randomized profiles, researchers can identify “individual-level” preferences and classify the participants into an “anti-minority” group and a “pro-minority” group based on their indicated decisions. The estimator finds that investors’ profitability ratings can explain investors’ heterogeneous contact decisions more than other mechanisms. For example, investors who prefer not to contact female founders expect women-led startups to have 16.40 percentile ranks lower potential financial returns than men-led startups. However, investors who prefer to contact female founders expect women-led startups to have 7.93 percentile ranks higher potential financial returns than men-led startups. However, investors’ availability ratings are not significantly different between the “pro-minority” groups and “anti-minority” groups. Similar “decision-based heterogeneous effects” also exist when investigating racial discrimination and agism. Therefore, holding different beliefs in the profitability of minority-led startups and majority-led startups is an important reason for the polarization in investors’ attitudes towards minority founders.

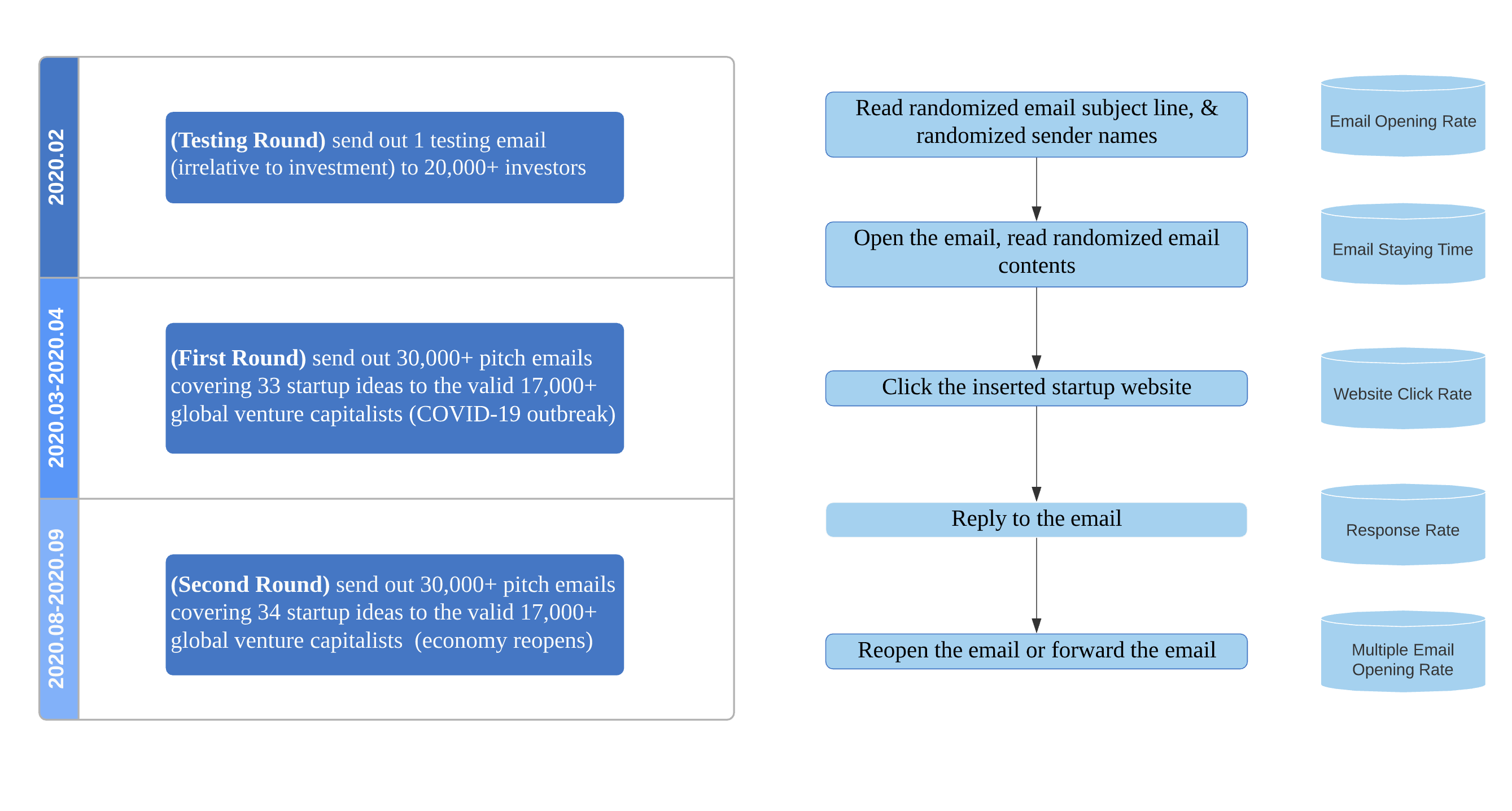

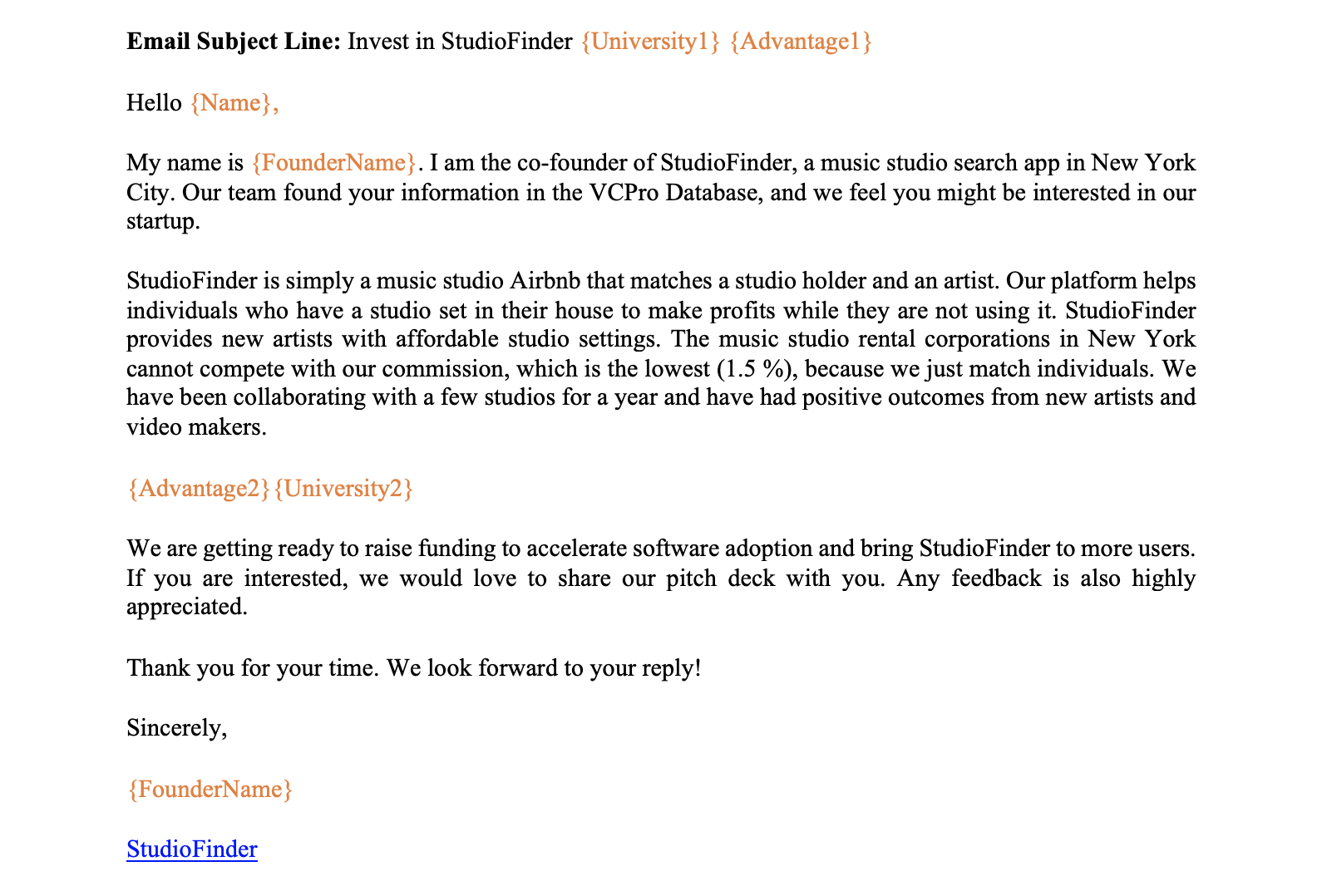

Although Experiment A identifies that discrimination mainly exists when investors evaluate highly-rated startups, it does not have enough statistical power to investigate how investors evaluate struggling startups. Hence, the paper follows up with Experiment B, a redesigned correspondence test that enables researchers to identify the nature of discrimination in the cold call, pitch email setting. During the COVID-19 outbreak (03-04/2020), I sent hypothetical pitch emails to more than 17,000 venture capitalists with randomized founder names indicative of gender and race, randomized founder educational backgrounds, and randomized startup project characteristics displayed in both the emails’ subject lines and in the emails’ contents. By utilizing new email tracking technology, I can monitor detailed information acquisition behavior for each investor, including email opening behavior, time spent on pitch emails, click rate on the inserted startup’s website, the contents in email replies and the email response rate.141414This experimental design and behavioral measurements generated enough experimental power to survive in the harsh experimental environment of the pandemic, when early-stage investors dramatically slowed down their investment pace (Howell et al. (2020)). Since most high-quality startups would prefer a “warm” fundraising method, Experiment B mainly studies how investors evaluate struggling startups.151515Before using this experimental design, the researcher originally tried to collaborate with real startup teams and send their randomized truthful information to investors. However, it was extremely hard to recruit enough real startups to cover major industries that VCs invest in. Startup founders are usually worried that the success rate of raising funding through cold call pitch emails is extremely low. Moreover, this “cold” method might make a bad impression on VCs, indicating that the startup has failed with other warmer fundraising methods.

Experiment B’s results confirm that investors are slightly biased towards female and Asian founders in the pitch email setting. Using minority names generally increases the email opening rate by roughly 1% compared to using majority names. After further testing the nature of bias, the paper finds that the bias towards female founders is likely driven by taste-based mechanisms. The positive “female name” effect is much larger for impact funds, and revealing additional quality signals does not shrink the gender gap. However, the bias towards Asians is likely driven by belief-based mechanisms because revealing additional quality signals reduces the racial gap. As Experiment B was mainly implemented between 03/2020-04/2020, it also finds a temporary discrimination against Asian founders during the COVID-19 outbreak. Investors spent 24% less time on pitch emails sent by Asian names compared to white names in March 2020. However, this discrimination quickly reversed starting in April 2020. Hence, discrimination behaviors might also be temporarily affected by big societal events.

The contribution of this paper is both empirical and methodological. Empirically, combining results from Experiment A and Experiment B, this paper shows that in the pre-screening stage, investors discriminate against minority groups when evaluating attractive startups and are biased towards minority groups when evaluating struggling startups. This distributional effect not only provides an explanation to reconcile contradictory results in the literature, but also confirms the “discrimination reversion” phenomenon that has been theoretically predicted by several fundamental discrimination theory papers (Morgan and Várdy (2009), Phelps (1972), Aigner and Cain (1977), Lundberg and Startz (1983)) but has never been empirically tested before.161616Another possible explanation to reconcile the literature is that investors do not exhibit implicit discrimination when replying to pitch emails, which is also consistent with the results of Gornall and Strebulaev (2020). However, Experiment B finds that investors check emails at different times during the day. Considering that implicit discrimination is already apparent when investors have a relatively light cognitive workload in Experiment A, it is very likely that implicit discrimination also affects investors’ behaviors when they check emails throughout the day. This makes this explanation less plausible. Experiment A also confirms the “pro-cyclical discrimination” phenomenon predicted by the model in Morgan and Várdy (2009). Furthermore, it documents the existence of homophily in a non-investment setting and a temporary, stronger discrimination against Asian founders during the COVID-19 outbreak. Therefore, this paper empirically contributes to both discrimination literature and entrepreneurial finance literature.

Methodologically, the main contribution of this study is to provide a framework to identify discrimination and its nature in a financial and high-skilled labor market after solving multiple challenges faced by commonly used methods through a series of redesigned field experiments. Moreover, the developed “decision-based heterogeneous effect” estimator, which uses rich data and “within-individual” level randomization in the IRR experiment, helps to measure how divided the society is and what drives the polarization of people’s attitudes towards minority groups.

To the best of my knowledge, this is also the first paper to implement the correspondence test and the IRR experiment in the same context and compare their results. The IRR experimental paradigm, which is an incentivized elicitation technique invented by Kessler et al. (2019), is motivated by the desire to provide a more ethical experimental design that can substitute for the standard correspondence test involving deception.171717Special thanks go to Corinne Low for her insightful discussions clarifying the following important nature of the IRR experiment. Following the widely accepted Becker-Degroot-Marschak elicitation techniques of willingness to pay, the IRR experiment provides an incentive structure for eliciting true preferences and provides within-individual level exogenous variations. Also, “the primary context of the IRR experiment is usually non-experimental, and subjects’ motivation for participating in the study is mainly to receive the commercial benefits”. Unlike a “survey,” an IRR experiment requires much more social resources in order to reveal true preferences. By comparing the results from these two experimental methods, this paper shows that in a high-skilled labor market, results from a correspondence test that mainly captures a “cold” setting may not match results from an IRR experiment that captures a “warm” setting, suggesting that neither may be generalizable without caveats. The rich data collected by the IRR experiment enable researchers to identify subtle mechanisms, test novel heterogeneous effects, distributional effects, and dynamic changes in different market conditions. Notwithstanding these impressive merits, increasing use of the IRR experimental method in the future may gradually decrease its ability to detect discrimination due to the potential consent form effect.181818After the IRR experimental design and the corresponding data analysis methods become more well-known among the public, experimental participants might carefully control their behaviors even in the second half the study. I leave addressing these limitations to future research.

This paper is organized as follows. Section 2 discusses the construction of the individual-level VC investor database. Section 3 presents the design of Experiment A and analyzes investors’ evaluations of startup profiles and donation behaviors. Section 4 describes the design of Experiment B and analyzes investors’ information acquisition behaviors. Section 5 provides a comparison of these two experiments, the link to discrimination theories, and related policy implications. Section 6 concludes.

2 Data

To implement these field experiments, I have constructed a cross-sectional, individual-level global venture capitalist database, which contains updated demographic information and contact information for 17,882 investors before 02/2020.191919All investors’ email addresses had been verified by a testing email before the experiments began. Since all experiments are implemented in English, only investors from English-speaking areas are included. This database combines multiple commercial databases and manually collected data. Detailed database descriptions and the key variable construction process are provided in Online Appendix A.

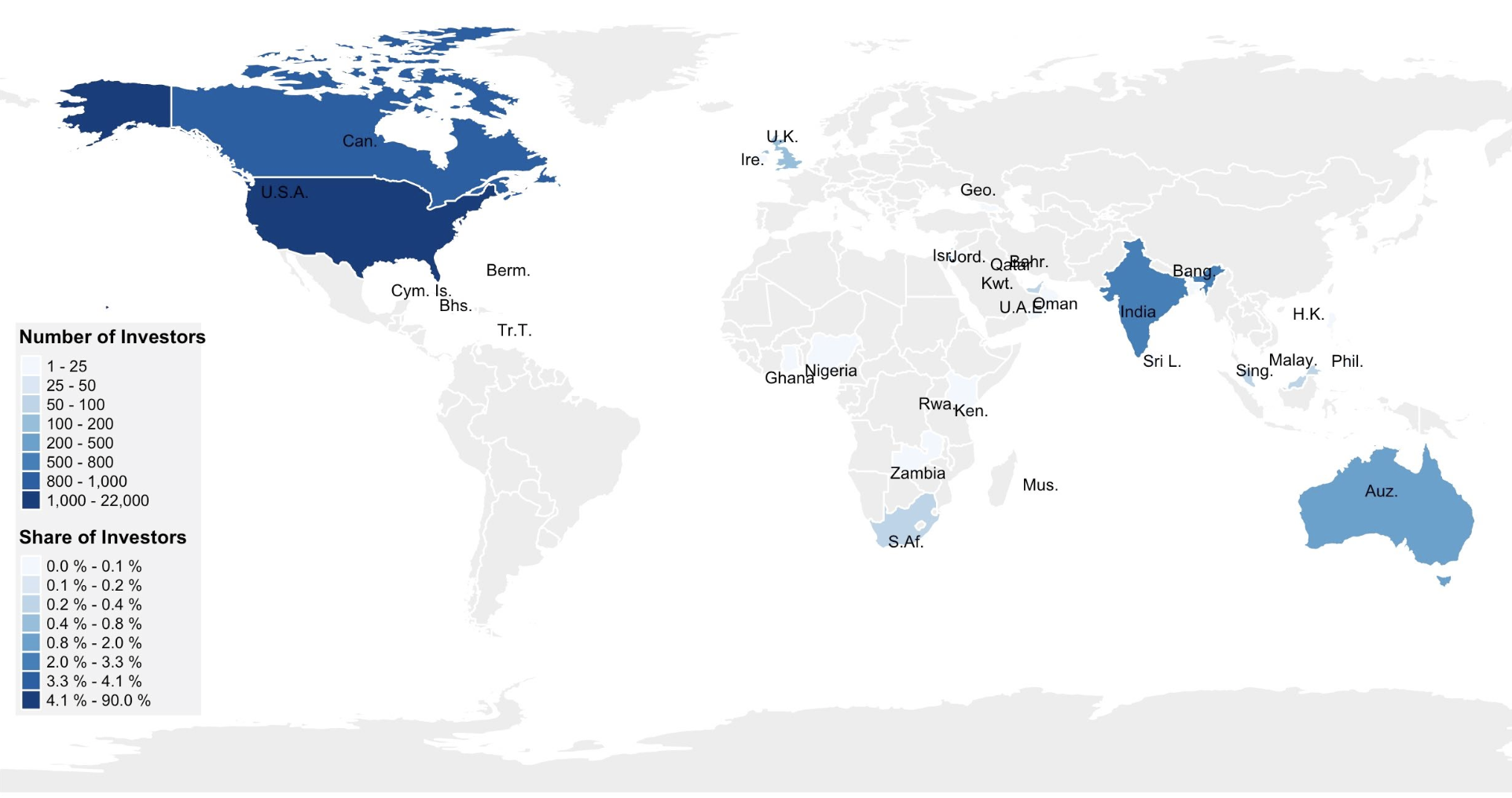

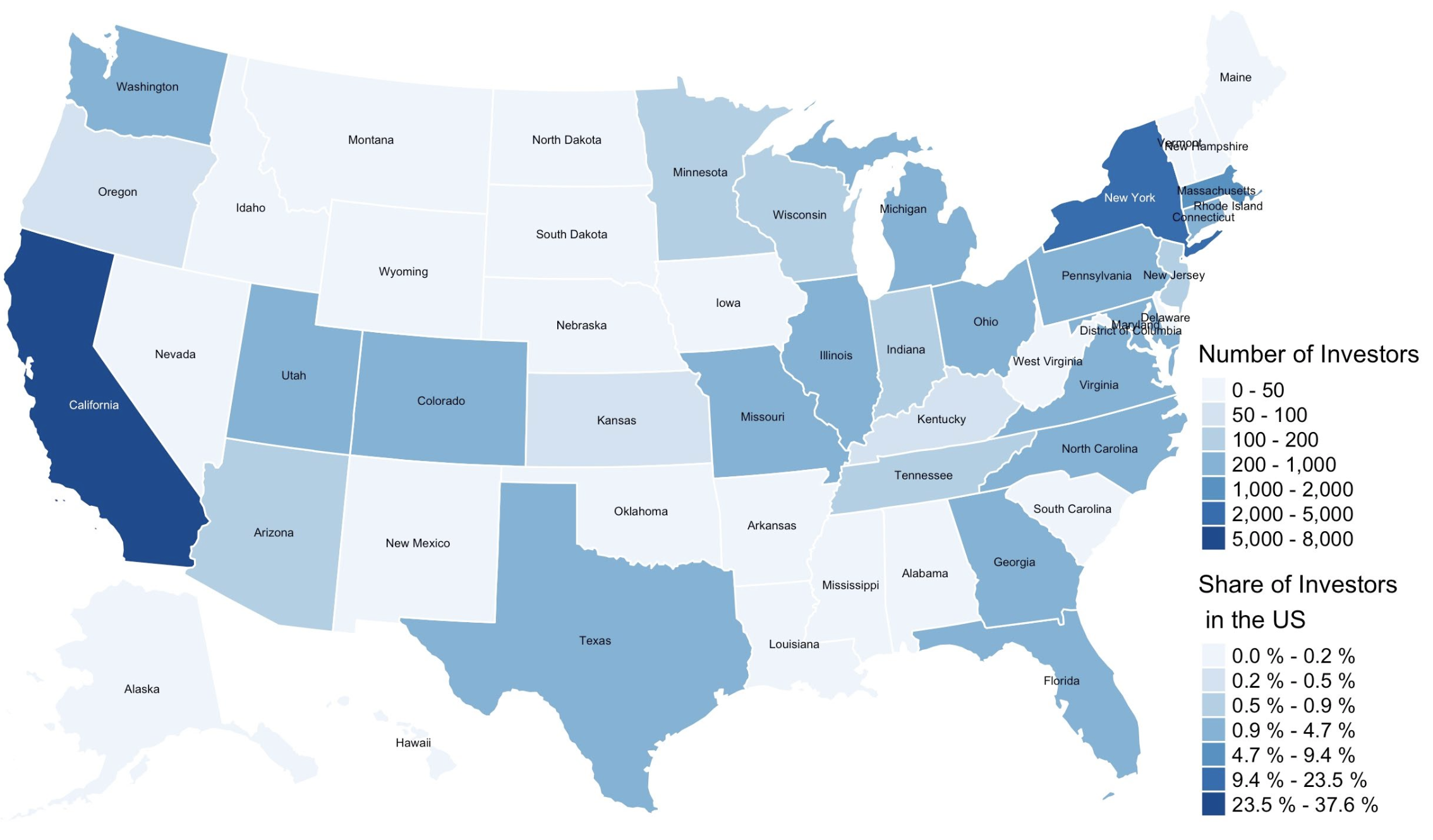

Despite the granular information provided by this database, it is important to realize the following three limitations. First, this database contains systematically more investors from the U.S. as well as more senior VCs due to data availability online and the data collection method used by data companies.202020Most of the commercial databases used here are provided by U.S. data companies and collected by English speakers with the exception of Zdatabase, which is the most comprehensive and timely database covering VC and PE activities in China. Hence, it may not be representative of the true geographical distribution of all venture capitalists in the world. Second, because of the high turnover rate within the VC industry, the contact information and status of these investors need to be updated frequently before use. Third, except for the key variables like gender, seniority, and location, other demographic variables are only available for relatively famous investors whose biographies are more readily available online.

The Summary Statistics of the 17,882 investors’ demographic information is provided in Table 1. Panel A reports the location distribution of these investors, showing that US-based investors account for 84.91% of this set of investors.212121Maps of investors’ global geographical distribution and U.S. geographical distribution are provided in Online Appendix Figure A1 and A2. Panel B shows that most investors are interested in the Information Technology industry. Other important preferred industries include Healthcare, Consumers, and Energy. Panel C summarizes investors’ background information. On average, female investors account for 24% of total investors. This is consistent with the NVCA/Deloitte survey results showing that women accounted for 21% of investment professionals in the U.S. VC industry in 2018 due to recent progress in increasing diversity.222222See “NVCA–Deloitte Human Capital Survey 2019.” Gompers et al. (2014) also show that women are under-represented among senior investment professionals in the VC industry. Senior investors, who are partners, presidents, C-level managers, or vice presidents and above, account for 84% of total investors in the sample. Most investors are institutional investors, and angel investors only account for 11% of the sample. Moreover, only 2% of all investors work in not-for-profit impact funds.232323Pitchbook classifies VC funds into not-for-profit funds and for-profit funds together with the description of their investment preferences. If I use indicative keywords in the fund descriptions to classify the VC funds following Barber et al. (2020), this percentage increases to 6%-8% depending on the keyword selection method.

3 Experiment A’s Design and Results

The goal of designing Experiment A as presented here is to elicit investors’ preferences for startups with a stronger incentive (i.e., real investment opportunities). Since venture capitalists add value to startups by providing both funding (i.e., investment) and non-monetary support,242424A large body of literature has investigated the non-monetary support of venture capitalists, see Lerner (2022), Bernstein et al. (2016), etc. Experiment A combines the following two preference elicitation techniques: i) the IRR experiment, designed to test discrimination and belief-based mechanisms in an investment setting, and ii) the dictator game, designed to test discrimination and potential taste-based mechanisms in a non-investment setting in which investors provide anonymous encouragement to startups during economic hardship.

3.1 Experimental Design

A. Recruitment Process and Sample Investors

Experiment A was implemented from 03/2020 - 09/2020 using only online recruitment methods. I sent invitation emails together with instruction posters to the 15,000+ U.S. venture capitalists who also participated in Experiment B during the same period.252525During the COVID-19 pandemic, Columbia IRB paused all field work which involves person-to-person activities due to COVID-19. The recruitment email templates and the instruction poster templates are provided in Online Appendix B Figure B7, Figure B8, Figure B9, and Figure B10. This ensures comparability across these experiments. To recruit real venture capitalists and create an experimental setting that closely mimics the real world, I have partnered with several real incubators and we have built a machine learning, algorithm-based matching tool called the “Nano-Search Financing Tool”. Developing these kinds of data-driven matching tools has become popular in the VC industry. Incubators and VC funds, such as Techstars, Social+ Capital, and Citylight Capital, have worked extensively on developing machine learning algorithms to help evaluate investments, seek deals, and complement face-to-face multiple stage investment strategies. Similarly, our tool aims to match investors with startups in the collaborating incubators and mainly captures investors’ preferences in the pre-selection stage (i.e., “ex ante screening” in Cornell and Welch (1996)).

In total, 69 real U.S. investors from 68 different VC companies participated in Experiment A, which provides 1,216 startup profile evaluation results.262626At the beginning of the study, each investor evaluated 32 profiles, and 6 investors finished the 32-profile version of the evaluation task. However, to recruit more investors, later participants only needed to evaluate 16 profiles. Also, one investor participated in the experiment twice for two different VC funds. Results are similar after removing the first 6 investors. The sample size is comparable with Kessler et al. (2019). Given that the response rate is roughly 0.5%, Table 2 compares the observable characteristics of recruited investors and the venture capitalists recorded in Pitchbook Database to check for sample selection bias during the recruitment process. Panel A shows that the recruited investors’ sectors of interest are representative and cover all major industries focused on by VC investors. Panel B shows that 67.1% of the recruited investors are early-stage investors, who are interested in the Seed stage. Panel C shows that while the sample investors are representative in terms of gender, 42% of investors belong to minority groups (i.e., Asian, Hispanic, African, etc.). This is higher than the percentage of minority investors in the U.S. Furthermore, 86% of recruited investors are in senior positions, as their contact information is more readily available in existing databases.

The major concern is whether Experiment A only recruits investors who systematically discriminate more against women and Asians. Since each experimental participant’s identity and affiliated VC company is observable, Panel E further compares the investment histories of the 69 recruited investors’ affiliated VC companies and those in Pitchbook. Results show that recruited investors are more likely to come from large and active VC companies. As the experiment was implemented during the pandemic recession, most early-stage VC investors shifted to “survival mode” and paused new investments (Howell et al. (2020)). Hence, only those large and active VC companies were still attracted by the potential investment opportunities offered by Experiment A. Importantly, recruited investors’ affiliated VC companies do not invest less in women-led startups compared to other investors in Pitchbook. Some might also speculate that recruited investors may not care about the incentives provided by Experiment A. Since Camerer and Hogarth (1999) shows that experimental subjects behave in a more pro-social way in weakly incentivized experimental settings, this implies that Experiment A might underestimate investors’ discrimination against women and Asians.

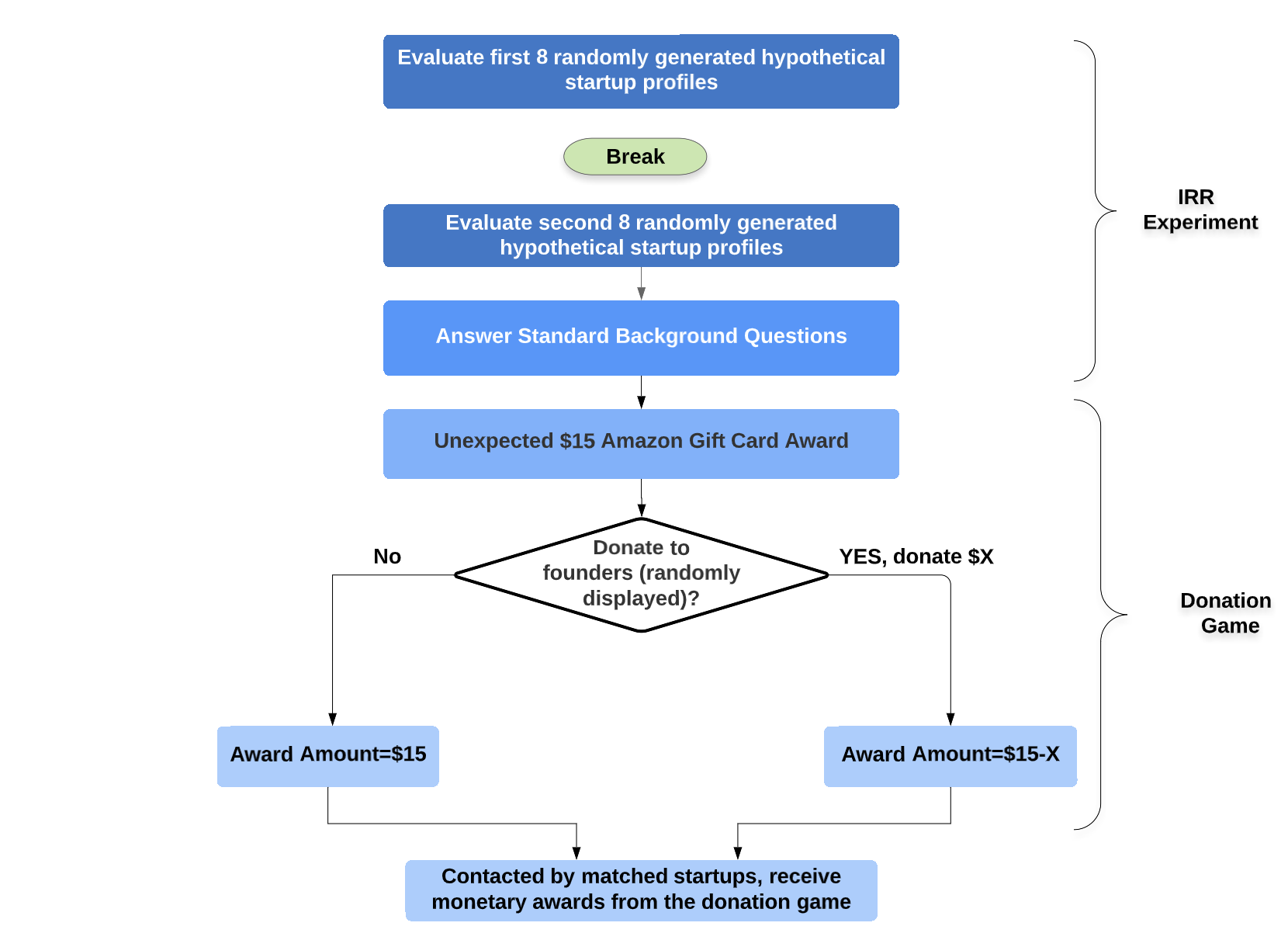

B. Survey Tool Structure

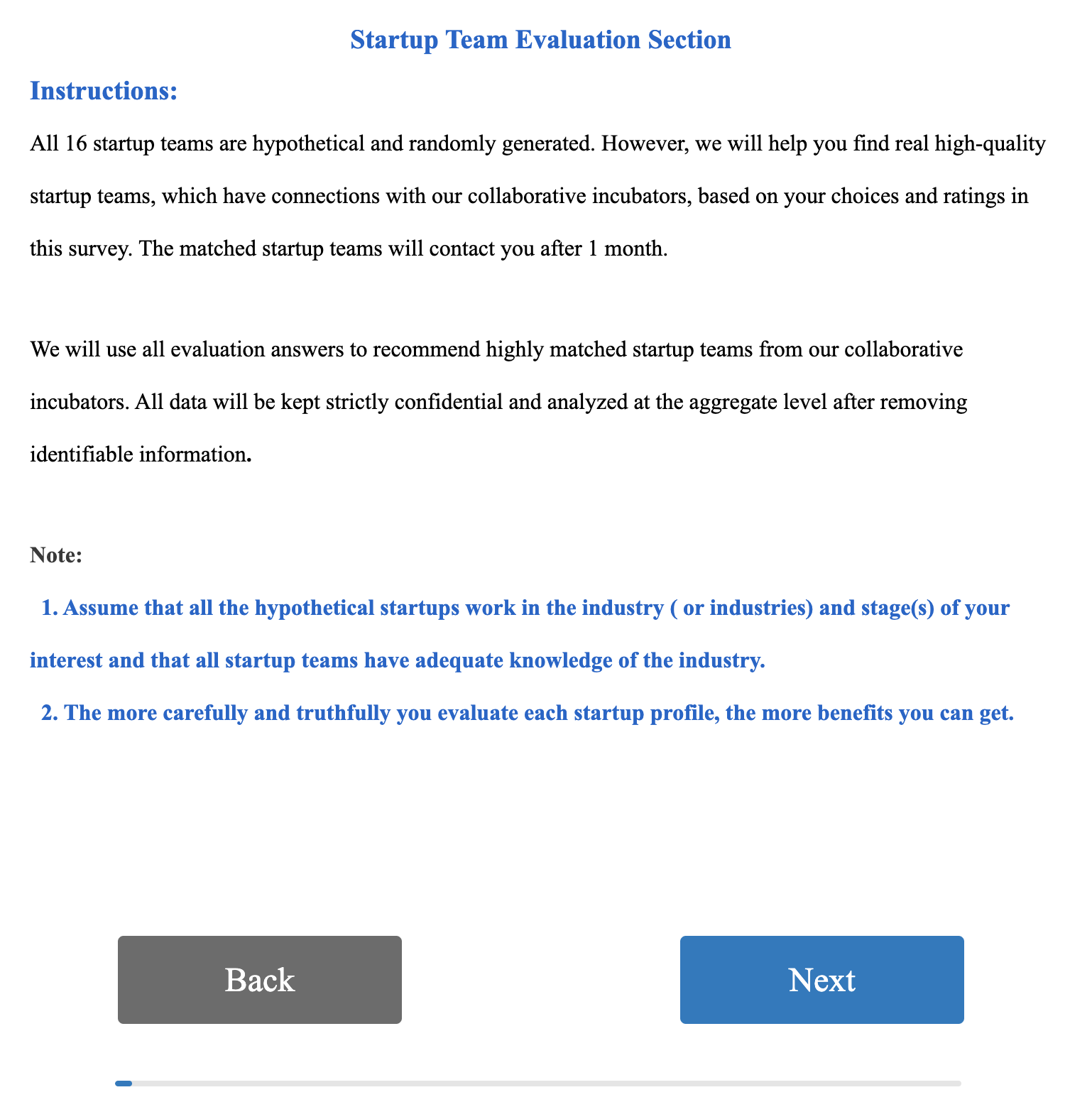

The survey tool mainly contains the following two sections. After reading the consent form, investors first enter the profile evaluation section (i.e., the IRR experiment section), in which they need to evaluate 16 randomly generated startup profiles and answer standard background questions. The second section is the donation section (i.e., the dictator experiment section), in which investors decide how much of an unexpected $15 Amazon Gift Card they want to donate to randomly displayed startup teams. Online Appendix Figure B1 provides a flowchart for Experiment A.

To help participants understand how the incentive works, I also provide an instruction page before the first profile evaluation section. Although investors know that all the startup profiles are hypothetical, this instruction page emphasizes that “the more accurately they reveal their preferences, the better outcomes the matching algorithm will generate (and the higher financial return that the lottery winner will obtain).” Moreover, since most VC investors only invest in startups in their industries and stages of interest (i.e., “qualify/disqualify” test), I ask all the participants to assume that the generated startups they will be evaluating are in their industries and stages of interest. The matching tool will collect each investor’s preferred industry and stage after the profile evaluation section.272727One can also design separate startup profiles with more customized business models for investors from different industries. I did not do this because the market changes very quickly in the entrepreneurial community, especially during the COVID-19 period. Startups’ business models created in the design stage are likely to be invalid during the recruitment stage. Moreover, to obtain insights from investors in diverse industries, Experiment A should provide general information that accommodate as many participants with diverse backgrounds as possible.

B.1 Profile Evaluation Section (IRR Experiment)

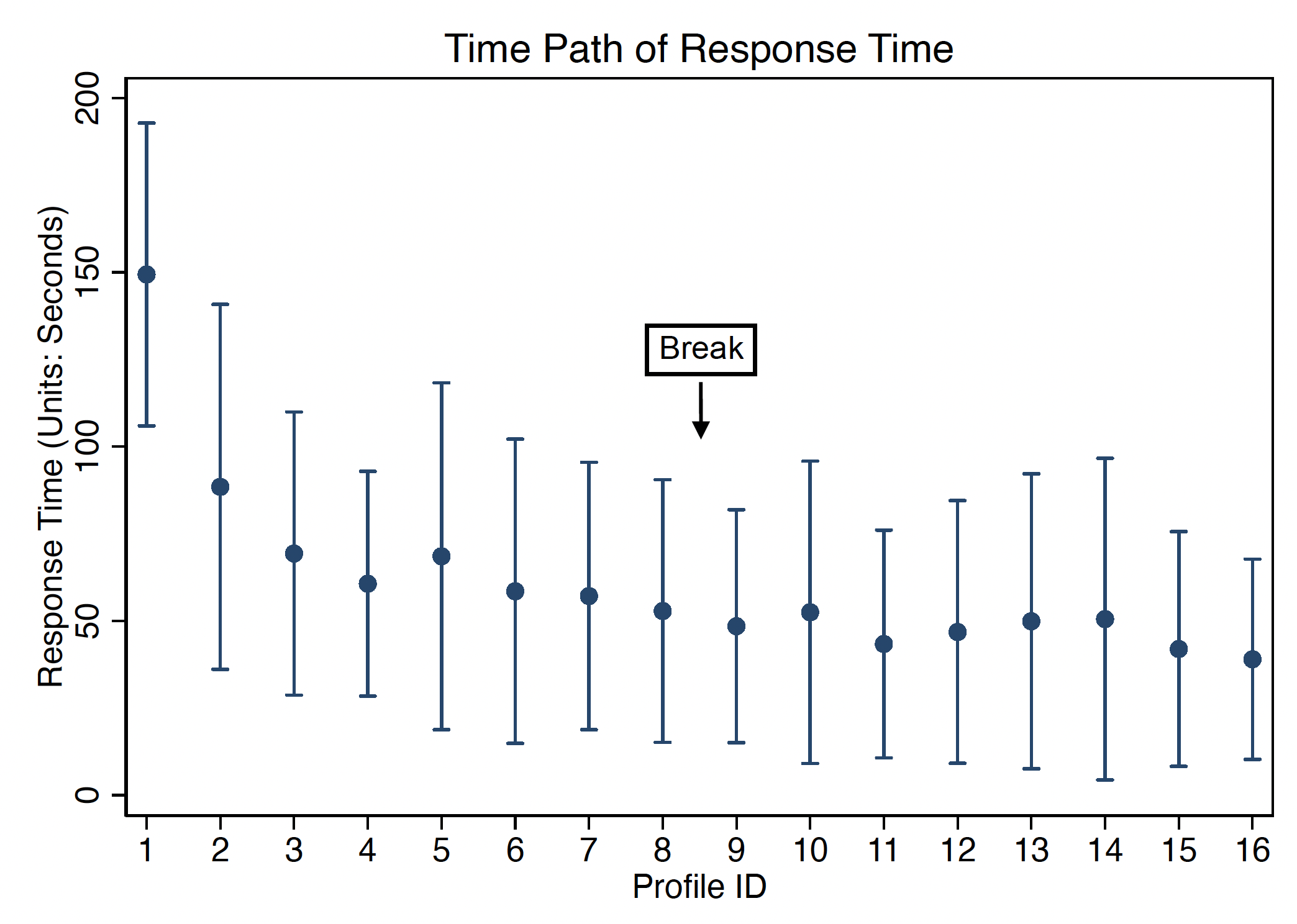

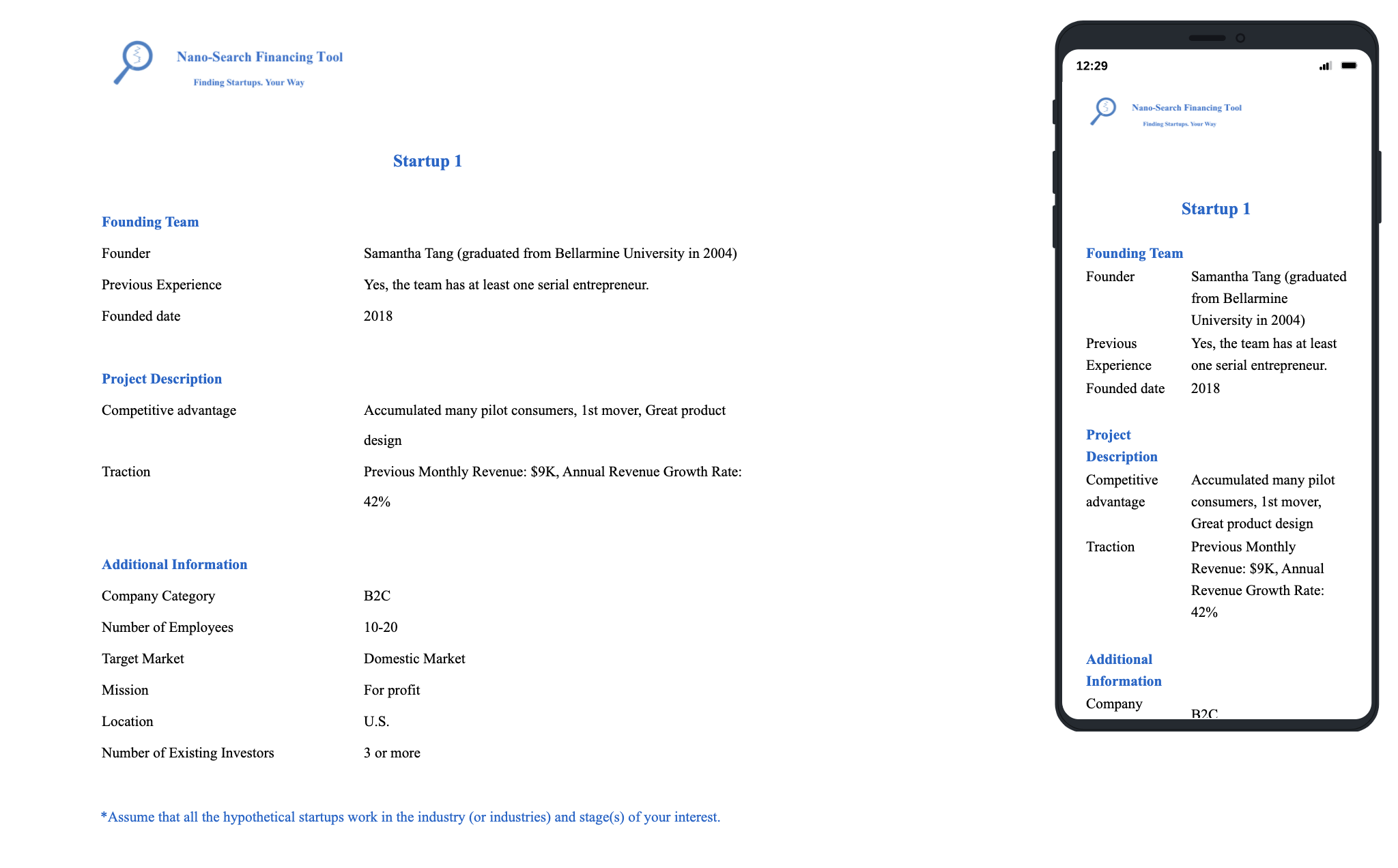

Following the factorial experimental design, Experiment A randomizes multiple startup characteristics simultaneously and independently in each created startup profile. The researcher first creates a set of startup team and project characteristics. Then the backend Javascript code randomly draws different characteristics and combines them together to dynamically create a hypothetical startup when each investor evaluates a new startup profile.282828Sometimes the random combination may generate unusual cases, such as a startup with 50+ employees that still does not generate profits (see Amazon’s history). However, such cases account for a small percentage of total generated cases. To test implicit discrimination, Experiment A also deliberately introduces a short break after investors evaluate the first eight startup profiles. This break presents a page indicating the investor’s progress and encouraging them to finish all the evaluations. All the randomization of different startup components is provided in Table 3.292929The detailed construction process of the startup characteristics is provided in Online Appendix B.

To make profiles more realistic, Experiment A implements the following two designs. First, the information provided about startups follows a “Crunchbase” format and is usually publicly available on LinkedIn, Crunchbase, or AngelList.303030Crunchbase is a commercial platform that provides public information about startups mainly in the U.S. Investors, like Plug and Play Tech Centers, sometimes go to these public platforms to seek relevant startups that fit their portfolios. The current design mimics this startup-seeking setting. Second, descriptions of startup founders’ experiences are all extracted from real startup founders’ biographies.

Manipulating Gender and Race. — To indicate the gender and race of the startup founder, Experiment A randomly assigns each hypothetical startup team member a first name highly indicative of gender (male or female) and a last name highly indicative of race (Asian or white). To make such information more salient, all the members in the same startup team are assigned names of the same gender and race. Moreover, Experiment A also includes the founder’s name in the evaluation questions and uses indicative words like “she/her/his/him/he”. Similar to other components, the combination of first names and last names is dynamically implemented by Qualtrics.313131Considering our collaborative incubators and startups have relatively more Asian founders and female founders, the ratio of female and male startup founders are both 50% to maximize the experimental power. A similar ratio is used for Asian founders and white founders. The detailed name selection process and the list of full names are provided in Online Appendix B Table B1.

Manipulating Age — The age of the startup founder is indicated by the graduation year from their college or graduate school rather than being listed directly. If a team has two co-founders, their age falls in the same range, which belongs to either the older group (who graduated before 2005) or the younger group (who graduated after 2005). I assume founders graduate from college at the age of 23,323232It is suspicious to list age directly in a startup’s profile because it is not common practice. Hence, using the graduation year as a proxy achieves more realism. Using 22 gives similar results. However, some investors may assume that founders graduate from graduate school rather than from an undergraduate program at these universities; hence, 23 is used. so the approximated age is calculated by the formula: age graduation year.

Evaluation Questions

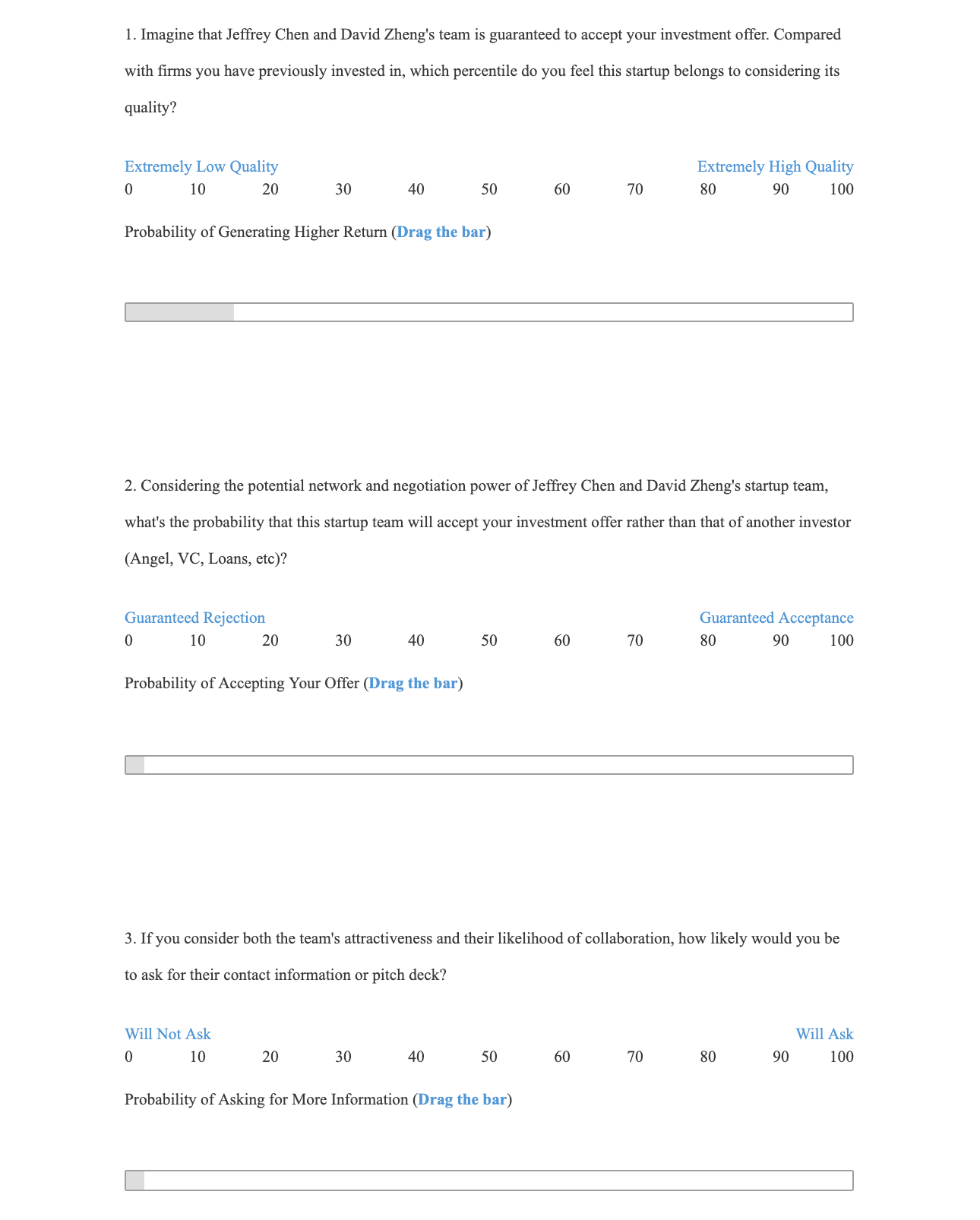

The evaluation questions include three mechanism questions and two decision questions. Considering that most venture capitalists are well-educated and market savvy, I use probability or percentile ranking questions rather than Likert scale questions.333333Using probability and percentile ranking questions has two advantages. First, these questions are more objective compared to the Likert scale. Second, the wide range from 1 to 100 provides richer evaluation results and additional statistical power. Brock and De Haas (2020) also use probability questions to replace Likert Scale questions when they recruit real Turkish bankers to evaluate different loan profiles. This design provides continuous outcome variables, which allows researchers to implement infra-marginal analysis or distributional analysis that explore how investor preferences vary across the distribution of startups’ attractiveness. Screenshots of evaluation questions are provided in Online Appendix B Figure B5, and Figure B6.

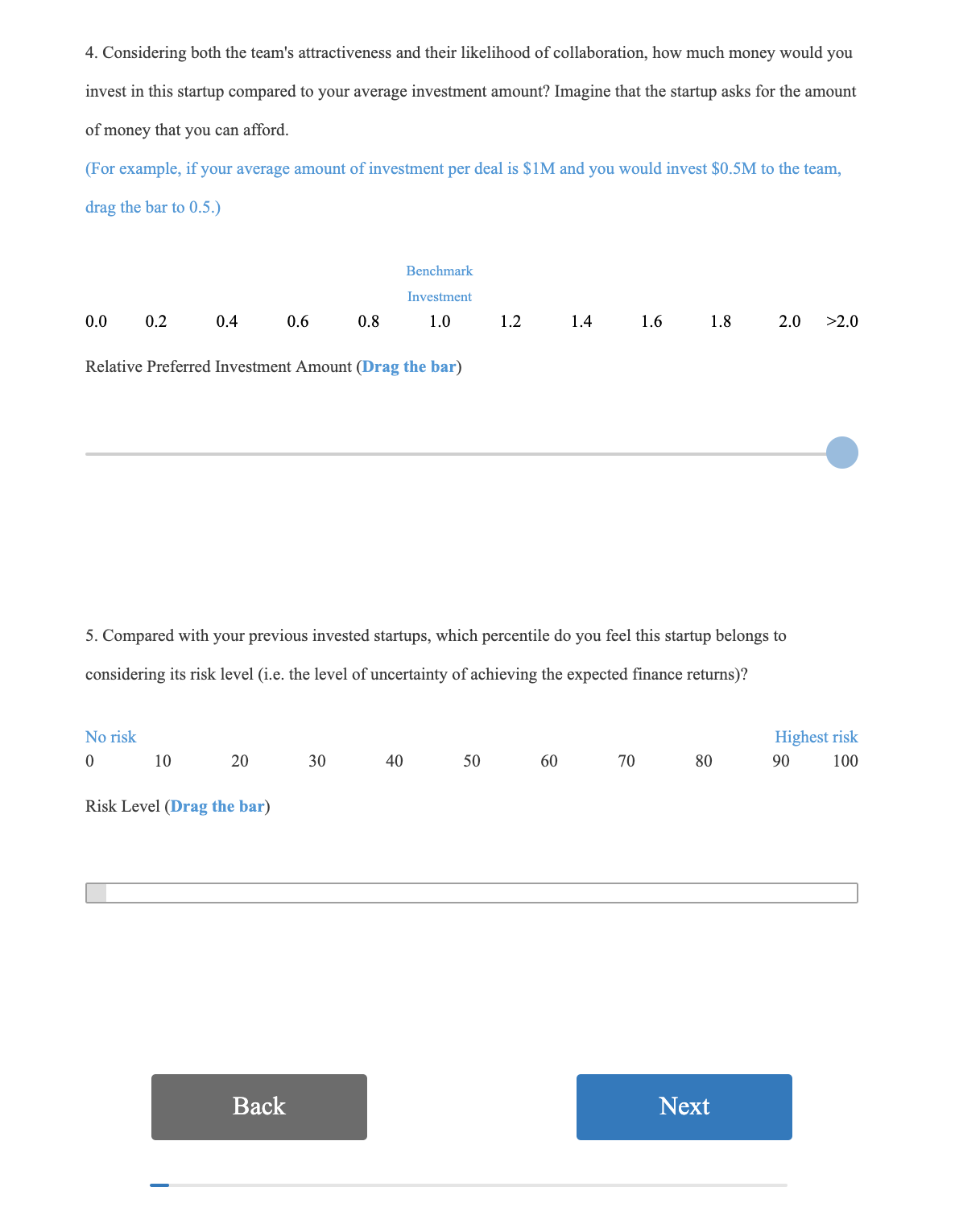

(Belief-based) Mechanism Questions — The mechanism questions are designed to test the following three standard, belief-based discrimination mechanisms. First, being a minority can be indicative of a startup’s future financial returns (i.e., the first moment). To test this mechanism, investors need to evaluate the percentile rank of each startup’s probability of generating higher financial returns compared to the startups they have previously invested in (i.e., “profitability” evaluations ). Second, given that the entrepreneurial financing process is essentially a two-sided matching process, investors also need to evaluate the probability that a startup will accept their investment rather than other investors’ (i.e., “availability” evaluations ). Third, investors may use the founder’s group membership as an indicator of a startup’s risk (i.e., the second moment). Hence, investors also evaluate the risk percentile rank of each startup profile (i.e., “risk” evaluations ). was not in the original design but was added later based on investors’ feedback for the purpose of checking robustness. Therefore, it only applies to a small number of investors receiving the matching incentive.343434 is placed after all the other evaluation questions to minimize its impact on the originally designed questions Due to the small sample size of , risk-related results are not reported.

Decision Questions — The two decision questions are designed to examine both the investor’s contact interest ratings () and intended investment interest ratings (). Specifically, asks for the relative investment magnitude rather than the absolute investment magnitude as different investors have different ranges of targeted investment amounts. In order to accommodate more investors, I have tried to make as standardized as possible.

Background Questions

After the investor evaluates all the profiles, Experiment A also collects standard background information about each participant to determine how representative the sample investors are and analyze potential heterogeneous effects based on predetermined investor characteristics.353535All the background questions are placed after the evaluation section to avoid priming subjects to think about any particular characteristics that the research project aims to test. Such background information includes investors’ preferred industries, stages, special investment philosophies, gender, race, and other standard demographic information.

B.2 Donation Section (Dictator Game)

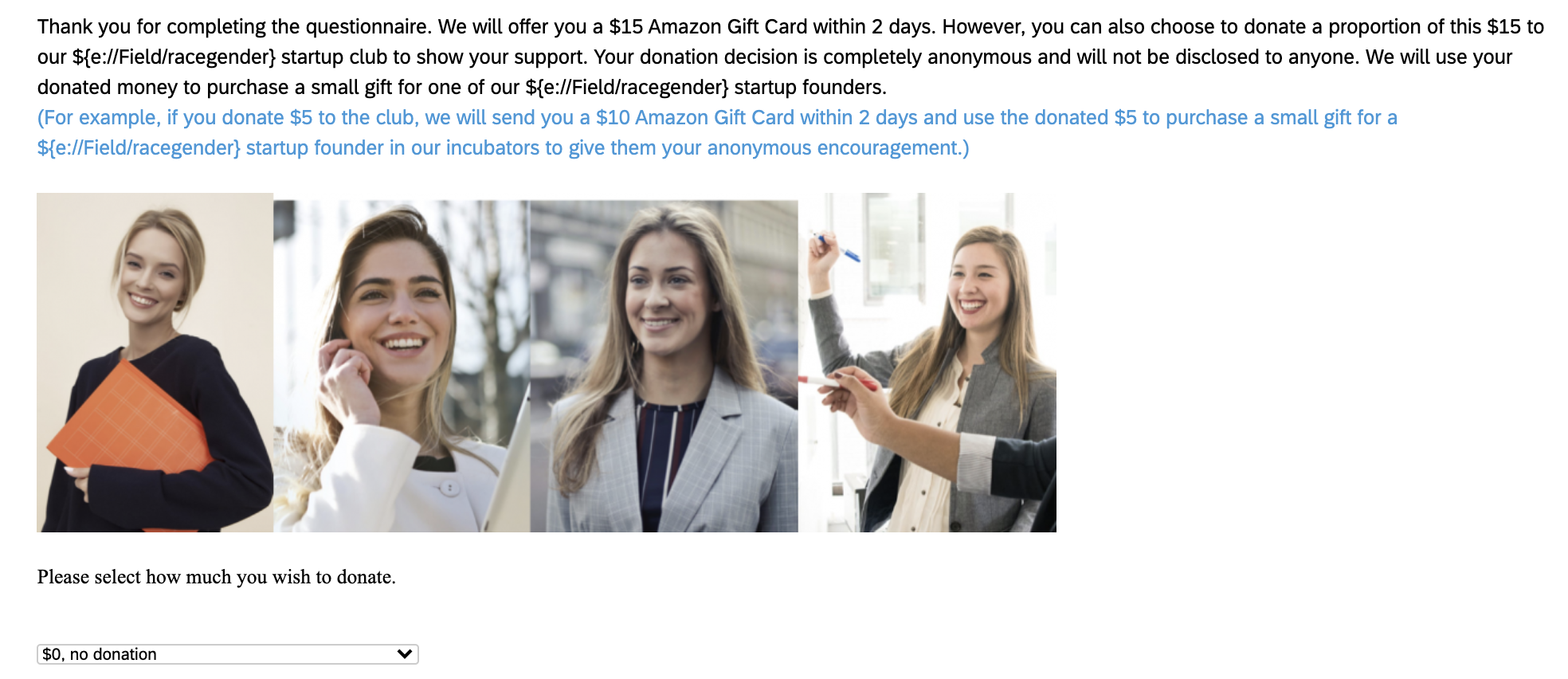

Experiment A also inserts a donation section at the end of the survey tool to investigate whether investors treat minority groups and majority groups differently when providing non-investment support. Investors are informed that they will receive an unexpected $15 Amazon Gift Card to thank them for participating in this experiment.363636To avoid polluting the incentive structure in Experiment A, the compensation with the $15 Amazon Gift Card is mentioned only at the very end of the survey tool rather than in the consent form. However, they can decide whether to donate a portion of the provided $15 to randomly displayed startup founders. For instance, if the investor donates $3, she/he will receive a $12 Amazon Gift Card. The researcher will use the donated money to purchase a small gift for the corresponding type of startup founders in our collaborative incubators and give them anonymous encouragement from investors during the pandemic recession.373737I provide a small gift rather than cash to founders because a small gift is usually more associated with warm encouragement, while giving a small amount of cash can sometimes be considered insulting.

Experiment A orthogonally randomizes the gender and race of displayed startup founders by changing the pictures displayed and the wordings used in the description. The options investors may randomly be provided with include donating to the “Women’s Startup Club” (mainly white female founders), “Asian Women’s Startup Club” (mainly Asian female founders), “Asian Startup Club” (mainly Asian male founders), or just “our Startup Club” (mainly white male founders). To make the information of gender and race more salient, I also add a picture containing four startup founders of the same gender and race so that experimental participants understand what type of founders they are donating to.383838The concern with using pictures in the experiment is that the appearance or other messages delivered by the pictures cannot be fully controlled. To ameliorate this issue, I use four founders’ pictures combined together to send the signal of gender and race. All the pictures are obtained from a public library (i.e., Wikimedia Commons, Freeimages, etc.) with no copyright problems. All individuals in the pictures are smiling and professionally dressed to make sure that they are as much on equal footing as possible. The detailed donation question and an example founder’s picture are provided in Online Appendix B Figure B11.

Limitations and Justifications — The donation game does not capture discrimination in the investment process. Instead, it provides insights into whether discrimination exists when investors provide non-investment support, which is also crucial for startups’ success. Some may be concerned that investors may not care about $15, suggesting that this sub-experiment does not have high enough stakes. According to Camerer and Hogarth (1999), this implies that the donation game underestimates the level of discrimination due to both extra noise and the “presentation effect”, which is a typical limitation of weakly incentivized experiments.

C. Incentive Structure

As a preference elicitation technique, one key point of the IRR experimental design is its incentive structure. The following incentives are designed not only to increase the stakes of Experiment A and impose costs for making inefficient and inaccurate evaluations, but also to bring real value to all the experimental participants.

Matching Incentive — For some randomly selected investors who receive the recruitment email (Version 1), I only provide the following “matching incentive” following Kessler et al. (2019). Basically, after each investor evaluates all the startup profiles, a machine learning algorithm is used to identify matching startups from the collaborative incubators. If the matched startups are also interested in the investor’s investment philosophy, they will contact the investor for a potential collaboration opportunity. The matching algorithm uses all of the investors’ evaluation answers to identify their investment preferences. Therefore, all five evaluation questions are incentivized by this incentive. A description of the algorithm is provided in the consent form.393939This “matching incentive” has the following merits. First, researchers can apply it to any other two-sided matching markets. Second, it can incentivize all the evaluation questions, unlike the monetary incentive. Third, if the designed matching algorithm can improve the matching efficiency, such an incentive can bring real value to both sides of the matching market. Despite the merits mentioned above, implementing this incentive often requires researchers to have certain social resources and connections.

Monetary Incentive — To increase the sample size, I provide both the “matching incentive” and an extra “monetary incentive”, as used by Armona et al. (2019), to the remaining randomly selected investors who received the recruitment email (Version 2). This “monetary incentive” is essentially a lottery in which 2 experimental participants will be randomly selected to receive $500 each plus an extra monetary return closely related to their evaluations of each startup’s quality. The more accurate their evaluations are of each startup’s profitability, the bigger the financial return they will obtain as a lottery winner.404040For example, consider if Peter Smith, one hypothetical experimental participant, is chosen as the lucky draw winner. In his survey, he indicates that on average, male teams are more likely to generate higher financial returns. In that case, the researcher can construct a portfolio containing more real startups with male teams. After one year, based on the financial performance of real startups in Pitchbook, this portfolio containing more startups with male teams generates a 10% return. Thus, Peter Smith receives $500 + $500*10% = $550 as his finalized monetary compensation one year after he participates in the survey. $500*10%=$50 is the “extra monetary return.” The historical return of the VC industry is roughly between -15% and +15%, which means that the range of expected monetary compensation is roughly between $425 and $575. However, this is only used to incentivize the “profitability evaluation question” (i.e., “Q1”). The evaluation results will be determined based on the Pitchbook data published in the 12 months following completion of the recruitment process. I separately informed these two lottery winners that they would receive the award at the end of July 2020. The evaluation algorithm is provided in the consent form (Version 2).414141This “monetary incentive” has both merits and limitations. First, it mimics the real investing process in which investors have a certain amount of principal and need to evaluate different startups accurately to generate maximum return. Second, it does not require many social resources. Third, researchers can apply it to more general situations besides a two-sided matching market. However, the current version can only incentivize the evaluation of startups’ profitability (i.e., ) to avoid distorting participants’ evaluations on other questions. If the collaboration likelihood (i.e., ) is added to the financial return algorithm, then all the participants may claim that the best startups would be willing to collaborate with them even if that is not true. Similarly, if contact interest ratings (i.e., ) and investment interest ratings (i.e., ) are added to the financial return algorithm, participants may be motivated to distort their true evaluations in order to maximize their financial return as both and can be affected by .

Justification — One concern with adding the “monetary incentive” is the possibility of attracting participants who do not value the matching incentive, which results in extra noise. Another concern is that the “monetary incentive” essentially elicits each subject’s judgement of how the market evaluates each startup’s profitability, which might be different from the subject’s own judgement of each startup’s profitability as incentivized by the “matching incentive”.424242Although “monetary incentive” and “matching incentive” elicit two slightly different sources of beliefs in a startup’s profitability, these beliefs are all individual-level investors’ beliefs of a startup’s profitability that help to prove the existence of “statistical discrimination” or belief-driven discrimination. In this experimental setting, these two quality judgements do not differ quantitatively. To address these concerns, I have compared the evaluation results of investors who receive only the “matching incentive” and those who receive both incentives. The comparison results are provided in Online Appendix B Table B6, showing that these two incentive structures do not cause systematically different evaluations. The interaction terms between the incentive structure and a startup’s gender and race are not significant. Moreover, this experiment discovers multiple highly significant startup team and project characteristics that are crucial for investors’ investment interest ratings as shown in Zhang and Weijie (2020). This means that investors understand the incentives and evaluate all the questions carefully.434343Researchers can also separately ask subjects questions that can test their understanding of the incentive (Casaburi and Willis (2018)).

3.2 Experimental Results

I denote an investor ’s evaluation of a startup profile on evaluation question as and estimate the following regression. Formally,

| (1) |

represents any founder’s demographic information, like gender and race. are investor fixed effects that account for different average ratings across investors. Since each type of startup characteristic is randomized orthogonally and independently, the coefficient has a causal interpretation. Standard errors are clustered at the investor level.

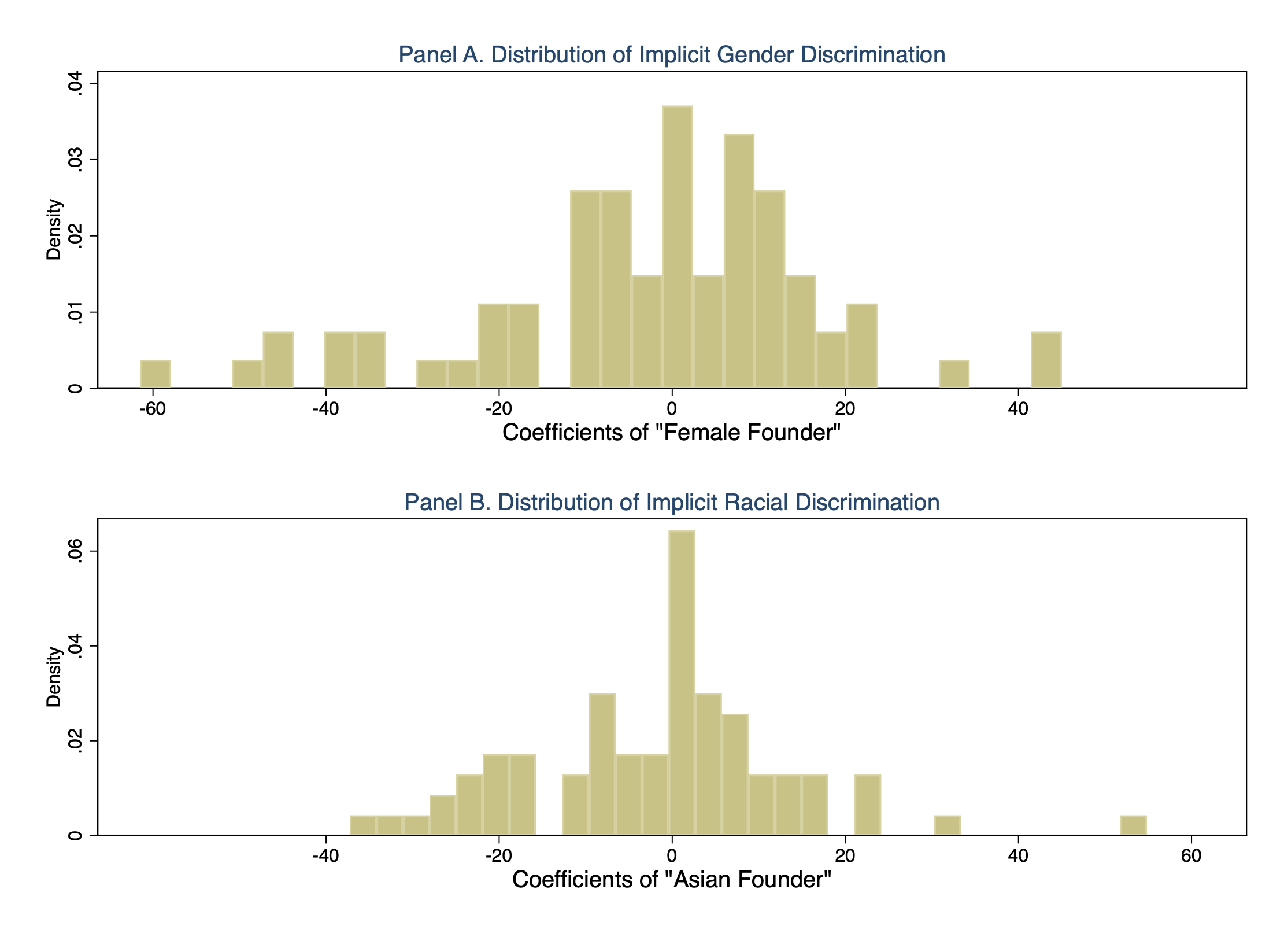

Online Appendix Table B3 reports corresponding regression results testing group-level ATE of a startup founder’s gender (Panel A), race (Panel B), and age (Panel C) using the total 1,216 profile evaluation results. “Female Founder”, “Asian Founder”, and “Older Founder” are indicators that equal one if the startup founder has a female first name, Asian last name, and graduated before 2005, respectively. They are equal to zero, otherwise. The dependent variables are investors’ evaluations of startups’ profitability (), availability (), contact interest ratings (), and investment interest ratings (). After adjusting p-values to account for multiple hypothesis testing, the study does not find any discrimination evidence in aggregate.444444The study also does not find investors spend significantly different amounts of time on evaluating majority founders’ and minority founders’ profiles. This rules out attention discrimination in the profile screening process (see Online Appendix B Table B12).

The lack of aggregate-level significant evidence occurs in almost all papers that use the IRR experimental method to detect socially sensitive preferences (Kessler et al. (2019), Zhang (2021)). This null result may potentially be due to the following reasons. First, investors understand that they are participating in a research project and hence might behave in a more friendly manner to minorities due to the Hawthorne effect. Second, as there are more minorities among recruited investors, sample selection bias might also contribute to the null result. Third, heterogeneous effects and implicit discrimination might exist as shown in Kessler et al. (2019). Fourth, if discrimination mainly exists at the top level, the aggregate-level ATE cannot capture it. All these reasons call for more thorough data analysis. As shown below, the study finds that discrimination against minorities mainly concentrates on top startups and exists in the second half of the study when investors become more fatigued or more familiar with the evaluation process.

A. (IRR Experiment) Discrimination in the Second Half of Study

A.1 (Average Treatment Effect) Implicit Discrimination Against Female Founders.

Given the aggregate-level null result, the study further investigates whether implicit gender and racial discrimination exists. “Implicit discrimination” refers to the attitudes or stereotypes that affect investors’ decisions in an unconscious manner. According to Bertrand et al. (2005b) and Cunningham and de Quidt (2015), implicit discrimination can significantly affect people’s behaviors when the task involves ambiguity, time pressure, evaluating mixed attributes, or causes a higher cognitive load and inattentiveness.

The task of screening startups in the pre-selection stage satisfies these criteria. First, the startup selection process usually involves considerable ambiguity since there are no clear standards for evaluating the attractiveness of each potential deal. Second, many investors need to evaluate a large number of startups quickly before narrowing down their potential investment targets. Considering that the level of fatigue introduced in this experiment is not high, any detected “implicit discrimination” against minorities may play a more important role in the real-world investment process.

Kessler et al. (2019) creates two methods of testing implicit discrimination using the IRR experiment: 1) comparing evaluations of the first half of the profiles and the second half of the profiles within each block; and 2) comparing evaluations of the first half of the study and evaluations of the second half of the study. The logic behind both methods is that when investors become more rushed or fatigued, their implicit preferences are more likely to emerge and affect their judgments. This discrimination due to the “fatigue effect” has been classified as implicit discrimination in the IRR experiment. Since only the second method has been pre-registered for this experiment, results of implicit discrimination in this paper rely on the comparison of evaluations in the first half of the study and those in the second half of the study.454545The pre-registered analysis plan for this experiment (AEARCTR-0004982) is restricted from access by the public, but is available upon request. The method of testing implicit discrimination is pre-registered on Page 5 of “Analysis Plan Version 1.pdf”.

Table 4 displays aggregate-level implicit discrimination results based on a founder’s gender (Panel A) and race (Panel B). It shows whether investors’ ratings of minority founders decline after the inserted short break by using the second method proposed by Kessler et al. (2019). “Second Half of Study” is an indicator variable for profiles shown among the last half of profiles viewed by the investor. In Column (1), the dependent variable is investors’ response time, defined as the number of seconds before each page submission and winsorized at the percentile (59.23 seconds on average). Each regression adds investor fixed effects and clusters standard errors at the investor level.

Results show that female founders receive significantly lower ratings in the second half of the study compared to those in the first half of the study. Column (1) shows that investors indeed spent 27 seconds fewer evaluating each profile after the inserted break, suggesting the potential existence of more fatigue and rushed evaluations at the end of the study. In Panel A Columns (2)-(5), all the interaction terms of “Female Founder” and “Second Half of Study” are negative. Specifically, the p-value of the interaction term in Column (5) is 0.02 and its Holm-Bonferroni p-value is 0.06 after accounting for multiple hypothesis testing. This suggests that investors’ investment interest ratings (i.e., ) of women-led startups decline by 10.3% compared with similar men-led startups when entering the second half of the study. The marginally significant interaction term in Column (1) suggests that statistical discrimination might play a role as investors’ profitability ratings (i.e., ) decline by 4.26%. Although the interaction terms of “Asian Founder” and “Second Half of Study” are not significant at the aggregate level, Section A.2 later shows that significant belief-driven discrimination against Asians with economically large magnitude does exist at the top level in the second half of the study.

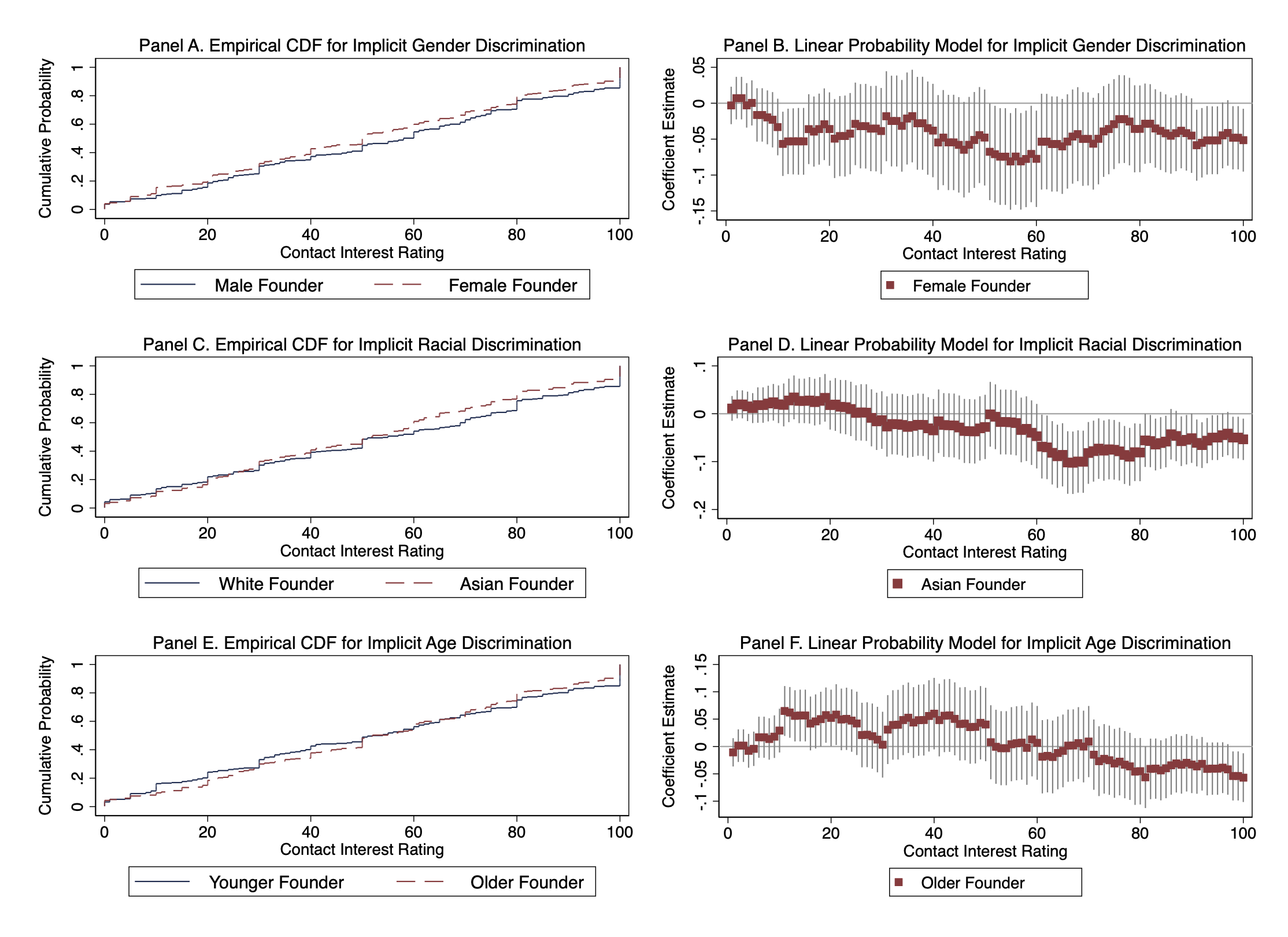

To further consolidate the result of implicit gender discrimination in Table 4, Figure 1 and Figure 2 demonstrate the time-path of investors’ response time and how investors’ evaluations vary across profiles as the study progresses to the end, respectively. In Figure 1, there is a clear pattern that investors’ response time gradually declines as the evaluation task progresses, confirming that attention is costly Bartoš et al. (2016). Importantly, response time does not temporarily increase after the break and becomes smallest at the end of the study.

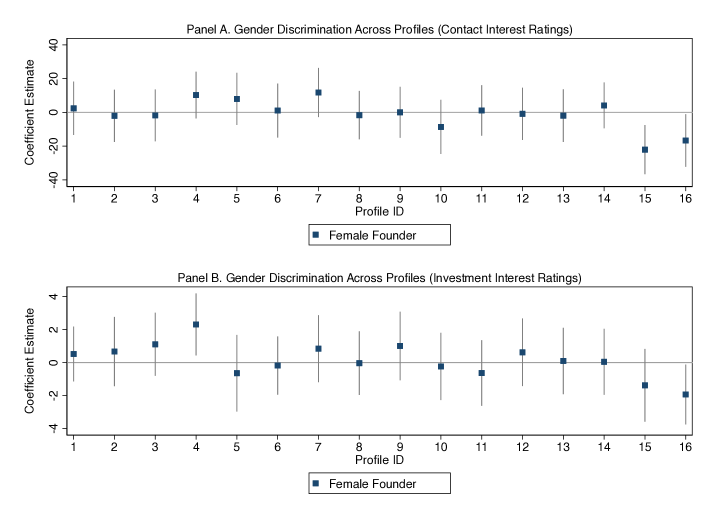

Figure 2 shows that investors’ gender discrimination based on contact interest ratings (i.e., ) and investment interest ratings (i.e., ) mainly concentrate at the end of the study in terms of both significance and magnitude. The x-axis is the profile ID and the y-axis reports the coefficient of “Female Founder” and the 95% confidence interval using the following regression for each profile ID . Panels A and B focus on and respectively. In Panel A, the coefficient of “Female Founder” is -22.10% for Profile 15 with p-value equal to 0.004, and becomes -16.67% for Profile 16, the final profile evaluated, with p-value equal to 0.04. This suggests that women-led startups are roughly 17% to 22% less likely to be contacted by investors at the end of the study. Similarly, in Panel B, the coefficient of “Female Founder” is -1.94 for Profile 16, which is statistically significant at the 5% level. This shows that women-led startups receive 19.4% less investment compared to similar men-led startups if the profile is displayed at the end of the evaluation section. Both the significance and economic magnitude of the discovered gender discrimination are strong when the evaluation task is close to the end, which is consistent with the implicit discrimination hypothesis (i.e., the “fatigue effect”). To further pin down the implicit discrimination channel, I will rule out other alternative interpretations below.

Rule Out Learning Effect One alternative interpretation of the findings in Table 4 and Figure 2 is a “learning effect”. This indicates a worse situation where investors consciously discriminate against women more when they are more familiar with the evaluation task. If the “learning effect” dominates, investors’ evaluations of other startup characteristics should be more accurate and less noisy as the IRR experiment progresses to the end. If the “fatigue effect” dominates, investors’ evaluations should demonstrate more noise at the end. Online Appendix Figure 4 demonstrates how investors evaluate founders’ educational backgrounds and startups’ traction across different profiles.464646These two characteristics have been well documented to possibly affect investors’ decisions in the entrepreneurial finance literature (Bernstein et al. (2017)), Kaplan et al. (2009). For the impact of other startup characteristics on investors’ investment, please read Zhang and Weijie (2020). It shows that investors’ evaluations of these non-sensitive startup characteristics have a larger variance for Profiles 15 and 16, which rules out the “learning effect” and further supports the “fatigue effect”. Moreover, after removing the first few evaluations of each investor, the “fatigue effect” still holds, indicating that “learning” may not be the main reason for the observed results.

Rule Out “Balance-the-Sample” Hypothesis Another alternative interpretation for the discovered “fatigue effect” is that investors may expect the overall population of entrepreneurs to follow the distribution in the real world, say “80-20”, rather than “50-50” as used in this experiment. Thus, near the end of the evaluation process, investors may be tempted to skew the sample in the direction they expect the population to be, leading to biased experimental results.474747Special thanks go to Peter DeMarzo who raised this brilliant point and suggested the corresponding testing method. “50-50” has been chosen to maximize the experimental power. However, using this ratio may suggest to investors that the experiment’s purpose is to test discrimination, making investors behave more friendly to minority groups, especially in the second half of the study where the balanced ratio is more obvious. To test this hypothesis, I have checked whether investors’ evaluation results are influenced by the “mixed profiles” they have already evaluated in the first half of the study. However, as shown in Online Appendix B Table B7, investors who evaluated more minority founders in the first half of the experiment were not systematically tougher on minority groups in the second half of the experiment. Moreover, the “50-50” ratio is also used for the randomization of founders’ educational backgrounds and the startups’ traction to maximize experimental power. If the “Balance-the-Sample” hypothesis dominates, similar “fatigue effect” should also exist for these two startup characteristics, which is not supported by Figure 4.

It should be noted that the IRR experiment does not directly observe whether investors knowingly discriminate against female founders. A rigorous interpretation of results above is that as the experiment goes on, investors get tired of the evaluation task and give lower ratings to women-led startups compared to similar men-led startups. For simplification purposes, discrimination that is associated with such “fatigue effect” or occurs in the second half of the IRR experiment is called “implicit discrimination” in this paper. Considering that the cognitive workload of evaluating these profiles is not large, the discovered “implicit discrimination” may potentially play an important role in an intensive pre-screening process in the VC industry.

A.2 (Distributional Effect) Implicit Discrimination Concentrates on Top Startups.

Several fundamental theory papers in discrimination have predicted an equilibrium situation in which evaluators discriminate against minority groups at relatively high rating scores and favor minority groups at very low rating scores (Phelps (1972), Aigner and Cain (1977), Lundberg and Startz (1983), Morgan and Várdy (2009)). The model in Morgan and Várdy (2009) also predicts that when evaluators are selective, this leads to minority underrepresentation in the workplace. However, when evaluators are sufficiently unselective, this leads to overrepresentation of minorities. These discrimination theories imply the existence of a distributional effect of discrimination across the spectrum of startups’ attractiveness. Although this theoretical “discrimination reversion” phenomenon has not been empirically tested before, it may potentially reconcile the contradictory results in empirical studies that test discrimination in the entrepreneurial financing setting.

Conflicting results in the literature have been generated by Ewens and Townsend (2020) and a classical correspondence test in Gornall and Strebulaev (2020). Both papers essentially study investors’ intentions to contact startups in the pre-screening stage. Compared to profitability ratings (i.e., ) that only measure one dimension of startups, contact interest ratings (i.e., ) provide more comprehensive evaluations of startups’ quality. This summary measure of all information acquired by evaluators is what test scores or rating scores mean in discrimination theory papers (Lundberg and Startz (1983)). Therefore, when testing the distributional effect of discrimination, contact interest ratings (i.e., ) are the most appropriate measures for the purpose of reconciling the literature.484848Online Appendix Table B8 and B9 also report quantile regression results using .

(Gender) Table 5 investigates whether implicit gender discrimination varies across startups’ received contact interest ratings (i.e., ) using quantile regressions. The sample includes profile evaluations in the second half of the IRR experiment. Motivated by the literature discussing gender issues in science or STEM fields (Carrell et al. (2010), Goldin (2014), and Kessler et al. (2019)) and the crucial importance of the tech sector in the entrepreneurial community (see Table 2), Panel A focuses on implicit gender discrimination among investors in the tech sector. Panel B uses all recruited investors’ evaluation results. In each of Columns [1]–[9], the dependent variable is the th percentile () of the distribution of startups’ received contact interest ratings (i.e., ). In Column [10], the dependent variable is the average investors’ contact interest ratings. Standard errors in parentheses are clustered at the investor level.

Results show that implicit gender discrimination against female founders is most prevalent for attractive startups. Panel A finds that in the tech sector, compared to similar men-led startups, investors are 10% less likely to contact women-led startups whose contact interest ratings are in the 90th and 60th quantile of the attractiveness distribution. The negative coefficients of “Female Founder” are statistically significant at the 5% level. Panel B confirms this phenomenon by using the full sample. For startups whose contact interest ratings are at the 50th, 60th, and 80th percentile position, women-led startups are 10%, 8%, and 7% less likely to be contacted by investors, respectively. Results are statistically significant at the 5% level. However, in both Panels A and B, this gender discrimination disappears for women-led startups whose contact interest ratings are below the 40th percentile of the attractiveness distribution. Experiment A might not have enough statistical power to test investors’ preferences towards women-led startups at very low rating scores, especially if the magnitude of this gender preference is small. Hence, this study uses Experiment B to capture the fundraising situation of struggling startups as shown in Section 4.

(Race) Table 6 tests similar distributional effect of implicit racial discrimination in the second half of the study using quantile regressions. Similar to implicit gender discrimination, discrimination against Asian founders is more salient among highly-rated startups. As shown in Panel A, investors in the tech sector are 9% less likely to approach Asian founders compared to similar white founders if their startups are rated at the 90th percentile. Panel B finds that investors in the full sample give 10% lower contact interest ratings to Asian founders whose startups are rated at the 80th percentile. This result is statistically significant at the 1% level. However, in both Panels A and B, the coefficients of “Asian Founder” become slightly positive for startups rated below the 20th percentile. Although this result is not statistically significant in the IRR experiment, it suggests the potential existence of weak preference towards Asian founders of startups with very low rating scores if the sample size is large enough (see Experiment B).494949Some might have a concern that the distributional effect of implicit gender and racial discrimination is driven by investors who have extreme preferences. Online Appendix Table B4 shows that results are robust after removing evaluations of investors with extreme preferences.

(Age) Although agism is not the main question of this paper, Online Appendix Table B5 finds that a “discrimination reversion” phenomenon also exists when testing agism in the second half of the study. Panel A finds that tech investors are 8% less likely to contact older founders compared to similar younger founders whose startups are rated at the 90th percentile. The coefficient of “Older Founder” is statistically significant at the 10% level. This is consistent with a large amount of anecdotal evidence and surveys that indicate wide-spread ageism during VCs’ investment process, especially in the tech sector.505050See Forbes “The Biggest Bias In Tech That No One Talks About” (April 10th, 2019) by Maren Thomas Bannon, an early-stage technology venture capitalist. However, for startups rated at the 20th and 40th percentile, investors are 10% more likely to approach older founders. Results are statistically significant at the 10% and 5% level, respectively. Panel B finds that the coefficient of “Older Founder” is -6% for startups rated at the 80th percentile and +7% for startups rated at the 40th percentile, which are both statistically significant at the 10% level.

Quantile regression results above show that the magnitude and direction of evaluators’ socially sensitive preferences, such as gender, race, and age discrimination, can vary across the distribution of candidates’ rating scores. This provides one possible explanation for the contradictory results in the literature. On the one hand, papers exploiting regression-based methods often use observational data that record relatively mature and promising startups.515151Standard databases often record startups that have successfully raised external funding. Also, startups whose information is posted on large fundraising platforms are relatively more mature and well-known than startups whose information is not recorded by these platforms. Hence, they mainly capture the middle and right part of the startup attractiveness distribution where significant implicit discrimination exists. On the other hand, the correspondence test often focuses on the cold call pitch email setting. According to Crunchbase, “Cold emails have a bad reputation in venture capital … and can come off as begging”.525252See “The Art of a Cold Email to a Venture Capitalist” posted on Crunchbase, July 17, 2020. Hence, high-rated startups generally do not choose this fundraising method and the correspondence test mainly captures the fundraising situations of struggling startups. Since different papers reveal investors’ preferences at different positions on the startup distribution, the direction and magnitude of their results might be different. Importantly, results of correspondence tests might not be generalizable to highly-rated startups’ fundraising situations.

(Investment Interest Ratings) There are several key differences between investors’ investment interest ratings (i.e., “Q4”) and contact interest ratings (i.e., “Q3”). First, contact interest ratings mainly capture whether a startup can raise funding from VC investors (i.e., extensive margin) while investment interest ratings mainly reflect how much funding an investor will invest in each startup (i.e., intensive margin). Extant literature and conflicting results mainly focus on the former subject, but scarce evidence exists for the latter. Second, investment interest ratings (i.e., “Q4”) are noisier than contact interest ratings (i.e., “Q3”) in the IRR experiment because this study does not provide any soft information about the startup founder, which is also crucial to investment decisions. Third, the investment intention is mainly affected by beliefs rather than tastes as suggested by Zhang and Weijie (2020). Therefore, the distributional effect measured by “Q4” is not used to reconcile the literature. Instead, it tests whether discrimination also exists along the intensive margin.535353The “intensive margin” here refers to whether investors provide a smaller amount of funding to women-led startups and Asian-led startups.

Table 7 shows the distributional effect of a startup founder’s gender and race on investors’ investment interest ratings in the second half of the study. Panels A and B focus on gender and racial discrimination, respectively. Panel A shows that investors provide 10% less funding to women-led startups compared to similar men-led startups if these startups are rated between the 30th and 60th percentile based on . Hence, implicit gender discrimination along the intensive margin is more significant among mid-level startups. However, Panel B shows that significant implicit racial discrimination still concentrates among top-level startups. For startups rated at the 90th percentile, Asian-led startups receive 20% less funding compared to similar White-led startups. This result is statistically significant at the 1% level. However, for startups rated below the 20th percentile, this racial discrimination disappears. The negative coefficients of “Female Founder” and “Asian Founder” in Panels A and B indicate that minority groups receive double the penalty along both the extensive margin (see Table 5 and Table 6) and the intensive margin (see Table 7).

A.3 (Pro-cyclical Discrimination) Implicit Discrimination Varies with Market Conditions.

Similar to Kessler et al. (2019), this subsection investigates how investors’ implicit discrimination varies in different market conditions as measured by investors’ internal thresholds. When the capital supply is abundant (limited) in the market during an economic boom (bust), investors are less (more) selective when investing in startups, and their internal thresholds become lower (higher). Figure 5 illustrates these dynamic changes in investors’ gender, racial, and age discrimination based on investors’ contact interest ratings. The sample includes all recruited investors’ evaluations in the second half of the IRR experiment. Panels A, C, and E provide the empirical cumulative density function (CDF) for a founder’s gender, race, and age across investors’ contact interest ratings, respectively. Panels B, D, and F provide the corresponding OLS coefficient estimates and their 90% confidence intervals for a founder’s gender, race, and age across investors’ contact interest ratings, respectively.545454Regressions used in Panels B, D, and F are the same as those used in Kessler et al. (2019): for each selected internal threshold , where if and if . The confidence intervals are calculated using robust standard errors. However, results are similar when clustering standard errors at the investor level.

Figure 5 shows that both the direction and magnitude of investors’ implicit gender, racial, and age discrimination can vary across investors’ internal thresholds. Panel A shows that the CDF for a female founder is generally to the left of the CDF for a male founder, which means that the CDF for a male founder first-order stochastically dominates the CDF for a female founder in most situations. Panel B shows that the coefficients of “Female Founder” are negative for most selected investors’ internal thresholds with the largest magnitude existing when the internal thresholds are around 60% of contact interest ratings. Results in Panels A and B suggest the existence of widespread implicit gender discrimination against female founders in most market conditions. Unless investors contact almost all startups on the market, it is generally more difficult for female founders to approach investors compared to similar male founders.

Panels C and D show that implicit racial discrimination mainly exists when investors’ internal thresholds are high. In Panel C, when contact interest ratings are above 30%, the CDF for an Asian founder is to the left compared with the CDF for a white founder. The opposite is seen when contact interest ratings are below 30%. Similarly, in Panel D, the coefficients of “Asian Founder” gradually become negative as investors’ internal thresholds increase. When internal thresholds are above 60% of contact interest ratings, these negative coefficients become statistically significant. This indicates that Asian founders face more difficulties in raising funding when the capital supply is low.

Panels E and F display a more salient “discrimination reversion” phenomenon of agism across investors’ internal thresholds. In Panel E, the CDF for an older founder gradually moves to the left compared with the CDF for a younger founder as investors become more selective in funding startups. In Panel F, the coefficients of “Older Founder” are significantly positive when contact interest ratings are around 20% and are significantly negative when contact interest ratings are close to 100%. Results indicate that implicit agism exists when investors only consider top startups.

These dynamic changes of implicit discrimination in various market conditions confirm the theoretical prediction of “pro-cyclical discrimination” in Morgan and Várdy (2009). Results are also fundamentally consistent with the distributional effect documented in the previous subsection. Both subsections show that implicit gender, racial, and age discrimination mainly exist when investors focus on top startups. However, when investors also consider startups with relatively low rating scores, discrimination against minority groups becomes smaller and might even reverse although the reversion is not statistically significant for gender and racial discrimination due to the small sample size of Experiment A.

A.4 Decision-based Heterogeneous Effect Estimator and Polarization of Discrimination Attitudes

In the real world, investors’ preferences towards a founder’s gender, race, and age are heterogeneous. Some favor minority founders, while some favor majority founders. In a divided society, different groups potentially make opposing decisions based on different motivations. For example, “pro-minority” investors’ decisions can be driven by taste if they simply want to support minorities rather than maximize financial returns. However, “anti-minority” investors’ investment decisions can be driven by belief if they perceive minority founders’ startups to be less profitable. Understanding the separate driving forces of these two different groups’ decisions has important policy implications. To test what separates investors and how divided the investment community is, this paper develops a consistent, “decision-based” heterogeneous effect estimator using the “leave-one-out” technique.