Naive Analytics Equilibrium (Draft)

Abstract

We study interactions with uncertainty about demand sensitivity.

In our solution concept (1) firms choose seemingly-optimal strategies

given the level of sophistication of their data analytics, and (2)

the levels of sophistication form best responses to one another. Under

the ensuing equilibrium firms underestimate price elasticities and

overestimate advertising effectiveness, as observed empirically. The

misestimates cause firms to set prices too high and to over-advertise.

In games with strategic complements (substitutes), profits Pareto

dominate (are dominated by) those of the Nash equilibrium. Applying

the model to team production games explains the prevalence of overconfidence

among entrepreneurs and salespeople.

Keywords: Advertising, pricing, data analytics, strategic

distortion, strategic complements, indirect evolutionary approach.

JEL Classification: C73, D43, M37.

1 Introduction

Researchers often assume that better measurement and accurate estimations of the sensitivity of demand allow firms to improve their advertising and pricing decisions. Arriving at such accurate estimations requires careful experimental techniques or sophisticated econometric methods that correct for the endogeneity of decision variables in the empirically observed data (see, e.g., Blake et al. 2015; Shapiro et al. 2019; Gordon et al. 2019; Sinkinson and Starc 2019 who estimate advertising effectiveness, and Berry, 1994; Nevo, 2001; Alé-Chilet and Atal, 2020 who estimate price elasticities).

Despite the emphasis on precision and unbiasedness by researchers, many companies have been slow to adopt these techniques (Rao and Simonov, 2019), often questioning the benefit of causal inference and precise measurement. This reluctance to measure effectiveness precisely is often attributed to implementation difficulties, lack of knowledge and cognitive limitations by decision makers, or moral hazard (Berman, 2018; Frederik and Martijn, 2019). Empirically, we often observe that firm advertising budget allocations are consistent with over-estimation of advertising effectiveness (see, e.g., Blake et al., 2015; Lewis and Rao, 2015; Golden and Horton, 2020), while pricing decisions are consistent with under-estimation of price elasticities (see, e.g., Besanko et al. 1998; Chintagunta et al. 2005; Villas-Boas and Winer 1999; see also Hansen et al., 2020 who demonstrate that common AI pricing techniques induce “too-high” prices ).

In this paper we challenge the assumption that better estimates are always beneficial for firms. Our results show that in many cases firms are better off with biased, less precise, measurements because of strategic considerations in oligopolistic markets. In equilibrium firms will converge to biased measurements because their profits are maximized when they act on these measurements. Moreover, the directions of the biases, as predicted in our model, fit the empirically observed behavior of firms well.

Highlights of the Model

We present a model where the payoffs of competing players (firms) each depend on her actions and on her demand, where the demand depends on the actions of all players. The players do not know the demand function, but can select actions and observe the realized demand. The game has two stages. In stage 1 each player hires a (possibly biased) analyst to estimate the sensitivity of demand. An analyst may under- or over-estimate the sensitivity of demand. In stage 2 each player chooses an action taking the estimate as the true value.

Our solution concept, called a Naive Analytics Equilibrium, is a profile of analysts’ biases and a profile of actions, such that (1) each action is a perceived best-reply to the opponents’ actions, given the biased estimation, and (2) each bias is a best-reply to the opponents’ biases in the sense that if a player deviates to another bias this leads to a new second-stage equilibrium, in which the deviator’s (real) profit is weakly lower than the original equilibrium payoff. The first-stage best-replying is interpreted as the result of a gradual process in which firms hire and fire analysts from a heterogeneous pool, and each firm is more likely to fire its analyst if its profit is low.

Summary of Results

Our model is general enough to capture price competition with differentiated goods (where the goods can be either substitutes or complements), as well as advertising competition (where the advertising budget of one firm has externalities on the competitors’ demand). Our results show that firms hire biased analysts in any naive analytics equilibrium, and that the direction of the bias is consistent with the empirically observed behavior of firms: in price competition firms hire analysts that under-estimate price elasticities, and in advertising competition firms hire analysts who over-estimate the effectiveness of advertising.111Our general result on the direction of the bias is related to Heifetz et al.’s (2007a) result in the setup of evolution of subjective preferences. We discuss this relation in Remark 2 in Section 4.3.

We also show that there is a Pareto-domination relation between the naive analytics equilibrium and the Nash equilibrium (of the game without biases), where its direction depends on the type of strategic complementarity. In a game with strategic complements (i.e., price competition with differentiated goods) the naive analytics equilibrium Pareto dominates the Nash equilibrium, while the opposite holds in a game with strategic substitutes (i.e., advertising competition with negative externalities). The intuition is that in a game with strategic complements (resp., substitutes), each player hires a naive analyst that induces a biased best reply in the direction that benefits (resp., harms) the opponents. This is so because these biases have a strategic advantage of inducing the opponents to change their strategies in the same (resp., opposite) direction, which is beneficial to the player.

Next, we analyze a standard functional form in each type of competition, and we explicitly characterize the unique naive analytics equilibrium in price competitions and in advertising competitions. We also present implications for market structure analysis when firms compete in prices in Section 6. Finally, we demonstrate that our model can be applied in more general settings. Specifically, in Section 5.4 we apply the model to a game of team production with strategic complementarity (see, e.g., Holmstrom, 1982; Cooper and John, 1988). We present two testable predictions in this setup: (1) players are overconfident in the sense of overestimating their ability to contribute to the team’s output, and (2) players contribute more than in the (unbiased) Nash equilibrium. These predictions are consistent with the observable behavior of entrepreneurs and salespeople, who often exhibit overconfidence.

Related Literature and Contribution

From a theoretical aspect, our methodology of studying a two-stage auxiliary game where each firm is first endowed with a biased analyst and then chooses her pricing/advertising level given results of the analysis is closely related to the literature on delegation (e.g., Fershtman and Judd, 1987; Fershtman and Kalai, 1997; Dufwenberg and Güth, 1999; Fershtman and Gneezy, 2001)222See also the related literature on the “indirect evolutionary approach” (e.g., Güth and Yaari, 1992; Heifetz and Segev, 2004; Dekel et al., 2007; Heifetz et al., 2007b; Herold and Kuzmics, 2009; Heller and Winter, 2020).. The delegation literature shows that in price competition, firm owners would design incentives for managers that encourage the managers to maximize profits as if the marginal costs are higher than their true value (see, in particular, Fershtman and Judd, 1987, p. 938).

Our model contributes to this literature but also differs from it in a few important aspects. First, in our setup the incentives of all agents are aligned and are based solely on the firm’s profit. A deviation of the firm from profit-maximizing behavior is due to (non-intentional) naive analytics, rather than due to explicitly distorting the compensation of the firm’s manager. Our novel mechanism is qualitatively different (as it relies on biased estimations rather than different incentives), and it induces testable predictions and policy implications which are different than those induced by delegation (as further discussed in Remark 1). Second an important merit of our model is its generalizability to a wide variety of phenomena and its applicability to wide class of games. The concept of biased estimation of sensitivity of demand can be applied in many seemingly-unrelated setups (e.g., price competition, advertising competition, and team production), while yielding sharp results about the direction of the observed biases as well as their magnitudes.

Our research is also related to solution concepts that represent agents with misconceptions (e.g., conjectural equilibrium (Battigalli and Guaitoli, 1997; Esponda, 2013), self-confirming equilibrium (Fudenberg and Levine, 1993), analogy-based expectation equilibrium (Jehiel, 2005), cursed equilibrium (Eyster and Rabin, 2005; Antler and Bachi, 2019), coarse reasoning and categorization (Azrieli, 2009, 2010; Steiner and Stewart, 2015; Heller and Winter, 2016), Berk-Nash equilibrium (Esponda and Pouzo, 2016), rational inattention (Steiner et al., 2017), causal misconceptions (Spiegler, 2017, 2019), and noisy belief equilibrium (Friedman, 2018). These equilibrium notions have been helpful in understanding strategic behavior in various setups, and yet they pose a conceptual challenge: why do players not eventually learn to correct their misconceptions? Much of the literature presenting such models points to cognitive limitations as the source of this rigidity. Our model and analysis offer an additional perspective to this issue by suggesting that misperceptions, such as naive analytics, may yield a strategic advantage and are likely to emerge in equilibrium. In this sense our approach can be viewed as providing a tool to explain why some misconceptions persist while others do not.

Structure

Section 2 presents a motivating example. In Section 3 we describe our model and solution concept. Our main results are presented in Section 4. Section 5 analyzes three applications: price competition, advertising competition, and team-production game. Section 6 demonstrates the implications of our model on analysis of market structures in oligopolies. The main text contains proof sketches and formal proofs are relegated to the appendix.

2 Motivating Example

Consider two firms each selling a product with price . The products are substitute goods. The demand of firm at day is given by:

where denotes the other firm. That is, the expected demand follows Bertrand competition with differentiated goods, and the daily demand of each firm has a random i.i.d demand shock, with value either or with equal probability. We assume that the marginal costs are zero, which implies that the profit of each firm is given by its revenue .

The firm managers do not know their demand functions, and they hire analysts to estimate the sensitivity of demand to price, in order to find the optimal price. The analyst at each firm asks the firm’s employees to experiment for a couple of weeks with offering a discount of in some of the days, and uses the average change in demand between days with and without the discount to estimate the elasticity of demand.

Importantly, the firm’s employees do not choose the days with discounts uniformly. The employees observe in each morning a signal that reveals the demand shock (say, the daily weather), and they implement discounts on days of low demand, possibly due to the employees having more free time in these days to deal with posting the discounted price. Setting discounts in this way creates price endogeneity through a correlation between prices and demand shocks .

There are two types of analysts: naive and sophisticated. A naive analyst does not monitor in which days the employees choose to give a discount, and implicitly assumes in his econometric analysis that the environment is the same in the days with discounts as in those without discounts. In contrast, sophisticated analysts either monitor the discount decisions to enforce a uniform distribution of discounts, or correct the correlation between the weather and discounts in their econometric analysis (e.g., by controlling for the weather).

A sophisticated analyst correctly estimates the mean change in demand

and thus he accurately estimates the elasticity of demand

By contrast, a naive analyst underestimates the mean change in demand to be:

and thus underestimates the elasticity of demand to be

where we denote .

Assume, for example, that and are such that (which is the optimal level of naivete as analyzed in Section 5.2). If each firm adjusts prices according to the estimated elasticity (i.e., slightly increasing the price if the estimated elasticity is more than 1, and slightly decreasing the price if less than 1), then the prices converge to a unique equilibrium in which the estimated elasticity of each firm is equal to one. Table 1 presents the prices, demands, and profits as a function of the type of analyst hired by each firm (the calculations are a special case of the analysis of Section 5.2).

| Prices | ||

|---|---|---|

| \ | 1 | 0.6 |

| 1 | 17, 17 | 19, 22 |

| 0.6 | 22, 19 | 25,25 |

| Demands | ||

|---|---|---|

| \ | 1 | 0.6 |

| 1 | 17, 17 | 19, 13 |

| 0.6 | 13, 19 | 15,15 |

| Profits | ||

|---|---|---|

| \ | 1 | 0.6 |

| 1 | 277, 277 | 351, 287 |

| 0.6 | 287, 351 | 375, 375 |

Observe that each firm’s profit increases when the firm hires a naive analyst, and decreases when it hires a sophisticated analyst, regardless of the type of analyst hired by the competing firm. The intuition is that a naive analyst induces a firm to underestimate the elasticity of demand, and as a result, to raise prices. This has a beneficial indirect strategic effect of inducing the competitor to increase prices as well. It turns out that the positive indirect effect outweighs the negative direct effect. Thus, if firms occasionally replace their analysts based on their annual profits (i.e., they are more likely to fire an analyst the lower the profit is), then the firms are likely to converge to both hiring naive analysts. This would induce both firms to choose higher prices and have higher profits relative to the Nash equilibrium prices arising with sophisticated analysts.

Our formal results show that these insights hold in a general model. Specifically, we show that in a large class of strategic interactions (incorporating both price competition and advertising competition, as well as both strategic complements and strategic substitutes) players (i.e., firms) choose to hire naive analysts. These naive analysts underestimate elasticity of demand in price competition, while they overestimate the effectiveness of advertising in advertising competition. Finally, we show that the equilibrium induced by naive analysts Pareto dominates the Nash equilibrium with sophisticated analysts in a game with strategic complements, while it is Pareto dominated by the Nash equilibrium in a game with strategic substitutes.

3 Model and Solution Concept

We introduce an analytics game in which competing firms hire analysts to estimate the sensitivity of demand, which is then used to determine the strategic choices of the firm. Next we present our solution concept of a naive analytics equilibrium.

3.1 Underlying Game

A naive-analytics game is a two stage game in which each of players (firms) hires an analyst who estimates the sensitivity of demand in the first stage (with a bias from a set of feasible biases , which corresponds to biased estimation functions in , as described in Section 3.2) and then makes a strategic choice that affects demand in the second stage. We first describe the structure of the second stage, which we call the underlying game and denote by . In the underlying game each firm makes a strategic choice that affects the demands and the profits of all firms, where is a (possibly unbounded) interval of feasible choices of firm . The interpretation of depends on the application, e.g.,: (1) it is equal to the price set by the firm in the motivating example, and (2) it is equal to the advertising budget in the application of Section 5.3.

We define the following notation: is the Cartesian product of these intervals. (resp., denotes the interior of (Resp., ). denotes all firms except firm and denotes all firms except and . In two-player games denotes the opponent of firm . denotes the strategy profile in which player plays strategy , while all other players play according to the profile (and we apply a similar notation for ). Finally, denotes the demand of firm .

The (true) payoff, or profit, of each firm , denoted by , depends on the firm’s demand and its strategic choice . We assume that the demand functions and payoff functions of all firms are continuously twice differentiable in all parameters in .

A necessary condition for a strategy to be a best reply to the opponents’ strategy profile is that it satisfies the following first-order condition:

| (3.1) |

Strategy is a local best reply to an opponents’ profile , if there is an open interval around such that for each in this interval. A sufficient condition for a strategy satisfying the FOC (3.1) to be a local best reply is the second-order condition .

3.2 Choice of Analysts and -Equilibrium

In order to maximize their profits when choosing , firms need to know or estimate the impact of their actions on their profits. Corresponding to the numbering of terms in (3.1), we assume that each firm knows (or correctly estimates): (i) the direct effect of its strategy on its profit ; and (ii) the effect of the firm’s demand on its profit . By contrast, we assume it is difficult for the firm to estimate (iii) the response of its demand to marginal changes in its strategy, i.e., to estimate . For example, during price competition firms know how their product’s prices affect their profit margins and how demand affects profit, but might not know how sensitive consumers might be to price changes. Similarly, in advertising competition (Section 5.3) firms know how increasing advertising spending affects their bottom line costs, but might not know the impact of their advertising on demand. Each firm therefore hires an analyst in the first stage who is tasked with estimating .

Let denote the interval of feasible biases of analysts, and we assume that includes an open interval around . Each analyst is characterized by a bias that causes him to estimate the marginal effect of the strategy on demand as instead of , where the bias function is continuously differentiable in both parameters and is strictly increasing in . We are interested in situations in which it is clear what the sign of is. Thus, we assume that has the same sign as , and that is increasing in .333The definitions and results can be adapted to a setup in which the analyst’s bias is the opposite sign of the sensitivity of demand, i.e., a negative for which the sign of is the opposite of the sign of . The outcome would be that in any naive analytics equilibrium firms hire analysts who are biased only with respect to the magnitude of but not with respect to its sign (i.e., firms hire only analysts with positive -s). We normalize to represent a calibrated (non-biased) analyst, i.e., . In the applications presented later in the paper, we will assume that the bias is multiplicative: . We denote this multiplicative bias by .

Let denote the biased estimation of analyst with bias . We denote the bias profile of all analysts by . An -analyst induces the firm to choose that solves the biased first-order and second-order conditions

| (3.2) |

instead of the unbiased conditions in (3.1).

There are many reasons why analysts might be biased. One example is inadvertently creating endogenous correlation between the firm’s strategy and demand without taking this correlation into account in the analysis. If a firm sets lower “sale” prices on days of low demand and higher regular prices on days of high demand, estimating price elasticities using the resulting data will show that consumers are less price sensitive than they actually are (as in Section 2). Another example is when firms set their advertising budgets differently in specific times such as before holidays, or weekends. This would create correlation in the levels of advertising with those of competitors. Ignoring this correlation during analysis may lead to a biased estimate of advertising effectiveness. We present micro-foundations for biased analytics towards the end of Section 5.2 (price competition) and Section 5.3 (advertising).

Next we define how the firms play in the second-stage, given the analysts’ biased profile . A strategy profile is an -equilibrium of the game if each player believes (based on her analyst’s estimated sensitivity of demand) that any small change to its strategy would decrease her perceived payoff. Formally

Definition 1 (-Equilibrium).

Fix a biasedness profile . A strategy profile is an -equilibrium if (1) , and (2) .

3.3 Naive Analytics Equilibrium (NAE)

In what follows we define our main solution concept. A naive analytics equilibrium (NAE) is a bias profile and a strategy profile, where (1) the strategy profile is an -equilibrium, and (2) each bias is a best-reply to the opponents’ bias profile (i.e., any unilateral deviation to another bias would induce a new -equilibrium with a weakly lower payoff to the deviator).

Definition 2.

A naive analytics equilibrium of is a pair , where:

-

1.

is an -equilibrium of the underlying game .

-

2.

for each , each , and each -equilibrium .

We do not interpret the equilibrium behavior in the first-stage as the result of an explicit maximization of sophisticated firms who know the demand function and calculate the optimal -s for their analysts. Conversely, we think of the firms as having substantial uncertainty about the demand function and its dependence on the behavior of various competitors. Due to this uncertainty, the firms hire analysts to estimate the sensitivity of demand. Occasionally (say, at the end of each year) firms consider replacing the current analyst with a new one (say, with a new random value of ), and a firm is more likely to do so the lower its profit is. If after several months it turns out that the new analyst decreases the firm’s profit, then the firm is likely to re-hire the old analyst. Gradually, such a process would induce the firms to converge to hiring most of the time analysts with values of that are best replies to each other, and thus constitute a naive analytics equilibrium . Various existing static solution concepts are motivated by assuming an analogous dynamic convergence process, see, e.g., Huck and Oechssler (1999); Dekel et al. (2007); Winter et al. (2017); Frenkel et al. (2018).

It is important to note that the observed data does not contradict the optimality of the strategic choices of the firms or the correctness of the estimations of the sensitivity of demand of the analysts. Consider, for example, a naive analytics equilibrium in the price competition described in Section 2. A firm that wishes to confirm that its price is indeed optimal (i.e., that it maximizes its profit given the demand) is likely to experiment with temporary changes in prices to see its influence on demand. Under the arguably plausible assumption that the analysis of such an experiment will be done with the same level of sophistication as the one leading to , the firm’s conclusion from the experiment would be that the sensitivity of demand is exactly as estimated by the firm’s naive analyst, and that the firm’s equilibrium strategy is optimal (e.g., it induces elasticity of in the motivating example, and thus maximizes the firm’s profit).

A firm in a naive analytics equilibrium that will deviate in the direction that increases profit, will induce a short-run increase in its expected profit; yet this temporary increase in profits might be difficult to measure in noisy environments. Moreover, as soon as the competitors observe the change in their demands (due to the firm’s deviation), they are likely to adjust their strategies toward their new (perceived) best replies. Following this adjustment, the deviating firm’s profit will decrease (which is formalized in Proposition 1 below).

Remark 1 (Delegation interpretation).

An alternative interpretation of our model (which we do not use in the paper) is of delegation. Let be a subjective payoff function such that maximizing with an unbiased estimation is equivalent to maximizing with a biased estimation of , i.e., for any strategy profile

Let be the set of all such subjective payoff function. One can reinterpret a NAE as an equilibrium of a delegation game (Fershtman and Judd, 1987) where in the first stage each firm’s owner simultaneously chooses a payment scheme for its manager, which induces the manager with a subjective payoff function in . In the second stage the managers play a Nash equilibrium of the game induced by the subjective payoffs. Although, both interpretations (namely, naive analytics and delegation) yield the same prediction about the equilibrium strategy profile, they differ in other testable predictions, as well as with their insights and policy implications (as discussed in Section 7). For concreteness, we focus on the comparison for price competition (as in the motivating example). The delegation interpretation predicts firms will correctly estimate the elasticity of demand and pay managers a payoff that increases in the firm profit and decreases in the firm’s sales (see, Fershtman and Judd, 1987, p. 938). The naive analytics interpretation predicts that firms will hire naive analysts that overestimate elasticity of demand, with a manager’s payoff scheme that depends directly on the firm’s profit. As mentioned elsewhere in the paper, we believe this latter prediction is more consistent with the empirically observed behavior of firms.

3.4 Robustness to Unilateral Sophistication

In this section we show that a naive analytics equilibrium is robust to any of the players unilaterally becoming patient and sophisticated, in the sense that each player plays the same strategy she would have played if she were an unbiased, sophisticated, and patient player, who plays the strategy that will maximize her payoff, given the biased responses of her opponents (i.e., her Stackelberg-leader strategy). Such a sophisticated player might represent a scenario, for example, where an E-commerce retailer sells goods to consumers, but also allows other third-party sellers to sell competing goods through the retailer’s website.

We begin by defining an -equilibrium as a profile in which player plays , all players except for play a perceived best-reply given their biases, and is a perceived best reply to some feasible bias in . Formally

Definition 3.

Fix player , strategy , and bias profile . Strategy profile is an -equilibrium if (1) and for each player , and (2) there exists such that and .

Next we define as the set of optimal strategies of an (unbiased) Stackelberg-leader player who faces opponents with bias profile .

Definition 4.

We say that is a Stackelberg-leader strategy against bias profile if there exists an -equilibrium , such that for any strategy and any -equilibrium . Let be the set of all such Stackelberg-leader strategies.

Next we characterize a naive analytics equilibrium as an -equilibrium in which everyone plays Stackelberg-leader strategies.

Proposition 1.

The pair is a naive analytics equilibrium iff (1) is an -equilibrium, and (2) for each player .

Sketch of proof; proof in Appx. D.1.

If is (resp., is not) a Stackelberg-leader strategy against bias profile , then there does not (resp., does) exist a bias that induces an -equilibrium where player plays a Stackelberg-leader strategy and gains a payoff higher than in . ∎

4 General Results

We answer 3 main questions about firms in a naive analytics equilibrium: (1) when are the players’ perceived best replies above or below their unbiased best replies (Section 4.2), (2) when do they underestimate or overestimate the sensitivity of demand through biased analytics (Section 4.3), and (3) when do they achieve payoffs that Pareto dominate the Nash equilibrium (Section 4.4). A summary of results is presented in Table 4.5 in Section 4.5.

4.1 Assumptions

Our first pair of assumptions require that (1) the externalities of any player’s strategy on any opponent’s payoff are all in the same direction, and (2) the partial derivative of increasing a player’s strategy on her payoff is in the same direction for all players, i.e., (i) all players have the same direction for the direct effect , and (ii) all players have the same direction for the indirect effect .

Assumption 1 (Monotone externalities).

The payoff externalities are either all positive or all negative for every and every .

Assumption 2 (Monotone partial derivatives).

-

i)

is either all positive or all negative for every and every .

-

ii)

is either all positive or all negative for every and every .

Assumptions 3–4 require the payoff function to be concave and satisfy either strategic complements or strategic substitutes. Moreover, we require that these properties hold with respect to any possible biased estimation of demand sensitivity. Thus, we call these properties robust concavity and robust strategic complementarity.

Assumption 3 (Robust concavity).

, , and .

Robust concavity implies that each opponent’s profile admits a unique perceived best reply, which we denote by , and we omit the superscript when denoting with the unbiased best reply, i.e., .

Assumption 4 (Robust strategic complementarity).

The cross derivatives are either all positive or all negative for every , , and .

Assumptions 3–4 can be replaced with stronger assumptions that depend only on the underlying game (and not on elements related to the biases: and ).

Assumption 3’.

for every and , where at least one of the two inequalities is strict.

Assumption 4’.

Either or , for every and , where at least one of the two inequalities is strict.

Next we assume that perceived best replies are bounded. Formally (where we write that iff for each )

Assumption 5 (Bounded Perceived Best Replies).

For each bias profile there exist profiles such that for each .

Assumption 5 implies that the signs of the two partial derivatives must differ, i.e.,

| (4.1) |

because otherwise there could not be an interior best-reply , for which . Further observe that Assumption 5 implies the existence of -equilibrium for each bias profile .

Proof.

Let be the set of profiles bounded between and (as defined in Assumption 5). The claim is implied by applying Brouwer fixed-point theorem on the convex and compact set and the continuous function . ∎

Our final assumption is required only in games with strategic substitutes with more than two players. Consider a situation in which some player deviates from an -equilibrium and then never further changes her play. Player ’s deviation induces the remaining players to adapt their strategies to a perceived best reply. This adaptation, in turn, induces these players to further adapt their strategies to a new perceived best reply. Assumption 6 requires that the players’ strategies keep the same direction of deviation with respect to the original -equilibrium after the secondary adaptation.

Assumption 6 (Consistent secondary adaptation).

Fix any bias profile , any -equilibrium , any player , and any strategy . Then for each player

It is immediate that Assumption 6 is vacuous (i.e., it always holds) if either (1) the game has two players (in which case ), or (2) the game has strategic complements (which implies that the original adaptation and the secondary adaptation are in the same direction). Thus, Assumption 6 is non-trivial only in the remaining case of a game with players and strategic substitutes.

4.2 Perceived Best Replies

Our first result characterizes whether the perceived best-replies of the agents are above or below the unbiased best reply in naive analytics equilibria. Specifically, it shows that the perceived best-reply of each player is above her unbiased best reply (i.e., ) in any naive analytics equilibrium iff the strategic complementarity has the same direction as the payoff externalities (i.e., ). Formally (where we write without specifying the quantifiers on the profile and players due to Assumption 1 (resp., 4) that imply that the sign of (resp., ) is the same for all players and profiles).

-

1.

for any iff .

-

2.

for any iff .

Proof.

Assume that . If opponents did not react to player unilaterally decreasing her strategy towards , then player would have gained from it, but the fact that is a Stackelberg-leader strategy means that decreasing player ’s strategy has a negative impact on player ’s payoff due to the opponents’ reaction (“” below). This can only happen if either the game has robust strategic complements and positive externalities, resulting in lower prices and payoffs if player decreases , or similarly if it has robust strategic substitutes and negative externalities (“” below), both of which imply that the strategic complementarity and the externalities have the same direction. The equilibrium response remains in this initial direction due to Assumption 6. The argument that implies that the strategic complementarity and the externalities are in opposite directions is analogous.

Appendix B presents an example that illustrates why Assumption 6 (consistent secondary adaptation) is necessary for Proposition 2 (and for the remaining results in this section). An immediate corollary of Proposition 2 is that the difference between perceived best reply and the unbiased best reply of all players is always in the direction that benefits (harms) the opponents in games with strategic complements (substitutes). Formally,

4.3 Direction of Analytics Bias

Our next result characterizes the condition for analysts to either overestimate or underestimate the sensitivity of demand in any naive analytics equilibrium. Specifically, we show that all players overestimate the sensitivity of demand (i.e., for each player ) iff the number of positive derivatives is even among the three monotone derivative: strategic complementarity , payoff externalities , and partial derivative .

Proposition 3.

Proof.

The result is derived as follows:

Remark 2.

Heifetz

et al. (2007a, Lemma 1) present

a similar result to Proposition 3 in a setup of evolution

of subjective preferences (which can also be interpreted as delegation)

for symmetric two-player games, under two strong assumptions:

(1) unique -equilibrium for each

, which allows to define a payoff function

for each bias profile, and (2) structural assumptions on :

strict concavity and

Our contribution is two-fold. First, the change of mechanism from

subjective preferences / delegation to biased analytics is important,

and it induces novel predictions and policy implications. Second,

we extend Heifetz

et al. (2007a, Lemma 1) to arbitrary -player

games and substantially relax the two strong assumptions mentioned

above.444The two strong assumptions are required for their dynamic convergence

result, namely, Heifetz

et al., 2007a, Theorem 2; we do not

present a formal dynamic convergence result in this paper. Note, in particular, that the assumption of

being concave does not hold in our applications, and is not required.

4.4 Pareto Dominance

Finally, we show that any naive analytics equilibrium of any game with strategic complements Pareto improves over the Nash equilibrium payoffs of the underlying game. Moreover, the converse is true for symmetric equilibria of games with strategic substitutes: Any symmetric naive analytics equilibrium of any game with strategic substitutes (which admits a symmetric Nash equilibrium) is Pareto dominated by the Nash equilibrium of the underlying game.

Definition 5.

Strategy profile is symmetric if for any pair .

-

1.

If (strategic complements), then there exists a Nash equilibrium s.t. for each : (i) and (ii) .

-

2.

If (strategic substitutes), then for each Nash equilibrium there exists a player s.t. . Moreover, if and are both symmetric profiles, then for each player .

Proof of part (1); see Appx. 4.4 for the similar proof of part (2) and for the lemmas.

Corollary 1 implies that for each . A standard argument for games with strategic complements (proven in Lemma 1) implies that there must be a Nash equilibrium , such that for each . We are left with showing that . Let be a -equilibrium. It is simple to see (and formally proven in Lemma 2) that for any . due to Lemma 2, this implies that for each . Proposition 1 implies that (due to being a Stackelberg-leader action with respect to ). Finally, the payoff externalities imply that . Combining the two inequalities yield that . ∎

4.5 Summary of Results

Assumptions 1–2 map to eight combinations of the signs of the strategic complementarity , payoff externalities and partial derivative . Effectively, these eight combinations define four unique classes of games since relabeling strategies as their negative values (i.e., replacing with ) results in essentially the same game with opposite signs to each of three monotone derivatives (see, Fact 1 in Appendix A). Table 4.5 summarizes our results for these four classes (and the remaining four classes are presented in Appendix A).

| Applications (Sections 5.2–5.4) | Strategic comp./sub. | |

|---|---|---|

| Payoff | ||

| Extr. | ||

| Partial derivative | ||

| Perceived best replying (Prop. 2) | Analytics bias | |

| (Prop. 3) | Pareto Dominance (Prop. 4) | |

| Price competition w. subs. goods (motiv. example) | + Strategic complements | |

| + | ||

| + | ||

| NAE | ||

| Advertising with positive exter. & team production | ||

| + | ||

| - | ||

| Pareto dominates NE. | ||

| Price competition with complement goods | - Strategic Substitutes | |

| - | ||

| + | ||

| Symmetric | ||

| Advertising with negative externalities | ||

| - | ||

| - | ||

| NE Pareto dominates sym. NAE |

5 Applications

We present three applications of our model: price competition, advertising competition, and team production. Before analyzing the applications, we present an auxiliary characterization result for the level of naivete in a naive analytics equilibrium.

5.1 Auxiliary Result: Characterization of

In what follows we obtain a useful characterization for the level of naivete in a naive analytics equilibrium. The presentation of this result is much simplified under the assumption of unique perceived best responses (which holds in all the applications).

Assumption 7.

For each player , strategy , and profile , there exists a unique -equilibrium, which we denote by .

Our next result shows that the magnitude of bias of player in assessing her sensitivity of demand (i.e., ) is a sum of the products of the impact of the player’s strategy on each of her opponent’s strategies (i.e., () times the impact of the opponent’s strategy on the player’s demand (i.e., ). Formally:

Claim 2.

Let be a naive analytics equilibrium of a game that satisfies Assumption 7. If , , and is differentiable at for each player then

5.2 Price Competition

Underlying Game

The underlying game is a price competition with linear demand (generalizing the motivating example of Section 2). Each seller sets a price , where if and if . Limiting the maximum price to is without loss of generality because setting a higher price implies that the seller’s demand cannot be positive. The demand of each firm is:555Our results remain the same if one adapts the demand function to be non-negative, i.e., . We refrain from doing so, as it will require rephrasing the assumptions of the general model (Section 4) in a more cumbersome way: assuming demand to be non-negative, and allowing the various monotone derivatives to be equal to zero when the demand is equal to zero.

| (5.1) |

where is a weighted mean price with weights and , and where , and for each . The sign of (which coincides with sign of ) determines whether the sold goods are substitutes ( as in the standard differentiated Bertrand competition) or complements ( as in a case of two stores that sell complementary goods, such as kitchen appliances and cooking ingredients, or as in the case of adjacent stores that sell unrelated goods, and a price decrease in one of the stores attracts more customers that also visit the neighboring store). The inequality constrains the cross-elasticity parameters to be sufficiently small relative to the own-elasticity parameters. If then we further require an additional upper bound on the the cross-elasticity: which implies Assumption 6.

Finally, the profit of each firm is given by . This profit function corresponds to constant marginal costs, which have been normalized to zero. Observe that game has strategic complements if and strategic substitutes if . Lemma 3 in Appendix D.3 shows that the price competition game admits a unique Nash equilibrium, which we denote by .

Results

Let be the analytics game with multiplicative biases , . Our first result shows that price competition satisfies all the assumptions of the general model, and that in any naive analytics equilibrium:

- 1.

-

2.

The prices are higher than in the Nash equilibrium; and

-

3.

The naive analytics equilibrium Pareto dominates (resp., is Pareto dominated by) the Nash equilibrium if the game has strategic complements (resp., substitutes).

, and .

The proof is presented in Appendix D.3.

Our next results explicitly characterize the unique naive analytics equilibrium in two important special cases (1) duopolies and (2) symmetric oligopolies. This characterization will be used in analyzing the impact of merges in Section 6. Proposition 6 shows that in duopolistic competition, both firms use the same level of naivete, which is decreasing in the ratio between the cross-elasticity parameters and the own-elasticity parameters. It is convenient to relabel the variables in the duopoly case as follows: (1) , and (2) . With this relabeling the demand function is simplified to be:

Proposition 6.

Assume that . Then admits a unique naive analytics equilibrium in which

Proof.

We note that the property that asymmetric firms must have the same biasedness level in a naive analytics equilibrium does not hold when there are more than two firms.

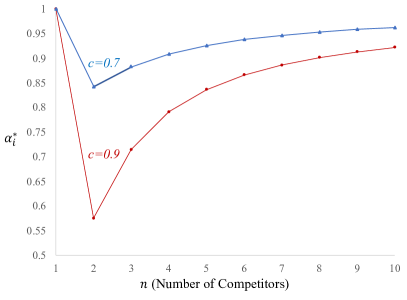

Next we characterize the unique symmetric naive analytics equilibrium in symmetric oligopolies, in which the demand parameters are the same for all firms: and for each firm . Proposition 7 shows that the level of bias depends only on the ratio and on , and that it is increasing in . The dependency on is non-monotone. A monopoly is unbiased (). By contrast, firms in duopoly have the strongest bias (i.e., is furthest from one), and the level of biasedness decreases (i.e., becomes closer to one) the larger the number of competitors (converging back to 1 when ). Formally,

Proposition 7.

Assume that the price competition is symmetric. Then admits a unique symmetric naive analytics equilibrium , where depends only on and and satisfies the following properties: (1) is increasing in for , (2) , (3) for , and (4)

The proof is given in Appendix D.4. The intuition for increasing in is the same as in the case of two competing firms. A monopoly has no strategic advantage from biased estimation (and, thus, ). The intuition why is increasing in for is that the larger the number of competing firms, the smaller the strategic impact of a player’s price on the biased best reply of her competitors, and thus the strategic advantage of having biased analytics decreases.

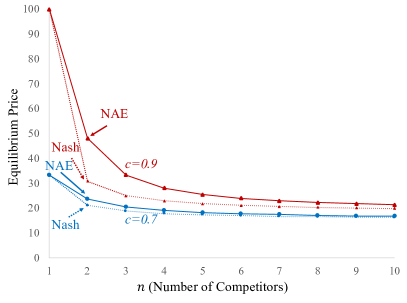

Proposition 7 is illustrated in Figure 5.1. The left panel shows the equilibrium level of bias in symmetric competition as a function of the number of competing firms for , , and . The right panel shows the (unbiased) Nash equilibrium prices and the naive analytics equilibrium prices in these cases. The figure shows that that the differences between the NAE and the Nash equilibrium prices are maximal for duopolies, and gradually decrease as increases. This suggests that a counter-factual economic analysis of the impact on two firms merging on the equilibrium prices, which ignores the biased analytics, would overestimate the price increase induced by a duopoly merging to a monopoly, and it would underestimate the price induced by all other mergers. This argument is detailed and illustrated in Section 6.

The left panel shows the symmetric naive analytics equilibrium level of biasedness as a function of the number of competing firms for and . The right panel shows the (unbiased) Nash equilibrium prices and the naive analytics equilibrium prices in each case.

Micro-Foundations for

We conclude this application by discussing plausible mechanisms that can induce analysts to unintentionally underestimate demand sensitivities and elasticities:

-

1.

The first mechanism has been illustrated in the motivating example (Section 2), and is described here again briefly. Suppose the daily demand of each firm has a random component for which the firm employees observe an informative signal. For example, the employees observe the weather forecast which is correlated with the realized demand. If the employees prefer to set lower sale prices on days with low demand, e.g., because they have more free time to change prices, then naive analysts who allow the employees to choose the days for price discounts would induce a correlation between low demand days and low prices. As a result, they will under-estimate of the elasticity of demand. A sophisticated analyst who closely ensures that price discounts are set uniformly at random, or accurately controls for the weather forecast in his econometric analysis, would yield an accurate estimation of the elasticity.

-

2.

The second mechanism is formalized in Appx. C.1, and is presented here briefly. Employees of competing stores might choose similar days for price discounts. One examples is setting discounts by season (holidays) or for specific days of the week (weekends). Another example is if the levels of their inventory is correlated and discounts are given when the inventory level is high. This correlation in prices would induce naive analysts who allow employees to set the days with price discounts to under-estimate the price elasticity, because in days with low prices the competitor is more likely to provide a discount as well, making the response to price discounts seem weaker.

5.3 Advertising Competition

Research that estimates the effectiveness of advertising often showed that extra care is required to arrive at non-biased estimates, and that not correcting for these biases often results in overestimating advertising effectiveness (Lodish et al., 1995; Blake et al., 2015; Gordon et al., 2019; Shapiro et al., 2019). In the second application of our model we analyze a duopoly competition in advertising to understand why firms might benefit from naive analytics that overestimates the effectiveness of advertising.

Underlying Game

The underlying game describes an advertising competition among two firms. Firm sells a product with exogenous profit margins per unit sold. The expected demand of each firm depends on the advertising budget of both firms:

| (5.3) |

where . When the feasible budget set is unrestricted (). When , we restrict the maximum budget to be (i.e., ). This restriction is without loss of generality as additional budget above cannot increase the firm’s demand when .

In this market a firm’s own advertising increases demand for its own product ( is positive), but the competitor’s advertising may affect the level of the increase. When the total category demand increases when the competitor advertises, which increases the effect of a firm’s own advertising. When the effect of a firm’s own advertising decreases in the competitor’s advertising due to competition (e.g., over the same customers). We require the sign of and to coincide. Positive -s might correspond to a new category of goods, in which advertising attracts attention to the category. Negative -s might correspond to a mature category in which advertising mainly causes consumers to switch among competing goods. The payoff of player is given by

| (5.4) |

We require the advertising externalities to be sufficiently small: , which implies well-behaved interior Nash equilibrium. Further, if we assume Lemma 6 in Appendix D.5 proves that advertising competition admits a unique Nash equilibrium, which we denote by .

Naive Analytics Equilibrium

Let be the analytics game with multiplicative biases, i.e., . Our result shows that advertising competition satisfies all the assumptions of the general model, and that in any naive analytics equilibrium:

-

1.

The firms hire analysts that overestimate the effectiveness of advertising (and the level of bias is the same for both firms);

-

2.

The advertising budgets are higher than in the Nash equilibrium; and

-

3.

The naive analytics equilibrium Pareto dominates (resp., is Pareto dominated by) the Nash equilibrium if the game has strategic complements (resp., substitutes).

, and .

The proof is presented in Appendix D.5.

Micro-Foundations for

We conclude this section by providing micro-foundational examples of cases that would cause firms to overestimate their advertising effectiveness:

-

1.

Similarly to price competition, correlation between advertising budgets of firms with positive externalities would cause an overestimate of ad effectiveness. If firms choose to increase budgets during the holidays, or just prior to weekends, they will observe an increase in demand beyond the effects of their own advertising. This correlation will create an overestimate of advertising elasticity.

-

2.

When online advertising is purchased on social media platforms, such as on Facebook, the advertiser provides the advertising platform a budget and a target metric. The platform’s algorithm then targets consumers in order to maximize the target metric under the budget constraint. One common such metric is sales or purchases, and a strategy to maximize this metric is to show ads to likely buyers of the product, or to past purchasers of the product. Under such a strategy, an analysis that compares the purchase rates of people that have seen ads to those that have not seen ads will overestimate the effectiveness of advertising (Berman, 2018).

-

3.

If firms respond to decreased demand by increasing their advertising budgets in the next time period, and if demand is noisy, a standard “regression to the mean” argument implies that demand is likely to increase in the next period regardless of the additional advertising budget. Failing to take this into account would lead to overestimation of the advertising effectiveness, as we formally present in Appendix. C.2.

5.4 Team Production and Overconfidence

Thus far we have interpreted as market demand and as bias due to naive analytics. We now demonstrate that our model applies in more general settings. Specifically, we apply the model to an underlying game of team production with strategic complementarity. Team production is common in partnerships and other input games (see, e.g., Holmstrom, 1982; Cooper and John, 1988; Heller and Sturrock, 2020). Examples include salespeople who are compensated based on the performance of the joint sales of a team, entrepreneurs who receive a share of the exit value of a startup, and academic co-authors who benefit from the impact of their joint paper. It is often observed that entrepreneurial firms are founded by teams of overconfident founders (Astebro et al., 2014; Hayward et al., 2006). Taking this perspective, we interpret as the contribution of each team member, and as the value created by the team. This analogy directly leads to interpreting as a bias player has when evaluating their contribution to the value created by the team, which can be seen as a measure of confidence. We show that in any naive analytics equilibrium all agents are overconfident in the sense of overestimating their ability to contribute to the team’s output (i.e., having ). In the case of entrepreneurship, for example, much of the past research explained overconfidence as necessary to overcome risk aversion and tackle uncertainty, that is, as a response to the entrepreneurial environment which is external to the firm.666See also Heller (2014) who demonstrates that overconfidence of entrepreneurs can help an investor in diversifying aggregate risk. Our results provide a novel foundation for the tendency of people (and, in particular, entrepreneurs) to be overconfident in the sense of overestimating one’s ability. We show that when skills are complementary, overconfidence contributes to increased team efficiency, and is a response to the internal firm environment. The results provide a novel explanation to why investors might prefer to invest in overconfident startup founders, why managers might prefer to hire overconfident sales people, and why academic researchers might prefer working with overconfident co-authors (see, Herz et al., 2020, for evidence suggesting that co-authors over-estimate their contributions to joint papers).

Underlying Game

We describe a team production game with strategic complements. Consider players, each choosing how much effort to exert in a joint project. The project yields a benefit to each agent , where is twice continuously differentiable in , strictly increasing, strictly concave, and supermodular, i.e., , , for any and any ). The payoff of each player is equal to her project’s benefit minus her effort: Observe that the above assumptions imply that the payoff function is strictly concave and satisfies strategic complementarity. Consequently all Nash equilibria of the underlying game are pure, and one of them, denoted by , has the lowest effort levels (i.e., for any Nash equilibrium ). Finally, we require that the marginal contribution of efforts are initially very high, while converging to zero for very large efforts, which implies that players always have bounded perceived best-replies. Specifically, we assume that the marginal contribution of a player’s effort converges to infinity (resp., zero) when the efforts converge to zero (resp., infinity) and the profile of efforts is symmetric:

Assumption 8.

For each player

Result

Let be an analytics game induced by . We show that satisfies assumptions 1–6, and as a result we can apply the results of Section 4 and show that in any naive analytics equilibrium: (1) all agents are overconfident in the sense of overestimating their own influence on the joint project, (2) exert more effort than in the lowest Nash equilibrium, and (3) the payoffs Pareto dominates the lowest Nash equilibrium. Formally (the proof is presented in Appx. D.6):

Proposition 9.

6 Implications for Market Structure Analysis

In this Section we demonstrate the implications of the naive analytics equilibrium concept for analysis of market structure in oligopolies. Data on product quantities and prices are often used to infer price-cost margins (PCM) to be used in analysis of mergers and market power (Nevo, 2000, 2001). In these analyses one often assumes that firms play a differentiated Bertrand competition, as in Section 5.2, and the observed price elasticities are used to infer the unobserved marginal costs of firms, to be used in simulation of different market structures.

We illustrate the implications of firms playing a naive analytics equilibrium on the results of this analysis. Assume three firms, numbered , and , play a symmetric differentiated Bertrand competition with demand , zero marginal costs and , . Appendix (D.7) explicitly calculates the unique pre-merger NAE , which is a special case of the symmetric oligopoly in Section 5.2.

Suppose firms and plan to merge, and an economist (e.g., a regulator) tries to predict the prevailing prices post-merger using pre-merger observed prices and quantities. The economist, not knowing that the firms are playing a naive analytics equilibrium with zero marginal costs, assumes that pre-merger each firm set its prices to maximize the payoff , with being firm ’s (unknown) marginal cost. Post-merger, the economist assumes firm will set prices to maximize while the merged firm will set prices and simultaneously to maximize the joint profit .

In reality, the firms will converge to a new naive analytics equilibrium with prices that depend on the equilibrium biases of the firms. We denote by the long-run analytics bias, and by the NAE prices in the long run. In the short run, the firms might have not adjusted their analytics yet, setting prices accordingly. We also denote by the equilibrium prices predicted by the economist who assumes firms have the same marginal costs after the merger, and no analytics bias. The analysis shows that the economist will estimate positive marginal costs for the firms, and that she will underestimate the new equilibrium prices after the merger.

Proposition 10.

Assume that pre-merger price competition is symmetric and that , and . Assume that post-merger firms and merge and set prices simultaneously for both goods. Then: (1) The economist will estimate . (2) The economist will underestimate post-merger prices: .

The proof appears in Appendix (D.7). The prices in the pre-merger naive analytics equilibrium will be above the Nash equilibrium prices, as shown in Proposition 5. These inflated prices will cause the economist to estimate a positive marginal cost above zero for all firms. Post merger, the firms will increase their prices due to the decreased competition. Despite the economist overestimating firm marginal costs, which would allow her to predict higher prices post-merger, this bias is not enough to compensate for underestimating the prices in a naive analytics equilibrium.

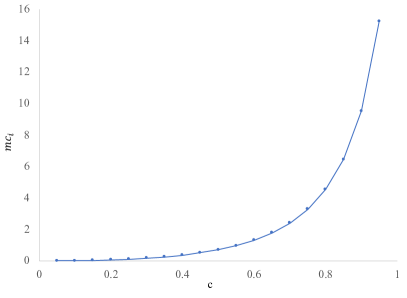

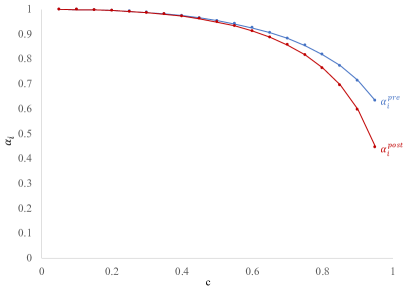

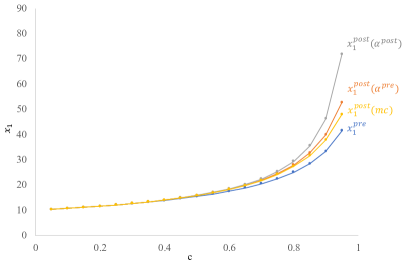

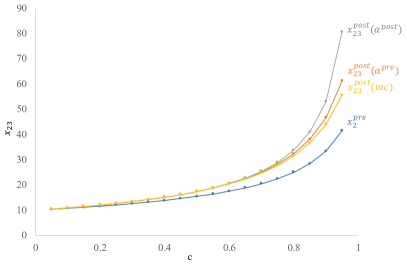

Figure 6.1 illustrates these results for , and . The top panels show that the estimated marginal costs are positive and increasing with (left), while the analytics biases are lower than 1, decrease with and (right). The bottom panels illustrate how the equilibrium prices change with for player (left) and the merged player (right). In all cases, the prices post-merger are higher than the prices pre-merger. However, the economist underestimates the price increase due to the merger, while the long-run price increases are the largest.

The left panel shows the marginal cost the economist estimates as a function of . The right panel shows the naive analytics equilibrium biases before and after the merger.

The left panel shows the equilibrium prices set by firm as a function of . The right panel shows the equilibrium prices set by firm pre-merger and the merged firm as a function of .

7 Conclusion

Naive analytics equilibrium can be used to analyze such games where players have uncertainty about the indirect impact of their actions on their payoffs, and allows players to use biased data analytics to estimate this impact. This scenario is common in economic applications such as price competition, advertising competition and team production.

The predictions of our results are consistent with commonly observed behaviors of firms and teams. In equilibrium, players are predicted to converge to biased estimates in the direction that causes their opponents to respond in a beneficial manner. In pricing competition, players are better off if they perceive consumers to be less price elastic than they actually are, which is a possible interpretation of observed firm pricing if they do not correct for price endogeneity in their econometric analysis. In advertising competition, it is observed that firms often overestimate the response to their advertising and over-advertise, as predicted by our results. These deviations from unbiased estimates cause deviations from the Nash equilibrium that can be beneficial or detrimental to players. When games have strategic complements, players will choose strategies that deviate from the Nash equilibrium in the direction that benefits the opponents, and their equilibrium payoffs will dominate those of the Nash equilibrium. The converse is true for games with strategic substitutes.

The results of our analysis provide testable empirical predictions about the direction and magnitudes of the biases. In particular, the analysis predicts that in duopolies, both firms will have similar level of biasedness (see, some supporting evidence in Table 2 of Villas-Boas and Winer, 1999). Another prediction is that biasedness is strongest in duopolistic competitions, it weakens as the number of competitors increase, and it disappears if there are many small competitors, or in a monopolistic market. These predictions could be tested in empirical data as well as serve as a basis for analysis about the adoption and sophistication of analytics in various industries. Further, our results may bring to question some of the assumptions used in practice when performing counterfactual analysis to estimate welfare and assess the impact of regulatory policy. In these analyses, it is often assumed that firms correctly perceive their economic environment and that any observed inconsistency with this assumption may be due to unobserved factors by researchers. However, the fact that firms misperceive the sensitivity of demand in a naive analytics equilibrium can substantially change the conclusions of counterfactual analysis used to assess the impact of market structure analysis, as we have demonstrated for the merger of competing firms in Section 6.

A second implication of our results is for research that focuses on biases in decision making from non-causal inferential methods. The research implicitly assumes that focusing on causality and more precise estimates are better for firm performance, which often translates to normative recommendation about firm practices (see, e.g., Siroker and Koomen (2013) and Thomke (2020) on A/B testing). Our results suggest that firms may be better off with opting for more naive heuristics, which are indeed quite popular because they are easy to implement. This may suggest that normative recommendations for deploying more sophisticated analytics capabilities should be made with caution in competitive environments.

References

- Alé-Chilet and Atal (2020) Alé-Chilet, J. and J. P. Atal (2020). Trade associations and collusion among many agents: Evidence from physicians. mimeo.

- Antler and Bachi (2019) Antler, Y. and B. Bachi (2019). Searching forever after. mimeo.

- Astebro et al. (2014) Astebro, T., H. Herz, R. Nanda, and R. A. Weber (2014). Seeking the roots of entrepreneurship: Insights from behavioral economics. Journal of Economic Perspectives 28(3), 49–70.

- Azrieli (2009) Azrieli, Y. (2009). Categorizing others in a large game. Games and Economic Behavior 67(2), 351–362.

- Azrieli (2010) Azrieli, Y. (2010). Categorization and correlation in a random-matching game. Journal of Mathematical Economics 46(3), 303–310.

- Battigalli and Guaitoli (1997) Battigalli, P. and D. Guaitoli (1997). Conjectural equilibria and rationalizability in a game with incomplete information. In Decisions, Games and Markets, pp. 97–124. Berlin: Springer.

- Berman (2018) Berman, R. (2018). Beyond the last touch: Attribution in online advertising. Marketing Science 37(5), 771–792.

- Berry (1994) Berry, S. T. (1994). Estimating discrete-choice models of product differentiation. RAND Journal of Economics 25, 242–262.

- Besanko et al. (1998) Besanko, D., S. Gupta, and D. Jain (1998). Logit demand estimation under competitive pricing behavior: An equilibrium framework. Management Science 44(11-part-1), 1533–1547.

- Blake et al. (2015) Blake, T., C. Nosko, and S. Tadelis (2015). Consumer heterogeneity and paid search effectiveness: A large-scale field experiment. Econometrica 83(1), 155–174.

- Chintagunta et al. (2005) Chintagunta, P., J.-P. Dubé, and K. Y. Goh (2005). Beyond the endogeneity bias: The effect of unmeasured brand characteristics on household-level brand choice models. Management Science 51(5), 832–849.

- Cooper and John (1988) Cooper, R. and A. John (1988). Coordinating coordination failures in keynesian models. Quarterly Journal of Economics 103(3), 441–463.

- Dekel et al. (2007) Dekel, E., J. C. Ely, and O. Yilankaya (2007). Evolution of preferences. Review of Economic Studies 74(3), 685–704.

- Dufwenberg and Güth (1999) Dufwenberg, M. and W. Güth (1999). Indirect evolution vs. strategic delegation: A comparison of two approaches to explaining economic institutions. European Journal of Political Economy 15(2), 281–295.

- Esponda (2013) Esponda, I. (2013). Rationalizable conjectural equilibrium: A framework for robust predictions. Theoretical Economics 8(2), 467–501.

- Esponda and Pouzo (2016) Esponda, I. and D. Pouzo (2016). Berk–nash equilibrium: A framework for modeling agents with misspecified models. Econometrica 84(3), 1093–1130.

- Eyster and Rabin (2005) Eyster, E. and M. Rabin (2005). Cursed equilibrium. Econometrica 73(5), 1623–1672.

- Fershtman and Gneezy (2001) Fershtman, C. and U. Gneezy (2001). Strategic delegation: An experiment. RAND Journal of Economics 32(2), 352–368.

- Fershtman and Judd (1987) Fershtman, C. and K. L. Judd (1987). Equilibrium incentives in oligopoly. American Economic Review 77, 927–940.

- Fershtman and Kalai (1997) Fershtman, C. and E. Kalai (1997). Unobserved delegation. International Economic Review 38, 763–774.

- Frederik and Martijn (2019) Frederik, J. and M. Martijn (2019). The new dot com bubble is here: It’s called online advertising. The Correspondent, November 6.

- Frenkel et al. (2018) Frenkel, S., Y. Heller, and R. Teper (2018). The endowment effect as blessing. International Economic Review 59(3), 1159–1186.

- Friedman (2018) Friedman, E. (2018). Stochastic equilibria: Noise in actions or beliefs? mimeo.

- Fudenberg and Levine (1993) Fudenberg, D. and D. K. Levine (1993). Self-confirming equilibrium. Econometrica 61(3), 523–545.

- Golden and Horton (2020) Golden, J. and J. J. Horton (2020). The effects of search advertising on competitors: An experiment before a merger. Management Science forthcoming.

- Gordon et al. (2019) Gordon, B. R., F. Zettelmeyer, N. Bhargava, and D. Chapsky (2019). A comparison of approaches to advertising measurement: Evidence from big field experiments at facebook. Marketing Science 38(2), 193–225.

- Güth and Yaari (1992) Güth, W. and M. Yaari (1992). Explaining reciprocal behavior in simple strategic games: An evolutionary approach. In U. Witt (Ed.), Explaining Process and Change: Approaches to Evolutionary Economics, pp. 23–34. Ann Arbor: University of Michigan Press.

- Hansen et al. (2020) Hansen, K., K. Misra, and M. Pai (2020). Algorithmic collusion: Supra-competitive prices via independent algorithms. mimeo.

- Hayward et al. (2006) Hayward, M. L., D. A. Shepherd, and D. Griffin (2006). A hubris theory of entrepreneurship. Management Science 52(2), 160–172.

- Heifetz and Segev (2004) Heifetz, A. and E. Segev (2004). The evolutionary role of toughness in bargaining. Games and Economic Behavior 49(1), 117–134.

- Heifetz et al. (2007a) Heifetz, A., C. Shannon, and Y. Spiegel (2007a). The dynamic evolution of preferences. Economic Theory 32(2), 251–286.

- Heifetz et al. (2007b) Heifetz, A., C. Shannon, and Y. Spiegel (2007b). What to maximize if you must. Journal of Economic Theory 133(1), 31–57.

- Heller (2014) Heller, Y. (2014). Overconfidence and diversification. American Economic Journal: Microeconomics 6(1), 134–53.

- Heller and Sturrock (2020) Heller, Y. and D. Sturrock (2020). Promises and endogenous reneging costs. Journal of Economic Theory, 105024.

- Heller and Winter (2016) Heller, Y. and E. Winter (2016). Rule rationality. International Economic Review 57(3), 997–1026.

- Heller and Winter (2020) Heller, Y. and E. Winter (2020). Biased-belief equilibrium. American Economic Journal: Microeconomics, forthcoming.

- Herold and Kuzmics (2009) Herold, F. and C. Kuzmics (2009). Evolutionary stability of discrimination under observability. Games and Economic Behavior 67, 542–551.

- Herz et al. (2020) Herz, N., O. Dan, N. Censor, and Y. Bar-Haim (2020). Opinion: Authors overestimate their contribution to scientific work, demonstrating a strong bias. Proceedings of the National Academy of Sciences 117(12), 6282–6285.

- Holmstrom (1982) Holmstrom, B. (1982). Moral hazard in teams. Bell Journal of Economics 13, 324–340.

- Huck and Oechssler (1999) Huck, S. and J. Oechssler (1999). The indirect evolutionary approach to explaining fair allocations. Games and economic behavior 28(1), 13–24.

- Jehiel (2005) Jehiel, P. (2005). Analogy-based expectation equilibrium. Journal of Economic Theory 123(2), 81–104.

- Lewis and Rao (2015) Lewis, R. A. and J. M. Rao (2015). The unfavorable economics of measuring the returns to advertising. Quarterly Journal of Economics 130(4), 1941–1973.

- Lodish et al. (1995) Lodish, L. M., M. Abraham, S. Kalmenson, J. Livelsberger, B. Lubetkin, B. Richardson, and M. E. Stevens (1995). How tv advertising works: A meta-analysis of 389 real world split cable tv advertising experiments. Journal of Marketing Research 32(2), 125–139.

- Nevo (2000) Nevo, A. (2000). Mergers with differentiated products: The case of the ready-to-eat cereal industry. The RAND Journal of Economics, 395–421.

- Nevo (2001) Nevo, A. (2001). Measuring market power in the ready-to-eat cereal industry. Econometrica 69(2), 307–342.

- Rao and Simonov (2019) Rao, J. M. and A. Simonov (2019). Firms’ reactions to public information on business practices: The case of search advertising. Quantitative Marketing and Economics 17(2), 105–134.

- Shapiro et al. (2019) Shapiro, B., G. J. Hitsch, and A. Tuchman (2019). Generalizable and robust tv advertising effects. mimeo.

- Sinkinson and Starc (2019) Sinkinson, M. and A. Starc (2019). Ask your doctor? direct-to-consumer advertising of pharmaceuticals. Review of Economic Studies 86(2), 836–881.

- Siroker and Koomen (2013) Siroker, D. and P. Koomen (2013). A/B testing: The most powerful way to turn clicks into customers. John Wiley & Sons.

- Spiegler (2017) Spiegler, R. (2017). Data monkeys: A procedural model of extrapolation from partial statistics. Review of Economic Studies 84(4), 1818–1841.

- Spiegler (2019) Spiegler, R. (2019). Behavioral implications of causal misperceptions. Annual Review of Economics 12, 81–106.

- Steiner and Stewart (2015) Steiner, J. and C. Stewart (2015). Price distortions under coarse reasoning with frequent trade. Journal of Economic Theory 159, 574–595.

- Steiner et al. (2017) Steiner, J., C. Stewart, and F. Matějka (2017). Rational inattention dynamics: inertia and delay in decision-making. Econometrica 85(2), 521–553.

- Thomke (2020) Thomke, S. H. (2020). Experimentation Works: The Surprising Power of Business Experiments. Harvard Business Press.

- Villas-Boas and Winer (1999) Villas-Boas, J. M. and R. S. Winer (1999). Endogeneity in brand choice models. Management Science 45(10), 1324–1338.

- Winter et al. (2017) Winter, E., L. Méndez-Naya, and I. García-Jurado (2017). Mental equilibrium and strategic emotions. Management Science 63(5), 1302–1317.

Online Appendices

Appendix A Classes with Relabeled Strategies ()

It is simple to see that relabeling strategies as their negative values (i.e., replacing with ) results in essentially the same game with opposite signs to and .

Fact 1.

Table A presents the 4 classes derived from the main-text classes by relabeling the strategies.

| . |

| Applications (Sections 5.2–5.4) | Strategic comp./sub. | |

|---|---|---|

| Payoff | ||

| Extr. | ||

| Partial derivative | ||

| Perceived best replying (Prop. 2) | Analytics bias | |

| (Prop. 3) | Pareto Dominance (Prop. 4) | |

| Price competition w. subs. goods discount | + Strategic complements | |

| - | ||

| - | ||

| NAE | ||

| Advertising with positive exter. budget cut | ||

| - | ||

| + | ||

| Pareto dominates NE. | ||

| Price competition w. compl. goods discount | - Strategic Substitutes | |

| + | ||

| - | ||

| Symmetric | ||

| Advertising with neg. externalities budget cut | ||

| + | ||

| + | ||

| NE Pareto dominates sym. NAE |

Appendix B Example why Assumption 6 is Necessary

Example 1 illustrates why Assumption 6 (consistent secondary adaptation) is necessary for Proposition 2 (and, thus, for the remaining results of Section 4).

Example 1.

Consider a 3-player game in which the firms are located in a circle, the demand of each firm is decreasing in all prices, and it mainly depends on its own price and on its clockwise neighbor’s price. That is the demand functions are given by (for some :

and the profit function of each firm is . Observe that the game has strategic substitutes () and negative externalities (), which implies that the strategic complementarity and payoff externalities are in the same direction. In what follows we show that in any naive analytics equilibrium, contradicting Proposition 2. Assume to the contrary that , which implies that Player gains from unilaterally decreasing her price towards the unbiased best reply. This decrease initially induces both competitors to increase their prices, but player’s 3 response is much stronger. This new higher price of player 3 induces player 2 to readjust her price by decreasing it below her initial NAE price, which increases the payoff of player 1. This implies that player 1 gains from the change in her opponents’ strategies. Thus, cannot be a Stackelberg-leader strategy, which contradicts being a naive analytics equilibrium.

Appendix C Microfoundations for biased estimation

C.1 Bias in Price Competition

Suppose the analysts hired by each of the two firms decide to experiment with prices to find the price elasticity of demand by alternating between a high price () and a low price (), setting a low price (discount) -share of the time. The experiment can be characterized by a level of sloppiness . In a fraction of the time, the analyst doesn’t monitor the firm’s employees and does not carefully supervise that the employees choose the discount times uniformly at random. Hence, it is possible, for example, that the firm’s employees will implement discounts on days of low demand, possibly due to the employees having more free time in these days to deal with posting different prices. In the rest of the time ( fraction), the analyst verifies that the prices are set randomly. Consequently, when either analyst sets prices uniformly at random, there will not be correlation between the firm’s prices. This happens fraction of the time. In the remaining fraction of the time, there might be correlation between the firm’s prices, which we denote by . The joint distribution of prices conditional on the correlation and the fractions is described in Table 4.

When calculating the price elasticity of demand to decide how to change prices, the analyst calculates:

| (C.1) |

Where is the difference in average demand between high priced and low priced periods, is the average realized demand, is the difference in price between high and low price periods, and is the average price set by the firm.

The demand observed by firm when setting price and when its competitor sets a price is .

Using the joint probabilities in Table 4, we find that and .

Plugging into (C.1), firm will estimate its price elasticity as:

| (C.2) |

while the true elasticity is . Hence the analyst will estimate the firm’s price elasticity as being lower than when and .

C.2 Bias in Advertising Competition

Assume the firm’s sales at time behave according to the linear model where is the average sales, is the level of advertising, that can be or with , and is demand shock which is distributed i.i.d . In this model, the true effect of advertising, equals 1.

The firm has a sales target and its advertising strategy is to increase advertising to if sales fall below at time , i.e., if , and otherwise set .

To estimate the effect of advertising, the firm looks at the difference in sales when advertising is increased or decreased (otherwise the change cannot be attributed to changes in advertising) and takes the average to calculate

| (C.3) |

More sophisticated approaches can take into account a weighted average of these estimates and also take into account the baseline sales when advertising does not change.

The left-hand part of the summand equals:

where is the standard Normal pdf and its cdf. The right-hand part equals:

Because is decreasing in , the sum in the numerator of (C.3) is larger than 2, which results in the firm overestimating the effectiveness of its advertising to be more than 1.

Appendix D Technical Proofs

D.1 Proof of Prop. 1 (Unilateral Sophistication)

Assume to the contrary that is a naive analytics equilibrium and . The fact that implies that there exist and -equilibrium such that . Let be a bias satisfying and (such exists due to part (2) of Definition 4). Then is -equilibrium that satisfies , which contradicts being a naive analytics equilibrium.