Domain adaptation under structural causal models

Abstract

Domain adaptation (DA) arises as an important problem in statistical machine learning when the source data used to train a model is different from the target data used to test the model. Recent advances in DA have mainly been application-driven and have largely relied on the idea of a common subspace for source and target data. To understand the empirical successes and failures of DA methods, we propose a theoretical framework via structural causal models that enables analysis and comparison of the prediction performance of DA methods. This framework also allows us to itemize the assumptions needed for the DA methods to have a low target error. Additionally, with insights from our theory, we propose a new DA method called CIRM that outperforms existing DA methods when both the covariates and label distributions are perturbed in the target data. We complement the theoretical analysis with extensive simulations to show the necessity of the devised assumptions. Reproducible synthetic and real data experiments are also provided to illustrate the strengths and weaknesses of DA methods when parts of the assumptions in our theory are violated.

Keywords: anticausal, conditionally invariant components, domain generalization, domain invariant projection, label shift, structural equation models

1 Introduction

Domain adaptation (DA) is a statistical machine learning problem in which one aims at learning a model from a labeled source dataset and expecting it to perform well on an unlabeled target dataset drawn from a different but related data distribution. Domain adaptation is considered a sub-field of transfer learning and also a sub-field of semi-supervised learning (Pan and Yang, 2009). The possibility of DA is inspired by the human ability to apply knowledge acquired on previous tasks to unseen tasks with minimal or no supervision. For example, it is common to believe that humans who learned driving in sunny days would adapt their skills to drive reasonably well in a rainy day without additional training. However, the scenario where the source and target data distribution is different (e.g. sunny vs. rainy) is difficult to handle for many machine learning systems. This is mainly because the classical statistical learning theory mostly focuses on statistical learning methods and guarantees when the training and test data are generated from the same distribution.

While existing DA theory is limited, more and more application scenarios have emerged where DA is needed and useful. DA is desired especially when obtaining unlabeled data is cheap while labeling data is difficult. The difficulties of labeling data typically arise due to the required human expertise or the large amount of human labor. For example, to annotate the ImageNet Large Scale Visual Recognition Challenge (ILSVRC) dataset (Russakovsky et al., 2015) with more than 1.2 million labeled images, it costs an average worker on the Amazon Mechanical Turk (www.mturk.com) about 0.5 seconds per image (Fei-Fei, 2010). Thus, annotating more than 1.2 million images requires more than 150 human hours. The actual time needed for labeling is much longer, due to the additional time spent on label verification and on labeling the images which are not used in the final challenge. Now if one is only interested in a similar but different task such as classifying objects in oil paintings, one cannot expect the ILSVRC dataset which contains pictures of natural objects to be representative. As a consequence, one needs to collect new data. It is relatively easy to collect digital images for the new task, but it is costly to label them if human experts have to be involved. Similar situations where the labeling is costly emerge in many other fields such as part-of-speech tagging (Ratnaparkhi, 1996; Ben-David et al., 2007), web-page classification (Blum and Mitchell, 1998), etc.

Despite the broad need of DA methods in practice, a priori it is impossible to provide a generic solution to DA. In fact, the DA problem is ill-posed if assumptions on the relationship between the source and target datasets are absent. One cannot learn a model with good performance if the target dataset can be arbitrary. As it is often difficult to specify the relationship between the source and target datasets, a large body of existing DA work are driven by applications. This line of work often focuses on developing new DA methods to solve very specific data problems. Despite the empirical success on these specific problems, it is not clear why DA succeeds or how applicable the proposed DA methods are to new related data problems. The growing development of domain adaptation calls forth a theoretical framework to analyze the existing methods and to guide the design of new procedures. More specifically, can one formulate the assumptions needed for a DA method to have a low target error? Can these assumptions be itemized, so that once specified the performance of different DA methods can be compared? More specifically, does the causal direction of the data generation or the type and location of data perturbation (Figure 1) affect the choice of the best DA method?

To answer the above questions, this work develops a theoretical framework via structural causal models that enables the comparison of various existing DA methods. Since there are no clear winning DA methods in general, the performance of DA methods has to be analyzed and compared with precise assumptions on the underlying data structure. Through analysis on simple models, we aim to give insights on when and why one DA method outperform others.

Our contributions:

Our contributions are three-fold. First, we develop a theoretical framework via structural causal models (SCM) to analyze and compare the prediction performance of existing DA methods, such as domain invariant projection (DIP) (Pan et al., 2010; Baktashmotlagh et al., 2013) and conditional invariance penalty (CIP) or conditional transferable component (Gong et al., 2016; Heinze-Deml and Meinshausen, 2021), under precise assumptions relating source and target data. In particular, we show that under linear SCM the popular DA method DIP is guaranteed to have a low target error when the prediction problem is anticausal without label distribution perturbation. However, DIP fails to outperform the estimator trained solely on the source data when there are perturbations on the label distribution or when the prediction problem is either causal or mixed-causal-anticausal. Second, based on our theory, we introduce a new DA method called CIRM and develop its variants which can have better prediction performance than DIP in mixed-causal-anticausal DA scenarios and those with label distribution perturbation. Third, we illustrate via extensive simulations and real data experiments that our theoretical DA framework enables a better understanding of the success and failure of DA methods even in cases where presumably not all assumptions in our theory are satisfied. Our theory and experiments make it clear that knowing the relevant information about the data generation process such as the causal direction or the existence of label distribution perturbation is the key to the success of domain adaptation.

The rest of the paper is organized as follows. In Section 2 we review previous ways to mathematically formulate the DA problem and summarize the existing DA methods. Section 3 contains background on structural causal models, our problem setup, a formal introduction of the DA methods to study and three simple motivating examples. In Section 4 we analyze and compare the performance of three DA methods (DIP, CIP and CIRM) under our theoretical framework. Based on whether the DA problem is causal, anticausal or mixed and whether there is label distribution perturbation, we identify scenarios where these DA methods are guaranteed to have low target errors. Section 5 contains numerical experiments on synthetic and real datasets to illustrate the validity of our theoretical results and the implication of our theory for practical scenarios.

2 Related work

Domain adaptation is a sub-field of the broader research area of transfer learning. More specifically, domain adaptation is also named transductive transfer learning (Pan and Yang, 2009; Redko et al., 2020). In this paper, we concentrate on the DA problem without diving into the broader field of transfer learning. Consequently, many previous work on transfer learning are omitted for the sake of space. We direct the interested readers to the survey paper by Pan and Yang (2009) and references therein for a literature review on transfer learning. Focusing on the DA problem, we first review existing theoretical frameworks of DA and then provide an overview of DA methods and algorithms.

Theoretical DA frameworks:

The DA problem is ill-posed if one does not specify any assumptions on the relationship between the source and target data distribution. For this reason, depending on how this relationship is specified, many ways to formulate the DA problem have been introduced.

Ben-David et al. (2007) were the first to provide a DA prediction performance bound via Vapnik-Chervonenkis (VC) theory for classifiers from a generic hypothesis class. Since this bound is obtained without making explicit assumptions on the relationship between the source and target data distribution, it involves a divergence term that characterizes the closeness of the source and target distribution. A follow-up from Ben-David et al. (2010) further formally proves the necessity of assuming similarity between source and target distribution to ensure learnability. Ben-David et al.’s work laid the foundation of many further studies that attempt to bound the target and source prediction performance difference via divergence measures (Mansour et al., 2009; Cortes and Mohri, 2011, 2014; Cortes et al., 2015; Hoffman et al., 2018). See also the survey paper by Redko et al. (2020) for a complete review of VC-theory-type DA prediction performance bounds.

One natural way to explicitly relate the source and target data distribution is to assume that both of them are generated via the same well-specified generative model and to treat the missing target label problem as a missing data problem. Given a well-specified probabilistic generative model, the problem of imputing the missing data is well-studied and it is commonly solved via the expectation maximization (EM) algorithm (see McLachlan and Krishnan, 2007). This idea of casting a DA problem to a missing data problem has been introduced in Amini and Gallinari (2003) and Nigam et al. (2006).

It is also possible to loosely relate the source and target data distribution by assuming that they differ only by a small amount. How to specify this “small amount” depends on applications. If one assumes that the source data distribution is contaminated so that it is total variation distance away from the target data distribution, then the problem goes back to the classical robust statistics literature (Huber, 1964; Yuan et al., 2019). More recently, Wasserstein distance or -divergence have been considered to describe the difference between source and target data distribution. These work and contributions are referred to as distributional robust learning (Sinha et al., 2018; Duchi and Namkoong, 2018; Gao et al., 2017). A closely related line of work directly assumes that target data points can be interpreted as source data points contaminated with arbitrary small additive noise quantified via norm constraints ( or ). This direction is called adversarial machine learning (Goodfellow et al., 2018; Raghunathan et al., 2018).

Another way to make the DA problem tractable is to assume that the conditional distribution is invariant across source and target data, where and denote the response (label) and covariates, respectively. The only difference between source and target distributions comes from the change in the distribution of the covariates . This type of assumption is called the covariate shift assumption (Quionero-Candela et al., 2009; Sugiyama and Kawanabe, 2012; Storkey, 2009). Alternatively, assuming the other conditional distribution distribution to be invariant is also plausible in certain applications. This approach has a similar name called the label shift assumption (Lipton et al., 2018; Azizzadenesheli et al., 2019; Garg et al., 2020).

Finally on the causality side, it has been pointed out by Pearl and Bareinboim (2014) that full specification of a structural causal model (SCM) allows to study transportability of learning methods on the relationship between variables in the structural causal model. We refer to this approach as full-SCM transfer learning. The full-SCM transfer learning approach is very powerful in describing many data generation models. However, the main drawback of this framework is that the full specification of the structural causal model might be difficult to learn in many applications with limited data. On the other hand, the pioneering work by Schölkopf et al. (2012) reveals that distinguishing between the causal and anticausal prediction may already be useful to facilitate the selection of DA and semi-supervised learning methods. Figuring out the right amount of causal information needed to carry out DA is one of our main motivations in this paper.

Previous DA methods:

While it is in general helpful to have theoretical DA frameworks to relate the source and target data, theory is not essential for the development of new DA methods. A large number of DA methods and algorithms were introduced with the focus of addressing DA for specific datasets. Here we highlight several popular ones.

Self-training (Amini and Gallinari, 2003) is one of the earliest DA methods which is originated in the semi-supervised learning literature (see the book by Chapelle et al., 2009). The self-training algorithm begins with an estimator trained on the source data, and gradually labels a part of unlabeled target data and then updates the estimator with appropriate regularization after combining newly labeled target data. It has been shown to have good empirical performance on several computer vision domain adaptation tasks with small labeled source datasets (Xie et al., 2020; Carmon et al., 2019). A theoretical analysis of the performance of self-training under a gradual shift assumption on Gaussian mixture data was recently provided by Kumar et al. (2020).

An important line of DA methods relate the source and target data by assuming the existence of a common subspace. Pan et al. (2010) first came up with the idea of projecting the source and target data onto a reproducing kernel Hilbert space to preserve common properties and applied the idea to text classification datasets. The existence of an intermediate subspace that relates source and target data was made precise in Gopalan et al. (2011) for visual objection recognition datasets. This method was further developed and analyzed for sentiment analysis and web-page classification (Blitzer et al., 2011; Gong et al., 2012; Muandet et al., 2013). Baktashmotlagh et al. (2013) simplified the idea of enforcing a common subspace to adding a regularization term based on the maximum mean discrepancy (MMD) (Gretton et al., 2012). Their method is named domain invariant projection (DIP) because the regularization term enforces a projection of the source and target data on the subspace to be invariant in distribution. Recently, with the development of deep neural networks and the introduction of generative adversarial nets based distributional distance measures, the common subspace approach was further extended to allow for neural network implementations (Ganin et al., 2016; Peng et al., 2019).

The empirical success of DIP like DA methods and their neural network variants such as in Ganin et al. (2016) has sparked a wide discussion on the general validity of these methods. Zhao et al. (2019) constructed a simple counterexample showing that domain invariant projection is not sufficient to guarantee successful domain adaptation. Furthermore, Zhao et al. (2019) provided a lower bound of the target error when the label distribution is perturbed. Johansson et al. (2019) illustrated via a simple example the danger of the blind use of distributional distance such as MMD for domain invariant penalization. Li et al. (2019) and Tachet des Combes et al. (2020) discussed the failure of DIP in the presence of target label perturbation and proposed label shift correction using conditional invariant features. However, it is not clear whether their proposed algorithms have any guarantees for estimating the conditional invariant features or achieving low target error. The mixed messages about the success and failure of DIP like DA methods motivate us to set up rigorous target error comparisons of DIP and other DA methods.

Another line of DA methods that is worth mentioning is the one that only makes use of source data. Gong et al. (2016) introduced conditional transferable components which consist of features that are have invariant distributions given the label. The search of conditional transferable components is achieved via a penalty that matches the conditional distribution for any label across source environments. A related idea was proposed by Heinze-Deml and Meinshausen (2021). They extract the conditionally invariant (or core) components (CICs) across data points that share the same identifier but have different style features. The invariance is enforced via adding a conditional variance penalty to the training loss. Enforcing the conditional invariance allows them to learn models that are robust across perturbed computer vision datasets. Later, other concepts of invariance beyond conditional invariance across source environments were developed, such as invariant risk minimization (Arjovsky et al., 2019). It should be noted that, though with a different focus, the idea of using the heterogeneity across multiple source datasets to learn invariant or robust models has also appeared in the causal inference literature (Peters et al., 2016; Meinshausen, 2018; Rothenhäusler et al., 2021). Based on these ideas, Rojas-Carulla et al. (2018) and Magliacane et al. (2018) provided guarantees for domain adaptation under the assumption that the conditional distribution of the label given some subset of covariates is invariant.

There are many other interesting DA methods that are less related to our work. For the sake of space, we direct the interested readers to the book by Chapelle et al. (2009) on semi-supervised learning and other surveys (Zhu, 2005; Wilson and Cook, 2020; Wang and Deng, 2018) for additional references.

3 Preliminaries and problem setup

In this section, we first provide a brief summary of structural causal models, which are essential components of our theoretical framework. Then we formalize our domain adaptation problem setup and introduce the DA methods we study. Finally, we provide three simple motivating examples to illustrate the need of a DA theory.

3.1 Background on structural causal models

Structural causal models (SCMs) (see Pearl, 2000) are introduced to describe causal relationships between variables in a system. A SCM integrates the structural equation models (SEMs) used in economics and social sciences, the potential-outcome framework of Neyman (1923) and Rubin (1974), and the graphical models developed for probabilistic reasoning and causal analysis. A SCM can be seen as a set of generative equations that describe not only the data generation process of the observational data, but also that of the intervention data. We refer the readers to Chapter 7 of the book by Pearl (2000) for a detailed description of SCM for causal inference. In the context of DA, SCMs can be used to describe both the data generation process of the source and target domains (or environments). The SCMs are specified via a set of structural equations with a corresponding causal graph to describe the relationship between variables.

While SCMs are very powerful tools to describe data generation processes in interventional environments, fully specifying a SCM for a DA problem has two main drawbacks in practice: first, defining the functional forms that relate variables in a SCM can be difficult for data involving many variables; second, even if the functional forms are specified, learning all the functions from data may result in a more complicated statistical learning task than the original DA problem. Focusing on solving DA problems, the way we address the two main drawbacks differentiates our work from the full-SCM transfer learning approach by Pearl and Bareinboim (2014).

To address the first drawback and to ease our theoretical analysis, we adopt a simplification that replaces all the functional models in the SCM with linear models as in previous work (Peters et al., 2016; Rothenhäusler et al., 2021, 2019). We call this simplified SCM a linear SCM. The simplification allows us to develop rigorous DA theory and to study more complicated DA problems as extensions of the linear case. Regarding the second drawback, we focus on DA methods that can be applied without relying on the full specification of the SCM. Only when we analyze the performance of these DA methods, we bring in SCMs to set forth the assumptions needed for the DA methods to have low target errors.

3.2 Domain adaptation problem setup

In this subsection, we set up the domain adaptation problem with () labeled source environments and one unlabeled target environment. Although SCMs are general enough to also handle classification problems, we focus our theory on regression to simplify the presentation. Later in Section 5, we show the adaptation of our results to the classification setting through numerical experiments.

For the -th source environment (), we observe i.i.d. samples drawn from the source data distribution , with for each . The -th dataset is also called the -th source environment. Furthermore, there are i.i.d. samples from the target distribution , but we only observe the covariates from . Here is used to denote the marginal distribution of on . The goal of the DA problem is to estimate a function , mapping covariates to the label, parametrized by so that the target population risk is “small”. Here the parameter space is a subset of a finite-dimensional space. The performance metric target population risk for an estimator is defined as

| (1) |

where is a loss function and it is set to the squared loss function if not specified otherwise. Similarly, we can define the -th source population risk as

| (2) |

In addition to the risk on an absolute scale, one can quantify the target population risk achieved by an arbitrary estimator on a relative scale by comparing it with the oracle target population risk , where is defined as

If we don’t assume any relationship between the source distribution and the target distribution , the target population risk of an estimator learned from the source and unlabeled target data can be arbitrarily larger than the oracle target population risk. Assumptions on the relationship between source and target distribution are needed to make the DA problem tractable. In this work, we consider the DA setting where source and target data are both generated through similar linear SCMs with additional structural assumptions on the interventions.

Domain adaptation under linear SCM with noise interventions:

For , the data distribution of the -th source environment is specified by the following data generation equations on from ,

| (3) |

and the target data distribution is specified via the same equation except for the noise distribution,

| (4) |

Here is an unknown constant matrix with zero diagonal such that is invertible, and are unknown constant vectors; and are dimensional random vectors drawn from the same noise distribution ; is a fixed function to model the change (or intervention) across source and target environments; is an unknown (random or non-random) intervention that changes from one environment to another. Note that the assumption on the invertibility of ensures the uniqueness of the data generation given a draw of the noise . This assumption is in general weaker than requiring the corresponding causal graph to be directed acyclic (Rothenhäusler et al., 2019).

The only difference between the source and target data distribution is due to the difference in intervention and . According to the SCM, the way we specify the difference between source and target distribution is through the term . This type of intervention is often called noise intervention or soft intervention (Eberhardt and Scheines, 2007; Peters et al., 2016). As a concrete example, if the mean shift noise intervention is considered, then we specify the function as , and define the intervention term with a deterministic vector in d+1. As another example, if the variance shift noise intervention is considered, then we specify as , where is the element-wise product. We focus our theoretical results on the mean shift noise intervention. Other types of noise interventions are discussed in numerical experiments. The linear SCM with noise interventions clearly does not cover all kinds of perturbations to the data. For example, our theory does not apply when the matrix is no longer invariant across source and target environments. We show via numerical experiments that assuming that the perturbations are due to noise interventions is plausible in many settings.

3.3 Oracle and baseline DA methods

As we aim to compare existing and new DA methods rigorously under our theoretical framework, it is useful to start with several estimators to establish the basis of comparison.

First, we introduce two oracle estimators. They are defined using the unobserved information such as target labels or SCM parameters.

-

•

OLSTar: the population ordinary least squares (OLS) estimator on the target data.

(5) This is the oracle target population estimator when we restrict the function class to be linear. Hence the target risk of OLSTar defines the lowest target risk that any linear DA estimator can achieve.

-

•

Causal: the population causal estimator via the linear SCM

(6) where appeared in the last row of the SCM matrix in Equation (3). Note that this formulation of the causal estimator assumes that there is no intervention on and the intercept is also zero. The Causal estimator is closely related to distributional robust estimators. That is, the Causal estimator is the robust estimator which achieves the minimum worse-case risk when the perturbations on the covariates are allowed to be arbitrary (Bühlmann, 2020). However, in our DA setting where observed target covariates provide additional information, it is no longer clear whether Causal still achieves the lowest target risk.

Second, we introduce two population estimators that only use the source data.

-

•

OLSSrc: the population OLS estimator on the single -th source environment.

(7) -

•

SrcPool: the population OLS estimator by pooling all source data together.

(8) where is the uniform mixture over source distributions . We omitted the SrcPool formulation with weighted mixtures because it is not the main focus of our study.

These two estimators are natural estimators in the classical statistical learning setting when the source and target data share the same distribution. A DA method that has larger target risk than SrcPool is clearly unfavorable. One goal throughout our paper is to understand under which conditions DA methods are guaranteed to outperform OLSSrc and SrcPool.

3.4 Advanced DA methods

In this subsection, we introduce three advanced DA methods. The first two have been introduced previously and the third one is our new DA method.

First, we consider the DA method called domain invariant projection (DIP). DIP is a subspace-based DA method which aims at learning a common intermediate subspace that relates the source and target domains. The specific form of DIP we study follows from Baktashmotlagh et al. (2013). Specifically, the population DIP estimator involves the following optimization problem

| (9) |

where measures the distance between two distribution, and are function classes that are specified through expert knowledge of the problem and is a positive regularization parameter. DIP, in its simple form, only uses a single source environment. Hence, without loss of generality, we used the first source data environment.

In Baktashmotlagh et al. (2013), maximum mean discrepancy (MMD) is used as the distributional distance measure and both and are set to be linear mappings. This DIP idea of matching the mappings of source and target data is extended later in many DA papers with various choices of distance and function classes (see e.g. Ghifary et al., 2016; Li et al., 2018). A noteworthy line of follow-up work consist of replacing the distribution distance and function classes in DIP with neural networks. For example, Ganin et al. (2016) introduced domain-adversarial neural network (DANN) which uses generative adversarial nets (GAN) in place of MMD to measure distributional distance and makes both and to be neural networks.

Analyzing the most generic form of DIP is out of the scope of this study. Instead, we start with a simple DIP formulation.

-

•

DIP-mean: the population DIP estimator where mean squared difference is used as distributional distance, is linear and is the singleton of the identity mapping and is chosen to be . DIP, in its simple form, only uses the data from one source environment and the target covariates. This form of DIP is defined as

(10) For simplicity, we use the shorthand notation DIP to refer to DIP-mean. The constraint in Equation (• ‣ 3.4) is called the DIP matching penalty.

Second, we introduce the conditional invariant penalty (CIP) estimator. Unlike DIP which projects the source and target covariates to the same subspace, CIP directly uses the label information in multiple source environments to look for the conditionally invariant components. CIP only makes use of source data.

-

•

CIP-mean: the population conditional invariance penalty (CIP) estimator where the conditional mean is matched across multiple source environments.

(11) where the equality between the conditional expectation is in the sense of almost sure equality of random variables. Note that CIP naturally requires , because when the CIP constraint becomes vacuous. For simplicity, we use the shorthand notation CIP to refer to CIP-mean.

CIP puts more regression weights on the conditionally invariant components from multiple source datasets via the conditional invariance constraint in Equation (• ‣ 3.4). The idea of conditional invariance penalty in the context of anticausal learning has appeared in multiple papers with slightly different settings. Gong et al. (2016) introduced conditional transferable components which are in fact conditionally invariant features. However, unlike the formulation above, Gong et al. (2016) propose to learn the conditional transferable components with only one source environment which requires assumptions that are difficult to check. On the other hand, the algorithm from Heinze-Deml and Meinshausen (2021) learns the conditionally invariant features from a single source dataset if multiple observations of data points that share the same identifier are present. They use their conditional variance penalty to enforce their algorithm to learn the conditionally invariant features in their specific datasets with identifiers. The same idea can be applied if we replace identifiers with source environments.

Third, we introduce our new DA estimator conditional invariant residual matching (CIRM).

-

•

CIRM-mean: the population conditional invariant residual matching estimator that uses all source environments to compute CIP and the -th source environment to perform risk minimization.

(12) where

(13) with denoting the uniform mixture of all source distributions. For simplicity, we use the shorthand notation CIRM to refer to CIRM-mean.

At first glance, the CIRM estimator is a combination of DIP and CIP. CIRM first uses CIP to compute a linear combination of conditionally invariant components to serve as a proxy of the label . To tackle the label distribution perturbation, CIRM then performs the DIP-type matching on the residual obtained by regressing on its proxy. We can show that the joint distribution of the residual together with the covariates do not suffer from the label distribution perturbation. CIRM is designed to be applied in DA scenarios with label distribution perturbation. Note that the idea of using domain-invariant features to tackle label distribution shift was proposed previously in Li et al. (2019) and in Tachet des Combes et al. (2020), while it was not clear how to formulate the exact algorithm so that its success and failure conditions can be analyzed. The intuition behind the CIRM construction becomes clearer after we state Theorem 5.

3.5 Simple motivating examples

Before we dive into theoretical comparisons of the DA methods, we go through three simple examples to illustrate the assumptions needed for DA methods to have low target risks. The simple examples have data generated via low-dimensional SCMs so that the DA estimators can be easily computed and understood.

3.5.1 Example 1: causal prediction

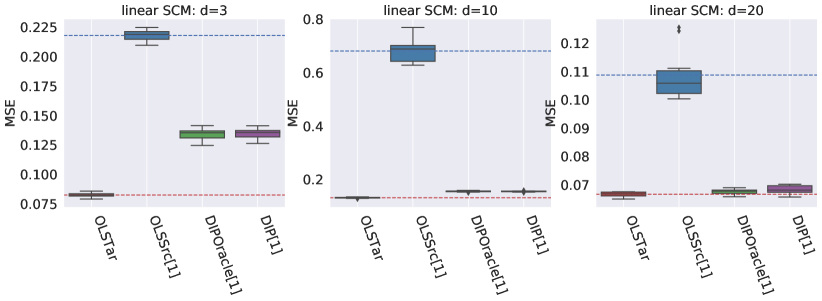

Example 1 has one source environment and one target environment. The data in the source and target environment are generated independently according to the following SCMs, with the causal diagram on the left and the structural equations on the right of Figure 2.

Here the noise variables follow independent Gaussian distributions with mean zero and variance for and variance for , namely, , . The type of intervention is mean shift noise intervention. That is, the function in Equation (3) is taken to be . The intervention is for the source environment and it is for the target environment. This example is called causal prediction, because the covariates are parents of the label . In other words, we are predicting the effect from the causes as illustrated in the causal diagram in Figure 2.

Given the source and target distribution, the population DA estimators in the previous subsection can be computed explicitly. We obtain

Note that OLSSrc, Causal and OLSTar share the same estimate , while DIP does not. The corresponding population source and target risks are summarized in the first two rows of Table 1. DIP has a larger target population risk than OLSSrc. In this example of causal prediction, using the additional target covariate information via DIP is making the target prediction performance worse. This is because DIP matching penalty in Equation (• ‣ 3.4) which is not satisfied by the oracle estimator OLSTar, makes DIP too restrictive.

| OLSTar (oracle) | Causal | OLSSrc | DIP | DIPAbs | |

|---|---|---|---|---|---|

| Ex 1, source risk | 0.200 | 0.200 | 0.200 | 0.333 | - |

| Ex 1, target risk | 0.200 | 0.200 | 0.200 | 16.333 | - |

| Ex 2, source risk | 2.600 | 0.200 | 0.040 | 0.086 | 0.044 |

| Ex 2, target risk | 0.040 | 0.200 | 2.600 | 0.086 | 0.667 |

| Ex 3, source risk | 0.200 | 0.200 | 0.040 | 0.066 | - |

| Ex 3, target risk | 0.040 | 1.200 | 0.200 | 4.066 | - |

3.5.2 Example 2: anticausal prediction

Example 2 has one source environment and one target environment. The data in the source and target environment are generated independently according to the following SCMs, with the causal diagram on the left and the structural equations on the right of Figure 3.

Here the noise variables follow independent Gaussian distributions with mean zero and variance for and variance for , namely, , The type of intervention is mean shift noise intervention, which is the same as in Example 1. The intervention is for the source environment and it is for the target environment. Compared to Example 1, the main difference is that the causal direction between the covariates and the label has changed. This example is called anticausal prediction, because the covariates are descendants of the label . We are predicting the cause from the effects as illustrated in the causal diagram in Figure 3.

In addition to the DA estimators used in the previous example, we introduce one more variant of DIP, DIPAbs. It is a made-up estimator to show that arbitrary choice of the function classes in DIP formulation (3.4) without consideration on the data generation process is in general a bad idea.

-

•

DIPAbs-mean: the population DIP estimator where mean squared difference is used as distributional distance, is element-wise absolute value followed linear mapping and is singleton of identity mapping and regularization parameter is chosen to be . For the -th source environment, it is defined as

(14)

The population estimators can be computed explicitly

For the other four estimators, none of the estimated perfectly agrees with that of the oracle OLSTar. The corresponding population source and target risks are summarized in the third and fourth rows of Table 1. DIP improves upon Causal and OLSSrc on the target population risk. However its target population risk is not as small as that of the oracle estimator OLSTar. DIPAbs also uses the target covariate information as DIP does, but DIPAbs performs worse than Causal or DIP in terms of target population risk.

3.5.3 Example 3: anticausal prediction when Y is intervened on

Example 3 is also an anticausal prediction problem similar to Example 2, except that the label is also intervened on. The data in the source and target environment are generated independently according to the following SCMs, with the causal diagram on the left and the structural equations on the right of Figure 4.

Here the noise variables follow independent Gaussian distributions with , , . The type of intervention is still mean shift noise intervention. The intervention is for the source environment and it is for the target environment. Compared to Example 2, the main difference is that the intervention on is nonzero as illustrated in the causal diagram in Figure 4.

The population estimators can be computed explicitly

Note that DIP has zero weight on the first coordinate but non-zero weight on the second because and share the same distribution. The corresponding population source and target risks are summarized in the last two rows of Table 1. In Example 3 when is intervened on, DIP is again worse than OLSSrc on the target population risk.

3.5.4 Lessons from the simple motivating examples

The three simple motivating examples reveal three observations. First, even though DIP has a low target risk in the anticausal prediction setting (Example 2), DIP is not likely to outperform OLSSrc in the causal prediction setting (Example 1). The fact that the additional target covariate information is not useful in causal prediction problem was previously pointed out by Schölkopf et al. (2012). Consequently, DIP-type methods (Baktashmotlagh et al., 2013; Ganin et al., 2016) which make use of the additional target covariate information can make target performance worse in causal prediction problems. Second, not all DIP variants have low target risks in the anticausal prediction setting. DIPAbs, despite using the target covariate information as DIP does, performs worse than Causal and DIP. In general, it is dangerous to treat DA methods as generic solutions that always work without consideration on the data generation process. We remark that DIPAbs is a made-up method. But one could imagine a case where the first part in DIP is set to be a neural network that can approximate a large class of functions, then it is no longer clear the DIP matching penalty that matches the source and target covariate distributions always helps to improve the target population risk. This danger of learning blindly invariant representations was pointed out previously via a simple nonlinear data generation model by Zhao et al. (2019). Third, when is intervened on, DIP can perform worse than OLSSrc. Actually, none of the DA methods in Table 1 can handle the intervention on well. The weakness of DIP in the presence of label perturbation has been observed previously in Zhao et al. (2019); Li et al. (2019); Tachet des Combes et al. (2020). Especially, Tachet des Combes et al. (2020) proposed the idea of using conditional invariant components for label shift correction. However, since their proposed method has no guarantees for estimating the conditional invariant components, it is not clear whether their methods have any guarantees for correcting the label shift.

The three examples are designed to demonstrate that the popular DA method DIP does not always outperform baseline methods such as OLSSrc or Causal. Besides, it also shows that the assumption of both source and data being generated from linear SCMs is not sufficient to guarantee DIP to have a low target risk. Additional assumptions on the data generation or on the intervention are needed. For example, knowing the causal direction of the data generation model or whether the label distribution is perturbed are all crucial information. Based on these examples, we ask the following questions:

-

1.

In addition to the linear SCM assumption, what other assumptions are needed for DIP to perform better than Causal or OLSSrc? If such assumptions exist, can one quantify the gap between the target risk achieved by DIP and the oracle target risk?

-

2.

If there is label distribution perturbation like in Example 3, are there DA methods that can outperform OLSSrc and have target risk guarantees?

-

3.

If the prediction direction is a mix of causal and anticausal, is domain adaptation still beneficial?

In the sequel, we address these questions one by one. The first question is addressed in Section 4.1. The second question is dealt with in Section 4.2 via the introduction of CIP and CIRM. The general solution to the third question remains open. Naive applications of DIP and CIRM are not optimal. We provide a partial answer to the third question in Section 4.3 and show that the mixed-causal anticausal DA problem can be reduced to the anticausal DA problem when the causal variables have been already identified.

4 Domain adaptation with theoretical guarantees

In this section, to answer the three questions in the last section with rigor, we establish target risk guarantees for the DA estimators DIP, CIP and CIRM in three settings. Subsection 4.1 focuses on the DIP performance in the anticausal DA setting without intervention on . Subsection 4.2 demonstrates the difficulty of DIP in the anticausal DA setting with interventions on and then proves the advantage of CIP and CIRM over DIP when multiple source environments are available. Subsection 4.3 shows how domain adaptation is still possible in the mixed causal anticausal DA setting.

4.1 Anticausal domain adaptation without intervention on Y

In this subsection, we study the anticausal domain adaptation with the additional assumption that the intervention on the covariates is a mean shift noise intervention and there is no intervention on the label . In the anticausal domain adaptation, all the covariates are descendants of the label in the SCM. First, we derive the target risk bound for DIP under these assumptions with a single source environment. Then we show how to make use of more source environments to improve the performance of DIP. Finally, we discuss ways to relax the mean shift noise intervention assumption.

4.1.1 Target risk guarantees of DIP with a single source environment

Before we state the main theorem, we introduce another oracle estimator to simplify the theorem statement. DIPOracle minimizes the mean squared error on target data while it uses the same matching penalty as DIP.

-

•

DIPOracle-mean: the population DIP estimator which uses target labels and the covariate distribution from the -th source and target environment.

(15)

Next, we state the data generating assumptions needed for DIP to have target risk guarantees. Since a single source environment is considered in this subsection, without loss of generality, we assume that the first source environment is used.

Assumption 1

Each data point in the source environment is generated i.i.d. according to distribution specified by the following SCM

each data point in the target environment is generated i.i.d. according to distribution specified with the same SCM except for the mean shift intervention term

where is invertible, the prediction problem is anticausal i.e. , , the intervention terms and are vectors in d+1, the noise terms and share the same distribution with

Additionally, the noise terms on and are uncorrelated .

Note that Assumption 1 does not require to be diagonal, meaning that the noise terms of can be correlated. Consequently, this assumption allows for unobserved confounders affecting the variables to exist. Under the assumptions above and that there is no intervention on , we obtain the following theorem on the target risk of DIP.

Theorem 1

Under the data generation Assumption 1 and the assumption of no intervention on i.e. , the target population risks of OLSTar, OLSSrc and DIP-mean satisfy

| (16) | ||||

| (17) | ||||

| (18) |

where is a projection matrix with rank ; is a matrix with columns formed by the vectors that complete the vector to an orthonormal basis. Here when the source and target distribution is not identical i.e. . When , meaning that the source distribution equals the target distribution, then and we have .

The proof of Theorem 1 is provided in Appendix B.1. Comparing Equation (18) with Equation (16), the target population risk of DIP is larger than that of OLSTar but it is lower than the target population risk of the Causal estimator (which equals to ). The target population risk of OLSSrc depends on the magnitude of the difference in intervention , while the target risk of DIP is independent of that magnitude. Consequently when the difference in intervention becomes large, DIP can outperform OLSSrc. Moreover, the first equality of Equation (18) shows that DIP achieves the same target population risk as DIPOracle. DIPOracle differs from OLSTar by only one linear constraint. The connection between DIP and DIPOracle intuitively explains why DIP target risk should be close to that of OLSTar.

In fact, with additional assumptions on how the interventions and are positioned and simplifications on the covariance matrix , we obtain the following corollary which clearly highlights the difference between the target population risk of DIP and the oracle target population risk of OSLTar.

Corollary 2

In addition to the assumptions in Theorem 1, suppose with , then

| (19) | ||||

| (20) | ||||

| (21) |

where if and otherwise.

Additionally, if is generated randomly from the Gaussian distribution , then for a constant satisfying , with probability at least , we have

| (22) |

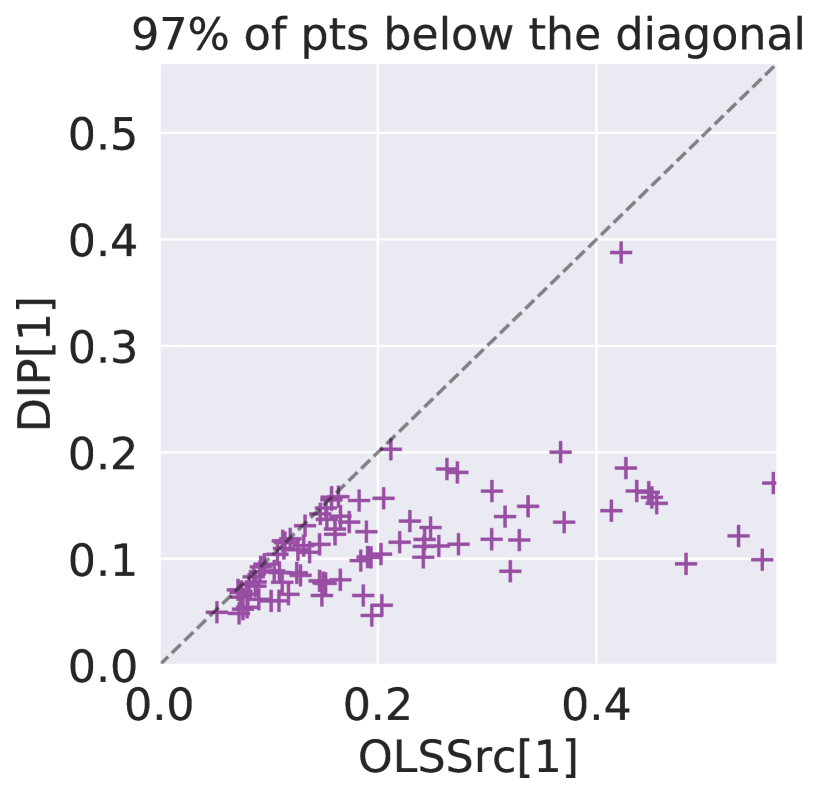

The proof of Corollary 2 is provided in Appendix B.2. Under the conditions of Corollary 2, Equation (21) shows that the gap between the target population risks of DIP and OLSTar is smaller when the direction of the difference in intervention becomes less aligned with the vector . When the intervention is generated randomly from a Gaussian distribution, the bound (2) shows that the gap between the target population risks of DIP and OLSTar is small with high probability. The gap only comes from an order term in the denominator of the target risk. So when the dimension is large, this difference in target population risk between DIP and OLSTar becomes negligible. As for OLSSrc, it is now clear from Corollary 2 that the target risk of OLSSrc depends on the magnitude of the difference in intervention . For brevity, we only provided the target risk upper bound of OLSSrc. The lower bound should hold similarly up to constant factors because the risks are derived with equality in Equation (20)-(21) and tight Gaussian concentration bounds are used to obtain the upper bounds. As the magnitude of the difference in intervention increases, OLSSrc will eventually have a larger target risk than DIP.

The intuition behind the success of DIP over OLSSrc is that the DIP matching penalty in Equation (• ‣ 3.4) allows the DIP estimator to equalize the source and target covariate intervention by projecting it to a common space. As a result, given the DIP matching penalty, computing least squares on the source data is the same as computing least squares on the target data. This observation also explains why the target risk of DIP matches that of DIPOracle. Having this intuition in mind, it is not hard to imagine extending the guarantees of DIP to the generic form of DIP in Equation (3.4) under appropriate assumptions. Specifically, under Assumption 1, as long as the function class is chosen such that the DIP matching penalty ensures the conditionals and to have the same distribution, then no matter how is chosen we always match the target risks of DIP and DIPOracle. Moreover, we know that target risk of DIPOracle is close to the oracle target risk over the function class . So the target risk of DIP in this extended setting is also close to the oracle one.

4.1.2 Benefit of more source environments for DIP

We show how to make use of more independent source environments to improve the performance of DIP. Here we consider () source environments, where for each the -th source environment is generated independently according to the source environment in Assumption 1 except for the unknown interventions and we still have . First, we state a corollary revealing that it is possible to pick the best source environment for DIP based on the best source risk. Second, we discuss the reason behind the performance improvement after picking the best source environment.

First, based on the proof of Theorem 1, we derive the following corollary on the source population risk.

Corollary 3

The proof of Corollary 3 is provided in Appendix B.3. According to Corollary 3, one can read off the target population risk directly from the source population risk. Since the choice of source environment 1 is arbitrary, the same result holds for any of the source environments. We have for any . Consequently, having more source environments allows one to apply DIP between each source environment and the target environment one by one, and then pick the estimator with the lowest source population risk to reduce the target population risk.

Second, we reason about the type of source environments that reduces the target population risk the most. According to Equation (16) and (18) in Theorem 1, the projection matrix is the term that makes the target population risks of DIP and DIP different (). If the vector is in the span of the projection matrix , then DIP achieves the oracle target population risk. Otherwise, the target population risk of DIP depends on the norm of the component of outside the span of the projection matrix .

The above intuition becomes clearer under the additional assumptions of Corollary 2. There we obtain a simple form for the projection matrix , where assuming . Under the same assumptions, the denominator in the DIP target risk in Equation (18) becomes . If is orthogonal to then DIP achieves the oracle target population risk. Otherwise, DIP has larger target population risk than OLSTar. With more source environments, it is more likely to find a source environment such that is closer to be orthogonal to .

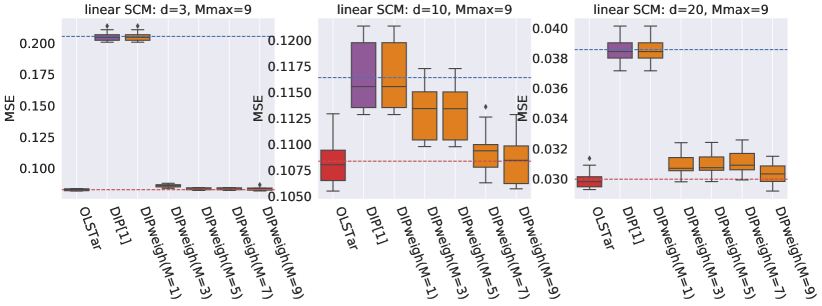

Based on the above intuition, we propose the following DIP variant that provides a weighting choice to take advantage of multiple source environments.

-

•

DIPweigh-mean: the population DIP estimator that makes use of multiple source environments based on the source risks.

(24) is a constant. Choosing to be is equivalent to choosing the source estimator with the lowest source risk. DIPweigh weights all the source predictions based on the source risk of each source environment.

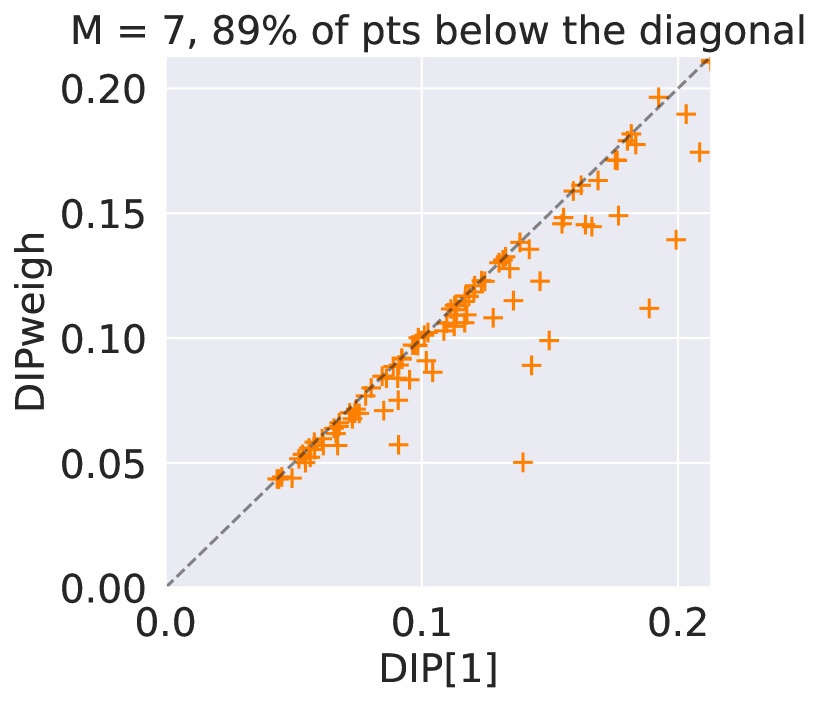

Here we introduce the weighted version of DIP rather than directly selecting the source estimator with the lowest source risk. The main intuition is that in finite sample, averaging the predictions from several source environments with low source risks can take advantage of a larger sample size. For example, in the presence of a less related source environment with very large sample size, one might still include it if the reduction in variance outweighs the increase in bias.

4.1.3 Failure scenarios of DIP

The target population risk guarantees of DIP in Theorem 1 rely on the anticausal data generation Assumption 1 and the assumption of no intervention on . We already showed in Example 1 that DIP cannot outperform OLSSrc in the causal prediction setting. Even in the anticausal prediction setting, we identify two scenarios where DIP-mean might have large target risk: when the DIP matching penalty is not well-suited for the underlying type of the intervention that generates the data and when there is intervention on .

Consider the following data generation model where the source environment is generated from the following SCM with interventions on the variance

and the target environment is generated from the same SCM except that the intervention on takes the form . Here denotes the -dimensional element-wise multiplication. This intervention is called variance shift noise intervention. The intervention term and are fixed vectors in d, and the noise terms are kept the same as in Assumption 1. Under the data generation model in this subsection, the matching penalty in DIP-mean (• ‣ 3.4) is always satisfied because both the left and right hand sides are zero. Consequently, DIP-mean becomes the same estimator as OLSSrc. Matching the mean between source and target distribution in this case is no longer a good idea, because the intervention is on the variance rather than the mean.

To adapt to the new type of intervention, one can consider DIP-std which puts the matching penalty on the standard deviations, DIP-std+ which puts the matching penalty on the means, standard deviations and 25% quantiles, or DIP-MMD which uses more generic distributional matching via MMD. The exact formulations consist of replacing the DIP mean matching penalty in Equation (• ‣ 3.4) with the appropriate matching penalties and they are formally introduced in Appendix A.1.

If the assumptions are set up such that the intervention type agrees with the matching penalty in DIP, analyzing the theoretical performance of DIP-std, DIP-std+ or DIP-MMD under linear SCMs works similarly as analyzing that of DIP-mean. Hence we leave out the theoretical guarantees of DIP-std, DIP-std+ or DIP-MMD for brevity. The empirical performance of DIP-std+ and DIP-MMD is shown through simulations and real data experiments in Section 5.

The second failure scenario of DIP is when there is intervention on . This failure scenario of DIP is already noticeable from Example 3 in Section 3.5.3. Here we provide a corollary that quantifies the additional target population risk made by DIP if there is intervention on .

Corollary 4

Under the data generation Assumption 1, the target population risk of OLSTar and DIP-mean satisfy

| (25) |

where is a projection matrix with rank . is a matrix with columns formed by the vectors that complete the vector to an orthonormal basis.

The proof of Corollary 4 is provided in Appendix B.3. According to Equation (4) in Corollary 4, the target population risk has an extra term that depends on the difference between target and source intervention. The target population risk of DIP is increases as the difference between target and source intervention increases. This corollary highlights the result that DIP has a large target risk when the intervention on is large.

4.2 Anticausal domain adaptation with intervention on Y

In this subsection, we study the anticausal domain adaptation where there is intervention on the label . As illustrated in Example 3 in Section 3.5.3 and in the last section, the intervention on can cause DIP to have a large target population risk. In fact, allowing arbitrary intervention on both and can also lead to unidentifiable cases where two data generation models result in the same target covariate distribution in the anticausal domain adaptation. If it were the case, any DA estimator based solely on the target covariate distribution will have large target risk. The following example illustrates one concrete unidentifiable case.

A simple unidentifiable example:

The target data is generated form the following SCM

where is -dimensional random variable, and . Assume we observe the target covariate distribution . Without observing the target label distribution, it is impossible to tell whether the intervention is , or . This is because all three interventions result in the same target covariate distribution. However, the conditional distribution are different. Consequently, any estimator of the conditional mean without access to the target label distribution can not get it correct.

To make the anticausal domain adaptation problem with intervention on tractable, additional assumptions on the structure of the interventions is needed. Here we adopt one type of assumptions introduced by Gong et al. (2016); Heinze-Deml and Meinshausen (2021). This line of work assumes the existence of conditionally invariant components (CICs) across all source and target environments. That is, there exists an unknown transformation of the covariates such that the conditional distribution is invariant across source and target environments.

In the following, we first prove target population risk guarantees for CIP and CIRM under the conditionally invariant components assumption. We show that the CIP and CIRM target risks are much less dependent on the intervention than the DIP target risk. Finally we discuss extensions and variants of CIP and CIRM.

4.2.1 Target risk guarantees of CIP and CIRM with multiple source environments and conditionally invariant components

We start by stating the data generation assumptions for CIP and CIRM to have target risk guarantees, namely a SCM and the existence of conditionally invariant components.

Assumption 2

There are () source environments. Each data point in the -th source environment is generated i.i.d. according to distribution specified by the following SCM

Each data point in the target environment is generated i.i.d. according to distribution specified with the same SCM except for the mean shift intervention term

where is invertible, the prediction problem is anticausal , the intervention term and are vectors in d+1, the noise term and share the same distribution with

In addition, the noise terms on and are uncorrelated . The interventions do not span the whole space (to ensure the existence of conditionally invariant components)

| (26) |

and the target intervention is in the span of source interventions

| (27) |

Compared to Assumption 1, Assumption 2 involves multiple source environments instead of one. Also, the way the source and target environments are generated up to Equation (26) is the same as in Assumption 1. Equation (26) assumes that the interventions do not span the whole covariate space d. It ensures the existence of a invariant linear projection of the covariates given the label . More precisely, this assumption allows us to find a vector which is orthogonal to the and the projection of the covariates has the same intervention term across source environments. This particular linear projection of the covariates becomes one conditionally invariant component. To make sure the same conditionally invariant component is also valid in the target environment, Equation (27) requires that the target intervention is in the span of source interventions.

Given the data generation assumption above, we have the following theorem on the target risk of CIP and CIRM.

Theorem 5

Under the data generation Assumption 2, the population target risks of CIP-mean and CIRM-mean for any satisfy

| (28) | ||||

| (29) | ||||

| (30) |

where , . is a projection matrix with rank where is a matrix with columns formed by an orthonormal basis of the orthogonal complement of . is a projection matrix defined in the same way as in Theorem 1.

The proof of Theorem 5 is provided in Appendix C.1. Comparing the target population risk of CIRM in Equation (30) with that of DIP in Equation (4), CIRM reduces the dependency on the difference in intervention . This is because we always have . The target population risk of CIRM when there is intervention on in Equation (30) has an additional term depending on when compared to that of DIP when there is no intervention on in Equation (18). The additional term becomes close to zero when is large.

In fact, without additional assumptions to Assumption 2, the dependence on or similar terms is unavoidable for any DA estimator. Because the Assumption 2 does not prevent from being in the , it can still result in a slightly unidentifiable example similar to the one presented at the beginning of Section 4.2. See Appendix D for ways to get rid of the dependence at the cost of small additional target risk.

In the same spirit of Corollary 2, we present a corollary that puts additional assumptions on the positions of the interventions and to make the results in Theorem 5 easier to understand.

Corollary 6

In addition to Assumption 2, suppose with , then

| (31) | ||||

| (32) | ||||

| (33) |

where , , is the matrix with columns formed by the orthonormal basis of and . Additionally, if are generated independently from Gaussian distribution and , , a constant , then with probability at least , we have and additionally

| (34) | ||||

| (35) | ||||

| (36) |

The proof of Corollary 6 is provided in Appendix C.2. Under the assumptions of Corollary 6, it is clear that for and sufficiently large, with high probability, CIRM has smaller target population risk than CIP when all interventions are equal . This is because the last term in Equation (32) become zero can be ignored and when . Intuitively, CIP only uses the conditionally invariant components (roughly coordinates) to build the estimator, while CIRM takes advantage of the other coordinates of (roughly coordinates).

The intuition behind CIRM becomes apparent after the theorem statement. CIRM is indeed a combination of DIP and CIP: it applies CIP in the first step to obtain the conditionally invariant component which serves as a proxy of the label to correct for the intervention on , then it applies DIP with the corrected target covariate distribution to improve the target prediction performance. The conditionally invariant components identified by CIP are useful to constitute a proxy of but they alone do not predict very well especially when there are only a few of them. DIP has good target risk guarantees when there is no intervention. When there is intervention, CIRM uses CIP to correct for the distribution perturbation and to create a residual which does not suffer from intervention, then apply DIP on the residual.

Since CIRM can be seen as applying DIP on the label-distribution-corrected source and target data, it is natural to introduce a weighted version of CIRM called CIRMweigh similar to DIPweigh (• ‣ 4.1.2). A precise formulation of CIRMweigh can be found in Appendix A.1.

Under the assumptions of Corollary 6, we summarize the target risk upper bounds of all DA methods in this paper in Table 2. For brevity, we only present the target population risk upper bounds under high probability when the interventions are generated i.i.d. Gaussian . The upper bounds are tight up to constant factors in the denominators because we first proved the exact target risks with equality and then applied Gaussian concentration to obtain the upper bounds. Consequently, the upper bounds serve the comparison purpose.

| Estimator | Target population risk upper bound interventions under general position | |

|---|---|---|

| OLSTar (oracle) | ||

| No intervention on (Corollary 2) | OLSSrc | |

| DIP | ||

| DIP | ||

| Intervention on with CICs sources (Corollary 6) | CIP | |

| CIRM |

4.2.2 On relaxing the assumptions needed for CIP and CIRM

We discuss two different relaxations of Assumption 2.

First, the two assumptions (26) and (27) in Assumption 2 can be replaced by a single assumption, namely there exists a non-zero vector such that and all have the same distribution. This is also equivalent to saying that the projection of the covariates on the direction is a conditionally invariant component. Stating the CIC assumption as we did in Assumption 2 has the advantage of separating the assumptions on the source interventions from those on the target intervention.

When the dimension is larger than the number of source environments , the assumption (26) on the dimension of the span of the source interventions is always satisfied. In the case of , the more source environments there are, the more likely that the target intervention is in the span of the source interventions.

Second, the mean shift noise intervention in Assumption 2 can be relaxed to other types of noise interventions. For example, the noise intervention can be the standard deviation shift as we did for DIP in Section 4.1.3. We may consider CIP-std which puts the conditional invariance penalty on the standard deviations, CIP-std+ which puts the conditional invariance penalty on the means, standard deviations and quantiles or CIP-MMD which uses generic distributional matching to make sure the conditional distribution of is invariant across source environments. CIRM can be extended similarly. We do not provide theoretical guarantees of these extensions and we only show their empirical performance through simulation and data experiments in Section 5.

4.3 Mixed-causal-anticausal domain adaptation

In this subsection, we consider the mixed-causal-anticausal DA setting where both causal and anticausal variables are present. In terms of the SCMs, neither the vector nor in Equation (3) is assumed to be zero. In terms of the graph associated with the SCM, some variables are descendants of the label and some variables are ancestors of . As we have seen in Example 1 and Example 2 in Section 3.5, DA methods such as DIP perform worse than Causal or OLSSrc in the causal setting, while DIP can have smaller target population risk than Causal or OLSSrc in the anticausal setting. When both causal and anticausal variables are present, it is no longer clear whether more sophisticated DA methods would be better than Causal or OLSSrc. To gain some intuition, we first show a simple mixed-causal-anticausal DA example to illustrate how the standard DIP, CIP and CIRM can have worse target risk than Causal. Then we introduce new algorithms to tackle the mixed-causal-anticausal DA problem.

4.3.1 A mixed-causal-anticausal DA example to illustrate the failure of the standard DIP, CIP and CIRM

Here we provide a simple mixed-causal-anticausal DA problem to illustrate the difficulty of the mixed-causal-anticausal setting. Example 4 is a DA problem with a large number of source environments () and one target environment. The data in the source and target environment are generated independently according to the following SCMs, with the causal diagram on the left and the structural equations on the right of Figure 5.

Here the noise variables follow independent Gaussian distributions with , . The noise variable of is set to zero. The type of intervention is mean shift noise intervention. The variable is never intervened on, so is conditionally invariant. For the first source environment, the intervention . For , where each coordinate is generated i.i.d. from and we ensure that the interventions span a subspace of dimension 3. For the target environment, the intervention is . Compared to Example 3, the inclusion of the causal covariates and makes the DA problem more complicated.

The population estimators when tends to can be computed explicitly

Note that with a large number of source environments, CIP and SrcPool both identify the conditional invariant component . The Causal estimator is the best because we made the noise variable on to be and the intervention on in the target to be 0. DIP does not find the Causal estimator because the intervention makes it difficult to align the covariate interventions between source and target. CIRM does not find the Causal estimator because even if it can correct for the label intervention, matching on the causal covariate is not a good idea due to similar reason we have seen applying DIP for causal prediction in Example 1. The corresponding population source and target risks are summarize in Table 3. We conclude that unlike in the anticausal DA setting, in the presence of both causal and anticausal covariates, CIRM which is based on the idea of domain invariant projection after label correction no longer outperforms SrcPool.

| OLSTar (oracle) | Causal | SrcPool | DIP | CIP | CIRM | |

|---|---|---|---|---|---|---|

| Ex 4, source risk | 1.000 | 1.000 | 0.100 | 0.000 | 0.100 | 0.000 |

| Ex 4, target risk | 0.000 | 0.000 | 0.100 | 4.000 | 0.100 | 1.000 |

One might argue that the superior performance of Causal over SrcPool is made up because we set the target label intervention to be zero. The concern is valid in general. However, it is not difficult to observe that no matter how we set there exist better estimators than SrcPool. In fact, if we know is the only causal variable, we can regress on and consider the prediction problem on the residuals. The resulting prediction problem is anticausal with intervention on . Consequently, it can be solved with DA methods discussed in Section 4.2. We formulate this idea precisely in the next subsection.

4.3.2 New DA methods for mixed-causal-anticausal domain adaptation

Instead of studying the most general mixed-causal-anticausal domain adaptation, we first restrict ourselves to the setting where the “rough causal structure around ” is known. That is, we know which covariates are the descendants of , denoted as , and we also know which covariates are the parents of or the parents of (denoted as ) as shown in Figure 6. Assuming the “rough causal structure”, we show that this mixed-causal-anticausal problem can be reduced to the familiar problem in the previous subsections. Assumption 3 makes data generation requirements precise.

Assumption 3

There are () source environments. Each data point in the -th source environment is generated i.i.d. according to distribution specified by the following SCM

Each data point in the target environment is generated i.i.d. according to distribution specified with the same SCM except for the mean shift intervention term

where , and are unknown constant matrices such that is invertible, and are unknown constant vectors, the intervention terms and are vectors in d+1, the noise terms and share the same distribution with

Additionally, the noise terms on and are uncorrelated, namely, .

Compared to the SCMs in Assumption 1 and 2, Assumption 3 introduces additional covariates which are the parents of or and are located at the first coordinates. In the most general DA problem, this information of which covariates are parents may not be available. The information about causal relationships can be obtained for example from domain experts or from the causal discovery literature. The causal discovery problem is well studied and we refer the readers to Glymour et al. (2019) for a review of the causal discovery methods. We leave the most general mixed-causal-anticausal domain adaptation and the design of new DA methods to future work.

Based on Assumption 3, we can introduce the intermediate random variables

| (37) |

The intermediate random variable can be seen as the residuals after regressing on the parent variables . We observe that the intermediate random variables satisfy the following SCMs

Using the intermediate random variables , the mixed-causal-anticausal DA problem can be reduced to the anticausal DA problem. Intuitively, it works as follows. First, regress and on the first covariates . Second, create a transformed dataset with new covariates and new labels from the corresponding residuals like how we define the intermediate random variables. Third, apply the DA methods in the anticausal DA setting to the transformed dataset. Finally, bring back the original covariates and labels in the final estimator.

Based on the above intuition, we introduce the following estimators for the mixed-causal-anticausal DA setting.

-

•

DIP-mean: the population domain invariant projection estimator for the mixed-causal-anticausal DA setting.

(38) where , , and the regression weights and are defined as

(39) (40)

Corollary 7

Under the data generation Assumption 3, and the assumption of no intervention on i.e. , the target population risks of OLSTar and DIP-mean satisfy

| (41) | ||||

| (42) |

where is a projection matrix with rank .

The proof of Corollary 7 is provided in Appendix C.4. The target risk results in Corollary 7 is very similar to those in Theorem 1. This is because we reduce the mixed-causal-anticausal DA problem without intervention on under Assumption 3 to the anticausal DA problem without intervention on under Assumption 1. According to Equation (42), the target population risk of DIP is lower than the target risk of Causal (which equals to ).

Based on the intuition of DIP, a similar strategy can be applied to extend CIP and CIRM to the mixed-causal-anticausal DA problems. The precise formulations of the extensions CIP and CIRM are introduced in Appendix A.1.

Just as Corollary 7 serves as the equivalent of Theorem 1 in the mixed-causal-anticausal DA setting, the equivalent of Theorem 5 can be established for CIP and CIRM. Additionally, we can also introduce the weighted version of CIRM, called CIRMweigh, following the discussion of CIRMweigh. The details are omitted.

5 Numerical experiments

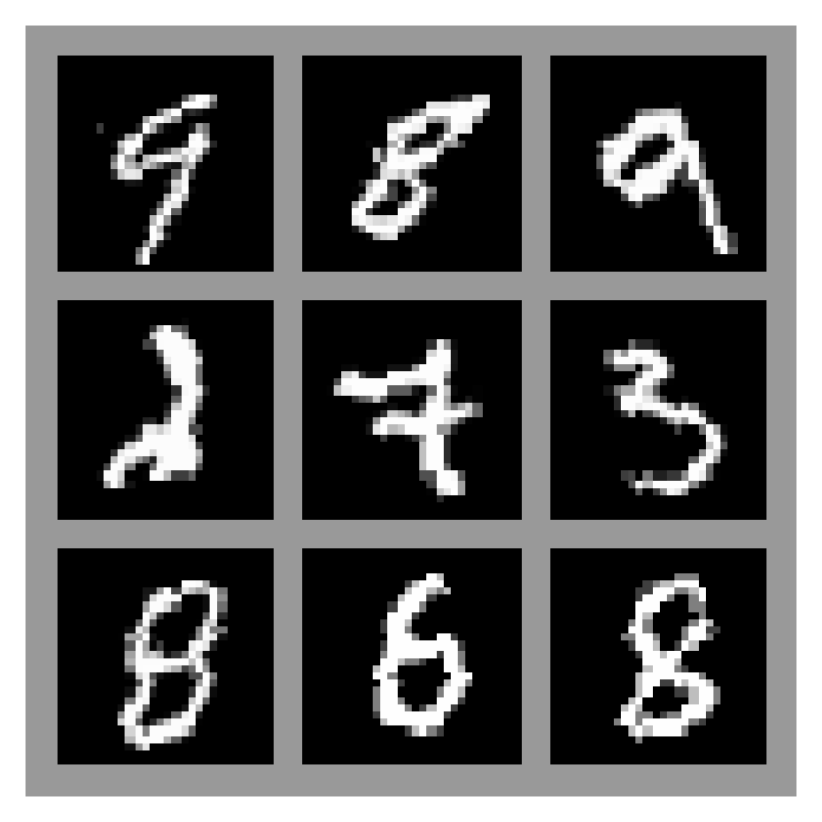

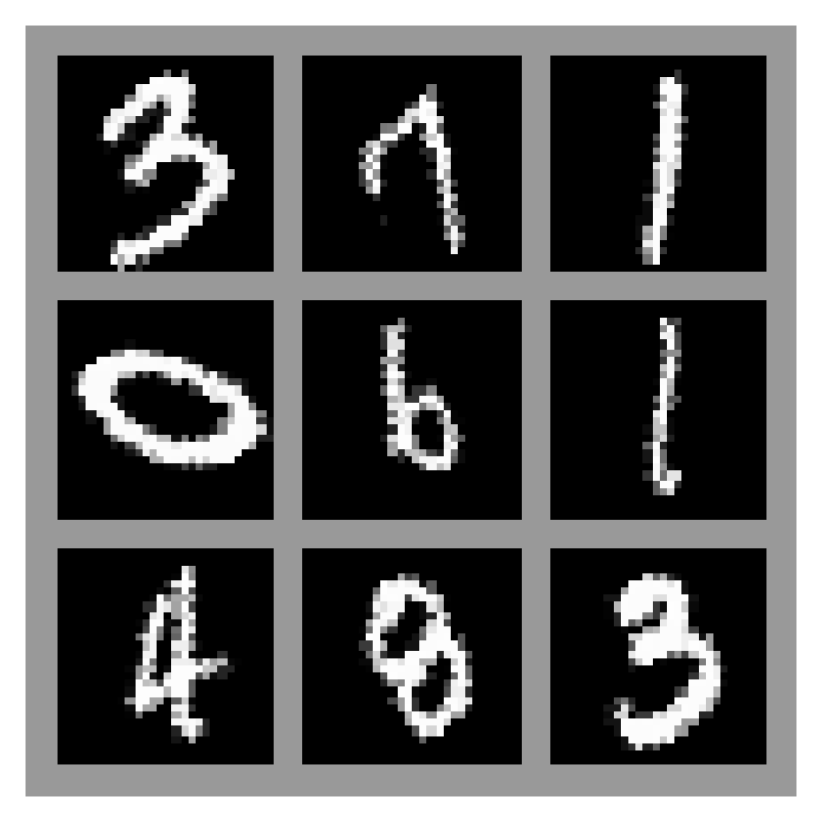

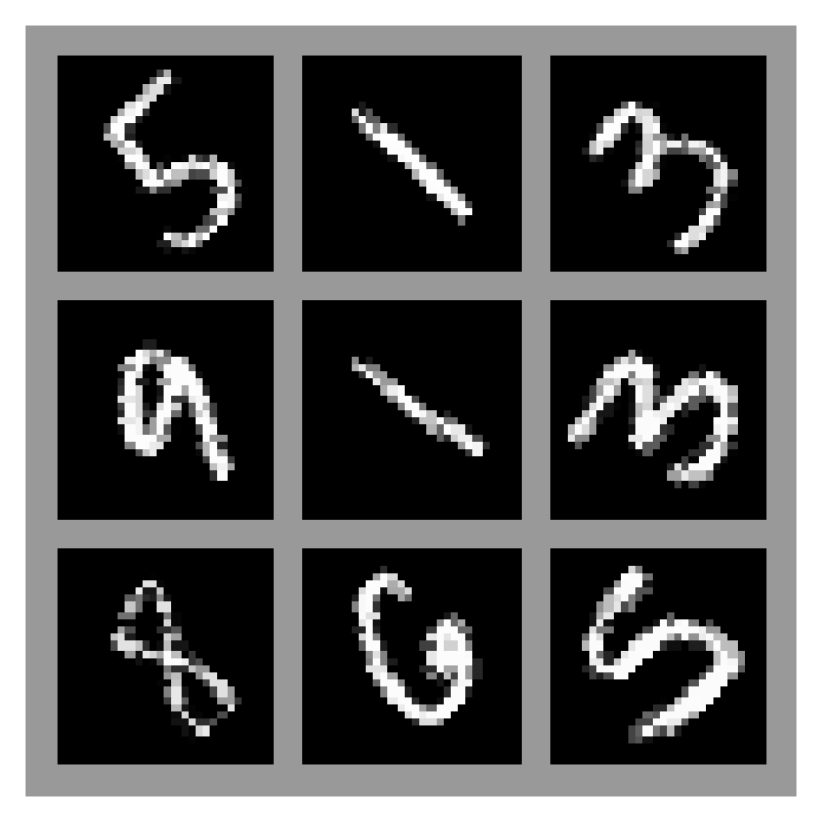

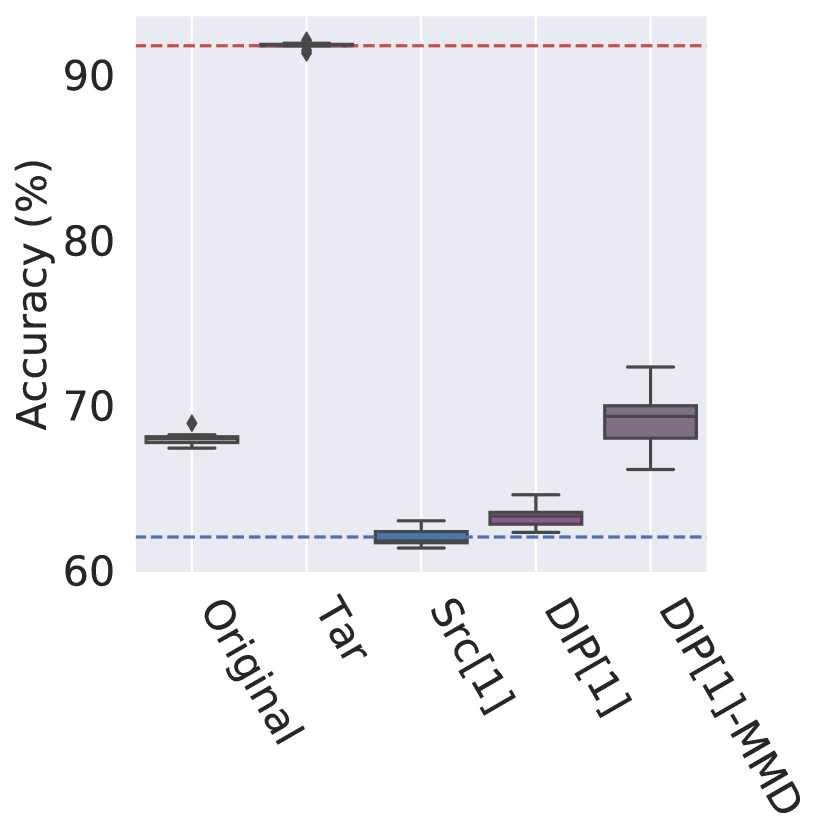

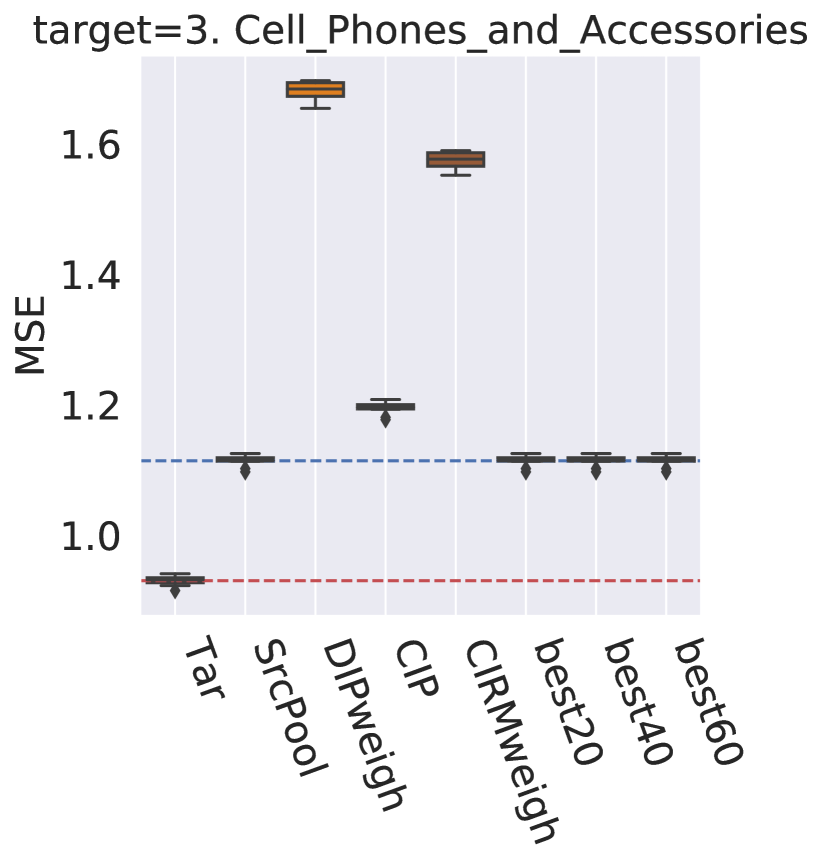

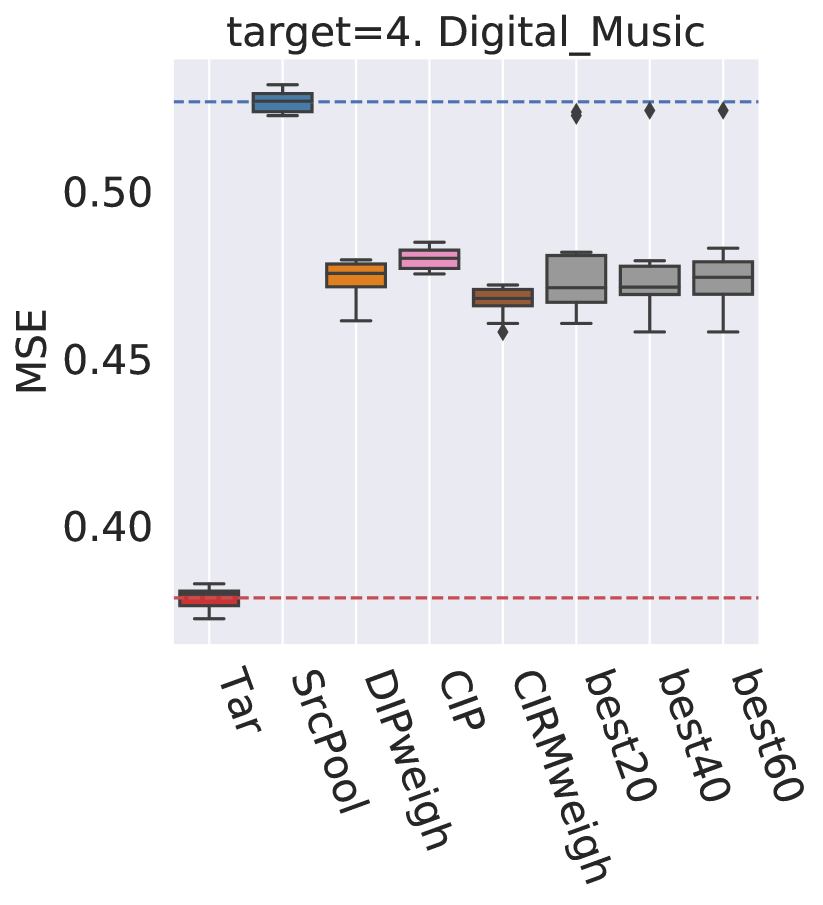

In this section, we numerically compare DA methods in simulated, synthetic and real datasets. The experiments are used to validate our theoretical results in finite sample data, to illustrate DA failure modes when assumptions are violated and to provide ideas of adapting DA methods to scenarios where not all assumptions are satisfied. Section 5.1 formulates the finite-sample DA estimators from the population DA ones to make sure our implementations are reproducible. Section 5.2 contains simulation experiments from deterministic or randomly generated linear SCMs. Section 5.3 discusses the performance of DA estimators on the MNIST dataset with synthetic interventions. Finally, Section 5.4 illustrates through a real data experiment that DA can be difficult in practice when not much domain knowledge about the data generating model is available.

Our code to reproduce all the numerical experiments is publicly available in the Github repository https://github.com/yuachen/CausalDA.

5.1 Finite-sample formulations and hyperparameter choices

Here we introduce the regularized formulations of the finite-sample DIP, CIP and CIRM. The DIP matching penalty in Equation (• ‣ 3.4) and the conditional invariance penalty in Equation (• ‣ 3.4) are enforced via regularization terms. The finite-sample versions of their variants can be formulated similarly after translating the constraints to regularization terms. For the sake of space, they are presented in Appendix A.2.

-

•

DIP-mean-finite: the finite-sample formulation of the DIP-mean estimator (• ‣ 3.4). The mean squared difference is used as distributional distance and is enforced via a regularization term,

(43) where is a positive regularization parameter that controls the match between the covariate mean of the source and target environment.

-

•

CIP-mean-finite: the finite sample formulation of the CIP-mean estimator (• ‣ 3.4). The conditional mean is matched across source environments and is enforced via a regularization term,

(44) where , and is a positive regularization parameter that controls the strength of the conditional invariant penalty. In the finite-sample formulation, the conditional expectation in the constraint of population formulation (• ‣ 3.4) is computed via regressing on . As a result, ’s are the residuals after regressing on .

-

•

CIRM-mean-finite: the finite-sample formulation of the CIRM-mean estimator (• ‣ 3.4). The residual after removing conditionally invariant components is matched between source and target environments. The matching is enforced via a regularization term.

(45) where with defined as

and is a positive regularization parameter similar to the one define in DIP. Just like the population CIRM depends on the population CIP, the finite-sample CIRM also depends on the finite-sample CIP with the same regularization parameter .

Regularization parameter choices:

Choosing the regularization parameters in finite-sample DA formulations such as in DIP formulation (• ‣ 5.1) is a difficult subject. Because the DA setting here assumes no access to any target labels, one cannot get good estimates of the target performance easily. The classical model selection strategies based on a validation set are no longer applicable in domain adaptation.

We make use of the fact that when DIP works as Theorem 1 predicts, the source population risk of DIP equals to the target population risk as shown in Corollary 3. The source finite-sample risk is close to the target finite-sample risk up to finite sample errors. So we would like to choose large enough so that the DIP matching penalty takes effect, but not too large so that the source finite risk remains reasonably small. We propose to choose the largest so that the source finite-sample risk is less than two times of the source finite-sample risk when is set to zero. The choice of “two times” is arbitrary here, the precise amount depends on the desired target finite-sample risk, the sample size and the variance of the source finite risk estimate. The precise amount is specified for each DA dataset separately. The regularization parameter in DIPweigh is chosen similarly.