Multiscale characteristics of the emerging global cryptocurrency market

Abstract

Modern financial markets are characterized by a rapid flow of information, a vast number of participants having diversified investment horizons, and multiple feedback mechanisms, which collectively lead to the emergence of complex phenomena, for example speculative bubbles or crashes. As such, they are considered as one of the most complex systems known. Numerous studies have illuminated stylized facts, also called complexity characteristics, which are observed across the vast majority of financial markets. These include the so-called “fat tails” of the returns distribution, volatility clustering, the “long memory”, strong stochasticity alongside non-linear correlations, persistence, and the effects resembling fractality and even multifractality.

The striking development of the cryptocurrency market over the last few years – from being entirely peripheral to capitalizing at the level of an intermediate-size stock exchange – provides a unique opportunity to observe its evolution in a short period. The availability of high-frequency data allows conducting advanced statistical analysis of fluctuations on cryptocurrency exchanges right from their birth up to the present day. This opens a window that allows quantifying the evolutionary changes in the complexity characteristics which accompany market emergence and maturation. The purpose of the present review, then, is to examine the properties of the cryptocurrency market and the associated phenomena. The aim is to clarify to what extent, after such an impetuous development, the characteristics of the complexity of exchange rates on the cryptocurrency market have become similar to traditional and mature markets, such as stocks, bonds, commodities or currencies.

The review introduces the history of cryptocurrencies, offering a description of the blockchain technology behind them. Differences between cryptocurrencies and the exchanges on which they are traded have been consistently shown. The central part of the review surveys the analysis of cryptocurrency price changes on various platforms. The statistical properties of the fluctuations in the cryptocurrency market have been compared to the traditional markets. With the help of the latest statistical physics methods, namely, the multifractal cross-correlation analysis and the -dependent detrended cross-correlation coefficient, the non-linear correlations and multiscale characteristics of the cryptocurrency market are analyzed. In the last part of this paper, through applying matrix and network formalisms, the co-evolution of the correlation structure among the 100 cryptocurrencies having the largest capitalization is retraced. The detailed topology of cryptocurrency network on the Binance platform from bitcoin perspective is also considered. Finally, an interesting observation on the Covid-19 pandemic impact on the cryptocurrency market is presented and discussed: recently we have witnessed a “phase transition” of the cryptocurrencies from being a hedge opportunity for the investors fleeing the traditional markets to become a part of the global market that is substantially coupled to the traditional financial instruments like the currencies, stocks, and commodities.

The main contribution is an extensive demonstration that, fuelled by the increased transaction frequency, turnover, and the number of participants, structural self-organization in the cryptocurrency markets has caused the same to attain complexity characteristics that are nearly indistinguishable from the Forex market at the level of individual time-series. However, the cross-correlations between the exchange rates on cryptocurrency platforms differ from it. The cryptocurrency market is less synchronized and the information flows more slowly, which results in more frequent arbitrage opportunities. The methodology used in the review allows the latter to be detected, and lead-lag relationships to be discovered. Hypothetically, the methods for describing correlations and hierarchical relationships between exchange rates presented in this review could be used to construct investment portfolios and reduce exposure to risk. A new investment asset class appears to be dawning, wherein the bitcoin assumes the role of the natural base currency to trade.

keywords:

Cryptocurrencies , Complexity measures , Cross-correlations , Fractals , Multiscaling , Complex networks , Lead-lag effect100

1 Introduction

Modern financial markets are characterized by a rapid flow of information. There is a huge number of transactions between market participants with different investment horizons. There are pension funds, for those time scale is years, and at the same time specialized algorithms operating at the level of seconds or even milliseconds (high-frequency trading). The market behaviour is the result of various influencing factors, ranging from economic data, results of companies, interventions of central banks, poll and referendum results, individual tweets of high-ranking people, and mutual interactions between participants. Through feedback, this leads to critical-like phenomena such as speculative bubbles or crashes. This happens often in hours or even minutes – the so-called “flash crashes”. These features undoubtedly fit into the characteristics of complex systems, such as a large number of elements, nonlinear interactions, structural self-organization, and emergent phenomena.

The first quantitative research on financial markets was the subject of Louis Bachelier’s work [1], in which he derived a formula for option price based on cumulative distribution function (CDF) of a stochastic process now called the Wiener process. Later Benoît Mandelbrot’s works turned out to be a groundbreaking achievement [2]. While examining cotton price fluctuations, he observed that, contrary to wide belief, their probability distribution function (PDF) is characterized by heavy, non-Gaussian tails. Mandelbrot was also the first to notice a fractal structure of stock price fluctuations.

More than a quarter century ago, statistical physicists started their serious research in financial markets, which led to an outburst of a new discipline – econophysics [3, 4]. Numerous studies carried out since then allowed researchers for a better understanding of the mechanisms governing various phenomena on both the macroscopic level (like speculative bubble formation, market crashes, asset cross-correlations, nonlinear autocorrelations, portfolio evolution, etc.) and the microscopic level (order book properties, efficacy of investing strategies, price formation, etc.). Along with the understanding, new models have been proposed that better describe and predict market behaviour and practical trading algorithms have been developed and applied especially in high-frequency trading.

All types of markets have been a subject of research since the beginning of econophysics: stock markets [5, 6, 7, 8], commodity markets [9, 10, 11], option and future contract markets [12, 13, 14], bond markets [15, 16, 17], real-estate markets [18, 19, 20], as well as the foreign currency market (Forex) [21, 22, 23]. Unlike typical complex systems studied by experimental physicists, these markets offer good quality data with minimum systematic errors, which is one of the reasons why so much attention they attract. However, there is an important issue that is inherently associated with all the above mentioned markets: they have already been existing for a long time before they become a subject of research. Therefore, we cannot investigate their evolution since their origin. Nevertheless, more or less a decade ago a brand new market was established – a cryptocurrency market, which offers precisely what the other markets lack – a possibility of observing their structural self-organization process from the very beginning to a rather mature form in a short period of time. A principal question is to what extent, after such dynamic development, complexity characteristics of the cryptocurrency market are similar to those of traditional markets, especially Forex.

The first cryptocurrency - Bitcoin (BTC) - was proposed in 2008 by a person or group of people under a nickname Satoshi Nakamoto [24]. The date of this new concept emergence does not seem to be accidental, because it is correlated with an epicenter of the global financial crisis of 2008-2010. In order to mitigate its effects, the central banks began to increase the monetary base (“printing money”) massively, which weakened trust in the traditional fiat currencies. The bitcoin protocol was based on a peer-to-peer network and the previously known public and private key cryptographic techniques together with a new consensus mechanism called “Proof of Work”. The idea behind bitcoin was to provide, for the first time in human history, a tool that would allow people anywhere to trust each other and carry out transactions via Internet without a central management institution. Instead of the current confidence in the state/central banks, confidence in technology was proposed.

The first widely recognized platform offering BTC-to-fiat-currency exchange was Mt. Gox founded in Feb 2011. Since then a spectacular development of the cryptocurrency market has occurred. There are already 3,600 different cryptocurrencies traded on 350 platforms with nearly 30,000 cryptocurrency pairs listed. Current capitalization of the entire market is about 350 billion USD (Oct 2020 [25]). It increased rapidly in 2017 during a speculative bubble referred to as ICO-mania [26, 27] reaching over 800 billion USD in the beginning of 2018. BTC valuation on some Korean platforms was even 20 000 USD. Currently, the market is highly decentralized with the same cryptocurrency pairs listed on many platforms. There is no single price to refer to unlike that provided by Reuters on Forex. Only for BTC there are quoted future contracts launched in Dec 2017 on the CME group [28]. Another characteristic property is that cryptocurrency transactions are most often made through the platforms in contrast to Forex with its over-the-counter market.

Aim of this work is to review the available results on the cryptocurrency market obtained with various methods of statistical physics with the multifractal formalism and the network approach in particular. Our work sketches briefly history of the cryptocurrency introduction (Sect. 2.1) and describes the blockchain technology standing behind them (Sect. 2.2), but its main part presents a review of the most important properties of the cryptocurrency price fluctuations. Price return distributions, autocorrelations, and inter-transaction times of cryptocurrency exchange rates are compared with their counterparts in Forex (Sect. 3). Non-linear auto- and cross-correlations together with multifractal-like characteristics on the cryptocurrency market are then described. Among others, it is shown that PDF/CDF form, autocorrelation functions, Hurst exponents, and multiscale properties depend on trading frequency (Sect. 4). Cross-correlations among the cryptocurrency exchange rate pairs within one trading platform and between two platforms, as well as between the cryptocurrency platforms and Forex are also discussed (Sect. 5). Triangle arbitrage effects are a subject of Sect. 5.2.3. Latest Covid-19 pandemic impact on correlations between cryptocurrencies and traditional financial markets is covered in Sect. 5.4. The last part of this review discusses results of a network approach (Sect. 6). It is shown that, currently, BTC is a natural base cryptocurrency for other cryptocurrencies.

2 The emergence and technology of cryptocurrencies

2.1 History: from barter through the blockchain

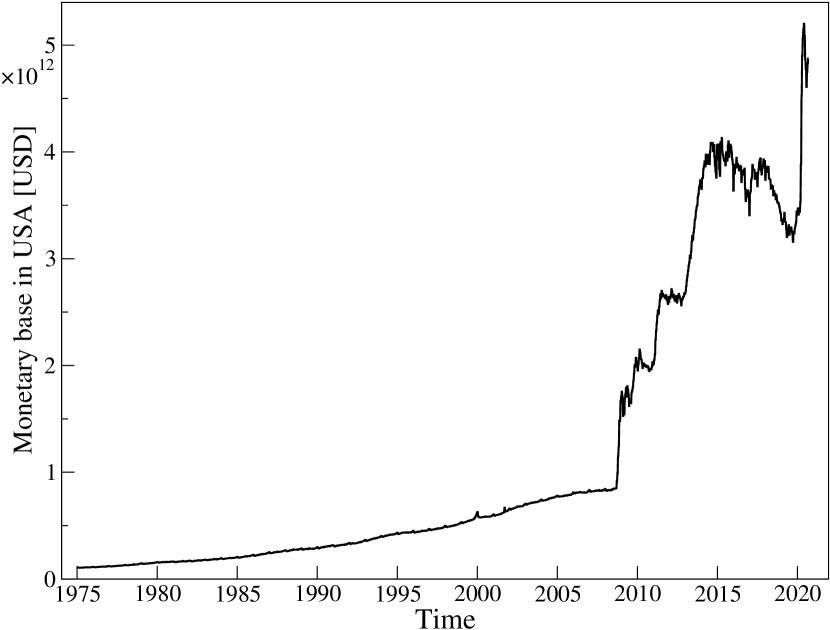

Human history has been paced by discrete events that shaped its course through discontinuously accelerating development. Without question, one of these events is the emergence of money in the form of standardized coins, which were introduced in Lydia around 600 years BC. This first generation of currency shaped Mediterranean culture in many ways [29], and spearheaded a continuous increase in trade exchanges. Merchants no longer had to resort to barter, good for good, or service for service. The second generation was paper money, which appeared in the Renaissance. It was introduced by Italian banks and subsequently taken over by the established national banks. The invention of banking and paper money disrupted the status quo of the feudal systems, by strengthening the nation-states which had the power to issue it. From this point onwards, the possibility of modulating the money supply upwards or downwards was easily available, eventually giving rise to modern capitalism [29]. The 20th century brought the appearance of electronic transactions, which further accelerated the circulation of currency throughout the economy, boosting growth. Crucially, paper and electronic money caused a total decoupling of fiat currencies from their fundamental value. After the collapse of the Bretton Woods system in 1971, exchange rates ceased to be linked to gold and based on trust in the state. From that point onwards, fiat currencies systematically lost their value, as shown for the example of the US dollar in Fig. 1. Moreover, since breaking with gold as a reference, the number of USD in circulation has kept increasing systematically, as visible in Fig. 2.

Currently, central banks can easily increase the supply of currency without any physical printing. After the financial crisis of the year 2008, all the major central banks significantly expanded their monetary base through quantitative easing programs (QE), as visualized in Fig. 2. Incidentally, around the same time, a radically new financial asset appeared. That was the first cryptocurrency, the Bitcoin [24]. The underlying revolutionary idea was to combine existing technologies in a novel way, namely asymmetric cryptography, together with a distributed database having a new “Proof of Work” consensus mechanism into a decentralized, secure register (the distributed ledger technology, DLT) blockchain [31].

The intention is that cryptocurrencies are not subjugated to any institution or government; rather, they are based on trust in technological infrastructure. They allow sending financial resources anywhere in the world with almost zero latency. The network users themselves provide the authentication mechanism. The cryptocurrency concept combines the advantages of cash, namely the transaction anonymity, with the speed and convenience of electronic transactions. Importantly, unlike traditional currencies, the Bitcoin by design has a built-in supply limitation mechanism, which helps prevent its loss of value.

Initially, the Bitcoin seemed to be only a technological curiosity, and there was no organized trade. Individual transactions for exchanging real goods via on-line discussion groups were described, such as buying two pizzas in May 2010 for 10,000 BTC [32]. However, the innovative idea soon began diffusing outside its original circle of computer geeks, extending towards the broader financial sector and, eventually, by virtue of the anonymity, also to criminal circles. The first widely recognized exchange, which enabled bitcoins to be traded for traditional currencies, Mt.Gox, was launched in July 2010. Soon after, the first on-line black market, Silk Road, was created: it allowed virtually unregulated trading of any goods, bolstered by bitcoin payment and full anonymity. Perhaps concerningly, this was the first practical application of the Bitcoin. It significantly increased demand and contributed to the first speculative bubble on bitcoin prices [26], which burst after Silk Road was shut down by the FBI in October 2013 and trading by the largest cryptocurrency exchange, Mt.Gox, was halted in February 2014, plausibly after a hack which led to the disappearance of 850,000 BTC.

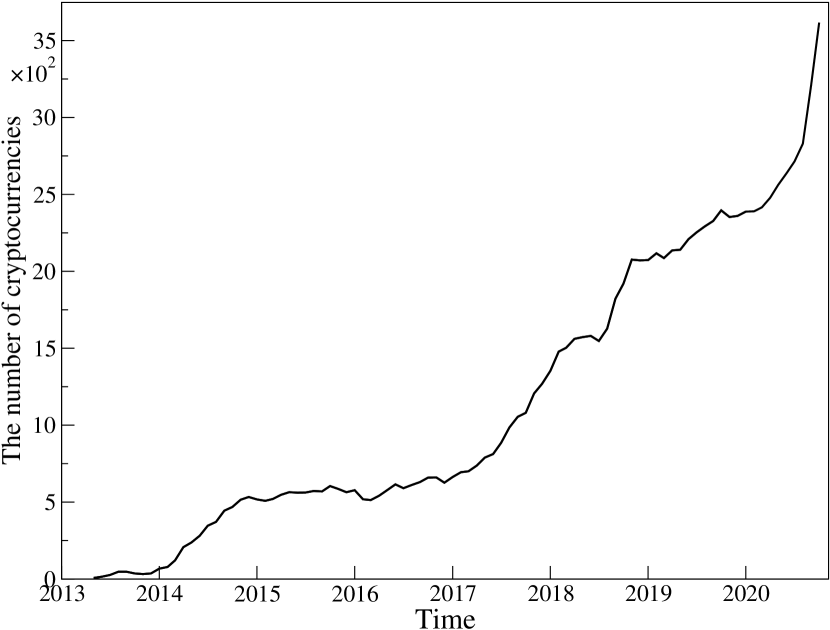

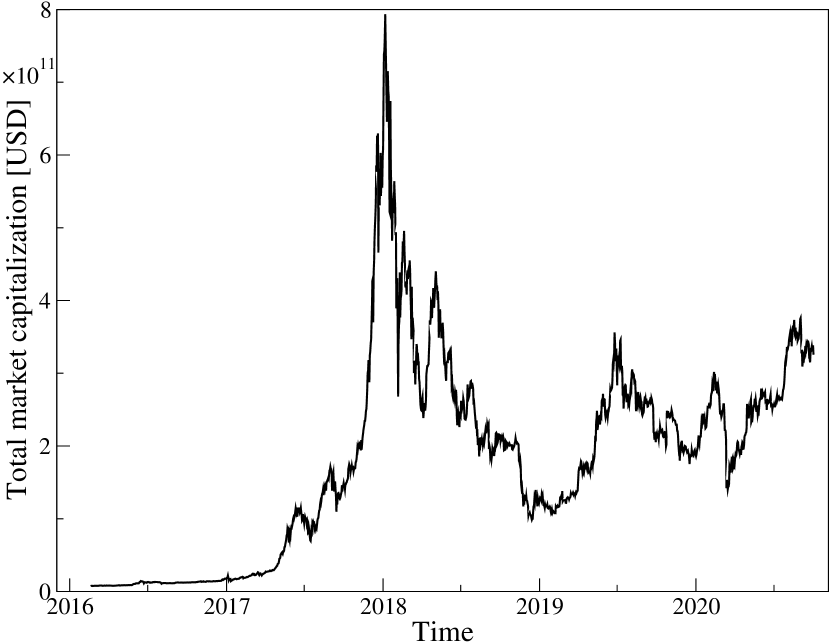

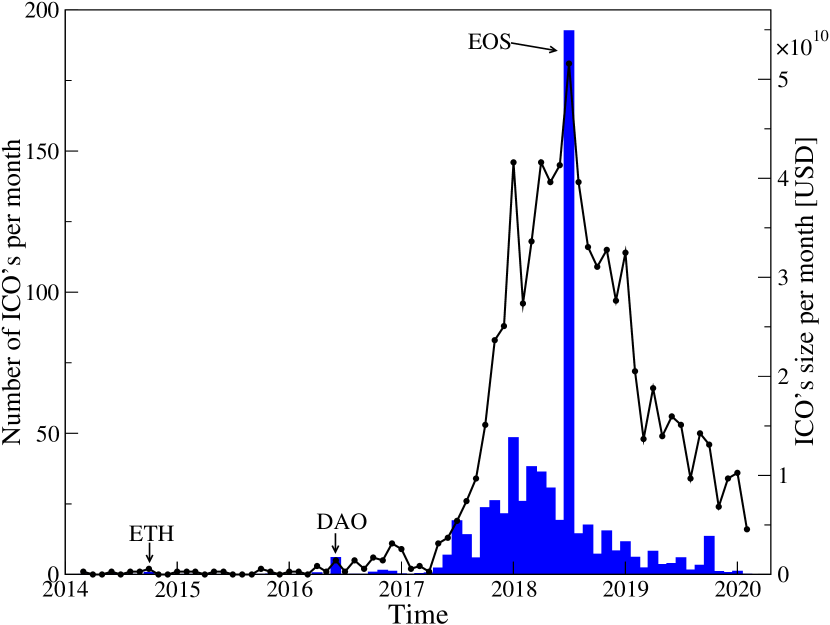

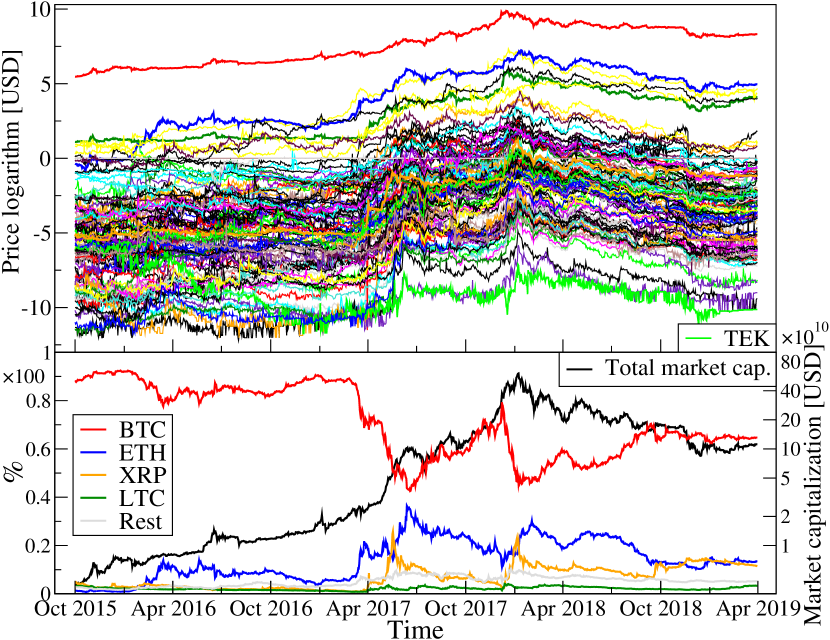

As recognition increased, the technology became increasingly widespread. Eventually, it turned out that the blockchain technology on which cryptocurrencies are based allows using for a decentralized registry not only for financial purposes but also for the execution of computer code (scripts) in a distributed form. At the end of 2013, the idea of an Ethereum distributed computing network was introduced. The project started in July 2015 [33]. The Ethereum platform allows anyone to create decentralized applications operating without the possibility of downtime, censorship, fraud, or tampering with their code. It also allows one to issue their own tokens via smart contracts, which consist of computer code performing a prescribed action under certain conditions on the Ethereum blockchain. This innovation quickly found application in raising capital via a simplified mechanism for various projects through the so-called Initial Coin Offer (ICO). In 2017, the ICO underwent a boom, which contributed to another speculative bubble on the cryptocurrency market, referred to as the ICO-mania [27]. At that time, the number of cryptocurrencies doubled from 700 to 1,400 by the end of 2017 (figure 4), and the capitalization of the entire market reached USD 800 billion (figure 5). Unavoidably, the bubble eventually burst in January 2018.

The current state of the blockchain technology can be compared to the dot-com bubble at the turn of the century. The considerable potential was already visible in the then possibilities of the Internet, but it was not known precisely which particular way the technology would develop. At that time, merely mention a company’s intention to engage in Internet-related activities would cause a sharp increase in share price [34]. A similar case was verified for the cryptocurrencies. With the first euphoric phase now well over, the bitcoin from top to bottom in December 2018 lost over 80 percent of its value (figure 3). Other cryptocurrencies have dropped by as much as 99 percent, with some unavoidably succumbing. Currently, the first practical applications of the blockchain are emerging; these will be discussed alongside the mechanics of cryptocurrencies in the next sections.

2.2 Core technology

The most straightforward approach for dispatching “electronic cash” would be using data files. However, digital data can inherently be replicated unlimitedly, which engenders a double-spending problem. Therefore, there was a need for a technology that could form an electronic register covering all transactions: transferring funds would, then, consist of swapping entries in the register. This type of record is commonplace in the electronic banking system, but central to the notion of a cryptocurrency was the aim of abandoning their central character, rendering them completely public instead. In this way, each user could verify transactions independently, yielding another valuable property, namely the impossibility of corrupting the registry history. This challenge was resolved through the use of peer-to-peer (P2P) networks, cryptographic techniques, and connecting transactions in blocks, and after that in a chain of blocks, the blockchain. In this section, without losing generality, the underlying technology will be presented, taking as an example the first cryptocurrency, the Bitcoin.

2.2.1 The network

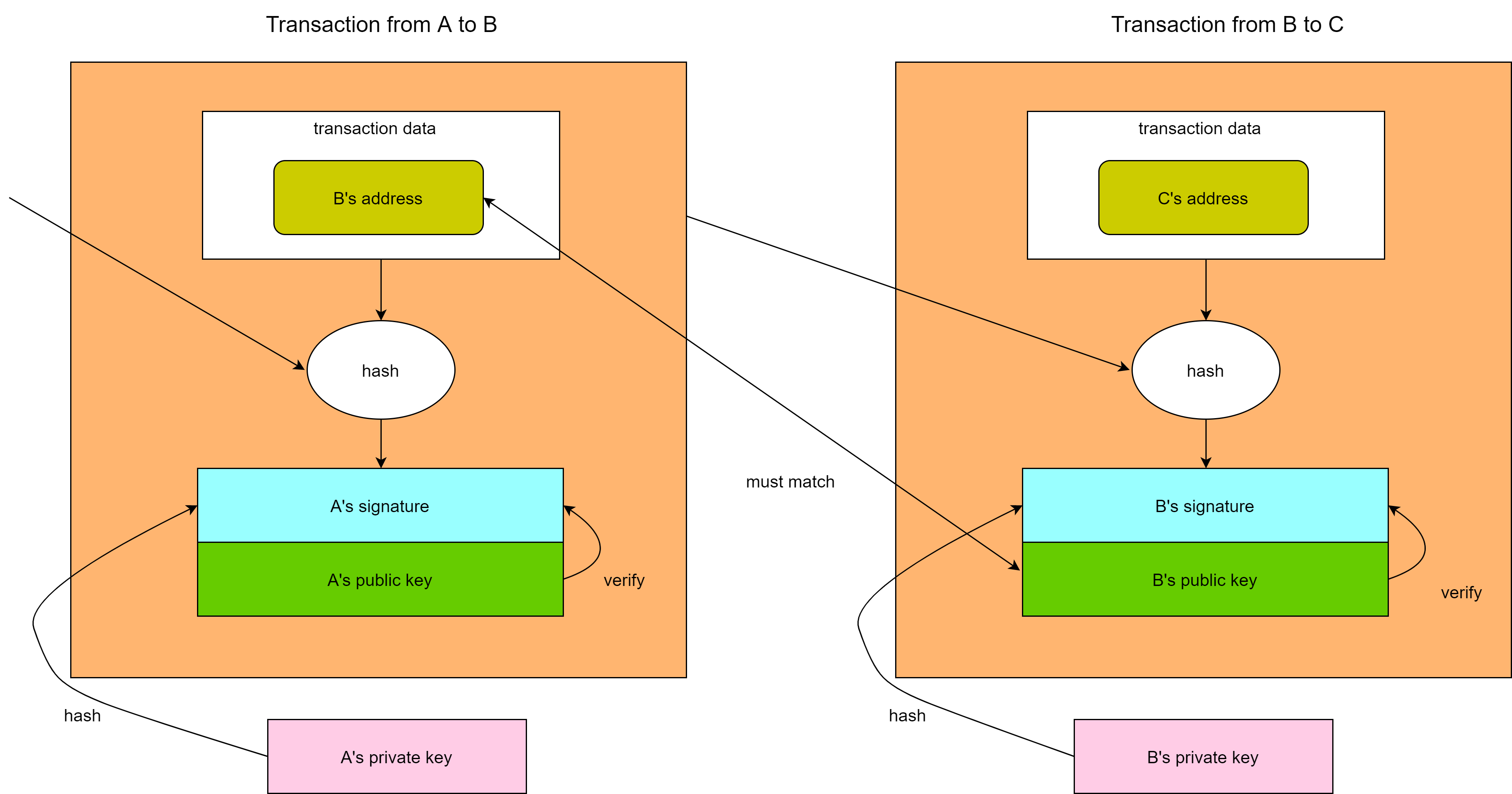

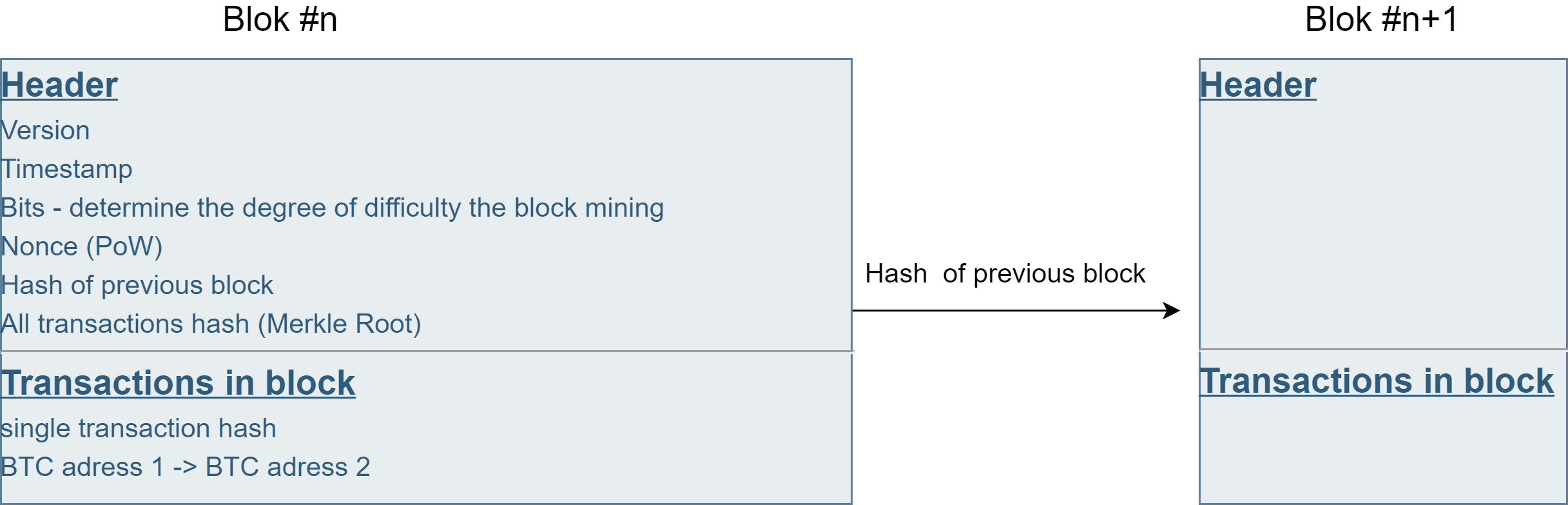

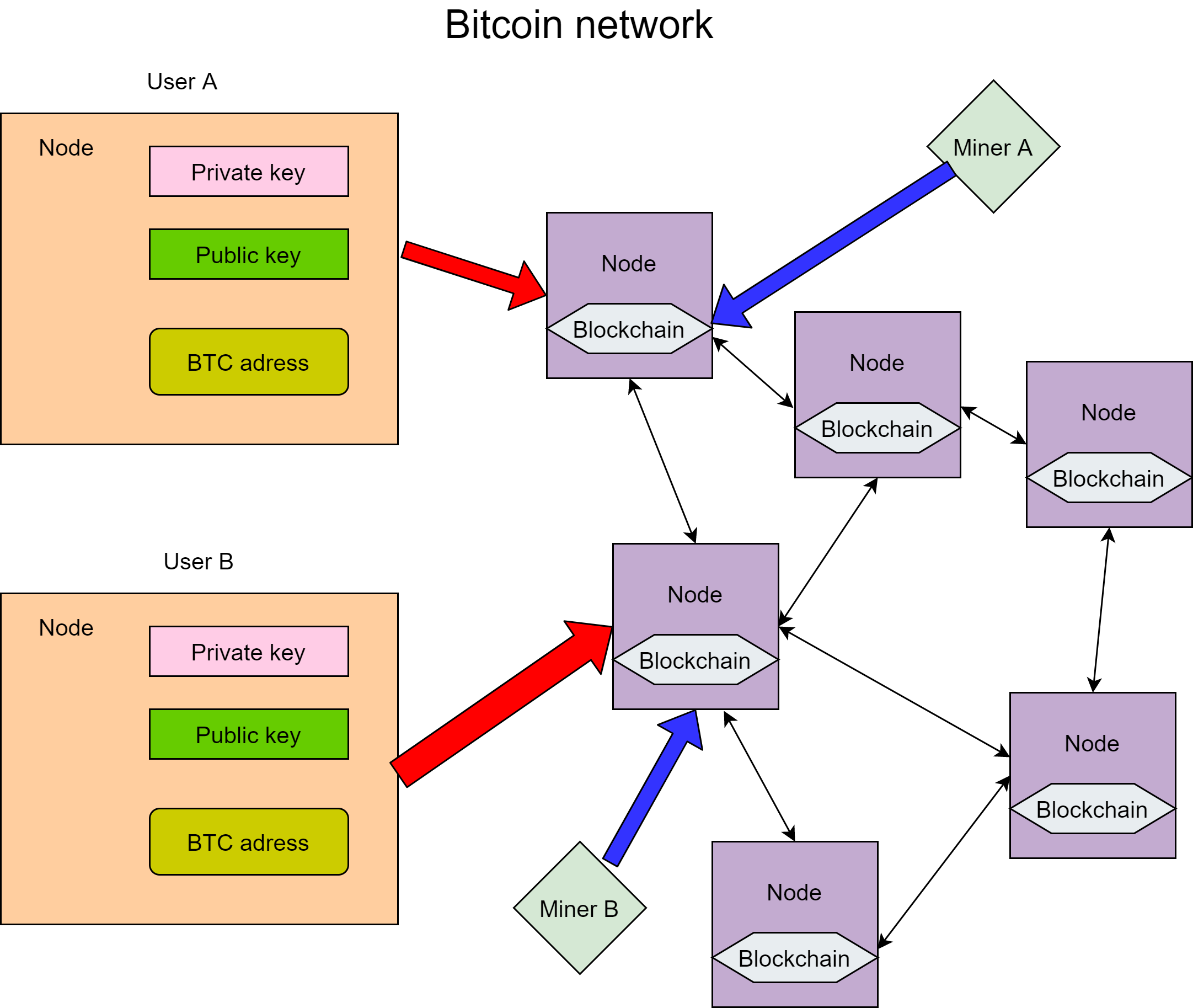

The Bitcoin is a virtual monetary entity and, as such, is devoid of any physical form. The minimum unit is 0.00000001 BTC (1 satoshi). Bitcoin blockchains are data files that contain information about past transactions and about the creation of new Bitcoins, providing a means of reward for closing a block with transactions. This is known as the Bitcoin network register. The blockchain consists of a sequence of blocks, wherein each subsequent block is built upon the previous one and contains information about new transactions in the network. The first block was created in 2009. Currently, as of October 2020 the chain counts nearly 650,000 blocks. As said, the Bitcoin blockchain is public: everyone can access all information about how many BTCs belong to a given address in the network. Further, the registry is not centralized: all network participants have their own blockchain copies and can modify them. There is no supervisory unit; however, there is a set of rules that each user must follow. As a consequence, the participants reciprocally control each other. To enter the Bitcoin network, a prospective user must use a network client or an external wallet. Enacting a transferring implies sending to the network information indicating that the recipient address is now the owner of the specified BTC amount. This information is distributed in a capillary form until all nodes have been informed about the transfer. Throughout this process, transaction integrity is provided by asymmetric cryptography, wherein the private key encrypts the transaction by the sender, and the other network users can read the message via the public key. In other words, this means that each transaction can be ascribed to a precise actor because no other has access to their private key. When information circulates through the network, everyone can read it but not re-encode an altered transaction. The scheme for sending BTC in the network is represented in figure 6. Each transaction is coded via the hash function, which for Bitcoin is dSHA256 [35].

For a virtual currency, the fundamental substrate to functioning is a means of determining how many units are circulating at any time-point and how many will be created. There must exist a consensus mechanism ensuring that all users agree to the ownership of the virtual currency. In the Bitcoin network, wherein users remain anonymous and do not have to entrust each other, proper operation requires that all nodes maintain consensus regarding the current state of the system among themselves. Most participants in the distributed network must agree and perform the same action: the Bitcoin’s key innovation is a mechanism that allows large-scale compliance of users on the network, solving the so-called Byzantine generals problem [36].

For the network to function efficiently, there is a need for entities that collect transactions, ascertain correctness, and combine into potential blocks: these are known as miners. As a reward for their activities, they receive an amount in newly-created Bitcoins alongside a usually small transaction fee, debited after block approval and inclusion in the primary chain. This happens when most network participants have reached a consensus to add a block candidate in their copy of the blockchain. Anyone can become a miner. The only requirement is the client software and the latest copy of the network registry. However, due to the sheer computational cost of the validating block process, miners arrange themselves into so-called “Mining pools” and make use of tailored high-performance computing solutions based on graphics processing units (GPU) or application-specific integrated circuits (ASICs) [37]. To be accepted, a new block must meet specific criteria. The result of the hash function, namely dSHA256 for the case of the Bitcoin, when applied to the data contained in the block must have a unique property: it must begin with a predetermined number of zeros. The number of starting bits resulting from hashing function which must be zero reflects the difficulty of confirming blocks. Miners collect transactions from the network (Fig. 8) and search for a number called “nonce”, given which the hash function will return the result with the specified number of zeros at the beginning. If they succeed, they immediately send their block to the network, and the other users can easily verify its correctness. The consensus mechanism among miners is that any miner who receives a new block from the corresponding result of the hash function (hash) includes it in the blockchain. From game theory, a strategy wherein all miners add correct blocks to their copy of the blockchain is Nash’s equilibrium state [38]. In other words, insofar as a miner believes that everyone else is acting fairly, their best option is to add a block to their copy. Operations on a blockchain version that is are not universally accepted are economically unprofitable because there is no reward for simply creating new blocks in it. This arrangement results in a consensus regarding the state of ownership of Bitcoins throughout the network, despite the absence of a centralized manager.

When confirming subsequent blocks, commonly known as “mining Bitcoins”, financial costs are incurred in the form of electricity consumption and the necessity to have specialized equipment. Nonce, the number required for closing a block, can be obtained only through an iterative process, i.e., a closed-form equation is prohibited by the formulation. For this reason, the consensus mechanism is referred to as a proof-of-work (PoW). Finding the correct result of a hash function with a specific number of zeros at the beginning requires, on average, a huge number of calculations [37]. Adding incorrect information (e.g., fictitious transactions) to the candidate for a block would cause his rejection, simply dissipating the energy used for the calculations. This is the reason finding the correct result from hashing is proof that a miner helps maintain the Bitcoin network.

Because each subsequent block contains the header from the previous one, it is impossible to alter past transactions without rebuilding the entire chain. Due to the time, difficulty, and cost of finding the right result of the hash function, it is economically unviable. The blockchain diagram is shown in Fig. 7. The Bitcoin protocol was created in such a way that the algorithm adjusts the difficulty in finding the right result of the hash function to the network computing power, so that a new block is created on average every 10 minutes [35]. The maximum block size is 1 MByte, determining how many transactions it can contain. As said, for the inclusion of a new block into the blockchain, miners receive a prize in the form of newly-created Bitcoins. The reward in halved every 210,000 blocks, up to the limit of 21 million Bitcoins [35]. It is possible that two miners would simultaneously and independently produce a new block and include it in their copy of the blockchain, causing multiple versions to appear. Such occurrences are dealt with applying the longest chain rule, i.e., the one for computing which the larger amount of power was invested is retained. This is a fundamental preservation mechanism. The pool rejects the shorter one during confirmation, and the miner receives no reward. A consequence is that blockchain technology is susceptible to so-called 51% attacks. When a miner has control over more than half of the computing power in the given network, they can confirm blocks faster than anyone else, thus manipulating transactions in the nearest attached blocks. The cost of carrying out such an attack on the Bitcoin network and other PoW-based networks was obtained in Ref. [39].

A limitation of the Bitcoin protocol is its low efficiency and the high costs of proof-of-work mechanism, which ensures network security. The primary costs are the non-recurring investment in computing power and the ongoing cost of electricity, which is currently at the level of that consumed by entire countries, such as Ireland and Denmark [40]. Another issue is the low network capacity. Bitcoin can handle, on average, only five transactions per second (TPS) [41]. By comparison, the Visa circuits handle on average about 1700 TPS [42]. In other words, one of the foundational advantages of the blockchain technology, namely the inability to make arbitrary changes to the blockchain, also results in a core rigidity. If one performs a transaction, this needs to be propagated to the entire network, and the previous version of the chain needs to be discarded, leading to the so-called “hard forks”. It should be noted that the Bitcoin protocol is not static, as it is subject to constant modifications. To date, a mechanism reducing the transaction size has been introduced, known as the “SegWit” (segregated witness), which packing more transactions into each lock. Work is currently underway on the introduction of the “Lightning Network”, which would allow micropayments to take place outside the main chain and thus which would increase network bandwidth, albeit at the price of reduced security.

2.2.2 Methods for attaining network-wide consensus

The near totality of cryptocurrencies are predicated, like the Bitcoin, on the initially-introduced proof-of-work (PoW) consensus algorithm. It protects against external attacks, however, it is inefficient. For this reason, faster algorithms have been developed and are being trialled. The second most popular algorithm after proof-of-work is the proof-of-stake (PoS) alongside its various modifications. Unlike with PoW, no miners are competing for calculating as soon as possible the right hash function value closing a block. Instead, the next block’s validator is a pseudo-random node from the network, the precise choice being based upon a combination of factors potentially including randomness and how many cryptocurrency units a given node has.

According to the PoS algorithm, blocks are “forged” and not mined as in the case with the PoW mechanism. Blockchain networks based on proof-of-stake also make use of transaction fees as rewards for “forgers”. However, whereas in the case of networks based on proof-of-work the reward for miners reward is a newly created cryptocurrency unit, in proof-of-stake networks the users who want to take part in the forging process must block for some time the number of cryptocurrency units in the network as a “stake”. The assumed rate’s size determines the chances of choosing a given node as the next validator, which will check the next block. The higher the stake, the higher their chances are. For the selection process not to favor only the richest, additional selection methods are added to the network. The two most commonly used are randomized block selection and coin age selection.

Every cryptocurrency using the proof-of-stake approach has its own set of rules determining who will become the validator of the next block. Security in the PoS algorithm is implemented via the built-in possibility of losing a blocked stake and the right to participate in future transactions as a punishment of passing a fraudulent transaction. As long as the stake remains higher than the reward, the validator will lose more cryptocurrency units than they would have gained when attempting to commit fraud. As for the PoW protocol, the PoS algorithm is vulnerable to 51% attack [43]. Such an attack can be perpetrated when a network node possesses more than half of the supply of a given cryptocurrency. In that case, they can then approve fraudulent transactions. The main advantage of the PoS algorithm is its efficiency. As the need for computationally-demanding calculations is relieved, no specialized user groups are needed to confirm blocks, enabling it be done faster than as compared to PoW.

A variation of the PoS algorithm is known as the delegated proof-of-stake (DPoS) [44]. It is based on the notion that the owners of a given cryptocurrency outsource block processing work to a third party. The latter are known as the so-called delegates, for whom the network users can cast votes, and who secure the network if they win the election. Their task is attaining consensus during the generation and approval of new blocks in the network. The weight with which each network user decides about its future during voting is proportional to the number of the units of a given cryptocurrency that they possess. The voting system varies depending on the project, but usually, each delegate presents an individual proposal related to their plan for the development of the network and then asks for votes. As a rule, rewards received by delegates for creating and confirming blocks are proportionally shared with their voters. Therefore, the DPoS algorithm is based on a voting system directly dependent on the reputation of delegates. If a selected node (delegate) does not work efficiently or breaks the rules, it is removed, and another one is selected in its place. In terms of performance, networks using DPoS are more scalable. As the number of users increases, they can process more transactions per second compared to networks using PoW and PoS algorithms. The next section surveys the Bitcoin protocol modifications and other possible blockchain technology applications in further detail.

2.3 Cryptoassets and diversified applications of the blockchain technology

A core aspect of the Bitcoin protocol is its open-source form: consequently, anyone can review, analyze, and copy the specifications, resulting in a rapid spread of the new technology. At first, mere Bitcoin clones were created, sharing the same network structure with minor modifications such as block size, hash function, mining limit, and creation time for new blocks. However, as the blockchain technology developed, novel projects expanding its use cases rapidly emerged. For instance, they allowed not only saving the transaction register but also executing code computer code in the form of a script. Throughout the impetuous development of the cryptocurrency market and all possible uses of blockchain technology, the original concept of a cryptocurrency began blurring. A more general concept was introduced: cryptoassets, which could be classified in three categories as a function of the applications: cryptocurrencies, cryptocommodities, and tokens [45].

Cryptocurrencies denote the first use of the blockchain technology and are intended to transfer funds. Modifications of the Bitcoin protocol are the most common. The first to maintain a significant position today is Litecoin (LTC), created in 2011. It is a clone embedding two changes. The first consists of reduced time between block extractions by a factor of four times and an increased maximum limit to 84 million, allowing a substantial increase in the speed of transaction confirmation [42]. The second is the use of another hash function, known as scrypt, which is more appropriate for implementing on standard processors for confirming blocks in the Litecoin network instead of requiring ASIC as in the case of Bitcoin.

The first cryptocurrency not based on the Bitcoin protocol was the Ripple [46], created in 2012. It does not implement the PoW consensus mechanism, implying that there are no miners in the network. Instead, it relies on a partially-centralized system called trusted nodes, which are responsible for confirming transactions. The idea behind Ripple is to provide connections between banks and stock exchanges to send money in real-time, which would entail using Ripple instead of fiat currencies for transfers outside national borders. Ripple tokens (XRP) were released by Ripple Labs. It currently owns most of this cryptocurrency. Currently111The data presented in this section are from October 2020., XRP is the fourth cryptocurrency in terms of capitalization. Its main competitor is Stellar (XLM), which also supports transactions between financial institutions. Unlike Ripple, the protocol is open source type and based on an own token. Both XRP and XLM tokens do not have a fixed supply limit and are, therefore, subject to inflation.

Since the Bitcoin blockchain is public and one can trace the transaction history of each mined coin, it is not entirely anonymous. The answer to this “drawback” was the emergence of cryptocurrencies ensuring complete undetectability to their users, the so-called “private coins”. This group of such cryptocurrencies includes: Dash, Monero, and Zcash. Dash (DASH) has a hybrid architecture based on two network layers: the first involves miners using the PoW mechanism, as in the case of Bitcoin, the second comprises the so-called “masternodes” using the PoS technique. Monero (XMR) ensures anonymity thanks to a RingCT, by which the addresses (public keys) of those who make transactions are hidden in the blockchain. It is considered the cryptocurrency providing the most significant anonymity and, as such, is regrettably in widespread use by criminals, for example, for demand ransom payments [47]. Zcash (ZEC) is based on a “zero-knowledge” protocol called ZK-Snarks. It is a cryptographic solution that allows confirming whether the information is correct without having to disclose it, thus ensuring the anonymity of both the sender and recipient of a transaction to be preserved, while concealing its entity. Anonymous addresses are called shielded addresses and are compatible with public addresses, such that one can perform a transaction from a public wallet to a protected one and vice versa. Zero-knowledge is also used by cryptocurrencies such as ZClassic (ZCL), Bitcoin Private (BTCP), PIVX, and Komodo (KMD). In the cryptocurrency group protecting anonymity, Dash and Zcash have a built-in maximum supply mechanism, whereas Monero does not.

The so-called cryptocurrency group also includes several Bitcoin hard forks. The Bitcoin Cash (BCH) represents the first Bitcoin division, wherein part of the community decided to disconnect and develop the project on a new blockchain. It entails increasing the block size from 1 to 8 MBytes, and then to 32MB. In the next division, Bitcoin Gold, the hash function was changed to Zhash, allowing efficient block confirmation on non-specialized hardware. Another variation, Bitcoin SV, stems from Bitcoin Cash and features a block size of 128 MBytes.

The second category of cryptoassets, cryptocommodities, serve as the basis for applications of the blockchain technology. They are “material” enabling the creation of decentralized applications and smart contracts. These are automatically executed computer codes that perform specific actions when certain conditions are met. Cryptocommodities operate as “fuel”, allowing one to pay for using a decentralized computing network.

Ethereum [33] was the first realization of such an idea. It was proposed in 2013 and launched in 2015 as an open-source computing platform based on the blockchain. It has been equipped with its own programming language, known as Solidity, through which one can program smart contracts and decentralized applications. It has its cryptocurrency called ether or ethereum (ETH), which serves as a payment unit for carrying out computational operations. Their price is expressed in the so-called units of “Gas” and depends on the computational complexity necessary to complete an operation. Ethereum, like Bitcoin, is based on blockchain technology and the PoW consensus mechanism. However, it uses another hash function, Ethash, that supports the efficient use of GPU hardware in the mining process. It does not have a fixed block size. Instead, each block requires a specific number of Gas units, which determines the computing power needed to complete the transactions it contains. The average time between blocks is about 15 seconds, and the maximum number of transactions per second is around 25. Unlike for Bitcoin, there is no upper limit on mining. In the future, the developers predict a transition to a PoS consensus mechanism, which would increase network bandwidth.

The Ethereum concept gained considerable popularity among the cryptocurrency community from the outset. In 2014, 18.5 million USD were collected from pre-sale, hallmarking the highest result of crowdfunding at that time. This result was beaten by a venture capital fund, the DAO, which aimed to raise capital for the development of blockchain startups and non-profit organizations. The fund took the form of a decentralized, autonomous organization built on the Ethereum blockchain in an intelligent contract. In 2016, it collected 11.5 million ethereum worth nearly 168 million USD. On this occasion, one of the pros/cons of blockchain was revealed, namely code unchangeability. It turned out that the DAO smart contract code had gaps that allow unauthorized funds to be transferred. A hacker attack took place in June 2016, during which 3.6 million ethereum were stolen. To reverse the effects and change the DAO code, the Ethereum blockchain had to be split. On the new, the withdrawal of funds was canceled, whereas on the old, now called Ethereum Classic (ETC), everything remained unchanged. Currently, the ethereum remains the second cryptocurrency in terms of capitalization.

The considerable success of the concept of smart contract, in particular the possibility of collecting funds under the Initial Coin Offer (see Fig. 9) on the Ethereum platform, spearheaded competition also offering the possibility of creating applications in a decentralized computing network. Major projects of this type include EOS and Cardano. The EOS [49] platform is based on the delegated proof-of-stake algorithm (DPoS). As there is no mining process, unlike with Bitcoin or Ethereum, the network can process up to 15,000 transactions per second. However, this is attained at the expense of security. Only 21 selected block producers are responsible for verifying transactions, who receive awards in the form of newly created EOS units for their activities. The maximum number of EOS tokens is set to one billion units. The programming language used on the platform is known as WebAssembly. The leading EOS network was launched in June 2018, hallmarking the most substantial ICO offer in history. In year-long offer, ended in June 2018, it raised 4.2 billion USD eclipsing the world’s biggest initial public offerings of the year and more than doubling the next biggest offering of that type (see Fig. 9).

On the other hand, Cardano [50] uses the PoS algorithm, known as Ouroboros. There are two independent layers of the network: billing and computational. The accounting layer is built upon the blockchain network. The Haskell programming language is used to create intelligent contracts. The maximum supply of ADA cryptocurrency is 45 billion units. Other platforms offering similar services as Ethereum are the Tron – TRX, Lisk – LSK, ICON – ICX. They are similarly based on the DPoS algorithm. PoS-based platforms are Tezos, NEO (called the Chinese equivalent of Ethereum), NEM (based on Proof of Importance - a variety of PoS), and Waves. As one can see, it is typical for cryptocommodities to move from the original PoW consensus mechanism towards PoS, since this allows faster processing of network operations, which is required for additional than transaction-register functions.

The third group are tokens, which are the youngest cryptoassets and can be referred to as direct applications of blockchain technology. They are most often used as means of payment in decentralized applications (dApps) built on cryptocommodities such as Ethereum or are issued in the ICO offers for the development of a blockchain venture. Typically, they don’t have their own blockchain. Blockchain technology, thanks to eliminating a central intermediary who earn on commissions can be used wherever there is possibility to connect sellers and buyers directly (for example Uber and Airbnb).

The combination of token and cryptocurrency categories denotes the so-called “stable coins”. Their exchange rate is usually related to fiat currency. The most popular is tether [51] (USDT), which linked to the US dollar in a one-to-one relationship. It relies on Bitcoin blockchain via the Omni Layer platform and is issued by the private company Tether Limited, which declares that its supply is fully covered in US dollars. Other notable stable coins are the DAI, PAX, TUSD, and USDC.

The latest applications of blockchain technology are so called decentralized finance (DeFi). This term refers to an ecosystem of financial applications that are built on blockchain networks. Most DeFi platforms take the form of decentralized apps (dApps). They use smart contracts to automate financial transactions. The idea behind DeFi is to create decentralized cryptocurrency borrowing and lending system and to provide monetary banking services [52]. The largest projects of this type are: Chainlink, Wrapped Bitcoin, Uniswap, Maker and Compound.

2.4 Cryptocurrency trading

Cryptocurrencies, as a new concept, would not have much value in the early stages of their existence if they could not be exchanged for traditional currencies. One of the first exchanges that offered such opportunities was the Mt.Gox, as mentioned earlier, but the present cryptocurrency market is profoundly divided and decentralized. Nowadays222The data presented in this section are from October 2020. there are 350 cryptocurrency exchanges around the world. Most of them are platforms trading only cryptocurrencies with each other, with transactions performed around the clock. This is a key feature distinguishing the cryptocurrency market from the Forex, wherein trading occurs only from Monday to Friday. The second fundamental difference lies in the form and participants of the trade: in the case of cryptocurrencies, it takes place mostly between individual investors [53], whereas on the Forex, trading takes place on the OTC (Over-The-Counter) market and its participants are mainly banks. The third difference is the lack of a reference price, which in the case of the Forex market is provided by Reuters. Only in the case of the bitcoin, there is a futures contract quoted on the CME Group [28].

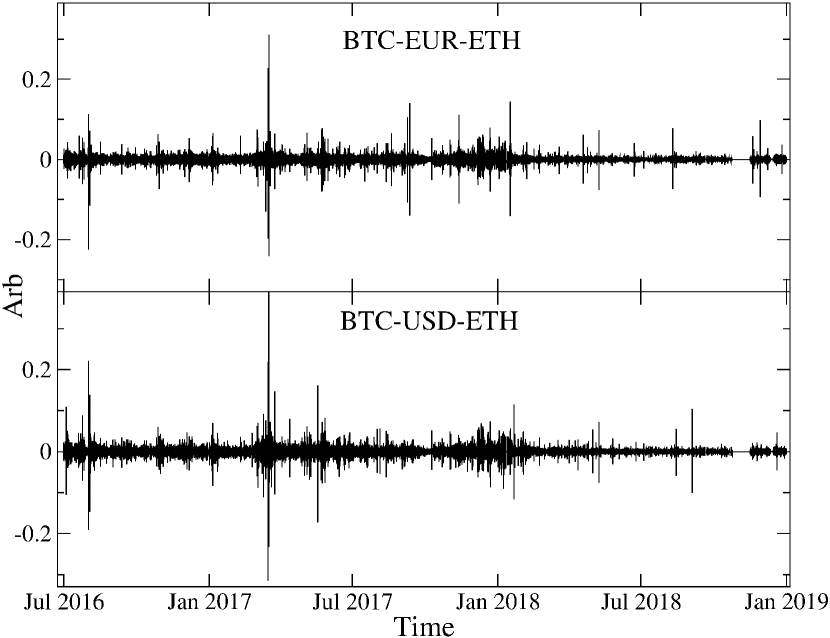

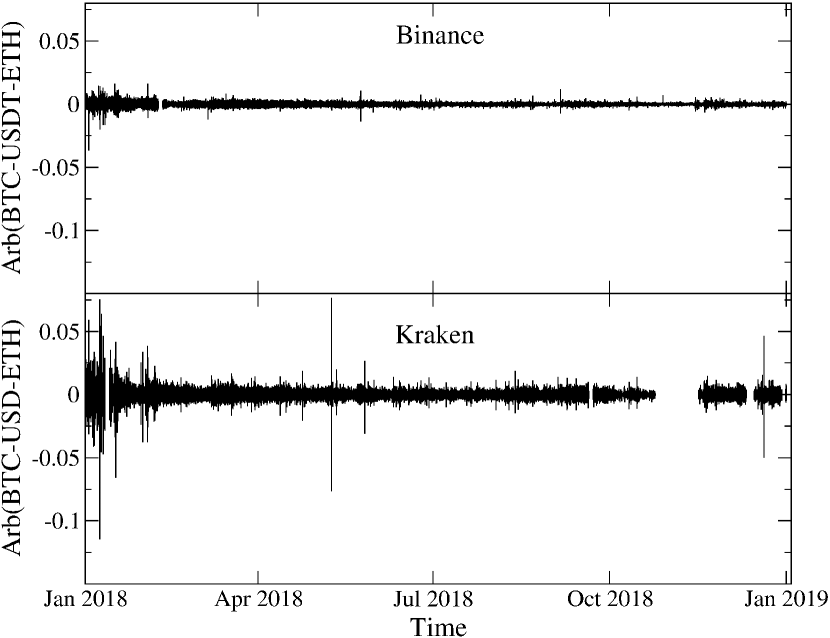

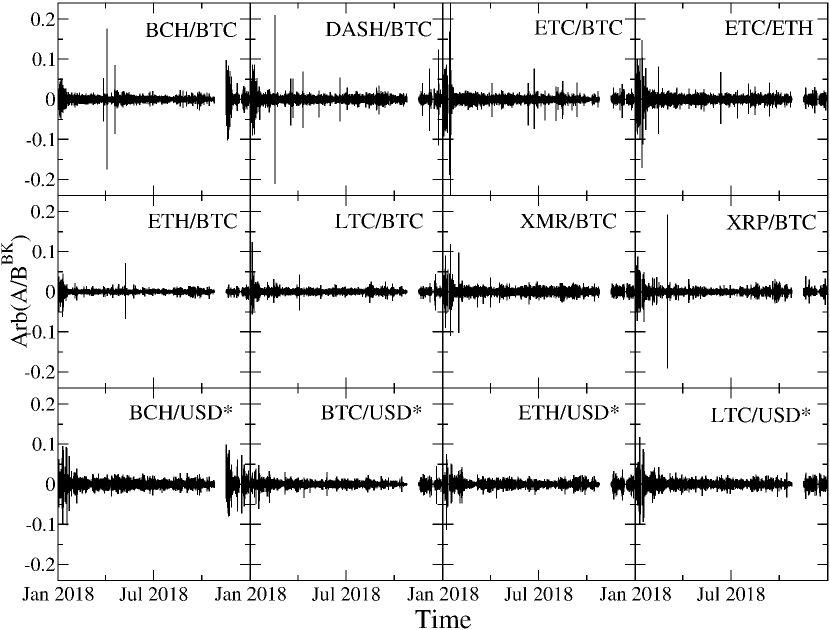

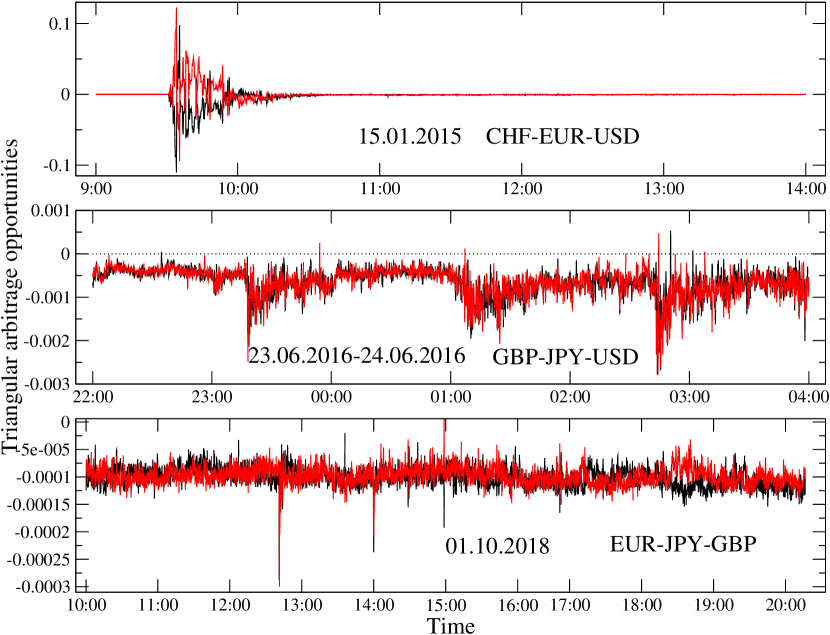

The decentralization of the cryptocurrency market means that the same cryptocurrency pairs are traded on different exchanges. Historically, significant valuation differences could be observed between exchanges [54]. For the stocks, this issue has been investigated and is called “dual-listed companies” [55, 56]. However, in the case of cryptocurrencies, which can be sent almost immediately between anywhere in the world, it represents a different kind of issue. The topic of trade comparison between cryptocurrency exchanges and arbitrage opportunities is covered in Sections 3.2 and 5.2.3. A common feature between the Forex and the cryptocurrency market is the possibility of triangular arbitrage [57, 58]. This will be discussed in detail in Section 5.2.3. A separate category not found in traditional financial markets is the so-called decentralized exchanges (DEX), where cryptocurrencies, through smart contracts, can be traded automatically, without any reliance on a central exchange server [59].

The statistical properties of the exchange rates of major cryptocurrencies will be analyzed in this review, considering the Binance, Bitstamp, and Kraken exchange rates. Binance [60] is currently the largest cryptocurrency exchange in terms of volume value. It was founded in July 2017 in China. After the regulation regarding trading in cryptocurrencies was tightened, the head office was moved to Malta in March 2018. At its inception, only cryptocurrency trade was conducted on it. Binance offers the ability to make transactions using approximately 800 different cryptocurrency pairs and additionally owns a cryptocurrency called the binance coin, which is used for paying commissions on the exchange. The exchange also offers the opportunity of carrying out ICO offers on it. Furthermore, daughter companies allowing exchanging cryptocurrencies for fiat currency. The Kraken exchange [61] was launched in September 2013, with headquarters in San Francisco and branches in Canada and Europe. It is the largest exchange in terms of volume value on cryptocurrency pairs expressed in Euro and currently offers 185 cryptocurrency pairs. The Bitstamp exchange [62] is one of the longest-running cryptocurrency exchanges. It was established in August 2011, and its head office of the exchange is in Luxembourg. The platform offers trading only on the most liquid cryptocurrencies, currently supporting 38 exchange rates.

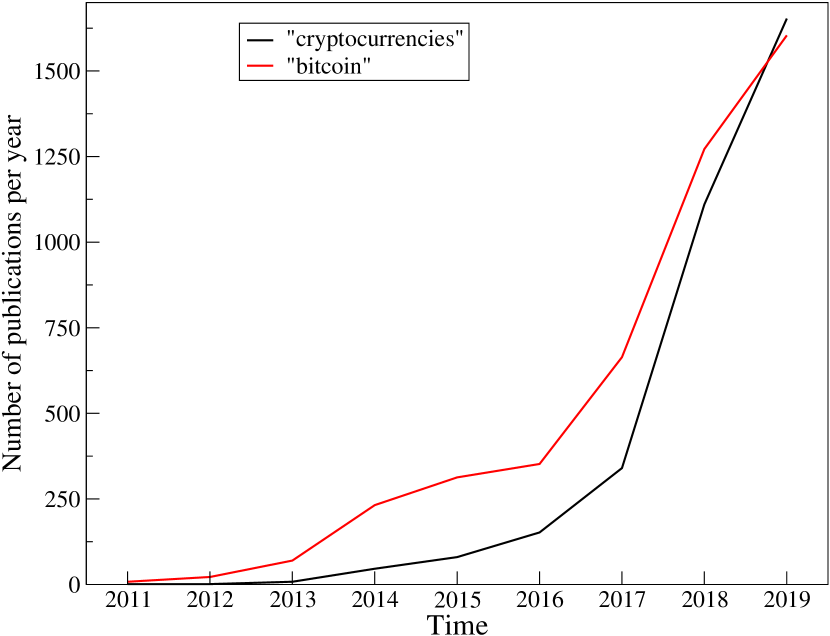

There was a sharp increase in the number of actively traded cryptocurrencies in 2017 (Fig. 4). Since then, the number of ICO offers has kept increased systematically (Fig. 9). The market capitalization also increased spectacularly, heralding the speculative bubble phase [26]. At the time of writing, approximately 3600 cryptocurrencies and nearly 30,000 exchange rates are present on the market [25]. The capitalization of the entire cryptocurrency market is on the order of 350 billion USD, and therefore comparable to middle-size stock exchange and largest American companies [64]. The spectacular development of the cryptocurrency market has attracted worldwide interest in the new asset, including the scientific community. The first works on the Bitcoin were published already in the period 2013-2015 [65, 66], but the real boom has only occurred since 2017 (figure 10). At first, scholars mainly examined the characteristics of the first cryptocurrency, the bitcoin [67, 68, 69]. Next, the community developed an interest in comparing it to other cryptocurrencies [70, 71, 72], which was followed by studies revealing correlations within the cryptocurrency market [73, 74, 75, 76, 77, 78, 79, 80] and its relationships to mature markets [81, 82, 83, 84, 85]. In particular, the possible uses of the bitcoin as a means of diversifying an investment portfolio and as a hedging instrument for the currency market [86], gold and commodities [87] and stock markets [88, 89, 90] were considered. A more detailed review of existing literature devoted to research on cryptocurrencies in the context of financial markets is available in Refs. [91, 92].

3 Statistical properties of fluctuations

3.1 Data

The presentation of results begins with the statistical properties of cryptocurrency price fluctuations from a brief description of the empirical data sets. Three issues are of interest here: (1) the cryptocurrency prices expressed in regular (fiat) currencies: US dollar and euro, with particular focus on bitcoin (BTC) as the most liquid and the most frequently traded cryptocurrency, (2) the cryptocurrency-cryptocurrency exchange rates, and (3) result comparison for two independent trading platforms.

The data were collected from the following sources. For BTC, the oldest cryptocurrency, the longest series of historical data was obtained from the Bitstamp exchange platform [62], offering the BTC price tick-by-tick quotes covering the interval 2012-2018 and expressed in USD. While the cryptocurrency market was expanding, more and more exchanges were created over time. They allowed trading not only BTC with USD, but also other cryptocurrencies with regular currencies, and even cryptocurrencies among themselves. A comparison between the properties of bitcoin and ethereum (ETH) was possible based on tick-by-tick quotes obtained from the Kraken platform [61]. The quotes covered an interval from mid-2016 to the end of 2018. A data set with quotes representing some less liquid cryptocurrencies, like litecoin (LTC) and ripple (XRP), unavoidably has to be smaller and covers only the entire year 2018, during which their trading frequency was sufficient to construct time-series without excessive constant-value intervals. To compare the properties of data from the different trading platforms, there is also consider a parallel set of the cryptocurrency quotes from Binance, the largest platform of this type. However, the sampling frequency of this set is 1 min, which provides us with 463,000 quotes for each exchange rate.

As a benchmark representing the regular currencies from the Forex, the EUR/USD exchange rate was considered, with quotes obtained from a broker, Dukascopy [93]. However, there is a significant difference between this dataset and the cryptocurrency datasets: the former excludes weekends and holidays, whereas the latter are recorded continuously.

In the following, three principal characteristics are reported: the average inter-transaction time (when available), which is denote by , the probability distribution function (PDF), and the autocorrelation function for the returns, defined as logarithmic exchange rate change over a fixed time interval : , where is an exchange rate of two distinct currencies or cryptocurrencies at time . The autocorrelations of both the signed returns and absolute returns (volatility) are of interest.

3.2 Average inter-transaction time

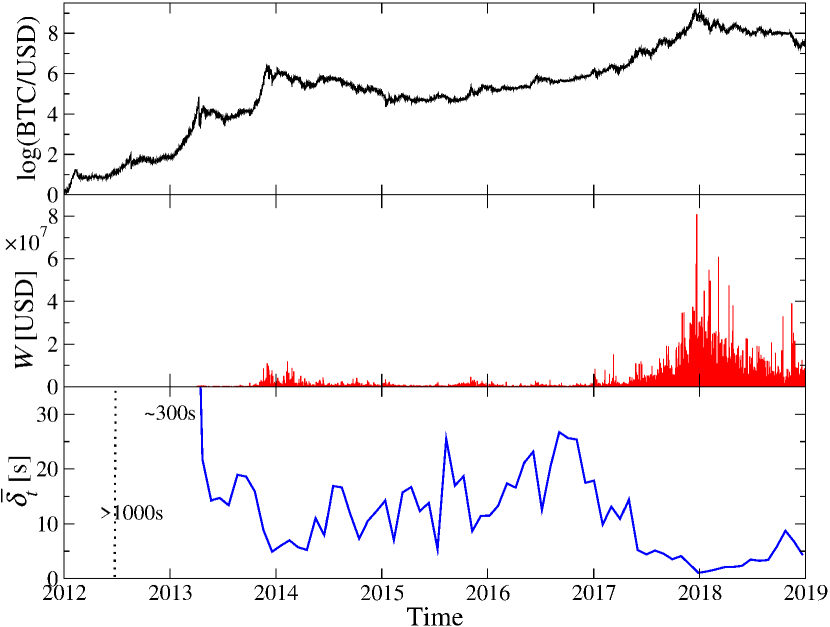

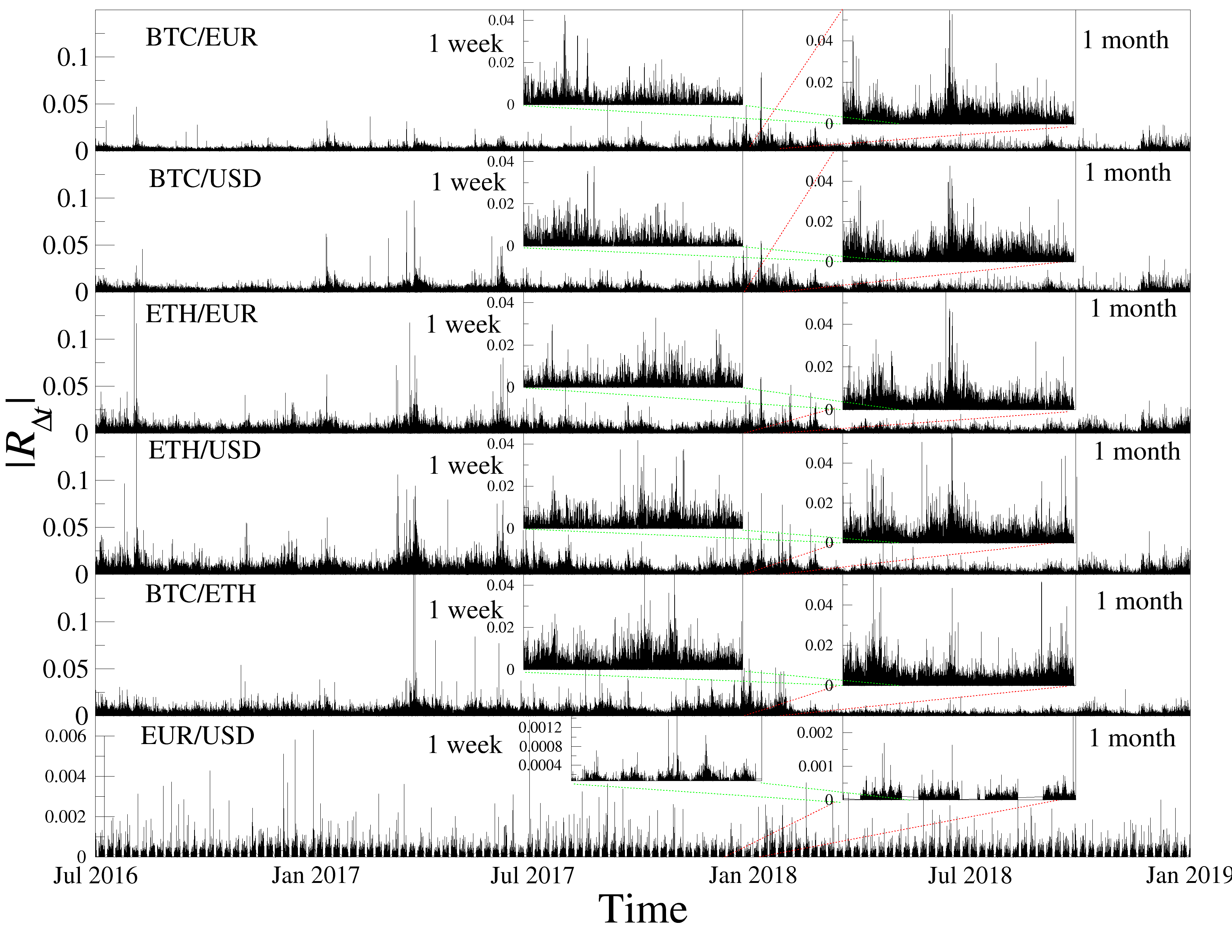

The analysis starts with the tick-by-tick quotes of the BTC/USD exchange rate as it is the most liquid and frequently traded cryptocurrency asset (Bitstamp quotes). Figure 11 shows the BTC/USD exchange rate, the BTC volume (in USD) traded during hour-long intervals, and average inter-transaction time calculated over monthly windows. There is an upward trend of BTC/USD throughout the years until the turn of 2017 and 2018. The trend was accompanied by a volume increase and a reduction in the average inter-transaction time. In 2012 and the first half of 2013, the trade volume was negligible. Subsequently, the peak of the first bull phase, at the turn of 2013 and 2014, was accompanied by an increase in volume and a reduction in the inter-transaction times. A side trend dominated the BTC/USD rate over the next three years and was associated with a volume decline and less frequent trading. A resume of the bull market towards the end of 2016, with spectacular growth in 2017 in particular, brought a further substantial increase in volume accompanied by a decrease in the average inter-transaction times. At the peak of the speculative bubble, at the turn of 2017 and 2018, the time between transactions became as short as around a second. A subsequent bear market caused a decrease in volume, which, however, remains above the pre-crash level observed in 2017. The average inter-transaction time was also affected but remains below 10 seconds.

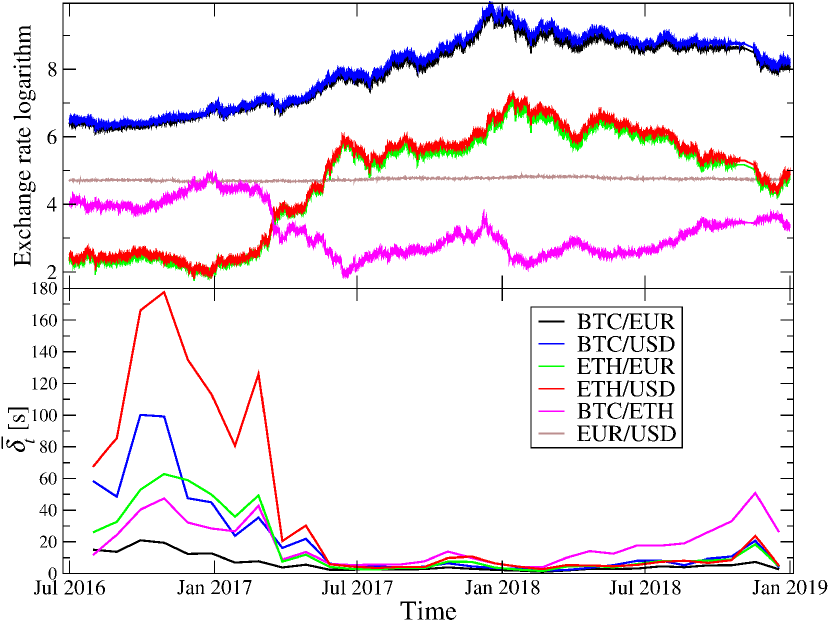

The mutual exchange rates (logarithms, top panel) and the inter-transaction intervals averaged over monthly windows (bottom panel) for the BTC, ETH, USD, and EUR based on the Kraken and Dukascopy data are shown in Figure 12. In parallel with Figure 11, one observes a gradual shortening of for the cryptocurrencies down to below 10 seconds in the bull-market phase (between mid-2017 and a trend reversal in early 2018). On the contrary, in the bear-market phase of 2018, a decrease in the BTC and ETH valuation in regular currencies was accompanied by an increase in . Only for BTC/EUR one still observed s. By looking at the exchange rate fluctuations over time, one can notice the considerably lower volatility of EUR/USD, almost resembling a flat line in the scale of Figure 12, as compared to the cryptocurrency-involving rates.

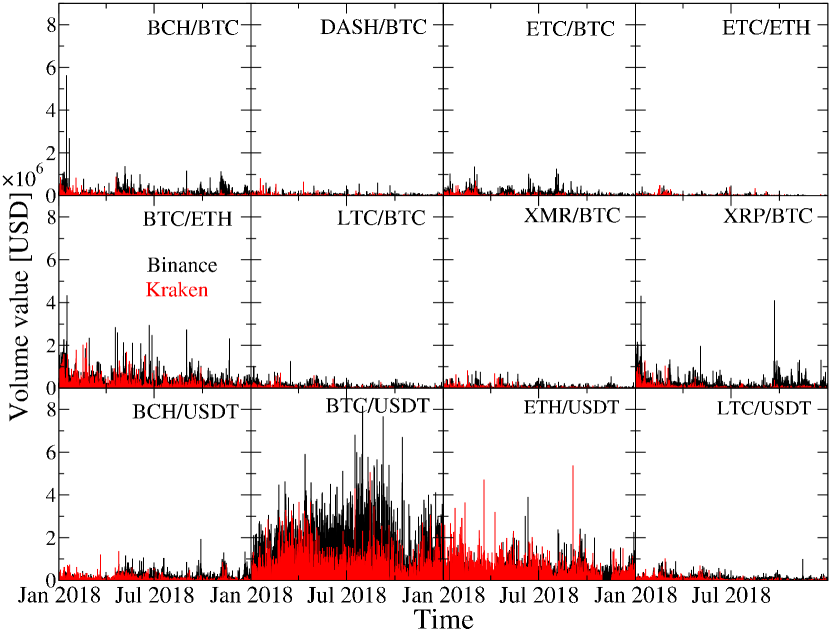

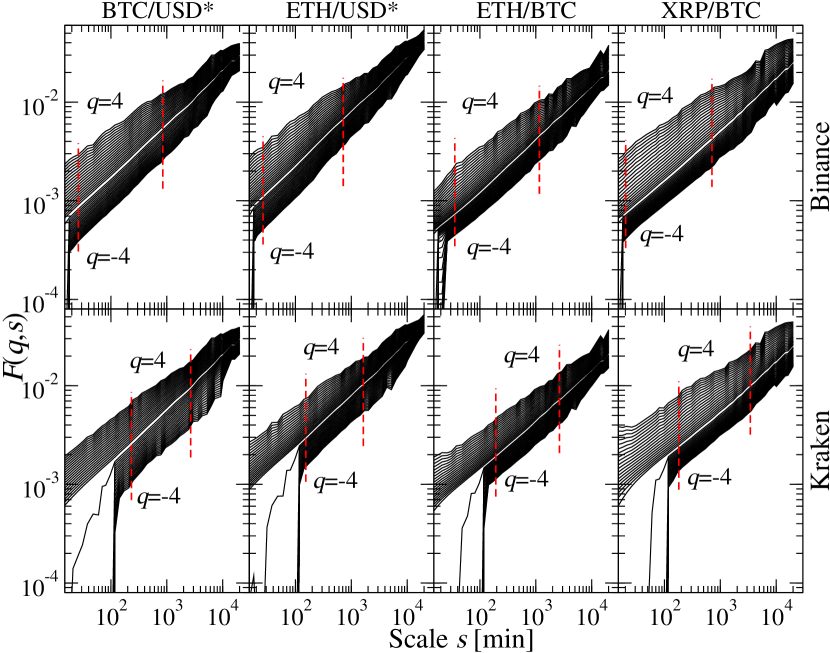

No strictly analogous result could be shown for the Binance dataset since it does not contain tick-by-tick quotes. Instead, the trading frequency can be related to the average length of intervals without trade (zero-return sequences) and the number of periods without trading. In Figure 13, the volume time-series from both exchanges were compared for 12 exchange rates involving both the most liquid cryptocurrencies (BTC, ETH) and the least liquid ones (DASH, XMR, LTC, XRP, BCH). Since on the Binance platform, the cryptocurrency value may only be expressed in terms of other cryptocurrencies, to facilitate the inter-platform comparison, the USD has to be replaced by a proxy – Tether (USDT), whose USD-based exchange rate fluctuates closely around 1. Therefore, the ETH/USD on Kraken corresponds to ETH/USDT on Binance. Figure 13 shows that a higher 1-min volume is seen on Binance for all exchange rates under consideration, which implies that the average inter-transaction time on Binance is shorter than on Kraken (see Table 1 in Sect. 3.3). The volume accumulates principally in BTC/USD and BTC/USDT, and then on ETH/USDT, BTC/ETH, and XRP/ETH.

3.3 Fluctuation distributions

At the dawn of scientific interest in the financial markets, it was believed that a normal distribution [1] could approximate the PDF of the stock market returns. Later, it was discovered by Benoît Mandelbrot that such distributions have significantly heavier tails and comply with the stable Lévy regime [2]. Consequently, the truncated Lévy distributions began to be used in this context [94]. Currently, it is accepted that, in mature financial markets, the CDFs of the absolute normalized returns in the bulk part develop fat tails of the form

| (1) |

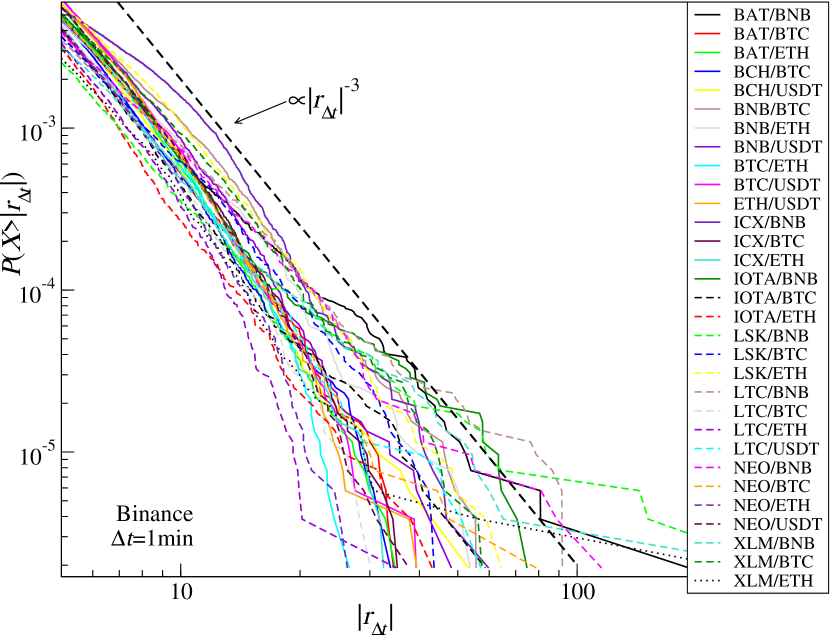

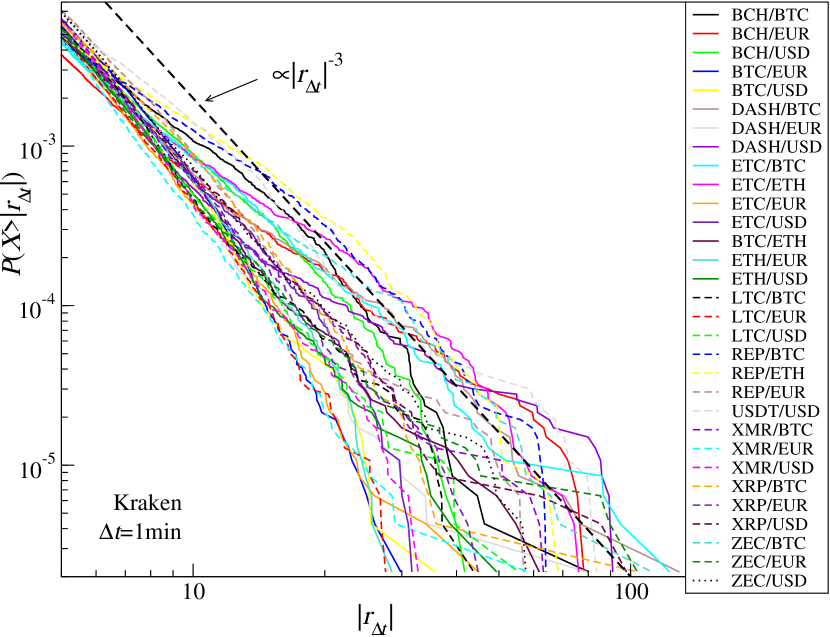

where with and denote, respectively, sample mean and standard deviation. This relationship with different values of has been reported for many different asset types, including shares, currencies, commodities, and cryptocurrencies [5, 6, 95, 23, 96, 97, 68, 58, 98].

In particular, high-frequency stock-market data is frequently described by an inverse cubic dependence [99, 6, 100], i.e., the one with . A well-known fact is that the tail thickness of the return PDFs/CDFs decreases as increases from second to minute, hour, and longer scales [101, 102, 71]. A normal or exponential distribution can already approximate the return distributions for daily data. On the other hand, the return distributions for over the range of a few seconds are closely matched by the power-type functions [101]. This can easily be explained by the central limit theorem, provided the returns are independent: as increases, the distribution should converge to a normal distribution [103].

In general, it often happens that the fluctuations of a power-law type are associated with some critical phenomenon that occurs in the dynamics of a given system. However, in the financial market case, it was pointed out [104] that such behaviour of the return distributions might be related solely to the finite-size effects in the number of active agents and, therefore, any particular form of a power-law PDF may be viewed as accidental and non-universal [105, 106], opposite to what was believed earlier [100].

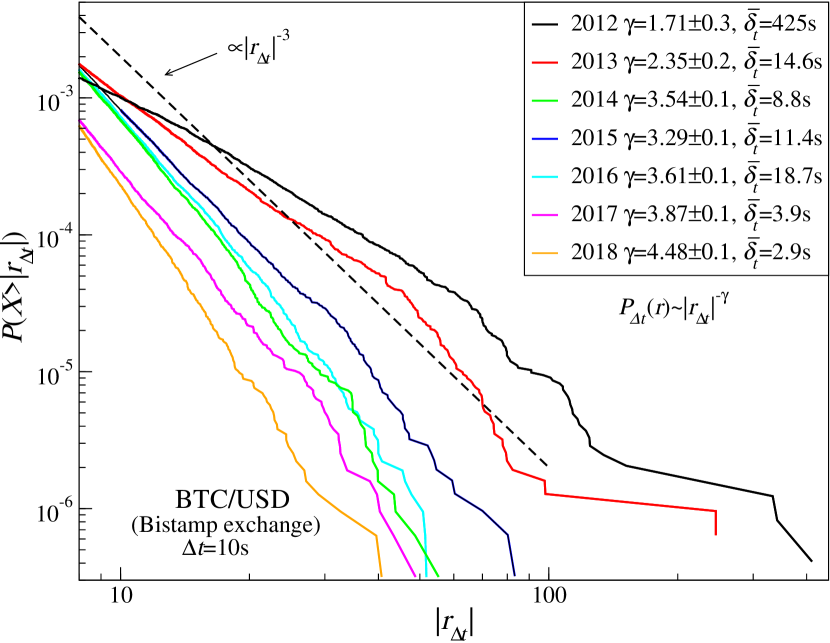

In order to calculate the cumulative probability distribution function (CDF), the tick-by-tick datasets from Bitstamp and Kraken were transformed to time-series of normalized returns , at a sampling frequency s. For the Bitstamp BTC/USD rate, it provides one with returns. As the analyzed period of 2012-2018 features diversified dynamics, the statistical properties of the returns have to be considered separately for each year. Figure 14 presents the CDFs of the absolute normalized returns. A power-type relation of the distribution tail (Eq.(1)) is observed for each year, at least over a part of the available return magnitudes, with the widest scaling range apparent in 2012. However, one has to notice that even in this latter case the power-law scale range does not exceed 1.5 decade, while its width gradually decreases each year and it falls well below one decade in 2018. This suggests that it is safer to consider these CDFs as only carrying some signatures of the power-law distributions and not being precisely the power-law ones.

There is evolution of the exponent from lower () towards higher values (), and the opposite trend for the estimation error. Furthermore, there is a relation between the shortening of the average inter-transaction time and the growing tail index , hallmarking a phenomenon observed in other financial markets as well. This relation can be interpreted as defining the internal time-flow of the market: the faster the trading and the shorter the inter-transaction intervals, the faster is the time-flow experienced by the assets and, consequently, the shorter are time-scales over which particular effects are observed [101]. The acceleration of market evolution is, therefore, a natural consequence of both the technological advances and the increasing market-participant influx that conjointly lead to higher transaction frequency. For example, for s, the return CDF tails for the BTC/USD, which were initially in the Lévy-stable regime with , became gradually thinner with in 2014 and in 2018 (figure 14). At present, the inverse-cubic scaling has to be addressed for a sampling frequency of s.

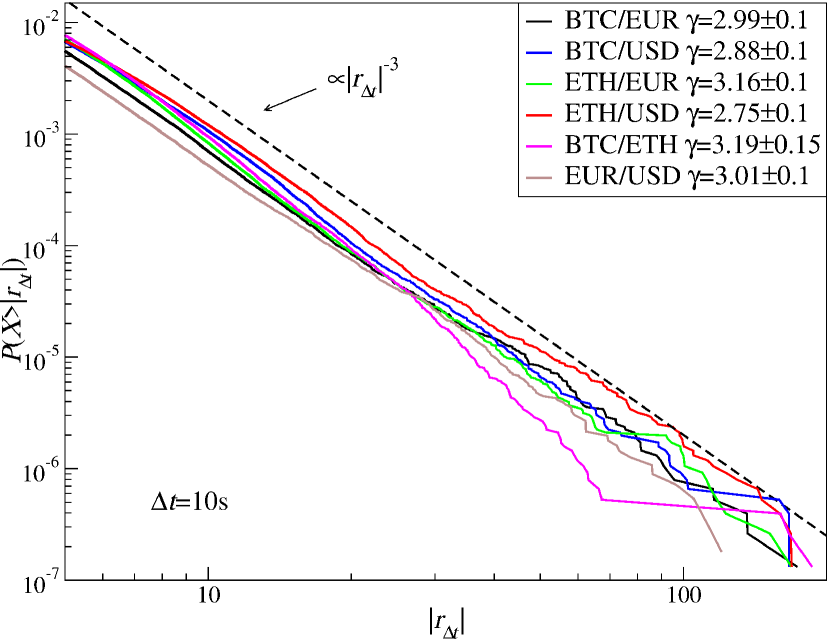

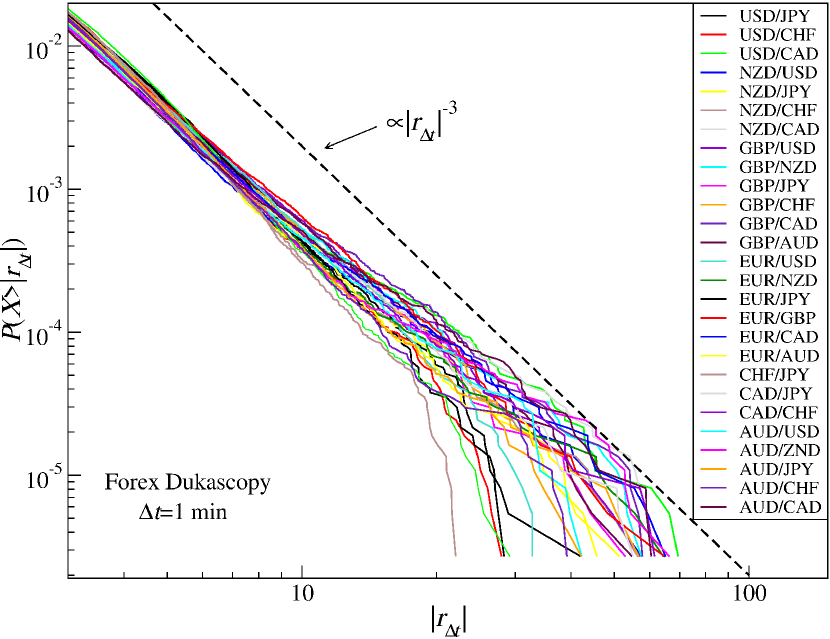

A comparison between the CDFs obtained for different exchange rates is presented in Figure 15 based on five return time-series from Kraken, namely BTC/USD, BTC/EUR, ETH/USD, ETH/EUR, and BTC/ETH (s, ), alongside the EUR/USD return time-series from Dukascopy (s, ). Here, the data covers the entire available interval, from mid-2016 through end-2018. Except for BTC/ETH, the distributions show a near power-law decay over about one decade, with the scaling exponent dwelling around . The values are slightly below this level for the BTC/USD and ETH/USD; these are the rates that, in a first part of the period under consideration, experienced the smallest trading frequency, with s. The BTC/EUR and ETH/EUR returns are characterized by that is the closest to 3, in parallel with the much more liquid Forex pair, EUR/USD, while the BTC/ETH crypto-crypto rate shows a slightly faster decay with .

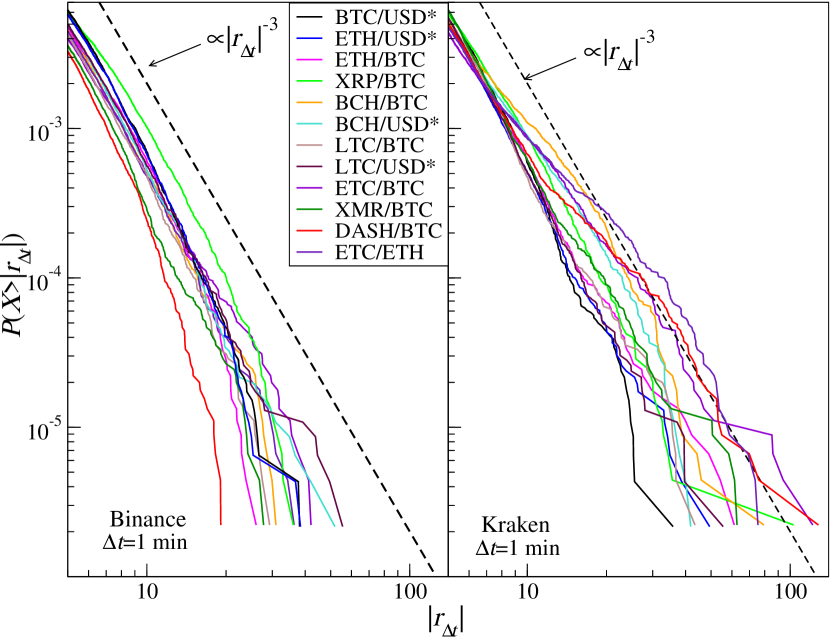

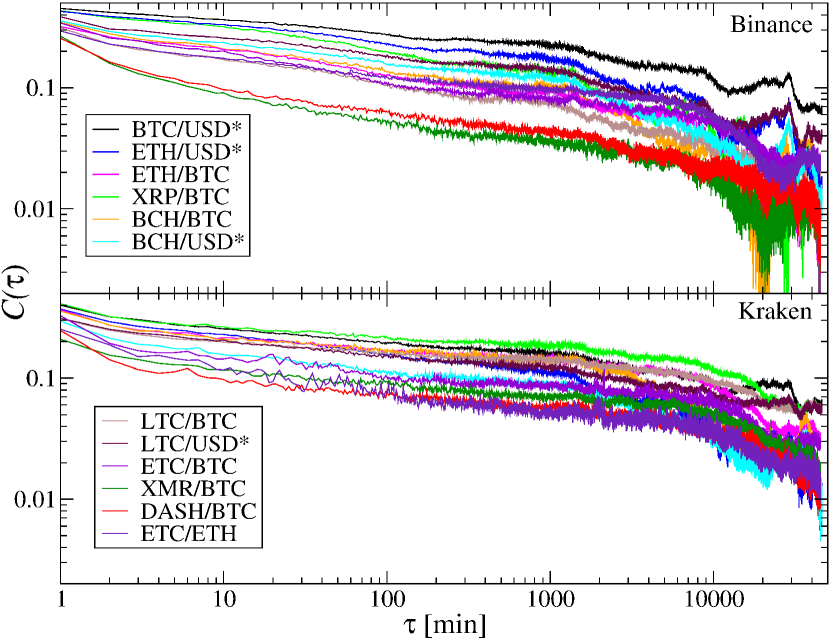

The results for the two different platforms, Kraken and Binance, are collated in Figure 16 and Table 1. By decreasing the sampling frequency to min (Jan-Dec 2018, ), the fluctuations of BTC and ETH can be compared with those of a few among the least-liquid cryptocurrencies, namely, XRP, BCH, LTC, XMR, DASH, ETC (all cryptocurrencies alongside their tickers are listed in the Appendix A). The exchange rates on Binance are characterized by a higher trading frequency (i.e., shorter average length and lower average number of non-trading periods, Table 1) compared to their counterparts on Kraken (see also Fig. 13). This affects the values of the exponent: while on both platforms, the exchange rate returns form CDFs with , the CDF tails for the exchange rate returns on Binance tend to decay faster than their counterparts on Kraken. This pattern is also discernible in Figure 16 and is in line with the observation that the trading frequency is related to the inner time-pace of a market. The less liquid exchange rates from Kraken have a slower internal time and, consequently, their rates of return distributions are characterized by thicker tails and poorer scaling (i.e., larger estimation error). By contrast, the CDFs for the rates with a higher trading frequency and volume resemble those characterizing the mature financial markets.

| [USD] | ||||||||

|---|---|---|---|---|---|---|---|---|

| Name | Bi | Kr | Bi | Kr | Bi | Kr | Bi | Kr |

| BTC/USD∗ | 3.450.1 | 3.630.15 | 1.07 | 1.61 | 8559 | 55360 | 196331 | 33998 |

| ETH/USD∗ | 3.390.1 | 3.40.1 | 1.10 | 1.78 | 16184 | 67807 | 61430 | 19711 |

| BTC/ETH | 3.300.1 | 3.180.2 | 1.09 | 2.62 | 12134 | 82074 | 60824 | 5250 |

| XRP/BTC | 2.910.1 | 2.990.15 | 1.20 | 3.50 | 41043 | 72556 | 31510 | 2763 |

| BCH/BTC | 3.360.1 | 2.350.15 | 1.25 | 4.39 | 29973 | 68059 | 16299 | 1251 |

| BCH/USD∗ | 3.360.1 | 2.610.15 | 1.40 | 3.83 | 40922 | 75427 | 15893 | 2151 |

| LTC/BTC | 3.420.1 | 3.340.15 | 1.17 | 5.09 | 34360 | 62675 | 13110 | 940 |

| LTC/USD∗ | 3.230.15 | 3.410.1 | 1.29 | 3.48 | 45208 | 79983 | 11793 | 1725 |

| ETC/BTC | 3.020.1 | 2.310.2 | 1.56 | 6.34 | 76691 | 55647 | 10164 | 709 |

| XMR/BTC | 3.680.15 | 3.210.15 | 1.37 | 6.58 | 47852 | 54832 | 4176 | 614 |

| DASH/BTC | 4.040.15 | 2.520.2 | 1.46 | 7.58 | 55684 | 49134 | 2777 | 416 |

| ETC/ETH | 3.340.1 | 2.180.2 | 2.30 | 9.15 | 82458 | 41861 | 1333 | 266 |

| Average | 3.380.11 | 2.930.16 | 1.35 | 4.66 | 40922 | 63785 | 35470 | 5816 |

Summarizing, it can be argued that, for a given exchange rate, in order to meet the characteristics typical of mature financial markets like the inverse-cubic dependence, a sufficiently high trading frequency is required. From the vantage point of the s, for the most liquid BTC/USD exchange rate on the Bitstamp platform, this was achieved in 2014; by contrast, on the Kraken the exchange the rates involving some of the least-liquid cryptocurrencies appear to be still in a “pre-cubic” immature phase.

3.4 Temporal autocorrelations

Another standard characteristic used to describe the financial returns is the autocorrelation function

| (2) |

where denotes the time-average. A typical behaviour of for the financial returns is its immediate decay either to zero or to below zero [107, 6, 108, 109, 23]. However, the autocorrelation function of volatility (i.e., absolute value of the returns) decays with an increasing according to a power law [110, 6, 111, 112, 113, 23]. The decay range corresponds to the average width of the volatility clusters [114]. This phenomenon, which can be observed across all markets, is a manifestation of long-term memory [96]: large fluctuations are statistically followed by large ones and small fluctuations by small ones [2]. The long-range autocorrelation, which is a linear effect in volatility, becomes a nonlinear correlation from the perspective of returns. Importantly, this implies that the returns can reveal multiscaling (see Section4).

It should be borne in mind that the autocorrelation function is a well-defined quantity only insofar as the data are drawn from a stationary process. Thus, if there is a trend in the data, it has to be removed beforehand. This also includes trivial periodic patterns. In the high-frequency financial data, one observes, for example, significant seasonal trends in volatility, including daily trends, weekly trends, and some longer-period trends. It is well-established that a satisfactory method of trend removal entails dividing each return corresponding to a time-point by the standard deviation of the returns calculated for the same moment over a sufficient number of trading days, i.e., , where indexes the intervals starting from the market opening.

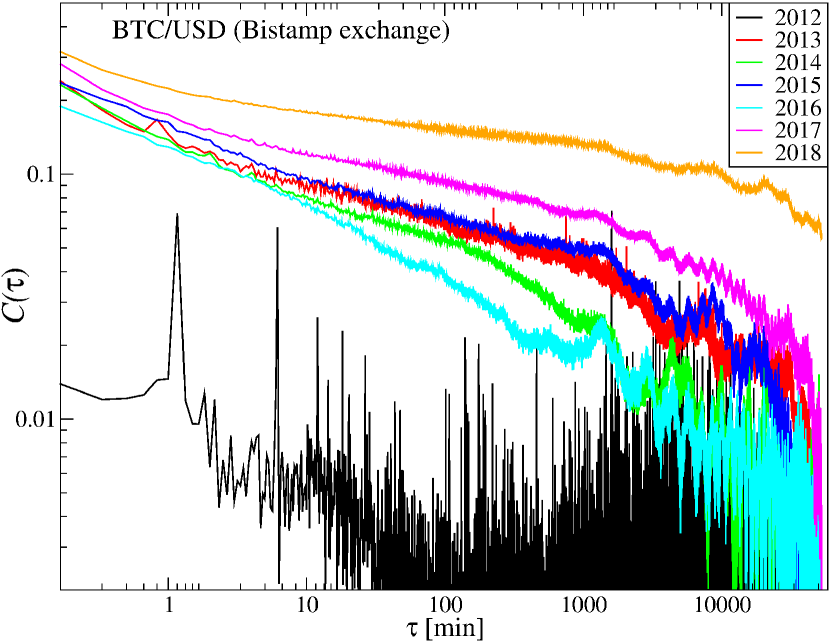

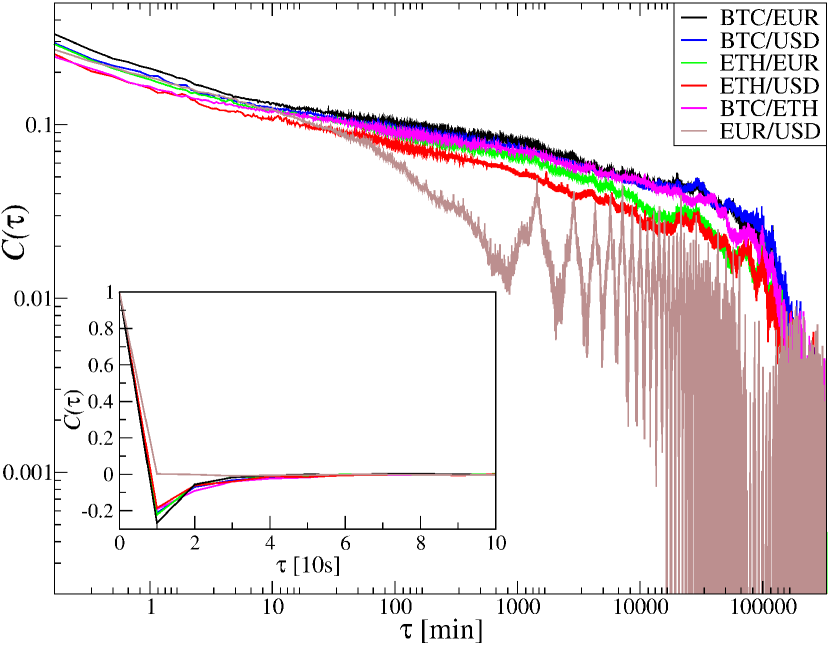

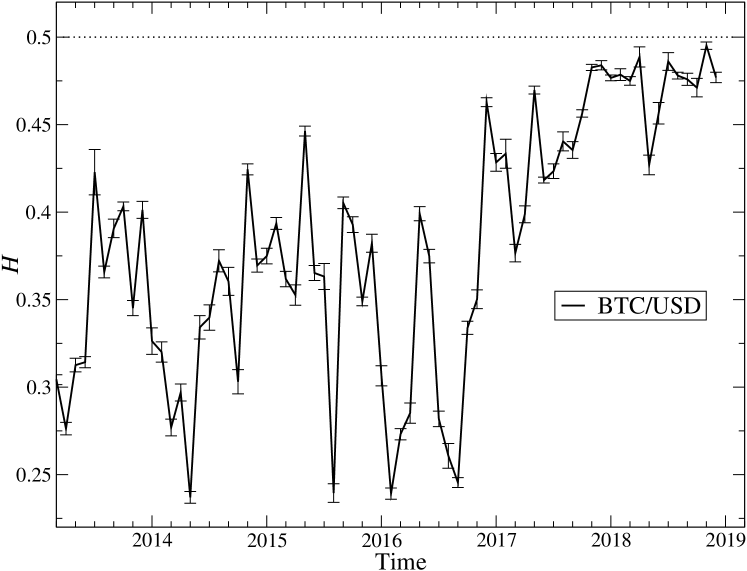

Figure 17 shows the autocorrelation function calculated for the BTC/USD volatility time-series split into annual parts. The quotes from the Bitstamp platform were first converted to absolute logarithmic returns, then detrended to remove seasonality. Similar to the CDF tails, a significant shift in the autocorrelation is observed between 2012 and the subsequent years. In the former, is only short-range correlated, with memory disappearing after a few minutes. However, long-range memory has a power-law form: accordingly, started to emerge already in 2013 and was systematically built up to reach substantial strength even for intervals as long as min by 2018. The effect of increasing the volatility autocorrelation time can be explained in terms of the increasing number of transactions carried out in a time unit.

The long-range, linear autocorrelation in volatility corresponds to non-linear correlations on the level of signed returns. In turn, non-linear correlations are responsible for the multifractal effects (see Sect. 4).

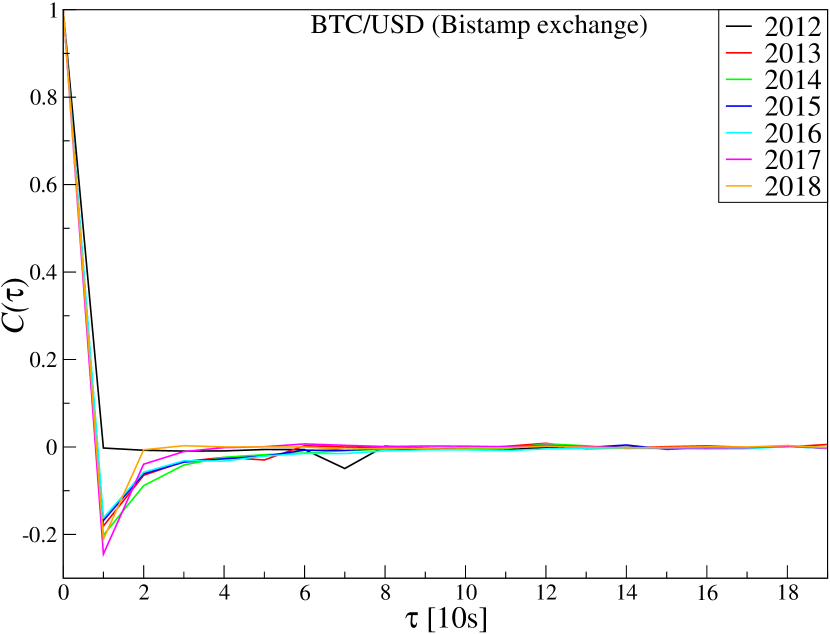

On the other hand, the autocorrelation function calculated for the original, signed returns does not indicate any linear memory effects for s (Figure 18). A negative value of is a statistical artifact related to isolated price jumps followed by price regression to a former level; these events are frequent on sampling frequencies comparable to the average inter-transaction interval. The observed autocorrelation function behavior for both returns and volatility resembles their counterparts on the other mature markets.

The volatility autocorrelations function for the BTC and ETH expressed in USD and EUR, as well as for BTC/ETH (Kraken), are displayed in Figure 19. For all cryptocurrency exchange rates under consideration, it decays with approximately according to a power-law up to about a week. However, in the case of EUR/USD (Dukascopy) the power-law regime breaks after already about one day, which can be accounted for by a shorter volatility-cluster length. This effect can be seen in Figure 20, where with s are shown for six exchange rates over the analyzed period. For the rates involving cryptocurrencies, the cluster length is an order of magnitude larger than for EUR/USD. Five cycles of high/low volatility during a week can be distinguished for the EUR/USD, while only three cycles per month are visible for the cryptocurrencies (insets in Fig. 20). Again, this can be explained by a higher trading frequency on the Forex than on Kraken. The average inter-transaction time is a few seconds on Kraken, whereas Forex transactions take place at least an order of magnitude faster.

Similarly to Bitstamp BTC/USD data, and indeed to all mature financial markets, the autocorrelation function for the returns (inset in Fig. 19) drops immediately to zero for the EUR/USD and even below zero for the cryptocurrency rates, indicating that no linear correlation exist for the signed returns.

The difference in average trading frequency between Binance and Kraken affects not only the return CDFs but also the volatility autocorrelation function. In both cases, one observes its power-law decay (Figure 21), but on Binance, it is faster: it breaks down already after about 1,000 minutes as opposed to about 10,000 on Kraken. In the case of signed returns, the autocorrelation function exhibits a typical behavior: it immediately drops to negative values and then oscillates around zero (not shown).

4 Multiscale correlations

The commonly used correlation measures in time-series analysis, such as the autocorrelation function, the spectral density [115] and the Pearson correlation coefficient [116], only provide information about linear interdependencies in the data. However, a typical feature of financial markets is the occurrence of nonlinear correlations [96, 117], which are the primary source of multifractality in their temporal dynamics (an additional factor reinforcing multifractality is related to the “fat tails” of the probability density function) [118, 119, 120, 121, 122, 117]. Multifractality is an attribute of many complex systems wherein a sufficiently large number of elements interact according to nonlinear laws [123]. This kind of system organization is a well-evident characteristic of the financial markets, which in this study are represented by the cryptocurrency market.

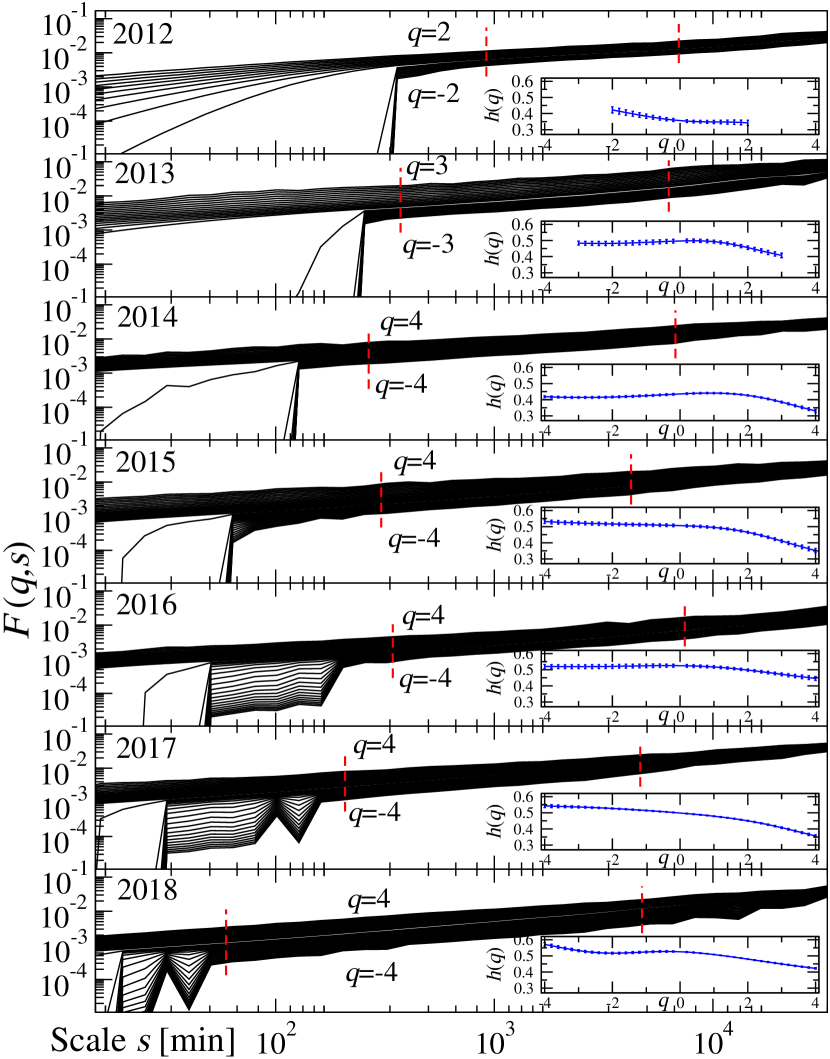

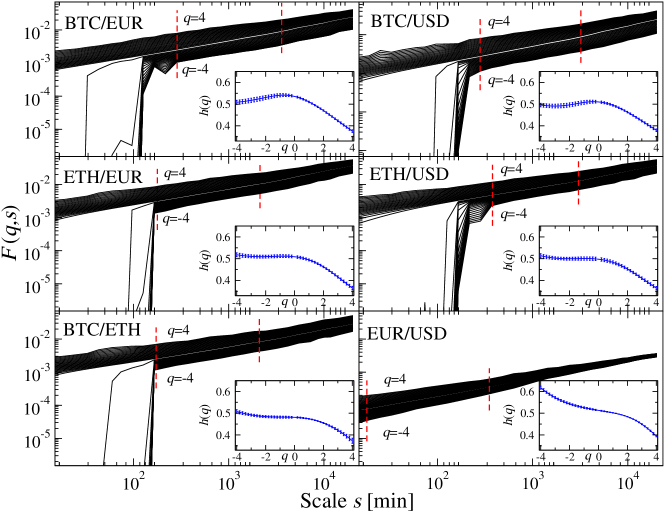

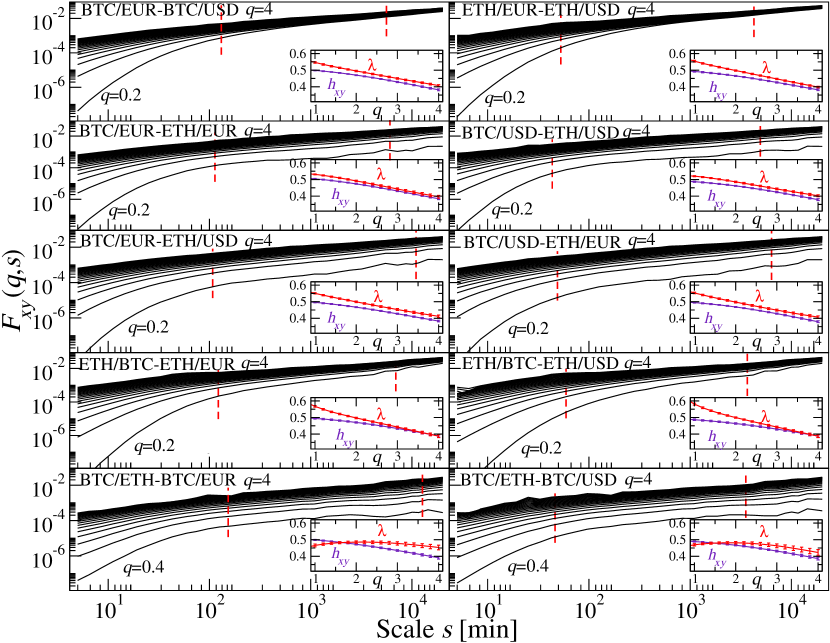

In Section 3.4, it was demonstrated that the power-law decay of the autocorrelation function estimated for absolute values of the log-returns reveals nonlinear correlations. Therefore, signatures of multiscaling can also be anticipated in the cryptocurrency market. In the following section, advanced methods for the quantitative description of nonlinear correlations based on the multifractal methodology will be presented: namely, the multifractal detrended fluctuation analysis (MFDFA), its generalization for the cross-correlation case, known as multifractal cross-correlation analysis (MFCCA), and the -dependent detrended cross-correlation coefficient . The analyses of the time-series data from the cryptocurrency market were carried out through these methods.

4.1 Detrending based multifractal methodology

Historically, the first method for analyzing fractal time-series is the rescaled range analysis (R/S), proposed by the British hydrologist Harold Edwin Hurst [124]. In his original work, Hurst introduced and applied the R/S algorithm to study the recurrent flooding on the river Nile. In the case of nonstationary data, to correctly quantify correlations in a signal, it is necessary to identify and remove trends, which is impossible to attain using the R/S algorithm. To address this fundamental shortcoming, in 1995, Peng et al. proposed the detrended fluctuation analysis (DFA), which can be applied to nonstationary data [125, 126]. Within the DFA method, the trend represented by the -th degree polynomial is subtracted. This procedure leads to the removal of nonstationarity from the data. However, the choice of the polynomial degree is crucial to obtain reliable results. If the polynomial degree is too high, the procedure could destroy the fluctuation structure. On the other hand, with too low a degree, the polynomial may not remove nonstationarity effectively [126, 127]. In most cases, a second-order polynomial is used for the analysis of financial data. Alternatives have been discussed in Ref. [127].

Multifractal detrended fluctuation analysis (MFDFA) is a more recent development of the DFA algorithm, covering the case of nonlinear correlations case [128]. Using the MFDFA, the nonlinear organization in a time-series is quantitatively described within a fractal formalism. In recent years, cross-correlation versions of the DFA and MFDFA methods have also been proposed. The generalization of the DFA to the cross-correlation case is known as the detrended cross-correlation analysis (DCCA) method [129], whereas multifractal detrended cross-correlation analysis (MF-DXA) is an extension of the MFDFA [119].

In the latter case, since the cross-correlation fluctuation function may assume positive and negative values, proposed formulas, related to calculation of the moments, lead to erroneous conclusions. To avoid this effect, many authors resort to taking the absolute values of the cross-correlation fluctuations functions, which, in turn, risks leading to the artifactual detection of multifractal cross-correlations even for uncorrelated signals [130]. A solution to this problem is offered by the multifractal cross-correlation analysis (MFCCA) algorithm, which has been proposed in Ref. [130].

An alternative to the DFA-based methods of quantifying multiscale correlations is provided by the algorithms using wavelet transforms like, e.g., the wavelet transform modulus maxima (WTMM) [131, 132, 133] and the multifractal cross-wavelet transform (MFXWT) [134] for the auto- and cross-correlation cases, respectively. However, this is MFCCA that is currently deemed to be the most reliable method for studying the multiscale correlations in the time series [135, 114].

The robustness of the time-series analysis carried out by means of the multifractal methodology has fuelled considerable popularity of the corresponding methods, and their application throughout highly diversified scientific fields [123] such as biology [136, 137], chemistry [138, 139], physics [140, 141], geophysics [142, 143], hydrology [144, 145], quantitative linguistics [146, 147], medicine [148, 149], meteorology [150, 151], music [152, 153], psychology [154, 155] and especially finance [156, 157, 158, 159, 160, 161, 162, 117].

Notwithstanding the broad application of the multifractal methodology, it must be noted that their proper application and drawing conclusions require certain experience, otherwise some serious misinterpretation of results might occur. One needs to realize that not all indications of multiscaling found in data may be considered an actual manifestation of multifractality in the strict mathematical sense. It was shown in literature that multiscaling can also be a finite-sample effect especially if the analyzed data has a fat-tail PDF [114]. In many instances of empirical data, including the financial data, multiscaling is observed over rather a moderate range of available scales like, e.g., one decade, while at the remaining scales other effects can be seen, like an exponential cut-off of the PDF tails or the outlier events, which do not fit into any fractal organization of the data. The multifractal methodology allows one for a reliable and convenient quantitative description of the temporal organization of nonstationary signals, including the heterogeneity of their singularities, while only sometimes it also allows for undoubted identification of a genuine multifractal structure.

4.1.1 MFCCA as a generalization of MFDFA and DCCA

The multifractal cross-correlation analysis (MFCCA) [130] allows for quantitative description of both the scaling properties of data and the degree of multiscale detrended cross-correlation between two time series. Given two time-series , , where , corresponding profiles are calculated according to

| (3) |

where and denote the means of the and time-series, respectively.

Then, the profiles and are divided into separate segments with length , starting at the beginning and at the end of the time-series, where . In each segment , a trend is identified by fitting a polynomial of degree , separately for the series – i – . As said, for financial time-series a typical choice is [135]. After removing the trend, cross-covariance is calculated

| (4) |

for segment and

| (5) |

for , and subsequently it is used to calculate the -th order covariance function [130]

| (6) |

where denotes the sign of . Fractal detrended cross-correlation between two time-series i is manifested in the scaling relationship

| (7) |

where and are the scaling exponents. The parameter acts as a filter which strengthens or suppresses the covariance calculated on segments having length . For positive , segments containing large fluctuations have a predominant impact on the sum in Eq.(6), whereas for negative , segments with small fluctuations dominate in . In the presence of multifractal cross-correlation, a dependence of on is observed, whereas for the monofractal case, is independent of .

Multifractal analysis of a single time-series by means of MFDFA [128] corresponds to a special case of the MFCCA procedure, wherein . Then Eq.(6) is reduced to

| (8) |

As in Eq.(7), fractality manifests itself in a power-law relation

| (9) |

where is the generalized Hurst exponent, which for corresponds to standard Hurst exponent [163]. In the case of a monofractal time series, is constant, whereas for a multifractal one, depends on . In the latter case, the time series reveals a sort of hierarchical organization of the returns [164].

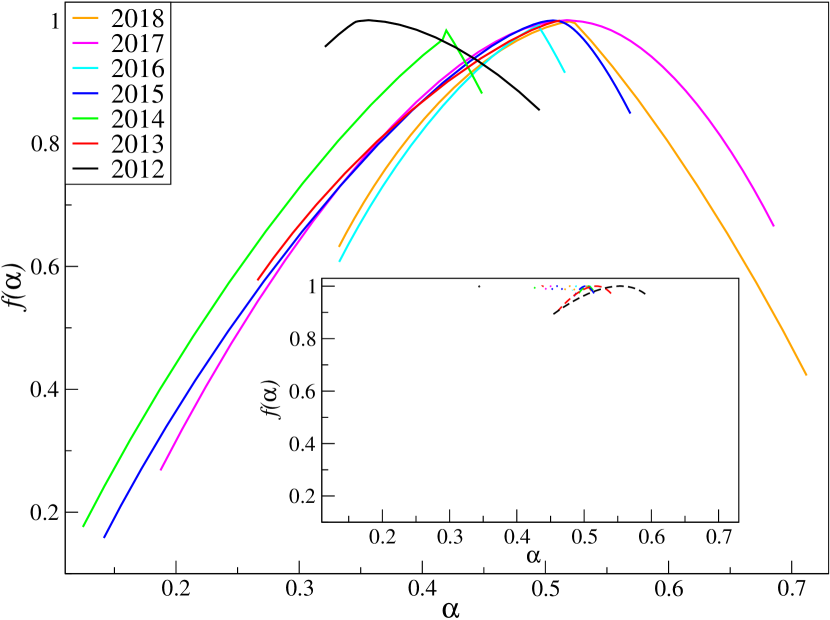

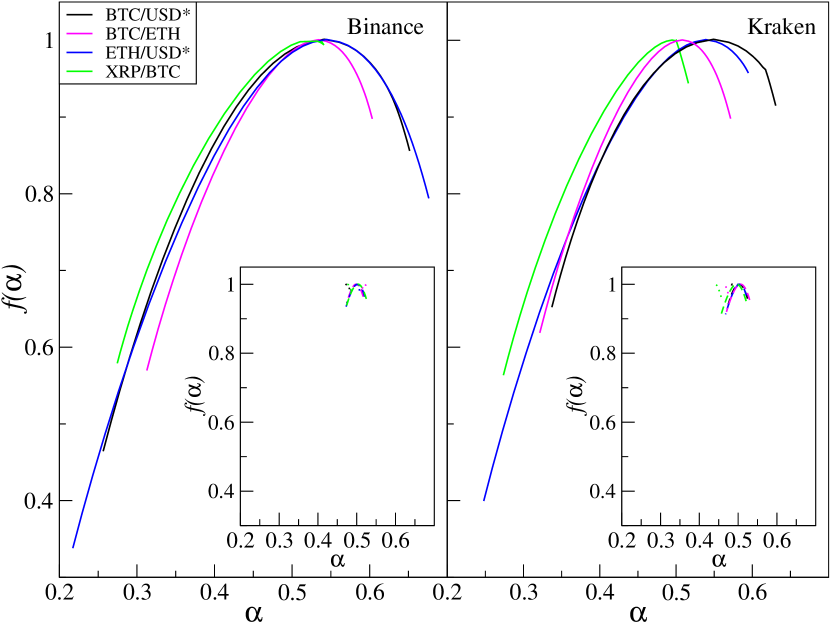

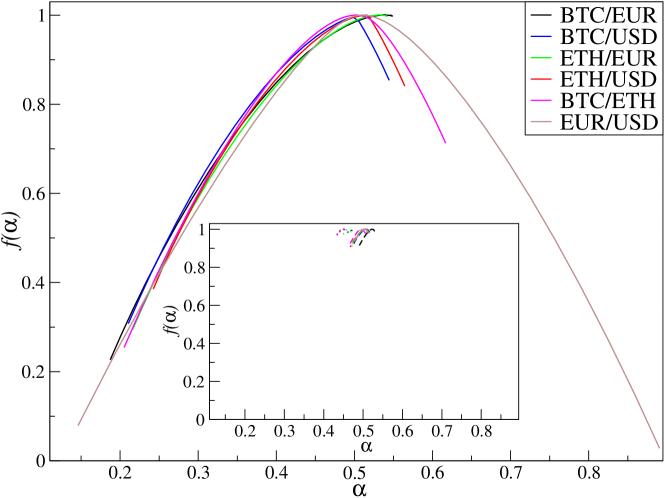

The singularity spectrum can be calculated by a Legendre transform:

| (10) |

where is the Hölder exponent, and is fractal dimension of the time series points with singularities . In the case of multifractals, the shape of the singularity spectrum characteristically resembles an inverted parabola.

Width of the singularity spectrum

| (11) |

where and are the minimum and maximum values of , is a quantity intended to measure the diversity of singularities present in time series. Even if the scaling range in of the fluctuation functions is limited to a decade or so and, thus, no actual multifractal structure exists in correlation of the time series, remains a convenient quantity to assess the detrended correlation heterogeneity.

Another important feature of the spectrum is its asymmetry (skewness), which can be measured by the asymmetry coefficient [164]

| (12) |

where , , and corresponds to the maximum value observed for . A positive coefficient denotes a left-sided asymmetry of the spectrum. This corresponds to a more developed multiscaling (stronger correlations) at the level of large fluctuations. In turn, a negative value of denotes a right-sided asymmetry, implicating small fluctuations as the dominant source of multiscaling.

To assess the strength of multifractal cross-correlation, the scaling exponent and the average of generalized Hurst exponents calculated for each time series separately

| (13) |

have to be compared. Thus, the difference between and is calculated

| (14) |

For perfect multiscale cross-correlation, , whereas for desynchronization between the time-series, [71, 98]. Additional notions about are given in Subsect. 4.1.3.