Off-Policy Interval Estimation with

Lipschitz Value Iteration

Abstract

Off-policy evaluation provides an essential tool for evaluating the effects of different policies or treatments using only observed data. When applied to high-stakes scenarios such as medical diagnosis or financial decision-making, it is crucial to provide provably correct upper and lower bounds of the expected reward, not just a classical single point estimate, to the end-users, as executing a poor policy can be very costly. In this work, we propose a provably correct method for obtaining interval bounds for off-policy evaluation in a general continuous setting. The idea is to search for the maximum and minimum values of the expected reward among all the Lipschitz Q-functions that are consistent with the observations, which amounts to solving a constrained optimization problem on a Lipschitz function space. We go on to introduce a Lipschitz value iteration method to monotonically tighten the interval, which is simple yet efficient and provably convergent. We demonstrate the practical efficiency of our method on a range of benchmarks.

1 Introduction

Reinforcement learning (RL) (e.g., Sutton & Barto, 1998) has become widely used in tasks like recommendation system, robotics, trading and healthcare (Murphy et al., 2001; Li et al., 2011; Bottou et al., 2013; Thomas et al., 2017). The current success of RL highly relies on excessive amount of data, which, however, is usually not available in many real world tasks where deploying a new policy is very costly or even risky. Off-policy evaluation (OPE) (e.g., Fonteneau et al., 2013; Jiang & Li, 2016; Liu et al., 2018a), estimating the expected reward of a target policy using observational data gathered from previous behavior policies, therefore holds tremendous promise for designing data-efficient RL algorithms by leveraging on previously collected data.

Existing OPE methods mainly focus on point estimation, which only provides a single point estimation of the expected reward. However, such point estimate can be rather unreliable as OPE often suffers from high error due to the lack of historical samples, policy shift or model misspecification. Further, for applications in high-stakes areas such as medical diagnosis and financial investment, a point estimate itself is far from enough and can even be dangerous if it is unreliable. Hence, it is essential to provide provably correct interval estimation of the expected reward, which is both trustful and theoretically correct.

To address this problem, we propose a general optimization-based framework to derive a provably correct off-policy interval estimation based on historical samples. Our idea is to search for the largest and smallest possible values of the expected reward, among all the Q-functions in a Lipschitz function space that are consistent with the observed historical samples. This interval estimator is provably correct once the true Q-function satisfies the Lipschitz assumption.

Computing our upper and lower bounds amounts to solving a constrained optimization problem in the space of Lipschitz functions. We introduce a Lipschitz value iteration algorithm of a similar style to value iteration. Our method is efficient and provably convergent. In particular, our algorithm has a simple closed form update at each iteration and is guaranteed to monotonically tighten the bounds with a linear rate under mild conditions. To speed up the algorithm, we develop a double subsampling strategy, which we only pick a random subsample of value functions to update in each iteration and use the same batch of data as constraints.

We test our algorithm on a number of benchmarks and show that it can provide tight and provably correct bounds.

Related Work Our work is closely related to the off-policy point estimation. There are typically two types of OPE methods, importance sampling (IS) based methods (e.g., Liu, 2001; Precup et al., 2000; Liu et al., 2018a; Xie et al., 2019) and value function or model based methods (e.g., Fonteneau et al., 2013; Liu et al., 2018b; Le et al., 2019; Feng et al., 2019) Another line of work combines these two methods and yields a doubly-robust estimator for off-policy evaluation (Jiang & Li, 2016; Thomas & Brunskill, 2016; Kallus & Uehara, 2019; Tang et al., 2020). In this work, we consider the black box setting when the behavior policy is assumed to be unknown (e.g., Nachum et al., 2019; Mousavi et al., 2020; Zhang et al., 2020; Feng et al., 2020).

IS-based point estimation methods naturally yield a confidence interval by standard concentration (Thomas et al., 2015b, a). Another major type of confidence interval estimation approaches leverages the statistical procedure of bootstrapping (White & White, 2010; Hanna et al., 2017). However, these confidence intervals are typically loose due to the curse of horizon. Moreover, they heavily rely on the assumption that the off-policy data is drawn i.i.d. from a particular behavior policy. But this is not always true since the policies usually evolve and depend on their previous policies.

Another related set of works are PAC-RL (e.g., Jin et al., 2018; Dann et al., 2018; Song & Sun, 2019; Yang et al., 2019), which mainly focus on the regret bound or sample complexity of the Q-learning exploration. As a side product, they also provide a confidence interval estimation for the value function. However, this line of work mostly focuses on the tabular or linear MDPs. In contrast, our work aims to handle the general continuous MDPs by leveraging Lipschitz properties of Q-functions. Song & Sun (2019) provides a metric embedding style Q-learning method, with a particular focus on finite horizon settings.

2 Background and Problem Settings

We firstly set up the problem of off-policy interval evaluation and then introduce the related background on Q-learning and Bellman equation.

Markov Decision Process A Markov decision process (MDP) consists of a state space , an action space , an unknown deterministic reward function , an unknown transition function , an initial state distribution , and a discounted factor . Throughout this work, we assume that the transition and reward function are deterministic for simplicity and we can easily draw samples from the initial state distribution .

In RL, an agent acts in a MDP following a policy , which prescribes a distribution over the action space given each state . Running the policy starting from the initial distribution yields a random trajectory , where represent the state, action, reward at time respectively. We define the infinite horizon discounted reward of as where is a discounting factor; is the horizon length of the trajectory, which we assume to approach infinite, hence yielding an infinite horizon problem; denotes the expectation of the random trajectories collected under the policy .

Black Box Off-Policy Interval Estimation We are interested in the problem of black-box off-policy interval evaluation, which requires arguably the minimum assumptions on the off-policy data. It amounts to providing an interval estimation of the expected reward of a policy (called the target policy), given a set of transition pairs collected under a different, unknown behavior policy, or even a mix of different policies; here and denote the next state and the local reward following respectively.

Q-function and Bellman Equation We review the properties of the Q-function that is most relevant to our work. The Q-function specifies the expected reward when following from the state-action pair and is known to be the unique fixed point of the Bellman equation:

| (1) |

where denotes the Bellman operator, and is the transition operator defined by

| (2) |

An expected reward associated with a Q-function is defined via

| (3) |

where we use to denote the joint initial state-action distribution.

Off-Policy Q-Learning Q-function can be learned in an off-policy manner. Assume we have a set of transition pairs . Under the assumption of deterministic transition and reward, we can estimate the Bellman operator on each of the data point:

which can be estimated with an arbitrarily high accuracy via drawing a large number of samples from . Assume belongs to a class of functions , we can estimate by finding a that satisfies the Bellman equation on the data points:

| (4) |

Compared with the exact Bellman equation (1), we only match the equation on the observed data (4), which may yield multiple or even infinite solutions of . Therefore, the function class needs to be sufficiently constrained in order to yield meaningful solutions. In practice, (4) is often solved using fitted value iteration (Munos & Szepesvári, 2008), which starts from an initial , and then perform iterative updates by

| (5) |

It is easy to see . With an estimation of , the expected reward in (3) can be estimated by Monte Carlo sampling from and .

3 Main Method

We now introduce our main framework for providing provably correct upper and lower bounds of the expected reward. For notation, we use to represent a state-action pair.

3.1 Motivation and Optimization Framework

When the fitted value iteration in (5) converges, it only provides one Q-function that yields a point estimation of the reward. To get an interval estimation, we expect the fitted value iteration to provide two Q-functions and , such that all possible consistent with the data points lie between and , e.g. , where means .

More concretely, consider a function set that is expected to include , we construct an upper bound of by

| (6) |

where is defined in (3). It is easy to see that if holds; this is because satisfies the constraints in the optimization, and hence as a result of the optimization.

It is worthy to note that we use the Bellman inequality constraint in (6), which would not cause any looseness compared to the equality constraint. To see this, note that the exact reward can be framed into (Bertsekas, 2000)

which implies that would converge to as data points increase.

We can construct the lower bound in a similar way:

| (7) |

Define as the interval estimation for , once the true lies in the function space , lies in provably.

Benefits of Our Framework Our optimization framework enjoys several advantages compared with the existing methods. First of all, unlike the standard concentration bounds, our bounds do not rely on the i.i.d. assumption of transition pairs . In RL settings, the historical transition pairs are highly dependent to each other: on one hand, in sequential data stream, the current step of state is the next state in the previous step; on the other hand, the behavior policy that generates the trajectories is also evolving during the learning process. Secondly, under our optimization framework, more data would enable us to add more constraints in our searching space and therefore get tighter bounds accordingly. This property allows a trade-off between the time complexity and the tightness of the bounds, which we will further discuss in section 4.1. Last but not least, the tightness of the bounds depends on the capacity of the function space , which naturally yields the nice monotonicity property. It is easy to see if , we will have .

Lipschitz Function Space

To implement this framework, it is important to choose a proper function set and solve the optimization process efficiently. Intuitively, should be rich enough to include the true value function, but not be too large to cause the bounds to be vacuous. In light of this, we propose to use the space of Lipschitz functions. Let be a metric space equipped with a distance . We propose to take to be a ball in the Lipschitz function space:

| where | (8) |

where is the Lipschitz norm of and is a radius parameter.

Although the Lipschitz space yields an infinite dimensional optimization, our key technical contribution is to show that it is possible to calculate the upper and lower bounds with an efficient fixed point algorithm. We form it as an optimization problem and solve it efficiently in a value iteration like fashion. In addition, in Section 3.4, we show that the size of the Lipschitz space enables us to establish a diminishing bound on the gap of the upper and lower bounds.

3.2 Optimization in Lipschitz Function Space

We propose a novel value iteration-like algorithm for solving the optimizations in (6) and (7). We focus on the upper bound (6), as the case of the lower bound is similar and discussed in Appendix A.

Our algorithm enjoys the same spirit as the fitted value iteration (5). We apply the Bellman operator on the current estimation of , and then use it as the constraint on the Bellman inequalities to obtain a new estimation.

Specifically, starting from an initial with , at the -th iteration, we update by

| (9) |

This update requires to solve a constrained optimization on the space For our choice of the Lipschitz function space, this yields a simple closed form solution.

Proposition 3.1.

Suppose , consider the optimization in (9) with . We have

| (10) |

Intuitively, in (10) yields an

upper envelope of all the possible Lipschitz functions that satisfy , and hence solves the optimization in (9), as is monotonically increasing with . The updates for the lower bound can be derived similarly by calculating the lower envelopes:

| (11) |

3.3 Convergence Analysis

Our algorithm enjoys two important and desirable properties: one is monotonic convergence, which indicates that you can stop any time, depending on your time budget, and still get a valid lower/upper bound; the other is linear convergence, which implies that it only needs logarithmic time steps to converge. Thanks to these properties, our method is much faster compared to directly solving the convex optimization in (6) with (stochastic) sub-gradient ascent.

The monotonic convergence relies on the initial upper bound we pick, which is inspired by the monotonicity of the Bellman operator. See Appendix B.1 for more details.

Theorem 3.2.

We establish a fast linear convergence rate for the updates in (10). The convergence result here does not need the initialization of .

Proposition 3.3.

Following the updates in (10) under arbitrary initialization, with constant we have

3.4 Tightness of Lipschitz-Based Bounds

We provide a quantitative estimation of the gap between the upper and lower bounds when using the Lipschitz function set. We show that it depends on a notion of the covering radius of the data points in the domain.

Theorem 3.4.

Let be the Lipschitz function class with Lipschitz constant . Suppose is a compact and bounded domain equipped with a distance . For a set of data points , we have

where is the discount factor and is the covering radius.

Typically, the covering radius in a bounded and compact domain asymptotically grows with , where is an intrinsic dimension of the domain (Cohen et al., 1985), if the support of the data distribution (where is getting from) covers , the stationary distribution of policy . This shows that the bound gets tighter as the number of samples get larger, but may decay slowly when the data domain has a very high intrinsic dimension. While it is possible to choose smaller space sets (such as RKHS) to obtain smaller gaps, it would sacrifice other properties such as capacity and simplicity.

4 Practical Considerations

We discuss some practical concerns of Lipschitz value iteration in this section.

4.1 Accelerating with Stochastic Subsampling

If we draw samples to estimate when updating with equation (10), we need times of calculations for each round. This comes from two sources, one is the updating of all terms of in each iteration, and the other is taking the maximum/minimum among all upper/lower curves when we calculate the upper/lower envelope function of . This is quadratic to the number of samples and therefore computationally expensive as the sample size grows large.

To tackle this problem, we propose a fast random subsampling technique. Instead of updating all in each iteration, we pick a batch of subsamples to update, where is a subset with fix size . The benefit of subsampling is that we can trade-off between time-complexity and tightness.

To be more precise, we can write down the new update scheme as follow:

| (14) | ||||

where is the sub-sample set in the iteration. A similar monotonic result can be shown in sequel.

Proposition 4.1.

We summarize the strategy in Algorithm 2.

The subsampling algorithm only needs time complexity in each iteration. Although this strategy does not converge to the exact optimal solution , it still gives valid (despite less tight) bounds. In the numerical experiments, we find that once the size of subsample set is sufficiently large, we get almost the same tightness as the exact optimal bounds.

4.2 On Estimating Lipschitz Norm

The only model assumption we need to specify is the function set ; we want , but not to be too large, since the estimated interval gets loose as increases. However, compared to other value-based function approximation methods that also need assumptions on model specification, our non-parametric Lipschitz assumption is obviously very mild.

In order to set hyperparameter , we would like to estimate the upper bound of , which is typically non-identifiable purely from the data. This is because, given a sufficiently large , we can always find a function that satisfies all the Bellman constraints with by twisting with a small function; see appendix C for more details. However, if we know or can estimate the Lipschitz norm of the reward and transition functions, then it is possible to derive a theoretical upper bound of with only mild assumptions.

Relative log mean error

|

Relative Reward

|

|

|

|---|---|---|---|

| number of trajectories | number of trajectories | Subsample Size | State |

| (a) | (b) | (c) | (d) |

Proposition 4.2.

Let be a metric space for state action pair and be a metric space for state . Suppose is separable so that if . If the reward function and the transition are both Lipschitz in the sense that

We can prove that if , we have

| (15) |

when is a constant policy. Furthermore, for optimal policy with value function , we have:

| (16) |

Theorem 4.2 suggests that if our target policy is close to the optimal, we can set if we can estimate and . This provides a way for estimating the upper bound of the Lipschitz norm of by leveraging the Lipschitz norm for the reward and transition functions. In practice, we can estimate and using historical data:

| (17) |

Diagnosing Model Misspecification from Data

Since the empirical maximum tends to underestimate the true maximization, simply using Proposition 4.2 may still underestimate the true Lipschitz norm. Luckily, we can diagnose if is too small to be consistent with data by only adding a few lines of diagnosis codes.

From Theorem 3.2 we know that for all , which are consistent with the finite sample Bellman equations, we have . Thus, if at some time (or after convergence), we find that for some , we can reject the following hypothesis:

In this way, we can see that . Then, we can increase by a constant factor and rerun our upper/lower bound algorithm. Note that we do not need to compare an infinite number of to check , as and . And hence, it is sufficient to check if there exists an index such that .

Relative Reward

|

|

Relative Reward

|

|

|---|---|---|---|

| number of trajectories | Subsample Size | number of trajectories | Subsample Size |

| (a) | (b) | (c) | (d) |

5 Experiments

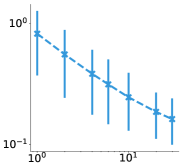

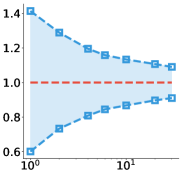

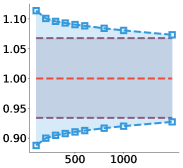

We test our algorithms in different environments. We follow Algorithm 2 with sub-sampling technique. In each environment, we evaluate the tightness of our bound by changing 1) the number of samples and 2) subsampling size . We also make a comparison with the exact bound with full sample size (i.e. ). We start hyperparameter estimated by Proposition 4.2 with empirical maximal, and use diagnose algorithm in the last section to gradually increase until it is consistent with data set where we set the increasing factor . We observed that diagnosis algorithm usually passes with the very initial . As a baseline, Thomas et al. (2015b) needs huge amounts of samples to get comparable tight bounds as ours, we demonstrate a comparison experiment in Appendix D.

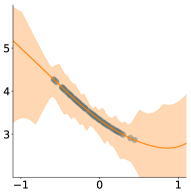

Synthetic Environment with A Known Value Function We consider a simple environment with one dimension state space and one dimension action space with a linear transition function. Given a target policy , we enforce our value function to be our predefined function. This is done by enforcing the reward function for this environment as the reverse Bellman error of , with be the transition operator in equation (2). We use Euclidean distance metric and under this metric we can prove that the Lipschitz constant is . See Appendix D for more details.

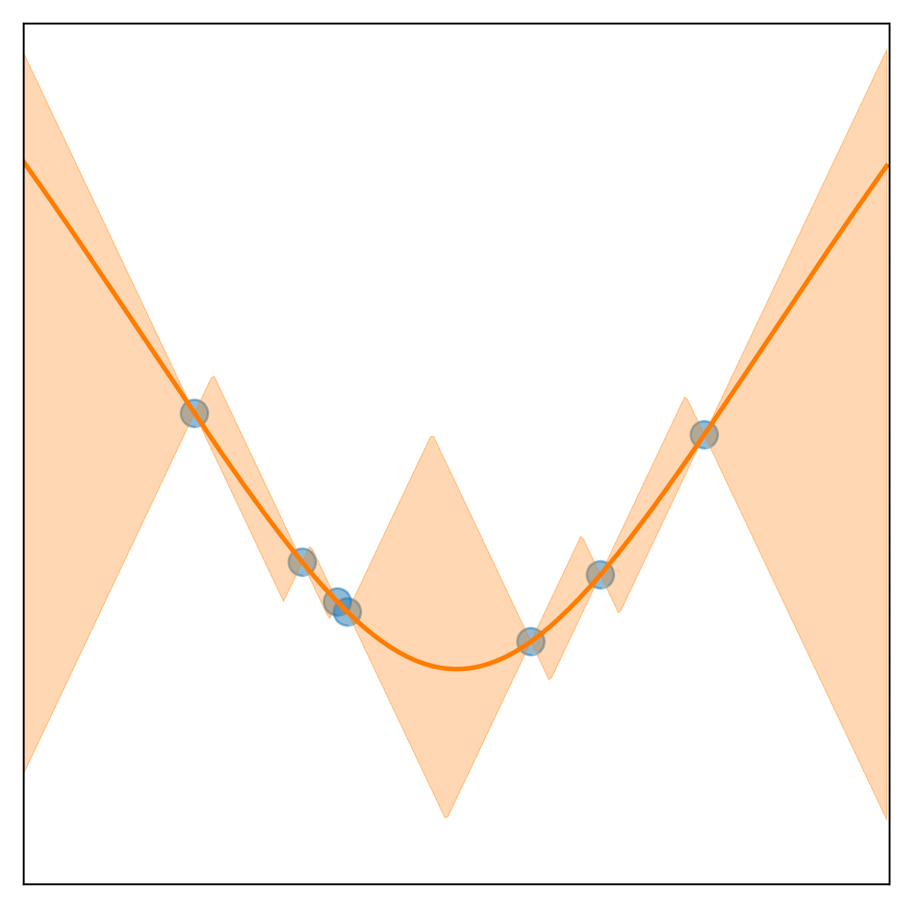

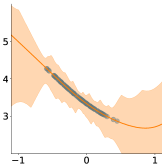

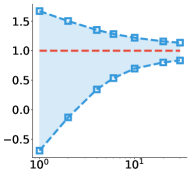

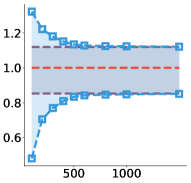

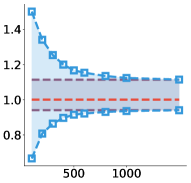

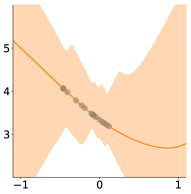

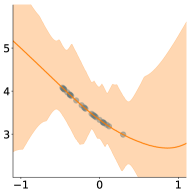

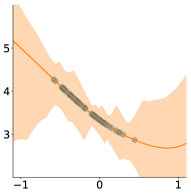

All the reported results are average over 300 runs using the following setting by default: number of trajectory Horizon length , discounted factor , Lipschitz constant and subsample size . We run Lipschitz value iteration for iteration to ensure almost convergence. From Figure 2(a)(b) we can see that as the number of sample size gets larger, the bound gets tighter. 2(c) indicates that with a sufficiently large subsample size, e.g. , we can achieve bounds accurately enough compared to whole sample algorithm (purple lines). We also demonstrate the landscape of evaluation for state value function and under the final Lipschitz value iteration for 100 data samples. Compare with the true value function, we can see that we get a tighter bound on a neighborhood region of data points compared to unseen region.

Pendulum Environment We demonstrate our method on pendulum, which is a continuous control environment with state space of and action space on interval . In this environment, we aim to control the pendulum to make it stand up as long as possible (for the large discounted case), or as fast as possible (for small discounted case). See Appendix D for more experimental setups.

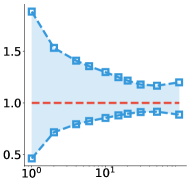

Figure 3(a)(b) shows a similar result indicating our interval estimation is tight and subsampling achieves almost same tightness with full samples.

HIV Simulator The HIV simulator described in Ernst et al. (2006) is a continuous state environment with 6 parameters and a discrete action environment with total 4 actions. In this environment, we seek to find an optimal drug schedule given patient’s 6 key HIV indicators. The HIV simulator has richer dynamics than the previous two environments. We follow Liu et al. (2018b) to learn a target policy by fitted Q iteration and use the -greedy policy of the Q-function as the behavior policy.

6 Conclusion

We develop a general optimization framework for off-policy interval estimation and propose a value iteration style algorithm to monotonically tighten the interval. Our Lipschitz value iteration on the continuous settings MDP enjoys nice convergence properties similar to the tabular MDP value iteration, which is worth further investigating. Future directions include leveraging our interval estimation to encourage policy exploration or offline safe policy improvement.

Broader Impact

Off-policy interval evaluation not only can advise end-user to deploy new policy, but can also serve as an intermediate step for latter policy optimization. Our proposed methods also fill in the gap of theoretical understanding of Markov structure in Lipschitz regression. We current work stands as a contribution to the fundamental ML methodology, and we do not foresee potential negative impacts.

Funding Transparency Statement

This work is supported in part by NSF CAREER #1846421, SenSE #2037267, and EAGER #2041327.

References

- Bertsekas (2000) Bertsekas, D. P. Dynamic Programming and Optimal Control. Athena Scientific, 2nd edition, 2000. ISBN 1886529094.

- Bottou et al. (2013) Bottou, L., Peters, J., Quiñonero-Candela, J., Charles, D. X., Chickering, D. M., Portugaly, E., Ray, D., Simard, P., and Snelson, E. Counterfactual reasoning and learning systems: The example of computational advertising. Journal of Machine Learning Research, 14:3207–3260, 2013.

- Cohen et al. (1985) Cohen, G., Karpovsky, M., Mattson, H., and Schatz, J. Covering radius—survey and recent results. IEEE Transactions on Information Theory, 31(3):328–343, 1985.

- Dann et al. (2018) Dann, C., Li, L., Wei, W., and Brunskill, E. Policy certificates: Towards accountable reinforcement learning. arXiv preprint arXiv:1811.03056, 2018.

- Ernst et al. (2006) Ernst, D., Stan, G.-B., Goncalves, J., and Wehenkel, L. Clinical data based optimal sti strategies for hiv: a reinforcement learning approach. In Proceedings of the 45th IEEE Conference on Decision and Control, pp. 667–672. IEEE, 2006.

- Feng et al. (2019) Feng, Y., Li, L., and Liu, Q. A kernel loss for solving the bellman equation. Neural Information Processing Systems (NeurIPS), 2019.

- Feng et al. (2020) Feng, Y., Ren, T., Tang, Z., and Liu, Q. Accountable off-policy evaluation with kernel bellman statistics. In International Conference on Machine Learning, 2020.

- Fonteneau et al. (2013) Fonteneau, R., Murphy, S. A., Wehenkel, L., and Ernst, D. Batch mode reinforcement learning based on the synthesis of artificial trajectories. Annals of Operations Research, 208(1):383–416, 2013.

- Hanna et al. (2017) Hanna, J., Stone, P., and Niekum, S. Bootstrapping with models: Confidence intervals for off-policy evaluation. In Proceedings of the 16th International Conference on Autonomous Agents and Multiagent Systems (AAMAS), May 2017.

- Jiang & Li (2016) Jiang, N. and Li, L. Doubly robust off-policy evaluation for reinforcement learning. In Proceedings of the 23rd International Conference on Machine Learning (ICML), pp. 652–661, 2016.

- Jin et al. (2018) Jin, C., Allen-Zhu, Z., Bubeck, S., and Jordan, M. I. Is q-learning provably efficient? In Advances in Neural Information Processing Systems, pp. 4863–4873, 2018.

- Kallus & Uehara (2019) Kallus, N. and Uehara, M. Efficiently breaking the curse of horizon: Double reinforcement learning in infinite-horizon processes. arXiv preprint arXiv:1909.05850, 2019.

- Le et al. (2019) Le, H., Voloshin, C., and Yue, Y. Batch policy learning under constraints. In International Conference on Machine Learning, pp. 3703–3712, 2019.

- Li et al. (2011) Li, L., Chu, W., Langford, J., and Wang, X. Unbiased offline evaluation of contextual-bandit-based news article recommendation algorithms. In Proceedings of the 4th International Conference on Web Search and Data Mining (WSDM), pp. 297–306, 2011.

- Liu (2001) Liu, J. S. Monte Carlo Strategies in Scientific Computing. Springer Series in Statistics. Springer-Verlag, 2001. ISBN 0387763694.

- Liu et al. (2018a) Liu, Q., Li, L., Tang, Z., and Zhou, D. Breaking the curse of horizon: Infinite-horizon off-policy estimation. In Advances in Neural Information Processing Systems, pp. 5361–5371, 2018a.

- Liu et al. (2018b) Liu, Y., Gottesman, O., Raghu, A., Komorowski, M., Faisal, A. A., Doshi-Velez, F., and Brunskill, E. Representation balancing mdps for off-policy policy evaluation. In Advances in Neural Information Processing Systems, pp. 2644–2653, 2018b.

- Mousavi et al. (2020) Mousavi, A., Li, L., Liu, Q., and Zhou, D. Black-box off-policy estimation for infinite-horizon reinforcement learning. In International Conference on Learning Representations, 2020.

- Munos & Szepesvári (2008) Munos, R. and Szepesvári, C. Finite-time bounds for fitted value iteration. Journal of Machine Learning Research, 9(May):815–857, 2008.

- Murphy et al. (2001) Murphy, S. A., van der Laan, M., and Robins, J. M. Marginal mean models for dynamic regimes. Journal of the American Statistical Association, 96(456):1410–1423, 2001.

- Nachum et al. (2019) Nachum, O., Chow, Y., Dai, B., and Li, L. Dualdice: Behavior-agnostic estimation of discounted stationary distribution corrections. In Advances in Neural Information Processing Systems, pp. 2315–2325, 2019.

- Precup et al. (2000) Precup, D., Sutton, R. S., and Singh, S. P. Eligibility traces for off-policy policy evaluation. In Proceedings of the 17th International Conference on Machine Learning (ICML), pp. 759–766, 2000.

- Song & Sun (2019) Song, Z. and Sun, W. Efficient model-free reinforcement learning in metric spaces. arXiv preprint arXiv:1905.00475, 2019.

- Sutton & Barto (1998) Sutton, R. S. and Barto, A. G. Reinforcement Learning: An Introduction. MIT Press, Cambridge, MA, March 1998. ISBN 0-262-19398-1.

- Tang et al. (2020) Tang, Z., Feng, Y., Li, L., Zhou, D., and Liu, Q. Doubly robust bias reduction in infinite horizon off-policy estimation. In International Conference on Learning Representations, 2020.

- Thomas & Brunskill (2016) Thomas, P. and Brunskill, E. Data-efficient off-policy policy evaluation for reinforcement learning. In International Conference on Machine Learning, pp. 2139–2148, 2016.

- Thomas et al. (2015a) Thomas, P., Theocharous, G., and Ghavamzadeh, M. High confidence policy improvement. In International Conference on Machine Learning, pp. 2380–2388, 2015a.

- Thomas et al. (2015b) Thomas, P. S., Theocharous, G., and Ghavamzadeh, M. High-confidence off-policy evaluation. In Twenty-Ninth AAAI Conference on Artificial Intelligence, 2015b.

- Thomas et al. (2017) Thomas, P. S., Theocharous, G., Ghavamzadeh, M., Durugkar, I., and Brunskill, E. Predictive off-policy policy evaluation for nonstationary decision problems, with applications to digital marketing. In Proceedings of the 31st AAAI Conference on Artificial Intelligence (AAAI), pp. 4740–4745, 2017.

- White & White (2010) White, M. and White, A. Interval estimation for reinforcement-learning algorithms in continuous-state domains. In Advances in Neural Information Processing Systems, pp. 2433–2441, 2010.

- Xie et al. (2019) Xie, T., Ma, Y., and Wang, Y.-X. Optimal off-policy evaluation for reinforcement learning with marginalized importance sampling. Neural Information Processing Systems (NeurIPS), 2019.

- Yang et al. (2019) Yang, L. F., Ni, C., and Wang, M. Learning to control in metric space with optimal regret. arXiv preprint arXiv:1905.01576, 2019.

- Zhang et al. (2020) Zhang, R., Dai, B., Li, L., and Schuurmans, D. GenDICE: Generalized offline estimation of stationary values. In International Conference on Learning Representations, 2020.

Appendix

Appendix A Lower Bound Results

We list all the results for the lower bound here.

A.1 The Lower Bound Value Iteration

Similar to upper bound, the general algorithm for lower bound iteratively finds the lower envelope of the previous points estimation .

| (18) | ||||

For Lipschitz functions, this yields a simple closed form solution.

A.2 Convergence Results

Similar to Theorem 3.2, we have a similar monotonic result for lower bound case.

Theorem A.2.

Similar to the linear convergence property of the upper bound case, we can establish a fast linear convergence rate for the updates in (11).

Proposition A.3.

Appendix B Proofs

We focus on the proofs for upper bounds, all the lower bound proofs follows similarly.

We establish the monotonic convergence of the iterative update in section 3.2. We start with the result for general function spaces and then apply it to the case of Lipschitz functions space, where can ensure that the optimization in (9) is solved by a properly defined upper envelope function.

Definition B.1.

Given a function space on domain and a set of data points , we define the upper envelope function of data points on to be

We say that is upper-self-contained if it is closed (under the infinity norm), and the upper envelope function is contained in for any data points that satisfies .

Similarly, we define the lower envelope function of data points on to be

We say that is lower-self-contained if it is closed (under the infinity norm), and the lower envelope function is contained in for any data points that satisfies .

Similar to contractive operator proof in value iteration, we also define the contractive property of upper/lower envelope operator and .

Definition B.2.

We say and are contractive if for two different sets of points data and , we have,

and

The following lemmas provide key properties for of this special function class. If is upper-self-contained, then the optimization in (9) is solved by the upper envelop function defined above. And similarly, if is lower-self-contained, then the optimization in (18) is solved by the lower envelop function defined above.

Lemma B.3.

Proof.

In addition, the upper and lower envelope functions is monotonic w.r.t. the data labels it goes through.

Lemma B.4.

In an upper-self-contained function space , suppose we have two sets of data points and , and and are their upper envelope functions respectively, and are their lower envelopes functions respectively, if , then we have

Proof.

This is directly from the definition,

where the first inequality holds because the feasible region of constraints is more general than when .

the proof for the lower envelope works similarly. ∎

Lemma B.5.

For a bounded upper-self-contained function class , if the upper envelope operator is contractive, then the maximum solution for the optimization framework equation (6) is the unique solution of the following upper-envelope Bellman equation:

| (22) | ||||

Proof.

Existence

Suppose is a optimum solution for (6), if satisfies equation (22) then we are done. Otherwise satisfies and . Consider , its corresponding upper-envelope function satisfies:

Thus . By Bellman inequality we have:

We have is in and also satisfies Bellman inequality. By repeating this process until it converge to , we will eventually get satisfies equation (22) and which means is also at least a optimal solution to optimization framework (6).

Uniqueness

Consider there are two functions and satisfy upper-envelope Bellman equation in (22). Consider , and let to denote the vector of , we have the infinity norm of to be:

where the last inequality is from contractive property. This means , and since are there corresponding upper-envelope, we have . ∎

Proposition 3.1 (and A.1)

B.1 Monotonic Convergence

It is well known that the Bellman operator is a contractive map when , with as the unique fixed point. Therefore, converges to as for any .

Another property of special importance in our work is the monotonicity of Bellman operator. For two functions and on , we say that if for . Then we have

Thus if we can establish (which known as the Bellman inequality (Bertsekas, 2000)), we have , which yields a sequence of increasingly tight upper bounds of . We leverage a similar idea to prove the monotonicity of our proposed algorithm.

We are ready to present our main result of convergence, in which we show that update (9) monotonically improves the bound and converges to the optimal solution of (6), if is upper-self-contained and is initialized properly such that they decrease during the first iteration.

Theorem B.6.

Assume is upper-self-contained function set whose corresponding upper envelope operator is contractive and our evaluate distribution is full support on , e.g. . If we initialize the updates in (9) with , such that

| (24) |

then we have

| (25) |

where . Therefore,

and .

Proof.

We focus on upper bound case, lower bound proofs follow similarly. Since is full support, from lemma B.3 we can see that is the upper envelope function of data points .

Now we prove the theorem by induction on for statement .

From the induction proof we can see that is a Cauchy sequence with a lower bound for every data point , we know it will finally converge to a function we denote as .

will satisfy the constraints .

On the other hand, from Lemma B.5 we know that it is the almost everywhere.

This leads to a monotone sequence of measures with a limit . ∎

A parallel result holds for the lower bound update (11), except that the initialization condition should be . See Appendix A for details.

Application to Lipschitz Function Space General convergence result can be easily applied to the case of Lipschitz functions. We show that the Lipschitz ball satisfies the upper-self-contained condition, and provide a simple initialization method to ensure condition 24. In addition, we establish a fast convergence rate for our algorithm.

Lemma B.7.

i) The Lipschitz ball is upper-self-contained whose envelope operators are contractive.

Therefore, the results in theorem 3.2 hold.

Proof.

i) Consider for given data points , we can see that:

we can see that is Lipschitz continuous.

For the contraction property, from Proposition 3.1 the upper envelope operator can be written in the following way:

then we have:

which implies contraction.

ii) For , we have:

Similarly we have . ∎

B.2 Linear Convergence

We are ready to prove the linear convergence result for Proposition 3.4 which follow the similar idea of proving linear convergence of value iteration.

Proposition 3.3

Proof.

Consider , where , we have:

Therefore we have , this leads to:

To conclude we have:

∎

B.3 Tightness of Lipschitz-Based Bounds

Theorem 3.4

Let be Lipschitz function class with Lipschitz constant . Suppose is a compact and bounded domain equipped with a distance . For a set of data points , we define its covering radius to be

We have

where is the Lipschitz constant and the discount factor.

Proof.

Consider , where and as the vector of upper and lower functions at point .

Since for all satisfies the finite points Bellman equation (see more details in Lemma B.5), we have:

Let , which is the epsilon ball radius given centers , typically . We have:

Thus we have:

Consider , we have:

Therefore we have:

∎

B.4 Additional Proofs

Proposition 4.1

Follow equation (14) with initialization follows (12), let to be the upper envelope function of data points , we have a similar monotonic result as theorem 3.2:

Proof.

The proof is the same as Theorem B.6, once we see that we gradually but they will always stay ahead the upper bound , but the convergence is the same as the original algorithm. ∎

Proof of Theorem 4.2

Let be a metric space for state action pair and be a metric space for state . Suppose is separable so that if . If the reward function and the transition are both Lipschitz in the sense that

We can prove that if , we have

| (27) |

when is a constant policy. Furthermore, for optimal policy with value function , we have:

| (28) |

Proof.

Suppose , where and is defined recursively.

If is a constant policy where , we can actually write as:

And similarly we have

Therefore we have:

The last inequality can be proved inductively by

For case we can have the similar derivation where at the beginning of the proof we have:

∎

Appendix C More Discussions on Lipschitz Norm

We show the non-identifiable results of upper bound of Lipschitz norm by constructing a set of possible functions that are consistent with the data but with an unbounded increasing Lipschitz norm.

We first show that if our function set provides at least two different solutions, we have a nontrivial solution in null space.

Lemma C.1 (Null Space of Finite Bellman Constraints).

There is a non-zero Lipschitz continual function with such that:

once the solution in is not unique.

Proof.

Suppose satisfies all the finite Bellman constraints. Consider , we have and

∎

Using the nontrivial solution in null space we can construct arbitrarily large Lipschitz norm solution of that are consistent with data.

Theorem C.2 (Non-identifiable of Upper Bound of Lipschitz Function).

If there is more than one Lipschitz functions satisfies finite Bellman constraints, For all we can always find satisfies Bellman constraint and .

Appendix D Experimental Settings

Comparison Results using Thomas BoundsThomas et al. (2015b)

We compare our method with lower bound estimation from Thomas et al. (2015b), whose bound leverage a sophisticated concentration bound by importance sampling estimators. Their method is based on the unbiased importance sampling (Precup et al., 2000) estimator of :

where is the trajectory and is the normalized and discounted average reward of a trajectory. They obtain a high confidence lower bounds for by leveraging the concentration inequality with an adjust threshold parameter specified by user.

| Number of Trajectories | 2 | 4 | 6 | 10 | 20 | 30 |

|---|---|---|---|---|---|---|

| Thomas Relative Lower Bound | -8.61e-03 | -2.87e-03 | -1.72e-03 | -9.56e-04 | -4.53e-04 | -2.97e-04 |

| Our Relative Lower Bound | -0.131 | 0.343 | 0.536 | 0.698 | 0.805 | 0.850 |

We empirically evaluate the method on Pendulum environment, where we use the same default settings as we conduct experiments for our algorithms. Table 1 shows the results compared to our lower bound. We pick the best result choosing the threshold number from and we set the confidence level of Thomas lower bound to be . All the numbers are the relative reward that divided by the ground truth.

We can see that Thomas’ lower bound is not sensitive to small number of samples, which is almost near 0. This is mainly because the importance ratio between the target policy and the behavior policy for each trajectory sample goes to 0 due to the curse of horizon (we use horizon length = 100 here) , which makes IS based estimator not a proper method for long (or infinite) horizon problems. As a consequence, concentration confidence bounds based on IS estimators could be potentially loose in such problems (The number of trajectories used in Thomas et al. (2015b) can be if they want to get a tight lower bound).

Synthetic Environment with A Known Value Function

The transition of this environment is a one dimension linear function:

and the target policy we use is

where Gaussian variance . And the historical data is pre-collected by a behavior policy similar to but with a larger variance.

|

|

|

|

The predefined q-function is where . For distance metric we use Euclidean distance . Under this distance metric, we can calculate the exact Lipschitz constant:

Pendulum Environment

We learn a feature map for by a two hidden layers neural network , where the input layer is state action pair , the first hidden layer is with hidden dimension matrix . We set as feature layer, where we let the concatenate the input layer and a relu of linear layer for the hidden layer as our feature. We add the input layer to our feature layer to ensure that our distance function is a true distance function (not a semi-distance one because requires ). And finally the last layer is a linear layer with output dimension as the output of q-function. Thus our approximate q-function can be represented as

where .

HIV simulator

We follow exactly the same settings as Liu et al. (2018b).