Lin, Ma, Nadarajah, Soheili

A Restarting Level Set Method

A Parameter-free and Projection-free Restarting Level Set Method for Adaptive Constrained Convex Optimization Under the Error Bound Condition

Qihang Lin

\AFFThe University of Iowa, Tippie College of Business,

qihang-lin@uiowa.edu

\AUTHORRunchao Ma

\AFFThe University of Iowa, Tippie College of Business,

runchao-ma@uiowa.edu

\AUTHORSelvaprabu Nadarajah

\AFFUniversity of Illinois at Chicago, College of Business Administration,

selvan@uic.edu

\AUTHORNegar Soheili

\AFFUniversity of Illinois at Chicago, College of Business Administration,

nazad@uic.edu

Recent efforts to accelerate first-order methods have focused on convex optimization problems that satisfy a geometric property known as error-bound condition, which covers a broad class of problems, including piece-wise linear programs and strongly convex programs. Parameter-free first-order methods that employ projection-free updates have the potential to broaden the benefit of acceleration. Such a method has been developed for unconstrained convex optimization but is lacking for general constrained convex optimization. We propose a parameter-free level-set method for the latter constrained case based on projection-free subgradient decent that exhibits accelerated convergence for problems that satisfy an error-bound condition. Our method maintains a separate copy of the level-set sub-problem for each level parameter value and restarts the computation of these copies based on objective function progress. Applying such a restarting scheme in a level-set context is novel and results in an algorithm that dynamically adapts the precision of each copy. This property is key to extending prior restarting methods based on static precision that have been proposed for unconstrained convex optimization to handle constraints. We report promising numerical performance relative to benchmark methods.

level set method, parameter free, projection free, accelerated methods, constrained convex optimization, error bound condition

1 Introduction.

In this paper, we consider a convex optimization problem with inequality constraints:

| (1) |

where for are convex real-valued functions and is a closed convex set onto which the projection mapping is easy to compute. Given , we say a solution to (1) is -optimal if and -feasible if and . There has been a large volume of literature on constrained convex optimization problems in deterministic settings [1, 2, 9, 14, 22, 23, 35, 36, 37, 38, 47] and significant, but comparatively less, activity in stochastic [21, 24, 47] settings.

Recent developments have focused on accelerating first order methods with linear convergence rates (without assuming strong convexity) based on a more general geometric property known as “error bound condition (EBC)”, which is

| (2) |

for some parameters and , where is the set of optimal solutions to (1) and denotes the Euclidean distance of to , which we refer to as solution distance. EBC provides a lower bound on the maximum of the optimality and feasibility gaps as a function of the solution distance, , and . A larger such lower bound is desirable as it implies that additional iterations that bring closer to are needed in the pursuit of an -optimal and -feasible solution. In contrast, if this lower bound is very small, iterations that move closer to may not result in significant optimality or feasibility progress. Smaller values of lead to larger lower bounds all else being the same and are thus preferred. For a fixed , we prefer a smaller because it corresponds to more favorable geometry closer to the optimal solution set, which is typically when the progress of first-order methods slows down. Specifically, when is close to the set of optimal solutions (i.e., is ), smaller leads to a larger lower bound. Piece-wise linear and strongly convex programs satisfy EBC for and , respectively. We refer to an algorithm as adaptive if its convergence rate improves (i.e., it accelerates) as and become smaller111We note that algorithms that exhibit acceleration for only specific values of (e.g., under strong convexity, which corresponds to ) would not be considered adaptive under our definition..

Adaptive methods for unconstrained or simply constrained222Here, simply constrained means in (1) and is a simple set, e.g., , a box or a ball. convex optimization problems have been explored. Almost all of them use in their step length [4, 7, 15, 17, 18, 20, 26, 30, 33, 35, 43, 48, 49] or in the frequency with which they restart [5, 6, 10, 11, 16, 25, 34, 39, 40, 41, 42, 44, 45] knowledge of , , and . Such parameters are unknown in general and their accurate estimation is challenging. Adaptive algorithms that are also parameter free (i.e., do not rely on the knowledge of unknown parameters) would therefore broaden or ease the applicability of accelerated methods. To the best of our knowledge, [8, 19, 32] are the only parameter-free adaptive methods that handle unconstrained problems. The method in [32] employs a subgradient scheme to solve copies of the problem with termination precisions for . Copy communicates its current solution to copy when a restart is triggered. Since the copies are based on pre-defined precision, this restarting subgradient method (RSG) can be interpreted as a static precision-based restarting scheme. A key feature of RSG is that it tracks the reduction in the objective function (i.e., progress made) to determine when to trigger a restart, as opposed to relying on the distance from (i.e., remaining progress). However, RSG is not designed to handle convex optimization problems with (potentially) complicated constraints. This method has been adapted to bundle methods in [8]. [19] applies a similar idea for smooth unconstrained convex optimization problems where the restarts are triggered based on the norm of proximal gradients. There is limited work ([31], [46]) on utilizing EBC for solving the constrained convex optimization problem (1). The work in [31] considers the case of and their algorithm relies on knowledge of . The method in [46] is for general but requires the knowledge of and , among other parameters, and requires a projection on , which is hard.

The goal of our paper is to develop an adaptive method for convex optimization with general convex constraints that is both parameter-free and projection-free333As is common in the literature when using the term projection-free, we do allow projections onto , which are inexpensive to compute and often available in closed form.. Extending RSG to handle general convex constraints would be the natural first avenue to consider to achieve our goal. Indeed, the -th copy in such an extension will solve the problem of finding an -optimal and -feasible solution, which entails balancing optimality and feasibility by defining a single objective. Defining such an objective is possible given optimal Lagrange multipliers or , which are both unknown. Thus extending RSG in this manner appears to be challenging.

| Smooth | Algorithm | ||

| EBC | Functions | parameters | Convergence rate |

| General [This paper] | No | None | |

| Yes | None | ||

| General [46]†† | No | , , | |

| Yes | , , , | ||

| [23, 24] | No | , | |

| Yes | , , | ||

| [38] | Yes | , , | |

| [31] | No |

We show that our goal can be achieved by developing a restarting level set method. Level-set methods [1, 22, 23, 24] convert the solution of the constrained optimization problem (1) into the solution of a sequence of unconstrained non-smooth optimization problems that depend on a scalar, referred to as the level parameter. The level parameter is chosen by approximately solving a one-dimensional root-finding problem 444An alternative approach to handle constraints is using the radial duality framework of [14, 31], where a constrained convex optimization problem is converted to an unconstrained convex optimization problem, but solving this converted problem relies on being able to do exact line searches to evaluate the gauge of the feasible set.. [1] provides a detailed discussion and complexity analysis of the level set approach. Subgradient algorithms to solve the aforementioned level-set subproblems are desirable as they are easy to implement. However, level set methods that leverage subgradient algorithms depend on unknown parameters, which may include an upper bound on the subgradient norm and/or a smoothness parameter [22, 23, 24]. Our contributions are the following:

-

•

We introduce a restarting level set method (RLS) that is both parameter-free and projection-free. It maintains copies, each distinguished by a level parameter and its associated sub-problem. Each restart of copy results in an update of the level parameters associated with copies . The restart of a copy is triggered by the progress made on the sub-problem objective. To the best of our knowledge, this is the first level set method based on projection-free subgradient oracles that is parameter-free, and is therefore of independent interest to the literature on level set methods.

-

•

RLS can be interpreted as a restarting scheme with dynamic precision, which is conceptually different from RSG. To elaborate, a fixed level parameter implicitly sets a precision for a subproblem. Since RLS updates the level parameter of multiple copies in every restart, it dynamically and implicitly updates the precision associated with copies. Our key algorithmic insights are that (i) triggering restarts based on the progress of the subproblem objective and (ii) dynamically changing the precision of subproblems at each restart by updating the level parameters side step the issues discussed earlier of extending RSG to handle general constrained convex optimization.

-

•

We establish that RLS is adaptive in addition to being parameter-free, that is, RLS exhibits acceleration under EBC. Its complexity for non-smooth problems is . The adaptive method in [46] has a complexity of but it depends on unknown parameters and requires a non-trivial projection onto . The additional factor in the RLS complexity can be interpreted as the cost of both relaxing parameter dependence and employing simple subgradient oracles. Despite this worsening, the dependence of RLS on is better. Table 1 shows that an analogous property holds in the smooth setting when comparing RLS with the approach in [46]. Although perhaps unfair to RLS, Table 1 also compares its complexity to algorithms designed for specific values of , all of which depend on unknown parameters. RLS worsens by the same logarithmic factor of relative to these more specialized algorithms and sometimes improves on the dependence with respect to .

-

•

We numerical test the performance of RLS on a synthetic linear program and a classification problem with fairness constraints. We are able to vary in the synthetic linear program and confirm numerically that the number of RLS iterations to find an -optimal and -feasible solution increases with and . For the classification problem with fairness constraints, we compare RLS against three parameter-free but non-adaptive benchmarks, which include the feasible level set method in [23], the subgradient method in [47], and the switching subgradient method in [2]. We find that the adaptive-nature of RLS leads to significantly faster convergence to an -optimal and -feasible solution than the three benchmarks.

This paper is organized as follows: In Section 2, we discuss a general level-set method for solving (1) and discuss its convergence rate. In Section 3, we present RLS and analyze its oracle complexity. In Section 4, we provide first order oracles for use with RLS in the non-smooth and smooth settings, also analyzing the iteration complexity of RLS in each case. In Section 5, we numerically compare RLS to other benchmarks. We conclude in Section 6.

2 Level set method.

Throughout the paper, we assume that there exists a computable feasible solution to (1) that strictly satisfies the constraint . This assumption is formalized below. {assumption} There exists a computable solution such that and .

We define the level-set function corresponding to (1) as:

| (3) |

where is called a level parameter and

| (4) |

Below, we summarize some of the well-known properties of that we use in our algorithm and analyses.

Lemma 2.1 indicates that is the unique root to the root-finding problem under Assumption 2. Moreover, as shown in Lemma 2.2, it is possible to find an -feasible solution and use the level parameter to bound the optimality gap.

Lemma 2.2

Given , if satisfies for some , then is -optimal and -feasible. Consequently, when , this solution is -optimal and -feasible.

Hence to tackle (1), a level-set method applies a root-finding scheme to solve with the goal of finding . Once such is found, then implies that is a nearly optimal and nearly feasible solution to (1). Notice that for any we have .

Algorithm 1 presents a level set method that generates a sequence of level parameters converging to . Given , each update of requires a vector satisfying , that is, condition (5). The convergence of Algorithm 1 relies on . Under this condition, it follows from Lemma 2.1(4) and that can be computed by solving because . Moreover, the level parameter converges to from below causing the quantity to converge to zero. Thus, Algorithm 1 terminates and the final solution is both -optimal and -feasible by Lemma 2.2.

| (5) |

Next, we present analysis that shows the correctness and complexity of Algorithm 1. This analysis depends on a condition measure that is defined as

| (6) |

The following lemma sheds light on some geometric properties of the condition measure . We skip proving this lemma as it directly follows from the definition of in (6) and the first and fourth properties in Lemma 2.1.

Lemma 2.3

It holds that for any and for any .

Lemma 2.3 establishes bounds on . In particular, when is less than , there is a natural lower bound of zero.

If , Lemma 2.4 shows that remains less than at each iteration of Algorithm 1 and that it converges to at a geometric rate.

Proof 2.5

Proof. Fix . Given and satisfying , we have

In addition, it follows that

| (7) |

where the first inequality holds because and the second one because for by Lemma 2.3. \Halmos

In Theorem 2.6 we characterize the number of outer iterations needed by Algorithm 1 to find an -optimal and -feasible solution to (1).

Theorem 2.6

Proof 2.7

Proof. Since Algorithm 1 starts with , Lemma 2.4 indicates that and (7) holds at each iteration . Since , recursively applying (7) for shows that for any . Hence, it follows from inequality (5) that . When , we get and the algorithm stops. Since , Lemma 2.2 then guarantees that the solution returned at termination is an -optimal and -feasible solution. \Halmos

Remark 2.8

The factor in the definition of arises because we leverage the natural lower bound of zero on , as discussed after Lemma 2.3. This choice results in the specific form of condition (5), which is a simplification of the analogous condition in [1], where the authors use non-trivial lower and upper bounds on . The lower bound used in [1] is easily computable only when the problem has certain structure. If such bounds can be computed efficiently, then the number of iterations taken by the algorithm in [1] does not depend on . We choose our simpler approach because it is implementable for more general class of problems and also facilitates clearer exposition of the key ideas underlying RLS in the next section.

3 Restarting level set method.

We define a sequence of pairs with and as a level set sequence of length if holds for some and each . It follows from Theorem 2.6 that the level set sequence generated in Algorithm 1 converges to an -optimal and -feasible solution when (i) satisfies (5) and (ii) . One way to find satisfying (5) is to solve the level-set subproblem (3) with , which we denote by :

| (9) |

Let represent the first-order method applied to (9). Although there are many choices for , it is difficult to numerically verify (5) because is unknown. As a result, we are not able to terminate at the right time. If is terminated too soon, the returned solution will not satisfy (5) and Algorithm 1 may not converge. If is terminated too late, Algorithm 1 will converge but consume longer run time than it actually needs.

To address this issue, we parallelize the sequential approach in Algorithm 1 by simultaneously solving multiple level-set subproblems with potentially different level parameters and restarting the solution of each such subproblem if a predetermined amount of progress in reducing its objective function has been made. We refer to this procedure as the restarting level set (RLS) method and describe its core idea next. It requires maintaining (with ) first order method instances denoted by . Given and , we initialize the level set sequence with for , , and for . We then apply to solve starting from for and denote by the solution computed by after iterations. The instances communicate with each other via restarts. We initiate a restart at instance when and the solution satisfies

| (10) |

for a constant . The sequence of steps associated with restart are shown in Definition 3.1.

Definition 3.1 (Restart at )

Set and for all . Restart from for .

In other words, initiating a restart at , we reset to begin at an updated initial solution equal to and solve the same level set subproblem as before the restart because is not updated. In contrast, for indices , changes because the restart changes . This new level set subproblem is solved by starting from the same initial solution that was used before the restart. If a restart is initiated at , we only perform the update . Restarts initiated at index have no effect on for , so those s will continue their iterations. Lemma 3.2 follows from our restarting updates.

Lemma 3.2

The level set sequence remains a level set sequence after each restart.

Remark 3.3

We highlight that restarts dynamically modify the precision with which subproblems need to be solved by instances to satisfy (5). Specifically, the precision of a solution at instance can be viewed as the deviation of from the optimal subproblem objective of . This difference satisfies

where the first inequality follows from Lemma 2.3 and the fact that the solution satisfies (5) and the second inequality holds since the initial solution does not satisfy (5). i.e. It follows from these inequalities that the precision is . A restart at changes or of instances and hence the value of at these instances. Therefore, RLS can be interpreted as an approach that dynamically modifies the precision required to satisfy (5) at a subset of instances, each time a restart is initiated as the result of there being sufficient progress in the subproblem objective function at some instance, that is, condition (10) is satisfied. The dynamic precision affects the choice of step sizes and smoothing parameters in the specific methods we employ in Section 4 for the non-smooth and smooth settings, respectively (see remarks 4.4 and 4.11).

Well-known choices of (e.g., subgradient decent) can be shown to meet the restart condition (10) after a finite number of iterations starting from when is sufficiently large. In particular, when , the number of iterations taken by to find a desirable solution can be bounded by an integer that is independent of and . We summarize this property in Assumption 3 and take it to be true in this section. We will present choices that satisfy this assumption in §4.

Consider , , , , and such that , , , and . There exists an initiated at which guarantees that the inequality holds after iterations if (5) is not satisfied by then, where is an integer depending on , and and independent of and .

To interpret RLS, it is useful to think of instance as being a proxy for the first order method applied to solve in iteration of Algorithm 1. By Lemma 3.2, the relationship between the values across iterations in Algorithm 1 are also maintained for the values across instances in RLS but some may not be computed based on a solution that satisfies (5). As a result, even though the initial level set parameter is less than , subsequent updates can push . Theorem 3.4 states key properties of RLS that allows it to nevertheless converge to a near-optimal and near-feasible solution, as we will discuss shortly.

Theorem 3.4

Given and , consider a level set sequence with where is defined in (8). At least one of the following two statements holds:

-

A.

There exists an index such that and ;

-

B.

The solution is an -optimal and -feasible solution.

Moreover, if statement A holds, it follows that the index is unique and we have and for .

Proof 3.5

Proof. Suppose statement A does not hold for any index . We show the statement holds. By the definition of a level set sequence, we have and for all . Since (by our assumption that does not hold), Lemma 2.4 guarantees that . Using the same argument and by induction, Lemma 2.4 implies and for any . Therefore, we have . Since with defined in (8), we have which indicates is an -optimal and -feasible solution by Lemma 2.2.

Next we prove the rest of the conclusion. Let denote the smallest index satisfying the conditions of statement A. If the conclusion is trivial since . Suppose . Since , following the definition of , we must have . Lemma 2.4 then guarantees that . Applying the same argument, we can show are all less than ( i.e. ) and hence the inequality must hold for any . In addition, recall that for any . Hence, the relationship shows for any . The index in is unique because it is straightforward to see which follows from the definition of and the inequality . Moreover, once there exists an index such that , we must have for all since

where the first inequality holds by the definition of and the second by Lemma 2.3. Therefore, given that , we must have for any . \Halmos

Given a level set sequence, we refer to the unique index in Theorem 3.4 as the critical index. At this index, we have but condition (5) does not hold. For all indices that precede the critical index, we have and condition (5) holds. Moreover, if and does not exist (intuitively ), it implies the solution is an -optimal and -feasible. Therefore, we would like to increase the critical index with restarts so that it eventually exceeds . Ideally, if one could initiate restarts at the critical index sufficiently many times, it would reduce by updating while ensuring (since is not updated when a restart is initiated at by Definition 3.1). Then one would expect condition (5) will hold at . Moreover, when this happens, by Lemma 2.4. Hence, repeated restarts at the critical index should intuitively increase its value.

Unfortunately, this intuition is of little algorithmic use since the critical index defined using is unknown. Therefore, RLS instead executes restarts at the smallest index at which condition (10) is satisfied. This index could be smaller than or greater than the critical index . We refer to as desirable restarts the ones initiated at index less than or equal to because such restarts may update or . By Assumption 3 and Theorem 3.4, a desirable restart must be initiated at with some in no more than iterations, unless . In the latter case the solution is -optimal and -feasible. The number of desirable restarts can be bounded by as we will establish later. Such restarts that occur before may already increase the critical index. If this does not happen, desirable restarts will start happening at and increase the critical index.

Algorithm 2 formalizes the steps of RLS. The inputs to this algorithm include the number of instances , a total budget on the number of iterations, a level parameter , a strictly feasible solution , and parameters , , and . By Assumption 2, we can set . For , an ideal value to use is defined in (8). However, since the parameters and in this bound are unknown, we compute a bound on by using a strictly feasible solution. In particular, we use

| (11) |

with and for and from Assumption 2. We show below is an upper bound on . We set in definition of when executing Algorithm 2.

Lemma 3.6

Proof 3.7

Proof. We prove this lemma by showing and for any . Since and , by the definitions of and , we have

| (12) |

By property 3 in Lemma 2.1, we must have which indicates for any . It follows from the convexity of and definition of in (6) that

| (13) |

This further implies that, for ,

| (14) |

where the first inequality is from (12), the second from (13) with , and the last from . \Halmos

The initialization step in Algorithm 2 assigns as starting solutions to all instances (i.e. for ) and sets the level parameters used in each using starting at . Algorithm 2 runs for a pre-specified number of iterations. At each iteration , it runs iterations simultaneously, one for each instance, until the condition (10) holds for some index. It then finds a smallest index for which and (10) hold. A restart is executed at . If the solution is -feasible and has a better objective function value than the best -feasible solution at hand, this solution is updated. Once the total of iterations have been reached, the -feasible solution with the least is output.

By Lemma 3.2, the sequence generated at each iteration of Algorithm 2 is a level set sequence. In addition, since , Theorem 3.4 guarantees that the critical index must exist unless an -optimal and -feasible solution is obtained. The correctness and complexity of Algorithm 2 rely on the following lemma which we will prove in the Appendix.

Lemma 3.8

The critical index is non-decreasing throughout Algorithm 2.

We count the total number of iterations taken by the RLS algorithm as the total number of iterations taken by instances between two consecutive desirable restarts times the total number of desirable restarts. Lemma 3.8 shows the critical index never decreases after desirable restarts. Since the critical index is at most (by its definition), this index varies between one to in an increasing order until it reaches . If the latter case happens, Assumption 3 and Theorem 3.4 ensure that in finite number of iterations condition (5) holds at all instances and hence an -optimal and -feasible solution must be found. Let denote the total number of desirable restarts before an -optimal and -feasible solution is found. Using the argument above, we can compute as follows. Suppose shows the number of desirable restarts starting at before an -optimal and -feasible solution is found with , assuming is the current critical index. Then

| (15) |

The first sum in the above equation accounts for the total number of desirable restarts that occur at each for all possible critical index . The second term however is the total number of desirable restarts that start at each instance with , where is the critical index and varies from zero to . Notice that some of the values between zero and in the above sums cannot be critical index. This could happen if the critical index is strictly positive at the beginning of Algorithm 2. In this case, all the smaller indices will never be a critical index since by Lemma 3.8, critical index does not decrease throughout the algorithm. We assume for such cases. The equation (15) can be re-written as

| (16) |

The equivalence between the second sum in (15) and the second one in (16) can be explained by considering each as elements of an upper triangle matrix where is a row index and is a column index. Then the sums of elements over rows and columns can be exchanged.

We provide upper bounds for and respectively in Lemma 6.9 and Lemma 6.7 in the Appendix. Using these bounds in (16), we obtain the total complexity of Algorithm 2 in Theorem 3.9.

Theorem 3.9

Proof 3.10

Proof. Suppose and respectively denote the number of iterations between two consecutive desirable restarts and the total number of desirable restarts performed by Algorithm 2 until an -optimal and -feasible solution is found. It then follows that the total number of iterations required by Algorithm 2 is , where is expressed in (16). To obtain the iteration complexity we only require to bound and .

An upper bound on : Consider a desirable restart and assume the critical index is after this restart. Suppose an -optimal and -feasible solution has not been found. We must have by Lemma 2.2. Assumption 3 indicates that in iterations, the inequality holds. This means that the next desirable restart must occur at one of the instances in at most iterations and is independent of and by Assumption 3. Since each iteration of Algorithm 2 simultaneously runs iterations, we get

| (19) |

An upper bound on : We claim that for any ,

| (20) |

and for any ,

| (21) |

We formally prove these claims in Lemma 6.7 and Lemma 6.9 in the Appendix. From the above inequalities it follows that the total number of desirable restarts can be bounded by

| (22) | |||||

The bound (17) then can be obtained by multiplying (19) and (22). \Halmos

4 First order subroutines

In this section, we provide two different first order methods (s) for smooth and non-smooth problems that can be used as subroutines in Algorithm 2 to solve . In particular, when the functions , defining are non-smooth, we use the standard subgradient descent (SGD) method as an which is an optimal algorithm for solving general non-smooth problems. When the functions , are smooth, we still require to solve minimization of a non-smooth function since is non-smooth because of the operator in its definition. In this case, we discuss the smoothing technique in [3, 23, 27] to obtain a smooth approximation of and then solve this approximation using Nesterov’s accelerated gradient method introduced in [28] which results in a better convergence result. We show these well-known methods satisfy Assumption 3. Since all , follow the same steps, we drop the index in and used in the first order methods described in this section to simplify our notations.

4.1 Non-Smooth Case.

First, let’s assume the functions , are non-smooth and denotes the set of subgradient of at . Suppose Assumption 2 and the error bound condition (2) hold. We also make the following assumption: {assumption} There exists such that for any and .

Notice that when the functions , are differentiable, Assumption 4.1 indicates that the gradients of all the functions will be bounded by . i.e. for any .

We next show that the SGD method using a specific step length rule satisfies Assumption 3 and can be used to solve the level-set subproblem .

Let be an initial solution, the SGD updates can be presented as

| (23) |

where denotes the projection onto , a step size, and a subgradient of with respect to . Recall that the projection mapping is easily computable since we assume the set is simple (e.g. , a box or a ball). It is clear that for any , , and under Assumption 4.1. The output of SGD can be chosen as the historically best iterate, i.e.,

| (24) |

Proposition 4.1 below presents a well-known convergence result of the SGD method.

Proposition 4.1 (See Theorem 3.2.2 in [29])

Notice that in the above proposition could be the projection of any , for , onto since by definition of and , it follows that for all .

Proposition 4.2 below indicates that the SGD method discussed above can be used as an in Algorithm 2 if the stepsizes are carefully chosen. To do so, it is sufficient to show that the SGD method with a specific choice of stepsize rule satisfies Assumption 3. Notice that some of the arguments used in the proof of Proposition 4.2 are borrowed from the proof of Proposition 3.2 in [12].

Proposition 4.2

Consider , , , , and such that , , , and . Let . The SGD method satisfies Assumption 3 with

| (26) |

Proof 4.3

Proof. Suppose does not satisfy (5), i.e. . We show for .

Remark 4.4

The step length used in SGD is likely to reduce at the instance that is restarted since becomes smaller as a result of updating the initial solution with a solution that satisfies (10). For all the proceeding instances, the step length after the restart would likely be larger since is a decreasing function of .

Corollary 4.5 below provides the overall complexity of Algorithm 2 by counting the total number of subgradient and function evaluations required in this algorithm.

Corollary 4.5

Proof 4.6

Proof. Theorem 3.9 guarantees that an -feasible and -optimal solution can be found in at most

| (31) |

iterations where , , and are respectively defined in (11), (18), and (26).

4.2 Smooth Case.

In this section, we assume assumptions 2 and 4.1 and the error bound condition (2) hold. Moreover, we make an additional assumption about the smoothness of the functions , in (1). {assumption} Functions , , are -smooth on for some . In other words, the functions , , are differentiable and for any and in .

Notice that although Assumption 4.2 ensures the functions , are smooth, the function may not be due to the operator in its definition. To address this issue, we use the smoothing techniques proposed in [3, 23, 27]. In particular, we consider exponentially smoothed function defined as

| (33) |

where is a smoothing parameter. Lemma 4.7 characterizes some of the important properties of .

This lemma suggests that if is appropriately selected, the function is a close approximation of the function . Hence, we can solve the problem instead of which involves minimizing a smooth function. To do so, we use the Nesterov’s accelerated gradient method in [28] (See (4.9) with ) which is an optimal algorithm for solving smooth convex optimization problems. To be self-contained, we present this method in Algorithm 3. In summary, this algorithm starts at but, instead of moving the current solution at the direction of a subgradient of , it moves this solution in the direction of the previously accumulated gradients denoted by . In particular, the auxiliary solution in Line 5 is the weighted average of all historical gradients where the weights are chosen such that the gradients of newer iterates receive larger weights than the previous ones. As soon as the direction is computed, the Accelerated Projected Gradient (APG) subroutine described in Algorithm 4, finds a solution on the line connecting and . The new update is then obtained by applying the gradient step at and the direction of negative of the gradient of . The step length in this gradient step, is the inverse of the local Lipschitz constant of around which is denoted by . Since the true value of is unknown, the APG subroutine follows a line search to find this parameter. More specifically, the line search starts with a given and at each iteration it increases this value by multiplying it by a constant factor . This procedure is repeated until the inequality is satisfied. After the solution is updated to , Algorithm 3 again reduces the estimated parameter by dividing it by a constant to ensure the APG subroutine starts the line search with a sufficiently small value in the next round. Taking smaller results in larger moves in the gradient steps at earlier stage of the line search. Following [28, Lemma 6], the values of and will only logarithmically affect the complexity of Algorithm 3. With these non-expensive additional computations, Algorithm 3 can achieve an accelerated convergence rate of as shown in Theorem 4.8555This theorem leverages equation (4.8) in [28], which is given in terms of the optimal solution . However, the same proof works for any solution ..

Proposition 4.9

Proof 4.10

Proof. Suppose does not satisfy (5), i.e. . We only need to show for . Let . and take . Since (34) holds for any , we get

| (36) |

where the second inequality follows from Lemma 4.7, the third from the error bound condition (2) and (27), and the last from the definition of and the fact that which holds because . Let

| (37) |

Remark 4.11

The smoothing parameter used in Algorithm 3 changes after each restart. In particular, it increases at the instance that is restarted since becomes smaller and it decreases in all the proceeding instances since is a decreasing function of .

Corollary 4.12

Suppose , , , , and are such that , , , and . Consider defined in (11) for . Suppose we execute Algorithm 2 with the accelerated gradient method described in Algorithm 3 where as instances for . This algorithm finds an -optimal and -feasible solution in at most

gradient and function evaluations, where is defined in (18).

Proof 4.13

Proof. The proof of this corollary is similar to the proof of Corollary 4.5 except that (35) is used as and that the number evaluations of and between two desirable restarts is instead of due to the line search scheme in Algorithm 4. According to Lemma 4 in [28], only some constant factors of and are suppressed in the big-O notation. \Halmos

5 Numerical Experiments.

We evaluate the numerical performance of Algorithm 2 on two different problems: (1) a simulated linear program and (2) a binary classification problem with fairness constraints. In the first problem, we construct a linear programming problem with known objection value that satisfies the error bound condition (2) with . This linear program is designed such that the growth parameter can be controlled. In our experiments, we vary the value of to better understand the behavior of Algorithm 2. We also try different values of which not only affects the precision of the solution obtained from our algorithm but also the number of instances since depends on (see (11)). We use a binary classification problem with fairness constraints to benchmark our proposed method against existing ones in the literature.

5.1 Simulated linear program.

The complexity of RLS (Algorithm 2) depends on the parameters , , , and where defined in (11) itself depends on the precision . To better understand the influence of some of these parameters on the behavior of our algorithm, we constructed a simple linear program for which , , and are known. We keep the parameters and fixed but vary using a simple trick. In particular, since depends on the scaling of the constraints, we modify our constraints by multiplying them with a constant factor such that the set of feasible solutions remains the same but the parameter changes depending on the value of . Our modified linear program is as follows:

| (39) | ||||

| s.t. |

The optimal solution and optimal value of this problem are respectively and . It is easy to see that (39) satisfies (2) with and . Notice that we added the constant to both sides of the constraints in (39) which has no effect on the optimal solution or optimal value. But it changes the growth parameter from 2 to . Hence, we can control the value of by varying the value of . In our experiments, we used SGD as an for all instances.

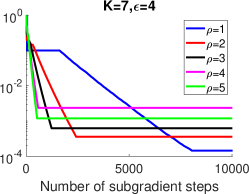

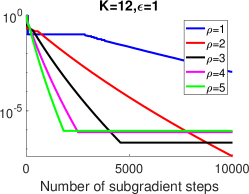

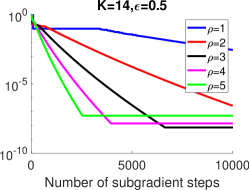

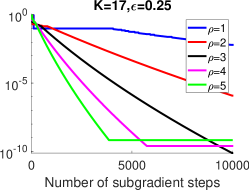

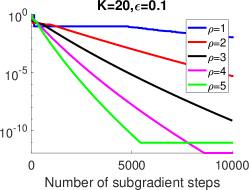

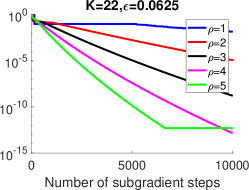

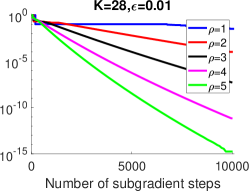

We set , and to each value in in Algorithm 2. For each value of , we chose to be 1, 2, 3, 4, and 5. We initialized RLS at and and terminated RLS after 10,000 subgradient updates.

To check the efficiency of RLS, we look at the quantity . It is easy to verify that when this quantity is zero, the solution is both feasible and optimal and when this quantity is positive, the solution is either infeasible or sub-optimal. The value of then accounts for the distance to infeasibility and sub-optimality. Ideally, any efficient iterative algorithms should reduce to zero very quickly. In Figure 1 we present in -axis for different values of where is the solution returned by RLS. The -axis shows the number of subgradient updates.

The plots in this figure show that the RLS method is more efficient when is larger (i.e. is smaller). Moreover, to achieve a small optimality gap and small infeasibility, we need to choose small which is consistent with our theoretical results.

|

|

|

|

|

|

|

|

|

5.2 Classification problem with fairness constraints.

Consider a set of data points where denotes a feature vector, and represents the class label for . Let and be two different sensitive groups of instances. We want to find a linear classifier that not only predicts the labels well (i.e., minimizes a loss function) but also treats each sensitive instance from and fairly. Such classification problems are suitable for applications such as loan approval or hiring decisions. For example, in the context of loan approval, we can ensure that loans are equally provided for different applicants independent of their group memberships (e.g., home-ownership or their gender). A correct classifier satisfies for all . One can train such a classifier by solving the following optimization problems that minimizes a non-increasing convex loss function subject to fairness constraints:

| (40) | |||||

| s.t. | (42) | ||||

where is a constant, and are respectively the number of instances in and , and finally is the probability of predicting in class . The constraint (42) guarantees that the percentage of the instances in that are predicted in class is at least a fraction of that in . The constraint (42) has a similar interpretation for instances in . Choosing an appropriate ensures that the obtained classifier is fair to both and groups. An analogous model was considered in [13].

Constraints (42) and (42) are non-convex, so we approximate this problem by a convex optimization problem following the approach described in [24]. In particular, we reformulate the first constraint as

by using . In addition, the function can be approximated by . Hence, we can rewrite the constraint (42) as a convex constraint:

Applying a similar convex approximation to (42), we obtain the following convex reformulation of (40):

| (43) | |||||

| s.t. | |||||

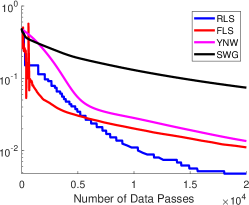

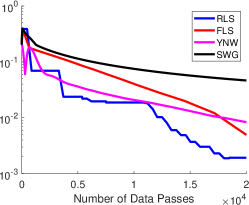

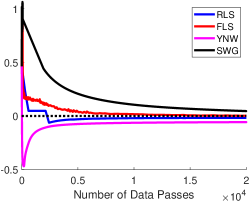

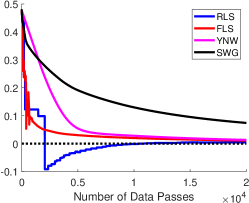

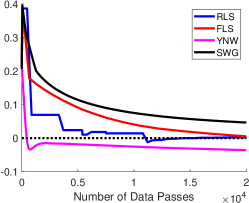

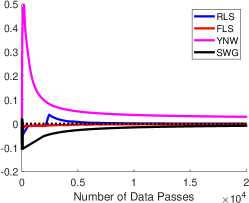

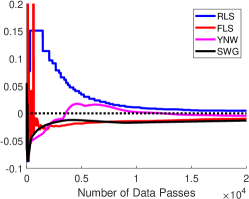

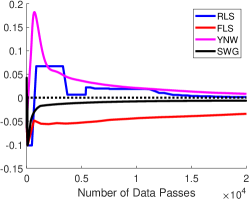

The above reformulation contains piece-wise linear functions (non-smooth) in its objective and constraints. Hence, this problem satisfies the error bound condition (2) with and an unknown value of . We implemented RLS (Algorithm 2) to solve (43) using SGD in each instance to solve the subproblem . We compare the performance of our method with three parameter-free but non-adaptive benchmarks: (1) the feasible level-set (FLS) method described in [23]; (2) the stochastic subgradient method by Yu, Neely, and Wei (YNW) in [47]; and (3) the switching gradient (SWG) method in [2] which is based on a mirror descent algorithm and a switching sub-gradient scheme 666We do not benchmark against adaptive methods for constrained convex optimization as they require knowledge of unknown parameters.. We choose these benchmarks as they are the most representative first-order methods that can solve “non-smooth” convex “constrained” optimization problems. The FLS is a level-set method guarantees the feasibility of the solutions generated at each iteration but does not exploit the error bound condition as our method does. Hence, it has a higher complexity bound for the class of problems that satisfy the error bound condition (2). YNW is a primal-dual method with dual variables updated implicitly while SWG is a pure primal method. We used the number of equivalent data passes performed by each algorithm as a measure of complexity.

Instances: To check the performance of the above mentioned methods, we considered three classification problems using (i) “LoanStats” data set from lending club777https://www.lendingclub.com/info/statistics.action which is a platform that allows individuals lend to other individuals; (ii) “COMPAS” data set from ProPublica888https://github.com/propublica/compas-analysis; and (iii) “German” data set from UCI Machine Learning Repository999https://archive.ics.uci.edu/ml/datasets/statlog+(german+credit+data).

The LoanStats data set contains information of loans issued on the loan club platform in the fourth quarter of 2018. The goal in this application is to predict whether a loan request will be approved or rejected. After creating dummy variables, each loan in this data set is represented by a vector of 250 features. We randomly partitioned this data set into a set of examples to construct the objective function and a set of examples to construct the constraints. The set in this application denotes the set of instances with “home-ownership = Mortgage”. All the other instances are considered in the set . The fairness constraints in this application guarantees that customers with mortgage will not be disproportionally affected to receive new loans.

The COMPAS dataset includes the criminal history, jail and prison time, and demographics along with other factors of 6,172 instances. The goal of this application is to predict whether a person will be rearrested within two years after the first arrest. This information, for example, helps judges make bail decisions by predicting defendants’ criminal recidivism risk. We used of the examples in this dataset to formulate the objective function and the remaining to formulate the constraints. We chose sets and to respectively be the sets of male and female instances to ensure fair treatments among different genders.

The German credit dataset describes financial details of customers and is used to determine whether the customer should be granted credit (i.e. is a good customer) or not (i.e. is a bad customer). This dataset contains 1,000 instances and 50 variables. We used of the examples to formulate the objective function and the remaining to formulate the constraints. Similar to COMPAS data, the sets and respectively denote male and female examples.

In all above applications, we chose , and . We terminated RLS and other three benchmarks when the number of data passes reached 20,000. However, we ran the two level-set methods, i.e., RLS and FLS, longer for 100,000 data passes to find the optimal value . In particular, we selected the smallest objective value among all -feasible solutions as a close approximation of . We used this value to compute and plot .

Algorithmic configurations: We next describe how we selected each of the parameters used in RLS, FLS, YNW, and SWG.

-

•

RLS: We executed Algorithm 2 on all of our instances with . We used cross-validation to chose a value for from and for from to minimize the value of at termination. Since the optimal value of (43) is positive, we set to satisfy the condition . Although the vector of all zeros could be used as an initial solution , we used a different value in our algorithm. In particular, the complexity bound of RLS shows that the algorithm requires less number of iterations if and is as small as possible. Hence, we followed a heuristic to obtain a better quality solution. We applied the SGD algorithm to minimize the function and used the returned solution after 40 iterations. Finding such solution accounted for less than 1% of our total-run time. Finally, we used where is computed according to the bound (11) for .

-

•

FLS: The FLS algorithm described in [23] requires two input parameters: and . To obtain , we first followed the same step as in RLS to obtain a feasible solution such that and then set . Since is feasible, using Lemma 2.1 we can guarantee that . We chose from that produces the smallest at termination.

-

•

YNW: We followed the guidance in [47] to setup YNW. Specifically, we chose the control parameters and as and , respectively, as a function of the total number of iterations , where is the weight of the gradient of the objective function and is the weight of the proximal term in the updating equation of in YNW. We chose the number of iterations such that its total data passes is . We used the all-zero vector as an initial solution to YNW. Of course, for a fair comparison, the number of data passes that RLS and FLS spend in searching the initial solution is included when comparing the performances of these algorithms.

-

•

SWG: The only input of SWG algorithm is the precision . We selected from to minimize the value of achieved by SWG at termination. It turned out gave the best performance for all the three datasets.

| LoanStats | COMPAS | German | |

|---|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

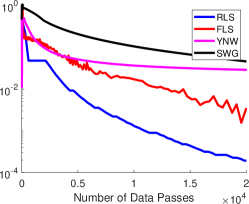

Results: Figure 2 displays the performance of RLS, FLS, YNW and SWG as a function of data passes. In particular, the -axis in this figure shows the number of data passes each algorithm performed while the -axis represents the feasibility and optimality of solutions returned by each method. More specifically, the -axis in the first row of this plot represents . As explained before, this quantity is zero when the solution is both feasible and optimal and positive otherwise. The speed at which converges to zero indicates how fast the solution becomes feasible and optimal at each iteration. The -axis in the second row represents that measures the optimality gap at and in the third row, checks whether the solution is feasible or not (if then is feasible).

We observe that RLS achieves the fastest reduction in the function on the three datasets. YNW has high constraints violation on LoanStats and German datasets. FLS and SWG are the only algorithms that maintain feasibility at each iteration and FLS reduces the optimaltiy gap faster than SWG. RLS achieves a good quality solution faster than FLS. Our computational results reveal that our algorithm compares favorable with other existing approaches in the literature.

6 Conclusion.

We develop an adaptive level-set method that is both parameter-free and projection-free for constrained convex optimization, that is, it accelerates under the error bound condition and does not require knowledge of unknown parameters or challenging projections for its execution. This method finds an -optimal and -feasible solution by considering a sequence of level-set subproblems that are solved in parallel using standard subgradient oracles with simple updates. These oracles restart based on objective function progress and communicate information between them upon each restart. We show that the iteration complexity of our restarting level set method is only worse by a log-factor in both the smooth and non-smooth settings compared to existing accelerated methods for constrained convex optimization under the error bound condition, all of which rely on either unknown parameters or sophisticated oracles (e.g., involving difficult projection or exact line search). Numerical experiments show that the proposed method exhibits promising performance relative to benchmarks on a constrained classification problem.

This section contains the proof of Lemma 3.8 and presents Lemma 6.7 and Lemma 6.9 that formally prove the inequalities (20) and (21) used in the proof of Theorem 3.9. For all the results included in this section, we need to introduce slightly different notations representing and to account for the number of restarts in each instance. More precisely, we use the notation and to respectively represent the solution in the th iteration of after restarts and the level parameter in after restarts.

Proposition 6.1

The function is an increasing function in for any .

Proof 6.2

Proof. The proof of this proposition follows from the convexity of in . In particular, let denote the sub-gradient of with respect to . It is straightforward to see for any . Hence, from convexity of in , it follows that for , we have which indicates \Halmos

Proposition 6.3

Consider , , and a strictly feasible solution used in Algorithm 2. Suppose is a critical index. For any , we have

| (44) |

Proof 6.4

Proof The proof of this proposition relies on the fact that the function is non-increasing in . The value of this function does not change if the restart is not desirable since and remain unchanged. It is easy to see that after each desirable restart, when increases, either or decreases. In both cases, the function reduces (see (10) and Proposition 6.1). Therefore, we can write

We claim . Assuming this claim is true, using the above inequality, Proposition 6.1, and the fact that , we obtain

In addition, since we obtain . The equation holds since initiated at does not change throughout the algorithm and the inequality follows from Theorem 3.4. To complete the proof, we need to show our claim is true. We actually show that this claim holds at any index . Since is a strictly feasible solution, it is straightforward to see and for all . Given , it follows from this equality and the updates of level parameters that can be written as a convex combination of and . In particular, . Our claim will then follow by applying this equation recursively since . \Halmos

Let be the smallest index at which the inequalities and hold (i.e. is the index found in Line 7 of Algorithm 2). RLS then initiates a restart at this index and also restarts all instances whose indices are greater than . Suppose this is the th restart at for . To understand how level parameters change after each restart, we reply on the following lemma where we provide a lower bound on for each .

Lemma 6.5

Suppose and are such that . Let be the index found in Line 7 of Algorithm 2. In addition, assume the level parameters for are updated as in Line 11, i.e., for . We then have

| (45) |

and

| (46) |

Proof 6.6

Proof. The equation directly follows from the steps of Algorithm 2. In particular, the level parameters are only updated for after each restart at index . Recall that the index is selected such that and Since and , we get

| (47) |

Now let’s consider the index :

| (48) | |||||

where we used the definitions of to obtain the first equality; (45) for the second; and (47) for the first inequality; Similarly for , we show

| (49) | |||||

where the second equality follows from and the last inequality form Proposition 6.1 and the fact that for which can be easily verified by combining (48) and (49) and the inequality . Applying (49) recursively along with (48) proves (46). \Halmos

Proof of Lemma 3.8: To prove this lemma, we claim that if the inequality (5) () is satisfied at some , it will continue to be satisfied after each restart. By Theorem 3.4, it will then follows that none of the indices that are smaller than the current critical index can become a critical index after the restarts. Therefore, the critical index cannot decrease throughout the algorithm. Our claim can be proved by defining the quantity , as follows:

| (50) |

We show is a non-decreasing function of when the inequality (5) holds at index . More precisely, we show the inequality holds for such . Therefore, assuming (5) is satisfied in restarts, it will continue to hold after next restart since .

Fix an index for which we have . The restarts that occur at larger indices than do not change since and remain the same. Therefore, we only focus on the restarts that either happen (i) at index or (ii) any smaller index than .

Case (i): When the restart occurs at index , it means we have found a solution such that and

Since and which follows from the restarting steps, we get

Using this inequality and the fact that , it is straightforward to see . This inequality further implies that

| (51) |

where the second inequality follows from and Lemma 2.3 that shows , and the third from the inequality which holds since the restart has occurred at index .

Case (ii): In this case we have and which follow from the restarting steps and Lemma 6.5. Hence,

| (52) |

where the inequality follows from the fact that the function is decreasing in for any (see Proposition 6.1). Considering (51) and (52), our proof is complete.

In the following lemmas we prove the inequalities (20) and (21) used in the proof of Theorem 3.9 in Section 3.

Lemma 6.7

Suppose , , and are such that and . Consider an index and as defined in (11) for . Let denote the total number of desirable restarts starting at until an -optimal and -feasible solution in found. Then we have

where is the total number of desirable restarts starting at with assuming is the critical index at the time of restart.

Proof 6.8

Proof. Using the definitions of and , it is easy to see that because by Lemma 3.8, the critical index is non-decreasing and can vary between and . Let’s consider a modification of the quantity defined in (50). In other words, we define

Since is smaller index than a critical index, using Theorem 3.4, for all we can verify that , and hence , and . In addition, Theorem 3.4 also indicates that the inequality (5) holds at . Hence, following the same proof as in the proof of Lemma 3.8, one can show

if the restarts occurs at index and

if the restarts occurs at an index smaller than . Suppose denotes the smallest restarting iteration at which the index becomes smaller than a critical index. By recursively applying the above inequality, we obtain

| (53) |

Given that is smaller than a critical index, following Theorem 3.4 we have which implies

| (54) |

where the last inequality follows from the fact that and is not -feasible and -optimal (see Lemma 2.2). On the other hand, since and remains the same throughout the Algorithm 2, we also get

| (55) |

It follows from (53), (54), and (55) that

We can then obtain our desirable bound on by taking a logarithmic transformation on both sides of the above inequality and organizing terms. \Halmos

Lemma 6.9

Suppose , , and are such that and . Consider a critical index and as defined in (11) for . Let denote the total number of desirable restarts starting at before the critical index increases or an -feasible and -optimal solution is found. Then

Proof 6.10

Proof. Suppose is the critical index between iterations and while there is no -feasible and -optimal solution is found in between (i.e. the critical index increases at iterations ). To bound , let’s consider two cases:

Case : All desirable restarts between and are from : Recall that the th restart happens when a solution is found such that and

Since and , the above inequality indicates that the function reduces by a factor of at each desirable restart since

In addition, since there is no -feasible and -optimal solution is found between and , by Lemma 2.2 we must have for any . Let denote the restarting iteration at which becomes a critical index. The above arguments, therefore, imply

| (56) |

We also know , where the first inequality follows from the fact that and the second from (44). Applying this inequality to (56) we obtain which results in finding an upper bound for . i.e.,

Case : At least one desirable restart between and happens at for some : Suppose, the first desirable restart from happens at iteration with . This means that all desirable restarts between and are from . Suppose and respectively denote the number of desirable restarts from between and and between and . Following the analysis of Case , one can show

It only remains to find an upper bound for . Suppose, after the desirable restart at , the solutions and the level parameters in and are and , respectively. We have

| (57) |

where the first inequality follows from (see Theorem 3.4), the second from Lemma 6.5, and the third from the fact that is not -optimal and -feasible. The last inequality holds since the critical index is no more than before an -optimal and -feasible is found (see Theorem 3.4).

We define

We show this quantity is non-increasing at each desirable restart. Especially, it reduces with a factor of if desirable restarts occur at . More precisely, we will prove

Finally, by providing a lower bound on for any , we show that this quantity can only be reduced by a finite number of desirable restarts.

First, let’s consider a case where and are generated by a restart at with . We then have and

| (58) |

where the first inequality follows from the definition of and the second from (see Lemma 6.5) and the fact that is a critical index and hence

Now suppose and are generated by a restart at , Since every desirable restart from happens when , we get

| (59) |

where we used and . Using (6.10) and (59) recursively and applying (44) and (6.10), we get

| (60) |

Moreover, since is not -optimal and -feasible between iterations and , from Lemma 2.2 and Theorem 3.4 we get

| (61) |

Recall that for any since remains the same throughout Algorithm 2. Finally, the inequalities (60) and (61) imply

which results in the following upper bound on :

Letting , the proof is complete. \Halmos

References

- Aravkin et al. [2019] Aravkin A, Burke J, Drusvyatskiy D, Friedlander M, Roy S (2019) Level-set methods for convex optimization. Mathematical Programming 174(1-2):359–390.

- Bayandina et al. [2018] Bayandina A, Dvurechensky P, Gasnikov A, Stonyakin F, Titov A (2018) Mirror descent and convex optimization problems with non-smooth inequality constraints 181–213.

- Beck and Teboulle [2012] Beck A, Teboulle M (2012) Smoothing and first order methods: A unified framework. SIAM Journal on Optimization 22(2):557–580.

- Bolte et al. [2017] Bolte J, Nguyen P, Peypouquet J, Suter W (2017) From error bounds to the complexity of first-order descent methods for convex functions. Mathematical Programming 165(2):471–507.

- Charisopoulos and Davis [2022] Charisopoulos V, Davis D (2022) A superlinearly convergent subgradient method for sharp semismooth problems. arXiv preprint arXiv:2201.04611 .

- Davis et al. [2019] Davis D, Drusvyatskiy D, Charisopoulos V (2019) Stochastic algorithms with geometric step decay converge linearly on sharp functions. arXiv preprint arXiv:1907.09547 .

- Davis et al. [2018] Davis D, Drusvyatskiy D, MacPhee KJ, Paquette C (2018) Subgradient methods for sharp weakly convex functions. Journal of Optimization Theory and Applications 179(3):962–982.

- Díaz and Grimmer [2021] Díaz M, Grimmer B (2021) Optimal convergence rates for the proximal bundle method. arXiv preprint arXiv:2105.07874 .

- Fercoq et al. [2019] Fercoq O, Alacaoglu A, Necoara I, Cevher V (2019) Almost surely constrained convex optimization. International Conference on Machine Learning, 1910–1919 (PMLR).

- Fercoq and Qu [2019] Fercoq O, Qu Z (2019) Adaptive restart of accelerated gradient methods under local quadratic growth condition. IMA Journal of Numerical Analysis 39(4):2069–2095.

- Fercoq and Qu [2020] Fercoq O, Qu Z (2020) Restarting the accelerated coordinate descent method with a rough strong convexity estimate. Computational Optimization and Applications 75(1):63–91.

- Freund and Lu [2018] Freund R, Lu H (2018) New computational guarantees for solving convex optimization problems with first order methods, via a function growth condition measure. Mathematical Programming 170(2):445–477.

- Goh et al. [2016] Goh G, Cotter A, Gupta M, Friedlander MP (2016) Satisfying real-world goals with dataset constraints. Advances in Neural Information Processing Systems, 2415–2423.

- Grimmer [2018] Grimmer B (2018) Radial subgradient method. SIAM Journal on Optimization 28(1):459–469.

- Grimmer [2019a] Grimmer B (2019a) General convergence rates follow from specialized rates assuming growth bounds. arXiv preprint arXiv:1905.06275 .

- Grimmer [2019b] Grimmer B (2019b) General convergence rates follow from specialized rates assuming growth bounds. arXiv preprint arXiv:1905.06275 .

- Grimmer [2021] Grimmer B (2021) General holder smooth convergence rates follow from specialized rates assuming growth bounds. arXiv preprint arXiv:2104.10196 .

- Iouditski and Nesterov [2014] Iouditski A, Nesterov Y (2014) Primal-dual subgradient methods for minimizing uniformly convex functions. arXiv preprint arXiv:1401.1792 .

- Ito and Fukuda [2021] Ito M, Fukuda M (2021) Nearly optimal first-order methods for convex optimization under gradient norm measure: An adaptive regularization approach. Journal of Optimization Theory and Applications 188(3):770–804.

- Johnstone and Moulin [2020] Johnstone PR, Moulin P (2020) Faster subgradient methods for functions with hölderian growth. Mathematical Programming 180(1):417–450.

- Lan and Zhou [2016] Lan G, Zhou Z (2016) Algorithms for stochastic optimization with expectation constraints. arXiv preprint arXiv:1604.03887 .

- Lin et al. [2018a] Lin Q, Ma R, Yang T (2018a) Level-set methods for finite-sum constrained convex optimization. International Conference on Machine Learning, 3112–3121.

- Lin et al. [2018b] Lin Q, Nadarajah S, Soheili N (2018b) A level-set method for convex optimization with a feasible solution path. SIAM Journal on Optimization 28(4):3290–3311.

- Lin et al. [2020] Lin Q, Nadarajah S, Soheili N, Yang T (2020) A data efficient and feasible level set method for stochastic convex optimization with expectation constraints. Journal of Machine Learning Research .

- Liu and Yang [2017] Liu M, Yang T (2017) Adaptive accelerated gradient converging method under h"o lderian error bound condition. Advances in Neural Information Processing Systems, 3104–3114.

- Necoara et al. [2019] Necoara I, Nesterov Y, Glineur F (2019) Linear convergence of first order methods for non-strongly convex optimization. Mathematical Programming 175(1-2):69–107.

- Nesterov [2005] Nesterov Y (2005) Smooth minimization of non-smooth functions. Mathematical programming 103(1):127–152.

- Nesterov [2013] Nesterov Y (2013) Gradient methods for minimizing composite functions. Mathematical Programming 140(1):125–161.

- Nesterov [2018] Nesterov Y (2018) Lectures on Convex Optimization, volume 137 (Springer).

- Polyak [1969] Polyak BT (1969) Minimization of unsmooth functionals. USSR Computational Mathematics and Mathematical Physics 9(3):14–29.

- Renegar [2016] Renegar J (2016) “efficient” subgradient methods for general convex optimization. SIAM Journal on Optimization 26(4):2649–2676.

- Renegar and Grimmer [2022] Renegar J, Grimmer B (2022) A simple nearly optimal restart scheme for speeding up first-order methods. Foundations of Computational Mathematics 22(1):211–256.

- Renegar and Zhou [2021] Renegar J, Zhou S (2021) A different perspective on the stochastic convex feasibility problem. arXiv preprint arXiv:2108.12029 .

- Roulet and d’Aspremont [2017] Roulet V, d’Aspremont A (2017) Sharpness, restart and acceleration. Advances in Neural Information Processing Systems, 1119–1129.

- Wei et al. [2018] Wei X, Yu H, Ling Q, Neely M (2018) Solving non-smooth constrained programs with lower complexity than : A primal-dual homotopy smoothing approach. Advances in Neural Information Processing Systems, 3995–4005.

- Xu [2020] Xu Y (2020) Primal-dual stochastic gradient method for convex programs with many functional constraints. SIAM Journal on Optimization 30(2):1664–1692.

- Xu [2021a] Xu Y (2021a) First-order methods for constrained convex programming based on linearized augmented lagrangian function. Informs Journal on Optimization 3(1):89–117.

- Xu [2021b] Xu Y (2021b) Iteration complexity of inexact augmented lagrangian methods for constrained convex programming. Mathematical Programming 185(1):199–244.

- Xu et al. [2017a] Xu Y, Lin Q, Yang T (2017a) Adaptive svrg methods under error bound conditions with unknown growth parameter. Advances in Neural Information Processing Systems, 3277–3287.

- Xu et al. [2017b] Xu Y, Lin Q, Yang T (2017b) Stochastic convex optimization: Faster local growth implies faster global convergence. International Conference on Machine Learning, 3821–3830.

- Xu et al. [2017c] Xu Y, Liu M, Lin Q, Yang T (2017c) Admm without a fixed penalty parameter: Faster convergence with new adaptive penalization. Advances in Neural Information Processing Systems, 1267–1277.

- Xu et al. [2016] Xu Y, Yan Y, Lin Q, Yang T (2016) Homotopy smoothing for non-smooth problems with lower complexity than . Advances In Neural Information Processing Systems, 1208–1216.

- Xu and Yang [2018] Xu Y, Yang T (2018) Frank-wolfe method is automatically adaptive to error bound condition. arXiv preprint arXiv:1810.04765 .

- Yan et al. [2019] Yan Y, Xu Y, Lin Q, Zhang L, Yang T (2019) Stochastic primal-dual algorithms with faster convergence than for problems without bilinear structure. arXiv preprint arXiv:1904.10112 .

- Yang and Lin [2018] Yang T, Lin Q (2018) Rsg: Beating subgradient method without smoothness and strong convexity. The Journal of Machine Learning Research 19(1):236–268.

- Yang et al. [2017] Yang T, Lin Q, Zhang L (2017) A richer theory of convex constrained optimization with reduced projections and improved rates. Proceedings of the 34th International Conference on Machine Learning-Volume 70, 3901–3910 (JMLR. org).

- Yu et al. [2017] Yu H, Neely M, Wei X (2017) Online convex optimization with stochastic constraints. Advances in Neural Information Processing Systems, 1428–1438.

- Zhang [2020] Zhang H (2020) New analysis of linear convergence of gradient-type methods via unifying error bound conditions. Mathematical Programming 180(1):371–416.

- Zhang et al. [2021] Zhang H, Dai YH, Guo L, Peng W (2021) Proximal-like incremental aggregated gradient method with linear convergence under bregman distance growth conditions. Mathematics of Operations Research 46(1):61–81.