Deep Learning for Individual Heterogeneity: An Automatic Inference Framework††thanks: The authors would like to thank Chris Hansen and Whitney K. Newey, the participants and discussants at the Chamberlain seminar and 2020 QME conference, as seminar participants at Columbia, NYU, UC Berkeley, UC Santa Barbara for useful discussions, comments, and suggestions.

Abstract

We develop methodology for estimation and inference using machine learning to enrich economic models. Our framework takes a standard economic model and recasts the parameters as fully flexible nonparametric functions, to capture the rich heterogeneity based on potentially high dimensional or complex observable characteristics. These “parameter functions” retain the interpretability, economic meaning, and discipline of classical parameters. In contrast to common implementations of machine learning in economics, these functions need not be predictions. We show that deep learning is particularly well-suited to structured modeling of heterogeneity in economics. First, we show how the network architecture can be easily designed to match the global structure of the economic model, delivering novel methodology that moves deep learning beyond prediction. Second, we prove convergence rates for the estimated parameter functions. These parameter functions are then the key input into the finite-dimensional parameter of inferential interest. We obtain valid inference based on a novel orthogonal score or influence function calculation that covers any second-stage parameter and any machine-learning-enriched model that uses a smooth per-observation loss function. No additional derivations are required and the score can be taken directly to data, using automatic differentiation if needed to obtain the components: the researcher need only define the original model and define the parameter of interest. A key insight is that we need not write down the influence function in order to evaluate it on the data. We apply this after deep learning, but our result can be used for any first-step estimator. Our framework covers, as special cases, well-known examples such as average treatment effects and partially linear models, but we also seamlessly deliver new results for such diverse examples as price elasticities, willingness-to-pay, and surplus measures in binary or multinomial choice models, average marginal and partial effects of continuous treatment variables, fractional outcome models, count data, heterogeneous production function components, and more. Across all these contexts inference can be made as automated as is currently available in special cases. We illustrate the utility of our framework with an application to a large scale advertising experiment for short-term loans. We show how economically meaningful estimates and inferences can be made that would be unavailable without our framework.

Keywords: Deep Learning, Influence Functions, Neyman Orthogonality, Heterogeneity, Structural Modeling, Semiparametric Inference

1 Introduction

The goal of this paper is to leverage modern machine learning and rich data to capture individual heterogeneity in the context of economic models. Parametric, structural models are a cornerstone of applied research in economics and social sciences. The parameters estimated in these models are interpretable, useful for policy, and disciplined by economic principles. We develop a methodology to maintain these advantages while simultaneously incorporating machine learning methods for flexibly estimating heterogeneity. Our idea is to recast the parameters of a model as flexible functions themselves: enriching the model without losing the structure. We estimate the parameters using deep learning, for which we provide new results. We then deliver second-step inference by deriving a novel influence function that applies to any such enriched model.

The starting point is a researcher-specified model that relates outcomes to the covariates of central interest, the policy or treatment variables . This model is encapsulated by a loss function for a vector of parameters that are estimated from the data. The model encodes structure that is grounded in economic principles and economic reasoning. To fix ideas, take the context of our empirical application where we revisit the data of Bertrand et al. (2010). Here is a customer’s binary choice to apply for a loan and are characteristics of the loan and an advertisement received, one of which is the interest rate offered. A standard approach to this problem would be a (structural) logistic binary choice model where the parameters are the coefficients on , including an intercept. Such a model has numerous advantages. First, the parameters have a clear and direct interpretation, and generally respect economic theory. Second, economically meaningful, and policy-relevant, summary parameters are easily computed, such as elasticities or measures of surplus. Further, the economic structure can be used to answer substantial policy questions. For example, although interest rates are only observed at certain values, we can use the model to study what would occur at other levels. Indeed, from basic economic principles like profit maximization, we can compute the optimal interest rate as a function of the parameters, say . All of these are only possible because of the economic structure imposed on the analysis.

However, if there is heterogeneity, which is almost a given in most contexts, the parameter estimates may not be reliable in practice, and this has spurred a push to move beyond rigid parametric models, which can only crudely capture heterogeneity, if at all. Heterogeneity can come in many forms or depend on many things. This fact, along with the increasing availability of large, complex data sets, has motivated the adoption of novel machine learning methods in economics, allowing researchers to study economic phenomena at levels of detail previously not possible.

Our approach to this problem allows for the use of powerful machine learning to capture rich heterogeneity, while simultaneously maintaining the structure and interpretability of the economic model, with all its advantages. To do this, we recast the model’s parameters as functions of observed characteristics , thus enriching the model to . These “parameter functions” allow for fully flexible heterogeneity but keep intact the structure of the economic model connecting and . In general we will not know either the functional form of nor which covariates are important. This is one strong motivation for applying modern machine learning methods. Our approach exploits the flexibility of machine learning within the structure dictated by economic models.

We thus deploy machine learning to directly estimate meaningful objects, which has several advantages compared to using ML to only obtain predictions. First, for any set of characteristics , gives the effect for an individual of “type” , and therefore retains all of the meaning, interpretability and usefulness of the original parameters. Additionally, we can “score” or “type” future individuals through their characteristics, because captures heterogeneity that can be used for future policy. Second, because we have maintained the economic model, we can leverage its structure to answer substantive questions. For example, in our data we can compute the personalized, targeted optimal interest rate .

Our approach of implementing ML by enriching an economic model thus directly address several major drawbacks of common applications of ML in economics. Typically, ML have largely been confined to prediction problems, or those that can be convert to prediction problems. These prediction functions are added to models only as nuisance functions. The term “nuisance” here is illustrative: it connotes that flexibility is required in some piece of the model, but is not per se interesting or meaningful. This is typical not just of ML, but of semiparametrics more broadly, and we aim to depart from this mindset. In the context of our application, for example, this might mean using ML to classify potential borrowers with an unstructured function : a pure prediction problem. Such an estimate would not only have worse statistical properties, it would lose the economic meaning of the original model. The results would not be interpretable directly and useful quantities would be difficult or impossible to extract. Further, without the discipline of the economic principles of the model, such estimates may make little sense.

To implement our approach we require estimates of the parameter functions and an inference engine for second-stage parameters of interest. We gives results for both steps. In both cases we make heavy use of the idea that we have enriched an economic model: it is this concrete structure that enables us to deliver broad and powerful results. For first stage estimation, we show that deep neural networks (DNNs) have a unique combination of strengths which makes them able to directly incorporate the structure of the economic model as well as handle modern data sets and complex heterogeneity. We prove new convergence rates in this context. For second step inference we give a new orthogonal score that can be widely and easily applied.

Deep neural networks have had incredible empirical success, matching or setting the state of the art in a wide range of tasks. But this has largely been in prediction problems, and indeed, most software is designed only to optimize prediction loss functions. We develop a novel, yet simple, architectural idea so that the global structure of the economic model is baked into the estimation directly and the parameter functions are recovered, instead of focusing on prediction. The idea is simple and implementation is straightforward, but this appears to have been mostly overlooked in the ML literature. Our ideas are in the vein of nonparametric M-estimation, which has a longer history but has relied on classical methods which are not equipped to handle the complex heterogeneity that is the hallmark of modern applications. DNNs also handle discrete data seamlessly in practice (as well as in theory), in contrast to classical methods. We prove new results for structured deep neural network estimates of , which crucially recover the parameter functions, not predictions, and depend on the dimension of , the heterogeneity, independent of the dimension of the variables of interest . Our results build on the recent work of Farrell et al. (2021) and contribute more broadly to the nonparametric M-estimation literature (see Chen (2007) for review and references).

Next, a feasible inference engine is required following the deep learning of in the enriched model. We obtain valid inference on a finite-dimensional parameter of interest that depends directly on the parameter functions . We achieve this by characterizing an influence function, or orthogonal score, for , and then making use of the recent results for influence function based estimators following machine learning. Our derivation builds directly on long-standing ideas in semiparametrics, chiefly Newey (1994), and for inference we follow the method of Chernozhukov et al. (2018), combining an orthogonal score with sample splitting. A drawback of this general approach to semiparametric inference is that the influence function must be known in advance, and this has perhaps hampered take-up among applied researchers. Most applications focus on a few special cases where the influence function is known (e.g. the case of average treatment effects). Our contribution to inference is to derive a single influence function that includes the correction term for any smooth per-observation loss . Thus, for any ML-enriched economic model inference can proceed without further calculations. We apply this after deep learning, but our influence function can be used in general, for any first step estimator meeting standard conditions, such as lasso, trees and forests, or classical sieve or kernel methods. Our influence functions recovers well known special cases such as average treatment effects and partially linear models, but immediately delivers new results for many other contexts, including selection models, choice models, fractional outcomes, and more broadly, smooth QMLE contexts and other such areas.

A key insight is that we only need to characterize the influence function and evaluate its empirical analogue at each data point, consequently obtaining a point estimator and standard errors, without needing to explicitly write it down. This can be contrasted with the typical approach of writing down the influence function, or orthogonal score, explicitly and then plugging in estimates of each nuisance function. Our goal is to make inference feasible in a wide variety of settings, not to focus on the properties of the score, such as efficiency comparisons, and this shift of mindset allows for broadly applicable methodology. An important tool here is automatic differentiation. The influence function depends only upon ordinary derivatives of the model and of the function defining the parameter of interest, as though the model were still parametric with homogeneous effects. In many cases, the derivatives of the model are already well known, and these forms can be used, but if not, the derivatives can be evaluated on the data automatically. For example, recall that in our empirical study, is the personalized optimal interest rate. This is not available in closed form, but rather as the solution to a fixed point problem. Therefore, the influence function for a parameter such as expected profits at the optimal personalized interest rates cannot be explicitly written down. Nonetheless, because is a smooth function of , and depends smoothly on , its derivatives can be evaluated at each data point with no trouble, allowing feasible inference. This would not be possible without our approach that retains the economic structure of the model.

Taken together, the combination of the specification we adopt, the availability of computing infrastructure, and the theory we present, offers a perfect package for applied researchers across economics and social science hoping to exploit ML but maintain discipline-specific knowledge and interpretability. Our work should be broadly useful by delivering a tractable and valid estimation and inference framework that covers many interesting contexts. The next section presents an overview of our methodological framework and its interpretation, and gives a brief overview of the main results. Our results related to many strands of recent literature, and we discuss these in context as they arise. Section 3 shows how deep learning is an excellent tool in our context and gives theoretical results. Section 4 discusses semiparametric inference, our novel influence function, and asymptotic normality. We apply our methods in Section 5 to an empirical study of short term loan applications. Section 6 gives a sense of the breadth of applicability of our results by discussing a number of examples, but is by no means exhaustive. Extensions are discussed in Section 7 and finally Section 8 concludes. Proofs are given in the appendix.

2 A Methodological Framework for Enriching Economic Models with Machine Learning

In this section we describe our framework enriching economic models to capture individual heterogeneity and give an informal summary of our results. The starting point is a standard, parametric economic model. We assume the researcher observes data on outcomes, , and on the covariates of central interest, or treatments, , which can be continuous, discrete, or mixed.111 Notation. Vectors and matrices will be written in boldface. Capital letters are used for population random variables; lower case for realizations. The expectation operator with respect to the true data generating process is denoted . The norm for a function is . The researcher relates these two with an economic model, which is encapsulated by a parametric per-observation loss function, , indexed by a parameter . For some parameter space , dictated by the structure of the problem, the researcher then solves , that is, standard M-estimation, including all (psuedo-/quasi-) likelihood-like settings. Two key aspects of this approach are: (i) are parameters, not predictions, and have economic meaning and (ii) the effects are homogeneous. We will retain (i) while removing (ii).

Our framework starts with the same parametric model, but recasts the parameters as functions of observed individual characteristics to allow for heterogeneity. Thus, in place of we will have , mapping , and we assume that the true parameter functions solve

| (2.1) |

for an appropriate function class (formalities are given below). We can thus capture heterogeneity in a fully flexible way, while retaining all the structure and interpretability of the standard model. For intuition, it is often useful to remember that at any value , has the same interpretation as , but for the “type” determined by . It is also useful to think of individual-specific effects, which may be what researchers are implicitly worried about when heterogeneity is a concern, that is minimizes for each . Such individual specific parameters are also as interpretable and meaningful as the original, homogeneous case, but of course cannot typically be recovered from the data, and may not be useful in the future, as person will not be seen again. One can think of as an approximation to , one that uses all available information, and thus captures the portion of heterogeneity useful for future policy targeting.

The functions are not prediction functions necessarily, nor do we view them as nuisance functions, a term which implies they are uninteresting. Section 3 shows why deep learning is well suited for structured modeling and gives a novel, yet simple architectural idea for doing so. This means that we use deep learning to recover meaningful functions, thus moving ML away from prediction tasks and toward estimation of scientifically and economically interesting objectives, a shift in mindset from the typical applications of machine learning. This implementation innovation and the convergence rates for the resulting estimated parameter functions are the two main contributions of this paper to deep learning, and to machine learning first stage parameters more broadly.

The key result is that we estimate the parameter functions at a fast enough rate for inference, and importantly, that the rate depends only upon the number of continuous heterogeneity covariates, denoted , and does not depend on dimension of the policy/treatment variables. That is, for our estimator of defined by (2.1), Theorem 1 establishes that

provided is sufficiently smooth and curved near the truth. This result relies on our novel architectural idea, where the structure of the model is baked directly into the deep net architecture. The architecture, and hence the optimization of the loss, targets the parameter functions, not predictions. This idea is illustrated in Figure 1.

The heterogeneous parameter functions are then key inputs into the final parameter of inferential interest, denoted . For a known, smooth function , chosen by the researcher, we conduct inference on

| (2.2) |

where is some fixed value of interest. Many economically interesting statistics take this form, in particular, depending on functions that are not predictions. To make inference feasible we derive an influence function for any such , which includes deriving the correction factor for any ML-enriched M-estimation problem. Regularity conditions are below; in particular, we assume the is pathwise differentiable. Beyond this, the form of can be generalized at the cost of notation.

The main theoretical contribution to second stage inference is the influence function calculation, yielding a Neyman orthogonal score, that is specific enough to be directly implemented while still being general enough to cover any enriched structural model based on a smooth per-observation loss function. From a practical point of view, two key ideas in our work are the use of computational differentiation (automatic or numerical) and the conceptual point of evaluating influence functions on the observed data rather than writing them down.

Theorem 2, in Section 4, gives the Neyman orthogonal score for any (sufficiently regular) such parameter and first stage coming from an ML-enriched model. Importantly, this score depends only on ordinary derivatives. Let and be the gradients of and with respect to and denote the conditional expectation of the Hessian of , all evaluated at . Then the Neyman orthogonal score is , where

This can be taken to the data directly. That is, given estimators and , we can evaluate at every data point without further derivation, which is all that is required for feasible estimation and inference. For many standard models, these derivatives are known. If not, they can obtained using automatic differentiation tools or other computational methods. In other words, once the researcher specifies their economic model via and parameter of interest via , the full influence function is known and ready to use. This holds for any sufficiently smooth functions, even if not available in closed form, as in our example with the optimal interest rate and corresponding profits.

The general form of this orthogonal score and what each piece represents conceptually should call to mind the parametric case. If were constant, then classical results for two-step estimation, as in Newey and McFadden (1994, Section 6), would yield the effect of the first stage on the second, and deliver an influence function that looks the same, but with and as constants, instead of conditional on . Thus our influence function result can be viewed as establishing the analogous result for fully nonparametric parameter functions. We view this familiarity as a strength, as it perfectly matches our core idea of enriching a well-understood economic model, and may help to demystify semiparametric inference.

Armed with this orthogonal score, we can obtain a point estimator and standard errors such that , allowing inference on any aspect of the vector . For example, if so the parameter of interest is a scalar,

is a valid 95% confidence interval. Obtaining this inference in practice is no more difficult than what is currently available for simple cases, like average treatment effects: we estimate the two nonparametric objects, and , and plug them in as needed. Estimation of is discussed in more detail below, and can rely on standard ML methods, including deep learning, and may require sample splitting. However, an important methodological point is that when is randomized this matrix can often be computed, as opposed to estimated. In general, two-step semiparametric inference often involves a denominator term such as this, and computing this term can yield more stable and robust results compared estimating it. See Remark 4 and our application in Section 5.

A special case of our framework that is useful for illustrating the main ideas, as well as prevalent in empirical and theoretical work, is when is a scalar and (2.1) is built around conditional mean restriction and the parameters are the intercept and the slopes. That is, let include a constant term and assume that for a known function ,

| (2.3) |

Recall that the are observed; this is not a random coefficient model.222One can consider the random coefficients model an alternative parametric model. As such, we conjecture that our framework can be adapted to those settings as well. We leave that to future research. Rather, we have made the intercept and slope fully heterogeneous in observables. Clearly, (2.3) can be implemented using (2.1), given an appropriate loss function. A crucial piece will be the first order condition of that loss, that is, what orthogonality condition to use. For example, if is the logistic link we may take to be the nonlinear least squares or the likelihood, which have different first order conditions, and this will change the influence function given later and thus impact implementation. O’Hagan (1978) may be the earliest treatment of a model like (2.3), and the structure here is often known as a “varying coefficient” model (Cleveland et al., 1991; Hastie and Tibshirani, 1993), “functional coefficient” model (Chen and Tsay, 1993), or “smooth coefficient” model (Li et al., 2002), and falls into the class of “extended linear models” as in Stone et al. (1997). Our results speak directly to this literature and to additive models, where , for non-overlapping subsets of , we will obtain rates for and .

The form of Equation (2.3) makes clear that our approach is to enrich a parametric relationship between the outcomes and policy variables , rather than restrict a fully nonparametric (prediction) model. It is better to view as an ML-enriched version of instead of as a restricted version of the a prediction model such as , which would be more typical of ML.

This distinction is both practically and theoretically important. Again, consider the binary choice model of our application. In our framework, the heterogeneous interest rate (price) effect is directly available as a coefficient function. Compare this to the unstructured prediction case: to recover the same conceptual quantity one would first estimate the prediction function and then obtain the derivative with respect to the rate variable (an element of ), that is, . This is possible, but cumbersome, and inference on the average may not be regular without weighting (see also Section 6.3). It would be difficult or impossible to recover measures such as elasticities or optimal prices. However, with our structural model, all of these are simple and automatic.

3 Structured Deep Learning for Parameter Functions

We now discuss in detail the deep neural network (DNN) estimation of the parameter functions and state our theoretical results for the first stage. DNNs have a unique combination of strengths which makes them an excellent choice, among machine learning methods, for recovering individual heterogeneity. The most obvious argument for deep learning is the incredible success DNNs have had across a wide variety of learning problems, in research applications and real-world use. They have been found to handle many different tasks and data types extremely well. In many applications the dimension of is large enough, and the heterogeneity complex enough, that classical methods will not work, but deep learning still yields excellent results. See Goodfellow et al. (2016) for a textbook treatment and Farrell et al. (2021) for recent literature and further introduction.

The primary use of DNNs has been for prediction, and much of the statistical study has been restricted to this case. We take DNNs beyond prediction, and use them to learn the (structural) parameter functions . To do so, we design a new architecture, shown in Figure 1, to measure the loss directly in terms of the parameter functions. The key idea is to decouple the final loss and the functions to be learned: we use DNNs to approximate the parameter functions in a penultimate “parameter layer”, and these are then combined according to the economic model in the final, “model layer” of the network. This is crucial because it forces the machine learning to be faithful to the economic structure and it allows us to learn the components of , which are of direct interest and required for learning . To approximate the functions we use standard fully-connected feedforward networks (multi-layer perceptrons, MLPs) and the rectified linear unit (ReLU) activation function.

This change, from to is simple, yet powerful. It allows for deep learning of individual heterogeneity on any interesting parameter function. These functions may be coefficients that ultimately go into a prediction, as in Equation (2.3), variances or covariances, or other parameters of the original model. To make this formal, let be a class of ReLU-DNNs that is restricted to our structured architecture, and also yields bounded. We then obtain by solving the empirical analogue of (2.1),

| (3.1) |

DNNs are not the only possible method that can be used, nor do we claim any formal optimality for them. Having said that, from a practical point of view, they are ideal for several reasons. First, we are able to easily and transparently make our estimator mirror the global structure of the model because DNNs learn a basis-function style representation, and in this way are akin to a global smoother.333The distinction between a global and local smoother is not universal or precise. Here, we use “global” to mean that the estimator imposes a global smoothing across the data, typified by a series estimator, whereas a “local” estimator imposes only local smoothing structure, typified by Nadaraya-Watson kernel regression. However, this need not match the notion of using global versus local data in estimation: for example, although series estimators are generally regarded as global, those such as splines or partitioning, through their specific basis functions, use only local data (Cattaneo and Farrell, 2013; Cattaneo et al., 2020b). More apt for the present purpose, we dub this property “structural compatibility”. This makes the machine learning faithful to the economics, rather than allowing the reverse. Although it is possible to embed “local” methods, such as kernel-based (Fan and Zhang, 2008) or tree-based (Zeileis et al., 2008; Athey et al., 2019; Chatla and Shmueli, 2020) estimators, doing so with DNNs is simple, transparent, and tractable, and as the economic model holds globally, we may wish to match this in estimation. Second, like tree-based methods, DNNs handle discrete covariates automatically, including fully flexible interactions. We do not need to restrict attention, in practice or in theory, to continuous . In nonparametric theory there is often no penalty in the rate of convergence for discrete variables (under standard assumptions), but realizing these gains in practice can be difficult, as most nonparametric estimators are designed with continuous variables in mind (such as those built upon basis expansions or kernel approximations). DNNs require no customization: the inputs shown in Figure 1 can be any mix of continuous and discrete data. By exploiting our structured architecture, we prove that only the dimension of the continuous elements of , the heterogeneity, affects the rates of convergence of our DNN estimators, neither discrete covariates nor impact the rate.

The handling of discrete covariates is a major advantage over classical sieve methods or methods that select series terms, such as the lasso. Classical methods are ill-equipped to handle modern complex, high-dimensional tasks, and, in practice, variable selection methods require pre-specifying the functional forms and interactions over which to search. However, such methods are structurally compatible in our sense, and our results contribute directly to the large body of work on nonparametric M-estimation (see Chen (2007) discussion and further references). Setting our methodology and theory apart from earlier work is that we explicitly advocate the enrichment of a standard structural model, relating and , rather than starting with a fully generic case. The more common starting point in semi- or nonparametric M estimation and inference would be a model such as , instead of our explicit enriched model and two step approach. Our approach is what allows us to deliver concrete, fully implementable results. Extensions to more general settings would be a useful future step, however.

Finally, it is worth mentioning that other recent work has considered the combination of deep learning and some form of structural modeling (examples include Wei and Jiang, 2019; Igami, 2020; Kaji et al., 2020; Chen et al., 2021). Typically, the goal is estimation of a parametric structural model and deep learning methods are applied to learn the mapping of data to parameters. Our focus, using deep learning to estimate individual-level heterogeneity, is quite different, and further, we give theoretical results on deep neural network estimation and subsequent inference which are not available in prior work. Babii et al. (2020) combine economics with prediction-focused machine learning, where economic reasoning is used to support assymetric in classification loss functions. This is another interesting avenue for merging economics with machine learning.

3.1 Convergence for Structured Deep Neural Networks

We now state our theoretical results for DNN estimation of the parameter functions . We will give a generic result, which necessarily requires high level conditions, and then illustrate more concrete ideas in the case of the slope and intercept parameter functions. The results in this section contribute to the recent literature on the statistical properties of deep learning and to the longer tradition of sieve M estimation. Our assumptions and results are reminiscent of both.

We require two sets of conditions: one covers the model and one gives regularity for and . For the loss function, we require Lipschitz continuity in general and, near the truth, sufficient curvature. Neither are restrictive and both are common in the nonparametric M estimation literature (cf Chen (2007) and others, where further references and use of other norms are discussed). These conditions are for estimation of ; further assumptions will be required for inference.

Assumption 1.

Suppose that are nonparametrically identified in (2.1), uniformly bounded, and that there are constants , , and that are bounded and bounded away from zero, such that

The curvature requirement will often be implied by restrictions on the Hessian or on the matrix . Such restrictions are natural in our setting, as they will be required for inference anyway, and are known to hold in many contexts. Some potentially interesting cases are ruled out, such as quantile regression. Modifications to our theory could allow for these cases: for example, Padilla et al. (2020) apply the methods of Farrell et al. (2021) to quantile regression.

Let be the population random variables, with an observation denoted . Let denote the continuously distributed elements of , and define , and take the rest to be binary random variables, without loss of generality. Part (iii) of this assumption restricts to smooth functions, which are known to be approximable by deep neural networks Yarotsky (2017, 2018); Hanin (2017).

Assumption 2.

(i) the elements of are bounded random variables. (ii) has compact connected support, taken to be . (iii) As functions of , the continuously distributed components of , , for , where for positive integers and , define the Hölder ball of functions with smoothness as

where , and is the weak derivative.

We now have the following result, proven in the appendix. Here we focus on smooth functions as well as the commonplace deep and wide multi-layer perceptrons (fully connected, feedforward neural networks). In the appendix, we give a more general result, one that is agnostic about the type of approximation, and hence the type of network. For example, the general results can be used to obtain faster rates or cover fixed-width, very deep networks (Farrell et al., 2021, Section 2.3).

Theorem 1.

Let , , be a random sample that obeys Assumptions 1 and 2. For solving (3.1), with structured according to Figure 1, with width and depth , it holds that

and

for large enough with probability , for , where the constant may depend on the dimensions , , and other fixed quantities in Assumptions 1 and 2.

The result of Theorem 1 speaks directly to the nonparametric M estimation literature. It shows that deep nets enjoy the same properties of other methods, but has the advantages discussed above. A theoretical drawback is that for a given smoothness level, this rate is not optimal. It is however sufficiently fast for inference and reflects the excellent empirical performance. This theorem fully takes deep learning away from prediction and toward learning economically meaningful parameters.

The conditions of Theorem 1 are necessarily high level, giving the generality of the setting. Verying these conditions in a given setting is required, but is often straightfoward. Importantly, because we are specifically focusing on enriching a parametric model, familiar analyses from the parametric case can aid in interpreting the conditions required. For example, our conditions are the natural analogues of what is required in well-understood QMLE problems, and the intuition from these can be ported directly.

To illustrate, return to the regression-type model of (2.3), where the model is and includes a constant term. The final loss in this case still revolves around prediction (beit a QMLE or nonlinear least squares), but our architectural idea is still important, because we need to learn the slope and intercept functions separately. This is shown in Figure 2. That figure also illustrates how our results apply immediately to generalized additive models, where the different components of are known to rely on different subsets of : we simply sever the appropriate links, so that separate networks feed into the parameter layer nodes.

For this model we can also illustrate the verification of the high level conditions with familiar, primitive assumptions in this case.

Assumption 3.

(i) The conditional expectation enters the loss through a known, real-valued transformation , where (i) and are continuously invertible and and belong to , for . (ii) Assumption 1 holds with replaced by , and the conditions therein apply to the scalar argument . (iii) The eigenvalues of are bounded and bounded away from zero uniformly in .

Condition (i) ensures that the loss function is sufficiently smooth while (ii) and (iii) ensures the curvature through the standard positive variance condition. These conditions are familiar from the parametric case. For example, consider condition (iii) in the original model . In such a model, the assumption that is positive definite would be standard. Leaning on the intuition that the enriched model is akin to running the original model for each , we see the condition is exactly what would be expected. Versions of these assumptions are also required in the semiparametric models that are special cases of , including treatment effects and partially linear models, as in Section 6.

These assumptions are sufficient for identification of the slope and intercept functions in this case. A similar verification should be done for other models, and may lean on prior work in parametric M estimation, as discussed for several cases in Section 6. Specializing Theorem 1 to this case, we have the following result.

Corollary 1.

Here we give two results. First, we show that we can estimate the heterogeneous intercept and slope parameters at the appropriate rate, depending on the dimension of the heterogeneity. This is direct from Theorem 1. This is required as economic constructs depend on these parameters, rather than on the conditional expectation as a whole.

We also state a result for estimating the regression function in the structural model (2.3). From a statistical point of view, this result establishes that structured DNNs have excellent performance in varying coefficient models, additive models, and other such cases, and therefore may be of independent interest. It is also useful for comparing to the more typical use of inference after ML, where the (prediction) function would be unstructured. The key feature to note is that the convergence rate depends only on the dimension of (the continuous component of) , not . Even if the final inference relies on conditional expectations, or if the parameter functions could be obtained from the unstructured predictions, naive estimation of these would give a much slower rate, dependent on (since includes an intercept). This would often be too slow for subsequent inference. For example, in our empirical illustration this would require 22 dimensional nonparametrics, which may be prohibitively high even for deep learning, and if the goal is to recover a measure of “linear” impact, such as a treatment effect, marginal effect, or other average derivative, an unnecessary complication.

That the rate depends only on is intuitively exactly what should happen: the heterogeneity is where the model is flexible. In our case, this result is due to our structured architecture, Figures 1 and 2, and not adaptive estimation. The model structure is enforced, not recovered. Certain specialized types of DNNs may in fact adapt to such structures (Bach, 2017; Bauer and Kohler, 2019; Schmidt-Hieber, 2019). First, this is not useful for our purposes because cannot be recovered. Second, experience has shown that imposing the structure of the model (2.1) improves estimation quality when the structure exists to allow for adaptivity.

For other recent theoretical results on deep learning in other contexts, see Liang (2018), Polson and Ročková (2018), Wang and Ročková (2020), Liang and Tran-Bach (2020), and references therein as well as in Farrell et al. (2021). One important aspect we do not address is regularization, neither the implicit regularization that may occur in the optimization nor explicit regularization of the network parameters themselves though norm penalties, weight decay, drop out, or other methods. In our applications we obtain excellent performance without using explicit regularization, though in low signal-to-noise scenarios adding explicit regularization to the implicit regularization may yield improvements, and has been shown to be optimal in an adversarial game with nature (Blanchet et al., 2020). The role of regularization, its implementation, and its consequences for estimation and subsequent inference, are major open questions for deep learning.

4 Influence Function and Semiparametric Inference

With the framework in place and estimates of the parameter functions in hand, we now turn to estimation and inference for from (2.2). The key contribution here, given in Theorem 2, is a novel Neyman orthogonal score for any such , given any model (2.1). Importantly, this score can be immediately taken to data, without additional derivations. Our framework is simultaneously general enough to cover a large number of settings, yet specific enough that the influence function can be fully characterized. As is standard, the orthogonal score depends on and a second nonparametric object, but the latter piece is also fully characterized and is therefore estimable without additional work. With this score, we can apply the methods and results of Chernozhukov et al. (2018) to immediately obtain asymptotic Normality. This is spelled out in Section 4.2 below.

4.1 Influence Function

Obtaining valid semiparametric inference does not require basing the estimation framework on an influence function (or Neyman orthogonal, doubly robust, or locally robust, scores). The major appeal of these methods is that we can obtain valid distributional approximations under weaker conditions on the first stage estimates, i.e., on how well recovers . These weaker conditions are known to hold for many ML methods, and in particular Section 3 shows that they hold for deep learning. In other words, it is useful to view the influence function as a tool for obtaining feasible inference, rather than being of direct interest itself, for efficiency considerations or other comparisons. This viewpoint is implicit in much recent work on inference after ML (e.g., Belloni et al., 2014; Farrell, 2015; Chernozhukov et al., 2018) but it is worthwhile to make it explicit to better understand how thinking this way greatly expands the breadth of what we can cover, including cases like the optimal interest rate, which cannot be given in closed form. The same motivation is explicit in the recent work on “auto-DML”, where the necessary pieces of the influence function are estimated from the data, and are thus need not be derived at all (Chernozhukov et al., 2020c, b; Chernozhukov et al., 2020a; Chernozhukov et al., 2020d; Chernozhukov et al., 2021). Our focus on interpretable parameter functions rather than regression functions distinguishes our setting from this line of work, which manifests in two central ways: (i) our first stage is more general, as we do not focus on regressions; (ii) our inference targets are broader in some ways, given the flexibility of the first stage, but we require to enter through evaluation at , ruling out examples such as integrals across data points.

Influence functions have a long history in econometrics. Newey (1994) remains the seminal treatment. We defer to that work and Ichimura and Newey (2015) for more background, including regularity conditions for existence of an influence function. Perhaps the most well known and commonly used influence function is that for average treatment effects, which we recover as a special case in Example 6.1. The history of this influence function is illustrative: it was characterized precisely first for the purposes of efficiency considerations (Hahn, 1998, 2004), later used to show certain plug-in estimators could be efficient (Hirano et al., 2003; Imbens et al., 2007), and finally only recently used for post-ML inference to exploit the weaker conditions (Farrell, 2015). The partially linear model (Section 6.3) is another standard example and followed a similar trajectory, most imporantly for our discussion being the first setting where inference was proven (uniformly) valid after variable selection (Belloni et al., 2014).

In both cases, the influence function was first derived and then its components estimated directly. This exercise has been repeated in numerous models for numerous parameters (see Section 6, and lists in Ichimura and Newey (2015) or Chernozhukov et al. (2020a)). In a sense, we follow this path: derive the correction factor for any setting in Section 2, obeying the regularity conditions below. However, our correction factor covers many settings, as we take advantage of the structure of the original model in the derivation. Thus, in any of these settings, inference is now as straightforward as it is for average treatment effects: two nonparametric pieces must be estimated, and these are combined into the orthogonal score, with sample splitting if needed. That is, we can follow the recipe of Chernozhukov et al. (2018). We broaden the application of these ideas and show how they work even in cases where we use automatic differentiation to obtain the piece of the score and the parameter of interest is not available in closed form. That is, we can still evaluate the influence function estimator, given below, on the data points. And so, while deriving correction terms for estimation is somewhat standard, or results are novel in their broad applicability. Our influence function nests many cases from the literature and delivers new results.

Our end result will reflect the core idea behind our framework: enriching a standard model by converting the parameters to parameter functions. In purely parametric two-step models, without heterogeneity, the influence function of the first step parameters themselves can be used to adjust the second step (Newey and McFadden, 1994, Section 6). Our result is the nonparametric generalization of this, and one strength of the result is this familiarity, which will aid in practice by making assumptions transparent and familiar and by guiding implementation.

To state the result, we will in fact require the gradient and Hessian of , defined via ordinary differentiation. Let be the -vector of first derivatives,

| (4.1) |

and as the matrix of second derivatives, that is with element given by

| (4.2) |

where and are the respective elements of the place-holder . The use of standard differentiation in these contexts has been used in some prior work.

We can now state our assumptions and give the main result of this section, the form of the orthogonal score. Our assumptions are mostly standard and ensure sufficient regularity for our influence function to be calculated and asymptotic normality obtained by resulting estimator. One conceptually important point is that in general these conditions are not sufficient for a causal interpretation, which will require some form of unconfoundedness or conditional exogeneity (as in Examples 6.1 or 6.3).

Assumption 4.

The following conditions hold on the distribution of , uniformly in the given conditioning elements. (i) Equation (2.1) holds and identifies , where is thrice continuously differentiable with respect to . (ii) . (iii) For of (4.2), is invertible with bounded inverse. (iv) The parameter of Equation (2.2) is identified and pathwise differentiable and is thrice continuously differentiable in . (v) and possess finite absolute moments and positive variance.

The most important assumptions here are that the first order condition of (2.1) holds and that is pathwise differentiable. The latter keeps focus on semiparametric contexts. The former follows our idea to take a well-defined parametric model, for which such identification would hold, and enrich the model with machine learning. Of course not all models of the form (2.1) will be so identified, and this must be verified.

For intuition, consider the case of the conditional mean restriction (2.3) where simple sufficient conditions can be stated. Many loss functions yield , in which case , with the derivative of with respect to its scalar argument, evaluated at the index , . Condition (iii) will then often be implied by other conditions on the model. For example, if is the logistic link and is bounded away from zero and one (which in turn may be implied by conditions on , , and the functions , such as boundedness). Or, in the context of treatment effects we need the standard overlap condition. Some version of the condition of positive variance, or invertibility of , is quite standard in semiparametric problems.

We can now state our influence function result, derived in Appendix B.

Theorem 2.

At this level of generality, this influence function is new to the literature and yields many new contexts for inference after ML. In some special cases we recover existing results, particularly under (2.3) with , such as average treatment effects (Section 6.1), partially linear models (Section 6.2), and average partial effects (Section 6.3). Most importantly, when the first stage is restricted to regression under the squared loss, Newey (1994) gives the form of the correction factor for a broader set of moment conditions than (2.2). Beyond these specific examples, our result appears new, both in generality and in the many concrete cases we give, such as choice models or linear IV models.

The form of the influence function is standard: a plug-in piece and a correction or debiasing piece. The correction term relies on three derivatives, , , and , and these can be computed easily using automatic differentiation, if they are unknown, and thus there is no derivation required before estimation can take place.

The form of the correction term, specifically , warrants further discussion. Behind this form is again the fact that we start with a model and enrich its parameters to be functions. This means that the parametric submodels that lie behind the pathwise derivative calculation simply trace through the space of the original, parametric structural model, which is well understood and well behaved. The fact that the model relates and in a known way, with parameters enriched using , is important as it allows for a simple isolation of the contribution of the nonparametric estimation. Due to this, and the two-step nature of our set up, this term does not depend on , which is helpful when several parameters are of interest in one application.

The function is a nuisance in the truest sense: it is required only because we use influence functions as a tool to obtain valid inference. The presence of an inverse function is commonplace in semiparametric inference problems. The matrix is never high dimensional, again due to our approach (cf Remark 1). Estimation or calculation of will simplify in many cases, particularly if one has prior knowledge that only a certain subset of the heterogeneity covariates, say , are relevant for . An extreme case is randomization (Remark 4 below). Another example occurs with being prices, which are known with certainty to be set by the firm according to only several characteristics of the market or consumer.

One appealing aspect of our influence function is that we do not have a nonparametric (conditional) density function. The matrix consists only of regression-type objects: we must project derivatives of the loss onto . Again we can use treatment effects for intuition: we know exactly what nonparametric regression object is required, the propensity score, and we must estimate it to form the empirical influence function in observational data or we can compute it in experiments. Our result is at the same level, given estimates , though it may appear more cumbersome in terms of actual coding. We discuss estimation in more detail in Section 4.2 and implementation in Section 5.

Two other parallels with treatment effects are worth noting regarding . First, in many problems, if is randomized, estimation is not required and can be computed directly (Remark 4), just as the propensity score need not be nonparametrically estimated in experiments. Second, as is standard in semiparametrics, ensuring that the “denominator” is bounded away from zero is crucial, which is the impetus behind the prevalent trimming on the propensity score. Although our results allow for estimation using the influence function without knowing its precise form, this is not always desirable in practice, as we may wish to trim based on more primitive objects if possible. In treatment effects, we cannot trim based on the propensity score unless that piece of the influence function is known. Trimming based on the propensity score is cleanly interpretable based on the overlap condition (Crump et al., 2008) and can be studied theoretically (Ma and Wang, 2020), and is therefore more appealing that regularization that is not grounded in economics. In practice, trimming or other regularization of , such as using , may be helpful.

Remark 1.

Our derivation deals directly with the nonparametric objects and we obtain a result familiar from parametric two-step models (Newey and McFadden, 1994). This can be contrasted with a seemingly-similar approach to inference that treats also evokes parametric two-step models. Here, the first stage parameters are those of the nonparametric estimator itself. If were a series estimator, for example, the parameters would be the coefficients on the basis functions. In the case of lasso, the parameters match the high-dimensional variables. One can then treat this as a (large) two-step parametric problem to obtain valid inference, as in Ackerberg et al. (2012). Applying this idea to deep learning is in some ways tempting, because fitting DNNs is maximum likelihood, which is in principle well understood. However, pursuing this approach would lead to impractical results due to the high dimensionality of modern ML methods. For example, the equivalent of in this case would be a square matrix of dimension equal to the number of parameters in the deep net, which can be extremely large. Computing and inverting such a matrix would be challenging or impossible practically and potentially invalid theoretically, and moreover, given our results, it is unnecessary. ∎

Remark 2.

The goal of Theorem 2 is to allow for feasible inference post-ML in a wide variety of empirically useful settings, rather than explicitly targeting efficient inference. However, in many cases our result matches the efficient influence function, such as for average treatment effects or heterogeneity-enriched linear models more generally. Interestingly, although (2.3) is more flexible than the usual partially linear model, which has constant slopes, we recover the usual result of efficiency under homoskedasticity in linear models, but not in nonlinear models. All of these are discussed in Section 6. We conjecture that our result yields efficiency more broadly, when the original model is based on a likelihood or exponential family, by arguing as in Remark 4.1 of Mammen and van de Geer (1997). ∎

Remark 3 (Orthogonal Loss Functions).

We use an orthogonal score for inference only, where the orthogonality is needed to ensure validity after learning the parameter functions in the first stage. An alternative approach recently considered is to exploit orthogonality in the estimation stage as well, or to perform these jointly. Foster and Syrgkanis (2020) used orthogonal scores to study M estimation problems with a nuisance parameter, i.e., in our notation. Tan (2020) used a modified loss function to obtain doubly robust inference on average treatment effects with high-dimensional sparse models, compared to the “consistency” type of robustness obtained by using the influence function based estimators. Nekipelov et al. (2020) considered a model like (2.3), but with high-dimensional sparse linear models, so that where many entries of vector are zero. Under the motivation that the “complexity of the control function is likely to be much larger than [that] of heterogeneous interactions”, they develop a loss function for estimation of the vector that is automatically orthogonal to estimation of other nuisance parameters. Similarly, in the context of heterogeneous effects of a binary treatment, where (2.3), under a linear link and binary scalar , is without loss of generality, Nie and Wager (2020) and Kennedy (2020) (and references therein) develop estimation procedures for which obtain better rates if the function has a simpler structure than . Common to these approaches is that the heterogeneity is in some way “simpler” than the rest of the problem, which is the opposite of our goal of capturing rich individual heterogeneity. ∎

It will be useful to explicitly state how Theorem 2 applies to the regression models (2.3). We will use this form in several examples in Section 6 and in two remarks below.

Corollary 2.

Here we can see exactly that requires projecting weighted first and second moments of . This is intuitive from linear models, where the conditional variance is the crucial object (Sections 6.1, 6.2, 6.3) and from other applications of generalized linear models and QMLE.

The following two remarks use Corollary 2 for two cases where simplifies, which are common enough in applications to be worth spelling out here.

Remark 4 (Randomized Treatments).

If is randomly assigned, or more generally is independent of , then often simplifies or can be directly computed. In many problems of interest, will not be a function of , only and (through ) . Thus under randomization, given , can be computed and need not be estimated, though it remains a function of in general, as opposed to simply a constant. In the case of (4.4), . If the distribution, denoted , is known, this object can be computed numerically for fixed functions (or if , these are not needed). This motivates the three-way sample splitting for nonlinear models discussed below. Note that this continues to apply under cases such as stratified randomization, where the relevant distribution will be known and depend on a very simple subset of the covariates. ∎

Remark 5 (Scalar Parameters with Univariate Treatments).

To state a simple, concrete result, consider the case where is scalar and (2.3) holds with scalar treatment variable, so that . Then we can invert manually. The (scalar) function in this case is more familiar and ease to compare to earlier results. Define , , and . Then Theorem 2 holds with

| (4.5) | ||||

We note here that the treatment may be discrete or continuous, in either case the form of the influence function remains the same. Again this result can be used to compare to other cases and ease implementation. ∎

4.2 Asymptotic Normality

With the orthogonal score of Theorem 2 in hand, we now turn to point estimation and inference for . We will apply the methods and results from Chernozhukov et al. (2018) and as such we keep the discussion brief. The crucial point here is that in order to form the point estimator and standard errors we need only to evaluate the influence function at each data point, and this can be done in the full generality of Theorem 2. This is still possible when, as mentioned above, the required elements are not available in closed form.

We will rely on sample splitting or cross fitting here, in order to obtain the desired theoretical result. From a theoretical point of view, sample splitting allows us to obtain a properly centered limiting distribution under weaker conditions on the first stage (deep neural network) estimates for all applications of our framework. However, from a practical point of view, sample splitting or cross fitting come with a cost that can be large in some applications. One obvious cost is computational: the machine learning must be done multiple times on the different subsamples. A more subtle cost, but crucial when sample sizes are small, is that the smaller (sub-)sample sizes can yield worse results. Sample splitting relies on the asymptotic fact for fixed , a sample of size is as good as the full sample of size . In practice, this may not hold, particularly for challenging nonparametric estimation problems. Farrell et al. (2021) show that for some estimands sample splitting is not needed for inference after deep learning under standard assumptions. It would be useful to extend that argument to more general settings.

For estimation of we may in fact require three-way splitting. Because the “outcome” required for these projections depends on the unknown , we will estimate on one subsample, use these to obtain on a second sample, and then use the final portion for the parametric estimation and inference. In typical cross fitting the first and second portions would be one sample. In two cases this three-way splitting is not needed. The first is under randomization when can be computed, given . Second, under (2.3) when is linear, and is simply the covariance matrix of , conditional on , and this can be estimated along with .

We will be brief in describing the estimation procedure, leaving further discussion to Chernozhukov et al. (2018) and Newey and Robins (2018). First, the observations are split into subsets, denoted by , . Let be the complement of . We then, for each , use to obtain estimates of and ; denote these by and . If needed, is further split in two pieces, using the first to get and the second for . The final estimator of is then

| (4.6) |

where is the cardinality of and is assumed to be proportional to the sample size . Along with the point estimator we will require an estimator of the asymptotic variance, which is given by . To estimate we use the variance analogue of (4.6):

| (4.7) |

Asymptotic normality of and consistency of will follow from Chernozhukov et al. (2018). To emphasize that our inference results, the orthogonal score in particular, are useful in semiparametrics broadly, including after ML estimation of any kind, we employ the following high-level conditions on the convergence rates of and .

Assumption 5.

Based on a sample of size , the estimators for and obey and for all .

Many nonparametric and ML estimators may satisfy this requirement. Importantly, Theorem 1 verifies these conditions for deep learning estimation of . Estimation of the elements of is a prediction problem, and therefore deep learning will also satisfy these rates, applying the results of Farrell et al. (2021) with the sample splitting discussed above. Often the squared error loss will be used here, but not always, particularly for discrete data or with nonlinear models, where a fractional outcome model or classification-based loss may be warranted.

We now have the follow result, establishing asymptotic normality and validity of standard errors. Let be the -long zero vector and be the -square identity matrix.

5 Application: Advertising and Personalized Interest Rates

5.1 Empirical Context

In this section we use our framework to replicate and extend the analysis presented in Bertrand et al. (2010). The data is from a large scale field experiment run on behalf of a financial institution in South Africa. Consumers were sent marketing material for short terms loans where a number of features of the advertising content and the interest rate offered were all randomized (full details are left to that paper). The vector of treatments is thus , where denotes the advertising content and the interest rate offered. The key outcome variable () is the indicator for whether or not the consumer applied for the loan. We will use a binary choice model, one of the workhorse models in applied economics. Other variables following the application were also tracked such as a default indicator () and the loan amount (). The data also contains a rich set of demographics () which we use to calibrate our measures of heterogeneity.

We conduct two analyses using their data. First, we replicate their analysis and extend it to allow for heterogeneity captured by our structured DNNs. We use our specification to compute the average marginal effect of each treatment and compare those to the results presented by the authors. Second, we use the results of the model (with some additional assumptions) to construct optimal personalized interest rate offers and compute the expected profits from implementing the personalization scheme, and we then conduct inference using our novel methodology.

5.2 Model and Implementation

Our setup adapts the framework outlined in Bertrand et al. (2010) and assumes that consumers have a utility

where the vector of parameter functions is partitioned to match . We assume that the are distributed i.i.d. Logistic which gives the standard Logit probabilities of response:

Using these probabilities we can construct the log-likelihood as

| (5.1) |

which has been enriched from the standard version. The negative of this will serve as the loss (2.1) for our problem. One can easily verify the high-level assumptions in this setting, particularly given that the binary choice model is widely studied and well understood. For example, it is straightforward to find that , which will be invertible under standard and commonly used economic assumptions.

We will obtain parameter function estimates by solving (3.1) using this and the architecture Figure 1. In our implementation we approximate the via a simple deep neural networks with two hidden layers with 80 and 40 nodes, respectively. Part of the simplicity of the network architecture stems from the fact that we have a smallish dataset and rather large dimension of the treatment vector . We use Tensorflow™ (Abadi et al., 2015) to construct the computational graph and optimize the likelihood using the ADAM optimizer (Kingma and Ba, 2014). For inference purposes with used three-fold cross fitting, using two thirds of the data to obtain and one third to obtain .444Complete details of the implementation are available upon request. We plan on releasing the code for the application soon.

5.3 Results and Quantities of Interest

The parameter functions are the key inputs into the target of inferential interest, . We will use our estimated and novel influence function to explore two derived quantities. First, we examine the marginal effect of the treatments and compare them to those presented in column (1) Table III of Bertrand et al. (2010) (on pages 291-294). We note that our specifications are slightly different since they use a Probit specification while we use the Logit. Second, we turn to a more ambitious goal of targeting and profit maximization, making more full use of the power of the framework.

Binary choice models are widely used in applications, often with price as (at least one of) the treatment variable(s). Our framework would immediately give inference for many standard, policy-relevant parameters in this context. Examples, beyond those shown below, include (i) the price elasticity at a price (here, interest rate) , which sets ; (ii) a measure of willingness to pay obtained by taking , where is the intercept; and (iii) expected consumer welfare, . Importantly, without our explicit use of an enriched structural model, it would not be easy to characterize these parameters and obtain inference.

5.3.1 Marginal Effects

For our specification, the average marginal effects for any given treatment can be written in closed form. Recall that is partitioned to match . Then, for example, the average marginal effect of a change in interest rates is

In our empirical results we set to the sample average for simplicity. Similarly quantities for the advertising content are readily available. Thus, by taking in (2.2), we can apply our framework, obtaining inference post-DNN easily.

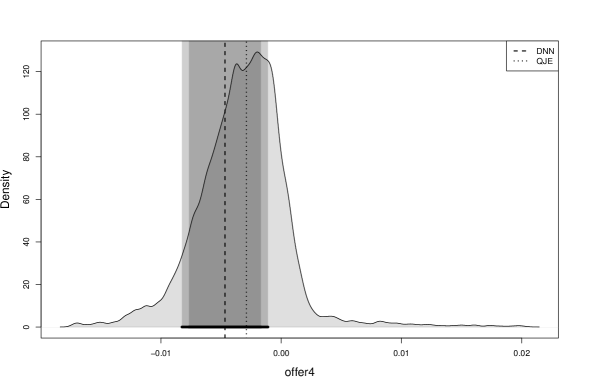

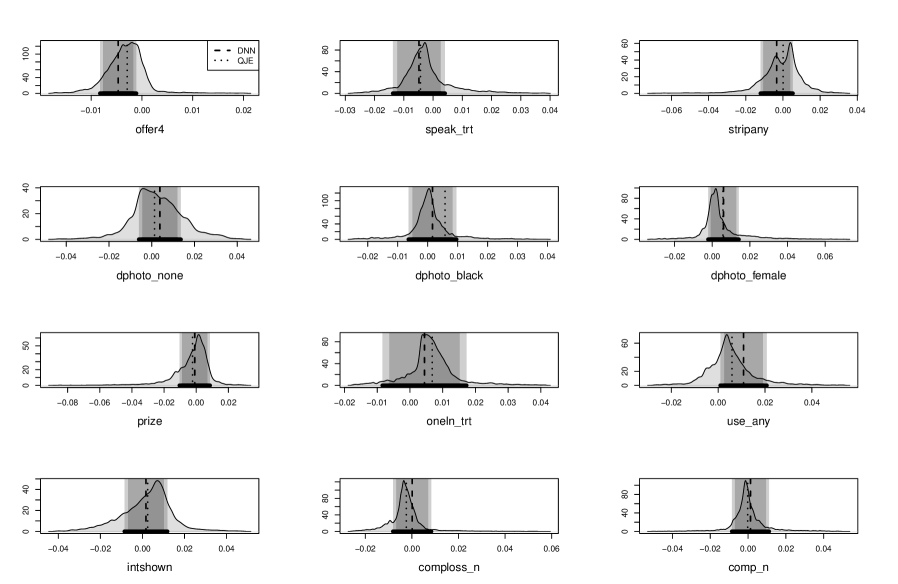

We present the results of our analysis in Table 1. For convenience we have also included the corresponding estimates of Bertrand et al. (2010) under the column heading QJE. As is evident, the deep net estimates match up with the results of the original paper quite well with the confidence interval containing the original estimates, which we can interpret as the original, overall, findings being robust to heterogeneity. In addition, we also uncover substantial heterogeneity in the estimates as demonstrated by the coefficient of variation of . A more useful depiction of these results are contained in Figures 3 and 4 which showcase the rich heterogeneity in the estimated effects. In each we present 90% and 95% confidence intervals for the average marginal effect, with vertical lines to indicate the estimate from our analysis as well as those from Bertrand et al. (2010). We see that although the average matches up roughly with the rigid parametric model, substantial heterogeneity exists, which will be important for targeting.

| Variable | DNN- | 95%CI(L) | 95%CI(U) | QJE | Coef. of Var. | |

|---|---|---|---|---|---|---|

| Interest Rate Offer | -0.0047 | -0.0083 | -0.0011 | -0.0029 | 0.1337 | 1.0211 |

| We speak your language | -0.0048 | -0.0137 | 0.0041 | -0.0043 | 0.2533 | 2.0542 |

| Special rate for you | -0.0034 | -0.0120 | 0.0053 | 0.0001 | 0.5001 | 4.4506 |

| No photo | 0.0038 | -0.0060 | 0.0136 | 0.0013 | 0.5723 | 3.4931 |

| Black photo | 0.0016 | -0.0064 | 0.0096 | 0.0058 | 0.5402 | 5.1348 |

| Female photo | 0.0060 | -0.0021 | 0.0141 | 0.0057 | 0.6820 | 2.3375 |

| Cell phone raffle | -0.0009 | -0.0104 | 0.0085 | -0.0023 | 0.4812 | 17.0059 |

| Example loan shown | 0.0044 | -0.0084 | 0.0173 | 0.0068 | 0.8631 | 1.9379 |

| No loan use mentioned | 0.0108 | 0.0009 | 0.0207 | 0.0059 | 0.7499 | 1.0936 |

| Interest rate shown | 0.0017 | -0.0085 | 0.0119 | 0.0025 | 0.6289 | 7.9903 |

| Loss comparison | 0.0001 | -0.0081 | 0.0083 | -0.0024 | 0.2342 | 89.3606 |

| Competitor rate shown | 0.0013 | -0.0085 | 0.0111 | -0.0002 | 0.4107 | 9.6790 |

5.3.2 Optimal Personalized Offers

Our framework allows for a rich specification of heterogeneity in the tastes of the consumer. We have shown how standard quantities of interest such as marginal effects can be easily constructed. We now demonstrate how the estimated heterogeneity can be translated into personalized offers and the simplicity with which one can conduct inference on quantities of interest (such as the mean interest rate offered or expected profits).

Given the rarity of defaults, the sample size is too small to uncover full heterogeneity, and therefore we assume that the probably of default given an interest rate is modeled by the function

We take these parameters as given. To write the firm’s expected profit for a given consumer, let be the loan amount and, since we focus on optimizing the interest rate given the parameters, abbreviate and . Then

| (5.2) |

The usual optimization machinery applies and we obtain

where and represent derivatives with respect to their scalar arguments, as before. Given the structural model, this simplifies to . The optimal interest rate offer, denoted , is therefore

| (5.3) |

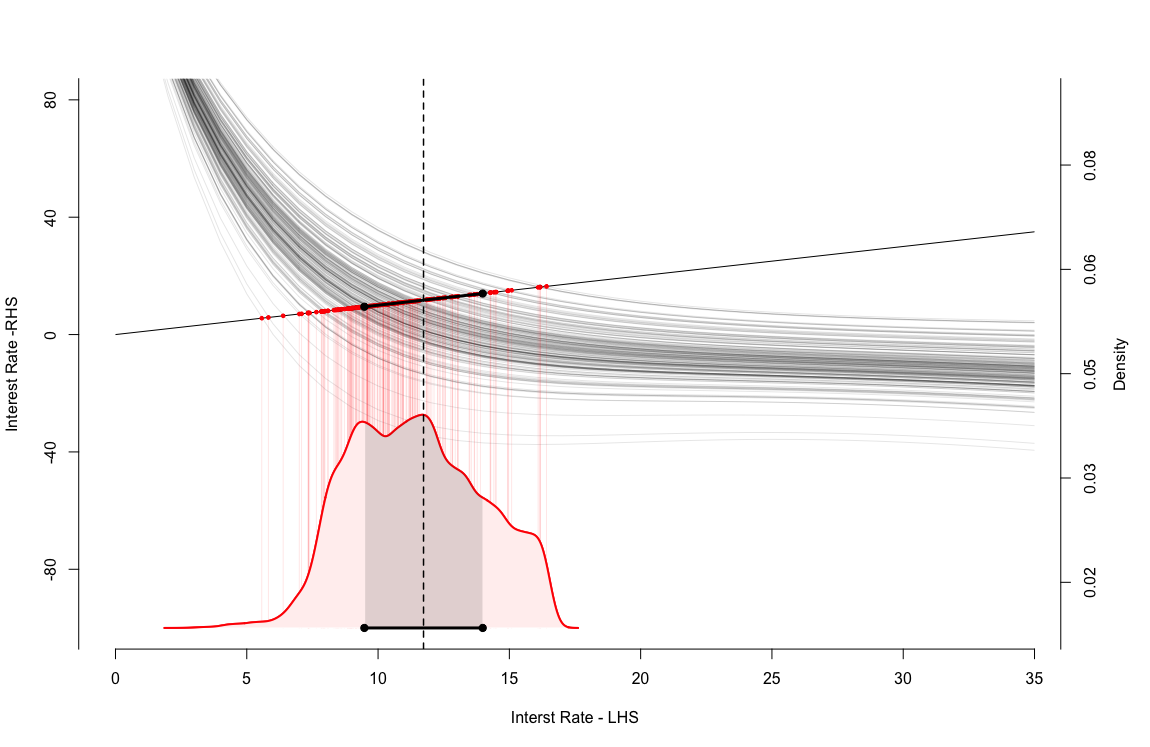

This is an implicit function but there will a unique fixed point since the numerator of the right hand side is decreasing in while denominator is increasing, for and . Figure 5 presents a visual representation of Equation (5.3). Each curve corresponds to a distinct consumer profile and the intersection with the line represents the fixed point The density then represents the kernel density of the optimal personalized offers across consumers. We note that while the fixed points are only shown for a subset of customers (to avoid clutter) the density is computed across the entire sample.

Even though is not available in closed form it remains a smooth function of the parameters , which is all that is required for our method to apply. We can therefore give inference for any statistic of the form (2.2). As a simple example, Figure 5 shows estimation and inference for , i.e. where the function is the same as the function . The vertical dashed line is the point estimate, found to be 11.37%, while a 95% confidence interval is shown as the grey region and black segment, founded to be .

Obtaining confidence intervals for more involved quantities is just as straightforward with our framework. We illustrate by computing the expected profits from setting the optimal personalized interest rate. From (5.2), this is expressed as

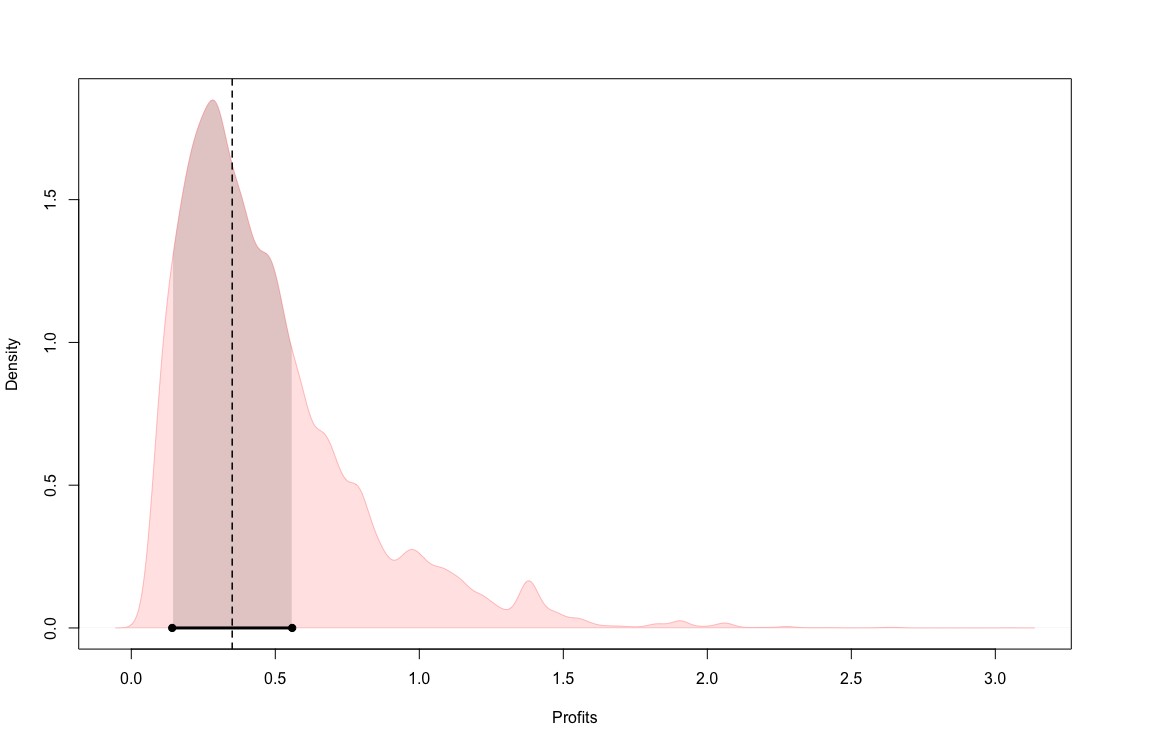

Then, given the optimal interest rates , and appealing to the envelope theorem we can obtain the influence function for this quantity ignoring the impact that perturbations in have on since . As such, the influence function for expected profits can be constructed in closed form (conditional on . Alternatively, one could use standard numerical differentiation or automatic differentiation engines to accomplish the same objective. In our analysis the numerical and exact derivatives give close to identical results. In our analysis we focus on the high risk segment (which is over 75% of the customers) and normalize the loan amount to . Since the interest rate is measured in percentage points, we interpret the expected profit construct as the net average expected income from offering a $100 loan at a personalized interest rate to each potential customer. We find that with a 95% confidence interval of . Figure 6 depicts the density of profits for each customer along with the estimate and confidence interval of expected profits. The personalized interest rate scheme delivers an incremental 5.7% in expected profits over the optimal (uniform) interest rate derived from the experiment alone. While a more serious application would incorporate a number of additional features into the model and analysis, we feel that our example above suffices as a proof of concept of the value of our approach for applied work.

5.4 Summary

This application showcases the simplicity with which parametric models can be extended to incorporate nonparametric heterogeneity via deep neural networks. The structure of the model is maintained which in turn preserves the interpretability of the parameter functions. Since inference in our framework is close to automatic (automatic for data from randomized experiments) it offers the applied researcher a sophisticated yet practical framework for analysis.

6 Examples

Here we discuss several examples that fall within our framework, both to demonstrate the applicability of our results to new and interesting examples as well as to compare to existing results. We emphasize that these examples, and more, are covered without additional derivations: knowing the forms below is useful but not necessary before applying our methodology. This discussion is not exhaustive. We begin with two familiar examples, average treatment effects and partially linear models, before moving on to other cases.

6.1 Average Effect of a Binary Treatment

Average treatment effects are a canonical semiparametric problem and the standard case in the recent literature on inference after machine learning (see references in Section 4.1). Here we have a scalar outcome and is the scalar binary treatment indicator. The model is (2.3) with , so that . Letting be the potential outcome under treatment , we find that and , so that represents the (heterogeneous) conditional average treatment effect, assuming unconfoundedness. Additional mean parameters could be added to cover average treatment effects for specific treatment groups as well as multi-valued treatments. See Cattaneo (2010) and Cattaneo and Farrell (2011) for inference using classical nonparametrics (series) and Farrell (2015) for machine learning (group lasso) results.

The naive approach to estimation would either involve unstructured modeling of or separate estimation (in the treatment and comparison groups) of and . Along with the propensity score, these would be inputs into the well-known doubly robust or influence function estimator (Robins et al., 1994; Hahn, 1998). The structured architectures of Figures 1 and 2 intuitively reflect the idea that and may share similar features, since they relate to the conditional means of the two potential outcomes, under treatment and control. This same notion has been used in the past for trees by Zeileis et al. (2008) and Athey and Imbens (2016), where the treatment and control groups share a partition, and by Farrell et al. (2021) for DNNs, most similar to the present case. Notice that this is different from assuming that the regression functions share similar features to the propensity score, or its inverse, which in general there is no reason to expect to hold, particular in high-dimensional or data-adaptive scenarios. For classical, low-dimensional series estimators, this has been exploited to prove that both regression imputation (Imbens et al., 2007; Cattaneo and Farrell, 2011) and inverse weighting (Hirano et al., 2003) are semiparametrically efficient.

Equation (2.2) gives the familiar average treatment effect by taking . In this case, the model (2.1) is without loss of generality beyond unconfoundedness, and hence setting to be squared loss, we recover the familiar efficient influence function. To see this, begin with the univariate form in (4.5), and use the fact that , , , and , the propensity score. Then, adding and subtracting and using the fact that , we have

In this example, the standard overlap assumption, that the propensity score is bounded away from zero and one, ensures that is well behaved: the determinant of , the initial denominator above.