appendixReferences (Appendix)

Consumer Theory with Non-Parametric

Taste Uncertainty and Individual Heterogeneity††thanks: The second author gratefully acknowledges financial support from the ACPR Chair (Regulation and Systemic Risks), and the ERC DYSMOIA. We thank Martin Burda, JoonHwan Cho, Rahul Deb, Jiaying Gu, Joann Jasiak, Kyoo il Kim, Yao Luo, Etienne Masson-Makdissi, Ismael Mourifié, Jesse Shapiro, Eduardo Souza-Rodrigues, and participants at the International Conference on Computational and Financial Econometrics (2020) and a seminar at the University of Toronto for useful comments. This research was enabled by support from Sci-Net (www.scinethpc.ca) and Compute Canada (www.computecanada.ca). Researcher(s) own analyses calculated (or derived) based in part on data from The Nielsen Company (US), LLC and marketing databases provided through the Nielsen Datasets at the Kilts Center for Marketing Data Center at The University of Chicago Booth School of Business. The conclusions drawn from the Nielsen data are those of the researcher(s) and do not reflect the views of Nielsen. Nielsen is not responsible for, had no role in, and was not involved in analyzing and preparing the results reported herein. The ACPR is not responsible for any of our results. The conclusions in this paper do not reflect the views of the ACPR.

Abstract

We introduce two models of non-parametric random utility for demand systems: the stochastic absolute risk aversion (SARA) model, and the stochastic safety-first (SSF) model. In each model, individual-level heterogeneity is characterized by a distribution of taste parameters, and heterogeneity across consumers is introduced using a distribution over the distributions in . Demand is non-separable and heterogeneity is infinite-dimensional. Both models admit corner solutions. We consider two frameworks for estimation: a Bayesian framework in which is known, and a hyperparametric (or empirical Bayesian) framework in which is a member of a known parametric family. Our methods are illustrated by an application to a large U.S. panel of scanner data on alcohol consumption.

Consumer Theory with Non-Parametric

Taste Uncertainty and Individual Heterogeneity

Keywords: Consumer Theory, Scanner Data, Stochastic Demand, Taste Heteroge- neity, Non-Parametric Model, Bayesian Approach.

1 Introduction

The recent availability of databases containing all dated purchases made by a large nu- mber of consumers (28,036 in our application) presents a modern challenge for the eco- nometrics of demand systems, requiring new models and estimation approaches (see, for example, Burda et al., 2008, 2012, for discrete choice, and Guha and Ng, 2019, Chernozhukov et al., 2020, and Dobronyi and Gouriéroux, 2020, for the first analyses of such data in the demand literature). This type of data is commonly called scanner data because its collection involves retailers or households scanning each purchased good on the date of purchase. This paper introduces two models of random utility for scanner data: the stochastic absolute risk aversion (SARA) model, and the stochastic safety-first (SSF) model. These models have the following advantages in comparison with the existing literature:

-

(i)

Both models are consistent with consumer theory: Every consumer maximizes a strictly increasing and strictly quasi-concave utility function. The latter prop- erty is not accommodated by existing approximations of the utility function like the quadratic approximation of the utility function (Theil and Neudecker, 1958; Barten, 1968), the translog utility model (Johansen, 1969; Christensen et al., 1975), or the Almost Ideal Demand System (Deaton and Muellbauer, 1980) and its extensions (Banks et al., 1997; Moschini, 1998).

-

(ii)

Both models are non-parametric. In each model, the utility function is indexed by a functional parameter characterizing the individual heterogeneity, allowing for infinite-dimensional heterogeneity. In this respect, our paper differs from the existing literature when finite-dimensional heterogeneity is considered (see Beckert and Blundell, 2008, Blomquist et al., 2015, \hyper@linkcitecite.blundell\@extra@b@citebBlundell, Horowitz, and Parey, \hyper@linkcitecite.blundell\@extra@b@citeb2017, and \hyper@linkcitecite.blundell-wp\@extra@b@citebBlundell, Kristensen, and Matzkin, \hyper@linkcitecite.blundell-wp\@extra@b@citeb2017, for some examples of finite-dimensional restrictions). Our approach is in line with Dette et al. (2016) who write, “in general the multivariate demand function is a non-monotonic function of an infinite-dimensional unobservable—the individual’s preference ordering.”

-

(iii)

Both models yield demand functions with non-separable heterogeneity (see the discussions in Brown and Walker, 1989, Beckert and Blundell, 2008, and Dette et al., 2016). They are also endowed with precise structural interpretations, as heterogeneity is introduced by means of a distribution of taste parameters, so that we can imagine consumers facing taste uncertainty, which they eliminate using expected utility.

-

(iv)

Both models are identified under weak restrictions. Identification follows from the use of panel data. Without such data, we lose identification (Hausman and Newey, 2016). Of course, the structure of scanner data is extremely important.

Each model is characterized by a basis of functions. This basis is used to generate a family of utility functions. A distribution is, then, placed over this family. To be precise, we start with a basis of increasing and concave functions. Let denote an element of this basis, where is a bundle and is a finite-dimensional vector of taste parameters. A family of utility functions is generated by taking the convex hull of the basis. Let denote an element of this family, where is a distribution on . This family is indexed by a functional parameter , which can be structurally interpreted as taste uncertainty (resolved after the consumer makes her decisions). The heterogeneity across consumers is introduced using a distribution on the set of probability distributions on . Therefore, each model combines uncertainty and heterogeneity: the uncertainty in taste for a given consumer is represented by , and the heterogeneity across consumers is captured by .

The paper considers a two-good framework with continuous support for . It is organized as follows: Section 2 introduces the stochastic absolute risk aversion (SARA) model and Section 3 introduces the stochastic safety-first (SSF) model. For each mo- del, we derive conditions on under which there exists a unique demand system, for each . In Section 4, the distribution of heterogeneity is introduced. When is known, we obtain a Bayesian framework in which the functional parameter has to be estimated. When is a member of a known parametric family, indexed by , we obtain an empirical Bayesian framework with a hyperparameter that has to be estimated, and a stochastic functional parameter that has to be filtered. In Section 5, we consider the identification of the taste distribution within each model. Next, we examine if it is possible to distinguish between stochastic risk aversion and stochastic safety-first. In Section 6, we use the Nielsen Homescan Consumer Panel to illustrate our methodology in an application to the consumption of alcohol. Section 7 concludes. The details of the Dirichlet process are in Appendix A; integrability is discussed in Appendix B; an optimization procedure for filtering the taste distributions after estimating is in Appendix C; details of the data are placed in Appendix D.

2 A Model with Stochastic Risk Aversion

This section introduces the first utility specification that we consider. It first describes the set of utility functions, then derives conditions under which there exists a unique demand system. The taste uncertainty is introduced using risk aversion parameters.

2.1 The Set of Utility Functions

There are two goods, denoted and . Let denote the non-negative orthant with interior . A consumer has preferences over the bundles in . Her preferences are summarized by a utility function of the form:

| (2.1) |

for every such that , where is a positive stochastic parameter characterizing the consumer’s degrees of absolute risk aversion with respect to goods 1 and 2, and is a joint distribution for this pair of stochastic taste parameters. Her preferences are, as a result, contained in a broad family of utility functions, indexed by a functional parameter . There are two interpretations of specification (2.1): (i) the preferences are summarized by a deterministic utility function in the convex hull gen- erated by a parametric family, or (ii) the consumer faces “taste uncertainty” and she resolves this uncertainty by using expected utility. We call these preferences stochastic absolute risk aversion (SARA) preferences.111These preferences differ from those used to describe consumer behaviour when facing ambiguity or uncertainty, as in, say, Halevy and Feltkamp (2005).

If is a point mass at such that , the stochastic parameters are constant, and reduces to . This function is strictly increasing because we have:222Here, means each component is strictly larger than .

| (2.2) |

at each such that , and concave (although not necessarily strictly concave) because the Hessian associated with the utility function:

| (2.3) |

is negative semi-definite, at each such that . This matrix is related to a bivariate measure of absolute risk aversion333Such a measure can be defined as: where is the diagonal matrix whose diagonal elements are the first derivatives of . (Richard, 1975; Karni, 1979, 1983; Grant, 1995). These properties translate into properties of the more general function: .

Proposition 1.

If preferences are SARA and the consumer’s taste distribution is not the mixture of point masses where is proportional to , then the utility function is strictly increasing with a negative definite Hessian everywhere on .

Proof.

The utility function is strictly increasing on because:

| (2.4) |

at every such that . Its Hessian is negative definite on because the sum of two 2-by-2 matrices of rank 1, whose columns are not proportional, has full rank. ∎

Proposition 1 implies that we have effectively constructed a family of well-behaved utility functions indexed by a functional parameter , describing the taste uncertainty, instead of the standard finite-dimensional parameter usually con- sidered in the literature.

Let denote the function defined by the implicit equation:

| (2.5) |

for every , and each (attainable) level of utility . This implicit equation has a unique solution because is strictly increasing on . The function is the indifference curve associated with the functional parameter and a utility level of — maps every value of to a value of for which attains a utility level of given . The implicit function theorem implies that is twice-continuo- usly-differentiable with respect to and:

| (2.6) |

on where denotes the marginal rate of substitution at —the rate at which the consumer is willing to exchange good 1 for good 2 given and . The indifference curve is strictly convex such that:

| (2.7) |

at every , since the Hessian of is negative definite everywhere on (see Lemma 1 in Dobronyi and Gouriéroux, 2020). This property is stronger than the sta- ndard assumption of strict quasi-concavity, which allows this derivative to be zero on a nowhere dense set (Katzner, 1968). This distinction is important for what follows.

Note that, after integrating out the taste uncertainty, the absolute risk aversions will depend on the consumption level. For instance, when and are independent with distributions and , the risk aversion for good 1 becomes:

| (2.8) |

where denotes , the portion of the utility function corresponding to good 1. Clearly, depends on . Indeed, it is the average of given the following modified density:

| (2.9) |

with respect to .

2.2 The Demand Function

Let denote a pair in which denotes expenditure and denotes the price of good 1, both normalized by the price of good 2. The consumer can purchase a bundle if, and only if, . She chooses a bundle that solves:

| (2.10) |

Let denote the solution to:

| (2.11) |

While (2.10) is restricted to bundles in the non-negative orthant, (2.11) allows for neg- ative values. The solution to (2.11) is characterized by the following system of first- order conditions:

| (2.12) |

The first equality says that the marginal rate of substitution equals the relative price . The second equality says that the budget constraint holds with equality. Equivalently, we can solve the equality:

| (2.13) |

for the first component , and then use the budget constraint in (2.12) to solve for . As long as is not almost surely equal to zero, the first-order partial derivative of the left side of this equality with respect to is strictly negative:

| (2.14) |

The function on the left side of (2.13) is, therefore, strictly decreasing in , implying that there exists a unique solution to (2.13), and a unique solution to (2.11). If is in , then coincides with the solution to (2.10). Else, the solution to (2.10) is on the boundary of . Let denote the solution to (2.10) given both and . There are three regimes of demand in the design space:

| (2.15) |

Because the utility function has strictly convex indifference curves everywhere on , the demand function is invertible in the second regime (see Proposition 2 in Dobronyi and Gouriéroux, 2020).

Proposition 2.

If preferences are SARA and the consumer’s taste distribution is not the mixture of point masses where is proportional to , then there exists a unique solution to the maximization problem in (2.10) given and , for every , almost surely, for every . There are three regimes of demand defined by (2.15). The resulting demand function is invertible in the second regime.

As a final remark, let us consider a risk-neutral consumer. In particular, let us ass- ume that and tend stochastically to zero, with means that tend to zero so that converges to a non-degenerate . By considering the Taylor expansion of utility, it can be shown that these preferences are represented by:

| (2.16) |

This representation is unique up to an increasing transformation. For this risk-neutral consumer, goods are considered to be perfect substitutes. It is known that such a consumer will consume only good 1 whenever , and only good 2 whenever .

2.3 Gamma Taste Uncertainty

As an illustration, let us assume that and are independent and that has a Gamma distribution with degree of freedom and scale factor , for . Under this specification, , where denotes the tensor product of distributions. By the Laplace transform of the Gamma distribution:

| (2.17) |

Under this specification, the absolute risk aversion for good 1 in (2.8) becomes:

| (2.18) |

which is hyperbolic in . The indifference curve associated with utility level is:

| (2.19) |

for every and such that:

| (2.20) |

It is easily shown that the second derivative of the indifference curve equals:

| (2.21) |

for some . This inequality confirms that the indifference curve is strictly convex. Furthermore, the MRS is equal to:

| (2.22) |

The unconstrained solution to the first-order condition in (2.12) is equal to:

| (2.23) |

The second component is deduced from the budget constraint in (2.12). By equation (2.15), the demand function coincides with over the set of pairs such that:

| (2.24) |

The three regimes of demand are illustrated in Figure 1 in the design space. The strict convexity of the indifference curve on implies that the demand function associated with this utility function is invertible on .

3 A Model with Stochastic Safety-First

We now consider a model with taste parameters that have a safety-first interpretation.

3.1 The Set of Utility Functions

In Section 2, we constructed a family of well-behaved utility functions by taking the convex hull generated by a particular basis. In this section, we consider another basis, consisting of functions with the form:

| (3.1) |

for every , where and . This function corresponds to the “safety-first” criterion, introduced into the literature on portfolio management by Roy (1952). In order to illustrate, let us consider the consumption of alcohol, as in Dobronyi and Gouriéroux (2020). Suppose that there are two groups of goods: group 1 consisting of drinks with low alcohol by volume such as beers and ciders, and group 2 consisting of drinks with high alcohol by volume such as wines and liquors. Assume that the quantities are measured in identical units such as volume of alcohol—that is, the total volume of the drink in litres multiplied by the alcohol by volume of the drink.444Quantities could be, alternatively, measured in calories. We can, then, add these volumes to aggregate two drinks with different sizes and/or percentages of alcohol. Here, is the consumer’s relative preference between the two groups of drinks, and is a “control” parameter, specifying her attempt to limit her intake of alcohol.

Now, let us introduce a distribution such that , , and define:

| (3.2) |

By the law of iterated expectations, we obtain:

| (3.3) |

We call these preferences stochastic safety-first (SSF) preferences.

Under mild regularity conditions:

| (3.4) | ||||

| (3.5) | ||||

| (3.6) | ||||

| (3.7) |

for every such that . These partial derivatives are strictly positive when has full support: , for . By taking the second-order derivatives:

| (3.8) |

for every such that , where in which denotes the conditional density of given , assuming that such a density exists. This matrix is both symmetric and negative definite when is continuous and is not constant. This result follows from the positivity of and the following equality:

| (3.9) |

which holds for every such that , in which denotes the modified density:

| (3.10) |

Proposition 3.

If preferences are SSF and the consumer’s taste distribution is con- tinuous with full support given , then the utility function is strictly increasing with a negative definite Hessian everywhere on .

Consequently, we have constructed another family of well-behaved utility functions indexed by a functional parameter , describing taste uncertainty.

3.2 The Demand Function

Let us revisit the utility maximization problem in (2.10). Under the safety-first spec- ification, the analogue of the unconstrained first-order condition in (2.13) is given by:

| (3.11) |

We obtain this equality by equating the marginal rate of substitution with the relative price , and then using the budget constraint to replace with . Under the regularity conditions from above, the left-hand side is strictly monotone in given , so that there exists a unique solution to the first-order condition. As in Section 2, we let denote this solution, and let denote the quantity .

Proposition 4.

If preferences are SSF and the consumer’s taste distribution is con- tinuous with full support given , then there exists a unique solution to the maximization problem in (2.10) given and , for every , almost surely, for every . There are three regimes of demand defined by (2.15). The resulting demand function is invertible in the second regime.

When the consumer’s preferences are SSF, the MRS has the form:

| (3.12) |

Thus, the rate at which the consumer is willing to exchange good 1 for good 2 given and is equal to the inverse of the expectation of her relative preference between goods , conditional on not surpassing her control parameter .

Some functionals of the distribution can be especially interesting. For instance, in an application to the consumption of alcohol, we might expect the conditional distribution of given to be concentrated around a single mode, characterizing an implicit alcohol limit for this consumer. Then, we can ask the following questions:

-

(i)

Is this limit positively correlated with ? In other words, is there a positive relationship between this limit and a preference for strong alcoholic beverages?

-

(ii)

Does a change in the maximum blood alcohol level for driving affect this limit?

These are questions that cannot be answered using classical demand systems like the Almost Ideal Demand System (Deaton and Muellbauer, 1980). In fact, tests based on the Almost Ideal Demand System have rejected rationality in applications to alcohol consumption (Alley et al., 1992). Clearly, it is possible that the Almost Ideal Demand System is misspecified.

3.3 Exponential Threshold Taste Uncertainty

In general, the first-order condition in (3.11) has no closed-form solution. However, its expression can be simplified for some taste distributions . As an illustration, let us assume that:

-

(i)

and are independent.

-

(ii)

follows an exponential distribution with survival function:

(3.13) -

(iii)

follows a distribution with Laplace transform: , .

Under this specification, we can first integrate with respect to within the expecta- tion in (3.11) in order to obtain the following condition:

| (3.14) |

Equivalently, we obtain:

| (3.15) |

This equation can be written in terms of the Laplace transform for . This yields:

| (3.16) |

which can also be written as:

| (3.17) |

Finally, by inverting this expression and rearranging the terms, we get:

| (3.18) |

The second component of the unconstrained solution in (3.11) is deduced from the budget constraint. It follows from equation (2.15) that the demand function coincides with if, and only if:

| (3.19) |

For instance, if follows a gamma distribution , then , and we obtain:

| (3.20) |

for . Moreover, by inverting this function, we get:

| (3.21) |

Therefore, the solution has the form:

| (3.22) |

and demand coincides with if, and only if:

| (3.23) |

The regimes of demand are illustrated in Figure 2 in the design space. Note, we can also verify that the Slutsky coefficient is strictly negative555This property holds for any Laplace transform of (see Appendix B). such that:

| (3.24) |

ensuring that the demand function is invertible over the set of pairs on which demand is strictly positive (see Section 2 in Dobronyi and Gouriéroux, 2020).

4 Individual Heterogeneity

Sections 2 and 3 introduced two utility specifications, both indexed by the functional parameter . Of course, different consumers can have different functional parameters. This individual heterogeneity is introduced in a second layer, by specifying a distribution over the set of distributions on , such as the Dirichlet process (see, for example, Navarro et al., 2006, for an application of the Dirichlet process in modelling individual differences). More precisely, we make the following theoretical assumption:

Assumption A1 (Latent Stochastic Model).

-

(i)

There are consumers.

-

(ii)

Consumers are segmented into homogeneous groups.

-

(iii)

Consumers in group have the utility function , for all .

-

(iv)

The taste parameters are independently drawn from a Dirichlet process .

Assumption A1 introduces a distribution over the functional taste parameter . This distribution characterizes the heterogeneity across homogeneous groups. It can encompass, for example, regional or demographic differences in preferences. This infinite-dimensional heterogeneity is non-separable in the stochastic demand equation.

The Dirichlet process can be constructed in three steps:

-

Step 1:

Consider the set of (Bernoulli) distributions on . This set is characterized by such that . A distribution defined on this set of distributions is a distribution defined on this parameter set. We can, for instance, introduce a beta distribution, denoted . The distribution has a continuous density:

(4.1) with respect to the Lebesgue measure over the simplex , where denotes the gamma function,666The gamma function is defined by , for each . and are positive scalar parameters.

-

Step 2:

The beta distribution can be extended to define a distribution on the set of discrete distributions with weights , , such that . This procedure leads to the Dirichlet distribution, denoted . The res- ulting distribution has continuous density:

(4.2) with respect to the Lebesgue measure over the simplex:

(4.3) (see, for example, Kotz et al., 2000, page 485, and Lin, 2016, for details).

-

Step 3:

Then, the Dirichlet distribution can be extended to define a distribution on a large set of distributions777The realizations of a Dirichlet process are, almost surely, discrete distributions. Although we assumed continuity to prove the existence of a unique demand system in Section 3, these realizations can approximate any continuous distribution. This discrepancy has no practical implications. defined on (see Appendix A). This procedure leads to the Dirichlet process. The Dirichlet process is characterized by a distribution on and a scaling parameter . The distribution can be thought of as the mean of the Dirichlet process, while the parameter manages its degree of discretization (see Appendix A). This extension of the Dirichlet distribution is much more complicated than the Dirichlet distribution, especially because the notion of the Lebesgue measure on the set of distributions, and the notion of a density, no longer exist (see Ferguson, 1974, Rolin, 1992, and Sethuraman, 1994).

Let us now discuss implications of Assumption A1: If the functional and scaling parameters of the Dirichlet process are known, then we are in a Bayesian framework (see, for example, Geweke, 2012, for a Bayesian analysis of revealed preference) in which the taste distribution has to be estimated. Otherwise, we can assume that the mean of our process is characterized by a finite-dimensional hyperparameter . Naturally, the hyperparametric model has two types of parameters: the hyperparameter to be estimated, and the functional parameters to be filtered.

5 Non-Parametric Identification

In this section, we consider the identification of the functional parameter within each model from the observation of a demand function. Then, we examine if we can distin- guish between the SARA and SSF models.

Intuitively, a consumer’s demand function is identified if we observe her making a lot of consumption decisions at a variety of designs . Clearly, we can identify her demand function if (i) her preferences are constant over time and we observe a large panel or experiment,888In this case, when the number of dates is large, we can have a segment for each consumer . or (ii) she belongs to a large homogeneous segment of consum- ers with identical preferences. This explains the form of Assumption A1 (as it allows for either interpretation). Later, we apply the segmented approach to scanner data in the application to the consumption of alcohol in Section 6.

With panel data, one no longer requires the assumption that demand is monotonic with respect to unobserved heterogeneity in order to achieve identification (see Figure 3, and the role of this assumption in Brown and Matzkin, 1995, Matzkin, 2003, and Hausman and Newey, 2016).

5.1 Within Model Identification

In the models introduced in Sections 2 and 3, and for any such that demand is inv- ertible, we can derive the inverse demand function, whose second component coincides with the MRS which can be integrated to obtain a unique preference ordering. Indeed, by construction, the integrability conditions (needed to recover a unique well-behaved preference ordering) are satisfied, implying that preferences are recoverable (see Samuelson, 1948, for a seminal discussion of integrability in the case of two goods, and Samuelson, 1950, Hurwicz and Uzawa, 1971, and Hosoya, 2016, for general approaches). However, the possibility to recover preferences from a consumer’s demand function does not imply that the distribution of taste uncertainty is identified. Indeed, two distinct taste distributions could produce an identical MRS.

For identification, we only consider the information contained in the demand function on the set of designs for which the components of the demand function are strictly positive. This restriction disregards some information that may be available in the first or third regimes of (2.15). In most datasets, when a component of the demand function equals zero, the price is not observed.

5.1.1 Stochastic Absolute Risk Aversion

In the stochastic absolute risk aversion (SARA) model, the identification condition is:

| (5.1) |

In the degenerate case in which is deterministic and equal to , the MRS red- uces to . Thus, in this special case, the two-dimensional parameter is identified up to a positive factor. This reasoning leads us to a question: Does this lack of identification also exist in an extended setting?

Let us first remark that the utility function is equal to the moment generating function for with a negative sign: . Because this moment generating function characterizes when the stochastic parameter is non-negative (see Theorem 1a in Chapter 13 on Tauberian Theorems in Feller, 1968), it is equivalent to consider the identification of either , or .999Note, the existence of the moment generating function does not imply the existence of all power moments and, even if all power moments exist, they do not necessarily characterize the distribution. A known example is the log-normal distribution used in the application (Heyde, 1963). As mentioned, we can always integrate the MRS to recover a unique preference ordering. That is, we can recover up to a monotonic transformation. We still need to discern the conditions on under which we can recover . Indeed, moment generating functions have properties that are not necessarily preserved under monotonic transformations.

We obtain the following result:

Proposition 5.

If preferences are SARA, then and lead to the same preference ordering, for all positive scalars .

Proof.

Let and denote the utility functions associated with and , respectively. Then, by definition, we must have:

| (5.2) |

where is strictly increasing for . Since is a monotonic transformation of , these utility functions yield the same preference ordering. ∎

This means that we can, at most, identify the class of moment generating functions . Note that, for any moment generating function , the transf- ormed function is also a moment generating function.

Let us now consider identification when and are independent:

Proposition 6.

Let denote the marginal moment generating function for , for . If preferences are SARA, and and are independent, then and lead to the same preference ordering if, and only if, for some , we have:

Proof.

The identification criterion becomes:

for all . This criterion can, then, be written as:

for all . Thus, we deduce that, if these distributions yield the same MRS, then:

for some , at every , for both . Because the log-transform of the moment generating function at zero equals zero, by integrating this equation, we get:

| (5.3) |

at every , for both . Equivalently, and . ∎

Proposition 6 implies that is identified under the independence of and . Indeed, we can recover the consumer’s preference ordering using traditional methods, and use the fact that all admissible preference orderings map to a unique class .

Of course, independence is a strong restriction. In the SARA model, it is equivalent to the additive separability of the utility function.101010In the case of two goods, additive separability is stronger than separability. To see this result, notice that, under independence, we obtain:

| (5.4) |

Since utility functions are unique up to strictly increasing transformations, this utility function is equivalent to:

| (5.5) |

which is an additively separable utility function. In Appendix E, we prove a generalization of Proposition 6 where stochastic taste parameters have a common component.

5.1.2 Stochastic Safety-First

In the SSF model, the identification condition is:

| (5.6) |

Let us now consider the validity of this condition under an independence assumption. Note, in the SSF model, independence is no longer equivalent to additive separability.

Proposition 7.

If preferences are SSF, and are independent, and the marginal distribution of is continuous, then is identified, and the marginal distribution of is identified up to some positive power transformation of its survival function.

Proof.

In the SSF model, the MRS is identified, and it satisfies:

| (5.7) |

where denotes the survival function of .

-

(i)

The expectation is identified because .

-

(ii)

By differentiating (5.7) with respect to , we get:

When , this equation becomes:

By rearranging, we get:

Because the partial derivative of the MRS with respect to is identified, the hazard function of the distribution of is identified up to a positive factor. Since , where is the cumulative hazard function of the distribution of , we can identify up to a positive power transformation.

∎

Proposition 7 provides no information on the identifiability of the distribution of beyond its first moment. It seems difficult to obtain a general identification result, but insights into our identification problem can be obtained by considering the two primary families of distributions that are invariant to positive power transformations, that are, the exponential family and the Pareto family.

-

(i)

Exponential family: Suppose that the marginal distribution of belongs to the exponential family, and that we have identified its survival function up to a positive power transformation such that , for some unknown . The MRS in (5.7) becomes:

(5.8) This expression does not depend on . Now, let denote the Laplace transform of . Under this notation, the equality in (5.8) implies:

Or, equivalently, . By integrating, we obtain:

where is a primitive of the MRS. Therefore:

Corollary 1.

Under the conditions of Proposition 7, if the marginal distribution of belongs to the exponential family, the following results hold:

-

(a)

The power transform is not identified.

-

(b)

The distribution of is identified under an identification restriction on .

We conclude that, under the conditions of Corollary 1, the distributions of and are non-parametrically identified up to a single scalar parameter .

-

(a)

-

(ii)

Pareto family: Let us now examine whether a similar result can be obtained for the Pareto family, in which , for some . The parameter characterizes the fat tails of the distribution of and the power transformation on the MRS. This survival function produces:

where denotes a ratio of quantities. Equivalently, we get:

(5.9) which only depends on the ratio . Therefore, we have constructed homothetic preferences. By equation (5.9):

is identified up to a multiplicative constant. Therefore, by integration, is identified up to and a multiplicative constant . However, as tends to infinity, this expression is equivalent to , where is a primitive of . This tail behaviour provides both the identification of and . This analysis is summarized by the following result:

Corollary 2.

Under the conditions of Proposition 7, if the marginal distribution of belongs to the Pareto family, the distributions of and are both non-parametrically identified.

5.2 Between Model Identification

Once the identification of the consumer’s taste distribution within each model is solved, we still need to consider the identification between the models. This analysis is needed to test whether preferences are consistent with SARA, or SSF, or both. It is important to know whether these two classes of preferences are nested or non-nested. If they are non-nested, we need to characterize their intersection and define a general class encompassing both types of preferences.

To illustrate, suppose that the consumer has SSF preferences:

| (5.10) |

where (i) and are independent, (ii) has distribution , and (iii) follows an exponential distribution (with unit intensity). Under this specification, we obtain:

| (5.11) |

To clarify this result, observe that, by conditioning on , we are left with the expec- tation of the minimum of a set containing a constant and a random variable with an exponential distribution. This utility function is a strictly increasing transformation of a SARA utility function:

| (5.12) |

where (i) follows a point mass at , and (ii) has distribution . Consequently, these utility functions, one SARA, and the other SSF, induce the same preference ordering over the consumption set.

5.3 Discussion

The possible lack of identification of each consumer’s taste distribution has to be taken into account in the economic interpretation of the results. However, it has to be noted that it does not create difficulties for structural inference, where the (scalar or functional) parameters of interest are the parameters characterizing the MRS, rather than the parameters characterizing the utility function.

The lack of identification is due to the special structure of the cone of increasing and concave functions defined on , and of the extremal elements of this cone. For finite increasing concave functions defined on , it is well-known that the extremal functions are of the type:

| (5.13) |

in which , for (see Blaschke and Pick, 1916), and that any finite positive increasing concave function can be written as:

| (5.14) |

where is a positive scalar and is the distribution of . Such functions are charac- terized by and . The set of extremal functions in (5.14) is a minimal set of extremal points generating the cone.

Such a property no longer holds for finite positive increasing concave functions defined on . Johansen (1974) has described a large set of extremal points of the type:

| (5.15) |

for which induces a covering with vertices of order 3 (see page 62 in Johansen, 1974), and has shown that this set is dense in the cone of finite continuous convex functions defined on a convex set in (see Theorem 2 in Johansen, 1974). A minimal set of extremal points generating this cone does not exist. This argument explains why Sections 2 and 3 consider specific convex subsets generated by parametric functions.

While we restrict our attention to SARA and SSF preferences (because the stochastic taste parameters have clear interpretations in these models), other convex hulls co- uld have been considered. For example:

- (i)

-

(ii)

The convex hull generated by a basis of the form:

(5.16) for every in which and . This basis corresponds to a first-order expansion of a utility function (see Johansen, 1969), and contains a Stone-Geary utility function as a limiting case. Indeed, as approaches zero, we obtain: . However, the convex hull generated by this basis is not flexible enough because it only contains weighted combinations of and . Similarly, the convex hull generated by a Stone-Geary basis only contains Stone-Geary utility functions, where the weights are the means of the taste parameters:

(5.17)

The Stone-Geary basis above can be adjusted to define another parametric basis. In particular, let us apply the transformation to the Stone-Geary utility function. This transformation yields:

| (5.18) |

This utility function forms a well-behaved basis because it is strictly increasing with a negative semi-definite Hessian. While and represent the same preference ordering, they will generate different families due to the strict concavity of . To illustrate, suppose that the stochastic parameters, and , are independently distributed with respect to uniform distributions on . This specification produces:

| (5.19) |

While is a Stone-Geary utility function, is a complicated non-linear function of and . Consequently, an uninteresting basis has been transformed into an interesting one. This procedure can be completed for any increasing, concave, and twice-differentiable transformation .

6 An Illustration

This section shows how to use the SARA and SSF models in a non-parametric framework. First, we specify the statistical model by introducing an assumption on the obs- ervations, and then we discuss statistical inference. The methodology is illustrated in an application to alcohol consumption using scanner data concerning individual purchase histories.

6.1 Assumptions on Observations

The behavioural models introduced in the previous sections can be completed with an assumption on the available observations. We consider panel data, indexed by the consumer and date . After a preliminary treatment of the purchase histories, we have a large number of consumers and a fixed number of observed dates. In the preliminary treatment, the goods are aggregated into two groups using a common quantity unit and the dated purchases are aggregated by month (see Section 6.3). Recall that, under Assumption A1, we have segments of homogeneous consumers.

We introduce the following assumption on the observations:

Assumption A2 (Observations).

-

(i)

We jointly observe , for all and , when .

-

(ii)

The individual histories are independent given all , .

-

(iii)

Designs are exogenous (independent of taste distributions ).

Assumption A2 describes the structure of the observations. It implies that we can imagine taste parameters being independently drawn from a Dirichlet process , designs being independently drawn from some distribution, and consumption satisfying , where is the group of consumer . Many papers assume that consumption is positive (see Section IV.A in \hyper@linkcitecite.blundell\@extra@b@citebBlundell, Horowitz, and Parey, \hyper@linkcitecite.blundell\@extra@b@citeb2017, for this assumption in an application to gasoline demand, as well as Assumption A5 in Dobronyi and Gouriéroux, 2020, for this assumption in an application to the consumption of alcohol); the SARA and SSF models allow for corner solutions. However, in many datasets (including the dataset used in the application in Section 6), there is a problem of partial observability. Let denote the expenditure (prior to normalization), and let denote the price of good (prior to normalization). Usually, we only observe the price of a good when the consumer buys a positive quantity of good . Then, we only observe (normalized) expenditure when the consumer buys a positive quantity of good 2, and we only observe the (normalized) price when the consumer buys a positive quantity of both goods (see Crawford and Polisson, 2016, for an approach to revealed preference that deals with this partial observability problem). This problem explains the specific form of Assumption 2(i).

For deriving the asymptotic properties of estimators, it is also necessary to specify the type of asymptotics to be considered:

Assumption A3.

Let denote the size of the homogeneous group.

-

(i)

, as , for all .

-

(ii)

, for some , where , for .

-

(iii)

, as .

Assumptions A3(i) and A3(ii) ensure that there are enough observations to non-parametrically estimate the demand function associated with the functional parameter on a sufficiently large subset of designs . Assumption A3(iii) guarantees enough filtered parameters to estimate the underlying Dirichlet process . In some special circumstances, is large, and Assumption A3 can be used with and —that is, a single consumer per group. Otherwise, grouping of homogeneous consumers is needed to identify the demand functions on sufficiently large subsets .

6.2 Estimation Method

The Dirichlet process is common in Bayesian estimation (see, for instance, Ferguson, 1974, and Li et al., 2019). This process is useful because it is flexible and, if observations are independently and identically drawn from an unknown distribution, the posterior distribution of this distribution has a closed-form expression. However, our framework is much more complicated for two reasons:

-

(i)

The observed consumption choices are not identically distributed because consumers make decisions at different expenditures and prices.

-

(ii)

It is difficult to derive a closed-form expression for the demand, as a function of the expenditure, the price, and the functional parameter characterizing taste uncertainty . It is, therefore, difficult to derive a closed-form expression for the distribution of conditional on .

These features of our model explain why estimation requires specific numerical algor- ithms. These specific algorithms have to be able to deal with the non-linear and high- dimensional features of the models. In the Bayesian framework, the Dirichlet process is fixed. In the hyperparametric framework, it is parameterized by a vector . These parameters have to be estimated and the functional parameters have to be filter- ed. These estimation approaches are described below.

6.2.1 Bayesian Framework

In a pure Bayesian framework, a Dirichlet process is fixed by selecting a mean distribution and a scaling parameter (see Appendix A). This distribution defines the common prior for the functional taste parameters . After, the data are used to compute the posterior distribution for the functional parameters . Under Assu- mption A2, the posterior distribution can be computed separately for each homogeneous group of consumers:

where denotes the group of consumers with preferences characterized by the taste parameter . This approach does not have to account for the potential identification problem discussed in Section 5. If a specific characteristic of is weakly identified, its posterior distribution will be close to the prior distribution.

In our framework, the observations , conditional on , must satisfy the deterministic first-order conditions implied by the model. These conditions have the following form:

| (6.1) |

for any observed pair . Equivalently:

| (6.2) |

for any observed pair . These conditions are moment restrictions, called MRS restrictions. In our big data framework, the number of MRS restrictions is very large, typically several hundred to a thousand. The posterior of is simply the distribution of given these deterministic restrictions on . If the taste parameters, and , are independent with marginal distributions, and , respectively, then the MRS restrictions are bilinear in and —specifically, these restrictions are linear in given , and linear in given . Later, this property is used to construct a numerically efficient optimization algorithm for filtering all the (see Appendix C).

6.2.2 Hyperparametric (or Empirical Bayesian) Framework

The hyperparametric (or empirical Bayesian) framework is a complicated non-linear state-space model with two layers of latent state variables. Such a framework can be characterized as follows:

-

(i)

Deep layer: Functional parameters , drawn from (parameterized by );

-

(ii)

Surface layer: Demand functions deduced from ;

-

(iii)

Measurement equations: Observed pairs , given .

We have partial observability of the demand function because the value of demand is observed at finitely many designs . Furthermore, unlike most state-space models, the state variables are infinite-dimensional.

6.2.3 Estimating the Hyperparameter

While it is difficult to derive analytically the distribution of given , it is easy to simulate its distribution for a given value of (see Appendix A for simulations from the Dirichlet distribution). Therefore, can be estimated by the method of simulated moments (MSM), or indirect inference (see McFadden, 1989, Pakes and Pollard, 1989, and Gouriéroux and Monfort, 1996). That is, is estimated by matching some sample and simulated moments of the pair .

To illustrate, consider a pure panel such that .111111When , we simulate observations for the draw from the Dirichlet process. The steps are the following:

-

Step 1:

Simulate draws from a Dirichlet process given the parameter . Each draw is associated with an individual consumer such that .

- Step 2:

-

Step 3:

Construct a collection of moments from the observed and simulated data:

Then, numerically solve the following problem:

(6.3) in which is a Euclidean norm with the form , for some positive-definite matrix .

Given the estimated hyperparameter , the taste distributions must be filtered. This step is equivalent to applying the Bayesian approach with the estimated Dirichlet distribution as the prior distribution (see Appendix C).

6.2.4 Filtering the Taste Distributions

Once the hyperparameter is estimated, we can filter by using the following steps:

-

Step 1:

Draw a taste distribution from the Dirichlet process given . Then, by construction, the taste distribution is a draw from the prior distribution.

-

Step 2:

Discretize on a grid of values for the taste parameters, and . Let denote the result. The aim of this step is to put on a grid for optimization.

-

Step 3:

Solve the minimization problem:

Let denote the solution. This solution approximates a drawing from the posterior.

-

Step 4:

Replicate these steps to obtain a sequence of solutions: , , where is the number of replications. The filtered is obtained by averaging over all simulations such that:

This procedure involves a high-dimensional argument , and a very large number of MRS restrictions. Indeed, we need several hundred grid points for , and, in the application, we have about one-thousand MRS restrictions, for each . If the taste parameters, and , are independent, this procedure can be numerically simplified by using the fact that these restrictions are bilinear (see Section 6.2.1 and Appendix C).

6.3 The Data

We use the Nielsen Homescan Consumer Panel (NHCP). Nielsen provides a sample of households with barcode scanners. Households are asked to scan all purchased goods on the date of each purchase. The prices are entered by the households or linked to retailer data by The Nielsen Company. The households that agree to participate are compensated through benefits and lotteries.

We focus on the consumption of alcoholic drinks (see Manning et al., 1995, for an application to alcohol consumption in economics). We classify drinks by type. Good 1 contains beers and ciders.121212The NHCP classifies ciders as wine, by default. We reclassify these beverages using product desc- riptions because most ciders have a low alcohol by volume (ABV). Good 2 contains wines and liquors. We disregard all non-alcoholic beers, ciders, and wines. We are left with 30,635 beers and ciders, and 108,439 wines and liquors, for a total of 139,074 drinks. We convert all measurement units to litres of alcohol by first converting all units to litres and then multiplying by the standard alcohol by volume (ABV) in each subgroup—specifically, 4.5% for beer and cider, 11.6% for wine, and 37% for liquor. For example, if a household buys two packs of six bottles of beer and each bottle contains 355 millilitres of beer, then the household buys 4.26 litres of this beer, or litres of alcohol. We use the standard ABV in each subgroup as a result of data limitations. Our sample only contains purchases made at stores, not purchases made at bars, or restaurants.

Measuring quantities in litres of alcohol has at least three advantages: (i) it can account for a quality effect, (ii) it is appropriate for analyzing most relevant structural objects (e.g. the effect of a change in taxation on alcohol consumption), and (iii) it yi- elds continuous quantities, permitting the application of standard tools in consumer theory (which could not be used if quantities were measured in, for example, bottles), and avoiding some common identification issues in the literature.

We restrict our sample to purchases made from August to November in 2016. This relatively short window is used to diminish the impact of changing tastes and product availability, and to avoid most federal holidays in the United States that are often associated with alcohol consumption such as Independence Day, Christmas Day, and New Year’s Eve. Our sample contains 28,036 households. Some additional details of this restricted sample are placed in Appendix D.

| Quantiles | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Var. | 0% | 25% | 50% | 75% | 100% | ||||

| 52.29 | 70.62 | 1.35 | 0.00 | 13.28 | 28.17 | 62.97 | 2,767.76 | 63,972 | |

| 70.36 | 44.19 | 0.62 | 0.05 | 46.41 | 62.55 | 83.41 | 2,893.65 | 33,077 | |

| 61.33 | 326.93 | 5.33 | 0.03 | 29.29 | 48.56 | 75.14 | 39,900.85 | 45,518 | |

| 1.60 | 3.48 | 2.17 | 0.00 | 0.27 | 0.74 | 1.83 | 228.57 | 45,518 | |

| 2.20 | 4.06 | 1.54 | 0.00 | 0.89 | 1.37 | 2.29 | 139.76 | 14,659 | |

The dated purchases are aggregated by month. For each household and month, the prices are constructed by dividing the total expenditure for each aggregate good (after accounting for the value of coupons) by the amount of alcohol of that aggregate good purchased by the household, when this amount is strictly positive. Then, we norm- alize by the price of good 2. This procedure yields four monthly observations per hou- sehold for a total of 112,144. A total of 63,936 observations have positive consumption such that . Table 1 gives summary statistics conditional on . The prices are conditional on being well-defined (see the discussion of partial observability on pages 23 and 24). For the interpretation of the results, recall that is the expenditure (prior to normalization), and that is the price of good (prior to normal- ization).

| 0.4298 | 0.2751 | |

| 0.1642 | 0.1307 |

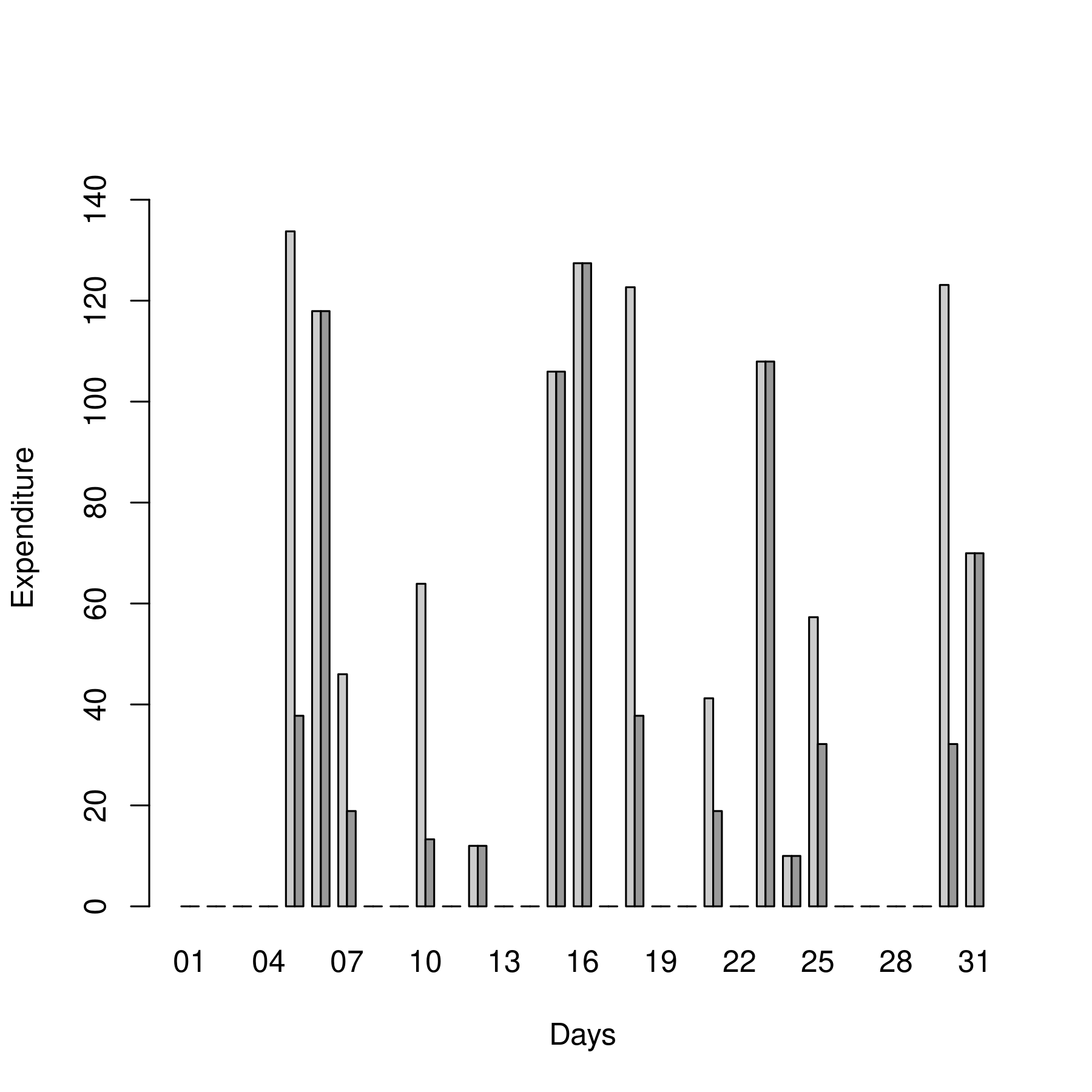

There are four regimes of observations: (i) zero expenditure on all goods, (ii) zero expenditure on good 1 and strictly positive expenditure on good 2, (iii) strictly pos- itive expenditure on good 1 and zero expenditure on good 2, and (iv) strictly positive expenditure on all goods. Table 2 provides the proportion of observations in each regi- me, and shows a large proportion of observations with zero expenditure. Recall, under Assumption A2, designs are drawn from a distribution. Therefore, we can interpret this result as a mass at zero in the marginal distribution of expenditure.

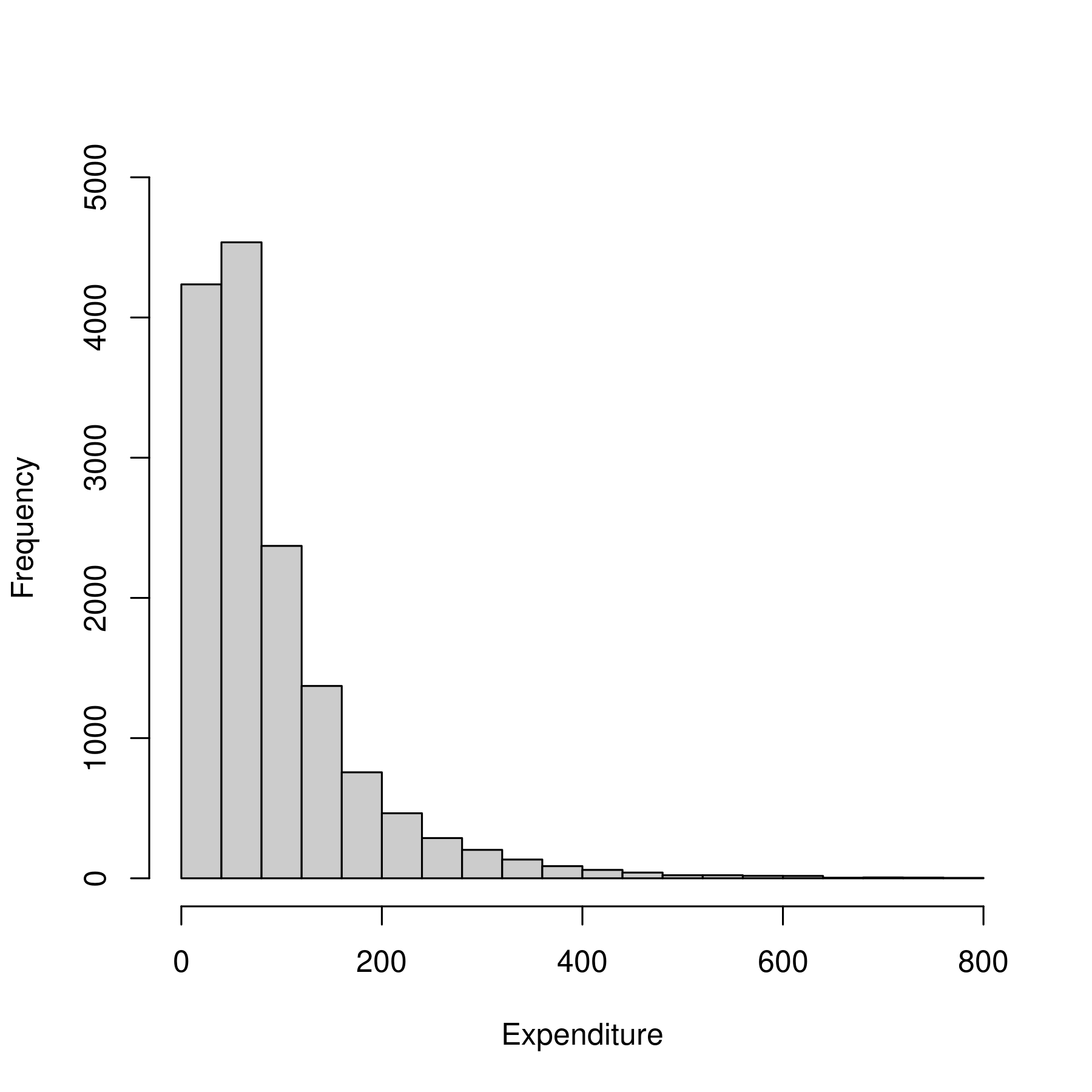

Figure 4 displays the sample distribution of expenditure by regime: the distribution of expenditure conditional on is on the left; the sample distributions of expenditure for the two other regimes with positive expenditure are on the right. The shape of the sample distribution of expenditure does not appear to vary all that much with the regime. That being said, the sample distribution conditional on has more probability attributed to higher expenditures.

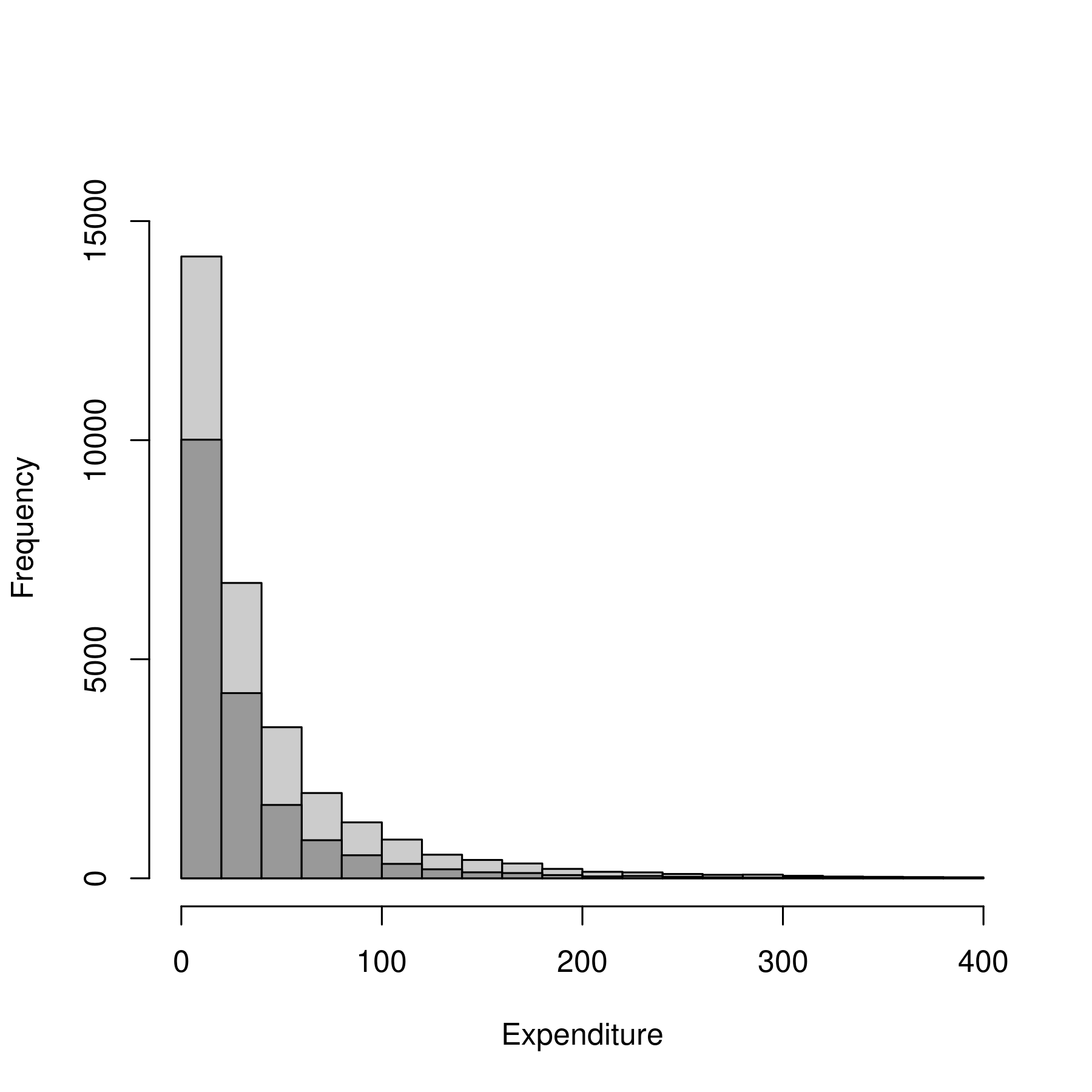

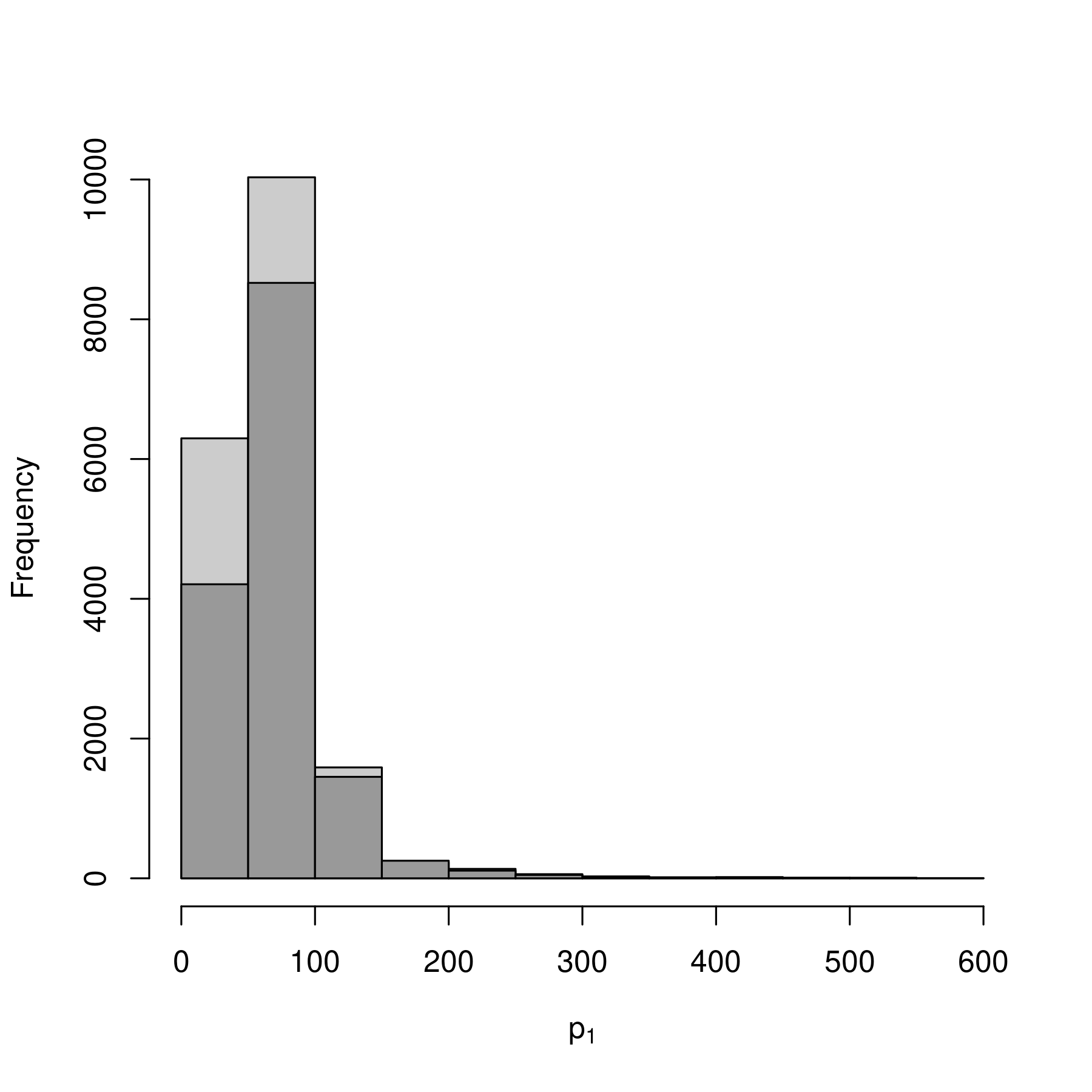

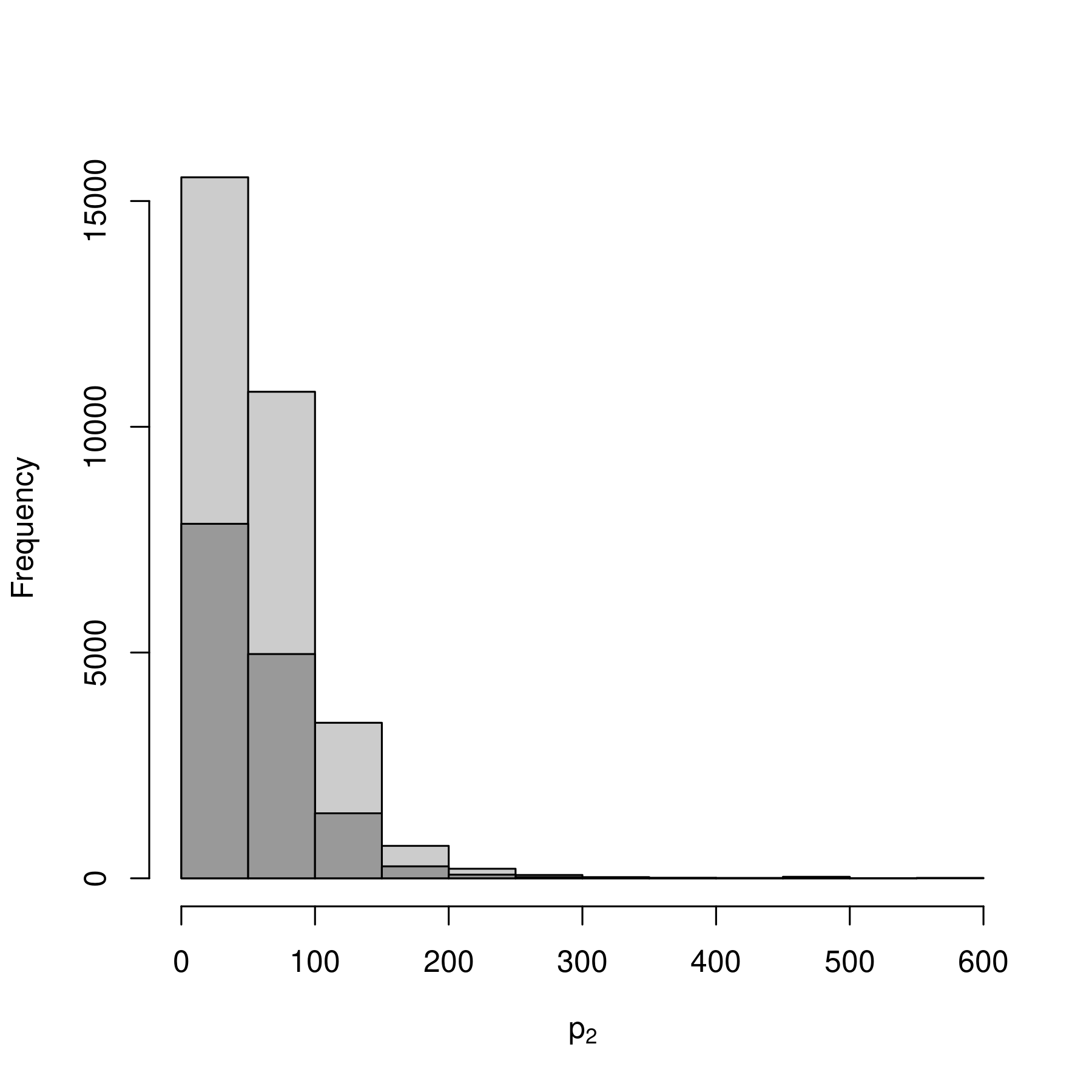

Figure 5 compares the sample distributions of prices by regime: the sample dis- tributions of are on the left; the sample distributions of are on the right. Although the sample distribution of differs from the sample distribution of , these distributions do not seem to be affected by the regime.

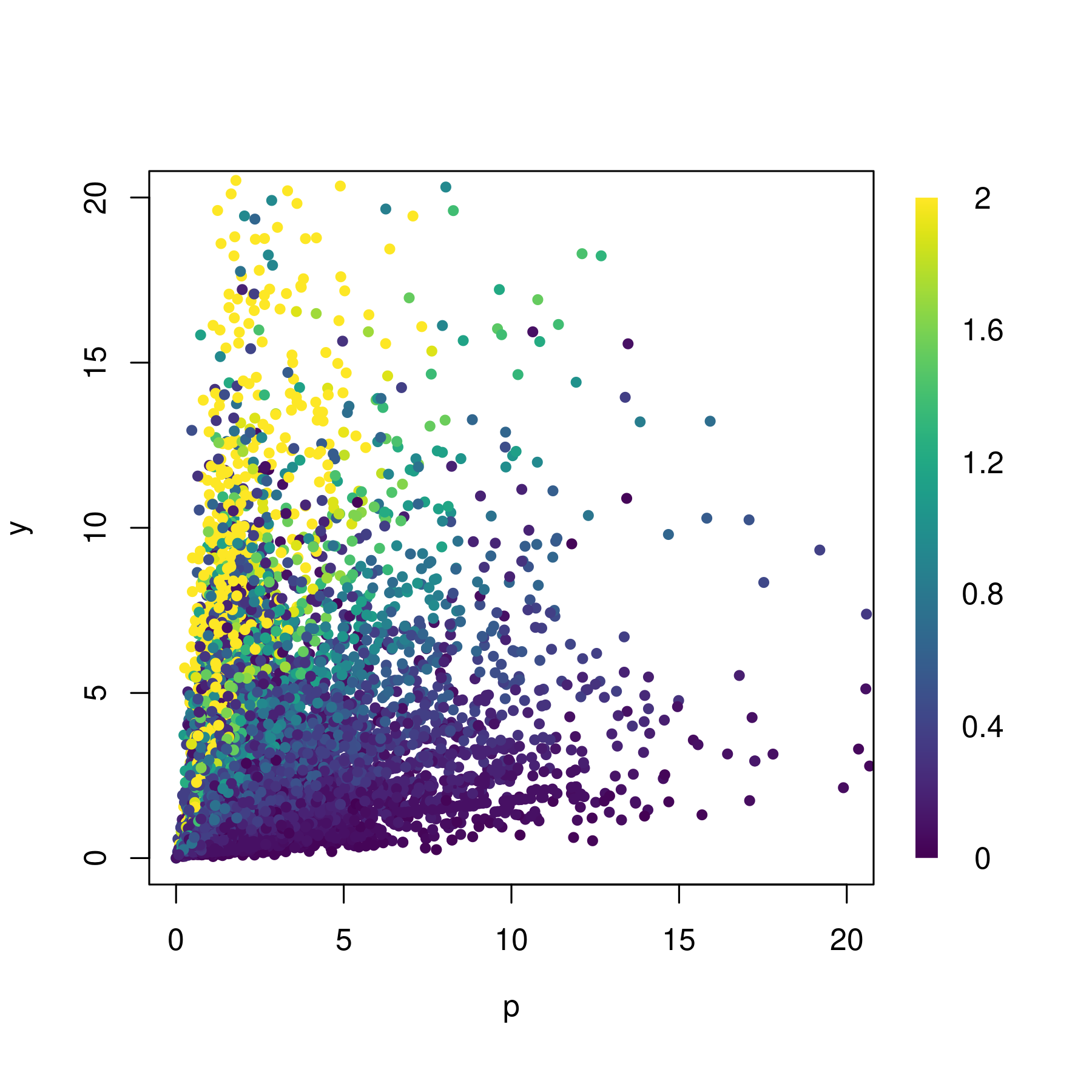

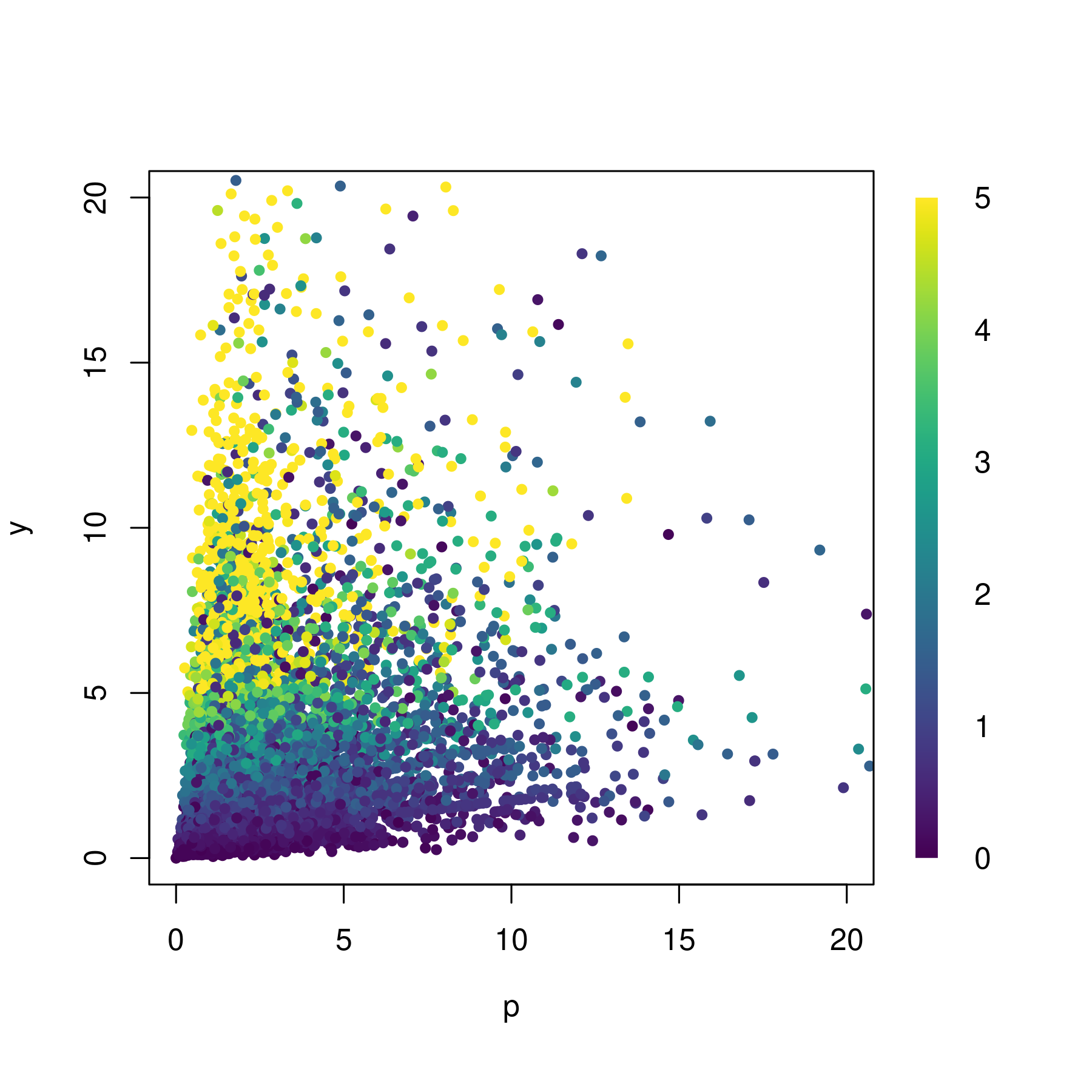

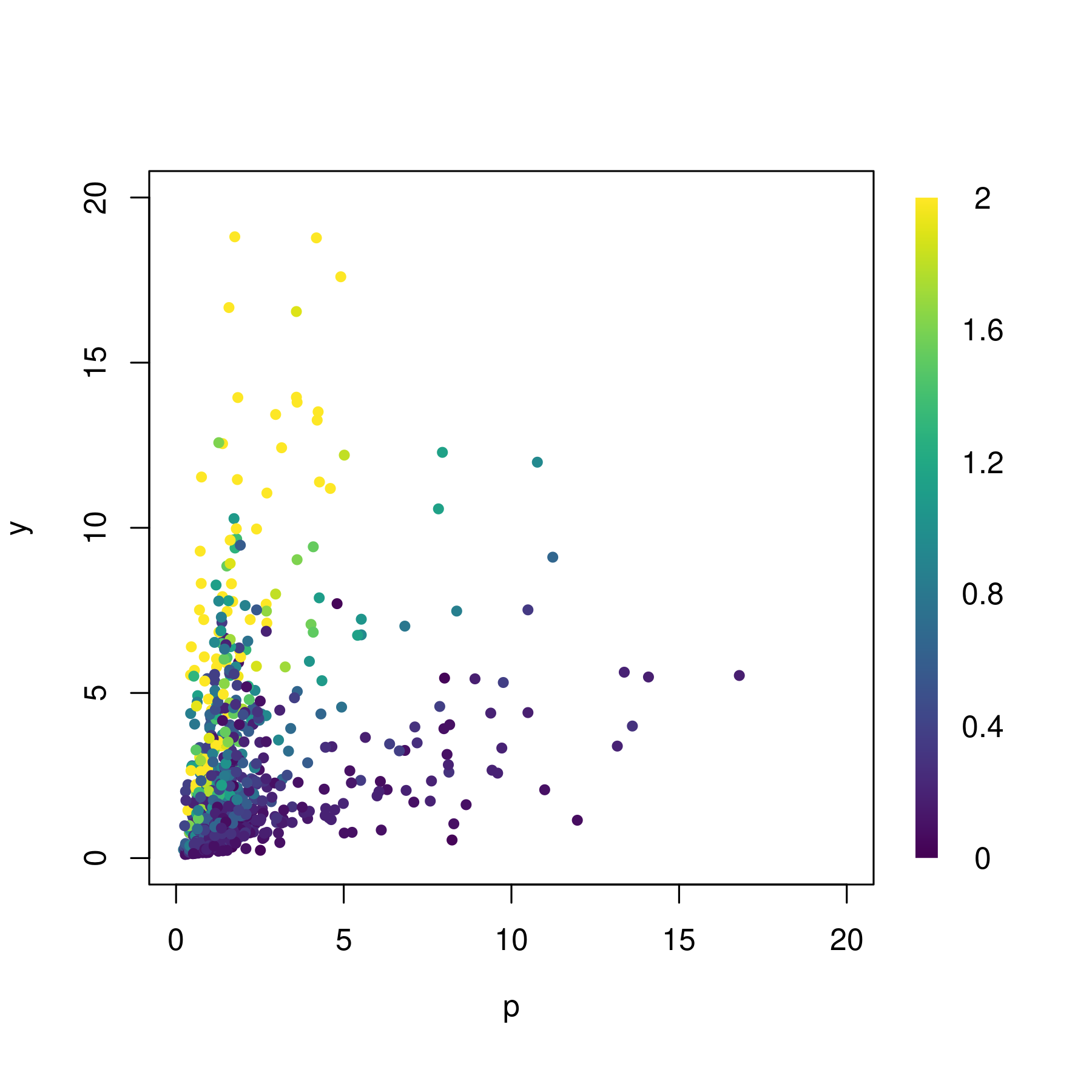

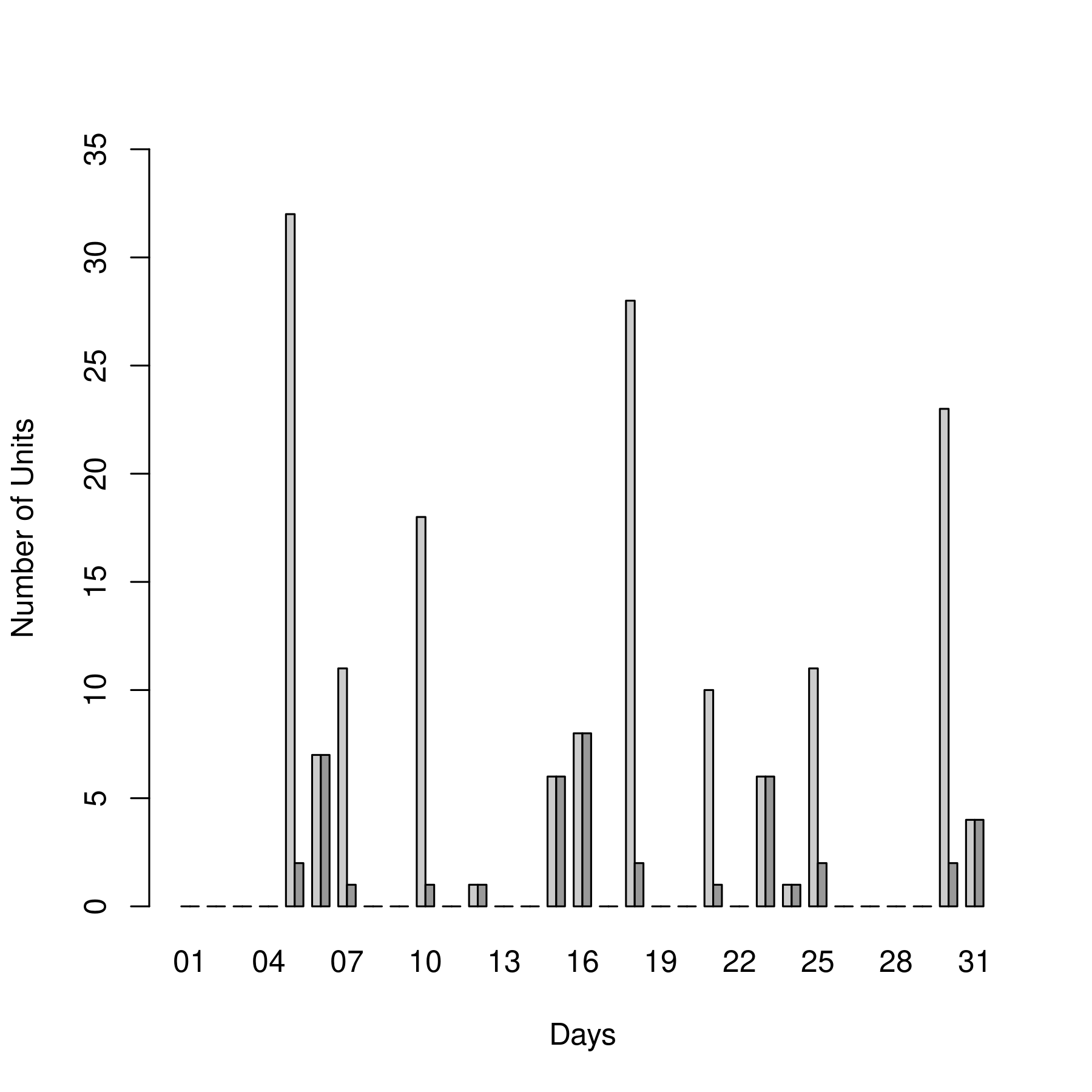

Figure 6 displays the sample distributions of (normalized) designs and the components of consumption given . As expected, the components of consumption are increasing in expenditure . Furthermore, the first component of consumption is more affected by changes in the price than the second component.

Since we consider a rather short window of time, we follow the segmented population approach. We segment the population by state. Large states (e.g. California) are segmented again by county. Specifically, a county is given its own segment if it has more than 70 observations with positive consumption and it is in a state with more than 1,000 observations with positive consumption. We are left with a total of 65 seg- ments, each corresponding to a state or county. The smallest segment is Wyoming, containing 15 observations with positive consumption; the largest state is Florida (after removing Broward, Hillsborough, Palm Beach, Pinellas, and Miami-Dade counties), containing 880 observations with positive expenditure; the mean number of observations with positive consumption per segment is approximately 226.

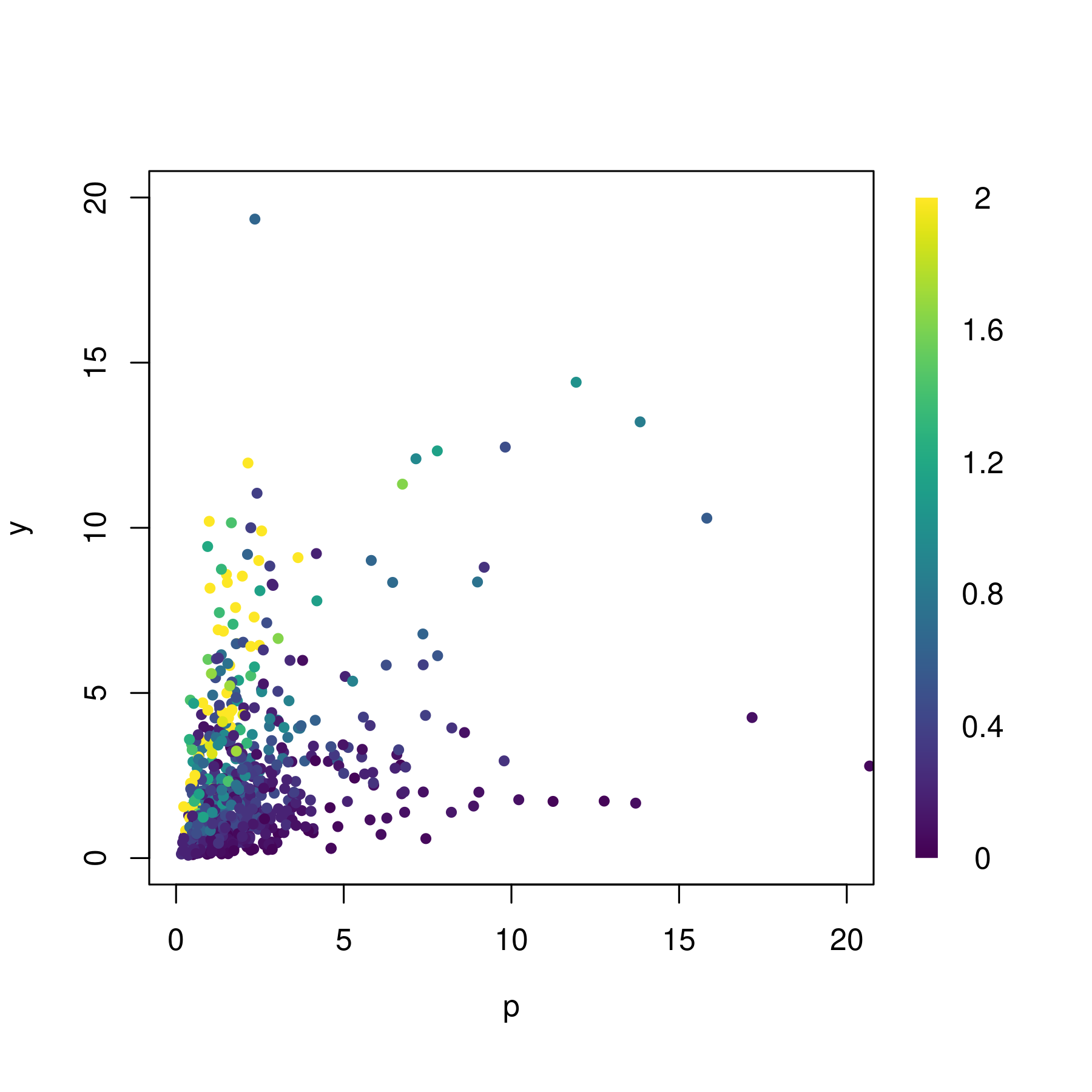

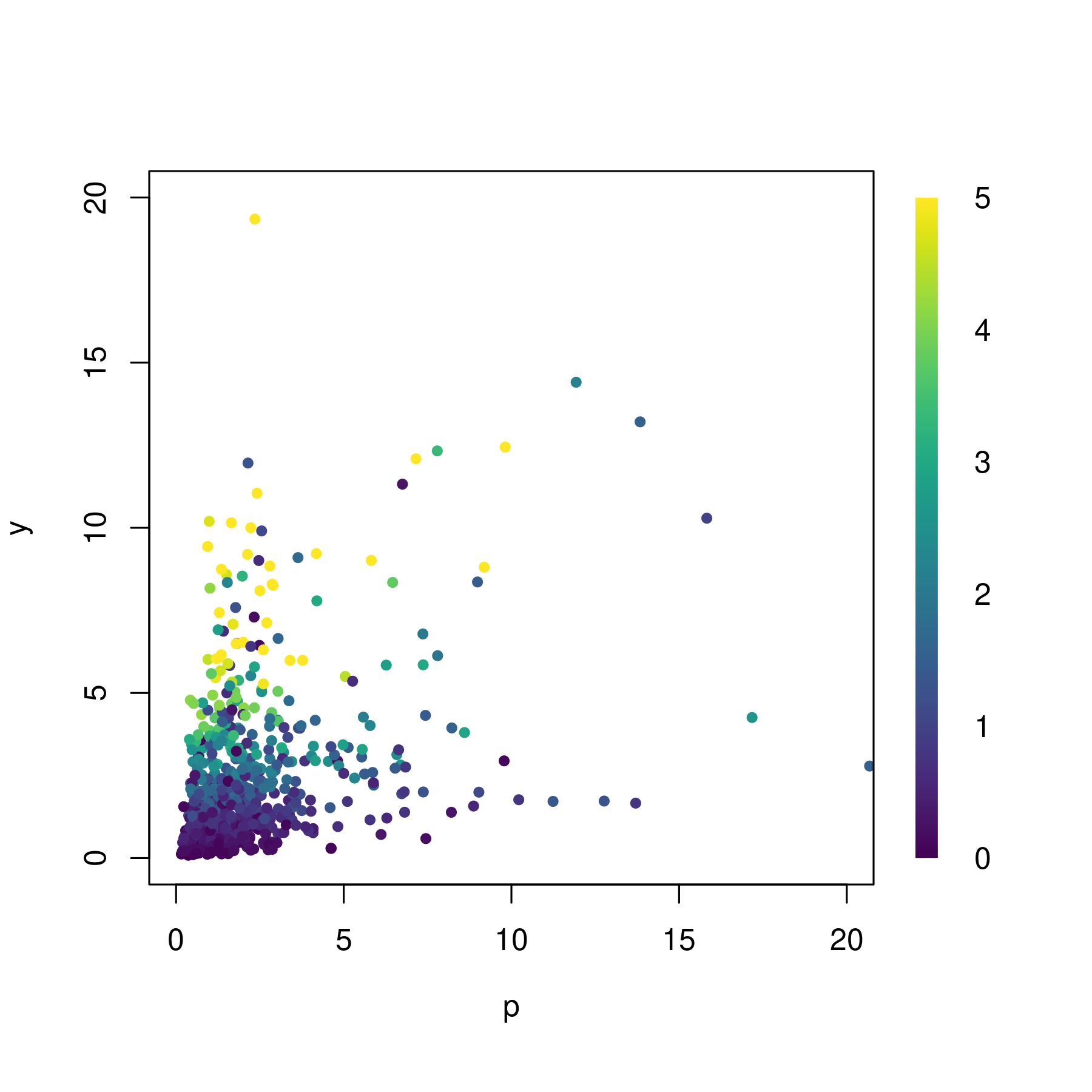

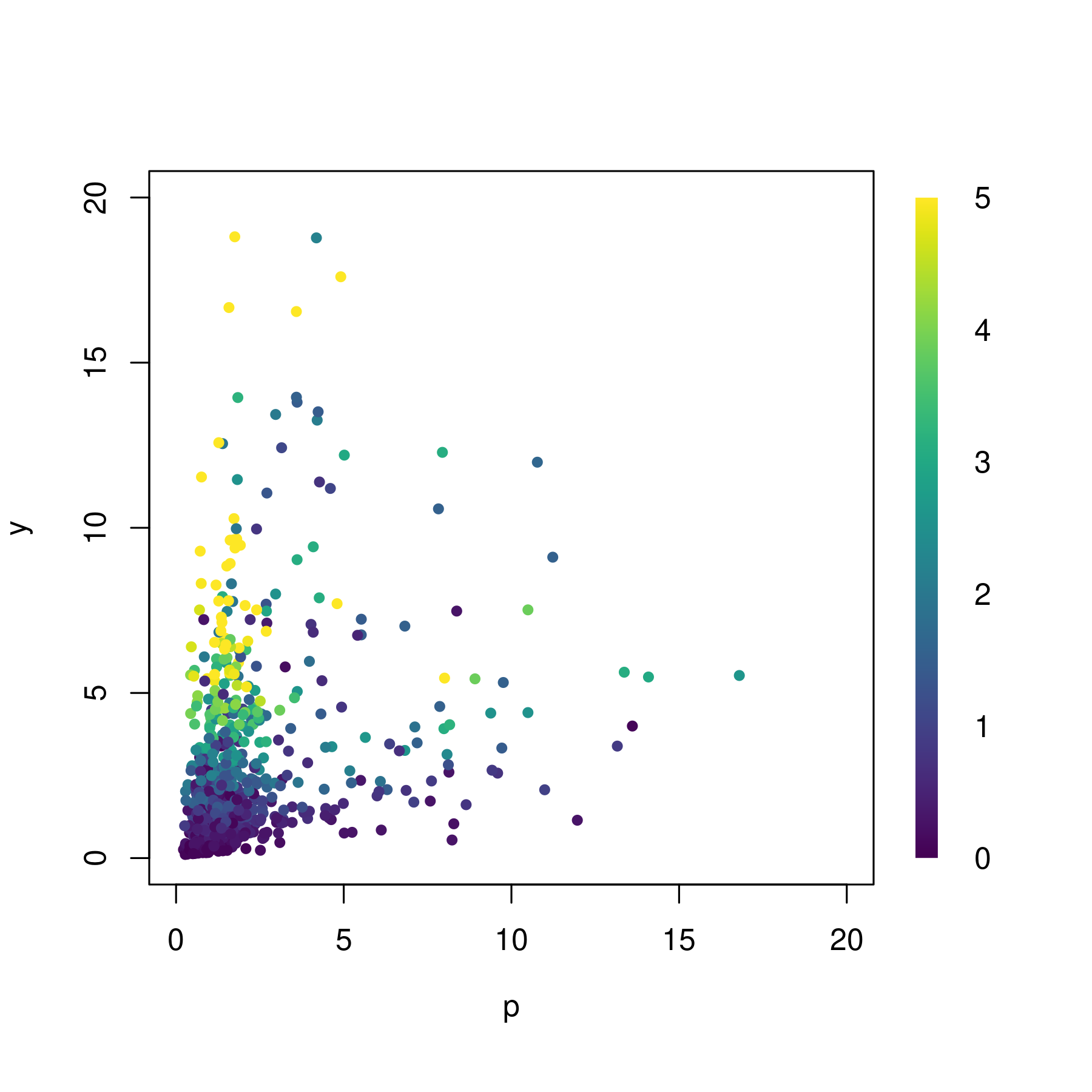

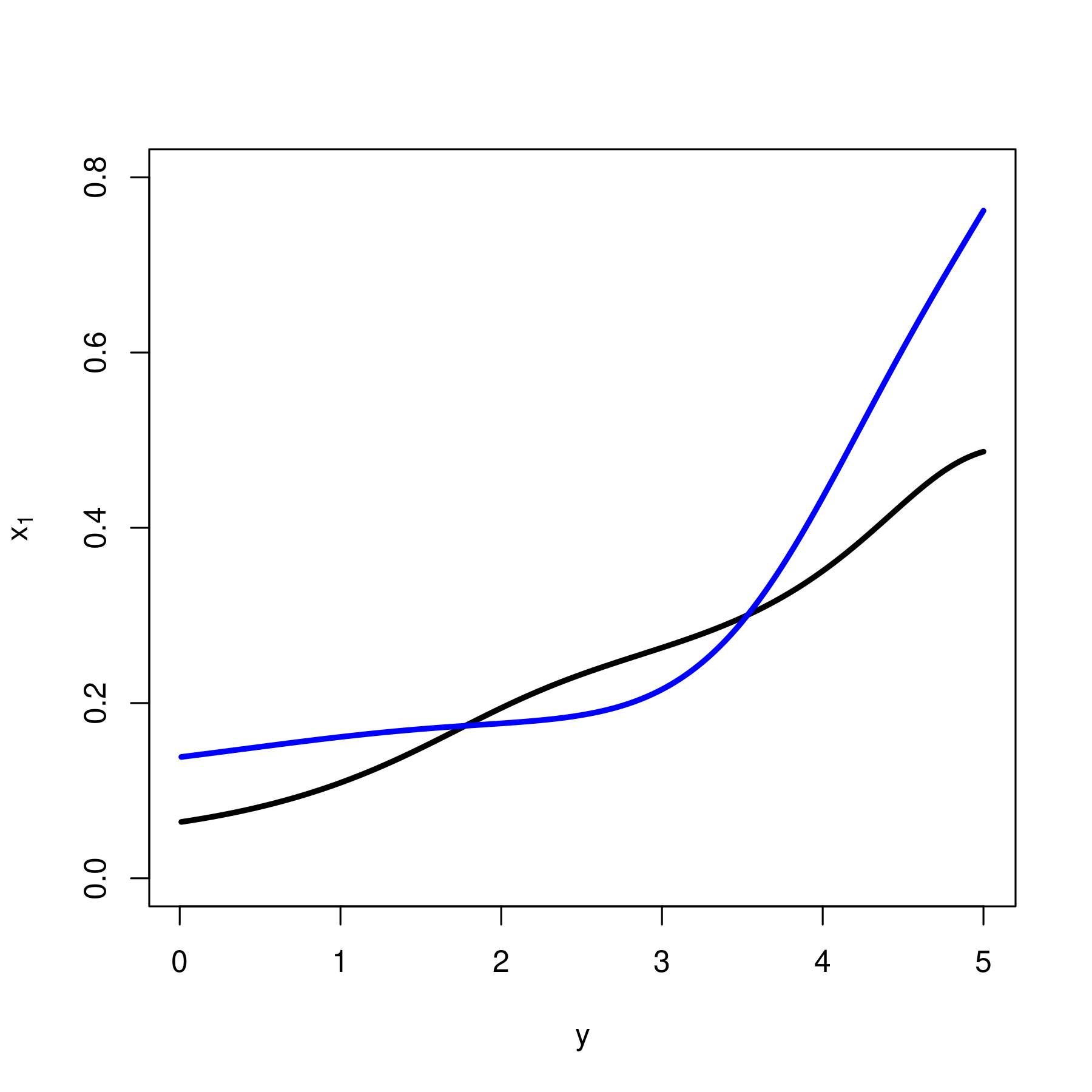

Figure 7 displays the sample distributions of (normalized) designs and the first component of consumption given in two of the larger segments: California (after removing Almeda, Los Angeles, Orange, Riverside, Sacramento, San Bernardino, and San Diego counties), and Florida (after removing Broward, Hillsborough, Palm Beach, Pinellas, and Miami-Dade counties).

Figure 8 displays the Nadaraya-Watson (kernel) estimates of the demand function for beer conditional on in California and Florida over a subset of the domain of designs. Demand for beer in California is lower and less responsive to price changes than in Florida. Figure 9 displays Engel curves for good 1 in California and Florida given .131313This price is chosen to be in a sufficiently dense region of the sample distribution (see Figure 7). These Engel curves cross.

6.4 Estimation Results

As an illustration, we consider the SARA model in the hyperparametric framework. We assume that the taste parameters, and , are independent. Under this assum- ption, the taste uncertainty is characterized by the marginal distributions, and . The marginal distribution of is independently drawn from a Dirichlet process , . The mean of is a log-normal distribution with parameters and , and the scale parameter of is . The utility function corresponding to this log-normal mean distribution, say , has a quasi closed-form expression. Indeed, under this distribution, we obtain:

where is distributed with respect to a standard normal distribution. Then:

where is the Lambert function, defined by the implicit equation:

[see equation (1.3) in Asmussen et al., 2016]. By drawing from the Dirichlet process, we will draw a stochastic utility function around the closed-form expression above. The hyperparameter has six components such that:

6.4.1 The Hyperparameter

As described in Section 6.2.2, the first step involves estimating the hyperparameter using the Method of Simulated Moments (MSM). The hyperparameter is calibrated by using the following (sample and simulated) moments computed for all of the 63,936 observations with positive consumption:

-

(i)

marginal moments of ;

-

(ii)

cross-moments of and ;

-

(iii)

cross-moments of , , , and .

The moments in (ii) are the moments used in the Almost Ideal Demand System (see Deaton and Muellbauer, 1980); the moments in (iii) are introduced in order to capture risk effects by comparison with the moments in (ii). The optimum is found using a random search algorithm over a sufficiently big support.141414Random search is more efficient than grid search in hyperparameter optimization (Bergstra and Yoshua, 2012).

To apply MSM, it is necessary to compute simulated consumption for every observation, at each step of the optimization algorithm. This procedure is computati- onally costly. Note that, the number of simulated observations with positive consumption is stochastic, and not necessarily equal to the number of observations with positive consumption in the sample. This aspect has no impact on the consistency of the MSM estimator.

The estimated hyperparameter is:

| (6.4) |

Therefore, the median level of risk aversion for the mean of the Dirichlet process151515This is not the absolute risk aversion of the utility function for the log-normal mean distribution which depends on the consumption level and has to be computed with a modified density. for is , and the median level of risk aversion for the mean of the Dirichlet process for is . The fact that is smaller than is expected: Since quantities are measured in terms of volume of alcohol, this result is consistent with the faster overall intake of alcohol when consuming drinks with a higher ABV. Moreover, the distribution of is much more concentrated around its mean than the distribution of , as the scaling parameter for is much larger than the scaling parameter for .

We do not report any standard errors because they are automatically small from the large number of observations. Indeed, the standard significance test procedures (such as comparing a t-statistic to the critical value of a standard normal at the 5% significance level) are not relevant in this big data framework. The highest degree of uncertainty concerns the filtered functional parameters since is a high-dim- ensional parameter and the number of observations in each segment is much smaller.

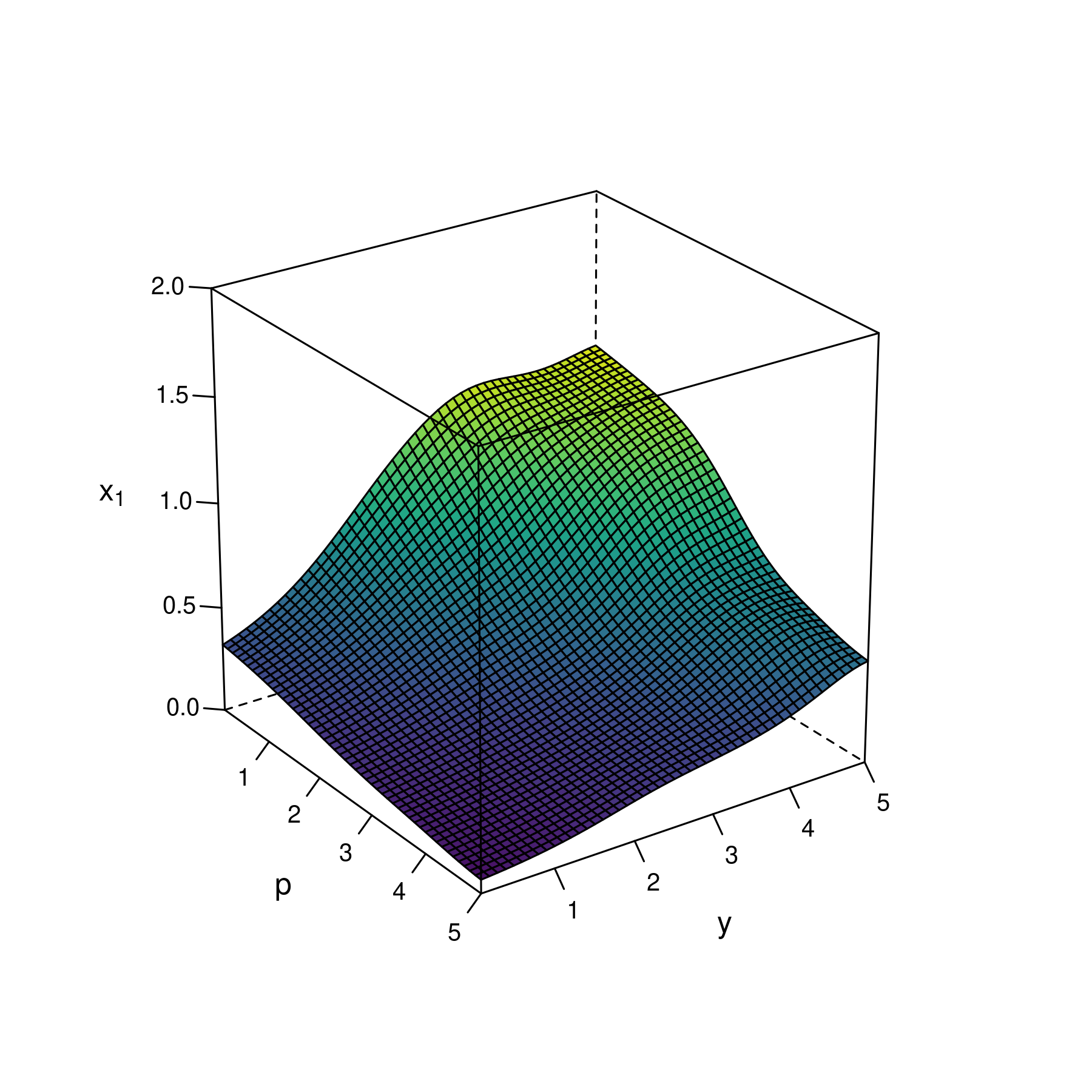

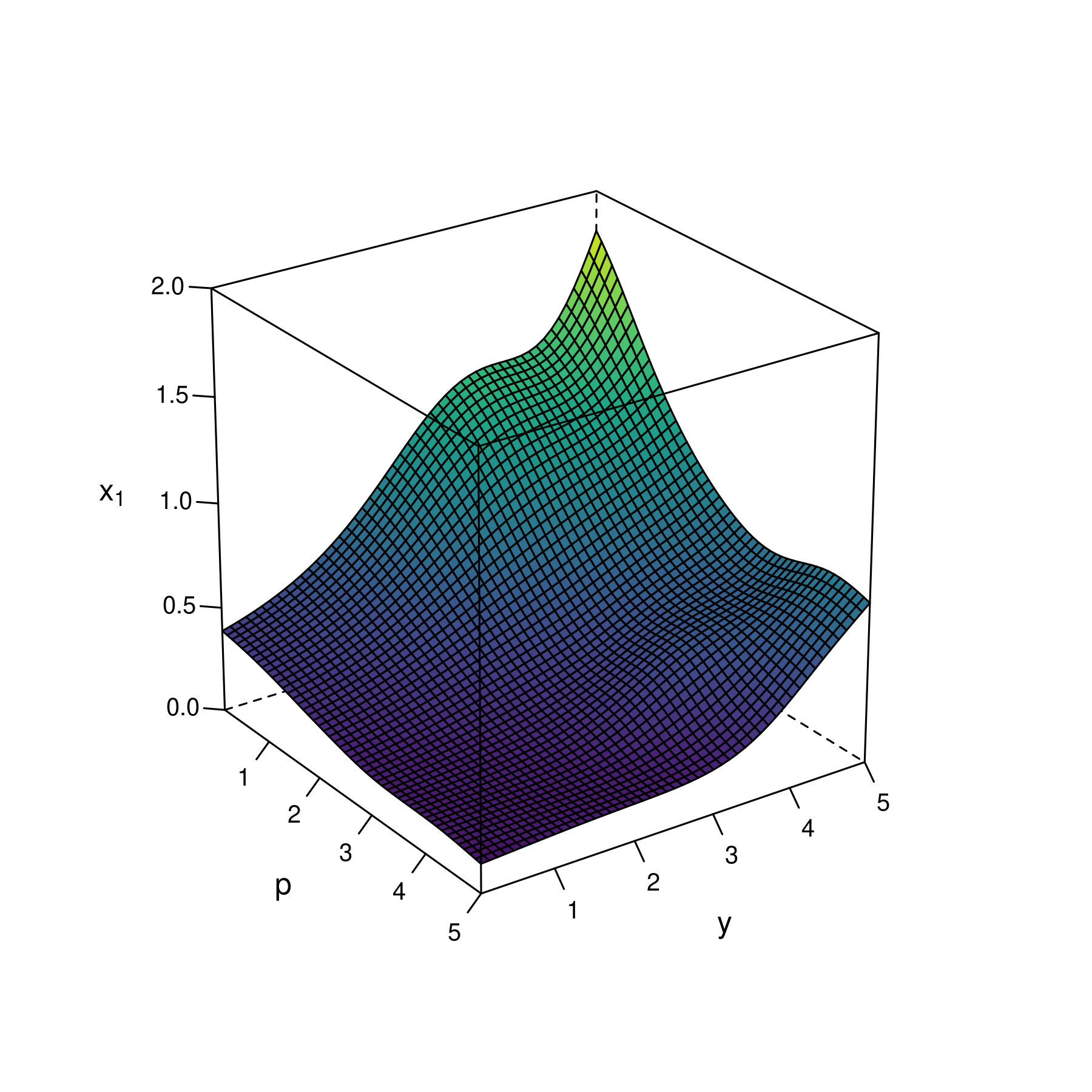

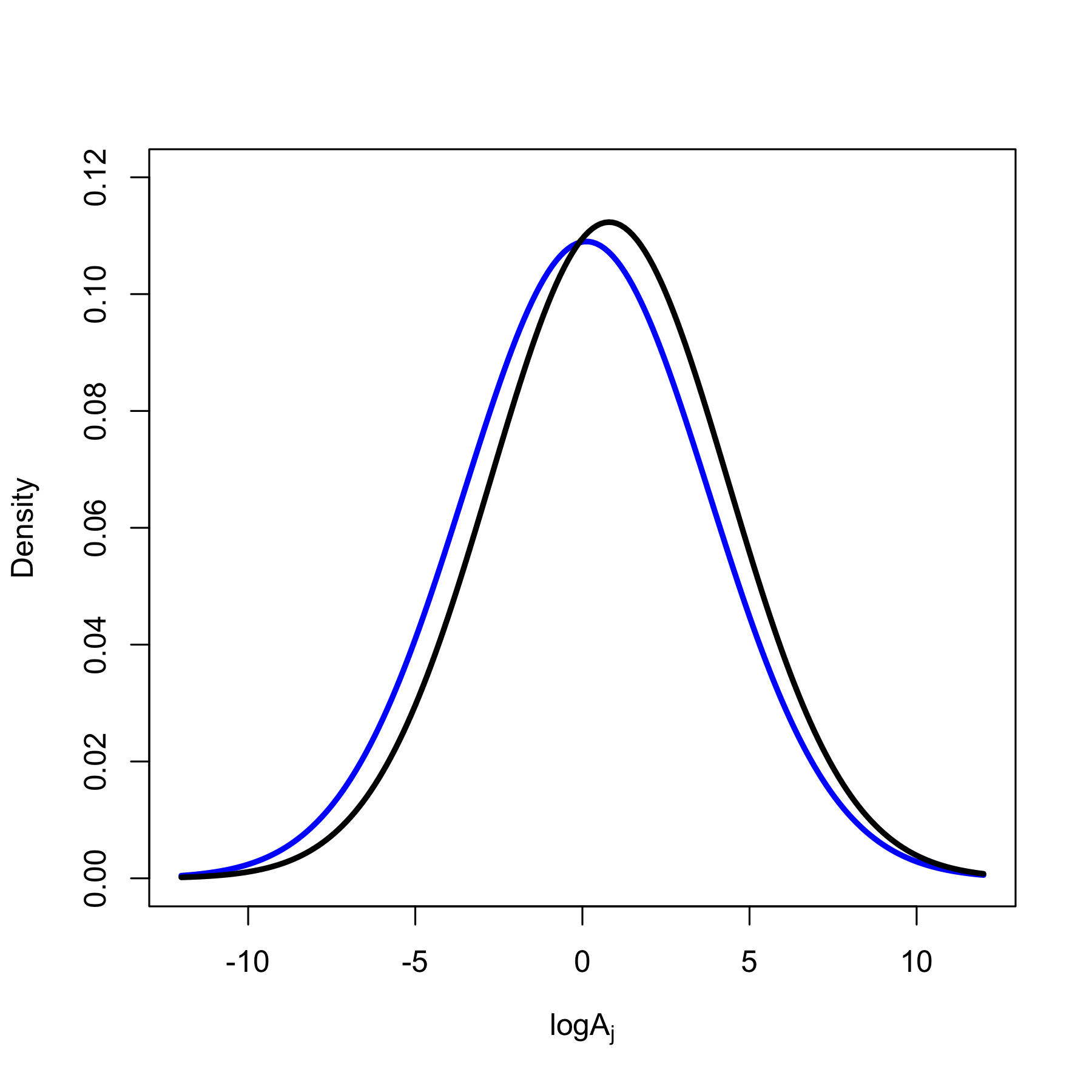

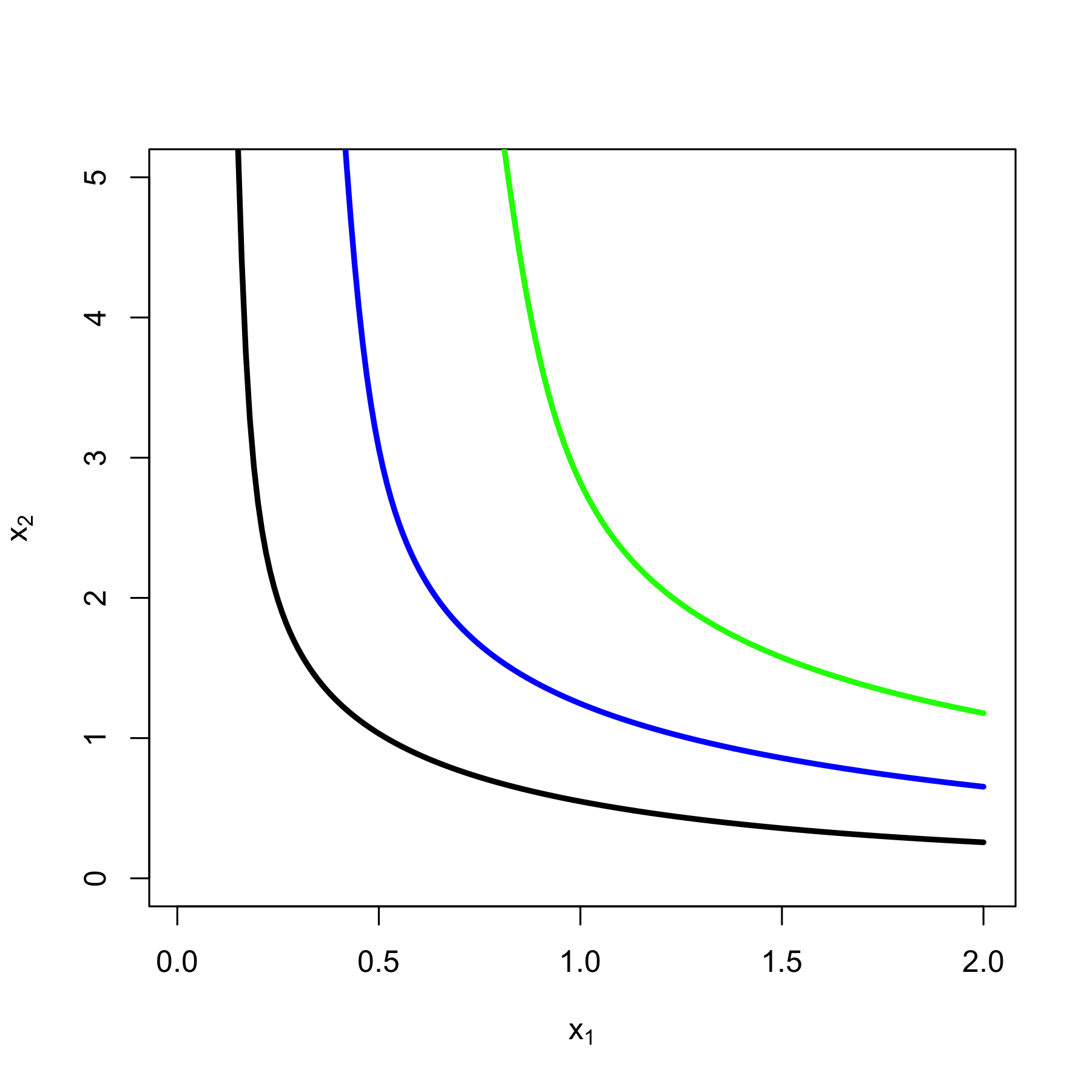

The means of these Dirichlet processes are displayed in the left panel in Figure 10. The right panel displays the indifference curves associated with utility levels , , and for a draw from the Dirichlet process given .

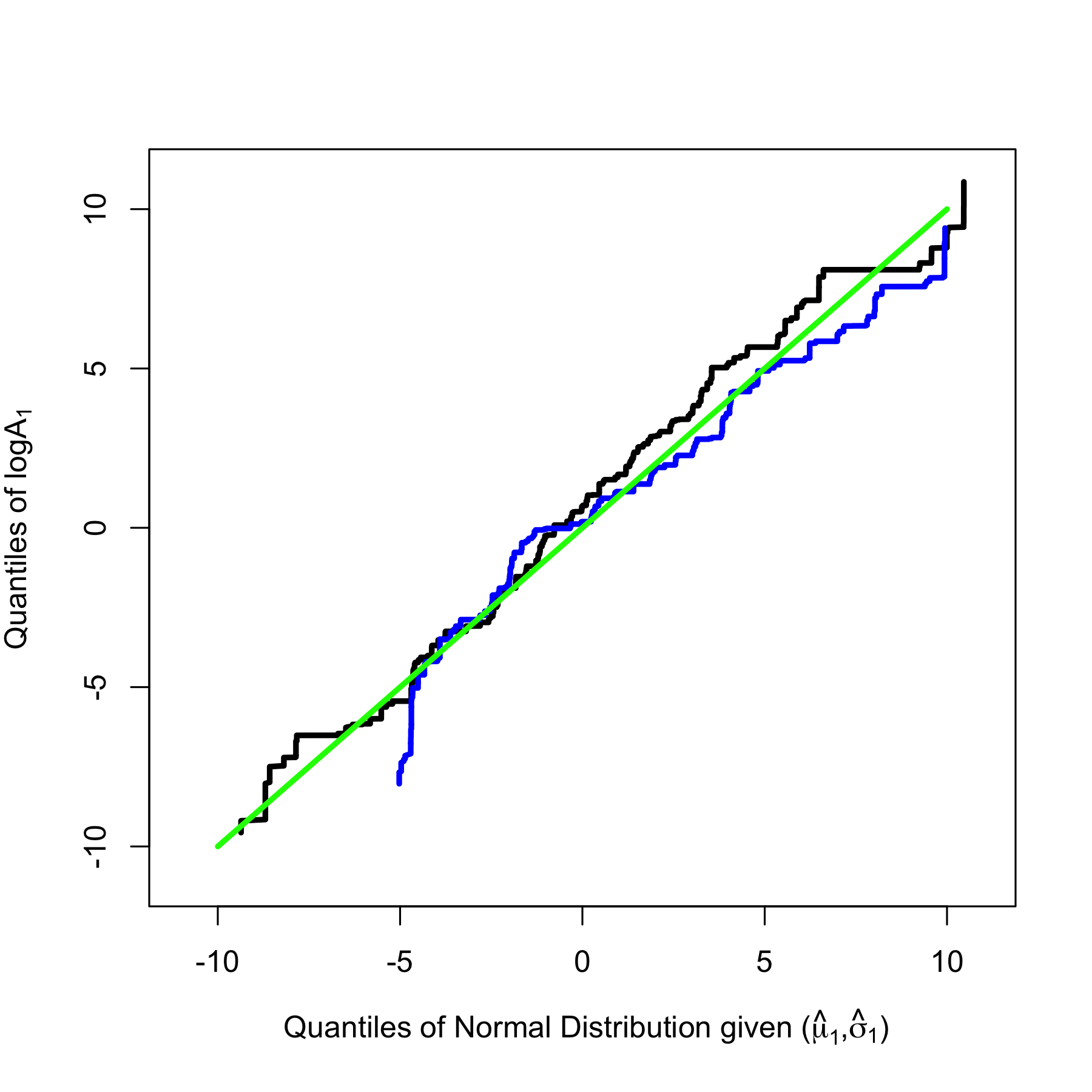

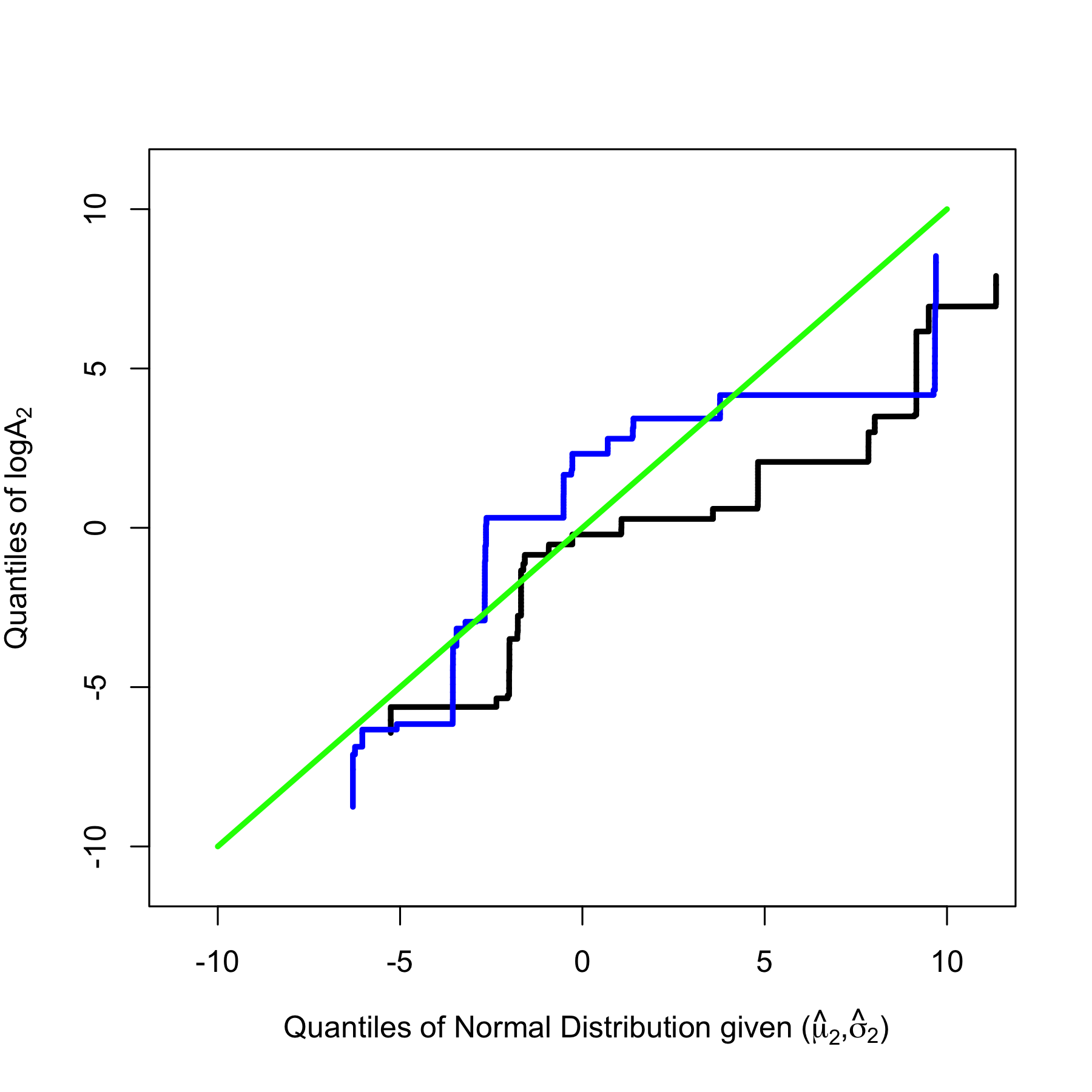

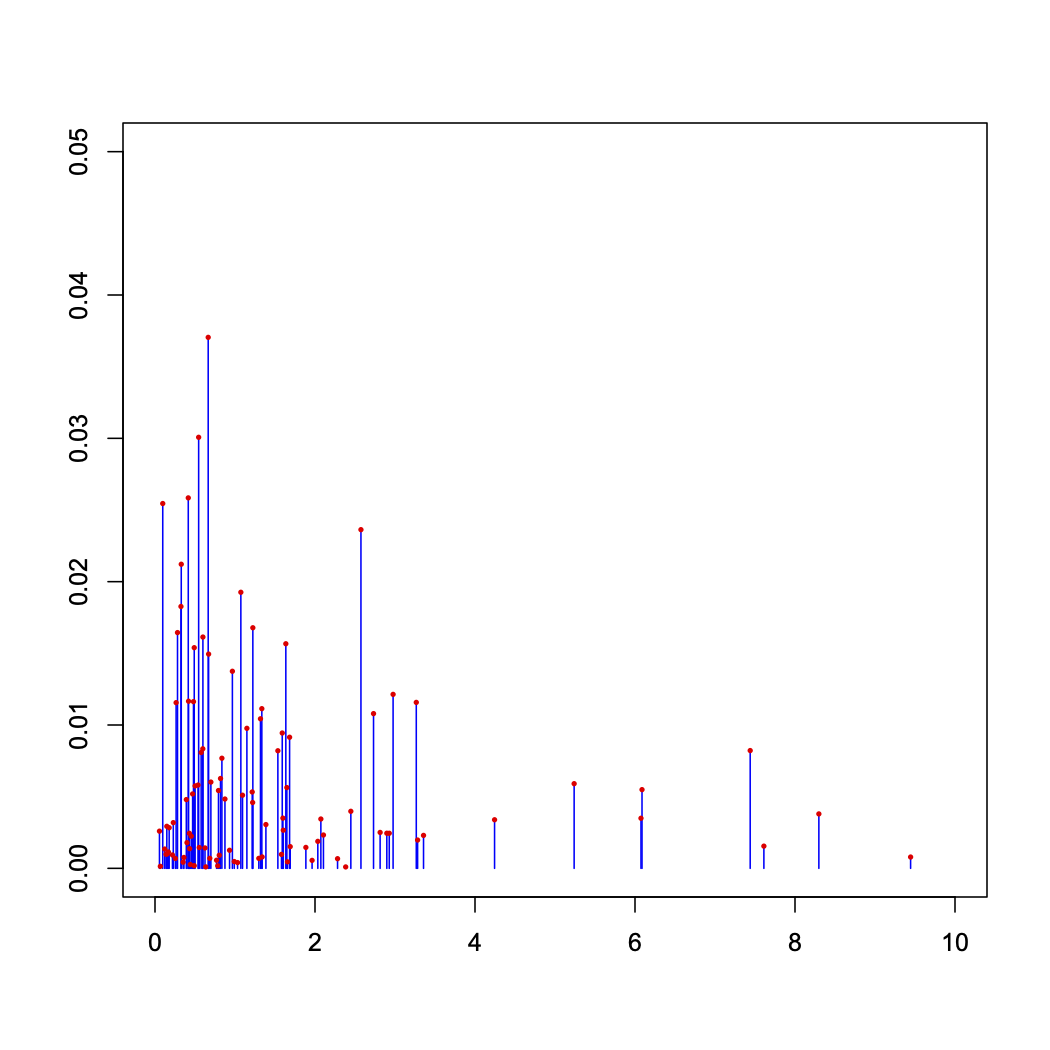

Figure 11 displays the Q-Q plots for two draws , , from the Dirichlet process given . In particular, we plot the quantiles of the realization of the distribution of against the quantiles of the normal distribution given the estimated hyperparameters , for . If these quantiles coincide exactly, they will lie on the 45-degree line. As expected, these Q-Q plots lie approximately around the 45-degree line. The draws , , for are closer the 45-degree line and “more continuous” than the draws , , for since .

Figure 11 illustrates how one might use the (estimated) hyperparameter for interpretation. Specifically, it is used to deduce the mean of the Dirichlet process, which is used as a benchmark for comparison with a drawn or filtered functional parameter .

6.5 Taste Distributions

This section uses the filtering approach described in Section 6.2.4 to recover . In the SARA model, the MRS restriction in (6.2) is:

When and are independent, this expression becomes:

| (6.5) |

To filter , these restrictions have to be imposed for every observation with positive consumption associated with segment . In California, there are 688 MRS rest- rictions, and, in Florida, there are 880. Appendix C shows how to numerically solve the resulting optimization problem given the bilinearity of the MRS restrictions under independence.

The marginal taste distributions were filtered using a grid with 500 points between and , equally spaced on the log-scale. All draws from the estimated prior were simulated by the stick-breaking method given breaks (see Appen- dix A). Exactly draws from the posterior were used to filter each distribution.

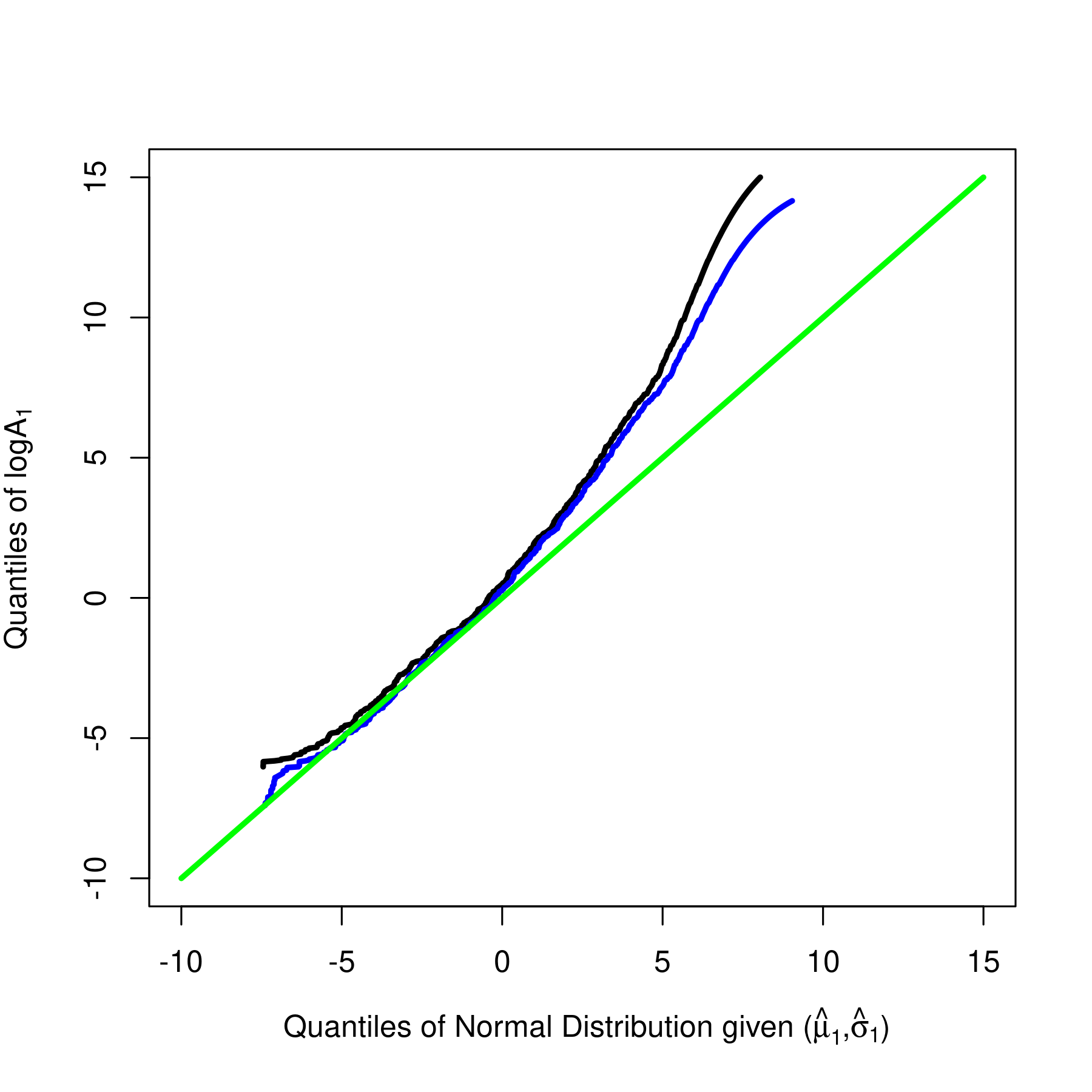

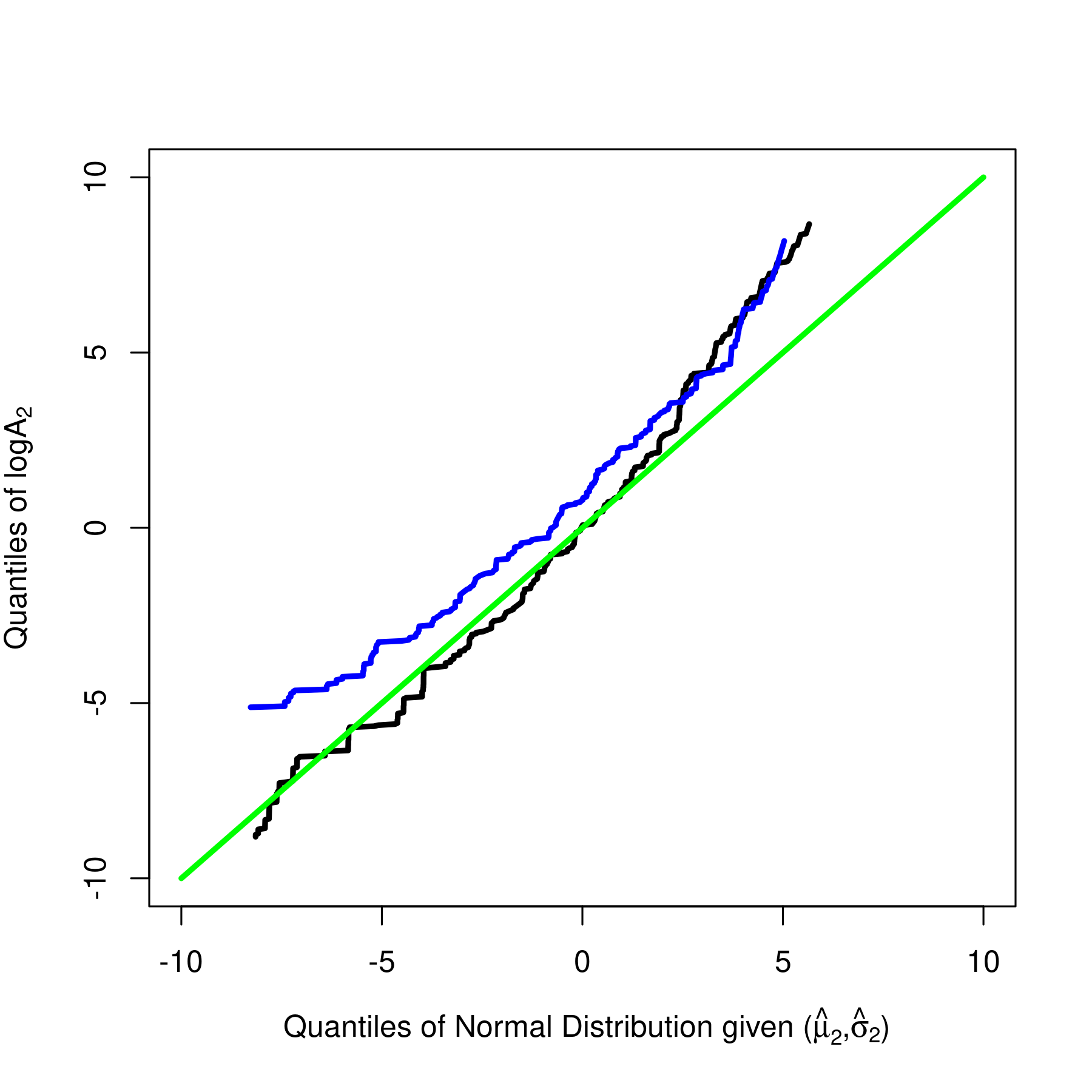

Figure 12 displays the Q-Q plots for the filtered taste parameters for California and Florida. As in Figure 11, the (estimated) hyperparameter is used to construct a benchmark for comparison. As expected, the filtered taste parameters are rather diff- erent from this benchmark. Here, the role of the estimated prior distribution diminishes with the number of observations. In both states, the slope on the left is steeper than the 45-degree line, suggesting that the posterior mean distribution for is more “dispersed” than its estimated prior mean distribution. The convexity of these curves also suggests fatter tails.

For the structural interpretation of these plots, assume that (i) the preferences are SARA, (ii) the taste parameters are independent, (iii) the marginal distribution of is the same in both states, and (iv) the marginal distribution of “shifts” such that , where and denote the marginal distributions of in these states. Under these assumptions:

| (6.6) |

and solving the utility maximization problem in (2.13) yields:

| (6.7) |

Similarly, if there is a “shift” in the marginal distribution of and the marginal dist- ribution of is the same in both states, we obtain:

| (6.8) |

The relationships given in (6.7) and (6.8) suggest that there exists a complicated non-linear relationship between such demand functions. Therefore, we cannot immediately deduce from Figure 12 which state has a higher demand for beer. For a more formal analysis, the utility functions associated with each posterior mean taste distribution must be used to derive a posterior MRS, or a posterior demand function.

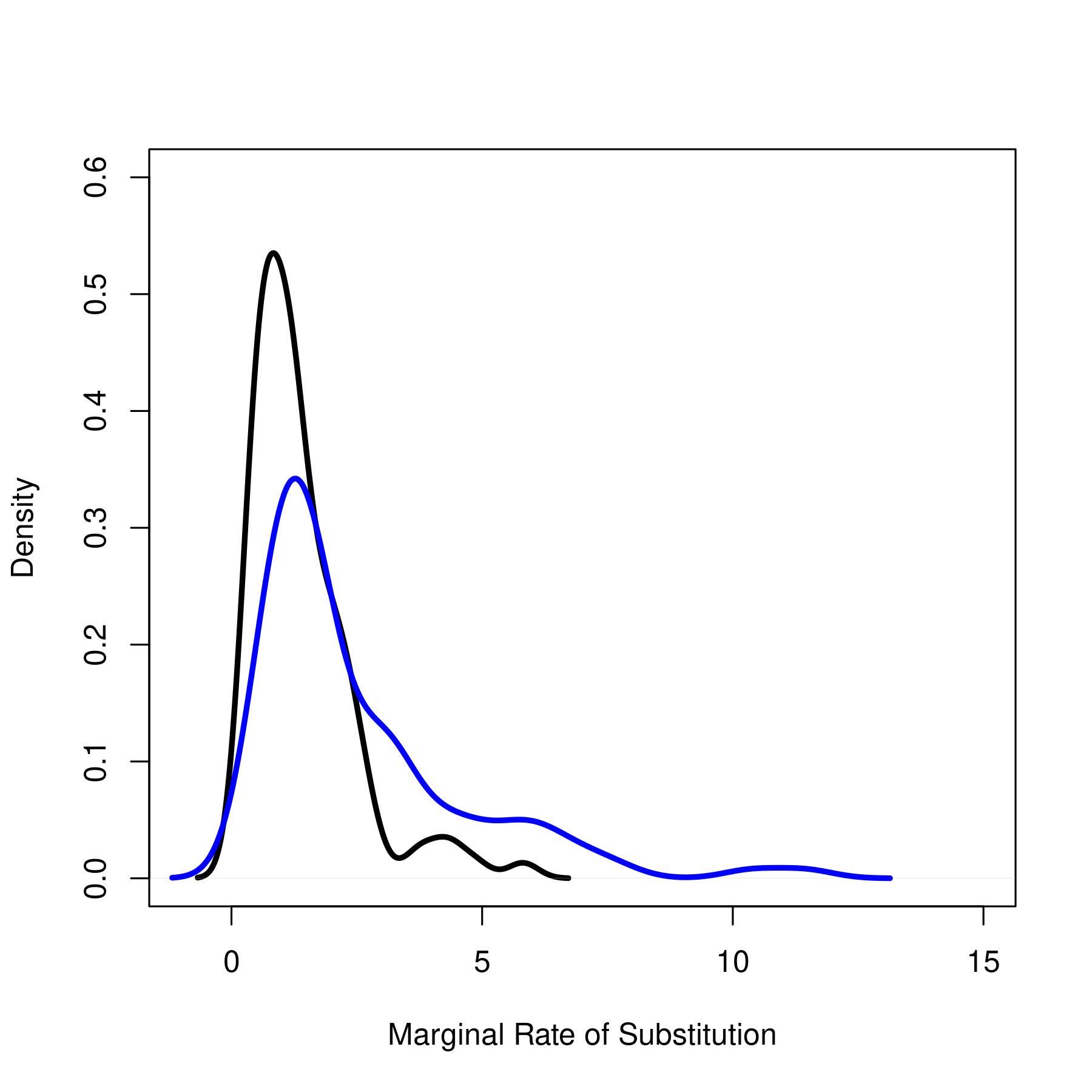

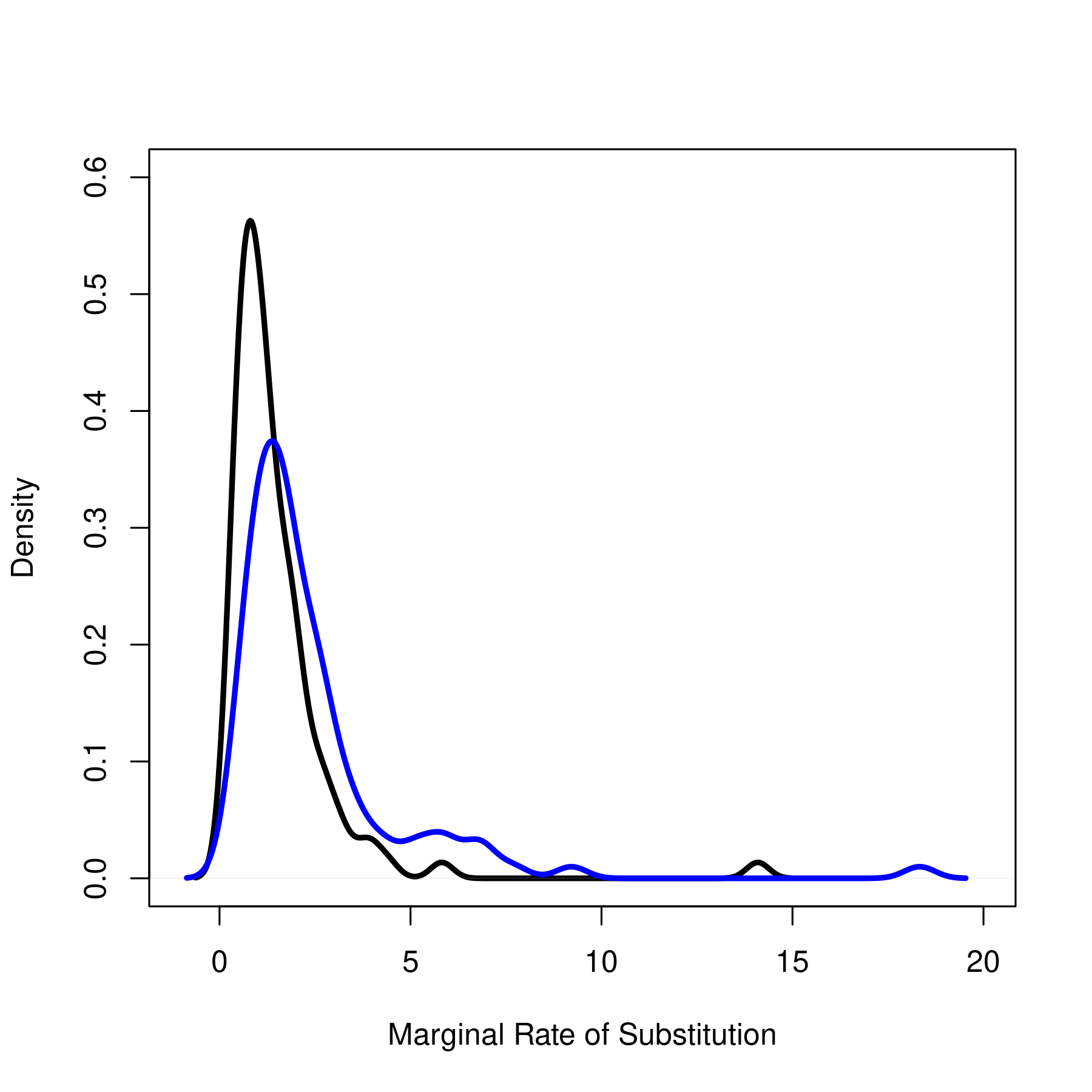

This analysis has to be completed with a discussion of accuracy. In this non-param- etric framework, the posterior distributions of and are infinite-indimesional and cannot be represented. However, posterior distributions of any scalar transformation of and can be derived using simulation. In this respect, it is important to know which scalar objects are of interest. Typically, we are interested in the MRS evalu- ated at a specific bundle, say , or counterfactual demand, corresponding to a particular design, say . Figure 13 displays the posterior distributions of the MRS, evaluated at two bundles, and , for California and Florida. In both states, these distributions are approximately log-normal (with is consistent with Dobronyi and Gouriéroux, 2020), and the posterior for has a much longer tail than the posterior for , implying that, the quantity of good 2 that must be given to the consumer in order to compensate her for one unit of good 2 (and keep her just as happy) is larger, on average, when she has more of good 2. This tail is longer in California.

The filtered taste distributions in Figure 12 are obtained by applying the algorithm in Appendix C and forcing the density to be non-negative at each iteration. The existence of negative “probabilities” can be a result of numerical uncertainty, the choice of grid, or misspecification. Specifically, it can arise if the consumer in segment does not maximize her SARA/SSF utility function (or any utility function) subject to the linear budget constraint. By analyzing these negative probabilities, we can construct a measure of the deviation from rationality. To illustrate, let and , respectively, denote the positive and negative components of the elementary probability associated with the grid point. The following ratio:

| (6.9) |

is a measure of bounded rationality. This ratio ranges between 0 and 1. The closer this ratio is to 1, the less compatible the data are with the hundreds of MRS restrictions imposed by the chosen model. This ratio is related to a subset of the literature conce- rned with such measures. Existing measures include Afriat’s Efficiency Index (Afriat, 1967; Varian, 1990), and the Money Pump Index (Echenique et al., 2011). In general, these indices are used to measure a single consumer’s deviation from rationality by evaluating how “close” her choices are to satisfying the Generalized Axiom of Revealed Preference (GARP), a necessary and sufficient condition for a finite number of choices to be consistent with the maximization of any locally non-satiated utility function. In our framework, the BR ratio can be used to measure the violation of the homogeneous segment assumption. Table 3 displays the BR ratios for California and Florida. The BR ratio for is smaller than the ratio for in each state; these ratios are roughly the same across states.

| State | ||

|---|---|---|

| California | 0.15 | 0.20 |

| Florida | 0.17 | 0.21 |

7 Concluding Remarks

This paper is one among pioneering papers attempting to tackle the challenges of performing structural demand analysis with scanner data (see also Burda et al., 2008, 2012, Crawford and Polisson, 2016, Guha and Ng, 2019, Chernozhukov et al., 2020, and \hyper@linkcitecite.dobronyi\@extra@b@citebDobronyi and Gouriéroux, 2020). The recent availability of scanner data permits new developments in the analysis of consumer behaviour. Here, we have shown that, by introducing homogeneous segments of consumers, we can consider a model of consumption with non-parametric preferences and infinite-dimensional heterogeneity, not only from a theoretical point-of-view, but also from a practical one. The distribution of individual heterogeneity in the population can be estimated, and the underlying non-parametric preferences can be filtered by using appropriate algorithms.

We developed an analysis for two goods for exposition. This feature of our analysis leaves the question: Can the methods developed in this paper be extended to a framework with, say, 100 goods? A completely unconstrained non-parametric analysis wou- ld encounter the curse of dimensionality. Specifically, we would need to estimate the distribution of the utility function (a non-parametric function with, in this scenario, 100 arguments). This task would be infeasible, even in our big data framework. But, the SARA model with independent taste parameters is a constrained non-parametric model. The structure of the SARA model reduces the non-parametric dimension of the problem, making it feasible. Indeed, when taste parameters are independent, we only need to estimate 100 one-dimensional distributions. A similar remark applies to the algorithm used to filter the taste distributions: The two steps based on the bilinear form of the MRS restrictions in a two good setting can be replaced with 100 successive steps based on the multilinear form of MRS restrictions in a 100 good setting, without increasing the numerical complexity.

Many of the results in this paper require taste parameters to be independent, but this requirement can be relaxed. For example, we can always consider a SARA model with the following form:

| (7.1) |

where is a common component, and is a good-specific taste parameter, for each . In such a framework, independence between , , and does not imply independence between the parameters:

| (7.2) |

but it does reduce the dimensionality of the problem: Instead of introducing a joint distribution on a space of dimension 2, the model only depends on three distributions on a space of dimension 1. This specification avoids the curse of dimensionality. (See Appendix E for a discussion of identification in this case with taste dependence.)

In this paper, consumers are assumed to be rational, and divided into homogeneous segments. Since, in each segment, the demand function can be non-parametrically estimated over a subset of its domain, the analysis can be continued to develop a test of the homogeneity of each segment, or, more generally, a non-parametric method for constructing homogeneous segments.

The approach developed in this paper uses standard ideas from consumer theory to make inference. This approach is appropriate when both quantities and prices have continuous supports. This feature makes this approach valid for some levels of good, consumer, and date aggregation. Hence, this approach can be used for, say, evaluating the effect of alcohol tax on alcohol consumption, but unreasonable for analyzing how a particular consumer will choose between hundreds of different brands of whiskey. To our knowledge, the tools needed to solve such a problem have not been developed yet.

References

- Afriat (1967) Afriat, S. (1967): “The Construction of Utility Functions from Expenditure Data,” International Economic Review, 8, 67–77.

- Alley et al. (1992) Alley, A., D. Ferguson, and K. Stewart (1992): “An Almost Ideal Demand System for Alcoholic Beverages in British Columbia,” Empirical Economics, 17, 401–418.

- Asmussen et al. (2016) Asmussen, S., J. Jensen, and L. Rojas-Nandayapa (2016): “On the Laplace Transform of the Lognormal Distribution,” Methodology and Computing in Applied Probability, 18, 441–458.

- Banks et al. (1997) Banks, J., R. Blundell, and A. Lewbel (1997): “Quadratic Engel Curves and Consumer Demand,” The Review of Economics and Statistics, 79, 527–539.

- Barten (1968) Barten, A. (1968): “Estimating Demand Equations,” Econometrica, 36, 213–251.

- Beckert and Blundell (2008) Beckert, W. and R. Blundell (2008): “Heterogeneity and the Non-Parametric Analysis of Consumer Choice: Conditions for Invertibility,” The Review of Economic Studies, 75, 1069–1080.

- Bergstra and Yoshua (2012) Bergstra, J. and Y. Yoshua (2012): “Random Search for Hyper-Parameter Optimization,” Journal of Machine Learning Research, 13, 281–305.

- Blaschke and Pick (1916) Blaschke, W. and G. Pick (1916): “Distanzschätzungen im Funktionenraum II,” Mathematische Annalen, 77, 277–302.

- Blomquist et al. (2015) Blomquist, S., A. Kumar, C. Liang, and W. Newey (2015): “Individual Heterogeneity, Nonlinear Budget Sets, and Taxable Income,” CESifo Working Paper.

- Blundell et al. (2017a) Blundell, R., J. Horowitz, and M. Parey (2017): “Nonparametric Estimation of a Nonseparable Demand Function under the Slutsky Inequality Restriction,” The Review of Economics and Statistics, 99, 291–304.

- Blundell et al. (2017b) Blundell, R., D. Kristensen, and R. Matzkin (2017): “Individual Counterfactuals with Multidimensional Unobserved Heterogeneity,” CeMMAP Working Paper.

- Brown and Walker (1989) Brown, B. and M. Walker (1989): “The Random Utility Hypothesis and Inference in Demand Systems,” Econometrica, 57, 815–829.

- Brown and Matzkin (1995) Brown, D. and R. Matzkin (1995): “The Random Utility Model from Data on Consumer Demand,” Discussion Paper, Yale University.

- Burda et al. (2008) Burda, M., M. Harding, and J. Hausman (2008): “A Bayesian Mixed Logit-Probit Model for Multinomial Choice,” Journal of Econometrics, 147, 232–246.

- Burda et al. (2012) ——— (2012): “A Poisson Mixture Model of Discrete Choice,” Journal of Econometrics, 166, 184–203.

- Chernozhukov et al. (2020) Chernozhukov, V., J. Hausman, and W. Newey (2020): “Demand Analysis with Many Prices,” Working Paper.

- Christensen et al. (1975) Christensen, L., D. Jorgenson, and L. Lau (1975): “Transcendental Logarithmic Utility Functions,” The American Economic Review, 65, 367–383.

- Crawford and Polisson (2016) Crawford, I. and M. Polisson (2016): “Demand Analysis with Partially Observed Prices,” University of Leicester Working Paper, 15/12.

- Deaton and Muellbauer (1980) Deaton, A. and J. Muellbauer (1980): “An Almost Ideal Demand System,” The American Economic Review, 70, 312–326.

- Dette et al. (2016) Dette, H., S. Hoderlein, and N. Neumeyer (2016): “Testing Multivariate Economic Restrictions Using Quantiles: The Example of Slutsky Negative Semidefiniteness,” Journal of Econometrics, 191, 129–144.

- Dobronyi and Gouriéroux (2020) Dobronyi, C. and C. Gouriéroux (2020): “Stochastic Revealed Preference: A Non-Parametric Analysis,” Working Paper.

- Echenique et al. (2011) Echenique, F., S. Lee, and M. Shum (2011): “The Money Pump as a Measure of Revealed Preference Violations,” Journal of Political Economy, 119, 1201–1223.

- Feller (1968) Feller, W. (1968): An Introduction to Probability Theory and its Applications, vol. 2, Wiley.

- Ferguson (1974) Ferguson, T. (1974): “Prior Distributions on Spaces of Probability Measures,” The Annals of Statistics, 2, 615–629.

- Geweke (2012) Geweke, J. (2012): “Nonparametric Bayesian Modelling of Monotone Preferences for Discrete Choice Experiments,” The Journal of Econometrics, 171, 185–204.

- Gouriéroux and Monfort (1996) Gouriéroux, C. and A. Monfort (1996): Simulation-Based Econometric Methods, New York: Oxford University Press.

- Gouriéroux et al. (1990) Gouriéroux, C., A. Monfort, and E. Renault (1990): “Bilinear Constraints: Estimation and Tests,” Essays in Honor of Edmond Malinvaud, Empirical Economics, MIT Press, 166–191.

- Grant (1995) Grant, S. (1995): “A Strong (Ross) Characterization of Multivariate Risk Aversion,” Theory and Decision, 38, 131–152.

- Guha and Ng (2019) Guha, R. and S. Ng (2019): “A Machine Learning Analysis of Seasonal and Cyclical Sales in Weekly Scanner Data,” NBER 25899.

- Halevy and Feltkamp (2005) Halevy, Y. and V. Feltkamp (2005): “A Bayesian Approach to Uncertainty Aversion,” Review of Economic Studies, 72, 449–466.

- Hausman and Newey (2016) Hausman, J. and W. Newey (2016): “Individual Heterogeneity and Average Welfare,” Econometrica, 84, 1225–1248.

- Heyde (1963) Heyde, C. (1963): “On a Property of the Lognormal Distribution,” Journal of the Royal Statistical Society Series B: Methodological, 29, 16–18.

- Hosoya (2016) Hosoya, Y. (2016): “On First-Order Partial Differential Equations: An Existence Theorem and its Applications,” Advances in Mathematical Economics, 20, 77–87.

- Hurwicz and Uzawa (1971) Hurwicz, L. and H. Uzawa (1971): “On the Integrability of Demand Functions,” in Preferences, Utility, and Demand: A Minnesota symposium, New York, chap. 6, 114–148.

- Johansen (1969) Johansen, L. (1969): “On the Relationships Between Some Systems of Demand Functions,” Liiketaloudellinen Aikakauskirga, 1, 30–41.

- Johansen (1974) Johansen, S. (1974): “The Extremal Convex Functions,” Mathematica Scandinavica, 34, 61–68.

- Karni (1979) Karni, E. (1979): “On Multivariate Risk Aversion,” Econometrica, 47, 1391–1401.

- Karni (1983) ——— (1983): “On the Correspondence Between Multivariate Risk Aversion and Risk Aversion with State-Dependent Preferences,” Journal of Economic Theory, 30, 230–242.

- Katzner (1968) Katzner, D. (1968): “A Note on the Differentiability of Consumer Demand Functions,” Econometrica, 36, 415–418.

- Kitamura and Stutzer (1997) Kitamura, Y. and M. Stutzer (1997): “An Information-Theoretic Alternative to Generalized Method of Moments Estimation,” Econometrica, 65, 861–874.

- Kotz et al. (2000) Kotz, S., N. Balakrishnan, and N. Johnson (2000): Continuous Multivariate Distributions, Volume 1: Models and Applications, New York: Wiley, 2nd ed.

- Ledoit and Wolf (2004) Ledoit, O. and M. Wolf (2004): “A Well-Conditioned Estimator for Large-Dimensional Covariance Matrices,” Journal of Multivariate Analysis, 88, 365–411.

- Li et al. (2019) Li, Y., E. Schofield, and M. Gönen (2019): “A Tutorial on Dirichlet Process Mixture Modeling,” Journal of Mathematical Psychology, 91, 128–144.

- Lin (2016) Lin, J. (2016): “On the Dirichlet Distribution,” Queens University, Kingston.

- Manning et al. (1995) Manning, W., L. Blumberg, and L. Moulton (1995): “The Demand for Alcohol: The Differential Response to Price,” Journal of Health Economics, 14, 123–148.