A Sparse Beta Regression Model for Network Analysis

Abstract

Network data are ubiquitous in modern science and humanity. This paper concerns a new generative model, suitable for sparse networks commonly observed in practice, to capture degree heterogeneity and homophily, two stylized features of a typical network. The former is achieved by differentially assigning parameters to individual nodes, while the latter is materialized by incorporating covariates. Similar models in the literature for heterogeneity often include as many nodal parameters as the number of nodes, leading to over-parametrization. For parameter estimation, we use the penalized likelihood method with an penalty on the nodal parameters, immediately connecting our estimation procedure to the LASSO literature. We highlight the differences of our approach to the LASSO method for logistic regression, emphasizing the feasibility of our model to conduct inference for sparse networks, study the finite-sample error bounds on the excess risk and the -error of the resulting estimator, and develop a central limit theorem for the parameter associated with the covariates. Simulation and data analysis corroborate the developed theory. As a by-product of our main theory, we study what we call the Erdős-Rényi model with covariates and develop the associated statistical inference for sparse networks, which can be of independent interest.

Key words: -model, asymptotic normality, consistency, degree heterogeneity, excess risk, homophily, LASSO, sparse networks.

1 Introduction

Network data are ubiquitous in today’s society thanks to unprecedented advances of data collection techniques. This paper concerns a new generative model to simultaneously capture degree heterogeneity and homophily, two stylized features of a typical network (Kolaczyk, 2009; Newman, 2018). The former refers to the fact that the nodes of a network differ, sometimes drastically, in their propensity in making connections, while the latter states that similar nodes are more likely to attach to each other than dissimilar ones, based on node attributes or covariates. Above all, our model is designed for sparse networks, which we define as networks in which the total number of connections can scale sub-quadratically in the order of with respect to , the number of nodes. A network is called dense otherwise. As is standard in the literature, the properties of our network model are studied under the setting where goes to infinity.

To fix ideas, assume that we have observed data organized as , where is the adjacency matrix with if node and are connected and otherwise, and are -dimensional covariates associated with these two nodes. Our model assumes that links are independently made with the probability of a connection between node and being

| (1) |

where with associated with the th node is the heterogeneity parameter, is the parameter for the covariates, and is a parameter common to all the nodes. For identifiability, we assume , so that with . Central to our model is the idea that the vector is sparse, although we do not assume that its support is known. If for all , model (1) becomes the Erdős-Rényi model with covariates as discussed in Section 2.3 for which we can handle very sparse networks. If a node contains ’some signal’, a positive parameter implies that it will be better connected than the baseline nodes whose parameters equal zero. Our model is a generalization of the sparse -model (SM) proposed in Chen et al. (2021) that does not consider covariates. As such, we name our model sparse -regression model or SRM for short. Below we highlight informally the main features of this new model:

-

1.

The parameter can be interpreted as the global density parameter of the network and is allowed to diverge to . As a result, can go to . In this sense, SRM is well suited for modeling sparse networks commonly seen in practice.

-

2.

The parameter can be understood as the local density parameter, where is a heterogeneity parameter distinguishing how node participates in network formation. Assuming a sparse allows us to differentially assign non-zero local parameters only to those nodes active in making connections, thus avoiding over-parametrization due to the number of the parameters in . In the most extreme case when is a zero vector, we will have a logistic regression model. The logistic regression in our context is different to the usual logistic regression model because we allow to go to . Details of this special case are presented in Section 2.3.

-

3.

The parameter can be seen as the covariate parameter to capture the effect of the covariate for initiating connections. Here can be either node-similarities or edge-covariates. For the former, one popular approach is to construct using and , the nodal covariates at node and that can be multivariate. For example, we can define , where is a function of its arguments. One possible choice of is , or some other metric, for measuring the similarity between node and . For this case, is a scalar parameter for characterizing the tendency of two similar nodes making a connection and a positive indicates homophily. Another choice is , the vector of absolute differences of and , where takes the role of weighting the importance of each covariate.

Our model is high-dimensional with unknown parameters, where the heterogeneity parameter admits a sparse representation with an unknown support. This fact immediately motivates the use of a penalized likelihood approach for estimation. A first idea is to employ an penalty on as in Chen et al. (2021) for SM when no covariates are considered. However, their argument for developing a computationally efficient algorithm is no longer applicable. This leads us to the use of an penalty on , where our estimator is obtained by solving

| (2) |

where is the negative log-likelihood defined in (3), is a tuning parameter, and is the -norm of . This formulation immediately connects our approach to the LASSO methodology (Tibshirani, 1996) developed for variable selection, enabling us to draw upon the vast literature on high-dimensional data analysis, especially for logistic regression.

We highlight that the model in (1) is sparse in terms of its parametrization and the density of the resulting network. The word sparse in SRM refers to the former. The latter is a natural consequence of the sparse representation of the parameter. For example, when is sparse with a finite support, by allowing to grow to at appropriate rates, the networks generated from this model will be sparse. When where is a zero vector of dimension , we show in Section 2.3 that this special version of SRM can model any network whose expected number of edges scales as with . That is, the network modeled by this special case of SRM can be almost arbitrarily sparse.

1.1 Main contributions

Our methodological contribution comes from proposing the SRM as the first model capable of capturing node heterogeneity differentially while accounting for covariates in the presence of network sparsity. In the literature, closely related models allowing node-specific parameters either ignore covariates and thus homophily (Chen et al., 2021), or overly parametrize by assigning parameters indistinguishably to all the nodes (Chatterjee et al., 2011; Graham, 2017; Yan et al., 2019, e.g.), leading to theoretical and practical difficulties in applying these models; See Chen et al. (2021) for some discussion.

Our first theoretical contribution is to analyze the performance of our estimator by establishing its consistency in terms of excess risk and -norm. Despite the somewhat superficial similarity of our estimator to the penalized logistic regression with an penalty, great care needs to be taken when applying results from LASSO theory to our estimator. Firstly, the design matrix of our model associated with is deterministic while that with is random, making the common assumptions made on the eigenvalues of the design matrix typically seen in LASSO not applicable. Furthermore, our approach differs from classical LASSO theory for logistic regression insofar that we do not assume that the linking probabilities between two nodes stay uniformly bounded away from zero, because otherwise the network will be dense. This assumption is often made in LASSO theory; see, for example, van de Geer & Bühlmann (2011), Theorem 6.4; Buena (2008), Theorem 2.4; or van de Geer (2008), Theorem 2.1. To our best knowledge, we are not aware of similar conditions explicitly stated in the literature, at least not to a model similar to ours. Importantly, our approach differs from classical LASSO theory in that the various parameters in the SRM have differing effective sample sizes, resulting in different rates of convergence. Loosely speaking, the effective sample size for each depends on the number of possible connections that the th node has, while and are both global parameters depending on the total number of edges. Remarkably, we recover almost the classical LASSO rate of convergence for excess risk and -error, up to an additional factor having an explicit relation to the expected edge density of a network, which is the price to pay for allowing vanishing link probabilities.

For statistical inference, the homophily parameter is often of major interest, as the heterogeneity parameter can be seen as nuisance. Our second theoretical contribution is to provide a central limit theorem for in the face of vanishing link probabilities. Remarkably, we show that this theorem holds without the need to apply the kind of debiasing usually required for LASSO estimators due to shrinkage (Zhang & Zhang, 2014). Crucially, inference for LASSO type estimators relies on finding a good approximation to the precision matrix, the inverse of the population Gram matrix, which can be challenging. In particular, it is routinely assumed in the proof of LASSO inference results that the minimum eigenvalue of the Gram matrix is bounded away from zero, uniformly in (van de Geer et al., 2014, e.g.). In our case, however, this matrix depends on the link probabilities and since we allow for many and , such a uniform lower bound assumption becomes invalid. Remarkably, we can overcome this difficulty as long as rates are chosen carefully. The ability to conduct inference with an asymptotically non-invertible Gram matrix and vanishing link probabilities is a significant improvement over many existing methods and a prerequisite for dealing with sparse networks.

As byproducts of our theory, we provide the theory for two special cases of SRM. First, we provide results analogous to Chen et al. (2021) in Section 2.2 when covariates are not considered, by replacing the -penalty on in SM by an -penalty. We also consider a simplified model of SRM in Section 2.3 when the heterogeneity parameter is not present, i.e. when , and present asymptotic normality results for its maximum likelihood estimator (MLE). We remark that the setup in the latter case is different to the usual logistic regression as we allow the global density parameter to diverge to and thus allow for sparse networks. The model studied in Section 2.3 can be seen as an extension of the Erdős-Rényi model by incorporating covariates, with an emphasis to model those networks that are sparse. This model does not appear analyzed previously and can be of independent interest.

From a computational viewpoint, the similarity between our formulation and LASSO logistic regression enables us to invoke standard algorithms developed for the latter, and thus the estimation of our model parameters can be done extremely fast. Our final contribution is to demonstrate the usefulness of our model via extensive numerical simulation and two real data applications.

1.2 Prior work

Real-world networks are often found to be sparse, with nodes exhibiting different numbers of links and nodes similar in attributes more likely to connect, among many other features. To understand the stochastic nature of these data, statistical analysis of networks has seen an increasing research interest in both theory and applications (Kolaczyk, 2009; Goldenberg et al., 2009; Fienberg, 2012; Kolaczyk, 2017).

The SRM becomes the Erdős-Rényi model if the heterogeneity and covariate parameters are absent (Erdős & Rényi, 1959, 1960; Gilbert, 1959). To generalize the Erdős-Rényi model to include degree heterogeneity, one intuitive idea is to assign node-specific parameters, one for each node. This gives rise to the -model which can be dated back to Holland & Leinhardt (1981) and has been thoroughly studied by Chatterjee et al. (2011) who proved the consistency of its MLE. Yan & Xu (2013) further proved the asymptotic normality of that MLE. See also Rinaldo et al. (2013), Karwa & Slavković (2016) and Yan, Qin & Wang (2016) for further results, and Yan, Leng & Zhu (2016) for a directed version of the -model. Since the -model associates each node with its own parameter, they are over-parametrized. To overcome this, Chen et al. (2021) proposed a sparse -model (SM) by assuming that a subset of the node-specific parameters are zero, while Zhang et al. (2021) applied a ridge penalty on the parameters. Another popular idea for incorporating degree heterogeneity is to assume that nodes in a network can be clustered into communities that share same connection patterns. This gives rise to the so-called stochastic block model (SBM); see Holland et al. (1983) for its formalization and Abbe (2018) for a review and recent developments.

Modeling the tendency for similar nodes to link up, also known as homophily, is best achieved by including covariates. For the -model, Graham (2017) first included nodal-covariates, giving rise to a models similar to (1) but with a dense . See Jochmans (2018) for further results and Yan et al. (2019) for a generalization to directed networks. For the SBM with covariates, Huang & Feng (2018) considered spectral clustering with adjustment, Binkiewicz et al. (2017) applied a modification of spectral clustering, Zhang et al. (2016) proposed to use a joint community detection criterion, while Yan & Sarkar (2021) resorted to convex relaxation that can be used for sparse networks.

Our estimation is closely connected to the LASSO methodology (Tibshirani, 1996), especially that developed for generalized linear models (van de Geer, 2008; Buena, 2008). For inference for LASSO type of estimators, it is found that debiasing is necessary to overcome the bias caused by shrinkage (Zhang & Zhang, 2014; van de Geer et al., 2014). One contribution of this work is that debiasing is shown to be not necessary for inference of the covariate parameter under suitable conditions.

1.3 Notations and the plan of the paper

We introduce the notations used in this paper. A network on nodes is represented as an undirected graph , consisting of a node set with cardinality and an edge set , which is a subset of all the two-element subsets of . We assume that the graphs studied are simple. Thus given a graph , we can identify it with a binary adjacency matrix , where , if and otherwise. We write as the degree of node , as the degree sequence, and as the total number of edges. By we mean for two sequences of positive numbers and . We call a network sparse if for some , where is the expectation with regard to the data generating process. A network is dense if .

For a vector , we use to denote its support and as the cardinality of . Let denote the vector -, - and -norm respectively. For any subset , we denote by the vector with components not belonging to set to zero. For convenience of notation, when dealing with a vector , we will number its elements as . Also, for any square matrix , we denote by its maximum eigenvalue and by its minimum eigenvalue. We use for some generic, strictly positive constant that may change between displays. For brevity, we denote the set of parameters collectively as and its true value as . We write as the support of . For ease of presentation, we introduce the shorthand notation and with cardinality to refer to all active indices including and .

The rest of the paper is structured as follows. In Section 2, we introduce the SRM and derive the consistency of the estimator in (2) in terms of excess risk and -norm. We then zoom in on two special cases of SRM. In Section 2.2, we show how the results from Section 2.1 can be applied to the SM without covariates. This is the model studied in Chen et al. (2021) where the parameters are estimated by penalizing the -norm of . Section 2.3 presents the theory for SRM when the heterogeneity parameter is not present. In Section 3, we derive a central limit theorem for our estimator of the homophily parameter without debiasing. We present extensive simulation results in Section 4 and apply our model to a friendship network of a corporate law firm and the world trade network in Section 5. Conclusion remarks are presented in Section 6. All the proofs are relegated to the Appendix.

2 Sparse -Regression Model

Recall the SRM as defined in (1). Given an observed adjacency matrix and the associated covariates , the negative log-likelihood of the model is seen as

| (3) |

Since is assumed sparse, it may be tempting to estimate the parameters of the model via the following regularized likelihood by penalizing the norm of

For the sparse -model without covariates, Chen et al. (2021) found that this non-convex optimization problem is computationally tractable, thanks to a key monotonicity lemma. The arguments leading to the conclusion of this lemma, however, do not extend to the current setting where covariates are included. This effectively means that the -norm penalized likelihood becomes a combinatorial problem for the SRM and an exhaustive search, which is computationally intractable, in the model space is inevitable. The above discussion is reminiscent of the familiar all best-subset selection procedure in regression.

One approach popular in high-dimensional data analysis is to replace the penalty on by its penalty, leading to our proposed estimation procedure in (2). An attractive feature of this formulation is that the resulting objective function is convex. On the computational side, the formulation in (2) is the same as penalized logistic regression with the LASSO penalty. Thus, to solve it in practice, we can use existing algorithms developed for LASSO and in particular, we can use the functions in the glmnet R package (Friedman et al., 2010) by properly setting up the design matrix and the constraints on . Our experience shows that this algorithm can effectively compute the estimator for a network with the number of nodes up to a few thousand. We remark that more scalable algorithms can be explored by exploiting the special structure of the design matrix for in (3).

In this paper, we focus on the finite-dimensional covariate case by assuming that , the dimension of the covariates , is fixed. We assume that are independent realizations from centered, uniformly bounded random variables. We do not require to be i.i.d. and may have correlated entries. These assumptions imply in particular, that there exist constants such that for all and for all . We assume further that , the homophily parameter associated with , lies in a compact, convex set , which means we may choose a universal independent of . Recalling the notation , we let denote the parameter space.

2.1 Theory

Since we aim to develop a theory for sparse networks, we allow to go to as tends to infinity. As a result, as , some link probabilities may go to zero as tends to infinity. In order to perform consistent estimation, it is clear that we need to restrict the rate at which probabilities may go to zero. Therefore, we assume that there is a non-random sequence as , such that almost surely for all :

Since a smaller allows sparser networks, we refer to as the network sparsity parameter. It effectively characterizes the maximum permissible sparsity of our network. Applying to the inequality above we get for all

which is equivalent to

Note that since , we have . The previous inequality can also be expressed in terms of the design matrix associated with the corresponding logistic regression problem, for which we give an explicit formula in (6) below, and is equivalent to This motivates the following estimation procedure: Given a sufficiently large constant , we define the local parameter space

| (4) |

and propose to perform estimation via

| (5) |

where is a tuning parameter. As we have seen in the equations above, any used in the definition of corresponds to some , which uniformly lower bounds the connection probability and thus can be seen as a proxy for the sparsity of our network. This type of restriction of the parameter space is similar to what was done in Chen et al. (2021), although they restricted the parameter values of and directly. The condition in (4) is slightly more general and somewhat more natural. Noting that is convex, we have a convex optimization problem in (5).

Note that, in (5), we replaced the condition by the less strict condition . The following Lemma, which is proved in Appendix A, shows that this is viable and that as long as the observed graph is neither empty nor complete and , a solution to (5) always exists and automatically fulfills .

Lemma 1.

Following the empirical risk literature (cf. Greenshtein & Ritov (2004), Koltchinskii (2011)) we will analyze the performance of our estimator in terms of excess risk. Define the (global) excess risk as

Since we define the local parameter space with respect to some rate , in our derivations we must account for the fact that this may be smaller than the true . In that case there is no way for us to find the true parameter and the best we can hope to achieve is to find the best local approximation of the truth , which we define as

Note that the truth fulfills

Hence, if , . In general, however, estimating is the best we can achieve when solving (5). Thus, we introduce the notion of local excess risk as in Chen et al. (2021), which measures how close a parameter is to the best local approximation in terms of excess risk:

Clearly, also fulfills and we may consider the excess risk of the best local approximation, , as the approximation error of our model. It accounts for the fact that our model might be misspecified, in the sense that the parameter is not large enough. As is usual in LASSO theory (cf. van de Geer & Bühlmann (2011), Chapter 6), it is tacitly assumed that this approximation error is small, i.e., we assume that is sufficiently large. Note that the global excess risk of our estimator decomposes as

where we can consider the approximation error as a deterministic bias. This is similar to the derivations in Chen et al. (2021).

As is commonly assumed in LASSO theory (cf. van de Geer & Bühlmann (2011), Chapter 6), we assume that the unpenalized parameters of are active. That is, . Denote the set of true active indices by with cardinality . For ease of notation, we introduce the set with cardinality to refer to all active indices including those of and .

We set up our problem in the language of LASSO theory for logistic regression. For each pair , denote by the vector containing one at the th and th position and zeros everywhere else. Define the matrices

Let be the vector containing only ones. Then the design matrix of (1) can be written as

| (6) |

where , consisting of the matrices and written next to each other, is the analogue to the design matrix in logistic regression. We number the rows of as . Here we see a crucial feature of our design matrix : While the parameters and appear in the link probability of all node pairs, each only appears in such probabilities. That means, while the effective sample size for and is , it is only for each entry of , i.e. it is of order smaller. This is also reflected in the different rates of convergence we obtain in Theorem 1 below.

A compatibility condition: A crucial assumption in LASSO theory is the so called compatibility condition (van de Geer & Bühlmann, 2011; van de Geer et al., 2014). It relates the quantities and

in a suitable sense made precise below and is crucial for deriving consistency results. Notice that the above quantity can be written as

where is the population Gram matrix of our design matrix . In the SRM however, the classical compatibility condition as for example defined for generalized linear models in van de Geer et al. (2014) does not hold. The reason for this is that and have different effective sample sizes. We need to account for this fact and therefore have to use a sample-size adjusted Gram matrix. To that end, we introduce the matrix

where is the identity matrix and we use 0 to denote the zero block matrix of appropriate dimensions. We now define the sample-size adjusted Gram matrix as

We consider the limit of the matrix entrywise.

We say the compatibility condition holds if the sample-size adjusted Gram matrix has the following property: There is a constant independent of such that for every with it holds that

To prove that has this property, we will use techniques similar to the ones used in Kock & Tang (2019). Their matrix structure is somewhat simpler than ours as they obtain an identity matrix where we obtain a special Toeplitz matrix. More precisely, we will first show that the compatibility condition holds for the matrix

To show that the compatibility condition also holds for , it will then suffice to show that and are close to each other in an appropriate sense. To this end, it is sufficient to impose the following eigenvalue restriction, which effectively quantifies how strongly the columns of may be correlated.

Assumption 1.

There are universal constants , independent of , such that for all , the minimum eigenvalue and the maximum eigenvalue of fulfil . Without loss of generality we assume .

We summarize these results in the following proposition which is proved in Appendix B.1.

Proposition 1.

Under Assumption 1, for and large enough, it holds that for every with ,

Proposition 1 requires . The large enough condition is made precise in the proof and requires that be such that , which is implied by and sufficiently large . Let us put this in the context of general LASSO theory. In general LASSO theory, to show that the -error goes to zero in probability for increasing , it is imposed that the sparsity of the true parameter fulfills

see for example van de Geer & Bühlmann (2011), Chapter 6. In our case the sparsity refers to and we thus should expect that the restrictions we have to impose on are based on the sample size associated with . To make our conditions on precise, define and let

| (7) |

Notice that essentially quantifies the approximation error we commit. We make the following assumption on .

Assumption 2.

.

That means, up to an additional factor – which is the price we have to pay for allowing our link probabilities to go to zero – the permissible sparsity for is the permissible sparsity in classical LASSO theory for an effective sample size of order . Clearly, assumption 2 is stronger than the condition in Proposition 1, which thus is not a major restriction.

In our proof, we reformulate our likelihood problem in the language of the sample size adjusted design matrix. This new formulation is entirely equivalent to the previous one in (5), but gives a different interpretation to the sample size adjusted Gram matrix. In particular, we introduce vectors and define

We may consider as a sample-size adjusted design matrix, in the sense that

Likewise, we re-define sample-size adjusted parameters. Here, we are effectively blowing up those columns of the design matrix corresponding to to compensate for the fact that has effective sample size of order smaller than and . The details can be found in Appendix B.2. Naturally, these changes will also result in a sample-size adjusted penalty parameter . For now, we simply remark that and refer the readers to Appendix B.2 for the details.

Theorem 1.

Theorem 1 has especially interesting implications if no approximation error is committed, that is in the case that .

Corollary 1.

Under the assumptions and with the definitions in Theorem 1, assume that no approximation error is made, i.e. . Then, with probability at least we have

with constant .

Corollary 1 gives us an explicit formula for how the sparsity of our network will affect our rate of convergence, which is particularly nice, since in many related works the conditions on network density enter the rate of convergence only indirectly as assumptions on the norm of the true parameter vector, see for example Chatterjee et al. (2011); Yan & Xu (2013). Also, notice that this is essentially the rate of convergence we would expect in the classical LASSO setting for logistic regression up to an additional factor . Let us consider the implications of Theorem 1 in more detail.

Note that . Hence, we may choose also of order . Recall that in the classical LASSO setting for logistic regression (cf. van de Geer & Bühlmann (2011)), when no approximation error is committed, when probabilities stay bounded away from zero and when we have the same effective sample size for each parameter, we obtain the rates

for the excess risk and

for the -error. In the setting of Corollary 1, we obtain

That is, up to an additional factor , we obtain the LASSO rate of convergence for sample size for the global excess risk. By the second line of the display above, we have immediately and at the rate expected from a LASSO type estimator with effective sample size (up to an additional factor). Furthermore, the third line implies that, again, up to an additional factor, for the error of , we obtain the rate of convergence we would expect for a LASSO type estimator with sample size . In particular, the assumptions we have to impose to obtain -consistency include the case , which is the condition that had to be imposed in the original -model for their strong consistency result (cf. Yan & Xu (2013), Theorem 1).

2.2 Sparse -model without covariates

By letting and consequently , the results for SRM derived in the previous sections have implications for the SM without covariates in Chen et al. (2021). In the case without covariates, the negative log-likelihood is given by

and our design matrix is simply The definitions of and do not change, as we can simply set in their original definitions. In this section we will abuse notation slightly by reusing the names from SRM, but redefining them to have the components corresponding to removed. For example, we will use for a generic parameter, to denote the truth, to denote the sparsity including the component etc. We think this is justified as it makes the connection to the respective objects in the model with covariates clearer. Our estimator reduces to

where by slight abuse of notation, for this section only, we define , for the reduced design matrix defined above and a rate .

We make definitions completely analogous to the case in which we observe covariates. We adapt the definitions of the excess risk in the canonical way by letting the components corresponding to and equal zero. We define the best local approximation as

and as before, we assume that all unpenalized parameters, i.e. in this case, are active. Since the sparsity assumptions of our parameter only concern , it is natural that we should need the same assumptions on as before, most notably Assumption 2. We have the analogue to Theorem 1:

Theorem 2.

A proof, which follows almost immediately from the case in which we do observe covariates, is given in Appendix B.7. It is interesting to put this result into context by comparing it with Theorem 2 in Chen et al. (2021). The parameter space over which Chen et al. (2021) are optimizing is not convex and the analogous notion of best local approximation we are using need not be well-defined in their setting. Thus, it is not possible to derive -error bounds for their estimator, as we do in Theorem 2. Nonetheless and quite remarkably, they are able to prove an existence criterion for their -constrained estimator and a high-probability, finite sample bound on its excess risk. To compare their results to ours, we consider a special case that they discuss at length. In particular, they consider the situation in which for some and for some and all , where and are such that . It is easy to see that under these assumptions we have . Consider the regime in which no approximation error is committed. Then, using an analogous argument as in the proof of Corollary 1, is of order . Recalling Assumption 2, we see that to obtain -consistency of our estimator, we need , which restricts the degree of network sparsity that our estimator can handle. Chen et al. (2021) need no such condition and only need to balance the global sparsity parameter with the local density parameter to have convergence of their excess risk to zero. This illustrates that to obtain our more refined consistency result in terms of -error, we understandably need to impose stricter assumptions on the permissible sparsity. We now compare the bounds on the excess risk. Note that Chen et al. (2021) scale their excess risk by , rather than as we do. To put the excess risk on the same scale, we denote by the excess risk rescaled to their setting. With this notation, we see that by Theorem 2 the error rate for the rescaled excess risk of our constrained estimator becomes

which by Assumption 2 is . From Chen et al. (2021), Theorem 2, it is seen that the rate for the excess risk of their constrained estimator is

This shows that in the regime necessary for -consistent parameter estimation, our estimator will always achieve a rate faster than the one in Chen et al. (2021). When we leave this regime, however, consistent estimation with respect to the -norm may no longer be possible and the estimator in Chen et al. (2021) can outperform our estimator.

2.3 SRM without

When , the linking probability in SRM becomes

| (9) |

which can be seen as a generalized Erdős-Rényi model with covariates incorporated. For this reason, we will abbreviate this model as ER-C.

We study the properties of the MLE of and under the sparse network regime. Towards this, following Chen et al. (2021), we encode the sparsity of the model (9) explicitly by assuming that a reparametrization of the global sparsity parameter takes the form

where effectively takes the role of from the previous sections and for a fixed independent of . To appreciate this reformulation, we see that the expected total number of edges of ER-C is of the order . When , ER-C becomes a standard logistic regression model with fixed parameters. It can generate arbitrarily sparse networks when . To the best of our knowledge, a model of this type that also accounts for covariates has not been studied in the literature before and thus the results below can be of independent interest.

We denote the true parameters and respectively. As in the previous section, we abuse notation slightly and denote a generic parameter as , the true parameter as and our estimator (defined below) as . We think this abuse of notation is justified as it allows a consistent notation with the other sections. We make the following assumptions.

Assumption 3.

The true parameter lies in the interior of .

Assumption 4.

The are i.i.d. realizations of the same random variable. The covariance matrix of , that is the matrix , is strictly positive definite with minimum eigenvalue .

Assumption 4 is analogue to Assumption 1 in the case with non-zero . We remark that the i.i.d. condition is used to simplify parts of the proofs and can be relaxed at the expense of lengthier proofs.

We consider the following function which is proportional to the negative log-likelihood of the ER-C up to a summand independent of the parameter

| (10) |

In the ER-C, the dimension of the parameter is fixed. Therefore, it is not necessary to employ a penalized likelihood approach as in the SRM and we estimate via maximum likelihood

| (11) |

where the argmin is taken over . The design matrix now takes the simplified form

As before, we enumerate the rows of as , where each is treated as a column vector, i.e. . Define the matrix as

which is invertible by Assumption 4. We have the following central limit theorem for , the proof of which can be found in Appendix D. Denote by the law of the multivariate normal distribution with zero mean vector and covariance matrix .

Since the expected number of observed edges in the ER-C is of order , the factor in Theorem 3 corresponds to the square root of the effective sample size. This means, having the link probabilities go to zero reduces the information we gain about and this information loss is made explicit in a rate of convergence slower than what we would obtain in a classical parametric setting. This finding is in line with the results in Chen et al. (2021), Proposition 1 and Theorem 1, in which a similar phenomenon was observed.

While we consider Theorem 3 to be interesting from a theoretical point of view, in practice, the sparsity rate parameter will not be known, which makes solving (11) and finding the MLE impossible. Remarkably, it is possible, though, to circumvent this problem with the following argument.

Notice that from Theorem 3 we obtain for any ,

where denotes the law of the univariate standard-normal distribution. We also may make use of the the identity

| (12) |

where is the MLE of the global sparsity parameter before reparametrization. In particular, can be found without knowledge of . Define the matrix

In Appendix D we show that , which in turn allows us to show for all . Then, by Slutzky’s theorem,

In other words, the matrix will be singular in the limit as the link probabilities go to zero. The rate is precisely the rate with which we need to multiply to stabilize it and make it converge to the non-singular matrix , whose inverse is the asymptotic covariance matrix in Theorem 3. Thus, the stabilizing rate for the asymptotic covariance and the sample size reducing rate will cancel out, allowing us to derive the component-wise limiting distribution of each without the knowledge of . In particular, looking at the case , we are able to calculate confidence intervals for the components of the covariate parameter without having to know . In summary, Theorem 3 allows the following corollary which is proved in Appendix D.

Corollary 2.

3 Inference for the Homophily Parameter

In this section we derive the limiting distribution for our estimator of the covariates weights when and thus . We will see that the same arguments used for deriving the limiting distribution for also work for and as a by-product of our proofs we also obtain an analogous limiting result for .

Our strategy will be inverting the KKT conditions, similar to van de Geer et al. (2014). The estimation in (5) is a convex optimization problem. Hence, by subdifferential calculus, we know has to be contained in the subdifferential of at . That is, there exists some such that

| (13) |

where is the gradient of evaluated at and for if and if , and for .

To ease notation a little we will use to refer to the unpenalized parameter subvector of . Thus, denoting the gradient of with respect to the unpenalized parameters only, evaluated at , we have

| (14) |

Denote by the Hessian of with respect to only, evaluated at . Denote . Now, consider the entries of . For all ,

where is the -th row of the design matrix , i.e. in particular if and for . In particular, we have the following matrix representation of . Let be the part of the design matrix corresponding to with rows . Also let . Then we have

Let and consider the corresponding population version:

To be consistent with commonly used notation, call and and

We will need to invert and and show that these inverses are close to each other in an appropriate sense. It is commonly assumed in LASSO theory (cf. van de Geer et al. (2014)) that the minimum eigenvalues of these matrices stay bounded away from zero. In our case, however, such an assumption is invalid.

Indeed, since , we find that for all , . Also, recall that by Assumption 1, the minimum eigenvalue of stays uniformly bounded away from zero for all . Then, for any and with components , we have

Hence, for finite all eigenvalues of are strictly positive and consequently this matrix is invertible. Using similar techniques as in the proof of Proposition 1 in the Appendix we can now show that with high probability the minimum eigenvalue of is also strictly larger than zero and thus for any and any finite (the exact derivations are given in Appendix C.1),

Thus, for every finite , is invertible with high probability. Since these lower bounds tend to zero with increasing , a careful argument is needed and we have to impose stricter assumptions than for our consistency result alone.

Assumption 5.

.

Assumption 5 is a slightly stricter version of the previously imposed Assumption 2. Previously we only needed a factor of to ensure that the -error for in Theorem 5 goes to zero. Notice, though, that these assumptions still allow sparsity rates for of small polynomial order. More precisely, up to a -factor and depending on the speed of , may still go to zero at a speed of order up to .

Theorem 4.

Remarkably, Theorem 4 does not require debiasing the estimates and for their inference, in comparison to the need for such for the usual LASSO estimates for other models due to the bias incurred by shrinkage (van de Geer et al., 2014). This bias is made explicit in equation (13): The penalized parameter values do not fulfill the first-order estimating equations exactly, but rather a bias of the form is incurred as prescribed by subdifferential calculus. While the unpenalized parameter estimates do fulfill the first-order estimating equations exactly, in standard settings this alone would still not be enough to ensure the asymptotic normality of . However, in our special case, due to the differing sample sizes between and , this is enough to allow us to derive a limiting distribution without a debiasing step. More precisely, deriving the limiting distribution of relies on a Taylor expansion of the negative log-likelihood . To derive Theorem 4, it is necessary, that in said Taylor expansion the bias incurred from the part of the likelihood relating to vanishes in probability. This essentially is a condition on the asymptotic correlation between the columns of the design matrix corresponding to and those corresponding to and . Due to each column in , the deterministic part of the design matrix relating to , being very sparse and having only non-zero entries, this bias vanishes fast enough to allow Theorem 4. See Appendix C.5 for details.

4 Simulation

4.1 SRM: Sparse -regression model

In this section we illustrate the finite sample performance of our penalized likelihood estimator with an extensive set of Monte Carlo simulations. We only show results for SRM and the estimator (5), as where applicable the results in the case without covariates are very similar. We check both the -convergence of our parameter estimates to the true parameter, as well as the asymptotic normality of by documenting the empirical coverage of confidence intervals.

Since our estimation involves the choice of a tuning parameter, we explored the use of the Bayesian Information Criterion (BIC) for model selection as well as a heuristic based on the theory developed in the previous sections to specify its value. While the former criterion is purely data-driven, the use of the latter is to ensure that our theoretical results are about right in terms of the rates. To make the dependence of our estimator (5) on the penalty parameter explicit, we denote the solution of (5) when using penalty by and write for its sparsity. The value of the BIC at is given by

and the penalty was chosen to minimize BIC.

To motivate the heuristic approach to tuning parameter selection, recall that Theorem 1 suggests that based on a confidence level picked by us, we should first define

and then based on that, choose as

Finally, the consistency results derived hold for any , where is the penalty parameter in the rescaled penalized likelihood problem, which relates to the penalty parameter in the original penalized problem (5) as . Looking back at the proof of Theorem 1, we see that the factor eight in the relation between and is a technical artifact we had to introduce to prove that the sample-size adjusted estimator as defined in Appendix B.2 was close enough to the sample-size adjusted best local approximation . If we assume that our estimator is close enough to the truth, we may ignore that factor and set . We pick and set to the maximum observed covariate value. It is known that in high-dimensional settings the penalty values prescribed by mathematical theory in practice tend to over-penalize the parameter values, see, for example, Yu et al. (2021). Decreasing the penalty by removing the factor eight is thus in line with these empirical findings.

For our simulation, we fixed by setting the covariate weights as and generated the covariates from a centered distribution as . We consider networks of sizes and in which the sparsity of is set as 7, 9, 10, and 12 respectively. We tested our estimator on three different model configurations with different combinations of and , resulting in networks with varying degrees of sparsity. For each simulation configuration, 1000 data sets are simulated. Specifically,

Model 1: We pick , where the number of ones increases with the network size to match the aforementioned sparsity level, and set ;

Model 2: We pick and set ;

Model 3: We pick and set .

In these three models, we allow to get progressively more negative to generate networks that are increasingly sparse, and allow the sparsity of to increase with network size . All three models get progressively sparser with increasing . Model 3 gives the sparsest networks when , with only around of all possible edges being present on average.

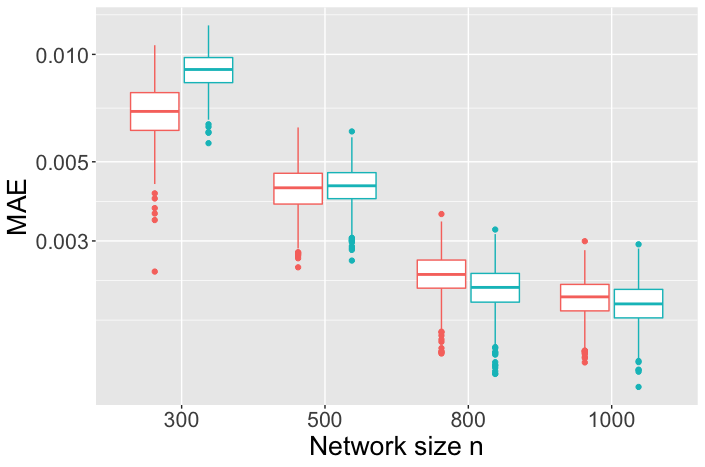

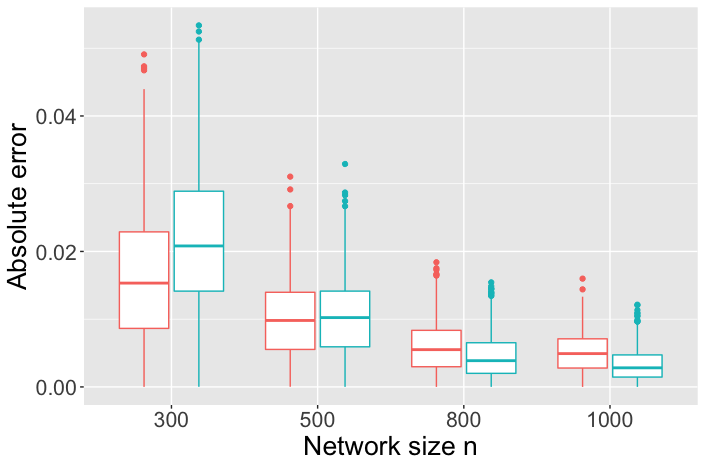

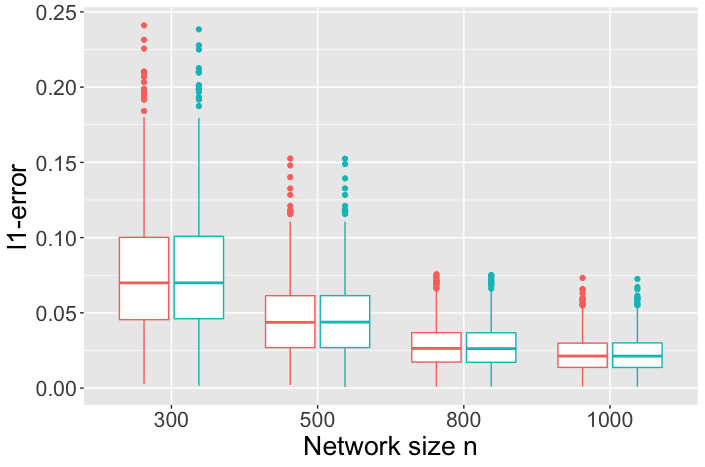

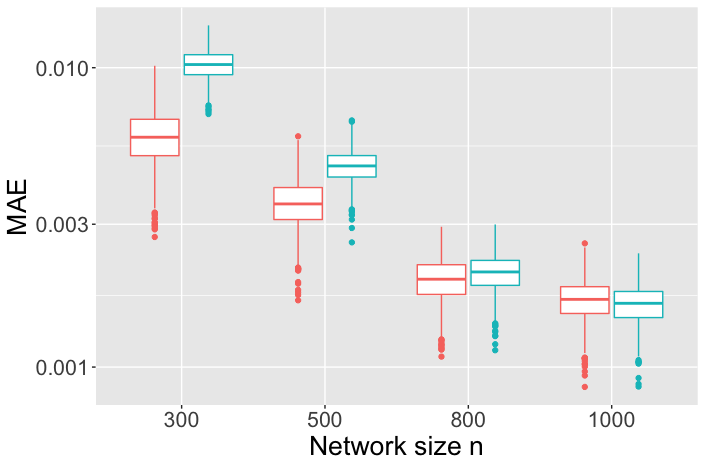

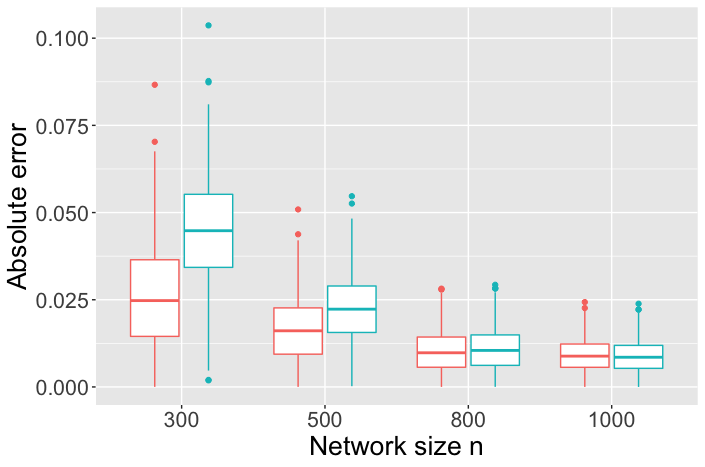

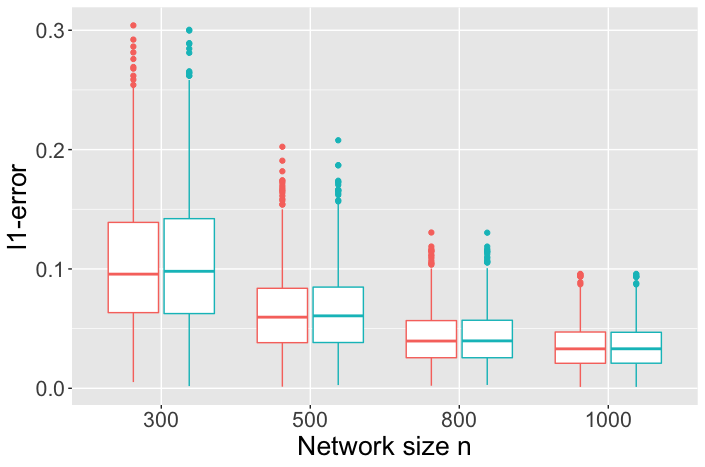

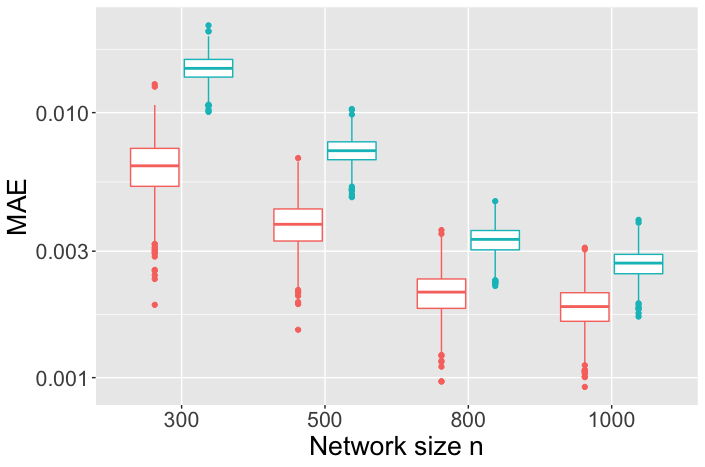

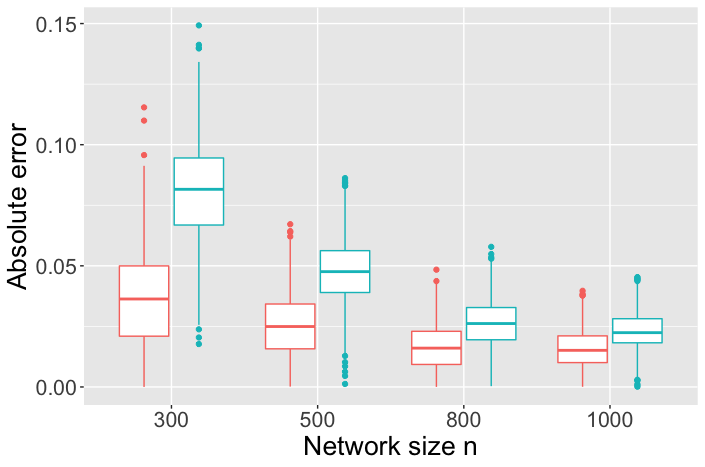

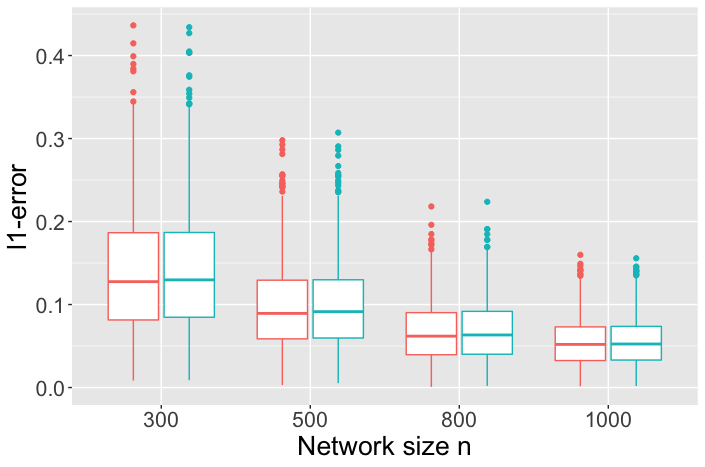

Consistency: We calculated the mean absolute error (MAE) for estimating , the absolute error for estimating and the -error for estimating . For Model 1 the results are shown in Figures 1(a)–1(c). While BIC performs slightly better for estimating and for smaller network sizes, our heuristic performs better for larger network sizes. The -error for estimating is almost the same between both model selection schemes across all network sizes. For both methods we can see that the various errors decrease with increasing network size. Model 2 gives similar results with slightly smaller errors produced by BIC for and for smaller networks and similar or slightly better errors produced by the heuristic for large networks (Figures 2(a), 2(b)). The error for is similar between both methods (Figure 2(c)). For Model 3, the various errors for parameter estimation are shown in Figures 3(a), 3(b) and 3(c). The error values are generally higher than in the other network models, which is to be expected due to the much higher sparsity of the network. Also, for this very sparse case, BIC is performing better than the heuristic. The heuristic consistently selects higher penalty values than BIC and we can see how this results in worse estimates for very sparse networks. Also, for the heuristic we choose one predefined penalty value for any network of a given size , while BIC can adapt to the observed sparsity. This illustrates the point made by Yu et al. (2021), that the penalty prescribed by mathematical theory tends to over-penalize the model. It is to be noted, though, that even in this very sparse regime both model selection techniques produce reasonable estimates that are close to the truth.

Asymptotic normality: Next, we consider the normal approximation for our estimator . We calculate the standardized -values

which by Theorem 4 asymptotically follow a distribution. This allows us to construct approximate -confidence intervals for as

where is the quantile of the standard-normal distribution and we use . We present the empirical coverage of these intervals and their median length for the different network sizes. Table 1 shows the results for across the different models and sample sizes. The results for are similar and are omitted to save space. The coverage is very close to the -level across all network sizes and all models and independent of which model selection criterion we use. This empirically illustrates the validity of the asymptotic results derived in Theorem 4. The median length of the confidence interval decreases with increasing network size and is similar between BIC and the heuristic. This is what we would expect since the estimates for are very similar between both methods as shown in Figures 1(c), 2(c), and 3(c). Comparing the length of the confidence intervals between Models 1, 2 and 3, we see that as the models become sparser, the median length increases, which is also to be expected.

| Coverage | CI | Coverage | CI | |||

| Pre-determined | BIC | |||||

| Model 1 | ||||||

| 300 | 0.949 | 0.182 | 0.950 | 0.182 | ||

| 500 | 0.944 | 0.110 | 0.944 | 0.110 | ||

| 800 | 0.953 | 0.069 | 0.954 | 0.069 | ||

| 1000 | 0.945 | 0.056 | 0.942 | 0.056 | ||

| Model 2 | ||||||

| 300 | 0.927 | 0.251 | 0.937 | 0.252 | ||

| 500 | 0.958 | 0.158 | 0.961 | 0.158 | ||

| 800 | 0.940 | 0.103 | 0.940 | 0.103 | ||

| 1000 | 0.945 | 0.083 | 0.947 | 0.083 | ||

| Model 3 | ||||||

| 300 | 0.931 | 0.333 | 0.939 | 0.335 | ||

| 500 | 0.937 | 0.225 | 0.942 | 0.226 | ||

| 800 | 0.939 | 0.159 | 0.942 | 0.159 | ||

| 1000 | 0.941 | 0.133 | 0.942 | 0.134 | ||

4.2 ER-C: The Erdős-Rényi model with covariates

In this section we illustrate the finite sample performance of the MLE in (11) in the ER-C (9). We focus on inference for the covariate weights, , in the more realistic case of unknown , that is, we use the identity (12) to estimate rather than . Our emphasis is on illustrating that the MLE can be used to perform inference in extremely sparse network settings. To that end we fixed the covariate dimension and a true parameter vector and varied the sparsity parameter . The exact model setup was as follows. We set and sampled the covariate values from a centered distribution. We used and . For the sparsity parameter we used the values or . As before, we sampled networks of sizes , and for each configuration we drew realizations of the ER-C and analyzed the performance of the MLE (11). The sparsest case is close to the maximum theoretically permissible sparsity and results in extremely sparse networks. For , on average, only out of the almost half million possible edges are observed in this setting.

The asymptotic normality for each component of allows us to construct confidence intervals at the 95%-level as prescribed by Corollary 2 and we assess the performance of our MLE by calculating the empirical coverage for each component. There is no significant difference in the empirical coverage or the average length of the confidence intervals between the various components of , which is why we only present them for in Table 2. As we can see, coverage is very close to the nominal confidence level of 95% and the length of the confidence intervals decrease with increasing network size. As expected, confidence intervals are larger for sparse networks. For we observe very wide confidence intervals, which is due to the very low effective sample size.

| Coverage | CI | Coverage | CI | Coverage | CI | |||

| n | ||||||||

| 300 | 0.941 | 0.193 | 0.956 | 0.711 | 0.944 | 2.892 | ||

| 500 | 0.955 | 0.118 | 0.938 | 0.541 | 0.967 | 2.505 | ||

| 800 | 0.943 | 0.075 | 0.950 | 0.424 | 0.951 | 2.235 | ||

| 1000 | 0.949 | 0.061 | 0.935 | 0.379 | 0.948 | 2.107 | ||

5 Data Analysis

We illustrate our results further by applying our estimator to two real world data sets

Lazega’s lawyer friendship data. In this data set, the 71 lawyers of a New England Law Firm were asked to indicate with whom in the firm they regularly socialized outside of work (Lazega, 2001). This is a frequently used network data set that was also analyzed, for example, in Yan et al. (2019), Jochmans (2018) and Snijders et al. (2006). For our analysis we focus on mutual friendships between lawyers as in Snijders et al. (2006), that is, we consider the network in which an undirected edge is placed between two lawyers when they both indicated to socialize with one another. The degrees of the resulting network range from to , with eight isolated nodes. The average degree is and the edge density is . It is to note that we did not remove the isolated nodes before doing inference. Alongside the network, the following variables were collected: The status of the lawyer (partner or associate), their gender (man or woman), which of three offices they worked in, the years they had spent with the firm, their age, their practice (litigation or corporate) and the law school they had visited (Harvard and Yale, UConn or other).

We fitted the SRM to this data set, by using as covariates between two nodes the positive absolute difference between these seven variables, where for categorical variables the difference is defined as the indicator whether the values are equal. Since our simulation studies suggest that BIC performs better for smaller networks, we use it for model selection. Model selection with the heuristic results in a slightly larger penalty and slightly different estimates, but overall very similar results. We constructed confidence intervals for the estimated covariate values at the -level. The resulting weights and confidence intervals for the covariates are shown in Table 3.

| Covariate | Point estimate | Confidence Interval |

| Same status | ||

| Same gender | ||

| Same office | ||

| Years with firm difference | ||

| Age difference | ||

| Same practice | ||

| Same law school |

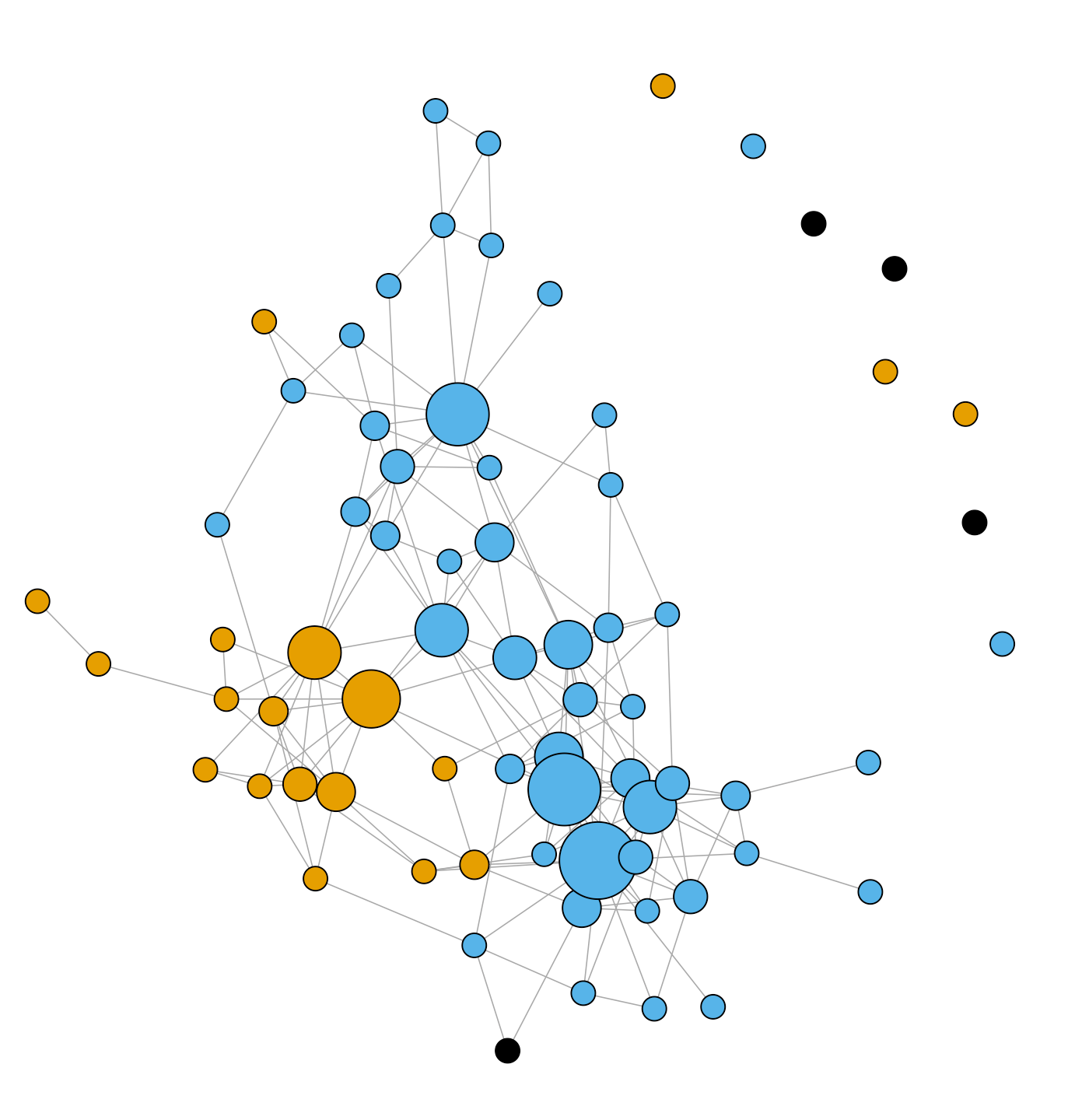

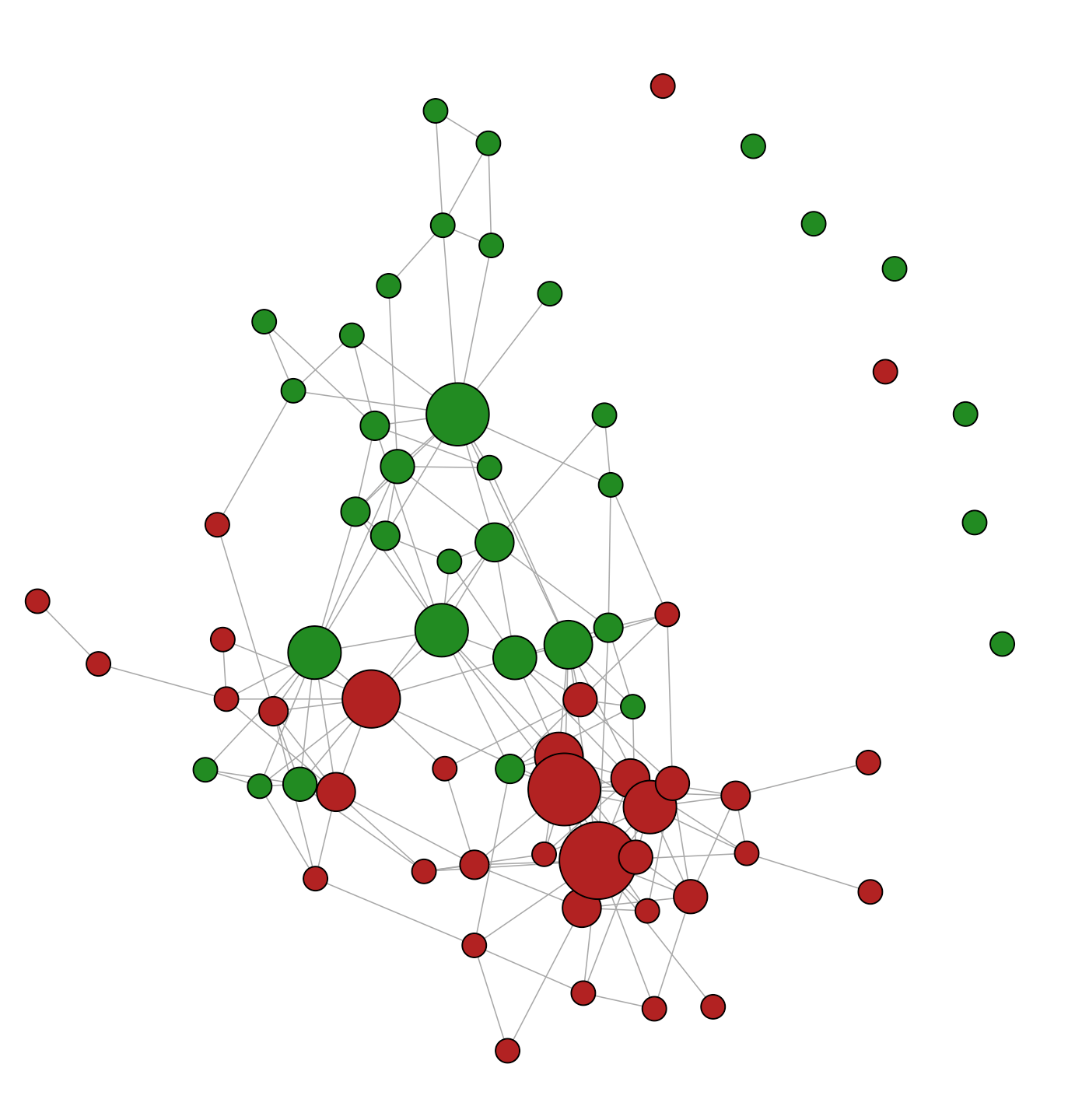

These findings are in line, both in terms of magnitude of estimated weight as well as, more importantly, the sign of each weight, with what we would expect and with the results in the aforementioned papers. In order of importance, working in the same office, having the same status, being of the same practice and having the same gender have a positive effect on friendship formations, whereas a big difference in age or tenure has a negative effect on friendship formation. While our point estimate for having gone to the same law school is positive, its confidence interval extends to the negative real line and we thus cannot make a definite statement about its effect on friendship formation. This effect is also present when doing model selection with our heuristic. To appreciate how the covariates influence the connection pattern, we visualize the network in Figure 4 by examining the effect of office in Figure 4(a) and that of status in Figure 4(b) respectively. We can see indeed that these two covariates have played important roles in shaping how connections were made.

Trade partnerships network. For our second data set, we analyzed mutually important trade partnerships between 136 countries/regions in 1990. This data was originally analyzed by Silva & Tenreyro (2006) and further analyzed in Jochmans (2018). Even back in 1990 almost every country would trade with every other country, resulting in a very dense network. To be able to make the underlying network formation mechanisms visible, we decided to only focus on important trade partnerships in which the trade volume exceeds a certain limit. More precisely, we place an undirected edge between two countries if the trade volume makes up at least of the importing countries total imports or if it makes up at least of the exporting countries total exports. This leaves us with an undirected network with 136 nodes and 1279 edges, meaning that we have an edge density of . The minimum degree of the resulting network was (Dominican Republic), the maximum degree was (USA), and the median degree was .

We analyze the same covariates as Jochmans (2018). That is, we have indicator variables common language and common border that take the value one if countries and share a common language or border and zero otherwise, log distance which is the log of the geographic distance between the countries, colonial ties which is one if at some point colonized or vice versa and zero otherwise, and preferential trade agreement which is an indicator whether or not a preferential trade agreement exists between the countries. Again, we chose BIC for model selection for the reasons outlined above. The results are summarized in Table 4. These results are in line with what one would expect. Having a preferential trade agreement has the strongest positive effect on mutual trade between countries. Speaking the same language, sharing a border or having colonial ties also has a positive effect, while a large geographical distance has a strong negative effect.

| Covariate | Estimated weight | Confidence Interval |

| Log distance | ||

| Common border | ||

| Common language | ||

| Colonial ties | ||

| Preferential trade agreement |

Notice that the confidence intervals for the categorical variables are all much larger than the one for the continuous variable log distance between countries. This is due to the fact that all the columns corresponding to categorical covariates are quite sparse, while the column corresponding to log distance contains only non-zero entries. Only 142 dyads are part of a preferential trade agreement and only 180 share a common border. Consequently the confidence intervals corresponding to these covariates are largest. Note that 1565 node pairs have colonial ties with one another and 1925 speak a common language. While the columns corresponding to these covariates are thus much more populated, they are still relatively sparse when compared to the total number of dyads.

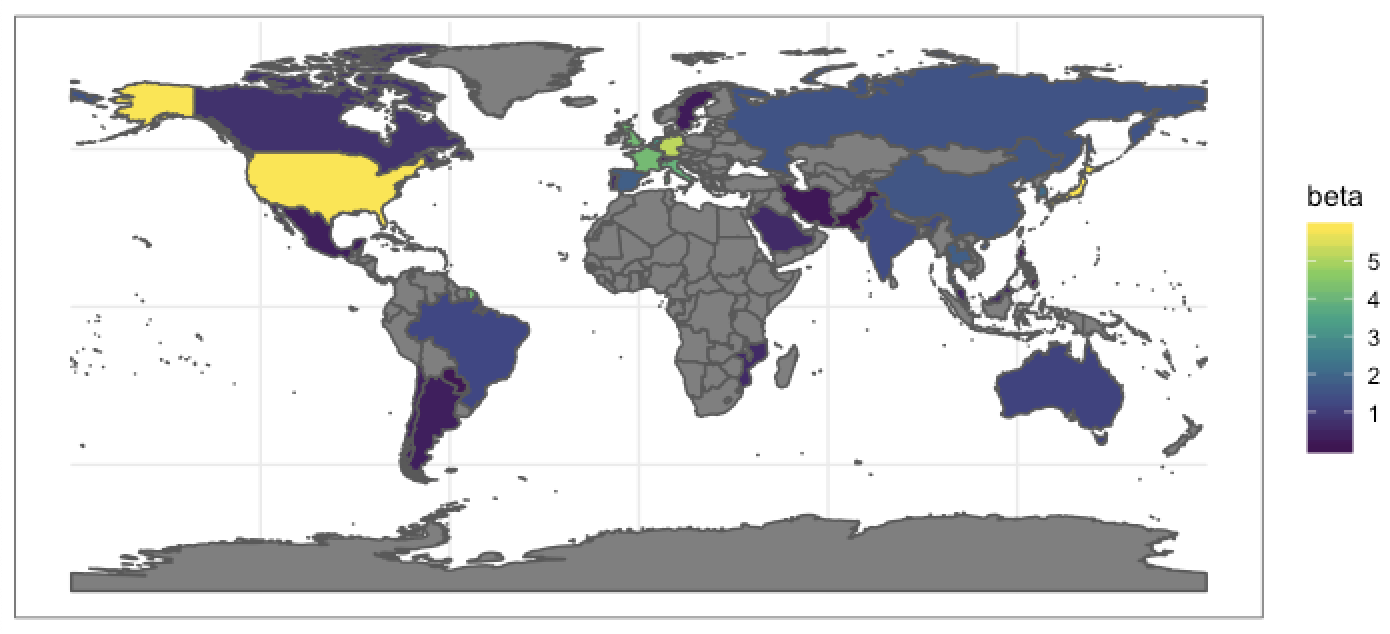

BIC selected active -entries, which are visualized on a map in Figure 5. We presented the top half of these countries/regions with their degree and GDP in Table 5. The ranking of the values correlates with our intuition of the economic power of the countries. However, we also pick up underlying network formation mechanisms that go beyond sheer economic power and that are neither explainable by only looking at network summary statistics (such as degree of a node) nor by only looking at economic metrics such as a country’s GDP. More precisely, we note that the top six positions are occupied by six of the seven G7 countries, which serves to show that the SRM works well for identifying the most important nodes in a network. Note however, that Japan has the largest , albeit having a smaller degree (122) and a significantly smaller GDP than the USA (degree = 126), which comes in second place. In general, the order of degrees no longer aligns exactly with the order of the -values as would have been predicted by the SM without covariates in Chen et al. (2021). Norway, for example, has a -value of zero, even though its degree of and GDP of US$ exceeds the degree and the GDP of several nodes with an active -value. An examination of Norway’s neighboring nodes reveals that it was trading mostly with countries that either are close geographically or have a large -value themselves (such as USA and Japan), meaning that the observed covariates are sufficient to explain the linking behavior of Norway. This illustrates that the SM with covariates is able to pick up subtleties in network formation that one might miss if one relied solely on network summary statistics such as the degree of a node or solely on non-relational summary statistics such as a country’s GDP.

| Degree | GDP (US$) | Degree | GDP (US$) | ||||

| Japan | 5.85 | 122 | 4.95e+12 | Korea | 2.11 | 34 | 3.42e+11 |

| USA | 5.82 | 126 | 6.51e+12 | Singapore | 2.06 | 37 | 5.39e+10 |

| Germany | 5.17 | 120 | 2.27e+12 | Hong Kong | 2.05 | 40 | 1.07e+11 |

| France | 4.16 | 103 | 1.47e+12 | Spain | 1.80 | 41 | 5.46e+11 |

| UK | 4.15 | 104 | 1.04e+12 | Thailand | 1.78 | 33 | 1.11e+11 |

| Italy | 3.92 | 95 | 1.03e+12 | China | 1.58 | 30 | 3.98e+11 |

| Netherlands | 3.15 | 73 | 3.75e+11 | Russia | 1.53 | 28 | 5.43e+11 |

| Belgium-Lux | 2.60 | 59 | 2.56e+11 | India | 1.33 | 32 | 2.75e+11 |

6 Conclusion

We have presented a new model named SRM that simultaneously captures homophily and degree heterogeneity in a network. We have shown that SRM is well suited to model sparse networks, thanks to the sparsity assumption on the nodal parameter that can effectively reduce the dimensionality of the model. We have presented theory for the penalized likelihood estimator based on an penalty on the nodal parameter, including consistency of the excess risk and the central limit theorem for the homophily parameter. Built on the LASSO theory, our theoretical contributions go beyond existing theory for LASSO as we have argued. The computation of our estimator leverages the recent vast algorithmic development on solving LASSO type problems. Thus, SRM represents an attractive model for networks with statistical guarantees and computational feasibility.

There are many important issues for future research. First, we assume fixed-dimensional covariates. Recent data deluge brings more and more data sets that have more variables than observations. How to generalize SRM to include growing dimensional covariates is worth further investigation. Second, it will be interesting to incorporate a low rank component in SRM in order to capture transitivity, the phenomenon that nodes with common neighbors are more likely to connect, as is done in Ma et al. (2020). Third, it will be interesting to see how SRM can be used to model networked data under privacy constraint, along the line of research initiated by Karwa & Slavković (2016) for the -model. Lastly, a growing list of networked data are observed along a temporal dimension (Jiang et al., 2020) and it will be interesting to extend our model to a time series context . These issues are beyond the scope of the current paper and will be explored elsewhere.

References

- (1)

- Abbe (2018) Abbe, E. (2018), ‘Community detection and stochastic block models: recent developments’, Journal of Machine Learning Research 18, 1–86.

- Bertsekas (1995) Bertsekas, D. (1995), Nonlinear Programming, Athena Scientific.

- Binkiewicz et al. (2017) Binkiewicz, N., Vogelstein, J. T. & Rohe, K. (2017), ‘Covariate-assisted spectral clustering’, Biometrika 104, 361–377.

- Bousquet (2002) Bousquet, O. (2002), ‘A bennett concentration inequality and its application to suprema of empirical processes’, Comptes Rendus Mathematique 334(6), 495–500.

- Buena (2008) Buena, F. (2008), ‘Honest variable selection in linear and logistic regression models via l1 and l1 + l2 penalization’, Electronic Journal of Statistics 2, 1153–1194.

- Chatterjee et al. (2011) Chatterjee, S., Diaconis, P. & Sly, A. (2011), ‘Random graphs with a given degree sequence’, Annals of Applied Probability 21(4), 1400–1435.

- Chen et al. (2021) Chen, M., Kato, K. & Leng, C. (2021), ‘Analysis of networks via the sparse beta-model’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 83(5), 887–910.

- Erdős & Rényi (1959) Erdős, P. & Rényi, A. (1959), ‘On random graphs I’, Publicationes Mathematicae (Debrecen) 6, 290–297.

- Erdős & Rényi (1960) Erdős, P. & Rényi, A. (1960), ‘On the evolution of random graphs’, Publ. Math. Inst. Hung. Acad. Sci 5, 17–60.

- Fienberg (2012) Fienberg, S. E. (2012), ‘A brief history of statistical models for network analysis and open challenges.’, Journal of Computational and Graphical Statistics 21, 825–839.

- Friedman et al. (2010) Friedman, J., Hastie, T. & Tibshirani, R. (2010), ‘Regularization paths for generalized linear models via coordinate descent’, Journal of Statistical Software 33(1), 1–22.

- Gilbert (1959) Gilbert, E. G. (1959), ‘Random graphs’, Annals of Mathematical Statistics 30, 1141–1144.

- Goldenberg et al. (2009) Goldenberg, A., Zheng, A. X., Feinberg, S. E. & Airoldi, E. M. (2009), ‘A survey of statistical network models’, Foundations and Trends in Machine Learning 2, 129–233.

- Graham (2017) Graham, B. S. (2017), ‘An econometric model of network formation with degree heterogeneity’, Econometrica 85, 1033–1063.

- Greenshtein & Ritov (2004) Greenshtein, E. & Ritov, Y. (2004), ‘Persistence in high-dimensional linear predictor selection and the virtue of overparametrization’, Bernoulli 10, 971–988.

- Holland et al. (1983) Holland, P. W., Laskey, K. & Leinhardt, S. (1983), ‘Stochastic blockmodels: First steps’, Social Networks 5, 109–137.

- Holland & Leinhardt (1981) Holland, P. W. & Leinhardt, S. (1981), ‘An exponential family of probability distributions for directed graphs’, Journal of the American Statistical Association 76, 33–50.

- Huang & Feng (2018) Huang, S. & Feng, Y. (2018), ‘Pairwise covariates-adjusted block model for community detection’. arXiv:1807.03469.

- Jiang et al. (2020) Jiang, B., Li, J. & Yao, Q. (2020), ‘Autoregressive networks’, arXiv preprint arXiv:2010.04492 .

- Jochmans (2018) Jochmans, K. (2018), ‘Semiparametric analysis of network formation’, Journal of Business & Economic Statistics 36(4), 705–713.

- Karwa & Slavković (2016) Karwa, V. & Slavković, A. (2016), ‘Inference using noisy degrees: Differentially private -model and synthetic graphs’, Annals of Statistics 44(1), 87–112.

- Kock & Tang (2019) Kock, A. B. & Tang, H. (2019), ‘Uniform inference in high-dimensional dynamic panel data models with approximately sparse fixed effects’, Econometric Theory 35(2), 295–359.

- Kolaczyk (2009) Kolaczyk, E. D. (2009), Statistical Analysis of Network Data: Methods and Models, Springer.

- Kolaczyk (2017) Kolaczyk, E. D. (2017), Topics at the Frontier of Statistics and Network Analysis: (Re)Visiting the Foundations, Cambridge University Press.

- Koltchinskii (2011) Koltchinskii, V. (2011), Oracle Inequalities in Empirical Risk Minimization and Sparse Recovery Problems. École d’été de probabilités de Saint-Flour XXXVIII-2008, Springer.

- Kra & Simanca (2012) Kra, I. & Simanca, S. R. (2012), ‘On circulant matrices’, Notices of the American Mathematical Society 59(3), 368–377.

- Lazega (2001) Lazega, E. (2001), The Collegial Phenomenon: The Social Mechanisms of Cooperation Among Peers in a Corporate Law Partnership, Oxford University Press.

- Ledoux & Talagrand (1991) Ledoux, M. & Talagrand, M. (1991), Probability in Banach Spaces, Springer-Verlag.

- Ma et al. (2020) Ma, Z., Ma, Z. & Yuan, H. (2020), ‘Universal latent space model fitting for large networks with edge covariates’, Journal of Machine Learning Research 21(4), 1–67.

- Newman (2018) Newman, M. (2018), Networks (2nd Edition), Oxford University Press.

- Rinaldo et al. (2013) Rinaldo, A., Petrović, S. & Fienberg, S. E. (2013), ‘Maximum likelihood estimation in the -model’, The Annals of Statistics 41(3), 1085–1110.

- Silva & Tenreyro (2006) Silva, J. M. C. S. & Tenreyro, S. (2006), ‘The log of gravity’, The Review of Economics and Statistics 88(4), 641–658.

- Snijders et al. (2006) Snijders, T. A. B., Pattison, P. E., Robins, G. L. & Handcock, M. S. (2006), ‘New specifications for exponential random graph models’, Sociological Methodology 36(1), 99–153.

- Tibshirani (1996) Tibshirani, R. (1996), ‘Regression shrinkage and selection via the lasso’, Journal of the Royal Statistical Society. Series B (Methodological) 58(1), 267–288.

- van de Geer (2008) van de Geer, S. A. (2008), ‘High-dimensional generalized linear models and the lasso’, The Annals of Statistics 36(2), 614–645.

- van de Geer & Bühlmann (2011) van de Geer, S. & Bühlmann, P. (2011), Statistics for High-Dimensional Data, Springer Series in Statistics, Springer-Verlag.

- van de Geer et al. (2014) van de Geer, S., Bühlmann, P., Ritov, Y. & Dezeure, R. (2014), ‘On asymptotically optimal confidence regions and tests for high-dimensional models’, The Annals of Statistics 42(3), 1166–1202.

- van der Vaart (1998) van der Vaart, A. (1998), Asymptotic Statistics, Cambridge Series in Statistical and Probabilistic Mathematics, Cambridge University Press.

- van der Vaart & Wellner (1996) van der Vaart, A. & Wellner, J. (1996), Weak Convergence and Empirical Processes, Springer Series in Statistics, Springer-Verlag.

- Yan & Sarkar (2021) Yan, B. & Sarkar, P. (2021), ‘Covariate regularized community detection in sparse graphs’, Journal of the American Statistical Association 116, 734–745.

- Yan et al. (2019) Yan, T., Jiang, B., Fienberg, S. E. & Leng, C. (2019), ‘Statistical inference in a directed network model with covariates’, Journal of the American Statistical Association 114(526), 857–868.

- Yan, Leng & Zhu (2016) Yan, T., Leng, C. & Zhu, J. (2016), ‘Asymptotics in directed exponential random graph models with an increasing bi-degree sequence’, The Annals of Statistics 44, 31–57.

- Yan, Qin & Wang (2016) Yan, T., Qin, H. & Wang, H. (2016), ‘Asymptotics in undirected random graph models parameterized by the strengths of vertices’, Statistica Sinica 26, 273–293.

- Yan & Xu (2013) Yan, T. & Xu, J. (2013), ‘A central limit theorem in the -model for undirected random graphs with a diverging number of vertices’, Biometrika 100, 519–524.

- Yu et al. (2021) Yu, Y., Bradic, J. & Samworth, R. J. (2021), ‘Confidence intervals for high-dimensional cox models’, Statistics Sinica 31, 243–267.

- Zhang & Zhang (2014) Zhang, C.-H. & Zhang, S. S. (2014), ‘Confidence intervals for low dimensional parameters in high dimensional linear models’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 76(1), 217–242.

- Zhang et al. (2016) Zhang, Y., Levina, E. & Zhu, J. (2016), ‘Community detection in networks with node features’, Electronic Journal of Statistics 10(2), 3153–3178.

- Zhang et al. (2021) Zhang, Y., Wang, Q., Zhang, Y., Yan, T. & Luo, J. (2021), ‘L-2 regularized maximum likelihood for -model in large and sparse networks’, arXiv preprint arXiv:2110.11856 .

Supplementary Materials

The supplementary material contains the main proofs.

Appendix A Proof of Lemma 1 in Section 2

Proof of Lemma 1.

We first show that a solution exists. Using duality theory from convex optimization (cf. Bertsekas (1995), Chapter 5), we know that for any there exists a finite such that the penalized likelihood problem is equivalent to the primal optimization problem

| (15) | ||||

Let be fixed. To obtain an estimate for , we minimize the function

It has derivative

We observe that

and

Furthermore, is continuous and strictly increasing in . Hence, there exists a unique value , such that . Since

for all , is a minimizer of . Since is invertible, we can apply the implicit function theorem with function , which gives us that the corresponding function is continuously differentiable. Plugging in for in (15), we are left with the minimization problem

| (16) | ||||

Since is compact, we are minimizing a continuous function over a compact set in (16). Hence it attains a minimum . By the definition of , must also be a solution of (15).

For the second claim of the Lemma, suppose there is an such that . Consider the following vector : for all let and , while keeping . Then, for all , i.e. is a feasible point for the penalized likelihood problem (5). Furthermore and However,

where the inequality follows from the minimality of . This gives

A contradiction to the optimality of . ∎

Appendix B Consistency with covariates

B.1 Proof of Proposition 1

Notice that the compatibility condition is clearly equivalent to the condition that

stays uniformly bounded away from zero. Recall the definition of . The key to proving Proposition 1 is to show that is close to in an appropriate sense and that fulfills for all and some universal . We then show that is bounded away from zero. Let us analyze the top left block matrix of , i.e. , first:

that is, has all ones on the diagonal and everywhere else. This is a special kind of Toeplitz matrix; a circulant matrix to be precise. It is known (see for example Kra & Simanca (2012)), that every circulant matrix has an associated polynomial and that the eigenvalues of are given by , where , denote the th roots of unity, i.e. where is the imaginary unit and . The associated polynomial of the matrix is

and thus the eigenvalues of are

where the eigenvalue has multiplicity . Hence, we observe the following: For any vector ,

where for the inequality we have used that for any semi-positive definite, symmetric matrix with smallest eigenvalue and any vector of appropriate dimension, we have . Thus, for any ,

Now, notice that for any , we have . This is easily seen by considering the cases and separately and rearranging. Thus,

where is the minimum eigenvalue of . By Assumption 1, we now have for ,

| (17) |

Now, we need to show that with high probability , which would imply that the compatibility condition holds with high probability for the sample size adjusted Gram matrix and the associated sample size adjusted design matrix. To that end, we have the following auxiliary Lemma found in Kock & Tang (2019). For completeness, we give the short proof of it. The notation is adapted to our setting.

Lemma 2 (Lemma 6 in Kock & Tang (2019)).

Let and be two positive semi-definite matrices and . For any set with cardinality , one has

Proof.

Denote by and . Let , with . Then,

Hence, and thus

Minimizing the left-hand side over all with proves the claim. ∎

This shows that to control , we need to control the maximum element-wise distance between and : . We will now show that in the setting of Proposition 1,

and thus, by Lemma 2, we have and i.e. the compatibility condition holds for .

Proof of Proposition 1.

To make referencing of sections of easier, we number its blocks as follows

For , we have (block ①). The entry at position (block ⑤) is also equal and so are blocks ③, ⑥, ⑦, ⑧ and ⑨. For the entries at positions with and as well as positions with and (blocks ② and ④), we have:

for , since we assume that . The claim now follows from Lemma 2. ∎

In the SM without covariates we define the matrices and completely analogously to the SRM by setting the blocks corresponding to the covariates to zero.

To be consistent with our numbering scheme from before, we number these four blocks from top left to bottom right as ①, ②, ④ and ⑤, skipping ③. The proof of Proposition 1 simplifies considerably when no covariates are present and we have the following lemma.

Lemma 3.

Under Assumption 2 and for large enough, the compatibility condition holds for the sample-size adjusted Gram matrix in the sparse model without covariates. That is, for every with ,

Proof.

Following the exact same steps as above for SRM, we find for any

| (18) |

for any . Using line by line the same arguments as in the proof of Proposition 1 we prove that the compatibility condition holds for the sparse model without covariates. More precisely, by Lemma 2, we know that , where . Looking back at the proof of Proposition 1, we only need the part of it that deals with blocks ② and ④, since and coincide in the blocks ① and ⑤. Doing the same calculation as in said proof, we see that for any entry in blocks ② or ⑤,

Under Assumption 2, that is where we define with the components corresponding to set to zero, this expression will be smaller than for large enough. Thus, for large enough, by Lemma 2 and inequality (18), . ∎

Notice that the bound in the lemma above are somewhat arbitrary and an artifact of how we pick our constants in the proof of that Lemma.

B.2 A rescaled penalized likelihood problem

We already mentioned in Section 2 that it is possible to present an equivalent formulation of the problem (5) in terms of a rescaled likelihood problem using the sample-size adjusted design matrix . We will rely heavily on this formulation which we now make precise.

Recall that in the definition of we effectively blew up the entries belonging to . The blow-up factor was chosen precisely such that we can now reformulate our problem as a problem in which each parameter effectively has sample size . That is, our original penalized likelihood problem can be rewritten as

| (19) | ||||

where and the argmin is taken over . Note that by the same arguments as before, is convex. Then, given a solution for a given penalty parameter to this modified problem (19), we can obtain a solution to our original problem (5) with penalty parameter , by setting

For a compacter way of writing, introduce the following notation: For any parameter , we introduce the notation

and also write . In particular we use the notation , to denote the re-parametrized truth and to denote the re-parametrized best local approximation. Note that for any , and hence the bound is the same in the definitions of and . Also, since rescaling the set still results in , there is no need to introduce a set . Note that if and only if .

For any , denote the negative log-likelihood function corresponding to the rescaled problem (19) as

Then, clearly and

Thus, fulfills

i.e. is the best local re-parametrized solution.

To give us a more compact way of writing, for any we introduce functions and denote the function space of all such by . We endow with two norms as follows.

Denote the law of the rows of on , i.e. the probability measure induced by , by . That is, for a measurable set ,

where if and zero otherwise, is the Dirac-measure. We are interested in the and norm on with respect to the measure on . Denote the -norm of simply by and let be the expectation with respect to :

and define the -norm as usual as the -a.s. smallest upper bound of :

Notice in particular, that for any : .

We make the analogous definitions for the unscaled design matrix. Define the probability measure induced by the rows of on as . It is easy to see that we can switch between these norms as follows. Given a parameter and its rescaled version , then clearly

Also note that for any

| (20) |