Antonello Maruotti\Affil1,\Affil2, Luca Merlo\Affil3 and Lea Petrella\Affil4 \AuthorRunningAntonello Maruotti et al. \Affiliations Department of Mathematics, University of Bergen, Bergen, Norway Department of Law, Economics, Political Sciences and Modern Languages, LUMSA University, Rome, Italy Department of Statistical Sciences, Sapienza University of Rome, Rome, Italy MEMOTEF Department, Sapienza University of Rome, Rome, Italy \CorrAddressLuca Merlo, Department of Statistical Sciences, Sapienza University of Rome, Piazzale Aldo Moro 5, 00185 Rome, Italy \CorrEmailluca.merlo@uniroma1.it \CorrPhone(+39) 06 49911 \CorrFax(+39) 06 49911 \TitleA two-part finite mixture quantile regression model for semi-continuous longitudinal data \TitleRunningA two-part finite mixture quantile regression model \Abstract This paper develops a two-part finite mixture quantile regression model for semi-continuous longitudinal data. The proposed methodology allows heterogeneity sources that influence the model for the binary response variable, to influence also the distribution of the positive outcomes. As is common in the quantile regression literature, estimation and inference on the model parameters are based on the Asymmetric Laplace distribution. Maximum likelihood estimates are obtained through the EM algorithm without parametric assumptions on the random effects distribution. In addition, a penalized version of the EM algorithm is presented to tackle the problem of variable selection. The proposed statistical method is applied to the well-known RAND Health Insurance Experiment dataset which gives further insights on its empirical behavior. \Keywords Correlated random effect models; LASSO; Non-parametric ML estimation; Quantile regression mixture models; Semi-continuous longitudinal data; Two-part models

1 Introduction

Semi-continuous data are non-negative and characterized by the coexistence of high kurtosis, positive skewness and an abundance of zeros observed often enough that there are compelling substantive and statistical reasons for special treatment (Belotti et al. (2015)). Modeling non-negative data with clumping at zero has a long history in the statistical literature and several competing models have been proposed (see Min and Agresti (2002) and Min and Agresti (2005) and references therein). Such data structure arises on many occasions: economics, actuarial sciences, environmental modeling and health services (see Liu (2009); Belasco and Ghosh (2012); Neelon et al. (2016a, b) and Farewell et al. (2017)).

Linear regression approaches can be considered as starting points of the analysis (see e.g. Iversen et al. (2015)). Nevertheless, parameter estimates are sensitive to extreme values and likely to be inefficient if the underlying distribution is not Gaussian (Zhou (2002) and Basu and Manning (2009)). Thus, other approaches have attracted researchers attention to model semi-continuous data. Among those, two-part models, introduced by Duan et al. (1983) and Mullahy (1986), play an important role.

This class of models helps handle excess of zeros and overdispersion: they involve a mixture distribution consisting in a mixing of a discrete point mass, with all mass at zero, and a discrete or continuous random variable. In particular, they are described by two-equations: a binary choice model is fitted for the probability of observing a positive-versus-zero outcome. Then, conditional on a positive outcome, an appropriate regression model is fitted for the positive outcome (see Belotti et al. (2015)). This statistical method introduces significant modeling flexibility by allowing the zeros and the positive values to be generated by two different processes. For these reasons, they have been deeply implemented especially in biomedical applications and in health economics as they well recover the two-step structure in the health demand process; see e.g. Diehr et al. (1999); Deb and Trivedi (2002); Alfò and Maruotti (2010); Mihaylova et al. (2011) and Maruotti and Raponi (2014).

The common structure of such models assumes that the effect of the covariates influence the mean of the conditional distribution of the response. However, in many real applications, the effect of the covariates can be different on different parts of the response distribution. In this cases it may be of interest to infer on the entire conditional distribution of the response variable using the quantile regression approach proposed in the seminal paper by Koenker and Bassett (1978) which allows for quantile-specific inference and it is typically used for modeling non-Gaussian outcomes.

Quantile regression methods have become widely used in literature mainly because they are suitable in all those situations where skewness, fat-tails, outliers, truncation, censoring and heteroscedasticity arise. They have been implemented in a wide range of different fields, both in a frequentist paradigm and in a Bayesian setting, spanning from medicine (see Cole and Green (1992); Royston and Altman (1994); Alhamzawi et al. (2012) and Waldmann (2018)), financial and economic research (see Bassett and Chen (2002); Bernardi et al. (2015); Petrella et al. (2018); Laporta et al. (2018); Tian et al. (2018); Bernardi et al. (2018) and Petrella and Raponi (2019)) and environmental modeling; see, e.g., Hendricks and Koenker (1992); Pandey and Nguyen (1999) and Reich et al. (2011) for a discussion. For a detailed review and list of references, Koenker (2005) and Koenker et al. (2017) provide an overview of the most used quantile regression techniques in a classical setting.

In longitudinal studies, quantile methods with random effects have been proposed in order to account for the dependence between serial observations on the same subject (see Marino and Farcomeni (2015); Alfò et al. (2017) and Marino et al. (2018)). Alfò et al. (2017), for example, defined a finite mixture of quantile regression models for heterogeneous data. Quantile regression and two-part models have also been positively considered in several studies: see for example Grilli et al. (2016); Heras et al. (2018); Sauzet et al. (2019) and Biswas et al. (2020). In particular, Biswas et al. (2020) considered a semi-parametric quantile regression approach to zero-inflated and incomplete longitudinal outcomes in a repeated measurements design study.

From an inferential point of view both classical and Bayesian inferential approaches have been used in the literature to estimate the parameters and the quantiles of the models. In the frequentist setting, the inferential approach used to estimate the parameters relies on the minimization of the asymmetric loss function of Koenker and Bassett (1978) while, in the Bayesian setting, the Asymmetric Laplace (AL) distribution has been introduced as a likelihood inferential tool (see Yu and Moyeed (2001)). The two approaches are well-justified by the relationship between the quantile loss function and the AL density: the minimization of the quantile loss function is equivalent, in terms of parameter estimates, to the maximization of the likelihood associated with the AL density. Therefore, the AL distribution could offer a convenient device to implement a likelihood based inferential approach in a quantile regression analysis.

The main goal of the present paper is to extend the two-part quantile regression modeling framework for mixed-type outcomes to longitudinal data using a frequentist approach. In particular, we consider a mixed effect logistic regression for modeling the probability of zero-nonzero outcome, and a linear mixed quantile regression model for the continuous positive outcomes.

Following Alfò et al. (2017), in order to prevent inconsistent parameter estimates due to misspecification of the random effects distribution, we adopt a non-parametric approach in which the random effect is left unspecified and approximated by using a discrete finite mixture. Within this scheme, our modeling framework reduces to a two-part finite mixture of quantile regressions where the components of the finite mixture represent clusters of units that share homogeneous values of model parameters.

We propose to estimate model parameters through Maximum Likelihood (ML) by using the AL distribution as a working likelihood. Specifically, estimation is carried out through the Expectation-Maximization (EM) algorithm. From a computational perspective, we generalize the work of Tian et al. (2014) and provide an efficient version of the EM algorithm with M-step updates in closed form using the well-known location-scale mixture representation of the AL distribution; see Kozumi and Kobayashi (2011).

In statistical modeling, one of the main issue is the identification of the relevant variables to be considered in the model. It is in fact quite common, using real data, that a large number of predictors are concerned in the initial stage of the analysis. In this situation the researcher would be interested in determining a smaller subset that exhibits the strongest effects. Several variable selection methods have been proposed in the literature, one of them is the penalized method which is particularly useful when

dealing with high dimensional statistical problems (see Wasserman and Roeder (2009) and Fan and Lv (2010)).

To improve estimation, to gain in parsimony and to conduct a variable selection procedure, we consider a Penalized EM (PEM) algorithm by introducing the Least Absolute Shrinkage and Selecting Operator (LASSO) penalty term of Tibshirani (1996).

The relevance of our approach is also shown empirically by the analysis of a sample taken from the RAND Health Insurance Experiment (RHIE). The RHIE is one of the largest social experiments ever completed in the U.S. to study the cost sharing and its effect on service use, quality of care and health expenditures; see Deb and Trivedi (2002). Healthcare data represents a striking example of semi-continuous data because they are non-negative, with substantial positive skewness, heavy tailed and, often, multi-modal, e.g. they exhibit a spike-at-zero for non-users. In this paper, we adopt the proposed two-part finite mixture of quantile regressions in order to investigate whether the effect of socioeconomic and household’s characteristics changes with the increase in conditional health spending. In accordance with the results of Deb and Trivedi (2002), our analysis shows that the two-part model identifies two groups of users: a group of reluctant users and a second group that often uses healthcare services. In addition, the effect of the included covariates is not uniform across quantiles but it changes sign and magnitude as the quantile level varies.

The rest of the paper is organized as follows. In Section 2, we introduce the two-part finite mixture quantile regression model. Section 3 illustrates the EM-based maximum likelihood approach, the closed form solutions and the PEM algorithm. In Section 4 we discuss the main empirical results while Section 5 concludes.

2 Methodology

2.1 Two-part quantile regression model

Let , , be a semi-continuous variable for unit at time and let be a time-constant, individual-specific, random effects vector having distribution with support where is used for parameter identifiability. The role of the random coefficients is to capture unobserved heterogeneity and within subject dependence. In a two-part model, the probability distribution of the outcome variable can be written as:

| (1) |

with

where denotes the occurrence variable for unit at time , is the indicator function, is the density function for the positive outcome given that and is a (monotone) transformation function of . The model is completed by defining the linear predictors for the binary and the positive parts of the model. We assume that the spike-at-zero process is governed by a binary logistic model such that:

| (2) |

where is the dimensional set of explanatory variables, is the parameter vector and is a subset of .

As mentioned in the Introduction, in order to determine the effect of explanatory variables on the tails of the distribution of the outcome and make inference at an arbitrary quantile level, we model the positive outcomes using the quantile regression approach. In the quantile regression literature, it is well established that the likelihood approach is based on the AL distribution of Yu and Moyeed (2001), which gives equivalent estimates to the minimization of the loss function in Koenker and Bassett (1978).

The functional form of the AL distribution for our model is the following:

| (3) |

where represents the -th quantile, with , of , is the scale parameter and denotes the quantile loss function of Koenker and Bassett (1978):

| (4) |

Because we are modeling positive values, to match the support of the AL density we consider the logarithmic transformation of the positive values of . In particular, we assume that for a given , conditionally on and after log-transforming the outcome variable, , the conditional density in (1) is an AL distribution as given in (3) whose location parameter is defined by the linear model:

| (5) |

where is a subset of covariates of .

For a fixed quantile level , responses are assumed to be independent conditional on the random vector and parameter estimates can be obtained by maximizing the likelihood function of the model defined in (1)-(5):

| (6) |

where denotes the global set of model parameters. The likelihood in (6) involves a multidimensional integral over the random coefficients whose corresponding distribution allows to explain differences in the response quantiles across individuals. Hence, the choice of an appropriate distribution should be data driven and resistant to misspecification (Marino and Farcomeni, 2015). In the next Section, we will discuss how we may avoid evaluating the integral in (6) for ML estimation.

2.2 Finite mixture of quantile regressions

In the literature, typically the Gaussian distribution is a convenient choice for from a computational point of view. In this case, we may approximate the integral in (6) using Gaussian quadrature or adaptive Gaussian quadrature schemes (see Winkelmann (2004) and Rabe-Hesketh et al. (2005)). A disadvantage of such approaches lies in the required computational effort, which is exponentially increasing with the dimension of the random parameter vector. For these reasons, potential alternatives availed themselves of simulation methods such as Monte Carlo and simulated ML approaches. However, for samples of finite size and short individual sequences, these methods may not provide a good approximation of the true mixing distribution (Alfò et al., 2017). As a robust alternative to the Gaussian choice, a Symmetric Laplace or a multivariate Student T random variable have been considered by Geraci and Bottai (2014) and Farcomeni and Viviani (2015). However, a parametric assumption on the distribution of the random coefficients could be rather restrictive and misspecification of the mixing distribution could lead to biased parameter estimates (see Alfò and Maruotti (2010)). In view of these considerations, in this work we exploit the approach based on the nonparametric maximum likelihood (NPML) estimation of Laird (1978). Instead of specifying parametrically the distribution we approximate it by using a discrete distribution on locations i.e. where the probability is defined by , for and is a one-point distribution putting a unit mass at . The proposed approach can be thought as an approximation of a fully parametric framework as the discrete support approximates a possibly continuous distribution for the random coefficients. To ease the notation, hereinafter we omit the quantile level but all parameters are allowed to depend on it. In this setting, the likelihood in (6) reduces to:

| (7) |

where is the parameter vector.

The likelihood in (7) is similar to the likelihood of a finite mixture of quantile regressions with clusters. More specifically, in the -th cluster the spike-at-zero process is governed by the binary logistic model, ; meanwhile the positive outcomes process is regulated by a linear mixed quantile with AL density in (3) having location parameter given by .

Therefore, our modeling framework reduces to a finite bivariate mixture model for each quantile level where heterogeneity sources that influence the binary decision process, are assumed to influence also the distribution of the positive outcomes through the latent structure defined by discrete multivariate random effects.

3 Estimation

In this Section, we propose a maximum likelihood approach based on the EM algorithm to estimate the parameters of the methodology illustrated in Section 2. Given the finite mixture representation in (7), each unit can be conceptualized as drawn from one of distinct groups: we denote with the indicator variable that is equal to if the -th unit belongs to the -th component of the finite mixture, and 0 otherwise. The EM algorithm treats as missing data the component membership . Thus, the log-likelihood for the complete data has the following form: {fleqn}[]

| (8) |

In the E-step, the presence of the unobserved group-indicator is handled by taking the conditional expectation of given the observed data and the parameter estimates at the -th iteration . At the -th iteration of the algorithm, we replace by its conditional expectation using the following update equation:

| (9) |

where . Conditionally on the posterior probabilities in (9), the M-step solutions are generally updated by maximizing with respect to using numerical optimization techniques.

The E- and M-steps are alternated until convergence, that is when the difference between the likelihood function evaluated at two consecutive iterations is smaller than a predetermined threshold. In this paper, we set this convergence criterion equal to . To avoid convergence to local maxima, for each value of , we initialize model parameters using a multi-start strategy: we considered 20 different starting points and retained the solution corresponding to the maximum likelihood value.

A considerable disadvantage of this procedure affects the M-step which could require a high computational effort and it could be very time-consuming especially when the set of explanatory variables is large. Therefore, in the next Section we develop a more efficient approach for estimating two-part quantile regression models, and to obtain a closed form of the ML estimator.

3.1 Closed form EM algorithm solutions

This Section develops an efficient estimation method for the two-part quantile regression problem based on the EM algorithm presented in Section 3. We reduce the computational burden of the algorithm compared to direct maximization of the likelihood and extend the work of Tian et al. (2014) to two-part mixture models. In particular, we obtain iteratively closed form expressions for the unknown parameters vector and the coefficient vectors for .

We use the location-scale mixture representation of the AL density considered in Kozumi and Kobayashi (2011) to specify the positive outcome process of the model in (5) as the following hierarchical model:

| (10) |

where , and . The constraints imposed on and must be satisfied in order to guarantee that coincides with the -th conditional quantile of .

Due to the independence of the ’s, one can obtain that the conditional distribution of is a Generalized Inverse Gaussian (GIG) distribution (see Tian et al. 2014, Section 2.3), namely:

| (11) |

In addition, from (10) the joint density of and is:

| (12) |

The underlying idea to obtain the updated parameter estimates of and for is to consider as an additional latent variable. According to (12), after omitting terms which of are not dependent on and , the complete data log-likelihood function is proportional to: {fleqn}

| (13) | |||

| (14) |

In the E-step, the conditional expectation of the complete log-likelihood function, given the observed data and the current parameter estimates at the -th iteration, , is given by: {fleqn}

| (15) |

| (16) | |||

| (17) |

where has been defined in (9) and . To compute , we can exploit the moment properties of the GIG distribution in (11). Hence, we have that:

| (18) |

In the M-step, we determine the update expressions by setting to zero the derivative of (16)-(17) with respect to and and solve the corresponding M-step equations. In conclusion, we obtain the following update expressions:

| (19) |

and

| (20) |

Equations (19) and (20) essentially, are equivalent to modified weighted least square estimator expressions where the quantile level is used to modify both the weights, , and the response variable through and .

3.2 Variable selection and the Penalized EM algorithm

When dealing with high-dimensional problems, it may be of interest to reduce the set of explanatory variables using penalized regression methods which allow for sparse modeling and enhance model interpretability. In this Section, we introduce a penalized version of the EM algorithm described in Section 3. In particular, we use the PEM algorithm, originally proposed by Green (1990), which leaves the E-step unchanged while it modifies the M-step by introducing a penalty function to achieve simultaneous shrinkage and/or variable selection. Here we consider the LASSO penalty term put forward by Tibshirani (1996) to shrink the coefficients of the positive outcomes, i.e. the vector , and simultaneously select a smaller subset of variables that exhibits the strongest effects. For a chosen quantile level and number of latent classes , the penalized log-likelihood for the complete data has the following form:

| (21) |

where has been defined in (8), is the LASSO penalty function and is a tuning parameter that regulates the strength of the penalization assigned to the coefficients of the model. The optimal value of is selected via 10-fold cross-validation which allows us to consider as a data-driven parameter.

4 Application

4.1 Data description

As stated in the Introduction, in this Section we present the application of the proposed methodology to the well-known RHIE dataset. These data have already been discussed by Deb and Trivedi (2002); Duan et al. (1983) and Manning et al. (1987). The RHIE is the most important health insurance study ever conducted to assess how medical care costs affect a patient’s use of health services and quality and it is widely regarded as the basis of the most reliable estimates of price sensitivity of demand for medical services.

The experiment, conducted by the RAND Corporation from 1974 to 1982, collects data from about 8000 enrollees in 2823 families, from six sites across the US. Each family was enrolled in one of fourteen different HIS insurance plans for either 3 or 5 years.

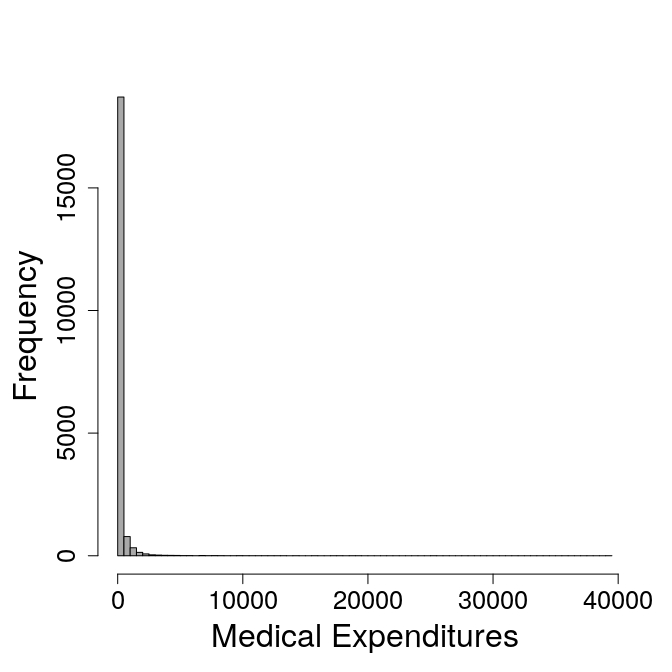

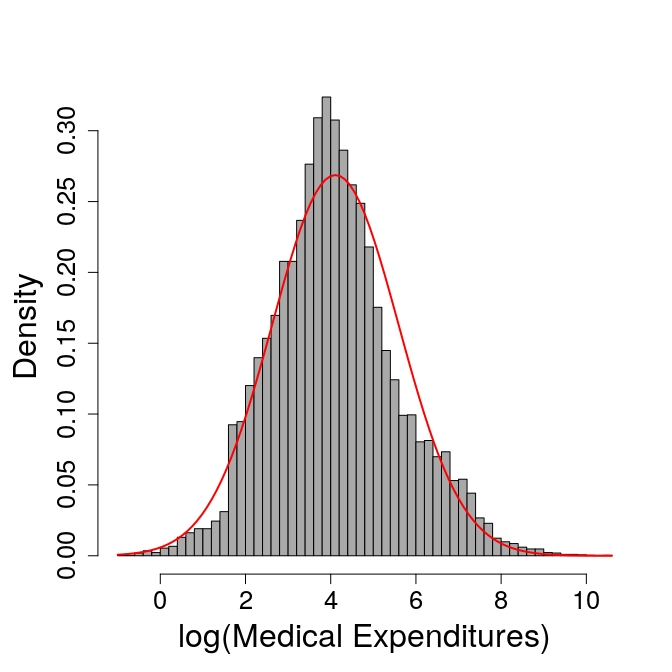

Our aim is to understand how available covariates influence healthcare decisions spending in U.S. families at different quantile levels of interest. We consider one measure of utilization: the total spending on health services (MED) defined as the sum of outpatient, inpatient, drugs, supplies and psychotherapy expenses expressed in U.S. dollars. The considered covariates are the same of the work of Deb and Trivedi (2002): they include personal characteristics such as sex (FEMALE), age (XAGE), race (BLACK) and education level (EDUCDEC). There are also socio-economic variables of the household such as income (LINC), number of components (LFAM) and the presence of a person aged 18 or less (CHILD). An interaction term between the gender and the presence of a child (FEMCHILD) is also included. Quantitative indicators of health condition are measured via an index of chronic conditions (DISEA) and through the existence of a physical limitation (PHYSLM) while the binary coding of self-rated health status (HLTHG, HLTHF, HLTHP) controls for variations in perceived healthcare conditions. The summary statistics are reported in Tables 1 and 2. By looking at Table 1, the proportion of zero expenditures is significant: 22% did not have any medical expenditure. Meanwhile, the right tail of the distribution is very long with the maximum expense being 39182.02 U.S. dollars which indicates the presence of overdispersion and potential outliers in the data. In addition, the dependent variable is severely skewed and presents a high kurtosis. From a graphical point of view, Figure 1 shows that the data is characterized by a substantial zero-mass health expenditure (left graph): zero expenditure indicates no utilization, and it may reflect population’ reluctance to spend on health care treatments. By looking at the right plot, also the logarithmic transformation of positive values does not follow a Gaussian distribution. Therefore, a two-part quantile regression model would be appropriate for these data. In particular, the binary decision process would estimate the association between the covariates and the probability of having any health care expenditure. Through the positive part of the model instead, our goal is to see whether the covariates have a different impact on health care expenditures at different quantiles. Indeed, by doing so, we can single out the impact of health determinants across extreme quantiles and non extreme quantiles reflecting the association with low-intensity primary health care services, at the 10-th and 25-th percentiles, and that with high-intensity such as the highly intensive and expensive technology care, at the 75-th and 90-th percentiles.

| Variable | Mean | S.D. | Skewness | Kurtosis | No Exp. (%) | Maximum | -th quantile | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.1 | 0.25 | 0.5 | 0.75 | 0.90 | |||||||

| MED | 171.568 | 698.201 | 20.189 | 734.007 | 22.055 | 39182.016 | 0.000 | 5.503 | 35.378 | 104.541 | 341.201 |

| Variable | Description | Mean | S.D. |

|---|---|---|---|

| LOGC | (coinsurance + 1), coinsurance | 2.384 | 2.042 |

| LFAM | (family size) | 1.248 | 0.539 |

| LINC | (family income) | 8.708 | 1.228 |

| XAGE | Age in years | 25.718 | 16.768 |

| FEMALE | If person is female: 1 | 0.517 | 0.500 |

| CHILD | If age is less than 18: 1 | 0.401 | 0.490 |

| FEMCHILD | FEMALE ∗ CHILD | 0.194 | 0.395 |

| BLACK | If race of household head is black: 1 | 0.184 | 0.387 |

| EDUCDEC | Education of the household head in years | 11.966 | 2.806 |

| PHYSLM | If the person has a physical limitation: 1 | 0.118 | 0.323 |

| DISEA | Index of chronic diseases | 11.244 | 6.742 |

| HLTHG | If self-rated health is good: 1† | 0.362 | 0.481 |

| HLTHF | If self-rated health is fair: 1† | 0.077 | 0.267 |

| HLTHP | If self-rated health is poor: 1† | 0.015 | 0.121 |

| MHI | Mental Health Index | 76.554 | 12.503 |

4.2 Marginal inferences from the two-part mixture quantile regression model

In this Section we present the results of the application to the RHIE data. We estimated the proposed LASSO penalized two-part finite mixture quantile regression at different quantile levels of interest , for a varying number of mixture components . We used the same covariates for both the binary process and the positive part of the model and we assumed that random intercepts are sufficient to capture heterogeneity between subjects even tough the generalization to multiple random effects is computationally inexpensive and straightforward thanks to the discrete mixture structure. Because the number of components is unknown a-priori, we select it according to the Bayesian Information Criterion (BIC)111, where denotes the number of free model parameters and is the number of individuals. (Schwarz et al. (1978)). Standard errors are obtained using a parametric bootstrap approach: we refitted the model to 250 bootstrap samples simulated from the estimated model parameters, and approximated the standard error of each parameter with its corresponding standard deviation computed on bootstrap samples. All computations have been implemented in the R software environment (version 3.5.2) with C++ object-oriented programming.

Table 3 reports the estimated penalized model coefficients and standard errors (in parentheses) for the binary (Panel A) and positive (Panel B) part of the model. Parameter estimates are displayed in boldface when significant at the standard 5% level. Panels C and D show the estimated masses of the bivariate discrete distribution of the random effects and the model fit summary at each quantile level, respectively.

Consistently with the findings of Deb and Trivedi (2002); Duan et al. (1983) and Bago d’Uva (2006), the selected number of mixture components is two for all investigated quantiles. Essentially, the two-part model demarcates two distinct subpopulations: a group of reluctant users who rarely accesses health services and a group of users that uses health services with high frequency. This claim is confirmed by the estimated mixing probabilities and locations which can be interpreted as high and low users. Group separation is all the more apparent as the quantile level increases with estimated masses at the 90-th quantile.

By looking at the binary process estimates in Table 3 (Panel A), one can see that all coefficients are statistically different from zero at the 5% significance level except LFAM, MHI and HLTHG and HLTHF at low and high quantile levels, respectively. The marginal inferences from the binary part of the two-part model suggest that the most important determinants of people’s willingness to spend on health services are related to socio-cultural and economic factors: income, age, sex, race ethnicity and education level have the expected signs and significance. The presence of a coinsurance health plan acts as a protection factor reducing the probability of consuming health services. Ageing, presumably, involves complications such as heart diseases, cancer, diabetes and many others that require (obligatory) hospitalization. The analysis points out also profound economic and ethnicity inequalities.

It is worth noting that the coefficient estimates vary as the quantile level varies, e.g. they generally show an upward or downward trend as the quantile increases. This may be due to the presence of correlation between the binary and the positive processes which is channeled via the latent structure defined by the discrete bivariate random effects.

Moving onto the analysis of the positive outcomes (Table 3, Panel B), our results are generally consistent with those of Deb and Trivedi (2002). The first thing one can notice is that not all variables have the same effect on healthcare consumption, i.e. they change in sign and magnitude and some of them have been set to zero at specific quantile levels. This highlights the importance of considering a quantile regression approach because such effects could not be detected by the classical mean regression.

As previously described, the presence of health insurance seems to act as a safety ledge: insured people spend less. This may reflect the fact that health care is largely provided by private hospitals and clinics. The results indicate also that individuals in larger families are more likely to be in the low-use group especially up to the 75-th quantile. As expected, the economic situation appears to be one of the main barriers that influence healthcare access for low income households. In relation to the gender, females have an higher spending pattern up to the 75-th percentiles which may be caused by hospitalization being parturition or its complications.

Other covariates also appear to have some explanatory power, notably XAGE, CHILD, FEMCHILD and BLACK. The elderly undergoes frequent checks and require more health services due to ageing phenomena to which they may be exposed to. The interaction term, FEMCHILD, and BLACK are negatively associated with the response indicating that, in the latter case, racial differences in the amount spent on medical care are persistent and confirms that among individuals who spend on care, blacks have lower expenditures than whites. Moreover, highly literate and educated individuals tend to follow a healthy lifestyle, be less reluctant to go through a visit to a physician, and thus spend more to preserve and improve their health. Variables controlling for the health status of the individual such as PHYSLM and DISEA are positively associated with healthcare expenses: supposedly, disabilities, physical limitations and diagnosis of chronic illnesses require highly intensive, technology care or newer, more costly treatments. Also, self-perceived health condition indicators are all positively associated with health expenses with a much steeper slope at the lower percentiles meanwhile, their impact seems to be negligible above the 75-th quantile.

Moreover, it is possible to see that the impact of several variables varies across quantiles: the effect of LOGC and BLACK is not uniform as the quantile increases but is worse on the left tail of the distribution of health expenditures.

Also, variables such as LINC, FEMALE, CHILD and FEMCHILD exhibit nonlinear effects: in particular, CHILD and FEMCHILD have a U-shaped and an inverted U-shape effect, respectively. EDUCDEC changes sign and magnitude across the quantile levels as well. As regards the estimated random intercepts, , we notice that the estimates increase with and this is consistent with increasing values of healthcare spending.

We conclude the analysis comparing our methodology with the Linear Quantile Mixed Model (LQMM) of Geraci and Bottai (2014). In particular, we fit a LQMM only on the positive values of the dependent variable under the assumption that the distribution of the random intercepts is a bivariate Gaussian while ignoring both the correlation between the binary and positive process and the sparsity induced through the LASSO regularization.

By looking at the parameter estimates in Table 4, we notice slight differences with respect to the results obtained using our methodology at low quantiles while, as we move from the left to the right tail of the response distribution, there are considerable differences. Such discrepancies in the two models might be traced back to the fact that the distribution of the random effects is not Gaussian. Indeed, the semiparametric mixture approach and the LQMM perform equivalently only if the random coefficients are Gaussianly distributed otherwise, the semiparametric mixture performs better being more flexible and able to accommodate departure from the Gaussianity assumption (see Alfò et al. (2017)).

| Covariate | -th quantile | ||||

|---|---|---|---|---|---|

| 10 | 25 | 50 | 75 | 90 | |

| Panel A: Binary process () | |||||

| LOGC | |||||

| LFAM | |||||

| LINC | |||||

| XAGE | |||||

| FEMALE | |||||

| CHILD | |||||

| FEMCHILD | |||||

| BLACK | |||||

| EDUCDEC | |||||

| PHYSLM | |||||

| DISEA | |||||

| HLTHG | |||||

| HLTHF | |||||

| HLTHP | |||||

| MHI | |||||

| Panel B: Positive process | |||||

| LOGC | |||||

| LFAM | |||||

| LINC | |||||

| XAGE | |||||

| FEMALE | |||||

| CHILD | |||||

| FEMCHILD | |||||

| BLACK | |||||

| EDUCDEC | |||||

| PHYSLM | |||||

| DISEA | |||||

| HLTHG | |||||

| HLTHF | |||||

| HLTHP | |||||

| MHI | |||||

| Panel C: | |||||

| Panel D: | |||||

| -10349.09 | -7446.91 | -6742.39 | -9394.92 | -12392.29 | |

| par | 36 | 35 | 36 | 36 | 29 |

| AIC | 20770.18 | 14963.82 | 13556.77 | 18861.84 | 24844.59 |

| BIC | 21055.04 | 15240.77 | 13841.63 | 19146.70 | 25081.97 |

| Covariate | -th quantile | ||||

|---|---|---|---|---|---|

| 10 | 25 | 50 | 75 | 90 | |

| LOGC | |||||

| LFAM | |||||

| LINC | |||||

| XAGE | |||||

| FEMALE | |||||

| CHILD | |||||

| FEMCHILD | |||||

| BLACK | |||||

| EDUCDEC | |||||

| PHYSLM | |||||

| DISEA | |||||

| HLTHG | |||||

| HLTHF | |||||

| HLTHP | |||||

| MHI | |||||

| Intercept | |||||

5 Conclusions

This paper introduces a two-part finite mixture of quantile regressions for mixed-type outcomes under a longitudinal setting. Random effect coefficients are added in both the binary and the positive decision mechanisms to account for zero inflation and unobserved heterogeneity. Rather than assuming a parametric distribution on the random coefficients distribution, we approximate it using a multivariate discrete variable defined on a finite number of support points. Estimation of the model parameters is based on a suitable likelihood-based EM algorithm. In addition, a LASSO penalized version of the algorithm is proposed as an automatic data-driven procedure to perform variable selection. The application of the proposed method to the RHIE on health behaviors and attitudes shows consistent results with existing studies.

The proposed approach can be further extended to consider time-varying sources of unobserved heterogeneity via individual-specific coefficients evolving according a hidden Markov chain. Secondly, we may extend the univariate quantile framework to a multivariate quantile regression setting taking into account for the correlation among the marginals of a multivariate response variable (Petrella and Raponi (2019)).

References

- Alfò and Maruotti (2010) Alfò, M. and Maruotti, A. (2010). Two-part regression models for longitudinal zero-inflated count data. Canadian Journal of Statistics, 38(2), 197–216.

- Alfò et al. (2017) Alfò, M., Salvati, N., and Ranallli, M. G. (2017). Finite mixtures of quantile and M-quantile regression models. Statistics and Computing, 27(2), 547–570.

- Alhamzawi et al. (2012) Alhamzawi, R., Yu, K., and Benoit, D. F. (2012). Bayesian adaptive Lasso quantile regression. Statistical Modelling, 12(3), 279–297.

- Bago d’Uva (2006) Bago d’Uva, T. (2006). Latent class models for utilisation of health care. Health Economics, 15(4), 329–343.

- Bassett and Chen (2002) Bassett, G. W. and Chen, H.-L. (2002). Portfolio style: Return-based attribution using quantile regression, pages 293–305. Physica-Verlag HD, Heidelberg. ISBN 978-3-662-11592-3. 10.1007/978-3-662-11592-3_15.

- Basu and Manning (2009) Basu, A. and Manning, W. G. (2009). Issues for the next generation of health care cost analyses. Medical Care, 47, S109–S114.

- Belasco and Ghosh (2012) Belasco, E. J. and Ghosh, S. K. (2012). Modelling semi-continuous data using mixture regression models with an application to cattle production yields. The Journal of Agricultural Science, 150(1), 109–121.

- Belotti et al. (2015) Belotti, F., Deb, P., Manning, W. G., and Norton, E. C. (2015). Twopm: Two-part models. The Stata Journal, 15(1), 3–20.

- Bernardi et al. (2015) Bernardi, M., Gayraud, G., Petrella, L., et al. (2015). Bayesian tail risk interdependence using quantile regression. Bayesian Analysis, 10(3), 553–603.

- Bernardi et al. (2018) Bernardi, M., Bottone, M., and Petrella, L. (2018). Bayesian quantile regression using the skew exponential power distribution. Computational Statistics & Data Analysis, 126, 92–111.

- Biswas et al. (2020) Biswas, J., Ghosh, P., and Das, K. (2020). A semi-parametric quantile regression approach to zero-inflated and incomplete longitudinal outcomes. AStA Advances in Statistical Analysis, pages 1–23.

- Cole and Green (1992) Cole, T. J. and Green, P. J. (1992). Smoothing reference centile curves: the LMS method and penalized likelihood. Statistics in Medicine, 11(10), 1305–1319.

- Deb and Trivedi (2002) Deb, P. and Trivedi, P. K. (2002). The structure of demand for health care: latent class versus two-part models. Journal of Health Economics, 21(4), 601–625.

- Diehr et al. (1999) Diehr, P., Yanez, D., Ash, A., Hornbrook, M., and Lin, D. (1999). Methods for analyzing health care utilization and costs. Annual Review of Public Health, 20(1), 125–144.

- Duan et al. (1983) Duan, N., Manning, W. G., Morris, C. N., and Newhouse, J. P. (1983). A comparison of alternative models for the demand for medical care. Journal of Business & Economic Statistics, 1(2), 115–126.

- Fan and Lv (2010) Fan, J. and Lv, J. (2010). A selective overview of variable selection in high dimensional feature space. Statistica Sinica, 20(1), 101.

- Farcomeni and Viviani (2015) Farcomeni, A. and Viviani, S. (2015). Longitudinal quantile regression in the presence of informative dropout through longitudinal-survival joint modeling. Statistics in Medicine, 34(7), 1199–1213.

- Farewell et al. (2017) Farewell, V., Long, D., Tom, B., Yiu, S., and Su, L. (2017). Two-part and related regression models for longitudinal data. Annual Review of Statistics and Its Application, 4, 283–315.

- Geraci and Bottai (2014) Geraci, M. and Bottai, M. (2014). Linear quantile mixed models. Statistics and Computing, 24(3), 461–479.

- Green (1990) Green, P. J. (1990). On use of the EM algorithm for penalized likelihood estimation. Journal of the Royal Statistical Society: Series B (Methodological), 52(3), 443–452.

- Grilli et al. (2016) Grilli, L., Rampichini, C., and Varriale, R. (2016). Statistical modelling of gained university credits to evaluate the role of pre-enrolment assessment tests: An approach based on quantile regression for counts. Statistical Modelling, 16(1), 47–66.

- Hendricks and Koenker (1992) Hendricks, W. and Koenker, R. (1992). Hierarchical spline models for conditional quantiles and the demand for electricity. Journal of the American Statistical Association, 87(417), 58–68.

- Heras et al. (2018) Heras, A., Moreno, I., and Vilar-Zanón, J. L. (2018). An application of two-stage quantile regression to insurance ratemaking. Scandinavian Actuarial Journal, 2018(9), 753–769.

- Iversen et al. (2015) Iversen, T., Aas, E., Rosenqvist, G., Hakkinen, U., and on behalf of the EuroHOPE study group (2015). Comparative analysis of treatment costs in EUROHOPE. Health Economics, 24, 5–22.

- Koenker (2005) Koenker, R. (2005). Quantile Regression. Cambridge University Press.

- Koenker and Bassett (1978) Koenker, R. and Bassett, G. (1978). Regression quantiles. Econometrica: Journal of the Econometric Society, 46(1), 33–50.

- Koenker et al. (2017) Koenker, R., Chernozhukov, V., He, X., and Peng, L. (2017). Handbook of quantile regression. CRC press.

- Kozumi and Kobayashi (2011) Kozumi, H. and Kobayashi, G. (2011). Gibbs sampling methods for bayesian quantile regression. Journal of Statistical Computation and Simulation, 81(11), 1565–1578.

- Laird (1978) Laird, N. (1978). Nonparametric maximum likelihood estimation of a mixing distribution. Journal of the American Statistical Association, 73(364), 805–811.

- Laporta et al. (2018) Laporta, A. G., Merlo, L., and Petrella, L. (2018). Selection of Value at Risk models for energy commodities. Energy Economics, 74, 628–643.

- Liu (2009) Liu, L. (2009). Joint modeling longitudinal semi-continuous data and survival, with application to longitudinal medical cost data. Statistics in Medicine, 28(6), 972–986.

- Manning et al. (1987) Manning, W. G., Newhouse, J. P., Duan, N., Keeler, E. B., and Leibowitz, A. (1987). Health insurance and the demand for medical care: evidence from a randomized experiment. The American Economic Review, pages 251–277.

- Marino and Farcomeni (2015) Marino, M. F. and Farcomeni, A. (2015). Linear quantile regression models for longitudinal experiments: an overview. Metron, 73(2), 229–247.

- Marino et al. (2018) Marino, M. F., Tzavidis, N., and Alfò, M. (2018). Mixed hidden Markov quantile regression models for longitudinal data with possibly incomplete sequences. Statistical Methods in Medical Research, 27(7), 2231–2246.

- Maruotti and Raponi (2014) Maruotti, A. and Raponi, V. (2014). On baseline conditions for zero-inflated longitudinal count data. Communications in Statistics - Simulation and Computation, 43(4), 743–760.

- Mihaylova et al. (2011) Mihaylova, B., Briggs, A., O’Hagan, A., and Thompson, S. G. (2011). Review of statistical methods for analysing healthcare resources and costs. Health Economics, 20(8), 897–916.

- Min and Agresti (2002) Min, Y. and Agresti, A. (2002). Modeling nonnegative data with clumping at zero: a survey. Journal of the Iranian Statistical Society, 1(1), 7–33.

- Min and Agresti (2005) Min, Y. and Agresti, A. (2005). Random effect models for repeated measures of zero-inflated count data. Statistical Modelling, 5(1), 1–19.

- Mullahy (1986) Mullahy, J. (1986). Specification and testing of some modified count data models. Journal of Econometrics, 33(3), 341 – 365.

- Neelon et al. (2016a) Neelon, B., O’Malley, A. J., and Smith, V. A. (2016a). Modeling zero-modified count and semicontinuous data in health services research part 1: background and overview. Statistics in Medicine, 35(27), 5070–5093.

- Neelon et al. (2016b) Neelon, B., O’Malley, A. J., and Smith, V. A. (2016b). Modeling zero-modified count and semicontinuous data in health services research part 2: case studies. Statistics in Medicine, 35(27), 5094–5112.

- Pandey and Nguyen (1999) Pandey, G. R. and Nguyen, V.-T.-V. (1999). A comparative study of regression based methods in regional flood frequency analysis. Journal of Hydrology, 225(1-2), 92–101.

- Petrella and Raponi (2019) Petrella, L. and Raponi, V. (2019). Joint estimation of conditional quantiles in multivariate linear regression models with an application to financial distress. Journal of Multivariate Analysis, 173, 70–84.

- Petrella et al. (2018) Petrella, L., Laporta, A. G., and Merlo, L. (2018). Cross-Country Assessment of Systemic Risk in the European Stock Market: Evidence from a CoVaR Analysis. Social Indicators Research, pages 1–18. 10.1007/s11205-018-1881-8.

- Rabe-Hesketh et al. (2005) Rabe-Hesketh, S., Skrondal, A., and Pickles, A. (2005). Maximum likelihood estimation of limited and discrete dependent variable models with nested random effects. Journal of Econometrics, 128(2), 301–323.

- Reich et al. (2011) Reich, B. J., Fuentes, M., and Dunson, D. B. (2011). Bayesian spatial quantile regression. Journal of the American Statistical Association, 106(493), 6–20.

- Royston and Altman (1994) Royston, P. and Altman, D. G. (1994). Regression using fractional polynomials of continuous covariates: parsimonious parametric modelling. Journal of the Royal Statistical Society: Series C (Applied Statistics), 43(3), 429–453.

- Sauzet et al. (2019) Sauzet, O., Razum, O., Widera, T., and Brzoska, P. (2019). Two-part models and quantile regression for the analysis of survey data with a spike. The example of satisfaction with health care. Frontiers in Public Health, 7, 146.

- Schwarz et al. (1978) Schwarz, G. et al. (1978). Estimating the dimension of a model. The Annals of Statistics, 6(2), 461–464.

- Tian et al. (2018) Tian, F., Gao, J., and Yang, K. (2018). A quantile regression approach to panel data analysis of health-care expenditure in organisation for economic co-operation and development countries. Health Economics, 27(12), 1921–1944.

- Tian et al. (2014) Tian, Y., Tian, M., and Zhu, Q. (2014). Linear quantile regression based on EM algorithm. Communications in Statistics-Theory and Methods, 43(16), 3464–3484.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the Lasso. Journal of the Royal Statistal Society. Series B, 58, 267–288.

- Waldmann (2018) Waldmann, E. (2018). Quantile regression: a short story on how and why. Statistical Modelling, 18(3-4), 203–218.

- Wasserman and Roeder (2009) Wasserman, L. and Roeder, K. (2009). High dimensional variable selection. Annals of Statistics, 37(5A), 2178.

- Winkelmann (2004) Winkelmann, R. (2004). Health care reform and the number of doctor visits—an econometric analysis. Journal of Applied Econometrics, 19(4), 455–472.

- Yu and Moyeed (2001) Yu, K. and Moyeed, R. A. (2001). Bayesian quantile regression. Statistics & Probability Letters, 54(4), 437–447.

- Zhou (2002) Zhou, X.-H. (2002). Inferences about population means of health care costs. Statistical Methods in Medical Research, 11(4), 327–339.