Beating the market with a bad predictive model

Faculty of Electrical Engineering

Czech Technical University in Prague

)

Abstract

It is a common misconception that in order to make consistent profits as a trader, one needs to posses some extra information leading to an asset value prediction more accurate than that reflected by the current market price. While the idea makes intuitive sense and is also well substantiated by the widely popular Kelly criterion, we prove that it is generally possible to make systematic profits with a completely inferior price-predicting model. The key idea is to alter the training objective of the predictive models to explicitly decorrelate them from the market, enabling to exploit inconspicuous biases in market maker’s pricing, and profit on the inherent advantage of the market taker. We introduce the problem setting throughout the diverse domains of stock trading and sports betting to provide insights into the common underlying properties of profitable predictive models, their connections to standard portfolio optimization strategies, and the, commonly overlooked, advantage of the market taker. Consequently, we prove desirability of the decorrelation objective across common market distributions, translate the concept into a practical machine learning setting, and demonstrate its viability with real world market data.

1 Introduction

The attempt to predict the future is at the core of any successful trading strategy. Traders continuously try to predict future prices of assets, such as stocks or commodities, to secure profits on their future positions. Similarly, bettors try to predict discrete future outcomes of random events, such as elections or sports matches, to secure profits on their realizations. Having a high-quality future prediction, one can confidently estimate the expected returns associated with the potential decisions to allocate assets and select securities for successful investments and speculations. The quality of each prediction then naturally reflects the amount of information used for the estimation. In an efficient market, it is assumed that all available information is already reflected in the current market price, and it is thus impossible to make any consistent profits through trading with such predictions [46]. It intuitively follows that in a partially inefficient market, where the market price reflects some but not all of the information, one needs the extra information, leading to predictions better than those reflected by the current market price, in order to profit.

Indeed, much of the existing literature on profiting in an inefficient market is based on the idea of well-informed investors, whose superior knowledge of the given domain enables to predict the future prices, or estimate outcome probabilities, more closely than the market, commonly quoting some aggregated estimation of the rest of the trading participants. This in turn enables them to secure profits using common investment strategies such as those of Markowitz [47] and Kelly [32], the performance of which is tightly connected to such an information advantage. While possessing more information leading to superior price estimation indeed enables to profit in this straightforward manner, we argue that in order to make positive returns, it is generally not necessary to estimate the true price better than the market. Instead, there is another and generally easier way to exploit market inefficiencies.

The core principle we utilize in this paper is the, commonly overlooked, inherent advantage of the market taker over the market maker, where the two price estimators are eventually penalized for their estimation errors in a very different manner. Consequently, in order to make profits, the trader does not need to estimate the true price of a mispriced asset better than the market and, instead of predictive pricing accuracy, should generally strive to optimize different performance measures. Specifically, we show that trader’s profits derived from a price estimator can be systematically increased by decreasing its partial correlation with the market, i.e. by decorrelating its residual estimation error w.r.t. the market. While this might seem similar in spirit to the common idea of profiting from using “extra information”, we demonstrate that the trader’s estimates can be easily based on inferior data sources and their information-theoretic value w.r.t. true price can be considerably lower than that reflected by the market. Consequently, the respective trader’s predictive model can thus be considered as “bad” by the means of regular quality measures.

While the proposed concept might seem theoretical in nature, it has important implications on common investment practices based on predictive modelling and portfolio optimization. Particularly, the current systems typically assume the asset price prediction and the subsequent investment decision making as two independent tasks. Namely, at first a statistical model is optimized to predict the future price as closely as possible which, translated into an expected rate of return, forms an input to the subsequent investment strategy designed to maximize some profit-based utility. While this typical workflow has the advantage of decomposing the problem, enabling for a more explicit risk management, we argue that it is considerably suboptimal since the two optimization tasks are not aligned, i.e. the predictive model accuracy optimization is oblivious of the subsequent profit-focused optimization. Consequently, maximizing model price estimation quality will commonly lead to suboptimal final profits. In contrast, with the proposed decorrelation objective, we target the profits more directly. This enables to generate consistent positive returns even with no information advantage and completely inferior price predicting models.

The paper is structured as follows. We introduce the necessary background, ranging from market modelling to portfolio optimization, in Section 2. In Section 3, we provide insights into essential conditions for model profitability, limitations of popular investment strategies, and the inherent market taker’s advantage. Section 4 then introduces the proposed concept of increasing profits through decorrelating from the market, its connection to the Kelly strategy, and translation into a machine learning objective. We then demonstrate the concept in a practical setting in Section 5. Finally, we review the related work in Section 6 and conclude in Section 7.

2 Background

| symbol | description | stock trading | two-way betting |

|---|---|---|---|

| assets being traded on the market | stocks, securities | sport matches | |

| market sides, in two-way markets | buy/sell (bid/ask) | home/away (back/lay) | |

| opportunities to trade assets at time | e.g. buy now | e.g. bet home | |

| relevant data available for opportunity | |||

| fundamental value of an asset | true value | true probability | |

| market maker , or simply “the market” | market maker | bookmaker | |

| market taker , or simply trader | trader | bettor | |

| distribution of market opportunities | all possible trades | all possible bets | |

| r.v. denoting fundamental asset value | price | probability | |

| r.v. denoting market maker’s pricing | price | probability | |

| r.v. denoting market taker’s pricing estimate | price | probability | |

| distribution of the price estimates (values) | |||

| model parameters | |||

| posterior distribution estimator (e.g. ) | |||

| time associated with a trade | |||

| market maker’s spread (margin) | spread | margin | |

| trading returns (profit) | rate of return | return on investment | |

| wealth of the market taker | capital | bankroll | |

| vector of the wealth allocations | allocation | wager |

2.1 Problem Setup

In this paper we assume a standard market setting where two or more parties participate in an exchange of some forms of assets. For the sake of this paper it is not important to distinguish between securities or other financial instruments, and we further refer to all these jointly as assets. While the analysis in this paper covers a wide variety of generic market settings, ranging from commodities to prediction markets, we will mostly consider two diverse enough examples of (i) stock and (ii) sports betting markets to keep the explanation grounded. Similarly, we do not restrict to any particular asset class, which can vary widely from financial derivatives to fantasy sports, however for clarity of explanation, we will consider a standard “bid-ask” setting for the stock, and a corresponding two-way222While we limit the explanation to two-way markets for clarity, the main concept proposed in this paper is directly applicable to -way markets, too. sports betting market, such as predicting the winner of a basketball game. Table 1 provides an overview of the joint notation used throughout the paper and across the two domains.

Opportunity

In a two-way market, each asset tradeable at time corresponds to an opportunity to buy () and sell () the asset, respectively. Given a certain time , this covers bids and asks for a certain stock, as well as bets on the home () and away () team win of a certain sport match. We will further refer to all existing market positions to trade a certain asset at a certain time jointly as opportunities . We further treat each opportunity as an independent trading unit denoted since, for the analysis in this paper, it is not necessary to distinguish the asset or time that each opportunity is associated with333i.e. two opportunities and over the same asset at two different times will be treated the same as two opportunities and over two different assets.. Nevertheless, where necessary, we will distinguish the side of the market an opportunity is to be traded at.

Price

Each opportunity is then associated with a certain price. In a stock market, it is simply the current price set up by the market maker to trade the asset, as used in the usual sense. In the prediction markets, the price reflects the bookmaker’s perceived probability of an outcome to occur. It is also commonly referred to as “odds”444which we use more specifically later to refer to the app. inverse of the probability value (Section 5.1) that determine the potential payouts received from a wager. While the particular calculations naturally differ between monetary prices and odds (Section 2.6), where it is not necessary to distinguish between the two, we will refer to these jointly as prices. We note that the market price of a buying opportunity may be different from the price to sell (Section 2.3), and similarly for the odds.

Fundamental Value

We further assume that each opportunity , i.e. an asset being traded at a given time, has some fundamental true value , which can be expressed as a positive real number and by those means compared to some price estimate (Section 2.5) in the same unit of measurement. For instance in a stock market, a fair market price should reflect the true expected value of the underlying corporation, given the current information context. Similarly in the betting market, fair odds would reflect the true (inverse) probability of the associated outcome to happen. Note that the true value of an asset at time is always the same for both sides () of the market. While the concept of a fundamental value can be seen as somewhat speculative, since it cannot be directly measured, we note that we merely require its theoretical existence for defining market efficiency (Section 2.2) and the related concepts (Section 2.6)555We also commonly use the term true fundamental value interchangeably with the mean future price since, assuming the same information context, the latter can be expected to converge to the former in the partially efficient markets assumed (Section 2.2)..

Makers and Takers

We commonly distinguish two types of the exchange participants as (i) market makers , also referred to as bookmakers, and (ii) market takers , also referred to as traders. The market makers continuously quote both sides () of the market at certain price levels resulting into trading opportunities . By continuously providing such quotes of asset prices, the makers bring constant liquidity to the market. The market takers are then selecting from the existing opportunities to issue specific buy and sell orders. We generally consider the problem analysed in this paper as a two-player game between a market maker and taker , where each player possesses a certain pricing policy over the market distribution of opportunities given by the game (world) environment. We further assume the two players to never switch their roles.

Beating the market

We then aim to design a strategy for the role of the market taker, i.e. some generic trader , to make positive profits against some particular market maker . For example, such strategy would allow a bettor to make consistent long-term profits while wagering against a particular bookmaker. Note that this is a zero-sum setting, where the profits of the market taker are at the direct expense of the market maker, as the fundamental value is objectively the same for all the participants666We use this to remove trivial non-zero-sum settings, where all the participants can mutually profit from trading, from the scope. While we acknowledge that different traders may subjectively evaluate an opportunity differently, e.g. due to distinct preferences for risk tolerance (Section 2.6), this would allow to trivially avoid the hard part of the introduced problem.. This is also the typical setting for a closed system of traders operating within the same time-frame, such as in intra-day trading, futures, options, or prediction markets. The important aspect here is that the only way to make positive profits in this setting is to “beat the average trader”, quoting the market price, by some margin (Section 2.3). In this paper, we then utilize the phrase “beating the market” to refer to profiting in this strictly competitive setting.

2.2 Market Efficiency

In a (strongly) efficient market, the current market price of an asset reflects all existing information, making it impossible for any trader to make consistent profit by outsmarting the market777Note that this does not imply that one needs comparably more information to beat an inefficient market. [16]. Particularly, the price of each opportunity being traded needs to be an unbiased estimate (Section 2.5) of its fundamental true value [59]. Note that this does not imply the price to be equal to the true value , but merely that the error of the estimation is fully due to an irreducible variance which is completely random (Section 2.5) [63]. The inherent randomness of the error then ensures that no trader can consistently beat the market to secure systematic profits.

In real world liquid markets, profit-maximizing traders continuously search for under-priced bids or over-priced asks to secure their profits, pushing the market price to quickly converge to the true value in the process. Thanks to this self-regulating mechanism, the market inefficiencies tend to vanish quickly over time [68, 17]. We note that the idea of an efficient market is a rather theoretical one, since in a market that would become completely efficient, the traders would loose the incentive to search for inefficiencies, in turn making the market inefficient again. Any real world market can thus be hardly considered as perfectly efficient, nevertheless some measurable degree of efficiency, such as statistical unbiasedness of the mean prices (Section 3.4), is typically present in liquid markets [21]. In this paper, we will further consider the most realistic setting of a partially (in-)efficient market where the market price is a very good estimate of the true value , but not a perfect one.

2.3 Market Maker’s Advantage

Market makers are essential to trading by providing constant liquidity to both sides of the market, for which they are typically favored by the exchange operator in terms of fees and commissions. However, the position of a market maker is a difficult one, since she needs to constantly price the assets as accurately as possible. An estimate too low can lead to exploitation on the buy side , and an estimate too high on the sell side , respectively. While the true value is an unknown real number, it would be in principle impossible to avoid exploitation in full.

To improve her position and secure profit, the market maker incorporates a so called spread (margin) into her estimates , causing the offered bid opportunity price to differ from the ask price by some . The spread then works as a safety patch on the market maker’s estimation error, preventing from one-sided exploitations by the market takers aiming at the discrepancy from the true value. A safe strategy for the market maker is then to set her estimate and spread such that , making it impossible for any trader to make any profit, while securing herself an instant profit of for each pair of orders traded at the opposing sides of the book.

However, given that is merely an estimate, it is still possible for the true value to fall outside the region888Naturally, this could be mitigated by increasing the , however a margin set too large will discourage investors from trading, consequently removing the market maker’s profit, too.. To further mitigate possible exploitation by the traders, the market maker can continuously adapt her estimate to the traders’ behavior. That is she can responsively move her estimate once the demand of one side of the market starts to prevail, indicating expected value perceived by the traders, stemming from a possibly erroneous price estimate . In the ideal case where she is continuously able to maintain a perfectly balanced book, so that half of the orders fall on the buy side and the other half on the sell side respectively, she is again guaranteed a unit profit of per trade. Note that the market maker’s profit in this case is independent of the true price .

On the other hand, the market maker can theoretically digress from this purely reactive position to actively speculate against the takers’ opinions and aim at a profit even higher than , at the cost of involving risk stemming from her, possibly erroneous, estimate . This effectively allows the market maker to speculate on the true price, which can lead to higher expected profits in settings where she possesses a superior price prediction model999Since the market maker typically needs an in-depth knowledge of the market to operate, she can often reasonably expect to also possess price estimates superior to the average trader.. This is very common, for instance, with bookmakers in the sport prediction markets [52]. Naturally, the market makers can combine the aforementioned methods.

We note we mostly omit the spread in calculations and simulations further in this paper for simplicity101010except for the actual experiments with real data (Section 5) where the spread is naturally present.. The underlying assumption is that the spread constitutes an independent offset on the market prices (and the resulting profits), and thus does not interfere with the main concepts introduced in this paper.

2.4 Market Modelling

Market modelling generally refers to the approach of fitting a statistical estimator to the available market-related data in order to capture its true distribution . Possession of such a model then enables to answer all sorts of statistical queries, including the essential estimation of the real value of market opportunities .

Data

The market-related data may come from various external sources such as news and economic signals and indicators, as well as from the market itself (e.g. the traders’ behavior). Recall that in an efficient market, all relevant data must be used by the market maker for pricing of each opportunity , however, in practice it is more likely that . The market takers can theoretically use the same data as the market maker , although their sources are typically more limited (e.g. Section 5.2). However, they commonly strive to gain at least some information advantage by obtaining data which are not available to , i.e. , and thus not reflected in the market price. Generally if , such information advantage is completely missing (e.g. Section 5.5), making it impossible to beat the market through superior price estimations111111However, we note that it is still possible to make profits in such a scenario (Section 3.2)., unless using a superior model.

Modelling

The models used to fit the data are generally some -parameterized functions, the properties of which also influence the quality of the estimation. Ultimately, one would strive to model the whole joint distribution over the data , enabling to answer all possible probabilistic queries about the domain, consequently leading to truly optimal investment decision making. Nevertheless, the common investment strategies (Section 2.7) are typically based merely on estimates of returns from the opportunities at hand, which restricts the task to modelling of a conditional of the true value .

For instance at the stock market, an estimate of the true value at a given time can be modelled from a retrospective observation of local evolution of the price time series, i.e. one can use the model to repeatedly predict the (mean) future market price within some time interval (information context) used for trading. Similarly, an estimate of the true probability in the betting market can be derived from repeated observations of the outcomes of the associated stochastic events aggregated over a large enough sample from the market.

Real Value

Generally, the true value of an asset at time can be a distribution itself, such as in the prediction markets. For instance, in an -way betting market where there are possible outcomes, the true value of each asset is the probability distribution over the discrete outcomes. However, in the case of the two-way market with binary exclusive outcomes we use for demonstration, it is a simple Bernoulli distribution with a single parameter . Therefore, the true value of an opportunity can still be considered as a single number , since the value of the complementary opportunity is simply determined by . Consequently, there is a direct correspondence with the bid-ask stock market setting which we exploit for comprehensibility in this paper121212However the proposed decorrelation concept (Definition 4.1) can be directly extrapolated into n-way markets, too.. It follows that we also consider both sides of the stock market to be available, i.e. with a short selling option, for consistency131313although this is also not necessary for the approach to work.. As a result, we can consider every opportunity to be associated with a single real value in this paper.

Mispricing

We assume a market that is not fully efficient (Section 2.2), i.e. there must be some mispriced opportunities which further need to be identifiable by some systematic means. The goal of the traders is then to identify such opportunities where by comparing the market price to their own estimate . Should the market price for an opportunity actually deviate from the true value in a non-random manner, such mispricing can be turned into positive returns. While the concrete calculation of the expected returns differs across the two market settings (Section 2.6), for the sake of this work it does not matter whether we try to predict future price distribution or unknown outcome probability distribution, as in both cases their correct estimation by leads to profits of the trader in the (partially) inefficient market setting assumed. Naturally, this depends on the qualities of the underlying price estimators.

2.5 Price Estimators

A price estimator is generally a -parameterized function mapping some input data associated with an opportunity onto a point price estimate

| (1) |

However, every prediction is associated with a certain level of uncertainty, which is either inherent141414Note that much of the information is often not just missing but principally unavailable, rendering the prediction problem inherently stochastic. or stemming from the missing information at the time of making (). One might thus want to quantify the uncertainty by associating each possible estimate for an opportunity with a probability, resulting into a posterior distribution estimation

| (2) |

where is the estimated price distribution for a single opportunity . Such distribution can be estimated, e.g., from histograms of past prices or event outcomes, marginalized over the same or “similar” conditions () [1]. When a point price estimate is needed, such as when we need to actually trade an asset at a particular price, it is common to take an expected value from , calculated by multiplying each point estimate with its associated probability estimation (or probability density ):

| (3) |

We note that most of the machine learning models provide directly the point estimates, realizing some functional mapping .

Point Estimates

The aforementioned (middle) market price of an opportunity can then be thought of as the market maker’s point estimate of the true price . Similarly, the market taker will also try to predict the actual true value, which we represent with her own point estimate , or simply . By the definition of her role, the market maker continuously evaluates each opportunity . We generally assume that the trader also has the ability to estimate (predict) the true price of each opportunity in the market151515Alternatively, a systematically selected subset can be considered instead.. The trader then must posses her own estimate, i.e. be generally different from 161616since e.g. copying the estimate from the market maker would not lead to any trading incentive., and the true value must be unknown at the time of trading, otherwise there would be no incentive to trade. Note that the true value is often unknown in principle, i.e. even retrospectively, such as the probability in the betting markets, indicating the need for statistical treatment of the problem.

Definition 2.1.

We can now generalize the reasoning about individual opportunities and estimates to reasoning over the whole joint market distribution capturing the relationships between the estimates across a whole set of opportunities generated by the market environment. For each such opportunity , we will thus operate with 3 distinct values we will refer to as (i) the true value , (ii) the market maker’s estimate and (iii) the market taker’s estimate .

Given the uncertainty, it follows that both the and estimates are always going to be to some extent erroneous, where the former guaranties existence of mispriced assets. Note that this is a necessary but insufficient condition for market inefficiencies to exist (Section 2.2).

Optimization

Typically, one optimizes the estimator by tuning its parameters to fit some historical market data relevant for the prediction of the underlying true value . Estimation of unknown parameters from empirical data is then one of the key problems in statistics [22]. There are several views on the problem. One class of approaches is to maximize probability of the observed data with methods such as maximum likelihood or maximum a-posteriori estimation. One can also directly search for an estimator with some desired target properties, such as minimum-variance unbiased estimator [75] or best linear unbiased estimator [26]. A very common methodology is Bayesian estimation, both with or without an informative prior, where one tries to minimize (posterior) expectation of some error function [7]. We take the latter approach, while noting that there are close connections between all the approaches.

Estimation Error

The quality of an estimator can then be expressed through its empirical error over some set of opportunities . Since we assume the role of the trader , we further present error measurements between the true values and the trader’s estimates . Some of the most popular error measures then include the mean square error ():

| (4) |

which is commonly used for regression tasks, such as the prediction of the true price , and the mean crossentropy ():

| (5) |

which is commonly used for classification tasks, such as predicting one of the discrete outcomes (e.g. ) of a sports match. Note that these correspond to the market sides . In the case of the two-sided markets corresponding to binary event outcomes, we can rewrite as

| (6) |

which can then also be also understood as a regression of the underlying value i of each opportunity .

These particular error functions are of special interest as minimizing generally corresponds to maximizing the data (log-)likelihood, while corresponds to maximizing the data likelihood with a linear gaussian model [37]. The crossentropy error is then also closely linked to a common measure of “distance” between probability distributions known as Kullback-Leibler divergence [35], which is defined as

| (7) |

since

| (8) |

where is the entropy of the true value distribution . Considering that true distribution being estimated does not change, its entropy can be considered a constant, rendering the cross-entropy error minimization equivalent to minimizing the the KL-divergence , sometimes also referred to as the relative entropy [7] (see Section 3.1 for further connections).

Bias and Variance

The estimation error can be commonly though of in terms of bias and variance, which are key concepts in the analysis of estimators’ quality [37]. Bias quantifies the expected difference between the price estimate and the true value:

| (9) |

while variance is the expected squared distance from the mean estimate:

| (10) |

While we naturally want to minimize both the quantities, this is typically hard to do as they commonly reflect opposing criteria, giving rise to the so called “bias-variance dilemma”, which is a central problem in statistical learning [22]. A common approach in statistics is to strive for a minimum-variance unbiased estimator, giving good results in most practical settings [75]. The constraint for unbiasedness reflects the necessity for the estimator not to differ systematically from the true price, i.e. the estimation should be correct on average. This constraint is very natural in the proposed market setting, since a systematically biased market price would be easy to directly detect and exploit (Section 3.4). Note also that any minimum-variance mean-unbiased estimator minimizes the , which can be alternatively expressed as:

| (11) |

2.6 Expected Returns

Being able to predict the future price in a stock market, or estimate the true probability in a prediction market, can be directly turned into positive returns in trading. Note we do not explicitly distinguish between the mean future price and true value, as in the fairly efficient market setting assumed (Section 2.2), the market price cannot systematically deviate from the true value for too long. Similarly in the prediction markets, the relative frequency of the observed outcomes will approach the true probability distribution in the long run. Being able to correctly estimate either of these thus guaranties systematic profits, even though actual profits might deviate from the expectation in short term.

Since the total profit is dependent on the actual amount invested, which is yet to be determined by the investment strategy (Section 2.7), the traders commonly assess relative profitability of individual opportunities through measures such as rate of return or, without assuming any time period, return on investment (ROI), which we further denote as . In general, is simply the relative return made from a unit investment w.r.t. the market price and the true value .

The uncertain, stochastic nature of the prediction problem renders the value estimates for a particular as random variables (Section 2.5). Consequently, a return derived from such an estimate will be a random variable, too. Instead of the actual we can thus again calculate with its expectation w.r.t. the used estimator , further denoted as . For the role of a trader , we can then define an expected of an opportunity based on estimator of the true price of some underlying asset as

| (12) |

where is the market price at which the trader executes the buy () or (short-)sell () orders, respectively. For example when we buy a stock for with the expectation to sell it later for on average, our expected ROI is ().

In a prediction market, the market price (odds) directly reflect the relative returns, and so the expected of an opportunity based on a probability estimated by can be calculated as

| (13) |

where is the probability estimated by the bookmaker for the binary outcomes of home () and away () team wins, respectively. For example, a bet of on an outcome with estimated probability , and associated bookmaker’s (decimal) odds of , i.e. yielding a net return of if realized, and a loss of if not, will also result into a ROI of ().

Although the average returns should converge to the true expected returns in the long run, these can still be very different from the predicted expected returns since generally . The discrepancy is of course conditioned by the quality of the predictor w.r.t. the true . The approach to minimize the prediction error (Section 2.5) then seems very natural, and there are also some theoretical guaranties like, for instance, in the case where , i.e. the investor possesses a price prediction model superior to the market maker in terms of cross-entropy, we are guaranteed to make long-term profits with optimal investment routines such as the Kelly strategy (Section 2.7).

Risk and Utility

To explicitly account for the discussed uncertainty involved in trading, the concept of risk assessment has been proposed. This means that instead of direct maximization of the expected returns, one should strive for a balance between the expected profit and risk, stemming from the uncertainty. The risk can then be quantified by statistical means such as the variance of the expected profit [47] or probability of a drawdown [12]. Note that apart from the quantifiable risk, there is also a structural risk stemming from the fact that, similarly to the expected returns, the assessment of risk is based on merely estimated parameters.

Not all investors then share the same preferences to balance the expected profit and risk in the same manner. To incorporate individual preferences into the decision making, the concept of a utility function has been proposed to steer the investment optimization process. A utility function generally maps each alternative onto a real number, defining a total ordering over some set of alternative investments. In our case it is some monotonically growing function transforming the net returns into a new real quantity to be optimized171717Given the stochastic setting, we will again consider expected utility instead.. The concept of risk is then closely connected to utility, as maximizing any concave utility function directly reflects a preference for risk aversion [3].

2.7 Investment Strategies

An investment strategy can be seen as the final step of the traders’s workflow. Given the expected returns from individual trading opportunities present at a time, the trader needs to decide on how to allocate her wealth across the available opportunities in order to optimize her utility , i.e. some requested trade-off between expected returns and risk. Formally, the investment strategy is a function mapping a vector of opportunities associated with the estimated returns onto a wealth allocation vector :

| (14) |

The vector of the wealth allocations , corresponding to portions of some current wealth , is then often referred to as a portfolio over the opportunities . There are several approaches to this problem and we will briefly review some of the most popular ones [41].

2.7.1 Uniform Portfolio

The most trivial investment strategy is a uniform, unit-staking strategy where one independently allocates the same absolute amount on every opportunity with an assumed positive expected return:

| (15) |

Despite being very naive, this strategy is also most robust against estimation errors [58], since the allocation simply remains constant no matter the circumstances. Note that the individual investments are not considered as fractions relative to the current wealth here, and so a small enough unit has to be chosen so that it is possible to invest into all profitable opportunities. Given that the allocated unit is small enough, this strategy will typically also have a very conservative risk profile, nevertheless the expected portfolio profits can be way below optimal. The size of then remains a hyperparameter the choice of which is left to the user.

2.7.2 Modern Portfolio Theory

A more principled approach is that of the Modern Portfolio Theory (MPT) [47] which strives to balance optimally between the expected return and risk. The general idea behind MPT is that a portfolio , i.e. a vector of asset capital allocations over some opportunities , is superior to , if its corresponding expected return (Section 2.6) is at least as great

| (16) |

and a given risk measure of the portfolio w.r.t. the returns is no greater

| (17) |

This creates a partial ordering on the set of all possible portfolios. When combined into a joint utility, we can trade-off the expected profit vs. risk by maximizing the following

| (18) |

where is a hyperparameter reflecting the user’s preference for risk.

In the most common setup, the of a portfolio is measured through the expected total variance of its profit , based on a given covariance matrix of returns of the individual opportunities, which can be again estimated from historical data (Section 2.4). MPT can then be expressed as the following constrained maximization problem:

| (19) | ||||||

| subject to |

Note that the capital allocations sum up to one as they simply reflect fractions of the current bankroll , and they can possibly be negative if short selling is enabled.

The main weakness of MPT is that the variance of profit is hardly a good measure of risk for profit distributions other than Gaussian [60]. Apart from the variance of the potential net returns , different risk measures have been proposed [47], such as standard deviation and coefficient of variation . Nevertheless these all share the same weakness. Generally, there is no agreed-upon measure of risk, rendering the whole concept a bit dubious. Moreover, the strategy only works with the opportunities currently at hand, and thus ignores any knowledge about the actual market distribution .

Sharpe Ratio

Apart from the choice of the risk measure, the inherent degree of freedom in MPT is how to select a particular portfolio from the efficient frontier (based on the choice of ). Perhaps the most popular way to avoid the dilemma is to select a spot in the pareto-front with the highest expected profits w.r.t. the risk. For the risk measure of , this is known as the “Sharpe ratio” [64], generally defined as

| (20) |

where is the expected return of the portfolio, is the standard deviation of the return, and is a “risk-free rate”. We do not consider any risk free investment in our setting, and so we can reformulate the optimization problem as

| (21) | ||||||

| subject to |

2.7.3 Kelly Criterion

The Kelly criterion [32, 71] assumes the investment problem in time181818Note this is in contrast to MPT which assumes the problem in an ensemble of traders at the same time, i.e. through expectation., i.e. it optimizes multi-period investments in contrast to MPT which is concerned only with single-period portfolio returns. It is based on the idea of expected multiplicative growth of a continuously reinvested bankroll . The goal is to a find a portfolio such that the long-term expected value of the resulting profit is maximal, which is equivalent to maximizing the geometric growth rate of wealth defined as

| (22) |

For its multiplicative nature, it is also known as the geometric mean policy, emphasizing the contrast to the arithmetic mean approaches (e.g. MPT) based directly on the expected value of wealth. The two can, however, be looked at similarly with the use of a logarithmic utility function, transforming the geometric into the arithmetic mean, and the expected geometric growth rate into the expected value of wealth, respectively. The problem can then be again expressed by the standard means of maximizing the (estimated) expected utility value as

| (23) | ||||||

| subject to |

Note that, in contrast to MPT, there is no explicit term for risk here, as the notion of risk is inherently encompassed in the growth-based view of the wealth progression, i.e. the long-term value of a portfolio that is too risky will be smaller than that of a portfolio with the right risk balance (and similarly for portfolios that are too conservative). The risk is thus captured by the logarithmic (concave) utility transformation itself.

The calculated portfolio is then provably optimal, i.e. it accumulates more wealth than any other portfolio chosen by any other strategy in the limit of . However, this strong result only holds given, considerably unrealistic, assumptions [32, 71, 57]. Similarly to MPT, we assume to know the true returns while calculating merely with estimates and additionally, given the underlying growth perspective, that we are repeatedly presented with the same opportunities from ad infinitum, making the optimality of the growth-based risk treatment in Kelly likewise a bit dubious. Despite the fact that the given conditions are impossible to meet in practice, the Kelly strategy is very popular, particularly its various modifications to mitigate the aforementioned issues.

Fractional Kelly

The result of the Kelly optimization problem is, for each opportunity, the ideal fraction one is ought to invest to achieve the maximal long-term profits. The fraction thus dictates an upper-bound on the possible profit, meaning that increasing the invested fraction further will actually decrease the long-term profit191919this is due to the assumed multiplicative, growth-based view of Kelly, which is in contrast to the additive MPT, where overbetting would merely increase the risk.. This is commonly known as “overbetting”. Since the true expected return is unknown, however, such a situation might occur even while betting with a fraction assumed to be optimal. Intentionally decreasing the calculated fraction by some ratio then decreases the risk of overbetting stemming from a possibly overvalued estimate. Such an approach is commonly referred to as “fractional Kelly” [45]. Ideally, one should estimate the optimal shrinkage as another hyperparameter [5, 74] based on backtesting performance, however, it is very common to simply choose a fixed ratio such as of the estimated optimal Kelly fraction , commonly referred to as “half Kelly” by practitioners. While there are other remedies to mitigate the risk with the Kelly criterion [12, 70], fractional Kelly is a very effective method which is widely adopted in practice due to its simplicity. In addition to mitigating the overbetting risk, it generally decreases volatility, which also tends to be considerably high with the plain Kelly criterion.

Correspondence to MPT

While Kelly is clearly based on different principles than MPT, there is an interesting close connection between the two strategies. Following [12], let us make an assumption for a Taylor series approximation that our net profits are not too far from zero , allowing us to proceed with the Taylor expansion of the optimized growth as

| (24) |

Now taking only the first two terms from the series we transform the expectation of logarithm into a new problem objective as follows

| (25) |

Note that, interestingly, the problem can now be rewritten to

| (26) | ||||||

| subject to |

corresponding to the original MPT formulation from Equation 19 for the particular user choice of . It follows from the fact that the geometric mean is approximately the arithmetic mean minus of variance [47], providing further insight into the connection of the two popular strategies of Kelly and Markowitz, respectively. While the solution is merely an approximation, it also tends to be more robust to estimation errors than the original Kelly, similarly to the fractional approach.

3 Problem Insights

We have introduced the main parts of a common workflow of a trader , who relies on a statistical estimator to predict true value of market opportunities based on some available relevant data , with the resulting estimates of the expected returns being fed into some subsequent portfolio optimization strategy to produce final wealth allocations . In this Section, we provide some key insights into the problem of profitability from the perspective of the predictive model .

Let us briefly recall the problem setup. We generally consider the problem of profiting from the trader’s perspective as a stochastic game against the market maker . The market maker uses an estimator to continuously price the incoming opportunities . Following some investment strategy, the trader then takes particular and actions (allocations) upon these opportunities , based on her own estimates produced by . Given some distribution of market opportunities , we can then set up the game in terms of three random variables corresponding to the true value, market maker’s, and market taker’s estimates, respectively. The goal of the trader (as well as the market maker) is then to maximize her expected (long-term) profits as measured by some utility underlying the chosen strategy .

3.1 From Accuracy to Profit

The key issue with the optimal investment strategies based on portfolio optimization is that they are inherently relying on accurate estimates of the asset returns. Their performance is then directly stemming from the quality of these estimates - the better the estimates, the higher the utility of the portfolio can be achieved in general. While this holds to an extent for most of the common portfolio optimization strategies202020the correspondence between Kelly and MPT is shown in Section 2.7.3, it is best demonstrated on the optimal investment approach of Kelly.

For simplicity of demonstration, let us consider an idealized case of an -way betting market with no margin (Section 2.3) on the market maker’s odds. Recall that the Kelly strategy is to find wealth fractions so as to

| (27) |

Note that in this idealized case, we calculate the expectation of returns w.r.t. the true distribution . It can then proved [15] that the solution to this constrained optimization problem yields

| (28) |

i.e. the optimal fraction of wealth to invest in each outcome (opportunity) is directly equal to the underlying true value (probability) . Interestingly, we can see that in this case, the optimal strategy for the investor is to completely ignore the market pricing and focus solely on having the true values predicted correctly, in which case she is guaranteed the maximal possible long term profits. This is commonly known amongst Kelly practitioners as “betting your beliefs”. Note that this strong result was derived from and thus it only holds if the true distribution is known or, more precisely, if the error in its estimate via as measured through the Kullback-Leibler divergence (Section 2.5) is zero [15]:

| (29) |

Naturally, it is close to impossible to estimate the true distribution perfectly in practice212121We exclude scenarios with known artificial distributions such as in casino games.. Let us thus extrapolate into more practical settings by relaxing the condition into a non-zero . Given that the optimal fractions should be equal to the true outcome probabilities , let us substitute back into the long term growth rate of wealth which Kelly seeks to maximize as

| (30) |

Now, following the proof from [15], this can be rewritten into

| (31) |

and consequently, using the formula for KL-divergence (Equation 7), back into

| (32) |

showing the important insight that, for Kelly, the growth of wealth of the trader is directly equal to the difference in quality of her estimates over the market prices in terms of KL-divergence from the true values . Consequently, positive returns can only be achieved iff the model of the trader achieves a lower cross-entropy error than the market (Section 2.5). Given the information theoretic interpretation of the relative entropy [35], this is sometimes referred to as the aforementioned “information advantage” of the trader over the market maker.

Implications

Note that this result was derived with the assumption of seeking growth-optimal investments, and its extrapolation beyond that setting may lead to wrong conclusions. Particularly, it is true that one does need a better222222We note we do not distinguish between and other measures of model accuracy here for simplicity. model to make positive profits if committed to invest optimally with Kelly, however, this does not imply that one needs a better model to make positive profits if one does not care about the growth optimality.

The constraint for better model accuracy in classic portfolio optimization techniques is then inherently connected to the notion of risk (Section 2.6), which is embedded together with expected returns into the same quantity being optimized. For instance, in the Markowitz’s model, it is easy to show that even negative return portfolio may be preferred to positive returns should the latter be associated with higher variance. From the Kelly’s perspective, overvalued positive return estimates may actually lead to negative growth due to overbetting (Table 2), and it is also commonly necessary to allocate certain amount of wealth onto opportunities (outcomes) with negative returns to achieve optimal portfolio performance in the long run [73].

Consequently, wrong assessment of the true prices and probabilities associated with either of such opportunities can lead to inappropriate (over-)investments, resulting into a negative overall profit, even in situations where positive returns could be generally achieved otherwise.

3.2 The Essence of Profit

While the performance of common portfolio optimization strategies is tightly bound to the accuracy of price predictions (Section 3.1), we argue that accuracy is not essential for profitability in general. This is best demonstrated by taking the, sophisticated but questionable, notions of risk out of the optimization scope, resorting back to simple strategies such as the uniform investments (Section 2.7.1). Consequently, one can simply base profitability directly on the ability to correctly detect opportunities with positive expected returns (Section 2.6). Note now that whether the expectation from an opportunity is deemed positive depends purely on the comparison between and . This boils down to the renown “buy low, sell high” policy to trade mispriced232323Note we again exclude spread (Section 2.3) from calculations in this Section for simplicity. assets simply as:

| (33) |

Naturally, to asses the actual return from a trade, the true asset value needs to be accounted for. In a stock market setting, the actual return from a supposedly profitable opportunity can then be defined as

| (34) |

and similarly in a prediction market as

| (35) |

Note that the true expected return can clearly be negative and that its absolute value is not dependent of the model’s estimate . However, the ability to correctly recognize the profitable opportunities through the comparison is naturally dependent on the ordering of the estimates w.r.t. and . Note nevertheless that this comparison-based quality is very different from the accuracy-based reasoning. Consequently, even if , a consistent profit can still be made, as we demonstrate through the following simple examples.

Example 3.1.

Assume that a fundamental value of an asset is , with the marker maker estimating the price at , and the market taker’s estimate being . Clearly, the market taker’s estimate is more erroneous here (e.g. ). Since the true value is not observable, she compares her evaluation of the asset to the currently offered , which she correctly evaluates as a profitable opportunity to buy the asset (since ). By buying one unit, her actual expected return from this trade will be positive at (i.e. ).

Example 3.2.

Similarly, assume true probability of an outcome to be , with the bookmaker estimating it at , with the corresponding fair odds set up to , and the bettor estimate being at . Clearly, the bettor’s estimate is more erroneous here (e.g. ). Nevertheless she has no choice but to use her estimate to asses the return on investment, which she correctly estimates as being positive (). Despite being very wrong numerically with her expectation of a ROI, by betting a unit of wealth, she can still expect to obtain the actual positive ROI of .

Note that the trader’s estimates in these examples could have been set arbitrarily larger (within the respective domain), making the corresponding model arbitrarily bad by the standard error measures.

Definition 3.1.

Followingly, let us define a more relaxed, necessary condition of essential profitability of a model simply as the consequent existence of one of the following market opportunities in :

-

1.

the market undervalues the true price, and the model estimates a higher value than the market,

i.e. -

2.

the market overvalues the true price, and the model estimates a lower value than the market,

i.e.

Using sufficiently conservative (small) wealth allocations, investments into either of these cases will lead to systematic profits of the market taker in the long run. On the contrary, no investment strategy can lead to positive profits without such opportunities in the portfolio.

Nevertheless the overall profitability of a model will naturally depend on the relative occurrence of such ’s in the actual market distribution (Definition 2.1). Let us now generalize the essence of profitability, from reasoning about the necessary relationships between individual estimates, to the properties of the whole market distribution . Following on the aforementioned “buy low, sell high” strategy with uniform investments, the expected profitability from a market distribution is clearly

| (36) |

We already know that the fundamental value is a principally unknown random variable and one can thus never perfectly assess the true return from any trade in advance, for which we resort to an estimate . However, the market distribution here is also principally unknown, for which one again needs to rely on statistics while estimating it from historical data as . Consequently, one can estimate the essential profitability of a model w.r.t. market pricing as

| (37) |

As with any investment strategy, the calculated expected returns can be very different from the actual return distribution , depending on the properties of the estimates (Section 2.6). However, profitability of the simple unit investment strategy leads to a much more relaxed and robust condition on the model quality, which is what we exploit to yield positive profits even with estimators of inferior predictive performance.

Drawbacks

We acknowledge that by deflecting from the accuracy-based view and focusing merely on the essential profitability with the unit investments, we downplay the role of explicit optimization of growth and risk in the formal strategies of Kelly and Markowitz, respectively. Nevertheless, as discussed in the respective Sections 2.7.3 and 2.7.2, these formal notions are based on rather unrealistic (wrong) assumptions, which is why additional risk management practices, such as the fractioning (Section 2.7.3), need to be commonly employed with the strategies anyway [45, 44, 74]. Consequently, sacrificing formal optimality w.r.t. unrealistic objectives in order to transition from negative to positive profits does no seem that big of a sacrifice.

3.3 Market Taker’s Advantage

The market maker’s advantage (Section 2.3) is a well-worn concept. However, there is also an advantage of the market taker which is rarely discussed explicitly, but is essential to the traders profitability. While the market maker has the obligation to continuously quote price of both sides of the market (Section 2.5), the taker has the crucial liberty to select only those of the resulting opportunities deemed profitable. That is she is to decide whether and which side of the market to trade the assets once the market maker’s prices have been laid out. As the second player, the difficulty of her task is reduced from the correct price estimation to the estimation of the market price error direction. While this might seem as a similarly difficult problem, the latter is a considerably easier task.

| values ordering | decision () | profit | proportion (in ) | Kelly |

|---|---|---|---|---|

| sell | 1/6 | overbet | ||

| buy | 1/6 | overbet | ||

| sell | 1/6 | underbet | ||

| sell | 1/6 | underbet | ||

| buy | 1/6 | underbet | ||

| buy | 1/6 | overbet |

For demonstration, consider the three values of the true value, market maker’s, and trader’s estimates, respectively, to be laid out completely at random, yielding a uniform market distribution where . The possible situations that emerge from the ordering of in such a setting are displayed in Table 2. Since neither of the estimators possesses any information w.r.t. , both and clearly perform equally by the means of arbitrary statistical estimation measures (Section 2.5). While one might thus expect this to be a neutral trading setting for both the sides, interestingly, the market taker would already be able to make a substantial profit with uniform investments by correctly identifying of the profitable opportunities.

Intuitively, this demonstrates a simple fact that it is generally more likely to overestimate an undervalued estimate than to further underestimate it, i.e.

| (38) |

and vice versa for an overvalued estimate:

| (39) |

Note, importantly, how this property of the completely uninformative is conveniently aligned with the essential profitability of the trader’s model (Definition 3.1). The concrete proportions of the individual situations will naturally depend on the particular distribution , nevertheless the property holds very generally for unskewed distributions with unbiased estimators (Section 3.4). Note the difference from the standard model accuracy measures which would all evaluate both models equally in . Nevertheless from the perspective of profitability, the situation is very different since, as opposed to the market maker, the market taker is not penalized for estimation errors in these two situations that emerge more often than not. Consequently in , the trader is in an inherent advantage of , which can be directly turned into the corresponding profits.

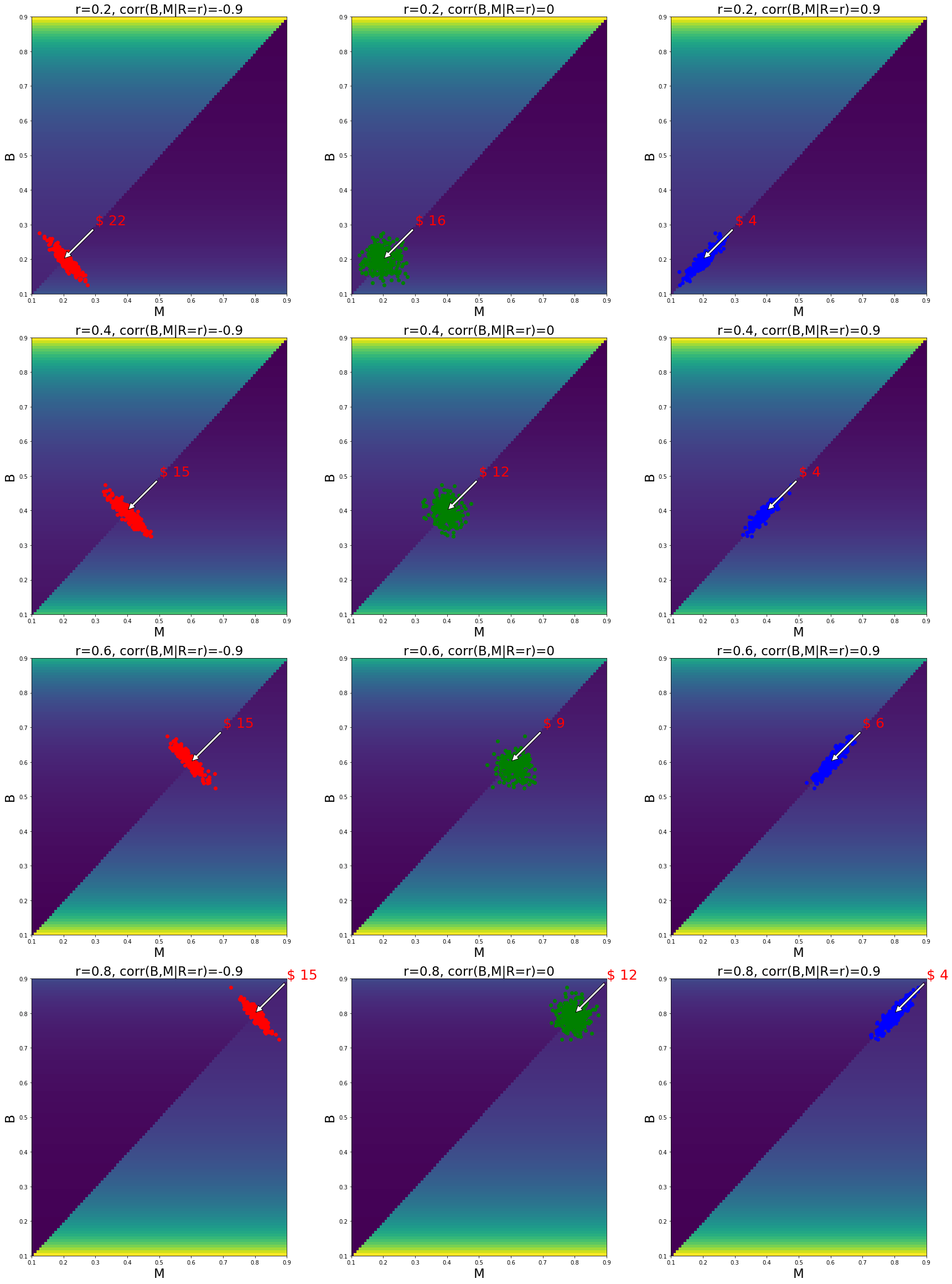

It is perhaps more instructive to demonstrate the concept on a particular level of true value . Without loss of generality, let us consider all opportunities with a real value being traded in an ideal two-way market (without spread). We can then plot a 2D projection of the market distribution by conditioning it as , and visualize the essential profitability (Definition 3.1) of the corresponding sub-regions of the distribution. The result is displayed in Figure 1. We can observe that the distribution of the profitable regions (green) is clearly in favor of the trader, and that the potential returns progressively increase with the error of the market maker, i.e. the distance of from .

Note that here we did not yet assume any particular (non-uniform) distribution of estimates, and this inherent advantage of the trader is thus completely oblivious of any information advantage as well as any other property of the price estimators. Rather, it stems purely from the unequal roles of the market maker and taker . Consequently, should they e.g. switch roles with the same estimation models (), the advantage would stay exactly the same on the side of the market taker .

3.4 Distribution of Estimates

While demonstrating the concept of the trader’s advantage, the uniform distribution of estimates with completely uninformed players from Section 3.3 seems rather unlikely in practice. In real world markets, the values are not going to be independent, but rather correlated with each other, since and are typically based on similar information sources and both try to model with similar techniques (Section 2.4). Let us now review common properties of the more realistic market distributions of these estimates.

Bias

The market makers are typically very good at being close to the real price, and we can assume their estimates to be unbiased w.r.t. true value , or, more formally:

| (40) |

which means that they are not systematically deviating when measured against the true value alone. Should a market maker be biased in this manner242424biased by more than in practice (Section 2.3)., it would be extremely easy to exploit her merely by trading all opportunities on the corresponding side of the market. Moreover we can reasonably assume her to be point-wise unbiased at each particular price level , i.e.

| (41) |

If that was not the case, the market maker would again be easily exploitable by correspondingly trading all possible assets within a certain price range , i.e. by buying all assets in price ranges where the maker systematically undervalues the assets, and vice versa for selling in overvalued price ranges. One can typically check from historical data that the market makers are not biased in this simple manner in any reasonably efficient market252525as we do in experiments in Section 5.3.1. Note that the unbiasedness is only one of the conditions for a fully efficient market (Section 2.2). There is generally no reason for the market taker to be biased in this trivial way either, unless a systematic error is present in her model , or she reversely reflects the market maker’s bias to exploit it.

Variance

Given the assumption that the models behind and are both unbiased estimators of , we can now focus merely on their (co-)variances. It is a common practice in statistical estimation of functions for one to look for an estimator with the smallest variance among the class of unbiased estimators (Section 2.5). Since we are working with function estimators, we are not interested in the total variance of the estimations , which includes variance due to variations in the true price itself as

| (42) |

but merely in the first term capturing the expected variance left w.r.t. predicting . Given the assumption of the point-wise unbiased estimates, the conditional variances w.r.t. are then equal to the covariances of the models, i.e.

| (43) |

Given the unbiasedness, these co-variances then directly reflect the quality (accuracy) of the underlying models of the market maker () and market taker (), respectively.

The last degree of freedom in terms of covariances in is the relationship between and , i.e. (). While the other two covariances have a clear common interpretation, the is more intriguing, but is also essential to the proposed profitability of inferior predictive models (Section 3.1). As we have seen in the case of the uniform market distribution , where both the players possess the same amount of information w.r.t. the true price, corresponding to the same accuracies of and , the trader is always in advantage. However not all distributions with equally informed players are as such, as demonstrated by the following example.

Example 3.3.

Assume a scenario where both the trader and market maker possess the exact same model. Clearly, their information value, accuracy and all statistical measures will be exactly the same, just as in the case of the uniform distribution . Nevertheless, the trader will not be in an advantageous position anymore. Since all her estimates coincide with the market price , it is not possible to detect any profitable opportunities where , even if they exist in the market distribution . Hence, the profitability of the trader in this case is clearly zero.

From the statistical viewpoint, one can note an underlying difference between the two example distributions in the third covariance term . Whereas in the uniform distribution, the two variables were completely independent, i.e. , here they are equal and thus display maximal possible covariance (). While this anecdotal reference to the connection between profitability and is rather informal, we analyse it in detail in the next Section 4.

4 Increasing Profit through Decorrelation

Recall that we have a two-way market with opportunities of some fundamental value , being priced by the market maker as and taker as , resulting into some market distribution of estimates (Definition 2.1). Let us now consider the context of the common properties (Section 3.4) of such market distributions , allowing assessments of model performance in terms of expected returns w.r.t. the distribution . Particularly, we will explore the aforementioned statistical relationship between the market maker and taker . To further standardize the relationship study, i.e. to take the individual variances of and out of scope, we now switch from covariance to correlation .

Definition 4.1.

We use the term decorrelation to refer to the concept of decreasing the partial correlation between a price estimator of the trader and the market maker w.r.t. the real value across opportunities endowed with some market distribution (Definition 2.1).

The main goal of this Section 4 is to show that enforcing smaller262626Note that utilize the term “decorrelation” to refer to decreasing the correlation even below zero. partial correlation of a price estimator generally increases its essential profitability (Definition 3.1) within common market distributions.

4.1 Unbiased Estimators

Let us first consider the common setting of unbiased price estimators, the reasoning behind which was introduced in Section 3.4.

Theorem 4.1.

The essential profitability (Definition 3.1) of an unbiased estimator with the lowest partial correlation with the market is maximal. Consequently, no deviation from such a model can thus increase the profitability further.

Proof.

Now for and an arbitrary , the probability distribution collapses into a linear function of the form

| (44) |

where the is set so that the mean values of both the marginals and are at (unbiased). The mean of the distribution thus lies on the line:

| (45) |

Clearly, since , we have also implying a negative slope of the function line. There are consequently only 2 possible price estimate orderings (regions in Figure 1) for all , both of which are profitable, as follows:

-

1.

implying stock returns , or likewise for betting

-

2.

implying stock returns , or likewise for betting

Note again that the individual values of returns do not depend on the value of but merely on the value order. From the assumed role of the trader , the only possible changes to the distribution (and profit) can be made via changes in her model estimates . However, any potential deviation from this distribution (line) with can only result into one of the following ordering (region) transitions:

-

1.

can change to either:

-

(a)

implying no change in the returns , or likewise

-

(b)

implying decrease in the returns to , or likewise

-

(a)

-

2.

can change to either:

-

(a)

implying no change in the returns , or likewise

-

(b)

implying decrease in the returns to , or likewise

-

(a)

ergo no deviation from can increase the profitability any further. ∎

Note that this also means that we cannot increase the returns even via transition into a perfect estimator with both , i.e. a perfect model which always returns the correct answer in a deterministic fashion (and for which the partial correlation would be undefined). This means that for the purpose of the essential profit generation (Definition 3.1), the variance of the model no longer acts as an error since it is completely turned into our advantage. Note this is in direct contrast to a correlated investor who, given a variance higher than the market maker, is doomed to obtain completely negative returns272727We also note that the transition between the two corner cases is somewhat smooth w.r.t. the returns for common market distributions, such as the elliptical distributions used for visualization.. A visualization of the correlation effect on the returns, with an example elliptical market distribution for the given setting, is depicted in Figure 2.

4.2 Biased Estimators

While common, the assumption of point-wise unbiased estimators might be seen as too strict in practice. The market maker is very unlikely to be overly biased, due to its constant exposure to the traders, who would likely exploit such easy opportunities (Section 3.4). Nevertheless the market takers are generally free to come up with all sorts of models. Let us briefly review the situation where the trader’s model , which we seek to optimize, is more biased than w.r.t. , i.e. .

In this setting, one can craft counterexamples showing that with is not universally the most profitable model anymore282828For instance, consider a distribution where the model is biased w.r.t. by some as (46) This -biased model is set to make maximal possible profit, and decreasing its correlation with will actually hurt its performance. However, achieving such a distribution of estimates is close to impossible in practice, as it is carefully crafted w.r.t. the unknown value of . Consequently, this scenario is highly unstable w.r.t. as well as variance of , a decreasing of which will paradoxically lead to complete loss of all returns.. While not the universally best possible model, a decorrelated will still perform very well in practice here. Particularly, it will be consistently better than a highly correlated model, even if the latter has a lower variance . Interestingly, it is also better than a model with zero variance (vertical line), i.e. given some bias, we are able to turn the variance into an advantage by decreasing correlation with . Lastly, the minimal correlation will be also typically better than no correlation for common elliptical or uniform conditional distributions. A visualization of this setting, where , is displayed in Figure 3 for an example elliptical distribution. Note that the same reasoning is also applicable to cases where the .

4.3 Having a Superior Model

The primary motivation behind the concept of lowering the correlation with the market is to make profits with models of inferior quality, which would commonly yield negative profits otherwise. We argued that such a situation is common, since the market (maker) price tends to be a very good estimate of the true value in any fairly efficient market (Section 3.4). Nevertheless, for completeness, let us consider the opposite case of having a superior model, i.e. a situation where . Following the statistical decomposition of estimation errors in terms of bias and variance (Section 2.5), let us separately consider two cases of such superiority through a model with (i) lower variance and (ii) lower bias.

Superior Variance

For a superior model with a lower conditional variance , the concept of decorrelation (Definition 4.1) no longer works as a consistent profit enhancement, even for common, realistic market distributions. Particularly, decreasing the correlation can actually decrease the returns in many scenarios. We again depict the concept on an example elliptical distribution in Figure 4. The variances of the estimators are exactly opposite to those from Figure 2. We can see that the returns with an independent model are lower than those of a highly correlated model . Note however that the decrease of returns in this case is smaller than the increase in the opposite case (i.e. shift from to in Figure 2). Finally, the profits of are still maximal.

Superior Bias

We have argued for the practical necessity of a market maker not to be systematically biased in Section 3.4, which leaves a little space for the trader to beat the market in terms of . Nevertheless it should be acknowledged that in the unlikely case that the market maker indeed is more biased than the trader, the concept of decorrelating the estimates for increased profits breaks down severely. The situation is depicted in Figure 5. We can see that in this setting, decreasing can easily work in a directly counterproductive fashion by consistently decreasing the profits.

Importantly, however, it should be noted that with a model that is superior by either means, i.e. where , there is no need in trying to decrease to make profits, since such a model needs no help with that to begin with. This can be conveniently detected in advance by measuring and trading the model with standard investment strategies (Section 2.7).

4.4 The Problem with Kelly

The scenarios we have demonstrated so far operated with the simple uniform investment strategy (Section 2.7), which allowed us to generate profits through decorrelation (Definition 4.1), even with models of inferior accuracy w.r.t. market. As indicated in Section 3.1, let us now explain why this cannot be done with the, more sophisticated, Kelly investment strategy.

We have shown that the growth of wealth with the Kelly strategy is directly equal to difference between the KL-divergence of the market maker from the true distribution and the trader from the true distribution , respectively, in Equation 32. It follows that a Kelly trader does not care at all about the particular relationships between which are essential to profitability (Section 3.2), since the only thing that matters is how close are our estimates to the true distribution as compared to the bookmaker. The two principally different views of the market distribution properties are depicted in Figure 6.

Consequently, it thus does not matter whether the opportunity seems to have a positive or negative expected profit, since an optimal Kelly trader will bet an amount derived merely from the expected growth corresponding to the information advantage w.r.t. . Given the knowledge of the true value distribution , this provably leads to more wealth than any other strategy. It is tempting to believe that it generally provides an upper bound to the amount of profit that can be made in any scenario. Nevertheless, such property cannot be extrapolated to the settings where we lack knowledge of the true probabilities, such as in the real world trading, which we demonstrate on the following example.

Example 4.1.

Consider a simple scenario of Kelly betting on a match (asset) with two equally probable exclusive outcomes , and the two corresponding opportunities priced by the bookmaker and the trader equally as follows

| (47) |

In this example, we again omit the bookmaker’s margin for simplicity and so, following the derivation from Section 3.1, the optimal vector of fractions to bet on the outcomes would be

| (48) |

Since the two estimates of and coincide, there is clearly no information advantage of the trader and consequently zero profit to be made with Kelly. And the situation is the same for any other strategy, too, since the expected profitability of the opportunities, following the expected profit definition from Equation 13, from the perspective of the trader is simply zero

| (49) |

Now consider altering the scenario by decorrelating the estimates of the trader as follows

| (50) |

Despite switching the estimates, we can clearly see that both the bookmaker and the trader are still equally distanced from the true value (by the means of as well as any other possible metric), leading again to no information advantage and, as expected, to a zero expected growth of wealth (Section 2.7.3):

| (51) |

Nevertheless, the essential profitability of the opportunities from the perspective of the trader is now

| (52) |

and betting uniformly (Section 2.7.1) some unit on the first opportunity , the trader would make a consistent profit of

| (53) |

despite it being different from her estimated .

The inability of Kelly to make profit in such profitable scenarios follows from its growth-based view of optimal investments (Section 2.7.3). While maximizing the growth , less than optimal investments are just as harmful as over-investment, despite the latter leading to definite ruin while the former only leads to sub-optimal growth. To distinguish between the two arguably different types of risk, various modifications of the Kelly criterion have been proposed to reflect the natural preference for avoiding the ruin at the cost of sub-optimal growth.

4.4.1 Fractional Kelly

Perhaps the most common remedy to mitigate the risk stemming from the erroneous estimates is fractional Kelly (Section 2.7.3). Let us demonstrate the effect of this risk management practice on the introduced setting from Example 4.1 as follows.

Example 4.2.

Being aware of the uncertainty in her estimates, the Kelly trader now decreases the optimal fraction by one-half, popularly referred to as “half-Kelly” betting. Considering the first scenario of coincidental estimates from Equation 47, the invested fractions are now thus decreased by half as

| (54) |

However, the growth of wealth, accounting for the half of it being held separately, stays inert at zero since

| (55) |

In words, the trader is still under-betting the the first opportunity , which is profitable, while putting a larger amount on the second opportunity , which is loss-making. Decreasing the fractions then cannot change the simple fact that the opportunity is not recognized correctly by the estimator w.r.t. essential profitability (Definition 3.1).

Consider now the latter scenario of the decorrelated estimates laid out in Equation 50. The invested fractions are again cut by half as

| (56) |