Spherical clustering

in detection of groups of concomitant extremes

Abstract.

There is growing empirical evidence that spherical -means clustering performs well at identifying groups of concomitant extremes in high dimensions, thereby leading to sparse models. We provide one of the first theoretical results supporting this approach, but also demonstrate some pitfalls. Furthermore, we show that an alternative cost function may be more appropriate for identifying concomitant extremes, and it results in a novel spherical -principal-components clustering algorithm. Our main result establishes a broadly satisfied sufficient condition guaranteeing the success of this method, albeit in a rather basic setting. Finally, we illustrate in simulations that -principal-components outperforms -means in the difficult case of weak asymptotic dependence within the groups.

Key words and phrases:

Angular measure; concomitant extremes; dimension reduction; principal components; spherical clustering.1. Introduction

Statistical analysis of high-dimensional data typically relies on various sparsity assumptions, unless structural domain knowledge is available. In the study of extremes, sparsity is especially important since the number of extreme observations is small by definition. The recent survey of Engelke and Ivanovs, (2021) reviews different notions of sparsity and the available tools in the context of extreme value statistics. Fundamental here is the notion of concomitant extremes (Chautru,, 2015; Goix et al.,, 2016), where the focus is on the groups of variables which can be large simultaneously while others are small. Importantly, extremal dependence can be modelled separately in these groups and then combined into a mixture model, thereby leading to dimension reduction.

Mathematically speaking, our interest is in the identification of the lower dimensional faces of charged with mass by the so-called exponent measure. Alternatively, we may look at the faces of the positive simplex charged with mass by the angular (spectral) probability measure. This task, however, is highly non-trivial since only approximate angles coming from a pre-limit distribution, which normally also puts mass on the interior of the simplex, can be obtained in practice.

Various approaches to identification of concomitant extremes and respective maximal sets have been explored in the literature, see Goix et al., (2016, 2017); Simpson et al., (2020); Chiapino et al., (2020); Meyer and Wintenberger, (2021); Jalalzai and Leluc, (2020). One of the basic ideas is to use a certain neighbourhood of a given face and to assign the respective mass to this face. The simplest method (Goix et al.,, 2016) amounts to thresholding the entries of the rescaled extreme observations. Such thresholding, however, often produces a large number of faces with few corresponding observations, see the discussion in Goix et al., (2017) and a numerical illustration in Figure 5 below. Certain grouping of faces is then necessary, see Chiapino et al., (2020).

A different approach was proposed by Chautru, (2015), and it amounts (ignoring a preliminary dimension reduction step) to spherical -means clustering (Dhillon and Modha,, 2001) of the approximate angles. Consistency of spherical clustering for a general cost function has been recently established by Janssen and Wan, (2020), who also advocated interpreting centroids as ‘prototypes of extremal dependence’. Each centroid, or cluster, can then be attributed to a certain face. One way of doing this is to use thresholding to define respective faces, which has been employed in the review of Engelke and Ivanovs, (2021) to obtain interpretable results for a real world 68-dimensional dataset. Importantly, this method can be seen as a reverse threshold-and-group approach. Finally, our problem is very different from those addressed by subspace clustering techniques for high-dimensional data (Gan et al.,, 2007, Ch. 15), which are popular in computer science.

Clustering in detection of concomitant extremes and prototypes of extremal dependence may seem intuitive to some extent, and there is growing empirical evidence in support of this method. The drawback is that there is no theoretical justification, apart from the consistency result by Janssen and Wan, (2020). Building upon this result, we provide some basic theory showing that the spherical clustering procedure must indeed work in certain cases. However, we also identify some pitfalls and show that an alternative cost function may be more appropriate for identification of concomitant extremes. It results in a novel spherical -principal-components (-pc) clustering algorithm (a similar approach in a different context was considered in the empirical study of Hill et al., (2013); see Remark 3.2 below). The name derives from the fact that the Perron–Frobenius eigenvectors of certain non-negative definite matrices with non-negative entries are used instead of the means in the updates of the algorithm. Interestingly, these matrices are the analogues of the cross-moment matrices used by Cooley and Thibaud, (2019) and Drees and Sabourin, (2021) in their principal component analysis of extremal dependence, whereas the bivariate case has been considered by Larsson and Resnick, (2012) in a different context.

Our main results, Theorem 4.2 and Theorem 5.2, provide sufficient conditions guaranteeing the success of clustering in detection of concomitant extremes, albeit in a rather basic setting, when the corresponding groups of coordinates are disjoint. Importantly, -means fails in some fundamental cases, whereas -pc is much more robust. Our counterexamples provide further intuition about the applicability of both methods. We conclude with a simulation study which confirms our findings and show that the -means algorithm, unlike -pc, has serious problems in the setting where many pairs in the groups of concomitant extremes exhibit weak asymptotic dependence. Arguably, this is one of the most important settings from the applications point of view (davison2013geostatistics). In many other cases the results are almost identical, including the 68-dimensional dataset of river discharges and, to a lesser extent, the dietary intake data from Janssen and Wan, (2020), which are analysed in Subsection 6.4 and the Supplementary Material, respectively.

2. Preliminaries on multivariate extremes

2.1. The angular distribution

Here we recall some elementary theory of multivariate extremes needed in this paper, and refer the reader to the monograph Resnick, (2008) and the surveys of Davison and Huser, (2015); Engelke and Ivanovs, (2021) for further reading. It is a common practice in extremes to first standardize the marginals and then study extremal dependence. Thus we assume that a random vector , of interest has unit Fréchet marginal distributions: for , . The fundamental regularity assumption on , called multivariate regular variation, can be stated as the weak convergence of the normalized conditional on its norm being large:

| (1) |

where the distribution of is called angular or spectral. This distribution is our main object of interest as it characterizes extremal dependence. It must be noted that any norm can be used here, but we choose the Euclidean norm so that lies in , which is convenient when considering angular dissimilarities in Section 3. Due to marginal standardization, the mean of must point to the centre of :

| (2) |

This property has a certain balancing effect which will come in use later.

The random vector satisfying (1) and having unit Fréchet marginals is in the max-domain of attraction of a max-stable distribution uniquely specified by the angle . It is said that admits asymptotic independence (complete dependence) if the limiting max-stable vector has mutually independent (completely dependent) components. The distribution of the corresponding angle is then as follows:

-

(i)

Asymptotic independence: the distribution of has mass at every standard basis vector.

-

(ii)

Asymptotic complete dependence: deterministic .

A common measure of pairwise asymptotic dependence is the tail dependence coefficient:

where 0 corresponds to the asymptotic independence in (i) and 1 to the complete dependence in (ii). These are the boundary cases also in other senses as demonstrated by the following result.

Lemma 2.1.

The constant in (2) satisfies , where the lower bound is achieved iff case (i) holds, and the upper bound is achieved iff case (ii) holds.

Proof.

Note that and take expectation to get the lower bound. The upper bound follows from . Equality in the latter readily implies that all are constant, whereas equality in the former implies that a.s. for all . ∎

In applications it is common to standardize the observations using the empirical marginal distribution functions and then to choose threshold large, but such that sufficiently many approximate angles are obtained for the statistical analysis of extremal dependence. This is exactly the procedure used by Janssen and Wan, (2020), whose consistency results we will employ in the following. The only difference is that we use unit Fréchet marginals instead of standard Pareto, but these are tail equivalent and no changes in the theory arise.

2.2. Concomitant extremes

In high-dimensional settings it is of crucial importance to identify the non-empty sets of indices such that , and the respective probabilities. We will focus on the maximal sets – those not included in other such sets. Let us define the corresponding faces of :

| (3) |

According to (2) the probabilities are positive for every , and so every index must be contained in at least one maximal set. The problem at hand is sparse if the cardinality of such sets is much smaller than and their number is manageable.

The case (i) of asymptotic independence corresponds to faces of dimension 1. A more interesting situation occurs when the indices can be partitioned so that asymptotic independence is present between the (disjoint) groups, but not necessarily within these groups. Then any prototype of extremal dependence must belong to some group and, ideally, each group should have a prototype, see Section 4 for further discussion. Thus we arrive to a basic test scenario, whereas applicability of the clustering method is much more general:

Assumption A.

There exists and a partition of the index set such that the union of the respective faces contains the support of the angular measure: . Without loss of generality we assume that the indices in are smaller than those in for all .

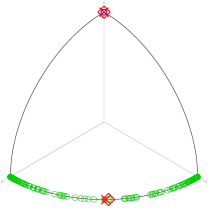

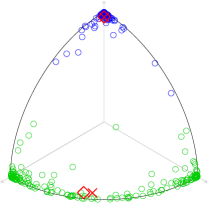

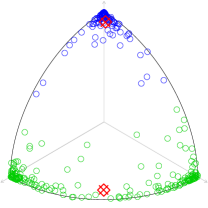

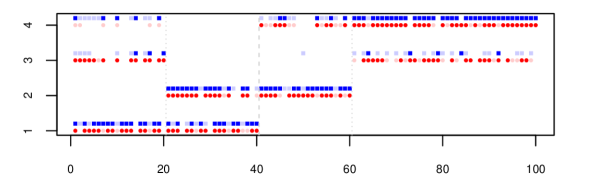

It may help to also assume that the above partition is unique, but this is not strictly required. The corresponding faces are mutually orthogonal: for all , and , and the only common element is the origin. Even in this scenario identification of the groups of concomitant extremes using approximate angles may not be straightforward. For a low-dimensional case of and the partition , Figure 1 depicts a sample from the exact angular law and two samples from its approximations as could arise in practice for different threshold levels . In these examples both clustering methods produce similar centroids (crosses for -means and lozenges for -pc) which are close to the respective faces, and thus the latter can be easily identified.

Let us define the corresponding submodels for which have the law of the restriction of to the indices in conditional on , and let be the respective probabilities. Under Assumption A we thus obtain a complete description of the law of as a mixture model. Furthermore, satisfies (2) with and so it is a legitimate angular model in dimension . Finally, we define the cross-moment matrices

| (4) |

where the latter is a block diagonal matrix with on the diagonal. Note that every is a non-negative definite matrix with trace , since . An expression of for the Hüsler-Reiss distribution is given in Supplementary Material, whereas Remark 3.5 provides connections to the literature on PCA for extremes.

3. Spherical clustering

3.1. Spherical dissimilarities and Voronoi diagrams

In this section we consider an arbitrary random variable not necessarily satisfying (2) and return to concomitant extremes in Section 4. Spherical clustering for a given integer amounts to the following stochastic program:

| (5) |

where is a continuous dissimilarity (cost) function. Here we assume that the dissimilarity function has the form for a strictly increasing continuous (reward) function . In words, the aim is to find centroids such that the expected dissimilarity of and the closest centroid is minimal. It is noted that the objective function is continuous in and the set is compact, which readily implies that the minimum must be attained. Uniqueness up to a permutation, however, is not guaranteed.

There is a wide choice of popular angular dissimilarity functions used in a variety of contexts (Palarea-Albaladejo et al.,, 2012), but the above form has an appealing property

where . Thus, for the given points the positive part of the unit sphere will be partitioned into sets by means of hyperplanes in passing through the origin:

| (6) |

For concreteness, here the equality is broken in favour of the smallest index. Note also that these form the Voronoi diagram of with respect to the Euclidean norm.

The most popular examples of such cost functions are the scaled Euclidean distance, the angular distance and cosine dissimilarity , plus we additionally define corresponding to the quadratic reward function :

| (7) |

The angular distance yields the angle between and as the fraction of the right angle , and such a distance will be useful in numerical experiments below. In clustering one of the most important properties is the simplicity and interpretability of the resulting procedure, and thus we will focus our attention on with . In this case the above clustering problem (5) reduces to maximizing the expected maximal reward . For we retrieve spherical -means clustering (Dhillon and Modha,, 2001), which is intimately related to classical -means. Finally, leads to what we call spherical -pc clustering, which is described below.

Remark 3.1.

Importantly, for we have , which implies higher cost for two almost orthogonal vectors as compared to the case. This provides some heuristic support for using the -pc method instead of -means in identification of groups of concomitant extremes.

Remark 3.2.

While revising this work, we discovered that a similar algorithm had been considered in Hill et al., (2013) under the name ‘perpendicular spherical -means’. The same cost function is used in this empirical work without observing a link to principal eigenvectors.

3.2. The optimal centroids and partitions

Let us provide some basic results underlying the spherical clustering procedure for the linear and quadratic reward functions. In the first case we will need the normalized means of restricted to the sets :

| (8) |

where the partition is given by (6) for an arbitrary choice of . In order to avoid division by 0 we take when . In the second case we define matrices

| (9) |

Note the difference between and defined in Section 2. These are non-negative symmetric matrices, which are also non-negative definite. We will be interested in the largest eigenvalue and the corresponding eigenvector of , assumed to have unit norm: . There may be more than one such eigenvector, but at least one of them must have non-negative entries by the Perron–Frobenius theorem, and we choose such. Hence we may assume that . If the matrix is positive or at least irreducible, then such a vector is unique.

The first result forms the basis of the clustering procedure, see (Dhillon and Modha,, 2001, Lem. 3.1) for the sample version in the case of the spherical -means algorithm.

Proposition 3.3.

Proof.

By definition of and we readily obtain

where the last inequality follows from the fact that only one term among is non-zero.

By definition of we have

| (10) |

where we use the standard fact that the quadratic form is maximized under the constraint by the principal eigenvector and the maximal value is given by the corresponding eigenvalue, see, e.g., (Overton and Womersley,, 1992, Thm. 1). It is left to observe that

| (11) |

since only one term among is non-zero. ∎

The above result suggests an iterative procedure for finding the optimal centroids where the updates , respectively , of the current centroids are used. This procedure will normally converge to a local maximum for the linear, respectively quadratic, reward function. By using a number of different starting centroids we may hope to discover the global maximum and thus solve (5) for the dissimilarity functions and . This is exactly the spherical -means procedure when and hence the means are used.

Importantly, instead of centroids we may optimize over partitions of :

Corollary 3.4 (Duality).

Proof.

The proof of the two cases is analogous, and we consider only the second case. Let be an optimal solution to the left-hand side problem, which exists. By the maximality and (10) we find that the optimal value is . So the supremum over partitions is no smaller. Take an arbitrary partition with the respective and observe that the associated value cannot exceed the maximum over the centroids, see (11). Hence the supremum over the partitions is achieved and the optimal values coincide. ∎

Remark 3.5.

Matrix has been used by Cooley and Thibaud, (2019) and Drees and Sabourin, (2021) in their principal component analysis of extremal dependence. Finding the best direction for corresponds to minimizing the expected dissimilarity:

In the trivial case of the corresponding centroid is the main PCA direction. No such links seem to exist for .

3.3. Spherical -principal-components algorithm

Here we state the algorithm for a discrete distribution putting mass at points , not necessarily distinct. Clearly, this setting includes the empirical law. Only a single iteration is described, since the rest is standard. R code is available at https://github.com/jev-ivanovs/spherical_clustering.

Algorithm 3.6.

Spherical -principal-components clustering – a single iteration.

| Input: the sample and current centroids . |

| Compute matrix of dot products |

| Let be the mean of row-wise maxima of |

| For each row of find the index of the (first) maximal value and store them in |

| For to |

| Calculate |

| Find the principal eigenvector of |

| Output: new centroids and the old value . |

It is easy to see that the running time complexity of this algorithm is , where is the complexity of finding the principal eigenvector of non-negative symmetric matrix, see Wang et al., (2018) for some basic algorithms and recent developments in this field. Assuming that the spectral gap is bounded away from 0 we may take , making -means and -pc comparable in the common situation when .

4. Spherical clustering and concomitant extremes

4.1. Problem formulation

The main goal of this work is to provide some theoretical results supporting clustering for identification of concomitant extremes. The dissimilarities and are continuous and hence the consistency result (Janssen and Wan,, 2020, Prop. 3.3) readily applies to both types of spherical clustering described above. In words, for high enough threshold yielding sufficiently many large observations we may expect that clustering of the approximate angles will result in centroids close to the true centroids of the angular distribution, given the latter ones are unique up to a permutation. Thus, we may focus on clustering of the exact angular distribution, that is, the distribution of . The balancing condition (2) will play a crucial role on this way. Some results are still true without this condition and so we stress when it is indeed required.

The basic test scenario is stated in Assumption A, and it gives rise to the following question:

| Will spherical clustering of under Assumption A produce one centroid in each face? |

We will see that this is not always the case, and our goal is to identify simple interpretable conditions implying such a result. It turns out that spherical -pc is preferable to spherical -means in this setting, since it is more robust and also allows for a substantial theory.

Figure 1 illustrates spherical -means clustering in the simple case of and different approximation levels of the angular distribution. Spherical -pc clustering results in exactly the same assignment of all points (blue/green) to the clusters. The centroids for the two methods are close to each other and also close to the respective faces, and in the case of sampling from the exact law they are, in fact, on the faces and .

4.2. Fundamental observations

A partial answer to our problem is given by the following characterization result, which readily follows from the clustering duality in Corollary 3.4. The difficult part is in establishing simple sufficient conditions, which we address in Theorem 4.2 and Theorem 5.2. Recall the definition of the submodels in Section 2 and that is the set of all partitions of into Borel sets (or sets of the form (6)).

Proposition 4.1.

Proof.

We focus on -means, since the other result is analogous. Note that the left-hand side of (12) is just and so by Corollary 3.4

yields an optimal set of centroids, since the given disjoint sets can be extended to a partition of . These indeed satisfy .

Next, suppose that some are optimal, and let be the sets in (6), which then yield the maximum. The faces are mutually orthogonal and so every vector in the support of also belongs to , unless for all . The latter vectors can be reshuffled between the associated clusters without changing the cost. So we may restrict to and the first statement follows. Moreover, assuming (2) we have and so its norm is .

In the case of -pc we also need to observe that the principal eigenvector of indeed belongs to , and the corresponding eigenvalue is . ∎

A simple critical test of any approach is given by the angular distribution corresponding to the asymptotic independence, see case (i) in Section 2. In this case any partition of indices yields faces satisfying Assumption A. We take for simplicity and partition the index set into and for some . For -means the necessary and sufficient condition (12) reads

where and correspond to the alternative partition. But the right-hand side is maximized at when is even and when is odd, and so we must choose index sets of essentially equal size to make faces identifiable using -means, see also Theorem 4.2 below. In the -pc case we note that whenever contains at least one standard basis vector. Thus, the necessary and sufficient condition (13) always holds for such .

In the above case the partitioning is arbitrary, but one can always construct another angle satisfying the moment constraints and arbitrarily close to such that a given partition becomes the only correct one (the respective faces support the law of ). This provides a class of examples where -means clustering fails to identify the supporting faces, because the dissimilarity is continuous, see also Janssen and Wan, (2020). Importantly, -pc does not readily fail in this case.

4.3. Spherical -means in the size-balanced case

The spherical -means procedure is guaranteed to identify the correct faces only when their dimensions satisfy a certain strict condition. If this assumption is violated, it is possible to construct a model where -means fails, see the above discussion.

Theorem 4.2.

Proof.

In view of (12) it is only required to show that

for any partition . We denote the right-hand side by and note that its maximum over subject to the constraint is attained under the assumption for all , see Lemma A.1. Letting be the number of non-zero entries in we get an upper bound on the sum of norms:

and the first statement follows. The case has been discussed above and here the optimal integers are such that . The proof is complete. ∎

5. Spherical -principal-components clustering and concomitant extremes

5.1. The main result

The eigenvalues of the matrices corresponding to the submodels, see Section 2, will play a crucial role in the following. When discussing some basic properties of these matrices we write and assume that . Also, let denote the th largest eigenvalue of a symmetric matrix , tacitly assuming when exceeds the order of . In the case (i) of asymptotic independence is a diagonal matrix with on the diagonal, so that . In the case (ii) of complete dependence is a matrix with constant elements yielding . The following lower bound on the largest eigenvalue is true in general.

Lemma 5.1.

Proof.

Consider the decomposition , where is the respective covariance matrix and is a vector of ones. All three matrices are non-negative definite, and the eigenvalues of the latter are . Next, we use the standard inequality: , which follows from the interpretation of as the maximum over quadratic forms, for example. Apply Lemma 2.1 to conclude. ∎

We are now ready to state our main result providing some basic theory supporting the use of clustering in detection of groups of concomitant extremes.

Theorem 5.2.

Importantly, this sufficient condition asserts that the second principal direction for any face provides a smaller cost reduction than the principal direction of any other face taking the respective probability weights into account. That is, the problem is balanced in this sense. Moreover, the above condition is implied when separates the first two eigenvalues of for all submodels , see Lemma 5.1. This is true, for example, for certain symmetric models, see Lemma 5.4 below, irrespective of the dimension.

Proof of Theorem 5.2.

Let be the diagonal blocks of . In view of (13), it is only required to show for any partition that

where . Lemma A.2 in the Appendix is crucial here, and it shows that the right-hand side is upper bounded by . Thus it is left to show that , which is indeed equivalent to the stated assumption, because of the block diagonal structure of .

5.2. Simple sufficient conditions

Let us discuss the condition in (15) for a fixed . Firstly, it is always true for a one- or two-dimensional face, where in the former case we tacitly assume that .

Lemma 5.3.

Assume (2) and . Then .

Secondly, certain symmetries imply this condition as, for example, invariance of the second moments under permutations.

Lemma 5.4.

Assume (2) and for all and all permutations . Then .

Proof.

Let be the common cross-moment. Observe from that , so that is a matrix with diagonal elements and off-diagonal . It is not difficult to check that and the other eigenvalues are all equal to . The proof is complete in view of Lemma 2.1. ∎

5.3. Counterexamples

Basic counterexamples to successful identification of faces are obtained by considering more groups of (almost) concomitant extremes than there are clusters. Assume that the index set can be partitioned into 3 sets , but we use with the partition and . Write and suppose that the leading eigenvalues satisfy

| (16) |

Now we readily find that an alternative partition and produces a strictly larger value:

showing that -pc will fail to identify the faces and , see Proposition 4.1 and (4). Of course, the failure is due to the wrong grouping of the three faces, but by continuity of the dissimilarity function we can perturb the model by introducing some small mass on without drastically changing the location of the optimal centroids, but making the partition and the only possibility.

6. Numerical experiments

6.1. The simulation framework

Firstly, we consider a dimensional model satisfying Assumption A with faces. The -means and -pc algorithms are compared by attempting to associate each pair of centroids with the two faces and computing certain scores. Secondly, we consider a more practical situation where the groups are not disjoint and the number of groups must be inferred from data. Finally, we apply both clustering algorithms to two real world datasets.

Here we briefly describe our basic model used in simulations. The random vector is taken to have a -variate max-stable Hüsler–Reiss distribution introduced in Hüsler and Reiss, (1989) and further studied in Engelke et al., (2015); Engelke and Hitz, (2020). This popular family has a good control of pairwise extremal dependencies which are encoded into the associated variogram matrix parametrizing the distribution. The variogram satisfying Assumption A with faces of dimensions and is produced randomly in a certain way detailed in the Supplementary Material. The pairwise tail dependence coefficients are likely to be very small in our parameter generation procedure. This may lead to a subdivision of a group of concomitant extremes into almost independent subgroups making the detection problem harder, see Section 4.

In each experiment we sample i.i.d. realizations of using the R package Engelke et al., (2019). We take of these vectors having the largest Euclidean norm and thus form approximate realizations of the angle . An example of the estimated matrix appears in Figure 3 (left). The mean is for asymptotically dependent and for the pairs with asymptotic independence.

One way to obtain faces from the centroids is to use a simple truncation procedure: for a chosen level . Another way is to find the index set with the minimal cardinality and such that the angle with the respective face is sufficiently small: , where

| (17) |

see also (7). The last equality follows from the fact that the minimizer is given by the normalized vector . Finding such is simple, since we only need to choose enough indices corresponding to the largest ’s. Note that by doing so we always pick a face yielding the smallest angle with among all faces of the same dimension. This latter approach is more consistent with the spherical clustering paradigm, and so we use it throughout our experiments. In fact, any dissimilarity in Section 3 would produce the same results up to changing the threshold appropriately.

6.2. Comparison of -means and -pc

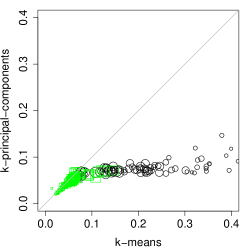

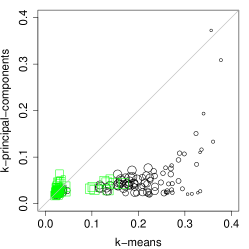

We replicate the following procedure times: we choose uniformly at random and generate a variogram corresponding to the partition and . Then we produce approximate realizations of the angle , apply both the -means and -pc algorithms using and 100 random restarts in each, and associate each pair of centroids with the two faces. For each centroid we calculate the angle to the corresponding face defined in (17) and the maximal entry over the indices defining the other face. That is, a small number indicates that the centroid is indeed close to its face, see Figure 2 where 19 and 8 black points are outside the plot range, respectively.

We call it an error when a centroid yields the angle and the maximal entry both exceeding 0.1. Out of 200 trials (faces) there are approximately errors for -means and only for -pc, and all of the latter are also the errors for the -means procedure. By increasing the threshold to 0.2 we get and of errors, and again all the errors in the latter are also errors in the former. Furthermore, these correspond to the first face and occur when it is relatively small. We also check that in all these cases permuting the assignment to faces does not resolve the issue.

In the above regime of weak asymptotic dependence the -pc method outperforms -means, which is also expected in view of the above developed theory and accompanying intuition. In the case of increased dependence within the faces both clustering methods perform extremely well, making identification of the corresponding faces an obvious task in this simplistic setting.

6.3. Non-orthogonal faces and the choice of

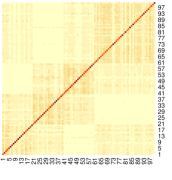

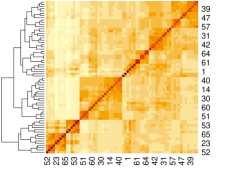

Recall that Assumption A is required for our theoretical guarantees alone. Here we consider a typical scenario where the groups of concomitant extremes have common elements and the number of groups must be inferred from data. We mix two datasets: half of the observations come from the above (randomly sampled) Hüsler–Reiss model with two groups and half from an analogous model with two groups . These are the underlying four faces to be identified. The estimated matrix of tail dependence coefficients is presented in Figure 3 (left). This image may give a false feeling that identification of groups is easy, and so we reorder the indices according to the standard heatmap routine in R based on hierarchical clustering, see Figure 3 (centre). Now the groups cannot be easily seen with a naked eye.

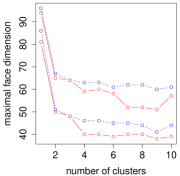

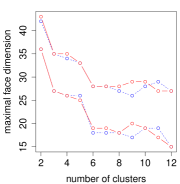

We run -means and -pc for and use restarts in each (much fewer would be sufficient for smaller ). The standard ‘elbow plot’ of the cost as a function of does not reveal a clear candidate for the number of clusters, and so is omitted. Importantly, our final goal is not to cluster the points but rather to determine the groups of concomitant extremes, hopefully leading to a sparse model. Thus, instead of plotting the cost function, we plot the maximal face dimension in Figure 3 (right) for two (angular) thresholds , which does suggest as an adequate candidate when using -pc (in red). Choosing the right is difficult in general, and one may look at various statistics depending on the problem and goals of the study. Providing some theory to aid this choice is an important open question.

Finally, we present the detected faces in Figure 4, where the same two thresholds are used. Note that smaller threshold leads to larger faces and we depict additional indices by light colors. Here and below the thresholds are chosen so that the recovered faces correspond to a sparse problem while (almost) all indices are contained in some group. In Figure 4, the centroids are ordered so that the respective faces can be associated with , and . Both methods produce relatively good results with -pc being visually a bit better. Choosing an appropriate threshold is non-trivial and this choice may depend on the ability to cope with faces of large dimension in a subsequent modelling step. Larger threshold values result in smaller faces. Some indices may not appear in any group indicating their high level of asymptotic independence from the rest. In practice, it may be reasonable to first establish the main directions/prototypes of extremes and then treat the remaining components in some way. Finally, thresholding of centroids is just one possibility to define faces, and many others exist (Chautru,, 2015).

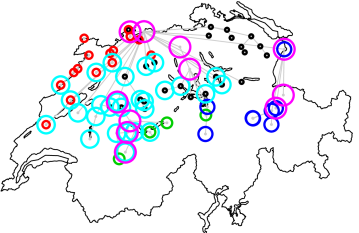

6.4. River discharges

We illustrate the two clustering approaches using river discharges at locations in Switzerland, see the review paper Engelke and Ivanovs, (2021) for a detailed description of this dataset. The data is standardized as described in Section 2 and then of observations are used to approximate the angular distribution, resulting in 202 samples. Unlike in the simulation experiments above, here we have a rather strong ‘asymptotic’ dependence between various components, see Figure 5 (left).

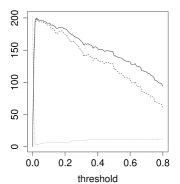

First, we investigate a basic thresholding approach without clustering as in the DAMEX algorithm (Goix et al.,, 2016), which assigns extreme observations (with respect to the max norm) to faces according to a chosen threshold. Figure 5 (centre) presents some statistics for various thresholds and also illustrates a common issue with this approach, see also Goix et al., (2017) and Chiapino et al., (2020) for further comments and possible solutions. This method results in a large number of faces with a single observation, and so further grouping is needed. Note that pruning such faces would remove a majority of the extreme observations. Upon reducing the threshold, we get one high-dimensional face containing most of the observations. In the above example of 4 non-orthogonal faces an analogous picture is obtained. Furthermore, similar issues (even if less pronounced) arise when using the alternative approach of Meyer and Wintenberger, (2021) in this and the previous examples.

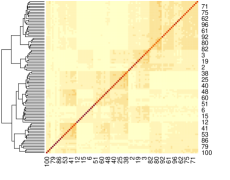

Next, we consider clustering approaches with a relatively small number of clusters , which is desirable in practice, since every cluster leads to a submodel requiring further investigation. In all cases the centroids produced by the two methods are very similar with the maximal angular distance of ; here we used 30000 restarts to limit the effect of suboptimal centroids. Figure 5 (right) illustrates the maximal face dimension as a function of , which suggests as an adequate number of faces. The obtained faces using are depicted in Figure 6, see also Engelke and Ivanovs, (2021) for a somewhat similar picture. These groups of concomitant extremes exhibit nice geographical patterns. The face dimensions are (from smaller to larger circles) containing extreme observations, respectively. It is noted that the -means centroids are almost the same, the cluster assignments of observations coincide, and the faces differ only slightly. A more careful analysis may proceed by using different thresholds for each centroid, or some other face attribution procedure.

In conclusion, the spherical clustering approach is a useful tool in the analysis of concomitant extremes in large dimensions. The two methods often produce similar results, but the -pc method may be better in the setting when the groups exhibit weak asymptotic dependence between many pairs of their components. Importantly, it comes with a theoretical guarantee applicable in a much broader context, which is the main contribution of this work.

Acknowledgement

The authors gratefully acknowledge financial support of Sapere Aude Starting Grant 8049-00021B “Distributional Robustness in Assessment of Extreme Risk”.

Appendix A Two Lemmas

The first result is required for the proof of Theorem 4.2.

Lemma A.1.

A maximizer of

satisfies for all : or both and have one positive entry at the same position. Moreover, if , then the maximum is attained under the assumption for all .

Proof.

The maximum is attained since it is the maximum of a continuous function over a compact set. Assume that for some index we have and , which is equivalent to . Let and be the norms when the th coordinate is ignored. We further assume that , which excludes the possibility of only one positive entry. It is enough to show that there exists a vector such that

so that the maximality fails. We will consider the two possibilities and , where is the th standard basis vector. It is clear that the positivity constraint is satisfied. Thus it is enough to show that

| (18) |

where , and , which can be proved by assuming that so that the first entry in the maximum is larger than the second, and taking squares of both sides twice.

Finally, any group of with a single strictly positive entry in the same position can be replaced by their sum and zero vectors without changing the sum of norms. ∎

The proof of Theorem 5.2 relies on the following non-standard upper bound on the sum of leading eigenvalues.

Lemma A.2.

Let be symmetric non-negative definite matrices of order . Then

| (19) |

Moreover, for any there exist as above yielding the equality.

Proof.

By the result of Fan, (1949), see also (Overton and Womersley,, 1992, Thm. 1), we have

| (20) |

and, in particular, .

Let vectors have unit norms and be such that , and let be mutually orthogonal vectors with unit norms obtained via the Gram–Schmidt process. That is, for all we have , where .

By (20) we have

where in the last step we use the assumption that are non-negative definite. Furthermore, for any we have the representation

Thus, we find a lower bound on the difference of interest:

But according to the constraints on we have

and it is left to check non-negativity of the terms

which is true due to assumed non-negative definiteness of all , and the first assertion is proven.

The second assertion is obtained by taking the matrices

where is an orthogonal matrix in the diagonalization of . Indeed, the matrices are non-negative definite summing up to , and the largest eigenvalues are for . ∎

Appendix B Hüsler–Reiss distribution

B.1. Random generation of variogram

A -dimensional max-stable Hüsler–Reiss distribution (Hüsler and Reiss,, 1989) is parametrized by a conditionally negative definite matrix , called a variogram. Every such matrix has a representation , where are the elements of some Hilbert space with norm , and every such construction yields a conditionally negative definite matrix, see (Vakhania et al.,, 1980, Property (g), p. 191). As usual, we impose a further non-degeneracy assumption that is strictly conditionally negative definite so that the associated exponent measure has a density (Engelke et al.,, 2015).

Suppose that has a max-stable Hüsler–Reiss distribution. Our main assumption requires a partition of the index set such that for all and , which is equivalent to (asymptotic) independence of the two groups of components of . Recall the formula for the bivariate tail dependence coefficient:

where is the survival function of the standard normal distribution, and note that is obtained in the limit case . In practice, large entries in the respective locations of would suffice, because of the weak convergence of the respective distributions.

In our experiments we randomly generate for according to the following procedure based on the aforementioned representation. Firstly, we generate -dimensional vectors with i.i.d. Pareto distributed components having shape parameter . Secondly, we add one more dimension by letting , where is a fixed large number. Then the variogram matrix is set to , where provides a scaling resulting in a suitable distribution of the tail dependence coefficients. Note that this procedure ensures that for and in different groups.

Finally, we use the R package (Engelke et al.,, 2019) to sample vectors from the Hüsler–Reiss distribution specified by . Note that given for a finite threshold provides only an approximation of the limiting angle. The distribution of the exact angle is addressed below.

B.2. The angular distribution and the matrix

Even though the exact matrix is not required for the simulation experiments, it can be used to verify the sufficient conditions in our main result. Below we determine the probability density function of (with respect to the Euclidean norm) and provide an expression for in terms of expectations of transformed Gaussian vectors.

As in Engelke et al., (2015), we consider the covariance matrix

For all we define the transformation

| (21) |

where stands for the simplex interior, and note that is a bijection with the inverse

It turns out that each column of the matrix corresponds (up to a permutation) to for a multivariate normal as specified below. The means and other moments of can be obtained in a similar way.

Lemma B.1.

For the -dimensional Hüsler–Reiss distribution with the variogram the density of the Euclidean angle is given by

| (22) |

where and is the density of the multivariate normal distribution with covariance matrix and mean vector . Furthermore, with being the density of , where and , the following identities hold:

Proof.

From Engelke et al., (2015) it is known that the exponent measure has the density

We note that for the polar coordinates

the absolute value of the Jacobian evaluates to , and so in these coordinates the density becomes

This must factorize into according to (Resnick,, 2008, Prop. 5.11(iv)) and the first result follows.

Let us compute the Jacobian of the transformation defined in (21) and restricted to the first values. We have

where , and so

Using formula (1) in Goberstein, (1980), we find that the last determinant is equal to

Thus, we have the relation , where and are restricted to the first elements. Comparing it with , we indeed find the stated relation between and . Finally, observe that

The proof is complete. ∎

The above result states that the last column of is given by the vector . By changing the indexing we may easily find the other columns. In particular, in the bivariate case with parameter we have

where is a standard normal. Sadly, the moments , are not explicit, and the same applies to the matrix .

References

- Chautru, (2015) Chautru, E. (2015). Dimension reduction in multivariate extreme value analysis. Electron. J. Stat., 9(1):383–418.

- Chiapino et al., (2020) Chiapino, M., Clémençon, S., Feuillard, V., and Sabourin, A. (2020). A multivariate extreme value theory approach to anomaly clustering and visualization. Computational Statistics, 35:607–628.

- Cooley and Thibaud, (2019) Cooley, D. and Thibaud, E. (2019). Decompositions of dependence for high-dimensional extremes. Biometrika, 106(3):587–604.

- Davison and Huser, (2015) Davison, A. and Huser, R. (2015). Statistics of extremes. Ann. Rev. Stat. App., 2:203–235.

- Dhillon and Modha, (2001) Dhillon, I. S. and Modha, D. S. (2001). Concept decompositions for large sparse text data using clustering. Machine learning, 42(1-2):143–175.

- Drees and Sabourin, (2021) Drees, H. and Sabourin, A. (2021). Principal component analysis for multivariate extremes. Electron. J. Statist., 15(1):908–943.

- Engelke and Hitz, (2020) Engelke, S. and Hitz, A. S. (2020). Graphical models for extremes. J. R. Stat. Soc. B., 82(4):871–932.

- Engelke et al., (2019) Engelke, S., Hitz, A. S., and Gnecco, N. (2019). graphicalExtremes: Statistical Methodology for Graphical Extreme Value Models. Available from https://CRAN.R-project.org/package=graphicalExtremes, R package version 0.1.0.

- Engelke and Ivanovs, (2021) Engelke, S. and Ivanovs, J. (2021). Sparse structures for multivariate extremes. Annu. Rev. Stat. Appl., 8(1):241–270.

- Engelke et al., (2015) Engelke, S., Malinowski, A., Kabluchko, Z., and Schlather, M. (2015). Estimation of Hüsler–Reiss distributions and Brown–Resnick processes. J. R. Stat. Soc. B., 77(1):239–265.

- Fan, (1949) Fan, K. (1949). On a theorem of Weyl concerning eigenvalues of linear transformations I. Proceedings of the NAS of the USA, 35(11):652.

- Gan et al., (2007) Gan, G., Ma, C., and Wu, J. (2007). Data clustering, volume 20. SIAM and ASA. Theory, algorithms, and applications.

- Goberstein, (1980) Goberstein, S. M. (1980). Evaluating ”uniformly filled” determinants. Col. Math. J., 19(4):343–345.

- Goix et al., (2016) Goix, N., Sabourin, A., and Clémençon, S. (2016). Sparse representation of multivariate extremes with applications to anomaly ranking. In Proceedings of the 19th International Conference on Artificial Intelligence and Statistics (AISTATS). JMLR: W&CP.

- Goix et al., (2017) Goix, N., Sabourin, A., and Clémençon, S. (2017). Sparse representation of multivariate extremes with applications to anomaly detection. J. Multivar. Anal., 161:12–31.

- Hill et al., (2013) Hill, M. O., Harrower, C. A., and Preston, C. D. (2013). Spherical -means clustering is good for interpreting multivariate species occurrence data. Methods Ecol. Evol., 4(6):542–551.

- Hüsler and Reiss, (1989) Hüsler, J. and Reiss, R.-D. (1989). Maxima of normal random vectors: between independence and complete dependence. Stat. Prob. Let., 7(4):283–286.

- Jalalzai and Leluc, (2020) Jalalzai, H. and Leluc, R. (2020). Informative clusters for multivariate extremes. arXiv:2008.07365.

- Janssen and Wan, (2020) Janssen, A. and Wan, P. (2020). -means clustering of extremes. Electron. J. Stat., 14:1211–1233.

- Larsson and Resnick, (2012) Larsson, M. and Resnick, S. I. (2012). Extremal dependence measure and extremogram: the regularly varying case. Extremes, 15:231–256.

- Meyer and Wintenberger, (2021) Meyer, N. and Wintenberger, O. (2021). Sparse regular variation. Advances in Applied Probability, 53(4):1115–1148.

- Overton and Womersley, (1992) Overton, M. L. and Womersley, R. S. (1992). On the sum of the largest eigenvalues of a symmetric matrix. SIMAX, 13(1):41–45.

- Palarea-Albaladejo et al., (2012) Palarea-Albaladejo, J., Martín-Fernández, J. A., and Soto, J. A. (2012). Dealing with distances and transformations for fuzzy -means clustering of compositional data. J. Classif., 29(2):144–169.

- Resnick, (2008) Resnick, S. I. (2008). Extreme Values, Regular Variation and Point Processes. Springer, New York.

- Simpson et al., (2020) Simpson, E. S., Wadsworth, J. L., and Tawn, J. A. (2020). Determining the dependence structure of multivariate extremes. Biometrika, 107(3):513–532.

- Vakhania et al., (1980) Vakhania, N. N., Tarieladze, V. I., and Chobanyan, S. A. (1980). Probability Distributions on Banach Spaces. Mathematics and Its Applications (Soviet Series). D. Reidel Publishing Company.

- Wang et al., (2018) Wang, J., Wang, W., Garber, D., and Srebro, N. (2018). Efficient coordinate-wise leading eigenvector computation. In Algorithmic Learning Theory, pages 806–820. PMLR.