Towards A First Step to Understand Flash Loan and Its Applications in DeFi Ecosystem

Abstract.

Flash Loan, as an emerging service in the decentralized finance ecosystem, allows users to request a non-collateral loan. While providing convenience, it also enables attackers to launch malicious operations with a large amount of asset that they do not have. Though there exist spot media reports of attacks that leverage Flash Loan, there lacks a comprehensive understanding of existing Flash Loan services.

In this work, we take the first step to study the Flash Loan service provided by three popular platforms. Specifically, we first illustrate the interactions between Flash Loan providers and users. Then, we design three patterns to identify Flash Loan transactions. Based on the patterns, transactions are determined. The evaluation results show that the Flash Loan services get more popular over time. At last, we present four Flash Loan applications with real-world examples and propose two potential research directions.

1. Introduction

Decentralized finance, aka DeFi, has been growing in recent years. Up to 31th Jan 2021, the total value locked (TVL) 111TVL of a specific protocol represents the total amount of assets staked by users. in DeFi has reached 28 billion USD (defipulse, 2020). A service called Flash Loan (i.e. uncollateralized loan), which does not exist in the traditional finance system, has drawn much attention. However, the introduction of Flash Loan is a double-edged sword.

On the one hand, it does bring in convenience (Saver, 2020) and facilitate the prosperity of DeFi. Traders without much capital can launch arbitrage, liquidation and asset swapping with Flash Loan. For instance, when traders discover a price difference among tokens between decentralized exchanges (DEXes), they can borrow a considerable amount of capital by Flash Loan (no collaterals are required) to maximize the profit.

On the other hand, Flash Loan also enables attackers to launch malicious operations with a large amount of capital that they do not have. Therefore, the attack consequences can be vastly amplified. In early 2020, two infamous incidents (Qin et al., 2020) caused a huge loss to bZx (bZx, 2020). The hacker took the advantage of Flash Loan to manipulate the market price and made considerable profits of USD and USD, respectively. Most recently, a hacker borrowed DAI (Maker, 2020) via Flash Loan to gain over USD through repeatedly swapping tokens in the EMN ((YFI), 2020) pool.

As such, there is an urgent need to demystify the Flash Loan ecosystem and understand the impact of potential security threats. Unfortunately, few studies have been proposed to serve this purpose. Specifically, previous studies mainly focused on profit optimization (Qin et al., 2020; Daian et al., 2019) and oracles (Liu and Szalachowski, 2020) used by protocols. To the best of our knowledge, none of them systematically demystified Flash Loan and its applications. To provide effective mitigations for Flash Loan, we still lack a comprehensive understanding of Flash Loan.

In this paper, we take the first step to systematically study Flash Loan and further design three patterns to identify Flash Loan transactions. Then, we determine all Flash Loan transactions until 31st Jan 2021 based on three proposed Flash Loan patterns. As a result, Flash Loan transactions are identified. To further demystify the behaviors behind Flash Loan, we perform an analysis on four Flash Loan applications and explain them with real-world examples.

This paper makes the following contributions:

-

•

We study three Flash Loan providers to understand the working process of Flash Loan.

-

•

We conduct full-chain measurements on Flash Loan transactions launched in the DeFi ecosystem. As far as we know, this is the first work to give a measurement for Flash Loan transactions based on real-world data.

-

•

We describe four types of Flash Loan applications with real-world examples and propose two potential research directions.

Paper organization: The rest of the paper is arranged as follows. Section 2 presents the related work. Section 3 elaborates on some concepts in Ethereum and DeFi. Section 4 illustrates the general idea of Flash Loan and explains its working process under different platforms. Section 5 conducts an evaluation on Flash Loan transactions. Section 6 describes four applications behind Flash Loan. Section 7 proposes two potential research directions. Finally, we conclude the paper in Section 8.

2. Related Work

Kaihua et al. (Qin et al., 2020) investigate two existing exploits that happened on 15th and 18th Feb 2020 and present the details of how traders leverage the Flash Loan mechanism with the trick of price manipulation to gain profits. They also propose a process to re-boost two exploits via optimized parameters. Lewis et al. (Gudgeon et al., 2020) leverage Flash Loan to execute a governance attack (Zoltu, 2020) on MakerDAO (MakerDAO, 2020). Moreover, the proposed strategy leads to a theft of 0.5B USD and unlimited mining of DAIs. Bowen et al. (Liu and Szalachowski, 2020) systematically study 4 oracle designs in DeFi via comparing their price deviations. Besides, they exhibit the potential vulnerabilities existing among 4 oracle designs. Kamps et al. (Kamps and Kleinberg, 2018) aggregate the information from the existing pump-and-dump schemes among the classic economic and propose a group of patterns with summarised criteria to identify potential pump-and-dump activities in crypto markets. Xu et al. (Xu and Livshits, 2019) also investigate 412 pump-and-dump activities to build a model that predicts the pump behavior for all assets exhibiting in DEXes by estimating its pump likelihood. Philip et al. (Daian et al., 2019) present the breadth of arbitrage bots and their profit-making strategies, which optimize users’ network latency and pay a high transaction gas fee to win priority gas auctions (PGAs). Furthermore, they highlight that bots’ revenue far exceeds the Ethereum block reward and transaction fees. They state that the blockchain consensus stability might be threatened with such high optimization fees. Eskandari et al. (Eskandari et al., 2019) also study the front-running issues across the 25 most active decentralized applications (DApps) on the Ethereum blockchain and summarized their proposed solutions into useful categories.

3. Background

The introduction of the blockchain technique (Nakamoto et al., 2008) has changed the financial ecosystem in the world. Especially with the invention of Ethereum (Wood, 2014), there has been a wave of developing the decentralized applications (DApps). Smart contracts, as the basis of DApps, enable a transparent environment and become essential components for the development of DeFi.

3.1. Common concepts on Ethereum

To make this work easy to understand, We first introduce a few common concepts in Ethereum.

Account. Ethereum is an account-centric blockchain system. There are two types of accounts: External Owned Account(EOA) and smart contract account (smart contract in short). The main difference between them is that EOAs are controlled by private keys, and smart contracts are controlled by codes. Basically, an EOA is created with the generation of the public and private key pair, and a smart contract is always created by an EOA or another smart contract. Both EOAs and smart contracts are identified by their addresses, like 0x16431837a35b5469675b2ba5d9b7575d25b721c3.

Digital Currency. Ether and the ERC20 token are two main types of digital currencies in Ethereum. Compared to Ether which is supported natively, ERC20 tokens are supported by smart contracts. Once a smart contract implements the interfaces of ERC20 token standard (erc, 2015), then the smart contract can act as an ERC20 token. Moreover, ERC20 tokens can only be transferred by invoking two ERC20 token standard functions: transfer and transferFrom.

Transaction. All actions on the Ethereum blockchain are based on transactions. A transaction have three purposes: transferring Ether, invoking a smart contract function, and deploying a smart contract. According to the circumstance, there exist two types of transactions: external transaction and internal transaction. The external transactions are initiated from EOAs. Alternatively, once a smart contract is invoked within an external transaction, the internal transaction will be triggered. The word ”transaction” written individually in the remaining paper indicates the collection of an external transaction.

Gas Fee. Gas is the unit to measure the computational resource used to run operations in Ethereum. To execute transactions on the Ethereum Network requires users to pay a certain amount of Ether (known as gas fee). The gas fee is equal to the value that gas used in the transaction times provided gas price. Since there is no limitation on defining the gas price, users can control the gas fee for their transactions by setting any gas price. Typically, the higher the gas price is, the faster the transaction is verified on the Ethereum blockchain.

Function and Event. The smart contract function is identified by the function signature, which is the first four bytes of the hash value (SHA3) of the function name with the parenthesized list of parameter types. If a user sets a function signature in front of a transaction’s call data, then the callee smart contract’s corresponding function will be invoked. Smart contracts’ developers usually leverage the event to record critical information. For example, the ERC20 token standard specifies an event Transfer to record the spender, receiver and amount of transferred ERC20 tokens. Similarly, an event is identified by the hash value (SHA3) of the event name with the parenthesized list of parameter types. When an event is triggered, a log with an event hash is recorded in Ethereum.

3.2. Primitives in DeFi

Decentralized finance is a transparent and permissionless finance ecosystem without relying on intermediaries such as banks. In Ethereum, DeFi is formed with open-source protocols deployed as smart contracts. In the following, we will introduce some primitives in DeFi.

Decentralized Exchange (DEX). In the centralized exchanges (CEXes), users entrust their capital to CEXes for trading, and CEXes need to guarantee security. Conversely, trading on DEXes does not require users to provide access to their private keys. Therefore, users can still have full control of their capital.

In particular, there are two main types of DEXes: Order Book and Automated Market Maker (AMM). Order Book DEXes usually maintain a list of buy and sell orders. They match the pair of orders with a compatible price in their database. As for AMM DEXes, they maintain various liquidity pools with a designed price calculating mechanism. The price of assets lying in the pool is usually calculated based on its price mechanism and existing liquidity. In comparison, trading in AMM DEXes is more flexible because there is no need for the matching process.

Lending. Lending platforms share interests for depositors to lock their capital in the liquidity pool and provide a collateral loan for borrowers. The lending platforms normally require traders to deposit more collateral than the borrowed assets with a certain ratio. Most of the lending platforms design a protection mechanism called liquidation to prevent the potential loss caused by price slippage on traders’ deposited collaterals. Once the collateralization ratio (collateral value/debt value) is reached, the lending platforms will first sell lenders’ collateral with a discount to liquidators. Then, a certain percentage of collateral will be charged to lenders as a penalty. We will discuss more details about liquidation in Section 6.

4. flash loan

In this section, we first explain the general idea of Flash Loan. Second, we elaborate on three famous Flash Loan providers and compare their differences in requirements of using. Furthermore, we summarize a Flash Loan pattern for each provider to identify Flash Loan transactions.

4.1. General Idea of Flash Loan

To request a loan in DeFi platforms, the user is usually required to deposit overcollateralized assets (i.e., digital cash or tokens). However, a new functionality called Flash Loan is developed to enable a non-collateral borrowing service. Moreover, a considerable amount of assets can be “generously” lent to users by Flash Loan as long as the borrowed assets can be paid back within the current transaction. Otherwise, the platform will instantly revert the transaction to get the lent assets back.

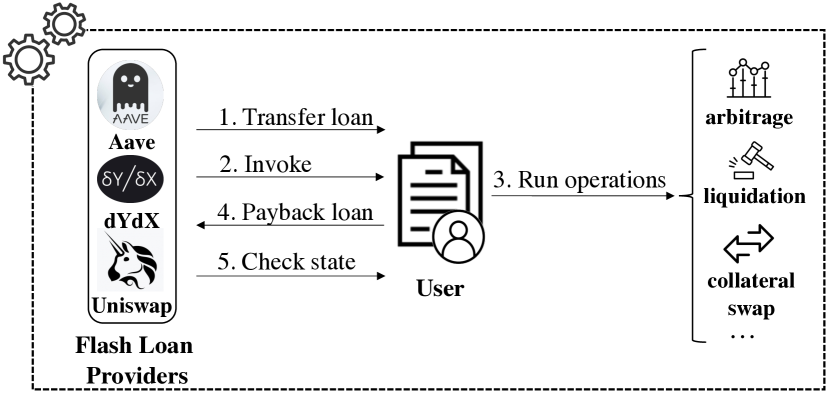

Figure 1 presents the general workflow of a Flash Loan transaction. There are two main entities: Flash Loan Providers and Users. To interact with Flash Loan Providers, Users are required to develop a smart contract. A user’s contract usually includes three parts: 1) borrowing the loan(s) from Flash Loan providers, 2) interacting with other smart contracts, and 3) returning the loan(s). To our best knowledge, there are three main Flash Loan providers (Aave, 2020) (dYdX, 2020) (Uniswap, 2020) supporting the Flash Loan service with or without certain fees.

Specifically, we generalize the workflow of a Flash Loan transaction into five steps. First, Flash Loan Providers transfer requested assets to Users. Second, they invoke Users’ pre-designed operations. Third, Users will interact with other contracts to execute operations with borrowed assets. Once the execution is completed, Users have to return the borrowed assets with or without the extra fee charged by Flash Loan Providers. Finally, Flash Loan Providers will check their balance. If they discover that no or non-sufficient assets are returned by Users, they will revert the transaction immediately. Note that all five steps are finished in one transaction.

4.2. Flash Loan Providers

In this section, we give a basic introduction of each Flash Loan provider and reveal their fee-charging mechanisms. Besides, we explain how users’ smart contracts interact with different Flash Loan providers.

4.2.1. Aave

Aave (Aave, 2020) is currently the second largest lending platform that locks over (defipulse, 2020) up to Jan 2021. As the first platform officially providing the Flash Loan service, Aave provides a native function called flashLoan 222function flashLoan(address _receiver, address _reserve, uint256 _amount, bytes calldata _params) designed in Aave’s official contract, i.e., the LendingPool contract, to trigger Flash Loan. Moreover, requesting Flash Loan in Aave charges of the borrowed assets as the fee.

How to prepare flash loan contract with Aave. For Aave’s Flash Loan, users need to develop a smart contract consisting of one execution function and one entry-point function. The execution function contains users’ designed operations for the loaned assets, e.g., trading in exchanges. Note that, the execution function has to be formed based on executeOperation 333executeOperation(address _reserve, uint256 _amount, uint256 _fee, bytes calldata _params) designed in Aave’s official contract FlashLoanReceiverBase.

In the entry-point function, users first need to prepare the function flashLoan to request a loan. Second, users can follow up with the function executeOperation to run the designed logic on the loaned assets. Third, returning loaned assets must be completed with the provided function transferFundsBackToPoolInternal 444transferFundsBackToPoolInternal(address _reserve, uint256 _totalDebt) after finishing executing operations. If Aave discover that the vault’s state is not balanced (no or non-sufficient assets are paid back to the vault), it will instantly revert the entire transaction. Once the preparation for the contract is done, users can deploy their contract to the chain and use the Flash Loan service from Aave by invoking the entry-point function.

Identify flash loan transactions from Aave. As aforementioned, Aave exposes a native function called flashLoan for users to utilize Aave’s Flash Loan. Once the function flashLoan is invoked successfully, it emits a unique event called FlashLoan 555FlashLoan(address indexed _target, address indexed _reserve, uint256 _amount, uint256 _totalFee, uint256 _protocolFee, uint256 _timestamp). Therefore, we can use this feature to identify Flash Loan transactions from Aave. As a result, we discover that there exist over transactions including Aave’s Flash Loan up to 31st Jan 2021.

4.2.2. dYdX

dYdX (dYdX, 2020) is a non-custodial platform providing services mainly including lending and borrowing on their supporting cryptoassets like ETH, USDC, and DAI. At the time of writing this paper, dYdX has locked over USD. According to our investigation, there is no native Flash Loan feature provided by dYdX. However, dYdX’s SoloMargin contract provides a function called operate 666function operate(Account.Info[] memory accounts, Actions.ActionArgs[] memory actions) that enables to bring a series of operations into one transaction to achieve Flash Loan for users. Surprisingly, dYdX does not charge any fee for invoking the function operate.

How to prepare flash loan contract with dYdX. The preparation for Flash Loan in dYdX is pretty similar to Aave’s. Users are required to develop a contract including one execution function, which contains users’ operating logic on the loaned assets, and one entry-point function. In the entry-point function, users first need to sequentially organize a list of provided (by dYdX) actions: withdraw, callFunction 777callFunction(address sender, Account.Info memory account, bytes memory data) and deposit. Then, users can leverage the function operate to run the actions one by one to perform Flash Loan logic. Note that, callFunction is acting as the execution function mentioned above to perform users’ operating logic. In details, withdraw helps users borrow assets from dYdX without any collateral. Then, callFunction is executed to run users’ particular operations on the loaned assets. Finally, deposit pays back the loan. Once the contract is well prepared and deployed on the chain, users can run Flash Loan in dYdX by invoking the entry-point function.

Identify flash loan transactions from dYdX. Though dYdX does not directly provide Flash Loan feature, users can still achieve Flash Loan service in dYdX by sequentially executing a series of actions: Operate, Withdraw, callFunction, Deposit. Note that, all actions have corresponding event logs: LogOperate, LogWithdraw, LogCall, and LogDeposit. Therefore, to identify transactions containing dYdX’s Flash Loan service, two conditions should be checked. First, all actions’ event logs should exist in a transaction. Second, all event logs have to follow a particular order showed below:

LogOperate LogWithdraw LogCall LogDeposit

Once two conditions are both satisfied in a transaction, we can confirm that it is a Flash Loan transaction from dYdX. Based on our experiment, around transactions are identified as Flash Loan transactions leveraging dYdX’s service.

4.2.3. UniswapV2

As one of the most famous DEX protocols, Uniswap (Uniswap, 2020) occupies around ( USD) of liquidity in DeFi ecosystem. Different from Aave and dYdX, Uniswap simply builds its Flash Loan feature called flash swap on the function swap 888swap(uint amount0Out, uint amount1Out, address to, bytes calldata data). In details, the function swap switches in between flash swapping and normal swapping based on the provided parameters. In terms of the fee, compared to the aforementioned Flash Loan providers, UniswapV2 charges the highest fee () based on users’ borrowed assets.

How to prepare flash loan contract with UniswapV2. A contract for using Flash Loan in UniswapV2 requires users code their designed operations in function IUniswapV2Callee which inherits from UniswapV2’s interface standard IUniswapV2Callee . The designed operations must include repayment action to success flash swap. Unlike the two Flash Loan providers previously analyzed, users do not need to develop any entry-point function to initiate a transaction. Instead, users first neet to find the targeted pair contract 999Uniswap has many pair contracts, which are published for users, to launch a swap on a pair of tokens. In UniswapV2, every pair contract supplies swap function. published by Uniswap. Then, through invoking the function swap with specific parameters, a Flash Loan transaction will be triggered. In particular, parameter to should be the address of the deployed contract, and the length of parameter data should be greater than zero.

Identify flash loan transactions from UniswapV2. Identifying Flash Loan transactions from UniswapV2 requires three steps. First, we verify the event PairCreated emitted by the UniswapV2Factory contract and collect a group of pair contracts (addresses) that supplies the swap function. Second, we verify the event swap emitted by triggering the function swap in all transactions. Lastly, once we confirm that the transaction invokes the swap function of pair contracts, we identify it as Flash Loan transaction from UniswapV2 through checking three conditions:

-

(1)

The length of the parameter data is greater than zero.

-

(2)

The internal transaction triggered by uniswapV2Call must include the invocation of transfer or transferFrom function.

-

(3)

The receiver address of transfer or transferFrom function must be the pair contract.

In conclusion, if all three conditions are fulfilled, the transaction can be confirmed as a operation of flash swap (i.e., Flash Loan in UniswapV2). Through applying the identifying pattern, around transactions are filtered.

Importantly, since our patterns strongly rely on the specific rule published by each Flash Loan provider, the identified Flash Loan transactions will not result in any false positive.

5. The Measurement of Flash Loan Transactions

In this section, we perform a measurement for Flash Loan transactions. As for the data set, we collect about one billion transactions (up to 31th Jan 2021) from the Ethereum blockchain ledger.

| Providers | # Transactions | # Receivers | # Average Use |

|---|---|---|---|

| Aave | |||

| dYdX | |||

| UniswapV2 |

Statistic Result. Through applying three Flash Loan patterns proposed in Section 4 over one billion collected transactions, Flash Loan transactions are identified. As shown in Table 1, users leverage Flash Loan in UniswapV2 most frequently, as there are () transactions. Following up, () Flash Loan transactions are found in dYdX, and () Flash Loan transactions are found in Aave. The second last column of Table 1 records the amount of Flash Loan receivers for each Flash Loan provider. According to the results, Flash Loan in dYdX has been used by most unique receivers () as well as there are and Flash Loan receivers in Aave and UniswapV2, respectively. In the last column of Table 1, it presents the average number of transactions launched by each receiver.

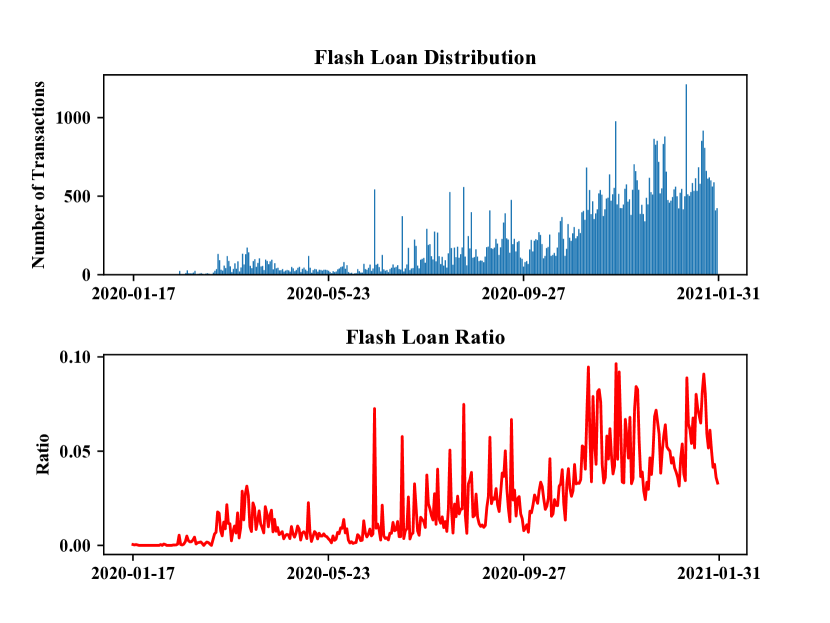

Trend. To further understand the popularity of Flash Loan in DeFi, we provide two time series for the number and the ratio (the number of Flash Loan transactions / the number of all transactions) of Flash Loan transactions in Figure 2. Note that, both the number and the ratio of Flash Loan transactions are increasing over the time.

Finding. Nowadays, Flash Loan service is getting more popular. Through measuring Flash Loan transactions, we discover that Flash Loan in UniswapV2 is used most intensively ( transactions per receiver), while Flash Loan in Aave ( transactions per receiver) is used least intensively.

6. Applications Of Flash Loan

Flash Loan can be used for legitimate purposes such as arbitrage, liquidation, etc. Besides, Flash Loan can also become a sharp knife for aggressive users to harm the DeFi ecosystem. In this section, we describe four applications of Flash Loan and discuss the benefit that Flash Loan brings to them.

6.1. Arbitrage

General speaking, arbitrage in DeFi is a behavior to gain benefits by trading in between platforms supplying different price for an asset. Since the DeFi market reacts slower for events happening in the network than the real-world market, traders can take advantage of the market’s inefficiencies to buy and sell the cryptoassets at a different price to gain financial benefits. Note that, arbitrage itself is not a malicious behavior. In fact, the arbitrage can be leveraged to balance the token prices between DEXes.

Benefit. With Flash Loan, traders can launch arbitrage without any pre-owned asset. In particular, if the price difference is found, the arbitrageurs can instantly borrow a considerable asset with Flash Loan service to earn benefits. Therefore, arbitrages with Flash Loan become “cost-free” as long as traders can afford the gas fee to launch the transaction.

Example. We will present an arbitrage that happened on 22nd Jan 2021 with four steps. First, in the transaction 1010100x2a0c2599f89d95a46f4f28712e99a71847d8f72af5bdc8942d6c9dd01d896624, the trader borrowed 1.13 Ether from dYdX. Second, 1.13 Ether was converted to 345 LPT tokens in Balancer (Balancer, 2020) through a trade. Third, another trade was triggered to trade 345 LPT tokens on the corresponding liquidity pool of Uniswap. As a result, 1.46 Ether were gained by the trader. Finally, the trader returned 1.13 Ether to dYdX from gaining. In this arbitrage case, the trader gained 0.33 Ether (around 538 USD at the time) by paying 0.05 Ether as the gas fee.

6.2. Wash Trading

Wash trading in DeFi is a behavior that creates fake trading volume for certain cryptoassets or platforms. Specifically, wash trading is a group of trades increasing the trading volume on the asset or platforms. In reality, wash trading can easily mislead users to perform financial operations on the targeted cryptoassets and platforms. Though some countries like the U.S. have banned washing trading to protect their traditional markets and the stock market, it is brought back to the crypto market again because of the popularity of cryptocurrency and the lack of legal management.

Benefit. With Flash Loan, wash traders can manipulate the market without a large amount of capital as long as they can afford the potential loss and the gas fee.

Example. In the transaction 1111110x8fc77fa516aca91715046c1f307397ac49d211244fced5734c480a660015f927 executed on 14th Jul 2020, the trader firstly borrowed 10 Ether from Aave. Then, five repeated trades were launched to increase the trading volume in the liquidity pool “Uniswap V2: DAI 2”. In details, for each trade, 2 Ether was first converted to DAI and all DAI would be instantly converted back to Ether at the pool. Finally, the user paid back the Flash Loan. There were no further operations except wash trading in this transaction. As a result, the trader lost 0.068 Ether in this transaction and paid 0.164 Ether as the gas fee.

6.3. Flash Liquidation

Liquidation is a behavior launched by the liquidator to buy undercollateralized assets from the lending platforms. There are two liquidation classes (Fixed Price Biding and Auction) involving three roles (platforms, liquidators and collateral keepers). For fixed price biding, the lending platforms like dYdX and Compound allow liquidators to buy undercollateralized assets from collateral keepers with a specific discount. Moreover, the lending platforms will apply a fixed amount of liquidation penalty to collateral keepers. Alternatively, the platforms like MakerDAO (MakerDAO, 2020) allow liquidators to compete on the keeper’s undercollateralized assets like an auction. The winners, who pay the higher gas fee to launch their transactions, can buy the undercollateralized collateral with a discount.

Benefit. With Flash Loan, anyone can become a liquidator to make profits without much capital by buying the undercollateralized assets with a specific discount.

Example. The transaction 1212120x38b706beda9426027081f2b6c1f2d6e68b2387d824a59e20a4d6decdfec43385 performed a liquidation on 3rd Nov 2020. In details, the liquidator first borrowed DAI from dYdX and swapped the DAI to USDT (Tether, 2021). Second, USDT was used to buy the asset from the undercollateralized position in Compound (Compound, 2020). Through exchanging the bought asset, the liquidator got DAI. Finally, after paying back the Flash Loan, DAI (about USD) remained as profits, which is greater than the gas fee (about USD).

6.4. Collateral Swap

Collateral swap in DeFi is a well-defined behavior consisting of two main steps:

-

•

Swapping: Redeeming the collateral from the old loan.

-

•

Operating: Lauching operations on redeemed collateral.

Since the crypto market is extremely unpredicted, timely closing existed collateral position becomes an urgent need for the holder to stop loss from severe slippages and liquidations.

Benefit. For users without sufficient capitals for Swapping, Flash Loan can solve their urgent need by providing “cost-free” assets to save their collaterals from the price slippage and the liquidation. Besides, Flash Loan also enables Swapping and Operating actions run within one transactions. It further prevents users from suffering the uncertainty (like slippage) between transactions.

Example. In the transaction 1313130xaf4ca18a0d3b94d948a9eeb47ba57c84c212aaeb7284b38ede6a0f6f549c3827 launched on 17th Mar 2020, the user performed a collateral swap to take out BAT (Swapping) and exchanged it to more stable asset USDC (Operating). As the context, the user previously opened a loan of DAI by depositing the asset BAT. In details, first, the user borrowed 25 DAI Flash Loan from Aave. Second, 25 DAI was paid to redeem out BAT (collateral). Third, the redeemed collateral was further swapped to a more stable asset USDC. Lastly, the user converted part of the USDC to pay back Aave’s Flash Loan. As a result, the user swapped his/her collateral to a more stable asset without holding any DAI.

In conclusion, Flash Loan provides a vast convenience for multiple applications (arbitrage, wash trading, liquidation, and collateral swap) in DeFi ecosystem. It can either bring traders benefits or be used maliciously. Thus, understanding the intention of the application is necessary for both traders and developers.

7. Future Research Directions

In this section, we propose two potential research directions.

Arbitrage. Arbitrages in DeFi happen nearly every day. By leveraging the smart contract and Flash Loan, many organizations and individuals create bots to launch designed operations. We believe that the arbitrage bots in DeFi can maximize traders’ profits if the information (i.e. price difference) can be timely detected and fed to the bot.

DeFi Attacks. With the increasing popularity of DeFi, attackers could steal money from DeFi platforms or individuals. Identifying malicious transactions, especially the zero-day attacks, is challenging due to complicated interactions between multiple entities (Figure 1). How to propose effective methodologies to detect attacks towards DeFi platform is still an open research question.

8. Conclusion

This paper takes the first step to study the working process of Flash Loan within three different platforms. In this work, we identified Flash Loan transactions and Flash Loan receivers. Furthermore, we evaluated the popularity of Flash Loan. To better understand the application behind the Flash Loan mechanism, we elaborated on four types of applications with real-world examples. Finally, we proposed two potential research directions in this area.

Acknowledgments

We thank the anonymous reviewers for the thorough reviews. This work was supported by the Leading Innovative and Entrepreneur Team Introduction Program of Zhejiang (2018R01005), and the Fundamental Research Funds for the Central Universities (K20210226).

References

- (1)

- erc (2015) 2015. ERC20 Token Standard. https://github.com/ethereum/EIPs/blob/master/EIPS/eip-20.md.

- Aave (2020) Aave. Last Accessed: Sep. 2020. Aave. aave.com.

- Balancer (2020) Balancer. Last Accessed: Oct. 2020. Balancer Exchange. balancer.exchange.

- bZx (2020) bZx. Last Accessed: Sep. 2020. bZx. bzx.network.

- Compound (2020) Compound. Last Accessed: Oct. 2020. Compound. https://compound.finance/.

- Daian et al. (2019) Philip Daian, Steven Goldfeder, Tyler Kell, Yunqi Li, Xueyuan Zhao, Iddo Bentov, Lorenz Breidenbach, and Ari Juels. 2019. Flash boys 2.0: Frontrunning, transaction reordering, and consensus instability in decentralized exchanges. arXiv preprint arXiv:1904.05234 (2019).

- defipulse (2020) defipulse. Last Accessed: Sep. 2020. DEFI PULSE. https://www.defipulse.com/.

- dYdX (2020) dYdX. Last Accessed: Sep. 2020. dYdX. dydx.exchange.

- Eskandari et al. (2019) Shayan Eskandari, Seyedehmahsa Moosavi, and Jeremy Clark. 2019. Sok: Transparent dishonesty: front-running attacks on blockchain. In International Conference on Financial Cryptography and Data Security. Springer, 170–189.

- Gudgeon et al. (2020) Lewis Gudgeon, Daniel Perez, Dominik Harz, Arthur Gervais, and Benjamin Livshits. 2020. The Decentralized Financial Crisis: Attacking DeFi. arXiv preprint arXiv:2002.08099 (2020).

- Kamps and Kleinberg (2018) Josh Kamps and Bennett Kleinberg. 2018. To the moon: defining and detecting cryptocurrency pump-and-dumps. Crime Science 7, 1 (2018), 18.

- Liu and Szalachowski (2020) Bowen Liu and Pawel Szalachowski. 2020. A First Look into DeFi Oracles. arXiv preprint arXiv:2005.04377 (2020).

- Maker (2020) Maker. Last Accessed: Sep. 2020. DAI Token. etherscan.io/token/0x6b175474e89094c44da98b954eedeac495271d0f.

- MakerDAO (2020) MakerDAO. Last Accessed: Oct. 2020. MakerDAO. makerdao.com.

- Nakamoto et al. (2008) Satoshi Nakamoto et al. 2008. Bitcoin: A peer-to-peer electronic cash system. (2008).

- Qin et al. (2020) Kaihua Qin, Liyi Zhou, Benjamin Livshits, and Arthur Gervais. 2020. Attacking the DeFi Ecosystem with Flash Loans for Fun and Profit. arXiv preprint arXiv:2003.03810 (2020).

- Saver (2020) DeFi Saver. Last Accessed: Oct. 2020. DeFi Saver. defisaver.com.

- Tether (2021) Tether. Last Accessed: Jan. 2021. Tether: Fiat currencies on the Bitcoin blockchain. https://tether.to/wp-content/uploads/2016/06/TetherWhitePaper.pdf.

- Uniswap (2020) Uniswap. Last Accessed: Sep. 2020. Uniswap. uniswap.org.

- Wood (2014) Gavin Wood. 2014. Ethereum: A secure decentralised generalised transaction ledger. Ethereum project yellow paper 151 (2014), 1–32.

- Xu and Livshits (2019) Jiahua Xu and Benjamin Livshits. 2019. The anatomy of a cryptocurrency pump-and-dump scheme. In 28th USENIX Security Symposium (USENIX Security 19). 1609–1625.

- (YFI) (2020) Yearn.finance (YFI). Last Accessed: Sep. 2020. EMN Token. etherscan.io/token/0x8b31d4A56dD29d18C817ef0fA3990d30ECC5D89b.

- Zoltu (2020) Micah Zoltu. 2020. How to turn $20M into $340M in 15 seconds. https://medium.com/coinmonks/how-to-turn-20m-into-340m-in-15-seconds-48d161a42311.