A Feasible Level Proximal Point Method for Nonconvex Sparse Constrained Optimization

Abstract

Nonconvex sparse models have received significant attention in high-dimensional machine learning. In this paper, we study a new model consisting of a general convex or nonconvex objectives and a variety of continuous nonconvex sparsity-inducing constraints. For this constrained model, we propose a novel proximal point algorithm that solves a sequence of convex subproblems with gradually relaxed constraint levels. Each subproblem, having a proximal point objective and a convex surrogate constraint, can be efficiently solved based on a fast routine for projection onto the surrogate constraint. We establish the asymptotic convergence of the proposed algorithm to the Karush-Kuhn-Tucker (KKT) solutions. We also establish new convergence complexities to achieve an approximate KKT solution when the objective can be smooth/nonsmooth, deterministic/stochastic and convex/nonconvex with complexity that is on a par with gradient descent for unconstrained optimization problems in respective cases. To the best of our knowledge, this is the first study of the first-order methods with complexity guarantee for nonconvex sparse-constrained problems. We perform numerical experiments to demonstrate the effectiveness of our new model and efficiency of the proposed algorithm for large scale problems.

1 Introduction

Recent years have witnessed a great deal of work on the sparse optimization arising from machine learning, statistics and signal processing. A fundamental challenge in this area lies in finding the best set of size out of a total of () features to form a parsimonious fit to the data:

| (1) |

However, due to the discontinuity of norm111Note that is not a norm in mathematical sense. Indeed, for any nonzero ., the above problem is intractable when there is no other assumptions. To bypass this difficulty, a popular approach is to replace the -norm by the -norm, giving rise to an -constrained or -regularized problem. A notable example is the Lasso ([31]) approach for linear regression and its regularized variant

| (2) | |||

| (3) |

Due to the Lagrange duality theory, problem (2) and (3) are equivalent in the sense that there is a one-to-one mapping between the parameters and . A substantial amount of literature already exists for understanding the statistical properties of models ([41, 32, 7, 39, 19]) as well as for the development efficient algorithms when such models are employed ([11, 1, 22, 34, 19]).

In spite of their success, models suffer from the issue of biased estimation of large coefficients [12] and empirical merits of using nonconvex approximations were shown in [26]. Due to these observations, a large body of recent research looked at replacing the -penalty in (3) by a nonconvex function to obtain sharper approximation of the -norm:

| (4) |

where , throughout the paper, is a nonsmooth nonconvex function of the form

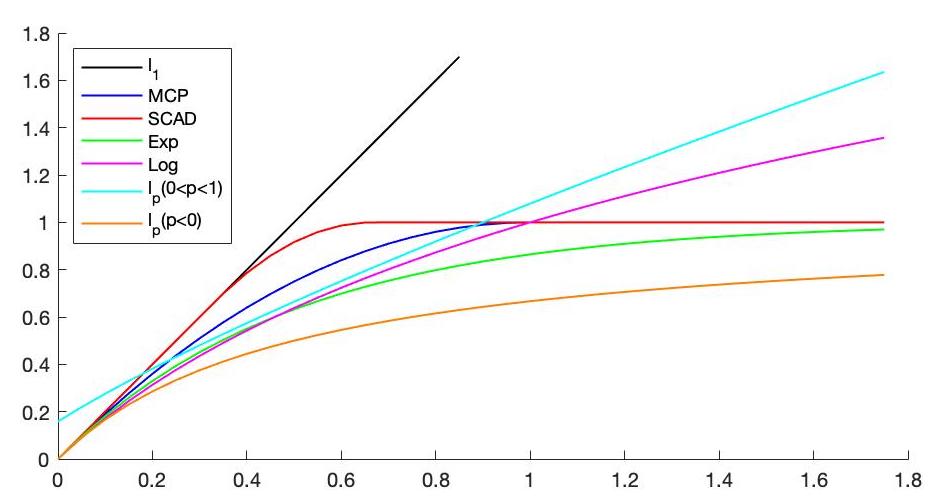

Here is a convex and continuously differentiable function, giving a DC form. This class of constraints already covers many important nonconvex sparsity inducing functions in the literature (see Table 2).

Despite the favorable statistical properties ([12, 38, 8, 40]), nonconvex models have posed a great challenge for optimization algorithms and has been increasingly an important issue ([36, 16, 17, 29]). While most of these works studied the regularized version, it is often favorable to consider the following constrained form:

| (5) |

since sparsity of solutions is imperative in many applications of statistical learning and constrained form in (5) explicitly imposes such a requirement. In contrast, (4) imposes sparsity implicitly using penalty parameter . However, unlike the convex problems, large values of do not necessarily imply small value of the nonconvex penalty .

Therefore, it is natural to ask whether we can provide an efficient algorithm for problem (5). The continuous nonconvex relaxation (5) of the -norm in (1), albeit a straightforward one, was not studied in the literature. We suspect that to be the case due to the difficulty in handling nonconvex constraints algorithmically. There are two theoretical challenges: First, since the regularized form (4) and the constrained form (5) are not equivalent due to the nonconvexity of , we cannot bypass (5) by solving problem (4) instead. Second, the nonconvex function can be nonsmooth especially for the sparsity applications, presenting a substantial challenge for classic nonlinear programming methods, e.g., augmented Lagrangian methods and penalty methods (see [2]) which assumes that functions are continuously differentiable.

Our contributions In this paper, we study the newly proposed nonconvex constrained model (5). In particular, we present a novel level-constrained proximal point (LCPP) method for problem (5) where the objective can be either deterministic/stochastic, smooth/nonsmooth and convex/nonconvex and the constraint models a variety of sparsity inducing nonconvex constraints proposed in the literature. The key idea is to translate problem (5) into a sequence of convex subproblems where is convexified using a proximal point quadratic term and is majorized by a convex function . Note that is a convex subset of the nonconvex set .

We show that starting from a strict feasible point222Origin is always strictly feasible for sparsity inducing constraints and can be chosen as a starting point., LCPP traces a feasible solution path with respect to the set . We also show that LCPP generates convex subproblems for which bounds on the optimal Lagrange multiplier (or the optimal dual) can be provided under a mild and a well-known constraint qualification. This bound on the dual and the proximal point update in the objective allows us to prove asymptotic convergence to the KKT points of the problem (5).

While deriving the complexity, we consider the inexact LCPP method that solves convex subproblems approximately. We show that the constraint, , has an efficient projection algorithm. Hence, each convex subproblem can be solved by projection-based first-order methods. This allows us to be feasible even when the solution reaches arbitrarily close to the boundary of the set which entails that the bound on the dual mentioned earlier works in the inexact case too. Moreover, efficient projection-based first-order method for solving the subproblem helps us get an accelerated convergence complexity of gradient [stochastic gradient] in order to obtain an -KKT point. In particular, refer to Table 1. We see that in the case where objective is smooth and deterministic, we obtain convergence rate of whereas for nonsmooth and/or stochastic objective we obtain convergence rate of . This complexity is nearly the same as that of the gradient [stochastic gradient] descent for the regularized problem (4) of the respective type. Remarkably, this convergence rate is better than black-box nonconvex function constrained optimization methods proposed in the literature recently ([5, 21]). See related work section for more detailed discussion. Note that the convergence of gradient descent does not ensure a bound on the infeasibility of the constraint , whereas the KKT criterion requires feasibility on top of stationarity. Moreover, such a bound cannot be ensured theoretically due to the absence of duality. Hence, our algorithm provides additional guarantees without paying much in the complexity.

| Convex (5) | Nonconvex (5) | |||

|---|---|---|---|---|

| Cases | Smooth | Nonsmooth | Smooth | Nonsmooth |

| Deterministic | ||||

| Stochastic | ||||

We perform numerical experiments to measure the efficiency of our LCPP method and the effectiveness of the new constrained model (5). First, we show that our algorithm has competitive running time performance against open-source solvers, e.g., DCCP [27]. Second, we also compare the effectiveness of our constrained model with respect to the existing convex and nonconvex regularization models in the literature. Our numerical experiments show promising results compared to -regularization model 3 and has competitive performance with respect to recently developed algorithm for nonconvex regularization model 4 (see [16]). Given that this is the first study in the development of algorithms for the constrained model, we believe empirical study of even more efficient algorithms solving problem (5) may be of independent interest and can be pursued in the future.

Related work There is a growing interest in using convex majorization for solving nonconvex optimization with nonconvex function constraints. Typical frameworks include difference-of-convex (DC) programming ([30]), majorization-minimization ([28]) to name a few. Considering the substantial literature, we emphasize the most relevant work to our current paper. Scutari et al. [26] proposed general approaches to majorize nonconvex constrained problems and include (5) as a special case. They require exact solutions of the subproblems and prove asymptotic convergence which is prohibitive for large-scale optimization. Shen et al. [27] proposed a disciplined convex-concave programming (DCCP) framework for a class of DC programs in which (5) is a special case. Their work is empirical and does not provide specific convergence results.

The more recent works [5, 21] considered a more general problems where for some general convex function . They propose a type of proximal point method in which large enough quadratic proximal term is added into both objective and constraint in order to obtain a convex subproblem. This convex function constrained subproblem can be solved by oracles whose output solution might have small infeasibility. Moreover these oracles have weaker convergence rates due to generality of function over . Complexity results proposed in these works, when applied to problem (5), entail iterations for obtaining an -KKT point under a strong feasibility constraint qualification. In similar setting, we show faster convergence result of . This due to the fact that our oracle for solving the subproblem is more efficient than those used in their paper. We can obtain such an oracle due to two reasons: i) convex surrogate constraint in LCPP majorizes the constraint differently than adding the proximal quadratic term, ii) presence of in the form of allows for developing an efficient projection mechanism onto the chosen form of . Moreover, our convergence results hold under a well-known constraint qualification which is weaker compared to strong feasibility since our oracle outputs a feasible solution whereas they can get a solution which is slightly infeasible.

There is also a large body of work on directly optimizing the constraint problem [3, 4, 13, 37, 42]. While [3] can be quite good for small dimension s, it remains unclear how to scale up for larger datasets. Other methods are part of the hard-thresholding algorithms, requiring additional assumptions such as Restricted Isometry Property. These research areas, though interesting, are not related to the continuous optimization setting where large-scale problems can be solved relatively easily. Henceforth, we only focus on the continuous approximations of -norm.

2 Problem setup

Assumption 2.1.

1. is a continuous and possibly nonsmooth nonconvex function satisfying:

| (6) |

2. is a nonsmooth nonconvex function of the form , where is convex and continuously differentiable.

| Function | Parameter | Function |

|---|---|---|

| MCP[38] | ||

| SCAD[12] | ||

| Exp[6] | . | |

| Log[33] | . | |

| [14] | . | |

| [24] | . |

Notations We use to denote standard Euclidean norm whereas -norm is denoted as . The Lagrangian function for problem (5) is defined as where . For nonconvex nonsmooth function in the form of (2), we denote its subdifferential333Various subdifferentials exist in the literature for nonconvex optimization problem. Here, we use subdifferential Definition 3.1 in Boob et al. [5] for nonconvex nonsmooth function . by . For this definition of subdifferential, we consider the following KKT condition:

The KKT condition For Problem (5), we say that is the (stochastic) - KKT solution if there exists and such that ,

| (7) | ||||

Moreover, for , we have that is the KKT solution or satisfied KKT condition. If , we refer to this solution as an -KKT solution in order to be brief.

It should be mentioned that local or global optimality does not generally imply the

KKT condition. However, KKT condition is shown to be necessary for optimality when Mangasarian-Fromovitz constraint qualification (MFCQ) holds [5]. Below, we make MFCQ assumption precise:

Assumption 2.2 (MFCQ [5]).

Whenever the constraint is active: , there exists a direction such that

For differentiable , MFCQ requires existence of such that , reducing to the classical form of MFCQ [2]. Below, we summarize necessary optimality condition under MFCQ.

3 A novel proximal point algorithm

| (8) |

LCPP method solves a sequence of convex subproblems (8). In particular, note that majorizes : implying that is a convex subset of the original problem. It can also be observed that adding a proximal term in the objective yields strongly convex for large enough . In the current form, Algorithm 1 requires a feasible solution of (8) and requirement of sequence is left unspecified. We first make the following assumptions.

Assumption 3.1 (Strict feasibility).

There exist sequence satisfying:

1. and a point of such that

2. The sequence is monotonically increasing and converges

to : .

In light of Assumption 3.1, starting from a strictly feasible point , Algorithm 1 solves subproblems (8) with gradually relaxed constraint levels. This allows us to assert that each subproblem is strictly feasible444For specific examples of , we show that origin is always the most feasible (and strictly feasible) solution of each subproblem and hence, does not require the predefined level-routine of LCPP to assert strict feasibility of subproblem. However, in order to keep generality of discussion, we perform the analysis under the level-setting.. Indeed, we have . This implies the existence of KKT solution for each subproblem. A formal statement can be found in the appendix. Moreover, all the proofs of our technical results can be found in the appendix and we just make statements in the main article henceforth.

Asymptotic convergence of LCPP method and boundedness of the optimal dual

Our next goal is to establish asymptotic convergence of Algorithm 1 to the KKT points. To this end, we require a uniform boundedness assumption on the Lagrange multipliers. First, we prove asymptotic convergence under this assumption then we justify it under MFCQ. Before stating the convergence results, we make the following boundedness assumption.

Assumption 3.2 (Boundedness of dual variables).

There exists such that a.s.

For the deterministic case, we remove the measurablity part in the above assumption and assert that . The following asymptotic convergence theorem is in order.

Theorem 3.3 (Convergence to KKT).

This theorem shows that any limit point of Algorithm 1 converges to a KKT point. However, it makes the assumption that dual is bounded. Since the optimal dual depends on the convex subproblems (8) which are generated dynamically in the algorithm, it is important to justify Assumption 3.2. To this end, we show that Assumption 3.2 is satisfied under a well-known constraint qualification.

Theorem 3.4 (Boundedness condition).

This theorem shows the existence of dual under the MFCQ assumption for all limit points of Algorithm 1. MFCQ is a mild constraint qualification frequently used in the existing literature [2]. In certain cases, we also provide explicit bounds on the dual variables using the fact that origin is most feasible solution to the subproblem. These bounds quantify how “closely" the MFCQ assumption is violated and provides explicitly the effect on the magnitude of the optimal dual. Additional results and discussion in this regard are deferred to the Appendix B. For the purpose of this article, we assume that the dual variables remain bounded henceforth.

Complexity of LCPP method

Our goal here is to analyze the complexity of the proposed algorithm. Apart from the negative lower curvature guarantee (6) of the objective function, we impose that has Lipschitz continuous gradients, This is satisfied by all functions in Table 2. Now we discuss a general convergence result of LCPP method for original nonconvex problem (5).

Theorem 3.5.

Suppose Assumption 3.1 and 3.2 hold such that for all . Let satisfy (9) where and is a summable nonnegative sequence. Moreover, is a feasible solution of the -th subproblem, i.e.,

| (10) |

If is chosen uniformly at random from to K then there exists a pair satisfying

where, , and expectation is taken over the randomness of and solutions , .

Note that Theorem 3.5 assumes that subproblem (8) can be solved according to the framework of (9) and (10). When the subproblem solver is deterministic then we ignore the expectation in (9). It is easy to see from the above theorem that for to be an -KKT point, we must have and must be small enough such that is bounded above by a constant. The complexity analysis of different cases now boils down to understanding the number of iterations of the subproblem solver needed in order to satisfy these requirements on and (or ).

In the rest of this section, we provide a unified complexity result for solving subproblem (8) in Algorithm 1 such that criteria in (9) and (10) are satisfied for various settings of the objective .

Unified method for solving subproblem (8) Here we provide a unified complexity analysis for solving subproblem (8). In particular, consider the form of the objective where is the random input of and satisfies the following property:

Note that, when , function is Lipschitz smooth whereas when , it is nonsmooth. Due to the possible stochastic nature of , negative lower curvature in (6) and the combined smoothness and nonsmoothness property above, we have that can be either smooth or nonsmooth, deterministic or stochastic and convex () or nonconvex (). We also assume bounded second moment stochastic oracle for when is a stochastic function: For any , we have an oracle whose output, , satisfies and .

For such a function, we consider an accelerated stochastic approximation algorithm (AC-SA) proposed in [15] for solving the subproblem (8) which can be reformulated as where is the indicator set function. AC-SA algorithm can be applied when . In particular, is -strongly convex and -Lipschitz smooth. Moreover, AC-SA requires computation of a single prox operation of the following form in each iteration:

| (11) |

for any . We show an efficient method for solving this problem at the end of in this section. For now, we look at convergence properties of the AC-SA:

Proposition 3.6.

Note that convergence result in Proposition 3.6 closely follows the requirement in (9). In particular, we should ensure that is big enough such that and sum to a constant. Consequently, we have the following corollary:

Corollary 3.7.

Note that Corollary 3.7 gives a unified complexity for obtaining KKT point of (5) in various settings of nonconvex objective . First, in order to get an -KKT point, must be of . If the problem is deterministic and smooth then . In this case, is a constant. Hence, the total iteration count is , implying that total iteration complexity for obtaining an -KKT point is of . For nonsmooth or stochastic cases, or is positive. Hence, implying the total iteration complexity , which is of . Similar result for the convex case is shown in the appendix.

Efficient projection We conclude this section by formally stating the theorem which provides an efficient oracle for solving the projection problem (11). Since , the linear form along with ball breaks the symmetry around origin which is used in existing results on (weighted) -ball projection [10, 18]. Our method involves a careful analysis of Lagrangian duality equations to convert the problem into finding the root of a piecewise linear function. Then a line search method can be employed to find the solution in time. The formal statement is as follows:

Theorem 3.8.

There exists an algorithm that runs in -time and solves the following problem exactly:

| (12) |

4 Experiments

The goal of this section is to illustrate the empirical performance of LCPP. For simplicity, we will consider the following learning problem:

where denotes the loss function. Specifically, we consider logistic loss for classification and squared loss for regression. Here is the training sample, and is the MCP penalty (see Table 2). Details of the testing datasets are summarized in Table 3. As we have stated, LCPP can be equipped with projected first order methods for fast iteration. We compare the efficiency of (spectral) gradient descent [16], Nesterov accelerated gradient and stochastic gradient [35] for solving LCPP subproblem. We find that spectral gradient outperforms the other methods in the logistic regression model and hence use it in LCPP for the remaining experiment for the sake of simplicity. Due to the space limit, we leave the discussion of this part in appendix. The rest of the section will compare the optimization efficiency of LCPP with the state-of-the-art nonlinear programming solver, and compare the proposed sparse constrained models solved by LCPP with standard convex and nonconvex sparse regularized models.

| Datasets | Training size | Testing size | Dimensionality | Nonzeros | Types |

| real-sim | 50347 | 21962 | 20958 | 0.25% | C |

| rcv1.binary | 20242 | 677399 | 47236 | 0.16% | C |

| mnist | 60000 | 10000 | 784 | 19.12% | C |

| gisette | 6000 | 1000 | 5000 | 99.10% | C |

| E2006-tfidf | 16087 | 3308 | 150360 | 0.83% | R |

| YearPredictionMSD | 463,715 | 51,630 | 90 | 100% | R |

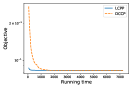

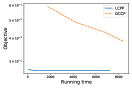

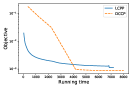

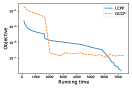

Our first experiment is to compare LCPP with existing optimization library for their optimization efficiency. To the best of our knowledge, DCCP ([27]) is the only open-source package available for the proposed nonconvex constrained problem. While the work [27] has made its code available online, we found that their code had unresolved errors in parsing MCP functions. Therefore, we replicate their setup in our own implementation. DCCP converts the initial problem into a sequence of relatively easier convex problems amenable to CVX ([9]), a convex optimization interface that runs on top of popular optimization libraries. We choose DCCP with MOSEK as the backend as it consistently outperforms DCCP with the default open-source solver SCS.

Comparison is conducted on the classification problem. To fix the parameters, we choose for gisette dataset and for the other datasets. For each LCPP subproblem we run gradient descent at most 10 iterations and break when the criterion is met. We set the number of outer loops as 1000 to run LCPP sufficiently long. We set in the MCP function. Figure 2 plots the convergence performance of LCPP and DCCP, confirming that LCPP is more advantageous over DCCP. Specifically, LCPP outperforms DCCP, sometimes reaching near-optimality even before DCCP finishes the first iteration. This observation can be explained by the fact that LCPP leverages the strengthen of first order methods, for which we can derive efficient projection subroutine. In contrast, DCCP is not scalable to large dataset due to the inefficiency in dealing with large scale linear system arising from the interior point subproblems.

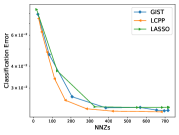

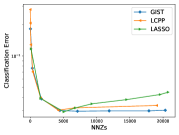

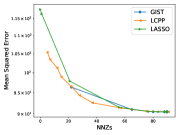

Our next experiment is to compare the performance of nonconvex sparse constrained models, which is then optimized by LCPP, against regularized learning models in the following form:

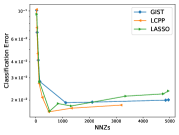

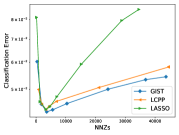

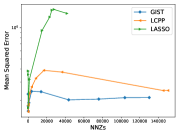

As described above, is the sparsity-inducing penalty function and is a loss function on the data. We consider both convex and nonconvex penalties, namely Lasso-type penalty and MCP penalty (see Table 2). We solve the Lasso penalty problem by linear models provided by Sklearn [23] and solve the MCP regularized problem by the popular solver GIST [16]. For simplicity, both GIST and LCPP set and in MCP function, and set the maximum iteration number as 2000 for all the algorithms. Then we use a grid of values for GIST and LASSO, and for LCPP accordingly, to obtain the testing error under various sparsity levels. In Figure 3 we report the 0-1 error for classification and mean squared error for regression. We can clearly see the advantage of our proposed models over Lasso-type estimators. We observe that nonconvex models LCPP and GIST both perform more robustly than Lasso across a wide range of sparsity levels. Lasso models tend to overfit with increasing number of selected features while LCPP appears to be less affected by the feature selection.

5 Conclusion

We present a novel proximal point algorithm (LCPP) for nonconvex optimization with a nonconvex sparsity-inducing constraint. We prove the asymptotic convergence of the proposed algorithm to KKT solutions under mild conditions. For practical use, we develop an efficient procedure for projection onto the subproblem constraint set, thereby adapting projected first order methods to LCPP for large-scale optimization and establish an complexity for deterministic (stochastic) optimization. Finally, we perform numerical experiments to demonstrate the efficiency of our proposed algorithm for large scale sparse learning.

Broader Impact

This paper presents a new model for sparse optimization and performs an algorithmic study for the proposed model. A rigorous statistical study of this model is still missing. We believe this was due to the tacit assumption that constrained optimization was more challenging compared to regularized optimization. This work takes the first step in showing that efficient algorithms can be developed for the constrained model as well. Contributions made in this paper has the potential to inspire new research from statistical, algorithmic as well as experimental point of view in the wider sparse optimization area.

Acknowledgments

Most of this work was done while Boob was at Georgia Tech. Boob and Lan gratefully acknowledge the National Science Foundation (NSF) for its support through grant CCF 1909298. Q. Deng acknowledges funding from National Natural Science Foundation of China (Grant 11831002).

References

- [1] A. Beck and M. Teboulle. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM Journal on Imaging Sciences, 2(1):183–202, 2009.

- [2] Dimitri P. Bertsekas. Nonlinear programming. Athena Scientific, 1999.

- [3] Dimitris Bertsimas, Angela King, and Rahul Mazumder. Best subset selection via a modern optimization lens. The annals of statistics, pages 813–852, 2016.

- [4] Thomas Blumensath and Mike E Davies. Iterative thresholding for sparse approximations. Journal of Fourier analysis and Applications, 14(5-6):629–654, 2008.

- [5] Digvijay Boob, Qi Deng, and Guanghui Lan. Stochastic first-order methods for convex and nonconvex functional constrained optimization. arXiv preprint arXiv:1908.02734, 2019.

- [6] P.S. Bradley and O. L. Mangasarian. Feature selection via concave minimization and support vector machines. In Proceedings of International Conference on Machine Learning (ICML’98), pages 82–90. Morgan Kaufmann, 1998.

- [7] Emmanuel J Candès, Yaniv Plan, et al. Near-ideal model selection by minimization. The Annals of Statistics, 37(5A):2145–2177, 2009.

- [8] Emmanuel J. Candes, Michael B. Wakin, and Stephen P. Boyd. Enhancing sparsity by reweighted l1 minimization. arXiv preprint arXiv:0711.1612, 2007.

- [9] Steven Diamond and Stephen Boyd. Cvxpy: A python-embedded modeling language for convex optimization. The Journal of Machine Learning Research, 17(1):2909–2913, 2016.

- [10] John Duchi, Shai Shalev-Shwartz, Yoram Singer, and Tushar Chandra. Efficient projections onto the -ball for learning in high dimensions. In Proceedings of the 25th international conference on Machine learning, pages 272–279, 2008.

- [11] Bradley Efron, Trevor Hastie, Iain Johnstone, and Robert Tibshirani. Least angle regression. Annals of Statistics, 32(2):407–499, 2004.

- [12] Jianqing Fan and Runze Li. Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American Statistical Association, 96(456):1348–1360, 2001.

- [13] Simon Foucart. Hard thresholding pursuit: an algorithm for compressive sensing. SIAM Journal on Numerical Analysis, 49(6):2543–2563, 2011.

- [14] Wenjiang J. Fu. Penalized regressions: The bridge versus the lasso. Journal of Computational and Graphical Statistics, 7(3):397–416, 1998.

- [15] Saeed. Ghadimi and Guanghui. Lan. Optimal stochastic approximation algorithms for strongly convex stochastic composite optimization i: A generic algorithmic framework. SIAM Journal on Optimization, 22(4):1469–1492, 2012.

- [16] Pinghua Gong, Changshui Zhang, Zhaosong Lu, Jianhua Z. Huang, and Jieping Ye. A general iterative shrinkage and thresholding algorithm for non-convex regularized optimization problems. International Conference on Machine Learning, 28(2):37–45, 2013.

- [17] Koulik Khamaru and Martin J. Wainwright. Convergence guarantees for a class of non-convex and non-smooth optimization problems. International Conference on Machine Learning, pages 2606–2615, 2018.

- [18] Yannis Kopsinis, Konstantinos Slavakis, and Sergios Theodoridis. Online sparse system identification and signal reconstruction using projections onto weighted balls. IEEE Transactions on Signal Processing, 59(3):936–952, 2011.

- [19] A. Kyrillidis and V. Cevher. Combinatorial selection and least absolute shrinkage via the clash algorithm. In 2012 IEEE International Symposium on Information Theory Proceedings, pages 2216–2220, 2012.

- [20] Guanghui Lan, Zhize Li, and Yi Zhou. A unified variance-reduced accelerated gradient method for convex optimization. In NeurIPS 2019 : Thirty-third Conference on Neural Information Processing Systems, pages 10462–10472, 2019.

- [21] Qihang Lin, Runchao Ma, and Yangyang Xu. Inexact proximal-point penalty methods for non-convex optimization with non-convex constraints. arXiv preprint arXiv:1908.11518, 2019.

- [22] Yurii Nesterov. Gradient methods for minimizing composite functions. Mathematical Programming, 140(1):125–161, 2013.

- [23] F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duchesnay. Scikit-learn: Machine learning in Python. Journal of Machine Learning Research, 12:2825–2830, 2011.

- [24] B. D. Rao and K. Kreutz-Delgado. An affine scaling methodology for best basis selection. IEEE Transactions on Signal Processing, 47(1):187–200, January 1999.

- [25] H. Robbins and D. Siegmund. A convergence theorem for non negative almost supermartingales and some applications. Optimizing Methods in Statistics, pages 111–135, 1971.

- [26] Gesualdo Scutari, Francisco Facchinei, Lorenzo Lampariello, Stefania Sardellitti, and Peiran Song. Parallel and distributed methods for constrained nonconvex optimization-part ii: Applications in communications and machine learning. IEEE Transactions on Signal Processing, 65(8):1945–1960, 2017.

- [27] Xinyue Shen, Steven Diamond, Yuantao Gu, and Stephen Boyd. Disciplined convex-concave programming. In 2016 IEEE 55th Conference on Decision and Control (CDC), pages 1009–1014. IEEE, 2016.

- [28] Ying Sun, Prabhu Sing Babu, and Daniel P. Palomar. Majorization-minimization algorithms in signal processing, communications, and machine learning. IEEE Transactions on Signal Processing, 65(3):794–816, 2017.

- [29] H.A. Le Thi, T. Pham Dinh, H.M. Le, and X.T. Vo. Dc approximation approaches for sparse optimization. European Journal of Operational Research, 244(1):26–46, 2015.

- [30] Hoai An Le Thi and Tao Pham Dinh. DC programming and DCA: thirty years of developments. Mathematical Programming, 169(1):5–68, 2018.

- [31] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), pages 267–288, 1996.

- [32] Martin J Wainwright. Sharp thresholds for high-dimensional and noisy sparsity recovery using -constrained quadratic programming (lasso). IEEE transactions on information theory, 55(5):2183–2202, 2009.

- [33] Jason Weston, André Elisseeff, Bernd Schölkopf, and Mike Tipping. Use of the zero-norm with linear models and kernel methods. The Journal of Machine Learning Research, 3:1439–1461, 2003.

- [34] Stephen J Wright, Robert D Nowak, and Mário AT Figueiredo. Sparse reconstruction by separable approximation. IEEE Transactions on Signal Processing, 57(7):2479–2493, 2009.

- [35] Lin Xiao and Tong Zhang. A proximal stochastic gradient method with progressive variance reduction. SIAM Journal on Optimization, 24(4):2057–2075, 2014.

- [36] Jun ya Gotoh, Akiko Takeda, and Katsuya Tono. DC formulations and algorithms for sparse optimization problems. Mathematical Programming, 169(1):141–176, 2018.

- [37] Xiao-Tong Yuan, Ping Li, and Tong Zhang. Gradient hard thresholding pursuit. The Journal of Machine Learning Research, 18(1):6027–6069, 2017.

- [38] Cun-Hui Zhang. Nearly unbiased variable selection under minimax concave penalty. Annals of Statistics, 38(2):894–942, 2010.

- [39] Cun-Hui Zhang, Jian Huang, et al. The sparsity and bias of the lasso selection in high-dimensional linear regression. The Annals of Statistics, 36(4):1567–1594, 2008.

- [40] Cun-Hui Zhang and Tong Zhang. A general theory of concave regularization for high-dimensional sparse estimation problems. Statistical Science, 27(4):576–593, 2012.

- [41] Peng Zhao and Bin Yu. On model selection consistency of lasso. Journal of Machine learning research, 7(Nov):2541–2563, 2006.

- [42] Pan Zhou, Xiaotong Yuan, and Jiashi Feng. Efficient stochastic gradient hard thresholding. In Advances in Neural Information Processing Systems, pages 1984–1993, 2018.

Appendix A Auxiliary results

A.1 Existence of KKT points

Proposition A.1.

Under Assumption 3.1, let . Then, for any , we have is strictly feasible for the -th subproblem. Moreover, there exists such that and:

| (13) | ||||

Proof.

Since satisfies so we have that first subproblem is well defined. We prove the result by induction. First of all, suppose is strictly feasible for -th subproblem: . Then we note that this problem is also valid and a feasible exists. Hence, algorithm is well-defined. Now, note that

where first inequality follows due to majorization, second inequality follows due to feasibility of for -the subproblem and third strict inequality follows due to strictly increasing nature of sequence .

Since -th subproblem has as strictly feasible point satisfying Slater condition so we obtain existence of and satisfying the KKT condition (13).

∎

A.2 Proof of Theorem 3.3

In order to prove this theorem, we first state the following intermediate result.

Proposition A.2.

Let denotes the randomness of . Assume that there exists a and a summable nonnegative sequence () such that

| (14) |

Then, under Assumption 3.1, we have

1. The sequence is bounded;

2. exists a.s.;

3. a.s.;

4. If the whole algorithm is deterministic then is bounded. Moreover, if , then the sequence is monotonically decreasing and convergent.

Proof.

Due to the strong convexity of , we have

| (15) |

for all satisfying . Taking and using feasibility of ( we have

Together with (9) we have

| (16) |

Since is summable, taking the expectation of and summing up all over all , we have . Moreover, Applying Supermartingale Theorem E.1 to (16), we have exists and a.s. Hence we conclude a.s. Part 4) can be readily deduced from (16). ∎

Now we are ready to prove Theorem 3.3.

For simplicity, we assume the whole sequence generated by Algorithm 1 converges to . Due to Proposition A.1, there exists a KKT point ). The optimality condition yields

| (17) |

Since is bounded, there exists a convergent subsequence that for some . Let us take in (17). In view of Proposition A.2, Part 3, we have almost surely. Then and a.s. due to the continuity of and , respectively. Then we have

implying that minimizes the loss function . Due to the first order optimality condition, we conclude a.s.

Moreover, using the complementary slackness, we have . Taking the limit of and noticing that , we have a.s . As a result, we conclude that is a KKT point of problem (5), a.s.

A.3 Proof of Theorem 3.4

From KKT condition of (13), is the optimal solution of the problem Therefore, for any , we have

| (18) |

We prove that is bounded a.s. by contradiction. If has unbounded subsequence with positive probability, then conditioned under that event, there exists a subsequence such that . Let us divide both sides of (18) by and expand by its definition. After placing , we have for all

| (19) |

Let be any limiting point a.s. of the sequence . By the statement of the theorem, we know that it exists and satisfies MFCQ assumption.

Passing to some subsequence if necessary, we have a.s.

Using Proposition A.2 Part 3, we have a.s. Moreover, using Proposition A.2 Part 2, we have exists a.s. This implies a.s.

Taking , since is bounded a.s. (due to existence of a.s.), we have

.

From Lipschitz continuity of norm and , we have a.s.,

and a.s., respectively. It then follows from (19) that for all , we have

In other words, we have

| (20) |

Moreover, due to complementary slackness and , the equality holds. Hence, in the limit, we have the constraint active a.s. Under MFCQ, there exists such that . However, from (20) we have since , leading to a contradiction to the event that contained unbounded sequence with positive probability. Hence, is bounded a.s.

Appendix B Explicit and specialized bounds on the dual

Here, we discuss some of the results for explicit bounds on the dual. In particular, we focus on the SCAD and MCP case. Similar results can be extended for Exp and case since these function follows two key properties (as we will see later in the proofs):

-

1.

for all for each of these functions.

-

2.

They remain bounded below a constant. See Figure 1.

We exploit these two structural properties of these sparse constraints to obtain specialized and explicit bounds on the optimal dual of problem 5. The following lemma is in order.

Lemma B.1.

Let be the the convex function which satisfies for all . Then the minimum value of defined as is achieved at for all .

Proof.

Note that is a convex function for any . So by first order optimality condition, if is the minimizer of then . This implies

Note that satisfies this condition since in that case . And due to assumption on , we have . Hence is always the minimizer. ∎

Now note that functions defined for our examples, such as SCAD or MCP. satisfy the assumption of bounded gradients in Lemma B.1. Now we use this simple result to show that is the most feasible solution for each of the subproblem (8) generated in Algorithm 1 and hence we can give an explicit bound for the optimal dual value for each subproblem.

Lemma B.2.

Suppose all assumptions in Lemma B.1 are satisfied. Then we have for any ,

| (21) |

Proof.

Note that where is defined in Lemma B.1. Since assumptions of Lemma B.1 hold, so we have that each individual is minimized at . Hence is the minimum value of . In view of Proposition A.1, we have that is strictly feasible solution with respect to constraint implying . Hence, we have

Here, last strict inequality follows due to the fact that and . Then, we have, optimal dual satisfies for all :

where third inequality follows due to the fact that Hence, we conclude the proof. ∎

Note that the bound in (21) depends on which can not be controlled, especially in the stochastic cases. In order to show a bound on irrespective of , we must lower bound the denominator in (21) for all possible values of . To accomplish this goal, we show the following two theorems in which we lower bound the term . Each of these theorem is a specialized result for SCAD and MCP function, respectively.

Theorem B.3.

Let be the SCAD function and such that . Also, let where is the largest nonnegative integer such that . Then, where is the function defined as

Theorem B.4.

Let be the MCP function and be such that Also let where is the largest nonnegative integer such that . Then where is the function defined as

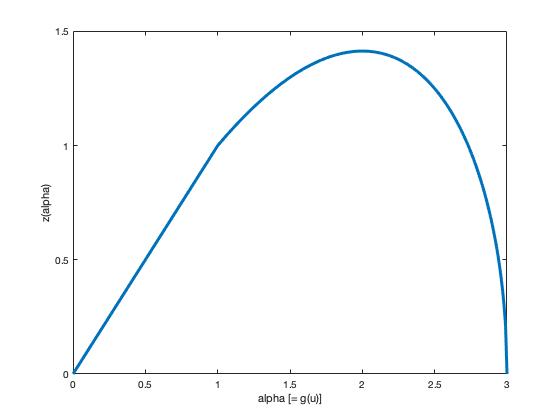

Note that Theorem B.3 states that lower bound when or . In essence, when is exact integral multiple of then lower bound turn out to be zero. However, for all other values of , the corresponding is strictly positive. This can be seen from the graph of below. Similar claims can be made with respect to MCP in Theorem B.4.

Now we are ready to show a bound on irrespective of . We give a specific routine to choose the values of such that we can obtain a provable bound on the denominator in (21) hence obtaining an upper bound on the for all irrespective of .

Proposition B.5.

Let be the SCAD function and where be the largest nonnegative integer such that . Then, for properly selected , we have that .

We note that very similar proposition for MCP can be proved based on Theorem B.4. We skip that discussion in order to avoid repetition.

Connection to MFCQ

In this section, we show the connection of MFCQ assumption in Theorem 3.4 with the bound in Theorem B.3.

Note that for the boundary points of the set where then the lower bound . In fact, carefully following the proof of Theorem B.3, we can identify that the lower bound is tight for ’s such that one of the coordinate satisfy and all other coordinates are . In this case, we see that such points do not satisfy MFCQ. At such points, we don’t have any strictly feasible directions required by MFCQ assumption. This can be easily visualized in the Figure 5 part (a) below. Note that and for any , the feasible region is merely the axis and hence there is no strict feasible direction. This implies MFCQ indeed fails at these points.

For the lower bound is nonzero and same holds for . Indeed, we see that for such cases, the points not satisfying MFCQ in case of vanish. This can be observed in Figure 5 part (b) and part (c). For the case of in part (b), these points become infeasible and for the case of in part (c), they are no longer boundary points.

Looking back at MFCQ from the result of Theorem B.3, we can see that how close is to shows how ‘close’ the problem is for violating MFCQ. Moreover, the lower bound on the denominator of (21) shows how quickly the dual will explode as the problem setting gets closer to violating MFCQ.

B.1 Proof of Theorem B.3

First, we show a lower bound for one-dimensional function and then extend it to higher dimensions. Suppose be such that . Note that since is SCAD function so must lie in the set . Key to our analysis is the lower bound on as a function of . Note that since

| (22) |

Also note that for all , we have and which implies for all . Hence, using this relation along with (22), we obtain

| (23) |

We note that for all and for all . Hence,

| (24) |

Now we design a lower bound when . For such values of , we have

Then, above relation along with (22), we have for all . Using this relation along with (23), (24) and noting the definition of function , we obtain a lower bound where .

Now note that for general high-dimensional , we have . Then . Since each individual , we can think of as a budget such that sum of must equal . In order to minimize the lower bound on , we should exhaust the largest budget from while maintaining the lowest possible value of the lower bound on . This clearly holds by setting such that . This can be clearly observed in the figure below.

Hence, if for some nonnegative integer , then we should set coordinates of satisfying in order to exhaust the maximum possible budget, , from and still keep the value of the lower bound on as . Hence, noting the definition of , the problem reduces to where summation is taken over remaining coordinates of and .

Lets recall from the analysis in 1-D case that if then so we obtain the lower bound while ’s satisfy the relation . Moreover, is a concave function with . Then we show that is a subadditive function. Using Jensen’s inequality, for all , we have . Using and the fact that , we have for any . Now using this relation along with (for ) we have

Adding the two relations, we obtain . Hence, is a subadditive function. Since then the we have . This bound is indeed achieved when we set one of and rest to . Hence, we conclude the proof.

B.2 Proof of Theorem B.4

As before, we proceed by assuming 1-D case, i.e., and and then extend it to general d-dimensional setting. Then, . Then, we write function in term of . Note that

Moreover, we also have (22). Then, noting the definition of , we obtain that .

For high dimensional , we use similar arguments as in the proof of theorem B.3. In particular, we set coordinates satisfying which exhausts the maximum possible budget from and still keeps the value of the lower bound on as . Finally, we reduce the problem to and lower bound is . As in the previous case, is concave function on nonnegative domain with hence it must be subadditive. So we obtain that . Hence, we conclude the proof.

B.3 Proof of Proposition B.5

We note that , where is the largest nonnegative integer such that . Clearly . Now, we divide our analysis in two cases:

Case 1: Suppose . Then we define for Algorithm 1 as .

Now, if then we have that . In this case, we obtain that denominator of (21) is at least .

In other case, suppose that . We also note that . Hence, we obtain . This implies . Then, using Theorem B.3, we obtain that . Using this relation, we obtain that .

So, when , we obtain that the denominator in (21) is at least .

Case 2: Now, we look at the second case where . In this case, we define . Then, we again note that implies .

In other case, we assume that , then again using Theorem B.3, we obtain . This implies .

Finally, then then due to concavity of , we obtain that .

Hence, combining the bounds in both cases, we obtain that denominator in (21) is always bounded below by .

Appendix C Proof of Theorem 3.5

As in the previous case, we show an important recursive property of iterates. We first state the theorem again:

Theorem C.1.

Suppose Assumption 3.1, 3.2 hold such that for all . Let denote the randomness of . Suppose for -th subproblem (8), the solution satisfies

where lies in the interval and is a sequence of nonnegative numbers. If is chosen uniformly randomly from to K then corresponding to , there exists pair satisfying

where, and .

We first prove the following important relationship on the sum of squares of distances of the iterates.

Proposition C.2.

Proof.

Note that since for all we have feasibility of for -th subproblem (due to (10)), then in view of Proposition A.1, we have that is strictly feasible for the -th subproblem. Consequently, using strong convexity of and optimality of , we have . Therefore, taking expectation conditioned on ob both sides of the above relation, we obtain

where second inequality follows from and third inequality follows from (9). Placing the definition of in above relation, we have

Summing up over and taking expectation conditioned on , we have

It then follows that

where the third and the last inequality follow from the property

Note that solution is feasible for the -th subproblem and hence, in view of Proposition A.1, we have that and hence is feasible solution for the main problem implying in the above relation. Then (25) immediately follows.

Now we prove that (26) holds. Note that

where the first inequality follows due to the strong convexity as well as the optimality of and the second inequality follows due to (9). Now summing the above relation from to and taking expectation conditioned on , we obtain

where the last inequality follows from (25) and the definition of . Hence, we conclude the proof. ∎

Now we present the unified convergence of proximal point as stated in Theorem 3.5.

Proof of Theorem 3.5.

Due to the KKT condition for the subproblem (8), we have

| (27) |

Using triangle inequality along with first relation in the above equation, we have . Therefore, noting the bound on from Assumption 3.2, we have

where the second inequality uses Lipschitz smoothness of . Summing the above relation from and the taking expectation conditioned on on both sides, we obtain

| (28) |

For the complementary slackness part of the KKT condition, first notice that . Therefore,

To prove the error of complementary slackness condition, observe that

where second inequality follows due to second relation in (27) and bound on from Assumption 3.2. Summing the above relation from and taking expectation conditioned on on both sides, we obtain

| (29) |

Now note that is a random variable due to randomness of . Now we bound expectation of . In view of (9), we have

Since, and noting that , , we have

Taking expectation on both sides of the above relation and then summing from to , we get

Using the above relation, we obtain

| (30) |

where . Note that here we used the fact . Now taking expectation on both sides of (28) and using bound on in (30), we obtain

Similarly, taking expectation on both sides of (29) and using (30), we obtain

Taking expectation on both sides of (26) and using (30), we obtain

Finally, setting , we have . Therefore, we have

and

Hence, we conclude the proof. ∎

C.1 Proof of Corollary 3.7

C.2 Convergence for the (stochastic) convex case

We have the following Corollary of Theorem 3.5 for the case in which objective is convex, i.e. .

Corollary C.3.

Proof.

Finite-sum problem

A special case of objective takes the finite-sum form thereby leading to the following subproblem

It is known that finite-sum problem can be efficiently solved by using variance reduction or randomized incremental gradient method [35, 20]. The complexity of LCPP on finite-sum problem can be further improved if we apply variance reduction technique for solving the subproblem. We comment on the complexity result in brief. In the finite-sum setting, the Nesterov’s accelerated gradient-based LCPP requires and number of stochastic gradient computations to solve each LCPP subproblem. Even though this number is a constant in terms of dependence on , number of terms () in the finite sum can be large. In comparison to these standard methods, the complexity of SVRG (stochastic variance reduced gradient) based LCPP method can be improved to for the case when is nonconvex satisfying (6) with , and to for convex problem where .

Appendix D Proof for the projection algorithm for problem (11)

We formulate the update as the following problem

| (31) |

Since the objective is strongly convex, problem (31) has a unique global optimal solution. Moreover, the problem is strictly feasible because of the strict feasibility guarantee (A.1) in the context of problem (8). Therefore, KKT condition guarantees that there exists such that

| (32) | ||||

| (33) |

The algorithm proceeds as follows. First, we check whether is feasible, if it is the case, then is the optimal solution. Otherwise, the constraint in (31) is active. Next, we explore the optimality condition (32). Given the optimal Lagrangian multiplier , for the -th coordinate of the optimal , one of the following three situations will occur:

-

1.

and .

-

2.

and .

-

3.

and .

For simplicity, let us denote and . Based on the discussion above, we can express as a piecewise linear function of .

Let us denote . We can deduce that

Above, the second equality uses the identity: for any . It can be readily seen that is a piecewise linear function with at most breaking points. We can sort these points in and then apply a line-search to find the root of in time.

Appendix E Supermartingale convergence theorem

In below, we state a version of supermartingale convergence theorem developed by [25].

Theorem E.1.

Let be a probability space and be some sub--algebra of . Let , be nonnegative -measurable random variables such that

where is a non-negative and summable: . Then we have

Appendix F Additional experiments

This section describes additional experiments for investigating the empirical performance of LCPP. We run all the algorithms on a cluster node with Intel Xeon Gold 2.6G CPU and 128G RAM.

Solving the subproblems

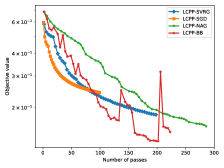

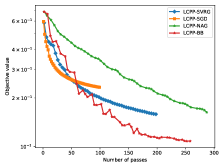

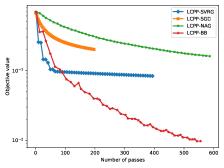

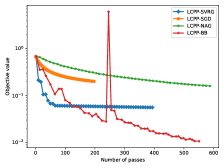

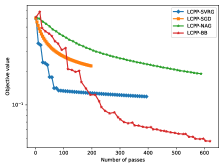

We compare the performance of different instances of LCPP for which the subproblems are solved by a variety of convex algorithms. Specifically, we consider LCPP-SVRG, LCPP-SGD, LCPP-NAG and LCPP-BB in which the subproblems are solved by proximal stochastic variance reduced gradient descent (SVRG [35]), proximal stochastic gradient descent (SGD), Nesterov’s accelerated gradient (NAG[22]) and spectral gradient (Barzilai-Borwein stepsize) respectively. We adopt the spectral gradient descent with non-monotone line search from [16] due to its superior performance in the reported experiments.

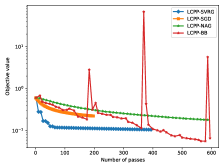

Figure 7 shows the objective vs. number of effective passes over the datasets. Here, each effective pass evaluates one full gradient. We find that stochastic algorithms (LCPP-SGD, LCPP-SVRG) converge more rapidly than deterministic algorithms (LCPP-NAG, LCPP-BB) in the earlier stage, but they do not obtain higher accuracy in the long run. In all the tested datasets, we can observe that LCPP-BB outperforms the other three methods. Moreover, we remark that stochastic gradient algorithms need to compute projections more frequently than deterministic algorithms. While our linesearch routine can efficiently perform projection, it is still more expensive than computing stochastic gradient, particularly, for the sparse data. Hence the overall running time of SGD algorithms is much worse than that of LCBB-BB. For the above reasons, we choose LCPP-BB as our default choice in the main experiment section.

Classification performance

We conduct an additional experiment to compare the empirical performance of all the tested algorithms in sparse logistic regression. We perform grid search based on five-fold cross-validation to find the best hyper-parameters. Then we retrain each model with the chosen hyper-parameter on the whole training dataset and report the classification performance on the testing data. Each experiment is repeated five times. Hyper-parameters: 1) GIST: , where is the size of training data, , 2) LCPP: , , where , 3) Lasso: we set where , , and is chosen by the l1_min_c function in Sklearn. Table 4 summarizes the testing performance (mean and standard deviation) of each compared method. We can observe from this table that LCPP achieves the best performance on three out of the four datasets.

| Datasets | GIST | LCPP | LASSO |

|---|---|---|---|

| gisette | |||

| mnist | |||

| rcv1.binary | |||

| realsim |