Department of Information Engineering,

University of Padova.

January 16, 2021

Sharper convergence bounds of Monte Carlo

Rademacher Averages

through Self-Bounding functions

Abstract

We derive sharper probabilistic concentration bounds for the Monte Carlo Empirical Rademacher Averages (MCERA), which are proved through recent results on the concentration of self-bounding functions. Our novel bounds are characterized by convergence rates that depend on data-dependent characteristic quantities of the set of functions under consideration, such as the empirical wimpy variance, an essential improvement w.r.t. standard bounds based on the methods of bounded differences. For this reason, our new results are applicable to yield sharper bounds to (Local) Rademacher Averages. We also derive improved novel variance-dependent bounds for the special case where only one vector of Rademacher random variables is used to compute the MCERA, through the application of Bousquet’s inequality and novel data-dependent bounds to the wimpy variance. Then, we leverage the framework of self-bounding functions to derive novel probabilistic bounds to the supremum deviations, that may be of independent interest.

Keywords:

Rademacher Complexity, Statistical Learning Theory, Self-bounding Functions, Concentration Inequalities.1 Introduction

Uniform convergence is a central problem in Statistical Learning Theory (Vapnik,, 1998). Obtaining tight and uniformly valid probabilistic bounds on the accuracy of empirical averages of sets of functions is a fundamental problem, with widespread and impactful applications in Machine Learning and Data Science (Anthony and Bartlett,, 2009; Shalev-Shwartz and Ben-David,, 2014; Mitzenmacher and Upfal,, 2017; Mohri et al.,, 2018). Probabilistic bounds on the largest error of the empirical averages are typically obtained by adding to the empirically estimated error a term that depends on the complexity of the functions. Both distribution-free concepts of complexity, such as the VC dimension (Vapnik and Chervonenkis,, 1971), and distribution and data-dependent complexities have been proposed as breakthroughs with great success for this problem ((Koltchinskii and Panchenko,, 2000; Mendelson,, 2002; Bartlett et al.,, 2002; Bartlett and Mendelson,, 2002; Blanchard et al.,, 2003; Bartlett et al.,, 2005; Koltchinskii,, 2006; Blanchard et al.,, 2008; Gnecco and Sanguineti,, 2008; Kloft and Blanchard,, 2011; Anguita et al.,, 2012; Cortes et al.,, 2013; Oneto et al.,, 2015; Lei et al.,, 2015; Oneto et al.,, 2017; Kuznetsov and Mohri,, 2017; Yousefi et al.,, 2018; Yin et al.,, 2019; Lei et al.,, 2019; Musayeva et al.,, 2019) and many others). In this work we provide new convergence bounds for one of the most interesting notions of data-dependent measure of complexity of sets of functions, the Rademacher Complexity. In particular, we show that it can be estimated in a Monte Carlo way obtaining “faster convergence rates” that depend on characteristic quantities of the set of functions and the sample.

A potential drawback of Rademacher Averages is that the “global” error that can be obtained may be characterised by the so called “slow” convergence rate of , where is the number of analysed samples; while such rate is essentially the best possible when some elements of a set of function achieve maximum variance (Boucheron et al.,, 2005), it may be substantially improved for the other functions, that are often more interesting to the analysis. Therefore, a rich collection of contributions (Koltchinskii and Panchenko,, 2000; Massart,, 2000; Bousquet et al.,, 2002; Mendelson,, 2002; Bartlett et al.,, 2005; Koltchinskii,, 2006, 2011; Mendelson,, 2014) have then focused on providing local estimates of the complexity, restricting the estimation to a proper subset of that contains only functions with lower variance. In such settings, one would hope to achieve sharper error bounds, with rates between and .

The slow convergence rate can be attributed to both the “global” computation of Rademacher Averages and from the application of probabilistic concentration inequalities based on the method of bounded differences, that is essentially tight only when there are elements of the set of functions under consideration that achieve maximum variance (Boucheron et al.,, 2013). Therefore, the study of novel concentration inequalities for the supremum of empirical processes that take advantage of smaller bounds to the variance has been a central focus of research, such as the fundamental contributions of Talagrand, (1994, 1995) and many others (Boucheron et al.,, 2000; Bousquet,, 2002; Boucheron et al.,, 2005, 2013).

The standard approach to bound the Rademacher Complexity is through the application of Massart’s Lemma (Massart,, 2000). An alternative, often much sharper, approach is to directly estimate the Rademacher Averages with the -Monte Carlo Empirical Rademacher Average () (defined formally in the next Section); this quantity is computed by sampling a finite number of vectors of Rademacher random variables, instead of evaluating its expectation (Bartlett and Mendelson,, 2002), and then obtaining a probabilistic upper bound to the Rademacher Complexity with concentration of measure inequalities.

In a recent work, De Stefani and Upfal, (2019) used the framework of uniform convergence and Rademacher Complexity to obtain error bounds to empirical averages in an adaptive setting: in their scenario, batch of functions are considered at successive steps, while allowing the choice of the functions to process at every iteration to be based on past information. To quantify the risk of “overfitting”, they leverage the , computing it efficiently as functions are processed. Their analysis relates the to its expectation through Bernstein’s inequality and on the Central Limit Theorem for martingales.

In other situations, in particular when the size of is large, it may be more expensive to compute the , limiting a more widespread practical consideration. In the context of Data Mining and Approximate Pattern Mining, Pellegrina et al., (2020) address this computational challenge, deriving a general and practical scheme to compute the by exploiting the combinatorial structure of in a branch-and-bound strategy. In all these applications, it is critical to apply sharp concentration results to have tight error rates.

The works we described (De Stefani and Upfal,, 2019; Pellegrina et al.,, 2020) achieve error bounds that relate the to its expectation, the Empirical Rademacher Average (ERA), using concentration inequalities based on the bounded difference property (or, equivalently, assuming maximum variance); for this reason, such error bounds are characterised by the slow convergence rate of , analogous to the worst-case rate of uniform convergence we discussed before. While, in theory, one could use an arbitrary large number of vectors of Rademacher random variables, and in particular to achieve error rates for estimating the ERA, this would imply the computation of a large number of supremums over , something impractical in almost all situations.

The question of whether the can be tightly estimated without using an impractically large number of Monte Carlo trials is an unexplored question. In fact, sharp variance-dependent concentration inequalities that relate the to its expectation are not available.

Our contributions. The main goal of this work is to provide a positive answer to this question: in Section 5 we derive novel concentration bounds for the whose convergence rates depend on characteristic quantities computable from the data, such as the empirical wimpy-variance of the set of functions, resulting in a significantly improved trade-off between the guaranteed convergence of the estimate and the number of required vectors of Rademacher random variables. To do so, we first establish, in Section 5.1, self-bounding properties of the MCERA. Then, we leverage such properties to derive, in Section 5.2, novel concentration inequalities for the MCERA w.r.t. its expectation, the ERA; such results follow from the sharp exponential concentration inequalities that self-bounding functions satisfy (Boucheron et al.,, 2000, 2009). Furthermore, in Section 5.3 we study the special case of , and prove a novel concentration inequality that directly relates the MCERA to the Rademacher Complexity, though the application of Bousquet’s inequality (Bousquet,, 2002), a central result in Statistical Learning Theory. As the rate of convergence of such bound depends on the unknown wimpy variance of the set of functions , we show that it can be tightly estimated from the available data using its empirical counterpart, the empirical wimpy variance. The guaranteed accuracy of such empirical estimator is proved with the powerful framework of self-bounding functions.

The new bounds we derive in this work are relevant to all methods based on the we introduced before and, given their generality, possibly others. In particular, we believe it would be interesting to fit our results in the framework of Localised Rademacher Averages, and that there are interesting new algorithmic applications of the that may benefit from our results, in particular in problems already tackled with methods based on Rademacher Averages; examples are the analysis of large networks (Riondato and Upfal,, 2018; de Lima et al.,, 2020), rigorous Pattern Mining (Riondato and Upfal,, 2015; Santoro et al.,, 2020) Statistical Hypothesis Testing (Pellegrina et al.,, 2019; Li and Barber,, 2019), and, potentially, many others.

Another interesting question we explore is whether the maximum difference between empirical averages and their expectation, quantities often denoted by Supremum Deviations (SDs), satisfy some form of self-bounding properties. Indeed, after introducing, in Section 6, the state-of-the-art variance-dependent bounds to the SDs, in Section 7 we show that the SDs are also self-bounding, for appropriate constants that depend on the maximum and minimum expected values of the functions in ; consequently, we derive novel concentration inequalities for the SDs, that may be of independent interest.

We conclude comparing our novel bounds and empirical estimators w.r.t. the state-of-the-art with some simulations, described in Section 8.

2 Preliminaries

We denote to be a class of real valued functions from a domain to the bounded interval , and let and , with , and . To simply address non-negativity issues, we assume w.l.o.g. that contains a constant function such that , for all .

Let a sample be a bag of size , such that . We assume that each element of is drawn i.i.d. from according to an unknown probability distribution . Our goal is to derive tight bounds on the difference between the average value of , computed on the sample , and its expectation , taken w.r.t. , that are valid for all functions . More formally, we define the positive Supremum Deviation (SD) and the negative supremum deviation as

As is unknown, it is not possible to directly compute such supremum deviations. However, fundamental results from Statistical Learning Theory allow to obtain probabilistic upper bounds to them, exploiting information obtainable from the data . We introduce the concepts of Rademacher Averages, that will be instrumental to achieve this goal.

First, let be a matrix such that each component of index is either or . The -Monte Carlo Empirical Rademacher Average () is defined as

Denote the Empirical Rademacher Average (ERA) as the expectation of the w.r.t. the assignments of the Rademacher random variables , where each is or independently and with equal probability:

Then, denote the Rademacher Complexity (RC) as the expectation of the ERA over ,

The following fundamental result, also known as “Symmetrization lemma”, show a precise relationship between the RC and the expected supremum deviation (Shalev-Shwartz and Ben-David,, 2014; Mitzenmacher and Upfal,, 2017).

Lemma 1

Therefore, upper bounding the RC yields upper bounds on the expected supremum deviations; consequently, one can obtain a probabilistic upper bound on the supremum deviations on the sample with the application of concentration inequalities, important tools of probability theory. Most importantly, the RC can be estimated directly on the available data using the . We now define important quantities that will appear in most of our bounds. First, we denote the wimpy variance of as

Then, we denote the empirical wimpy variance of computed on as

We also define another quantity of interest , defined as the supremum mean absolute value of , computed over , that is

In the next Sections we succinctly introduce the most widely used concentration inequalities methods: in Section 3.1 we introduce the method of bounded differences; in Section 3.2 we present the definitions and recent results on self-bounding functions. The concept of self-bounding functions, as we will discuss later, are essential to prove our novel bounds. We remand for a more exhaustive coverage of the topic to the book of Boucheron et al., (2013).

3 Concentration Inequalities

In this Section we introduce two of the most widely employed methods to prove concentration results for functions of independent random variables.

3.1 The Method of Bounded Differences

Let be a vector of variables , each taking values in a measurable set and let be a measurable function. We now introduce the bounded difference property, that is often easy to prove in many settings.

Definition 1 (Bounded difference property)

A function has the bounded difference property if, for each , , there is a nonnegative constant such that:

| (1) |

A central result is given by the following Theorem, that shows that is well concentrated around its mean (taken w.r.t. ), and that the the rate of convergence depends on the constants of the bounded difference property.

Theorem 3.1 (McDiarmid, (1989))

Let be a function with the bounded difference property with constants , for . Let be independent random variables taking value in , and let . Then it holds

Also, it holds

3.2 Self-Bounding Functions

Self-bounding functions are an important class of “well-behaved” functions that enjoys sharp concentration inequalities of their empirical estimates w.r.t. their expected values. We report their definitions and remand to Boucheron et al., (2013) a more in-depth exposition of the subject.

Let be a vector of variables , each taking values in a measurable set and let be a non-negative measurable function. Then denote a function from . In the following definition, we introduce -self-bounding functions; we note that they may also be denoted by strongly -self-bounding functions.

Definition 2 (-self-bounding function)

A function is a -self-bounding function if, for all ,

and

where is obtained by dropping the -th component of .

An often convenient choice of to prove that is self-bounding is

We now introduce weakly -self-bounding function.

Definition 3 (Weakly -self-bounding function)

A function is weakly -self-bounding if, for all ,

Note that a -self-bounding function is also a weakly -self-bounding function.

The next Theorem shows that if is self-bounding, then it is sharply concentrated w.r.t. its expectation (taken w.r.t. ).

Theorem 3.2 (Boucheron et al., (2009))

Let be a vector of independent random variables, each taking values in a measurable set and let be a non-negative measurable function such that has finite mean . Let , and define . Denote and .

If is -self-bounding, then for all ,

If is weakly -self-bounding and for all , all , , then for all ,

If is weakly -self-bounding and for each and , then for ,

Moreover, if is weakly -self-bounding with for all and , then

A stronger result for -self-bounding functions can be stated.

Theorem 3.3 (Boucheron et al., (2000))

Let be a vector of independent random variables, each taking values in a measurable set and let be a non-negative and bounded measurable function. Let .

If is a -self-bounding function, then, it holds, for ,

and, for ,

4 Standard probabilistic bounds

In this Section we report standard bounds to the ERA and the SDs, that are proved using the bounded difference methods, and a standard bound for the RC based on the self-bounding property of the ERA.

4.1 Standard Probabilistic Bound to the ERA

The following result provides a probabilistic upper bound to the ERA from its estimate given by the is obtained through the application of the bounded differences method.

Theorem 4.1

Proof

It is simple to prove that has the bounded difference property with constants , for all . Therefore, the bound follows from Theorem 3.1. ∎

4.2 Standard probabilistic bounds to the RC

A known property of the ERA is that it is a self-bounding function (see, for instance, Example 3.12 of Boucheron et al., (2013) and Oneto et al., (2013)). This implies concentration bounds, proved by Boucheron et al., (2000), that are often sharper than the ones obtained through the bounded difference property.

Theorem 4.2

Let, for , . For all , it holds

| (2) |

Also, with probability , it holds

| (3) |

Proof

From (3) it is clear that, as the ERA gets smaller, the rate of convergence for estimating the RC is between and , an essential improvement in most cases (Boucheron et al.,, 2013). This intuitively suggests why tight bounds to the ERA are useful and required to reach faster rates of convergence, something not achievable with the “slow rate” bound of Theorem 4.1 (at least, not achievable without impractical large Monte Carlo trials), as we will show with simulations in Section 8.

4.3 Standard Probabilistic Bounds to the SDs

The following result gives standard bounds to the Supremum Deviations using their bounded difference property.

Theorem 4.3

Let . Then, it holds

| (4) |

The same holds for .

Proof

It is simple to show that has the bounded difference property with constants , for all . Thus, the bounds follows from Theorem 3.1. ∎

5 New probabilistic bounds to the ERA

In this Section we show that a careful application of recent results for self-bounding functions allows to prove novel bounds to the ERA from the , whose convergence rates depend on usually easy-to-compute functions of the elements of on the sample . In Section 5.1 we show that the is, in fact, -self-bounding and weakly -self-bounding for appropriate values of , , , and . In Section 5.2 we show that this implies novel probabilistic bounds to the ERA. First, define , the “empirical” version of , as

5.1 Self-bounding properties of the

In this Section we prove self-bounding properties of the . We demand the proofs to the Appendix.

The first result states the -self-bounding property of the .

Theorem 5.1 ()

Let a matrix , and define the function as

If , then is a -self-bounding function.

The second result regards the weakly -self-bounding property of the .

Theorem 5.2 ()

Let a matrix , and define the function as

Then is a weakly -self-bounding function.

5.2 New probabilistic bounds on the ERA

In this Section, we show that the self-bounding properties of the we proved yield sharp exponential concentration bounds that relate the to its expectation, the ERA, with significantly improved convergence rates w.r.t. the standard bound of Theorem 4.1. All the proofs can be found in the Appendix.

The first result is based on the self-bounding property of the we proved in Theorem 5.1.

Theorem 5.3 ()

Let be an matrix of Rademacher random variables, such that independently and with equal probability. Then, for all ,

| (5) |

The second result is based on the weakly self-bounding property of the we proved in Theorem 5.2.

Theorem 5.4 ()

Let be an matrix of Rademacher random variables, such that independently and with equal probability. Then, for all ,

| (6) |

We may observe that the denominators of the exponents of (5) and (6) are not known a priori, but depend on the ERA , the quantity we actually want to bound. We remark that plugging an upper bound to is sufficient for the validity of the results. To this aim, we may simply observe that

obtaining that the r.h.s. of (5) and (6) are upper bounded by, respectively,

We now present alternative bounds that only depend on empirical quantities, that are often sharper than plugging the above upper bound to the ERA.

Theorem 5.5 ()

With probability it holds

| (7) |

Also, with probability , it holds

| (8) |

We remark that appropriate lower bounds to the ERA can be similarly derived from the self-bounding properties proved in Section 5.1 and the application of Theorem 3.2.

By directly comparing the bounds we derived by Theorems 5.3 and 5.4 with the one given by Theorem 4.1, we can conclude that the former will be tighter when at least one of the following is satisfied:

As discussed before, since , a sufficient condition for our results to be sharper is given by

In particular, our novel results allow to bound the ERA below with an of the order of

matching the rate of convergence of the ERA to the RC given by Theorem 4.2, instead of the slow rate bound. We also remark that, when we bound , both and are deterministic quantities since the sample is fixed; thus, they can be used to select the probabilistic result to apply, as they do not depend on the realisation of any random variable.

5.3 New special bounds for

An interesting case in applications is when only vector of Rademacher random variable is used to compute the . In addition of being faster to compute than , Pellegrina et al., (2020) show that in this case one may obtain a sharper bound to the SDs with only one and direct application of the bounded difference method, considering pairs composed by Rademacher random variables and samples of as i.i.d. random variables form an appropriate joint distribution. We now present a variant of their result, that upper bounds the RC instead of the SDs, that is useful to us to be compared with the novel result we prove with Theorem 5.7.

Theorem 5.6 (Theorem 4.6, Pellegrina et al., (2020))

It holds

thus, with probability , it holds

They also remark that applying the result to the range centralised set of functions

is often convenient as it gives the sharpest constants in the bound (as for is equal to ).

We now derive an analogous but significantly sharper bound, whose convergence rate depends on the wimpy variance of . Our proof, postponed to the Appendix, is based on the application of a left tail of Bousquet’s inequality.

Theorem 5.7 ()

With probability , it holds

| (9) | ||||

| (10) |

We may observe that (10) may be sharper than the combined application of (6) and (2) when , since the empirical wimpy variance appears in (6) with a factor , while the wimpy variance in (10) has a factor . On the other hand, one should have (or compute on the data) an upper bound to to apply the result, while Theorem 5.4 only requires to compute its empirical counterpart .

Nevertheless, we show that the empirical wimpy variance yields a sharp upper bound to the wimpy variance . Our analysis again relies on the powerful framework of self-bounding functions.

Theorem 5.8 ()

For , it holds

| (11) |

Furthermore, with probability , it holds

| (12) |

This result shows that the empirical wimpy variance is an accurate empirical estimator of the wimpy variance ; we believe such observation may have interesting applications in establishing “global” fast rates of convergence of the SDs, as shown by Oneto et al., (2016).

6 Variance-dependent probabilistic bounds to the Supremum Deviations

In this section we state a central result in Statistical Learning Theory, due to Bousquet, (2002), the sharpest refinement of a number of improvements of the work of Talagrand, (1994) on bounds on the deviation of the suprema of empirical processes. This result can be applied to derive bounds on the supremum deviations that depend on the maximum variance of the functions of . These bounds can be dramatically sharper than the ones obtainable with the bounded differences method if is sufficiently smaller than its maximum possible value (equal to from Popoviciu, (1935) inequality on variances).

We first report the result of Bousquet (in the version stated by Theorem A.1 of Bartlett et al., (2005)).

Theorem 6.1 (Theorem 2.3, Bousquet, (2002))

Let , be independent random variables distributed according to a probability distribution , and let be a set of functions from to . Assume that all functions satisfy and . Let . Then, for any ,

where , and .

Variance-dependent bounds to the SDs follow from Theorem 6.1.

Theorem 6.2

Let , and define and the function . Then, it holds

| (13) |

Also, with probability at least , it holds

| (14) |

The same results are valid for .

7 New probabilistic bounds to the Supremum Deviations

Bousquet, (2003) shows that Theorem 6.1 can be applied to analyze the concentration of the supremum of empirical processes for sets of functions satisfying a sub-additive property, a variant of the -self-bounding property with relaxed requirements; in fact, the supremum deviation is sub-additive (see Section 6 and Lemma C.1 of (Bousquet,, 2003)), but is not, in general, -self-bounding. Still, in this Section we show that the supremum deviation is -self-bounding, for appropriate values of that depend on the maximum and minimum expectations of the elements of . Consequently, we obtain novel bounds to the supremum deviation by applying concentration results for self-bounding functions, similarly to what we did for the .

We first prove self-bounding properties for the supremum deviations. Define and as the gaps between the boundaries of the codomains of functions in and their expectations, such that

Theorem 7.1 ()

Assume . Let be

Then, is a -self-bounding function.

Theorem 7.2 ()

Assume . Let be

Then, is a -self-bounding function.

We now apply the concentration inequalities given by Theorem 3.2 to obtain novel bounds on the supremum deviations. The first results regards the concentration of .

Theorem 7.3 ()

Let be

Then, it holds

| (15) |

Consequently, with probability ,

| (16) |

An analogous result is valid for .

Theorem 7.4 ()

Let be

Then, it holds

| (17) |

Consequently, with probability ,

| (18) |

We may observe that the novel bounds we proved are less versatile than the result of Bousquet, as they may give faster convergence rates (w.r.t. the bounded difference method) for only one side of the deviation at a time (i.e., either for or ) instead of both simultaneously; this is because, for the same , and cannot be both small. However, we observe that such results may be applicable to properly selected subsets of , in a localized fashion. It is not trivial to directly compare these bounds with Bousquet’s, in particular (13) as it is implicit. However, we observed that our new bounds are slightly sharper than Bousquet’s for some range of the values of the quantities involved in the equations, since some of the constants are more favourable. In particular, we can see that, when , the dependence of the additive error term for of (16) (and (18)) on is lower than the one in (14) by a factor ; therefore, when the squared term dominates the error term, (16) (resp. (18)) is smaller than (14) when (resp., ), as we will discuss in Section 8 with some simulations. Therefore, we conclude that the combination of Theorem 6.2 and our new results gives opportunities to obtain sharper bounds to the SDs of general families of functions.

These results depend on, respectively, the maximum or minimum expected values of elements of , while Bousquet’s inequality requires an upper bound to their maximum variance; a problem in applications is how to handle the cases where these quantities are not known in advance: one intuitive solution is to estimate them from the data.

Regarding the maximum variance , we point out that the bounds and to the expectations of may be sufficient to handle it; in fact, from Bhatia and Davis, (2000), one has that, for all ,

| (19) |

with equality when has binary codomain . Consequently, we have that

Therefore, bounds to and are of interest, as they suffice for the application of our results and Bousquet’s inequality, and may give particularly good bounds for binary functions. Thus, in the following, we show that it is possible to sharply estimate both and from the data, analogously to the empirical estimator for the wimpy variance we proved in Section 5.3. The proofs are in the Appendix.

Define the empirical estimators and of, respectively, and as

Theorem 7.5 ()

For , it holds

| (20) |

Furthermore, with probability , it holds

| (21) |

Theorem 7.6 ()

For , it holds

| (22) |

Furthermore, with probability , it holds

| (23) |

8 Simulations

In this Section we perform some simulations to compare our new bounds with standard available bounds, presented in Section 4.

In Section 8.1 we compare different upper bounds to the ERA, computed from the . In Section 8.2 we compare different approaches to bound the RC from either direct bounds from the , or with intermediate bounds to the ERA. In Section 8.3 we compare the variance-dependent bound on the SDs, from Bousquet’s inequality, with our novel bounds, presented in Section 7.

8.1 Bounds to the ERA

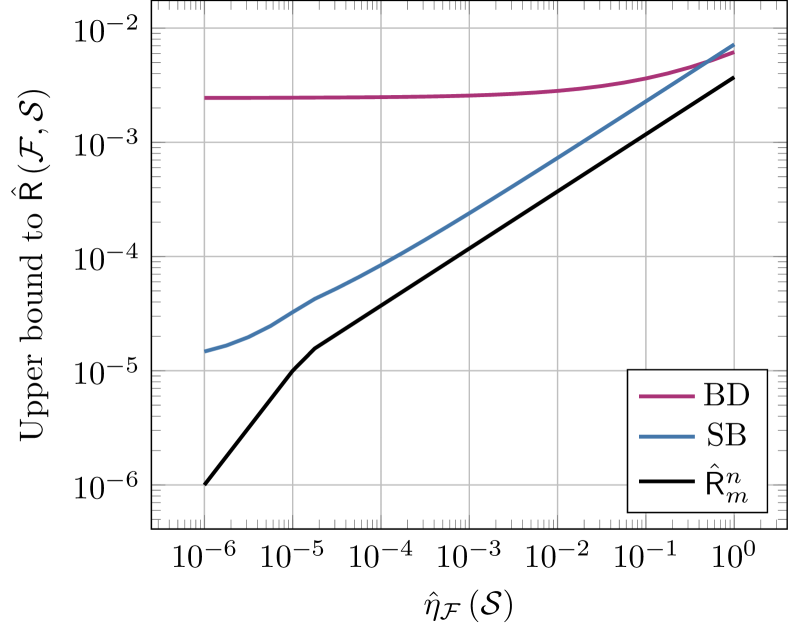

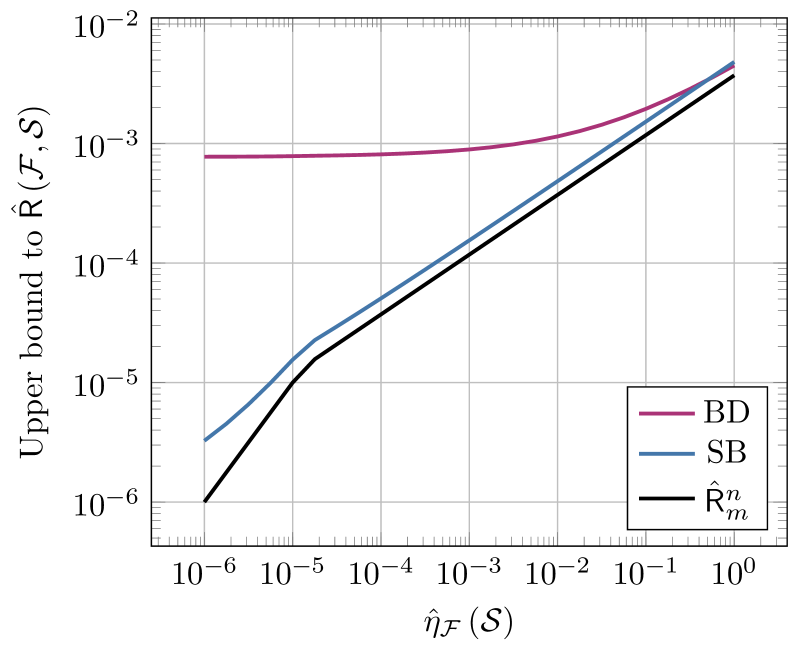

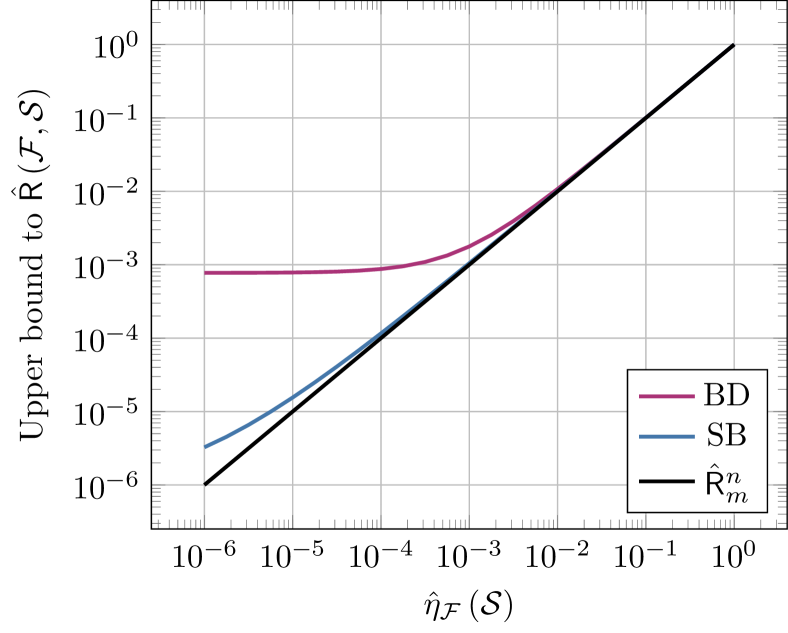

In this Section we compare the standard bound given by the bounded difference method presented in Section 4.1 with the novel bounds presented in this work in Section 5.

To do so, we fix , , and we simulate some values for the MCERA as functions of in the interval . For all such values, we compute upper bounds to the ERA using the standard bound of Theorem 4.1 and our novel bound of Equation 7, fixing in all cases . For a given value of , we set to

| (24) |

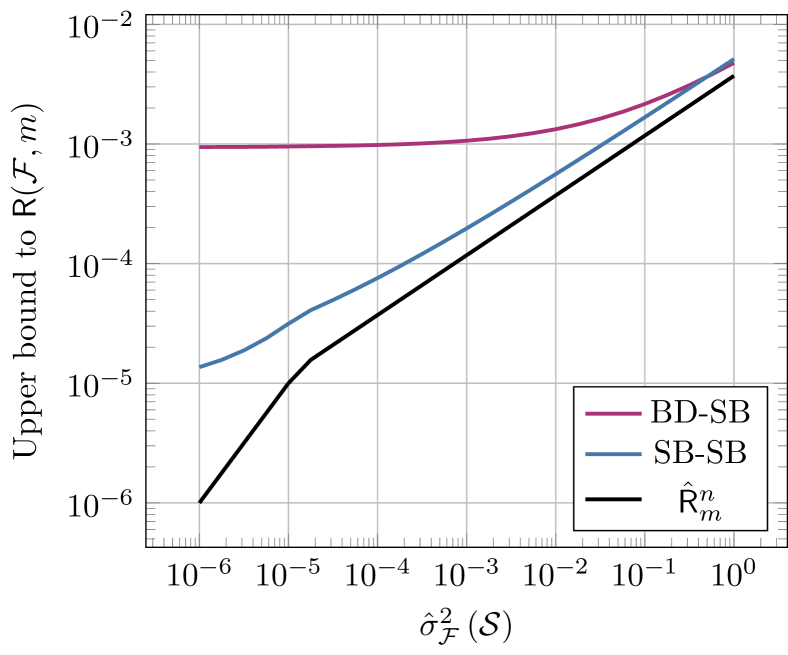

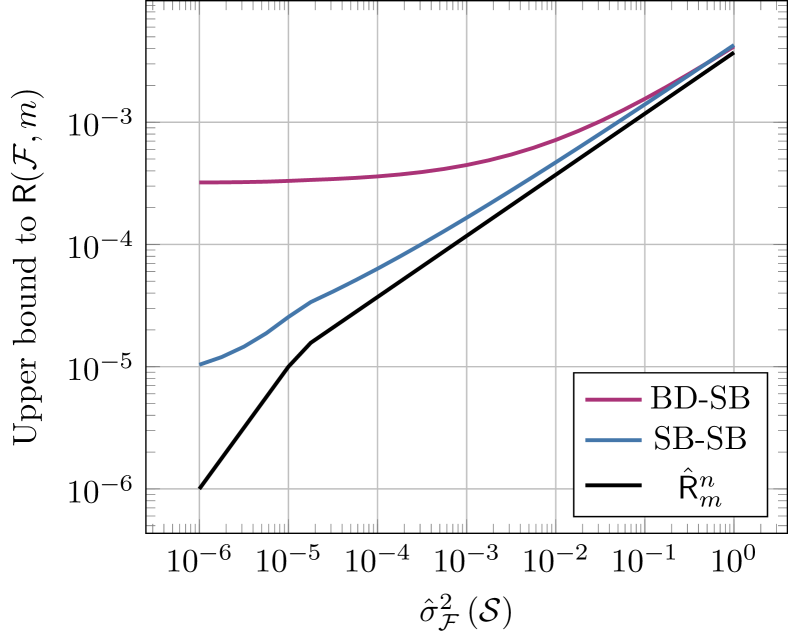

with . This quantity gives a bound to the that is comparable to one given by Massart’s Lemma for a family of functions of size , in order to simulate a realistic rate of decay of the ERA (Boucheron et al.,, 2013). The results for are shown in Figures 1(a)-1(c). We also consider the worst-case , least favourable for our bounds, in Figure 1(d).

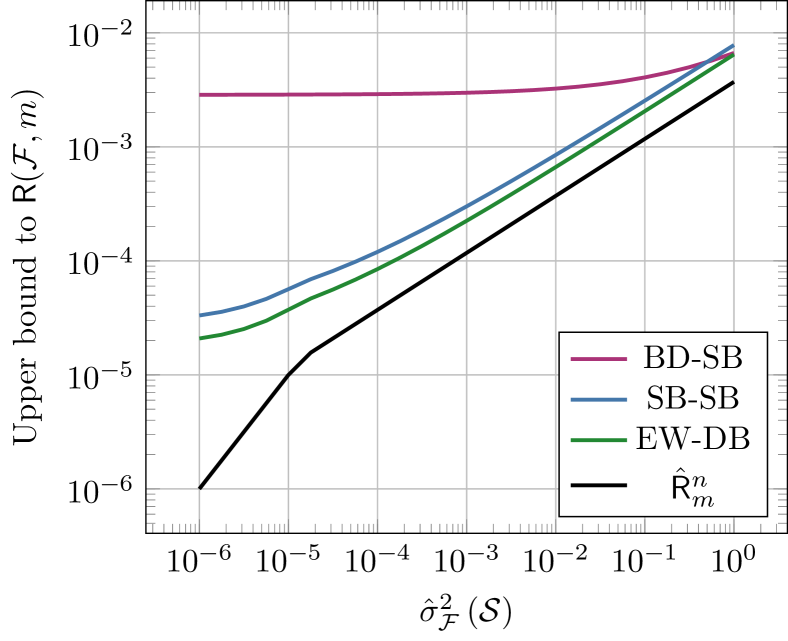

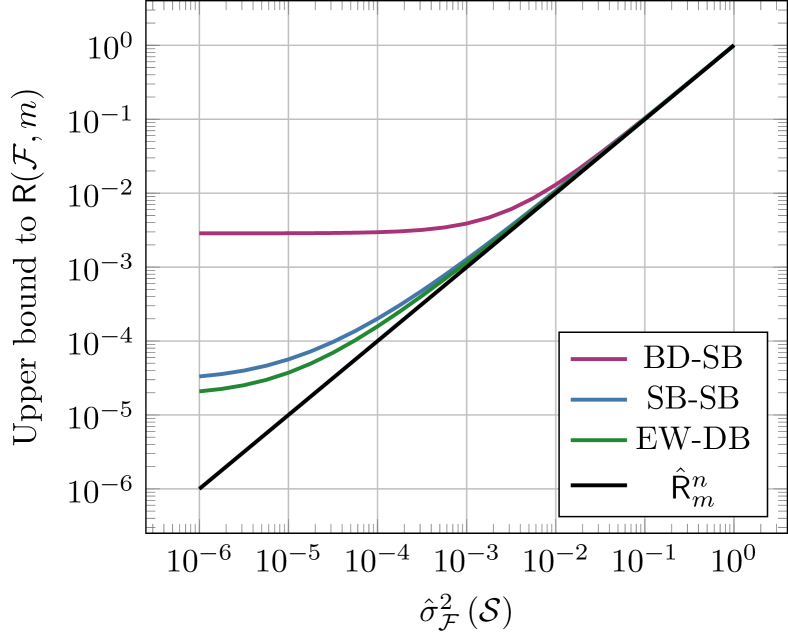

8.2 Bounds to the RC

In this Section we evaluate different upper bounds to the RC . In particular, we compare the composition of standard bounds (Theorems 4.1 and 4.2) and two alternative approaches based on our contributions: we consider the combination of the standard self-bounding bound to the RC from the ERA (Theorem 4.2), and our novel bound of Equation 7 from the to the ERA. For , we also evaluate the accuracy of the direct bound to the RC from the (Equation 10), bounding the wimpy variance from the empirical wimpy variance, as showed by Theorem 5.8 (Equation 12). We use the same parameters of Section 8.1, but we vary in the interval . To simulate values for , we use again (24) replacing by , and also consider the case . Results for different values of are shown in Figure 2.

We conclude from Figure 2 that the slow rate given by estimating the ERA though the standard bound (BD-SD) propagates to the bound to the RC , following the same trend observed in Section 8.1, with analogous results for different values for . Therefore, our novel bounds are essential to achieve faster rates of convergence for estimating the RC from the . We further observe that, in the case (Figures 2(a) and 2(d)), our novel direct bound (EW-DB, Equation 10) achieve even sharper guaranteed accuracy w.r.t. the “full self-bounding” approach (SB-SB), due to some of the constants being more favourable, and thanks to the sharp empirical estimator of the wimpy variance (Equation 12), as we discussed in more details in Section 5.3.

8.3 Bounds to the SDs

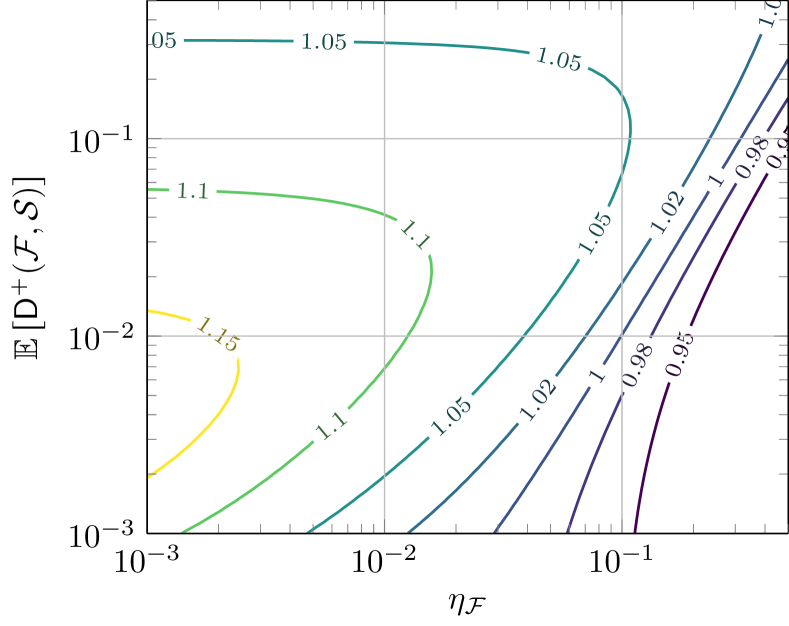

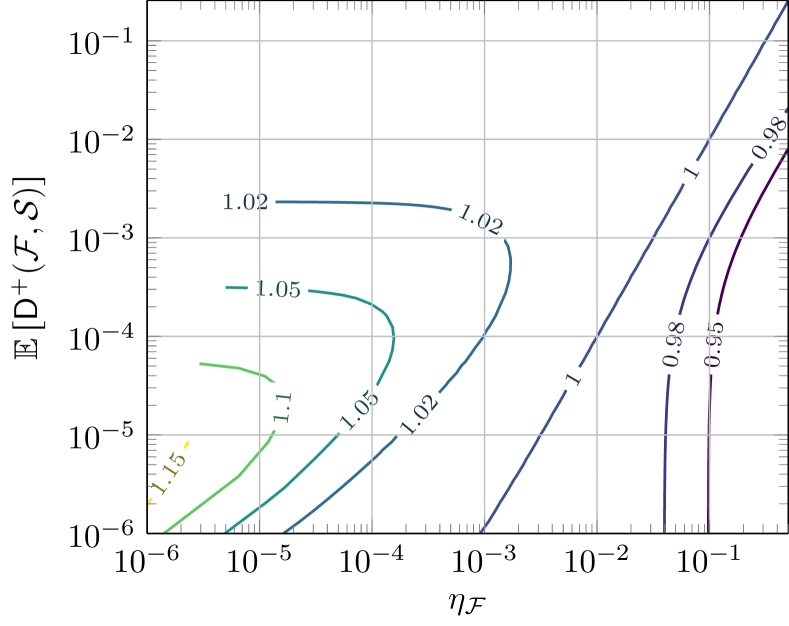

Next, we consider our newly introduced bounds to the SDs (SB, from Theorems 7.3 and 7.4) to assess their behaviour w.r.t. the variance-dependent bound (VD), obtained through Bousquet’s inequality (Theorem 6.2). To do so, we consider the setting of binary functions , of interest, for example, for evaluating the performance of classification models with - loss. This setting simplifies the evaluation of to , required by Bousquet’s inequality. We focus on bounding , using Bousquet’s inequality (14) and our novel result (16). We compute both values varying and over (so that, in such case, ), and compute the ratio between the upper bounds to . We report in Figure contour plots (with levels ) for such measurements, fixing and .

From Figure 3 we can conclude that, as intuitively guessed in Section 7, there is a region of values of and in which our novel bound is tighter, that is the region close to where . We may see that such difference is more pronounced with relatively average size samples (Figure 3(a)), but still present for larger samples (Figure 3(b)).

9 Conclusions

In this work we studied the self-bounding properties of the , and show that they allow to derive novel sharper concentration bounds w.r.t. its expectation. Obtaining tight error rates on the is of central importance to obtain tight probabilistic upper bounds on the Rademacher Averages and, therefore, uniform deviation bounds to the maximum deviation between empirical means and their expectations of sets of functions.

While in this work we focused on deriving concentration results valid with high probability in finite samples, another interesting direction is to combine the self-bounding properties we proved with asymptotical concentration results, such as the Central Limit Theorem for martingales (Hall and Heyde,, 2014). In fact, De Stefani and Upfal, (2019) (in their Theorem 6) have shown how to apply this result to bound the Supremum Deviation from the ; as they discuss, in many applications asymptotic bounds may be preferred as they may be sharper than their finite-sample counterparts, in particular when the size of the analysed data is sufficiently large and the convergence to the normal distribution is reasonably accurate. The self-bounding properties we proved in this work imply tighter bounds on the variance of the random processes modelled by such martingales (see Chapter 6.11 of Boucheron et al., (2013)); therefore, an interesting question is whether our results could enable a sharper application of the Central Limit Theorem for martingales in such setting.

Then, we remark that extending Theorem 9 to directly bound the SDs and for should be possible, provided that a careful analysis of the maximum variance of a properly modified set of functions (analogous to the set defined in the proof of Theorem 5.7) is handled. De Stefani and Upfal, (2019) follow this idea (in their Theorems 2 and 4) to directly bound the RC or SDs from the ; the resulting bounds are derived by controlling the covariances of the random variables involved in their martingales. We believe that combining such derivations with our application of Bousquet’s inequality is an interesting direction to explore, as, according to our simulations (Section 8.2), such approach seems quite promising.

Finally, we conclude by observing that there is a gap between the guaranteed concentration of -self-bounding functions and general (weakly) -self-bounding functions (i.e., see the bounds of Theorems 3.2 and 3.3), as the latter do not enjoy the same Bennet-type bounds of the former; the same holds between the two sides of Bousquet’s inequality (see Section 12.5 of (Boucheron et al.,, 2013), and Theorem 6.1 and Corollary 1). Filling these gaps is an interesting and important research question. We point out that, in case stronger results on the concentration of self-bounding functions may be obtained, they would immediately be applicable to obtain even stronger convergence bounds for , thanks to its self-bounding properties we have shown in this work.

10 Acknowledgments

We would like to thank Fabio Vandin for fruitful discussions and precious comments that improved this manuscript.

Appendix 0.A Missing proofs

0.A.1 Proof of Theorem 5.1

See 5.1

Proof

Denote the function , for and , as

This function correspond to where the element of coordinates of is replaced by ; in addition, we take the infimum over . We remark that, even if is the argument of to simplify notation, never appears in the definition of , as required in the definition of self-bounding functions. To show that is -self-bounding, according to the definition, we have to show that, for all , the inequalities

and

| (25) |

all hold for some non-negative and . First, follows from writing as

and from the observation that one argument of the is equal to , therefore the minimum is either equal to or . We now prove that, if , , for all and for all and .

Let be one of the functions of attaining the supremum of . Then we continue

| (26) |

We first observe that

obtaining

Therefore, we continue from (26) as follows:

We now prove (25) for and .

| (27) |

concluding the proof. ∎

0.A.2 Proof of Theorem 5.2

See 5.2

0.A.3 Proof of Theorem 5.3

See 5.3

Proof

Define the set of functions

composed by all functions divided by ; clearly, , . We now show that (consequently, also ) is a non-negative function:

From Theorem 5.1, we have that is a -self-bounding function. This implies that it is also a weakly -self-bounding function. Then, note that . We combine these facts with Theorem 3.2, obtaining, for ,

We observe that , , and that . We make these substitutions, obtaining

We further substitute by , obtaining the statement. ∎

0.A.4 Proof of Theorem 5.4

See 5.4

0.A.5 Proof of Theorem 5.5

See 5.5

Proof

We prove the first inequality, as proving the second is analogous. From Theorem 5.3, we have that, with probability ,

An upper bound to can be obtained by finding the fixed point of the function

In fact, it is trivial to prove the following.

Lemma 2

Let . The fixed point of

is at

Thus, we apply Lemma 2 to obtain, after simple calculations, the statement.

0.A.6 Proof of Theorem 5.7

See 5.7

Proof

Define the set of functions as

where is a Rademacher random variable. Therefore, we observe that, from independence of the random variables and ,

We now need the following left tail bound of Bousquet’s inequality.

0.A.7 Proof of Theorem 5.8

See 5.8

Proof

We first prove that

by observing, through Jensen’s inequality, that

We now show that is a -self-bounding function. Let the function , and, for , let the function be

First, it holds , and , for all and all , as . We now prove that . Let be one of the functions of attaining the supremum for ; then,

Consequently, we have

that concludes the proof that is a -self-bounding function. We now apply Theorem 3.3 to obtain a probabilistic bounds to the expectation of ; we have

The fact that has two implications: first, we have that

then, due to the monotonicity of in , we have

obtaining the first bound of (11). The second follows from the fact that , as pointed out by Boucheron et al., (2000). The inequality (12) follows from bounding the rightmost term of (11) below , and by applying Lemma 2. ∎

0.A.8 Proof of Theorem 7.1

See 7.1

Proof

Let be

Notice that, as done before, is ignored in the definition of . Let be one of the functions in that attains the supremum for . We then have

We then observe that ; assuming that , we have . We then continue with

obtaining the statement. ∎

0.A.9 Proof of Theorem 7.2

See 7.2

Proof

Define the set of functions . We have that , that , and that . Therefore,

Then, we may observe that

Thus, we apply Theorem 7.1 to and to show that it is -self bounding, obtaining the statement. ∎

0.A.10 Proof of Theorem 7.3

See 7.3

0.A.11 Proof of Theorem 7.4

See 7.4

0.A.12 Proof of Theorem 7.5

See 7.5

Proof

We follow similar steps taken in the proof of Theorem 5.8. We first prove that

by observing, through Jensen’s inequality, that

We now show that is a self-bounding function. Let the function , and, for , let the function be

First, it holds , as , and by definition of . We now prove that . Let be one of the functions of attaining the supremum for ; then,

Consequently, we have

that concludes the proof that is a -self-bounding function. We now apply Theorem 3.3 to a family of functions that is scaled by (i.e., as we did in the proof of Theorem 5.3) to obtain a probabilistic bounds to the expectation of ; we have

As in the proof of Theorem 5.8, implies that

and

By combining these two observations, we obtain the first bound of (20). The second follows from the fact that , as pointed out by Boucheron et al., (2000). The inequality (21) follows from bounding the rightmost term of (11) below , and by applying Lemma 2. ∎

0.A.13 Proof of Theorem 7.6

See 7.6

References

- Anguita et al., (2012) Anguita, D., Ghio, A., Oneto, L., and Ridella, S. (2012). In-sample and out-of-sample model selection and error estimation for support vector machines. IEEE Transactions on Neural Networks and Learning Systems, 23(9):1390–1406.

- Anthony and Bartlett, (2009) Anthony, M. and Bartlett, P. L. (2009). Neural network learning: Theoretical foundations. Cambridge University Press.

- Bartlett et al., (2002) Bartlett, P. L., Boucheron, S., and Lugosi, G. (2002). Model selection and error estimation. Machine Learning, 48(1-3):85–113.

- Bartlett et al., (2005) Bartlett, P. L., Bousquet, O., Mendelson, S., et al. (2005). Local rademacher complexities. The Annals of Statistics, 33(4):1497–1537.

- Bartlett and Mendelson, (2002) Bartlett, P. L. and Mendelson, S. (2002). Rademacher and Gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3(Nov):463–482.

- Bhatia and Davis, (2000) Bhatia, R. and Davis, C. (2000). A better bound on the variance. The American Mathematical Monthly, 107(4):353–357.

- Blanchard et al., (2008) Blanchard, G., Bousquet, O., Massart, P., et al. (2008). Statistical performance of support vector machines. The Annals of Statistics, 36(2):489–531.

- Blanchard et al., (2003) Blanchard, G., Lugosi, G., and Vayatis, N. (2003). On the rate of convergence of regularized boosting classifiers. Journal of Machine Learning Research, 4(Oct):861–894.

- Boucheron et al., (2005) Boucheron, S., Bousquet, O., and Lugosi, G. (2005). Theory of classification: A survey of some recent advances. ESAIM: probability and statistics, 9:323–375.

- Boucheron et al., (2000) Boucheron, S., Lugosi, G., and Massart, P. (2000). A sharp concentration inequality with applications. Random Structures & Algorithms, 16(3):277–292.

- Boucheron et al., (2013) Boucheron, S., Lugosi, G., and Massart, P. (2013). Concentration inequalities: A nonasymptotic theory of independence. Oxford university press.

- Boucheron et al., (2009) Boucheron, S., Lugosi, G., Massart, P., et al. (2009). On concentration of self-bounding functions. Electronic Journal of Probability, 14:1884–1899.

- Bousquet, (2002) Bousquet, O. (2002). A Bennett concentration inequality and its application to suprema of empirical processes. Comptes Rendus Mathematique, 334(6):495–500.

- Bousquet, (2003) Bousquet, O. (2003). Concentration inequalities for sub-additive functions using the entropy method. In Stochastic inequalities and applications, pages 213–247. Springer.

- Bousquet et al., (2002) Bousquet, O., Koltchinskii, V., and Panchenko, D. (2002). Some local measures of complexity of convex hulls and generalization bounds. In International Conference on Computational Learning Theory, pages 59–73. Springer.

- Cortes et al., (2019) Cortes, C., Greenberg, S., and Mohri, M. (2019). Relative deviation learning bounds and generalization with unbounded loss functions. Annals of Mathematics and Artificial Intelligence, 85(1):45–70.

- Cortes et al., (2013) Cortes, C., Kloft, M., and Mohri, M. (2013). Learning kernels using local rademacher complexity. Advances in neural information processing systems, 26:2760–2768.

- de Lima et al., (2020) de Lima, A. M., da Silva, M. V., and Vignatti, A. L. (2020). Estimating the percolation centrality of large networks through pseudo-dimension theory. In Proceedings of the 26th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 1839–1847.

- De Stefani and Upfal, (2019) De Stefani, L. and Upfal, E. (2019). A rademacher complexity based method for controlling power and confidence level in adaptive statistical analysis. In 2019 IEEE International Conference on Data Science and Advanced Analytics (DSAA), pages 71–80. IEEE.

- Gnecco and Sanguineti, (2008) Gnecco, G. and Sanguineti, M. (2008). Approximation error bounds via rademacher’s complexity. Applied Mathematical Sciences, 2(4):153–176.

- Grünwald and Mehta, (2020) Grünwald, P. D. and Mehta, N. A. (2020). Fast rates for general unbounded loss functions: From erm to generalized bayes. Journal of Machine Learning Research, 21(56):1–80.

- Hall and Heyde, (2014) Hall, P. and Heyde, C. C. (2014). Martingale limit theory and its application. Academic press.

- Kloft and Blanchard, (2011) Kloft, M. and Blanchard, G. (2011). The local rademacher complexity of lp-norm multiple kernel learning. In Advances in Neural Information Processing Systems, pages 2438–2446.

- Koltchinskii, (2006) Koltchinskii, V. (2006). Local Rademacher complexities and oracle inequalities in risk minimization. The Annals of Statistics, 34(6):2593–2656.

- Koltchinskii, (2011) Koltchinskii, V. (2011). Oracle Inequalities in Empirical Risk Minimization and Sparse Recovery Problems: Ecole d’Eté de Probabilités de Saint-Flour XXXVIII-2008, volume 2033. Springer Science & Business Media.

- Koltchinskii and Panchenko, (2000) Koltchinskii, V. and Panchenko, D. (2000). Rademacher processes and bounding the risk of function learning. In High dimensional probability II, pages 443–457. Springer.

- Kontorovich, (2014) Kontorovich, A. (2014). Concentration in unbounded metric spaces and algorithmic stability. In International Conference on Machine Learning, pages 28–36.

- Kuznetsov and Mohri, (2017) Kuznetsov, V. and Mohri, M. (2017). Generalization bounds for non-stationary mixing processes. Machine Learning, 106(1):93–117.

- Lei et al., (2015) Lei, Y., Dogan, U., Binder, A., and Kloft, M. (2015). Multi-class svms: From tighter data-dependent generalization bounds to novel algorithms. Advances in Neural Information Processing Systems, 28:2035–2043.

- Lei et al., (2019) Lei, Y., Dogan, Ü., Zhou, D.-X., and Kloft, M. (2019). Data-dependent generalization bounds for multi-class classification. IEEE Transactions on Information Theory, 65(5):2995–3021.

- Li and Barber, (2019) Li, A. and Barber, R. F. (2019). Multiple testing with the structure-adaptive benjamini–hochberg algorithm. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 81(1):45–74.

- Massart, (2000) Massart, P. (2000). Some applications of concentration inequalities to statistics. Annales de la Faculté des sciences de Toulouse: Mathématiques, 9(2):245–303.

- McDiarmid, (1989) McDiarmid, C. (1989). On the method of bounded differences. Surveys in combinatorics, 141(1):148–188.

- Mendelson, (2002) Mendelson, S. (2002). Improving the sample complexity using global data. IEEE transactions on Information Theory, 48(7):1977–1991.

- Mendelson, (2014) Mendelson, S. (2014). Learning without concentration. In Conference on Learning Theory, pages 25–39.

- Mitzenmacher and Upfal, (2017) Mitzenmacher, M. and Upfal, E. (2017). Probability and computing: Randomization and probabilistic techniques in algorithms and data analysis. Cambridge university press.

- Mohri et al., (2018) Mohri, M., Rostamizadeh, A., and Talwalkar, A. (2018). Foundations of machine learning. MIT press.

- Musayeva et al., (2019) Musayeva, K., Lauer, F., and Guermeur, Y. (2019). Rademacher complexity and generalization performance of multi-category margin classifiers. Neurocomputing, 342:6–15.

- Oneto et al., (2013) Oneto, L., Ghio, A., Anguita, D., and Ridella, S. (2013). An improved analysis of the Rademacher data-dependent bound using its self bounding property. Neural Networks, 44:107–111.

- Oneto et al., (2015) Oneto, L., Ghio, A., Ridella, S., and Anguita, D. (2015). Local rademacher complexity: Sharper risk bounds with and without unlabeled samples. Neural Networks, 65:115–125.

- Oneto et al., (2016) Oneto, L., Ghio, A., Ridella, S., and Anguita, D. (2016). Global rademacher complexity bounds: From slow to fast convergence rates. Neural Processing Letters, 43(2):567–602.

- Oneto et al., (2017) Oneto, L., Navarin, N., Donini, M., Ridella, S., Sperduti, A., Aiolli, F., and Anguita, D. (2017). Learning with kernels: a local rademacher complexity-based analysis with application to graph kernels. IEEE transactions on neural networks and learning systems, 29(10):4660–4671.

- Pellegrina et al., (2020) Pellegrina, L., Cousins, C., Vandin, F., and Riondato, M. (2020). Mcrapper: Monte-carlo rademacher averages for poset families and approximate pattern mining. In Proceedings of the 26th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 2165–2174.

- Pellegrina et al., (2019) Pellegrina, L., Riondato, M., and Vandin, F. (2019). SPuManTE: Significant pattern mining with unconditional testing. In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, KDD ’19, pages 1528–1538, New York, NY, USA. ACM.

- Popoviciu, (1935) Popoviciu, T. (1935). Sur les équations algébriques ayant toutes leurs racines réelles. Mathematica, 9:129–145.

- Riondato and Upfal, (2015) Riondato, M. and Upfal, E. (2015). Mining frequent itemsets through progressive sampling with Rademacher averages. In Proceedings of the 21st ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, KDD ’15, pages 1005–1014. ACM.

- Riondato and Upfal, (2018) Riondato, M. and Upfal, E. (2018). ABRA: Approximating betweenness centrality in static and dynamic graphs with Rademacher averages. ACM Trans. Knowl. Disc. from Data, 12(5):61.

- Santoro et al., (2020) Santoro, D., Tonon, A., and Vandin, F. (2020). Mining sequential patterns with vc-dimension and rademacher complexity. Algorithms, 13(5):123.

- Shalev-Shwartz and Ben-David, (2014) Shalev-Shwartz, S. and Ben-David, S. (2014). Understanding Machine Learning: From Theory to Algorithms. Cambridge University Press.

- Talagrand, (1994) Talagrand, M. (1994). Sharper bounds for Gaussian and empirical processes. The Annals of Probability, 22(1):28–76.

- Talagrand, (1995) Talagrand, M. (1995). Concentration of measure and isoperimetric inequalities in product spaces. Publications Mathématiques de l’Institut des Hautes Etudes Scientifiques, 81(1):73–205.

- Vapnik, (1998) Vapnik, V. N. (1998). Statistical learning theory. Wiley.

- Vapnik and Chervonenkis, (1971) Vapnik, V. N. and Chervonenkis, A. Y. (1971). On the uniform convergence of relative frequencies of events to their probabilities. Theory of Probability & Its Applications, 16(2):264.

- Yin et al., (2019) Yin, D., Kannan, R., and Bartlett, P. (2019). Rademacher complexity for adversarially robust generalization. In International Conference on Machine Learning, pages 7085–7094. PMLR.

- Yousefi et al., (2018) Yousefi, N., Lei, Y., Kloft, M., Mollaghasemi, M., and Anagnostopoulos, G. C. (2018). Local rademacher complexity-based learning guarantees for multi-task learning. The Journal of Machine Learning Research, 19(1):1385–1431.