Neural Approximate Sufficient Statistics for Implicit Models

Abstract

We consider the fundamental problem of how to automatically construct summary statistics for implicit generative models where the evaluation of the likelihood function is intractable but sampling data from the model is possible. The idea is to frame the task of constructing sufficient statistics as learning mutual information maximizing representations of the data with the help of deep neural networks. The infomax learning procedure does not need to estimate any density or density ratio. We apply our approach to both traditional approximate Bayesian computation and recent neural likelihood methods, boosting their performance on a range of tasks.

1 Introduction

Many data generating processes can be well-described by a parametric statistical model that can be easily simulated forward but does not possess an analytical likelihood function. These models are called implicit generative models (Diggle & Gratton, 1984) or simulator-based models (Lintusaari et al., 2017) and are widely used in science and engineering domains, including physics (Sjöstrand et al., 2008), genetics (Järvenpää et al., 2018), computer graphics (Mansinghka et al., 2013), robotics (Lopez-Guevara et al., 2017), finance (Bansal & Yaron, 2004), cosmology (Weyant et al., 2013), ecology (Wood, 2010) and epidemiology (Chinazzi et al., 2020). For example, the number of infected/healthy people in an outbreak could be well modelled by stochastic differential equations (SDE) simulated by Euler-Maruyama discretization but the likelihood function of a SDE is generally non-analytical. Directly inferring the parameters of these implicit models is often very challenging.

The techniques coined as likelihood-free inference open us a door for performing Bayesian inference in such circumstances. Likelihood-free inference needs to evaluate neither the likelihood function nor its derivatives. Rather, it only requires the ability to sample (i.e. simulate) data from the model. Early approaches in approximate Bayesian computation (ABC) perform likelihood-free inference by repeatedly simulating data from the model, and pick a small subset of the simulated data close to the observed data to build the posterior (Pritchard et al., 1999; Marjoram et al., 2003; Beaumont et al., 2009; Sisson et al., 2007). Recent advances make use of flexible neural density estimators to approximate either the intractable likelihood (Papamakarios et al., 2019) or directly the posterior (Papamakarios & Murray, 2016; Lueckmann et al., 2017; Greenberg et al., 2019).

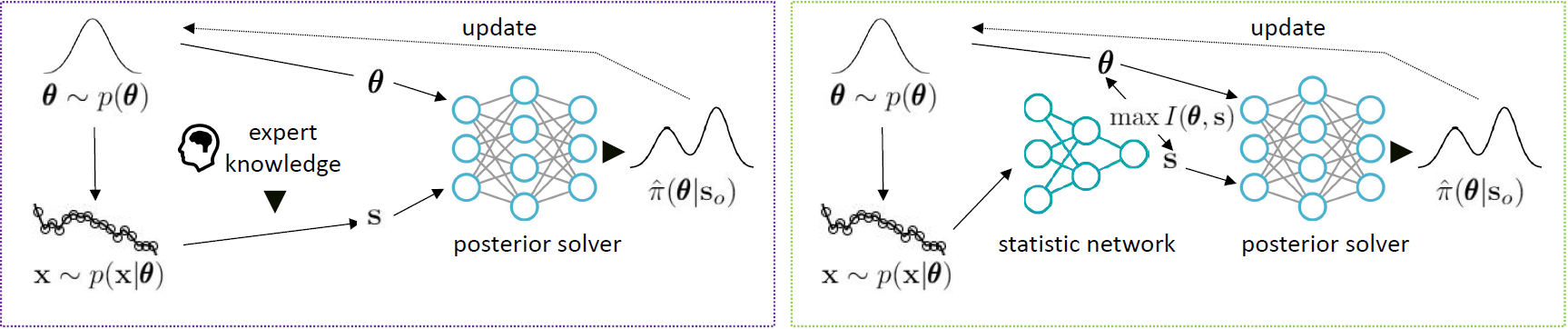

Despite the algorithmic differences, a shared ingredient in likelihood-free inference methods is the choice of summary statistics. Well-chosen summary statistics have been proven crucial for the performance of likelihood-free inference methods (Blum et al., 2013; Fearnhead & Prangle, 2012; Sisson et al., 2018). Unfortunately, in practice it is often difficult to determine low-dimensional and informative summary statistic without domain knowledge from experts. In this work, we propose a novel deep neural network-based approach for automatic construction of summary statistics. Neural networks have been previously applied to learning summary statistics for likelihood-free inference (Jiang et al., 2017; Dinev & Gutmann, 2018; Alsing et al., 2018; Brehmer et al., 2020). Our approach is unique in that our learned statistics directly target global sufficiency. The main idea is to exploit the link between statistical sufficiency and information theory, and to formulate the task of learning sufficient statistic as the task of learning information-maximizing representations of data. We achieve this with distribution-free mutual information estimators or their proxies (Székely et al., 2014; Hjelm et al., 2018). Importantly, our statistics can be learned jointly with the posterior, resulting in fast learning where the two can refine each other iteratively. To sum up, our main contributions are:

-

•

We propose a new neural approach to automatically extract compact, near-sufficient statistics from raw data. The approach removes the need for careful handcrafted design of summary statistics.

-

•

With the proposed statistics, we develop two new likelihood-free inference methods namely SMC-ABC+ and SNL+. Experiments on tasks with various types of data demonstrate their effectiveness.

2 Background

Likelihood-free inference. LFI considers the task of Bayesian inference when the likelihood function of the model is intractable but simulating (sampling) data from the model is possible:

| (1) |

where is the observed data, is the prior over the model parameters , is the (possibly) non-analytical likelihood function and is the posterior over . We assume that, while we do not have access to the exact likelihood, we can still sample (simulate) data from the model with a simulator: . The task is then to infer given and the sampled data: where . Note that is not necessarily the prior .

Curse of dimensionality. Different likelihood-free inference algorithms might learn in different ways, nevertheless most existing methods suffer from the curse of dimensionality. For example, traditional ABC methods use a small subset of closest to under some metric to build the posterior (Pritchard et al., 1999; Marjoram et al., 2003; Beaumont et al., 2009; Sisson et al., 2007), however in high-dimensional space measuring the distance sensibly is notoriously hard (Sorzano et al., 2014; Xie et al., 2017). On the other hand, recent advances (Papamakarios et al., 2019; Lueckmann et al., 2017; Papamakarios & Murray, 2016; Greenberg et al., 2019) utilize neural density estimators (NDE) to model the intractable likelihood or the posterior. Unfortunately, modeling high-dimensional distributions with NDE accurately is also known to be very difficult (Rippel & Adams, 2013; Van Oord et al., 2016), especially when the available training data is scarce.

Our interest here is not to design a new inference algorithm, but to find a low-dimensional statistic that is (Bayesian) sufficient:

| (2) |

where is a deterministic function also learned from . We conjecture that the learning of might be an easier task than direct density estimation. The resultant statistic could then be applied to a wide range of likelihood-free inference algorithms as we will elaborate in Section 3.2.

3 Methodology

3.1 Neural sufficient statistics

Our new deep neural network-based approach for automatic construction of near-sufficient statistics is based on the infomax principle, as illustrated by the following proposition (also see Figure 1):

Proposition 1.

Let , , and be a deterministic function. Then is a sufficient statistic for if and only if

where is deterministic mapping and is the mutual information between random variables.

Proof. We defer the complete proof to the appendix. This proposition is a variant of Theorem 8 in (Shamir et al., 2010) with an adaption to the likelihood-free inference scenario. ∎

This important result suggests that we could find the sufficient statistic for a likelihood function by maximizing the mutual information (MI) between and . Moreover, as our interest is in maximizing MI rather than knowing its precise value, we can maximize a non-KL surrogate, which may have an advantage in e.g. estimation accuracy or computational efficiency (Székely et al., 2014; Hjelm et al., 2018; Ozair et al., 2019). To this end, we utilize the following two non-KL estimators:

Jensen-Shannon divergence (JSD) (Hjelm et al., 2018): this non-KL estimator is shown to be more robust than KL-based ones. More specifically, it is defined as:

| (3) |

where is the softplus function. With this estimator, we set up the following objective for learning the sufficient statistics, which simultaneously estimates and maximizes the MI:

| (4) |

where the two deterministic mappings and are parameterized by two neural networks. Note that we have used the law of the unconscious statistician (LOTUS) from equation 3 to equation 4. The mini-batch version of this objective is given in the appendix.

Distance correlation (DC) (Székely et al., 2014): unlike the JSD estimator, this estimator does not need to learn an additional network , and can be learned much faster. It is defined as:

| (5) |

where . Similar to the case of the JSD estimator, we set up the following objective for learning the sufficient statistics:

| (6) |

where the deterministic mapping is parameterized by a neural network. Again LOTUS is used from equation 5 to equation 6. The mini-batch version of this objective is given in the appendix.

A comparison between the accuracy and efficiency of these two MI estimators (as well as other estimators (Belghazi et al., 2018; Ozair et al., 2019)) for infomax statistics learning is in the appendix.

With enough training samples and powerful neural networks, we can obtain near-sufficient statistics with either or , depending on the estimator. The statistic of data is then given by

| (7) |

In the above construction, we have not specified the form of the networks and . For , any prior knowledge about the data could in principle be incorporated into its design. For example, for sequential data we can realize as a transformer (Vaswani et al., 2017), and for exchangeable data we can realize as a exchangeable neural network (Chan et al., 2018). Here we simply adopt a fully-connected architecture for , and leave the problem-specific design of as future work. For , we choose it to be a split architecture where are both MLPs. Therefore we separately learn low-dimensional representations for and before processing them together. This could be seen as that we incorporate the inductive bias into the design of the networks that and should not interact with each other directly, based on their true relationship (for example, consider the likelihood function of exponential family: ).

We are left with the problem of how to select , the dimensionality of the sufficient statistics. The Pitman-Koopman-Darmois theorem (Koopman, 1936) tells us that sufficient statistics with fixed dimensionality only exists for exponential family, so there is no universal way to select . Here, we propose to use the following simple heuristics to determine :

| (8) |

where is the dimensionality of (which typically satisfies ). The rationale behind this heuristics is that the dimensionality of the sufficient statistics in the exponential family is , and exponential family has been proven reasonably accurate for posterior approximation (see e.g. Thomas et al., 2021; Pacchiardi & Dutta, 2020). By doubling the dimensionality of the statistics to we are likely to have a better representative power than the exponential family while still keeping small.

Furthermore, we have the following proposition comparing our method to the existing

posterior-mean-as-statistic approaches (Fearnhead & Prangle, 2012; Jiang et al., 2017).

Proposition 2.

Let and . Let be a deterministic function that satisfies

then is generally not a maximizer of and hence it is not a sufficient statistic.

Proof. We defer the proof to the appendix. ∎

This proposition tells us that unlike our method, the existing (posterior-)mean-as-statistic approaches widely used in likelihood-free inference community lose information about the posterior, and it is only optimal for predicting the posterior mean (Fearnhead & Prangle, 2012; Jiang et al., 2017). When using this statistics in inference, it may yield inaccurate estimates of e.g. the posterior uncertainty. Nonetheless which statistics to use depends on the task, e.g. full posterior vs. point estimation.

3.2 Dynamic statistics-posterior learning

The above neural sufficient statistic could, in principle, be learned via a pilot run before the inference starts, as, for example, done in the work by Drovandi et al. (2011); Fearnhead & Prangle (2012); Jiang et al. (2017). Such a strategy requires extra simulation cost, and the learned statistic is kept fixed during inference. We propose a dynamic learning strategy below to overcome these limitations.

Our idea is to jointly learn the statistic and the posterior in multiple rounds. More concretely, at round , we use the current statistic to build the -th estimate to the posterior: , and at round +1, this estimate is used as the new proposal distribution to simulate data: . We then re-learn and with all the data up to the new round. In this process, and refine each other: a good helps to learn more accurately, whereas an improved as a better proposal in turn helps to learn more efficiently.

The theoretical basis of this multi-rounds strategy is provided by Proposition 1, which tells us that the sufficiency of the learned statistics is insensitive to the choice of , the marginal distribution of in sampled data . This means that we are indeed safe to use any proposal distribution at any round in multi-rounds learning, and in such case after round will be a mixture distribution formed by the proposal distributions of the previous rounds, i.e. .

In practice, any likelihood-free inference algorithm that learns the posterior sequentially naturally fits well within the above joint statistic-posterior learning strategy. Here we study two such instances:

Sequential Monte Carlo ABC (SMC-ABC) (Beaumont et al., 2009). This classical algorithm learns the posterior in a non-parametric way within multiple rounds. Here, we consider a variant of it to better make use of the above neural sufficient statistic, and to re-use all previous simulated data. The new SMC-ABC algorithm estimates the posterior at the -th round as follows. We first sort data in according to the distances . We then pick the top- s whose corresponding distances are the smallest. The picked s then follow as below:

| (9) |

where the threshold is implicitly defined by the ratio (which automatically goes to zero as ). We then fit with the collected s by a flexible parametric model (e.g. a Gaussian copula), with which we can obtain the -th estimate to the posterior by importance (re-)weighting:

| (10) |

The whole procedure of this new inference algorithm, SMC-ABC+, is summarized in Algorithm 1.

Sequential Neural Likelihood (SNL) (Papamakarios et al., 2019). This recent algorithm learns the posterior in a parametric way, also in multiple rounds. The original SNL method approximates the likelihood function by a conditional neural density estimator , which could be difficult to learn if the dimensionality of is high. Here, we alleviate such difficulty with our neural statistic. The new SNL algorithm estimates the posterior at the -th round as follows. At round , where we have simulated data , we fit a neural density estimator as:

| (11) |

where is the current statistic network and is a neural density estimator (e.g. Durkan et al. (2019); Papamakarios et al. (2017)). With being moderately large and flexible enough, this would yield us . We then obtain the -th estimate of the posterior by Bayes rule:

| (12) |

The whole procedure of this new SNL algorithm, denoted as SNL+, is summarized in Algorithm 2.

4 Related Works

Approximate Bayesian computation. ABC denotes techniques for likelihood-free inference which work by repeatedly simulating data from the model and picking those similar to the observed data to estimate the posterior (Sisson et al., 2018). Naive ABC performs simulation with the prior, whereas MCMC-ABC (Marjoram et al., 2003; Meeds et al., 2015) and SMC-ABC (Beaumont et al., 2009; Sisson et al., 2007) use informed proposals, and more advanced methods employ experimental design or active learning to accelerate the inference (Gutmann & Corander, 2016; Järvenpää et al., 2019). To measure the similarity to the observed data, it is often wise to use low-dimensional summary statistics rather than the raw data. Here we develop a way to learn compact sufficient statistics for ABC.

Neural density estimator-based inference. Apart from ABC, a recent line of research uses a conditional neural density estimator to (sequentially) learn the intractable likelihood (e.g SNL Papamakarios et al. (2019); Lueckmann et al. (2019)) or directly the posterior (e.g SNPE Papamakarios & Murray (2016); Lueckmann et al. (2017); Greenberg et al. (2019)). Likelihood-targeting approaches have the advantage that they could readily make use of any proposal distribution in sequential learning, but they rely on low-dimensional, well-chosen summary statistic. Posterior-targeting methods on the contrary need no design of summary statistic, but they require non-trivial efforts to facilitate sequential learning. Our approach (e.g SNL+) can be seen as taking the advantages from both worlds.

Automatic construction of summary statistics. A set of works have been proposed to automatically construct low-dimensional summary statistics. Two lines of them are most related to our approach. The first line (Fearnhead & Prangle, 2012; Jiang et al., 2017; Chan et al., 2018; Wiqvist et al., 2019; Dinev & Gutmann, 2018) train a neural network to predict the posterior mean and use this prediction as the summary statistic. These mean-as-statistic approaches, as analyzed previously in Proposition 2, indeed do not guarantee sufficiency. Rather than taking the predicted mean, the works (Alsing et al., 2018; Brehmer et al., 2020) take the score function around some fiducial parameter as the summary statistic. However, these score-as-statistic methods are only locally sufficient around . Our approach differs from all these methods as it is globally sufficient for all .

MI and ratio estimation. It has been shown in the literature that many variational MI estimators also estimate the ratio up to a constant (Nowozin et al., 2016; Nguyen et al., 2010). Therefore our MI-based statistic learning method is closely related to ratio estimating approaches to posterior inference (Hermans et al., 2020; Thomas et al., 2021). The differences are 1) we decouple the task of statistics learning from the task of density estimation for LFI, which grants us the privilege to use any infomax representation learning methods that are ratio-free (Székely et al., 2014; Ozair et al., 2019); and 2) even if we do estimate the ratio, we do this in the low-dimensional space based on a sufficient statistics perspective, which is typically easier than in the original space.

5 Experiments

5.1 Setup

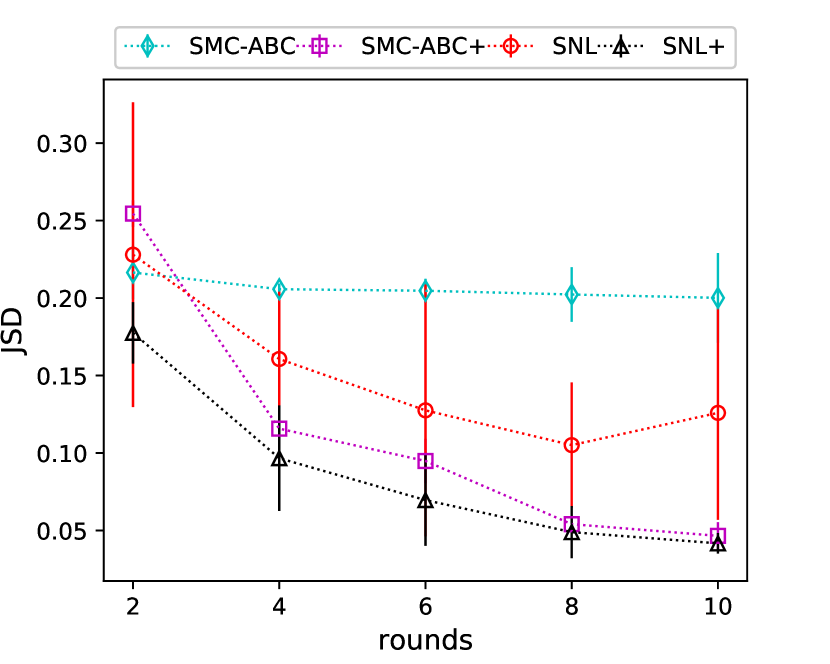

Baselines. We apply the proposed statistics to two aforementioned likelihood-free inference methods: (i) SMC-ABC (Beaumont et al., 2009) and (ii) SNL (Papamakarios et al., 2019). We compare the performance of the algorithms augmented with our neural statistics (dubbed as SMC-ABC+ and SNL+) to their original versions as well as the versions based on expert-designed statistics (details presented later; we call the corresponding methods SMC-ABC’ and SNL’). We also compare to the sequential neural posterior estimate (SNPE) method111More specifically, the version B. We compare with SNPE-B (Lueckmann et al., 2017) rather than the more recent SNPE-C (Greenberg et al., 2019) due to its similarity to SRE shown in (Durkan et al., 2020). which needs no statistic design, as well as the sequential ratio estimate (SRE) method (Hermans et al., 2020) which is closely related to our MI-based method222For fair comparison, we control that the neural network in SRE has a similar number of parameters/same optimizer settings as in our method. See the appendix for more details about the settings of the neural networks.. All methods are run for 10 rounds with 1,000 simulations each. The results presented below are for the JSD estimator; the DC estimator achieves similar accuracy (see appendix).

Evaluation metric. To assess the quality of the estimated posterior, we compare the Jensen-Shannon divergence (JSD) between the approximate posterior and the true posterior for each method (see appendix). For the problems we consider, the true posterior is either analytically available, or can be accurately approximated by a standard rejection ABC algorithm (Pritchard et al., 1999) with known low-dimensional sufficient statistic (e.g ) and extensive simulations (e.g ).

| SMC’ | SMC+ | SNL’ | SNL+ | SRE | SNPE |

|---|---|---|---|---|---|

5.2 Results

We demonstrate the effectiveness of our method on three models: (a) an Ising model; (b) a Gaussian copula model; (c) an Ornstein-Uhlenbeck process. The Ising model does not have an analytical likelihood but the posterior can be approximated accurately by rejection ABC due to the existence of low-dimensional, discrete sufficient statistic. The last two models have analytical likelihoods and hence analytical posteriors. These models cover the cases of graph data, i.i.d data and sequence data.333We chose to conduct experiments on these models rather than common tasks like M/G/1 and Lotka-Volterra since they lack a known true likelihood, making it hard to verify the sufficiency of the proposed statistics. How to evaluate LFI methods on models without known likelihood is still an open problem (Lueckmann et al., 2021).

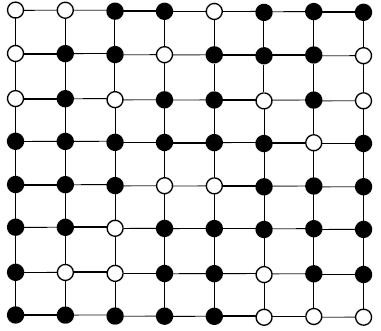

Ising model. The first model we consider is a mathematical model in statistical physics that describes the states of atomic spins on a lattice (see Figure 1(a)). Each spin has two states described by a discrete random variable , and is only allowed to interact with its neighbour. Given parameters , the probability density function of the Ising model is:

where denotes that spin and spin are neighbours. is also called the Hamiltonian of the model. The likelihood function of this model is not analytical due to the intractable normalizing constant . However, sampling from the model by MCMC is possible. Note that the sufficient statistics are known for this model: . The true posterior can easily be approximated by rejection ABC with the low-dimensional sufficient statistics and extensive simulations. Here, we assume that is known, and the task is to infer the posterior of under an uniform prior (in this case the sufficient statistic becomes only 1D: ). The true parameters are .

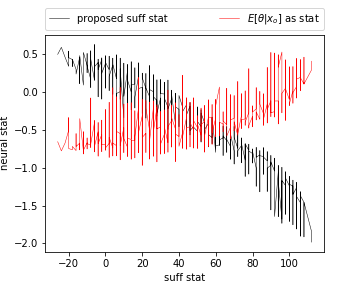

In Figure 1(c), we investigate whether the proposed statistic could achieve sufficiency. Ideally, if the learned statistic in our method does recover the true sufficient statistic well, the relationship between and should be nearly monotonic (note that both and are here 1D). To verify this, we plot the relationship between and . We see from the figure that learned by our method does, approximately, increase monotonically with , suggesting that recovers reasonably well. In comparison, the statistics learned with the widely-used posterior-mean-as-statistics approach only weakly depends on the true sufficient statistic; it is nearly indistinguishable for different . In other words, it loses sufficiency. The result empirically verifies our theoretical result in Proposition 2.

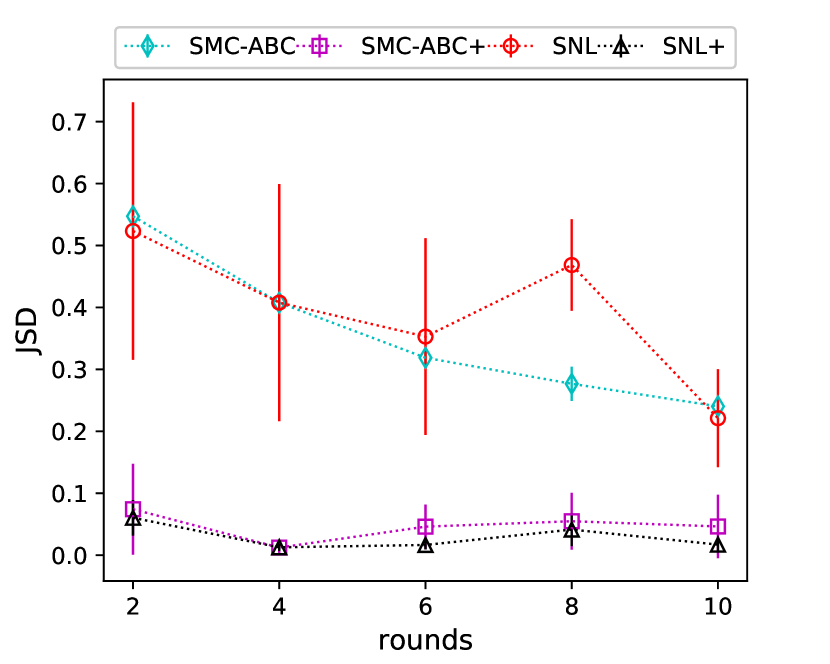

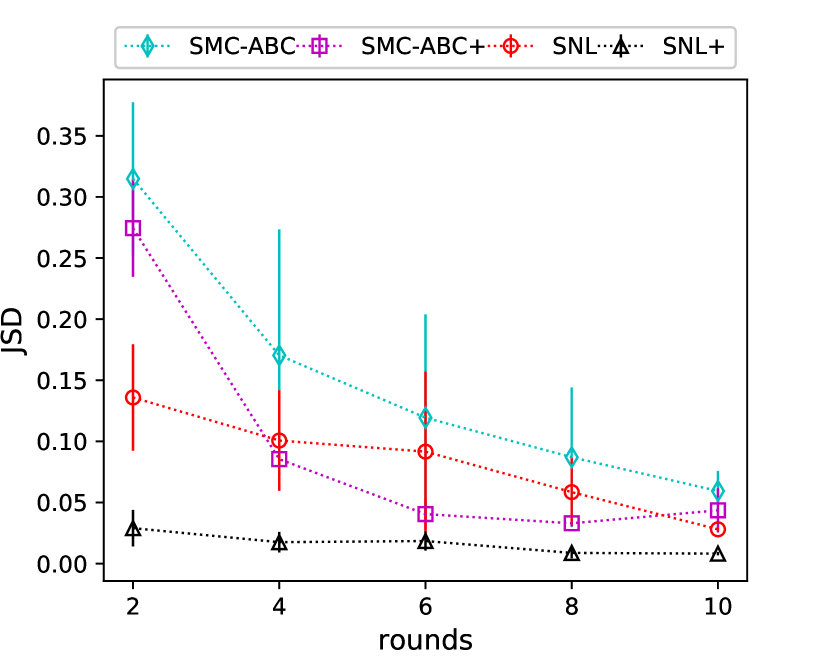

Figure 1(b) further shows the JSD between the true and learned posterior for different methods across the rounds (the vertical lines indicates standard derivation, each JSD is obtained by calculating the average of 5 independent runs. The results shown in the below experiments have the same setup). It can be seen from the figure that for this model, likelihood-free inference methods augmented with the proposed statistic (SMC-ABC+, SNL+) outperform their original counterparts (SMC-ABC, SNL) by a large margin. In Table 1, we further compare our statistics with the expert designed statistics, from which one can see their close performance (here the expert statistics is taken as the true sufficient statistics ). We further see that our method also outperforms SRE which directly estimates the ratio in high-dimensional space (note that the true likelihood is of the form ) as well as SNPE (version B). The reason why SNPE(-B) does not perform more satisfactorily might be that it relies on importance weights to facilitate sequential learning, which can induce high variance that makes the training unstable.

|

|

|

| Truth | SMC | SMC+ |

|

|

|

| SNL | SNL+ |

| SMC’ | SMC+ | SNL’ | SNL+ | SRE | SNPE |

|---|---|---|---|---|---|

Gaussian copula. The second model we consider is a 2D Gaussian copula model (Chen & Gutmann, 2019). Data for this model can be generated with aid of a latent variable as follows:

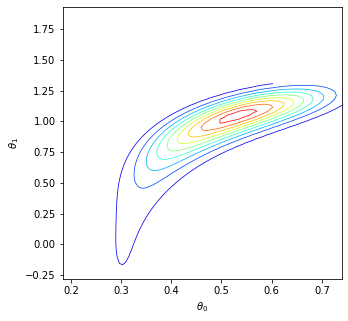

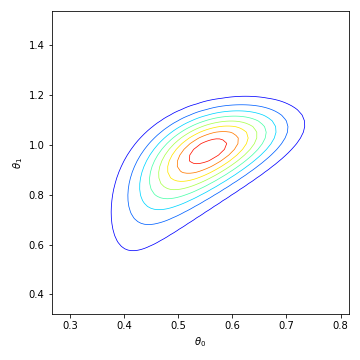

where , , are the cumulative distribution function (CDF) of the standard normal distribution, the CDF of and the CDF of respectively. We assume that a total number of 200 samples are i.i.d drawn from this model, yielding a population that serves as our observed data. Note that the likelihood of this model can be computed analytically by the law of variable transformation. To perform inference, we compute a rudimentary statistic to describe , namely (a) the 20-equally spaced quantiles of the marginal distributions of and (b) the correlation between the latent variables in , resulting in a statistic of dimensionality 41. A uniform prior is used: and .

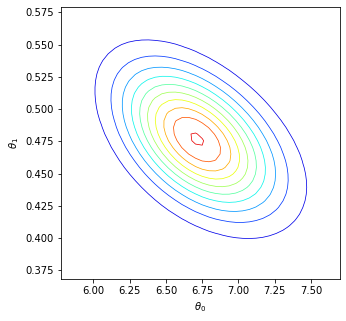

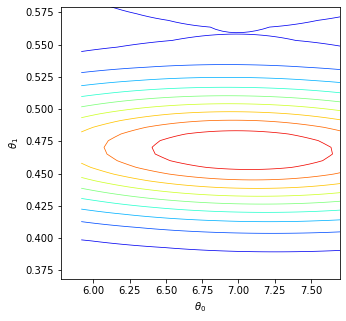

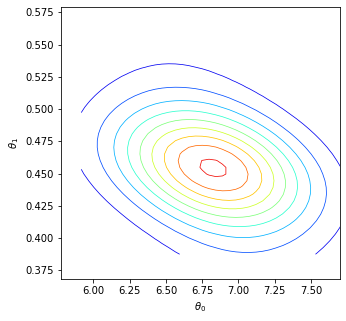

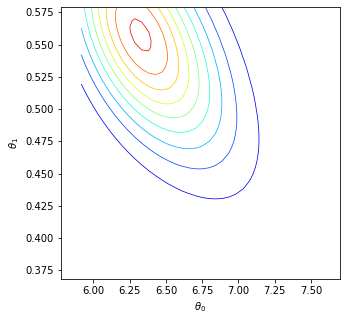

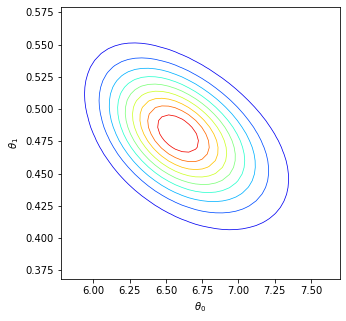

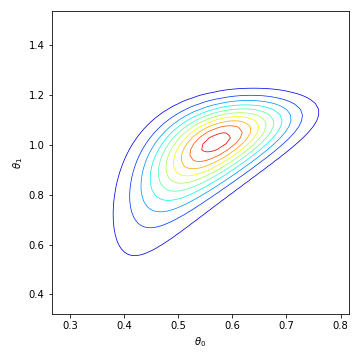

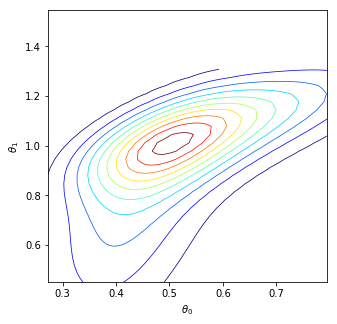

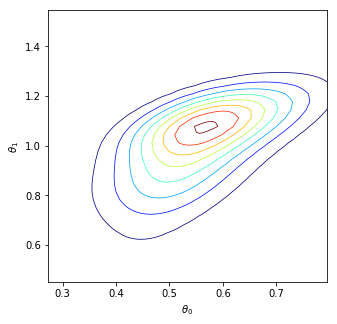

In Figure 2(b), we demonstrate the power of our neural sufficient statistic learning method on the Gaussian copula problem. Overall, we see that the proposed method improves the accuracy of existing likelihood-free inference methods, as well as their robustness, see e.g. the reduced variability for SNL+ (the high variability in SNL may be due to the lack of training data required to learn the 41-dimensional likelihood function well). This is also confirmed by the contours plots in Figure 2(c). In Table 2 we further compare the proposed statistic with the expert-designed low-dimension statistic (here the expert statistic is taken to be the -equally spaced marginal quantiles and the correlations between ), from which we see that our proposed statistic achieves a better performance. For this model, the average performance of our method is slightly worse than that of SNPE. However, SNPE has a higher variability, so that the difference in performance is actually not significant.

|

|

|

| Truth | SMC | SMC+ |

|

|

|

| SNL | SNL+ |

| SMC’ | SMC+ | SNL’ | SNL+ | SRE | SNPE |

|---|---|---|---|---|---|

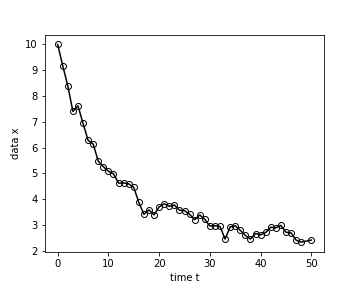

Ornstein-Uhlenbeck process. The last model we consider is a stochastic differential equation (SDE). Data in this model is sequentially generated as:

where , and . This SDE can be simulated by the Euler-Maruyama method, and has an analytical likelihood. It has a wide application in financial mathematics and the physical sciences. Here, the parameters of interest are , and a uniform prior is placed on them: . The true parameters are set to be .

Figure 3(b) compares the JSD of each method against the simulation cost. Again, we find that the proposed neural sufficient statistics greatly improve the performance of both SMC-ABC and SNL. In Table 3, we compare our statistics to expert statistics (here the expert statistics are taken as the mean, standard error and autocorrelation with lag 1, 2, 3 of the time series). It can be seen that our statistics perform comparably to the expert statistics. Our method also seems to outperform SRE and SNPE.

6 Conclusion

We proposed a new deep learning-based approach for automatically constructing low-dimensional sufficient statistics for likelihood-free inference. The obtained neural approximate sufficient statistics can be applied to both traditional ABC-based and recent NDE-based methods. Our main hypothesis is that learning such sufficient statistics via the infomax principle might be easier than estimating the density itself. We verify this hypothesis by experiments on various tasks with graphs, i.i.d and sequence data. Our method establishes a link between representation learning and likelihood-free inference communities. For future works, we can consider further infomax representation learning approaches, as well as more principle ways to determine the dimensionality of the sufficient statistics.

References

- Alsing et al. (2018) Justin Alsing, Benjamin Wandelt, and Stephen Feeney. Massive optimal data compression and density estimation for scalable, likelihood-free inference in cosmology. Monthly Notices of the Royal Astronomical Society, 477(3):2874–2885, 2018.

- Bansal & Yaron (2004) Ravi Bansal and Amir Yaron. Risks for the long run: A potential resolution of asset pricing puzzles. The journal of Finance, 59(4):1481–1509, 2004.

- Beaumont et al. (2009) Mark A Beaumont, Jean-Marie Cornuet, Jean-Michel Marin, and Christian P Robert. Adaptive approximate Bayesian computation. Biometrika, 96(4):983–990, 2009.

- Belghazi et al. (2018) Mohamed Ishmael Belghazi, Aristide Baratin, Sai Rajeshwar, Sherjil Ozair, Yoshua Bengio, Aaron Courville, and Devon Hjelm. Mutual information neural estimation. In International Conference on Machine Learning, pp. 531–540. PMLR, 2018.

- Blum et al. (2013) Michael GB Blum, Maria Antonieta Nunes, Dennis Prangle, Scott A Sisson, et al. A comparative review of dimension reduction methods in approximate bayesian computation. Statistical Science, 28(2):189–208, 2013.

- Brehmer et al. (2020) Johann Brehmer, Gilles Louppe, Juan Pavez, and Kyle Cranmer. Mining gold from implicit models to improve likelihood-free inference. Proceedings of the National Academy of Sciences, 117(10):5242–5249, 2020.

- Chan et al. (2018) Jeffrey Chan, Valerio Perrone, Jeffrey Spence, Paul Jenkins, Sara Mathieson, and Yun Song. A likelihood-free inference framework for population genetic data using exchangeable neural networks. In Advances in Neural Information Processing Systems, pp. 8594–8605, 2018.

- Chen & Gutmann (2019) Yanzhi Chen and Michael U Gutmann. Adaptive gaussian copula abc. In The 22nd International Conference on Artificial Intelligence and Statistics, pp. 1584–1592. PMLR, 2019.

- Chinazzi et al. (2020) Matteo Chinazzi, Jessica T Davis, Marco Ajelli, Corrado Gioannini, Maria Litvinova, Stefano Merler, Ana Pastore y Piontti, Kunpeng Mu, Luca Rossi, Kaiyuan Sun, et al. The effect of travel restrictions on the spread of the 2019 novel coronavirus (covid-19) outbreak. Science, 368(6489):395–400, 2020.

- Cover et al. (2003) Tm Cover, Ja Thomas, and J Wiley. Elements of information theory. Tsinghua University Pres, 2003.

- Diggle & Gratton (1984) Peter J Diggle and Richard J Gratton. Monte Carlo methods of inference for implicit statistical models. Journal of the Royal Statistical Society. Series B, pp. 193–227, 1984.

- Dinev & Gutmann (2018) Traiko Dinev and Michael U Gutmann. Dynamic likelihood-free inference via ratio estimation (dire). arXiv preprint arXiv:1810.09899, 2018.

- Drovandi et al. (2011) Christopher C Drovandi, Anthony N Pettitt, and Malcolm J Faddy. Approximate Bayesian computation using indirect inference. Journal of the Royal Statistical Society: Series C (Applied Statistics), 60(3):317–337, 2011.

- Durkan et al. (2019) Conor Durkan, Artur Bekasov, Iain Murray, and George Papamakarios. Neural spline flows. arXiv preprint arXiv:1906.04032, 2019.

- Durkan et al. (2020) Conor Durkan, Iain Murray, and George Papamakarios. On contrastive learning for likelihood-free inference. arXiv preprint arXiv:2002.03712, 2020.

- Fearnhead & Prangle (2012) Paul Fearnhead and Dennis Prangle. Constructing summary statistics for approximate Bayesian computation: semi-automatic approximate Bayesian computation. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 74(3):419–474, 2012.

- Greenberg et al. (2019) David Greenberg, Marcel Nonnenmacher, and Jakob Macke. Automatic posterior transformation for likelihood-free inference. In International Conference on Machine Learning, pp. 2404–2414, 2019.

- Gutmann & Corander (2016) Michael Gutmann and Jukka Corander. Bayesian optimization for likelihood-free inference of simulator-based statistical models. Journal of Machine Learning Research, 17(1):4256–4302, 2016.

- Hermans et al. (2020) Joeri Hermans, Volodimir Begy, and Gilles Louppe. Likelihood-free mcmc with amortized approximate ratio estimators. In International Conference on Machine Learning, pp. 4239–4248. PMLR, 2020.

- Hjelm et al. (2018) R Devon Hjelm, Alex Fedorov, Samuel Lavoie-Marchildon, Karan Grewal, Phil Bachman, Adam Trischler, and Yoshua Bengio. Learning deep representations by mutual information estimation and maximization. In International Conference on Learning Representations, 2018.

- Järvenpää et al. (2018) M. Järvenpää, M.U. Gutmann, A. Vehtari, and P. Marttinen. Gaussian process modeling in approximate Bayesian computation to estimate horizontal gene transfer in bacteria. Annals of Applied Statistics, 2018.

- Järvenpää et al. (2019) M. Järvenpää, M.U. Gutmann, A. Vehtari, and P. Marttinen. Efficient acquisition rules for model-based approximate Bayesian computation. Bayesian Analysis, 14(2):595–622, 2019. doi: doi:10.1214/18-BA1121.

- Jiang et al. (2017) Bai Jiang, Tung-yu Wu, Charles Zheng, and Wing H Wong. Learning summary statistic for approximate bayesian computation via deep neural network. Statistica Sinica, pp. 1595–1618, 2017.

- Kingma & Ba (2014) Diederik P Kingma and Jimmy Ba. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980, 2014.

- Koopman (1936) Bernard Osgood Koopman. On distributions admitting a sufficient statistic. Transactions of the American Mathematical society, 39(3):399–409, 1936.

- Lintusaari et al. (2017) J. Lintusaari, M.U. Gutmann, R. Dutta, S. Kaski, and J. Corander. Fundamentals and recent developments in approximate Bayesian computation. Systematic Biology, 66(1):e66–e82, January 2017.

- Lopez-Guevara et al. (2017) T. Lopez-Guevara, N.K. Taylor, M.U. Gutmann, S. Ramamoorthy, and K. Subr. Adaptable pouring: Teaching robots not to spill using fast but approximate fluid simulation. In Sergey Levine, Vincent Vanhoucke, and Ken Goldberg (eds.), Proceedings of the 1st Annual Conference on Robot Learning (CoRL), volume 78 of Proceedings of Machine Learning Research, pp. 77–86, November 2017.

- Lueckmann et al. (2017) Jan-Matthis Lueckmann, Pedro J Goncalves, Giacomo Bassetto, Kaan Öcal, Marcel Nonnenmacher, and Jakob H Macke. Flexible statistical inference for mechanistic models of neural dynamics. In Advances in Neural Information Processing Systems, pp. 1289–1299, 2017.

- Lueckmann et al. (2019) Jan-Matthis Lueckmann, Giacomo Bassetto, Theofanis Karaletsos, and Jakob H Macke. Likelihood-free inference with emulator networks. In Symposium on Advances in Approximate Bayesian Inference, pp. 32–53, 2019.

- Lueckmann et al. (2021) Jan-Matthis Lueckmann, Jan Boelts, David S Greenberg, Pedro J Gonçalves, and Jakob H Macke. Benchmarking simulation-based inference. arXiv preprint arXiv:2101.04653, 2021.

- Mansinghka et al. (2013) Vikash K Mansinghka, Tejas D Kulkarni, Yura N Perov, and Josh Tenenbaum. Approximate bayesian image interpretation using generative probabilistic graphics programs. In Advances in Neural Information Processing Systems, pp. 1520–1528, 2013.

- Marjoram et al. (2003) Paul Marjoram, John Molitor, Vincent Plagnol, and Simon Tavaré. Markov chain Monte Carlo without likelihoods. Proceedings of the National Academy of Sciences, 100(26):15324–15328, 2003.

- Meeds et al. (2015) Edward Meeds, Robert Leenders, and Max Welling. Hamiltonian abc. In Proceedings of the Thirty-First Conference on Uncertainty in Artificial Intelligence, pp. 582–591, 2015.

- Nguyen et al. (2010) XuanLong Nguyen, Martin J Wainwright, and Michael I Jordan. Estimating divergence functionals and the likelihood ratio by convex risk minimization. IEEE Transactions on Information Theory, 56(11):5847–5861, 2010.

- Nowozin et al. (2016) Sebastian Nowozin, Botond Cseke, and Ryota Tomioka. f-gan: Training generative neural samplers using variational divergence minimization. In Advances in neural information processing systems, pp. 271–279, 2016.

- Ozair et al. (2019) Sherjil Ozair, Corey Lynch, Yoshua Bengio, Aaron Van den Oord, Sergey Levine, and Pierre Sermanet. Wasserstein dependency measure for representation learning. In Advances in Neural Information Processing Systems, pp. 15604–15614, 2019.

- Pacchiardi & Dutta (2020) Lorenzo Pacchiardi and Ritabrata Dutta. Score matched conditional exponential families for likelihood-free inference. arXiv preprint arXiv:2012.10903, 2020.

- Papamakarios & Murray (2016) George Papamakarios and Iain Murray. Fast -free inference of simulation models with bayesian conditional density estimation. In Advances in Neural Information Processing Systems, pp. 1028–1036, 2016.

- Papamakarios et al. (2017) George Papamakarios, Theo Pavlakou, and Iain Murray. Masked autoregressive flow for density estimation. In Advances in Neural Information Processing Systems, pp. 2338–2347, 2017.

- Papamakarios et al. (2019) George Papamakarios, David Sterratt, and Iain Murray. Sequential neural likelihood: Fast likelihood-free inference with autoregressive flows. In The 22nd International Conference on Artificial Intelligence and Statistics, pp. 837–848. PMLR, 2019.

- Pritchard et al. (1999) Jonathan K Pritchard, Mark T Seielstad, Anna Perez-Lezaun, and Marcus W Feldman. Population growth of human y chromosomes: a study of y chromosome microsatellites. Molecular biology and evolution, 16(12):1791–1798, 1999.

- Rippel & Adams (2013) Oren Rippel and Ryan Prescott Adams. High-dimensional probability estimation with deep density models. arXiv preprint arXiv:1302.5125, 2013.

- Shamir et al. (2010) Ohad Shamir, Sivan Sabato, and Naftali Tishby. Learning and generalization with the information bottleneck. Theoretical Computer Science, 411(29-30):2696–2711, 2010.

- Sisson et al. (2018) S.A. Sisson, Y Fan, and M.A. Beaumont. Handbook of Approximate Bayesian Computation., chapter Overview of Approximate Bayesian Computation. Chapman and Hall/CRC Press, 2018.

- Sisson et al. (2007) Scott A Sisson, Yanan Fan, and Mark M Tanaka. Sequential Monte Carlo without likelihoods. Proceedings of the National Academy of Sciences, 104(6):1760–1765, 2007.

- Sjöstrand et al. (2008) Torbjörn Sjöstrand, Stephen Mrenna, and Peter Skands. A brief introduction to pythia 8.1. Computer Physics Communications, 178(11):852–867, 2008.

- Sorzano et al. (2014) Carlos Oscar Sánchez Sorzano, Javier Vargas, and A Pascual Montano. A survey of dimensionality reduction techniques. arXiv preprint arXiv:1403.2877, 2014.

- Székely et al. (2014) Gábor J Székely, Maria L Rizzo, et al. Partial distance correlation with methods for dissimilarities. Annals of Statistics, 42(6):2382–2412, 2014.

- Thomas et al. (2021) Owen Thomas, Ritabrata Dutta, Jukka Corander, Samuel Kaski, Michael U Gutmann, et al. Likelihood-free inference by ratio estimation. Bayesian Analysis, 2021.

- Van Oord et al. (2016) Aaron Van Oord, Nal Kalchbrenner, and Koray Kavukcuoglu. Pixel recurrent neural networks. In International Conference on Machine Learning, pp. 1747–1756. PMLR, 2016.

- Vaswani et al. (2017) Ashish Vaswani, Noam Shazeer, Niki Parmar, Jakob Uszkoreit, Llion Jones, Aidan N Gomez, Lukasz Kaiser, and Illia Polosukhin. Attention is all you need. arXiv preprint arXiv:1706.03762, 2017.

- Weyant et al. (2013) Anja Weyant, Chad Schafer, and W Michael Wood-Vasey. Likelihood-free cosmological inference with type ia supernovae: approximate Bayesian computation for a complete treatment of uncertainty. The Astrophysical Journal, 764(2), 2013.

- Wiqvist et al. (2019) Samuel Wiqvist, Pierre-Alexandre Mattei, Umberto Picchini, and Jes Frellsen. Partially exchangeable networks and architectures for learning summary statistics in approximate bayesian computation. In International Conference on Machine Learning, pp. 6798–6807, 2019.

- Wood (2010) Simon N Wood. Statistical inference for noisy nonlinear ecological dynamic systems. Nature, 466(7310):1102, 2010.

- Xie et al. (2017) Haozhe Xie, Jie Li, and Hanqing Xue. A survey of dimensionality reduction techniques based on random projection. arXiv preprint arXiv:1706.04371, 2017.

Appendix A Theoretical proofs

A.1 Proof of Proposition 1

Proof. Firstly, assume is a sufficient statistic. By the definition of sufficient statistic we know . Then we have the Markov chain for the data generating process. On the other hand, since and is a deterministic function we have the Markov chain . By data processing inequality we have for the first chain and for the second chain. This implies that i.e is the maximizer of . For the other direction, since , we have . Note that is a Markov chain, from Theorem 2.8.1 of Cover et al. (2003) we can get and is conditionally independent given . This implies is sufficient. ∎

A.2 Proof of Proposition 2

Proof. We can write the objective as . On the other hand we have . By comparing them, we see they are generally not equivalent. Equivalence only holds in special cases (e.g. Gaussians). ∎

Appendix B More Experimental details and results

B.1 Detailed experimental settings

Neural networks settings. For the statistic network in our method (for both JSD and DC estimators), we adopt a -100-100- fully-connected architecture with being the dimensionality of input data and the dimensionality of the statistic. For the network used to extract the representation of , we adopt a -100-100- fully-connected architecture with being the dimensionality of the model parameters . For the critic network, we adopt a -100-1 fully connected architecture. ReLU is adopted as the non-linearity in all networks. For SRE, which is closely related to our method, we use a -144-144-100-1 architecture. This architecture has a similar complexity as our networks. All these neural networks are trained with Adam (Kingma & Ba, 2014) with a learning rate of and a batch size of 200. No weight decay is applied. We take 20% of the data for validation, and stop training if the validation error does not improve after 100 epochs. We take the snapshot with the best validation error as the final result.

For the neural density estimator in SNL/SNPE, which is realized by a Masked Autoregressive Flow (MAF) (Papamakarios et al., 2017), we adopt 5 autoregressive layers, each of which has two hidden layers with 50 tanh units. This is the same settings as in SNL. The MAF is trained with Adam with a learning rate of and a batch size of 500 and a slight weight decay (). Similar to the case of MI networks, we take 20% of the data for validation, and stop training if the validation error does not improve after 100 epochs. The snapshot with the best validation error is taken as the result.

Sampling from the approximate posterior/learnt proposal. For fair comparison, we adopt simple rejection sampling for all LFI methods (ABC, SNL, SNPE, SRE) when sampling from the learnt posterior, so that each LFI method only differs in the way they learn the posterior. No MCMC is used.

Empirical version of objective functions. Recall that in the JSD estimator, the statistic network is trained with the following objective together with the critic network :

the mini-batch approximation to this objective is:

where is the -th random permutation of the indexes and the pair are randomly picked from the data . Here we set and is the batch size.

In the DC estimator, the statistic network is trained by the following objective:

where . The mini-batch approximation to this objective is:

where . Here are the indexes in the mini-batch. is again the batch size.

JSD calculation between true posterior and approximate posterior. The calculation of the Jensen-Shannon divergence between the true posterior and approximate posterior , namely , is done numerically by a Riemann sum over equally spaced grid points with being the dimensionality of . The region of these grid points is defined by the min and max values of 500 samples drawn from . When we only have samples from the true posterior (e.g. the Ising model), we approximate by a mixture of Gaussian with 8 components.

B.2 Additional experimental results

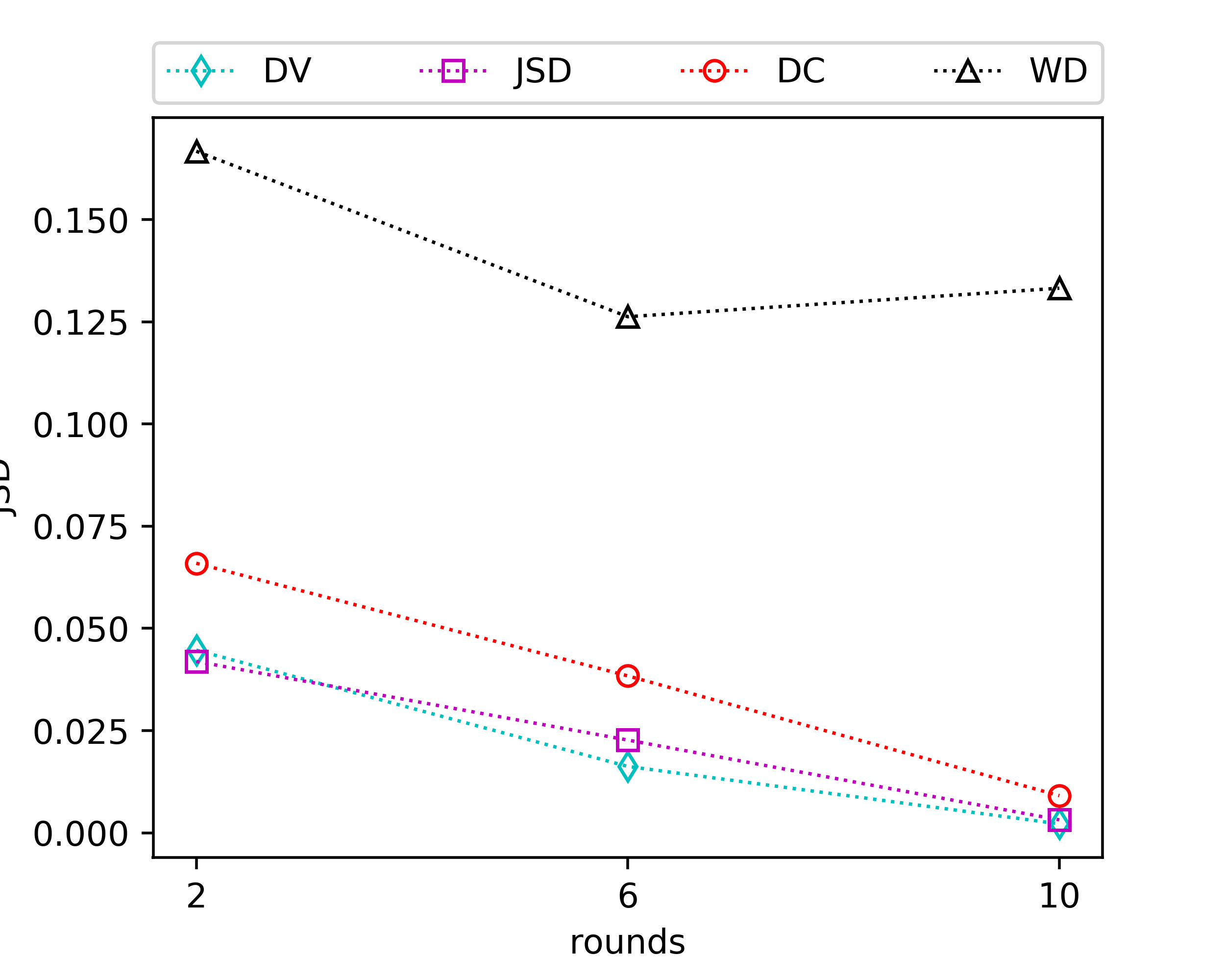

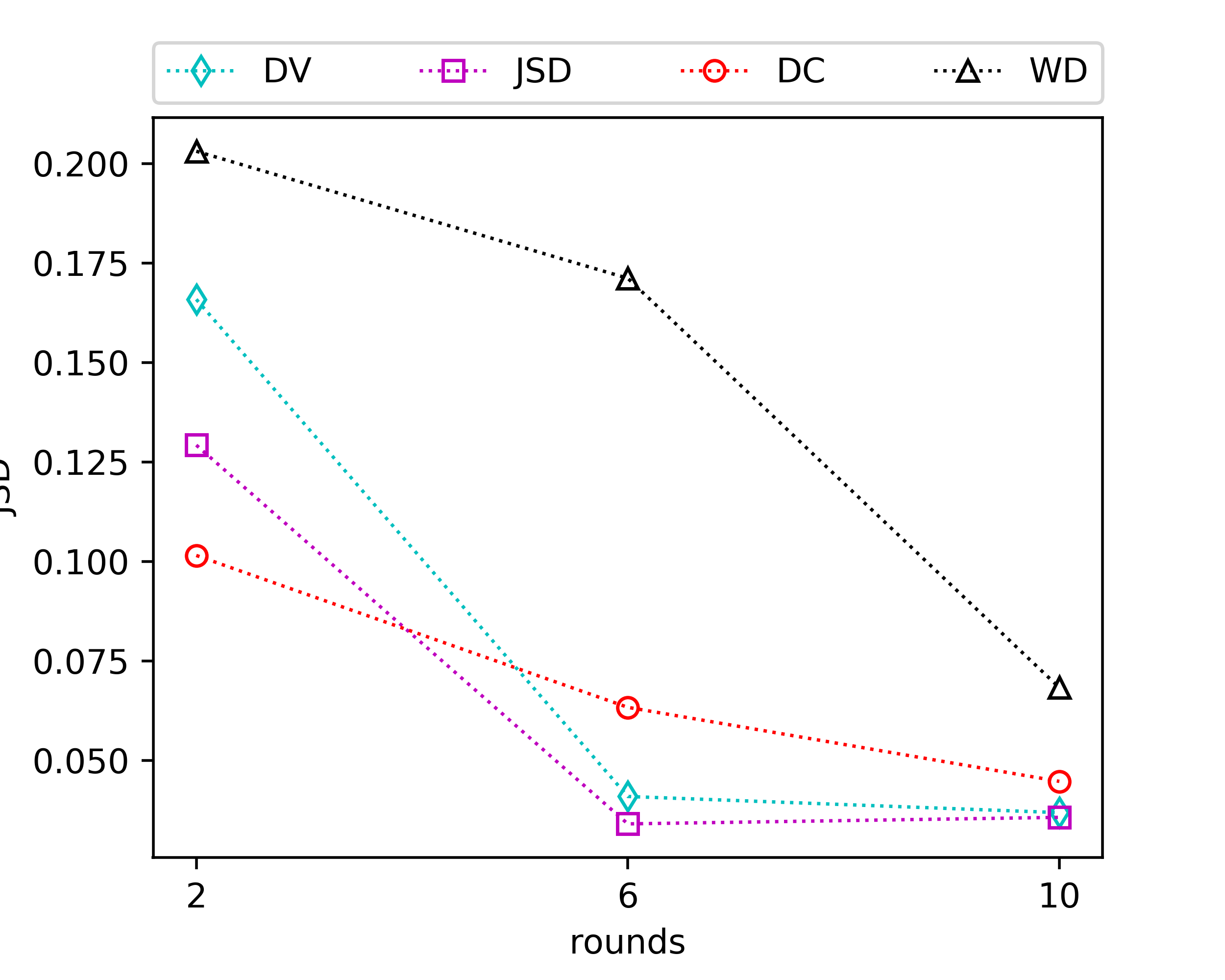

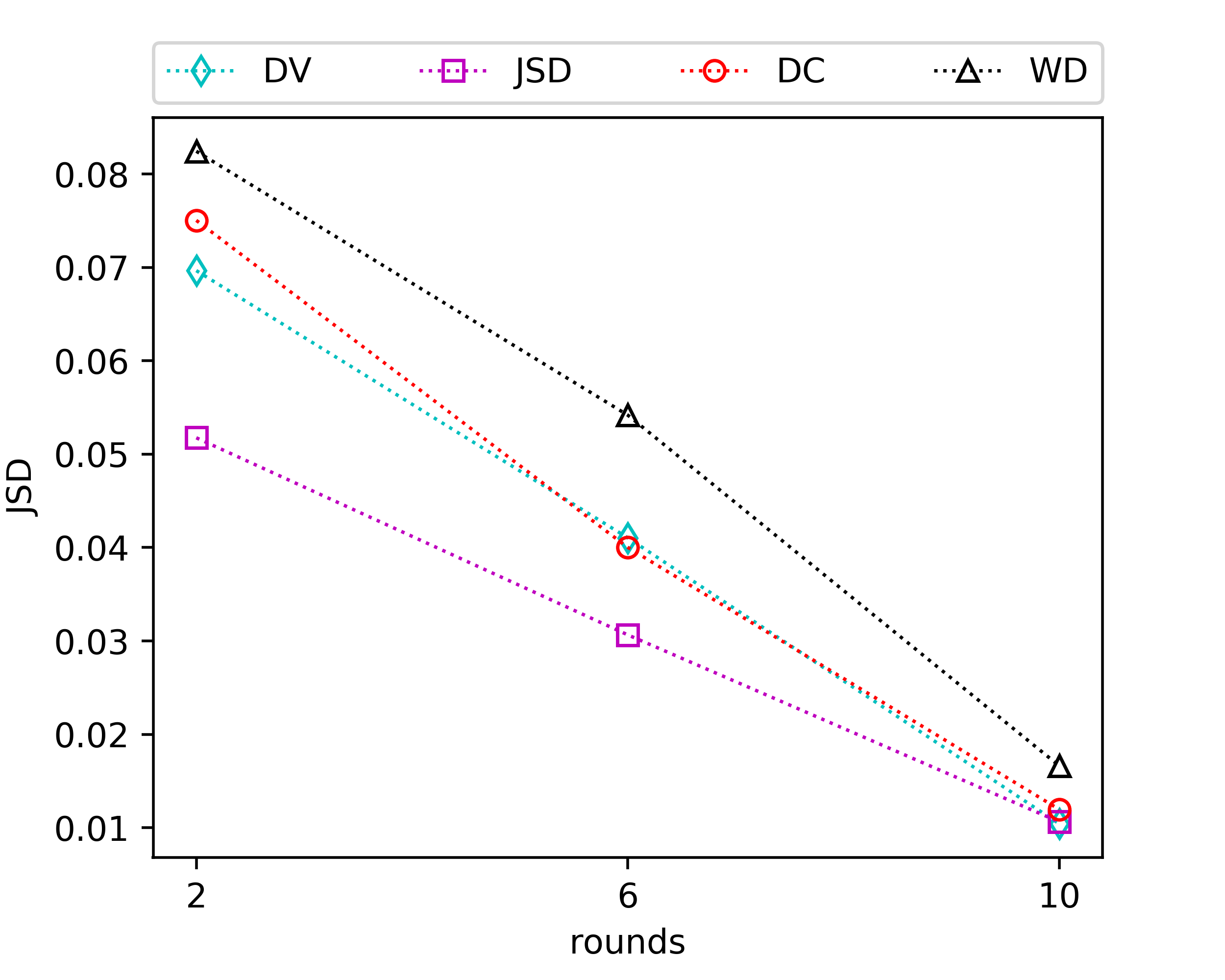

Comparison of different MI estimators. We compare the performances of four MI estimator for infomax statistics learning: Donsker-Varadhan (DV) estimator (Belghazi et al., 2018), Jensen-Shannon divergence (JSD) estimator (Hjelm et al., 2018), distance correlation (DC) Székely et al. (2014) and Wasserstein distance (WD) (Ozair et al., 2019). We highlight that the last two estimators (DC and WD) are ratio-free. We compare the discrepancy between the true posterior and the posterior inferred with the statistics learned by each estimator, as well as the execution time per each mini-batch. The results, which are averaged over 5 independent runs, are shown in the figure and the table below.

From the figure we see that the JSD estimator generally yields the best accuracy among the four estimators. In terms of execution time, the DC estimator is clearly the winner, with its execution time being only 1/15 of the other estimators. However, the accuracy of the DC estimator is still comparable to the JSD estimator, especially when the number of training samples is large (e.g. 10,000). According to these results, we suggest using JSD in small-scale settings (e.g. early rounds in sequential learning), and use DC in large-scale ones (e.g. later rounds in sequential learning).

| Ising model | Gaussian copula | OU process | |||||||||

| DV | JSD | DC | WD | DV | JSD | DC | WD | DV | JSD | DC | WD |

| 115 | 124 | 6 | 230 | 154 | 167 | 10 | 288 | 143 | 158 | 13 | 256 |

Contrastive learning v.s. MLE. In the experiment in the main text, we discover that our method does not always achieve the best performance; it does not work better than SNPE-B on the Gaussian copula problem. Here we would like to investigate why this happens.

Upon a closer look, we discover that SRE, which is closely related to our method when used with the JSD estimator, is outperformed by SNPE-B on the Gaussian copula problem. Remark that both SRE and our method, when used with the JSD estimator, uses contrastive learning rather than MLE. Since both of these two contrastive learning methods do not perform better than the MLE-based SNPE-B, it makes us suspect the reason is due to imperfect contrastive learning. To verify this, we further conduct experiments for SNPE-C, which shares the same loss function with SRE but with a different parameterization to the density ratio (SRE: fully-connected network; SNPE-C: NDE-based parameterization. This NDE is the same as in SNL). The result is as follows:

| Ising model | Gaussian copula | OU process | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| SRE | SNPE-B | SNPE-C | SNL+ | SRE | SNPE-B | SNPE-C | SNL+ | SRE | SNPE-B | SNPE-C | SNL+ |

| 0.083 | 0.058 | 0.030 | 0.017 | 0.052 | 0.037 | 0.047 | 0.042 | 0.022 | 0.018 | 0.016 | 0.009 |

Surprisingly, we find that SNPE-C also perform less satisfactorily than SNPE-B on the Gaussian copula problem. This suggests that contrastive learning might be less preferable than MLE on the Gaussian copula problem, which might also explain the less satisfactory performance of our method.