A data-driven P-spline smoother

and the P-Spline-GARCH models111 Financial support of the European Union’s Horizon 2020 research and innovation program ”FIN- TECH: A Financial supervision and Technology compliance training programme” under the grant agreement No 825215 (Topic: ICT-35-2018, Type of action: CSA), the European Cooperation in Science & Technology COST Action grant CA19130 - Fintech and Artificial Intelligence in Finance - Towards a transparent financial industry, the Deutsche Forschungsgemeinschaft’s IRTG 1792 grant, the Yushan Scholar Program of Taiwan, the Czech Science Foundation’s grant no. 19-28231X / CAS: XDA 23020303, and the DFG project FE 1500/2-1 are greatly acknowledged. Both authors declare that they have no conflict of interest.

Yuanhua Fenga222Corresponding address: Yuanhua Feng, Paderborn University, Warburgerstr. 100, D-33098 Germany.

Email: yuanhua.feng@uni-paderborn.de; Tel. +49 5251 603379 and Wolfgang Karl Härdleb

aDepartment of Economics, Paderborn University

bSchool of Business and Economics, Humboldt University Berlin

Abstract

Penalized spline smoothing of time series and its asymptotic properties are studied. A data-driven algorithm for selecting the smoothing parameter is developed. The proposal is applied to define a semiparametric extension of the well-known Spline-GARCH, called a P-Spline-GARCH, based on the log-data transformation of the squared returns. It is shown that now the errors process is exponentially strong mixing with finite moments of all orders. Asymptotic normality of the P-spline smoother in this context is proved. Practical relevance of the proposal is illustrated by data examples and simulation. The proposal is further applied to value at risk and expected shortfall.

Keywords: P-spline smoother, smoothing parameter selection, P-Spline-GARCH, strong mixing, value at risk, expected shortfall

JEL Codes: C14, C51

A data-driven P-spline smoother

applied to economic and financial time series

1 Introduction

P-spline (penalized spline) regression (Eilers and Marx, 1996) becomes a very popular nonparametric smoothing technique due to its flexibility and computational advantages. The idea of P-splines traces back to O’Sullivan (1986). See also Ruppert et al. (2003). In this paper, P-spline smoothing of time series with a truncated polynomial basis will be investigated. Asymptotic properties of this approach with independent errors are e.g. studied by Wand (1999), Hall and Opsomer (2005), Kauermann (2005), Claeskens et al. (2009) and Xiao (2019). P-spline regression with correlated errors is e.g. discussed in Krivobokova and Kauermann (2007). See also Kauermann et al. (2011). However, asymptotic properties of P-splines under stationary time series errors and data-driven selection of the smoothing parameter in this context are not yet well studied.

We first adapted some asymptotics of Claeskens et al. (2009) and Wand (1999), hereafter CKO09 and WMP99, to P-spline regression under stationary errors. It is shown that this approach is consistent under weak regularity conditions and the asymptotic variance is affected by the correlated errors. But, the estimates still achieve the same optimal rate of convergence as in the i.i.d. case. Furthermore, an approximation of the optimal smoothing parameter is obtained following WMP99 and a self-contained IPI (iterative plug-in, Gasser et al., 1991) algorithm for selecting the smoothing parameter is developed. This algorithm is fully nonparametric, where the unknown variance factor is estimated by a data-driven log-window approach (Bühlmann, 1996). The proposal is compared to a recently proposed data-driven local cubic regression (Feng et al., 2020).

Both data-driven approaches are applied to estimate a smooth scale function in GARCH (generalized autoregressive conditional heteroskedasticity, Engle, 1982; Bolllerslev, 1986) by means of the log-transformation of the squared returns. This idea provides new, automatically non-negative estimates of the scale function in a Semi-GARCH (semiparametric GARCH) model (Feng, 2004). The case with the P-spline estimator is an extension of the Spline-GARCH of Engle and Rangel (2008) (without exogenous variables) and will be called a P-Spline-GARCH. A Semi-GARCH model can be applied to decompose risk measures into a baseline, a conditional and a local component, which helps to improve the estimation quality and forecasting of market risk. For more information on those approaches and their applications, we refer the reader to Amado et al. (2018).

If parametric GARCH models, such as the GARCH, the APARCH (asymmetric power ARCH, Ding et al., 1993) or the EGARCH (exponential GARCH, Nelson, 1991) are fitted to the standardized returns, new variants of the Semi-GARCH, Semi-APARCH and Semi-EGARCH models will be defined. It is shown that the errors in the log-data under those models have finite moments of all orders, are strongly mixing with exponential decay and have exponentially decay autocorrelations as well. Moreover, it is shown that the P-spline smoother obtained from the log-data is asymptotically normal. The practical performance of the proposals is illustrated by different data examples and further confirmed through a simulation study, which show that the error in the estimated volatility of a GARCH model can be clearly reduced by the proposed approaches. For instance, for two selected examples, the mean average absolute error of the estimated volatility obtained by a Semi-GARCH model is just about 35% or 45% of that of a parametric GARCH model, respectively. It is found that the two nonparametric approaches perform quite similarly. The performance of the local cubic regression is slightly better, but the P-spline smoother is more flexible and runs much faster.

Like GARCH models, the Semi-GARCH approaches can be applied to forecast the VaR (value at risk, JPMorgan, 1996) and ES (expected shortfall, Acerbi and Tasche, 2002), a risk measure with superior aggregation properties to VaR. The former is used in the current Basel Accord and is being replaced by the latter in the forthcoming finalization of Basel III (see Basel Committee on Banking Supervision, BCBS, 2016, 2017). Application of the Semi-GARCH models in this context is illustrated by two examples of one-day out-of-sample forecasts of VaR and ES calculated at the - and confidence levels for a period of about one year, as required by the BCBS (2016, 2017). Hence, our proposals provide useful alternatives to parametric GARCH models for forecasting quantitative risk measures. Now, whether Semi-GARCH approaches perform better than parametric GARCH models or not depends on the data under consideration. Detailed discussions on those topics with a comparative study will be carried out elsewhere.

The paper is organized as follows. The P-spline smoother is studied in Section 2. The IPI-algorithm is developed in Section 3. Section 4 studies the application to Semi-GARCH models. The empirical results and simulation study are reported in Sections 5 and 6. Application of Semi-GARCH models to VaR and ES is illustrated in Sections 7. Final remarks in Section 8 conclude. Proofs of the results are put in the appendix.

2 P-spline smoother for time series

We now discuss P-spline smoother in nonparametric regression with time series errors.

2.1 The additive nonparametric time series model

Consider the modeling of a time series , , with a deterministic trend, the commonly used nonparametric regression model in this context is given by

| (1) |

where denotes the rescaled time, is a smooth trend and is a zero mean stationary error process with autocovariances . This paper proposes to estimate in (1) by a P-spline smoother. Our main focus is on the development of a suitable data-driven algorithm for selecting the smoothing parameter under stationary errors without any parametric assumptions on , so that the estimation of is fully nonparametric. This requires the development of a data-driven nonparametric estimation of the variance factor in the proposed approximation of the optimal smoothing parameter, where and denotes the spectral density of . This will be done by adapting the data-driven lag-window estimator of in Bühlmann (1996) to the current context under suitable regularity conditions.

2.2 The proposed P-spline smoother

The commonly used P-splines are those with the B-Spline basis because of its numerical stability and computational efficiency. In the current paper, we will however use P-splines with a truncated polynomial basis for smoothing time series due to the following reasons: 1) Such a proposal is a direct extension of the quadratic splines used in Engle and Rangel (2008) and 2) The useful approximation of the optimal smoothing parameter in WMP99 is obtained for the truncated polynomial basis. This result will be adapted to P-splines with correlated errors. Previous studies on this topic are e.g. Krivobokova and Kauermann (2007) and Kauermann et al. (2011). Asymptotic results for P-spline regression under independent errors are obtained by Hall and Opsomer (2005), CKO09 and Xiao (2019).

In the following equidistant internal knots, , …, together with and , will be used. The -th order P-Spline regression estimator is the minimizer of the following penalized least squares

| (2) |

where are the truncated polynomial splines and is the penalty or smoothing parameter. Define ,

The -th order P-spline estimator of takes the form of a ridge regression given by

| (3) |

which is a linear smoother with a symmetric smoother matrix . One clear difference between local polynomial regression and P-spline smoothing is that the former is carried out at all estimation points while the latter is computed over the intervals determined by the knots, which runs usually much quicker.

In this paper, defined above following WMP99 will be used during the estimation procedure and in particular in the IPI-algorithm to be developed. However, the main part of the asymptotic discussion is based on CKO09. To simplify the representation of those results, the smoothing parameter defined by those authors, i.e. , will be employed in the asymptotic results adapted from their work. The specifications of and are equivalent to each other. But the use of has some numerical advantage. Let . For further discussion we introduce the following regularity conditions.

A1. is at least -times continuously differentiable, i.e. .

A2. is a stationary process with absolutely summable acf .

A3. internal equidistant knots are used, where with

A4. The smoothing parameter is of the order with .

A5. and are chosen so that , where is as defined in (13) of CKO09.

Condition A1 is a standard assumption in nonparametric regression. A2 is a standard assumption in nonparametric regression models with short memory time series errors. The asymptotic results in CKO09 are mainly obtained based on these results for regression splines in Zhou et al. (1998), under Assumptions 1 to 3 stated therein. A3 in this paper is the same as their Assumption 3, but with equidistant knots. Their Assumptions 1 and 2 are automatically fulfilled by the equidistant design considered here. The condition in A4 ensures that the shrinkage bias tends to zero, as . The other requirement is made for simplicity and is unnecessary. The proposed P-spline smoother can even be estimated consistently for some , as . However, such a choice is far from the optimal one and is not suggested. Condition A5 ensures that our discussion is within the large number of knots scenario of CKO09. For the equidistant design we have the following approximation with

| (4) |

The proof of (4) is given in the appendix. This result allows us to check whether A5 is fulfilled in practice or not. For fixed and , is a decreasing function of .

Let denote a generic . Analogously to (17) and (18) in CKO09 on the asymptotic bias and the asymptotic variance of P-spline regression with a truncated polynomial basis and a large number of knots such that , we have

Lemma 1.

Under Assumptions A1 – A5 the P-spline estimator is consistent with the pointwise asymptotic bias and asymptotic variance of the following orders (of magnitude)

| (5) |

| (6) |

where is the length of the interval between two consecutive knots.

The proof of Lemma 1 is omitted, because those results are the same for models with i.i.d. or short memory stationary errors. Lemma 1 shows that the P-spline smoother is consistent under very weak conditions. The optimal smoothing parameters are and , respectively. If and with are used, then under A1, A2 and A5, achieves the so-called optimal rate of convergence given by Stone (1982) for any nonparametric regression estimator of a function . If , the P-spline smoother is still consistent after a slight adjustment of A4. Now, the results reduce to those in (15) and (16) of CKO09 for the scenario with a small . This will not be considered further.

A crucial problem for the practical implementation of the proposed P-spline smoother is the development of a suitable data-driven algorithm for selecting . Results in Lemma 1 are not suitable for this purpose, because the corresponding constants are unknown. Hall and Opsomer (2005) claimed that the result in their (35) might be used to develop a plug-in algorithm for selecting . But they also indicated that their formula is too complex to be attractive for practical use. This idea will hence not be considered here. In this paper we will follow the idea of WMP99 to obtain a rough approximation for and then use it to develop an IPI-algorithm for selecting . Note that the finite sample MASE (mean averaged squared error) of is given by

| (7) |

where stands for the average squared finite sample bias in the MASE and is the finite sample (global) variance part. According to (2) of WMP99, we have

| (8) |

where for a vector . Note that is not affected by the correlated errors. But, the variance of depends on . By means of standard techniques in nonparametric regression with time series errors we obtain the following approximation

| (9) |

This adapts the well-known fact in nonparametric regression with correlated errors to the current case. The proof of (9) is given in the appendix. Two changes comparing to the corresponding result under i.i.d. errors are: 1) Instead of the variance of the errors, is determined by the total sum of all autocovariances of and 2) This result is only an approximation and an exact finite sample formula is now no longer available.

Using the arguments in WMP99 we can obtain the following approximation of

| (10) |

A sketched proof of (10) is given in the appendix. See also Kauermann (2005) for similar results obtained under a linear mixed model. If the errors are uncorrelated, we have and reduces to that given in (4) of WMP99. On the one hand, is an extension of (4) in WMP99. On the other hand, our result can be thought of as a simplification of that given in Section 2.6 of WMP99 based on the complete covariance matrix of . This simplified result is easy to use in practice.

A plug-in algorithm for choosing can be developed based on (10). A great advantage of compared to the asymptotically optimal bandwidth in local polynomial regression is that here only a pilot estimate of itself is required. We will see that is obtained under the further condition , which may not be fulfilled in a practically relevant case. Hence, seems to be a biased approximation of . Nevertheless, WMP99 indicated that this formula is very useful for choosing the smoothing parameter in P-splines under i.i.d. errors. This fact will also be confirmed by the data examples and the simulation in this work. Hence, we propose the use of .

3 The IPI-algorithm for P-splines smoothing

Our proposal consists of an IPI-algorithm for estimating and a main procedure.

3.1 The IPI-algorithm for estimating

Denote the estimate in the -th iteration obtained with the smoothing parameter by . Let be the corresponding residuals. The sample autocovariances of , say, can be calculated. Then the variance factor is estimated through

| (11) |

where is the window-width (of the lag-window estimator) used in the -th iteration and are weights calculated using the Bartlett-window. In this paper we propose to select the optimal using the IPI-algorithm of Bühlmann (1996) with some minor adjustments, which reads as follows. See also Feng et al. (2020). For this purpose, the following stronger assumptions on the error process instead of A2 are required.

A2′. is a stationary process with absolutely summable cumulants up to order 8 and quickly decaying acf such that . Moreover, let denote the first generalized derivative of . It is assumed that .

A2′ summarizes the regularity conditions for the consistency of the following IPI-algorithm in Bühlmann (1996). It implies that . The relationship between A2′ and the commonly used -mixing condition in the current context is also discussed there. In particular, A2′ is fulfilled by an ARMA process with finite eighth moment.

The proposed IPI-algorithm to estimate reads as follows.

-

i)

Set the initial window-width to be with denoting the integer part.

-

ii)

Global stage: In the -th iteration, is estimated. Then the integral of the first generalized derivative of , , is estimated using the Bartlett-window and the window-width . One obtains by inserting the estimates into (5) of Bühlmann (1996). The procedure will be carried out iteratively until it converges or 20 iterations are achieved. We obtain .

-

iii)

Local adaptation for estimating : Calculate and again but using the window-width . Put those estimates into the formula of the local optimal bandwidth at in (5) of Bühlmann (1996) to obtain .

The rate of convergence of the resulting is of the order , which can be improved further, if a more complex -window is used. A minor adjustment we made is that the inflation factor instead of in the original proposal is used, because, as noted by Bühlmann (1996), smaller inflation factors improve the rate of bias. A small simulation shows that the adjusted inflation factor works better than the theoretically optimal one. But now, a few more iterations are required. We do not fix the number of iterations but propose to run the procedure until convergence is reached. Furthermore, we propose the use of a larger starting window-width compared to that used in the original procedure so that the resulting estimates are more stable. Indeed, the selected window-width is usually not affected so much by , if the procedure converges. Roughly speaking, the procedure can be carried out using any suitable initial window-width. Throughout the above procedure only the Bartlett-window is used. The resulting are -consistent and the rate of convergence of is not affected by the errors in .

3.2 The main IPI algorithm

Based on the formula of , WMP99 proposed a plug-in algorithm for selecting by means of some pilot procedure and showed that this idea works well in practice. However, we will not use his algorithm directly due to the following reasons: 1. A correlation adaptive pilot procedure is not well studied in the literature. And 2. Even if such a pilot method exists, it is usually based on a search procedure and runs very slowly. If the sample size is very large, like by the data examples considered in this paper, the computing time of an algorithm for selecting based on a search procedure will be too long. Because of similar reasons, some other ideas for selecting the smoothing parameter in P-splines with a truncated polynomial basis, e.g. those proposed by Kauermann (2005), Krivobokova and Kauermann (2007) and Krivobokova (2013), will also not be considered.

In this paper we will adapt the well-known IPI-idea of Gasser et al. (1991) for kernel or local polynomial regression to select . This IPI-algorithm is similar to Wand’s method, but without the use of a pilot rule and runs much faster. The effect of the correlation is considered from the first iteration. The proposed algorithm processes as follows.

-

1.

Put the number of knots to be and set .

-

2.

In the -th iteration for , estimate using the smoothing parameter .

-

3.

Calculate the residuals and estimate using the proposed IPI-algorithm.

-

4.

Obtain by inserting and into (10).

-

5.

Repetitively carry out Steps 2 to 5 until , for , or 20 iterations are achieved. Denote the finally selected smoothing parameter by .

Note that both, and , are fixed independently of . We will see that, for from a very large range, is not affected by the choice of this initial value. Of course the required number of iterations may depend on the distance between and . The value is just fixed for simplicity in application. Concerning the choice of , it is found that, if is large enough, any can be indeed used. In most of the cases, the proposed algorithm is already stable for any . However, sometimes the estimation quality could be affected, if . Furthermore, it is worth indicating that the proposed IPI-algorithm is stable for any , if it is large enough, and it even works well with . The selected adapts to automatically, so that the estimation quality is almost not affected. But we do not propose the use of a too large , e.g. with , because this will strongly increase the computing time without improving the estimation results. If is too large, the estimation quality can even become slightly worse. This matter will be further discussed in Section 6. The default choice is suggested following Ruppert (2002) and we find that this is a suitable choice for the proposed IPI-algorithm. A further requirement on the proposed IPI-algorithm is that A5 must be fulfilled by and for given . It is easy to show that this condition is fulfilled in any practically relevant case. Some concrete examples will be given in Sections 5 and 6. Moreover, in the implementation in R, is solved by the generalized inverse, because the common matrix inverse operator usually does not work in this case.

The nice practical performances of this IPI-algorithm will be illustrated in sections 5 to 7 using data examples, through a simulation study and by applying the proposals to VaR and ES. The most important theoretical property of is stated in the following.

Theorem 1.

Under the assumptions of Lemma 1, the selected smoothing parameter by the proposed IPI-algorithm for the P-spline smoother of time series is a consistent estimator of such that

| (12) |

The proof of Theorem 1 is omitted. It holds, because both, and are consistent. The rate of convergence of to will not be discussed in the current paper. Note however that Theorem 1 does not mean that is a consistent estimator of . The proposed IPI-procedure converges very quickly. Only a few iterations are usually required, although the stopping criterion is very strict. Following Lemma 1, and are already consistent in the first iteration. Several further iterations are needed to reduce the effect of .

4 Application to the Semi-GARCH models

The proposed data-driven P-spline smoother can be applied to smooth time series in different research areas. In particular, it provides a new tool for smoothing macroeconomic time series. In this paper we will employ this approach to develop new variants of the Semi-GARCH class by means of the log-transformation. Let be some stock prices or the values of some financial index, , and denote the (log-) returns. To analyze the slowly changing local (unconditional) variance and the conditional heteroskedasticity simultaneously, we define the following model

| (13) |

where are i.i.d. random variables with zero mean and unit variance, stands for the local variance function and denotes the conditional variance of with . In this model, is assumed to be a smooth scale function. The product of the local and conditional variances, , is called the total variance of . It is assumed that has a unit variance so that the model is uniquely defined. This implies that . For the practical implementation we put .

The above definition provides a wide extension of the Semi-GARCH model (Feng, 2004). If it is further assumed that follow a unit GARCH model, we have

| (14) |

where with . Due to the restriction , the scale parameter is no longer free. Equations (13) and (14) together define a Semi-GARCH with the standard GARCH model in the parametric part. If the scale function changes over time, the Semi-GARCH model should be employed.

Engle (2003) indicated that is a weighted sum of long-, middle- and short-term volatility effects with the weights ; ; and , respectively. A Semi-GARCH model is indeed approximately a GARCH model with a time-varying scale parameter, i.e. with a time-varying weight for the long-term unconditional variance. By means of a Semi-GARCH model the total volatility is decomposed into a long-run (local) component , a short-run (conditional) heteroskedasticity and the standard deviation of as the baseline volatility factor. The estimate reflexes the current volatility level and helps to improve the estimation and forecasting of the volatility.

The function can e.g. be estimated by kernel or (non-negatively constrained) local linear regression based on the multiplicative model. Following Engle and Rangel (2008), can also be estimated from the log-transformation of the squared returns. Now, the non-negativity of is automatically guaranteed. Assume that a.s. (almost sure). Further discussions are sometimes given in an a.s. sense without explanation, if no confusion arises. Define , , , and , where is the error process with and is a constant determined by the distribution of . Now, shares the additive model (1) and can be estimated using any well-developed nonparametric regression technique for time series. An estimator of is then given by . Our proposal in this paper is to estimate using the P-spline smoother. The approach defined in this way is an extension of the Spline-GARCH and is hence called a P-Spline-GARCH.

By means of this approach, an equivalent scale function can be estimated consistently via under very weak moment conditions and without any parametric assumptions on . To obtain a consistent estimator of however, the condition is still required, which is the same moment condition as required for fitting a parametric GARCH model and is assumed throughout this paper. Having obtained and , the standardized returns can be calculated. Any suitable GARCH model, like the standard GARCH, the APARCH or the EGARCH, can be fitted to . Now, we will show that is asymptotically normal under common regularity conditions. For simplicity, the above three models will be considered as explicit examples. But the results of Theorems 2 and 3 below hold in more general cases. The following (sufficient) moment conditions are required, if the original process follows a GARCH or an APARCH model.

A6. The pdf of , say, is defined according to (1) in Fernndez and Steel (1998), hereafter FS98, but standardized. It is further assumed that and .

Innovation distributions in well-known packages for GARCH models are usually defined following the proposal of Fernndez and Steel (1998), including the - and skewed--distributions with df, the normal and skewed normal distributions as well as the - and skewed -distributions as special members, where stands for the generalized error distribution. They imply that a.s. and . Conditions for the existence of higher order moments of the GARCH and APARCH models are studied by He and Teräsvirta (1999a, b) and Ling and McAleer (2002), among others. Those conditions are jointly determined by and the parameters of the model under consideration. For the EGARCH model, we need the following adjusted version of A6.

A6′. The moment generating function (mgf) of exists in , for some , and , where are the EGARCH coefficients as defined in (2.1) of Nelson (1991).

The conditions required for the existence of the mgf of is not changed. The stronger condition in A6′ on is required so that the mgf’s of and exist, because in an EGARCH, is determined by . This condition is fulfilled by the and the skewed with a shape parameter , including the normal and skewed normal distributions with . Moreover, we assume that , instead of to exclude possible long memory cases. For further discussions we still need the strong mixing property of the above models. Related results may e.g. be found in Carrasco and Chen (2002), and Lee and Shin (2004). Now, we have

Theorem 2.

Let A6 for GARCH and APARCH, and A6′ for EGARCH hold, then

-

i)

The mgf’s of the log-processes , and all exist and hence all of these log-processes have finite moments of all orders.

Assume further that the conditions on the mixing properties of GARCH and APARCH, or those on the mixing properties of the EGARCH(1, 1) as given e.g. in Carrasco and Chen (2002), and Lee and Shin (2004), respectively, hold, then

-

ii)

The log-processes in i) are all -mixing with exponentially decay and

-

iii)

The acf’s of those processes also decay exponentially.

The proof of Theorem 2 is given in the Appendix. Theorem 2 i) provides some very nice properties of the log-innovation process. Theorem 2 ii) extends the exponential -mixing (and hence geometric ergodic) property of squared GARCH, APARCH and EGARCH to the corresponding log-processes, which reflect the fact that mixing properties of a positive process will not be affected by the log-transformation. For the EGARCH, ii) and iii) are given for a first order model only, because we do not find known mixing properties of general EGARCH(, ) models. The result in Theorem 2 iii) extends a well-known fact for a log-normal process to more general case, which together with those in Theorem 2 i) ensures that assumption A2′ required by the data-driven lag-window estimator of is fulfilled. Now, we are ready to prove the asymptotic normality. Let denote a sequence of estimates with the corresponding smoothing parameters . Furthermore, we introduce the following adjusted assumptions.

A3′. The number of knots is chosen by with

A4′. The smoothing parameter is chosen of the optimal order .

The lower bound of in A3′ is made so that the approximation bias is asymptotically negligible. The upper bound is taken to simplify the proof of Theorem 3, which ensures in are all of the order . A4′ means that the chosen penalty term is of the optimal order. According to (4), a reasonable choice is , which satisfies A3′ and also implies A5. The constants in the asymptotic bias and variance may depend on . This will however not affect our proof of the asymptotic normality and will not be considered in detail. Hence, we will denote a generic by for simplicity. Under A4′, the P-spline smoother achieves the optimal rate of convergence with and , where and is a sequence of constants in the finite sample variances. A suitable central limit theorem for a weighted sum of a strongly mixing sequence is given by Peligrad and Utev (1997), hereafter PU97, which applies to the proposed P-spline smoother. Following their results we have

Theorem 3.

Let A1, A3′, A4′ and A5 hold. Under the conditions of Theorem 2, we have

| (15) |

This result can be extended to the case with together with the assumption that the approximation bias is still asymptotically negligible. Now, asymptotic normal distribution is only determined by the asymptotic variance with a lower rate of convergence. Asymptotic normality of a kernel estimator, say, of the scale function in the Semi-GARCH model obtained from the multiplicative model directly is proved in Feng (2004). Following Theorem 2, his results can be extended to a general class of Semi-GARCH models with an estimate of the scale function obtained independent of the used parametric volatility models in the second stage. However, Theorem 3 is on the asymptotic normality of , not on that of . It is clear that in the current context the resulting is no longer asymptotically normal but asymptotically log-normal.

The effect of the errors in on the parameter estimation based on the standardized returns can be studied following Theorem 3 in Feng (2004). Two related facts are that the optimal smoothing parameter is not the optimal choice for the further parameter estimation and the parameter estimation from the standardized returns with is no longer -consistent. Detailed discussion on this topic is omitted to save space. All results in this section hold for the local polynomial estimator of obtained from the log-transformation of the squared returns under corresponding conditions.

5 Real data examples

In the following, the proposed P-spline smoother is employed to estimate the scale functions in the returns of three indexes, namely the Standard and Poor 500 (S&P), the DAX 30 (DAX) and the Nikkei 225 (NIK), from January 1988 to April 2018, and of three German companies, i.e. the SAP SE (SAP), the Siemens AG (SIE) and the Allianz SE (ALV), from January 1997 to April 2018, downloaded from Yahoo Finance. As indicated by Harvey et al. (1994), the centralized returns are (a.s.) non-zero. Hence, is well defined in practice and there is no computational problem with possible zero returns. The main results are obtained with the default choices and . The obtained results are then compared to those of a data-driven local cubic regression under stationary time series errors (Feng et al., 2020). The latter is well-developed and is used here as a benchmark. The Alg. B there is used as the authors suggested. This comparative study will be further carried out through the simulation study in the next section. As far as we know, this is the first empirical study to compare the performance of data-driven P-splines to that of a data-driven local regression. In the following the abbreviation Semi-GARCH stands for a model with the standard GARCH in the parametric part or for a generic model in this class. That with APARCH in the second part will be called Semi-APARCH. The parametric models will be fitted using the ‘fGarch’ package in R. The Semi-EGARCH will not be considered, because it cannot be fitted by ‘fGarch’.

The chosen for P-splines and the selected bandwidth () for the local cubic regression for all examples are listed in the first part of Table 1, where the integer in brackets under indicates the number of required iterations. A surprising finding is that, for the chosen , the amount of the smoothing parameter according to the definition in (2) is at the same level as that of the bandwidth of a local cubic regression. Usually, will increase with . However, the orders of those two quantities are not the same. And the variation of is clearly larger than that of , indicating that those two smoothing parameters have different features. The return series and the estimated scale functions using both approaches are displayed in Figure 1 for the examples of S&P, DAX and SAP. We see, the obtained results using both approaches are quite similar. The differences at the endpoints or around the extrema of a scale function may be sometimes slightly clear. Note that the data-driven local cubic regression achieves the optimal rate of convergence. It hence confirms that the proposed data-driven P-spline smoother works well in practice.

To show the possible effect of on , the IPI-algorithm with was further carried out with different within a wide range. The results for and 3.2, as well, are given in the second part of Table 1. The biggest differences between selected using different are all smaller than and are hence negligible. The required number of iterations can be affected by slightly. Moreover, in all cases the condition is clearly fulfilled by and in each iteration. The smallest value of is that for the DAX with . Now, we have , which is clearly bigger than 1. It is also shown that adapts to automatically, so that is almost not affected by the choice of , provided that . Those results are omitted to save space.

6 A simulation study

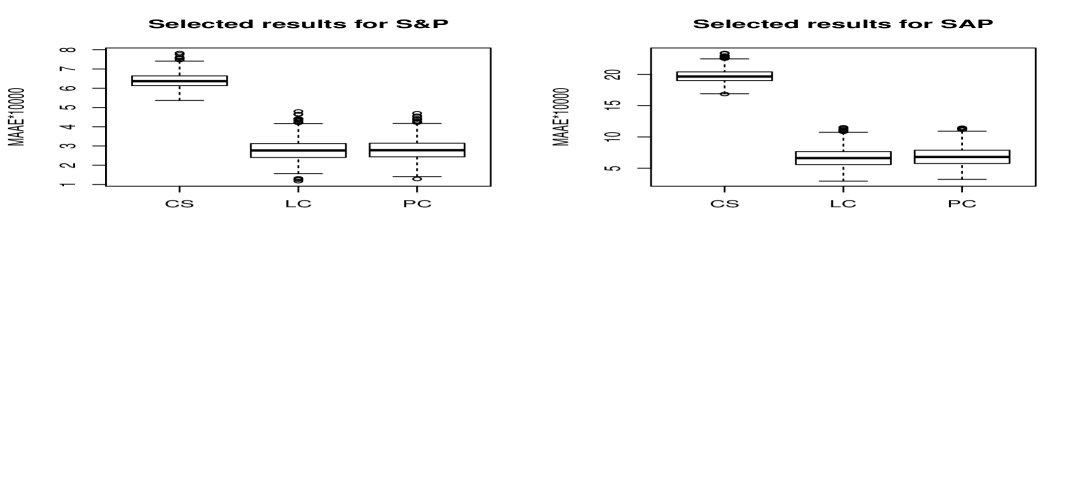

In the second stage, a suitable GARCH model can be fitted to the standardized returns . Then the total volatility can be calculated. The aim of the following simulation study is to show whether and how far the estimation quality of the volatility can be improved by a Semi-GARCH approach compared to that of a GARCH model. So far as we know such topics were not yet investigated in the literature. In contrast to most of the simulation studies in this context, the quality of , or the further resulting parameter estimation from the residuals or standardized returns will not be discussed. Moreover, the two estimated scale functions of S&P and SAP instead of some artificially designed scale functions will be used as the underlying scale functions. Here, the results of the local cubic regression are used, so that they are independent of the choice of . The two GARCH(1, 1) models under conditional normal distribution with and , will be employed as the error processes (in the multiplicative model). Where the coefficients are adjusted slightly so that their sum is exactly 1. The two sample sizes and are used in the two cases, respectively. Therefor, only one sample size in each case is considered. The simulation was carried out using the local cubic regression (LC) and cubic P-splines (PC) with , 20, …, 70, denoted by PC1, …, PC7, respectively. In each case replications were carried out. The parametric GARCH model under constant scale assumption (CS) is taken as a comparison.

We propose to assess the quality of the estimated volatility by given approach ‘X’ using a goodness-of-fit measure defined in the following. Firstly, we define an error criterion MAAE (mean average absolute error) of the estimated volatility over all replications

| (16) |

where is the estimated (total) volatility series in the -replication by approach ‘X’ and stands for the corresponding true simulated volatility series. Denoting by the MAAE obtained by the comparison, a goodness-of-fit measure, called the reduction of the MAAE (RMAAE in ) of approach ‘X’ comparing to , is defined by

| (17) |

which indicates the amount of the reduced errors in the estimated volatility obtained by a Semi-GARCH approach compared to that of a parametric GARCH model.

Here, we have obtained and 19.75 for the two data sets. The means of , (in %) and the means of or , respectively, are listed in Table 2. We see, the estimation quality of the volatility for the S&P index is much higher than that for the SAP stock price. Furthermore, the absolute error in the volatility estimated by a GARCH model can be clearly reduced by a Semi-GARCH approach. If the scale function is estimated by the LC-method, this reduction is roughly 56.3% for S&P and 66.0% for SAP. The improvement in the latter case, when the estimation quality is poorer, is more clear than that in the former case. The results for the PC-approach depend on slightly. A clear finding is that should not be used. For the SAP-example and are optimized by and increases slightly with for . But the results with are almost the same as those with . For the S&P-example, decreases slightly, if increases. Here, the value, which minimized , is larger than 70. However, for all , we have . That is, the effect of any seems to be very limited. The reason for this is that adapts automatically to the change of so that the resulting estimates are almost not affected. In both cases the suggested default choice with is suitable. The use of a in the latter case is also unnecessary. In comparison with the LC-approach, the estimation quality of the PC approach with is slightly poorer. But, the computing time of the latter is clearly shorter than one fifth of that required by the LC-approach. Boxplots of the AAE for all replications for the three approaches CS, LC and PC4 are displayed in Figure 2. We see, the reduction in the estimation error made by a Semi-GARCH model is uniformly over all replications. And the maximal estimation error of a Semi-GARCH approach among all replications is still smaller than the minimal error of the GARCH method.

7 Forecasting VaR and ES by Semi-GARCH

Now, we will show how a Semi-GARCH approach can be applied to forecast VaR and ES. For this purpose the models are fitted without the last returns, which are then used for backtesting the one-day rolling forecasts of VaR and ES. Here, the negative returns, , will be used as the losses, because they correspond to the ratios of the linearized losses. See (2.5) in McNeil et al. (2015). The forecasting of ES-forecasts based on a Semi-GARCH model will be described. The forecasting of VaR is similar. For simplicity, it is assumed that the mean of the returns is constant. And only the conditional -distribution will be considered to save space. Furthermore, we simply propose to use the last estimate of the scale function, , as the forecast for the unconditional standard deviation for the next year. Then the rolling one-day forecasts of ES are given by

| (18) |

where is the ES of a rescaled -distribution with the df= and variance 1. Here, are the forecasts of the conditional variances following a unit GARCH model, which hence have to be calculated by the descaled returns , . According to (2.25) in McNeil et al. (2015) we have, for ,

| (19) |

where , and are the density, distribution and quantile functions of a -distribution with the df=, respectively. Note that corresponds to a VaR at the confidence level with , which is a function of and . Now, is slightly bigger than 0.99 so that the -ES is slightly bigger than the -VaR.

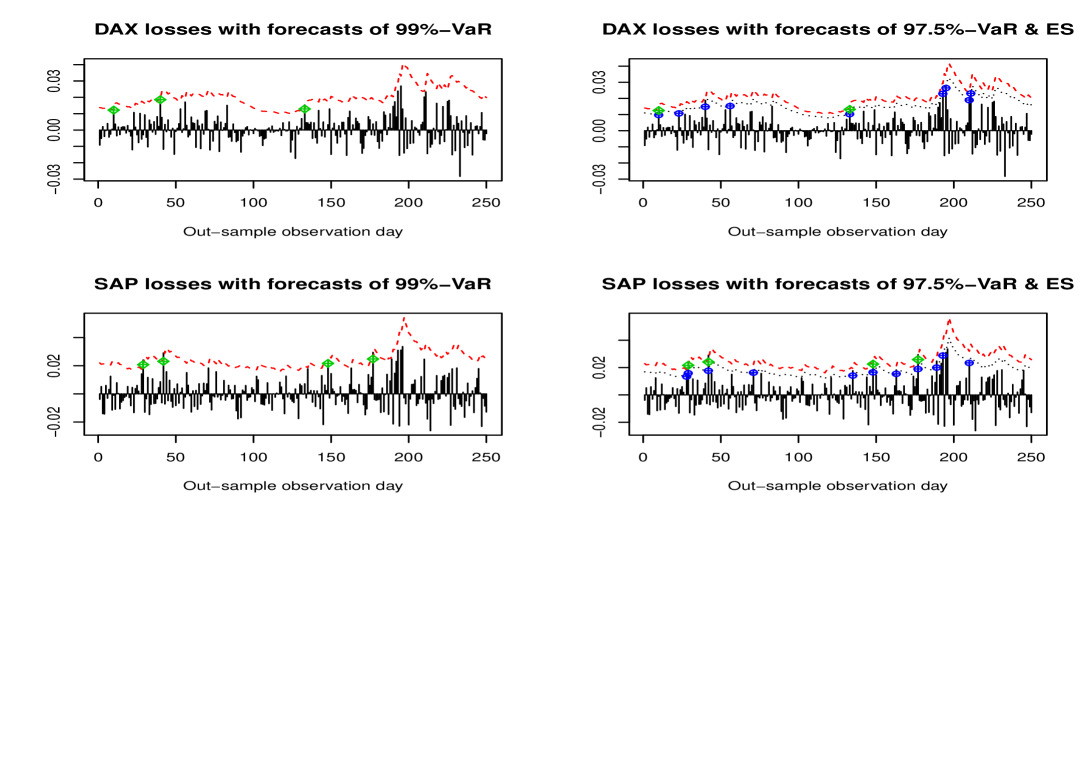

The above idea is illustrated by calculating 250 out-of-sample forecasts of VaR at both -levels and ES at the -level for the DAX and SAP, where the model was estimated using P-spline scale function and an in-sample till about April 2017. The results with an APARCH(1, 1) in the parametric part are displayed in Figure 3. We see, the estimated -ES are quite similar to the estimated -VaR. The POT (points over the threshold) for DAX and SAP are 3 and 4 for the -VaR, and 9 and 11 for the -VaR, respectively. The first three are within their green zones, i.e. [0, 4] and [0, 10] for and , respectively, and the last lies at the beginning of its yellow zone, according to the Traffic-Light approach proposed by the BCBS for backtesting the VaR. The POT for the -ES are 2 and 4, respectively, with one point fewer than that for the VaR in the first case. This is as expected, because under the -distribution, the POT for the -ES is usually equal to, but sometimes smaller than that for the -VaR. Those examples show that the Semi-GARCH approaches provide useful alternatives to the parametric GARCH models for measuring quantitative risk. It is also found that, although the in-sample performance of a Semi-GARCH approach is usually better than that of a parametric GARCH model, the out-of-sample forecasts of VaR and ES using a Semi-GARCH model are not necessarily better than those obtained by a parametric model. Moreover, the selected bandwidth based on the in-sample is not necessarily the best for calculating the out-of-sample forecasts of VaR or ES. Those problems and related topics, such as the backtesting of VaR and ES, will be studied in more detail elsewhere.

8 Concluding remarks

In this paper a P-spline smoother for time series with an IPI-algorithm for selecting the smoothing parameter is proposed without any parametric assumption on the errors. This algorithm is developed based on an approximation of the optimal smoothing parameter obtained following WMP99, which works well in practice. Comparing to the traditional local cubic regression, the P-spline smoother is more flexible and runs much faster. The proposal is applied to estimate the scale function in a Semi-GARCH model from the log-transformation of the squared returns. This leads to a so-called P-spline-GARCH. Properties of the log-processes and asymptotic normality of the resulting trend estimate are studied in detail. Practical performance of the P-Spline-GARCH is illustrated by a number of examples. A simulation study confirms that the errors in the estimated volatility of a GARCH model can be strongly reduced by means of a Semi-GARCH approach. Moreover, it is shown that the proposals can be employed for forecasting VaR and ES. Further studies on the application of Semi-GARCH approaches to VaR and ES are of great interest. It is also worth to extend the current proposal to P-splines with the B-spline basis or to models with long-range dependent errors. Possible semiparametric extensions of long-memory GARCH models, such as the FIGARCH (Baillie et al., 1996) or FIEGARCH (Bollerslev and Mikkelsen, 1996), are also of great interest.

Acknowledgments: The data were downloaded from Yahoo Finance. We are grateful to Prof. Tatyana Krivobokova, University of Göttingen, for detailed explanation about their asymptotic results on P-splines with truncated polynomial basis. We would like to thank Prof. Timo Teääsvirta, CREATES, Aarhus University, and Prof. Luo Xiao, North Carolina State University, for sending us their most recent research papers. Our thanks also go to Prof. Thomas Gries, Mr. Marlon Fritz, Mr. Sebastian Letmathe and Mr. Xuehai Zhang, Paderborn University, for helpful discussion and suggestions.

References

-

Acerbi, C. and Tasche, D. (2002). Expected Shortfall: a natural coherent alternative to Value at Risk. Econ. Notes, 31, 379-388.

-

Amado, C., Silvennoinen, A. and Teräsvirta, T. (2018). Models with multiplicative decomposition of conditional variances and correlations. Preprint, Aarhus University.

-

Baillie, R., Bollerslev, T. and Mikkelsen, H. (1996). Fractionally integrated generalised autoregressive conditional heteroscedasticity, J. Econometr., 74, 3–30.

-

BCBS (2016). STANDARDS: Minimum capital requirements for market risk.

-

BCBS (2017). Dec 2017 Basel III: Finalising post-crisis reforms.

-

Bellingsley, P. (1995). Probability and Measure Theory (3rd ed.). Wiley, New York.

-

Bollerslev, T. (1986) Generalized autoregressive conditional heteroskedasticity. J. Econometrics 31, 307–327.

-

Bollerslev, T. and Mikkelsen, H.O. (1996). Modeling and Pricing Long Memory in Stock Market Volatility. J. Econometr., 73, 151-184.

-

Bühlmann, P. (1996). Locally adaptive lag-window spectral estimation. J. Time Ser. Anal., 17, 247-270.

-

Claeskens, G., Krivobokova, T., and Opsomer, J. (2009). Asymptotic properties of penalized spline estimators. Biometrika, 96, 529–544.

-

Carrasco, M., Chen, X., 2002. Mixing and moment properties of various GARCH and stochastic volatility models. Econometric Theory 18, 17-39.

-

Davis, R. A. and Mikosch, T. (2009). Probabilistic Properties of Stochastic Volatility Models. in Andersen, T.G., Davis, R.A., Kreiß, J.-P. and Mikosch, T. (ed): Handbook of Financial Time Series, pp. 255-267, Springer, Berlin.

-

Ding, Z., C.W.J. Granger and R.F. Engle (1993) A long memory property of stock market returns and a new model. J. Empirical Finance 1, 83-106.

-

Eilers, P.H.C. and Marx, B.D. (1996). Flexible smoothing with B-splines and penalties (with discussion). Statist. Sci., 11, 89-121.

-

Engle, R.F. (1982) Autoregressive conditional heteroskedasticity with estimation of U.K. inflation, Econometrica 50, 987–1008.

-

Engle, R.F. (2003) Risk and volatility: Econometric models and financial practice. Nobel Lecture, available at http://nobelprize.org.

-

Engle, R.F. and Rangel, J.G. (2008). The Spline-GARCH model for low-frequency volatility and its global macroeconomic causes. Rev. Financ. Stud., 21, 1187-1222.

-

Feng, Y. (2004). Simultaneously modelling conditional heteroskedasticity and scale change. Econometric Theory, 20, 563-596.

-

Feng, Y., Gries, T. and Fritz, M. (2020). Data-driven local polynomial for the trend and its derivatives in time series. Revised for a journal.

-

Fernndez, C. and Steel, M.F. (1998). On bayesian modeling of fat tails and skewness. J. Amer. Statist. Ass., 93 359-371.

-

Gasser, T., Kneip, A. and Köhler, W. (1991). A flexible and fast method for automatic smoothing. J. Amer. Statist. Assoc., 86, 643-652.

-

Hall, P., and Opsomer, J. (2005). Theory for penalised spline regression. Biometrika, 92, 105-118.

-

Harvey, A., Ruiz, E. and Shephard, N. (1994). Multivariate stochastic variance models. Rev. Econ. Stud., 61, 247-264.

-

He, C. and Teräsvirta, T. (1999a). Forth moment structure of the GARCH process. Econometric Theory 15 824–846.

-

He, C. and Teräsvirta, T. (1999b). Statistical properties of asymmetric power ARCH process. In R.F. Engle and H. White (eds). Cointegration, Causality, and Forecasting: Festschrift in Honour of Clive W.J. Granger, pp. 462-474. Oxford University Press, Oxford.

-

JPMorgan (1996). RiskMetrics Technical Document (4th ed). JPMorgan, New York.

-

Kauermann, G. (2005). A note on smoothing parameter selection for penalized spline smoothing. J. Statist. Pl. Infer., 127, 53–69.

-

Kauermann, G., Krivobokova, T. and Semmler, W. (2011). Filtering Time Series with Penalized Splines. Stud. Nonl. Dynam. & Econometr., 15, 1-28.

-

Krivobokova, T. and Kauermann G. (2007). A note on penalized spline smoothing with correlated errors. J. Amer. Statist. Assos., 102, 1328-1337.

-

Krivobokova, T. (2013). Smoothing parameter selection in two frameworks for penalized splines. J. R. Statist. Soc. B, 75, 725-741.

-

Lee, O. and Shin, D. W. (2004). Strict stationarity and mixing properties of asymmetric power GARCH models allowing a signed volatility. Economics Letters, 84, 167-173.

-

Li, Y. and Ruppert, D. (2008). On the asymptotics of penalized splines. Biometrika, 95, 415-436.

-

Ling, S. and McAleer, M. (2002). Necessary and sufficient moment conditions for the GARCH(r,s) and asymmetric power GARCH(r,s) models. To appear in Econometric Theory, 18, 722-729.

-

McNeil, A., Frey, R. and Embrechts, P. (2015). Quantitative Risk Management: Concepts, Techniques and Tools, 2e. Princeton University Press, Princeton.

-

Nelson, D. B. (1991). Conditional heteroskedasticity in asset returns: A new approach. Econometrica. 59, 347-370.

-

O’Sullivan, F. (1986). A statistical perspective on ill-posed inverse problems. Statist. Sc., 1, 502–518.

-

Peligrad, M. and Utev, S. (1997). Central limit theorem for linear processes. Ann. Probab., 25, 443-456.

-

Ruppert, D. (2002). Selecting the number of knots for penalized splines. J. Comput. Graph. Statist., 11, 735-757.

-

Ruppert, D., Wand, M.P. and Carroll, R.J. (2003). Semiparametric Regression. Cambridge University Press, Cambridge, UK.

-

Stone, C.J. (1982). Optimal global rates of convergence for nonparametric regression. Ann. Statist., 10, 1040-1053.

-

Wand, M.P. (1999). On the optimal amount of smoothing in penalised spline regression. Biometrika, 86, 936-940.

-

Xiao, L. (2019). Asymptotic theory of penalized splines. Elctr. J. Statist., 13, 747-794.

-

Xiao, L., Li, Y., Apanasovich, T.V. and Ruppert, D. (2012). Local Asymptotics of P-splines. Preprint, North Carolina State University.

-

Zhou, S., Shen, X. and Wolfe, D. A. (1998). Local asymptotics for regression splines and confidence regions. Ann. Statist., 26, 1760-1782.

Appendix. Technical details and proofs of results

The proof of (4). For , in CKO09 reduces to

| (A.1) |

where and is a constant that depends only on and the design density. In our case the design density is the uniform one on with , . The design points satisfy . Speckman (1985) showed tat now . That is . (4) is proved by inserting this into (A.1).

The proof of (9).

Let with , then for any are asymptotically equivalent to some kernel weights. Li and Ruppert (2008) and Xiao et al. (2012) provided the asymptotic equivalent kernels of P-splines with the B-spline basis. The asymptotic equivalent kernels in the current context are obtained by Hall and Opsomer (2005) under a white-noise framework. Following Lemma 1, the asymptotic properties of are asymptotically equivalent to those of a th order kernel regression with automatic boundary correction and the corresponding bandwidth . Hence, all are at most of the order and vary regularly in the interior part. Note that, . Choose and , such that , as . Define and for given . For given , and , we have and the following decomposition

For given , the second sum in splits up into two terms

Straightforward analysis results in and . This leads to

Furthermore, it can be shown that

and . We obtain

| (A.2) |

A sketched proof of (10).

The proof of this result is similar to that given in WMP99 by replacing there with . Hence, we will only provide some complements about the two approximations used in his proof. Firstly, the derivation of begins with the Taylor expansion of

where is the identity matrix. The result in (10) is then obtained by assuming that the approximation bias is asymptotically negligible. The latter approximation is ensured by the assumptions of Lemma 1. However, the assumption he used for the Taylor expansion is unnecessary and also unreasonable, because in the current case should tend to . What we need here is indeed . Note that the order of is , only if is fixed. When , the order of entries of this matrix changes from the first column to the last, and from the first row to the last, as well. The smallest elements occur in the low-right corner. It is easy to show that the last diagonal element is of the order and the other elements in that corner are also of this order. Hence, the largest terms of occur in the low-right corner. Detailed analysis shows that those elements are of the order . Thus, the required condition for the Taylor expansion is indeed or . Further proof of this result follows the arguments in WMP99.

Remark A.1. The necessary condition we obtained is very strong. In particular, it is not fulfilled, if is of the optimal order as obtained by CKO09 with and , because now is at least of the order . The condition is usually also not fulfilled by a practically relevant data set. Hence, seems to be only a suboptimal approximation of . The search for a better approximation of is an important open question.

Proof of Theorem 2. i) We first prove the results for the innovation process , which is the same in all of the three models. Denote the pdf’s of , and by , and , respectively. The proof will be first given an original distribution proposed by FS98. Following Equation (1) in FS98, is defined based on a pdf in , which is unimodal and symmetric around 0, such that and the latter is decreasing in . A scalar parameter is added to this distribution to introduce asymmetry. Let and . Then is defined by

| (A.3) |

where , if and only if . The pdf of the two-to-one transformation is given by

| (A.4) |

for . Now, insert the transformation further into , after some simplification we have

| (A.5) |

A6 implies that as , which results in further as and as . Thus, at least exists for with and and has finite moments of all orders, where almost surely.

Moreover, it is easy to show that the above results are not affected by a linear transformation with , including the standardization as a special case. The reasons for this are, in the above proof: 1) The unimodal property is not required; 2) If there is a mode at zero is unnecessary; and 3) Whether is increasing for or not, or decreasing for or not, is indeed also not required in the proof given above. Thus those results are preserved after a necessary standardization.

Now, consider in GARCH and APARCH. Assume that the initial values all started from their invariant measures. Following the definition of a GARCH or an APARCH model, we have and the pdf of , say, is zero for . Hence, for any . This together with the above proof shows that the mgf of at least exists in . This shows that that the mgf of exits, too. The two processes and also have finite moments of all orders. The proof of the results for in the EGARCH under A6′ is straightforward and is omitted, because is now a linear process.

ii) Furthermore, because the strong mixing property is defined via -fields and the log-transformation is measurable and almost surely well defined. Hence, the mixing properties and the rate of the mixing coefficients of the original process will be all taken over by the log-transformed process. See Davis and Mikosch (2009). The strong mixing properties of the squared GARCH, APARCH and EGARCH models with exponentially decaying mixing coefficients as given e.g. in Carrasco and Chen (2002), and Lee and Shin (2004) hold immediately for the corresponding log-processes. That is, all of those log-processes are strongly mixing with exponential decay.

iii) The relationship between the mixing coefficients of a strongly mixing stationary process with , , and its autocorrelations is given by

where is some constant. See Davis and Mikosch (2009) and references therein. Hence, also decay exponentially, if decay exponentially. In the current case, we have further because the processes under consideration all have finite moments of all orders. These results are very helpful for analyzing non-negative processes after the log-transformation. This finishes the proof of Theorem 2.

Proof of Theorem 3. Most of the results on the asymptotic normality of partial sums or of the sample mean under different strong mixing and moment conditions, such as that in Bellingsley (1995), are not directly applicable to the proposed P-spline smoother. However, one of the central limit theorems given in PU97 can be applied to a general linear estimator, including the P-spline smoother or the local polynomial regression estimator considered in this paper as special cases.

Denote by the sequence of the smoother matrices, we have

where are the weights of the P-spline smoother in the corresponding row of . Let be the finite sample variance of . Define and . Then we have and . Now, we only need to show that is asymptotically standard normally distributed, because,

by definition and hence,

The remaining proof is hence to show that Condition (2.1) on the weights , Condition (2.2) on the uniform integrability of and Condition (c) required by Theorem 2.2 in PU97 on the mixing property and finite moments of are all fulfilled by .

Note first that is a strictly and weakly stationary process with finite moments of all orders, and strongly mixing with exponentially decay mixing coefficients. Also is non-degenerate. Hence, Condition (c) of Theorem 2.2 in PU97 is clearly fulfilled. Because of the strong and weak stationarity, forms a uniformly integrable family. Condition (2.2) in PU97 is satisfied. Moreover, the proposed P-spline smoother is asymptotically equivalent to some kernel estimator of order . But the explicit forms of such asymptotic kernels are very complex and are seemingly not yet well studied in the literature for P-spline smoothers with a truncated polynomial basis. To overcome this difficulty, we hence introduced a slightly stronger restriction on the order of magnitude of the number of knots in A3′, which simplifies our proof very much, but is of course unnecessary. Note that the order of is bounded by the magnitude order of the weights of regression splines with . Under A3′ we have

Under A4′ we have . Thus, . This implies . The standardization condition together with the formula of the asymptotic variance ensures that , i.e. . This means that . Condition (2.1) in PU97 is fulfilled by the standardized weights . Thus

Theorem 3 is proved.

| S&P | DAX | NIK | SAP | SIE | ALV | ||

| 7641 | 7660 | 7457 | 5365 | 5444 | 5433 | ||

| 0.20 | 40 | 0.1607 | 0.2289 | 0.2314 | 0.1753 | 0.1551 | 0.2140 |

| (5) | (6) | (5) | (5) | (4) | (4) | ||

| loc. cub. () | 0.1811 | 0.2188 | 0.2222 | 0.1966 | 0.1840 | 0.2046 | |

| 0.05 | 40 | 0.1607 | 0.2289 | 0.2314 | 0.1753 | 0.1551 | 0.2140 |

| (5) | (7) | (7) | (5) | (4) | (5) | ||

| 0.80 | 0.1607 | 0.2290 | 0.2314 | 0.1753 | 0.1551 | 0.2141 | |

| (7) | (7) | (7) | (7) | (6) | (6) | ||

| 3.20 | 0.1607 | 0.2290 | 0.2314 | 0.1753 | 0.1551 | 0.2141 | |

| (7) | (7) | (7) | (7) | (6) | (6) | ||

| Data | Stat | LC | PC1 | PC2 | PC3 | PC4 | PC5 | PC6 | PC7 |

|---|---|---|---|---|---|---|---|---|---|

| S&P | 2.7924 | 3.0019 | 2.8454 | 2.8225 | 2.8207 | 2.8195 | 2.8187 | 2.8181 | |

| 56.258 | 52.932 | 55.404 | 55.760 | 55.787 | 55.805 | 55.817 | 55.826 | ||

| 0.1550 | 0.1272 | 0.1413 | 0.1415 | 0.1474 | 0.1523 | 0.1565 | 0.1601 | ||

| SAP | 6.7182 | 6.9481 | 6.9593 | 6.9158 | 6.9161 | 6.9165 | 6.9169 | 6.9173 | |

| 65.963 | 64.794 | 64.736 | 64.956 | 64.954 | 64.952 | 64.950 | 64.948 | ||

| 0.1973 | 0.1685 | 0.1887 | 0.1844 | 0.1924 | 0.1990 | 0.2046 | 0.2095 |