Equilibrium price in intraday electricity markets111This study was supported by FiME (Finance for Energy Market Research Centre) and the “Finance et Développement Durable - Approches Quantitatives” EDF - CACIB Chair.

Abstract

We formulate an equilibrium model of intraday trading in electricity markets. Agents face balancing constraints between their customers consumption plus intraday sales and their production plus intraday purchases. They have continuously updated forecast of their customers consumption at maturity with decreasing volatility error. Forecasts are prone to idiosyncratic noise as well as common noise (weather). Agents production capacities are subject to independent random outages, which are each modelled by a Markov chain. The equilibrium price is defined as the price that minimises trading cost plus imbalance cost of each agent and satisfies the usual market clearing condition. Existence and uniqueness of the equilibrium are proved, and we show that the equilibrium price and the optimal trading strategies are martingales. The main economic insights are the following. (i) When there is no uncertainty on generation, it is shown that the market price is a convex combination of forecasted marginal cost of each agent, with deterministic weights. Furhermore, the equilibrium market price follows Almgren and Chriss’s model and we identify the fundamental part as well as the permanent market impact. It turns out that heterogeneity across agents is a necessary condition for the Samuelson’s effect to hold. (ii) When there is production uncertainty, the price volatility becomes stochastic but converges to the case without production uncertainty when the number of agents increases to infinity. Further, on a two-agent case, we show that the potential outages of a low marginal cost producer reduces her sales position.

Key words: Equilibrium model, intra-day electricity markets, Samuelson’s effect, martingale optimality principle, coupled forward-backward SDE with jumps.

1 Introduction

Because electricity cannot be stored, the development of competitive electricity markets has led to the introduction of intraday markets. The purpose of these markets whose time-horizon does not exceed more than 36 hours is to allow electricity market players to balance their position between their customers consumption and their generation for each hour of the day and avoid expensive imbalance costs. The development of intermitent renewable electricity generation have increased the interest of both market players and academics for these markets. Indeed, because of the high uncertainty of wind generation production, the need of short-term balancing mechanism has increased. Empirical studies of intraday market show an increase in trading volume in the last years and convergent stylised facts about liquidity and volatility of intraday prices; liquidity as measured by market depth and volatility both increase with time closer to delivery (see Kiesel et. al. (2017) [19], Balardy (2018) [5], Kremer et. al. [20], Glas et. al. (2020) [14]).

This phenomenom is known as the Samuelson’s effect, since it was first posited and explained by Samuelson (1965) [26]. This effect states that the volatility of futures prices contract increases as time gets closer to delivery. And indeed, trading in intraday market consists in trading during less than 36 hours a futures contract for delivery for a maturity given by a fixed hour. This pattern of increasing volatility of electricity futures prices has been found for other maturities. Jaeck and Lautier (2016) [18] finds that Samuelson’s effect holds on all tested electricity markets (German, Nordic, US, Autralia) for monthly contract delivery.

In Samuelson’s paper, the effect is obtained as the consequence of two hypothesis: the spot price is mean-reverting and the futures price is the conditional expectation of the spot price. Further, for Bessembinder et. al. (1996) [7], mean-reversion in the context of commodity prices is linked to storability: when prices are high, agents reduce storage making the price decrease and vice versa, resulting in a mean-reversion effect. In the context of electricity, the storage hypothesis does not seem appropriate to explain the effect. Further, all prices of storable commodities do not exhibit this behaviour (see Jaeck and Lautier (2016) [18]). Anderson and Danthine (1983) [3] and Anderson (1985) [4] formulated a more general hypothesis, named the state variable hypothesis to explain why some commodity prices exhibith the Samuelson’s effect and others do not. They state that the monotonocity (if any) of the volatility of futures prices depends on the way uncertainty on the equilibrium between demand and supply is resolved. In particular, in the case where volatility of demand uncertainty decreases with time, the futures price volatility may decrease. This is the case of intraday electricity market (demand forecasts error tend to decrease quickly with delivery) and nevertheless, intraday prices still exhibit an increase of volatility. Another explanation for the occurence or not of the Samuelson’s effect has been formulated by Hong (2000) [17]. Hong (2000) shows in an equilibrium model of commodity futures trading how information asymmetry may also sustain violation of Samuelson’s hypothesis. In the case of electricity markets and in particular intraday markets, both the energy regulator and the European financial regulation under REMIT compels producers and retailers to provide immediate communication to the market operator of any information that may affect the equilibrium between supply and demand before taking appropriate trading positions. These regulations are intented to reduce as much as possible asymmetry of information between players and yet, the intraday electricity prices still exhibit a pattern of increasing volatility. More recently Féron et. al. (2020) [13] models an intraday market Nash equilibrium in the context of identical agents trading at a fundamental price plus a liquidity premium while the market price is defined à la Almgren and Chriss by a fundamental price plus a linear permanent impact induced by the average inventory level (because there is no market clearing condition, the average inventory is non-zero). In this context, they recover the Samuelson’s effect as the result of strategic behaviour of agents.

In this paper, we develop an equilibrium model of intraday trading for a fixed hour of delivery with the purpose to explain and understand the optimal trading strategies of market players as well as the market price dynamics. We consider that the market is composed of agents having each a forecast at time of their customers consumption at time . We suppose that the volatility of the demand forecast is deterministic and decreases with time, capturing the empirical evidence of increasing demand forecast with time to delivery (see Nedellec et. al. [23]). The demand forecast off each agent is affected both by an individual brownian noise and a collective brownian noise with correlation , reflecting the dependence of market players to weather and global economic conditions. Further, each agent is endowed with a generation capacity with linear marginal cost of coefficient . Further, evolves following a Markov chain, capturing by this way the possibility of power plant outages driving the marginal cost of an agent from a low to a high cost. Agents can buy or sell power for delivery at time at the market price plus a liquidity premium proportional to the trade . This premium translates the potential diffferent market access cost of agents. The objective of each agent is to minimise the expected total trading cost plus the costs of imbalance where represents agent’s own perception of the cost of imbalance, and are the inventory and the production of the agent at . Although the cost of imbalance is fixed by the electricity network operator and is the same for any market player, we allow for different evaluation of the cost of imbalance, translating the possibility that some players may have strong reluctance for imbalances while other might not care as much. All information is considered public. A market equilibrium is defined as trading strategies and a market price such that each agent has minimised her criteria and the market clears for the market price. This model owes agent’s features to Aïd et. al. (2016) [1] and Tan and Tankov (2018) [27].

In this framework, we obtain the following results. We prove existence and uniqueness of the equilibrium. The proof is based on the martingale optimality principle in stochastic control, and existence of solution to backward stochastic differential equations (backward SDEs) with jumps, for which we provide a complementary existence result to Becherer (2002) [6]. We show that both the equilibrium price and the optimal trading strategies are martingales, and they are characterized in terms of a coupled system of forward-backward SDE that we solve with explicit formulae.

In the case where there is no production cost uncertainty, we observe that the market price is a convex combination of the forecasted marginal cost of each agent where the weights are deterministic functions of time. The optimal trading rate of each agent consists in comparing her forecasted marginal cost to the market price and to take position accordingly, i.e. to sell (resp. to buy) if it is lower (resp. higher). Although simple, this strategy is commonly used in intraday electricity trading desks of power utilities. Further, we show that the equilibrium price has the form of Almgren and Chriss model [2]. We identify the fundamental part of the price as the average forecasted marginal cost to satisfy the demands and identify the market permanent impact of each agents. Permanent market impacts are deterministic function of time with a monotony depending on the agent. If all agents are identical, the market equilibrium reduces to its fundamental component because of the market clearing condition. The closed-form expression derived for the price and the trading strategies allows us to provide insight on the dynamics of the price volatility defined as the quadratic variation of the price. If all agents are identical, the price volatility monotonicity is fully determined by the volatility of the demand forecasts. In our case where the demand forecasts volatilities are decreasing in time, it implies that if the Samuelson’s effect is to hold, agents must be heterogeneous. Thus, the Anderson and Danthine state variable hypothesis is not sufficient to explain increasing price volatility in a context of decreasing demand forecast error. We provide numerical illustrations where the mixing of agents of two different types allows to have decreasing or increasing volatility functions depending on the proportion of the agent’s type. Further, heterogeneity of agents as expressed by their marginal cost, market access quality and dependence to weather can be observed. Thus, explaining price volatility by heterogeneity leads to testable predictions.

In the case where there is production cost uncertainty, we show that if the number of agents is large, the equilibrium tends to the case of no production cost uncertainty because of the independence of jumps in the Markov chains between agents. Further, in the case of two players where the second player is affected by a potential jump that will switch her production cost from a lower marginal cost to a higher marginal cost compared to the first player, we observe that she moves from a selling position to a buying position as the probability of jumps increases. Although limited, this result gives credit to idea of precautionary position when entering in intraday market, i.e. selling less than the total quantity of marginal cost lower than the price.

The paper is structured as follows. Section 2 describes precisely the model. Section 3 provides the main results in terms of optimal strategies of each player for a given price process. Section 4 provides the market equilibrium characterization by solving explicitly the coupled system of forward-backward SDE, and the martingale properties of the equilibrium price. Section 5 gives the description of the market equilibrium in the case of no production uncertainty while section 6 provides the result in the other case.

2 The equilibrium model

We consider an economy with power producers which can buy/sell energy on an intraday electricity market. Their purpose is to satisfy the demand of their customers at a given fixed time , minimizing trading costs.

2.1 Single agent optimal execution problem

Following [1], we formulate the optimization problem of a single agent in the economy on a finite time horizon . We begin introducing some notations.

Consider a complete probability space and a finite set of cardinality , where is a positive integer. We fix the following quantities at the initial time :

-

•

the initial demand forecasts of the agents ;

-

•

the initial production capacities ;

-

•

the initial net positions of the agents of sales/purchases of electricity in the intraday electricity market .

On we consider independent real-valued Brownian motions ,,, and independent continuous-time homogenous Markov chains ,, . We assume that and are independent. Moreover, every Markov chain is supposed to have finite state space , starting point at time : it represents the uncertainty over time on the production capacity of agent . We denote by the intensity matrix of . We also denote by the augmentation of the filtration generated by and . Finally, denotes the predictable -algebra on associated with .

The demand forecast of agent evolves on according to the equation

| (2.1) |

where , and is a decreasing function of time. In applications, we use the following form for

| (2.2) |

for some and . The volatility captures the main features of demand forecast error at the intraday time horizon: it decreases at the root of the time to maturity and may have a residual term , capturing the incompressible demand forecast errors (see for instance [23] and the references within for an overview of the field of short term electricity demand forecast). Further, the dynamics of takes into account the potential common dependence of realised demands to weather conditions. In order to satisfy the terminal demand , agent have the two following possibilities.

-

•

Power production. The agent can choose to product a quantity , facing at the terminal time the cost

(2.3) -

•

Trading in intraday electricity market. Let denote the agent net position of sales/purchases of electricity at time , delivered at the terminal date , which is given by

where , called the trading rate, is chosen by the agent.

We define an admissible pair of controls for each agent as a pair in , where

The expected total cost for agent is given by

| (2.4) |

where and are positive constants, while denotes the intraday electricity quoted price, which will be endogenously determined in the following class of processes:

the set of all -adapted processes such that

The agent’s optimisation problem consist in trading at minimal cost to achieve a given terminal target, taking into account the liquidity cost of her sales or purchases. We take potentialy different impact parameter per agent , capturing here the potential different liquidity cost faced by market players. In this sense, we deviate from Almgren and Chriss (2001) [2] and Aïd et. al. (2001) [1], in the sense that there is no permanent market impact in agent’s problem. Further, although in intraday electricity market, the same penalty cost is applied by the Transmission System Operator to any market player, we capture the idea that agents may have different appreciation of the cost of imbalances by using different imbalance cost parameter . Thus, each agent is characterised by her cost function with Markov chain , her valuation of imbalances , her liquidity access , her demand forecast error function and her correlation with the common noise .

The optimization problem of agent consists in minimizing the expected total cost (2.4) over all admissible pairs of controls in . In order to solve such an optimization problem, we begin noting that we can easily find the optimal for agent . As a matter of fact, in the expected total cost (2.4) the control appears only at the terminal time . Then, the optimal is a non-negative -measurable random variable minimizing the quantity

It is then easy to see that is given by

2.2 Auxiliary optimal execution problem

In the present section, inspired by [1], we consider a relaxed version of the optimization problem for agent , where the control is not constrained to be nonnegative, but it belongs to the set defined as

The optimization problem of agent now consists in minimizing the expected total cost (2.4) over all admissible pairs of controls in . From the expression of in (2.4), it is straightforward to see that the optimal control is given by:

Plugging into , we find (to alleviate notation, we still denote by the new expected total cost, that now depends only on the control )

| (2.5) |

In conclusion, the optimization problem of agent consists in minimizing (2.5) over all controls . Because of the presence of the stochastic process , we cannot solve such an optimization problem by means of the Bellman optimality principle, and, in particular, via PDE methods. For this reason, we rely on the martingale optimality principle, which can be implemented using only probabilistic techniques, based in particular on the theory of backward stochastic differential equations. More specifically, we solve the optimization problem of every agent finding optimal trading rates , which depend on the price process . Given the exogenous demands and production capacities , the equilibrium price is then obtained imposing the equilibrium condition

| (2.6) |

Remark 2.1

Despite the homogeneous description of market players, the market model above allows to take into account a diversity of agents like pure retailers, pure producers or pure traders. Pure retailers have uncertain terminal demand but no generation plant. They can be represented taking a constant Markov chain taking a large value . Pure producers have no demand to satisfy and are represented by the Markov chain of their generation cost. Finally, pure traders have neither a demand to satisfy nor generation asset, but only an initial inventory position.

3 Martingale optimality principle and optimal trading rates

The aim of this section is to find an optimal trading rate of agent for every fixed price process . In order to do it in the present non-Markovian framework (the non-Markovian feature is due to the presence of the process ), we consider a value process given by

| (3.1) |

for all , with , , satisfying suitable backward stochastic differential equations, namely (3.7), (3.13), (3.18) below. Then, the optimal trading rate is obtained using the martingale optimality principle, namely imposing that for such a the value process is a true martingale, while it has to be a submartingale for any other trading rate (for more details on the martingale optimality principle see items (i)-(ii)-(iii) in the proof of Theorem 3.6 below).

The present section is organized as follows. We firstly consider the three building blocks of formula (3.1), namely equations (3.7), (3.13), (3.18) (whose forms are chosen in order to satisfy the martingale/submartingale requirements of the value process) and prove an existence and uniqueness result for each of them. Then, exploiting the properties of the value process , we prove the main result of this section, namely Theorem 3.6.

3.1 Notations and preliminary results

First of all, we introduce some notations. We denote by the jump measure of the Markov chain , which is given by , where is the Dirac delta at . We also denote by the compensator of , which has the following form (see for instance Section 8.3 and, in particular, Theorem 8.4 in [9]):

In addition to the set previously defined, we introduce the following sets:

-

•

: the set of all bounded càdlàg -adapted processes on .

-

•

: the set of all càdlàg -adapted processes satisfying

. -

•

: the set of all -predictable processes satisfying .

-

•

: the set of all -measurable maps satisfying

Here denotes the Borel -algebra of , which turns out to be equal to the power set of , since is a finite subset of .

Construction of .

Let us construct the first building block of formula (3.1), namely . First of all, for every , consider the following system of (recall that the set has cardinality ) coupled ordinary differential equations of Riccati type on the time interval :

| (3.2) |

for every .

Lemma 3.1

For every , there exists a unique continuously differentiable solution to the system of equations (3.2). Moreover, every component of is non-negative on the entire interval .

Proof. For simplicity of notation, we fix and denote simply by . Notice that system (3.2) can be equivalently rewritten in forward form as follows:

| (3.3) |

with , for all . By the classical Picard-Lindelöf theorem (see for instance Theorem II.1.1 in [15]), it follows that there exists an interval on which system (3.2) admits a unique solution denoted by . Let us prove that such a solution can be extended to the entire interval , so that, in particular, is defined on .

According to standard extension theorems for ordinary differential equations (see for instance Corollary II.3.1 in [15]), it is enough to prove that the solution does not blow up in finite time. This holds true for system (3.3) as a consequence of the two following properties:

-

1)

every component of is non-negative on the entire interval ;

-

2)

the sum is bounded from above by a constant independent of .

We begin proving item 1). Define , with . We prove that every , , is strictly positive on and identically equal to zero on (in the case , every is strictly positive on the entire interval ). If there is nothing to prove. Therefore, suppose that , so that there exists such that . Since for every we have , then and, by continuity, every component is strictly positive on the interval . It remains to prove that every is identically equal to zero on . Using equation (3.3), this latter property follows if we prove that every is equal to zero at (as a matter of fact, if this is true, then from equation (3.3) we deduce that every remains at zero for all ). In order to prove that every is zero at , we proceed by contradiction and assume that there exists such that . Then, it follows from equation (3.3) that . This is in contradiction with the fact that is strictly positive on (which implies that ). This concludes the proof of item 1).

Let us now prove item 2). Taking the sum over in equation (3.3), we obtain

| (3.4) |

By Young’s inequality () we find

| (3.5) |

with

Plugging (3.5) into (3.4), we end up with

which concludes the proof of item 2).

By Lemma 3.1, we know that there exists a unique -solution to system (3.2). Then, define the stochastic process

| (3.6) |

As it will be proved in Proposition 3.2 below, solves the following backward stochastic differential equation on , driven by the Markov chain , with quadratic growth in the component :

| (3.7) |

for all , where

| (3.8) |

and

| (3.9) |

Proposition 3.2

Proof. Let be the pair given by (3.6) and (3.9). Notice that belongs to . As a matter of fact

and

where recall that is the cardinality of the set . It remains to prove that solves equation (3.7). Applying Itô’s formula to between and , we find

| (3.10) |

Now, since , equation (3.2) can be rewritten as follows

Therefore

| (3.11) |

On the other hand, we have

| (3.12) |

Hence, plugging (3.11) and (3.12) into (3.10), we obtain equation (3.7).

Construction of .

Let us construct the second ingredient of formula (3.1), namely , which will be denoted by to emphasize its dependence on . For every and any , consider the following linear backward stochastic differential equation on , driven by the Brownian motions and the Markov chains :

| (3.13) |

where

| (3.14) |

Notice that equation (3.13) has zero terminal condition at time : . We also observe that the generator depends linearly on the component and it is random (as it depends on and ). We now address the problem of existence and uniqueness of a solution to equation (3.13), for which we need the following martingale representation result.

Lemma 3.3

For every square-integrable real-valued -measurable random variable , there exist , , , such that

| (3.15) |

Proof. The result is standard and follows for instance from Example 2.1-(2) in [6]. For completeness, we report the main steps of the proof. Denote by (resp. ) the augmentation of the filtration generated by (resp. ). It is well-known that if is -measurable (resp. -measurable) then representation (3.15) holds; indeed, in this case representation (3.15) is such that (resp. and , ) are equal to zero.

It is then easy to see that representation (3.15) also holds for every of the form , with and , , being respectively -measurable and -measurable. The claim follows from the fact that the linear span of the random variables of the form is dense in (the space of square-integrable real-valued -measurable random variables).

Proposition 3.4

For every and any , the backward equation (3.13) admits a unique solution . Moreover, is given by

| (3.16) |

for all , where .

Proof. Existence. Fix , and define (to alleviate notation, we write rather than as is fixed throughout the proof; we adopt the same convention for all the other quantities involved in the proof)

Since is a square-integrable real-valued -measurable random variable, we can apply Lemma 3.3 from which we deduce the existence of , , , such that

| (3.17) |

Now, define as (the càdlàg version of)

Since , we see that . Moreover, taking the conditional expectation with respect to in (3.17), we obtain

Finally, we define as . Then, noting that

applying Itô’s formula to , we get

where

This proves that solves equation (3.13); moreover, since , it easy to see that such a solution belongs to .

Construction of .

Let us finally construct the third and last ingredient of formula (3.1), namely , which will be denoted by to emphasize its dependence on . For every and any , consider the following backward stochastic differential equation on , driven by the Brownian motions and the Markov chains :

| (3.18) |

where

| (3.19) |

Notice that equation (3.18) has zero terminal condition at time : .

Proposition 3.5

For every and any , the backward equation (3.18) admits a unique solution . Moreover, is given by

for all .

Proof. The result can be proved proceeding along the same lines as in the proof of Proposition 3.4, noting that the backward equation is still linear (in this case, the generator does not even depend on the unknowns).

3.2 Main result

We can finally state our main result, which provides the optimal trading rate of agent given a fixed price process .

Theorem 3.6

Proof. Concerning equation (3.20), notice that such an equation is deterministic with stochastic coefficients, so it can be solved pathwise. More precisely, (3.20) is a first-order linear ordinary differential equation (with stochastic coefficients), so that it admits a unique solution which can be written in explicit form. It is then clear that such a solution is continuous and -adapted, since all the coefficients are also -adapted.

It remains to prove items 1) and 2). To this end, fix and (to alleviate notation, in the sequel we do not explicitly report the dependence on ; so, for instance, we simply write instead of ). The admissibility of follows directly from its definition, using the integrability properties of , , , , . Let us now prove item 2). In order to prove the optimality of , we implement the martingale optimality principle. More precisely, we construct a family of processes , for every , satisfying the following properties:

-

(i)

for every , we have

-

(ii)

is a constant independent of .

-

(iii)

is a submartingale for all , and is a martingale when .

Notice that when is given by then , with satisfying (3.20). Suppose for a moment that we have already constructed a family of stochastic processes , , satisfying points (i)-(ii)-(iii). Then, observe that, for any , we have

which proves the optimality of . It remains to construct , , satisfying (i)-(ii)-(iii). Given , we take as in (3.1), namely

for all , with , , satisfying respectively (3.7), (3.13), (3.18).

From the definition of , it is clear that (i) holds. Moreover, since , , are independent of , we see that (ii) holds as well. It remains to prove item (iii). By Itô’s formula we obtain , where

It is easy to see that when the drift becomes zero. So, in particular, is a true martingale. In order to conclude the proof, we need to prove that in general we have , that is is a submartingale for any . To this end, it is useful to rewrite as a quadratic polynomial in the variable :

Since , is nonnegative for every value of if and only if the discriminant is nonpositive. Notice however that the discriminant cannot be strictly negative, otherwise this would give a contradiction to the fact that is zero. In conclusion, the discriminant has be identically equal to zero, namely

Rewriting it in terms of the variable , we find

Now, we see that , , (defined in (3.8), (3.14), (3.19), respectively) are such that the above equality is always satisfied, regardless of the value of . It follows that is nonnegative, which implies that is a submartingale and concludes the proof.

4 Equilibrium price

In the present section we use the explicit expression of in (3.21) together with the equilibrium condition (2.6) to find the equilibrium price process (Theorem 4.1). We also find the dynamics of the equilibrium price process (Theorem 4.2), and obtain notably the martingale property of the equilibrium price process.

Theorem 4.1

There exists a unique solution , with being a continuous process, , , , satisfying the following coupled forward-backward system of stochastic differential equations:

| (4.1) | |||||

| (4.2) | |||||

where

| (4.3) |

Moreover, coincides with of equation (3.20), while coincide with of equation (3.13). Finally, is the price process satisfying the equilibrium condition (2.6) with as in (3.21).

Proof. Existence and uniqueness for system (4.1)-(4.2) can be proved proceeding along the same lines as in the proof of Lemma 2.2 in [22], the only difference being that is a Poisson random measure in [22]. We also notice that, proceeding as in the proof of Proposition 3.1 in [22], we obtain the following estimate:

| (4.4) |

where is a positive constant depending only on , , , , , , , .

Finally, regarding the last part of the statement, it is easy to see that coincides with of equation (3.20), while coincide with of equation (3.13). Finally, it is also clear that is the equilibrium price process, as formula (4.3) follows directly from the equilibrium condition (2.6) and the definition of in (3.21).

Theorem 4.2

The equilibrium price process is a martingale. More precisely, the dynamics of is given by

| (4.5) | ||||

for all . Similarly, the optimal trading strategies are martingales.

Proof. Recall that

where , , , satisfy respectively equations (2.1), (3.7), (4.1), (4.2). Then, an application of Itô’s formula yields

with the martingale term as in (4.5) and

where recall that ( stands for )

| (4.6) | ||||

Hence, can be rewritten as

By the expression of in (4.6), we find

which proves that is a martingale. Finally, let us consider an optimal trading strategy . By formula (4.6), we have

with

where we used the fact that is a martingale. Then, we see that proceeding along the same lines as for we deduce that is a martingale.

We now provide a formula for the solution to the coupled forward-backward system of equations (4.1)-(4.2). To this end, the following formula (4.7) for the -component turns out to be particularly useful, especially in the case without jumps (as it will be shown in the next section). In the general case, formula (4.7) provides compact expressions for both the equilibrium price and the forward process, see formulae (4.13) and (4.14) of Proposition 4.3. In particular, formula (4.13) for the equilibrium price allows in turn to find a more explicit formula for the optimal trading rates in the case for every (see Corollary 4.4).

Proposition 4.3

The following formula holds (notice that , for every ):

| (4.7) |

for all , where is as in (4.3), with as in (4.9), denotes the transpose of the column vector with all entries equal to one, while , , , , are column vectors of dimension given by

| (4.8) |

with

| (4.9) | ||||

| (4.10) | ||||

| (4.11) |

Moreover, the matrices and are defined as

| (4.12) |

In addition, the equilibrium price is given by

| (4.13) |

Finally, (4.1) can be rewritten as follows:

| (4.14) |

with , where denotes the matrix with all entries equal to and

Proof. We split the proof into three steps.

Proof of formula (4.7). We begin recalling from (3.16) that is given by the following formula:

| (4.15) |

for all , where . Now, an application of Itô’s formula yields that the process is a martingale and, in particular, it holds that

As a consequence, recalling that the dynamics of is given by (4.5), we see that

| (4.16) |

where is given by (4.11). Hence, by the martingale property of and (4), we can rewrite formula (4) as follows

| (4.17) |

where and are given by (4.9) and (4.10), respectively. Using formula (4.3) for , we find

The latter can be written in matrix form as follows

| (4.18) |

where is the column vector of dimension given in (4.8). In order to solve for , we rewrite (4.18) as follows

| (4.19) |

where is the identity matrix. Hence, we can solve for if the matrix on the left-hand side of (4.19) is invertible. We now prove that this holds true and the inverse matrix of is given by

| (4.20) |

Let us first check that , so that (4.20) is well-defined. To this regard, notice that the -th element , which is given by formula (4.9), can also be written as follows

| (4.21) |

Let us prove equality (4.21). By the definition of , we have

Taking the conditional expectation with respect to , we find

By the martingale property of , we see that

| (4.22) |

from which (4.21) follows. Now, multiplying the above equality by and summing with respect to , we obtain

namely . Recalling from Proposition 3.2 that is non-negative and belongs to , we deduce that is a strictly positive real number. This shows that (4.20) is well-defined.

Let us now prove that the matrix on the right-hand side of (4.20) is the inverse matrix of . To this end, notice that

| (4.23) |

where we recall that , namely is the trace of the matrix . Then, by direct calculation, it is easy to see that

which shows the validity of (4.20). This allows us to solve for in (4.19), so that we obtain

By (4.23) and the property , valid for every , we find

Since and , this yields

Finally, noting that , we conclude that formula (4.7) holds.

Proof of formula (4.13). Rewriting (4.3) in matrix form, we obtain

Plugging formula (4.7) into the above equality, we find

Notice that , so that

which proves formula (4.13).

Proof of formula (4.14). We recall from Theorem 4.1 that solves the following ordinary differential equation with stochastic coefficients:

The latter can be written in matrix as follows:

Using the expressions of and in (4.7) and (4.13), respectively, we find

Noting that and (where we recall that denotes the matrix with all entries equal to ), we obtain

which corresponds to formula (4.14).

Using Proposition 4.3, it is possible to provide more precise results for the optimal trading rates and the equilibrium price, when agents have no systematic bias on their forecasts ().

Corollary 4.4

Proof. (i) When for every , the expression of in (4.7) reads (notice that the vector in (4.7) is equal to zero)

Similarly, the expression of in (4.13) becomes

Then, it holds that

| (4.26) |

Thus, by (5.1), (3.21), (4.26), the optimal trading rate at equilibrium can be written as (we denote )

which yields equality (4.24) recalling that .

5 The case without jumps

In the present section we focus on the case where there are no jumps, so that the terminal condition of is deterministic and given by , for some fixed . We also assume that for all , , meaning that market players have unbiaised forecasts of their terminal demand. In such a framework, solves the following backward equation:

Hence, is given by

| (5.1) |

In the present framework we can give more precise formulae, compared to Corollary 4.4, for the optimal trading rates and the equilibrium price when ; moreover, we can provide a formula for the volatility of the equilibrium price. For sake of notations, we write .

Corollary 5.1

Suppose that for every .

-

(i)

The equilibrium price is given by (recall that , so in particular )

(5.2) (5.3) and the optimal trading rate is given by

(5.4) -

(ii)

The dynamics of the equilibrium price writes

(5.5) -

(iii)

In particular, the volatility of the equilibrium price process is deterministic, and satisfies

(5.6) -

(iv)

Moreover, if , , , for every , then

(5.7) If in addition all players have the same cost functions, namely , for every , then the volatility of the equilibrium price is a decreasing function of time and it is given by

(5.8) where , for every .

Proof. Item (i). By formula (4.24), we have in the case without jumps ()

where we used that

Noting , we get

Thus, summing up all the trading rates, we find

| (5.9) |

with

| (5.10) |

Items (ii) and (iii). Using formula (5.2) and that the noise terms are only due to , we find

which corresponds to formula (5.5). From such a formula we immediately get (5.6).

Item (iv). Formula (5.7) is a direct consequence of (5.6). Finally, if all cost functions are identical, namely , for every , then by (5.7) we immediately get (5.8), which proves that the volatility is decreasing in .

Remark 5.2

-

(i)

The item (i) in Corollary 5.1 shows that the equilibrium price is a convex combination of the forecasted marginal cost to produce the quantity . The quantity is the best estimator an agent can have on the quantity she will have to produce at time . The weights of the convex combination are deterministic functions of time. Further, for any agent, the optimal trading strategy is simply to compare its forecasted marginal cost to the equilibrium price . If the forecasted marginal cost is higher (resp. lower) than , she buys (resp. sell).

-

(ii)

Using (5.2), we can rewrite as

The process is an uncontrolled process which is the fondamental price in the Almgren and Chriss [2] model of intraday trading. The factors reads as the permanent market impact of each agent. Note that if agents are identical, reduces to its fundamental component because of the market clearing condition.

-

(iii)

In the formula (5.6) of the volatility, the volatility functions of demand forecasts are supposed to be decreasing in time, reflecting the fact that closer to maturity market players know better their demand. If all the functions were non-increasing, it would result that the volatility would decrease, making the Samuelson’s effect not holding. But, the monotonicity of the functions are not obvious. Nevertheless, since the functions form a convex combination, it holds that:

As a consequence, it cannot hold that all the functions have the same monotonicity on the interval . If the market players are homogeneous (same cost , same penalisation of imbalances , same market access and same dependence to common noise ), all functions are constant equal to and the volatility reduces to:

In this homogeneous case, the monotonicity of the volatility function is fully determined by the monotonicity of the volatility of the demand forecasts. Apart from this limiting case, the monotonicity of depends on the heterogeneity of the agents.

As a consequence, if the demand forecasts have decreasing volatility (i.e. increasing quality), heterogeneity is a necessary condition for the Samuelson’s effect to hold.

-

(iv)

Under the assumptions for the validity of formula (5.8), we see that converges to zero as goes to infinity when , while the limit is strictly positive when . This result translates in the following remark: in a market with no production shocks, prices move because agents face a common economic factor.

-

(v)

Rewriting (5.2), it holds that

Hence, when there are no market frictions, i.e. all the are zero, all the functions are constant, and thus, the equilibrium price still exists.

| Type 1 | Type 2 | |

|---|---|---|

| Figure 1 (Left) | , , , | , , , |

| , . | , , . | |

| Figure 1 (Right) | , , , | , , , |

| , . | , . |

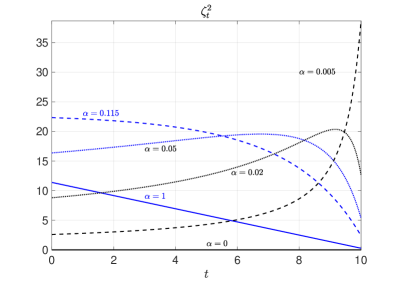

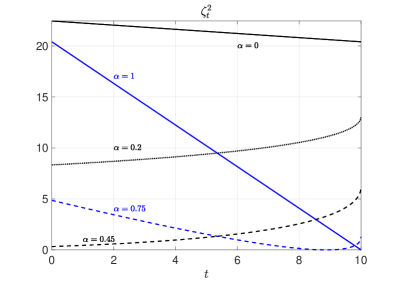

Numerical illustrations.

To illustrate how heterogeneity may induce rich behaviour of the price volatility, we consider the case of mixing two types of agents with characteristics given by Table 1. Parameters value do not pretend to have any significant meaning compared to an observed market and are only provided for illustration of a potential behaviour. We consider two cases. In the first one, agents are not affected by a common noise while in the second case, the first type of agent is positively affected by the common noise and the second case is negatively affected. Figure 1 (Left) illustrates the first situation and Figure 1 (Right) the second one. The fraction designates the proportion of agents of type 1.

In the first situation, we observe that when there are only agents of type 1, the volatility is decreasing. As we introduce more and more agents of type 2, the volatility is still decreasing but becomes concave (). Then, passed a certain threshold, the volatility is no longer monotonic and starts to increase. For a large amount of agents of type 2 (), the volatility is purely increasing. In the end, when there are only agents of type 2, the volatility is zero because .

In the second situation, the same phenomenon occurs but at a higher proportion of agents of type 2. As soon as there almost half agents of type 2, the volatility becomes increasing.

6 The case with jumps

In the present section we consider the case with jumps only and make the following assumptions.

-

a)

for every , the demand forecast is perfect and ;

-

b)

the set is made of two states ( stands for good and for bad), with ;

-

c)

for every , the Markov chain has state space , initial state at time and intensity matrix given by

where is a fixed strictly positive real number. In other words, each agent has an intensity rate to jump from the good state to the bad state and a zero intensity rate to jump from the bad state to the good state (so, in particular, if an agent is in the bad state, then she/he stays in the bad state);

In this framework, for every , the Riccati type system of equations (3.2) becomes

| (6.1) | ||||

| (6.2) |

We recall that the backward stochastic differential equation (3.7), driven by the Markov chain , is such that

| (6.3) |

In the case with jumps, (4.7) is not an explicit formula for , as a matter of fact the quantity depends on (see (4.10) and (4.11)) and therefore on itself. However, if then formula (4.7) becomes

Recalling estimate (4), we see that is bounded by a constant which is independent of . As a consequence, the quantities and appearing in formula (4.7) can be neglected for large enough, so, in particular, we obtain an approximate formula for which is explicit.

Differently, consider the case with only two players, so , moreover and . Under those assumptions, we are able to determine the equilibrium price process together with the optimal trading strategies.

Proposition 6.1

Suppose that assumptions a)-b)-c) stated at the beginning of this section hold true. Moreover, assume that , and .

Firstly, consider the following function of and , which is linear in :

| (6.4) | ||||

with , given by (6.3) and

Now, the process satisfying (4.1) is the solution to the following linear ordinary differential equation:

| (6.5) |

Moreover, the equilibrium price process is given by

| (6.6) |

Finally, the optimal trading strategies are as follows:

| (6.7) |

Proof. Since it follows that in (4.11) is identically zero, therefore is also equal to zero. Moreover, as , the equilibrium condition (2.6) gives , so that

| (6.8) |

As a consequence, by formula (4.7), for , we obtain

with as in (6.4). Now, by (4.17) we have

| (6.9) |

which corresponds to equality (6.6). Moreover, recalling formula (3.21), namely

we see that (6.7) holds true. It remains to prove that the process is the solution to equation (6.5). To this end, we recall from Theorem 4.1 that solves the following equation

Using relation (6.9), equality and also (6.8), we see that the above equation coincides exactly with equation (6.5).

Numerical illustration.

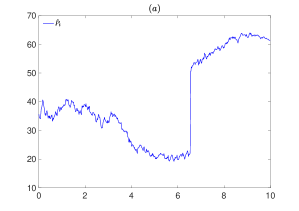

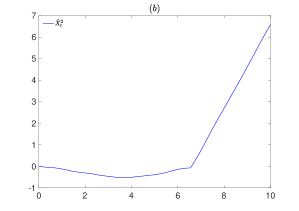

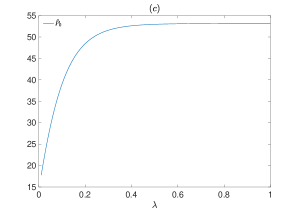

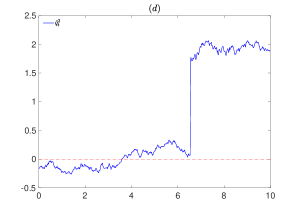

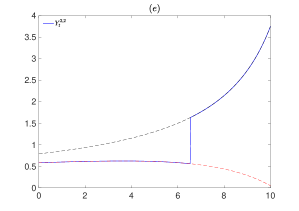

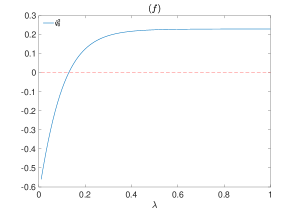

Figure 2 provides an illustration of the price behaviour for the case of Proposition 6.1. We took , , , and and , and . Simulation starts in the good state for agent 2. We observe that agent 2 starts by selling power (d) because her marginal cost is lower than the marginal cost of the other agent. And when the jump occurs, she moves to a buying position. The price immediatly jumps. We also observe on figures (c) that , the price at initial time, is an increasing function of the probability of jumps. The initial trading rate of agent 2, , is also an increasing function of the probability of jumps. For low values, it is negative (the agent sells power) and beyond a certain threshold, she becomes a buyer.

References

- [1] R. Aïd, P. Gruet, H. Pham. An optimal trading problem in intraday electricity markets. Mathematics and Financial Economics, 10(1):49–85, 2016.

- [2] R. Almgren, N. Chriss. Optimal execution of portfolio transactions. Journal of Risk 3:5–40, 2001.

- [3] R. W. Anderson, J. P. Danthine The time pattern of hedging and the volatility of futures prices. Review of Economic Studies, 50:249-266, 1983.

- [4] R. W. Anderson. Some determinants of the volatility of futures prices. Journal of Futures Markets, 5(3):331–341, 1985.

- [5] C. Balardy. An empirical analysis of the bid-ask spread in the german power continuous market. CEEM Working papers, #35, 2018.

- [6] D. Becherer. Bounded solutions to backward SDE’s with jumps for utility optimization and indifference hedging. Ann. Appl. Probab., 16(4):2027–2054, 2002.

- [7] H. Bessembinder, J. F. Coughenour, P. J. Seguin, M. M. Smoller. Is there a term structure of futures volatilities? Reevaluating the Samuelson hypothesis. Journal of Derivatives, 4(2):45–58, 1996.

- [8] H. Bessembinder, M.L. Lemon. Equilibrium Pricing and Optimal Hedging in Electricity Forward Markets. Journal of Finance, 57(3):1347–1382, 2002.

- [9] R. W. R. Darling, J. R. Norris. Differential equation approximations for Markov chains. Probability Surveys, 5:37–79, 2008.

- [10] L. Dong, H. Liu. Equilibrium forward contracts on nonstorable commodities in the presence of market power. Operations Research, 55(1):128–145, 2007.

- [11] P. Drobinski, M. Mougeot, D. Picard, R. Plougonven, P. Tankov. Renewable Energy: Forecasting and Risk Management. Springer Proceedings in Mathematics & Statistics, Mathematics of Planet Earth Collection, 2017.

- [12] I. Ekeland, D. Lautier, B. Villeneuve. Hedging pressure and speculation in commodity markets. Economic Theory 68(1):83–123, 2019.

- [13] O. Féron, P. Tankov, L. Tinsi. Price formation and optimal trading in intraday electricity markets. available on arxiv, arxiv:2009.04786, 2020.

- [14] S. Glas, R. Kiesel, S. Kolkmann, M. Kremer, N. Graf von Luckner, L. Ostmeier, K. Urban, C. Weber. Intraday renewable electricity trading: Advanced modeling and numerical optimal control. Journal of Mathematics in Industry, 10(3) :1–17, 2020.

- [15] P. Hartman. Ordinary differential equations. Volume 28 of Classics in Applied Mathematics, SIAM, Philadelphia, PA. Corrected reprint of the second (1982) edition, with a foreword by P. Bates, 2002.

- [16] A. Henriot. Market Design with Centralized Wind Power Management: Handling Low-Predictability in Intraday Markets.” The Energy Journal, 35(1):99–117, 2014.

- [17] H. Hong. A model of returns and trading in futures markets. Journal of Finance, 55(2):959–988, 2000.

- [18] E. Jaeck, D. Lautier. Volatility in electricity derivative markets: The Samuelson effect revisited. Energy Economics, 59:300-313, 2016.

- [19] R. Kiesel, F. Paraschiv. Econometric analysis of 15-minute intraday electricity prices. Energy Economics, 64:77-90, 2017.

- [20] M. Kremer, F. E. Benth, B. Felten, R. Kiesel. Volatility and Liquidity on High-frequency Electricity Futures Markets: Empirical Analysis and Stochastic Modeling. Int. J. of Theoretical and Applied Finance 23(4):1-30, 2020.

- [21] M. Kremer, R. Kiesel, F. Paraschiv. An Econometric Model for Intraday Electricity Trading. to appear in Philosophical Transactions of the Royal Society A, 2020.

- [22] J. Li, Q. Wei. estimates for fully coupled FBSDEs with jumps. Stochastic Processes and their Applications, 124(4):1582–1611, 2014.

- [23] R. Nedellec, J. Cugliari, Y. Goude GEFCom2012: Electric load forecasting and backcasting with semi-parametric models. International Journal of forecasting, 30(2):375–381, 2014.

- [24] R. Pindyck. The Dynamics of Commodity Spot and Futures Markets: A Primer. The Energy Journal, 22(3):1–129, 2001.

- [25] B. R. Routledge, D. J. Seppi, C. S. Spatt. Equilibrium forward curves for commodities. Journal of Finance, 55(3):1297–1338, 2000.

- [26] P. A. Samuelson. Proof that properly anticipated prices fluctuate ranndomly. Industrial Management Review, 6(2):41-49, 1965.

- [27] Z. Tan, P. Tankov. Optimal Trading Policies for Wind Energy Producer SIAM J. of Financial Mathematics, 9(1), 315–346, 2018.