Optimal Insurance under

Maxmin Expected Utility

Abstract.

We examine a problem of demand for insurance indemnification, when the insured is sensitive to ambiguity and behaves according to the Maxmin-Expected Utility model of Gilboa and Schmeidler [43], whereas the insurer is a (risk-averse or risk-neutral) Expected-Utility maximizer. We characterize optimal indemnity functions both with and without the customary ex ante no-sabotage requirement on feasible indemnities, and for both concave and linear utility functions for the two agents. This allows us to provide a unifying framework in which we examine the effects of the no-sabotage condition, marginal utility of wealth, belief heterogeneity, as well as ambiguity (multiplicity of priors) on the structure of optimal indemnity functions. In particular, we show how the singularity in beliefs leads to an optimal indemnity function that involves full insurance on an event to which the insurer assigns zero probability, while the decision maker assigns a positive probability. We examine several illustrative examples, and we provide numerical studies for the case of a Wasserstein and a Rényi ambiguity set.

Key words and phrases:

Optimal Insurance, Ambiguity, Multiple Priors, Maxmin-Expected Utility, Heterogeneous Beliefs.1. Introduction

A foundational, and by now folkloric problem in economic theory and the theory of risk exchange is the problem of demand for insurance indemnification. Specifically, an insurance buyer, or decision maker (DM), faces a random insurable loss, against which she seeks coverage through the purchase of an insurance policy. The price of this coverage is termed the policy premium, and the insurance pricing functional is called the premium principle. The premium principle is assumed to be known by the DM, and to be given by the certainty equivalent of the insurer’s utility. Although this is a classical problem, it has traditionally been confined to the accustomed framework of Expected-Utility Theory (EUT), going back to the pioneering work of Arrow [7, 8] and Mossin [57]. With the impetus of the von Neumann-Morgenstern [74] then newly minted theory of choice under uncertainty (the EUT), Arrow [7] shows the optimality of deductible insurance (a zero indemnification below a fixed threshold of loss, and a linear indemnification above) in an EUT framework, when the DM is risk-averse, the insurer is risk-neutral, and the two parties have the same beliefs about the underlying loss probability distribution. This foundational result has subsequently been extended in multiple directions. For instance, Raviv [62] proposes a bargaining approach where the insurer is risk-averse; Dana and Scarsini [28] introduce background risk of the DM, and Cummins and Mahul [27] study limited liability via an exogenous upper limit on the indemnity. Numerous other extensions and modifications of the classical insurance demand framework have been proposed, and we refer to Gollier [44] and Schlesinger [67] for surveys thereof.

Ambiguity in Insurance Demand

The vast majority of this literature remains within the confines of the classical EUT, an entirely objective Bayesian approach to decision-making under uncertainty. Yet, ever since the major challenges to the foundations of EUT that the work of Allais [4] and Ellsberg [34] has put forward, decision theory has been pulling away from parts of the axiomatic foundations of EUT, in favour of non-EU models that can rationalize behavior depicted by Allais [4] and Ellsberg [34], as well as other cognitive biases that are not captured by EUT. Arguably, one of the most important achievements of the modern theory of choice under uncertainty is the remarkable development spurred by the work of Ellsberg [34], in the study of what came to be known as ambiguity, or model uncertainty. Two main approaches to the rationalization of attitudes toward ambiguity have been explored in the literature on axiomatic decision theory: the non-additive prior approach, and the multiple additive priors approach. These two approaches do intersect, but they are not equivalent. The first category is based on the seminal contributions of Yaari [77] (Dual Theory, or DT), Quiggin [61] (Rank-Dependent Expected-Utility, or RDEU), and Schmeidler [68] (Choquet-Expected Utility, or CEU), which encompasses the previous two models. The second category was initiated by Gilboa and Schmeidler [43] (Maxmin-Expected Utility, or MEU) and further refined by Ghirardato et al. [40] (the -maxmin model), Klibanoff et al. [52] (the KMM model), and Amarante [5] who provides a unifying framework.

While the literature on non-EU preferences in risk-sharing or optimal insurance design problems is considerably thinner than the literature on risk-sharing with EU preferences, behavioral preferences, and ambiguity in particular play an increasing role in this literature. Yet, Machina [55] points out that the robustness of standard optimal insurance results under situations of ambiguity is still very much an open question, despite a growing literature on the topic. For instance, Bernard et al. [14] and Xu et al. [76] study RDEU preferences of the DM and risk-neutral EU preferences of the insurer, and they derive optimal insurance indemnities. Ghossoub [42] extends the analysis to account for more general premium principles. Also within the first category of ambiguity representation as a non-additive prior, Jeleva [50] considers the case of a DM who is a CEU-maximizer. In the second category of ambiguity representation as a collection of additive priors and an aggregation rule, Alary et al. [1] and Gollier [45] consider the case of an ambiguity-averse DM, in the sense of KMM. However, they consider a finite state space and restrict the set of priors to have a given parametric form.

Despite its appeal, for its ability to provide a separation of the effect of ambiguity aversion from that of risk aversion, as well as for its capability to define the notion of ambiguity neutrality, the KMM model, as a model of ambiguity with multiple priors, is arguably not as intuitive or popular as the MEU model of Gilboa and Schmeidler [43]. The MEU model gives rise to decision-making problems that can be embedded into to a larger class of model uncertainty problems, which lie at the core of the theory of distributionally robust optimization (DRO). In this framework, a decision-making problem is often modelled via a maxmin formulation: the agent is uncertain about the underlying model (prior), and therefore formulates an objective function using a collection of (additive) priors, also referred to as the ambiguity set. The agent then aims to maximize the objective under the worst-case model (e.g., Ben-Tal et al. [13]). However, the intuitiveness and wide popularity of the MEU model notwithstanding, there has surprisingly been no study of optimal insurance contracting when the DM is a MEU-maximizer, to the best of our knowledge. This paper fills this void. Specifically, we extend the classical setup and results in two ways: (i) the DM is endowed with MEU preferences; and (ii) the insurer is not necessarily risk-neutral (that is, the premium principle is not necessarily an expected-value premium principle). The main objective of this paper is to determine the shape of the optimal insurance indemnity when the DM is sensitive to ambiguity and behaves according to MEU.

This Paper’s Contribution

In the literature on optimal insurance contracting, a popular assumption is the no-sabotage condition, typically imposed as an ex ante condition of feasibility of insurance indemnities. This condition stipulates that the insured (ceded) risk and the retained risk are comonotonic (they are both nondecreasing functions of the underlying loss). Under the no-sabotage condition, the DM has no incentive to under-report the underlying loss, nor does the DM have an incentive to create incremental losses. This condition is also sometimes referred to as incentive compatibility, or a condition that avoids ex post moral hazard; and it is further studied by Huberman et al. [48] and Carlier and Dana [23]111We refer to Carlier and Dana [23] for a discussion of various notions of ex ante admissible contracts.. In this paper, we characterize optimal insurance contracts under MEU, both with and without the no-sabotage condition. In doing so, this paper sheds light on the consequences of the no-sabotage assumption on the construction of optimal insurance indemnities, in the presence of belief heterogeneity as well as multiple priors for the DM.

Our main results are the following. First, we examine in Section 3 the general case in which the insurer is a risk-averse EU-maximizer, and the DM is a MEU-maximizer with a concave utility function, displaying decreasing marginal utility of wealth. We provide an implicit characterization of optimal indemnity functions, both with and without the no-sabotage condition on feasible indemnities. Optimal indemnity functions can be formulated as a solution to an ordinary differential equation, which can then be easily solved numerically in practice.

Second, as a special case of the above setting, we examine in Section 4 the situation in which the insurer is risk-neutral, and hence the premium principle is an expected-value premium principle, as is commonly assumed in the literature (e.g., Bernard et al. [14] and Xu et al. [76]). In this case, we provide an explicit, closed-form characterization of optimal indemnity functions in the absence of the no-sabotage condition, and an implicit characterization in the presence of the no-sabotage condition. In particular, by doing so, we provide in both cases (with and without the no-sabotage condition) a crisp depiction of the effect of heterogeneity in beliefs between the two parties, showing how the singularity in beliefs leads to an optimal indemnity function that involves full insurance on an event to which the insurer assigns zero probability, but not the DM. This an important and intuitive feature of our optimal contracts in this case. We then illustrate these results with an example.

Third, as a further special case, we examine the situation in which both parties display constant marginal utility of wealth, that is, their utility functions are linear. We show that in this case, a particular type of layer insurance (also called tranching) is optimal if the no-sabotage condition is imposed, which we derive in closed form. Layer insurance contracts consist of a finite number of long and short positions on various stop-loss contracts of the underlying risk. If the no-sabotage condition is not imposed, the optimal indemnity makes use of a partition of the state space in three sets, providing no insurance for events in the first set, full insurance for events in the second set, and proportional insurance for events in the third set. Artzner et al. [9] (and Delbaen [31]) show that the class of MEU preferences with linear utility is related to the class of coherent risk measures. Therefore, our analysis can be used to derive optimal insurance contracts when the DM is endowed with a general coherent risk measure. To the best of our knowledge, this has not been studied in the literature when the DM and seller have heterogeneous beliefs regarding the underlying probability distribution.222This is studied by Birghila and Pflug [16] in the context of homogeneous beliefs regarding the underlying probability distribution. Layer indemnity contracts play an important role in insurance, as deductible or truncated deductible contracts are important examples thereof. Truncated deductibles or layer-type insurance indemnities are indeed commonly observed in reinsurance markets, where tranches of aggregate losses of the insurer are ceded to a reinsurer (e.g., Albrecher et al. [2]).

Lastly, we examine in Section 5 some numerical examples to illustrate our results. By specifying the structure of the DM’s ambiguity set , we are able to obtain explicitly the worst-case probability measure for the problems analyzed in Sections 3 and 4. In particular, we examine the special case in which the DM’s set of priors forms a neighborhood around the insurer’s probability measure. First, when the insured is risk-averse, is a Wasserstein ambiguity set, and the insurer is risk-neutral, we are able to characterize the saddle point of the problem in Section 4. In this case, the optimal indemnity is a deductible contract, while the worst-case measure dominates the insurer’s probability measure in the sense of first-order stochastic dominance. In the second example, we consider a general setting in which both participants are risk-averse, and is the Rényi ambiguity set. In a discretized framework, we use a successive convex programming algorithm to solve the ordinary differential equation in Section 3. We then assess the influence of the ambiguity set on the optimal value. In particular, we show numerically that a larger ambiguity set yields a lower certainty equivalent of final wealth for the DM, but increases the willingness-to-pay for insurance. Moreover, for both examples, the impact of the no-sabotage condition on the feasible set of insurance indemnities is illustrated.

Other Related Literature

This paper contributes to the literature on heterogeneity in beliefs between the DM and the insurer. Heterogeneity in beliefs has been studied recently in the context of optimal (re)insurance by Ghossoub [41], Boonen and Ghossoub [18, 19], and Chi [25]. All of these studies focus on unambiguous subjective preferences on the side of the DM (that is, a unique subjective prior on the state space), but they differ in the formulation of the objective function that is optimized.

Heterogeneous beliefs can arise for different reasons. For instance, in the Subjective Expected Utility (SEU) theory of De Finetti [29] and Savage [65], disagreements about (subjective) beliefs are a result of differences in preferences over alternatives. Moreover, in epistemic game theory, the celebrated Agreement Theorem of Aumann [11] states that if agents have common priors, then the Harsányi Doctrine holds, that is, disagreements about probabilities result only from information asymmetry. Furthermore, disagreement about (posterior) beliefs can be a direct consequence of relaxing the controversial and heavily criticized common priors assumption (e.g., [12, 46, 56]).

On a practical level, an insurance buyer may have private information about the distribution of the insurable loss. The insurer may use another probability measure, based on an average historical distribution of losses in the insurer’s portfolio over a relevant time frame. For instance, the price of insurance may seem low for insurance buyers facing relatively high risks. This observation forms the basis of adverse selection in insurance markets (e.g., [26, 36]). Jeleva and Villeneuve [51] study heterogeneous beliefs in an adverse selection model in an insurance market with two future states of the world. Moreover, heterogeneity in reference probabilities may also be driven by ambiguity on the side of the insurer, rather than the insurance buyer (e.g., [6, 47]). More precisely, the insurer may experience ambiguity about the underlying probability distribution, and hence use a pricing rule that would be deemed more prudent than one based on the probability distribution used by the insurance buyer.

By explicitly incorporating model uncertainty into the problem formulation via a set of priors , the present paper also falls within the DRO framework. In this perspective, insurance contracts can be seen as saddle points of a DRO problem. The benefit of this technique is twofold. First, the worst-case approach ensures that the optimal decision is not sensitive to possible model misspecification. Second, in many situations, there exist tractable reformulations or algorithms to solve these distributionally robust models, even when the corresponding non-ambiguous problem (that is, when there is a unique prior) cannot be efficiently solved. The idea of incorporating multiple models in the decision-making process dates back to the fundamental work of Scarf [66] in the inventory management applications. He considers a robust formulation of the newsvendor problem, where the optimal strategy is constructed over all possible demand functions with known mean and variance. This initial idea is further developed in the work of Ben-Tal et al. [13] and Bertsimas and Sim [15], among others. A key concept in DRO is the structure of the set of priors, known here as the ambiguity set. Clearly, the choice of the ambiguity set influences the worst-case model, and thus the optimal decision, while it also facilitates a tractable reformulation and efficient algorithm implementation. The existing literature has focused so far on two types of ambiguity sets: those built using the moment-based approach (e.g., [30, 66, 78]), and those built using the statistical distance-based approach (such as the Kullback-Leibler divergence in [22], the -ball in [70], or the Wasserstein distance in [35]). Each such choice comes with useful structural properties, but also with shortcomings that need to be dealt with. Ultimately, it is the available set of observations and the type of application that would dictate a suitable choice of .

The rest of the paper is organized as follows. Section 2 presents the setup of our problem together with the necessary background. In Section 3, we consider the case in which both the insurer and DM have concave utility functions, and the DM is a MEU-maximizer. We characterize optimal indemnity functions both in the presence and absence of the no-sabotage condition. Section 4 considers the particular case of a risk-neutral insurer, and provides some illustrating examples. Section 5 reports numerical illustrations, and Section 6 concludes the paper. Some definitions and technical proofs are provided in Appendices A to D.

2. Setup and preliminaries

Let be a nonempty collection of states of the world, and equip with a -algebra of events. A DM is facing an insurable state-contingent loss represented by a random variable on the measurable space , with values in the interval , for some . We denote by the sub--algebra of on generated by the random variable .

Let denote the vector space of all bounded, -valued, and -measurable functions on , and let be its positive cone. When endowed with the supnorm , is a Banach space (e.g., [33, IV.5.1]). By Doob’s measurability theorem [3, Theorem 4.41], for any there exists a bounded, Borel-measurable map such that . Moreover, if and only if the function is nonnegative.

Definition 2.1.

Two functions are said to be comonotonic (resp., anti-comonotonic) if

For instance any is comonotonic and anti-comonotonic with any . Moreover, if , and if is of the form , for some Borel-measurable function , then is comonotonic (resp., anti-comonotonic) with if and only if the function is nondecreasing (resp., nonincreasing).

Let denote the linear space of all bounded finitely additive set functions on , endowed with the usual mixing operations. When endowed with the total variation norm , is a Banach space. By a classical result (e.g., [33, IV.5.1]), is isometrically isomorphic to the norm-dual of , via the duality . Consequently, we can endow with the weak∗ topology .

Let denote the collection of all countably additive elements of , and let denote its positive cone. Then is a -closed linear subspace of . Hence, is -complete, i.e. is a Banach space. Denote by

the collection of probability measures on . We shall endow with the weak∗ topology inherited from .

For any and , let denote the cumulative distribution function (cdf) of with respect to the probability measure , and let denote the left-continuous inverse of the (i.e., the quantile function of ), defined by

2.1. The DM’s and the Insurer’s Preferences

The DM can purchase insurance against the random loss in a perfectly competitive insurance market, for a premium set by the insurer. In return for the premium payment, the DM is promised an indemnification against the realizations of . An indemnity function is a random variable on , for some bounded, Borel-measurable map , which pays off the amount in state of world , corresponding to a realization of . That is, we can identify the set of indemnity functions with a subset of . For each indemnity function , we define the corresponding retention function by . As the name suggests, is the retained loss after insurance indemnification.

The DM has a preference relation over insurance indemnification functions (or over wealth profiles) that admits a MEU representation as in Gilboa and Schmeidler [43], of the form

| (2.1) |

where is a concave utility function, and is a (unique) weak∗-compact and convex subset of . Moreover, we assume that the DM’s preferences satisfy the Arrow-Villegas Monotone Continuity axiom as in Chateauneuf et al. [24], so that , i.e., all priors are countably additive. Additionally, the DM’s utility function satisfies the following assumption.

Assumption 1.

The utility function is strictly increasing, concave and continuously differentiable.

Let be the DM’s initial wealth. After purchasing insurance coverage for a premium , the DM’s terminal wealth is a random variable given by

The insurer’s preference over admits an EU representation of the form

for a utility function satisfying Assumption 1 and a probability measure .

The insurer has an initial wealth , and faces an administration cost, often called an indemnification cost, associated with the handling of an indemnity payment. As customary in the literature (e.g., Bernard et al. [14] and Xu et al. [76]), we assume that for a given indemnity function , this indemnification cost is a proportional cost of the form , for a given safety loading factor specified exogenously and a priori. Hence, the insurer’s terminal wealth is the random variable given by

2.2. Admissible Indemnity Functions

In Arrow’s [7] original formulation of the optimal insurance problem under EUT, an ex ante condition of feasibility of indemnity schedules is the requirement that these be nonnegative and no larger than the realization of the loss in each state of the world. This is often referred to as the indemnity principle, and it translates into the requirement that an admissible set of indemnities be restricted to those that satisfy . We shall denote this set of indemnity functions by :

| (2.2) |

A desirable property of optimal indemnities is that an indemnity function and the corresponding retention function be both nondecreasing functions of the loss , that is both comonotonic with (and hence and are comonotonic). Indeed, if fails to be comonotonic with , then the DM has an incentive to under-report the loss; whereas if fails to be comonotonic with , then the DM has an incentive to create additional damage. These situations of ex post moral hazard are not desirable, and one often seeks additional ex ante conditions that would rule out such behavior from the DM. In the setting of Arrow [7], the optimal indemnity is a deductible contract of the form , for some . For such contracts, both the indemnity and retention functions are comonotonic with the loss, and optimal indemnities are de facto immune to the kind of ex post moral hazard described above. However, outside of EUT, optimality of deductible contracts does not always hold, and optimal indemnities might suffer from the aforementioned type of moral hazard, as in Bernard et al. [14].

In order to rule out ex post moral hazard that might arise from a misreporting of the loss by the DM, an additional condition is often imposed ex ante on the set of feasible indemnity schedules (as in Xu et al. [76]). Such a condition is called the no-sabotage condition, and it stipulates that admissible indemnity functions and the corresponding retention functions be comonotonic, hence resulting in the feasibility set given by:

Since is of the form , with for all , we can write as

| (2.3) |

The no-sabotage condition is also sometimes referred to as incentive compatibility by Xu et al. [76], and it is further studied by Huberman et al. [48] and Carlier and Dana [23]. The latter discuss various classes of ex ante admissible contracts, as well as their implications of optimal indemnities.

Remark 2.2.

Let denote the set of all continuous functions on (and hence bounded), equipped with the supnorm . Note that is a uniformly bounded subset of consisting of Lipschitz-continuous functions , with common Lipschitz constant . Therefore, is equicontinuous, and hence compact by the Arzelà-Ascoli theorem (e.g., [33, Theorem IV.6.7]).

In this paper, we will characterize optimal indemnity functions, both with and without the no-sabotage condition, in order to examine the impact of such an ex ante requirement on feasible indemnity schedules. This will first be done in the general setting of a MEU-maximizing DM with a concave utility and an EU-maximizing insurer with concave utility (Section 3), and then in a setting where the insurer is risk-neutral (hence uses an expected-value premium principle).

3. Optimal Indemnity Functions

In this section, we investigate the DM’s problem of demand for insurance indemnification, when the DM is ambiguity-sensitive and has preferences admitting a MEU representation of the form given in eq. (2.1), whereas the insurer is a risk-averse EU-maximizer with a concave utility function . We first examine in Section 3.1 the class of indemnities that are nonnegative and cannot exceed the loss (as defined in eq. (2.2)), and we provide in Theorem 3.2 a closed-form characterization of the optimal indemnity in this case. We then consider in Section 3.2 the class of indemnities that are such that both indemnity and retention functions are nondecreasing functions of the loss (as defined in eq. (2.3)). In that case, Theorem 3.4 provides an implicit characterization of the optimal indemnity function.

Let denote the set of admissible indemnity functions, which could be either the set defined in eq. (2.2), or the set defined in eq. (2.3). For a given insurance budget and a compact and convex set of probability measures, the optimal indemnity function is obtained as the solution of the problem

| () |

where is a given safety loading factor. The constraint in () is interpreted as the insurer’s participation constraint.333All of this paper’s results can be derived for any participation constraint of the form , with . To maintain a direct economic interpretation, we choose throughout the paper , i.e., the insurer’s reservation utility. Observe that , for all and all , and thus Problem () is finite.

Remark 3.1.

By the Lebesgue Decomposition Theorem, for any there are finite nonnegative countably additive measures and on such that , where and . Hence, for each , there exists some and such that and . In particular, since is -measurable, there exists a nonnegative Borel measurable function such that .

3.1. Without the No-Sabotage Condition

Theorem 3.2.

Suppose that the utility functions and satisfy Assumption 1 and are, in addition, strictly concave and such that and .444The limit conditions on and are the customary Inada [49] conditions, often encountered in the literature. Let as defined in eq. (2.2) be the set of admissible indemnity functions. Then there exists such that an optimal solution of Problem () is of the form:

| (3.1) |

where

-

(a)

is such that , with ;

-

(b)

is such that ;

-

(c)

;

-

(d)

and are of the form:

-

Case 1.

If , then and , where solves

-

Case 2.

If , then and solves

-

Case 1.

-

(e)

is such that .

Proof.

Define the set . Observe that for , and , we have and

and thus the set is convex. Moreover, the objective function in () is continuous and concave in and continuous and linear in , while is weak∗-compact and convex set. Hence the Sion’s Minimax Theorem states that there exists a saddle point such that

For , to characterize the optimal indemnity , we focus on the following inner problem:

| (3.2) | ||||||

| s.t. |

Problem (3.2) is a convex optimization problem, since the constraint can be equivalently written as , where is a convex utility function. For , let and be as in Remark 3.1, and consider the following two problems:

| (3.3) |

| (3.4) |

Observe that is a feasible solution for Problem (3.3) and it holds that

for any feasible solution for Problem (3.3). Hence is optimal for (3.3).

Now, let be an optimal solution for Problem (3.4). We claim that is optimal for Problem (3.2). To see this, we remark that

where the last inequality follows from the feasibility of for (3.4). Hence is feasible for Problem (3.2). The optimality of is then derived similar to [41, Lemma C.6].

Next, we focus on the optimal indemnity that solves Problem (3.4). The associated Lagrange function is

where is the Lagrange multiplier. As the domain of is convex and is continuous and concave in and linear in , the strong duality holds, i.e.,

where the optimal value of Problem (3.4) is finite, since () is finite. For fixed , a necessary and sufficient condition for to be the optimal solution of Problem (3.4) is

| (3.5) |

By direct computation, (3.5) becomes

| (3.6) |

Define the following sets, depending on Lagrange multiplier :

First, observe that on and , condition (3.6) holds for all only if

| (3.7) |

Next, define the set . To obtain the structure of in (3.4), we distinguish the following cases, depending on .

- Case 3.2.1.

-

Case 3.2.2.

If , then and , for all . Thus , for any feasible .

The indemnity , depending on , is the optimal solution of Problem (3.4) if there exists some such that . To see this, define the constant , for some large . Then for any , we obtain

It follows that , a contradiction; hence the feasible set of reduces to the compact interval and the strong duality of Problem (3.4) yields

where . ∎

Note that the optimal indemnity in eq. (3.1) provides full insurance over the event , whenever the DM’s worst-case measure is such that . Note also that on the event , satisfies an ordinary differential equation for which an analytical expression is difficult to provide in general. However, for particular choices of , we can obtain numerically the structure of , as well as (see Example 5.3 in Section 5).

3.2. With the No-Sabotage Condition

Next we analyze the case when the set of Problem () is restricted to the set of indemnities satisfying the no-sabotage condition. In this case the feasibility set becomes:

| (3.9) |

Remark 3.3.

Since is a compact subset of the space (see Remark 2.2), and is a closed subset of , it follows that is compact.

Theorem 3.4.

Suppose that the utility functions and satisfy Assumption 1. Let as defined in eq. (2.3) be the set of admissible indemnity functions. Then there exists such that the optimal solution of Problem () is , -a.s. and is of the form

where

-

(a)

is such that , with ;

-

(b)

is such that ;

-

(c)

is a Borel measurable function such that ;

-

(d)

, where , and

for some Lebesgue measurable and -valued function ;

-

(e)

is such that .

Proof.

Similar to Theorem 3.2, there exists a saddle point such that

| (3.10) |

where given in eq. (3.9) is compact (see Remark 3.3). For , the inner optimization problem in (3.10) becomes:

| s.t. |

where and , depending on , are defined in Remark 3.1. Similar to Theorem 3.2, the optimal indemnity function can be obtained as , where solves Problem (3.11) below.

| (3.11) |

The Lagrange function of Problem (3.11) is

where is the Lagrange multiplier. By strong duality, for fixed , a necessary and sufficient condition for to be the optimal solution of Problem (3.11) is

| (3.12) |

Since , we can extend the domain of the integral above in (3.12) over . By direct computation, (3.12) becomes: for all ,

| (3.13) |

As any is absolutely continuous, it is almost everywhere differentiable on , and hence (3.13) becomes

for all ; hence is of the form:

where and is some Lebesgue measurable and -valued function. The existence of the Lagrange multiplier that guarantees the existence of the solution follows similar to Theorem 3.2. ∎

Theorem 3.4 above provides a general characterization of the optimal solution of Problem (), when the set of admissible indemnity functions is given by . The exact structure of the optimal indemnity may be difficult to interpret, due to its implicit form. However, under the (more common) assumption of risk-neutrality of the insurer, closed-form solutions for can be obtained, as seen in the next section.

4. The case of a Risk-Neutral Insurer

In this section, we examine the case of a risk-neutral insurer, that is, when the utility function is linear. We first consider in Section 4.1 the subcase in which the DM’s utility function is concave, and characterize the optimal indemnity both without and with the no-sabotage condition. In the former case, we obtain a closed-form characterization of the optimal indemnity (Proposition 4.1), whereas in the latter case, the optimal indemnity is determined implicitly (Proposition 4.3). The results are illustrated in Example 4.4 for a specific ambiguity set , and closed-form solutions are obtained. We then examine in Section 4.2 the subcase in which the DM’s utility function is linear. In that case, we also characterize the optimal indemnity both with and without the no-sabotage condition, and then provide two illustrative examples.

4.1. The Case of a Concave Utility for the DM

| () |

If , then we can eliminate the constraint in Problem (), as the DM’s budget is large enough. In this case, the optimal indemnity is -a.s. In the following, we assume that .

4.1.1. Without the No-Sabotage Condition

Proposition 4.1.

Suppose that the utility function satisfies Assumption 1 and is, in addition, strictly concave and such that and . Let as defined in eq. (2.2) be the set of admissible indemnity functions. Then there exists such that an optimal solution of Problem () is of the form:

| (4.1) |

where

-

(a)

is such that , with ;

-

(b)

is such that ;

-

(c)

;

-

(d)

and are given by:

-

Case 1.

If , then and , -a.s., where is such that ;

-

Case 2.

If , then , -a.s. and , where is defined as .

Proof.

Letting be the retention random variables, Problem () becomes

| (4.2) | ||||||

| s.t. |

where . For fixed , define the convex set . Problem (4.2) fulfills the conditions of Sion’s Minimax Theorem, and thus there exists some and such that

For , the inner problem becomes:

| (4.3) | ||||||

| s.t. |

where and are defined in Remark 3.1. Based on the splitting technique in [41, Lemma C.6], the optimal retention function can be obtained as , where solves Problem (4.4) below.

| (4.4) |

Following the proof of Theorem 3.2, for a fixed , a necessary and sufficient condition for to be the optimal solution of Problem (4.4) is

| (4.5) |

Next, we define the following sets, depending on Lagrange multiplier :

Clearly, condition (4.5) holds for all only if

| (4.6) |

Next, define the set . To characterize in (4.4), we consider the following cases:

-

Case 4.1.1.

If , then and thus . On , satisfies the following condition:

By equation (4.6) and strict monotonicity of , the first order condition yields:

(4.7) which depends on the state of the world only through and .

-

Case 4.1.2.

If , then and , for all . Moreover, in this case, ; otherwise, , -a.s., leading to a contradiction, since . Thus, according to (4.6), , for any feasible .

The retention is the optimal solution of Problem (4.4) if there exists some such that . We will denote this as , to emphasize the dependence on . Now define the function , . Since is continuous in , and , by Lebesgue Dominated Convergence Theorem, it follows that is continuous in . Moreover, is a nondecreasing function of and satisfies , for some and . If , there exists some such that . Otherwise, .

4.1.2. With the No-Sabotage Condition

The following result characterizes the optimal indemnity , when the no-sabotage condition is enforced.

Proposition 4.3.

Suppose that the utility function satisfies Assumption 1 and let as defined in eq. (2.3) be the set of admissible indemnity functions. Then there exists such that the optimal solution of Problem () is , -a.s. and is of the form

where

-

(a)

is such that , with ;

-

(b)

is such that ;

-

(c)

is a Borel measurable function such that ;

-

(d)

, where , and

for some Lebesgue measurable and -valued function ;

-

(e)

is such that .

4.1.3. Example

The following example analyzes the structure of the optimal and in Propositions (4.1) and (4.3), respectively, when all probability measures in are absolutely continuous with respect to , with a particular structure of the Radon-Nikodým derivatives. This is done both with and without the no-sabotage condition. Specifically, we assume that each is such that with

| (4.8) |

for some nonnegative and increasing weight function satisfying . Such measure transformations have a long tradition in insurance pricing, dating back to the Esscher transform (e.g., Bühlmann [21]), in which the function takes the form , for a given . More generally, Furman and Zitikis [37, 38, 39] discuss the general class of weighted premium principles where pricing is done via measure transformations as in eq. (4.8).

Suppose that the utility function satisfies Assumption 1, and assume that insurer’s probability measure has a continuous cdf over .

Example 4.4.

Let the DM’s ambiguity set be defined as follows:

where is a collection of nonnegative increasing weight functions, such that for all . Appendix B provides conditions under which the set is convex and weak∗-compact.

First we analyze the case when the feasible set of indemnities is , as defined in eq. (2.2). By definition of , any optimal is absolutely continuous with respect to . Moreover, by monotonicity of , there exists some such that , for and , for , i.e., the set in Proposition 4.1 is precisely .

Next, let , as defined in eq. (2.3). Following the setting of Proposition 4.3, the utility need not to be strictly concave, but only concave. According to Proposition 4.3, the optimal retention can be equivalently written as

Observe that the function , is a continuous, decreasing function, as it is the product of two decreasing functions. We distinguish the following cases:

-

Case 1.

If , then , for all , and thus .

-

Case 2.

If , then , for all , and thus .

-

Case 3.

If , then there exists some such that , for all and , for all . This implies that for all , , and thus , for . Moreover, for , it holds that

Therefore, there exists some such that for all ,

Therefore, for all , and , for all . In this case, and thus .

4.2. The Case of a Linear Utility for the DM

In this section we assume that the utility functions of both the DM and the insurer are linear. Proposition 4.5 characterizes the optimal indemnity in the absence of the no-sabotage condition. If the admissible set of indemnities is , then using the results of Proposition 4.3, we obtain a closed-form expression for the optimal indemnity in the presence of the no-sabotage condition, namely, a layer-type insurance indemnity. The section ends with two examples of the ambiguity set , for which we derive each time the optimal insurance contract.

| () |

where is the retention function and . Clearly, if , then , -a.s., and so we focus on the case .

4.2.1. Without the No-Sabotage Condition

Proposition 4.5.

Let as defined in eq. (2.2) be the set of admissible indemnity functions. Then there exists such that an optimal solution of Problem () is of the form:

where

-

(a)

is such that , with ;

-

(b)

is such that ;

-

(c)

is given by:

-

Case 1.

If , then , i.e., can be written as

where

-

(i)

;

-

(ii)

;

-

(iii)

;

-

(iv)

is such that ;

-

(v)

-

(i)

-

Case 2.

If , then , i.e., can be written as

where .

-

Case 1.

Proof.

The proof is similar to the proof of Proposition 4.1, in the case . According to (4.3), there exists some such that for and as in Remark 3.1, is the optimal solution of the following problem:

According to [41, Lemma C.6], the optimal retention is of the form , where solves the problem below.

As both the objective function and the constraint are linear in , a sufficient condition for to be optimal is that it minimizes pointwisely the integrand of the associated Lagrange function:

where is the Lagrange multiplier. To obtain the structure of optimal , depending on , we consider again the following sets:

It is clear that and . Next, let . We distinguish the following cases:

-

Case 4.5.1.

If , then and the corresponding retention is , for some arbitrary .

-

Case 4.5.2.

If , then and , for some arbitrary . Observe that in this case , otherwise , a contradiction.

Similar to Proposition 4.1, there exists such that the slackness condition below holds:

| (4.9) |

Now, based on the optimal value of , one can specify a choice of and , respectively, and thus characterize an optimal . To see this, let , for a Borel measurable function such that . If , then and the corresponding retention becomes , for some . Otherwise, and , for some .

If , then and an optimal retention in this case is , where the constant is defined as

Note that , since , according to eq. (4.9). If , and one can choose , where . ∎

4.2.2. With the No-Sabotage Condition

In this section, we assume that is nonatomic, i.e., is a continuous random variable for .

If the set of admissible indemnities is such that the indemnity and the retention function are increasing function of the loss, then according to Proposition 4.3, the optimal retention is such that:

| (4.10) |

where , for any , and is a Lebesgue measurable and -valued function. Let and be the smallest and the largest value in , respectively. Moreover, let and . As , then , for all , i.e., .

If is not connected, then using the notations above, we can extend the definition of the set over as follows: if such that , then . Observe that , for , with .

Next, we proceed by considering the following cases:

-

Case 1.

If , then , for all , and , for all . Hence,

for some Lebesgue measurable function. In particular, if is chosen as , then , -a.s.

-

Case 2.

If , then for all , it holds that

In this case, let . If no such exists, then , for all , i.e., , -a.s. Otherwise,

where is a Lebesgue measurable function. Similar to the previous case, one can choose and thus , -a.s.

-

Case 3.

If , define the function ,

Let . Since the set of discontinuities of is at most countable, it follows that

is the set of disjoints intervals such that is continuous. The functions can be extended over a compact interval by taking and . Then for each , , the procedure is as follows: we construct a piecewise linear underestimator and a piecewise linear overestimator of over , which allows us to determine the sign of ; this sign, in turn, gives the marginal retention function corresponding to , according to eq. (4.10). The optimal is thus of the form

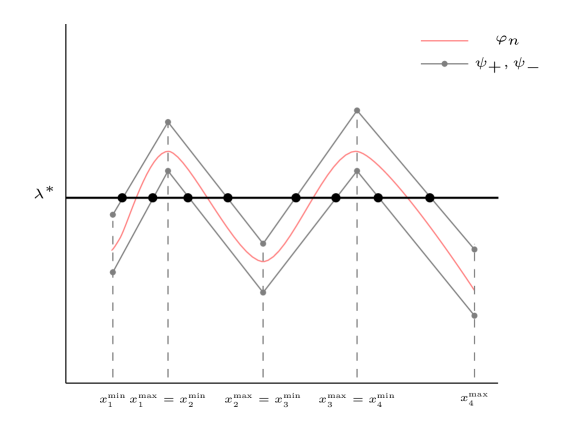

Fix and consider . For a small enough , let be a -underestimator and -overestimator of , respectively and let , and be their associated systems, as defined in Appendix C, for , and a system of breakpoints for . Figure 1 illustrates the -underestimator and -overestimator for some function . According to eq. (4.10), the marginal retention function switches from to , depending on the sign of , for all . We observe that if there exists some such that

(4.11) then there exists some such that . The structure of is determined by a case-by-case analysis, depending on the slope of both -underestimator and -overestimator:

-

Subcase 1.

If , then , for and , for . In Figure 1 the situation is depicted for instance over the segment , when and , for and , .

-

Subcase 2.

If , then , for and , for . This is the case over in Figure 1 , when and , for and , .

-

Subcase 3.

If , is parallel with -axis over . In this case, we only need to check the relation between and : if , then , while if , then , for all . Otherwise, if , then (. In particular, can be chosen to be over this interval.

Figure 1. -underestimator and - overestimator of . It follows that the optimal retention function on is of the form: for each and ,

-

Subcase 1.

Remark 4.6 (Coherent Risk Measures).

Since and since the location of the minimum is not affected by adding and subtracting constants to the objective function in Problem (), Problem () can readily be reformulated as follows:

| () |

Now, by Artzner et al. [9] and Delbaen [31], the expression is equivalent to a coherent risk measure of the random gain . Hence, Problem () can be seen as the objective to minimize a coherent risk measure of final wealth under a premium budget constraint.

4.2.3. Examples

For the following examples, we assume that is a continuous random variable for .

Example 4.7.

In this example, we consider again the ambiguity set in Example 4.4, i.e.,

where is defined in Example 4.4.

First we analyze the case when , as defined in eq. (2.2). Observe that the worst-case measure satisfies . Based on the same argument as in Example 4.4, the set in Proposition 4.5 is , for some . Now, according to Proposition 4.5, the structure of depends on the sign of , where is the optimal Lagrange multiplier of Problem (). If , then there exists some such that , for and , for . Otherwise, , and in this case, . With these observations, the optimal retention of Problem () is given by:

where , and .

Now, suppose that , as defined in eq. (2.3). Then according to Proposition 4.3, the optimal retention is determined by

for all .

Define the function , . Let and be two random variables, whose probability distribution are and , respectively, and let and be the corresponding probability densities. Since is increasing in , then is smaller than in the likelihood ratio order, i.e., , and hence, by [69, Theorem 1.C.1.], is smaller than in the hazard ratio order, i.e., . Thus, the function is increasing in . For , there exists some such that , for . In this case, the optimal retention is of the following form:

for some Lebesgue measurable and -valued function . In particular, for , the optimal indemnity is , for some .

Example 4.8.

Assume that the state-space is a Polish space. Let be distortion functions such that is a strictly increasing, strictly concave function satisfying and , for . As before, let be the continuous cdf corresponding to the insurer’s belief . Moreover, let be probability measures, whose corresponding cdf’s are defined as , . In the presence of model ambiguity, DM considers the ambiguity set to be the convex hull of these probabilities, i.e., . Observe that, by construction, , for any . As is a Polish space, according to Prohorov’s Theorem, is weak∗-compact if it is closed and tight. Since the generating set is finite, it follows that is a closed set. To prove the tightness property, observe that , for and for all .

Next, observe that for any , there exists some with such that . For any and any ,

where the first inequality holds by Markov’s inequality. Hence, is tight and thus weak∗-compact.

Next, consider Problem () with the ambiguity set defined above. It is a problem of minimization of a linear function in , and thus minimization of a concave function in over a convex and compact set. As the ambiguity set is not empty, the optimal solution is an extreme point of , i.e., .

In this setting, let be the admissible set of indemnities in Proposition 4.5. Since on , the optimal retention in Example 4.7 simplifies further to:

where is given in Proposition 4.5.

For as defined in eq. (2.3) and , Proposition 4.3 states that the optimal retention is such that

for all .

Define the continuous function , . Let and be the probability densities of and , respectively. Note that for any distortion , is increasing in . Now let and be two continuous random variables such that and . Similar to Example 4.7, , and thus, the function is increasing in . For , there exists some such that , for . In this case, the optimal retention is of the following form:

for some Lebesgue measurable and -valued function . If is strictly increasing, then .

5. Numerical Examples

This section presents numerical examples that illustrate the structure of the optimal indemnity obtained in Sections 3 and 4, when the ambiguity set is constructed as a specific neighbourhood around a reference/ baseline distribution. Throughout this analysis, we assume that the underlying space is a Polish space, equipped with its Borel sigma-algebra.

As above, is a nonnegative random variable representing the insurable loss, whose true distribution may be unknown. The insurer’s belief regarding the loss can be the empirical distribution, derived from experts’ opinion or estimated using standard statistical tools. The DM’s ambiguity regarding the realizations of is described by a -neighbourhood around defined as:

| (5.1) |

where is some discrepancy measure between probability measures and , and is a tolerance level/ambiguity radius. The mapping satisfies if and only if . It is worth mentioning that the worst-case distribution depends not only on the choice of , but also on the ambiguity radius . In general, the size of is connected to the amount of observations available: if is close to zero, the impact of ambiguity is negligible; while large values of indicate high levels of model uncertainty. The question of how to optimally choose the ambiguity radius is an ongoing stream of research in robust optimization. The data-driven approach estimates either by evaluating the discrepancy between the empirical model and the calibrated model, or using measure concentration inequalities to target a certain confidence level , i.e., (see [35, Theorem 3.4 and the discussion afterwards], [17, Section 5.1]). We investigate this method in Example 5.2, when the ambiguity set is constructed using the Wasserstein metric. Another approach interprets as the degree of ambiguity about the reference model and thus argues that this choice depends on the risk preferences of market participants (e.g., [20, 75]). In Example 5.3, we follow the latter approach and solve Problem () for different levels of ambiguity. This allows us to analyze the impact of ambiguity on the optimal indemnity and the worst-case distribution .

The following observation characterizes the change in the DM’s expected utility, as a function of the ambiguity radius . This dynamic is later illustrated in Figure 7 in Example 5.3.

Remark 5.1.

For a fixed premium budget , let (defined in eq. (3.9)) be the feasible set of indemnities in Theorem 3.4. Moreover, for a discrepancy measure and some ambiguity radii , let and be the corresponding ambiguity sets, as defined in eq. (5.1). Let and be the saddle points of Problems (), for and , respectively. It holds that

where the first inequality follows from , as . Hence, for increasing values of , the optimal DM’s expected utility decreases.

Example 5.2 (Wasserstein ambiguity set).

We examine the structure of the saddle point in the setting of Problem (), when the insurer is risk-neutral and the admissible set of indemnities is as defined in eq. (2.3). The DM’s ambiguity about the realizations of is characterized by the ambiguity set given by

where is the Wasserstein distance on , with the -norm being the underlying metric (e.g., [71]):

The Wasserstein distance is a metric on , satisfying if and only if . With this metric, is convex and weak∗-compact. See Villani [73] for further properties of the Wasserstein distance.

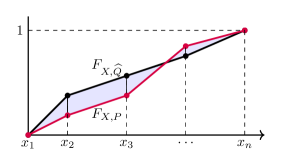

Let be the insurer’s belief regarding the loss . In this example, we assume that is a truncated Generalized Pareto distribution with an upper bound , with shape and scale parameters and , respectively. Next, we simulate from the distribution , and obtain the empirical distribution. We then construct a piecewise linear approximation of this empirical distribution, with given knots , where the partition is chosen arbitrarily, but kept fixed all throughout. That is, is given by a system . Note that by construction, . The corresponding density is piecewise constant on each interval , for . More precisely, is the slope of the line passing through the points and , i.e., , for .

This representation of allows us to compute the Wasserstein distance between and , and thus to characterize the alternative distributions via the system , for the same segments , . For two such distributions, the Wasserstein distance is the sum of the areas of the trapezoids with corners formed by and (see the shaded area in Figure 2), i.e.,

| (5.2) |

where the function defined below is convex in each component (e.g., [60]):

The alternative measure is represented by an -dimensional vector , where is the constant forming the piecewise constant density of . More precisely, the alternative cdf will be linear on each interval , and will differ from only in the cumulative probabilities . Thus, will be the slope of the line passing through the points and . The representation of is shown in Figure 2. Therefore, the variable must satisfy , where for , the matrix is defined as follows:

| (5.3) |

Using the matrix above, can also be represented via , for .

Next, to identify the optimal , we follow the equivalent formulation of Problem () and describe the decision variable in terms of retention function . We assume that is piecewise linear between the segments , , and describe the corresponding values as . Moreover, the variable is feasible for Problem () if and , where the matrix is defined in eq. (5.3).

With these representations for and , the objective function in () is approximated using the trapezoid rule on intervals , , as follows:

The trapezoid rule allows us to determine the number of segments used in the linear approximation of , by specifying a priori the target error bound. The error bound for this method is given by

| (5.4) |

where the constant satisfies . As example, let DM’s utility be , for , the initial wealth and the premium budget . By direct computation, we get

As before, we select and , where the upper bound of the random variable is equal to . If the largest possible error between the objective function in () and its approximation is , then according to eq. (5.4), . Therefore, to solve (), we choose points of approximation .

The error introduced by solving () in terms of instead of can be used to estimate the ambiguity radius . The estimator depends on the number of piecewise linear segments and thus, it is informed by the data. In particular, we propose to approximate as

as dominates in the first stochastic order. In our setting, is estimated to be around .

In sum, Problem () is approximated by the following problem:

| (P) |

where and is computed as in eq. (5.2). The objective function in (P) is concave in and linear in , while the constraints are convex in and linear in . Problem (P) is solved via successive convex programming (SCP – see [59]). The idea is to approximate the infinite dimensional ambiguity set by a finitely generated set , obtained iteratively from solving the inner problem in (P). The algorithm starts with , , and solves the outer problem:

| (P) |

The solution acts as input for the inner problem:

| (P) |

The new is added to the discrete set, i.e., , , and the outer Problem (P) is solved using the updated . The algorithm stops when no new model is found. The convergence of the algorithm is proven in Pflug and Pichler [59]. For completeness, a sketch of the proof of this results in our setting is presented in Appendix D.

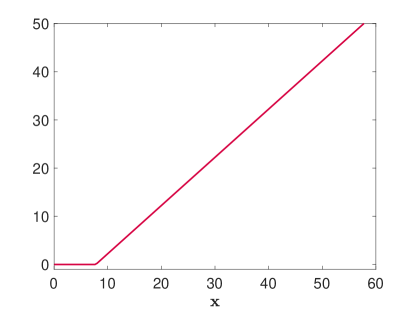

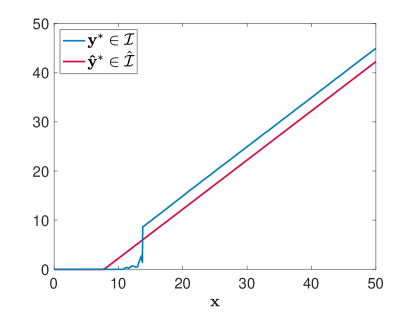

For the implementation, we resume the input for (P): the DM’s initial wealth is and the utility is , for , while the premium budget and the safety loading is . For , we simulate from the distribution , and construct the piecewise linear approximation of the empirical distribution on the partition . The cdf will play the role of the baseline distribution in Problem (P). Finally, the ambiguity radius is estimated to be around . Figure 3 shows one of the saddle points of Problem (P): the optimal is a deductible indemnity with a deductible , while the corresponding dominates in the first stochastic order.

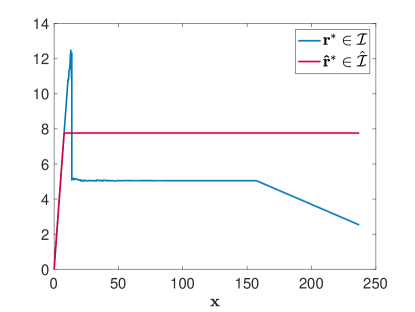

Next, we study a problem related to Problem (P), in which retention function is required only to be bounded by , i.e. , where as defined in eq. (2.2). In Figure 4 (left) we display the difference between the optimal retention functions of Problem (P), for the sets and , respectively. Figure 4 (right) provides a closer look at the corresponding indemnities and , respectively. While the deductible contract is optimal when the no-sabotage condition is present (the red line in Figure 4), the indemnity can be decreasing with respect to the loss in the absence of this condition (see the blue line in Figure 4).

Example 5.3 (Rényi ambiguity set).

For this example we focus on Problem (), when the admissible set of indemnities is as defined in eq. (2.3). Let DM’s ambiguity set be given by

where is the Rényi divergence of order between and , i.e.,

We observe that for every , if and only if . When , is the well-known Kullback-Leibler divergence. Moreover, since is a Polish space, for any ambiguity radius and degree the set is a convex and compact in the topology of weak convergence (e.g., [72, Theorem 20]). For more on the properties of the divergence , we refer to [64] and [53].

To illustrate our results, we follow the existing literature and consider a discretely distributed loss . For a sample of size , we assume without loss of generality that , and we denote this -sample by . For our example, a random sample of size is drawn from a truncated exponential distribution with mean , and with an upper bound . Moreover, the insurer’s belief is the empirical distribution of the sample . Let be the insurer’s probability mass function (pmf), where , , , .

Let be the indemnification function corresponding to the loss . Following the approach in [10], the feasibility constraints and , for , are represented by and , where is defined in eq. (5.3).

Moreover, belongs to if it satisfies the following conditions:

-

(i)

is a pmf: ;

-

(ii)

is absolutely continuous with respect to : if such that , then .

-

(iii)

lies in a Rényi ambiguity set around :

where .

To simplify the notation, let .

Observe that Problem (Pn) is a convex optimization problem, as the objective function is concave in and linear in , for , while the constraints are convex in and , for any . Similarly to Example 5.2, Problem (Pn) is solved in a step-wise manner, by splitting the initial problem into an inner Problem (P):

| (P) |

and outer Problem (P):

| (P) |

where is a finite set of alternative pmfs, obtained as worst-case solutions in previous iterations of Problem (P). More precisely, the algorithm starts with the initialization . The outer Problem (P) receives as input the singleton and yields an optimal solution . The indemnity is then used as input for (P), which gives a new pmf . The new is added to a finite set of feasible models , which is the input for (P). The algorithm continues until no new model is added to . A sketch of the proof of convergence is provided in Appendix D.

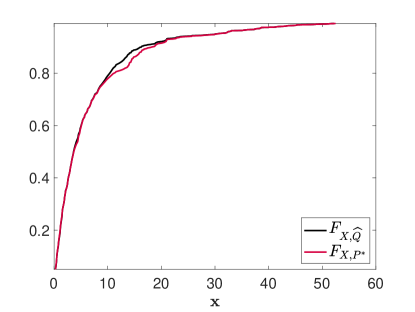

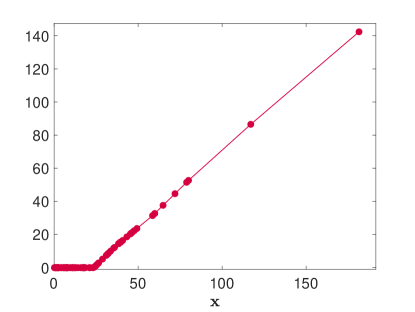

To obtain an explicit solution, let the DM’s initial wealth be , the budget be , the safety loading be , and the DM’s utility be . The insurers’ initial wealth is , and the utility is . For the ambiguity set , we choose the ambiguity radius and the order of Rényi divergence . Figure 5 shows the optimal indemnity (left) and the worst-case distribution , corresponding to (right).

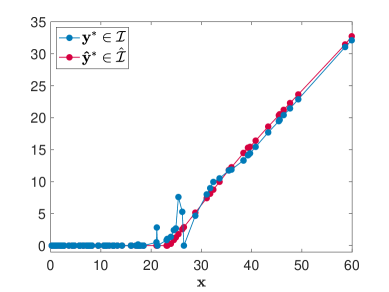

We also solve Problem (Pn) for the same ambiguity set , when the feasibility set is as defined in eq. (2.2). This implies that the constraint is removed from the optimization Problem (Pn). Figure 6 illustrates the difference between the optimal indemnities corresponding to and .

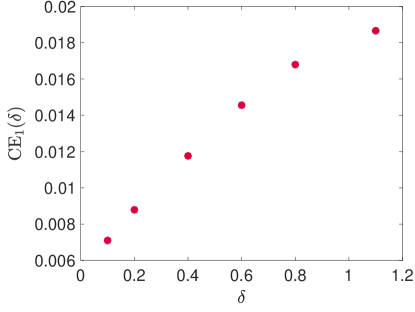

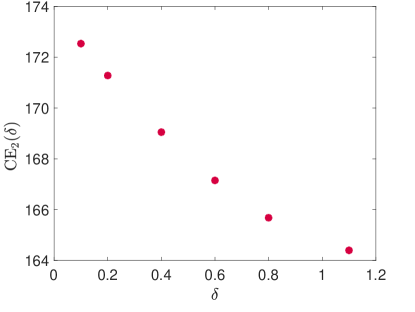

We next investigate the decrease in optimal expected utility, when the ambiguity set increases. Certainty equivalence is used to quantify the impact of ambiguity radii on the optimal value of Problem (Pn).

For each , let be an optimal solution of (Pn) and define the certainty equivalents and as follows:

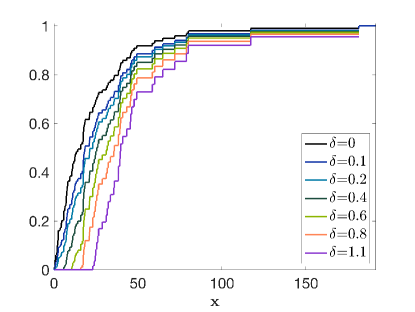

where is the probability measure corresponding to . The constant quantifies the marginal benefit of the optimal insurance contract, which we interpret as the willingness-to-pay for insurance. Moreover, measures the certainty equivalent of DM’s final position. Figure 7 displays the changes in certainty equivalents for increased values of ambiguity radius. The left figure shows that a larger ambiguity radius yields a higher marginal benefit of the optimal insurance contract. This implies that the DM has a higher willingness-to-pay for the optimal insurance contract if the ambiguity set gets larger. On the other hand, the certainty equivalent of the final wealth position decreases when the ambiguity set gets larger because the DM is more ambiguity-averse (Figure 7 (right)).

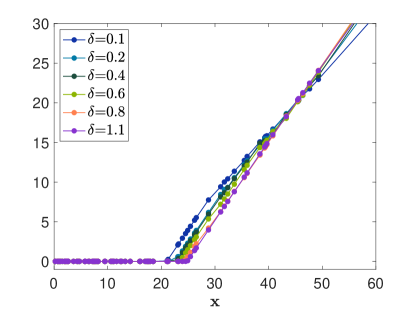

Figure 8 (left) provides a closer look at the optimal indemnities , when the ambiguity set becomes wider. Figure 8 (right) shows the worst-case distribution for several values of . For increasing values of the ambiguity radius, it can be observed that each dominates all the previous distributions in the first stochastic order.

6. Conclusion

The impact of ambiguity on insurance markets in general, and insurance contracting in particular, is by now well-documented. One of the most popular and intuitive ways to model sensitivity of preferences to ambiguity is the Maxmin-Expected Utility (MEU) model of Gilboa and Schmeidler [43]. Nonetheless, to the best of our knowledge, none of the theoretical studies of risk sharing in insurance markets in the presence of ambiguity have examined the case in which the insured is a MEU-maximizer. This paper fills this void. Specifically, we extend the classical setup and results in two ways: (i) the decision maker (DM) is endowed with MEU preferences; and (ii) the insurer is an Expected-Utility-maximizer who is not necessarily risk-neutral (that is, the premium principle is not necessarily an expected-value premium principle). The main objective of this paper is then to determine the shape of the optimal insurance indemnity in that case.

We characterize optimal indemnity functions both with and without the customary ex ante no-sabotage requirement on feasible indemnities, and for both concave and linear utility functions for the two agents. The no-sabotage condition is shown to play a key role in determining the shape of optimal indemnity functions. An equally important factor in characterizing optimal indemnities is the singularity in beliefs between the two agents.

We subsequently examine several illustrative examples, and we provide numerical studies for the case of a Wasserstein and a Rényi ambiguity set. Specifically, we provide a successive convex programming algorithm to compute optimal insurance indemnities in a discretized framework. The Wasserstein and Rényi distances are two popular metrics to construct probability ambiguity sets. We show in numerical examples that a larger ambiguity set yields a lower certainty equivalent of final wealth, but increases the willingness-to-pay for insurance.

Appendix A Proof of Proposition 4.3

For the retention random variable, Problem () becomes

| (A.1) | ||||||

| s.t. |

where . The Sion’s Minimax Theorem yields that there exists a saddle point such that . For , the inner optimization problem becomes:

| s.t. |

where and are as in Remark 3.1, and , for some Borel measurable function . The splitting technique in [41, Lemma C.6] states that the optimal retention function can be obtained as , where solves Problem (A.2) below.

| (A.2) |

Therefore, the optimal solution is 1-Lipschitz -a.s., as long as is 1-Lipschitz on . Similar to Theorem 3.4, a necessary and sufficient condition for to be the optimal solution of Problem (A.2) is

| (A.3) |

where is the Lagrange multiplier associated to Problem (A.2). As any is absolutely continuous, it is almost everywhere differentiable on , and hence (A.3) becomes

for all ; hence is of the form

| (A.4) |

for some Lebesgue measurable and -valued function . The existence of such that follows similar to Theorem 3.4.

Appendix B Convexity and Compactness of in Examples 4.4 and 4.7

Lemma B.1.

For a fixed , let be the set defined as follows:

| (B.1) |

where is a collection of nonnegative increasing weight functions, such that , for all . Then the following hold:

-

(i)

If is a convex cone, then is convex.

-

(ii)

If is uniformly absolutely continuous with respect to some , then is weak∗-compact.

Proof.

Remark B.2.

Proposition B.3.

If is order bounded in the Banach lattice , with a constant upper bound and a nonnegative lower bound having nonzero -norm, then is uniformly absolutely continuous with respect to .

Proof.

Suppose that is order bounded in , with a constant upper bound and a nonnegative lower bound having nonzero -norm. Then there exists and , such that , , and , for each . Consequently, for each ,

Hence, for each and each ,

Consequently, for each , letting , it follows that for each and each ,

Hence, is uniformly absolutely continuous with respect to . ∎

Appendix C -approximation of a Continuous Function

Let be a function defined on a compact interval . For the definition of piecewise linear approximation of , we follow the notation in [58].

Definition C.1.

-

•

A function is a piecewise linear function (pwl) with line-segments if , , and , such that the following holds:

-

•

A pwl function is called -approximation of with if:

(C.1) -

•

We call function a -underestimator of function if condition (C.1) is satisfied along with

We call function a -overestimator of if is a -underestimator of .

To simplify the notation, we characterize a pwl function associated to via the system , where and are the breakpoint of the -th segment.

According to [32], if the function defined on the compact set is continuous, then for any scalar , there exists a continuous -approximation. Moreover, [63, Corollary 2.1] states that if a -approximation of exists, then for , the functions and define an -underestimator and an -overestimator, respectively, of .

Appendix D Convergence of the Algorithm in Examples 5.2 and 5.3

The convergence of the SCP algorithm in Examples 5.2 and 5.3 is proven in Pflug and Pichler [59, Proposition B.6]. Below we present a sketch of the proof for the general setting of Problem (). Recall that the sets in (3.9) and in (5.1) are compact and the mapping is jointly continuous.

Proof.

Let ; by Remark 5.1, it follows that

| (D.3) |

Since is bounded, the iterations (D.1) -(D.2) form a decreasing sequence that converges to . By compactness of , the sequence has at least one cluster point. Let be one of the cluster points.

We would like to show first that . Assume by contradiction that ; then there exists some such that . Since is continuous in , there exists some in a neighborhood of such that , which contradicts eq. (D.3).

Next, we show that . Again assume that there exists some such that . By construction, we have . Taking yields , a contradiction. ∎

References

- [1] D. Alary, C. Gollier, and N. Treich. The Effect of Ambiguity Aversion on Insurance and Self-Protection. Economic Journal, 123(573):1188–1202, 2013.

- [2] H. Albrecher, J. Beirlant, and J.L. Teugels. Reinsurance: Actuarial and Statistical Aspects. John Wiley & Sons, 2017.

- [3] C.D. Aliprantis and K.C. Border. Infinite Dimensional Analysis - edition. Springer-Verlag, 2006.

- [4] M. Allais. Le Comportement de l’Homme Rationnel Devant le Risque: Critique des Axiomes et Postulats de l’école Américaine. Econometrica, 21(4):503–546, 1953.

- [5] M. Amarante. Foundations of Neo-Bayesian Statistics. Journal of Economic Theory, 144(5):2146–2173, 2009.

- [6] M. Amarante, M. Ghossoub, and E.S. Phelps. Ambiguity on the Insurer’s Side: The Demand for Insurance. Journal of Mathematical Economics, 58:61–78, 2015.

- [7] K.J. Arrow. Uncertainty and the Welfare Economics of Medical Care. American Economic Review, 53(5):941–973, 1963.

- [8] K.J. Arrow. Essays in the Theory of Risk-Bearing. Chicago: Markham Publishing Company, 1971.

- [9] P. Artzner, F. Delbaen, J.M. Eber, and D. Heath. Coherent Measures of Risk. Mathematical Finance, 9(3):203–228, 1999.

- [10] A.V. Asimit, V. Bignozzi, K.C. Cheung, J. Hu, and E.-S. Kim. Robust and Pareto Optimality of Insurance Contracts. European Journal of Operational Research, 262(2):720–732, 2017.

- [11] R.J. Aumann. Agreeing to Disagree. Annals of Statistics, 4(6):1236–1239, 1976.

- [12] R.J. Aumann. Common Priors: A Reply to Gul. Econometrica, 66(4):929–938, 1998.

- [13] A. Ben-Tal, L. El Ghaoui, and A. Nemirovski. Robust Optimization. Princeton University Press, 2009.

- [14] C. Bernard, X. He, J.A. Yan, and X.Y. Zhou. Optimal Insurance Design under Rank-Dependent Expected Utility. Mathematical Finance, 25(1):154–186, 2015.

- [15] D. Bertsimas and M. Sim. The Price of Robustness. Operations Research, 52(1):35–53, 2004.

- [16] C. Birghila and G.C. Pflug. Optimal XL-Insurance under Wasserstein-Type Ambiguity. Insurance: Mathematics and Economics, 88:30–43, 2019.

- [17] J. Blanchet, F. He, and K. Murthy. On Distributionally Robust Extreme Value Analysis. Extremes, pages 1–31, 2020.

- [18] T.J. Boonen and M. Ghossoub. On the Existence of a Representative Reinsurer under Heterogeneous Beliefs. Insurance: Mathematics and Economics, 88:209–225, 2019.

- [19] T.J. Boonen and M. Ghossoub. Optimal Reinsurance with Multiple Reinsurers: Distortion Risk Measures, Distortion Premium Principles, and Heterogeneous Beliefs. Insurance: Mathematics and Economics, Forthcoming.

- [20] T. Breuer and I. Csiszár. Measuring Distribution Model Risk. Mathematical Finance, 26(2):395–411, 2016.

- [21] H. Buhlmann. An Economic Premium Principle. ASTIN Bulletin, 11(1):52–60, 1980.

- [22] G.C. Calafiore and L. El Ghaoui. On Distributionally Robust Chance-Constrained Linear Programs. Journal of Optimization Theory and Applications, 130(1):1–22, 2006.

- [23] G. Carlier and R.A. Dana. Pareto Efficient Insurance Contracts when the Insurer’s Cost Function is Discontinuous. Economic Theory, 21(4):871–893, 2003.

- [24] A. Chateauneuf, F. Maccheroni, M. Marinacci, and J.M. Tallon. Monotone Continuous Multiple Priors. Economic Theory, 26(4):973–982, 2005.

- [25] Y. Chi. On the Optimality of a Straight Deductible under Belief Heterogeneity. ASTIN Bulletin, 49(1):243–262, 2019.

- [26] P.-A. Chiappori and B. Salanie. Testing for Asymmetric Information in Insurance Markets. Journal of political Economy, 108(1):56–78, 2000.

- [27] J.D. Cummins and O. Mahul. The Demand for Insurance with an Upper Limit on Coverage. Journal of Risk and Insurance, 71(2):253–264, 2004.

- [28] R.A. Dana and M. Scarsini. Optimal Risk Sharing with Background Risk. Journal of Economic Theory, 133(1):152–176, 2007.

- [29] B. De Finetti. La Prévision: Ses Lois Logiques, Ses Sources Subjectives. Annales de l’Institut Henri Poincaré, 7(1):1–68, 1937.

- [30] E. Delage and Y. Ye. Distributionally Robust Optimization Under Moment Uncertainty with Application to Data-Driven Problems. Operations Research, 58(3):595–612, 2010.

- [31] F. Delbaen. Coherent Risk Measures on General Probability Spaces. Advances in finance and stochastics. Essays in Honour of Dieter Sondermann, pages 1–37, 2002.

- [32] J.J. Duistermaat and J. AC Kolk. Multidimensional Real Analysis I: Differentiation. Cambridge University Press, 2004.

- [33] N. Dunford and J.T. Schwartz. Linear Operators, Part 1: General Theory. Wiley-Interscience, 1958.

- [34] D. Ellsberg. Risk, Ambiguity, and the Savage Axioms. Quarterly Journal of Economics, 75(4):643–669, 1961.

- [35] P. M. Esfahani and D. Kuhn. Data-Driven Distributionally Robust Optimization Using the Wasserstein Metric: Performance Guarantees and Tractable Reformulations. Mathematical Programming, 171(1-2):115–166, 2018.

- [36] A. Finkelstein and J. Poterba. Adverse Selection in Insurance Markets: Policyholder Evidence from the UK Annuity Market. Journal of Political Economy, 112(1):183–208, 2004.

- [37] E. Furman and R. Zitikis. Weighted Premium Calculation Principles. Insurance: Mathematics and Economics, 42(1):459–465, 2008.

- [38] E. Furman and R. Zitikis. Weighted Risk Capital Allocations. Insurance: Mathematics and Economics, 43(2):263–269, 2008.

- [39] E. Furman and R. Zitikis. Weighted Pricing Functionals with Applications to Insurance. North American Actuarial Journal, 13(4):483–496, 2009.

- [40] P. Ghirardato, F. Maccheroni, and M. Marinacci. Differentiating Ambiguity and Ambiguity Attitude. Journal of Economic Theory, 118:133–173, 2004.

- [41] M. Ghossoub. Budget-Constrained Optimal Insurance With Belief Heterogeneity. Insurance: Mathematics and Economics, 89:79–91, 2019.

- [42] M. Ghossoub. Optimal Insurance under Rank-Dependent Expected Utility. Insurance: Mathematics and Economics, 87:51–66, 2019.

- [43] I. Gilboa and D. Schmeidler. Maximum Expected Utility with a Non-Unique Prior. Journal of Mathematical Economics, 18(2):141–153, 1989.

- [44] C. Gollier. The Economics of Optimal Insurance Design. In G. Dionne (ed.), Handbook of Insurance – ed. . Springer, 2013.

- [45] C. Gollier. Optimal Insurance Design of Ambiguous Risks. Economic Theory, 57(3):555–576, 2014.

- [46] F. Gul. A Comment on Aumann’s Bayesian View. Econometrica, 66(4):923–927, 1998.

- [47] R.M. Hogarth and H. Kunreuther. Risk, Ambiguity, and Insurance. Journal of Risk and Uncertainty, 2(1):5–35, 1989.

- [48] G. Huberman, D. Mayers, and C.W. Smith Jr. Optimal Insurance Policy Indemnity Schedules. Bell Journal of Economics, 14(2):415–426, 1983.

- [49] K. Inada. On a Two-Sector Model of Economic Growth: Comments and a Generalization. The Review of Economic Studies, 30(2):119–127, 1963.

- [50] M. Jeleva. Background Risk, Demand for Insurance, and Choquet Expected Utility Preferences. The Geneva Papers on Risk and Insurance Theory, 25(1):7–28, 2000.

- [51] M. Jeleva and B. Villeneuve. Insurance Contracts with Imprecise Probabilities and Adverse Selection. Economic Theory, 23(4):777–794, 2004.

- [52] P. Klibanoff, M. Marinacci, and S. Mukerji. A Smooth Model of Decision Making under Ambiguity. Econometrica, 73(6):1849–1892, 2005.

- [53] F. Liese and I. Vajda. Convex Statistical Distances. Teubner, 1987.

- [54] F. Maccheroni and M. Marinacci. A Heine-Borel Theorem for (). RISEC, 48(3):353–362, 2001.

- [55] M.J. Machina. Non-Expected Utility and the Robustness of the Classical Insurance Paradigm. In G. Dionne (ed.), Handbook of Insurance Economics, Second Ed. Springer, New York, 2013.

- [56] S. Morris. The Common Prior Assumption in Economic Theory. Economics and Philosophy, 11(2):227–253, 1995.

- [57] J. Mossin. Aspects of Rational Insurance Purchasing. Journal of Political Economy, 76(4):553–568, 1968.

- [58] S.U. Ngueveu. Piecewise Linear Bounding of Univariate Nonlinear Functions and Resulting Mixed Integer Linear Programming-Based Solution Methods. European Journal of Operational Research, 275(3):1058–1071, 2019.

- [59] G. C. Pflug and A. Picher. Multistage Stochastic Optimization. Springer, 2014.

- [60] G.C. Pflug, A. Timonina-Farkas, and S. Hochrainer-Stigler. Incorporating Model Uncertainty Into Optimal Insurance Contract Design. Insurance: Mathematics and Economics, 73:68–74, 2017.

- [61] J. Quiggin. A Theory of Anticipated Utility. Journal of Economic Behavior & Organization, 3(4):323–343, 1982.

- [62] A. Raviv. The Design of an Optimal Insurance Policy. The American Economic Review, 69(1):84–96, 1979.

- [63] S. Rebennack and J. Kallrath. Continuous Piecewise Linear Delta-Approximations for Univariate Functions: Computing Minimal Breakpoint Systems. Journal of Optimization Theory and Applications, 167(2):617–643, 2015.

- [64] A. Rényi. On Measures of Entropy and Information. In Proceedings of the Fourth Berkeley Symposium on Mathematical Statistics and Probability, Volume 1: Contributions to the Theory of Statistics. University of California Press, 1961.

- [65] L.J. Savage. The Foundations of Statistics (2nd revised edition) – ed. 1954. New York: Dover Publications, 1972.

- [66] H. Scarf. A Min-Max Solution of an Inventory Problem. Studies in The Mathematical Theory of Inventory and Production, 1958.

- [67] H. Schlesinger. The Theory Insurance Demand. In G. Dionne (ed.), Handbook of Insurance. Kluwer Academic publishers, 2000.

- [68] D. Schmeidler. Subjective Probability and Expected Utility without Additivity. Econometrica, 57(3):571–587, 1989.

- [69] M. Shaked and J.G. Shanthikumar. Stochastic Orders. Springer, 2007.

- [70] A. Thiele. Robust Stochastic Programming with Uncertain Probabilities. IMA Journal of Management Mathematics, 19(3):289–321, 2008.

- [71] S.S. Vallender. Calculation of the Wasserstein Distance Between Probability Distributions on the Line. Theory of Probability & Its Applications, 18(4):784–786, 1974.