Choosing News Topics to Explain Stock Market Returns

Abstract.

We analyze methods for selecting topics in news articles to explain stock returns. We find, through empirical and theoretical results, that supervised Latent Dirichlet Allocation (sLDA) implemented through Gibbs sampling in a stochastic EM algorithm will often overfit returns to the detriment of the topic model. We obtain better out-of-sample performance through a random search of plain LDA models. A branching procedure that reinforces effective topic assignments often performs best. We test methods on an archive of over 90,000 news articles about S&P 500 firms.

1. Introduction

News sentiment has been widely observed to help forecast stock market returns. The ability of news topics to explain contemporaneous returns has received less attention. Topics are relevant because, for example, news of a fraud investigation at a company may explain a negative return, while a new product announcement will often be associated with positive returns. Topics may also be relevant to explaining return volatility. Furthermore, topics that are useful for explaining contemporaneous returns may also be useful for forecasting future returns. For example, a 2% stock price drop associated with a topic about accounting scandals may be associated with continued price drops in the future; whereas a 2% stock price drop associated with a topic about a large hedge fund liquidation may be expected to reverse over the short-term. Not all 2% price drops are created equal, and being able to associate a particular move to an underlying reason may yield important insights about what comes next. This paper fits into a broader research agenda that aims to first explain contemporaneous price moves, and only then to think about forecasting future ones. See (Tetlock, 2014) and references there for background on news and text analysis in financial economics.

With these considerations in mind, we are interested in finding topics in news text specifically designed to explain market responses. This is a problem of supervised topic modeling, in which a news article about a company is labeled with the company’s contemporaneous stock return on the day the news article is released.

We study the use of the supervised Latent Dirichlet Allocation (sLDA) framework of (Mcauliffe and Blei, 2008). In the sLDA generative model, a document’s label is generated through a function of the proportions of words in the document associated with each topic. The topic model is otherwise as in plain LDA (Blei et al., 2003). In most applications of sLDA, the labels are discrete and the objective is to classify documents. Our goal is to explain contemporaneous returns (or volatility), so we face a regression problem rather than a classification task. We also sketch a foundation for this formulation based on finance theory.

SLDA can be implemented through a combination of Gibbs sampling and a stochastic EM algorithm, as in the R package lda and (Boyd-Graber and Resnik, 2010). The “M” step updates coefficients by regressing returns (labels) on the topic distribution in each document. The “E” step updates topic assignments conditional on a document’s words and label.

We show that the performance of the algorithm is very sensitive to the relative weight applied to the text and label in the “E” step, where the relative weight is controlled by a variance parameter in the regression model. With too much weight on the labels, the “E” step will often drive the algorithm to overfit returns to the detriment of the topic model, resulting in poor out-of-sample performance in explaining returns. We provide some theoretical explanation for this behavior. With too little weight on the labels, sLDA tends to find the same topics as plain LDA.

To get around this difficulty, we propose a random search of alternative LDA estimates that reinforces topic assignments that help explain returns. In our branching method, we start with multiple independent runs of LDA through Gibbs sampling. Of these, we select the one that yields the best explanatory power for returns. This winner becomes the starting point for a new set of LDA runs, and the process repeats. Crucially, in each round the winner is selected through cross-validation. This ensures that our selection process favors topic assignments that explain returns (out of sample) while avoiding the overfitting that results from the in-sample estimates used in the “E” step of the stochastic EM algorithm.

We compare this branching algorithm (and some simpler alternatives) with plain LDA and sLDA. In regressions of returns on topic assignments of a hold-out sample, we find that the search methods improve over plain LDA and significantly outperform sLDA. Stock market returns are of course very difficult to explain (Roll, 1988), so the absolute levels of in our regressions are very small, but the relative improvements using the methods we propose are substantial.

To get a sense of the magnitudes, consider the analysis in (Tetlock et al., 2008). Using over 20 years of stock return data for S&P 500 firms, they find a regression with a rich set of forecasting variables (lagged prices, accounting information, and text-based measures of news flow) has an for next day returns of roughly 0.2%. A similar regression for same day returns has an of 0.45%. Both are in-sample numbers. Our topic model’s out-of-sample ability to explain contemporaneous returns far exceeds the 0.45% threshold from the prior literature, and may, in fact, represent a sort of natural bound on how much of contemporaneous return variation is explainable in the first place, with the remainder being inexplicable noise.111(Nguyen and Shirai, 2015) uses an LDA-type model to forecast whether the next day’s stock move will be up or down – a very different task than obtaining an expected return from a regression – and finds that, for a sample of five stocks over the course of one year, discussion topics on Yahoo Finance Message Board lead to a 56% correct classification rate. Given the small sample size of the analysis, the statistical significance of this finding is not clear.

2. Supervised Topic Models

This section discusses topic models, from plain LDA to sLDA.

2.1. Latent Dirichlet Allocation

A corpus is a collection of documents, and a document is a collection of words. A topic is a probability distribution over words in a corpus. For example, one topic might assign relatively high probability to the words “debt,” “credit,” and “rating,” and another topic to the terms “China,” “Japan,” and “Asia.” We observe words but not the identity of their associated topics. The word “bond,” might result from a debt markets topic or from an Asian markets topic. To infer the latent topic assignments from the observed text, we need a model of how text is generated.

Let denote a corpus of documents, in which is the th word in document , and is the total number of words in document . Words are drawn from a collection wide vocabulary of size ; we identify the vocabulary with the set and take each word to be an element of this set. Suppose the text is generated by topics. Let , where is the topic assignment for .

LDA posits that the corpus is generated as follows:

-

(1)

For each topic , generate a random probability distribution over the vocabulary ;

-

(2)

For each document , generate a random probability distribution over the set of topics ;

-

(a)

For each ,

-

(i)

draw topic from the distribution

-

(ii)

draw word from the distribution

-

(i)

-

(a)

In Step (1), each is drawn from a Dirichlet distribution with parameters , and in Step (2), each is drawn from a Dirichlet distribution with parameters . (A Dirichlet distribution is a distribution over nonnegative vectors with components that sum to 1.) We will make the standard assumptions that , , and that these hyperparameters are known along with . In our implementation, we use the standard values of and .

The LDA generative model implicitly determines the joint distribution of topic assignments and words. Only the words are observed, so inference in LDA entails estimating or approximating the posterior distribution of topic assignments given the text. From , one can estimate the topic distributions and the prevalence of each topic in each documents. For example, based on the proportion of words assigned to each topic, we might conclude that a news article is 45% about Asian markets, 30% about debt markets, and 25% about other topics.

For LDA inference, we use the collapsed Gibbs sampling method of (Griffiths and Steyvers, 2004). Gibbs sampling draws samples (approximately) from the posterior distribution . The procedure iteratively sweeps through the topic assignments, at each step resampling the assignment conditional on and conditional on the collection of all assignments other than the th. The update probabilities take the form

| (1) |

where , counts the number of times word is assigned to topic under the assignments , and counts the number of words in document assigned to topic under the assignments . These counts exclude and . Through repeated application of (1) the distribution of the assignments converges to the posterior distribution .

2.2. Supervised LDA

The generative model for sLDA expands the LDA model to include the generation of a label , , for each document. In our main application, a document consists of all news articles about a company in a given trading period (either intraday or overnight), and is that period’s stock return for that company.

In sLDA, labels are driven by the distribution of document topics. For each document , let denote the vector of topic frequencies

so is the fraction of words in document assigned to topic . Here, denotes the indicator function of the event . For some vector of coefficients and standard deviation parameter , we add to the LDA generative model the step

-

(2)(b)

Generate from the normal distribution with mean and variance .

Our goal is to compute an estimate of along with the topic model. Given a new news article about a company, we could then apply the trained LDA model to estimate topic frequencies in the new article and forecast the company’s contemporaneous trading period stock return as . This would be useful when seeing a news article for the first time and being unsure of how the market should react to that article, as well as in studying whether observed price responses to news are consistent with historical norms.

Gibbs sampling under LDA can be expanded for inference under sLDA. Under the sLDA generative model, the labels are independent of the text given the topic assignments . The posterior of given and has the form

The factor is determined entirely by the LDA part of the model and is unaffected by the labels. In this formulation, we are treating and as unknown parameters rather than imposing a prior distribution.

Using the conditional normality in Step (2)(b), we get

with the normal density with mean and variance .

The stochastic EM algorithm combines Gibbs sampling with regression for inference in sLDA. Given topic assignments , the “M” step runs a regression of the labels , , on the frequency vectors , , to compute an estimate . (We do not include a constant in this regression because the components of each sum to 1.) Given , the “E” step runs (multiple iterations of) the Gibbs sampler to update the topic assignments; but the Gibbs sampler now tilts the probabilities in (1) to favor topic assignments that do a better job explaining labels. Let denote the topic proportions for document when is set to and all other assignments are unchanged. Then (1) is replaced with

| (3) | |||||||

Compared with (1), (3) will give greater probability to topic if that assignment increases the factor — in other words, if that assignment reduces the error in explaining the label with the current coefficients . We will return to the important question of choosing in (3) in Sections 4 and 7.

2.3. Foundation in Financial Economics

Before proceeding with our investigation into choosing topics to explain returns, we briefly outline a basis for this investigation in financial economics and provide an underpinning for Step (2)(b), which posits a linear relation between news topics and returns.

Campbell (Campbell, 1991) shows that stock returns can be decomposed into changes in investor beliefs about future dividend growth and future discount rates. In their analysis, the stock return from day to day can be approximated as

| (4) |

where is a constant, is a constant discounting factor, is the time log dividend, is an expectation taken over the investor’s information set at time , and the change-in-beliefs operator is shorthand for .

We conjecture that the information in news articles affects investor beliefs about future discount rates and future dividend growth. In particular, we assume that, for firm , explainable period-over-period changes in investor beliefs about future discount rates and future dividend growth are both linear functions of trading period’s ’s average document-topic assignments for , i.e. . This represents the average document-topic assignments of all news articles mentioning that came out from the end of trading period to the end of trading period . In addition, we assume the unexplainable change in investor beliefs is normally distributed. Both of these assumptions are satisfied if, for example, the state variables follow a vector autoregressive process as in (Campbell, 1991). Under these conditions, firm ’s returns can be written as

| (5) |

for some vector . The in (4) is redundant because the elements of sum to one. (5) is the response equation in our sLDA framework.

3. News and Stock Market Data

Our text data consists of news articles from the Thomson Reuters (TR) archive between 2015 and 2019. We select articles that mention firms in S&P 500 index on the day the article appears. We stem words, remove stop words, drop words that appear less than 7 times total, and drop articles with fewer than 50 words. This leaves a vocabulary of 48,966 words. We exclude articles that mention more than three companies. The process yields 90,544 articles.

If trading period is overnight, then it contains news that came out from 4pm of the prior trading day to 9:30am of the present day. If it is intraday, the trading period contains news articles from 9:30am to 4pm of the present day. We count any news over the weekend or holiday as belonging to the overnight trading period from the prior market close (4pm) to the next market open (9:30am). All times are New York times. We separate these time periods because this study is part of a larger project to understand differences between intraday and overnight news and returns.

In each trading period we combine all news articles that mention a single company into a single document and label that document with the stock return (or squared return) for that company. For articles mentioning multiple companies, we label the article with the average stock return of the underlying companies. We obtain stock returns from CRSP.

Some of our analysis also assigns a sentiment score to each article. We calculate sentiment as the difference between the number of positive and negative words in the article divided by the total number of words. We use the Loughran-McDonald (Loughran and McDonald, 2011) lexicon to determine positive and negative words because it is tailored to financial news. Summary statistics for our trading period labels are: returns have a mean of -1.6e-05 and a standard deviation (SD) of 0.0228; squared returns have a mean of 0.0005 and a SD of 0.0042; and for sentiment the mean is -0.013 and the SD is 0.0231.

4. Performance of sLDA

The parameter in the Gibbs step (3) can naturally be thought of as an estimate of the true standard deviation of the residuals . But it can also be viewed as a mechanism for controlling the relative weight put on the text data and the labels in choosing the topic assignments , with smaller values of putting greater weight on the labels. Indeed, as , becomes infinite at and zero everywhere else.

This relative weighting role for is closely related to the Power-sLDA method of (Zhang and Kjellström, 2014) and the prediction constrained method of (Hughes et al., 2018), both of which seek to find topics that improve label predictability. (Those methods do not use Gibbs sampling.) Power-sLDA effectively allows different documents to use different values of , with smaller values for longer documents. PC-sLDA puts a lower bound on the (in-sample) predictability of labels from topic frequencies. When translated to our setting, this corresponds to choosing through the Lagrange multiplier of the lower-bound constraint, so requiring greater in-sample predictability leads to a smaller .

In our setting, choosing small to improve label-predictability can give disastrously bad results. A small can distort the topic model to overfit the labels, rendering the model useless for out-of-sample predictions. Interestingly, (Boyd-Graber and Resnik, 2010) report unstable results in trying to tune and fix it at 0.25.

In Section 7, we explain what happens theoretically as . But the results of Table 1 provide a simple illustration. We run sLDA with fixed and report the in-sample after the final ”M” step. Using the estimated coefficients , we also calculate an out-of-sample (predictive) on a holdout sample. (See Section 5 for details of this calculation.) At small values of , the in-sample approaches 1, suggesting that the topic model is doing an unreasonably good job explaining returns. But the predictive becomes very negative, revealing serious overfitting to the training data. In choosing topic assignments to fit the training labels at the expense of the validity of the topic model, the algorithm loses any ability to predict returns out of sample. The problem becomes particularly acute with a large number of topics. With more topics, we are more likely to encounter the scenario described in (6), below, and more likely to find meaningless topic assignments that produce nearly perfect in-sample fits to the data.

| 10 Topics | 200 Topics | |||

| In-sample | Out-sample | In-sample | Out-sample | |

| 0.9 | 0.0013 | -0.0005 | 0.019 | 0.015 |

| 0.75 | 0.001 | -0.0008 | 0.0081 | 0.0032 |

| 0.5 | 0.001 | -0.0007 | 0.009 | 0.0017 |

| 0.25 | 0.001 | -0.0007 | 0.019 | 0.018 |

| 0.1 | 0.0009 | -0.0007 | 0.012 | 0.007 |

| 0.01 | 0.0009 | -0.0012 | 0.014 | 0.009 |

| 0.001 | 0.0012 | -0.001 | 0.028 | 0.017 |

| 1e-04 | 0.0009 | -0.0002 | 0.41 | -0.332 |

| 1e-05 | 0.0094 | -0.0062 | 0.95 | -0.441 |

| 1e-06 | 0.96 | -5.16 | 0.98 | -0.17 |

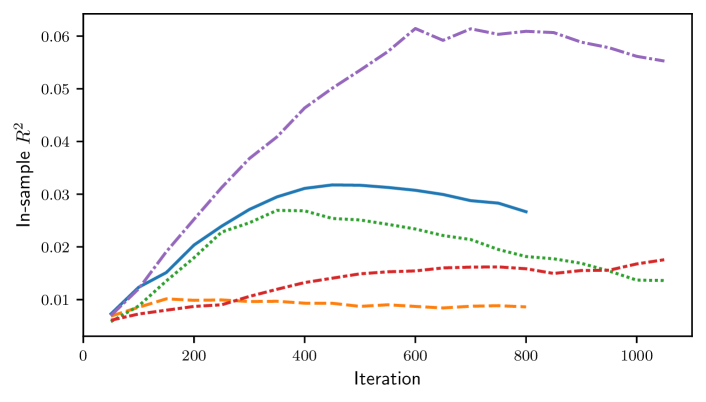

Choosing a larger or more accurate value of can help but does not eliminate the problem. If is too large, sLDA reduces to LDA. The true value in Step (2)(b) of the generative model is the standard deviation of the residuals , . It therefore seems reasonable to estimate from the residuals in the regression in each “M” step. Figure 1 shows the evolution of in-sample across independent runs of this method. At a fixed number of iterations, the results vary widely, and along a single path the in-sample sometimes climbs rapidly and then falls. We study this case in greater detail in Section 7, and here we describe less formally why it often fails.

From a regression perspective, the root of the problem with the Gibbs/EM algorithm is that it uses the same data to estimate the coefficients and to select the regressors . This offers too much flexibility and can lead to serious overfitting. Any error in the current estimate of gets amplified when the Gibbs sampler favors topic assignments tailored to ; at the next “M” step, the errors are further amplified when the new is optimized for flawed topic assignments, and the process repeats.

For example, Section 7 considers the case that, for fixed ,

| (6) |

or, through a relabeling of topics,

| (7) |

Then each can be expressed as a convex combination For a topic assignment with , , and all other , we have

| (8) |

In other words, if at some stage in our EM iterations we get a vector of coefficients that satisfy (7), then a degenerate set of topic assignments as in (8) will lead to near-perfect in-sample label fits, but these assignments largely ignore information in the text data.

The Gibbs/EM algorithm, therefore, has two types of overfitting:

-

•

M-overfitting: The usual tendency of regression coefficients to provide better estimates in-sample than out-of-sample;

-

•

E-overfitting: The less familiar result of adapting the regressors to improve fits to labels with fixed. This is problematic even if , the true vector of coefficients.

To address these shortcomings, we need to separate the estimation of coefficients from the estimation of topic assignments.

5. Branching LDA

We achieve this separation through a more computationally intensive process that reinforces topic assignments that perform better out-of-sample. We compare a few alternatives. All methods split the data into training, validation, and test (holdout) samples.

LDA. As a baseline, we run ordinary collapsed Gibbs sampling for LDA for 700 iterations on the training and validation data. We regress the labels on the final topic assignments to compute estimated coefficients , using only the training and validation data. We then apply the trained LDA model to assign topics to the holdout sample and compute topic proportions for the held out documents. Using the coefficient vector from the training data, we calculate estimates of the labels in the holdout sample. We evaluate performance using the predictive , , where is the average label in the holdout sample, and the sums run over documents in the holdout sample. Importantly, we do not re-estimate through a regression on the holdout sample. We repeat this process 10 times. We use 10 replications here and below to see a range of outcomes with reasonable computational effort.

Best-Of LDA. We start with plain LDA. After an initial period of 250 iterations, we keep 10 subruns spaced 50 iterations apart. For each subrun, we evaluate a predictive on the validation sample, using cross-validation: we randomly split the validation sample into five subsets; we estimate on four subsets; evaluate the predictive on the fifth subset; and average the predictive over the five ways of doing this split. We repeat this process for 10 independent runs. This gives us 10 topic assignments after 250 iterations, 10 after another 50 iterations, and so on. At each number of iterations, we pick the best model as measured by the average predictive on the validation sample. (We have also experimented with keeping the second best model as a form of regularization.) This leaves us with 10 winning models. We evaluate their predictive s on the holdout sample using the procedure described for plain LDA.

Branching LDA. We start with 10 independent plain LDA runs, and, after an initial period of 250 iterations, use the cross-validation procedure described under Best-Of LDA to compute a predictive for each of these. The run with the highest predictive becomes the parent run. We then branch the Gibbs sampler into 10 new independent “child” runs. Each child run starts with an identical topic assignment to the parent. After 50 iterations, we again use the cross-validation procedure described under Best-Of LDA to compute a predictive for the 10 child runs and the parent run. The best of these eleven runs becomes the new parent. (We have also experimented with keeping the second best subrun and excluding the previous parent as forms of regularization.) We continue the Gibbs sampling with 10 independent child runs for 50 iterations, and repeat the process 8 times. We evaluate the parents from the last 10 branchings based on their predictive on the holdout sample.

Best-Of LDA and Branching LDA are two of many possible ways to address the two types of overfitting described at the end of Section 4. We never estimate on the same data we use to evaluate predictions, so we never commit M-overfitting. More importantly, we never use the current estimate to steer the Gibbs sampler, so we never commit E-overfitting; we instead use for cross-validation. Nevertheless, compared with plain LDA, these methods reinforce outcomes of the LDA Gibbs sampler that perform best at estimating labels in the validation set, and we will see that this translates to improved performance on the holdout set. Of the many realizations of the topic assignments that are roughly equally good at explaining the text , we are searching for those that do a better job explaining the labels .

6. Numerical Results

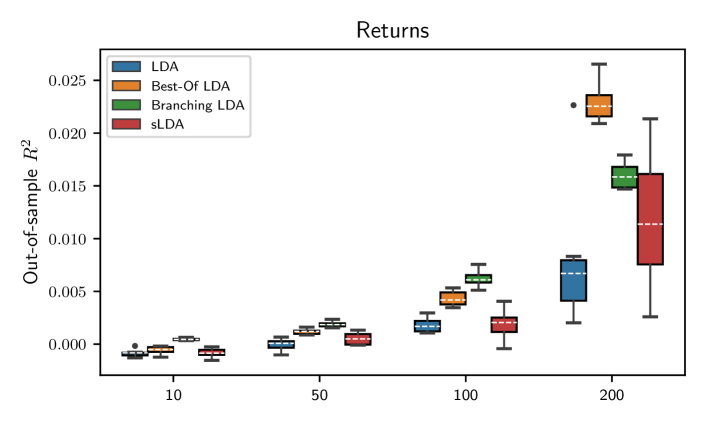

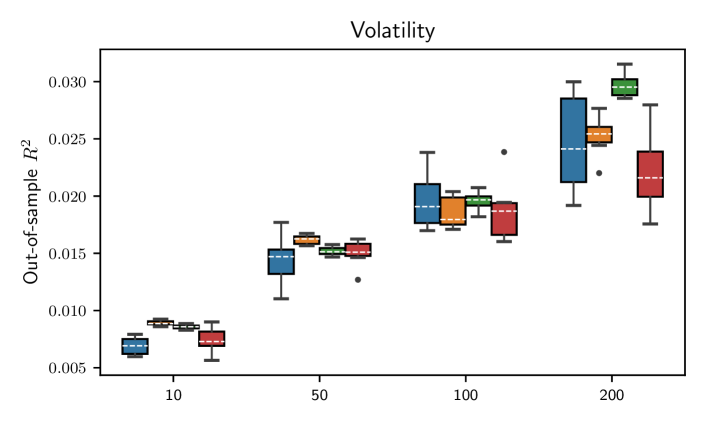

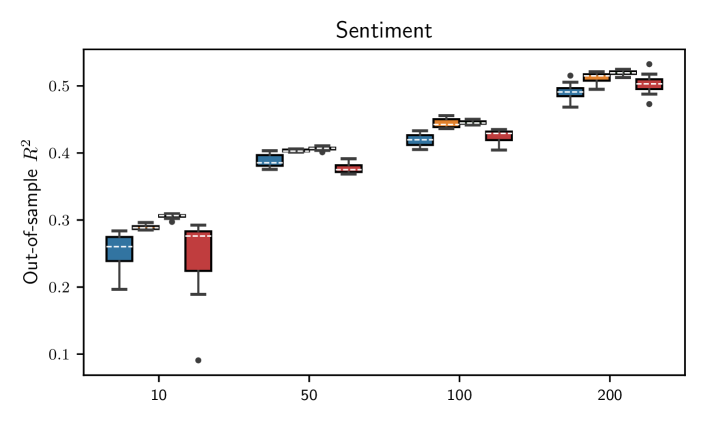

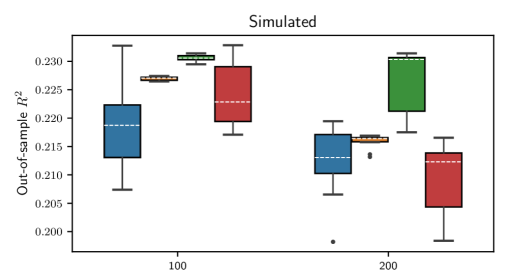

We compare results with four types of labels. As a benchmark, we use data simulated under the sLDA generative model; this allows us to compare methods when the model is correctly specified. We test 100- and 200-topic models using 5,000, 90,000, and 524, which is the average number of words per document in our TR data. Our simulated labels have an of 0.25 when regressed on topic frequencies. With the TR data, we let be either the stock return for each company in each period, or the squared return (volatility), or the same-trading-period news sentiment. The returns and volatilities are contemporaneous with the topic assignments. We include sentiment because it has an of around 0.5, whereas the s for returns and volatility are very small.

For each of these four types of labels, we compare four methods (LDA, Best-Of LDA, Branching LDA, and sLDA) through box plots of 10 predictive s for each method. (We use 10 to see a range of outcomes with reasonable computational effort.) We repeat the comparison for 10, 50, 100, and 200 topics, except that the simulated data uses only 100 and 200. For sLDA, we fix the parameter at the standard deviation of the labels . Using a fixed value reduces the risk of overfitting, and using the standard deviation of the labels (rather than an arbitrary value like 0.25) ensures that has roughly the right magnitude.

As can be seen from Figure 2, in all cases, the highest median performance (shown by a dashed white line in the box plots) is produced by either Best-Of or Branching LDA. This consistent pattern confirms the value of our overall approach to searching for topic models while avoiding overfitting.

In explaining returns (top panel), Branching LDA is the consistent winner at 10, 50, and 100 topics. In all comparisons, LDA and sLDA show the greatest dispersion in results. Best-Of and Branching produce more consistent results. In the context of the in-sample 0.45% for contemporaneous returns in (Tetlock et al., 2008), our 100- and 200-topic model results are impressive. It should be noted that our ’s are out-of-sample since we don’t re-estimate the vector in the holdout sample; this makes our results that much more noteworthy.

Finding topics to explain sentiment (third panel) should be an easier case for sLDA because sentiment has a much higher . But Branching LDA performs a bit better at all four numbers of topics.

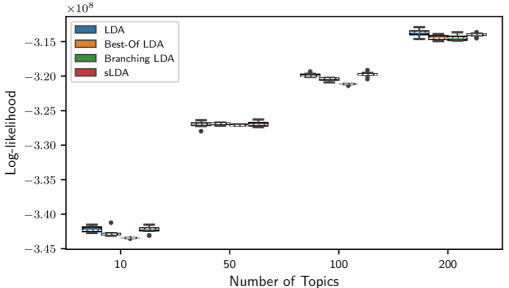

Figure 4 compares log-likelihoods across experiments for returns. These log-likelihoods are calculated from the training data for the text data only, ignoring the labels, following the standard procedure used for plain LDA. They therefore provide measures of the quality of fit to the text data. Two features stand out: at a given number of topics, there is very little variation within each method, and there is very little variation across methods. The methods perform roughly equally well in fitting the training text. Branching LDA achieves a slightly lower log-likelihood, but this is entirely appropriate given its higher predictive . By reinforcing the fit to the labels, we expect to give up some fit to the text.

As a check on the topics identified by the various methods, we show examples in Table 2. For each method, we pick the run that produced the highest predictive for returns in a 200-topic model. For each such winning run, we find the three most negative and most positive topics, as measured by the coefficient estimates . For each of these topics, we show the top 10 most probable words.

All of the topics displayed look sensible, and a couple show up consistently across methods. Of the LDA topics, the third negative and second positive topic are a bit surprising as candidates for most influential topics, as is the second most negative topic under sLDA. In contrast, Best-Of LDA and Branching LDA find interesting candidates for their most positive topics. These comparisons are anecdotal, but they support the quality of the text portion of models designed to explain returns.

| LDA | Coefficient | ||

| Negative | 1 | price cut drop fall fell lower declin analyst quarter weak | -0.098 |

| 2 | insid https video watch morn trade reut short transcript open | -0.011 | |

| 3 | climat coal carbon emiss energi cruis gas fuel environment norway | -0.009 | |

| Positive | 1 | quarter revenu analyst expect earn estim profit result forecast rose | 0.015 |

| 2 | korea korean hospit hca seoul tenet oper kim jin lee | 0.011 | |

| 3 | deal offer buy acquisit cash close merger bid combin agre | 0.011 | |

| Best-Of LDA | |||

| Negative | 1 | analyst fall stock drop cut fell forecast price declin expect | -0.090 |

| 2 | bankruptci debt file creditor apollo restructur oper fund protect manag | -0.013 | |

| 3 | store sale retail maci toy depart brand holiday subrat patnaik | -0.008 | |

| Positive | 1 | fund hedg manag investor activist capit elliott ackman stock invest | 0.014 |

| 2 | quarter revenu analyst expect profit estim rose earn forecast net | 0.011 | |

| 3 | deal offer buy acquisit close cash bid combin merger agre | 0.011 | |

| Branching LDA | |||

| Negative | 1 | quarter expect cut profit price analyst result forecast lower drop | -0.063 |

| 2 | store retail sale dollar sruthi maci home ramakrishnan general tree | -0.008 | |

| 3 | investig letter inform probe statement review request issu regul alleg | -0.008 | |

| Positive | 1 | board activist investor icahn sharehold elliott fund manag stake director | 0.019 |

| 2 | quarter revenu profit analyst earn expect cent net estim rose | 0.011 | |

| 3 | deal buy acquisit close merger combin agre transact acquir cash | 0.010 | |

| sLDA | |||

| Negative | 1 | quarter fell drop fall analyst expect declin forecast cut sale | -0.139 |

| 2 | solar energi power wind project renew electr sunedison panel develop | -0.007 | |

| 3 | ipo offer public price stock initi rang rais lanc net | -0.006 | |

| Positive | 1 | growth sale profit quarter expect revenu forecast result margin analyst | 0.016 |

| 2 | quarter revenu analyst cent expect profit estim earn rose net | 0.014 | |

| 3 | deal buy acquisit merger close combin busi acquir cash agre | 0.012 | |

7. Analysis of the Parameter

This section formalizes the observations in Section 4 on E-overfitting in sLDA. We examine what happens when the parameter is too small or when it is estimated through regression residuals.

7.1. Small

Building on (2.2), consider approximate posterior distributions

| (9) |

with and . We use the notation to emphasize that (9) is only an approximation to the true posterior in (2.2). We always use an approximation in practice because and are unknown.

For fixed , let the minimum taken over all possible assignments of the topics to the words in the corpus. denotes the minimum mean squared error (MSE) achievable for fixed . Denote by the set of topic assignments that achieve the minimum MSE for .

The value of at could be larger or smaller than the value of at the true coefficient vector , so is not a reliable measure of the ability of topics to predict the labels ; and, for , membership of in is not a reliable measure of the ability of the topic assignments to explain the data . In particular, for , there is no reason to expect that true or representative topic assignments are in .

Despite the fact that the topic assignments in are not particularly meaningful, we will see that the approximate posterior (9) concentrates probability on this set when is small, and largely ignores the information from the text data. Without an estimate of the true parameter , one may inadvertently choose too small. More importantly, the methods of (Zhang and Kjellström, 2014) and (Hughes et al., 2018) indirectly drive to smaller values by raising the Gaussian factor in the posterior to a power greater than 1.

For , let .

Proposition 7.1.

As , the approximate posterior (9) becomes concentrated on :

Proof.

This result shows that if is small then the approximate posterior concentrates probability on the topic assignments that approximate the labels well (the topic assignments in ), which may not be particularly meaningful, especially if . The topic model (through ) plays a secondary role by determining the relative weight of the assignments .

7.2. Residual

The breakdown in Proposition 7.1 results from using an arbitrary value for . An alternative is to use the standard regression estimate,

| (11) |

where, as before, is the number of documents and is the number topics. For any coefficient vector , consider the approximate posterior

| (12) |

Suppose (7) holds. In a document with words, the components of are multiples of , so can be approximated by to within , yielding the bound

| (13) |

Assume for simplicity that all documents have words. It follows that this choice of makes

| (14) |

With a large number of words per document , we can achieve a near-perfect fit to the labels through a “degenerate” assignment of words to just topics 1 and 2, as in (8), ignoring the text data.

In contrast to (14), we do not expect the standard deviation of the true errors (under the sLDA generative model) to vanish as increases. Nevertheless, we will show that the approximate posterior (12), based on the regression standard error estimate (11), overweights degenerate topic assignments achieving (8) and (14).

To make this idea precise, we need to consider a sequence of problems through which the number of words per document and the number of documents increase, holding fixed the number of topics and the vocabulary size . Within the LDA generative model, we can think of as derived from the first words in the first documents in an infinite array. The labels work slightly differently because depends on the proportions of topic assignments in document among the first words, so all change as increases. With approaching as increases, this is a minor point.

We want to compare the (approximate) posterior probabilities of two sets of topic assignments and , given . For , we have in mind topic assignments that ignore the words to achieve the near-perfect fit to labels in (8). We capture the idea that the assignments are more consistent with the true topic assignments by assuming that the resulting error standard deviation

| (15) |

remains bounded away from zero. (Under the sLDA generative model, with the true vector we expect to approach the true standard deviation .) Thus, we expect “good” topic assignments to belong to

whereas the “bad” topic assignments satisfying (8) belong to

We use the notation in (12), but we drop as an explicit parameter on the left to simplify notation. For any topic assignments and , the ratios and measure the relative (approximate) posterior probabilities of and given and (exact posterior probabilities) given , respectively. The ratio of ratios

measures how this relative probability is affected by the labels compared with the text . Larger values of indicate that the approximate posterior (12) with included shifts more weight to relative to . The following result shows that this ratio grows fast for and , indicating that (12) overwhelmingly shifts weight from “good” to “bad” topic assignments.

Proposition 7.2.

Roughly speaking, the limit in (16) says that grows faster than , for some , and (17) says that it grows faster than , for some . Thus, as either the number of words per document grows or the number of documents grows, (12) puts much more probability on than , relative to what the text model alone would do.

Proof.

From (12) we get

| (18) |

But

means that is bounded away from zero, so

;

and implies that , for

some constant , so .

Applying these limits

in (18) yields (16).

For (17), observe that because is bounded away

from zero as increases and is bounded above

by , for some , we have ,

for all sufficiently large , for some . As ,

(17) follows.

∎

8. Conclusions

We have developed an approach to finding topics in news articles to explain stock returns, volatility, and other types of labels. Supervised topic modeling requires balancing the ability of a model to explain labels and text simultaneously. We have shown that a standard stochastic EM approach to sLDA is vulnerable to serious overfitting. We avoid overfitting through a random search of LDA topic assignments while reinforcing configurations that perform well in cross-validation. Our approach improves over standard methods in tests on a large corpus of business news articles. The tools developed here are part of a broader investigation into differences between intraday and overnight news and returns.

References

- (1)

- Blei et al. (2003) David M Blei, Andrew Y Ng, and Michael I Jordan. 2003. Latent dirichlet allocation. JMLR 3, Jan (2003), 993–1022.

- Boyd-Graber and Resnik (2010) Jordan Boyd-Graber and Philip Resnik. 2010. Holistic sentiment analysis across languages: Multilingual supervised latent dirichlet allocation. In EMNLP. 45–55.

- Campbell (1991) John Campbell. 1991. A variance decomposition for stock returns. The Economic Journal (1991), 157–179.

- Griffiths and Steyvers (2004) Thomas L Griffiths and Mark Steyvers. 2004. Finding scientific topics. PNAS 101, suppl 1 (2004), 5228–5235.

- Hughes et al. (2018) Michael Hughes, Gabriel Hope, Leah Weiner, Thomas McCoy, Roy Perlis, Erik Sudderth, and Finale Doshi-Velez. 2018. Semi-supervised prediction-constrained topic models. In AISTAT. 1067–1076.

- Loughran and McDonald (2011) Tim Loughran and Bill McDonald. 2011. When is a liability not a liability? Textual analysis, dictionaries, and 10-Ks. Journal of Finance 66, 35–65.

- Mcauliffe and Blei (2008) Jon D Mcauliffe and David M Blei. 2008. Supervised topic models. In NeurIPS. 121–128.

- Nguyen and Shirai (2015) Thien Hai Nguyen and Kiyoaki Shirai. 2015. Topic modeling based sentiment analysis on social media for stock market prediction. In ACL. 1354–1364.

- Roll (1988) Richard Roll. 1988. R2. Journal of Finance 43 (3), 541–566.

- Tetlock et al. (2008) P. Tetlock, M. Saar-Tsechansky, and S. Macskassy. 2008. More Than Words: Quantifying Language to Measure Firms’ Fundamentals. Journal of Finance 63, 3 (2008), 1437–1467.

- Tetlock (2014) Paul C Tetlock. 2014. Information transmission in finance. Annu. Rev. Financ. Econ. 6, 1, 365–384.

- Zhang and Kjellström (2014) Cheng Zhang and Hedvig Kjellström. 2014. How to supervise topic models. In ECCV. Springer, 500–515.