Asymptotic Randomised Control with applications to bandits

Abstract

We consider a general multi-armed bandit problem with correlated (and simple contextual and restless) elements, as a relaxed control problem. By introducing an entropy regularisation, we obtain a smooth asymptotic approximation to the value function. This yields a novel semi-index approximation of the optimal decision process. This semi-index can be interpreted as explicitly balancing an exploration–exploitation trade-off as in the optimistic (UCB) principle where the learning premium explicitly describes asymmetry of information available in the environment and non-linearity in the reward function. Performance of the resulting Asymptotic Randomised Control (ARC) algorithm compares favourably well with other approaches to correlated multi-armed bandits.

Keywords: multi-armed bandit, Bayesian bandit, exploration–exploitation trade-off, Markov decision process, entropy regularisation, asymptotic approximation

MSC2020: 60J20, 93E35, 90C40, 41A58

1 Introduction

In many situations, one needs to decide between acting to reveal data about a system and acting to generate profit; this is the trade-off between exploration and exploitation. A simple situation where we face this trade-off is a multi-armed bandit problem, where one need to maximise the cumulative rewards obtained sequentially from playing a bandit with arm. The reward of an arm is generated from a fixed unknown distribution, which must be inferred ‘on-the-fly’.

More recently, multi-armed bandit problems are often formulated as a statistical problem (see e.g. [4, 20, 23, 11]), rather than an optimisation problem because of the computational cost. Many novel algorithms for bandit problems are often proposed using heuristic justifications and are then shown to give theoretical guarantees in terms of a regret bound. Even though these constructive designed algorithms works well in some settings, it still fails to address a few issues which may appear in learning. This includes asymmetry of information, incomplete learning and effect of the horizon (see Section 3.2).

This paper aims to address these issues by considering the multi-armed bandit problem as an optimisation problem for a Markov Decision Process (MDP) over an infinite time horizon, as originally proposed by Gittins and Jones [15]. The underlying state of the MDP corresponds to the posterior distribution which is an infinite state space and takes value in high dimension. Solving such an MDP is generally computationally infeasible. To overcome the computational issues, we modify the entropy regularised control formulation of Reisinger and Zhang [21] and Wang, Zariphopoulou and Zhou [32] to study discrete time bandit setting and obtain an asymptotic approximation to the value function when the posterior variance is relatively small. This approximation results in a randomised index strategy which enjoys a natural interpretation as a sum of the instantaneous reward (exploiting) and the learning premium (exploring).

The main contribution of this work is to develop conceptual insight into a general class of learning (bandit) problems from first principles. We aim to understand how to make decisions when information from each arm interacts with the others in asymmetric manner (i.e. when there is an arm which could be more informative than others), and also aim to understand the connection between reward, observation and learning mechanism when rewards are non-linear in the unknown parameter. Our result inspires the design of a learning algorithm which performs well numerically with cheap computational costs. In this work, we do not aim to provide a regret analysis of the derived algorithm.

The paper proceeds as follows. In Section 2, we describe how we formulate various classes of bandit problems in terms of a discrete-time diffusion process. By considering the diffusion dynamic in a regime with small uncertainty (e.g. small posterior variance), we propose the Asymptotic Randomised Control (ARC) algorithm together with a sketch derivation and summary of our main results. In Section 3, we give an overview of well-known approaches for bandit problems and discuss some limitations of these algorithms under a specific setting, and how the ARC algorithm addresses these limitations. We also discuss the connection between the resulting ARC algorithm and other approaches for bandit problems. In Section 4, we run a numerical experiment to show that when the uncertainty is small, the ARC algorithm is numerically accurate, and draw comparisons with other approaches for bandit problems in different settings. Finally, in Section 5, we provide a formal derivation of the ARC approach where the further technical results are given in the appendix.

Notation:

For any function , we write for a tensor of degree with dimension corresponding to the partial derivatives of . We write for Euclidean tensor products. In particular, is a standard inner product when are vectors and when and are square matrices. We also write for the corresponding Euclidean norm. For any (Borel) random variables and a -algebra , we write and for the conditional law of given and , respectively. We write , for the -th standard basis vector with an appropriate dimension, , and for the identity matrix with dimension . Throughout the proof, we shall introduce a generic constant to quantify an upper bound. This constant does not depend on variables introduced throughout the paper.

2 Asymptotic Randomised Control (ARC) approach

This section gives an overview of the Asymptotic Randomised Control (ARC) method for a general class of learning problem with a sketch derivation. We defer a rigorous mathematical justification to Section 5.

We first introduce a heuristic description of our learning (bandit) problem from Bayesian perspective. Let be an underlying (unknown) parameter with prior describing the rewards of our bandit system. When the -th arm, of the arms, is chosen at time , we observe a random variable where is independent for each conditional on and obtain a reward 333This particular structure allows our agents to observe more than just a reward.. The objective of our agent is to find a sequence of decisions taking values in based on available information to maximise

| (2.1) |

where and is the -algebra corresponding to our observation up to time .

We see from (2.1) that depends only on the posterior distribution of at time . Therefore, we can formulate the maximisation of (2.1) as a Markov Decision Process (MDP) with a posterior distribution as an underlying state.

2.1 Bandit structures

We first give a few examples of bandit structures where we can describe posterior distributions with a finite dimensional state process (taking values in an infinite state space).

2.1.1 Gaussian distribution for correlated structure

Suppose the prior for is a multivariate normal with dimension and the observation from the -th bandit at time is given by a -dimensional random vector with where and is a diagonal matrix with non-negative entries. We formally allow the -th entry of to be , if this is the case, we shall interpret that the -th component of is not observed.

For simplicity, we will demonstrate the calculation when all entries of are positive. The case with zero entries can be achieved either by simply taking the limit of the derived result or by considering each component separately.

Let denote the filtration describing our observation up to time . Suppose that our posterior at time is given by . By standard Bayesian inference, we can show that

where

By the Woodbury identity, , and hence

| (2.2) |

where .

Therefore, we can write the objective (2.1) as an MDP with the objective

| (2.3) |

where is the density of . The corresponding underlying state satisfying (2.2) is a discrete version of a diffusion process where the prior distribution is encoded as an initial state.

It is worth pointing out that this set-up covers various classes of multi-armed bandit problem which can be found in the literature:

Example 2.1 (Classical bandit).

Example 2.2 (Linear bandit).

Example 2.3 (Structural bandit).

The case when , and corresponds to the structural bandit studied in Rusmevichientong et al. [23].

Example 2.4 (Classical bandit with additional information).

Suppose , , , and the -th entry of is positive for all . In this case, the reward of the -th arm is only associated with the parameter (as only depends on the -th component of ). However, when the -th arm is chosen, we also observe some information associated to , provided that the -th entry of is positive. We will use this example to demonstrate learning with asymmetric information in Section 3.3.

Example 2.5 (Semi-bandit feedback).

Example 2.6 (Non-diagonal covariance structure).

Suppose that, when the -th arm is chosen at time , we observe with a corresponding reward function , where is a positive-definite matrix. By eigen-decomposition, we can write where is an orthogonal matrix and is a diagonal matrix with positive entries. Define , and . Since is invertible, observing is equivalent to observing and . Thus, we recover the prescribed framework.

2.1.2 General distribution for independent structure

Suppose that has a prior and when the -th arm is chosen at time , we observe Due to independence in the prior and observation, the posterior of also maintains independence of its components. Therefore, we can evaluate the posterior update of each separately.

For simplicity of discussion, we consider examples when is one-dimensional. The argument for more general cases can be easily extended to as long as and are a conjugate pair for all and . We implicitly allow to be degenerate, corresponding to the case when no information regarding is revealed when the -th arm is chosen.

In the following examples, we formulate the multi-armed bandit problem in terms of an MDP with an underlying discrete diffusion dynamic , as in (2.2). The process is interpreted as an estimator of , while is the inverse precision of the estimate evolving in a deterministic manner. Here, we will only illustrate the corresponding dynamics of the underlying state . The objective function can then be written in the same manner as in (2.3).

Example 2.7 (Binomial bandit).

Suppose that the prior of is and . We again denote by our observations up to time and assume that . When the -th arm is chosen at time , one can check that the posterior becomes with

| (2.4) |

where satisfies .

Example 2.8 (Poisson bandit).

Suppose that the prior of is and . Assume that . When the -th arm is chosen at time , the posterior becomes with

| (2.5) |

where satisfies .

2.2 From multi-armed bandit to diffusive control problem

Inspired by the dynamics (2.2), (2.4) and (2.5), we introduce a general framework of a discrete time diffusion control problem which can be used to studied the multi-armed bandit.

Let be a probability space equipped with two independent IID sequences of random variables and . We define the filtration . Here, represents a random seed used to select a random decision in each time step, whereas represents the randomness of the outcome.

At time , our agent chooses an action taking values in produced by randomly selecting from a probability simplex where is -predictable. Without loss of generality, we assume that where

Let be a collection of measurable functions describing our feedback actions. For each , we define the corresponding posterior dynamics by taking values in by and

| (2.6) |

where a measurable function is given in a form

| (2.7) |

with , , , .

We also write and . For notational simplicity, when clear from context, we will indicate as a subscript in the probability measure and omit the superscript on .

As illustrated in (2.1) and elaborated in (2.3), the objective of our control problem is to solve

| (2.8) |

where . We assume that satisfies the following assumption.

H. 1.

is -times differentiable, and there exists a constant such that for any with ,

H. 2.

is a compact set and there exists a constant and a norm on such that

-

(i)

For any and , .

-

(ii)

For any , and , .

-

(iii)

For any , and , , .

-

(iv)

For any , and ,

-

(v)

For any , and , we have

Conceptually, (H.2) says that our precision (our knowledge) of the parameter always improves with more observation. (H.2) says that the updated parameter estimate always lies in our parameter set . (H.2) are the structural assumptions allowing to express our results in terms of and . Finally, (H.2) appears naturally through the propagation of the information as discussed in (2.2), (2.4) and (2.5). (H.2) is the key assumption for the asymptotic analysis that will be considered in the later section.

Remark 2.1.

It is worth emphasising that the above set-up covers examples discussed in Section 2.1. In particular, if the expected reward is linear in and , then the corresponding function is linear in and does not depend on ; consequently becomes trivial. Furthermore, we also see that the dynamics (2.2), (2.4) and (2.5) can be written in the form (2.7) and satisfy (H.2)-(H.2), with appropriate norms and with , and , respectively. Moreover, we can see that (2.2) and (2.4) also satisfy (H.2). Unfortunately, does not satisfy (H.2) since is unbounded. We may overcome this issue by replacing with its smooth truncation to ensures that (H.2) holds and consider this as an approximation to the original Poisson bandit problem.

Remark 2.2.

We may modify (H.2) to consider an ergodic diffusion with small perturbation which is closely related to the Kalman-filtering theory. We state the corresponding assumption here for precision of our discussion. Nonetheless, we will focus on (H.2) for clarity, and discuss how to extend our analysis to this framework in Remark 2.4 and Theorem 2.4.

H. 3.

(H.2) holds with replaced by

-

For any and , .

2.3 Learning premia and index strategies (Inspiration of the ARC)

Solving (2.8) requires us to solve the Bellman equation with as an underlying state which is generally computationally intractable. Thanks to the nature of learning problems, we see from (H.2) that the state (which corresponds to the posterior parameters) will not change much when is small. In this section, we explore the intuition behind a few learning approaches, which inspire us to study the second order asymptotic expansion of (2.8) over small and obtain the ARC algorithm.

Consider the classical Gaussian bandit as discussed in Example 2.1, which corresponds to the case , , and is a family of diagonal matrices with positive entries. In this setting, Gittins [14] shows that the optimal solution to (2.8) is given in terms of an index strategy where the agent always chooses an arm to maximise an index where with increases in (see also [3, 24] for an approximation). In short, we see that the index is a sum of two terms:

| (2.9) |

where the exploitation gain describes the expected reward that the agent will obtain given the current estimate whereas the learning premium describes the benefit for learning.

This observation inspires an optimistic principle to design learning algorithms using an upper-confidence bound (UCB) (see e.g. [2, 16, 11]). Roughly speaking, the UCB approach chooses an arm based on an index of the form (2.9) where the learning premium scales with uncertainty of the estimate reward. Since we add uncertainty as an additional reward, one could interpret this as a claim that the agent should have a preference for uncertain choices (in order to encourage learning). This is a misleading conclusion as the following example shows.

Example 2.9 (Uncertainty Preference).

Let consider a bandit with two arms. Suppose that the reward of the first arm is sampled from where is not known, while the reward of the second arm is fixed and always . Suppose that we only collect the reward of the arm that we choose, but we always observe the reward of the first arm. Hence, we do not have to play the first arm to learn . Thus, most decision makers (without taking any risk/ uncertainty aversion) will choose arms purely based on the estimate of . In particular, they will choose the first arm if the estimate and choose the second arm otherwise.

In the above example, we see that the reward of the first arm is more uncertain than the second arm, but a preference for uncertainty does not benefit our decision444In fact, in many behavioural models, people display a bias (pessimism) against risk and uncertainty (see e.g. [7, 17, 19] for general settings and [8] for the classical bandit setting). In practice, many decision makers still prefer the second arm in Example 2.9 even if to avoid risky and uncertain outcomes.. A better interpretation of the optimistic principle is that we have a preference for information gain or the ‘reduction’ in uncertainty (rather than the uncertainty itself). In the case of classical bandit, the information gain corresponds to the uncertainty of the estimate which suggests the misleading conclusion that we prefer an uncertain choice.

The above observation leads us to ask, ‘how we can quantify information gain?’ Consider a simple greedy approach, where we always stick with the best policy from the estimate at time , i.e. for a fix , let where . Since ,

| (2.10) |

the first inequality follows from the fact that we cannot make a better decision than the best decision with known , and the second inequality follows from the Gaussian maximal inequality (see e.g. Chernozhukov et al. [6, Theorem 1]).

The greedy strategy could be interpreted as a first order approximation to the optimal solution, considering only Exploitation gain in (2.9). This decision introduces error (relative to the best strategy) with order . This perspective suggests an index (like) strategy, where we choose the learning premium as a second order approximation (with respect to ).

Unfortunately, as discussed in Reisinger and Zhang [21] in a continuous time setting, the solution to (2.8) is, in general, non-smooth and thus difficult to obtain asymptotic approximation. To overcome this difficulty, we introduce an entropy regularisation (see also [32, 33]) to analyse (2.8) when is small. We later show that this approximation (and its corresponding strategy) introduces error with order , compared to for the naive greedy approach.

2.4 From a regularised control problem to ARC algorithm

In this section, we will use an entropy regularised control to construct an approximation to the value function (2.8) and sketch a derivation of the corresponding ARC algorithm to solve the diffusive control problem, introduced in Section 2.2. The proof of the error of the approximation will be provided in Section 5.

We first observe that for , we can approximate the maximum function by

| (2.11) |

where is a smooth (entropy) function and is a small regularisation parameter. We also observe that a standard corollary to Fenchel’s inequality (see e.g. Rockafellar [22]) yields

| (2.12) |

Remark 2.3 (Shannon Entropy).

Definition 2.1.

Let be a smooth entropy (Definition 5.2) and . Define

| (2.13) |

As inspired by the discussion in Section 2.3, we would like to construct a function where the -th component of corresponds to an ‘incremental reward’ over a single step for choosing the -th option. In particular, let us assume that when is sufficiently small, the value function (2.13) is approximated by the maximum amongst the values of the available options, i.e.,

| (2.14) |

By the dynamic programming principle and the dynamic (2.6)-(2.7), we can rewrite (2.13) as

| (2.15) | ||||

| (2.16) |

Using the approximation (2.14) on the LHS and applying (2.11), we obtain from (2.16) that

In particular, this suggests the approximation

| (2.17) |

Since our dynamics form a discrete diffusion process, a discrete-time version of Ito’s lemma suggests that we can choose

| (2.18) |

where is given by

| (2.19) |

Here, , and ,

| (2.20) |

where (which is determined by for the case of Shannon Entropy given in Remark 2.3).

2.5 Description of the main results

In earlier section, we introduce an entropy regularisation and obtain an approximation of . Unfortunately, derivatives of the smooth approximation explode as . This means that approximation error (2.21) may explode if we take while fixing . Therefore, we will quantify errors in terms of and .

Theorem 2.1 (Error bound in the regularised control problem).

Introducing the entropy regularisation in (2.13) yields an error while error bounds for our approximation (Theorem 2.1) explodes as . To solve the unregularised problem (2.8), we choose the regularised parameter as a function of to balance the trade-off between the regularisation error and the approximation error.

Theorem 2.2 (Error bound in the unregularised control problem).

We see from (2.22) that when , this asymptotic strategy introduces error of order , compared with for the naive greedy approach (Section 2.3).

The follow theorem shows that our approximate optimal strategy can identify the true model parameter asymptotically when the expected cost is uniformly bounded.

Theorem 2.3 (Complete learning).

Suppose that (H.1) and (H.2) and let be such that for some constant and . Suppose further that

-

(i)

For any policy , the event 555This says that if every arm is chosen infinitely often, then the path corresponding to converges to ..

-

(ii)

The cost function is uniformly bounded.

-

(iii)

The function where is a smooth entropy function (Definition 5.2) satisfies666The Shannon entropy satisfies this property.: for any compact set , there exists a non-empty open ball, , such that .

Then for all , a.s. where is the path of the parameter corresponding to the feedback policy .

Remark 2.4.

Our main results assume (H.2), which is inspired by the multi-armed bandit problem (Section 2.1) for learning. The nature of the learning results in a transient state process for . This is reflected in (H.2) where our precision is non-increasing over . In general, we can extend our approximation result to the case when our precision is recurrent and takes value in a (small) compact set , as often happens when using more general Kalman filtering settings. All of our analysis follows by using and for all . In particular, we have the following theorem.

2.6 Summary of the ARC Algorithm

We now summarise how our approximation of the regularised control problem yields an explicit algorithm for a (correlated) multi-armed bandit.

Recall the setting of our bandit which has arms with an unknown parameter as described at the beginning of Section 2. When the -th arm is chosen, we observe a random variable and obtain a reward . Suppose further that the observation distribution and the prior of the unknown parameter form a conjugate pair for all and we can parameterise the posterior distribution by such that the dynamics of these posterior parameters satisfy (H.2). Broadly speaking, will be a posterior mean of and will behave as a posterior variance (or some quantity which is inversely proportional to the number of observation).

In summary, to use the ARC algorithm, we need to evaluate some functions explicitly and choose a few hyper-parameters for the decision making.

Hyper-parameters

-

(i)

The discount factor : This parameter reflects how long we are considering this sequential decision. A heuristic choice is where is the number of rounds of decisions.

-

(ii)

Smooth max approximator : This is a function to approximate the maximum function (which yields the corresponding entropy ). For computational convenience, we propose to take which corresponds to the Shannon entropy, . More general choices of can be chosen by considering Definition 5.2.

-

(iii)

Regularised function : We choose a regulariser (a function of and ) to reflect our learning preferences. We see in (2.22) that choosing where gives the least order for the sub-optimal bound.

Relevant functions

-

(i)

The expected reward and its first two derivatives: We need to evaluate and compute and .

-

(ii)

Evolution of posterior parameter: Let be the posterior update after observing . We need to evaluate

-

(iii)

Learning function: Given hyper-parameters and problem environment (), we can evaluate the function via (2.19) with and write .

We describe the procedure of the ARC algorithm as follow.

3 Comparison with other approaches to bandit problems

3.1 General Approaches

There are various approaches to study bandit problems, and theoretical guarantees are typically proved in specific settings (see e.g. Lattimore and Szepesvári [20]). We summarise the broad idea of a few approaches and extend them to our setting using Bayesian inference when needed. For simplicity, we write and , write for the posterior/prior of with the parameterisation and write for the posterior update of when the -th arm is chosen.

- •

- •

- •

-

•

Upper Confidence Bound (UCB) [1, 2, 16] : At each time , we choose an arm with the maximum index where is the number of plays, is the -quantile of the random variable conditional on the posterior parameter . Here, is a hyper-parameter that can be chosen by the decision maker. Kaufmann et al. [16] prove a theoretical guarantee of optimal order for the Bernoulli bandit when ; their simulations suggest that typically performs best.

N.B. There are many variations of the UCB algorithm proposed in various settings. The algorithm described above is known as the Bayes-UCB which has a clear extension to the general setting described in this paper.

-

•

Knowledge Gradient (KG) [28]: At each time , we choose an arm with the maximum index .

N.B. In [28], the KG algorithm is proposed for the classical and linear Gaussian bandit together with an explicit expression for . In general, we may estimate this expression by using Monte-Carlo simulation, but this can be costly.

- •

ARC as a combination of the other algorithms:

The ARC algorithm appears as a combination of KG and BE through Itô’s lemma, which results in a random index decision whose index can be decomposed as the sum between Exploitation gain, , and Learning premium, , as in UCB. This learning premium takes into account asymmetry of available information and a curvature when the reward is non-linear (see section 3.3 for explicit evaluation of ).

More precisely, recall that ARC makes choices based on the (arg)softmax which fundamentally picks an arm with the maximum index . This maximum is determined at random as in the BE, but using a modified index as in UCB. The decision is modified through the learning term , which can be seen as . In short, is an approximation of the KG index using smooth max approximation and a second order expansion through Itô’s lemma.

Computation Efficiency:

-GD, BE, TS, UCB and ARC are algorithms where we can often find an explicit expression and thus requires low computational power. KG, on the other hand, requires evaluation of the expectation of the maximum involving a high-dimension state (which only has an explicit expression in the Gaussian case). Implementing KG in general can be achieved by Monte-Carlo simulation which is costly. Similarly, the IDS requires evaluation of one-step regret and information gain which is expensive in general.

3.2 Shortcomings of bandit algorithms

Even though many of the algorithms discussed in Section 3.1 perform well in many settings, they may fail to address a few phenomena which may appear in learning. For clarity, we shall illustrate these shortcomes in extreme scenarios. Many practical examples of these scenarios can be found in Russo and and Roy [26].

Incomplete Learning:

Consider a decision rule which depends only on the posterior parameter . If we start with a bad posterior/prior, we may end up always choosing the worse option, if our early experiences are misleading.

Consider a bandit with arms: The first arm always gives a fixed reward; the second arm’s reward is generated from an unknown distribution. For any strategies that satisfy the property described above, whenever this strategy decides to play the first arm, it will never play the second arm again. However, we can see that if the mean reward of the first arm has unbounded support, the probability that the reward of the first arm is larger than the second arm is strictly positive. This probability never changes when the first arm is abandoned. This means that we have a strictly positive probability of always playing sub-optimal options.

This is a problem for -GD (when ) and KG algorithms.

Information Ignorance:

Many works on bandit assume that all arms have an identical structure. Therefore, they fail to capture the setting where each arm provides different information.

Consider a bandit with arms where every arm except the first always gives a strictly positive reward from an unknown distribution. The first arm is informative but yields no reward; it always gives a reward , but will allow us to observe rewards of all other arms. Playing the first arm helps us to learn faster. Unfortunately, this arm will be ignored by many bandit algorithms as it never has the best reward and many bandit algorithms choose an arm based on the posterior distribution for the reward, but do not consider the information gain.

This is a problem for -GD (when ), TS, and UCB algorithms. It is worth noting that BE and -GD (for ) only choose the first arm by random. Hence, they still play worse arms, even if they do not give any meaningful information and never yield the best reward.

Horizon effect:

A few algorithms are designed based on the principle that the decision should not vary when the terminal time is far away and hence propose a stationary policy. When the horizon is short, these algorithms may still choose to explore, even if these explorations do not benefit future decisions.

This is a problem for -GD, BE, TS and IDS algorithms.

3.3 Addressing Learning using ARC

The ARC algorithm addresses flaws discussed in Section 3.2 . Since we can vary a hyper-parameter , which has a natural interpretation as the future weight, we directly address the horizon effect . We also see in Theorem 2.3 that ARC is a complete learning algorithm in the sense that the uncertainty parameter (posterior variance) converges to as which means that we can asymptotically identify the true parameter .

To see how ARC address the information ignorance, we consider an explicit computation of the ARC algorithm for the Gaussian bandit with additional information (Example 2.4).

We recall the setting of this example here for convenience of the reader. When the -th arm is chosen, we observe a random variable for where and collect the reward . We see that the reward of the -th arm depends only on and the reward of each arm also differs depending on the function . Furthermore, when is small, the variance of the observation is large. This mean that choosing the -th arm tells us very little about . In other words, our information on the reward of the -th arm does not improve much when is small (and vice versa for large ).

Assume that the Shannon entropy (Remark 2.3) is used as our regulariser. The decision maker chooses using the (soft-) argmax of the index where we can give an explicit expression (see Lemma A.5) for by

| (3.1) |

The term can be interpreted as a learning premium for choosing the -th arm describing the reduction of uncertainty as discussed in Section 2.3. describes the importance of the future in our preferences. comes from summing the (learning) benefit of playing the -th arm to the -th arm: describes how much we can reduce uncertainty of the -th arm777One can see from (2.2) that this quantity describes the reduction in the (uncertainty) parameter .; represents the uncertainty, while tells us how much information we would gain. We also have the term which rescales the learning benefit due to how our parameters impact the reward function (in particular, the curvature of the reward). Finally, the term describes how much we actually need to learn. In particular, when we have an arm such that for , the -th arm is much better than the others, and we probably do not need to learn further. In this case, we have and for all .

4 Numerical Experiments

In this section, we run numerical experiments to illustrate the accuracy of the approximation and run a simulation to compare performance of the ARC algorithm to other algorithms.

4.1 Comparison to the optimal solution for bandit

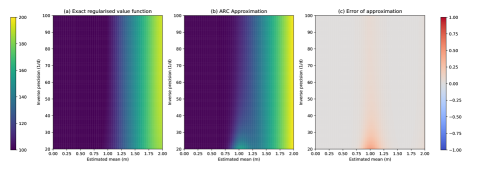

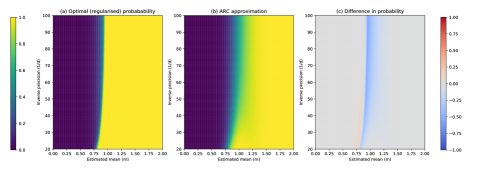

To illustrate that our approximation gives a reasonable answer, we compare our estimated value function and its corresponding control to the exact value function in a simple setting.

Suppose that our bandit has two arms. The first arm always gives the reward ; the second arm always gives reward . We observe the reward of the first arm only when the first arm is chosen. Formulating this as a relaxed control (2.13) with dynamic in (2.2) gives

with and . The transition (2.7) of the problem is given by

We solve the above problem explicitly using Monte Carlo simulation. In particular, we start our iteration with and iteratively compute on the grid ,

where is the number of Monte Carlo simulations and are such that . We then interpolate and repeat the procedure until converges to . The corresponding optimal (feedback) probability to choose the first arm is given by

where . On the other hand, our ARC approximation gives

where and .

We now compare with when and . In the numerical experiment, we use and consider and . We see in Figure 1 (which shows the value functions) and Figure 2 (which shows the probability of choosing the risky arm) that the ARC approximation gives a close estimate of the regularised problem.

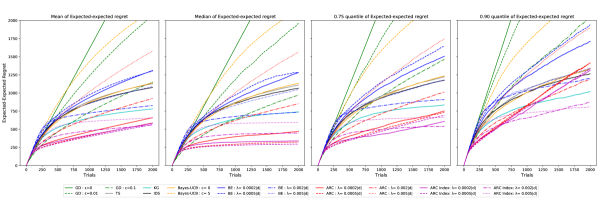

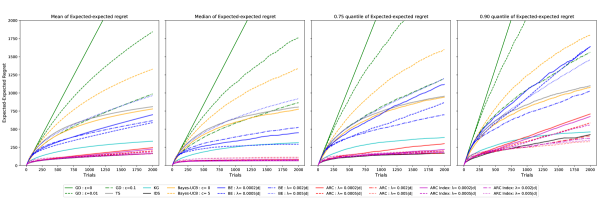

4.2 Simulation results

A common performance measure which is used in the multi-armed bandit literature [26, 11, 4, 16, 18] is the regret

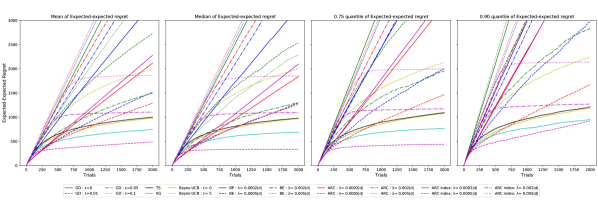

In this section, we will compare the regret of the ARC algorithm with other approaches described in Section 3.1 under environments; classical bandit, bandit with an informative arm and linear bandit. In each of these environments, we consider decisions on a -armed bandit with horizon steps over simulations. In the -th simulation, we sample the true parameter and then simulate interaction between each of the algorithms and the environment with the parameter starting from an initial belief corresponding to a non-informative prior. We then use our simulated output to demonstrate means, medians, 0.75 quantiles and 0.90 quantiles of the map for each of our considered algorithms.

Simulation Environment:

We consider the following environment for our simulation. Let be an unknown parameter taking values in .

-

•

Classical bandit. When choosing the -th arm, we observe and receive the reward sampled from the distribution .

-

•

Bandit with an informative arm. When choosing the -th arm with , we observe and receive the reward sampled from the distribution . When the -st arm is chosen, we receive a reward sampled from and in addition, we observe a sample from . In particular, playing the first arm allows us to observe the rewards of other arms without choosing them, but this arm yields a smaller reward than others.

-

•

Linear bandit. When choosing the -th arm, we observe and receive a reward sampled from the distribution where for and .

Hyper-parameters of bandit algorithms:

We will consider the KG and IDS by introducing Monte-Carlo samples to evaluate the required expectations. We will set the parameter for KG and ARC. The function considered in the BE and ARC will be given in the form where is the matrix operator norm and use Shannon entropy (Remark 2.3) to regularise the ARC algorithm. Unmentioned hyper-parameters will appear as a description of the algorithm in the regret plot.

ARC index strategy:

For numerical efficiency, we introduce an index strategy inspired by the ARC algorithm. In contrast to the ARC, instead of making a decision based on the probability simplex with given in (2.18), we simply choose the arm which maximises .

Discussion of numerical simulations:

We see in Figures 3, 4 and 5 that both ARC and ARC index strategy with appropriate hyper-parameter perform very well compared to other algorithms. We see that the ARC approaches perform significantly better than other approaches in the setting for the bandit with an informative arm. This performance is as good as IDS but requires significantly lower computational cost, since every term can be evaluated explicitly. In fact, the computational cost of the IDS proved too expensive to demonstrate for the linear bandit with arms and was therefore omitted.

The ARC algorithm derived in this paper performs well with appropriate hyper-parameter choices. It is also worth pointing out one obstacle found in the derived ARC algorithm when running numerical simulations with many arms available. We see that taking may not allow to decay sufficiently fast (even though Theorem 2.3 ensures that this ultimately converges to ). In particular, with many arms, we should be able to identify some arms which are significantly worse than the others. Such arms will be rarely played, which leaves large for a long time. We found in the numerical simulation that when following the ARC procedure, the agent identifies the reward of the very best few arms correctly (i.e. we obtain close estimates to the rewards of a few best arms). Unfortunately, since does not decay sufficiently fast, this leads the ARC algorithm to randomly choose among some small number of options, even if it identifies the best arm correctly. This explains why we observe linear trends in the regret plot for the simple ARC but with a low gradient.

To overcome this effect, we considered the ARC index strategy, which does not require to decay to zero to terminate decision to a single (best) arm. Here, we see in Figure 3, 4 and 5 that the gradient of the regret of the ARC index converges to zero, that is, we eventually identify the best arm. In general, one may also choose the function depending on to truncate our consideration to the best arm.

5 Proof of the main results

5.1 Convex analysis and smooth max approximator

In (2.11) and (2.12), we briefly introduce and as a smooth version of the maximum function and its derivative, obtained via the convex conjugation of the regularisation function . One well-known choice of which gives an analytical expression is the Shannon entropy. We can also consider other choices of by constructing the smooth max approximator explicitly888Examples of explicit constructions can be found in Zhang and Reisinger [21, Remark 3.1]..

We observe that in (2.11) can be expressed as where

| (5.1) |

In particular, is the convex conjugate of (see e.g. Rockafellar [22]). In fact, (5.1) is also known as a ‘nonlinear expectation’ 999Nonlinear Expectations (or equivalently ‘risk measures’) are a classical tool in mathematical finance to study decision making under uncertainty. defined on a finite space (see Coquet et al. [9]).

Definition 5.1.

We say a function is a convex nonlinear expectation if it satisfies:

-

(i)

Monotonicity: If , then ;

-

(ii)

Translation Equivariance: For all , ;

-

(iii)

Convexity: For any , ;

where the inequalities are interpreted component-wise.

The following theorem shows that using as a smooth max approximator is equivalent to having bounded. This will allow us to quantify the difference between a non-regularised (2.8) and regularised control problem (2.13) by . The proof is given in Appendix A.

Theorem 5.1.

Let be a convex nonlinear expectation. The following are equivalent.

-

(i)

There exists such that for all .

-

(ii)

There exists such that .

-

(iii)

There exists a bounded function such that (5.1) holds.

-

(iv)

For , we have as .

We now introduce a smooth entropy regulariser as the convex conjugate of a smooth max approximator.

Definition 5.2.

We say a function is a smooth max approximator if it is a -times differentiable convex nonlinear expectation with uniformly bounded derivatives such that Theorem 5.1 holds. We say a bounded function is a smooth entropy if is a convex conjugate of some smooth max approximator101010One can check that the Shannon Entropy (Remark 2.3) is a smooth entropy..

For a smooth max approximator , we write , and .

Remark 5.1.

If is a smooth max approximator, then and are uniformly bounded. Moreover, it follows from Fenchel’s inequality that In particular, can be interpreted as a smooth version of the argmax, as in (2.12).

5.2 Analysis of the regularised control problem over finite horizon

The objective of this section is to approximate the finite horizon value function as a sum of the (smooth) maximum of the incremental rewards.

Definition 5.3.

Let be a smooth entropy (Definition 5.2) and . Define

| (5.2) |

We will show that , with an approximate optimal policy . Here, the incremental reward with -steps to go is

| (5.3) |

where is given in (2.19).

The idea behind the analysis is to consider an asymptotic expansion as . Due to our learning structure (H.2), the change in the underlying state are (in expectation) of order . Hence, the global Lipschitz property of implies that the instantaneous reward changes with . Hence, we can use Taylor’s theorem to obtain an asymptotic expansion in and keep the terms up to order .

We first show that the perturbation error in the learning term is of order and can be ignored in our approximation. The proofs of the following two lemmas are in Appendix A.

Lemma 5.2.

Now, we consider the second order approximation of the smooth maximum over the incremental reward . We show that is the second order approximation (in expectation) of the (smooth) maximum incremental reward.

Lemma 5.3.

Since describes an incremental reward with -steps to go, we may approximate the optimal value function (5.2) by with an estimate optimal strategy .

Theorem 5.4.

Proof.

We will prove by induction that the upper-bounds for (5.4) and (5.5) are given by where is a constant in Lemma 5.3.

It is clear from (2.11) that . Hence, the required inequality holds for .

Assume that the required inequality holds for .

Define We see that

| (5.6) |

where the second equality follows from substituting and the final inequality follows from (2.11)-(2.12) and the fact that

By our inductive hypothesis, Lemma 5.3 and (H.2), we see that

Similarly, to prove (5.5), we define in the same manner as but replace by . The similar argument yields for all and .

5.3 Analysis of the regularised control problem over infinite horizon

We see that the error bound of our approximation in Theorem 5.4 is uniform in . We can now prove Theorem 2.1 by taking in Theorem 5.4.

Proof of Theorem 2.1.

Fix and .

Since as , it follows from a Tauberian theorem (Theorem A.2) that

| (5.7) |

Next, we will prove that as . By (H.2) together with the Cauchy–Schwarz inequality, we can show that for any , . In particular, . By (H.1), there exists a constant , such that

| (5.8) |

Moreover, since is a smooth entropy, is bounded and so as . Combining this with (5.8), we obtain

| (5.9) |

For any policy , let . By the similar argument as in (5.8), we can find a constant such that . Since and , it suffices to show that for any fixed , as . Given this, the required convergence follows from a Tauberian theorem (Theorem A.3).

Fix . By (H.1) and (H.2), there exists a constant such that for all . For any , it follows from the mean value inequality that

| (5.10) |

Fix and choose such that, for all , we have .

As discussed in Section 2.2, we recall that the action corresponding to the policy is given by . By (5.10), for , the probability that the actions corresponding to and disagree at time , provided they agree up to time , satisfies

Let be the the event that the actions corresponding to and agree up to time , i.e. . This gives , i.e. .

5.4 Analysis of the (unregularised) control problem

This section is dedicated to prove Theorem 2.2.

Proof of Theorem 2.2.

Through the following argument, let be a generic constant, depending only on and the bounds in (H.1) and (H.2) which could be different between lines.

We will first show that there exists a constant such that

| (5.12) |

where .

Observe that

and write

| (5.13) |

Since is bounded, for any , for all and for all . Combining this observation with (5.13) and Theorem 2.1, we see that

Since is compact, . Therefore, (5.12) follows from our assumption that for some constant .

Let be the optimal (stationary) feedback policy of (2.8), i.e. . For each , let

We next show, by induction, that where with the constant given in (5.12).

It is clear from the definition of that the required inequality holds for . Assume that the required inequality holds for . Observe that

where . By the induction hypothesis and (H.2), , and thus . Hence, the induction step follows from (5.12).

The main inequality of this theorem follows from the fact that as which can be proved in the similar manner as the proof that as in Theorem 2.1. ∎

5.5 Complete Learning

We have discussed in Section (3.2) that some bandit algorithms e.g. greedy or KG may suffer from incomplete learning. Theorem 2.3 show that the ARC algorithm overcomes this limitation, in the sense that as . This section is dedicated to prove this result.

Proof of Theorem 2.3.

By (H.1), (H.2) and the fact that , there exists a constant such that . Since and is compact, is uniformly bound on . Combining this with the boundedness of yields for some constant .

Fix , and and consider the events , and .

For , takes values in a compact set. Hence, there exists such that for . In particular, for any , as . Therefore,

We can deduce from assumption that . Therefore, . The required result follows by considering the event . ∎

Appendix A Proofs of relevant results

Theorem A.1 (Robust Representation).

A convex nonlinear expectation admits a representation of the form where and

Furthermore, is the maximal function which represents , i.e. if there exists such that (5.1) holds with , then for all .

Proof of Theorem 5.1.

: Fix . Consider where for all and is the -th basis vector in . By , . Hence, .

As is arbitrary, it follows that . The result then follows by considering intersection over all .

:

By Theorem A.1, we can write where with

As and ,

Moreover, by (5.1), we have . Therefore, is bounded.

:

Fix and define . Then

Hence, as .

Find such that

By rearranging the inequality above, the result follows. ∎

Proof of Lemma 5.2.

Through the following argument, let be a generic constant, depending only on and the bounds in (H.1) and (H.2) which could be different between lines.

Recall expressions for , , from (2.20). Since is -times differentiable with bounded derivatives (H.1), the terms , , and are differentiable with bounded derivative. Moreover, since is a smooth entropy, the corresponding smooth max approximator has a bounded derivative. In particular, and . For , it follows from the mean value inequality that

By similar arguments as above applying to (H.2), we show that for any , and , .

where is defined to be a rectangle in and the final inequality follows from the convexity of the norms and (H.2).

Proof of Lemma 5.3.

Let where is a given constant. By (H.1) and Definition 5.2, is 3-times differentiable. Consider the Taylor’s approximation

| (A.1) |

where all derivatives are evaluated at and denotes the remaining terms.

By (H.1) and Definition 5.2, the second and third derivatives of are . Moreover, by (H.2), and . Applying these bounds to the third order terms and the remaining second order term, we obtain . Here, the bounded constant is uniform over .

Taking the expectation of (A.1), we see that

| (A.2) |

where . Now write

| (A.3) |

From Definition 5.2, for . By (H.1), any terms involving derivatives of in (A.3) are uniformly bounded. By the mean value theorem and (H.2), (A.2) yields

| (A.4) |

where .

Denote . Consider . We see that . Therefore, (A.4) yields

| (A.5) |

Since the first derivative of is bounded and does not depend on , it follows from the mean value theorem that

| (A.6) |

where the final inequality follows from Lemma 5.2. Combining (A.5) and (A.6), the result follows.

∎

Theorem A.2 (Tauberian theorem 1).

Let be a real-value sequence converging to and . Then as .

Proof.

Fix and find such that for all , . Since is also bounded, we can find such that for any , for all . Hence, for any ,

Hence, . Since is arbitrary, we obtain the required result. ∎

Theorem A.3 (Tauberian theorem 2).

Let and be functions with a constant such that and as for all . Then for any , as .

Proof.

Fix and find such that for all and , where such exists due to the linear growth condition.

Since as , we can find such that for any , for all . For any ,

Hence, . Since is arbitrary, we obtain the required result. ∎

Lemma A.4.

Consider the case when and . Suppose that , and where is sufficiently smooth and . Then for every ,

Proof.

Since is sufficiently smooth, and . By integration by parts, . Substituting this into the expression for , the result follows. ∎

Lemma A.5.

Proof.

Lemma A.6.

For the one-dimensional linear bandit with and prior with Shannon entropy (Remark 2.3), we have

where .

Proof.

We note that and we have

In particular, Substituting these into Lemma A.4, we can write and obtain the required result. ∎

References

- [1] R. Agrawal, Sample mean based index policies by regret for the multi-armed bandit problem, Advances in Applied Probability, (1995), pp. 1054–1078.

- [2] P. Auer, N. Cesa-Bianchi, and P. Fischer, Finite-time analysis of the multiarmed bandit problem, Machine Learning, (2002), p. 235–256.

- [3] M. Brezzi and T. Lai, Optimal learning and experimentation in bandit problems, Journal of Economic Dynamics and Control, (2002), pp. 87–108.

- [4] G. Burtini, J. Loeppky, and R. Lawrence, A Survey of Online Experiment Design with the Stochastic Multi-Armed Bandit, arXiv:1510.00757v4, (2015).

- [5] N. Cesa-Bianchi, C. Gentile, G. Lugosi, and G. Neu, Boltzmann Exploration Done Right, in NIPS’17: Proceedings of the 31st International Conference on Neural Information Processing Systems, 2017.

- [6] V. Chernozhukov, D. Chetverikov, and K. Kato, Comparison and anti-concentration bounds for maxima of Gaussian random vectors, Probability Theory and Related Fields, (2013).

- [7] S. N. Cohen, Data-driven nonlinear expectations for statistical uncertainty in decisions, Electronic Journal of Statistics, (2016), pp. 1858–1889.

- [8] S. N. Cohen and T. Treetanthiploet, Gittins’ theorem under uncertainty, Electronic Journal of Probability, (2022), pp. 1–48.

- [9] F. Coquet, Y. Hu, J. Mémin, and S. Peng, Filtration consistent nonlinear expectations and related -expectations, Probability Theory and Related Fields, (2002), pp. 1–27.

- [10] E. Even-Dar, S. Mannor, and Y. Mansour, Action elimination and stopping conditions for the multi-armed bandit and reinforcement learning problems, Journal of Machine Learning Research, (2006).

- [11] S. Filippi, O. Cappé, A. Garivier, and C. Szepesvári, Parametric bandits: the Generalized Linear case, in NIPS’10: Proceedings of the 23rd International Conference on Neural Information Processing Systems, 2010.

- [12] H. Föllmer and A. Schied, Stochastic Finance: an introduction in discrete time, De Gruyler, 2016.

- [13] M. Frittelli and E. R. Gianin, Putting order in risk measures, Journal of Banking & Finance, (2002), pp. 1473–1486.

- [14] J. Gittins, Multi-armed Bandit Allocation Indices, John Wiley and Sons, 1989.

- [15] J. C. Gittins and D. M. Jones, A dynamic allocation index for the sequential design of experiments, in Progress in Statistics, J. Gani, ed., Amsterdam: North Holland, 1974, pp. 241–266.

- [16] E. Kaufmann, O. Cappé, and A. Garivier, On Bayesian Upper Confidence Bounds for Bandit problems, in Artificial intelligence and statistics, 2012, pp. 592–600.

- [17] J. M. Keynes, A Treatise on Probability, Macmillan and Co., 1921. Reprint BN Publishing, 2008.

- [18] J. Kirschner and A. Krause, Information directed sampling and bandits with heteroscedastic noise, Proceedings of Machine Learning Research, (2018), pp. 1–28.

- [19] F. H. Knight, Risk, Uncertainty and Profit, Houghton Mifflin, 1921. reprint Dover 2006.

- [20] T. Lattimore and C. Szepesvári, Bandit Algorithms, Cambridge University Press, 2019.

- [21] C. Reisinger and Y. Zhang, Regularity and stability of feedback relaxed control, SIAM Journal on Control and Optimization, (2021), pp. 3118–3151.

- [22] R. Rockafellar, Convex Analysis, Princeton university press, 1972.

- [23] P. Rusmevichientong, A. Mersereau, and J. N. Tsitsiklis, A Structured Multiarmed Bandit Problem and the Greedy Policy, in Proceedings of the IEEE Conference on Decision and Control, 2009.

- [24] D. Russo, A note on the equivalence of upper confidence bounds and gittins indices for patient agents, Operations Research, (2021), pp. 273–278.

- [25] D. Russo and B. V. Roy, An information-theoretic analysis of thompson sampling, Journal of Machine Learning Research, (2016), pp. 1–30.

- [26] , Learning to Optimize via Information-Directed Sampling, Operations Research, (2017), pp. 1–23.

- [27] D. Russo, B. V. Roy, A. Kazerouni, I. Osband, and Z. Wen, A tutorial on thompson sampling, Foundations and Trends in Machine Learning, 11 (2018), pp. 1–96.

- [28] I. O. Ryzhov, W. B. Powell, and P. I. Frazier, The knowledge gradient algorithm for a general class of online learning problems, Operations Research, (2012).

- [29] S. P. Singh, T. Jaakkola, M. L. Littman, and C. Szepesvári., Convergence results for single-stepon-policy reinforcement-learning algorithms, Machine Learning, (2000).

- [30] W. R. Thompson, on the likelihood that one unknown probability exceeds another in view of the evidence of two samples, Biometrika, (1933), pp. 285–294.

- [31] J. Vermorel and M. Mohri, Multi-armed bandit algorithms and empirical evaluation, in European Conference on Machine Learning., 2005.

- [32] H. Wang, T. Zariphopoulou, and X. Zhou, Reinforcement learning in continuous time and space:a stochastic control approach, Journal of Machine Learning Research, (2020), pp. 1–34.

- [33] D. Šiška and L. Szpruch, Gradient Flows for Regularized Stochastic Control Problems. arXiv:2006.05956.

Acknowledgments.

Samuel Cohen also acknowledges the support of the Oxford-Man Institute for Quantitative Finance, and the UKRI Prosperity Partnership Scheme (FAIR) under the EPSRC Grant EP/V056883/1, and the Alan Turing Institute. Tanut Treetanthiploet thanks the University of Oxford for research support while completing this work, and acknowledges the support of the Development and Promotion of Science and Technology Talents Project (DPST) of the Government of Thailand and the Alan Turing Institute.