Projection techniques to update the truncated SVD of evolving matrices

Abstract

This paper considers the problem of updating the rank- truncated Singular Value Decomposition (SVD) of matrices subject to the addition of new rows and/or columns over time. Such matrix problems represent an important computational kernel in applications such as Latent Semantic Indexing and Recommender Systems. Nonetheless, the proposed framework is purely algebraic and targets general updating problems. The algorithm presented in this paper undertakes a projection viewpoint and focuses on building a pair of subspaces which approximate the linear span of the sought singular vectors of the updated matrix. We discuss and analyze two different choices to form the projection subspaces. Results on matrices from real applications suggest that the proposed algorithm can lead to higher accuracy, especially for the singular triplets associated with the largest modulus singular values. Several practical details and key differences with other approaches are also discussed.

Keywords:

Singular Value Decomposition, evolving matrices, Lanczos bidiagonalization, latent semantic analysis, recommender systems

1 Introduction

This paper considers the update of the truncated SVD of a sparse matrix subject to additions of new rows and/or columns. More specifically, let be a matrix for which its rank- (truncated) SVD is available. Our goal is to obtain an approximate rank- SVD of matrix

where denotes the matrix of newly added rows or columns. This process can be repeated several times, where at each instance matrix becomes matrix at the next level. Note that a similar problem, not explored in this paper, is to approximate the rank- SVD of after modifying its (non-)zero entries, e.g., see [31].

Matrix problems such as the ones above hold an important role in several real-world applications. One such example is Latent Semantic Indexing (LSI) in which the truncated SVD of the current term-document matrix needs to be updated after a few new terms/documents have been added to the collection [3, 7, 31]. Another example is the update of latent-factor-based models of user-item rating matrices in top-N recommendation [6, 19, 23]. Additional applications in geostatistical screening can be found in [13, Chapter 6].

The standard approach to compute is to disregard any previously available information and apply directly to an off-the-shelf, high-performance, SVD solver [2, 12, 29, 10, 27]. This standard approach might be feasible when the original matrix is updated only once or twice, however becomes increasingly impractical as multiple row/column updates take place over time. Therefore, it becomes crucial to develop algorithms which return a reasonable approximation of while taking advantage of . Such schemes have already been considered extensively for the case of full SVD [4, 9, 17] and rank- SVD [3, 23, 28, 31]. Nonetheless, for general-purpose matrices it is rather unclear how to enhance their accuracy.

1.1 Contributions.

-

1.

We propose and analyze a projection scheme to update the rank- SVD of evolving matrices. Our scheme uses a right singular projection subspace equal to , and only determines the left singular projection subspace.

-

2.

We propose and analyze two different options to set the left singular projection subspace. A complexity analysis is also presented.

-

3.

We present experiments performed on matrices stemming from applications in LSI and recommender systems. These experiments demonstrate the numerical behavior of the proposed scheme and showcase the various tradeoffs in accuracy versus complexity.

2 Background and notation

The (full) SVD of matrix is denoted as where and are unitary matrices whose ’th column is equal to the left singular vector and right singular vector , respectively. The matrix has non-zero entries only along its main diagonal, and these entries are equal to the singular values . Moreover, we define the matrices , , and . The rank- truncated SVD of matrix can then be written as . We follow the same notation for matrix with the exception that a circumflex is added on top of each variable, i.e., , with , , and .

The routines and return the number of rows of matrix and non-zero entries of matrix , respectively. Throughout this paper will stand for the norm when the input is a vector, and the spectral norm when the input is a matrix. Moreover, the term will denote the column space of matrix , while will denote the linear span of a set of vectors. The identity matrix of size will be denoted by .

2.1 Related work.

The problem of updating the SVD of an evolving matrix has been considered extensively in the context of LSI. Consider first the case , and let such that is orthonormal and is upper trapezoidal. The scheme in [31] writes

where the matrix product denotes the compact SVD of the matrix .

The above idea can be also applied to . Indeed, if matrices and are now determined as , we can approximate

where the matrix product now denotes the compact SVD of the matrix .

When coincides with the compact SVD of , the above schemes compute the exact rank- SVD of , and no access to matrix is required. Nonetheless, the application of the method in [31] can be challenging. For general updating problems, or problems where does not satisfy a “low-rank plus shift” structure [32], replacing by might not lead to a satisfactory approximation of . Moreover, the memory/computational cost associated with the computation of the QR and SVD decompositions in each one of the above two scenarios might be prohibitive. The latter was recognized in [28] where it was proposed to adjust the method in [31] by replacing matrices and with a low-rank approximation computed by applying the Golub-Kahan Lanczos bidiagonalization procedure [8]. Similar ideas have been suggested in [30] and [26] where the Golub-Kahan Lanczos bidiagonalization procedure was replaced by randomized SVD [10, 25] and graph coarsening [26], respectively.

3 The projection viewpoint

The methods discussed in the previous section can be recognized as instances of a Rayleigh-Ritz projection procedure and can be summarized as follows [28, 30]:

-

1.

Compute matrices and such that and approximately capture and , respectively.

-

2.

Compute where , and denote the leading singular values and associated left and right singular vectors of , respectively.

-

3.

Approximate by the product .

Ideally, the matrices and should satisfy

Moreover, the size of matrix should be as small as possible to avoid high computational costs during the computation of .

Table 1 summarizes a few options to set matrices and for the row updating problem. The method in [28] considers the same matrix as in [31] but sets where denotes the leading left singular vectors of . The choice of matrices and listed under the option “Algorithm 1” is explained in the next section. Note that the first variant of Algorithm 1 uses the same as in [31] and [28] but different . This choice leads to similar or higher accuracy than the scheme in [31] and this is also achieved asymptotically faster. A detailed comparison is deferred to the Supplementary Material. The second variant of Algorithm 1 is a more expensive but also more accurate version of the first variant.

| Method | ||

|---|---|---|

| [3] | ||

| [31] | ||

| [28] | ||

| Alg. 1 | ||

| Alg. 1 |

3.1 The proposed algorithm.

Consider again the SVD update of matrix , with . The right singular vectors of trivially satisfy . Therefore, we can simply set and compute the leading singular triplets of the matrix . Indeed, this choice of is ideal in terms of accuracy while it also removes the need to compute an approximate factorization of matrix . On the other hand, the number of columns in matrix is now equal to instead of in [31] and , in [28, 30]. This difference can be important when the full SVD of is computed as in [28, 30, 31].

Our approach is to compute the singular values of in a matrix-free fashion while also skipping the computation of the right singular vectors . Indeed, the matrix is only needed to approximate the leading singular vectors of . Assuming that an approximation and of the matrices and is available, can be approximated as .

The proposed method is sketched in Algorithm 1. In terms of computational cost, Steps 4 and 5 require approximately and Floating Point Operations (FLOPs), respectively. The complexity of Step 3 will generally depend on the algorithm used to compute the matrices and . We assume that these are computed by applying the unrestarted Lanczos method to matrix in a matrix-free fashion [21]. Under the mild assumption that Lanczos performs iterations for some which is greater than or equal to , a rough estimate of the total computational cost of Step 3 is FLOPs. The exact complexity of Lanczos will depend on the choice of matrix . A detailed asymptotic analysis of the complexity of Algorithm 1 and comparisons with other schemes are deferred to the Supplemental.

4 Building the projection matrix

The accuracy of Step 5 in Algorithm 1 depends on the accuracy of the approximate leading singular values and associated left singular vectors from Step 3. In turn, these quantities depend on how well captures the singular vectors [14, 18]. Therefore, our focus lies in forming such that the distance between the subspace and the left singular vectors is as small as possible.

4.1 Exploiting the left singular vectors of .

The following proposition presents a closed-form expression of the ’th left singular vector of matrix .

Proposition 4.1

The left singular vector associated with singular value is equal to

where satisfies the equation

and for any (when ).

-

Proof.

Deferred to the Supplementary Material.

The above representation of requires the solution of a nonlinear eigenvalue problem to compute . Alternatively, we can express as follows.

Proposition 4.2

The left singular vector associated with singular value is equal to

where the scalars are equal to

-

Proof.

Deferred to the Supplementary Material.

Proposition 4.2 suggests that setting should lead to an exact (in the absence of round-off errors) computation of . In practice, we only have access to the leading left singular vectors of , . The following proposition suggests that the distance between and the range space of is at worst proportional to the ratio .

-

Proof.

Deferred to the Supplementary Material.

Proposition 4.3 implies that left singular vectors associated with larger singular values of are likely to be approximated more accurately.

4.1.1 The structure of matrix .

4.2 Exploiting resolvent expansions.

The choice of presented in Section 4.1 can compute the exact provided that the rank of is exactly . Nonetheless, when the rank of is larger than and the singular values are not small, the accuracy of the approximate returned by Algorithm 1 might be poor. This section presents an approach to enhance the projection matrix .

Recall that the top part of is equal to . In practice, even if we knew the unknown quantities and , the application of matrix for each , is too costly. The idea presented in this section considers the approximation of , by for some fixed scalar .

Lemma 4.1

Let

such that . Then, we have that for any :

-

Proof.

Deferred to the Supplementary Material.

Clearly, the closer is to , the more accurate the approximation in Lemma 4.1 should be. We can now provide an expression for similar to that in Proposition 4.2.

Proposition 4.4

The left singular vector associated with singular value is equal to

-

Proof.

Deferred to the Supplementary Material.

Proposition 4.4 suggests a way to enhance the projection matrix shown in Proposition 4.3. For example, we can approximate by , which gives the following bound for the distance of from .

-

Proof.

Deferred to the Supplementary Material.

Compared to the bound shown in Proposition 4.3, the bound in Proposition 4.5 is multiplied by . In practice, due to cost considerations, we choose a single value of that is more likely to satisfy the above consideration, e.g., .

4.2.1 Computing the matrix .

The construction of matrix shown in Lemma 4.5 requires the computation of the matrix . The latter is equal to the matrix that satisfies the equation

| (4.1) |

The eigenvalues of the matrix are equal to , and for any , the matrix is positive definite. It is thus possible to compute by repeated applications of the Conjugate Gradient method.

Proposition 4.6

Let and denote the -norm of the error after iterations of the Conjugate Gradient method applied to the linear system , where . Then,

where and .

- Proof.

Corollary 4.1

The effective condition number satisfies the inequality .

Proposition 4.6 applies to each one of the right-hand sides in (4.1). Assuming that the matrix can be formed and stored, the effective condition number can be reduced even further. For example, solving (4.1) by the block Conjugate Gradient method leads to an effective condition number [20]. Additional techniques to solve linear systems with multiple right-hand sides can be found in [15, 16, 24].

Finally, notice that as increases, the effective condition number decreases. Thus from a convergence viewpoint, it is better to choose . On the other hand, increasing leads to worse bounds in Proposition 4.5.

4.3 Truncating the matrix .

When the number of right-hand sides in (4.1), i.e., number of rows in matrix , is too large, an alternative is to consider , where denotes the rank- truncated SVD of matrix . We can then replace by , since .

The matrix can be approximated in a matrix-free fashion by applying a few iterations of Lanczos bidiagonalization to matrix . Each iteration requires two applications of Conjugate Gradient to solve linear systems of the same form as in (4.2). A second approach is to apply randomized SVD as described in [10, 5]. In practice, this amounts to computing the SVD of the matrix where is a real matrix with at least columns whose entries are i.i.d. Gaussian random variables of zero mean and unit variance.

4.3.1 The structure of matrix .

5 Evaluation

Our experiments were conducted in a Matlab environment (version R2020a), using 64-bit arithmetic, on a single core of a computing system equipped with an Intel Haswell E5-2680v3 processor and 32 GB of system memory.

| Matrix | rows | columns | /rows | Source |

|---|---|---|---|---|

| MED | 5,735 | 1,033 | 8.9 | [1] |

| CRAN | 4,563 | 1,398 | 17.8 | [1] |

| CISI | 5,544 | 1,460 | 12.2 | [1] |

| ML1M | 6,040 | 3,952 | 165.6 | [11] |

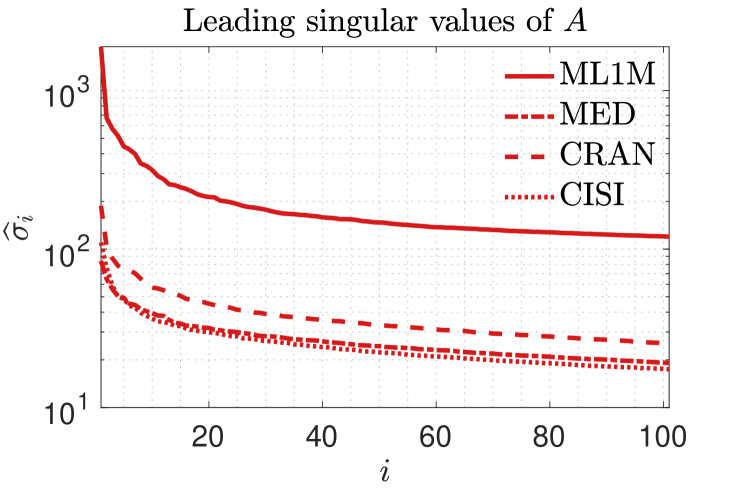

Table 2 lists the test matrices considered throughout our experiments along with their dimensions and source from which they were retrieved. The first three matrices come from LSI applications and represent term-document matrices, while the last matrix comes from recommender systems and represents a user-item rating matrix. The leading singular values of each matrix listed in Table 2 are plotted in Figure 1.

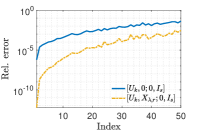

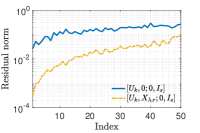

Throughout this section we focus on accuracy and will be reporting: a) the relative error in the approximation of the leading singular values of , and b) the norm of the residual , scaled by . The scalar is set as where the latter singular value is approximated by a few iterations of Lanczos bidiagonalization.

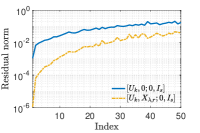

5.1 Single update.

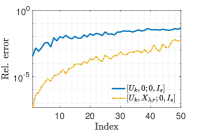

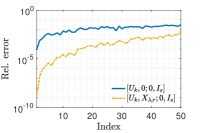

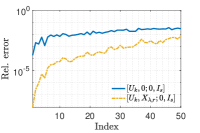

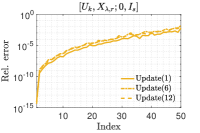

In this section we consider the approximation of the leading singular triplets of where , i.e., the size of matrices and is about half the size of . We run Algorithm 1 and set as in Propositions 4.3 and 4.5. For the enhanced matrix , the matrix is computed by randomized SVD where and the number of columns in matrix is equal to (recall the discussion in Section 4.3). The associated linear system with right-hand sides is solved by block Conjugate Gradient.

Figure 2 plots the relative error and residual norm in the approximation of the leading singular triplets of . As expected, enhancing the projection matrix by leads to higher accuracy. This is especially true for the approximation of those singular triplets with corresponding singular values .

In all of our experiments, the worst-case (maximum) relative error and residual norm was achieved in the approximation of the singular triplet . Table 3 lists the relative error and residual norm associated with the approximation of the singular triplet as varies from ten to fifty in increments of ten. As a reference, we list the same quantity for the case . As expected, enhancing the projection matrix by leads to higher accuracy, especially for higher values of .

| MED | CRAN | CISI | ML1M | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| err. | res. | err. | res. | err. | res. | err. | res. | |||||

| \tikzmarkin[hor=style mygrey]r10 | 0.036 | 0.234 | 0.026 | 0.176 | 0.025 | 0.214 | 0.031 | 0.156\tikzmarkendr10 | ||||

| 0.031 | 0.184 | 0.021 | 0.155 | 0.023 | 0.189 | 0.012 | 0.143 | |||||

| \tikzmarkin[hor=style mygrey]r30 | 0.021 | 0.114 | 0.017 | 0.134 | 0.017 | 0.161 | 0.008 | 0.121\tikzmarkendr30 | ||||

| 0.009 | 0.091 | 0.013 | 0.111 | 0.012 | 0.134 | 0.005 | 0.112 | |||||

| \tikzmarkin[hor=style mygrey]r50 | 0.004 | 0.053 | 0.007 | 0.098 | 0.007 | 0.081 | 0.003 | 0.076\tikzmarkendr50 | ||||

| N/A | 0.045 | 0.269 | 0.045 | 0.199 | 0.287 | 0.250 | 0.041 | 0.173 | ||||

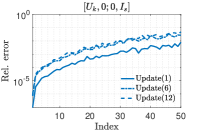

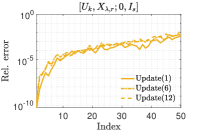

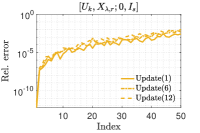

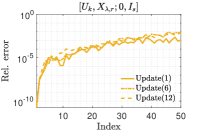

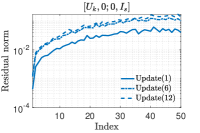

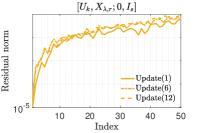

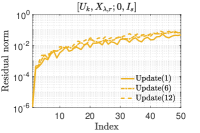

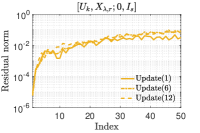

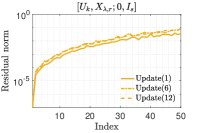

5.2 Sequence of updates.

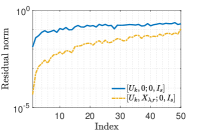

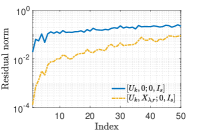

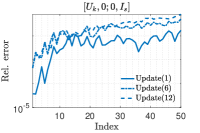

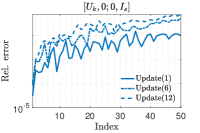

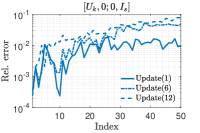

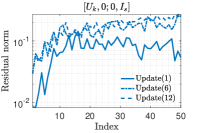

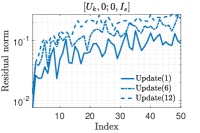

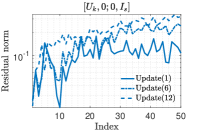

In this experiment the rows of matrix are now added in batches, i.e., we first approximate the leading singular triplets of matrix , then of matrix , etc. Here, denotes the step-size and denotes the total number of updates. Note that after the first update, the matrices and no longer denote the exact leading left and right singular vectors of the submatrix of matrix . We set and plot the accuracy achieved after one, six, and twelve updates, in Figures 3 and 4. Notice that enhancing by leads to similar accuracy for all updates, while in the opposite case accuracy deteriorates as the updates accumulate. On a separate note, the accuracy of the leading singular triplets of is higher when matrix is added to in batches rather than in a single update as in the previous section.

| MED | CRAN | CISI | ML1M | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Method | err. | res. | err. | res. | err. | res. | err. | res. | ||||

| [31] | 0.046 | 0.172 | 0.043 | 0.192 | 0.054 | 0.274 | 0.002 | 0.058 | ||||

| \tikzmarkin[hor=style mygrey]el10 Alg. 1 | 0.001 | 0.045 | 0.008 | 0.090 | 0.002 | 0.054 | -5 | 0.007 \tikzmarkendel10 | ||||

| [31] | 0.067 | 0.212 | 0.064 | 0.255 | 0.075 | 0.224 | 0.022 | 0.131 | ||||

| \tikzmarkin[hor=style mygrey]el20 Alg. 1 | 0.004 | 0.073 | 0.005 | 0.076 | 0.003 | 0.053 | 0.002 | 0.040 \tikzmarkendel20 | ||||

| [31] | 0.076 | 0.384 | 0.060 | 0.290 | 0.084 | 0.330 | 0.023 | 0.123 | ||||

| \tikzmarkin[hor=style mygrey]el30 Alg. 1 | 0.006 | 0.067 | 0.008 | 0.088 | 0.004 | 0.070 | 0.001 | 0.041 \tikzmarkendel30 | ||||

Table 4 lists relative error and residual norm associated with the approximation of the singular triplet by Algorithm 1 and the method in [31]. The number of sought singular triplets was varied from ten to thirty. Comparisons against the method in [28] were also performed but not reported since the latter was always less accurate than [31]. Overall, Algorithm 1 provided higher accuracy, especially for those singular triplets whose corresponding singular value was closer to .

6 Conclusion

This paper presented an algorithm to update the rank- truncated SVD of evolving matrices. The proposed algorithm undertakes a projection viewpoint and aims on building a pair of subspaces which approximate the linear span of the leading singular vectors of the updated matrix. Two different options to set these subspaces were considered. Experiments performed on matrices stemming from applications in LSI and recommender systems verified the effectiveness of the proposed scheme in terms of accuracy.

References

- [1] http://web.eecs.utk.edu/research/lsi/.

- [2] J. Baglama and L. Reichel, Augmented implicitly restarted Lanczos bidiagonalization methods, SIAM Journal on Scientific Computing, 27 (2005), pp. 19–42.

- [3] M. W. Berry, S. T. Dumais, and G. W. O’Brien, Using linear algebra for intelligent information retrieval, SIAM Review, 37 (1995), pp. 573–595.

- [4] M. Brand, Fast online SVD revisions for lightweight recommender systems, in Proceedings of the 2003 SIAM International Conference on Data Mining, SIAM, 2003, pp. 37–46.

- [5] K. L. Clarkson and D. P. Woodruff, Numerical linear algebra in the streaming model, in Proceedings of the forty-first annual ACM symposium on Theory of computing, 2009, pp. 205–214.

- [6] P. Cremonesi, Y. Koren, and R. Turrin, Performance of recommender algorithms on top-n recommendation tasks, in Proceedings of the fourth ACM conference on Recommender systems, 2010, pp. 39–46.

- [7] S. Deerwester, S. T. Dumais, G. W. Furnas, T. K. Landauer, and R. Harshman, Indexing by latent semantic analysis, Journal of the American society for information science, 41 (1990), pp. 391–407.

- [8] G. Golub and W. Kahan, Calculating the singular values and pseudo-inverse of a matrix, Journal of the Society for Industrial and Applied Mathematics, Series B: Numerical Analysis, 2 (1965), pp. 205–224.

- [9] M. Gu, Stanley, and S. C. Eisenstat, A stable and fast algorithm for updating the singular value decomposition, tech. rep., 1994.

- [10] N. Halko, P.-G. Martinsson, and J. A. Tropp, Finding structure with randomness: Probabilistic algorithms for constructing approximate matrix decompositions, SIAM Review, 53 (2011), pp. 217–288.

- [11] F. M. Harper and J. A. Konstan, The movielens datasets: History and context, ACM transactions on interactive intelligent systems, 5 (2015), pp. 1–19.

- [12] V. Hernandez, J. E. Roman, and V. Vidal, SLEPc: A scalable and flexible toolkit for the solution of eigenvalue problems, ACM Transactions on Mathematical Software (TOMS), 31 (2005), pp. 351–362.

- [13] L. Horesh, A. R. Conn, E. A. Jimenez, and G. M. van Essen, Reduced space dynamics-based geo-statistical prior sampling for uncertainty quantification of end goal decisions, in Numerical Analysis and Optimization, Springer, 2015, pp. 191–221.

- [14] Z. Jia and G. Stewart, An analysis of the Rayleigh-Ritz method for approximating eigenspaces, Mathematics of computation, 70 (2001), pp. 637–647.

- [15] V. Kalantzis, C. Bekas, A. Curioni, and E. Gallopoulos, Accelerating data uncertainty quantification by solving linear systems with multiple right-hand sides, Numerical Algorithms, 62 (2013), pp. 637–653.

- [16] V. Kalantzis, A. C. I. Malossi, C. Bekas, A. Curioni, E. Gallopoulos, and Y. Saad, A scalable iterative dense linear system solver for multiple right-hand sides in data analytics, Parallel Computing, 74 (2018), pp. 136–153.

- [17] M. Moonen, P. Van Dooren, and J. Vandewalle, A singular value decomposition updating algorithm for subspace tracking, SIAM Journal on Matrix Analysis and Applications, 13 (1992), pp. 1015–1038.

- [18] Y. Nakatsukasa, Accuracy of singular vectors obtained by projection-based SVD methods, BIT Numerical Mathematics, 57 (2017), pp. 1137–1152.

- [19] A. N. Nikolakopoulos, V. Kalantzis, E. Gallopoulos, and J. D. Garofalakis, Eigenrec: generalizing PureSVD for effective and efficient top-N recommendations, Knowledge and Information Systems, 58 (2019), pp. 59–81.

- [20] D. P. O’Leary, The block Conjugate Gradient algorithm and related methods, Linear Algebra and its Applications, 29 (1980), pp. 293–322.

- [21] Y. Saad, Numerical methods for large eigenvalue problems: revised edition, SIAM, 2011.

- [22] Y. Saad, M. Yeung, J. Erhel, and F. Guyomarc’h, A deflated version of the Conjugate Gradient algorithm, SIAM Journal on Scientific Computing, 21 (2000), pp. 1909–1926.

- [23] B. Sarwar, G. Karypis, J. Konstan, and J. Riedl, Incremental singular value decomposition algorithms for highly scalable recommender systems, in Fifth international conference on computer and information science, vol. 1, Citeseer, 2002, pp. 27–8.

- [24] A. Stathopoulos and K. Orginos, Computing and deflating eigenvalues while solving multiple right-hand side linear systems with an application to quantum chromodynamics, SIAM Journal on Scientific Computing, 32 (2010), pp. 439–462.

- [25] S. Ubaru, A. Mazumdar, and Y. Saad, Low rank approximation using error correcting coding matrices, in International Conference on Machine Learning, 2015, pp. 702–710.

- [26] S. Ubaru and Y. Saad, Sampling and multilevel coarsening algorithms for fast matrix approximations, Numerical Linear Algebra with Applications, 26 (2019), p. e2234.

- [27] S. Ubaru, A.-K. Seghouane, and Y. Saad, Find the dimension that counts: Fast dimension estimation and Krylov PCA, in Proceedings of the 2019 SIAM International Conference on Data Mining, SIAM, 2019, pp. 720–728.

- [28] E. Vecharynski and Y. Saad, Fast updating algorithms for latent semantic indexing, SIAM Journal on Matrix Analysis and Applications, 35 (2014), pp. 1105–1131.

- [29] L. Wu and A. Stathopoulos, A preconditioned hybrid SVD method for accurately computing singular triplets of large matrices, SIAM Journal on Scientific Computing, 37 (2015), pp. S365–S388.

- [30] I. Yamazaki, S. Tomov, and J. Dongarra, Sampling algorithms to update truncated SVD, in 2017 IEEE International Conference on Big Data, IEEE, 2017, pp. 817–826.

- [31] H. Zha and H. D. Simon, On updating problems in latent semantic indexing, SIAM Journal on Scientific Computing, 21 (1999), pp. 782–791.

- [32] H. Zha and Z. Zhang, Matrices with low-rank-plus-shift structure: partial SVD and latent semantic indexing, SIAM Journal on Matrix Analysis and Applications, 21 (2000), pp. 522–536.

Supplementary Material

Asymptotic complexity

The asymptotic complexity analysis of the method in [31] is as follows. We need FLOPs to form and compute its QR decomposition. The SVD of the matrix requires FLOPs. Finally, the cost to form the approximation of matrices and is equal to FLOPs.

The asymptotic complexity analysis for the “SV” variant of the method in [28] is as follows. We need FLOPs to approximate the leading singular triplets of , where is greater than or equal to (i.e., is the number of Lanczos bidiagonalization steps). The cost to form and compute the SVD of the matrix is equal to where the first term stands for the actual SVD and the rest of the terms stand for the formation of the matrix . Finally, the cost to form the approximation of matrices and is equal to FLOPs.

The asymptotic complexity analysis of Algorithm 1 is as follows. First, notice that Algorithm 1 requires no effort to build . For the case where is set as in Proposition 4.3, termed as “Alg. 1 (a)”, we also need no FLOPs to build . The cost to solve the projected problem by unrestarted Lanczos is then equal to FLOPs, where is greater than or equal to (i.e., is the number of unrestarted Lanczos steps). Finally, the cost to form the approximation of matrices and is equal to FLOPs. For the case where is set as in Proposition 4.5, termed as “Alg. 1 (b)”, we need

FLOPs to build , where is greater than or equal to (i.e., is either the number of Lanczos bidiagonalization steps or the number of columns of matrix in randomized SVD).

| Scheme | Building | Building | Solving the projected problem | Other |

|---|---|---|---|---|

| [31] | - | |||

| [28] | - | |||

| Alg. 1 (a) | - | - | ||

| Alg. 1 (b) | - |

The above discussion is summarized in Table 5 where we list the asymptotic complexity of Algorithm 1 and the schemes in [31] and [28]. The complexities of the latter two schemes were also verified by adjusting the complexity analysis from [28]. To allow for a practical comparison, we replaced all variables with since in practice these variables are equal to at most a small integer multiple of .

Consider now a comparison between Algorithm 1 (a) and the method in [31]. For all practical purposes, these two schemes return identical approximations to . Nonetheless, Algorithm 1 (a) requires no effort to build . Moreover, the cost to solve the projected problem is linear with respect to and cubic with respect to , instead of cubic with respect to the sum in [31]. The only scenario where Algorithm 1 can be potentially more expensive than [31] is when matrix is exceptionally dense, and both and are very small. Similar observations can be made for the relation between Algorithm 1 (b) and the methods in [28], although the comparison is more involved.

Proofs

Proof of Proposition 4.1

The scalar-vector pair satisfies the equation . If we partition the ’th left singular vector as

we can write

The leading rows satisfy . Plugging the expression of in the second block of rows and considering the full SVD leads to

The proof concludes by noticing that

where for the case , we have for any . In case , the Moore-Penrose pseudoinverse is considered instead.

Proof of Proposition 4.2

Since the left singular vectors of span , we can write

The proof concludes by noticing that the top part of can be written as

Proof of Proposition 4.3

We have

The proof follows by noticing that due to Cauchy’s interlacing theorem we have , and thus

Proof of Lemma 4.1

We can write

where for any . Let us now define the scalar . Then,

Accounting for all powers , gives

Since , it follows that for any we have . Therefore, the geometric series converges and . It follows that .

We finally have

This concludes the proof.

Proof of Proposition 4.4

First, notice that

Therefore, we can write

The left singular vector can be then expressed as

The proof concludes by noticing that by Lemma 4.1 we have .

Proof of Proposition 4.5

The proof exploits the formula

It follows