How to detect a salami slicer: a stochastic controller-stopper game with unknown competition

Abstract

We consider a stochastic game of control and stopping specified in terms of a process , representing the holdings of Player 1, where is a Brownian motion, is a Bernoulli random variable indicating whether Player 2 is active or not, and is a non-decreasing process representing the accumulated “theft” or “fraud” performed by Player 2 (if active) against Player 1. Player 1 cannot observe or directly, but can merely observe the path of the process and may choose a stopping rule to deactivate Player 2 at a cost . Player 1 thus does not know if she is the victim of fraud and operates in this sense under unknown competition. Player 2 can observe both and and seeks to choose the fraud strategy that maximizes the expected discounted amount

whereas Player 1 seeks to choose the stopping strategy so as to minimize the expected discounted cost

This non-zero-sum game appears to be novel and is motivated by applications in fraud detection; it combines filtering (detection), non-singular control, stopping, strategic features (games) and asymmetric information. We derive Nash equilibria for this game; for some parameter values we find an equilibrium in pure strategies, and for other parameter values we find an equilibrium by allowing for randomized stopping strategies.

1 Introduction

“Salami slicing” is a well known concept of fraud, where a thief or a fraudster repeatedly steals small amounts - so small that the net loss from the system is hard to detect at each instant. Albeit a small intensity of theft, aggregated over time or over a large number of victims, the accumulated amount stolen may become large if not detected in time. The essence of a salami slicing strategy is thus to trade-off between maximizing short-time profits and avoiding detection. Classical examples include penny shaving, i.e., consistently rounding off a large number of transactions up to the nearest penny and stealing the difference (cf. [23]), modifying the fuel tank capacity of rental cars so that customers pay for slightly more fuel than they consume at each rental (see [5]), and stealing one coin from each fare box of a public transportation agency (see [20]). Further examples in the same spirit can easily be thought of in the context of, e.g., poaching of game or fish (where the poacher would trade-off between an offensive strategy and being detected), a spy who steals classified information (again, a balance between exploitation and detection is a natural ingredient), computer networks with possible information leakage or botnet defense (cf. [9, Sec. 7.1.10] and [29] where mean field games of botnet defense are studied). Yet another related example is in the context of online privacy issues, where individuals knowingly give away small pieces of information about themselves, but would refuse to do so if they knew that this information was fully exploited against them.

An essential ingredient in a salami slicing strategy is the possibility to avoid detection by the presence of natural stochastic fluctuations in the underlying system; an observed fluctuation may then be due to such stochasticity, or stem from a fraudster being active (or from a combination of both). In this paper, we model the natural fluctuations by a Brownian motion and assume that the account holder, i.e., the possible victim and fraud detector, can only observe the total effect of natural fluctuations and the accumulated theft. Moreover, we equip the account holder with the possibility to deactivate the potential fraudster at any time at a given cost . As discussed above, there is then a natural trade-off for the fraudster between stealing large amounts and being detected. From the perspective of fraud detection on the other hand, the account holder has to balance the losses of potential fraud against the cost of deactivation.

1.1 Mathematical problem formulation

Let be a probability space on which a standard Brownian motion and an independent Bernoulli random variable with are given, where . We consider a two-player stochastic game in which the players are referred to as “account holder” (Player ) and “fraudster” (Player ). Let the stochastic process be given by

where is a non-decreasing stochastic process chosen by the fraudster. The interpretation is that represents the wealth of the account holder, is an indicator of whether the fraudster is active () or not (), represents the account holder’s initial belief that the fraudster is active, and corresponds to the accumulated amount stolen by the fraudster (if active).

We assume that the strategy of the fraudster is -adapted, where is the augmented filtration generated by and . The interpretation is that the fraudster knows whether he is active or not, as well as observes the natural fluctuations, i.e., , in the account, and based on this information decides how to steal.

The account holder, on the other hand, is assumed not to have direct access to the underlying Brownian motion , but can merely observe the path of the aggregate process . The account holder is equipped with a stopping control as follows: at any time, she may choose to deactivate the fraudster by paying a fixed amount , thereby ruling out the possibility for an active fraudster to continue stealing. The control of the account holder is thus represented by a random time. In Sections 1-3, the account holder strategy will be chosen from the class of stopping times with respect to , which is the augmented filtration generated by . Then, in Section 4, we will also consider randomized stopping times.

Definition 1.

A continuous -adapted non-decreasing process with is said to be a fraud strategy and an -stopping time is said to be a stopping strategy. The set of fraud strategies is denoted by , and the set of -stopping times is denoted by . Given a pair , the expected cost for the account holder is defined as

| (1) |

and the expected payoff for the fraudster is defined as

| (2) |

where the discount rate is a positive constant.

Remark 2.

For admissibility, we require that the fraud strategy is continuous. An alternative specification would allow for strategies that are merely right-continuous with left limits, where then additional care in the definition of and in the case of a lump sum payment and simultaneous stopping is needed. For example, replacing the upper limit of integration in (1) and (2) by would correspond to a specification giving precedence to the stopper. However, since a jump in would immediately reveal the existence of the fraudster, it is (at least heuristically) clear that the account holder would stop at the first jump time, thereby reducing that set-up to the present case with only continuous fraud strategies.

In the above set-up the account holder naturally seeks to choose a strategy to minimize the cost (1), whereas the fraudster seeks to choose a strategy to maximize (2), and we define a Nash equilibrium accordingly.

Definition 3 (Nash equilibrium).

A pair of strategies is a Nash equilibrium (NE) if it satisfies

| (3) |

for any pair .

Remark 4.

We have equipped the fraudster with the filtration so that any fraudster strategy is on the form for non-decreasing -adapted processes and . However, since neither nor depends on , but only on , the specification of is superfluous. In fact, a game which is strategically equivalent to the one introduced is obtained if is replaced with

The functionals and have the following interpretations. Imagine that before the game starts, i.e., at time , neither player knows , and that the value of will be revealed to Player 2 at . is then the expected payoff for Player 2 at time , whereas is the expected payoff at time 0 in case . These games are referred to as the ex ante game and the interim version of the game, respectively (see [1, 18] for classical theory of games under incomplete information). Also note that and that, in the definition of a NE, the second inequality in (3) can be replaced by .

Remark 5.

An essential feature of our game is that the account holder cannot observe the strategy used by the fraudster, but can only observe the path of the aggregate process . Our setup and terminology thus differs from that of, e.g., [7] and [35], where a strategy is a map from the set of controls of one player to the set of controls of the other player.

1.2 Literature review

While the present problem belongs to a new class of stochastic games — the novel feature being the presence of unknown competition, or a “ghost” (cf. the below) — it does belong in a wider sense to the literature on combined stochastic control and stopping games and to the literature on stochastic games under asymmetric information. Without aspiring to completeness, we give a brief review of such related papers.

The controller-and-stopper game was introduced as a zero-sum game in discrete time in [32]. In the seminal study [27], the zero-sum controller-and-stopper game is studied in a one-dimensional diffusion setting. In [21] a zero-sum game between a stopper and a singular controller of a one-dimensional diffusion is studied and, depending on which of the controller and the stopper has the first-move advantage, two different solutions are obtained (cf. Remark 2 above). A similar game is considered in [22] in a model based on a spectrally one-sided Lévy process. Further literature on zero-sum controller-and-stopper games include [2, 4, 10, 28, 34], whereas [6, 25] study non-zero-sum versions.

The first study of a stochastic differential game under asymmetric information is [7] (see also [8]). In particular, in [7] a zero-sum stochastic differential game under asymmetric information where two players control a multi-dimensional diffusion is studied. It is shown that the game has a value, which is the solution in a dual sense to an associated Hamilton-Jacobi equation. In [15], a continuous time zero-sum game where one player observes a Brownian motion, and one does not, is studied using an approach which relies on an approximating sequence of corresponding discrete time games. Numerical approximation for stochastic differential games with asymmetric information is studied in [3] and [16]. Another strand of this literature studies stopping games under asymmetric information, see, e.g., [12, 13, 14, 17, 30].

A key feature of the problem studied in this paper is the presence of unknown competition in the sense that Player 2 — the fraudster — may be non-existent (inactive), effectively leaving the unknowing Player 1 — the account holder — playing a game against a “ghost”. In contrast to [7], where the players can observe the realization of the other player’s control, it is essential in our set-up that the actions of the fraudster are not directly observable by the account holder (if they were, the account holder would detect the fraudster as soon as the control is non-zero). It appears that this is the first study of a stochastic game with unknown competition and a continuously controllable state process — the only other paper to consider dynamic stochastic games under unknown competition is, according to our knowledge, [11], in which a Dynkin (stopping) game is studied and where the term “ghost” is introduced. In particular, in [11] the effect of unknown competition in a Dynkin game is studied in a setting where each of the two players is uncertain whether the other player exists or not; using methods from filtering theory it is shown that a key feature of the equilibrium solution to that problem is that randomized stopping strategies should be used in such a way that the other player’s adjusted belief process, i.e., the conditional probability of active competition, stays below a certain boundary. For related studies within the economics literature see [19] and [33], where auctions with unknown competition in a non-dynamic setting are studied.

Admittingly, the current set-up models a rather stylized version of fraud detection, and naturally has its limitations from an applied perspective. For example, the set-up of a fraudster that is either active or inactive may seem unrealistically static, and one could allow for a more dynamic presence of, possibly, several fraudsters. Also, the account holdings are assumed unlimited so that the analysis below becomes independent of the present value of , whereas limited resources would be a natural ingredient in many applications. Moreover, the set of possible actions (stop or not stop) of the account holder is rather scarce; applications in resource extraction would call for a continuous action space also for her. It is our hope that the methods developed in the present paper will facilitate and encourage further research into dynamic stochastic games under unknown competition.

2 Applications of filtering theory

The Nash equilibria we identify below are specified in terms of the conditional probability the account holder assigns to the event that the fraudster is active, and we therefore require some elements of filtering theory. Moreover, in our Nash equilibria the fraud strategies are absolutely continuous in the sense that for a positive process .

Let us first view the situation from the perspective of the account holder. If the fraudster uses a fixed strategy on the form , then, under the assumption that also satisfies certain integrability conditions, we obtain from filtering theory (see, e.g., [31, Chapter 8]) that the innovations process

is a Brownian motion with respect to . Moreover,

where

and the process satisfies

| (4) |

with . Note that if is in particular -adapted (which is the case for the equilibria we identify in this paper, as we will see), then so that

The process given by (4) is the conditional probability of the existence of the fraudster provided the fraudster uses the strategy . However, it is essential in our problem set-up that the actual strategy is not directly observable, which means that we also need to take the effect of possible deviations from a NE into account. To do that we note that if the fraudster deviates from and instead uses a strategy , then the dynamics in (4) can be expressed as

thus showing exactly how the fraudster may manipulate the belief of the account holder, i.e. the process , by controlling the process . Observe that the dynamics of given by (2) depends on the actual strategy used by the fraudster as well on the account holder’s assumption of the fraud strategy . In particular, if we condition on (the fraudster is active) and suppose that the fraudster uses an arbitrary strategy , possibly different from as assumed by the account holder, then is given by

| (6) |

Furthermore, if the fraudster uses the strategy as assumed by the account holder, and if is -adapted so that , then the drift in (6) is which is positive, and in this case the fraudster thus gradually reveals her existence to the account holder. However, note that the drift can also be negative (at most , corresponding to a flat portion of ), or, at the other extreme, arbitrarily large (corresponding to a rapidly increasing ).

3 A pure Nash equilibrium

We provide heuristic calculations in Section 3.1 to obtain a candidate NE. The candidate NE is summarized in Section 3.2, and further properties are obtained in Section 3.3. In Section 3.4 we then verify that this candidate indeed constitutes a NE.

3.1 Deriving a candidate Nash equilibrium

In this section we will look for a NE, cf. Definition 3. We emphasize that the calculations in this section are mainly motivational; a formal verification result is provided in Section 3.4 below.

It is reasonable to guess that if the account holder is sufficiently sure that the fraudster is active, she will pay the amount to deactivate the fraudster, and that, from the viewpoint of the fraudster, there should exist an optimal push rate, depending on the account holder’s current belief, which solves the trade-off between stealing and avoiding detection. In fact, we will look for a NE where the fraud strategy is of the form

| (7) |

for some non-negative function to be determined (from now on denotes such a function), and the stopping strategy takes the form of a threshold time

for some , where corresponds, in equilibrium, to the conditional probability for the account holder that the fraudster is active.

More precisely, given , consider a pair given by

| (8) |

with and . Then the dynamics of conditioned on are

| (9) |

Hence, if the account holder uses a threshold strategy for the process , the active fraudster faces a stochastic control problem

with the underlying process being given by (8) or, equivalently,

| (10) |

with given by (9) with .

Remark 6.

In the system (8) we use the function (to be determined) to specify the dynamics of , rather than as in Section 2. We will see below (cf. Proposition 12) that if the fraudster uses the control , then is -adapted; consequently, in that case, , and then coincides with . Hence corresponds, in equilibrium, to the conditional probability for the account holder that the fraudster is active.

Using the dynamic programming principle we expect that if corresponds to a NE fraud strategy — i.e. if with given by (9) is optimal in (10) — then it should hold that

| (11) |

for all constants in the continuation region of the NE stopping strategy, i.e. for . (To ease the presentation we have suppressed the dependence on in the functions in (11), a convention we will use throughout the paper.) Similarly, by optimality of we expect equality in (11) when , i.e.,

| (12) |

for . Subtracting (11) from (12) yields

for all , which implies that

and hence

for . Inserting

into (12) and multiplying by yields a non-linear ordinary differential equation

| (13) |

This can be integrated, and using separation of variables we find

The general solution thus satisfies

where

are the distribution function and the density of the standard normal distribution, respectively.

Imposing the boundary conditions (which we expect since there is no possibility left for the fraudster to steal after ) and (corresponding to unbounded possibilities for the fraudster to steal in the limit as ) yields

| (14) |

The function implicitly given in (14) is thus a candidate equilibrium value function for the fraudster (recall, however, that the threshold is yet to be determined).

We now turn to the perspective of the account holder. For a given fraud strategy of the form (7), the account holder faces an optimal stopping problem

| (15) |

where we expect that the underlying process given by (8) (with ) coincides with , and that

where is a Brownian motion with respect to , see Section 2. Arguing heuristically, we may thus use iterated expectations to replace with in (15) and then we expect, based on the dynamic programming principle, that

| (16) | ||||

where the boundary conditions come from the account holder having zero expected cost if there is no fraudster and from immediate stopping at the boundary .

Recall from the discussion above that a NE fraud strategy should satisfy

(the second equality is derived from (14)), which inserted into (16) gives

| (17) |

for . Comparing with (13) we see that is a particular solution to (17). Moreover, making the Ansatz for the homogenous part (for some function to be determined) yields

Inserting these expressions into (17) and using that by (13) we find that the homogeneous part of (17) can be written as

The linear ordinary differential equation

has general solution

where

and

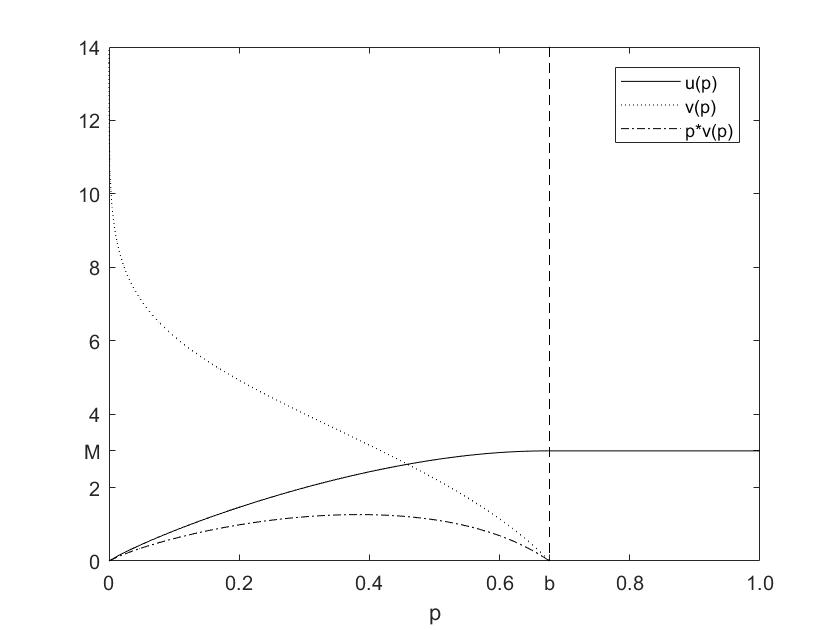

A candidate for the equilibrium value function of the account holder is thus

| (18) |

where and (and which is hidden implicitly in ) are yet to be determined.

Before turning to these constants, we make some observations concerning the function .

Lemma 7.

The function satisfies

-

(i)

;

-

(ii)

;

-

(iii)

;

-

(iv)

.

Proof.

(i) is immediate from the standard estimate

(ii) then follows since (i) implies as . (iii) is obvious. Finally, (iv) follows from . ∎

We now impose boundary conditions for the candidate equilibrium value function . More precisely, we wish to determine the constants , and so that, first of all, and . Recalling and , and using (ii) and (iii) from Lemma 7, we get from (18) that

so

To determine the unknown stopping boundary , we impose the principle of smooth fit from optimal stopping theory, which for us takes the form . We have that

so

Differentiation of (14) gives

| (20) |

and plugging this and into (3.1) yields

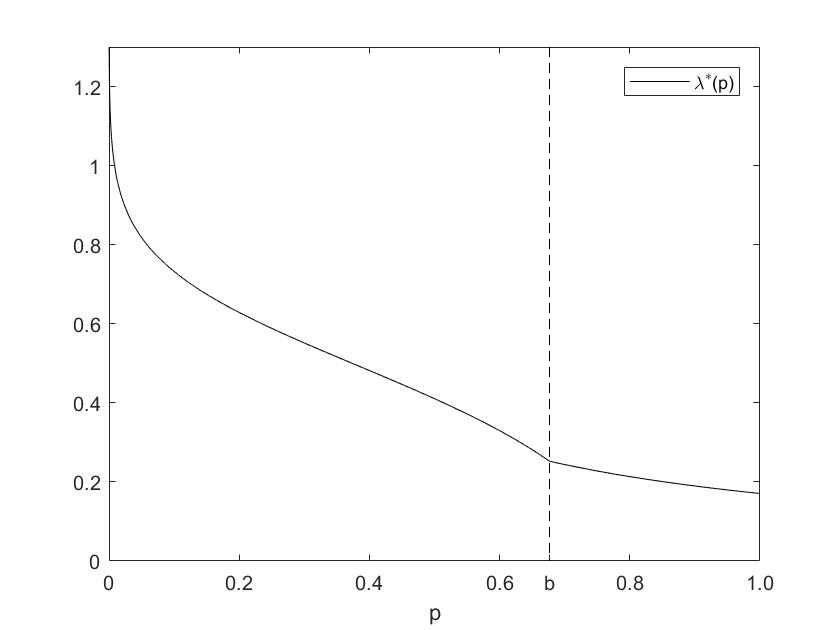

3.2 The candidate Nash equilibrium

We now summarize the specification of our candidate Nash equilibrium . Let

| (21) |

and assume that

| (22) |

(this bound has not been discussed yet, but we include it here as it is essential in the verification below, cf. Lemma 11 below). The expression (21) for is increasing in , and thus

Define (the candidate equilibrium value function for the fraudster in the interim version of the game, cf. Remark 4) by

| (23) |

and (the candidate equilibrium value function for the account holder) by

| (24) |

Next, let

| (25) |

(using (20) one sees that the second line of (25) corresponds to a continuous extension of ). Furthermore, let for be defined by

| (26) |

with and . Our candidate NE is given by with

| (27) |

and

| (28) |

Remark 8.

Suppose a fraud strategy is given. Then is given by on and by on . Thus the second equation of (26) is a stochastic differential equation driven by a continuous semimartingale with drift and diffusion coefficients

| (29) |

and

| (30) |

respectively. These coefficients are Lipschitz on any interval , , so a strong solution exists, at least up to a potential explosion at .

To show that the process cannot reach zero in finite time we will use the following lemma.

Lemma 9.

There exist constants and such that, for all , it holds that

Proof.

Recall that so that , and that . Thus there exist constants such that for all it holds that

The result thus follows by setting . ∎

Proposition 10.

Proof.

Suppose a fraud strategy is given. The existence of a strong solution was established in Remark 8. To see that (31) holds, note that it suffices to show that (31) holds on , since it then follows from comparison (see [36, Chapter IX.3]) that (31) holds also on since is non-decreasing (implying that the drift for is minimal when ). Again by comparison, it suffices to check non-explosion at for the SDE

for any constant . For such a diffusion, the densities of the scale function and speed measure are

and

respectively. Using Fubini’s Theorem, we thus obtain

(here and below , denote positive constants). From (23) we have

| (32) |

which differentiated yields

Using the above and Lemma 9 (assuming that is small enough) we find that

Consequently, (31) follows by Feller’s test for explosion.

Now consider defined in (28). Then the dynamics for in (26) can be written as

| (33) |

Note that the diffusion coefficient in (33) is also in this case given by (30), and that the drift coefficient is given by (29) on , and by

| (34) |

on . However, the drift coefficient (34) is also locally Lipschitz and we thus obtain the existence of a strong solution as in the case above. Using also that in (25) is a positive function (which is easy to verify) we conclude that is a continuous non-decreasing process adapted to , so . ∎

3.3 Properties of the candidate Nash equilibrium

In this section we derive a few further properties of the candidate Nash equilibrium that are needed in the verification below.

Proof.

To prove the claim we will show that the function is concave provided . Indeed, concavity of together with the smooth fit condition imply . For the concavity of it follows from (16) that it suffices to prove for all .

To do that, note that

where we used (32). Consequently,

Since follows from , and since

it follows that , which completes the proof. ∎

We next establish that if the fraudster uses the candidate NE strategy then the process corresponds to the account holder’s conditional probability of existence of the fraudster (in line with Section 2).

Proposition 12.

Proof.

First observe that is -adapted, so that , where . Consequently, by [31, Chapter 8.1] we have

where the innovations process

is a Brownian motion with respect to (formally, to use [31, Theorem 8.1] one needs to localize by, e.g., setting ; however, since does not reach 0 in finite time by Proposition 10, there is no problem when letting ). Thus

and by (26),

so by uniqueness of solutions we find that . Therefore, , and (35) holds. ∎

3.4 A verification theorem for the pure Nash equilibrium

In this subsection we verify that the pair defined above indeed constitutes a NE for our game, provided where is defined in (22).

Theorem 13.

(Verification.) Assume that the account holder’s cost for stopping satisfies . Then the pair defined in (27) and (28) is a NE in the sense of Definition 3. Moreover, the corresponding equilibrium value functions for the account holder and the fraudster (in the interim version of the game) are given by (24) and (23), i.e.,

Proof.

Optimality of . We first show that is an optimal stopping time for the account holder provided the fraudster uses , i.e., that for any stopping time .

By construction, , and the limits and both exist, which is sufficient to apply Itô’s formula in its standard form, cf. [26, Problem 3.6.24]. Moreover,

| (36) |

for all . Indeed, for , (36) holds with equality by (17), and for we have so

| (37) |

where we used and .

Hence, using that the dynamics of satisfies (35) and Itô’s formula, we obtain for any stopping time

| (38) | |||||

The stochastic integral on the right hand side of (38) is in fact a martingale term since the integrand is bounded. Therefore, taking expectation in (38), and using also Lemma 11, Proposition 12, Fubini’s theorem and iterated expectations, yields

Using monotone convergence we thus find that

Repeating the above argument with instead of gives

and monotone convergence thus yields

Consequently,

Optimality of . We now fix as defined in (27) and show that the strategy defined by (28) is an optimal strategy for the fraudster, i.e., that for any fraud strategy . Note that the dynamics of in (26) can when conditioning on be written as

| (39) |

Let be an arbitrary fraud strategy, and consider the process

Using Itô’s formula, (13) and (25), we find that

for . Consequently, is a lower bounded martingale with bounded quadratic variation. The optional sampling theorem thus implies that

so since was arbitrary.

Conversely, if , then (39) reduces to

We now claim that a.s. To see this, first note that the process cannot reach in finite time by Proposition 10. Moreover, the time-changed process

is a 3-dimensional Bessel process, for which it is well-known that is finite a.s.; since cannot reach 0, this implies that also a.s.

Redefining with and recalling that we thus find, with optional sampling, that

Thus

which, in view of Remark 4, completes the proof. ∎

Remark 14.

A closer inspection of the proof above shows that the specification of on is somewhat arbitrary. In fact, any specification with on (cf. (37)) would give a NE .

Remark 15.

In equilibrium, the relation

holds (indeed, this can be checked by applying Itô’s formula to the right hand side and then compare with the equilibrium dynamics of ). In the other direction, we have been unable to determine the exact form of the functional mapping of a path of into a value of .

4 A Nash equilibrium with randomized stopping

In order to find an equilibrium for the remaining case, in which the cost of stopping satisfies , we will in this section expand the class of allowed stopping strategies for the account holder to include randomized stopping rules. Thus, instead of looking for an equilibrium with a threshold time as in Section 3.1 we here look for an equilibrium with a randomized stopping time specified by an intensity with which the account holder stops; in particular, the equilibrium intensity depends on the conditional probability the account holder assigns to the existence of the fraudster.

Definition 16 (Randomized stopping time).

Let be the family of right-continuous non-decreasing processes which are adapted to the filtration and with . Let be a random variable which is Exp(1)-distributed and independent of all other random sources. A randomized stopping time is a random variable of the form

where . We say that the random time is generated by the process , and we denote the class of randomized stopping times by .

Given a pair , we define as before the expected cost

for the account holder, the ex ante expected payoff

for the fraudster, and the expected payoff

for the fraudster in the interim version of the game.

Definition 17 (Mixed stopping Nash equilibrium).

A pair of strategies is a mixed stopping Nash equilibrium (msNE) if

or, equivalently,

for any .

4.1 Derivation of a mixed stopping Nash equilibrium

In this section we will look for a msNE in the sense of Definition 17. We use heuristic reasoning to obtain a candidate equilibrium which we later verify in Section 4.4. As in Section 3.1 we consider a process given by

for some non-negative function to be determined. We will look for a msNE where the fraud strategy is of the kind (7) and the stopping strategy is a randomized stopping time generated by a process on the form for some function ; thus specifies the intensity with which the account holder stops. Moreover, we conjecture that has the form

for some with , where the infinite intensity should be understood as immediate stopping whenever . From the fraudster’s perspective, martingale arguments as in Section 3.1 again suggest that with , the equilibrium value function should on the interval satisfy

for all and

| (40) |

cf. (11) and (12), respectively. Consequently,

| (41) |

which inserted in (40) leads to a non-linear equation

| (42) |

on . Specializing to the interval where , we have that

with general solution

Imposing the boundary condition yields so that, for ,

or, equivalently,

| (43) |

However, since the account holder does not stop with certainty at , we do not impose , so the constant remains to be specified.

Next, we expect, as in Section 3.1, that the value function of the account holder satisfies

in the interval where stopping does not happen. Solving the equation above using (41) and the boundary conditions and gives

| (44) | |||||

for .

By the indifference principle in game theory, we also expect that the expected cost for the account holder is constantly equal to for where the intensity of stopping is positive. Imposing on the interval , and using martingale arguments as above, we find that

so that

for . By (41) we thus have

| (45) |

and integration yields

Imposing the boundary condition (with the motivation that there is no possibility for the fraudster to act after reaching ) gives

| (46) |

for .

Note that in (44), the free boundary and the value (equivalently, and the constant in (43)) are still unknown. Imposing the smooth fit condition gives

which simplifies to

| (47) |

Moreover, imposing we obtain from (43) and (45) that

| (48) |

Using (43) in (48) we find that

| (49) |

so (47) simplifies to

| (50) |

Moreover, inserting the second expression for in (48) into (50) yields

i.e.,

| (51) |

Note that (51) is an equation in the single unknown variable .

Lemma 18.

Assume that . Then equation (51) has a unique positive solution . Moreover, .

Proof.

Let . Then and for , so a solution to exists in by continuity. Differentiation yields

Thus, is strictly decreasing up to and increasing for . Consequently, since the solution must be unique and satisfy . ∎

4.2 The candidate msNE

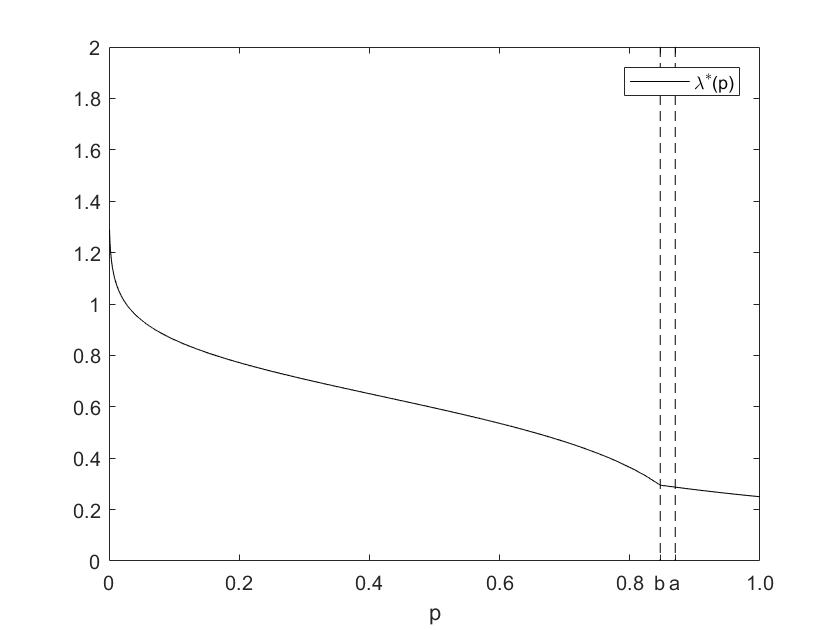

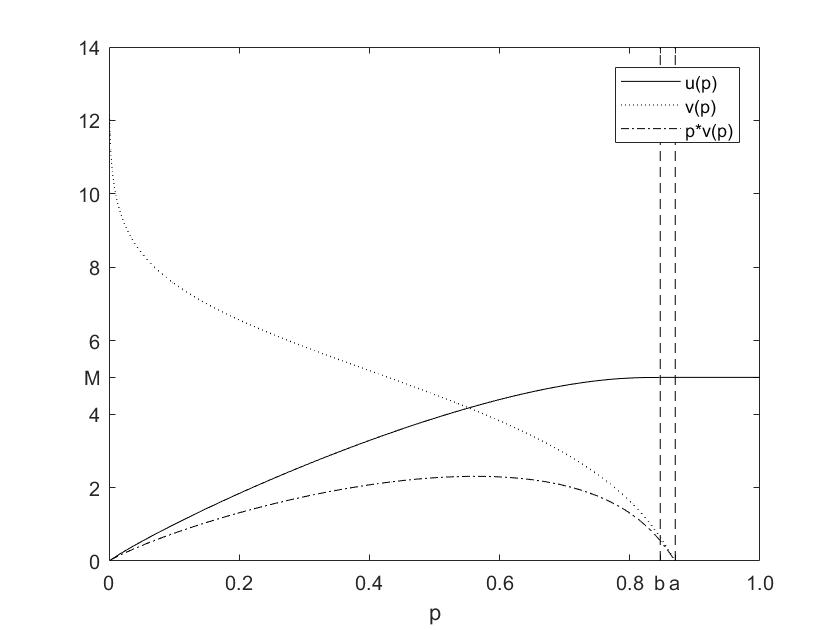

We now summarize by describing our candidate for a msNE and the corresponding value functions for the case

| (52) |

Let be the unique positive solution of

| (53) |

cf. Lemma 18, and let

| (54) |

(in Section 4.3 below we verify that ) and

cf. (49) and (46), respectively. Define (the candidate equilibrium value function for the fraudster in the interim version of the game) by

| (55) |

and (the candidate equilibrium value function for the account holder) by

| (56) |

Set

and

Furthermore, let for be defined by

with and . Our candidate msNE is then given by

| (57) |

with and , and

| (58) |

4.3 Properties of the candidate msNE

Proof.

From (49) and (53) we know that

so it suffices to check that

or, equivalently,

| (59) |

for all . However, (59) is a well-known inequality that holds for all ; for completeness, we provide the following argument from [37]. Define

and note that as and as since

as . Moreover,

If for some , then there exists a with and , which contradicts (4.3). Consequently, , which proves (59). ∎

Proof.

As in the proof of Lemma 11 it suffices to show that for and we therefore assume that in this proof. By definition of , and we have that

and

We obtain

where .

Using the definition of and differentiation of the expression for we also find that

Hence,

where and

Since , it follows that (4.3) evaluated at equals , so that

Next,

so . Thus we are done if we can show that

is a decreasing function (since this implies that for ). To do that, differentiate to get

which is negative since for all . ∎

4.4 Verification for the mixed stopping Nash equilibrium

In this section we prove that the candidate msNE defined in Section 4.2 is indeed a msNE.

Theorem 21.

(Verification.) Assume that the account holder’s cost for stopping satisfies . Then, the pair defined in (57) and (58) is a msNE in the sense of Definition 17. Moreover, the corresponding equilibrium value functions for the account holder and the fraudster (in the interim version of the game) are given by (56) and (55), i.e.,

Proof.

Optimality of . First note that

| (62) |

for . In fact, (62) holds with equality on by construction, and for we have so

Consequently, with fixed, Itô’s formula gives

where we note that the stochastic integral is a martingale. Now fix an -stopping . By optional sampling,

where the second equality follows using iterated expectations since , see Proposition 12. Letting gives

by monotone convergence.

Now consider a randomized stopping time generated by , and let for (so that ). Then , and

so

For the reverse inequality, consider . Since on the event , we have for that

as by monotone convergence. Consequently,

so

Optimality of . Let us now fix the stopping strategy generated by

where

If the fraudster uses a strategy , the process satisfies

on the event . We then want to show that is an optimal response for the fraudster. More precisely, we want to show

for any fraud strategy .

To do that, first define a process by

where

is a jump process with intensity . Note that

so is a lower bounded local martingale. Consequently,

so by monotone convergence we find that .

On the other hand, consider the case . Note that satisfies

for . Since is bounded, we thus have

for some , which shows that is uniformly integrable. Consequently,

is a martingale, and optional sampling gives

The arguments used in Theorem 13 show that a.s. Consequently, by uniform integrability,

Therefore, monotone convergence yields

Thus

which completes the proof. ∎

Remark 22.

As in the case with a pure NE described in Section 3, the specification of on can be done in several ways; we have chosen to use the same formula on as on .

References

- [1] Aumann, R. and Maschler, M. Repeated games with incomplete information. MIT Press, Cambridge, MA, 1995.

- [2] Baghery, F., Haadem, S., Øksendal, B., and Turpin, I. Optimal stopping and stochastic control differential games for jump diffusions. Stochastics, 85 (2013), no. 1, 85-97.

- [3] Baňas, Ľ., Ferrari, G., and Randrianasolo, T. Numerical approximation of the value of a stochastic differential game with asymmetric information. arXiv preprint, (2019), arXiv:1912.13248.

- [4] Bayraktar, E., and Huang, Y. J. On the multidimensional controller-and-stopper games. SIAM J. Control Optim, 51 (2013), no. 2, 1263-1297.

- [5] Bosworth, S., Kabay, M. and Whyne, E. Computer Security Handbook, 5th ed. John Wiley & Sons, 2009.

- [6] Campi, L., and De Santis, D. Nonzero-sum stochastic differential games between an impulse controller and a stopper. J. Optimiz. Theory. App. 186 (2020), 688-724.

- [7] Cardaliaguet, P. and Rainer, C. Stochastic differential games with asymmetric information. Appl. Math. Optim. 59 (2009), no. 1, 1-36.

- [8] Cardaliaguet, P., and Rainer, C. Pathwise strategies for stochastic differential games with an erratum to ”stochastic differential games with asymmetric information”. Appl. Math. Optim. 68 (2013), no. 1, 75-84.

- [9] Carmona, R., and Delarue, F. Probabilistic Theory of Mean Field Games with Applications II. Springer Nature, (2018).

- [10] Choukroun, S., Cosso, A., and Pham, H. Reflected BSDEs with nonpositive jumps, and controller-and-stopper games. Stoch. Process. Appl. 125 (2015), no. 2, 597-633.

- [11] De Angelis, T. and Ekström, E. Playing with ghosts in a Dynkin game. Stoch. Process. Appl. 130 (2020), no. 10, 6133-6156.

- [12] De Angelis, T., Ekström, E. and Glover, K. Dynkin games with incomplete and asymmetric information. To appear in Math. Oper. Res. (2020+).

- [13] De Angelis, T., Merkulov, N., and Palczewski, J. On the value of non-Markovian Dynkin games with partial and asymmetric information. arXiv preprint, (2020), arXiv:2007.10643.

- [14] Gensbittel, F. and Grün, C. Zero-sum stopping games with asymmetric information. Math. Oper. Res. 44 (2019), no. 1, 277-302.

- [15] Gensbittel, F., and Rainer, C. A two-player zero-sum game where only one player observes a Brownian motion. Dyn. Games. Appl., 8 (2018), no. 2, 280-314.

- [16] Grün, C. A probabilistic-numerical approximation for an obstacle problem arising in game theory. Appl. Math. Optim. 66 (2012), no. 3, 363-385.

- [17] Grün, C. On Dynkin games with incomplete information. SIAM J. Control Optim. 51 (2013), no. 5, 4039-4065.

- [18] Harsanyi, J. Games with incomplete information played by ”Bayesian” players. I. The basic model. Management Sci. 14 (1967), 159-182.

- [19] Harstad, R., Kagel, J. and Levin, D. Equilibrium bid functions for auctions with an uncertain number of bidders. Econom. Lett. 33 (1990), no. 1, 35-40.

-

[20]

Henton, D. (27 Dec 2010). ”LRT thief stole nearly $2.4 million, one coin at a time”.

Edmonton Journal. Retrieved 27 August 2019.

https://www.pressreader.com/canada/edmonton-journal/20101227/283025461071328 - [21] Hernández-Hernández, D., Simon, R. S., and Zervos, M. A zero-sum game between a singular stochastic controller and a discretionary stopper. Ann. Appl. Probab. 25 (2015), no. 1, 46-80.

- [22] Hernández-Hernández, D., and Yamazaki, K. Games of singular control and stopping driven by spectrally one-sided Lévy processes. Stoch. Proc. Appl. 125 (2015), no. 1, 1-38.

- [23] M.E. Kabay. Network World Security Newsletter, 07/24/02.

- [24] Karandikar, R. On pathwise stochastic integration. Stochastic Process. Appl. 57 (1995), no. 1, 11-18.

- [25] Karatzas, I., and Li, Q. BSDE approach to non-zero-sum stochastic differential games of control and stopping. In Stochastic Processes, Finance and Control: A Festschrift in Honor of Robert J Elliott (2012), 105-153.

- [26] Karatzas, I. and Shreve, S. Brownian motion and stochastic calculus. Second edition. Graduate Texts in Mathematics, 113. Springer-Verlag, New York, 1991.

- [27] Karatzas, I., and Sudderth, W. D. The controller-and-stopper game for a linear diffusion. Ann. Probab. 29 (2001), no. 3, 1111-1127.

- [28] Karatzas, I., and Zamfirescu, I. M. Martingale approach to stochastic differential games of control and stopping. Ann. Probab. 36 (2008), no. 4, 1495-1527.

- [29] Kolokoltsov, V. N. and Bensoussan, A. Mean-field-game model for botnet defense in cyber-security. Appl. Math. Optim. 74 (2016), no. 3, 669-692.

- [30] Lempa, J., and Matomäki, P. A Dynkin game with asymmetric information. Stochastics, 85 (2013), no. 5 , 763-788.

- [31] Liptser, R. and Shiryaev, A. Statistics of random processes. I. General theory. Second edition. Stochastic Modelling and Applied Probability. Springer-Verlag, Berlin, 2001.

- [32] Maitra, A. P., and Sudderth, W. D. The Gambler and the Stopper. Lecture Notes-Monograph Series, Inst. Math. Statist.) 30 (1996), 191–208

- [33] McAfee, P. and McMillan, J. Auctions with a stochastic number of bidders. J. Econom. Theory 43 (1987), no. 1, 1-19.

- [34] Nutz, M., and Zhang, J. Optimal stopping under adverse nonlinear expectation and related games. Ann. Appl. Probab. 25 (2015), no. 5: 2503-2534.

- [35] Possamaï, D., Touzi, N., and Zhang, J. Zero-sum path-dependent stochastic differential games in weak formulation. Ann. Appl. Probab., 30 (2020), no. 3, 1415-1457.

- [36] Revuz, D. and Yor, M. Continuous martingales and Brownian motion. Third edition. Grundlehren der Mathematischen Wissenschaften, 293. Springer-Verlag, Berlin, 1999.

- [37] Sampford, M.R. Some inequalities on Mill’s ratio and related functions. Ann. Math. Statistics 24 (1953), 130-132.