Change point detection based on method of moment estimators

Abstract

A change point detection procedure using the method of moment estimators is proposed. The test statistics is based on a suitable -process. The asymptotic behavior of this process is established under both the null and the alternative hypothesis and the consistency of the test is also proved. An estimator for the change point is proposed and its consistency is derived. Some examples of this method applied to a parametric family of random variables are presented.

Keywords: Change point problems; Asymptotic Distribution; Consistency

1 Introduction

An important issue in statistics concerns to test on structural change problems. This problem arises naturally in quality control context, where one is faced about the output of a production line and would find any departure from an acceptable standard of the production. From the statistical point of view, the problem consists in testing whether there is a statistically significant change point in a sequence of chronologically ordered data. The problem for an i.i.d. sample was first considered in the paper of Page [14], see also Hinkley [7], and, for a general survey of the change point detection and estimation, see Chen and Gupta [4]. The parameter change point problem became very popular in regression and time series models. This is because these models can be used to describe structural changes that often occur in financial and economic phenomena (due for example to a change of political situation or to a change of economic policy) or in environmental phenomena (due to sudden changes in weather situation or in the case of a natural catastrophe). For regression models see, for example, Hinkley [6], Quandt [16], Brown et al. [1], Chen [2]. For time series models, see for example, Picard [15]. Ling [11] and Lee et al. [10]. For a general review of parametric methods and analysis, refer also to Csörgő and Horváth [5] and to Chen and Gupta [3].

The aim of this paper is to show a very simple approach for change point detection, using the partial sum process based on the method of moment estimator. This idea naturally turns out from a general approach to change point problems, developed in Negri and Nishiyama [13] based on the partial sum processes of estimating equations, called the Z-process method. To understand how the idea arises, let us recall some results about change point problem. The partial sum process is defined as

where is a parametric family of probability densities with respect to a measure , defined on a suitable measurable space, and . Let be an independent sequence of -valued random variables from this parametric model. Introduce the gradient vectors . Let be the maximum likelihood estimator (MLE) for the full data . The MLE is a special case of -estimators, that is, is the solution to the estimating equation

To detect if there is a change point, Horváth and Parzen [8] are apparently the firsts to introduce the test statistics based on the Fisher-score process

| (1) |

where is a consistent estimator for the Fisher Information matrix . It is straightforward that

in the Skorohod space , where is a vector of independent standard Brownian bridges and denotes the convergence in distribution in Skorohod space with respect the sup norm. This was proved by Horváth and Parzen [8], although they didn’t discuss the asymptotic behavior of the test under the alternative. Negri and Nishiyama [12] took the same approach to the change point problem for an ergodic diffusion process model based on the continuous observation and proved also the consistency of the test under an alternative which has sufficient generality. The general approach to change point problem by Negri and Nishiyama [13] is not just a simple generalization of Fisher-score process method in the case of independent random sequences proposed by Horváth and Parzen[8], but in their framework it is possible to treat new applications in broad spectrum of statistical change point problems including not only models for ergodic dependent data but also non-ergodic cases. Moreover, as it is very important in discussing any kind of statistical testing hypotheses problems, to study the behavior of the test statistics under certain alternatives, an argument to prove the consistency of the test based on the proposed method under some specified alternatives is also developed.

This paper starts from the consideration that in the test statistics based on the Fisher-score process (1) and its generalization, the -process can be considered also when the estimating equations are introduced to define the method of moment estimator (MME). This estimator is the solution of a particular estimating equation and so the -process arise naturally without be a gradient of a -process as in the case of the MLE. The MME has the advantage to be defined under very mild conditions and to be very simple to compute.

The main result of this paper is to prove that the test statistics based on the -process that generates the MME converges to the supremum of a Brownian Bridge. Moreover the asymptotic properties under the alternative are easily deduced. The form of the test statistics suggest also a procedure not only to establish if there is a change point, but if it is the case, where or when this change point appears. The estimator of the change point is introduced as the instant where the test statistics attains its maximum. The consistency of this estimator is also proved.

The rest of the paper is organized as follows. In the next Section some general notations are given. In Section 3 the MME estimator is defined. The change point problems is presented in Section 4. In particular in Subsection 4.1 the asymptotic properties under the null hypothesis are proved. In Subsection 4.2 the asymptotic properties under the alternative are considered. The estimation of the change point and the asymptotic behavior of the estimator are presented in Subsection 4.3. Finally in Section 5 a simulation study on the Gamma distribution is presented.

2 Notation

Let be the space of functions defined on taking values in a finite-dimensional Euclidean space, which are right continuous and have left hand limits; we equip this space with the Skorohod metric. Throughout this paper, all random processes, denoted as , are assumed to take values in . See for example Kallemberg [9] for these definitions.

In what follows, the parametric space is a bounded, open, convex subset of , where is a fixed positive integer. The word “vector” always means “-dimensional real column vector”, and the word “matrix” means “ real matrix”. The Euclidean norm is denoted by for a vector where denotes the -th component of , and by for a matrix where denotes the -component of . Note that and for vector and matrices . The notations and denote the transpose. The notations and mean the convergence in probability with respect to a probability measure and the convergence in distribution, as , respectively.

3 Method of moments estimator

Let us recall, following Van der Vaart [17], the MME. Some notations we will use along all the paper are introduced in this section. The method of moments estimator gives the estimate by comparing functionals of sample and their theoretical moments. In general it can be view as a -estimator. Let be an i.i.d. sample from a distribution on a measurable space . Suppose that the parameter . Let be a measurable function on . We write . Let’s introduce the -dimensional vector

where is the expected value with respect to, the symmetric matrix

and the the derivative matrix

Define

The solution of the system of equations is called method of moments estimator. If is one-to-one then the moment estimator is uniquely determined as . See Van der Vaart [17] for more details and properties of MME’s.

4 Change point problem

Let be a measurable space, and let a parametric family of probability densities with respect to , where , be given. Let be an independent sequence of -valued random variables from this parametric model.

We consider the following testing problem (change point problem):

: the true value does not change during ;

versus any alternative that for the moment we can state as : there is a change in some .

Let us denote with the probability measure under . To deal with this change point problem let us introduce the partial sum process

The method of moments estimator is the solution to .

Define the derivative matrix as , where .

4.1 Asymptotic properties under the null hypothesis

In this section the asymptotic distribution under the null hypothesis of the test statistic is proved. The main result is given by Theorem 4.5. Before to state it some preliminary results are proved.

Theorem 4.1

Let us suppose that is invertible and that . Then

Moreover

where is a -dimensional standard normal random variable.

Proof. The first line can be proved as in Van der Vaart [17]. The second line is proved as a special case of Lemma 4.2 below.

Lemma 4.2

Let be a -dimensional standard Brownian motion. It holds

in .

Proof. The result follows from Donsker’s theorem.

Lemma 4.3

Let be a standard Brownian motion in . It holds

in .

Proof. It follows from the Taylor expansion that

The term appearing above is a random vector on the segment connecting and . Now it follows from Lemma 4.2 that

Lemma 4.4

Let define

It holds that .

Proof. The result follows by the strong law of large number observing that .

To test if there is a change in the parameter value, let us introduce the statistic

| (2) |

This test statistics has the form very similar to (1). In (2) the MME appears instead of the MLE, the matrix plays the role of the consistent estimator of the Fisher Information matrix. Moreover the -process involved have different form. The asymptotic distribution is in any case the supremum of the norm of a vector of Brownian Bridge.

Theorem 4.5

Let the conditions of the above Lemmas hold true. Then

Proof. The claim follows from Lemma 4.3 and the continuous mapping theorem.

4.2 Asymptotic properties under the alternative

Let us suppose that under the alternative hypothesis there exists a certain instant where the value of the parameter changes. More precisely in the most typical form the alternative in the change point problems can be defined as follow.

: there exists a constant such that the true value is for , and for , where .

Lemma 4.6

Under , converges in probability to , where is the solution of the following equation

Proof. The result follows by Theorem 5.7 and 5.9 of Van der Vaart [17].

Theorem 4.7

Let , and as defined in . Let us define . Let the smallest eigenvalue of . Let us assume that and . Then the test based on the statistics is consistent.

Proof. We can prove as in Lemma 4.4 that under it holds . Here is the probability measure corresponding to before the change and corresponding to after the change point. It can be proved that under it holds

Hence

This complete the proof.

4.3 Estimation of the change point

As an estimator of the change point, let us define

where .

Let us introduce the following function.

Definition 4.8

Let and . Let us define the following function

| (3) |

Note that for we have

Theorem 4.9

Under , converges in probability to .

Proof. Observe that

Remembering that by Lemma 3.6 we have

Since the condition

holds, and the maximizer of is , the result follows by Corollary 3.2.3 of Van der Vaart and Wellner [18].

5 Example and simulation study

We apply our method to test if there is change point in a Gamma model. Let be i.i.d. Gamma random variables. For , , , the density is given by

where . Define by . We have

Define and . The moment estimator is given by

When the null hypothesis is rejected, we estimate the chance point with the proposed statistics . We simulate values of a Gamma distribution, for different values of , to asses the asymptotic results we have presented in the previous Sections.

First of all, we estimate the empirical size of the test under the Null hypothesis for different values of the parameters of the Gamma distribution. Then, we compute the empirical power of the test under the alternative that there is a change point in the parameter. Finally we study the consistency of the change point estimator.

The set up of the design of our simulation study is the following. The number of the Monte Carlo experiments is . In the simulation study we set the change point in three different points, respectively . Moreover we choose different values of the parameters for the change point. To study the asymptotic behavior of the test statistics under the Null and the Alternative Hypothesis and to study the consistency of the estimator of the change point estimator we set three different values of the number of observations, respectively .

The level of the test is fixed at . The critical values of the test statistics have been reported in Lee et al. [10]. For the given level the critical value is .

Results

The empirical size of the test is less and closed to the theoretical value for any and any choice of the parameters. See Table 1.

| 0.0233 | 0.0276 | 0.0429 | ||

| 0.0217 | 0.0291 | 0.0374 | ||

| 0.0274 | 0.0307 | 0.0432 |

Regarding the empirical power, it increases and it reaches 1 as increases. For example in the case reported in Table 2, the test reaches empirical power equal 1 for when the change point is settled at . The empirical power is 0.995 for and only 0.170 for . Anyway in the worst case the empirical power reaches 1 for as the asymptotic result suggest.

| 0.9795 | 1 | 1 | |

| 0.6813 | 0.9953 | 1 | |

| 0.0650 | 0.1696 | 1 |

Moreover the empirical power convergence to 1 is reached for lower values of as the distance between the parameter increase. This can be seen in Tables 3 and 4, where the parameter change from 1 to 2 and 4 respectively.

| 0.67 | 0.96 | 1 | |

| 0.68 | 0.99 | 1 | |

| 0.07 | 0.17 | 1 |

| 1 | 1 | 1 | |

| 0.69 | 1 | 1 | |

| 0.06 | 0.17 | 1 |

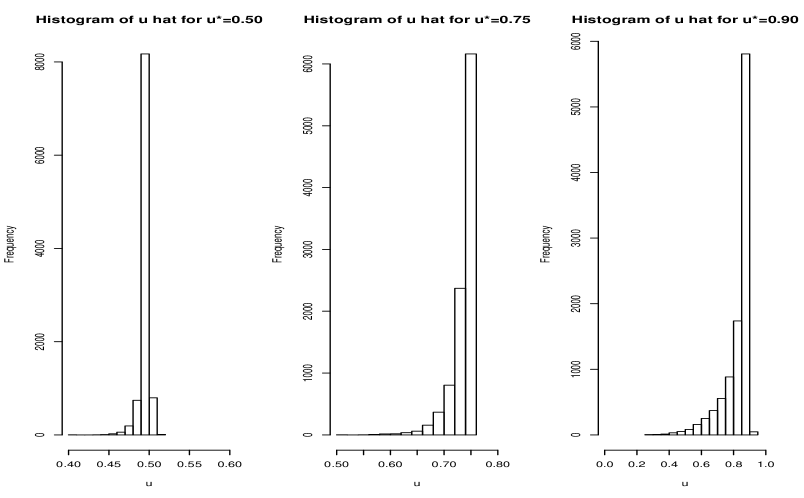

As discussed in Section 4.3 we propose an estimator for the change point . The estimator is computed for any trajectory as the argument where the test statistics attains its maximum. In the Figure 1 the histogram of the 10000 values of is plotted for for the change point reported reported in Table 2, where the parameter remain unchanged whereas the parameter change from to .

This is a case where the empirical power is 1, so the change point is always detected and it is correctly estimated. Indeed, it can be seen that for the three values of in each histogram its maximum is attained in correspondence of the class that contain the true value . In Table 5, the mean, the standard deviation (sd) and the estimated value for the root mean square error (RMSE) for the estimator are computed for the three different values of when , the parameter while the parameter changes from 0.01 to 0.05 at the point .

| mean | sd | est. RMSE | |

|---|---|---|---|

| 0.50 | 0.497 | 0.006 | 0.007 |

| 0.75 | 0.737 | 0.022 | 0.025 |

| 0.90 | 0.831 | 0.090 | 0.114 |

The mean value is closer to the true value as far as the change point is closer to 0.50. Moreover the variability (measured with the standard deviation) increases as the change point approaches the end of the period of observation. The values of the estimated RMSE closed to the standard deviation are an evidence that the estimator is unbiased.

All the simulation results presented in this section are consistent with the theoretical results. We can conclude the our procedure is able to establish if there is a change point in our model and when the test reject the null hypothesis the change point can be estimate without big error.

Acknowledgements. This work was supported by the Department of Management, Information and Production Engineering, Grant 2017 (I.N.) and by Grant-in-Aid for Scientific Research (C), 15K00062, 18K11203, from Japan Society for the Promotion of Science (Y.N.).

References

- [1] Brown, R. L., Durbin, J. and Evans, J. M. (1975). Techniques for testing the constency of regression relationships over time. With discussion. J. Roy. Statist. Soc. Ser. B. 37, 149-192.

- [2] Chen, J. (1998). Testing for a change point in linear regression models. Comm. Statist. Theory Methods, 27, 2481-2493.

- [3] Chen, J. and Gupta, A. K. (2000). Parametric Statistical Change Point Analysis. Borkäuser, Boston.

- [4] Chen, J. and Gupta, A. K. (2001). On change point detection and estimation. Comm. Statist. Simulation Comput. 30, 665-697.

- [5] Csörgő, M. and Horváth L. (1997). Limit Theorems in Change-Points analysis. Wiley, New York.

- [6] Hinkley, D. V. (1969). Inference about the intersection in two-phase regression. Biometrika. 56, 495-504.

- [7] Hinkley, D. V. (1970). Inference about the change-point in a sequence of random variables. Biometrika 57, 1-17.

- [8] Horváth, L. and Parzen, E, Limit theorems for Fisher-score change processes. In: Change-point Problems, (Edited by Carlstein, E., Müller H.-G. and Siegmund, D.) IMS Lecture Notes – Monograph Series 23, 157-169, (1994).

- [9] Kallenberg, O. (2002) Foundations of Modern Probability. (2nd ed.) Springer-Verlag, New York Berlin Heidelberg.

- [10] Lee, S., Ha, J., Na, O. and Na, S. (2003). The cusum test for parameter change in time series models. Scand. J. Statist. 30, 781–796.

- [11] Ling, S. (2007). Testing for change points in time series models and limiting theorems for NED sequences. Ann. Statist. 35, 1213-1237.

- [12] Negri, I. and Nishiyama, Y. (2012). Asymptotically distribution free test for parameter change in a diffusion process model, Ann. Inst. Statist. Math. 64, 911-918.

- [13] Negri, I., Nishiyama, Y. (2017). -process method for change point problems with applications to discretely observed diffusion processes. Stat. Methods Appl.. 26, 231-250.

- [14] Page, E. S. (1955). A test for a change in a parameter occurring at an unknown point. Biometrika 42, 523-527.

- [15] Picard, D. (1985). Testing and estimating change-points in time series. Adv. in Appl. Probab. 17, 841-867.

- [16] Quandt, R. E. (1960). Tests of the hypothesis that a linear regression system obeys two separate regimes. J. Amer. Statist. Assoc. 55, 324-330.

- [17] Van der Vaart, A.W. (1998). Asymptotic Statistics. Cambridge University Press, Cambridge.

- [18] Van der Vaart, A.W. and Wellner, J.A. (1996). Weak Convergence and Empirical Processes: With Applications to Statistics. Springer-Verlag, New York.