Optimal Liquidation in a Mean-reverting Portfolio

Abstract. In this work we study a finite horizon optimal liquidation problem with multiplicative price impact in algorithmic trading, using market orders. We analyze the case when an agent is trading on a market with two financial assets, whose difference of log-prices is modelled with a mean-reverting process. The agent’s task is to liquidate an initial position of shares of one of the two financial assets, without having the possibility of trading the other stock. The criterion to be optimized consists in maximising the expected final value of the agent, with a running inventory penalty.

The main result of this paper consists in finding a classical solution of the Hamilton-Jacobi-Bellman (HJB) equation associated to this problem, which is proved to not coincide with the value function. However, we find the value function as a solution to the forward-backward stochastic differential equation (FBSDE) associated to the problem. We provide numerical tests showing that the HJB and FBSDE solutions are close to each other and analysing performance of the described model. We also prove a verification theorem and a comparison principle for the viscosity solution to the HJB equation.

Keywords. Optimal liquidation, closed form solution, price impact, dynamic programming, viscosity solution, stochastic maximum principle, FBSDE approximation.

AMS MSC2010: 91G80, 93E20, 49J20, 49L20, 49L25.

JEL Classification: C6, G1.

1 Introduction

A standard service of investment banks is the execution of large trades. Unlike for small trades, the liquidation of a large portfolio is a complex task. It is usually impossible to immediately execute a large liquidation task or it is only possible at a high cost due to insufficient liquidity. Hence, the ability of exercising an order in a way that minimizes execution costs for the client is of primary importance. The objective of this paper is to determine the adaptive trading strategy that maximizes the expected final cash value of an asset sale. We address this question in the continuous-time liquidity model introduced by Almgren [4] with an infinite time horizon and linear price impact.

The optimal liquidation problem under price impact has been studied extensively in the literature. Bertsimas and Lo [5] use a linear price impact model and solve a discrete optimal control problem to minimize expected trading costs. Almgren and Chriss [2, 3], Huberman and Stanzl [8] introduce the volatility as a trading cost. Almgren [4] employs nonlinear impact functions and discusses the continuous-time limit of the models in Almgren and Chriss [2, 3] in more details. Almgren [1] considers optimal liquidation in a market with stochastic liquidity and stochastic volatility. Kharroubi and Pham [10] consider real trading that occurs in discrete time. Obizhaeva and Wang [13] include price impact by modelling the limit order book directly. For an overview of continuous-time price impact models, see Cartea et al. [7] and the references therein.

All the literature we have inspected on the optimal liquidation strategy is based only on the stock that the agent needs to liquidate. However, there may be additional information available in the market, such as the price of a correlated stock, which could be helpful to better predict the stock price movements. A model based on both asset prices may generate a more reliable adaptive liquidation strategy, which not only relies on the price of the liquidating stock, but also on that of the correlated stock.

In this paper we analyze the case when an agent trades on a market with two financial assets whose difference of log-prices has a mean-reverting behavior. The agent’s task is to liquidate the initial position of shares of one stock, without the possibility of trading the other stock. This technique is often employed when modeling a pair of stocks in pair trading in which the agent tries to make money out of a couple of correlated stocks by selling one stock and buying the other, to take advantage of the mean-reverting behavior of the co-integration factor between the two stocks. In our setting the agent can only sell stock, but cannot trade the other stock. Moreover, we define the difference of the log-prices to be an Ornstein-Uhlenbeck process which is the continuous-time analogue of the discrete-time AR(1) process and makes its parametrization an easy task, see Cartea et al. [7, Section 3.7] and Brockwell and Davis [6, Chapter 3] for further details on parametrization of such processes.

The main contributions of this paper are that we prove the value function is the unique continuous viscosity solution to the HJB equation which is complicated with three state variables, that we find the representation of the classical solution under some mild conditions, which opens the way of finding the optimal value and strategy with the Monte-Carlo simu- lation, and that we show the value function and the optimal liquidation rate depend only on observable data which allow a straightforward calculation at each moment in time. Although the classical solution to the HJB equation is proved to be not coincident with the value function, numerical tests show that it is close to the value functionn, by proving that it is close to the approximated solution of the FBSDE associated to the optimization problem.

The rest of the paper is structured as follows. Section 2 describes the settings of the problem, defines the value function, writes the HJB equation and states the main theorem (Theorem 2.2) that the value function is the unique continuous viscosity solution to the HJB equation. Section 3 finds a classical solution of the HJB equation under some mild conditions on the model parameters and derives the objective function as a sum of classical solutions to three different parabolic PDEs which can be solved one by one. Section 4 finds value function and optimal trading speed as solution to an FBSDE obtained by applying stochastic maximum principle to our problem. Section 5 is the numerical section and it is divided in two parts. Subsection 5.1 compares the closed form solution obtained in section 3 with the solution of the FBSDE in section 4, which is approximated using a deep learning algorithm. Subsection 5.2 provides some numerical tests to assess our model and compares its performance with that of two other strategies based on two geometric Brownian motion approximations of the liquidating stock price. Section 6 concludes. Appendix A contains the proofs of Theorem 2.2, Propositions 3.1 and 3.6.

2 Model

Let be a filtered probability space, where is the natural filtration generated by two independent standard Brownian motions and , augmented by all -null sets. Let be the fixed terminal time, the price of a stock in the market, satisfying the following geometric Brownian motion (GBM):

| (2.1) |

where , are positive constants, is the growth rate, the volatility rate, the price of the stock that the agent aims to liquidate, the cointegration factor between stocks and , defined by , and follows an Ornstein-Uhlenbeck (OU) process

| (2.2) |

where , are positive constants, the correlation coefficient, the mean reversion speed, the volatility. The cointegration factor behaves as a mean-reverting process, which implies a period of time in which the process outperforms (or underperform) is followed by a moment in which the two stocks have similar prices.

Let denote the rate of selling the stock, which is a decision (control) variable decided by the agent and is said admissible if it is a progressively measurable, non-negative and square integrable process. Denote by the set of all admissible control processes.

Let denote the inventory left at time and the initial amount of stock owned by the agent. The process depends on the trading strategy and follows the equation:

| (2.3) |

Let denote the wealth process, satisfying the following equation:

where is the temporary price impact factor, which is the same as that in Cartea et al. [7].

Denote by the vector of three state variables and the state space, given by with . Moreover, denote the initial price of the stock by . We group the three state processes into a vector . Let , we define the 3-dimensional stochastic process as the solution to the following SDE

| (2.4) |

where

| (2.5) |

The optimal liquidation problem is defined by:

| (2.6) |

where is a stopping time defined by , the first time when all stock is liquidated before terminal time or otherwise. The first term inside expectation is the wealth value at , the second the terminal liquidation value and the last three the running inventory penalties. The terminal liquidation value is the cash from liquidating all the inventory left at terminal time at a price penalized by a quantity proportional to the amount of remaining stocks. Inventory penalties are not financial costs, but incorporate the agent’s urgency for executing the trade. Denote by , the conditional expectation operator at time .

The value function of problem is defined by

| (2.7) |

where

| (2.8) |

where is defined by .

To solve the control problem , we adopt the dynamic programming principle and derive the following HJB equation for the value function:

| (2.9) |

on , with terminal condition and boundary condition , where is the operator defined by

Theorem 2.1 (Verification Theorem).

Let be a function in and satisfy the following growth condition

for fixed . Assume there exists a measurable function such that

with terminal condition and boundary condition . Let the SDE

| (2.10) |

admit a unique solution, given an initial condition , where and are defined in . Let . Then coincides with the value function .

Equation is a nonlinear PDE with three state variables and . We show the value function is a viscosity solution of , see Pham [14] for its definition and properties.

Theorem 2.2.

The value function defined in is the unique viscosity solution of the HJB equation .

If we strengthen the condition on the control set, we have continuity of the value function. Let be fixed and let . Then, we define the set as

| (2.11) |

Proposition 2.3.

Let the set of admissible controls be reduced to for fixed . Then the value function , defined in , is continuous on .

3 Classical solution to HJB equation

It is in general difficult to find a classical solution of equation . We show in this section that, under some mild conditions, we can achieve that. From equation we get the optimal rate of trading as

| (3.1) |

Substituting in equation , we have

| (3.2) |

The PDE is nonlinear and difficult to solve. To simplify it we try to eliminate the last term containing the operator. In the following, we assume that the function satisfies for any . Under this assumption, reduces to

| (3.3) |

By inspecting the terminal conditions, we postulate a solution of the following form:

| (3.4) |

Substituting to equation , collecting terms with coefficients and , and setting each term equal to , we derive the following system of PDEs on :

| (3.5) |

with terminal conditions .

The last equation in is a Riccati type equation and has a closed form solution given by

| (3.6) |

It is easy to verify that is a negative and increasing function.

Recall that function must satisfy for any , which is equivalent to the following:

| (3.7) |

Since is positive and is negative, condition holds if

| (3.8) |

Proposition 3.1.

Assume the model parameters satisfy the following condition:

| (3.9) |

Then solution in satisfies condition and is given by

| (3.10) |

for , where , and are functions defined by

| (3.11) |

Moreover, the optimal control is given by

| (3.12) |

Note that for any fixed parameters , one can always choose and such that is satisfied, and that in can be written, with the help of the Feynman-Kac formula, as

| (3.13) |

Combining with Proposition 3.1, we have the following result:

Theorem 3.2.

Assume condition is satisfied. Then equations in admit classical solutions , and given by , and respectively.

Proposition 3.3.

Let be defined as in , let be any positive real number, let be big enough and let . Then, , as defined in .

Remark 3.4.

Let be defined as in . By the fact that is locally Lipschitz, we get that , drift and diffusion coefficients of SDE are locally Lipschitz. Existence and uniqueness of solution to equation follow by applying Karatzas and Shreve [9, Theorem 2.5].

Remark 3.5.

Let condition be satisfied and , and be the classical solutions to the equations in as in Theorem 3.2. As proved in Remark 3.4 and Proposition 3.3, all conditions of verification Thorem 2.1 are satisfied except for continuity of . Indeed function is not continuous for , unless on . Hence, does not necessarily coincide with the value function in , unless it is proved to be continuous on .

As proved in Proposition 3.3, the optimal control lies in the more restrictive control set defined in . Proposition 2.3 ensures that if the control set is reduced to , then the value function is continuous. We conclude that if is not identically equal to , then the solution to the HJB equation does not coincide with the value function.

If we reduce our model to a one stock model as that in Cartea et al. [7] with the same parameters, i.e., , then condition is satisfied. Using and , we get and for any , which makes in continuous in the whole domain. We can apply Theorem 2.1 to verify that coincides with the value function .

Proposition 3.6.

Assume condition is satisfied and , and are the classical solutions to the equations . Then, function

coincides with the value function in on .

If condition is not satisfied, then it is not clear if HJB equation admits a classical solution, however, Theorem 2.2 states that the value function is the unique viscosity solution to the HJB equation .

Remark 3.7.

The model can be extended to cover limit orders as well by introducing a premium for executing limit orders instead of market orders (see Cartea et al. [7]) and a new state variable as a measure of uncertainty in filling limit orders. We can prove all theorems in this more general setup and, under similar conditions to that in , prove the existence of a classical solution to the HJB equation that coincides with the value function. The model can also be extended to the multi-dimensional case, in which an agent aims to liquidate different stocks on a basket of correlated stocks .

4 FBSDE approach

In this section we approach the control problem , by using the stochastic maximum principle (c.f. Pham [14, Theorem 6.4.6] and Li and Zheng [12]). It is a standard approach to write the value function defined in as a solution to an FBSDE and to find the optimal control from the maximization of the Hamiltonian associated to the optimization problem. To apply stochastic maximum principle, we approximate problem , by replacing the stochastic terminal time with a fixed terminal time . We rewrite the value function as

| (4.1) | ||||

From SDE , we get that the only component of the state process depending on the control is . We define the Hamiltonian as

The BSDE associated to our problem is

with terminal condition , where

Using the stochastic maximum principle approach, it follows that the optimal trading strategy coincides with the control function that maximizes the Hamiltonian , which is

| (4.2) |

In the following we prove that the solution to the above BSDE can be used to find the optimal strategy of the optimization problem . The proof of the theorem below immediately follows from Pham [14, Theorem 6.4.6] using concavity of Hamiltonian with respect to variables and maximality of in for the Hamiltonian .

Theorem 4.1 (Stochastic maximum principle).

Suppose that the FBSDE

| (4.3) |

admits a solution and that is a progressively measurable, non-negative and square integrable process. Then , defined in , is the optimal control of problem .

In the following section we focus on finding a solution to FBSDE , which is a coupled non-linear Forward-Backward SDE and, to our knowledge, cannot be explicitly solved. In the numerical section below, we use a deep learning-based method, following the one presented in Weinan et al. [15], to find an approximated solution to FBSDE and we show that the closed form control in is close to the approximated version of the optimal control in .

5 Numerical Tests

This section is divided in two parts. The first subsection shows that the closed form control deriving from the HJB equation and the neural network (NN) approximated control deriving from the FBSDE approach are close to each other. In the second subsection we compare the performance of the closed form control based on and with respect to the optimal strategy based on two simplified models based on geometric Brownian motion approximations of the liquidating stock price.

5.1 Neural network approximation vs. closed form control

In this subsection we compare the control obtained through the NN approximated solution of the FBSDE with the closed form control in . To numerically find the solution of the FBSDE we apply a similar method to the one in Weinan et al. [15]. We adapt [15, Framework 3.2] to our case by generalizing the implementation to a coupled FBSDE setting with a multidimensional backward equation. The method consists into a neural network approximation of the two solutions and of the FBSDE , where the backward equation is transformed into a forward equation and initial condition and process are chosen in order to minimize the loss

| (5.1) |

in order to guarantee the terminal condition .

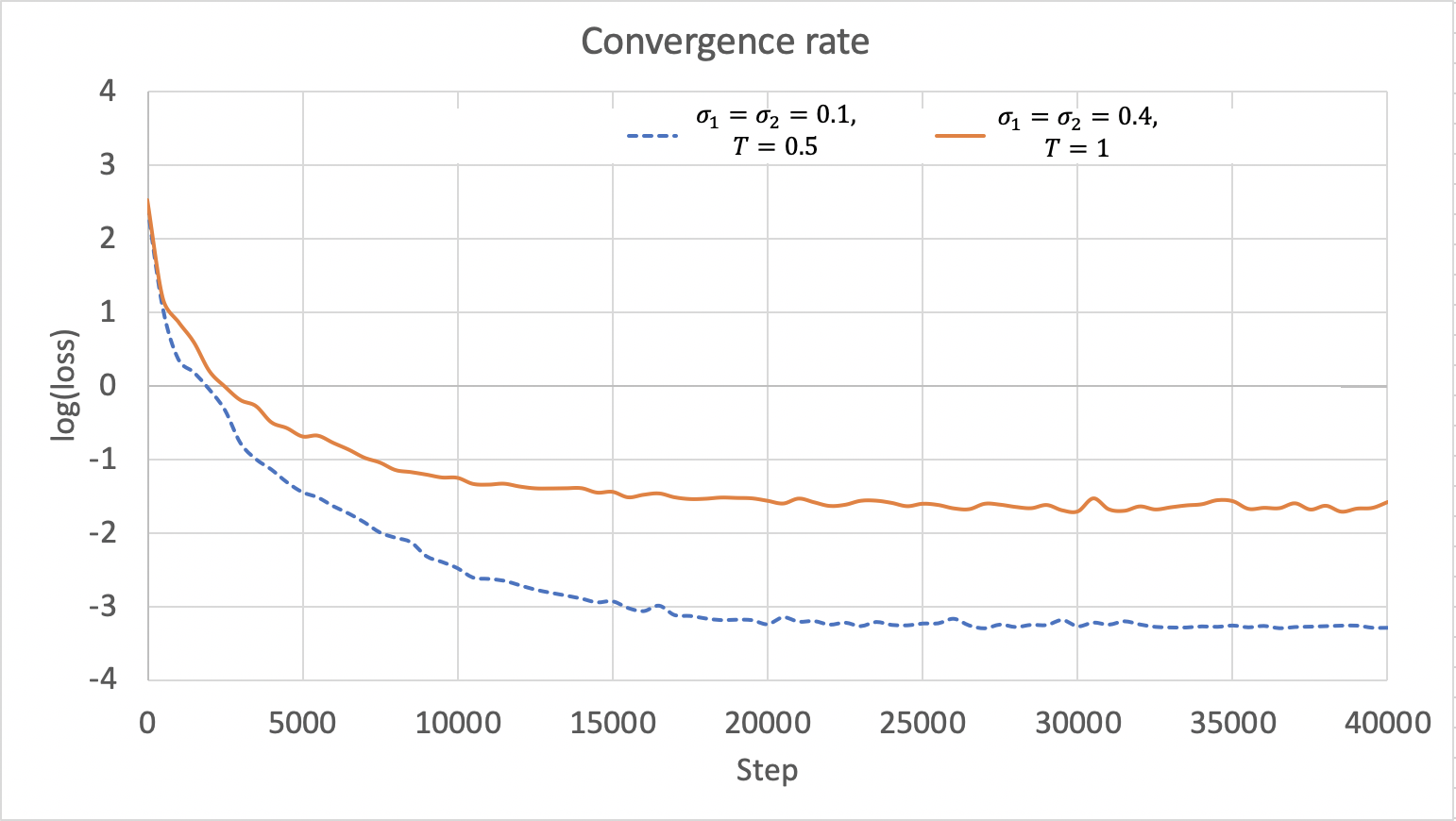

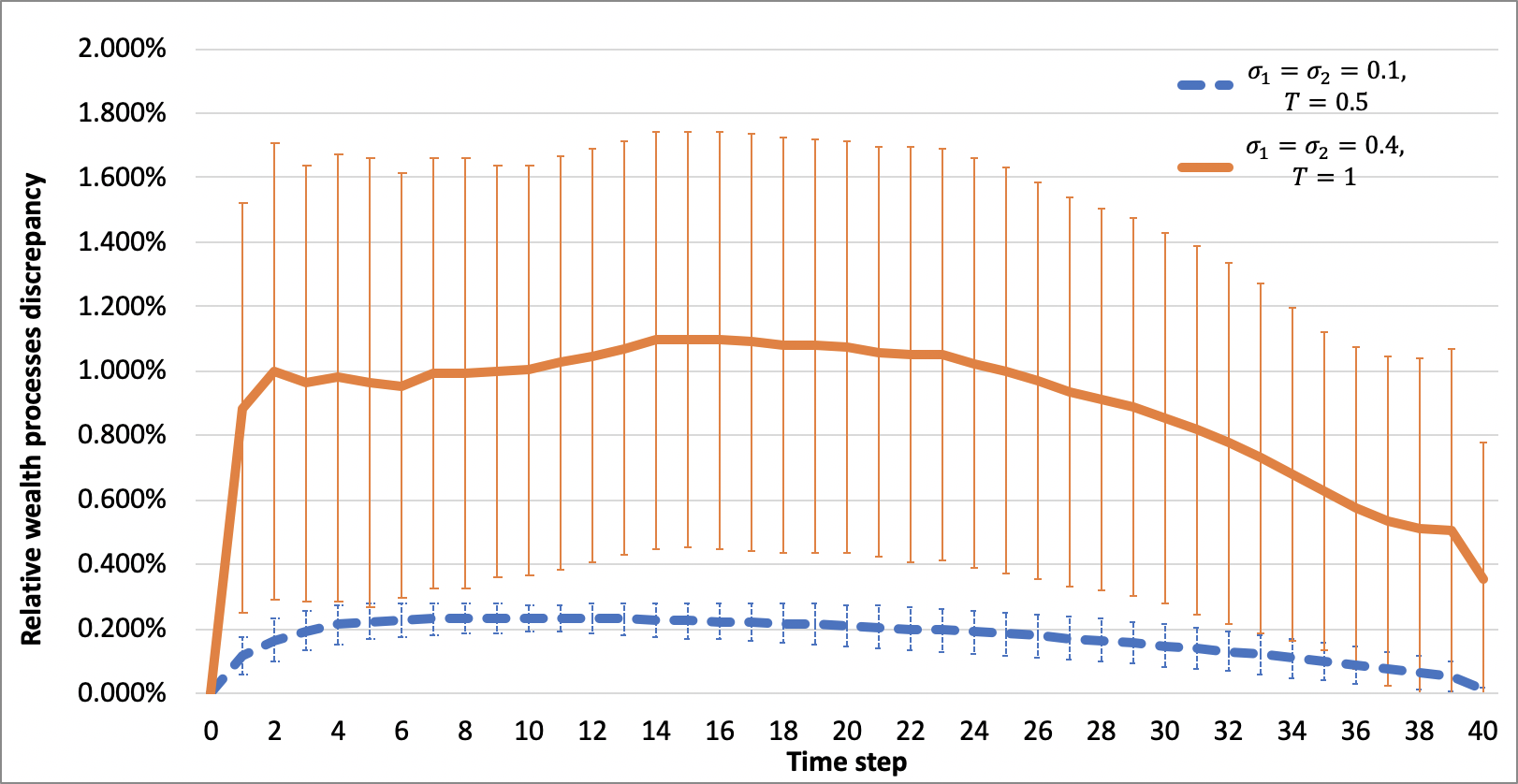

We run several neural network approximations for different model parameters choices and we compare the results of the FBSDE method with the closed form control from Section 3. To compare the two methods, we divide the time interval in 40 time steps. To calculate the approximated solution of the FBSDE , we use a 4 layers neural network as in Weinan et al. [15] with a batch set made of 64 realizations of and a validation set made of 256 realizations. In all numerical examples, we stop training the neural network after 40.000 steps. To calculate the integrals in used in the representation of the control , we apply a quadrature approximation formula. We denote optimal control calculated using NN approximation of the FBSDE solution as , the inventory process and the wealth process . For each parameter choice we compare the closed form control with , the inventory process with and the wealth process with .

In the following we show numerical results for 2 different sets of parameters, both satisfying condition . The only differences between the two following settings are volatilities and the terminal time .

Setting 5.1.

.

Setting 5.2.

.

In Figure 1 is displayed the convergence of loss function under Settings 5.1 and 5.2, which reaches a value lower than after 40.000 training steps in all cases.

As a second step, we calculate the average relative discrepancy between and over many different realizations of the Brownian motion under the two different model parameters sets defined above. In Figure 2 is drawn the average and standard deviation of the quantity along 400 different realizations of , for each time step . We notice that in the low volatility case the relative errors is low and never exceeding 0.3%, while in the hight volatility case the discrepancy increases its magnitude to a value of 1%.

In Table 1 we group the relative discrepancies in Figure 2 and we also consider relative discrepancies of inventories over many different realizations of Brownian motion and for different model parameters choices. In Table 1 is shown the average and standard deviation of the quantities and along 400 different realizations of . We calculate these figures for both Settings 5.1 and 5.2.

| Settings | Av. Rel. Discr. M | Av. Rel. Discr. Q | Runtime | Runtime | ||||

|---|---|---|---|---|---|---|---|---|

| Mean | St. Dev. | Mean | St. Dev. | closed form | NN | |||

|

|

0.170% | 0.00057 | 0.105% | 0.00044 | 210 sec. | 6850 sec. | ||

|

|

0.886% | 0.00601 | 0.665% | 0.00463 | 213 sec. | 7120 sec. | ||

In Table 2 we show that the approximation made by removing the stopping time from optimization problem and fixing it to a terminal time as in in scarcely affects the value function. Indeed, in Table 2 is shown that the average and standard deviation of the relative discrepancy along 400 different realizations of are close to . We calculate these figures for both Settings 5.1 and 5.2.

| Settrings | Mean() | St. Dev.() | ||

|---|---|---|---|---|

|

|

0.0079 | 0.0041 | ||

|

|

0.0271 | 0.0181 |

In all examples we have shown, the results of the two different methods are close to each other. This increases our confidence in considering the solution of the HJB equation and the trading speed found in Section 3 respectively equal to the value function and the optimal trading speed of the problem. The computing time necessary to approximate integrals inside the closed form control representation is around 0.5 seconds for each realization of . To get an acceptable convergence of the neural network we waited 40.000 steps, taking around 110 minutes for each setting. Once the NN is trained, the computational time for the optimal strategy is around 0.6 seconds for each realization. In conclusion, the NN solution requires a time-consuming initial training that may cause delays any time the model needs to be recalibrated. Once the NN has been trained, the runtimes of the two methods are almost equivalent.

5.2 Closed form model vs. single stock models

In this section we compare our model based on both processes and with two simplified models based only on one stock price: one is to approximate the stock price with a GBM , whose first two moments are equal to those of , and the other is to set the cointegration factor to , whose effect is to approximate the stock price with that of . Although in both cases the stock price is approximated with a GBM, the first one is more accurate as it uses the information of the cointegration factor . To get the optimal strategy related to approximation , we compare the stock price with a GBM satisfying the following stochastic differential equation (SDE):

where and are deterministic functions that ensure the first two moments of and are the same for , seen at time 0. Since and are lognormal variables, simple calculus gives

Remark 5.3.

Note that the initial value of the cointegration factor appears in , which ensures the two processes and , seen at time , are the same in distribution. They are different, seen at later time , as is determined by two Brownian motions but by one only. In our numerical test, we approximate the price with the GBM by fixing the cointegration factor to its initial values throughout the whole trading period .

We solve the stochastic control problem with the same objective function as the one in without the last term and with instead of . The HJB equation is given by

| (5.2) |

on , with terminal condition and boundary condition . The optimal trading strategy has the following form

Moreover, equation can be solved using a method similar to the one used in Section 3. Since the solution does not depend on , the equation is easier to be solved.

The second approximation is to use only the price , the optimal trading strategy has the same formula as that in with equal to .

We compare the performance of our strategy with those of the approximations in different settings. By simulating , we can evaluate the performances of the strategies , and respectively based on the price , the GBM price and the price . To compare the distributions of the cash value , we run 100 different realizations of process and, by calculating the trading rate for each realization, get the agent’s final wealth. We assume that the trader executes orders at equally spaced moment in the interval . In particular, we consider 100 trades, occurring every . The data used for numerical tests are the following: . Similar numbers are used in Cartea et al. [7]. These parameters satisfy condition .

Table 3 summarizes the key statistics of agent’s final wealth using the three different strategies.

| Strategy based on | Exp. Val. | St. Dev. | \nth5 Perc. | \nth95 Perc. |

|---|---|---|---|---|

| Price | 723.3 | 79.8 | 598.2 | 861.8 |

| GBM approx. | 718.8 (-0.6%) | 95.2 (19.3%) | 567.3 (-3.5%) | 877.3 (1.8%) |

| Stock | 718.3 (-0.7%) | 95.8 (20.1%) | 561.6(-6.1%) | 877.8 (1.9%) |

Table 3 shows that the strategy has the best performance in producing the highest expected value and the lowest standard deviation for agent’s final wealth, which indicates using the information of both stocks is highly useful in increasing the final wealth and reducing the risk. The strategy is also the one that guarantees the highest final wealth with 95% confidence.

Table 4 summarizes the key statistics of agent’s final wealth with change of one parameter while all other parameters are kept the same. In particular, we compare the performance for different correlation coefficient , penalty coefficients , and volatility . Table 4 shows again that strategy using the information of two stocks outperforms those using only one stock.

| Param. Choice | Strategy based on | Exp. Val. | St. Dev. | \nth5 Perc. | \nth95 Perc. |

|---|---|---|---|---|---|

| Price | 713.3 | 68.4 | 619.0 | 824.0 | |

| GBM approx. | 711.2 | 91.6 | 583.8 | 866.5 | |

| Stock | 710.7 | 95.6 | 579.7 | 883.9 | |

| Price | 718.2 | 73.6 | 610.8 | 850.4 | |

| GBM approx. | 712.7 | 93.2 | 579.3 | 877.1 | |

| Stock | 713.0 | 102.8 | 568.5 | 880.4 | |

| Price | 724.9 | 105.4 | 586.4 | 931.9 | |

| GBM approx. | 720.9 | 110.3 | 541.2 | 982.9 | |

| Stock | 714.9 | 115.1 | 539.4 | 986.9 | |

| Price | 715.7 | 90.8 | 586.0 | 857.7 | |

| GBM approx. | 715.1 | 109.3 | 548.9 | 887.0 | |

| Stock | 714.9 | 113.9 | 541.7 | 897.8 | |

| Price | 709.0 | 85.0 | 579.6 | 854.9 | |

| GBM approx. | 708.0 | 115.2 | 549.8 | 921.7 | |

| Stock | 707.5 | 116.2 | 542.7 | 923.7 | |

| Price | 729.5 | 87.7 | 599.5 | 881.8 | |

| GBM approx. | 726.9 | 112.9 | 564.5 | 928.2 | |

| Stock | 725.7 | 113.7 | 560.5 | 924.6 |

We also observe that for increasing values of penalty parameters , we get decreasing expected value and standard deviation of terminal wealth. This is due to the urgency of liquidation introduced by these penalizations, which implies that when trader’s risk aversion is higher, the optimal strategy concentrates the liquidation on the initial part of period , leading to a less volatile but lower expected final wealth.

The opposite behavior can be inferred from different choices of volatility . The higher the volatility of cointegration process, the lower the expected final wealth (and the higher the standard deviation).

We also perform a robustness test on three strategies by randomly choosing volatilities and from uniform distributions in which and . We run 300 different simulations of stock price .

| Strategy based on | Exp. Val. | St. Dev. | \nth5 Perc. | \nth95 Perc. |

|---|---|---|---|---|

| Price | 712.7 | 90.6 | 566.2 | 892.2 |

| GBM approx. | 711.9 | 117.5 | 558.2 | 982.1 |

| Stock | 709.4 | 125.2 | 545.6 | 991.8 |

6 Conclusion

We have proved that the value function is the unique viscosity solution of the HJB equation associated to our model, that, under some mild conditions, the HJB equation admits a semi-closed integral representation which makes the calculation for agent’s optimal liquidation rate easy and fast. However, the solution of the HJB equation does not always coincide with the value function. We attacked the problem from another perspective, using stochastic maximum principle to solve it. Numerical tests show that the approximate solution of the FBSDE is close to the solution of the HJB equation. This fact increases our confidence in considering the solution of the HJB equation and the trading speed found in Section 3 respectively equal to the value function and the optimal trading speed of the problem. Numerical tests show that, independent of market conditions, our strategy based on two stock prices outperforms other single stock strategies and approximations with the highest expected final wealth and the lowest standard deviation, is as robust as other strategies known in the literature, based on a single stock.

Appendix A Proofs

We first introduce some notations and relations that are used in the proofs. Denote by and

| (A.1) | ||||

The objective function can be written as

Denote by , the solution of (2.1), (2.2), and (2.3) with the initial condition and square integrable feasible control and . We omit the superscript in and we denote it as when the initial conditions are clear from the context. Using the standard stochastic analysis for stochastic differential equations, we have (see, e.g., Krylov [11])

| (A.2) |

Lemma A.1.

Let be a constant and , then there exists a constant such that for any

| (A.3) |

and for any

| (A.4) |

Proof.

Process , defined in , has explicit formulation

Using Ito’s formula, we have the process satisfies the following SDE

The SDE above satisfies conditions of Krylov [11, Corollary 2.6.12], then there exists a constant such that . Using that for any , on , we get :

Finally, we apply similar arguments to get :

∎

Lemma A.2.

Let and . There exists , independent of , such that

| (A.5) |

Proof.

Using results on GBM (cf. [14, Theorem 1.3.15] and [11, Corollary 2.6.12]) and using , we have that, for any , there exists a constant independent of and such that

| (A.6) |

Hence, for any there exists , independent of , so that

The explicit formulations for processes and give

| (A.7) | ||||

Here we have used the fact that for , on . Using similar argument as in , we get that there exists such that

∎

A.1 Proof of Theorem 2.1

We follow the proof of Verification Theorem Pham [14, Theorem 3.5.2] to show that and coincide on . The two main differences between our setting and Pham’s setting are that solution does not satisfy a quadratic growth condition and the presence of a stopping time in the definition of value function in our case. We define sequence of stopping time similarly as in [14, proof of Theorem 3.5.2], by capping it with the stopping time :

We notice that and the stopped process is a martingale. Let be fixed. By taking the expectation of the Ito’s representation of , we get

| (A.8) |

Since is a solution to the HJB equation , for a general

and applying it to , we get

| (A.9) |

We apply the dominated convergence theorem to previous inequality. Both sides are bounded by an integrable process independent on . By using boundedness of process and Holder inequality, we have that

which is bounded independently on , using and square integrability of control process . By , Holder inequality, growth condition on and recalling that is bounded, we conclude that for any , there exists independent of such that

We apply the dominated convergence theorem to by sending :

Since is continuous on , by sending to , we obtain by the dominated convergence theorem:

By terminal and boundary condition of HJB equation , we know that , so we have

which implies that

From arbitrariness of , it follows that on .

To prove that on , we proceed as before, by getting a similar version of in which the control process is substituted by the optimal control :

By applying optimality of , we get

Proceeding as before, we apply dominated convergence theorem to both sides of previous expression. By sending and then sending to , we get

By terminal condition of the HJB equation, , so we have

This shows that on .

A.2 Proof of Theorem 2.2

To prove the result, we first give a technical lemma.

Lemma A.3 (Comparison Principle).

Let (respectively ) be an upper semicontinuous viscosity subsolution (resp. lower semicontinuous viscosity supersolution) to the following HJB equation

| (A.10) |

for any . Assume there exist and such that

| (A.11) |

for any . If

| (A.12) |

then on .

Proof.

The Lemma is proved following Pham [14, proof of Theorem 4.4.5]. The main difference between our statement and Pham [14, Theorem 4.4.5] is our functions and are not polynomially growing and are defined in a subset of space. We apply the first step in [14, proof of Theorem 4.4.3], which provides an equivalent formulation for the HJB equation . Let be specified later, and , then and are respectively subsolution and supersolution to

| (A.13) |

for any . With a slight abuse of notation, in the remaining of the proof, we denote , respectively , and we replace equation with .

We adapt second step of [14, proof of Theorem 4.4.3] to show that there exists a function such that for any , is a supersolution to . Define , where and are as in . Define for any

where and is defined in . We observe that is nonnegative and infinitely many times differentiable on . An explicit calculation shows that

We observe that and there exists a constant such that and for any . Simple calculus shows that . Then, we get

| (A.14) |

Choosing so that , we get that for any , the function is, as , a supersolution to . Moreover, from definition of , and from growth conditions on , we have that for and , grows more rapidly than and . For and , and are finite, while . This implies that for any , there exists an open and bounded set so that and

| (A.15) |

To conclude the proof of the Lemma, we need to show that

| (A.16) |

However, using , upper semicontinuity of , lower semicontinuity of and that , we get that

| (A.17) | ||||

| (A.18) |

By applying , and we reduce our objective from to the proof of

| (A.19) |

To prove the above statement, we assume by contradiction that . On the bounded set , functions and are uniformly Lipschitz and is uniformly continuous. Then, by following Pham [14, proof of Theorem 4.4.5], we get that for any , , which is a contradiction. We conclude that for any , and so both and hold true. By taking limit of going to in , we get that in , which concludes the proof. ∎

We now prove Theorem 2.2. By analysing value function , we get the following upper and lower bounds. Using boundedness of process and , there exists such that for any ,

On the other hand, by choosing , there exists such that for any

Here in the last inequality we have used . All conditions in [14, Propositions 4.3.1 and 4.3.2] are satisfied. In particular, [14, Condition (3.5)] holds true in and is locally vounded as proved in upper and lower bounds above. Then, by applying Pham [14, Propositions 4.3.1 and 4.3.2], we prove that the value function is a viscosity solution to the HJB equation .

Using the above upper and lower bounds we get that satisfies the growth condition . Then, using Comparison Principle Lemma A.3, we conclude that value function is the unique viscosity solution of HJB equation . ∎

A.3 Proof of Proposition 2.3

To prove the result, we first give one technical lemma.

Lemma A.4.

Let be fixed and let , defined in , be the set of admissible controls. Then, the value function , defined in , has the following property:

| (A.20) |

for any and , where is a constant independent of .

Proof.

Let be fixed and . We assume w.l.o.g. that . Denote and the two solutions to with initial conditions and respectively and the stopping times and . We observe that

| (A.21) |

We fix a control . We observe that -a.s., since -a.s. for any , by the assumption . Recall that

| (A.22) |

we get that

| (A.23) |

Using uniformly boundedness of with respect to , obtained by , we get that there exists independent of and of control such that

| (A.24) |

Using and merging and we get that there exists independent of and of control such that

| (A.25) |

Similarly to , we get that there exists independent of and of control such that

| (A.26) |

and that

| (A.27) |

Using boundedness of and , we get

| (A.28) |

Merging , and and applying and , we conclude that there exists independent of and of control such that

| (A.29) | ||||

Finally,

By using Holder’s inequality with parameters and , we get

Hence, using boundedness of process , for any

| (A.30) | ||||

All previous inequality can also be obtained when . By merging inequalities , and into and using arbitrariness of control and , we have proved . ∎

Continuity of value function is proved using Lemma A.4. Let be fixed. We assume w.l.o.g. that . We observe that

| (A.31) |

However, uniformly on for as stated in Lemma A.4. If we apply Dynamic Programming Principle [14, Remark 3.3.3], we get that for any there exists such that

Using boundedness of and , it is easy to show that there exists such that

By using Lemma A.4, boundedness of , -integrability of and for any and Holder inequality, we get that there exists independent of and such that

| (A.32) | ||||

We observe that using Holder inequality with coefficients and

| (A.33) |

Here in the last inequality we used Jensen’s inequality for . Reminding that and applying , , and to , we get that, uniformly on

From arbitrariness of we conclude that previous limit converges to . Continuity of follows from , by sending . The same results can be obtained when .

A.4 Proof of Proposition 3.1

Define for any , . Condition is equivalent to proving that for any . A simple calculus on second PDE in shows that function satisfies the following PDE:

on , with terminal condition .

We check that conditions of Feynman-Kac Theorem are fulfilled for function . As we have proved in , is twice differentiable and bounded from above and function is linearly exponential on variable . Hence, we get the following Feynmann-Kac representation for :

| (A.34) |

where is the solution to the following SDE:

is an OU process and for any fixed , is a normal distributed random variable with first two moments equal to

Calculus on normally and log-normally distributed random variables gives

| (A.35) | ||||

By applying to we get result in .

We now prove that integral in is nonnegative. From definition of and in we have

can be written as

| (A.36) |

where is defined as

To prove that for any , we show that, under condition , is nonnegative. Observing that

we get that for any , the minimum point of satisfies the following equation

By evaluating in ,

If condition is satisfied, then and from we conclude that is nonnegative. ∎

A.5 Proof of Proposition 3.3

Using boundedness of and , linearity of in and linear exponential growth of with respect to , we conclude there exist such that

| (A.37) |

Applying Holder inequality, we get there exists such that

Using , we conclude that there exists , independent of and , such that

which implies . ∎

References

- [1] Almgren, R. (2012). Optimal Trading with Stochastic Liquidity and Volatility. SIAM Journal on Financial Mathematics, 3(1), 163-181.

- [2] Almgren, R., Chriss, N. (1999). Value under liquidation. Journal of Risk, 12(12), 61-63.

- [3] Almgren, R., Chriss, N. (2001). Optimal execution of portfolio transactions. Journal of Risk, 3(2), 5-39.

- [4] Almgren, R. (2003). Optimal execution with nonlinear impact functions and trading-enhanced risk. Applied Mathematical Finance, 10(1), 1-18.

- [5] Bertsimas, D., Lo, A. W. (1998). Optimal control of execution costs. Journal of Financial Markets, 1(1), 1-50.

- [6] Brockwell, P., Davis, R., Deveaux, R., Fienberg, S. (2016). Introduction to Time Series and Forecasting. Springer.

- [7] Cartea, A., Jaimungal, S., Penalva, J. (2015). Algorithmic and High-Frequency Trading. Cambridge University Press.

- [8] Huberman, G., Stanzl, W. (2005). Optimal liquidity trading. Review of Finance, 9(2), 165-200.

- [9] Karatzas, I., Shreve, S. E. (1991). Brownian motion and stochastic calculus. Springer.

- [10] Kharroubi, I., Pham, H. (2010). Optimal Portfolio Liquidation with Execution Cost and Risk. SIAM Journal on Financial Mathematics, 1(1), 897-931.

- [11] Krylov, N., Balakrishnan, A. V. (1980). Controlled diffusion processes. Springer.

- [12] Li, Y., Zheng, H. (2015). Weak Necessary and Sufficient Stochastic Maximum Principle for Markovian Regime-Switching Diffusion Models. Journal of Applied Mathematics and Optimization, 71(1), 39-77.

- [13] Obizhaeva, A., Wang, J. (2013). Optimal trading strategy and supply/demand dynamics. Journal of Financial Markets, 16(1), 1-32.

- [14] Pham, H. (2010). Continuous-time Stochastic Control and Optimization with Financial Applications. Springer.

- [15] Weinan, E., Jiequn H., Arnulf, J. (2017). Deep Learning-Based Numerical Methods for High-Dimensional Parabolic Partial Differential Equations and Backward Stochastic Differential Equations. Communications in Mathematics and Statistics. Springer, 5 (4), 349-380.