Pricing and Hedging the No-Negative-Equity Guarantee in Equity-Release Mortgages

Abstract

We provide a practical superhedging strategy for the pricing and hedging of the No-Negative-Equity-Guarantee (NNEG) found in Equity-Release Mortgages (ERMs), or reverse mortgages, using a discrete-time model. In contrast to many papers on the NNEG and industry practice we work in an incomplete market setting so that deaths and property prices are not independent under most pricing measures. We give theoretical results and numerical illustrations to show that the assumption of market completeness leads to a considerable undervaluation of the NNEG. By introducing an Excess-of-Loss reinsurance asset, we show that it is possible to reduce the cost of the superhedge for a portfolio of ERMs with the average cost decreasing rapidly as the number of lives in the portfolio increases. All the hedging assets, with the exception of cash, have a term of one year making the availability of a property hedging asset from over-the-counter derivative providers more realistic. We outline how a practical multi-period ERM pricing and hedging model can be built. Although the prices identified by this model will be higher than prices under the completeness assumption, they are considerably lower than those under the Equivalent Value Test mandated by the UK’s Prudential Regulatory Authority.

KEYWORDS: Equity-release mortgages; Reverse mortgages; No-negative-equity-guarantee; Incomplete markets; Superhedging

JEL classification: G13; G22; G38.

MSC classifications: 91G05; 91G10; 91G20 .

1 Introduction

Equity-release mortgages(ERMs) or reverse mortgages have become very popular in recent years, both with income-poor capital-rich homeowners wishing to release some equity in their properties and with insurers seeking higher-yielding assets to back their annuity portfolios as yields on gilts and bonds have dropped to historic lows (according to the UK’s Equity Release Council, insurers issued £3.92 billion of ERM loans in 2019).

Given the relatively large size of ERM assets backing pensioners’ annuities and the complex derivative embedded in these contracts, concerns have been raised over the valuation approach adopted by insurers (see [dowd2018asleep], [dowd2019valuation] and [IrishERM]).

Under a typical ERM policy, the homeowner receives a loan at the start of the contract. The loan increases with interest until the homeowner dies or sells the property at time . Almost all ERM policies have what is called a ”No Negative Equity Guarantee” (NNEG) which means that the homeowner is not liable for the shortfall

| (1) |

between the accumulated loan amount and the sale proceeds .

We assume initially that is the same for all policies in the portfolio (our results are generalised in subsection LABEL:VaryingLoans to the case where loan amounts differ). This means that if there are deaths in year in a portfolio of ERM policies, the insurer would lose cashflows to the value of

This shows that all lifetime mortgages with the NNEG contract condition embody a derivative with the payout

| (2) |

We refer to the option with the payout (2) as the NNEG option (or NNEG, for short) and the embedded property put option with payout (1) as the property put.

At the time of writing, UK insurance companies typically value ERMs by using a discounted (expected) cashflow (DCF) approach. The cost of the NNEG option for each time period is calculated as the expected number of deaths times the cost of the property put (usually calculated using the Black-Scholes formula). For a risk-free discount rate of zero and a pricing measure with the correct marginals, this is equivalent to

| (3) |

We believe that there is a significant problem with this valuation approach because, by (2), we should rather be calculating . If and are independent under (for example, if is the independence coupling of and ), then we do have

| (4) |

Unfortunately, because the insurance markets are incomplete, there are many pricing measures or equivalent martingale measures (EMM) . Under most of these EMMs , (4) does not hold. According to asset pricing theory (see [MathArbit2006] or [follmer2011stochastic] for an introduction in discrete time), there will be a range of arbitrage-free prices , where

| (5) |

and

| (6) |

The price of the NNEG option calculated using the DCF method will lie in the range and is unlikely to be sufficiently large to construct a hedge that will cover all of the claims under the NNEG option.

We note that there is a promising result in the paper of Jacka et al. (§2.3 in [jacka2015coupling]) in which they show that a continuous-time -Markov chain and -Brownian motion under a common filtration are necessarily independent. This would appear to justify the assumption of independence between the deaths (Markov) process and the property-price process for continuous-time models of the ERM. However, in practice there are many reasons that could invalidate the independence assumption (for example, ERMs are discretely-valued and hedged rather than continuously-hedged and trading costs are present, to name but two).

Without a coherent hedging strategy to handle the complex nature of the NNEG option, over-the-counter derivative providers are less likely to provide insurers with hedging assets.

The main contribution of this paper is that we find a superhedging strategy for the NNEG option which turns out to be remarkably cheap. This is surprising because superhedges are usually prohibitively expensive to set up (but on the positive side superhedges are very prudent) and are not usually regarded as feasible hedging strategies.

We do so by assuming the availability of a realistic additional hedging asset— an excess of loss reinsurance (XoL) contract — and use it to price a portfolio of ERMs simultaneously.

The motivation for this approach is the following: for an ERM portfolio consisting of infinitely-many lives the Strong Law of Large Numbers (SLLN) would allow us to guarantee the proportion of lives that die and therefore we could perfectly hedge the NNEG at a cost of per ERM by purchasing property put options, where is the cost of the property put.

By assuming that there is a reinsurance contract available that pays out the excess number of deaths above

| (7) |

where , we can price the portfolio of ERMs as though the portfolio had close to infinitely many lives.

Indeed, in Theorem LABEL:SuperhedgePrices, we show that a cheapest superhedge for the NNEG option will be one of the following superhedges constructed from the candidate hedging assets (cash, a property stock, the XoL contract and life assurances on each of the lives):

-

•

a single Group Life Assurance (GLA) costing

-

•

property puts costing

-

•

property puts and a single XoL contract with excess costing , where is the price of the XoL contract

and, then in Proposition LABEL:AsymptoticHedge, we show that, for sufficiently large and sufficiently small, the cheapest superhedge is always property puts and an XoL contract with excess . The average cost per life of this superhedge is

In effect, the price of the reinsurance contract is the price to be paid to gain access to the SLLN. Notice that, by (3), the ”DCF Black-Scholes” approach gives a value of only to the NNEG which is the same value as the the hypothetical portfolio consisting of infinitely-many lives mentioned earlier.

The use of an excess slightly larger than the average number of deaths reflects the reality that reinsurance would not be available without some such ”experience margin”. A very useful financial consequence is that a Large Deviations Principle will apply to the price of the reinsurance contract and its cost per life will be very small for even relatively small portfolios of lives. In fact, in Proposition LABEL:XoL_LDP, for the single-period model, we show that the price of the reinsurance contract tends to zero exponentially fast as the number of lives goes to infinity.

All the assets, with the exception of cash, will have a term of one period (usually a year) only. One reason for this is that we shall be using a static mark-to-market hedge-and-forget strategy. At the end of each year the superhedge will cover all claims occurring during the year plus a potential release of surplus. The use of short-term disposable assets for hedging makes sense in practice: over-the-counter derivative providers are more willing to provide property derivatives linked to residential property or property indices if the term of the contract is short (see summary of responses to Question 8 in CP48/16 [CP48/16])

The single-period superhedge can be easily extended to multiple time periods. When the first time period terminates, any surplus released from the superhedge contributes to the setup costs of the superhedge for the next period. In order to ensure that there is sufficient release of surplus to construct the next superhedge, the hedging strategy should be calculated working backwards in time. For example, for a model with time periods and lives, a multinomial tree model can be constructed with nodes at time . Starting at time , the superhedge for each time -node is given by Theorem LABEL:SuperhedgePrices. Using the superhedging costs determined in the previous time step, the superhedges for the time -nodes can then be determined using linear programming. Continuing in this way the cheapest time-zero superhedge can be found.

The number of nodes in the tree and hence the number of linear optimisation problems that need to be solved by the computer is not excessive. For example, for years with annual time intervals and lives, there would only be nodes at time .

2 Numerical results for the NNEG option

2.1 Single-period results

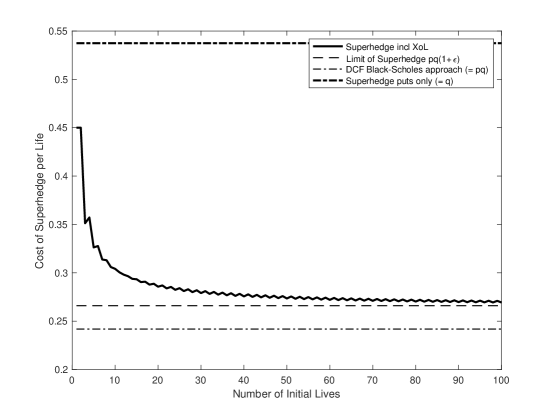

The graph in figure 1 shows how the average cost of the cheapest superhedge reduces with increasing number of lives .

The probability of death is and the cost of the property put is . The XoL price is calculated assuming that the number of deaths is Bernoulli-distributed with parameters and is given by (7) with .

We can see from the graph that, for small , the cheapest superhedge costs which corresponds to holding a GLA. Note that for these small values of , and the XoL contract reduces to a GLA on lives and that . For larger , the superhedging strategy of holding one XoL contract with excess and property puts becomes cheaper as predicted by Theorem LABEL:SuperhedgePrices and Proposition LABEL:AsymptoticHedge.

2.2 Multi-period results

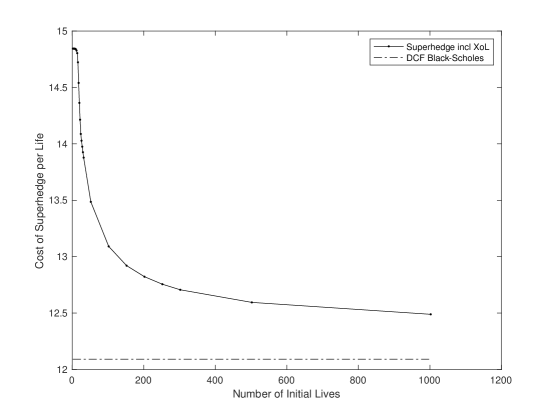

We built a practical multi-period model in Matlab which can calculate the superhedging cost and strategy for the NNEG using the method described in the introduction. We chose parameters similar to those in Table 1 in [dowd2019valuation] for comparison purposes. Our parameters were the following:

-

•

the age of policyholders at the start of the ERM contract is 70

-

•

the initial house price is 100

-

•

house price volatility is 15% p.a.

-

•

the initial loan amount is 40 with loan interest of 5% p.a.

-

•

the risk-free rate is 0% p.a.

-

•

the mortality table used is A67/70 with no adjustments for early redemptions or long term care exits

-

•

the dividend yield (deferment rate) for the property stock is assumed to be zero

The results of the multi-period model for varying number of lives is shown in figure 2. The value ”DCF Black-Scholes” in the figure is the value of the NNEG determined using (4) for multiple periods. i.e. it is equal to , where is the expected number of deaths in period and is the price of a European put option at time zero, with term and strike equal to the accumulated loan amount at time t. The ERM actuaries often call this the risk-neutral Black-Scholes NNEG value. As can be seen from figure 2, it is significantly lower than the superhedge even for a large number of lives .

2.3 Impact of deferment rates

A modification of the risk-neutral Black-Scholes approach used by some insurers is the so called ”real-world Black-Scholes” valuation approach, where house prices are inflated at a rate in excess of the risk-free interest rate, producing an even lower value for the NNEG than the risk-neutral Black-Scholes approach!

Because insurers were/are using these low valuations for the NNEG in the net cashflow calculation for the construction of securitised assets to back their annuity portfolios, the Equivalent Value Test (EVT) was introduced by the UK’s Prudential Regulatory Authority (PRA) as a “diagnostic tool” to help insurers assess whether the yields on their securitised securities is excessive (see the UK’s PRA publication SS2/17 on illiquid assets [SS2/17]). For the EVT test, the PRA chose the Black-Scholes model for a dividend-paying stock to value the NNEG using the concept of ”deferment rates” to justify the use of such a model. This model can produce values for the NNEG which are considerably higher than those of the standard Black-Scholes non-dividend-paying stock model for reasonable dividend rates. A dividend(deferment) rate of was used to produce the values in Table 1 in [dowd2019valuation]. The lowest NNEG value quoted there was 31.5 which is between two and three times higher than the ”Superhedge including XoL” NNEG cost in figure 2.

3 Setting

We represent time by . At time , we assume that there are identical lives, each of whom purchases a lifetime mortgage. The financial market consists of an insurance market with assets which are insurance contracts written on the lives and a non-insurance market consisting of a cash bond and a property stock. We assume that all assets are liquid and can be traded frictionlessly. Any long or short position may be held in the assets. We refer to the combined insurance and non-insurance market as the Combined Market.

To simplify the presentation, we assume that the Combined Market is normalised. i.e. all price processes have been discounted by the cash bond price process. The superhedging strategies or pricing measures are not affected by working in a normalised market.

If one wishes to explicitly model the effects of interest, then one can multiply the relevant formulae by the factor , where is the assumed rate of interest earned by the original cash bond. For example, the undiscounted version of the NNEG payout (2) is . The pricing constraints (10) - (12) are unaffected because we simultaneously inflate the asset payouts and divide by for discounting. For a similar reason, there is no net effect on duality equation (LABEL:eq:DualityEquality).

3.1 The probabilistic framework

The Combined Market is represented by the measurable space , where and is the powerset of .

Corresponding values are as follows:

For , so that is the indicator for an up-jump in the property price index. Similarly if is the indicator that the th life has died by time 1, then . The number of deaths is given by the random variable . We sometimes write instead of if we wish to emphasise the number of lives.

3.2 The non-insurance market

The non-insurance market consists of the following assets:

-

1.

A (normalised) cash bond with a constant price of one.

-

2.

A tradable property stock (which could be an asset provided by an over-the-counter provider such as a derivative on a property index or residential properties) whose value the price processes of the properties are assumed to follow. The model for the price process of the property stock is assumed to be a binomial tree

for , where is the price at time zero of the property stock. To ensure that the binomial stock model does not have arbitrage, we assume that .

3.3 The insurance market

The insurance market consists of the following assets commencing at time and written on the lives:

-

1.

single-life assurances written on each of the lives for a price . If the life dies over , then the contract pays out an amount of one; otherwise the contract expires worthless. We denote its price process by . So and , for and .

-

2.

A group life insurance (GLA) written on all lives costing . The GLA pays out an amount of one for each life that has died over the period . The GLA has the price process . The payout or price at time one of the GLA is

(8) Note that the GLA is a redundant asset because it can be constructed from a holding of single-life assurances, each costing . However, we see later that, for superhedging, only a GLA and not individual single-life assurances is needed.

-

3.

An excess of loss reinsurance (XoL) on the lives with excess . We denote its price process by . The payout or price of the XoL at time one is given in terms of the total number of deaths by

(9) If we wish to emphasize that and are functions of the number of lives , then we denote them by and . If we wish to emphasise the probability of death as well, we write .

3.4 The lifetime mortgage

At time the insurer issues identical lifetime mortgages with loan amount . The loan amount is assumed to be less than the value of the property. We assume that any interest added to the loan is included in the loan amount . We do not consider any other contract terminations or redemptions such as long-term care (LTC) or downsizing. The hedging and pricing strategy developed in this paper could be easily extended to incorporate LTC exits if there are LTC insurance contracts available to use as hedging assets.

3.5 The set of pricing measures

We denote by the reference measure on .

Assumption 3.1.

Under , the random variables are independent and Bernoulli-distributed with probability of success(death) of .

Note that for simplicity we have assumed that lives are independent under the reference measure . The probability measure will be used as a reference measure against which all pricing measures must be absolutely-continuous. We work with the larger class of absolutely-continuous pricing measures rather than equivalent pricing measures because the extremal pricing measures for (6) which we find in Theorem LABEL:SuperhedgePrices are only absolutely-continuous.

Note that the superhedging price is not increased if we take the supremum in (6) over the larger set of all absolutely-continuous pricing measures with respect to (see Remark 1.36 in [follmer2011stochastic]).

In order to calculate the superhedging price of the random payouts (2) in the Combined Market, we need to determine , the collection of probability measures on which are absolutely-continuous with respect to and such that all discounted asset price processes are martingales under .

Definition 3.2.

Members of are called absolutely-continuous martingale measures (ACMMs).

The constraints imposed on to belong to are:

-

1.

must satisfy

After simplifying, we obtain the standard Binomial tree stock pricing constraint

(10) -

2.

must satisfy the single-life assurance pricing constraint

(11) -

3.

must satisfy the XoL pricing constraint:

(12)

The pricing constraints (10) - (12) suggest, that for pricing the NNEG option, we can replace the single life pricing constraint (11) by the weaker GLA constraint

| (13) |

and use a subset of of exchangeable measures defined below:

Definition 3.3.

The set of exchangeable measures is defined to be the set of all under which the sequence of random variables is exchangeable for .

Note that, in the definition of exchangeability, the first element representing property prices is not included in the exchangeable sequence.

Proposition 3.4.

Given and , for satisfying

{IEEEeqnarray}rCl

1 &= ∑_k=0^n z_k,

q = ∑_k=0^n y_k,

np = ∑_k=0^n kz_k,

X_0^e = ∑_k=0^n (k-e)^+z_k,

there exists such that

{IEEEeqnarray}rCl

x_k &= Q’(D_1=k,S_1=S_0u)

y_k = Q’(D_1=k,S_1=S_0d),

for .

Proof.

Define as follows: for with , let

{IEEEeqnarray}rCl

Q’ ((0,ω_1,⋯,ω_n)) &= 1(nk)y_k,

Q’ ((1,ω_1,⋯,ω_n)) = 1(nk)x_k.

Then

{IEEEeqnarray}rCl

Q’ (D_1=k,S_1=S_0d) &= y_k,

Q’ (D_1=k,S_1=S_0u) = x_k.

From its construction, it is clear that is an exchangeable measure on . We prove that is a martingale measure by showing that it satisfies (10) - (12). For (10),

Note that, from (3.5) and (3.5), it follows that . Then for (11),

{IEEEeqnarray*}rCl

Q’(i^th life dies) & = ∑_k=1^n Q’(i^th life dies and D_1=k)

= ∑_k=1^n Q’(i^th life dies—D_1=k)Q’(D_1=k)

= ∑_k=1^n (n-1k-1)(nk) Q’(D_1=k) ,by exchangeability

= 1n∑_k=1^n kz_k

= 1n (np), by (3.4)

= p.

For (12), {IEEEeqnarray*}rCl ∑_k=0^n (k-e)^+Q’(D_1=k) = ∑_k=0^n (k-e)^+z_k = X_0^e.

It follows that is an ACMM and . ∎

Corollary 3.5.

Let . Given any , there exists such that so that

| (14) |

Proof.

We require that the Combined Market is arbitrage-free. This imposes the following upper bound on the price of the XoL contract:

Proposition 3.6.

A necessary and sufficient condition for the Combined Market to be arbitrage-free is that the price of the XoL contract must satisfy

| (15) |

Proof.

Suppose that

| (16) |

We create a portfolio which will allow us to make a risk-free profit at time . At time , we sell an XoL contract with excess and purchase GLAs on the lives. This can be done at a non-positive cost since

| (17) |

from (16). At time there are deaths. We have to pay a claim of and we receive from the GLA assurance. It is straightforward to show that and for strict inequality holds and so the portfolio is an arbitrage.

For the converse, if (15) holds then,by Theorem LABEL:SuperhedgePrices below, there exists an ACMM . Let . Then is an EMM and therefore there is no arbitrage in the market. ∎

Note that the construction of an EMM in the above proposition shows that these are multiple EMMs and so the Combined Market is incomplete.

4 Pricing the NNEG option

We use the following result in the proof of Theorem LABEL:SuperhedgePrices - namely, the well known (and straightforward to prove) weak duality pricing result

| (18) |

Note that, without loss of generality we may assume that the loan amount of the lifetime mortgage lies between the upper and lower prices of the property stock i.e.

| (19) |

because, if , then is -a.s. zero and the price of the hedge is zero. Conversely, if , then since

{IEEEeqnarray*}rCl

(L-S_1)^+ &= L-S_0u+S_0u-S_1

= L-S_0u+(S_0u-S_1)^+,

it follow that

{IEEEeqnarray*}rCL

E^Q[D_1(L-S_1)^+] & = (L-S_0u)E^Q[D_1] + E