Online Action Learning in High Dimensions: A Conservative Perspective

Abstract

Sequential learning problems are common in several fields of research and practical applications. Examples include dynamic pricing and assortment, design of auctions and incentives and permeate a large number of sequential treatment experiments. In this paper, we extend one of the most popular learning solutions, the -greedy heuristics, to high-dimensional contexts considering a conservative directive. We do this by allocating part of the time the original rule uses to adopt completely new actions to a more focused search in a restrictive set of promising actions. The resulting rule might be useful for practical applications that still values surprises, although at a decreasing rate, while also has restrictions on the adoption of unusual actions. With high probability, we find reasonable bounds for the cumulative regret of a conservative high-dimensional decaying -greedy rule. Also, we provide a lower bound for the cardinality of the set of viable actions that implies in an improved regret bound for the conservative version when compared to its non-conservative counterpart. Additionally, we show that end-users have sufficient flexibility when establishing how much safety they want, since it can be tuned without impacting theoretical properties. We illustrate our proposal both in a simulation exercise and using a real dataset.

Keywords: Bandit, online learning, high dimensions, LASSO, regret

1 Introduction

In this paper we propose modifications to the original -greedy heuristics to work with high-dimensional contexts considering a more conservative perspective. Our framework can be especially useful for practical applications where an agent uses the experience and the repeated observation of a large pool of covariates to conservatively learn the best course of action relatively to some reward.

More specifically, consider a simple example in consumer behavior where few accidental discoveries may have a positive impact on users experience but, as time passes, they tend to increasingly remain loyal to a set of similar vendors. An intuitive example relates to the case where a consumer may be impressed after visiting a completely new restaurant but, after some disappointments, she becomes more and more reluctant to accept suggestions outside her set of preferred restaurants. Other examples from different markets could be provided as well. Now consider a recommendation system that wants to employ a learning rule looking to explore profitable opportunities in this example. One feature that stands out from the above-mentioned pattern is the fact that a proper learning rule should not stop to suggest completely new restaurants (maybe at random) since, eventually, a pleasant discovery can be made. However, it should progressively discourage randomness and stimulate exploitation of not the best action but in a set of preferred similar vendors. We understand such rule under the conservative philosophy introduced in Wu et al. (2016) since, for the algorithm to be useful, exploration of new actions should be done with caution.

The original -greedy, described in Auer et al. (2002), seems to be a valid substrate to be used in setups similar to the example above, since the selection of actions fully at random is already performed at a decreasing rate (). However, it exploits only the best empirical action, which has some drawbacks, such as to be time consuming in contexts when the difference in payoff between the best and second bests strategies is small (Wu et al. (2016)). In our example, it would also be meaningless to suggest only the best vendor. Therefore, while remaining loyal to the -greedy philosophy, in this paper we augment it with a new exploitation option that brings more safety to its decision-making in a high-dimensional setup. The resulting rule is based on increasing the frequency of time that a preferred set of actions is exploited while reducing the incidence of randomly selected actions in the -greedy. It can be understood as a conservative extension of the works in Bastani and Bayati (2020) and Kim and Paik (2019), which explore, non-conservatively, algorithms similar to the -greedy in high-dimension contexts.

1.1 Motivation and Comparison with the Literature

A multiarmed bandit problem can be interpreted as a sequential problem, where a limited set of resources must be allocated between alternative choices to maximize utility. The properties of the choices are not fully known at the time of allocation and may become better understood as time passes, provided a learning rule with theoretical guarantees is available. A particularly useful extension of the bandit problem is called the contextual multiarmed bandit problem, where observed covariates yield important information to the learning process in the sense that the supposed best policy may be predicted; see, for instance, Auer (2003); Li et al. (2010); Langford and Zhang (2008).

Contextual multiarmed bandit problems have applications in various areas. For instance, large online retailers must decide on real-time prices for products and differentiate among distinct areas without complete demand information; see, for example, den Boer (2015). Arriving customers may take purchase decisions among offered products based on maximizing their utility. If information on consumers’ utility is not available, the seller could learn which subset of products to offer (Sauré and Zeevi (2013)). Further, the reserve price of auctions could be better designed to maximize revenue (Cesa-Bianchi et al. (2013)). Mechanisms design in the case where agents may not know their true value functions but the mechanism is repeated for multiple rounds can take advantage of accumulated experience (Kandasamy et al. (2020)). Also, sequential experiments or programs, including public policies (Tran-Thanh et al. (2010) devises an algorithm that consider costly policies), may be assigned under the scope of learning problems. In this regard, excellent works can be found in Kock and Thyrsgaard (2017), Kock et al. (2018) and Kock et al. (2020).

Designing a sequence of actions to minimize error is a difficult task and, for a considerable period in the past, was also a computationally intractable goal. In this respect, several heuristics with well-behaved properties have emerged in the literature, such as Thompson sampling (Agrawal and Goyal, 2012; Russo and van Roy, 2016), upper confidence bounds (Abbasi-Yadkori et al., 2011) and greedy algorithms (Auer, 2003; Bastani et al., 2020; Goldenshluger and Zeevi, 2013).

It is very well documented the recent growing availability of large datasets and their usage for different sectors of society. One of the drivers of this recent popularity can be assigned to shrinkage estimators applied to sparse setups, relative to their potential to catalyze the benefits of huge information sets into strong predictive power. This superior performance is certainly useful for learning problems based on the observation of large pools of covariates, but there is not an extensive list of papers providing theoretical properties of such bandits. Among few others, we cite Carpentier and Munos (2012), Abbasi-Yadkori et al. (2012), Deshpande and Montanari (2012), Bouneffouf et al. (2017), Bastani and Bayati (2020), Kim and Paik (2019) and Krishnamurthy and Athey (2020).

Our work is mostly related to Bastani and Bayati (2020) and to Kim and Paik (2019). Both papers provide theoretical properties for algorithms that are similar to the high-dimensional -greedy we provide in this paper. Minor differences appear as, for example, the fact that exploration at random in the algorithm studied in Bastani and Bayati (2020) is performed at pre-determined specific instants of time and its frequency does not decrease as time passes. The later is also present in Kim and Paik (2019). However, our work completely distinguishes from these papers by adapting the high-dimensional -greedy to work in a more conservative fashion, by giving more preference to promising actions while reducing the frequency that random actions are adopted, restricting the associated risk. As so, it is potentially more suitable to practical applications where pleasant surprises are still valued from random actions, at a decreasing rate, but there is a set of similar options where any one of them is often a good option to be adopted by a learning rule. In summary it is a conservative extension of Bastani and Bayati (2020) and to Kim and Paik (2019) that respect, in a flexible way, limitations and particularities imposed by some practical applications.

1.2 Main Takeaways

We add to the high-dimensional bandit literature, by showing that distinct levels of restrictions in the exploration of new actions can be settled by using variations of the original multiarmed -greedy heuristic. We first expand the -greedy rule to high-dimensional contexts leading to an algorithm that is similar to the ones used in Kim and Paik (2019) and Bastani and Bayati (2020). Then, we combine it with a competing exploitation mechanism that comprises, at each time step, a number of actions that lead to the best predicted rewards. We call it as the order statistics searching set.

From the empirical perspective, we provide an algorithm that can be used to implement the main rule proposed in this paper. In general terms, it is equipped with an initialization phase where information about parameters is gathered by attempting distinct actions and, after that, the rule properly said starts with the main exloration-exploitation phase. In a simulation study, we show its robustness with respect to a reasonable range for the variables imputed by end-users.

From the theoretical point of view, we show that the cumulative regret of the conservative high-dimensional -greedy algorithm is reasonably bounded. Aside the benefit that an order statistics searching set can be less time consuming when rewards are very close to each other (Wu et al. (2016)), we also show in this paper that even with separable payoffs (in probability), there are conditions related to the amount of viable actions that being conservative leads to a stricter bound on regret.

We prove that the cumulative regret of the proposed algorithm is sub-linearly bounded, respecting an upper bound growing at no more than , and seems to be an improvement on the bound found in Kim and Paik (2019) on a similar non-conservative algorithm (). The work in Bastani and Bayati (2020) found an upper bound of which seems to have a worse dependence on than ours. When the order statistics searching set is considered as an alternative exploration mechanism, in addition to the benefits already mentioned regarding harmful actions, we show that the -growing rate above mentioned can be reduced by a factor of .

In addition, we show that it is viable to pick any cardinality for the order statistics searching set and still respect the theoretical limits established in this paper. Recall an important trade-off: under the conservative approach one should be caution to explore new actions but, a learning rule should explore to be accurate in the long run. In this sense, allowing end-users to choose any cardinality for the order statistics searching set is the same as letting them to choose the “size” of safety, tuning the algorithm to the specifics of the environment/market they are inserted.

The algorithm proposed in this paper outperforms simple and adapted (to the high-dimensional context) counterparts in a simulation exercise, while seems to be effective, presenting good learning properties, when applied to a a real recommendation system dataset.

1.3 Organization of the Paper

The rest of this paper is structured as follows. Section 2 establishes the framework and the main assumptions for the regret analysis, while Section 3 depicts the main algorithm. In section 4 we derive the theoretical results of the paper and in section 5 we provide a sensitivity analysis of the algorithm with relation to parameters set by the user and a comparison among simple and adapted algorithms. Section 6 exhibits the performance of our proposed learning rule when applied on a real recommendation system data set. Section 7 concludes this work. All proofs are relegated to the Appendix and to the Supplementary Material.

1.4 Notation

Regarding the notation used in this paper, we provide in this subsection general guidelines. Definitions and particularities are presented throughout the paper. Bold capital letters represent matrices, small bold letters represent vectors and small standard letters represent scalars. Matrices or vectors followed by subscript or superscript parentheses denote specific elements. For example, is the -th column of matrix , is the element of , while is the -th scalar element of vector . Let be an arbitrary vector space. The symbol is the usual vector norm on , while is the ball defined in around a point , the set . Let be an arbitrary set. Then, is used to represent its cardinality, while and are the traditional floor and indicator function, respectively, the later taking the value of 1 when .

2 Setup and Assumptions

Consider an institution, a central planner or a firm, in this paper simply called the planner, that wants to maximize some variable (reward). In order to do that, it has to choose at each instant of time an action (arm) among some alternatives inside a finite set . We consider each , , arbitrary.

Define the action function , such that for each , informs that at time the action selected by the planner was . Let and define to be the set that stores all values of when the action was adopted and let to be its cardinality.

Let to be a probability space. When choosing actions, the planner also observes covariates at each time step, e.g., individual characteristics of its target sample, as well as the sequence of its past realizations which we consider to be identically and independently distributed (iid) draws from . It also knows the past rewards111At time , the planner observes but does not yet know . , only when was implemented before . The range222For ease of notation, in our setup, is a scalar random variable, but the reader will recognize throughout this paper that this choice is not restrictive. Multivariate versions are allowed. of is a subset of , while that of is a subset of , where may grow with the sample size. To simplify notation, in the rest of this paper we do not exhibit this dependence (between and ) explicitly.

The connection between covariates and rewards is stated as follows:

Assumption 1 (Contextual Linear Bandit).

There is a linear relationship between rewards and covariates of the form:

| (1) |

where is an idiosyncratic shock and , belongs to the parametric space . Furthermore:

-

i.

, , .

-

ii.

, the sequence is composed of independent centered random variables with variance .

Remark 1.

Assumption 1 restrains our setup to linear bandit problems. Rewards are action/time-dependent, in the sense that not only the dynamics of impacts the level of rewards but, depending on the chosen policy , the mechanism () that “links” covariates to rewards is different. Moreover, we require covariates to be bounded in absolute terms and a sequence of errors, with finite variance. Both assumptions are easier to be satisfied in most practical applications and are necessary to guarantee that instantaneous regrets (defined below) do not have explosive behavior.

Two pieces of nomenclature have been used: actions chosen by the planner and “mechanisms” (parameters) through which these actions operate impacting rewards. Assumption 2 connects them.

Assumption 2 (Metric Spaces).

There is an h-Lipschitz continuous function , such that , .

Remark 2.

Assumption 2 is a restriction on the joint behavior of the two relevant metric spaces we are working with, the set of actions and the parametric space. Its main purpose is to avoid the possibility that small changes in actions could result in too different mechanisms, which would not be reasonable in several practical situations. In the case considered by Assumption 2 we have that for two actions , , both belonging to , , for the Lipschitz constant and and , relevant metrics for the two spaces.

One of the most useful instruments to assess the effectiveness of online learning algorithms is the regret function, which, in general, may be studied in its instantaneous or cumulative version. In general, a regret function represents the difference (in expected value) between the reward obtained by choosing an arbitrary action and the one that would be obtained if the best action were adopted. Clearly, the term best action does not have an absolute meaning, but relative to alternatives that belong to the same set of actions. A sequential rule is not learning at all to choose actions if its cumulative regret grows linearly or at a more convex rate (). Good algorithms achieve, for example, (Wu et al. (2016)). Definition 1 formalizes these concepts.

Definition 1.

(Regret Functions) The instantaneous () regret function of implementing any policy at time , leading to the reward , and the respective cumulative () regret until time are defined as:

Motivated by the high-dimensional context, we perform Lasso estimation in the following sections. This estimator operates on the well-known sparsity assumption, i.e., that in the true model, not all covariates are relevant to explain a given dependent variable. Regarding this aspect, we define the sparsity index in Definition 2 and impose the compatibility condition for random matrices in the Assumption 3, which is standard in the high-dimensional literature.

Definition 2.

(Sparsity Index) For any and , define and the sparsity index as .

Assumption 3.

(Compatibility Condition) Define and . For an arbitrary -matrix and , such that , for some , , with such that:

where and are the empirical and population covariance matrices of , respectively.

Finally, we impose a bounding condition for the density of covariates near a decision boundary, as in Tsybakov (2004), Goldenshluger and Zeevi (2013) and Bastani and Bayati (2020), among others.

Assumption 4.

(Margin Condition) Consider the Lasso penalty parameter chosen at , . For , , , such that for any :

Remark 3.

Assumption 4 is related to the behavior of the distribution of “near” a decision boundary. In these cases, there is a possibility for rewards to be so similar that small deviations in estimation procedures could lead to suboptimal policies being selected by the algorithms. With this assumption, we impose some separability (in probability) for the rewards, in the sense that there is a strictly positive probability that the reward () for a given policy is strictly greater than that of any other policy . In contrast to other papers, we establish an upper bound for the constant as a function of the intrinsic parameters of the problem.

3 Algorithms and Estimation Procedures

One of the most important feature of every learning rule relates to the way it sequentially selects actions. In general, at each time step, an algorithm should decide between: exploit and adopt the action that leads to the most profitable reward, in a predicted sense in the case of contextual learning, or explore and implement a different one, according to some criteria. The expected outcome of exploitation is to reduce regret by adopting actions that empirically have been outperforming the available alternatives. However, besides the fact that the future may eventually not reflect the past, eroding the intrinsic value of past good actions, if an algorithm does not explore it simply does not discover good actions that have not been sufficiently tested in the past. As a consequence, the learning rule could remain stuck, for long periods of time, on suboptimal actions (best only in the past). This exploitation-exploration trade-off is well-known in the learning literature and dictates the properties of the regret function. See, for example, Auer (2003) and Langford and Zhang (2008).

The vast majority of learning algorithms take the above mentioned problem into consideration while pursuing the main goal of a “well-behaved” bound for their regret functions. The -greedy heuristic is no different. In the way it is presented in Auer et al. (2002), first one should define a decaying exploration weight , for example the one suggested by the authors, , and . Then, at each time step, the rule should explore with probability and choose a random action inside the set of possible actions, , drawn from . With probability it exploits choosing the action that leads to the best empirical average reward, , .

The above-defined rule is appropriate for multiarmed bandits (without context). To extend it to cases where covariates play an important role, one should simply change the criterion for exploitation and replace the best empirical average reward for the best predicted reward, that is, , but now, where, considering Assumption 1, . We compute each considering a high-dimensional context and we call the resulting learning rule as the HD -Greedy.

The algorithm updates considering available information when was implemented in the past. Specifically, at an arbitrary instant of time , let to be an matrix containing observed covariates at instants of time , provided that . Likewise and are the observed rewards and error terms, respectively. Then, we update by Lasso:

| (2) |

where is the lasso penalty parameter. Following the suggestions in Kim and Paik (2019) and in Bastani and Bayati (2020), as already introduced in Assumption 4, we consider to be time-dependent () and bounded by (see Corolary 1 for further details).

Without previous knowledge, in order to have initial estimates of each at the beginning of the learning problem, we impose an initialization phase to the HD -Greedy, which consists to try every action, observe the respective outcomes and estimate parameters according to equation (2). We require it to last , which implies that every action in is implemented times, . The initialization phase is also present in the conservative version of the HD -Greedy.

The properties of similar versions of the HD -Greedy were investigated in Bastani and Bayati (2020) and Kim and Paik (2019). In the former, the authors employ the forced-sampling exploration, which prescribes, in a deterministic way, a set of times when each action must be adopted. Although it may be similar to our initialization phase, the HD -Greedy does not explore actions at fixed instants of time, but in a ex-ante unknown frequency, remaining literal to the learning rule defined in Auer et al. (2002). Consequently, comparing the post-initialization (most important) phase of the HD -Greedy with the algorithm in Bastani and Bayati (2020) we see that, differently from the forced-sampling, exploration in our algorithm may occur at a low (high) rate, depending on a future unknown sequence of trials. Theoretical properties of HD -Greedy are, in some sense, a generalization of those provided in Bastani and Bayati (2020), regarding different exploration regimes. Also, the HD -Greedy adopts a decreasing weight for exploration, which seems to be not used both in Bastani and Bayati (2020) and in Kim and Paik (2019). We do not deeply investigate the possible impacts that both these differences may have on the performance of algorithms, because the HD -Greedy is treated in this paper as a benchmark for its conservative variant (our main contribution). However, we infer that they may not exert great influence, since the theoretical properties of the HD -Greedy are comparable and, in some cases, better than the results obtained by the cited authors (See Section 4 for further details).

The conservative version of the above described algorithm, called in this paper as CHD -Greedy, inserts a competing exploitation mechanism in the HD -Greedy learning rule that comprises, at each time step, a number of actions that lead to the best predicted rewards. We call it as the order statistics searching set.

Recall the standard definition of order statistics, which for the case of predicted rewards computed at each time step considering all possible actions, takes the form:

For , let be the set of the best predictions at time which we consider as new option for exploitation, such that , . to avoid extremes. In fact, if for some , , the overall effect would be to increase the weight to exploit the action with the best estimated reward, and we would be under the scope of the (non-conservative) HD -Greedy algorithm. On the other hand, when is higher, possibly close to , the learning rule would be encouraging random exploration and, again the non-conservative version would be dictating the learning properties. In this sense, the bounds on serve the purpose to guarantee that the resulting learning rule is more conservative than its precursor. Definition 1 presents the CHD -Greedy algorithm.

Definition 3 (CHD -Greedy Algorithm).

Let , , and be defined as in Auer et al. (2002), . Let , and be the weight for the conservative exploitation. Then, the CHD -Greedy algorithm is:

4 Finite Sample Properties of Regret Functions

In this section we present the main contributions of this paper in the form of two theorems. Both proofs, developed in the Appendix, rely on a few Lemmas in the Supplementary Material. More specifically, the proof strategy is as follows: Lemmas 1 and 2 establish the finite-sample properties of the parameters estimated by Lasso in equation (2), taking into consideration the framework proposed, while Lemmas 3, 4 and S.18 provide theoretical properties for the cumulative regret in the initialization phase and for the instantaneous regret of both HD and CHD -Greedy algorithms, respectively. Theorem 1 is a compilation of the above results and is the main contribution of the paper, as it provides the bound for the cumulative regret functions of the CHD -Greedy algorithm. Theorem 2 extends the main result and provides conditions that guarantees the conservative version to be the best course of action.

Theorem 1 (Cumulative Regret of CHD -Greedy algorithms).

Notice in the proof of Theorem 1 that the cumulative regret of the HD -Greedy algorithm is the most important term in the bound of its conservative version. This fact is a recognition that the second term of does not grow at a faster rate than the first one. As already mentioned, the suggested upper bound growing at no more than seems to be an improvement on the bound found of a non-conservative similar algorithm in Kim and Paik (2019) (). The work in Bastani and Bayati (2020) found an upper bound of which has a worse dependence on than ours.

Theorem 2 (Flexibility and Dominance of CHD -Greedy algorithm).

Provided that the conditions required by Lemmas 4 and S.18 are satisfied, the upper bound for the CHD -Greedy algorithm does not depend on and, at least with probability , for an increasing sequence , if :

where is defined in Lemma 2, is provided in Lemma 4, while and are defined in Lemma S.18, where is the usual plugged with .

Theorem 2 represents our additional contribution to the high-dimensional online learning literature by providing supplemental guarantees for practitioners with mild restrictions in exploration of new actions. In these cases, limitations imposed by practical applications naturally bound exploration to be confined in a restrictive, possibly time-varying, set of actions. In these cases, it would be preferable to have some flexibility in the action screening process without impacting the algorithm’s properties. Theorem 2 can be helpful in this regard since it provides the flexibility to explore groups of different sizes according to the users’ needs. Additionally, it suggests that this approach (being conservative) would not only be advisable (by operational limitations in real applications), but also the best course of action in terms of stricter bounds, provided that the set of viable actions is sufficiently large. In these cases the bound of the HD -Greedy can be reduced by a factor that grows at no more than (See Theorem 1 for negative second term on ).

5 Simulations and Sensitivity Analysis

Choosing any policy at each instant of time generates the well-known problem of bandit feedback, which in general terms, relates to the fact that a planner following an arbitrary algorithm obtains feedback for only the chosen action. Rewards from the adoption of other actions are not observable and the best possible one, at each time , remains unknown to the planner, which impairs the online evaluation of regrets. Also, this characteristic can lead to incorrect premature conclusions, for example, in cases when a action had not been frequently tested in the past. In this case, it may be labeled as suboptimal, while in fact, it simply did not have sufficient opportunity to prove itself. In general, bandit feedback poses serious problems for the evaluation of different learning rules and comparison of algorithms using real data sets. If a target action, different than the implemented one, is to be evaluated, difficulties arise, leading, for example, to alternatives such as counterfactual estimation (Agarwal et al., 2017). In this section we circumvent this problem by analyzing the properties of the CHD -Greedy algorithm in a simulated exercise.

First we evaluate the sensitivity of the algorithm with respect to changes in: (1) the number of available actions, ; (2) the weight attributed for the exploitation in the higher-order statistics searching set, ; and (3) the cardinality of the higher-order statistics searching set, . Notice that, since the CHD -Greedy algorithm inherits most of its characteristics from the non-conservative version, it would be expected for the HD version to present similar behavior, at least for changes in .333Recall that the HD -Greedy algorithm does not count with or . Second, we also compare both CHD and the HD algorithms with a few related alternatives.

General Setup: We set ; covariates are generated from a truncated Gaussian distribution such that Assumption 1.i translates to , . The dimension of is , and the sparsity index is . , and . We consider as the number of times that each action is implemented in the initialization phase.444We do not explicitly test the sensitivity of the algorithm to since, given our specification, this variable affects only the duration of the initialization phase and the precision of the parameters estimates right after this stage. For the first, we use , since the duration of the initialization phase is set to . Each action has its own parameter drawn independently from a probability distribution. The simulation is repeated times, and the results are presented as the average regret. That is, the instantaneous regret at a specific time is the average of 50 simulated instantaneous regrets at this same time.

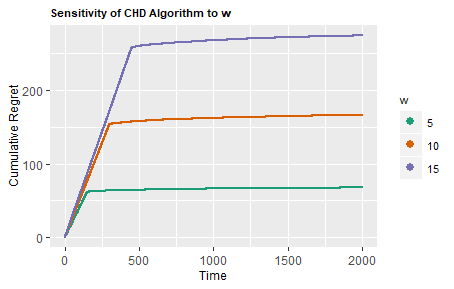

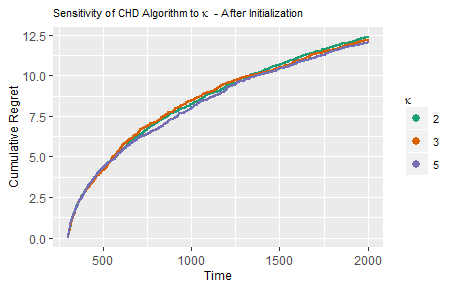

Sensitivity to : We set , and .

From the proof of Theorem 1, one can verify that the cumulative regret function is increasing in . This can be attributed to the specifics of our framework, since the higher the value of , the longer the initialization phase, implying that the sub-linear growth of the exploration vs. exploitation phase bound would take longer to operate. Consequently, the levels of cumulative regret increase with . Recall, however, that low values of may not guarantee that the CHD -Greedy algorithm respects a stricter bound than its non-conservative alternative. These arguments are illustrated in Figure 1.

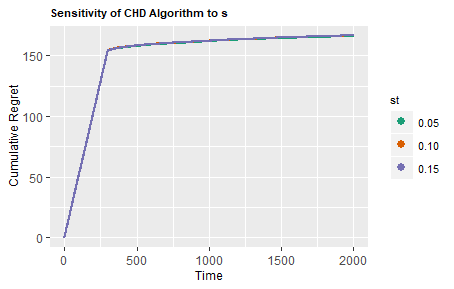

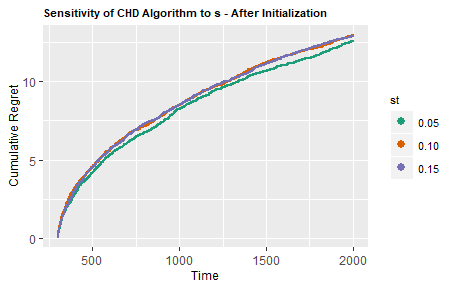

Sensitivity to : Figure 2(a) illustrates that the performance of CHD -Greedy algorithm is highly robust to small variations in and Figure 2(b) is just an amplification of Figure 2(a) for . Simulations are conducted for , and .

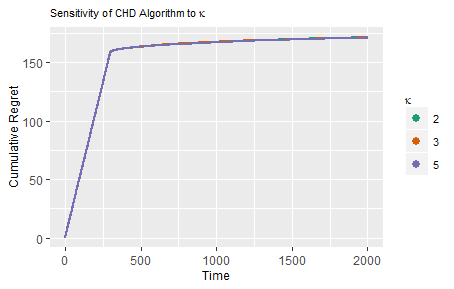

Sensitivity to : Figures 3(a) and 3(b) present the sensitivity of the algorithm to values of , and . The first panel comprises all time steps, and the second is for . The results can be associated to the first part of Theorem 2 that implies that bounds are not -dependent. In fact, these figures present the simulated performance of the CHD -Greedy algorithm and not its bounds for different values of but, in a similar fashion, observe in Figure 3(b) that cumulative regrets intersect each other and none of the curves dominate the others for the entire period tested.

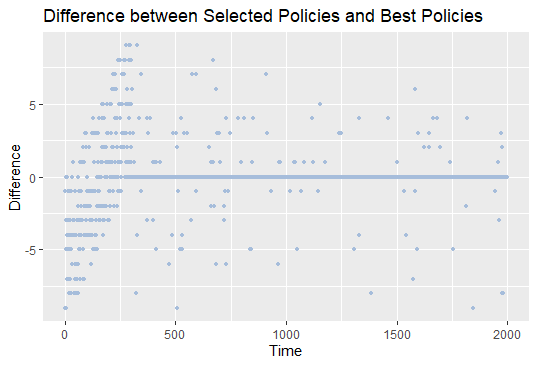

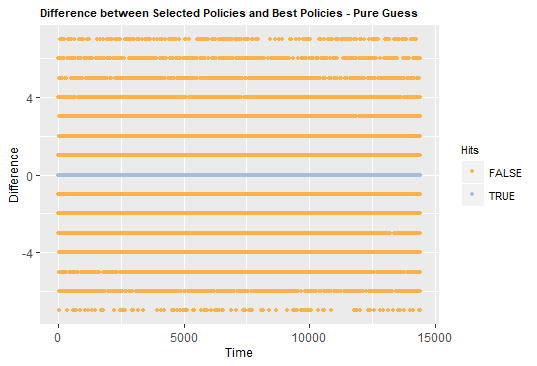

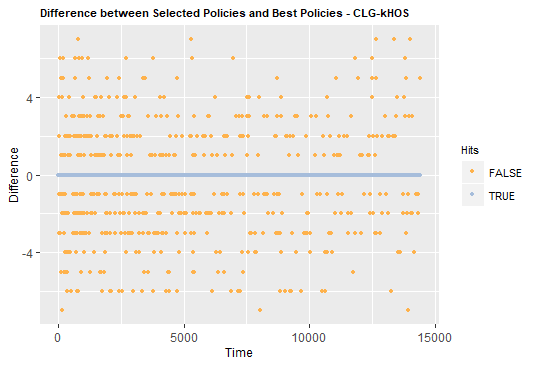

Figures 4(a) and 4(b) explore different ways of visualizing the performance of the CHD -Greedy algorithm. The first presents the difference in the action selected by our learning rule at each time step and the respective best one, exemplified by a simulation with , and . In this figure, a point with a difference at zero means that the algorithm selected the best action, while any other value for difference implies a sub-optimal action adopted. Compared to the initialization period, the exploration-exploitation phase makes fewer mistakes, qualitatively attesting the learning process.

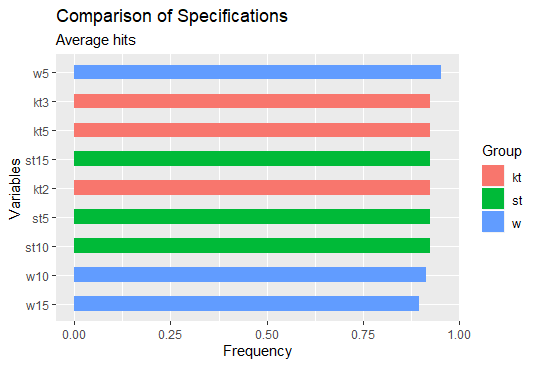

Figure 4(b) exhibits the average (across simulations and across the time horizon) frequency of hits, restricted to the post-initialization period, of the CHD algorithm for varying parameters: , and . Performance seems to be fairly robust and, considering 50 simulations and 2000 time steps for each one of them, the worst specification adopts the best action approximately of the time on average, while the best one reaches .

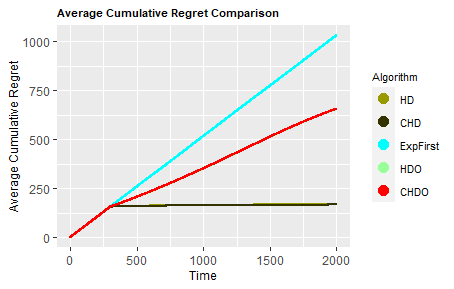

5.1 Comparison to Related and Adapted Algorithms

As far as we know, the CHD -Greedy algorithm is the first conservative high-dimensional learning rule, which impairs a proper comparison exercise. Therefore, in a simulation exercise, we contrast it with its non-conservative version (HD -Greedy) and three additional adapted algorithms, named in this paper as: HDO -Greedy, CHDO -Greedy and Expfirst. The general setup assumed in the beginning of this section is expanded to consider , and and the same initialization phase is implemented for all algorithms. We briefly discuss each algorithm in the sequence.

HDO and CHDO -Greedy algorithms: These are the counterparts of HD and CHD -Greedy algorithms, but using OLS as the estimation methodology to update estimated parameters when is selected. In a high-dimensional sparse context, we would expect lasso to outperform a poorly defined OLS estimator. Inclusion of these algorithms in the comparison set serves to corroborate one of the motivations of this work, by contrasting the differences in performance in a online learning problem, resulting from distinct estimation procedures in a high-dimensional context.

ExpFirst: This is a kind of exploitation-only algorithm. The initialization phase is the same as in the other algorithms and estimation of for selected actions in this stage is carried out as in the high-dimensional case, employing lasso. However, after initialization, the algorithm does not explore anymore. That is, it always selects the policy that presented the minimum regret in the initialization. In a different setting, provided that some new assumptions are in place, Bastani et al. (2020) have shown that exploitation-only algorithms can achieve logarithmic growth in the OLS-estimation context.

Figure 5(a) compares the average cumulative regrets (across 50 simulations) of the CHD -Greedy with those of its peers, above discussed. Notice that the CHD algorithm largely outperforms, except when compared to its non-conservative version, in which case the improvement in the average cumulative regret is modest. Figure 5(b) amplifies Figure 5(a) and focus only on these two algorithms, considering the post-initialization phase ().

6 Application: Recommendation System

6.1 Data and Exploratory Analysis

The dataset is obtained from Kaggle Database Repository555Restaurant Recommendation Challenge, Version 2, from https://www.kaggle.com/mrmorj/restaurant-recommendation-challenge. The dataset is provided public under the license CC BY-NC-SA 4.0, which provides users the right to share, copy, redistribute the material in any medium or format and adapt, remix, transform, and build upon the material for noncommercial purposes. and we use it to build a recommendation engine to predict which restaurants customers are most likely to order from, given their characteristics. Information on this data set was initially gathered by Akeed666Akeed is a mobile application that customers can download to their smart phones. It will allow customers in Oman to order food from their favorite vendors and have it delivered to their addresses., an app-based food delivery service in Oman.

We work with a share of the original dataset considering 15 features777Several features of the original data set were discarded since they have the vast majority of their entries as missing values or they are categorical variables with only one category. and observations comprising customers and their respective transactions with 8 vendors. The training sample has observations for 927 different customers, used for the initialization stage of our algorithm. The testing sample has observations containing customers which can be new ones or repeated when compared to the training sample.

Table 1 provides descriptive statistics for each of the 15 variables we consider. Notice that in the column labeled as “type” only two categories appear: “original” if the variable came from the original data set or “new” if it were created under the scope of this paper. Regarding the former type, we find labels created quite self-explanatory but any question about the meaning of any variable can be settled by visiting https://www.kaggle.com/mrmorj/restaurant-recommendation-challenge. We define the new variables as: Age of Customer Register – number of days since the customer has first registered; Age of Vendor Register – number of days since the vendor has first registered; Frequent Vendor – total number of transactions made by a specific vendor with any customer; Frequent Customer – total number of transactions made by a specific customer with any vendor; and Distance from Customer to Vendor – euclidean distance between a customer and a vendor based on latitude and longitude values.

6.2 Framework and Results

The framework proposed in previous sections is suitable for sequential problems of decision making. In order to comply with this, we interpret the dataset as being sequential, in the sense that at each time step only a customer arises, chooses a vendor and purchases items. We allow the same customer to arise multiple times both in the training and in the testing samples. Also, as defined in Section 2, the cardinality of the set of possible actions () is, in this context, the number of selected vendors we would like to recommend, indexed by . At every instant of time a customer appears and our algorithm should recommend a vendor, based on observed covariates.

To gather information about customers preferences we run a initialization stage by offering every vendor to every customer in the training sample. Since we know every customers’ choices, we compute a unit reward if we are right in our recommendation or a zero reward otherwise. Therefore, after this phase we have sufficient information to estimate the sequence in equation (2). In the long run, each customer in the test sample also arises at each time step when we are supposed to recommend a vendor following the online learning rule proposed in this paper. Recall that each is updated once the action is adopted.

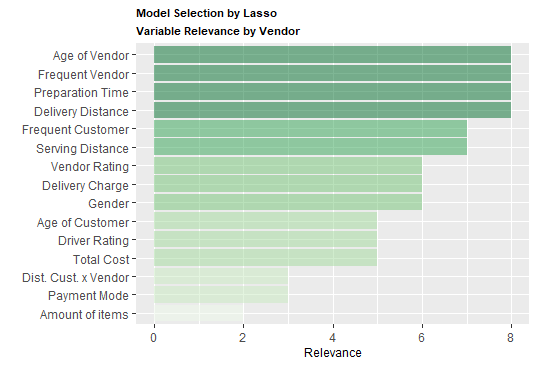

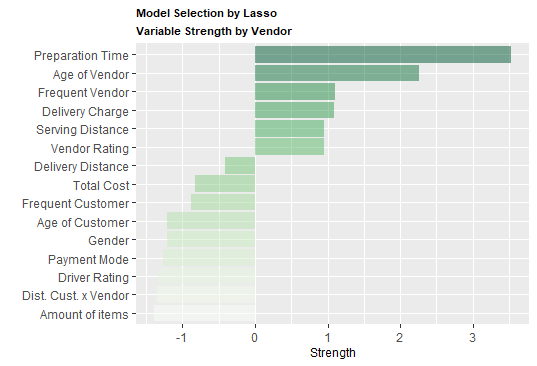

Figure 6 exhibits two related measures for the variable selection of the LASSO estimation, equation (2). Fix an arbitrary variable . Define the relevance () and strength ( of the -th variable as: and , where is the -th entry of estimated beta for vendor . Intuitively, is about how frequent across vendors a variable is selected as relevant to explain the customers’s preferences, and relates to the potential to impact rewards.

The left panel of Figure 6 exhibits the relevance of each variable, while the second panel is about the demeaned strength in the LASSO estimation. From both panels, it is possible to infer that preferences are strongly influenced by how frequent is the vendor in performing transactions, preparation time and if it is an experienced vendor regarding the time elapsed since it first registered in the app. To see this, take age of vendor register as example. It is selected by LASSO as a relevant variable for all 8 vendors and the absolute sum of its estimated entries across all these 8 vendors is the second largest.

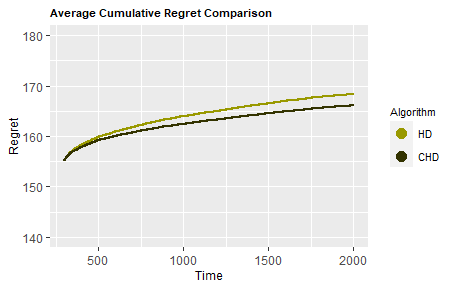

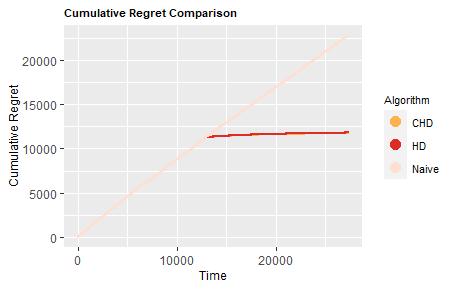

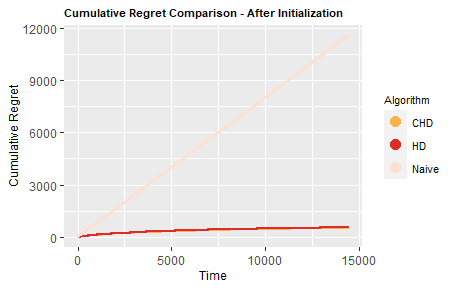

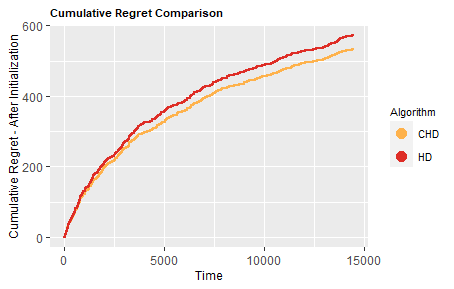

Main results are presented in Figures 7 and 8. The objective here is to explore the benefits of being conservative in a framework where users might be loyal to a set of specific vendors. For this, we compare the CHD -Greedy with its non-conservative version, using as a benchmark a naive rule that always guess. The later can be understood as a algorithm restricted to its exploration only. The top left panel of Figure 7 compares the algorithms, while the right panel focus on the post-initialization stage. Notice that the naive benchmark regret grows at an apparently linear rate, while both CHD and HD algorithms learns to choose actions in the long run.

Figure 8 provides the comparison between CHD and HD algorithms in the post-initialization phase. Results indicate that the rules provided in this paper effectively learn through experience with mild differences between them. Moreover, it is interesting to highlight that the comparative performance between both algorithms is very similar to what was observed in the right panel of Figure 5, when the learning rules were tested in a controlled environment. Another way to qualitatively attest the learning process of the CHD algorithm is looking at Figure 9, that presents a comparison for the frequency of hits between the naive (which never learns) and CHD. A customer would agree with a recommendation made by the naive algorithm of the exploration versus exploitation stage, while for the CHD rule, matching achieves .

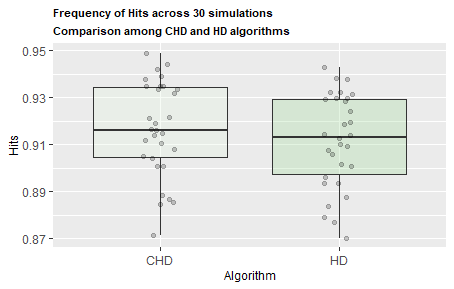

Since the results so far are conditional on the 8 pre-selected vendors, we perform a simple robustness check that consists of running 30 simulations, where in each of them we select randomly a different set of 8 vendors and, consequently, a different set of customers and their respective transactions. This exercise may be understood as a robustness to different sets of customers’s preferences and to different sets of vendors features (which may impact preferences). Figure 10 compares the frequency of hits in the exploration versus exploitation phase for the CHD and HD -greedy algorithms. One can see that previous conclusions do not change, regarding the learning capacity and the potential benefits the algorithms would generate to a recommendation system. Actually, the observed frequencies of hits are not too much dispersed and the two respective coefficients of variation are very similar (0.4082 and 0.4080, respectively), indicating that both learning rules operate similar to different sets of inputs.

7 Concluding Remarks

In this paper, we contribute to augment the basket of online learning solutions related to contextual bandits in high-dimensional scenarios. We extend a popular multiarmed bandit heuristic, the decaying -greedy heuristic, to high-dimensional contexts and we augment it with a conservative exploitation solution. The resulting learning rule can be useful for practical applications where an agent uses the experience and the repeated observation of a large pool of covariates to conservatively learn the best course of action relatively to some reward.

For a decreasing -greedy multiarmed bandit, we find that adding a high-dimensional context to the original setting does not substantially jeopardize the original results, except that in our case, regret not only grows reasonably with time but also depends on the covariate dimensions, as the latter grows with the former in high-dimensional problems. We find an upper bound growing less that which seems to be comparable and, in some cases, even better than similar alternatives in the literature.

Moreover, we show that the consideration of a higher-order statistics searching set as an alternative to random exploration introduces safety to the decision-making process, without deteriorating the regret properties. More specifically, we show that the regret bound when the order statistics searching set is considered is at most equal to but mostly better than the case when random searching is the sole exploration mechanism, provided that the cardinality of the set of actions is sufficient large. Furthermore, we show that the upper bound on the cumulative regret function of the CHD -Greedy algorithm is not affected by the cardinality of the higher-order statistics searching set, which, per se, provides flexibility for end-users facing constraints on the number of viable actions.

In a simulation exercise, we show that the algorithms proposed in this paper outperform adapted competitors. Also, by employing both algorithms at a recommendation system data base, we confirm their learning trough experience, attesting their potential usefulness for companies that want to leverage their profits with an accurate recommendation engine.

Appendix A Proof of Theorem 1

Proof.

For , the cumulative regret of both HD -Greedy and CHD -Greedy algorithms are given by Lemma 3 in the Supplementary Material.

For , Lemmas 4 and S.18 indicates that, with probability , instantaneous regret of both algorithms are bounded. Considering the whole period , there exists such that, at least, with probability all instantaneous regret are bounded. Following this line, we first compute the cumulative regret for the HD Greedy algorithm until time and then, express the regret for the conservative version as a function of the first. Since is a decreasing function of , using Lemma 10 in the Supplementary Material:

Adding the period before , then with probability at least , the total cumulative regret for the HD -Greedy until time is bounded as:

For the CHD -Greedy algorithm, from Lemma S.18:

For an chosen by the end-user:

Finally, also with probability at least , the total cumulative regret for the CHD -Greedy algorithm until time is bounded as:

Provided that , Theorem 2 indicates that:

and as a whole is strictly lower than the bound for . ∎

Appendix B Proof of Theorem 2

Proof.

For the second part of the theorem, note that from the results of Lemmas 4 and S.18 in the Supplementary Material, we know that for every and for , at least with probability (see Theorem 1):

For the CHD -Greedy to have a stricter instantaneous bound than its non-conservative version, it is sufficient that:

which is guaranteed to occur when:

| (3) |

The LHS of equation (3) unfolds three cases of interest:

Case 1: Consider the set , where is arbitrarily chosen to guarantee that . On , the LHS of equation (3) has positive curvature and a discriminant of , indicating the existence of two real roots, .

Then, for any , it is sufficient for our purposes to analyze when can be greater than or equal to the largest root (). Since is increasing with , we require that:

| (4) |

where for values of .

Refer to the discussion made in Remark 4 in the Supplementary Material for the cases when is an increasing sequence. Coupled with a decreasing relationship between and (see Lemma 2), case 1 () is the most important situation for the high-dimensional case studied in this work. Nonetheless we also briefly provide below the analysis for the other cases.

Case 2: Consider the set where, like case 1, is chosen to guarantee a negative curvature for the LHS of equation (3). The discriminant is the same as in case 1 () but, easy calculations show that for our result to hold, since .

Case 3: Consider the set . In this case, is sufficient for our result to hold, for the counterpart of the above-defined .

For the first part of this theorem, recall that

| (5) |

None of the terms in inequality (5) depend on , which completes the proof. ∎

References

- Abbasi-Yadkori et al. (2011) Y. Abbasi-Yadkori, D. Pál, and C.Szepesvári. Improved algorithms for linear stochastic bandits. In J. Shawe-Taylor, R.S. Zemel, P.L. Bartlett, F. Pereira, and K.Q. Weinberger, editors, Advances in Neural Information Processing Systems 24, pages 2312–2320. 2011.

- Abbasi-Yadkori et al. (2012) Y. Abbasi-Yadkori, D. Pál, and C. Szepesvári. Online-to-confidence-set conversions and application to sparse stochastic bandits. In Proceedings of the 15th International Conference on Artificial Intelligence and Statistics, pages 1–9, 2012.

- Agarwal et al. (2017) A. Agarwal, S. Basu, T. Schnabel, and T. Joachims. Effective evaluation using logged bandit feedback from multiple loggers. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 687––696, 2017.

- Agrawal and Goyal (2012) S. Agrawal and N. Goyal. Analysis of Thompson sampling for the multi-armed bandit problem. In Proceedings of the 25th Annual Conference on Learning Theory, pages 39.1–39.26, 2012.

- Auer (2003) P. Auer. Using confidence bounds for exploitation-exploration trade-offs. Journal of Machine Learning Research, 3:397–422, 2003.

- Auer et al. (2002) P. Auer, N. Cesa-Bianchi, and P. Fischer. Finite-time analysis of the multiarmed bandit problem. Machine Learning, 47:235–256, 2002.

- Bastani and Bayati (2020) H. Bastani and M. Bayati. Online decision-making with high-dimensional covariates. Operations Research, 68:276–294, 2020.

- Bastani et al. (2020) H. Bastani, M. Bayati, and K. Khosravi. Mostly exploration-free algorithms for contextual bandits. working paper 1704.09011, arXiv, 2020.

- Bühlmann and van de Geer (2011) P. Bühlmann and S. van de Geer. Statistics for High-Dimensional Data: Methods, Theory and Applications. Springer, 2011.

- Bouneffouf et al. (2017) D. Bouneffouf, I. Rish, G.A. Cecchi, and R. Féraud. Context attentive bandits: Contextual bandit with restricted context. In Proceedings of the 26th International Joint Conference on Artificial Intelligence, pages 1468–1475, 2017.

- Carpentier and Munos (2012) A. Carpentier and R. Munos. Bandit theory meets compressed sensing for high dimensional stochastic linear bandit. In Proceedings of the 15th International Conference on Artificial Intelligence and Statistics, pages 190–198, 2012.

- Carvalho et al. (2018) C.V. Carvalho, R.P. Masini, and M.C. Medeiros. ArCo: An artificial counterfactual approach for high-dimensional panel time-series data. Journal of Econometrics, 207:352–380, 2018.

- Cesa-Bianchi et al. (2013) N. Cesa-Bianchi, C. Gentile, and Y. Mansour. Regret minimization for reserve prices in second-price auctions. In Proceedings of the 24th Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1190–1204, 2013.

- den Boer (2015) A.V. den Boer. Dynamic pricing and learning: Historical origins, current research, and new directions. Surveys in Operations Research and Management Science, 20:1–18, 2015.

- Deshpande and Montanari (2012) Y. Deshpande and A. Montanari. Linear bandits in high dimension and recommendation systems. In Proceedings of the 50th Annual Allerton Conference on Communication, Control, and Computing, pages 1750–1754, 2012.

- Goldenshluger and Zeevi (2013) A. Goldenshluger and A. Zeevi. A linear response bandit problem. Stochastic Systems, 3:230–261, 2013.

- Kandasamy et al. (2020) K. Kandasamy, J.E. Gonzalez, M.I. Jordan, and I. Stoic. Mechanism design with bandit feedback. working paper 2004.08924, arXiv, 2020.

- Kim and Paik (2019) Gi-Soo Kim and Myunghee Cho Paik. Doubly-robust lasso bandit. In Advances in Neural Information Processing Systems, volume 32. Curran Associates, Inc., 2019.

- Kock and Thyrsgaard (2017) A.B. Kock and M. Thyrsgaard. Optimal sequential treatment allocation. working paper 1705.09952, arXiv, 2017.

- Kock et al. (2018) A.B. Kock, D. Preinerstorfer, and B. Veliyev. Functional sequential treatment allocation. working paper 1812.09408, arXiv, 2018.

- Kock et al. (2020) A.B. Kock, D. Preinerstorfer, and B. Veliyev. Treatment recommendation with distributional targets. working paper 2005.09717, arXiv, 2020.

- Krishnamurthy and Athey (2020) S.K. Krishnamurthy and S. Athey. Survey bandits with regret guarantees. working paper 2002.09814, arXiv, 2020.

- Langford and Zhang (2008) J. Langford and T. Zhang. The epoch-greedy algorithm for multi-armed bandits with side information. In J.C. Platt, D. Koller, Y. Singer, and S.T. Roweis, editors, Advances in Neural Information Processing Systems 20, pages 817–824. 2008.

- Li et al. (2010) L. Li, W. Chu, J. Langford, and R.E. Schapire. A contextual-bandit approach to personalized news article recommendation. In Proceedings of the 19th International Conference on World Wide Web, pages 661––670, 2010.

- Li et al. (2021) Wenjie Li, Adarsh Barik, and Jean Honorio. A simple unified framework for high dimensional bandit problems, 2021.

- Lin and Bai (2011) Z. Lin and Z. Bai. Probability Inequalities. Springer-Verlag, 2011.

- Russo and van Roy (2016) D. Russo and B. van Roy. An information-theoretic analysis of Thompson sampling. Journal of Machine Learning Research, 17:2442––2471, 2016.

- Sauré and Zeevi (2013) D. Sauré and A. Zeevi. Optimal dynamic assortment planning with demand learning. Manufacturing & Service Operations Management, 15:387–404, 2013.

- Tran-Thanh et al. (2010) L. Tran-Thanh, A. Chapman, J.E. Munoz De Cote Flores Luna, and A. Rogers N.R. Jennings. Epsilon–first policies for budget–limited multi-armed bandits. In Proceedings of the 24th AAAI Conference on Artificial Intelligence, pages 1211–1216, 2010.

- Tsybakov (2004) A. Tsybakov. Optimal aggregation of classifiers in statistical learning. Annals of Statistics, 32:135–166, 2004.

- Wang et al. (2018) Xue Wang, Mingcheng Wei, and Tao Yao. Minimax concave penalized multi-armed bandit model with high-dimensional covariates. In Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 5200–5208, 2018.

- Wu et al. (2016) Yifan Wu, Roshan Shariff, Tor Lattimore, and Csaba Szepesvári. Conservative bandits, 2016.

| Variables | Mean | Std | Maximum | Minimum | type |

|---|---|---|---|---|---|

| Amount of items purchased | 2.23 | 1.99 | 38 | 1 | Original |

| Total Cost | 12.09 | 9.45 | 131 | 0 | Original |

| Payment Mode | 1.35 | 0.76 | 5 | 1 | Original |

| Driver Rating | 0.56 | 1.51 | 5 | 0 | Original |

| Delivery Distance | 3.70 | 4.02 | 14.97 | 0 | Original |

| Gender | 0.90 | 0.30 | 1 | 0 | Original |

| Delivery Charge | 0.40 | 0.35 | 0.7 | 0 | Original |

| Serving Distance | 14.13 | 2.82 | 15 | 5 | Original |

| Preparation Time | 14.04 | 2.25 | 20 | 10 | Original |

| Vendor Rating | 4.36 | 0.21 | 4.8 | 4 | Original |

| Frequent Vendor | 4.36 | 0.21 | 4.8 | 4 | New |

| Frequent Customer | 4.36 | 0.21 | 4.8 | 4 | New |

| Age of Vendor Register | 642.46 | 125.91 | 805 | 429 | New |

| Age of Customer Register | 616.71 | 160.69 | 952 | 255 | New |

| Distance from Customer to Vendor | 0.54 | 0.34 | 1.75 | 0 | New |

Supplementary Material

Online Action Learning in High Dimensions: A Conservative Perspective

Appendix S.1 Auxiliary Lemmas

Lemma 1 (Finite-Sample Properties of ).

Proof.

This proof has been already provided in other papers, such as Carvalho et al. (2018). For the sake of completeness, we provide its main steps, even though it is a well-known result.

In equation (2), if is the minimum of the optimization problem, then, for , it is true that

Using Assumption 2, we can replace in the above expression to obtain the basic inequality (see Bühlmann and van de Geer (2011) page 103):

| (S.1) | ||||

Define , and the same for replacing for , where and .

The first term on the right side of (S.1) can be bounded in absolute terms as:

On , we have that

| (S.2) |

Using our previous definitions (see Section 2) for and and the respective counterparts for the estimators, by the triangle inequality of the left-hand side of equation (S.2), we have that:

Recall that Assumption 3 also requires that . Then, using Lemma 6, provided that , we have that . Substituting in (S.3):

Since for any , , , multiplying the last expression by 2 and using the fact that , we have:

| (S.4) |

∎

Lemma 2 (Finite-Sample Properties of - Continuation).

Proof.

Provided that , on , that , where , Lemma 1 indicates that . Then,

| (S.5) |

where the second equality is De Morgan’s law and the first inequality is an application of the union bound.

For the first term of (S.5), given that , is a positive random variable, for , we employ the Markov inequality to obtain:

| (S.6) |

For the second term in (S.5), we also have that is a positive random variable. Then, by the Markov inequality, for :

| (S.8) |

Recall that and, therefore, its elements are given by

Define the function , such that for bounded random variables taking values in a subset of , , :

where is defined in Assumption 1.i.

Then, equation (S.8) can be rewritten as:

| (S.9) |

Now, notice that and that for , such that :

Lemma 3 presents the cumulative regret for the initialization phase (), which is common to both HD -Greedy and CHD -Greedy algorithms. On the other hand, Lemmas 4 and S.18 exhibit results for their instantaneous regret for .

Lemma 3 (Initialization Regret).

Given the duration for the initialization phase and provided that Assumptions 1 and 2 are satisfied, the cumulative regret for both HD -Greedy and CHD -Greedy algorithms in the initialization phase () is bounded as:

where .

Proof.

Let the sequence comprises the indexes for the actions in that lead to best rewards for each , that is, each , such that . Considering Definition (1), the regret for the initialization phase is for an arbitrary action adopted at . We can bound by considering the worst case possible: to adopt wrong actions for all , in which case, . By Assumption 1:

| (S.11) |

The right-hand side of equation (S.11) can be bounded in absolute terms as:

Lemma 4 (Instantaneous Regret of the HD -Greedy Algorithm).

Proof.

For , define in the same way as in the proof of Lemma 3 and consider the definition of the action function in Section 2. Then, by the law of total expectation, the instantaneous regret of the HD -Greedy algorithm is:

| (S.12) |

By the learning rule of the HD -Greedy algorithm (see Section 3), we have that:

| (S.13) |

From the properties of the maximum of a sequence of random variables, we have the following fact applied to the last term of (S.13):

since for any sequence of sets , , the event is a subset of every .

Note that

| (S.14) |

Bounding the term in absolute value and using the triangle inequality, we find that:

Therefore,

| (S.15) |

Now consider the set defined in Lemma 1. Provided that for every , and that , where , results of Lemmas 1 and 2 indicates that with probability , for every , . Using this fact in equation S.15 and Assumption 4, we find that:

| (S.16) |

As described in Section 3, the authors in Auer et al. (2002) suggest , for , and . Since equation (S.17) is valid for it suffices to take , such that . In this case:

Finally, recall the definition of made in Lemma 3. Then, with probability , the instantaneous regret of the HD -Greedy algorithm after the initialization phase can be bounded as:

∎

Corollary 1.

Suppose that for each , , . Then:

Proof.

This is a straightforward proof, since one plugs the proposed into defined in Lemma 4. ∎

The suggested time dependency for in Corollary 1 is adapted from Bühlmann and van de Geer (2011) and very similar to the versions used in other papers in this literature such as: Wang et al. (2018), Bastani and Bayati (2020), Kim and Paik (2019) and Li et al. (2021).

Remark 4.

Recall that in some parts of the paper, as in Assumption 4, we assume the existence of and , such that for each , . The path established for in Corollary 1 restricts the range of its possible values and sheds light on its respective bounds. For example, from the results of Lemma 2, an increasing sequence guarantees that occurs at higher probabilities as time passes. This is the most interesting case in our high-dimensional setup and, for this to occur, it is sufficient that, at each incremental time step , the growth in the problem dimension is less than . In this case, is a increasing sequence and its lower bound would be , for the dimension at the beginning of the problem. The upper bound can be easily established considering that we study learning problems with finite horizon.

Lemma 5 (Instantaneous Regret of the CHD -Greedy Algorithm).

Proof.

For any , define in the same way as in the proof of Lemma 3 and consider the definition of the action function in Section 2. Then, by the law of total expectation, the instantaneous regret of the CHD -Greedy algorithm is:

| (S.19) |

By the learning rule of the CHD -Greedy algorithm (see Section 3), we have that :

| (S.20) |

The last term of the right side of equation (S.20) is the same as the last term of in the HD -Greedy algorithm. Regarding the first term of equation (S.20), by the definition of (Section 3):

| (S.21) |

Now notice that restricted to the set of higher-order statistics, the event , for . This implies that is is the most probable to occur since it is the lowest possible order statistic. Then, employing the union bound, we have that:

| (S.22) |

Using Assumption 1, it is clear from the developments made in Lemmas 3 and 4 that . Moreover, using Assumption 2, provided that , the parametric space, Lemmas 1 and 2 indicates that, on , with probability :

where is defined in Lemma 3.

Then, equation (S.22) leads to:

| (S.23) |

since, as an intermediate-order statistic, , for , which in this case, we can take .

However, notice that

Then,

| (S.24) |

Therefore, for , is sufficient to replace the above requisite of Lemma 9 and we restate it as:

Define and, with probability , the instantaneous regret of the CHD -Greedy algorithm, equation (S.19), can be bounded as:

∎

Note from Lemmas 3, 4 and S.18 that all bounds are increasing with , and , this last one as a function of the initialization period. The intuition behind this fact is clear since the larger the level of dissimilarity among policies or the larger the number of policies to be tested is, the greater the difficulty for the algorithm to select the right policy. In particular, the initialization phase should also be longer, in order to gather information over a large set of alternatives.

Lemma 6.

Suppose that the -compatibility condition holds for the set with cardinality with compatibility constant and that , where

Then, for the set , the -compatibility condition holds as well, with .

Proof.

See Corollary 6.8 in Bühlmann and van de Geer (2011) ∎

Lemma 7.

For arbitrary and , consider independent centered random variables , such that , there is a that bounds the variance as . Moreover, let be such that for , there is a such that

Proof.

See Lemma 14.24 in Bühlmann and van de Geer (2011) ∎

Lemma 8.

Let be independent random variables and be real-valued functions satisfied for ,

for and (easily satisfied for large ). Then,

Proof.

See Lemma 14.12 in Bühlmann and van de Geer (2011) ∎

Lemma 9.

Let . For :

Proof.

This is an application of Höeffding’s inequality to random variables that follow a binomial distribution. For more details, see Lemma 7.3 of Lin and Bai (2011) ∎

Lemma 10.

If is a monotone decreasing function and is a monotone increasing function, both integrable on the range , then:

Proof.

This is a well-known fact for monotone functions linked to left and right Riemann sums. ∎