Ruin problems for risk processes with dependent phase-type claims

Oscar Peralta111Cornell University, School of Operations Research and Information Engineering, Rhodes Hall, Ithaca 14850, New York, United States. E-mail: op65@cornell.edu, Matthieu Simon 222Département de Mathématique, Place du Parc 20 , B-7000 Mons, Belgium. E-mail: matthieu.simon@umons.ac.be. Previously at Universitat de Barcelona, Departament de Matemàtica Econòmica, Financera i Actuarial, 690 Avinguda Diagonal, Barcelona E-08034, Spain.

Abstract

We consider continuous time risk processes in which the claim sizes are dependent and non-identically distributed phase-type distributions. The class of distributions we propose is easy to characterize and allows to incorporate the dependence between claims in a simple and intuitive way. It is also designed to facilitate the study of the risk processes by using a Markov-modulated fluid embedding technique. Using this technique, we obtain simple recursive procedures to determine the joint distribution of the time of ruin, the deficit at ruin and the number of claims before the ruin. We also obtain some bounds for the ultimate ruin probability. Finally, we provide a few examples of multivariate phase-type distributions and use them for numerical illustration.

AMS Subject Classifications: 91B30, 91B70, 60J28.

Key Words: Risk processes; risk of ruin; dependent claims; multivariate phase-type distributions; Markov-modulated fluid flows.

1 Introduction

A risk process is a stochastic processes of the form

| (1.1) |

where , , is a counting process and is a family of nonnegative random variables. Such processes are commonly used in risk theory to represent the level of reserves of an insurance company that collects premiums at continuous rate and reimburses the claims that occur according to . A fundamental problem in this context is to determine the probability that the reserves becomes negative in finite time, and, when it happens, after how long.

The most classical risk process was introduced by Cramér [11] and is called the Cramér-Lundberg process. It assumes that the variables are i.i.d. and that is a Poisson process, independent of the claim sizes. Since then, this model was generalised in various ways: we refer to Asmussen and Albrecher [2] for an introduction to the fundamental risk model and its major extensions.

Most of the results in the literature concern risk processes in which the claim sizes are independent and identically distributed. However, there are many circumstances where models with dependent claims appear to be more appropriate. Indeed, large groups of people are often subject to common risks stemming from economic, environmental or epidemiological factors, for instance. Moreover, claims that are not identically distributed can be relevant in various situations, for example when the reaction capacity of the threatened population can evolve over time. Different risk models with dependent claims have already been considered in the literature; see e.g. Albrecher et al. [1], Constantinescu et al. [10], Bladt et al. [8] and references therein.

In this paper, we consider a risk process of the form (1.1) in which the claim sizes are random vectors taken from a family of multivariate phase-type distributions. The random vectors that we consider have several advantages: firstly, their components are neither independent nor identically distributed in general, and dependence between components can be incorporated in a simple and intuitive way. Secondly, they are easy to characterise and admit simple and explicit expressions for the joint density and the correlation matrix. Finally, they are designed to facilitate the analysis of the corresponding risk process through the study of an appropriate embedded Markov-modulated fluid flow.

We use this embedding method to derive an explicit formula for a transform of the ruin time , the severity at ruin and the number of claims until ruin in terms of some first passage matrices related to the embedded fluid flow. We present a recursive procedure to compute this transform numerically. We also briefly explain how the approach can be easily extended to the analysis of risk processes in a random environment. Next, we obtain simple bounds for the ultimate ruin probability of our model, in terms of the ruin probability for risk processes with independent Erlang claims. These bounds are quite improvable, but they allow to check whether the ultimate ruin is almost sure or not in a variety of situations. Finally, we conclude with some numerical illustrations where we compare the ruin probabilities for different risk models with multivariate phase-type distributed claims.

The paper is organised as follows. In Section 2, we first briefly review the main properties of univariate phase-type distributions. Next, we introduce our class of multivariate phase-type distribution and provide a few examples. In Section 3, we turn to the analysis of the risk process. We first detail the construction of the embedded Markov-modulated fluid flow and use it to determine a transform of , and . We then present our bounds for the ultimate ruin probability. Finally, in Section 4, we present a few numerical illustrations.

2 Dependent phase-type distributions

2.1 Univariate phase-type distributions

Throughout the text, denotes a vector of zeros and denotes a vector of ones, with appropriate size and orientation.

Let be a time-homogeneous Markov jump process defined on a state space , where contains transient states and is an absorbing state. The generator of is then of the form

where is a matrix containing the transition rates between the transient states and is the vector containing the transition rates from the transient states to the absorbing state. The initial probability vector of on , with components for , is assumed to satisfy . We say that a random variable has a phase-type distribution of size with initial distribution and sub-generator matrix , and write , if is distributed as the time before absorption in :

Phase-type distributions have been popularized by the work of Neuts [17, 18]. Since then, they have been used in many application fields. One of their advantages is that they characterisation is easy and intuitive: if , then its density function is

| (2.1) |

for , and the moments of are given by

| (2.2) |

see e.g. Latouche and Ramaswami [16, Chapter 2] or Neuts [18, Chapter 2]. Note that the expression for the density is intuitive since the component is the probability that is in state (and therefore not absorbed yet) at time if it started from state , while the vector contains the probabilities of absorption on the infinitesimal time interval (conditional on the process not being absorbed by time ). Also, the formula is straightforward since is the average time spent in state before absorption given that the starting state is .

Phase-type distributions benefit from various interesting closure properties. For instance, they are stable under convolutions: if and are independent, then where

and (see [16, Section 2.6]). Moreover, if is a Bernoulli random variable independent from and with parameter , then where

Finally, let us mention that the class of phase-type distributions is dense (in the weak convergence sense) within the class of distributions with support on (see e.g. Breuer and Baum [9, Theorem 9.14]). Together with the previous properties, this makes phase-type distributions a very powerful tool to model and analyse a wide range of random phenomena.

2.2 Multivariate phase-type distributions

Different classes of multivariate phase-type distributions have been considered in the literature. The first one was introduced by Assaf et al. [3] who proposed the following definition: let be a Markov jump process as in Section 2.1 and consider a collection of subsets such that , is stochastically closed for all (i.e. if the process enters , it never leaves it) and . A random vector is said to follow a multivariate phase-type () distribution if

The authors derived various properties of these distributions, including a closed expression for their joint density.

The class of () distribution was then extended to the family of distributions by Kulkarni [15]. A random vector is said to follow a distribution if there exists a collection of non-negative numbers such that

Unlike the distributions, there is no closed-form formula for the joint density of , so its analysis is, in most cases, limited to its Laplace transform. This class was further extended in Bladt and Nielsen [7] who considered those random vectors such that follows an univariate phase-type distribution for any .

In this paper, we introduce another class of multivariate phase-type distributions which is suitable for our analysis of risk processes. For such processes, the claim sizes are determined sequentially over time, that is, they are sampled one after the other. This motivates the following definition.

Let and be a Markov jump process defined on the state space

where each is some finite subset of transient states and is an absorbing state. Assume that its generator is of the following form when written according to the state decomposition above:

| (2.3) |

and the initial state is given by the probability vector , so that the process starts from the subset . Here, is the transition rate from to , . For , the matrix contain the transition rates from to . Finally, the vector contains the transitions from to the absorbing state .

From now on, we say that the vector follows a multivariate phase-type distribution if is the amount of time spent by in the subspace before absorption:

| (2.4) |

Note that each component is almost surely finite since each subset is assumed to be transient. Our class of multivariate phase-type distributions is clearly a subset of the class introduced by Kulkarni [15]. The case was analysed in Bladt et al. [8, Theorem 6.10], where the authors showed that the vector and the matrices , , and can be chosen in such a way that and are phase-type-distributed with any feasible goal covariance.

From the structure (2.3) of the generator , it is clear that the components are determined sequentially in : the process starts in and is known as soon as it leaves for . Then, is known as soon as the process leaves for , and so on. This is the key feature that will allow us to apply the fluid embedding technique in the next section, where we consider risk processes with multivariate phase-type claims.

Let us first have a look at the distribution of . From (2.4) and the structure (2.3) of , it is easy to see that

where and for ,

| (2.5) |

This follows from the fact that is the probability that the process is in phase when entering given entered in phase . So, the marginal density and the moments of are obtained from (2.1) and (2.2). The components of can be dependent since the state occupied by when entering a subset depends on the trajectories of in . The joint distribution of is given below, and is a straightforward extension of the corresponding results for absorbing Markov arrival processes (see e.g. Latouche and Ramaswami [16]).

Proposition 2.1.

The density function of is given by

| (2.6) |

for .

Proof.

A closed expression for the covariances between the components of can also be easily obtained:

Proposition 2.2.

Proof.

The covariance between and is given by , and , are known from (2.2). To obtain , we start from the Laplace transform of , which is easily derived by integration in (2.6). For a -dimensional vector of nonnegative components,

| (2.8) |

Using that

for any square matrix such that is invertible, we obtain

It suffices to use that for all to obtain the announced expression from the last equality. ∎

We now present some examples of vectors following a multivariate phase-type distribution. They will be used later for illustration in the setting of risk processes.

Example 1. Let be a vector of independent random variables . Then has a multivariate phase-type distribution of representation (2.3) where , for and .

Example 2. Let and be two collections of independent random variables such that and for all . Let () be some constants in . Define the random vector as follows: First, with probability and with the complementary probability . Next, the value of , is chosen sequentially according to the value of : if , then

If , then

The vector has a multivariate phase-type distribution with parameters

where and .

Example 3. Fix and consider the random vector of representation (2.3) with the matrices and such that ,

where is an stochastic matrix, is a probability vector with components, is a positive rate and . The initial probability vector is arbitrary. Here, the states in can be seen as successive stages of duration Exp() each. If the process enters in the -th stage, then is the sum of at most i.i.d variables Exp(). The dependences between the components of comes from the fact that the initial stage visited in depends on the last stage visited by through the transition matrix and the vector .

3 Risk process with multivariate phase-type claims

In this section, we consider the risk process given by

| (3.1) |

where is a Poisson process of intensity and, for all , the vector is independent of and follows a multivariate phase-type distribution with representation (2.3). The parameters correspond respectively to the initial level of reserves and the premium rate. We are interested in the distribution of three statistics related to this model: the time of ruin

| (3.2) |

the deficit at ruin and the number of claims that occurred up to time . Our aim is to determine their joint distribution through the transform

| (3.3) |

for , and .

We are going to determine (3.3) through the study of a Markov-modulated fluid flow closely related to the risk process (3.1). This method is sometimes called fluid embedding and has already been used in the setting of risk theory (see e.g. Badescu and Landriault [4] for an overview). Compared to existing models, a difference here is that we need to consider an infinite phase space for the embedded fluid flow. The construction of the fluid model and its links with the risk process are detailed in Section 3.1. In Section 3.2, we use this fluid approach to derive an expression for (3.3).

3.1 The embedded Markov-modulated fluid flow

A Markov-modulated fluid flow (MMFF) is a stochastic process where is called the level and is called the phase. The dynamics are the following: is a Markov jump process on a state space characterized by its generator . To each phase in one associates a rate . The process takes its values in , has continuous trajectories and is such that

In other words, the level process evolves in a piecewise linear fashion, at rate when . It is convenient to reorganize the phase space and partition into two subspaces and . Denoting by the diagonal matrix of rates, we can write and according to this subdivision :

To the risk process in (3.1), we associate the MMFF defined on the infinite phase space where and are two copies of . To differentiate between these sets, we write

where and are two copies of . In the sequel, the matrices , , and have the following form according to this state partition:

| (3.4) | ||||

and is such that and , where denotes the identity matrix of infinite dimension.

Built this way and when starting from with initial phase distribution vector , the process evolves like in (3.1) except that each jump in is replaced by a linear decrease of the level at the unit rate, for a duration equal to the size of the jump. Note that the matrices and need to be constituted by infinitely many blocks in order to maintain the same dependence between the sojourn times in the subspaces for the MMFF than for the components of the multivariate phase-type distribution with representation (2.3). Let us describe the first stages of the embedded process in more detail: the MMFF starts from a phase , chosen according to the vector , and stays in that phase for a period of time Exp() during which the level process increases at rate . Then there is a transition to the corresponding phase in and the level starts decreasing at rate . The duration of this decrease is where is a unitary column vector with -th component equal to one. The matrix contains the absorption rates triggering a transition to , and the choice of the chosen state in at that time also determines the state which will be occupied at the first passage to , that is, the initial phase for the phase-type duration representing the second claim.

More formally, the risk process and its associated MMFF are linked by a change of time: denoting

the time spend by the MMFF in up to time and , it holds that

The levels crossed by on a time interval are the same as the ones crossed by on the interval . In particular, the time of ruin defined in (3.2) corresponds in the MMFF to the time with , that is,

Moreover, the variable corresponds in the MMFF to the level occupied at the first passage to a phase in after . Finally, the variable corresponds in the MMFF to the number of transitions from to up to time .

3.2 Ruin probabilities and time of ruin

We can now derive an expression for the transform (3.3), in terms of the blocks of two first passage matrices related to the MMFF . First, fix some . The first matrix is such that for all , , ,

The second one is such that for , , ,

They give the Laplace transforms of the time spent in before the first passage to level zero in the MMFF, starting from level zero in an ascending phase (for ) or from level in a descending phase (for ). From the structure (3.4) of the generator of , they have an upper triangular block structure when written according to the phase subdivision for and for :

| (3.5) |

| (3.6) |

The transform (3.3) is easily expressed in terms of the blocks in (3.5) and (3.6):

Proposition 3.1.

For any , , and ,

| (3.7) |

Proof.

Remark. Taking and and in (3.7), we obtain

| (3.8) |

The probability of ultimate ruin

can be approximated as precisely as desired by computing (3.8) for large enough.

In order to apply Proposition 3.1 and compute the transform (3.7), we need a procedure to compute the various blocks of and . To this end, first note that from the definition of , it is easy to show (see e.g. Ramaswami [21]) that can be expressed under exponential form

where is a sub-generator with the same block structure as , i.e.

| (3.9) |

In the next proposition, we show that the blocks and can be obtained recursively. The notation is for the Kronecker delta.

Proposition 3.2.

The matrices are given by

| (3.10) |

and, for ,

| (3.11) |

The matrices are given by

| (3.12) |

for .

Proof.

We first derive an equation for (, ). For that, we assume that the MMFF starts from and . As , the process stays in phase for a duration before going to the only phase available from . Conditioning on , we thus obtain

So, in matrix notation,

| (3.13) |

and integrating by parts, we obtain

Since , we have that . Using the block structure (3.6), (3.9), we find that

and therefore

| (3.14) |

Let us turn to the matrix . The MMFF starts now from and with . By conditioning on the time up to the first transition from to , we obtain

Differentiating with respect to , we find

Finally, we take in the last equality. As and , it yields (3.12). Equations (3.10) and (3.11) are obtained by injecting (3.12) in (3.14). ∎

Thanks to block subdivision (3.5), the dimensions of the matrices that must be repeatedly inverted to numerically compute the matrix P in the above procedure are equal to the dimensions of the blocks . In most practical cases, these matrices have moderate size or can be assumed to have a special structure that can be exploited to decrease the computational cost of their inversion. The various blocks of are easily computed from Equation (3.12). Once these blocks are known, the blocks of the exponential matrix can be computed efficiently using the special structure of by following for instance Kressner et al. [14] where the authors propose an efficient incremental procedure to compute the (block-triangular) square matrix constituted by the first block lines and columns of , from the (previously obtained) square matrix constituted by the first block lines and columns of .

Particular case where and for all . In this case, where . In other words, the claim sizes have the same distribution as the inter-arrival times in a Markov arrival process of parameters (see Neuts [19]). From Proposition 2.2,

Observe that the matrices and depend here on the difference only. Denoting and for any , we have from Proposition 3.2 that

| (3.15) |

and, for ,

| (3.16) |

Moreover,

| (3.17) |

The formula in Proposition 3.1 can be easily adapted with these new matrices. More importantly, the transform (3.3) with has a simpler and more compact expression in this particular case:

Corollary 3.3.

When and for all ,

| (3.18) |

where is the minimal nonnegative solution of the Riccati equation

| (3.19) |

and where .

Proof.

Let us define

| (3.20) |

Then is the Laplace transform of the time spent in before the first passage to level zero in the MMFF, starting from level zero in an ascending phase and is the Laplace transform of the time spent in before the first passage to level zero in the MMFF, starting from level in an descending phase. Formula (3.18) is immediate from these interpretations.

The issue of numerically solving the Riccati equations that arise in fluid queues, like Equation (3.19), has been investigated by various authors over the past several decades. This has led to the development of various stable and efficient procedures such as the logarithmic reduction algorithm (see Latouche and Ramaswami [16]), as well as the algorithms proposed in Bini et al. [6] and Guo [12]. For instance, the stability of some of the aforementioned algorithms is affirmed in [12] when the dimension of the matrix in question is . Note that the matrix provides us with a simple criterion to check whether the ruin occurs almost surely in finite time or not: if is stochastic (i.e. ), then the exponential of is also stochastic, and therefore we have from (3.18) that

whatever the value of is.

3.3 Risk process in a random environment

In this section, we briefly explain how the method presented in Sections 3.1 and 3.2 can be easily extended to the analysis of risk processes in a Markov environment. Let be a Markov jump process on a state space with , characterized by its generator and initial probability vector . Consider the process in which the reserves has the dynamics

| (3.21) |

Here, is a Markov-modulated Poisson process with intensity when is in state . As before, for all , the vectors are independent of and follow a multivariate phase-type distribution with representation (2.3). In other words, is a risk process under the influence of the random environment . The premium rate and the claim arrival rate depend on the state of at time .

This risk process can be analysed through an embedded Markov-modulated fluid flow slightly more general than in Section 3.1, with generator of the form

with, for all ,

where , is the identity matrix with the same dimension as , is the identity matrix of dimension and is the Kronecker product. The rate matrices are

where . The equality in Proposition 3.1 is still valid in this case, for matrices , and with the same definition and block structure as in Section 3.2. The equations in Proposition 3.2 need to be adapted to the new generator , but it can be easily done by following the same argument as in the proof of Proposition 3.2.

Remark. This extension also allows us to analyse the same risk process as in (3.1) except that the inter-arrival times between two claims are no longer exponential but rather distributed as independent random variables. For that, it suffices to use the extension above with and for all (where ), and , with the same rate matrices as in Section 3.1.

3.4 Probability of ultimate ruin

A natural question about the risk process defined by (3.1) is whether it will get ruined in finite time with probability one, whatever the initial reserves are. One way to answer that question would be to compute the r.h.s. of (3.8) with large enough, but is is sometimes more convenient to have simpler criteria. Here, we develop a quick method which can help to assess whether the ultimate ruin is certain or not. It is based on bounding the process (3.1) with simple stochastic processes in the stochastic ordering sense.

We first recall the following definitions. First, the dominating eigenvalue of a square matrix is the eigenvalue which has the largest real part. If is the sub-generator matrix associated to a phase-type distribution, then it can be shown that its dominating eigenvalue is real and strictly negative (see e.g. [20]). Next, let and two positive random variables with density functions and . We say that dominates in the sense of the usual univariate stochastic order () if

see e.g. Shaked and Shanthikumar [22].

Lemma 3.4.

Let . Let and be the size and the dominant eigenvalue of , and . Fix , and . Then

where and .

Proof.

Since is a nonnegative row vector,

| (3.22) |

In other words, the hazard rate of is smaller than the one of , a relation commonly written as . By [22, Theorem 1.B.1] it implies that .

To obtain the second inequality, note first that from He et al. [13, Corollary 2.1], we have where . Now, if , let be independent of (with if ). Then a.s., which yields since . ∎

The concept of stochastic ordering is extended to the multivariate setting in the following way: Let and be two -dimensional random vectors with density functions and . We say that dominates in the sense of the usual stochastic order () if

for all increasing set (i.e. for all set such that and is nonnegative implies ).

It is often hard to extend univariate stochastic ordering properties to the multivariate setting. However, an extension of Lemma 3.4 to the particular class of multivariate phase-type distributions given by (2.6) can be obtained as follows:

Lemma 3.5.

Let follow the law given by (2.6). Let and the largest dimension and dominant eigenvalue amongst the matrices , and . Fix , and . Then

where and are -dimensional random vectors with i.i.d. entries which are - and -distributed, respectively.

Proof.

We prove the result for only, the case easily follows by induction on . For a fixed increasing set , define the sets and . We have that

Note that the quotient in the last two equalities is a probability vector, and thus the function is a phase-type density for each fixed . We can therefore apply Lemma 3.4 to obtain

where is the density function of an Erlang random variable with parameters and . Consequently,

where we applied Lemma 3.4 again in the second-to-last step. This yields . The second inequality follows by similar arguments, replacing with and inverting the inequalities above. ∎

Let us go back to our risk process defined by (3.1), in which the claim sizes are given by a sequence of phase-type random variables with representation (2.3). Lemma 3.4 allows us to bound the ultimate ruin probability in this process: assume that

-

(A1)

The dimensions of are bounded by ,

-

(A2)

The sequence is bounded from above by ,

-

(A3)

The dominating eigenvalues of are bounded from above by .

Let and be two i.i.d. sequences with and for all , and define the two risk processes and such that

where , and are as in (3.1). Then,

Proposition 3.6.

Under the assumptions (A1), (A2) and (A3),

Proof.

The processes and are Cramér-Lundberg processes with exponential or Erlang claims, and the corresponding ultimate ruin probabilities are given by very simple and explicit formulae (see e.g. Amsussen and Albrecher [2, Chapter IX]). An application of the bounds in Proposition 3.6 is that they often provide a quick test to check whether our risk process (3.1) gets almost surely ruined in finite time or not, by using the relations

and

In most situations where , our bounds are not tight enough to give a good estimate of the ultimate ruin probability, and using formula (3.8) with large enough provides much better results. Improving the bounds of Proposition 3.6 will be the object of further work.

4 Numerical illustrations

Example 2 (continued). Let us consider the risk process (3.1) in which the claims are distributed as in Example 2 of Section 2.2. It covers the case where the claims can take two possible forms. For instance, could have a moderate expectation and variance to represent the size of a regular claim. The variable could have a much higher expectation and/or variance to represent the size of scarce but more severe claims. The probabilities and regulate the contagion effect in the kind of claims: for instance, high values for the probabilities mean that a moderate claim is often followed by another moderate claim. High values for the probability would mean that once a severe claim occurs, the probability that more severe claims will occur successively is high. The dependence in of these probabilities can reflect the fact that the company has the means to learn from the past and decrease the risk of severe claim and the number of their successive occurrence.

For this illustration, we assume that the variables are exponentially distributed with parameter and that the are Erlang variables with parameters and . The probabilities are kept constant: for all . The probabilities increase with as for some .

Tables 1 and 2 show the means, variances and some correlations of the vector when the parameter values are , , , and . The choice of a sequence increasing to one implies that the expectation and variance of quickly start to decrease to get closer and closer to the expectation and variance of the exponential distribution with parameter . The correlations between and its direct neighbours decrease to zero when , but they remain significantly different from zero for quite high values of .

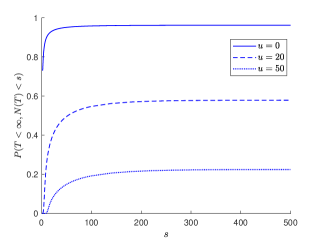

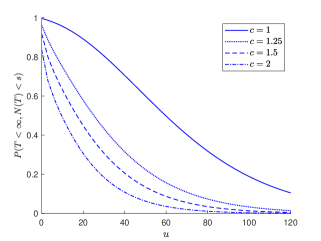

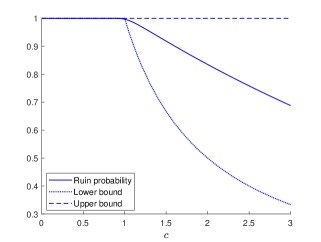

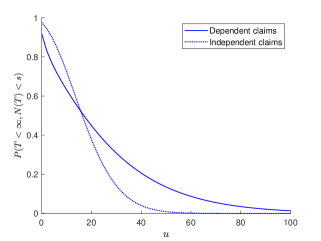

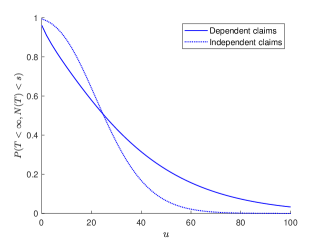

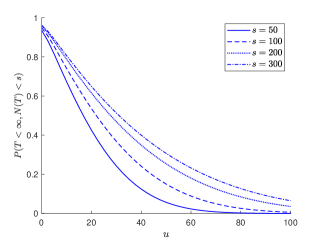

In Figure 1, we show two Graphs of the ruin probability as a function of , for different values of and and when , , , , and . Obviously, the ruin probabilities increase with , and we see that in each case converges quite quickly as increases. Taking between 100 and 200 already yields a result very close to the ultimate ruin probability . The first graph in Figure 2 shows the same ruin probability but this time as a function of the initial capital and for different values of , when and the other parameter values are as before. The second graph in Figure 2 shows the graph of as a function of when and the other parameter values are as before; together with the lower and upper bounds obtained from Proposition 3.6. As is large, we have that is approximately equal to the ultimate ruin probability. In this example, we see that the upper bounds is always equal to one and therefore useless. The lower bound, however, starts to decrease as the same time the true ruin probability does, and allows us to say that the ultimate ruin is almost sure for between 0 and 1.2 (and therefore computing the ruin probability for these values using the exact formula (3.8) is not needed). In Figure 3, we compare the ruin probability obtained for two different models: the one with dependent claims as before, and a model where the claims have the same distribution (i.e. but are independent (see Example 1 in Section 2.2). Here, , , , , , , and (left graph) or (right graph). It is generally accepted in the literature that more dependence between claims means a higher risk of ruin. This is what we observe here: the model with dependent claims yields higher ruin probabilities when is large enough, and the ruin probabilities associated to the dependent model remain significantly positive for much larger values of than the corresponding model with independent claims.

| 2.20 | 2.52 | 2.55 | 2.48 | 2.39 | 2.28 | 2.18 | 2.09 | |

| 5.56 | 6.29 | 6.34 | 6.22 | 6.01 | 5.77 | 5.51 | 5.25 |

| 1 | 0.34 | 0.23 | 0.16 | 0.12 | 0.09 | 0.07 | 0.05 | |

| 1 | 0.40 | 0.28 | 0.21 | 0.15 | 0.12 | 0.09 | ||

| 1 | 0.42 | 0.31 | 0.23 | 0.18 | 0.14 | |||

| 1 | 0.44 | 0.33 | 0.25 | 0.19 | ||||

| 1 | 0.45 | 0.34 | 0.26 |

|

|

|

|

|

|

Example 3 (continued). Let us now consider the risk process (3.1) in which the claims are distributed as in Example 3 of Section 2.2. In the setting of risk processes, it can represent situations where the severity of the first claims (in the sense of the number of exponential stages they go through) has an impact on the severity of the claims to come.

For a fixed integer , we choose as the transition matrix

and for all . The rates and the probabilities will be either constant or given by

| (4.1) |

so that the mean duration of each exponential stage decreases over time (from 1 to 0.5) while the probability of going through one more stage slightly increases (from 0.9 to 0.95).

Table 3 shows the means, variances and some correlations of when . For larger values of , the expectation and variance of decrease slowly to stay around 3.35 and 4.6, respectively. The correlations between and is significant when only, but Corr remains around 0.14 as goes to infinity.

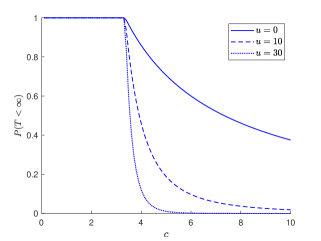

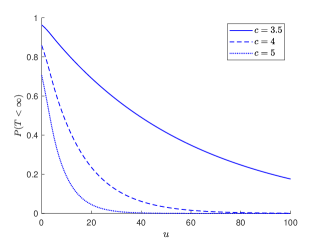

In Figure 4, we show the ruin probability as a function of the initial capital when , and , are given in (4.1) and for different values of and . In Figure 5, we change some parameter values: we still take and but and are now constant. In that way, the claims are dependent but identically distributed and the model is an example of the particular case discussed at the end of Section 3.2. The graphs show the ultimate ruin probability as a function of or . Observe that this probability is equal to one for lower than 4, whatever the initial capital. This could have been obtained directly by using that given in (3.19) is stochastic in these cases.

| 4.81 | 3.34 | 3.57 | 3.46 | 3.46 | 3.44 | 3.43 | 3.42 | |

| 8.05 | 5.90 | 5.91 | 5.55 | 5.38 | 5.26 | 5.17 | 5.10 | |

| 0.23 | 0.10 | 0.12 | 0.12 | 0.13 | 0.13 | 0.13 | 0.13 |

|

|

|

|

Acknowledgements

The authors acknowledge the support of the Australian Research Council Center of Excellence for Mathematical and Statistical Frontiers (ACEMS). Oscar Peralta was additionally supported by the Australian Research Council DP180103106 grant and the Swiss National Science Foundation Project .

Data availability

Data sharing not applicable to this article as no datasets were generated or analysed during the current study.

References

- [1] H. Albrecher, C. Constantinescu, and S. Loisel. Explicit ruin formulas for models with dependence among risks. Insurance: Mathematics and Economics, 48(2):265–270, 2011.

- [2] S. Asmussen and H. Albrecher. Ruin Probabilities, volume 14 of Second Edition. World Scientific Publishing Co. Pte. Ltd., 2010.

- [3] D. Assaf, N. Langberg, T. Savits, and M. Shaked. Multivariate phase-type distributions. Operations Research, 32(3):688–702, 1984.

- [4] A. Badescu and D. Landriault. Applications of fluid flow matrix analytic methods in ruin theory - a review. Revista de la Real Academia de Ciencias Exactas, Físicas y Naturales. Serie A. Matemáticas, 103(2):353–372, 2009.

- [5] N. Bean, M. O’Reilly, and P. Taylor. Hitting probabilities and hitting times for stochastic fluid flows. Stochastic Processes and their Applications, 115(9):1530–1556, 2005.

- [6] D. Bini, B. Iannazzo, G. Latouche, and B. Meini. On the solution of algebraic Riccati equations arising in fluid queues. Linear Algebra and its Applications, 413(2):474–494, 2006.

- [7] M. Bladt and B. F. Nielsen. Multivariate matrix-exponential distributions. Stochastic models, 26(1):1–26, 2010.

- [8] M. Bladt, B. F. Nielsen, and O. Peralta. Parisian types of ruin probabilities for a class of dependent risk-reserve processes. Scandinavian Actuarial Journal, 2019(1):32–61, 2019.

- [9] L. Breuer and D. Baum. An Introduction to Queueing Theory and Matrix-analytic Methods. Springer, 2005.

- [10] C. Constantinescu, E. Hashorva, and L. Ji. Archimedean copulas in finite and infinite dimensions - with application to ruin problems. Insurance: Mathematics and Economics, 49(3):487–495, 2011.

- [11] H. Cramér. On the Mathematical Theory of Risk. In Collected Works II, pages 601–678. Springer Berlin Heidelberg, Berlin, Heidelberg, 1930.

- [12] C. Guo. Efficient methods for solving a nonsymmetric algebraic Riccati equation arising in stochastic fluid models. Journal of Computational and Applied Mathematics, 192(2):353–373, 2006.

- [13] Q.-M. He, G. Horváth, I. Horváth, and M. Telek. Moment bounds of ph distributions with infinite or finite support based on the steepest increase property. Advances in Applied Probability, 51(1):168–183, 2019.

- [14] D. Kressner, R. Luce, and F. Statti. Incremental computation of block triangular matrix exponentials with application to option pricing. Electronic Transactions on Numerical Analysis, 47:57–72, 2017.

- [15] V. Kulkarni. A new class of multivariate phase type distributions. Operations Research, 37(1):151–158, 1989.

- [16] G. Latouche and V. Ramaswami. Introduction to Matrix Analytic Methods in Stochastic Modeling. ASA-SIAM series on statistics and applied probability. Society for Industrial and Applied Mathematics, 1999.

- [17] M. Neuts. Probability distributions of phase type. In Liber Amicorum Prof. Emeritus H. Florin, pages 173–206. Department of Mathematics, University of Louvain, Belgium, 1975.

- [18] M. Neuts. Matrix-geometric Solutions in Stochastic Models: An Algorithmic Approach. Dover Publications, 1981.

- [19] M. F. Neuts. A versatile markovian point process. Journal of Applied Probability, pages 764–779, 1979.

- [20] C. A. O’Cinneide. Characterization of phase-type distributions. Stochastic Models, 6(1):1–57, 1990.

- [21] V. Ramaswami. Matrix-analytic methods for stochastic fluid flows. In D. Smith and P. Hey, editors, Teletraffic Engineering in a Competitive World, pages 1019–1030. Proceedings of the 16th International Teletraffic Congress, Elsevier Science, Amsterdam, 1999.

- [22] M. Shaked and J. G. Shanthikumar. Stochastic orders. Springer Science & Business Media, 2007.