Portfolio optimization with a

prescribed terminal wealth distribution

Abstract

This paper studies a portfolio allocation problem, where the goal is to reach a prescribed wealth distribution at final time. We study this problem with the tools of optimal mass transport. We provide a dual formulation which we solve by a gradient descent algorithm. This involves solving an associated Hamilton-Jacobi-Bellman and Fokker–Planck equation by a finite difference method. Numerical examples for various prescribed terminal distributions are given, showing that we can successfully reach attainable targets. We next consider adding consumption during the investment process, to take into account distributions that are either not attainable, or sub-optimal.

Keywords: portfolio allocation, wealth distribution target, optimal mass transport, HJB, Fokker–Planck, gradient descent

1 Introduction

Over the past decades, there has been a vast amount of research on portfolio allocation. Perhaps the most iconic result is the portfolio selection theory by Markowitz (1952), which states that investors should determine the allocation of wealth on the basis of the trade-off between return and risk. The classical objective function in a portfolio optimization problem is to maximize the expected return given variance level. However, the first and second moments of the return of a portfolio is only a simplified description of the wealth. Researchers then introduced objective functions that include more moments, such as skewness, to provide a more accurate statistic description of the distribution of the return (see, for example, Kraus and Litzenberger 1976 and Lee 1977).

The whole distribution of the portfolio wealth would provide investors a complete information, and instead of optimizing the first moments of the distribution, our paper introduces an objective function which includes a target distribution of the terminal wealth. We address the problem of controlling the portfolio allocation process to reach the prescribed terminal distribution. Of course, as we will see not all distributions are attainable.

On the one hand, this problem can be categorized as a stochastic control problem. The state variable is influenced by a process whose value is decided at any time , and we define such a process as a control. We can treat the portfolio allocation process as a control in the investment process. We aim to design the time path of the portfolio allocation process such that it steers the portfolio wealth from an initial state to a prescribed terminal distribution.

One the other hand, designing a continuous semimartingale having prescribed distributions at given times can be addressed with the optimal mass transport (OMT) theory. The optimal transport problem is an old problem first addressed in the work of Monge (1781), and was later revisited by Kantorovich (1942) leading to the so-called Monge–Kantorovich formulation. A comprehensive review of the extensions and applications of the Monge–Kantorovitch problem can be found in the book by Rachev and Rüschendorf (1998) and the books of Villani (2003, 2008). The original formulation of the problem looks for a map that pushes a distribution to another distribution . Later, Benamou and Brenier (2000) reinterpreted the problem in a fluid mechanics framework, where one is not looking only for an optimal transport map, but instead for the whole trajectory of the mass distribution over time. This contribution opened the way to the problem of continuous optimal transport.

Stochastic extensions of the discrete and time continuous OMT problem have then flourished, see e.g. Mikami and Thieullen (2006), Tan et al. (2013), Mikami (2015), Henry-Labordère et al. (2016). Beyond its mathematical interest, the optimal mass transport problem has applications in many fields, in economy, meteorology, astrophysics (Brenier et al. 2003, Loeper 2006), image processing (Ferradans et al. 2014), finance (Dolinsky and Soner 2014, Henry-Labordère 2017).

The novelty of this paper is to provide a new perspective on portfolio optimization inspired by OMT. An investor must decide how to allocate her portfolio between a risky and a risk-free asset. The price of the risky asset is modelled by a semimartingale, with prescribed drift and diffusion coefficients. By controlling the portfolio allocation, she wants the distribution of the wealth to match, or be close to, a given target distribution. Depending on the risky asset diffusion coefficients, not all target distributions are attainable (think for example of too high an expected return versus variance), or optimal (one could reach a “better” distribution than the target). We consider two different approaches: either relaxing the terminal constraint by penalization, or adding a consumption process, whereby the investor can either inject or withdraw cash from the portfolio in order to reach the target.

The rest of the paper is organized as follows. In Section 2, we formulate the problem. Then we introduce the dual formulation in Section 3. In Section 4, we provide a gradient descent algorithm to solve the dual problem, and the numerical results are presented in Section 5. We give examples for general target distributions with various penalty functionals in Section 5.1. We consider the addition of consumption/cash input in Section 5.2 and Section 5.3.

2 Problem Formulation

Let be a Polish space equipped with its Borel -algebra. We denote the space of continuous functions on with values in , the space of bounded continuous functions and the space of continuous functions, vanishing at infinity. Let be the space of Borel probability measures on with a finite second moment. Denote by the space of finite signed measures on with values in , be the subset of non-negative measures. When is compact, the topological dual of is given by . But when is non-compact, is larger than . For convenience, we often use the notation . We say that a function belongs to if and . Let denote non-negative real numbers, and denote the set of symmetric positive semidefinite matrices.

Let we denote by the filtration generated by the canonical process. The process is a -dimensional standard Brownian motion on the filtered probability space .

We consider a portfolio with risky assets and one risk-free asset, the risk-free interest being set to 0 for simplicity. We assume the drift and covariance matrix of the risky assets are known Markovian processes. Without loss of generality, we set the time horizon to be . The price process of the risky assets is denoted by , and the th element of follows the semimartingale

| (1) |

where is the diffusion coefficient matrix.

The process is a Markovian control. For , the portfolio allocation strategy represents the proportion of the total wealth invested into the risky assets, and is the proportion invested in the risk-free asset. We define the concept of admissible control as follows.

Definition 1.

An admissible control process for the investor on is a progressively measurable process with respect to , taking values in a compact convex set . The set of all admissible is compact and convex, denoted by .

We denote by the portfolio wealth at time . Starting from an initial wealth , the wealth of the self-financing portfolio evolves as follows,

| (2) | ||||

| (3) |

2.1 Portfolio optimization with a prescribed terminal distribution

We denote by the distribution of . In this problem, we know the initial distribution of the portfolio wealth , we are given a prescribed terminal distribution and a convex cost function .

With and a process , the realized terminal distribution of the portfolio wealth is ( is not necessarily the same as ). We want to be close to our target , hence we introduce a functional to penalize the deviation of from . At the same time, we want to minimize the expectation of the transportation cost from to . Combining the expected transportation cost and the penalty functional, our objective function is

| (4) |

where the feasible in (4) should satisfy the initial distribution

| (5) |

and the Fokker–Planck equation

| (6) |

However, the feasible set for defined by equality (6) is not convex, which means we may not be able to find the optimal solution. To address this issue, we introduce the following definition.

Definition 2.

We define maps as and . Then define , and , . Measures and are absolutely continuous with respect to .

We show that and are connected in the following way:

Proposition 1.

When (resp. ), the necessary and sufficient condition for the existence of an satisfying Definition 2 is (resp. ), where .

Proof.

See Section A.1. ∎

Using notations and , the Fokker–Planck equation (6) becomes linear and the SDE of the portfolio wealth reads

| (7) | ||||

| (8) |

From Proposition 1, at time , it is possible that the optimal drift is not saturated, i.e., . It means that the drift function in SDE (7) can be greater and eventually we can reach a better terminal wealth with a higher expectation. Then, instead of using this unsaturated drift to reach the prescribed terminal distribution, we can use the drift to attain a more ambitious distribution, and the extra part in the drift can be interpreted as cash saving. In this case, even when we have multiple assets () in the portfolio, optimal portfolios should lie on the curve , as in the case. Any portfolio lying below the curve represents a less than ideal investment because for the same level of risk (variance), we could achieve a greater return. This is consistent with the efficient frontier in modern portfolio theory (Markowitz 1952).

Now we define the concept of cash saving at time as . When the prescribed terminal distribution is not ambitious enough, to ensure we have as much cash saving as we can, we define the new feasible set as () and we can see the set is convex. To penalize measures out of the set , we define a cost function such that

| (9) |

where is a convex function and is a delta function defined as

| (10) |

Now we are ready to introduce formally the problem:

Problem 1.

Starting from an initial distribution , with a prescribed terminal distribution and a cost function (9), we want to solve the infimum of the functional

| (11) |

over all satisfying the constraints

| (12) | |||

| (13) |

2.2 Assumptions

We make the following assumptions which will hold throughout the paper.

Assumption 1.

The probability measure , is absolutely continuous with respect to the Lebesgue measure.

Assumption 2.

The penalty functional is lower semi-continuous and convex. We have if and only if almost everywhere.

Assumption 3.

-

(i)

The function is non-negative, lower semi-continuous and strictly convex in .

-

(ii)

The cost function is coercive in the sense that there exist constants and such that

-

(iii)

For all , and for any , we have

and

For simplicity, we write if there is no ambiguity.

3 Duality

In this section, we introduce the dual problem to Problem 1, this allows us to give optimality condition for the primal problem. First of all, we find out the convex conjugate of the cost functional, which will be used in the later proof.

3.1 Convex Conjugate

Define a function as

where is the convex conjugate of . Since is non-negative, it is obvious that

If we restrict the domain of its convex conjugate to , then

| (14) |

Because the function to be optimized is linear and , we can see the optimal in (14). With being convex and lower-semicontinuous, we have

The supremum is pointwise in time and space, and we can write

| (15) |

3.2 Dual Problem

Now we can state our main result. A key element in the dual problem is the Hamilton–Jacobi–Bellman (HJB) equation:

| (16) |

For any solution of the HJB equation (16), Itô’s formula yields,

Adding the penalty functional to both sides yields

| (17) |

Taking the infimum of the left hand side of (17) over and taking the infimum of the right hand side of (17) over , we get

The following result shows that optimizing the left hand side yields an equality.

Theorem 1 (Duality).

When is continuous, there holds

| (18) |

where the supremum is taken over all satisfying

| (19) |

Proof.

This proof is an application of the Fenchel–Rockafellar duality theorem, e.g., Brezis (2010, Theorem 1.12). From the constraint (12), we have that for all ,

| (20) |

Integrating by parts we obtain

| (21) |

Because of equation (15), we can reformulate the primal problem (11) as a saddle point problem:

| (22) |

Adding the Lagrangian penalty (21) to the functional (22), then Problem 1 can be written as

We write for the convex conjugate of functional :

Here we define the functional by

| (23) |

Its convex conjugate is defined as

| (24) |

If we restrict the domain to , with (15) and Assumption 2, we have

Indeed, if is not positive in (24), we would let and for some such that and let . If or are not absolutely continuous with respect to , we can find some such that but or . Then we let and , and by letting depending on the sign of and .

Next, we say that the set is represented by if

Then define as follows,

| (25) |

Notice that is well-defined, indeed, it does not depend on the choice of . If both represent , then , , , . It follows that . The set of represented functions is a linear subspace, and is linear with respect to in the convex set. Hence is convex and its convex conjugate is

Or equivalently,

We find that if satisfies (21), and otherwise.

Now we can express our objective functional as

The second equality is because if does not equal to at time . We prove the third equality in Section A.2.

We can let , then . We can see and it is continuous in at this point, and being finite at this point. Finally, the conditions of Fenchel duality theorem in Brezis (2010, Theorem 1.12) are fulfilled, and it implies

over the set being represented by , and satisfying .

Therefore we express in terms of :

under the constraint As a consequence of Fenchel duality theorem, the infimum in the primal problem is attained if finite. This completes the proof. ∎

Actually, using the same proof as in Guo et al. (2019), we can write the dual formulation in the following way:

Corollary 1.

When is continuous, there holds

| (26) |

where the supremum is running over all functions , and is a viscosity solution of the Hamilton–Jacobi–Bellman equation

| (27) |

Because the minimal objective function (11) is a trade-off between the cost function and the penalty functional, the optimal in the dual problem (26) will not in general ensure that reaches , unless the penalty functional goes to infinity for . When is attainable, it can be realized by choosing the penalty functional as an indicator function

| (28) |

Using the penalty functional (28) is equivalent to adding the terminal constraint . This also recovers our problem to the classical optimal transport problem.

Corollary 2.

Proof.

This proof is very similar to the one of Theorem 1, hence the repetitive steps are omitted here. Being different from the proof of Theorem 1, in this case, we define the functional by

Then its convex conjugate of is

We restrict the domain to , we have

Note that is equal to if and is equal to otherwise, which is equivalent to in (28). Define by (25), let , the conditions of Fenchel duality theorem in Brezis (2010, Theorem 1.12) are fulfilled. Therefore, we get

over the set being represented by , and satisfying . For the same reasons as in Corollary 1, we can express in terms of :

where is a viscosity solution of the Hamilton–Jacobi–Bellman equation (27). ∎

4 Numerical Methods for the Dual Problem

There has been a vast amount of numerical algorithms for the optimal mass transport problem. Gradient descent based methods are widely used to solve the reformulated dual problem of the Monge–Kantorovich problem, for example, by Chartrand et al. (2009) and Tan et al. (2013). Cuturi (2013) looked at transport problems from a maximum entropy perspective and computed the OT distance through Sinkhorn’s matrix scaling algorithm. This algorithm is also used for the entropic regularization of optimal transport by Benamou et al. (2019).

In this paper, we also use a gradient descent based method to solve the dual problem in Section 3. We know is the solution of the HJB equation (27). For a given terminal function , we can calculate by solving the HJB equation backward.

4.1 Finite Difference Scheme

First of all, to get , we solve the following PDE

| (30) |

with a given terminal boundary condition backwardly, using an implicit finite difference scheme. We let

| (31) |

In the numerical setting, we use time steps and space grid points. We use a constant time step and a constant spatial step . We discretize the PDE (30) using a forward approximation for , a central approximation for , and a standard approximation for . With some manipulation, we get the discretized form of (30) as

| (32) |

where the optimal controls and depend on . It is difficult to check the stability condition in our PDE because the optimal are unknown, but fortunately implicit finite difference methods have a weaker requirement than explicit finite difference methods. At the -th time step of the implicit finite difference method, although we do not have the true values for , we can make an initial guess of using the known values , then use a fixed-point iteration scheme to generate a sequence until converges. This method is also implemented in Guo et al. (2019).

With the optimal drift and diffusion known, we can now propagate forward with the Fokker–Planck equation (12) to find the empirical terminal density . With an initial wealth , the initial distribution is a Dirac Delta distribution . Since we used implicit finite difference to solve the HJB equation (30) backward, we use an explicit scheme for the forward Fokker–Planck equation (12). Then the discretized form is

| (33) |

4.2 Optimization algorithm

A key role in the gradient descent method is the optimality condition. By providing a gradient, the computation is faster and more accurate. For convenience, we define another function

| (34) |

and . Then we need to find an optimal to minimize . The change of w.r.t is

| (35) | ||||

| (36) |

We know that in (34) satisfies If we add a small variation to and denote as and as for short, then we get which is equivalent to

| (37) |

Multiplying PDE (37) by an arbitrary density function and with integration by parts, we have

Since the equation holds for all admissible , we get

| (38) |

Substituting (38) into (36), we can see an optimal terminal function should satisfy the optimality condition

| (39) |

Remark 1.

When is defined as (28), the corresponding optimality condition is

| (40) |

Now we are ready to solve the dual problem numerically. In Algorithm 1, we state the gradient descent based algorithm to look for the optimal in (26). It includes solving the HJB equation and the Fokker–Planck equation with a finite difference method combined with a fixed-point iteration, as described in Section 4.1. A similar numerical scheme can be found in Guo et al. (2019) for calibrating volatilities by optimal transport.

Initial guess

while and do

5 Numerical Results

In this section, we will apply Algorithm 1 and demonstrate various numerical examples. We also consider the situations with cash saving and cash input during the investment process.

5.1 Penalty functional with an intensity parameter

Before we demonstrate the numerical results, we need to choose an appropriate penalty functional . There is a range of methods to measure distribution discrepancy. A comprehensive survey on the distance or similarity measures between probability density functions (PDFs) is provided by Cha (2007). Note that our choice of penalty functional is not restricted to metrics, as long as satisfies Assumption 2 and describes similarity of the two PDFs.

The most intuitive choice is the norm of the difference. This quadratic function is convex and easy to implement. In the first example, we use the squared Euclidean distance as the penalty functional and as the cost function. We define the penalty functional as

where the parameter can be regarded as the intensity of the penalty for the inconsistency. Then the dual problem (26) can be expressed explicitly as

| (41) |

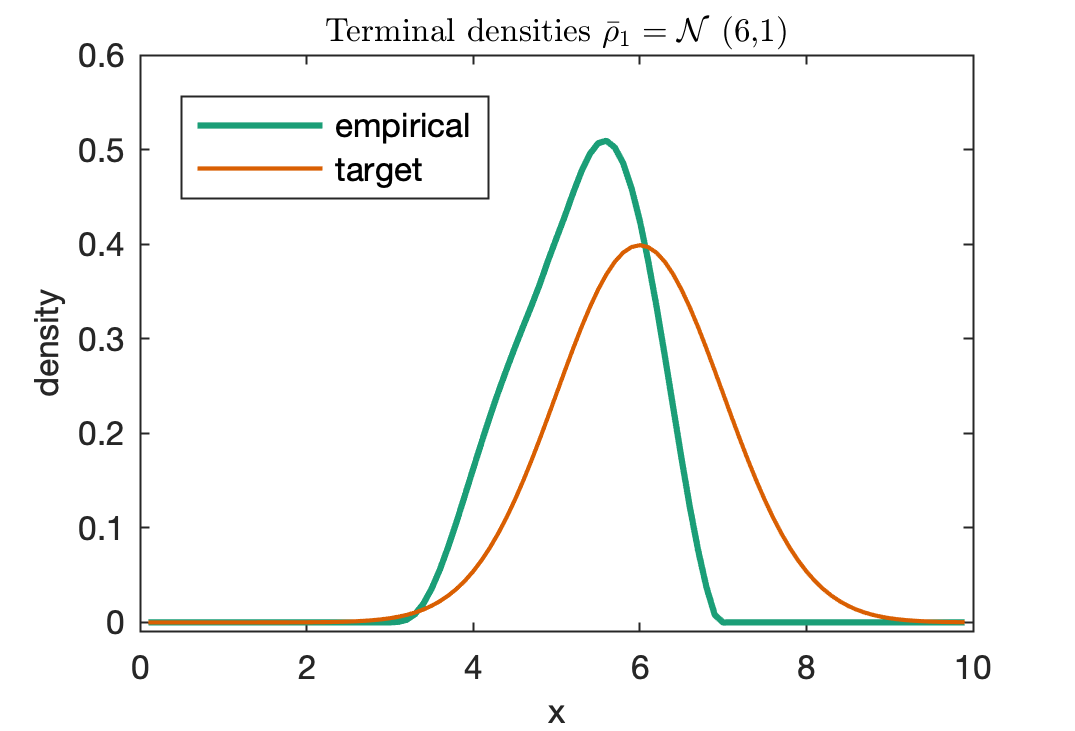

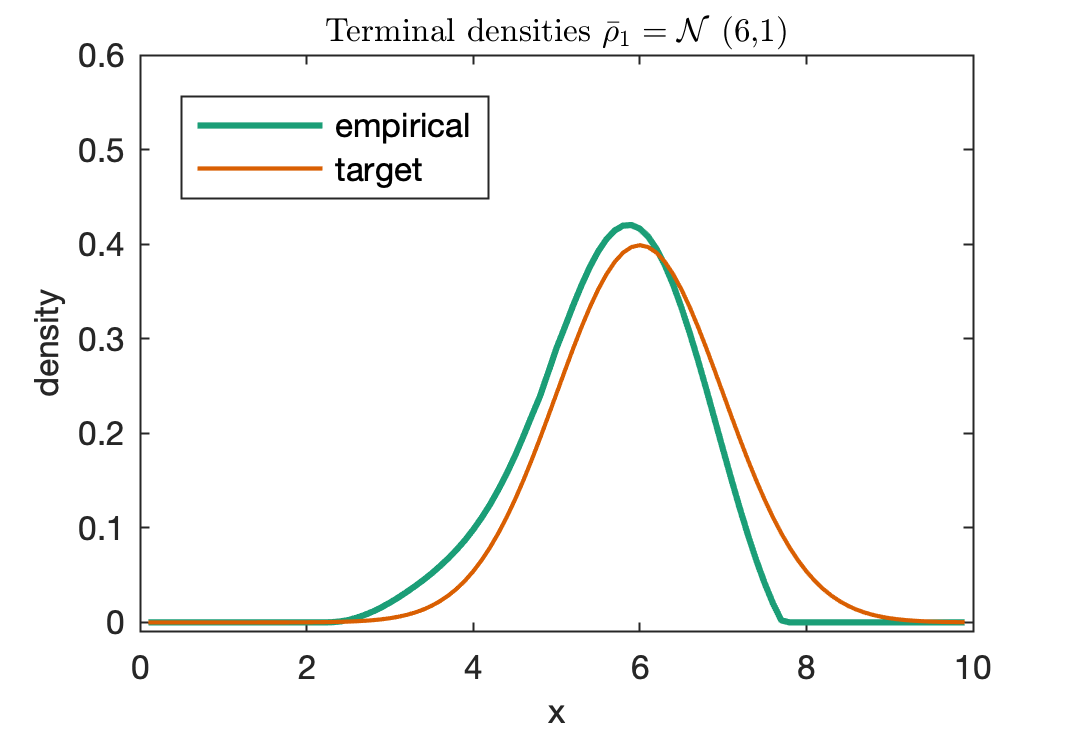

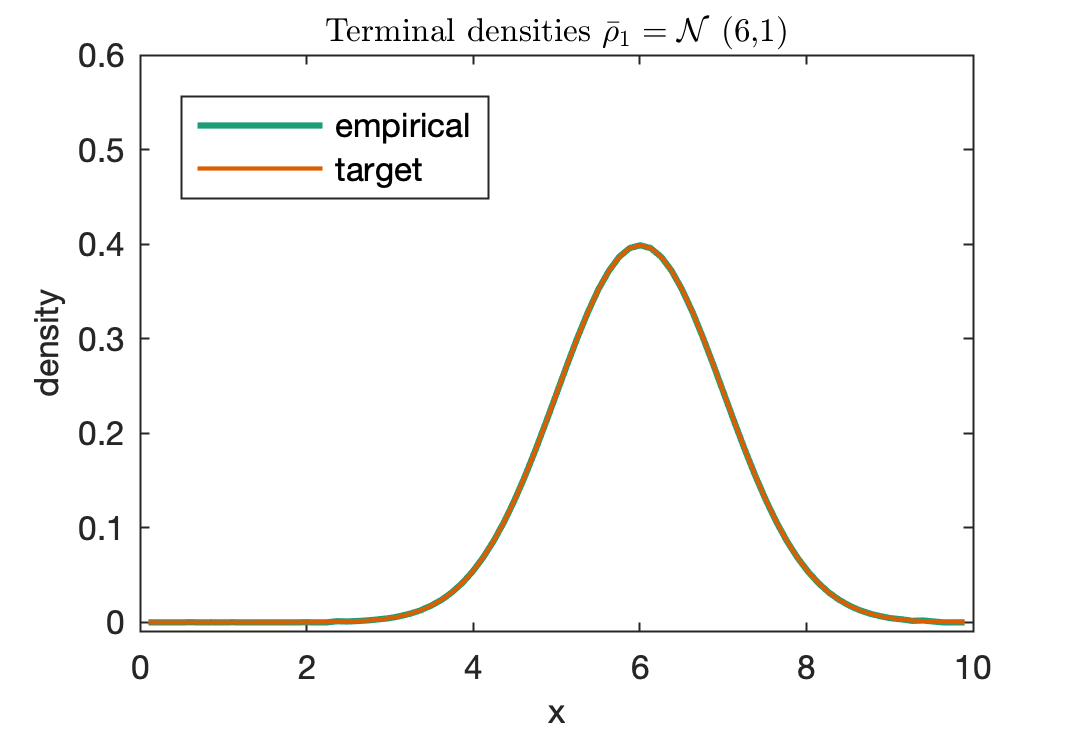

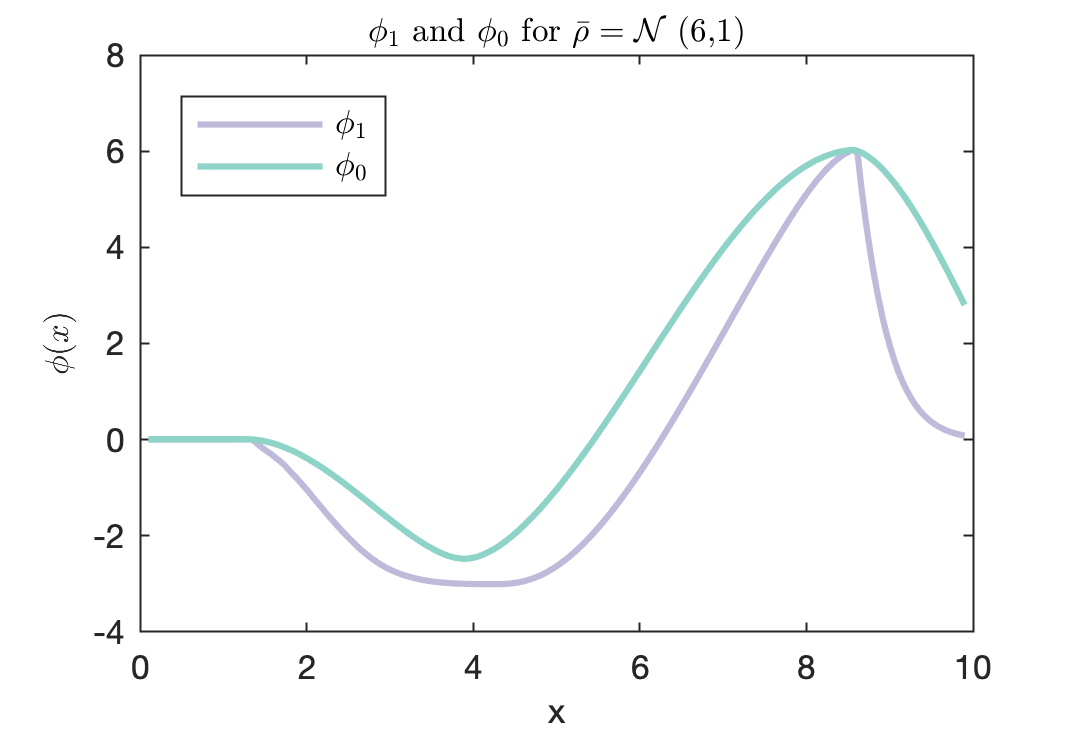

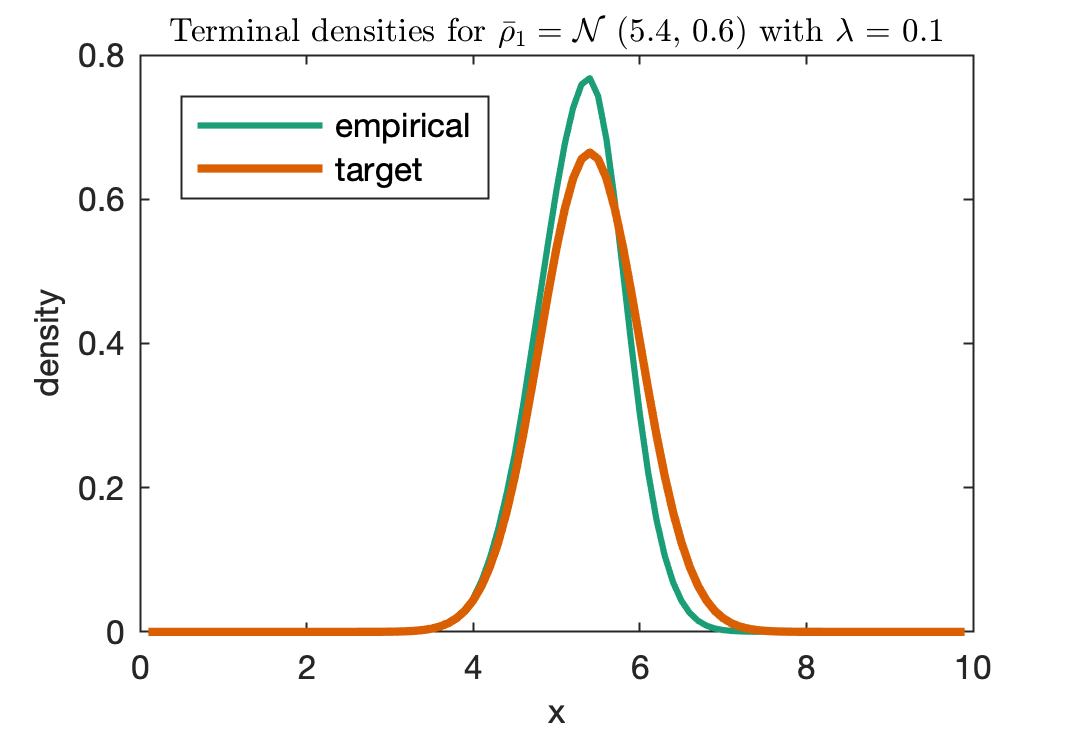

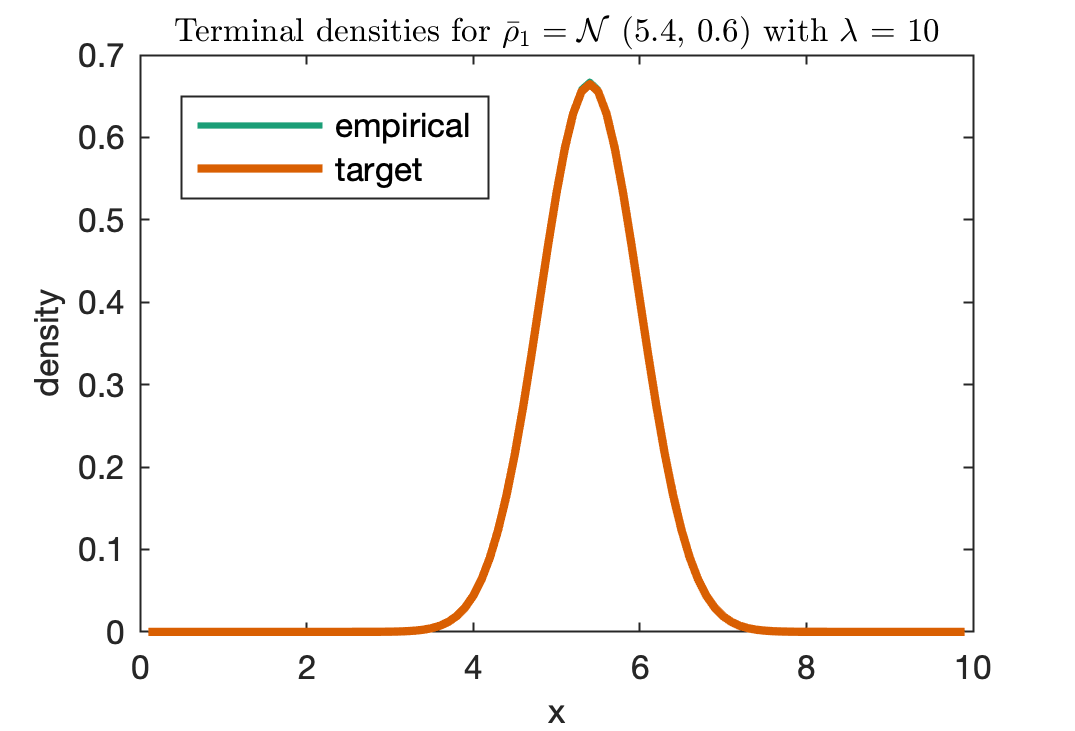

In this and the following numerical examples, we set the initial wealth . Figures 1a and 1b compare the empirical distribution of the terminal wealth () and the prescribed terminal distribution () for different intensities , where 111We denote a Normal distribution with mean and standard deviation .. We can see that gets closer to as we increase the intensity of the penalty. In figures 1c and 1d, we use the penalty functional (28), which is equivalent to setting . As shown in Figure 1c, this penalty functional makes attain the target , and the plot 1d illustrates the optimal function and the corresponding we got from Algorithm 1.

Compared to other research where the prescribed distributions are restricted to Gaussian, our method applies to a wide choice of , such as heavy-tailed and asymmetric distributions. In Figure 5.1, we illustrate an example where is a mixture of two Normal distributions, where

In Figure 5.1, we plot how the Euclidean distance changes with respect to . As we increase the intensity parameter , the Euclidean distance between and decreases. As goes to infinity, the distance asymptotically goes to zero.

![[Uncaptioned image]](/html/2009.12823/assets/mix_normal_PDE.png) \captionof

\captionof

figuremixture of Normal distributions

![[Uncaptioned image]](/html/2009.12823/assets/metric_lambda.png) \captionof

\captionof

figureDistance metric vs.

The Kullback–Leibler (K–L) divergence introduced in Kullback and Leibler (1951), is also known as relative entropy or information deviation. It measures the divergence of the distribution from the target , the more similar the two distributions are, the smaller the relative entropy will be. This measurement is widely used in Machine Learning to compare two densities because it has the following advantages: this function is non-negative; for a fixed distribution , is convex in ; if and only if everywhere. There are also caveats to the implementation of this penalty function. We may face or division by zero cases in practice; to address this, we can replace zero with an infinitesimal positive value.

In this case, the penalty functional is defined as

| (42) |

and the dual problem (26) can be expressed explicitly as

In Figure 2, we compare the empirical terminal density and the target when is defined by (42) and . The initial wealth and we set in Figure 2a and in Figure 2b.

5.2 Distribution of the wealth with cash saving

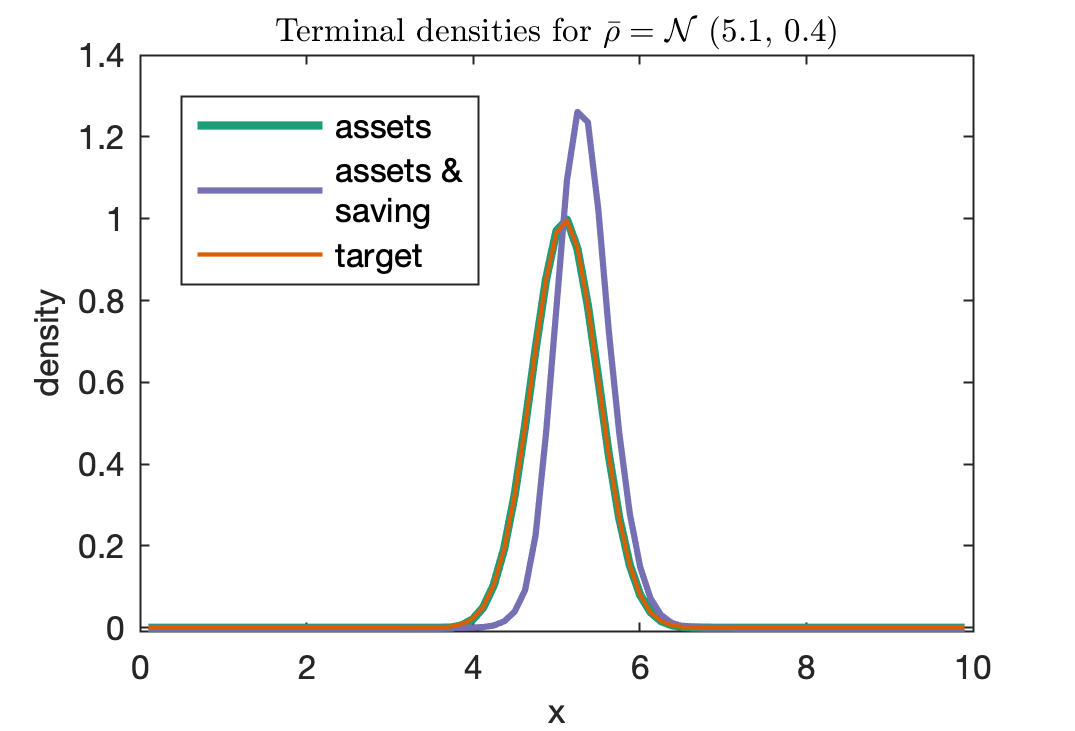

In this section, we consider the cash saving during the investment process. From previous parts, we have the constraint . However, when the prescribed target is not ambitious enough, we will find the optimal drift is not saturated, i.e., in (31). In this case, we can actually attain a more ambitious distribution and have an accumulated cash saving during the investment process. Our goal in this section is to show that we can reach a better terminal distribution, in the sense that the terminal wealth has a higher expected value, when we take cash saving into account.

Denote the accumulated cash saving up to time , and the evolution of is

If we add up the cash saving and the portfolio wealth , we can get a new process wealth with cash saving. Define , it is obvious to see that follows the dynamics

Denote by the distribution of at time , then satisfies the following Fokker-Planck equation

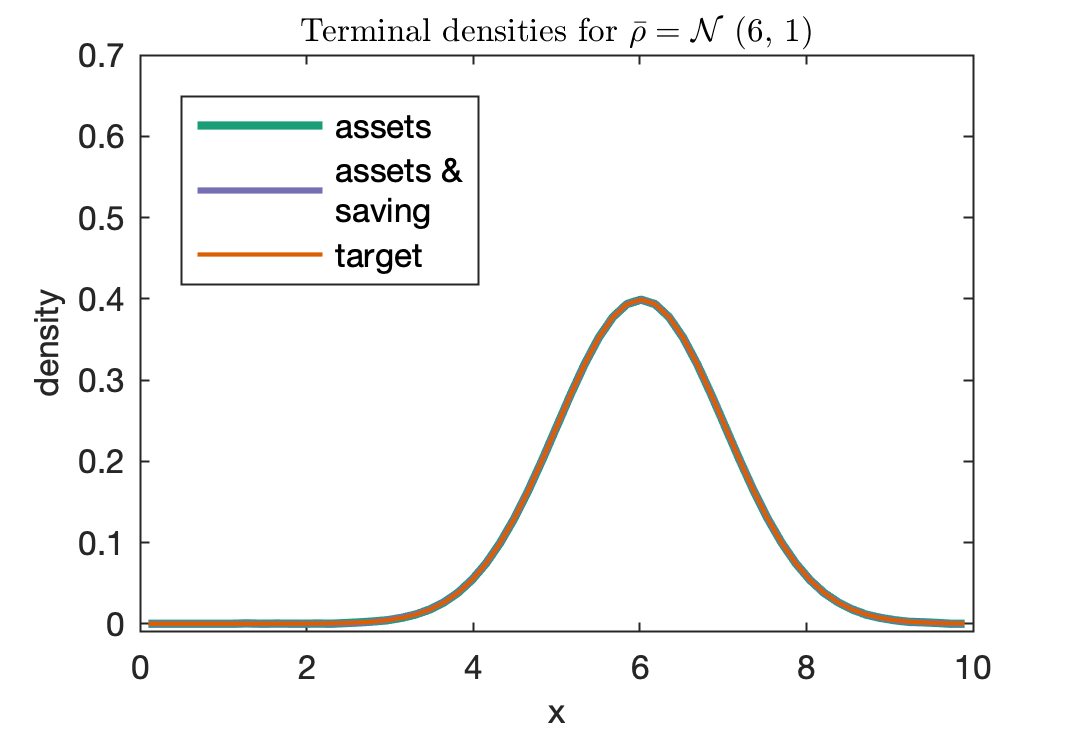

Therefore, after solving for the optimal , over time, we can find the densities of as well as . We keep using the squared Euclidean distance as the penalty functional and as the cost function. Figure 3 compares the densities for (terminal wealth), (terminal wealth with cash saving) and the prescribed target density. In Figure 3a, with a rather conservative target , although has attained the target, the distribution for the wealth with cash saving gathers at a higher value. When we set a higher target , as in Figure 3b, we see there is no cash saved in the process since the paths for and overlapped.

5.3 Distribution of the wealth with cash input

As stated in Proposition 1, we always have for a self-financing portfolio. However, in this section, we remove the constraint , and we allow instead. Then the part can be interpreted as the extra cash we invest during the process. In this case, theoretically, we can attain any prescribed target distribution as we want (see Tan et al. 2013, Remark 2.3). For the which is unattainable by the self-financing portfolio, we can now attain it with the help of cash input. However, to limit the use of cash, we design a cost function as follows,

| (43) |

where are positive constants. In the cost function (43), we use the term to penalize the part . By varying , we can control the strength of penalty and hence control the cash input flow. When is small, we are allowed to put in cash without being penalized excessively. When is large, we have to pay a high price for the cash input; consequently, the usage is limited. The terms and add coercivity to the function to ensure the existence of the solution, we set to be small positive real values.

With the optimal drift and diffusion , the dynamics of the wealth is

If there is no cash input, the maximum drift is . Denote the accumulated cash input up to time , and follows the dynamics

Define as the path without the cash input. Then the dynamics of is

Let the density of be , then follows the following Fokker-Planck equation

Finally, we can see the effect of cash input by comparing and .

5.3.1 Attainable target

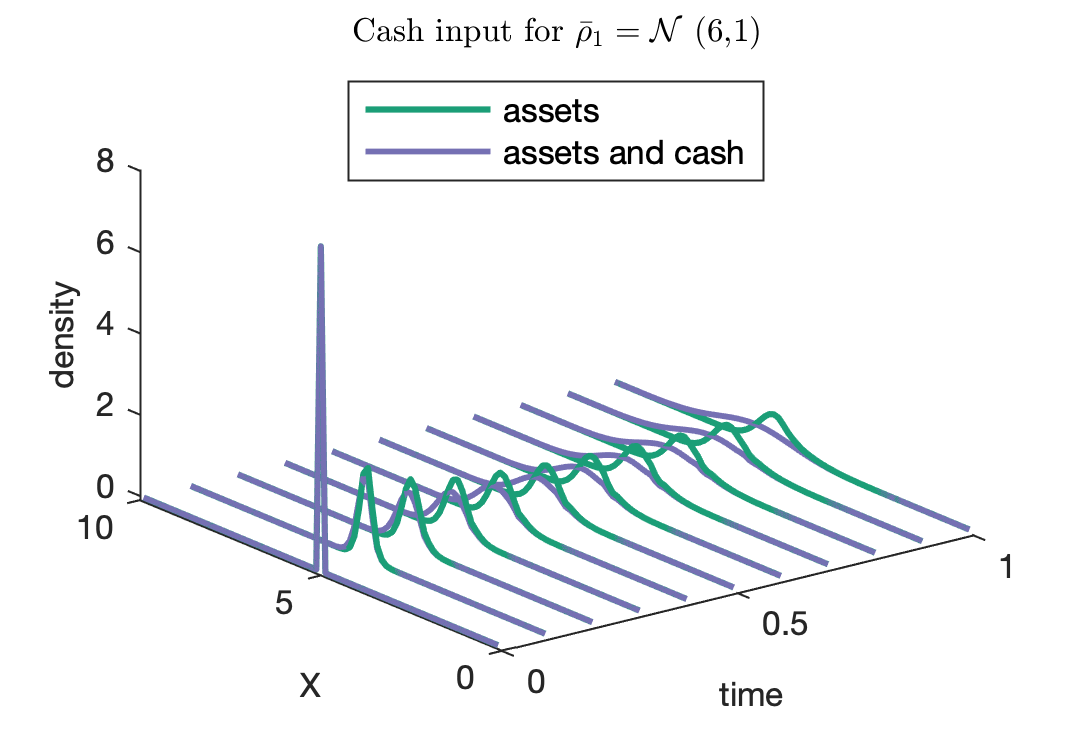

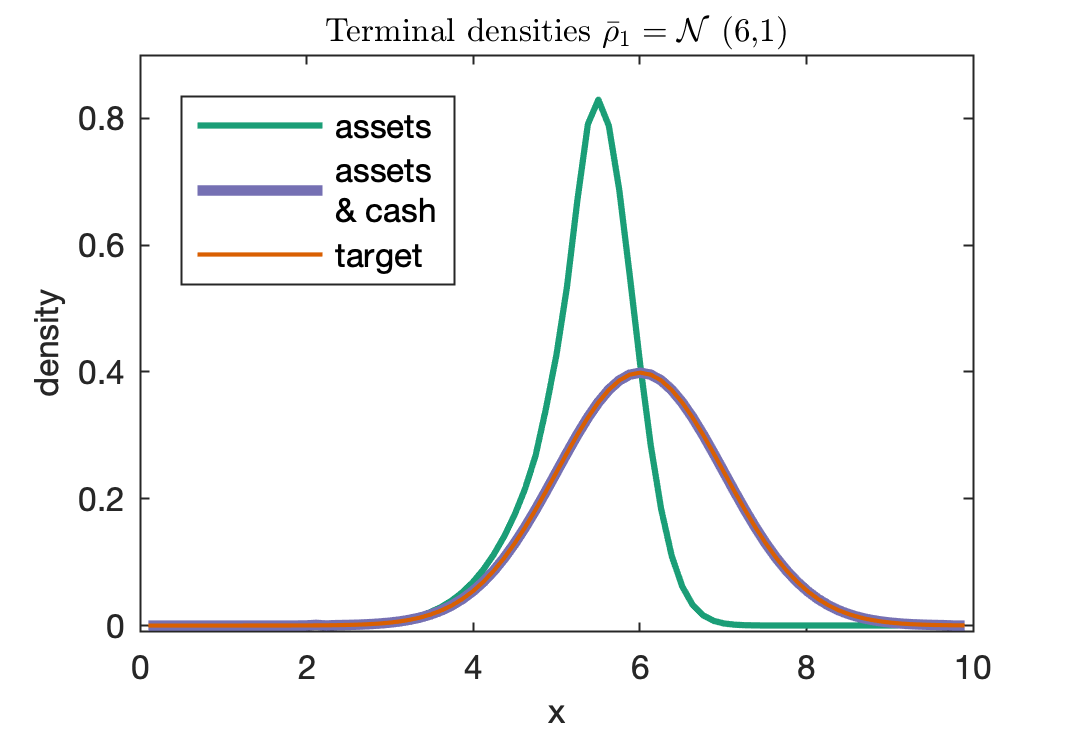

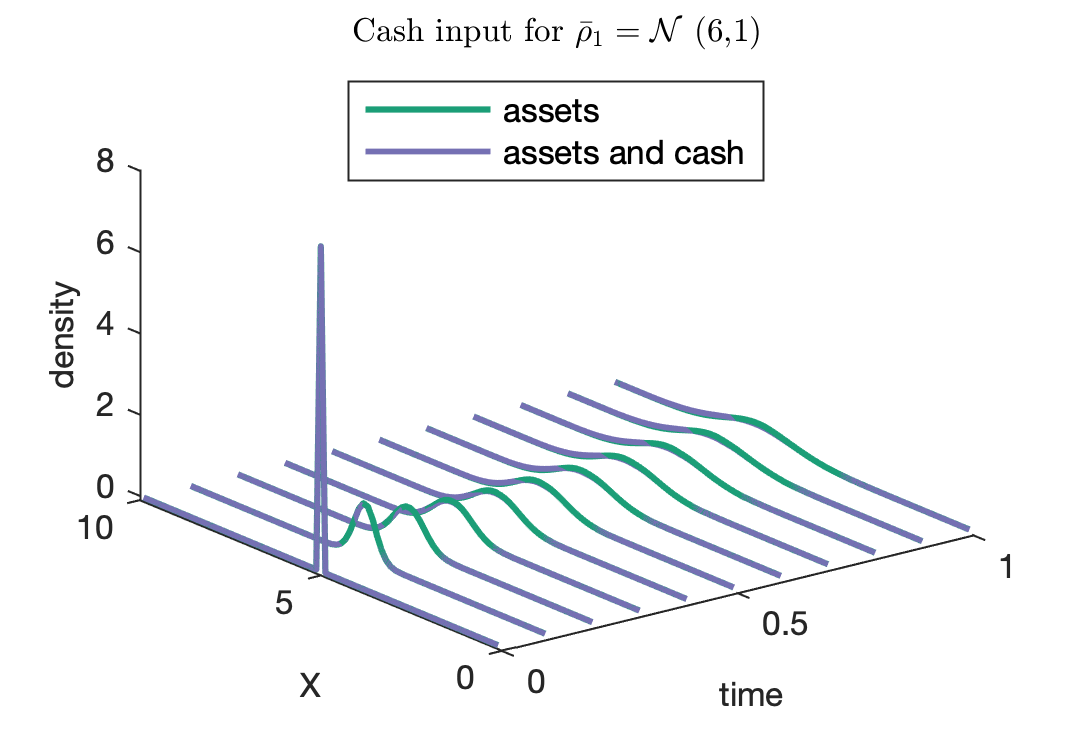

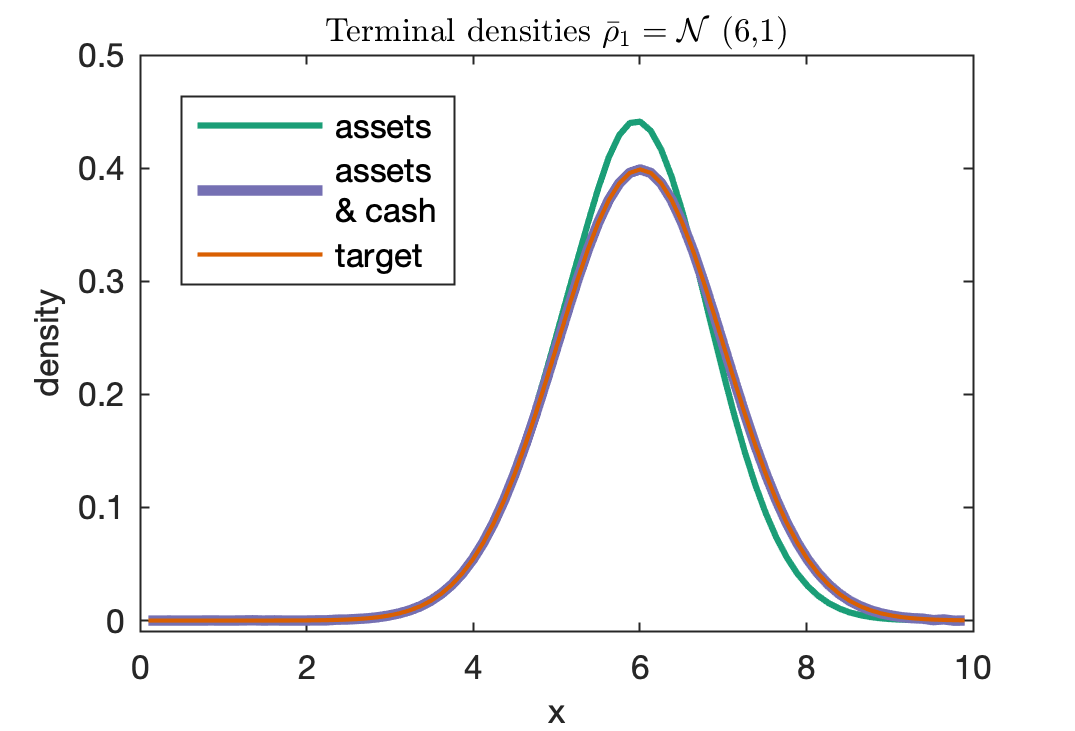

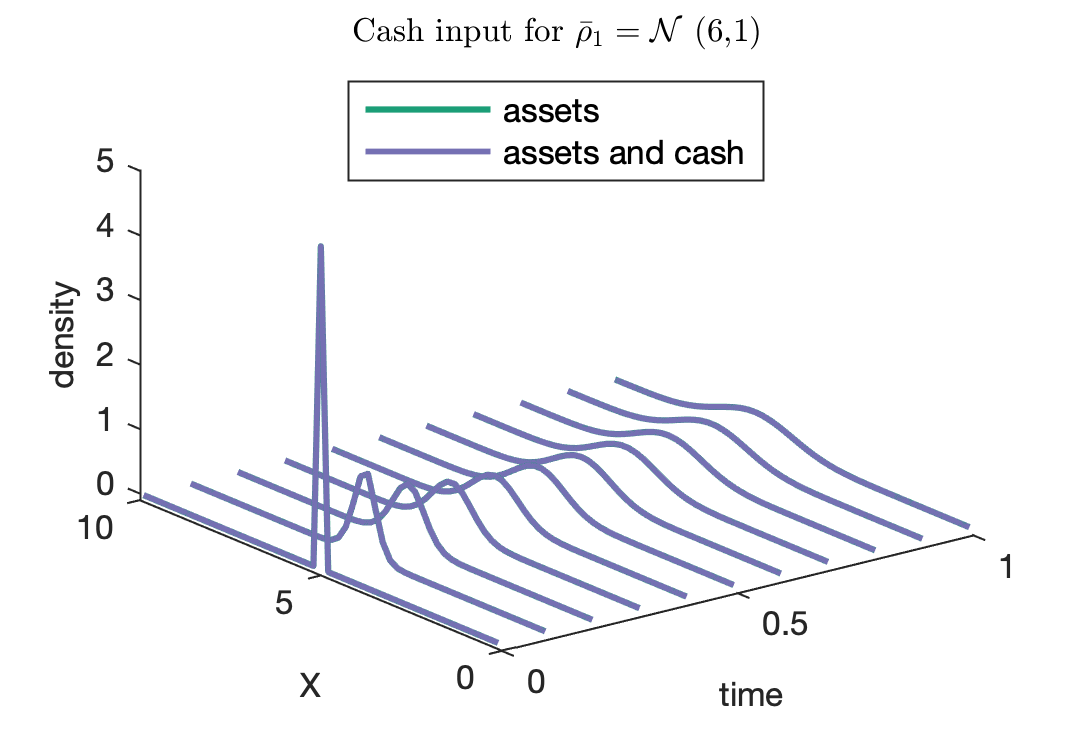

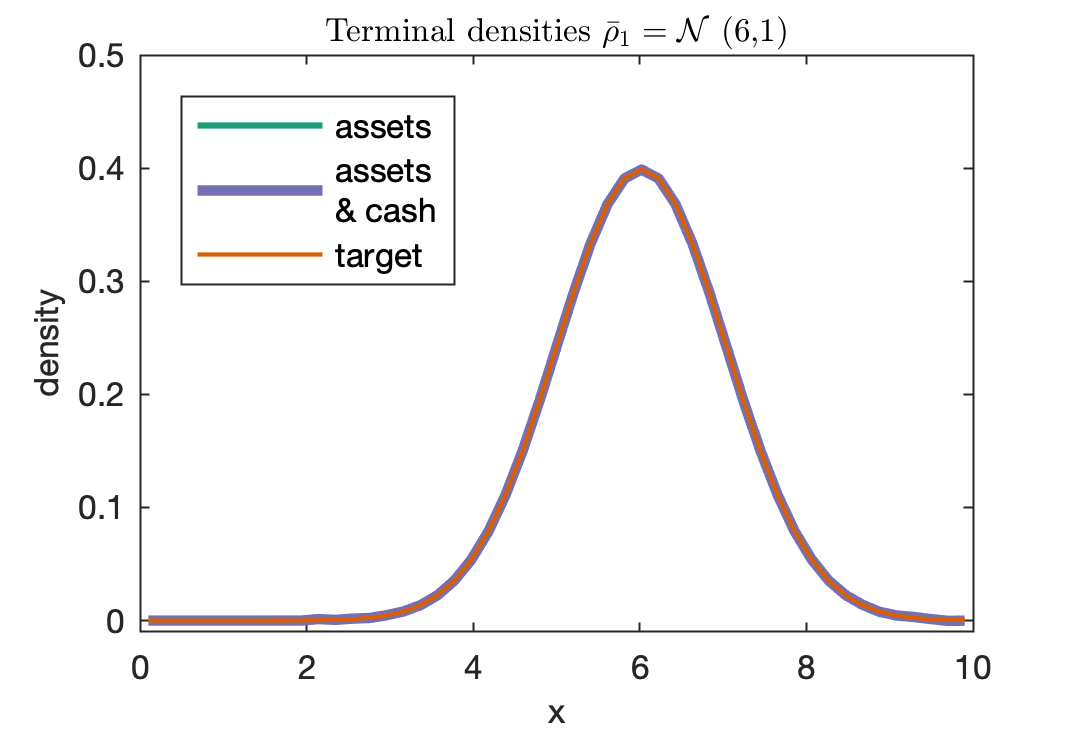

In the first example, we aim at the terminal distribution , which is attainable by the self-financing portfolio. We use the squared Euclidean distance as the penalty functional and equation (43) as the cost function. Figure 4 demonstrates the time evolution of (assets) and (assets and cash input), and it compares and for various values. At the beginning, we set the coefficient in Figure 4a. There is a clear difference between the paths for assets and assets and cash, which means we have input a significant amount of cash over time. As we increase the value of in Figure 4b, the difference between and becomes less obvious. When , the paths with or without cash input coincide in Figure 4c because the high cost has prevented the cash input in this context. Since the target is attainable, we can still reach it even without cash input, as shown in the second plot of 4c.

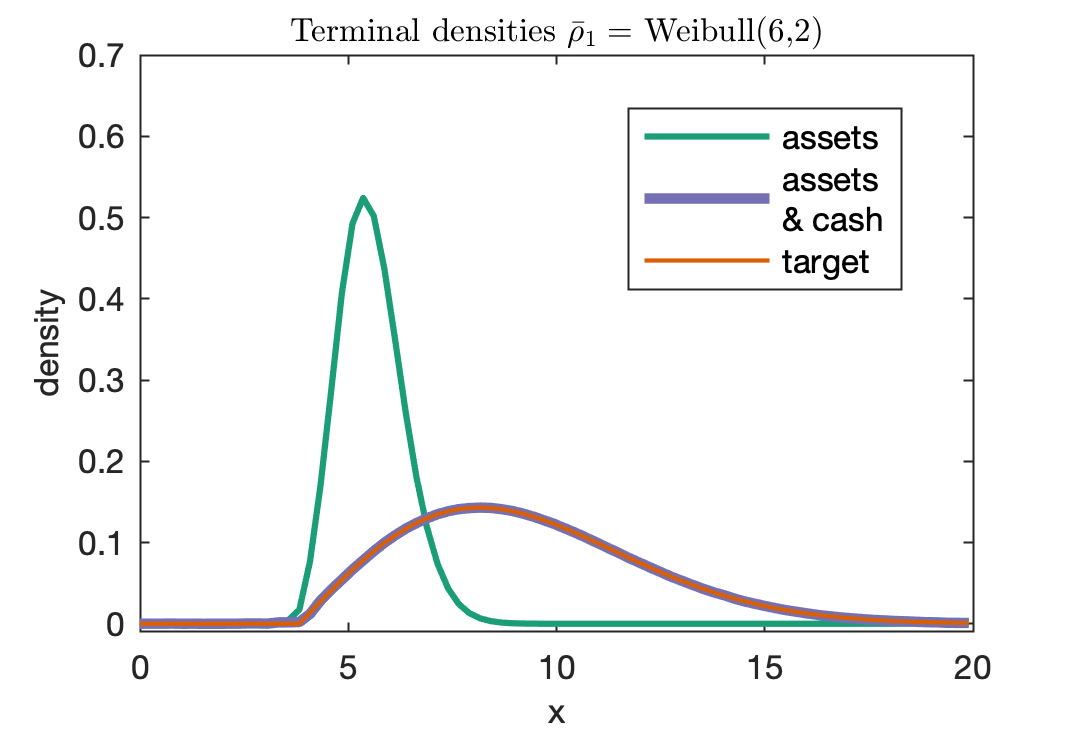

5.3.2 Unattainable target

To see the effect of cash input, here we demonstrate an example with an unattainable target. For instance, we may target at a terminal distribution with no left tail but a heavy right tail, in other words, there is very little risk for the wealth to fall below some level. Therefore, we set in Figure 5a, where is almost zero. In this example, the coefficient in (43) is not a constant anymore. Instead, we let be a function of time so that we can control the cash input flow over time. We define for and for . In the time-evolution plot (the left one of Figure 5a), we can see that the paths for assets and assets and cash start to differentiate from . Similarly, we can see the same effect in Figure 5b, where we set and we define for and for . In these two examples, the targets and are unattainable under the constraint . However, we can make the empirical terminal density reach by inputting cash wisely.

6 Conclusion

The ability to specify the whole distribution of final wealth of interest as portfolio optimization target gives a greater flexibility over classical objective functions such as expected utility or moment-based objectives such as the mean-variance framework and its extensions. In this article, we construct a portfolio and the dynamics of the portfolio wealth is a semimartingale. Starting from an initial wealth, by controlling the portfolio allocation process, we are able to steer the portfolio wealth to a prescribed distribution at the terminal time. This problem is closely related to optimal mass transport (OMT). In the problem formulation, in addition to the conventional cost function in OMT, we also design a penalty functional to measure the divergence of the empirical terminal density from the prescribed one. We take into consideration the possible consumption during the investment process, and show that we can actually reach a better terminal density when there is no consumption. When the target density is attainable, our problem can recover the classical OMT problem by choosing an indicator function as the penalty function. When the target terminal density is unattainable by the self-financing portfolio, we devise a strategy to reach it by allowing cash input during the investment process. We proved a duality result for the primal problem and solved it with a gradient descent based algorithm. Our numerical results verify the accuracy and validity of this algorithm.

References

- Benamou and Brenier (2000) Benamou, J.-D. and Y. Brenier (2000). A computational fluid mechanics solution to the Monge-Kantorovich mass transfer problem. Numerische Mathematik 84(3), 375–393.

- Benamou et al. (2019) Benamou, J.-D., G. Carlier, and L. Nenna (2019). Generalized incompressible flows, multi-marginal transport and Sinkhorn algorithm. Numerische Mathematik 142(1), 33–54.

- Brenier et al. (2003) Brenier, Y., U. Frisch, M. Henon, G. Loeper, S. Matarrese, R. Mohayaee, and A. Sobolevskii (2003). Reconstruction of the early universe as a convex optimization problem. arxiv (september 2003). arXiv preprint astro-ph/0304214.

- Brezis (2010) Brezis, H. (2010). Functional analysis, Sobolev spaces and partial differential equations. Springer Science & Business Media.

- Cha (2007) Cha, S.-H. (2007). Comprehensive survey on distance/similarity measures between probability density functions. City 1(2), 1.

- Chartrand et al. (2009) Chartrand, R., B. Wohlberg, K. Vixie, and E. Bollt (2009). A gradient descent solution to the Monge-Kantorovich problem. Applied Mathematical Sciences 3(22), 1071–1080.

- Cuturi (2013) Cuturi, M. (2013). Sinkhorn distances: Lightspeed computation of optimal transport. In Advances in neural information processing systems, pp. 2292–2300.

- Dolinsky and Soner (2014) Dolinsky, Y. and H. M. Soner (2014). Martingale optimal transport and robust hedging in continuous time. Probability Theory and Related Fields 160(1-2), 391–427.

- Ferradans et al. (2014) Ferradans, S., N. Papadakis, G. Peyré, and J.-F. Aujol (2014). Regularized discrete optimal transport. SIAM Journal on Imaging Sciences 7(3), 1853–1882.

- Guo et al. (2019) Guo, I., N. Langrené, G. Loeper, and W. Ning (2019). Robust utility maximization under model uncertainty via a penalization approach. arXiv preprint arXiv:1907.13345.

- Guo et al. (2019) Guo, I., G. Loeper, and S. Wang (2019). Calibration of local-stochastic volatility models by optimal transport. arXiv preprint arXiv:1906.06478.

- Henry-Labordère (2017) Henry-Labordère, P. (2017). Model-free hedging: A martingale optimal transport viewpoint. CRC Press.

- Henry-Labordère et al. (2016) Henry-Labordère, P., X. Tan, and N. Touzi (2016). An explicit martingale version of the one-dimensional Brenier’s theorem with full marginals constraint. Stochastic Processes and their Applications 126(9), 2800–2834.

- Kantorovich (1942) Kantorovich, L. V. (1942). On the translocation of masses. In Dokl. Akad. Nauk. USSR (NS), Volume 37, pp. 199–201.

- Kraus and Litzenberger (1976) Kraus, A. and R. H. Litzenberger (1976). Skewness preference and the valuation of risk assets. The Journal of finance 31(4), 1085–1100.

- Kullback and Leibler (1951) Kullback, S. and R. A. Leibler (1951). On information and sufficiency. The annals of mathematical statistics 22(1), 79–86.

- Lee (1977) Lee, C. F. (1977). Functional form, skewness effect, and the risk-return relationship. Journal of financial and quantitative analysis 12(1), 55–72.

- Loeper (2006) Loeper, G. (2006). The reconstruction problem for the Euler-Poisson system in cosmology. Archive for rational mechanics and analysis 179(2), 153–216.

- Markowitz (1952) Markowitz, H. (1952). Portfolio selection. The journal of finance 7(1), 77–91.

- Mikami (2015) Mikami, T. (2015). Two end points marginal problem by stochastic optimal transportation. SIAM Journal on Control and Optimization 53(4), 2449–2461.

- Mikami and Thieullen (2006) Mikami, T. and M. Thieullen (2006). Duality theorem for the stochastic optimal control problem. Stochastic processes and their applications 116(12), 1815–1835.

- Monge (1781) Monge, G. (1781). Mémoire sur la théorie des déblais et des remblais. Histoire de l’Académie Royale des Sciences de Paris.

- Rachev and Rüschendorf (1998) Rachev, S. T. and L. Rüschendorf (1998). Mass Transportation Problems: Volume I: Theory, Volume 1. Springer Science & Business Media.

- Tan et al. (2013) Tan, X., N. Touzi, et al. (2013). Optimal transportation under controlled stochastic dynamics. The annals of probability 41(5), 3201–3240.

- Villani (2003) Villani, C. (2003). Topics in optimal transportation. Number 58. American Mathematical Soc.

- Villani (2008) Villani, C. (2008). Optimal transport: old and new, Volume 338. Springer Science & Business Media.

Appendix A Appendices

A.1

Proof of Proposition 1.

Firstly, we prove the necessity. We can use eigen-decomposition and write the covariance matrix , where and the th column of is the eigenvector of , and is the diagonal matrix whose diagonal elements are the corresponding eigenvalues, .

For any given , . We define , then , where denotes the norm. Similarly, . Therefore we have the relationship between and as

Define , we can write the above inequality as .

For given satisfying , we want to show that there exists , such that , . First of all, since , there exists a vector whose norm satisfies . Then will be equivalent to . With Cauchy–Schwarz inequality, holds. Therefore there exists a vector such that and . With this , there exists an .

The case for dimension is trivial, hence omitted here. ∎

A.2

Proposition 2.

We denote the set of that can be represented by . Then we have

Proof.

Following closely the argument in Villani (2003, Section 1.3), we define the space of continuous functions on , going to at infinity. For , we decompose , where . For any , we have .