Network geometry and market instability

Abstract

The complexity of financial markets arise from the strategic interactions among agents trading stocks, which manifest in the form of vibrant correlation patterns among stock prices. Over the past few decades, complex financial markets have often been represented as networks whose interacting pairs of nodes are stocks, connected by edges that signify the correlation strengths. However, we often have interactions that occur in groups of three or more nodes, and these cannot be described simply by pairwise interactions but we also need to take the relations between these interactions into account. Only recently, researchers have started devoting attention to the higher-order architecture of complex financial systems, that can significantly enhance our ability to estimate systemic risk as well as measure the robustness of financial systems in terms of market efficiency. Geometry-inspired network measures, such as the Ollivier-Ricci curvature and Forman-Ricci curvature, can be used to capture the network fragility and continuously monitor financial dynamics. Here, we explore the utility of such discrete Ricci curvatures in characterizing the structure of financial systems, and further, evaluate them as generic indicators of the market instability. For this purpose, we examine the daily returns from a set of stocks comprising the USA S&P-500 and the Japanese Nikkei-225 over a 32-year period, and monitor the changes in the edge-centric network curvatures. We find that the different geometric measures capture well the system-level features of the market and hence we can distinguish between the normal or ‘business-as-usual’ periods and all the major market crashes. This can be very useful in strategic designing of financial systems and regulating the markets in order to tackle financial instabilities.

1 Introduction

For centuries science had thrived on the method of reductionism– considering the units of a system in isolation, and then trying to understand and infer about the whole system. However, the simple method of reductionism has severe limitations Anderson (1972), and fails to a large extent when it comes to the understanding and modeling the collective behavior of the components of a ‘complex system’. More and more systems are now being identified as complex systems, and hence scientists are now embracing the idea of complexity as one of the governing principles of the world we live in. Any deep understanding of a complex system has to be based on a system-level description, since a key ingredient of any complex system is the rich interplay of nonlinear interactions between the system components. The financial market is truly a spectacular example of such a complex system, where the agents interact strategically to determine the best prices of the assets. So new tools and interdisciplinary approaches are needed Vemuri (1978); Gell-Mann (1995), and already there has been an influx of ideas from econophysics and complexity theory Mantegna and Stanley (2007); Bouchaud and Potters (2003); Sinha et al. (2010); Chakraborti et al. (2011, 2015) to explain and understand economic and financial markets.

The traditional economic theories, based on axiomatic approaches and consequently less predictive power, could not foresee event like the sub-prime crisis of 2007-2008 or the long-lasting effects of such a critical financial crash on the global economy. Researchers advocated that new concepts and techniques Battiston et al. (2016) like tipping points, feedback, contagion, network analysis along with the use of complexity models Lux and Westerhoff (2009) could help in better understanding of highly interconnected economic and financial systems, as well as monitoring them. There have been numerous papers in the past that have addressed similar concerns and tried to adopt new approaches for studying financial systems. Since the correlations among stocks change with time, the underlying market dynamics generate very interesting correlation-based networks evolving over time. The study of empirical cross-correlations among stock prices goes back to more than two decades Mantegna (1999a, b); Laloux et al. (1999); Plerou et al. (1999); Gopikrishnan et al. (2001); Kullmann et al. (2002). One of commonly adopted approaches for the modeling and analysis of complex financial systems has been correlation-based networks, and it has emerged as an important tool Mantegna (1999a, b); Plerou et al. (2002); Onnela et al. (2003); Tumminello et al. (2005); Pharasi et al. (2018, 2019); Chakraborti et al. (2020a).

A network or graph consists of nodes connected by edges. In real-world networks, nodes represent the components or entities, while edges represent the interactions or relationships between nodes. In the context of financial markets, the nodes represent the stocks and the edges characterize the correlation strengths (or their transformations into distance measures). The network formed by connecting stocks of highly correlated prices, price returns, and trading volumes are all scale-free, with a relatively small number of stocks influencing the majority of the stocks in the market Chi et al. (2010). Hierarchical clustering has been used to cluster stocks into sectors and sub-sectors, and their network analysis provides additional information on the interrelationships among the stocks Tumminello et al. (2007, 2010). The cross-correlations among stock returns allow one to construct other correlation-based networks such as minimum spanning tree (MST) Mantegna (1999a, b); Onnela et al. (2003); Miccichè et al. (2003) or a threshold network Kumar and Deo (2012). Another approach to monitor the correlation-based networks over time, referred to as structural entropy, quantifies the structural changes of the network as a single parameter. It takes into account the number of communities as well as the size of the communities Almog and Shmueli (2019) to determine the structural entropy, which is then used to continuously monitor the market. The thermodynamical entropy Wang et al. (2019) can also be used to describe the dynamics of stock market networks as it acts like an indicator for the financial system. Very recently, based on the distribution properties of the eigenvector centralities of correlation matrices, Chakraborti et al. Chakraborti et al. (2020b) have proposed a computationally cheap yet uniquely defined and non-arbitrary eigen-entropy measure, to show that the financial market undergoes ‘phase separation’ and there exists a new type of scaling behavior (data collapse) in financial markets. Further, a recent review by Kukreti et al. Kukreti et al. (2020) critically examines correlation-based networks and entropy approaches in evolving financial systems. To understand the topology of the correlation-based networks as well as to define the complexity, a volume-based dimension has also been proposed by Nie et al. Nie and Song (2018). There have also been some novel studies where the financial market has been considered as a quasi-stationary system, and then the ensuing dynamics have been studied Stepanov et al. (2015); Rinn et al. (2015); Chetalova et al. (2015); Heckens et al. (2020); Wang et al. (2020).

Introduced long ago by Gauss and Riemann, curvature is a central concept in geometry that quantifies the extent to which a space is curved Jost (2017). In geometry, the primary invariant is curvature in its many forms. While curvature has connections to several essential aspects of the underlying space, in a specific case, curvature has a connection to the Laplacian, and hence, to the ‘heat kernel’ on a network. Curvature also has connections to the Brownian motion and entropy growth on a network. Moreover, curvature is also related to algebraic topological aspects, such as the homology groups and Betti numbers, which are relevant, for instance, for persistent homology and topological data analysis Carlsson (2009). Recently, there has been immense interest in geometrical characterization of complex networks Krioukov et al. (2010); Bianconi (2015); Sandhu et al. (2015); Sreejith et al. (2016); Bianconi and Rahmede (2017). Network geometry can reveal higher-order correlations between nodes beyond pairwise relationships captured by edges connecting two nodes in a graph Kartun-Giles and Bianconi (2019); Iacopini et al. (2019); Kannan et al. (2019). From the point of view of structure and dynamics of complex networks, edges are more important than nodes, since the nodes by themselves cannot constitute a meaningful network. Hence, it may be more important to develop edge-centric measures rather than node-centric measures to characterize the structure of complex networks Sreejith et al. (2016); Samal et al. (2018).

Surprisingly, geometrical concepts, especially, discrete notions of Ricci curvature, have only very recently been used as edge-centric network measures Sandhu et al. (2015); Ni et al. (2015); Sreejith et al. (2016); Sandhu et al. (2016); Samal et al. (2018); Ni et al. (2019). Furthermore, curvature has deep connections to related evolution equations that can be used to predict the long-time evolution of networks. Although the importance of geometric measures like curvature have been understood for quite some time, yet there has been limited number of applications in the context of complex financial networks. In particular, Sandhu et al. Sandhu et al. (2016) studied the evolution of Ollivier-Ricci curvature Ollivier (2007, 2009) in threshold networks for the USA S&P-500 market over a 15-year span (1998-2013) and showed that the Ollivier-Ricci curvature is correlated to the increase in market network fragility. Consequently, Sandhu et al. Sandhu et al. (2016) suggested that the Ollivier-Ricci curvature can be employed as an indicator of market fragility and study the designing of (banking) systems and framing regulation policies to combat financial instabilities such as the sub-prime crisis of 2007-2008. In this paper, we expand the study of geometry-inspired network measures for characterizing the structure of the financial systems to four notions of discrete Ricci curvature, and evaluate the curvature measures as generic indicators of the market instability.

It is noteworthy that in the present paper, the term ‘curvature’ refers to four notions of discrete Ricci curvature investigated here, which are as such intrinsic curvatures, and not extrinsic curvatures as has been considered elsewhere in the context of complex networks (see e.g., Aste et al. Aste et al. (2005)). Recall that extrinsic geometry is given by embedding the networks in a suitable ambient space (which in practice is the hyperbolic plane or space), and thereafter, the geometric properties induced by the embedding space are studied (see, e.g. Saucan et al. (2020)). While this approach is intuitive and conducive to simple illustrations, such network embeddings are distorting, except for the special case of isometric embeddings. In contrast, the intrinsic approach to networks is independent of any specific embedding, and hence, of the necessary additional computations and any distortion. Moreover, such an intrinsic approach allows for the independent study of such powerful tools as the Ricci flow, without the vagaries associated with the embedding in an ambient space of certain dimension (see, e.g. Saucan (2012)). Furthermore, the Ollivier-Ricci curvature has been employed to show that the ‘backbone’ of certain real-world networks is indeed tree-like, hence intrinsically hyperbolic Ni et al. (2015). Specific to financial networks, Sandhu et al. Sandhu et al. (2016) have shown that Ollivier-Ricci curvature, which is of course an intrinsic curvature, presents a powerful tool in the detection of financial market crashes. In this work, we have considered three additional notions Sreejith et al. (2016); Saucan et al. (2020) of discrete Ricci curvature for the study of financial networks.

In the present paper, we examine the daily returns from a set of stocks comprising the USA S&P-500 and the Japanese Nikkei-225 over a 32-year period, and monitor the changes in the edge-centric geometric curvatures. A major goal of this research is to evaluate different notions of discrete Ricci curvature for their ability to unravel the structure of complex financial networks and serve as indicators of market instabilities. Our study confirms that during a normal period the market is very modular and heterogeneous, whereas during an instability (crisis) the market is more homogeneous, highly connected and less modular Onnela et al. (2003); Scheffer et al. (2012); Pharasi et al. (2019); Chakraborti et al. (2020a). Further, we find that the discrete Ricci curvature measures, especially Forman-Ricci curvature Sreejith et al. (2016); Samal et al. (2018), capture well the system-level features of the market and hence we can distinguish between the normal or ‘business-as-usual’ periods and all the major market crises (bubbles and crashes). Importantly, among four Ricci-type curvature measures, the Forman-Ricci curvature of edges correlates highest with the traditional market indicators and acts as an excellent indicator for the system-level fear (volatility) and fragility (risk) for both the markets. We also find using these geometric measures that there are succinct and inherent differences in the two markets, USA S&P-500 and Japan Nikkei-225. These new insights will help us to understand tipping points, systemic risk, and resilience in financial networks, and enable us to develop monitoring tools required for the highly interconnected financial systems and perhaps forecast future financial crises and market slowdowns.

2 Ricci-type curvatures for edge-centric analysis of networks

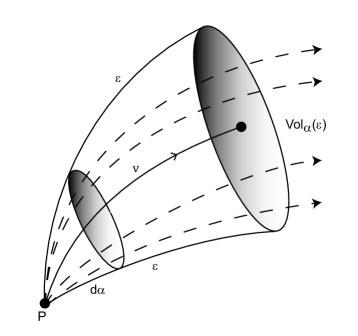

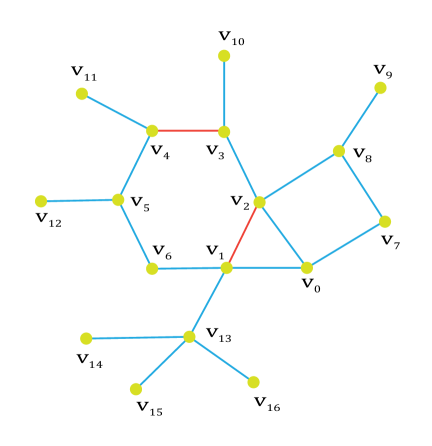

The classical notion of Ricci curvature applies to smooth manifolds, and its classical definition requires tensors and higher-order derivatives Jost (2017). Thus, the classical definition of Ricci curvature is not immediately applicable in the discrete context of graphs or networks. Therefore, in order to develop any meaningful notion of Ricci curvature for networks, one has to inspect the essential geometric properties captured by this curvature notion, and find their proper analogues for discrete networks. To this end, it is essential to recall that Ricci curvature quantifies two essential geometric properties of the manifold, namely, volume growth and dispersion of geodesics. See Electronic Supplementary Material (ESM) Figure S1 for a schematic illustration of the Ricci curvature. Further, since classical Ricci curvature is associated to a vector (direction) in smooth manifolds Jost (2017), in the discrete case of networks, it is naturally assigned to edges Samal et al. (2018). Thus, notions of discrete Ricci curvatures are associated to edges rather than vertices or nodes in networks Samal et al. (2018). Note that no discretization of Ricci curvature for networks can capture the full spectrum of properties of the classical Ricci curvature defined on smooth manifolds, and thus, each discretization can shed a different light on the analyzed networks Samal et al. (2018). In this work, we apply four notions of discrete Ricci curvature for networks to study the correlation-based networks of stock markets.

Ollivier-Ricci curvature

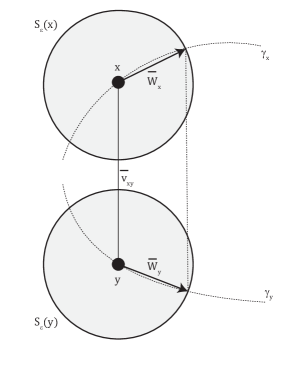

Ollivier’s discretization Ollivier (2007, 2009) of the classical Ricci curvature has been extensively used to analyze graphs or networks Lin and Yau (2010); Lin et al. (2011); Bauer et al. (2012); Jost and Liu (2014); Ni et al. (2015); Sandhu et al. (2015, 2016); Samal et al. (2018); Ni et al. (2019); Sia et al. (2019). Ollivier’s definition is based on the following observation. In spaces of positive curvature, balls are closer to each other on the average than their centers, while in spaces of negative curvature, balls are farther away on the average than their centers (ESM Figure S2). Ollivier’s definition extends this observation from balls (volumes) to measures (probabilities). More precisely, the Ollivier-Ricci (OR) curvature of an edge between nodes and is defined as

| (1) |

where and represent measures concentrated at nodes and , respectively, denotes the Wasserstein distance Vaserstein (1969) (also known as the earth mover’s distance) between the discrete probability measures and , and the cost is the distance between nodes and , respectively. Moreover, the Wasserstein distance which gives the transportation distance between the two measures and , is given by

| (2) |

with being the set of probability measures that satisfy

| (3) |

where is the set of nodes in the graph. The above equation represents all the transportation possibilities of the mass to . is the minimal cost or distance to transport the mass of to that of . Note that the distance in Eq. 2 is taken to be the path distance in the unweighted or weighted graph. Furthermore, the probability distribution for has to be specified, and this is chosen to be uniform over neighbouring nodes of Lin et al. (2011).

Simply stated, to determine the OR curvature of an edge , in Eq. 1 one compares the average distance between the neighbours of the nodes and anchoring the edge in an optimal arrangement with the distance between and itself. Importantly, the average distance between neighbours of and is evaluated as an optimal transport problem wherein the neighbours of are coupled with those of in such a manner that the average distance is as small as possible. In the setting of discrete graphs or networks, OR curvature by definition captures the volume growth aspect of the classical notion for smooth manifolds, see e.g. Samal et al. (2018) for details. In this work, we have computed the average OR curvature of edges (ORE) in undirected and weighted networks using Eq. 1.

Forman-Ricci curvature

Forman’s approach to the discretization of Ricci curvature Forman (2003) is more algebraic in nature and is based on the relation between the Riemannian Laplace operator and Ricci curvature. While devised originally for a much larger class of discrete geometric objects than graphs, an adaptation to network setting was recently introduced by some of us Sreejith et al. (2016). The Forman-Ricci (FR) curvature of an edge in an undirected network with weights assigned to both edges and nodes is given by Sreejith et al. (2016)

| (4) |

where denotes the edge under consideration between nodes and , denotes the weight of the edge , and denote the weights associated with the nodes and , respectively, and denote the set of edges incident on nodes and , respectively, after excluding the edge under consideration which connects the two nodes and . Furthermore, some of us have also extended the notion of FR curvature to directed networks Saucan et al. (2019a). In case of discrete networks, FR curvature captures the geodesic dispersal property of the classical notion Samal et al. (2018). In ESM Figure S3, we illustrate, using a simple example, the computation of FR curvature in an undirected graph. In this work, we have computed the average FR curvature of edges (FRE) in undirected and weighted networks using Eq. 4.

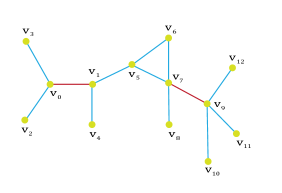

From a geometric perspective, the FR curvature quantifies the information spread at the ends of edges in a network (Figure 1; ESM Figure S3). The higher the information spread at the ends of an edge, the more negative will be the value of its FR curvature. Specifically, an edge with high negative FR curvature is likely to have several neighbouring edges connected to both anchoring nodes, and moreover, such an edge can be seen as a funnel at both ends, connecting many other nodes. Intuitively, such an edge with high negative FR curvature can be expected to have high edge betweenness centrality as many shortest paths between other nodes, including those quite far in the network, are also likely to pass through this edge. Previously, some of us have empirically shown a high statistical correlation between FR curvature and edge betweenness centrality in diverse networks Sreejith et al. (2017); Samal et al. (2018).

Menger-Ricci curvature

The remaining two curvatures studied here are adaptations of curvatures for metric spaces to discrete graphs. Indeed, both unweighted and weighted graphs can be viewed as a metric space where the distance between any two nodes can be specified by the path length between them. Among notions of metric, and indeed, discrete curvature, Menger Menger (1930) has proposed the simplest and earliest definition whereby he defines the curvature of metric triangles formed by three points in the space as the reciprocal of the radius of the circumscribed circle of a triangle . Recently, some of us Saucan et al. (2019b, 2020) have adapted Menger’s definition to networks. Let be a metric space and be a triangle with sides , then the Menger curvature of is given by

| (5) |

where . In the particular case of a combinatorial triangle with each side of length 1, the above formula gives . Furthermore, it is clear from the above formula that Menger curvature is always positive. Following the differential geometric approach, the Menger-Ricci (MR) curvature of an edge in a network can be defined as Saucan et al. (2019b, 2020)

| (6) |

where denote the triangles adjacent to the edge . Intuitively, if an edge is part of several triangles in the network, such an edge will have high positive MR curvature (Figure 1). In ESM Figure S4, we illustrate, using a simple example, the computation of MR curvature in an undirected graph. In this work, we have computed the average MR curvature of edges (MRE) in undirected financial networks by ignoring the edge weights and using Eq. 6.

Haantjes-Ricci curvature

We have also applied another notion of metric curvature to networks which is based on the suggestion of Finsler and was developed by his student Haantjes Haantjes (1947). Haantjes defined the curvature of a metric curve as the ratio between the length of an arc of the curve and that of the chord it subtends. More precisely, given a curve in a metric space , and given three points on , between and , the Haantjes curvature at the point is defined as

| (7) |

where denotes the length, in the intrinsic metric induced by , of the arc . In networks, can be replaced by a path between two nodes and , and the subtending chord by the edge between the two nodes. Recently, some of us Saucan et al. (2019b, 2020) have defined the Haantjes curvature of such a simple path as

| (8) |

where, if the graph is a metric graph, , that is the shortest path distance between nodes and . In particular, for the combinatorial metric (or unweighted graphs), we obtain that , where is as above. Note that considering simple paths in graphs concords with the classical definition of Haantjes curvature, since a metric arc is, by its very definition, a simple curve. Thereafter, the Haantjes-Ricci (HR) curvature of an edge Saucan et al. (2019b, 2020) can be defined as

| (9) |

where denote the paths that connect the nodes anchoring the edge . Note that while MR curvature considers only triangles or simple paths of length 2 between two nodes anchoring an edge in unweighted graphs, the HR curvature considers even longer paths between the same two nodes anchoring an edge (Figure 1). Moreover, for triangles endowed with the combinatorial metric, the two notions by Menger and Haantjes coincide, up to a universal constant. In ESM Figure S4, we illustrate, using a simple example, the computation of HR curvature in an undirected graph. In this work, we have computed the average HR curvature of edges (HRE) in undirected financial networks by ignoring the edge weights and using Eq. 9. Moreover, due to computational constraints, we only consider simple paths of length between the two vertices at the ends of any edge while computing its HR curvature using Eq. 9 in analyzed networks. Note that both Menger and Haantjes curvature are positive in undirected networks, and they capture the (absolute value of) geodesics dispersal rate of the classical Ricci curvature.

3 Data and Methods

Data description

The data was collected from the public domain of Yahoo finance database Yah for two markets: USA S&P-500 index and Japanese Nikkei-225 index. The investigation in this work spans a 32-year period from 2 January 1985 (02-01-1985) to 30 December 2016 (30-12-2016). We analyzed the daily closure price data of stocks for days for USA S&P-500 and stocks for days for Japanese Nikkei-225 markets. ESM Tables S1 and S2 give the lists of 194 and 165 stocks (along with their sectors) for the USA S&P-500 and Japanese Nikkei-225 markets, respectively, and these stocks are present in the two markets for the entire 32-year period considered here.

Cross-correlation and distance matrices

We present a study of time evolution of the cross-correlation structures of return time series for stocks (Figure 1). The daily return time series is constructed as , where is the adjusted closing price of the stock at time (trading day). Then, the cross-correlation matrix is constructed using equal-time Pearson cross-correlation coefficients,

where , indicates the end date of the epoch of size days, and the means as well as the standard deviations are computed over that epoch.

Instead of working with the correlation coefficient , we use the ‘ultrametric’ distance measure:

such that , which can be used for the construction of networks Mantegna (1999a, b); Onnela et al. (2003); Kumar and Deo (2012).

Here, we computed daily return cross-correlation matrix over the short epoch of days and shift of the rolling window by days, for (a) stocks of USA S&P-500 for a return series of days, and (b) stocks of Japan Nikkei-225 for days, during the 32-year period from 1985 to 2016. We use epochs of days (one trading month) to obtain a balance between choosing short epochs for detecting changes and long ones for reducing fluctuations. In the main text, we show results for networks constructed from correlation matrices with overlapping windows of days, while in ESM, we show results for networks constructed from correlation matrices with non-overlapping windows of days.

Network construction

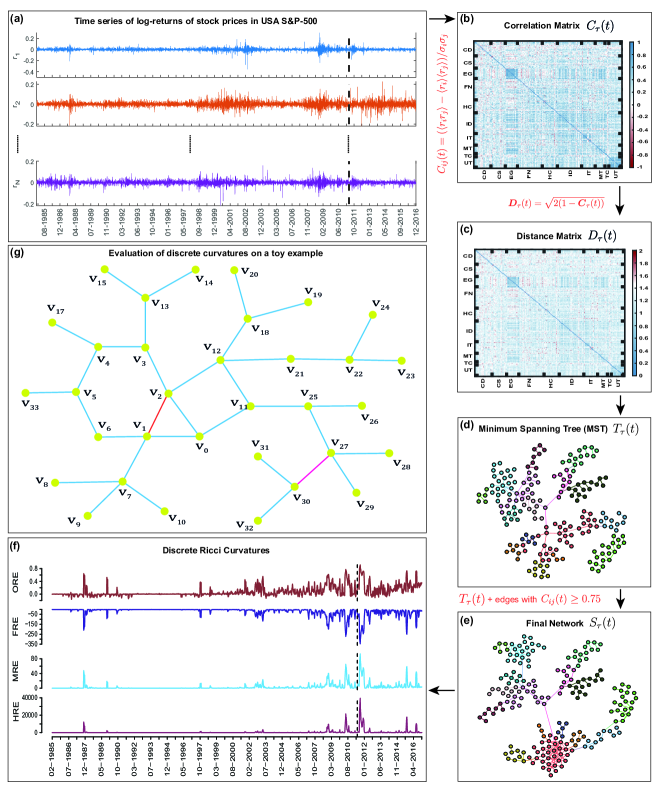

For a given time window of days ending on trading day , the distance matrix constructed from the correlation matrix between the 194 stocks in USA S&P-500 index or the 165 stocks in Japan Nikkei-225 index, can be viewed as an undirected complete graph where the weight of an edge between stocks and is given by the distance . For the time window of days ending on trading day , we start with this edge weighted complete graph and create the minimum spanning tree (MST) using Prim’s algorithm Prim (1957). Thereafter, we add edges in with to to obtain the graph (Figure 1). We will use the graph to compute different discrete Ricci curvatures and other network measures. We remark that the procedure used here to construct the graph follows previous works Onnela et al. (2003); Sandhu et al. (2016) on analysis of correlation-based networks of stock markets.

Intuitively, the motivation behind the above method of graph construction can be understood as follows. Firstly, the MST method gives a connected (spanning) graph between all nodes (stocks) in the specific market. Secondly, the addition of edges between nodes (stocks) with correlation ensures that the important edges are also captured in the graph .

Common network measures

Given an undirected graph with the sets of vertices or nodes and edges , the number of edges is given by the cardinality of set , that is , and the number of nodes is given by the cardinality of set , that is . The edge density of such a graph is given by the ratio of the number of edges divided by the number of possible edges, that is, . The average degree of the graph gives the average number of edges per node, that is, . In case of an edge-weighted graph where denotes the weight of the edge between nodes and , one can also compute its average weighted degree which gives the average of the sum of the weights of the edges connected to nodes, that is, where . For any pair of nodes and in the graph, one can compute the shortest path length between them. Thereafer, the average shortest path length is given by the average of the shortest path lengths between all pairs of nodes in the graph, that is,

The diameter is given by the maximum of the shortest paths between all pairs of nodes in the graph, i.e., . The communication efficiency Latora and Marchiori (2001) of a graph is an indicator of its global ability to exchange information across the network. The communication efficiency of a graph is given by

Modularity measures the extent of community structure in the network and community detection algorithms aim to partition the graph into communities such that the modularity attains the maximum value Girvan and Newman (2002). The modularity is given by the equation Girvan and Newman (2002); Blondel et al. (2008)

where and give the sum of weights of edges attached to nodes and , respectively, and give the communities of and , respectively, and is equal to 1 if else 0. Here, we use Louvain method Blondel et al. (2008) to compute the modularity of the edge-weighted networks. Network entropy is an average measure of graph heterogeneity as it quantifies the diversity of edge distribution using the remaining degree distribution Solé and Valverde (2004). denotes the probabibility of a node to have remaining (excess) degree and is given by where denotes the probability of a node to have degree . The network entropy of a graph is then given by

The above-mentioned network measures were computed in stock market networks using the python package NetworkX Hagberg et al. (2008).

GARCH() process

The generalized ARCH process GARCH() was introduced by Bollerslev Bollerslev (1986). The variable , a strong white noise process, can be written in terms of a time-dependent standard deviation , such that , where is a random Gaussian process with zero mean and unit variance.

The simplest GARCH process is the GARCH(1,1) process, with Gaussian conditional probability distribution function

| (10) |

where and ; is an additional control parameter. One can rewrite Eq. 10 as a random multiplicative process

| (11) |

For calculating this we have used an in-built function from MATLAB garch (https://in.mathworks.com/help/econ/garch.html).

Minimum Risk Portfolio

We calculated the minimum risk portfolio in the Markowitz framework, as a measure of risk-aversion of each investor with maximized expected returns and minimized variance. In this model, the variance of a portfolio shows the importance of effective diversification of investments to minimize the total risk of a portfolio. The Markowitz model minimizes with respect to the normalized weight vector , where is the covariance matrix calculated from the stock log-returns, is the measure of risk appetite of investor and is the expected return of the assets. We set short-selling constraint, and which entails a convex combination of stock return for finding the minimum risk portfolio. For calculating this we have used an in-built function from MATLAB Portfolio (https://in.mathworks.com/help/finance/portfolio.html).

4 Results and Discussion

We analyze here the time series of the logarithmic returns of the stocks in the USA S&P-500 and Japanese Nikkei-225 markets over a period of 32 years (1985-2016) by constructing the corresponding Pearson cross-correlation matrices . We then use cross-correlation matrices computed over time epochs of size days with either overlapping or non-overlapping windows (i.e. shifts of or days, respectively) and ending on trading days to study the evolution of the correlation-based networks and corresponding network properties, especially edge-centric geometric measures. Figure 1 gives an overview of our evaluation of discrete Ricci curvatures in correlation-based threshold networks constructed from log-returns of market stocks. Figure 1(a) shows the daily log-returns over the 32-year period (1985-2016). An arbitrarily chosen cross-correlation matrix over time epoch of days and days ending on 04-05-2011 and corresponding distance matrix are shown in Figure 1(b) and (c), respectively. The minimum spanning tree (MST) constructed from the distance matrix is shown in Figure 1(d). Thereafter, a threshold network is constructed using MST and edges with , as shown in Figure 1(e). The discrete Ricci curvatures are computed from the threshold networks. In Figure 1(f), we show the evolution of the discrete curvatures in threshold networks over the 32-year period. In Figure 1(g), we motivate the four discrete Ricci curvatures considered here using a simple example network.

A major goal of this research is to evaluate different notions of discrete Ricci curvature for their ability to unravel the structure of complex financial networks and serve as indicators of market instabilities. Previously, Sandhu et al. Sandhu et al. (2016) have analyzed the USA S&P-500 market over a period of 15 years (1998-2013) to show that the average Ollivier-Ricci (OR) curvature of edges (ORE) in threshold networks increases during periods of financial crisis. Here, we extend the analysis by Sandhu et al. Sandhu et al. (2016) to (a) two different stock markets, namely, USA S&P-500 and Japanese Nikkei-225, (b) a span of 32 years (1985-2016), (c) four traditional market indicators (namely, index log-returns , mean market correlation , volatility of the market index estimated using GARCH(1,1) process, and risk corresponding to the minimum risk Markowitz portfolio of all the stocks in the market), and (d) four notions of discrete Ricci curvature for networks. Since discretizations of Ricci curvature are unable to capture the entire properties of the classical Ricci curvature defined on continuous spaces, the four discrete Ricci curvatures evaluated here can shed light on different properties of analyzed networks Samal et al. (2018). In particular, some of us have introduced another discretization, Forman-Ricci (FR) curvature, to the domain of networks Sreejith et al. (2016). Note that OR curvature captures the volume growth property of classical Ricci curvature while FR curvature captures the geodesic dispersal property Samal et al. (2018). Nevertheless, our empirical analysis has shown that the two discrete notions, OR and FR curvature, are highly correlated in model and real-world networks Samal et al. (2018). Importantly, in large networks, computation of the OR curvature is intensive while that of the FR curvature is simple as the later depends only on immediate neighbours of an edge Samal et al. (2018). Therefore, we started by investigating the ability of FR curvature to capture the structure of complex financial networks.

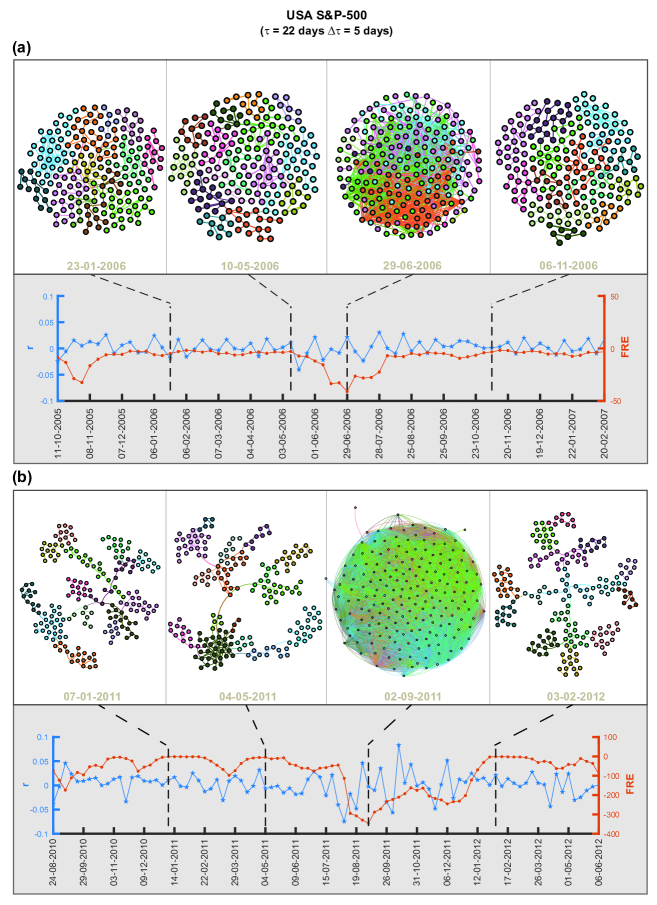

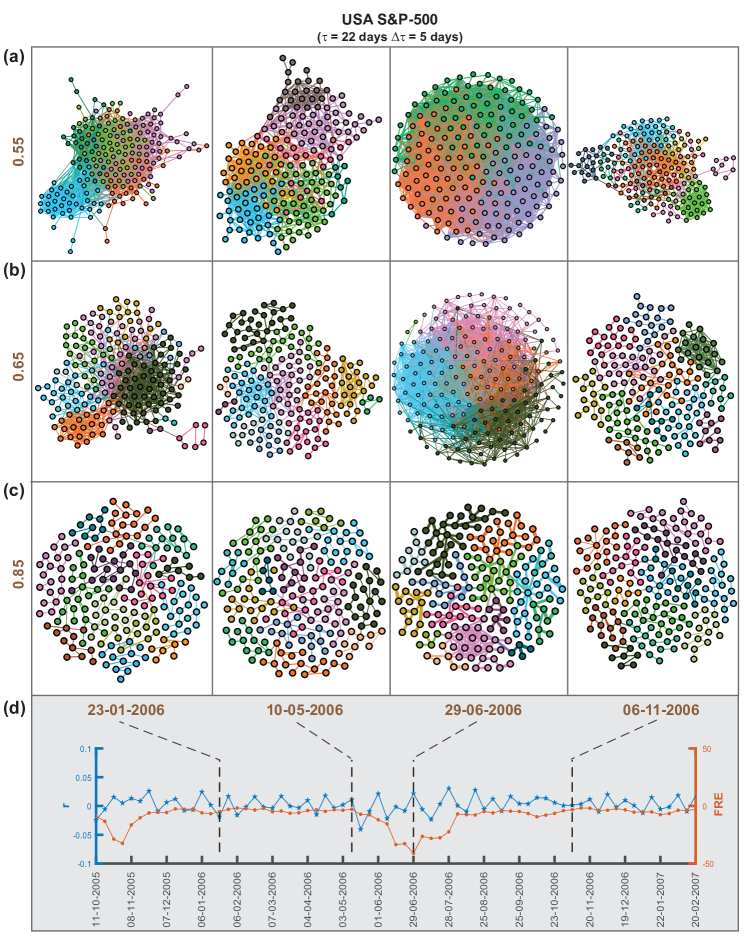

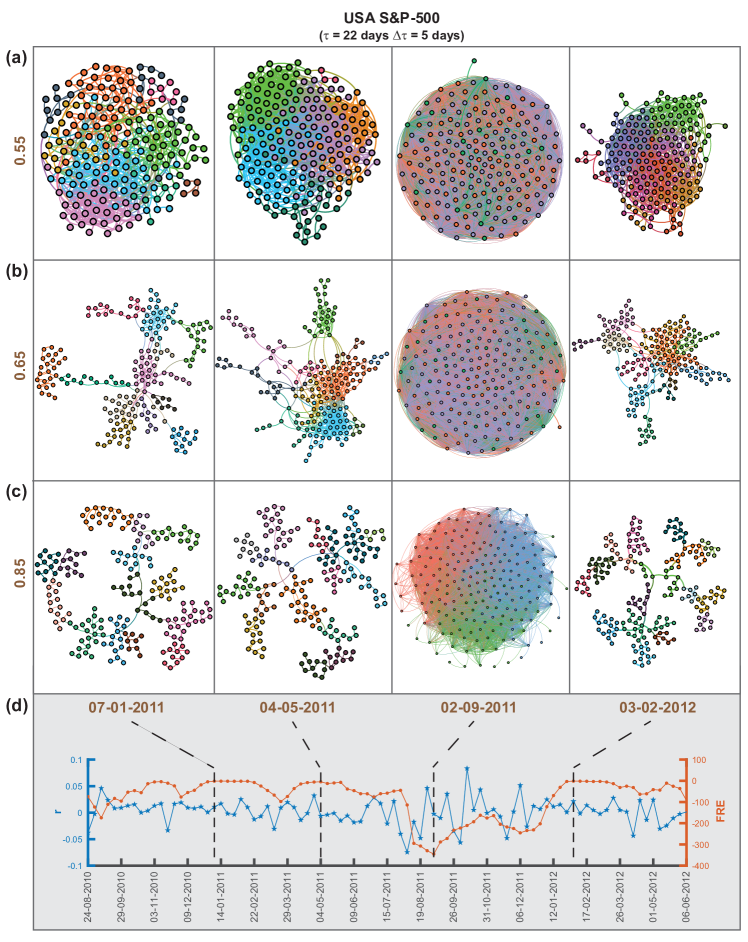

Figure 2 shows the comparisons of threshold networks, as well as the behaviour of index log-returns and average FR curvature of edges (FRE), for (a) bubble and (b) crash periods, of the USA S&P-500 market. The upper panel of Figure 2(a) shows the threshold networks near the US Housing bubble period (2006-2007) at four distinct epochs of days ending on trading days equal to 23-01-2006, 10-05-2006, 29-06-2006 and 06-11-2006, with threshold . Number of edges and communities in these four threshold networks are and , respectively. The colour of the nodes correspond to the different communities determined by Louvain method Blondel et al. (2008) for community detection. The plots of log-returns of S&P-500 index (blue color line) and FRE (sienna color line) around the US Housing bubble period are shown in the lower panel of Figure 2(a). Threshold networks show higher number () of edges and lower number () of communities for high (negative) values of FRE, but there is not much variation of . In ESM Figure S5, we show that the FRE captures the same features for three other thresholds , , and , and the numbers of edges and communities for each threshold is listed in ESM Table S3. The measure FRE is sensitive to both local (sectoral) and global (market) fluctuations, and shows a local minimum during bubble. Note that during a bubble, only a few sectors of the market perform well compared to the others (the stocks within the well-performing sectors are highly correlated, but the inter-sectoral correlations are low). It is hard to identify bubble by only monitoring the market index as the returns do not show much volatility. Figure 2(b) shows the same for the period around the August 2011 stock markets fall at four distinct epochs of days ending on trading days equal to 07-01-2011, 04-05-2011, 02-09-2011 and 03-02-2012, with threshold . Number of edges and communities in these four threshold networks are and , respectively. During the crash, the threshold network shows sufficiently higher number of edges and extremely low number of communities. In ESM Figure S6, we show that the FRE captures the same features for three other thresholds , , and , and the numbers of edges and communities for each threshold is listed in ESM Table S3. The plots of log-returns of S&P-500 index (blue color line) and FRE (sienna color line) are shown around the August 2011 stock markets fall period in the lower panel of Figure 2(b). Note that during a market crash displays high volatility and FRE shows a significant decrease (local minimum). Earlier Sandhu et al. Sandhu et al. (2016) had focussed on OR curvature as an indicator of crashes. Here, we additionally show that discrete Ricci curvatures, especially FR curvature, are sensitive and can detect both crash (market volatility high) and bubble (market volatility low).

It is often difficult to gauge the state of the market by simply monitoring the market index or its log-returns. There exist no simple definitions of a market crash or a market bubble. The market becomes extremely correlated and volatile during a crash, but a bubble is even harder to detect as the volatility is relatively low and only certain sectors perform very well (stocks show high correlation) but the rest of the market behaves like normal or ‘business-as-usual’. Traditionally, the volatility of the market captures the ‘fear’ and the evaluated risk captures the ‘fragility’ of the market. Some of us showed in our earlier papers that the mean market correlation and the spectral properties of the cross-correlation matrices can be used to study the market states Pharasi et al. (2018) and identify the precursors of market instabilities Chakraborti et al. (2020a). A goal of this study is to show that the state of the market can be continuously monitored with certain network-based measures. Thus, we next performed a comparative investigation of several network measures, especially, the four discrete notions of Ricci curvature.

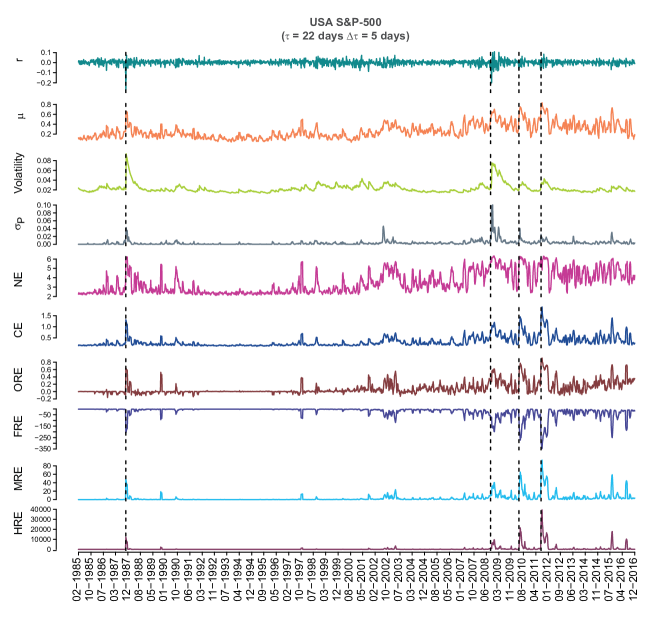

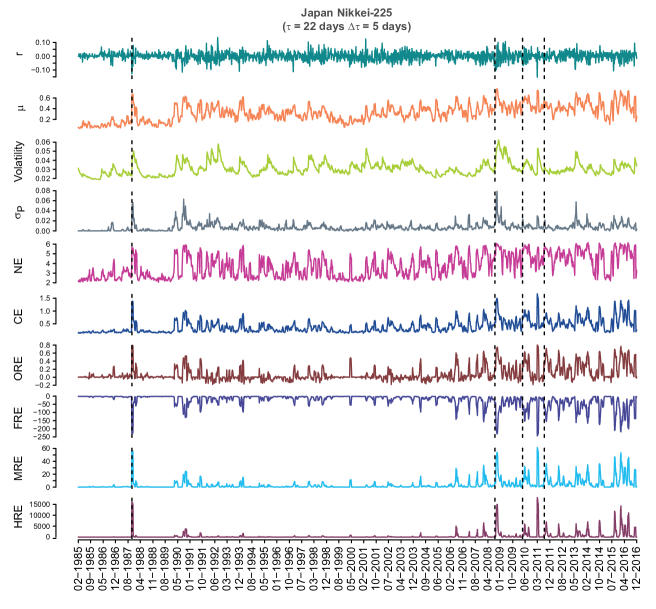

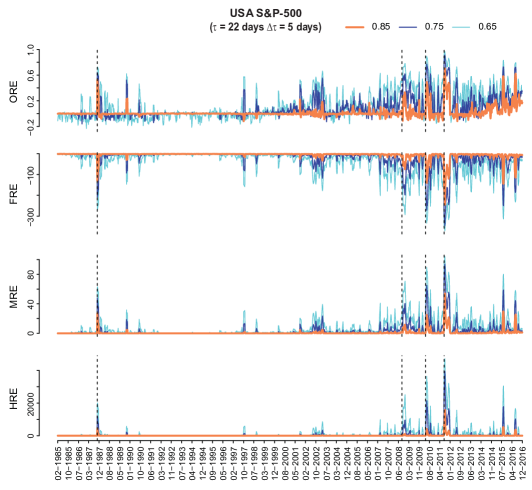

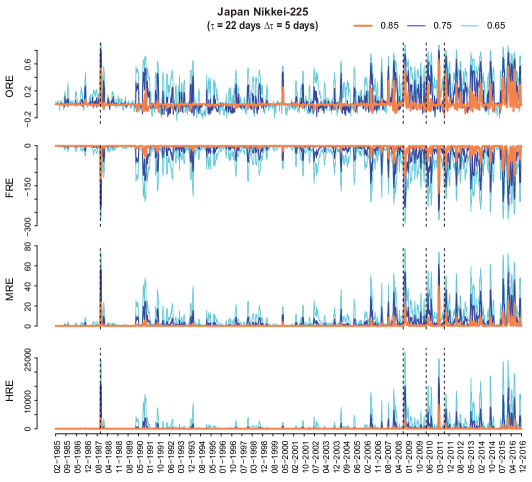

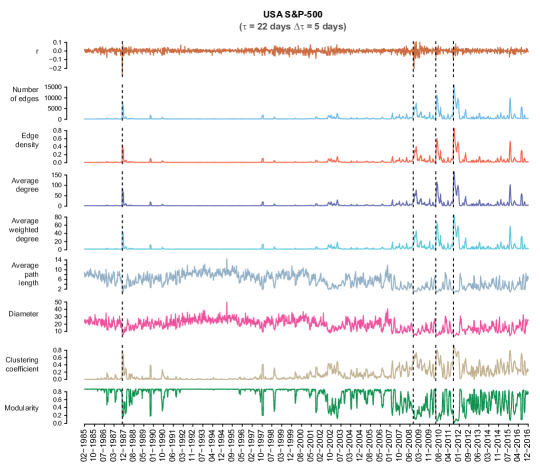

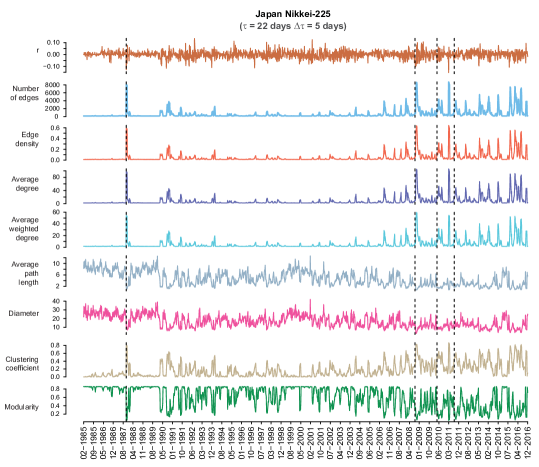

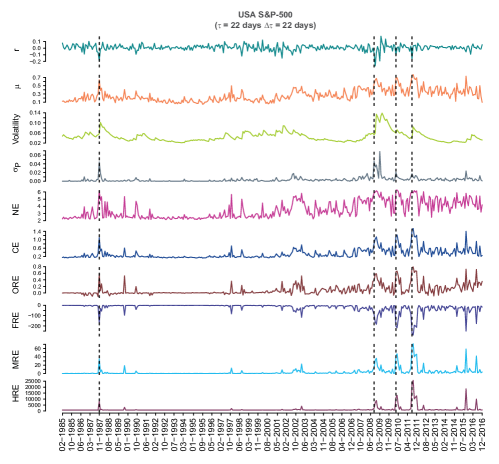

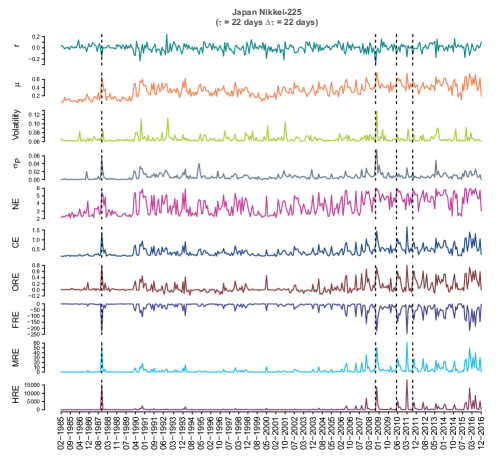

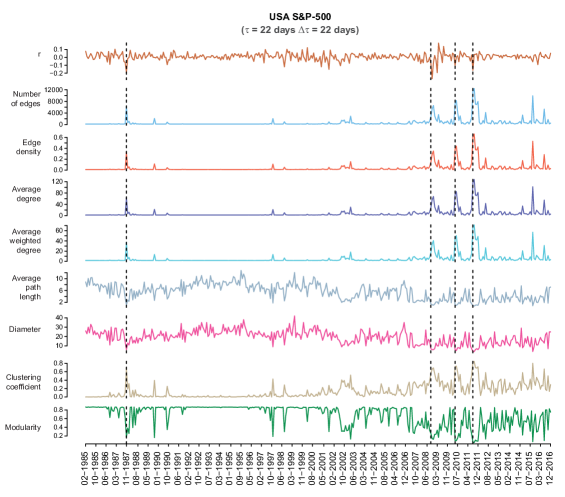

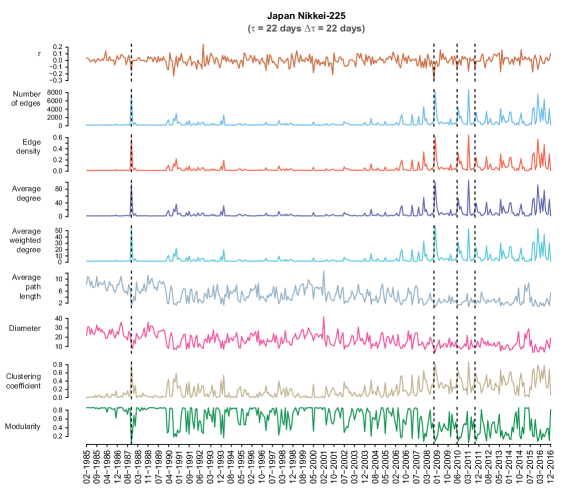

Figures 3 and 4 show for USA S&P-500 market and Japanese Nikkei-225 market, respectively, the temporal evolution of the market indicators and network measures, mainly edge-centric Ricci curvatures computed from the correlation matrices of epoch size days and overlapping shift of days, over a 32-year period (1985-2016). From top to bottom, the plots represent index log-returns , mean market correlation , volatility of the market index estimated using GARCH(1,1) process, risk corresponding to the minimum risk Markowitz portfolio of all the stocks in the market, network entropy (NP), communication efficiency (CE), average of OR, FR, MR and HR curvature of edges. We find that the four Ricci-type curvatures, namely, ORE, FRE, MRE and HRE, along with the other important indicators of the markets, viz., the log-returns , volatility, minimum risk and mean market correlation , are excellent indicators of market instabilities (bubbles and crashes). We highlight that the four discrete Ricci curvatures can capture important crashes and bubbles listed in Table 1 in the two markets during the 32-year period studied here.

In ESM Figure S7, we show the temporal evolution of the four discrete Ricci curvatures computed in threshold networks obtained using three different thresholds, (cyan color), (dark blue color) and (sienna color), for the two markets. It is seen that the absolute value of ORE, FRE, MRE and HRE decreases with the increase in the threshold used to construct . Regardless of the three thresholds used to construct the threshold networks , we show that the four discrete Ricci curvatures are fine indicators of market instabilities.

In previous work, Sandhu et al. Sandhu et al. (2016) had contrasted the temporal evolution of ORE in threshold networks for USA S&P-500 market with NE, graph diameter and average shortest path length. Here, we have studied the temporal evolution of a larger set of network measures in threshold networks for USA S&P-500 and Japanese Nikkei-225 markets computed from the correlation matrices of epoch size days and overlapping shift of days, over a 32-year period (1985-2016). From Figures 3 and 4, it is seen that NE and CE are also excellent indicators of market instabilities. In fact, we find that common network measures such as number of edges, edge density, average degree, average shortest path length, graph diameter, average clustering coefficient and modularity are also good indicators of market instabilities (ESM Figure S8).

In ESM Figures S9 and S10, we show the temporal evolution of the market indicators and several network measures (including edge-centric Ricci curvatures) computed from the correlation matrices of epoch size days and non-overlapping shift of days, over a 32-year period (1985-2016) in the two markets. It can be seen that our results are also not dependent on the choice of overlapping or non-overlapping shift used to construct the cross-correlation matrices and threshold networks.

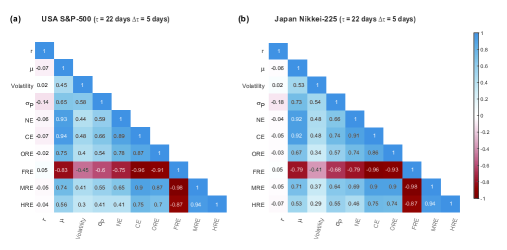

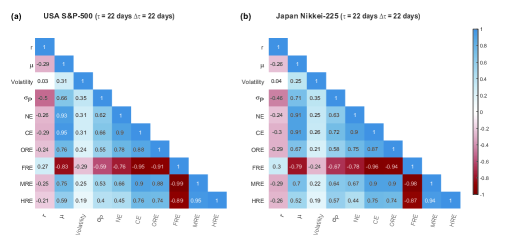

Figure 5 shows the correlogram plots of (a) USA S&P-500 and (b) Japanese Nikkei-225 markets, for the traditional market indicators (index returns , mean market correlation , volatility, and minimum portfolio risk ), network properties (NE and CE) and discrete Ricci curvatures (ORE, FRE, MRE and HRE), computed for epoch size days and overlapping shift of days. In ESM Figure S11, we show the correlogram plots for the traditional market indicators and network properties including discrete Ricci curvatures computed for epoch size days and non-overlapping shift of days in the two markets. Notably, FRE shows the highest correlation among the four discrete Ricci curvatures with the four traditional market indicators in the two markets, and thus, FRE is an excellent indicator for market risk that captures local to global system-level fragility of the markets. Furthermore, both NE and CE also have high correlation with the four traditional market indicators. Therefore, these measures can be used to monitor the health of the financial system and forecast market crashes or downturns. Overall, we show that FRE is a simple yet powerful tool for capturing the correlation structure of a dynamically changing network.

| Serial number | Major crashes and bubbles | Period | Affected region |

|---|---|---|---|

| 1 | Black Monday | 19-10-1987 | USA, Japan |

| 2 | Friday the mini crash | 13-10-1989 | USA |

| 3 | Early 90s recession | 1990 | USA |

| 4 | Mini crash due to Asian financial crisis | 27-10-1997 | USA |

| 5 | Lost decade | 2001-2010 | Japan |

| 6 | 9/11 financial crisis | 11-09-2001 | USA, Japan |

| 7 | Stock market downturn of 2002 | 09-10-2002 | USA, Japan |

| 8 | US Housing bubble | 2005-2007 | USA |

| 9 | Lehman Brothers crash | 16-09-2008 | USA, Japan |

| 10 | Dow Jones (DJ) Flash crash | 06-05-2010 | USA, Japan |

| 11 | Tsunami and Fukushima disaster | 11-03-2011 | Japan |

| 12 | August 2011 stock markets fall | 08-08-2011 | USA, Japan |

| 13 | Chinese Black Monday and 2015-2016 sell off | 24-08-2015 | USA |

5 Conclusion

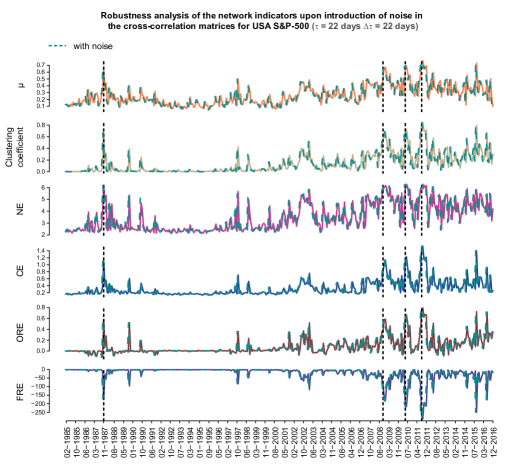

In this paper, we have employed geometry-inspired network curvature measures to characterize the correlation structures of the financial systems and used them as generic indicators for detecting market instabilities (bubbles and crashes). We reiterate here that it is often difficult to gauge the state of the market by simply monitoring the market index or its log-returns. There exist no simple definitions of a market crash or a market bubble. The market becomes extremely correlated and volatile during a crash, but a bubble is even harder to detect as the volatility is relatively low and only certain sectors perform very well (stocks show high correlation) but the rest of the market behaves like normal or ‘business-as-usual’. We have examined the daily returns from a set of stocks comprising the USA S&P-500 and the Japanese Nikkei-225 over a 32-year period, and monitored the changes in the edge-centric geometric curvatures. Our results are very robust as we have studied two very different markets, and for a very long period of 32 years with several interesting market events (bubbles and crashes; see Table 1). We showed that the results are not very sensitive to the choice of overlapping or non-overlapping windows used to construct the cross-correlation matrices and threshold networks (Figures 3-4; ESM Figures S8-S10). Further, the choice of the thresholds for constructing networks also has little influence on their behaviour as indicators (ESM Figures S5-S7). In addition, to test the robustness of our methodology in the current paper, we have added small amounts of Gaussian noise to the empirical correlation matrices for the USA S&P-500 market, and reproduced the evolution of the topological properties as well as the geometric curvature measures over the 32-year period. Specifically, we have found that the results are not sensitive to small amounts of noise or random reshuffling of data (ESM Figure S12). We found that the four different notions of discrete Ricci curvature captured well the system-level features of the market and hence we were able to distinguish between the normal or ‘business-as-usual’ periods and all the major market crises (bubbles and crashes) using the network-centric indicators. Our studies confirmed that during a normal period the market is very modular and heterogeneous, whereas during an instability (crisis) the market is more homogeneous, highly connected and less modular.

Interestingly, our methodology picks up many peaks other than the major crashes and bubbles; these are neither spurious nor false positives. Unlike the major crashes and bubbles which are well-documented in the financial literature (or listed in internet sources, see Table 1), many of these peaks correspond to interesting events that are not well understood or recorded in the literature. In fact the financial markets are often driven by endogenous and exogenous factors. Moreover, there are often multiple reasons leading to a market crash or a bubble burst. The study and characterization of such market events, including exogenous shocks, bubble bursts, and anomalies, corresponding to such peaks has already been done in our earlier papers Pharasi et al. (2018, 2019); Chakraborti et al. (2020a, b). The findings of the present paper are in concordance with the earlier ones.

It is important to note that partial correlations can detect direct as opposed to plausibly indirect connections among components of the stock market. In the Econophysics literature (see e.g. Refs. Kenett et al. (2010); San Miguel et al. (2012); Millington and Niranjan (2020); Sharma et al. (2017); Chakraborti et al. (2020b)), researchers have used partial correlations for analyzing the dynamics and constructing networks of stock markets. Partial correlations are particularly relevant when people study eigenvalue spectra (market, group and random modes), or network centrality measures, by first filtering out the spurious correlations. However, it has been observed Millington and Niranjan (2020); Chakraborti et al. (2020b) that partial correlations are less successful in picking the cluster or group dynamics, and the networks arising from partial correlations are also less stable. In this contribution, we are more interested in the market indicators and the use of discrete Ricci curvatures as generic indicators, for which we prefer to work with the more stable correlation matrices.

Also, we find from these geometric measures that there are succinct and inherent differences in the two markets, USA S&P-500 and Japan Nikkei-225. Importantly, among four Ricci-type curvature measures, the Forman-Ricci curvature of edges (FRE) correlates highest with the traditional market indicators and acts as an excellent indicator for the system-level fear (volatility) and fragility (risk) for both the markets. These new insights may help us in future to better understand tipping points, systemic risk, and resilience in financial networks, and enable us to develop monitoring tools required for the highly interconnected financial systems and perhaps forecast future financial crises and market slowdowns. These can be further generalized to study other economic systems, and may thus enable us to understand the highly complex and interconnected economic-financial systems.

Author contributions

A.S. and A.C. designed research; A.S., H.K.P., S.J.R., H.K., E.S., J.J. and A.C. performed research and analyzed data; A.S., H.K.P. and S.J.R. prepared the figures; A.S. and A.C. supervised the research; A.S., E.S., J.J. and A.C. wrote the manuscript with input from the other authors. All authors have read and approved the manuscript.

Acknowledgement

A.S. acknowledges financial support from Max Planck Society Germany through the award of a Max Planck Partner Group in Mathematical Biology. E.S. and J.J. acknowledge support from the German-Israeli Foundation (GIF) Grant I-1514-304.6/2019. H.K.P. is grateful for financial support provided by UNAM-DGAPA and CONACYT Proyecto Fronteras 952. A.C. and H.K.P. acknowledge support from the projects UNAM-DGAPA-PAPIIT AG100819 and IN113620, and CONACyT Project Fronteras 201.

Data Availability

All data used are openly available for download on the websites of the relevant sources mentioned in the text and stated in the references section. All relevant data and codes for this study have been uploaded and made publicly available via the GitHub repository: https://github.com/asamallab/StockMarkNetIndicator.

Correspondence to: Areejit Samal (asamal@imsc.res.in ) or Anirban Chakraborti (anirban@jnu.ac.in)

References

- Anderson (1972) P. W. Anderson, Science 177, 393 (1972).

- Vemuri (1978) V. Vemuri, Modeling of Complex Systems: An Introduction (Academic Press, New York, 1978).

- Gell-Mann (1995) M. Gell-Mann, Complexity 1, 16 (1995).

- Mantegna and Stanley (2007) R. N. Mantegna and H. E. Stanley, An introduction to econophysics: correlations and complexity in finance (Cambridge University Press, Cambridge, 2007).

- Bouchaud and Potters (2003) J.-P. Bouchaud and M. Potters, Theory of Financial Risk and Derivative Pricing: from Statistical Physics to Risk Management (Cambridge University Press, 2003).

- Sinha et al. (2010) S. Sinha, A. Chatterjee, A. Chakraborti, and B. K. Chakrabarti, Econophysics: an introduction (John Wiley & Sons, 2010).

- Chakraborti et al. (2011) A. Chakraborti, I. Muni Toke, M. Patriarca, and F. Abergel, Quantitative Finance 11, 991 (2011).

- Chakraborti et al. (2015) A. Chakraborti, D. Challet, A. Chatterjee, M. Marsili, Y.-C. Zhang, and B. K. Chakrabarti, Physics Reports 552, 1 (2015).

- Battiston et al. (2016) S. Battiston, J. D. Farmer, A. Flache, D. Garlaschelli, A. G. Haldane, H. Heesterbeek, C. Hommes, C. Jaeger, R. May, and M. Scheffer, Science 351, 818 (2016).

- Lux and Westerhoff (2009) T. Lux and F. Westerhoff, Nature Physics 5, 2 (2009).

- Mantegna (1999a) R. N. Mantegna, Computer Physics Communications 121-122, 153 (1999a).

- Mantegna (1999b) R. N. Mantegna, The European Physical Journal B 11, 193 (1999b).

- Laloux et al. (1999) L. Laloux, P. Cizeau, J.-P. Bouchaud, and M. Potters, Physical Review Letters 83, 1467 (1999).

- Plerou et al. (1999) V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. Nunes Amaral, and H. E. Stanley, Physical Review Letters 83, 1471 (1999).

- Gopikrishnan et al. (2001) P. Gopikrishnan, B. Rosenow, V. Plerou, and H. E. Stanley, Physical Review E 64, 035106 (2001).

- Kullmann et al. (2002) L. Kullmann, J. Kertész, and K. Kaski, Physical Review E 66, 026125 (2002).

- Plerou et al. (2002) V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. N. Amaral, T. Guhr, and H. E. Stanley, Physical Review E 65, 066126 (2002).

- Onnela et al. (2003) J.-P. Onnela, A. Chakraborti, K. Kaski, J. Kertesz, and A. Kanto, Physical Review E 68, 056110 (2003).

- Tumminello et al. (2005) M. Tumminello, T. Aste, T. Di Matteo, and R. N. Mantegna, Proceedings of the National Academy of Sciences 102, 10421 (2005).

- Pharasi et al. (2018) H. K. Pharasi, K. Sharma, R. Chatterjee, A. Chakraborti, F. Leyvraz, and T. H. Seligman, New Journal of Physics 20, 103041 (2018).

- Pharasi et al. (2019) H. K. Pharasi, K. Sharma, A. Chakraborti, and T. H. Seligman, “Complex market dynamics in the light of random matrix theory,” in New Perspectives and Challenges in Econophysics and Sociophysics, edited by F. Abergel, B. K. Chakrabarti, A. Chakraborti, N. Deo, and K. Sharma (Springer International Publishing, Cham, 2019) pp. 13–34.

- Chakraborti et al. (2020a) A. Chakraborti, K. Sharma, H. K. Pharasi, K. Shuvo Bakar, S. Das, and T. H. Seligman, New Journal of Physics 22, 063043 (2020a).

- Chi et al. (2010) K. T. Chi, J. Liu, and F. C. Lau, Journal of Empirical Finance 17, 659 (2010).

- Tumminello et al. (2007) M. Tumminello, T. Di Matteo, T. Aste, and R. N. Mantegna, The European Physical Journal B 55, 209 (2007).

- Tumminello et al. (2010) M. Tumminello, F. Lillo, and R. N. Mantegna, Journal of economic behavior & organization 75, 40 (2010).

- Miccichè et al. (2003) S. Miccichè, G. Bonanno, F. Lillo, and R. N. Mantegna, Physica A: Statistical Mechanics and its Applications 324, 66 (2003).

- Kumar and Deo (2012) S. Kumar and N. Deo, Physical Review E 86, 026101 (2012).

- Almog and Shmueli (2019) A. Almog and E. Shmueli, Scientific Reports 9, 10832 (2019).

- Wang et al. (2019) J. Wang, C. Lin, and Y. Wang, Complexity 2019, 1817248 (2019).

- Chakraborti et al. (2020b) A. Chakraborti, Hrishidev, K. Sharma, and H. K. Pharasi, Journal of Physics: Complexity 2, 015002 (2020b).

- Kukreti et al. (2020) V. Kukreti, H. K. Pharasi, P. Gupta, and S. Kumar, Frontiers in Physics 8, 323 (2020).

- Nie and Song (2018) C.-x. Nie and F.-t. Song, Entropy 20, 177 (2018).

- Stepanov et al. (2015) Y. Stepanov, P. Rinn, T. Guhr, J. Peinke, and R. Schäfer, Journal of Statistical Mechanics: Theory and Experiment 2015, P08011 (2015).

- Rinn et al. (2015) P. Rinn, Y. Stepanov, J. Peinke, T. Guhr, and R. Schäfer, EPL 110, 68003 (2015).

- Chetalova et al. (2015) D. Chetalova, R. Schäfer, and T. Guhr, Journal of Statistical Mechanics: Theory and Experiment 2015, P01029 (2015).

- Heckens et al. (2020) A. J. Heckens, S. M. Krause, and T. Guhr, Journal of Statistical Mechanics: Theory and Experiment 2020, P103402 (2020).

- Wang et al. (2020) S. Wang, S. Gartzke, M. Schreckenberg, and T. Guhr, Journal of Statistical Mechanics: Theory and Experiment 2020, P103404 (2020).

- Jost (2017) J. Jost, Riemannian Geometry and Geometric Analysis, 7th ed. (Springer International Publishing, 2017).

- Carlsson (2009) G. Carlsson, Bulletin of the American Mathematical Society 46, 255 (2009).

- Krioukov et al. (2010) D. Krioukov, F. Papadopoulos, M. Kitsak, A. Vahdat, and M. Boguná, Physical Review E 82, 036106 (2010).

- Bianconi (2015) G. Bianconi, EPL 111, 56001 (2015).

- Sandhu et al. (2015) R. Sandhu, T. Georgiou, E. Reznik, L. Zhu, I. Kolesov, Y. Senbabaoglu, and A. Tannenbaum, Scientific Reports 5, 12323 (2015).

- Sreejith et al. (2016) R. P. Sreejith, K. Mohanraj, J. Jost, E. Saucan, and A. Samal, Journal of Statistical Mechanics: Theory and Experiment 2016, P063206 (2016).

- Bianconi and Rahmede (2017) G. Bianconi and C. Rahmede, Scientific Reports 7, 41974 (2017).

- Kartun-Giles and Bianconi (2019) A. P. Kartun-Giles and G. Bianconi, Chaos, Solitons & Fractals: X 1, 100004 (2019).

- Iacopini et al. (2019) I. Iacopini, G. Petri, A. Barrat, and V. Latora, Nature communications 10, 2485 (2019).

- Kannan et al. (2019) H. Kannan, E. Saucan, I. Roy, and A. Samal, Scientific reports 9, 13817 (2019).

- Samal et al. (2018) A. Samal, R. P. Sreejith, J. Gu, S. Liu, E. Saucan, and J. Jost, Scientific Reports 8, 8650 (2018).

- Ni et al. (2015) C. Ni, Y. Lin, J. Gao, X. D. Gu, and E. Saucan, in 2015 IEEE Conference on Computer Communications (INFOCOM) (IEEE, 2015) pp. 2758–2766.

- Sandhu et al. (2016) R. S. Sandhu, T. T. Georgiou, and A. R. Tannenbaum, Science Advances 2, e1501495 (2016).

- Ni et al. (2019) C. Ni, Y. Lin, F. Luo, and J. Gao, Scientific Reports 9, 9984 (2019).

- Ollivier (2007) Y. Ollivier, Comptes Rendus Mathematique 345, 643 (2007).

- Ollivier (2009) Y. Ollivier, Journal of Functional Analysis 256, 810 (2009).

- Aste et al. (2005) T. Aste, T. Di Matteo, and S. Hyde, Physica A: Statistical Mechanics and its Applications 346, 20 (2005).

- Saucan et al. (2020) E. Saucan, A. Samal, and J. Jost, Network Science , 1 (2020).

- Saucan (2012) E. Saucan, Journal of Mathematical Imaging and Vision 43, 143 (2012).

- Scheffer et al. (2012) M. Scheffer, S. R. Carpenter, T. M. Lenton, J. Bascompte, W. Brock, V. Dakos, J. van de Koppel, I. A. van de Leemput, S. A. Levin, E. H. van Nes, M. Pascual, and J. Vandermeer, Science 338, 344 (2012).

- Lin and Yau (2010) Y. Lin and S.-T. Yau, Math. Res. Lett. 17, 343 (2010).

- Lin et al. (2011) Y. Lin, L. Lu, and S.-T. Yau, Tohoku Mathematical Journal 63, 605 (2011).

- Bauer et al. (2012) F. Bauer, J. Jost, and S. Liu, Math. Res. Lett. 19, 1185 (2012).

- Jost and Liu (2014) J. Jost and S. Liu, Discrete & Computational Geometry 51, 300 (2014).

- Sia et al. (2019) J. Sia, E. Jonckheere, and P. Bogdan, Scientific Reports 9, 9800 (2019).

- Vaserstein (1969) L. N. Vaserstein, Probl. Peredachi Inf. 5, 64 (1969).

- Forman (2003) R. Forman, Discrete & Computational Geometry 29, 323 (2003).

- Saucan et al. (2019a) E. Saucan, R. P. Sreejith, R. P. Vivek-Ananth, J. Jost, and A. Samal, Chaos, Solitons & Fractals 118, 347 (2019a).

- Sreejith et al. (2017) R. P. Sreejith, J. Jost, E. Saucan, and A. Samal, Chaos, Solitons & Fractals 101, 50 (2017).

- Menger (1930) K. Menger, Mathematische Annalen 103, 466 (1930).

- Saucan et al. (2019b) E. Saucan, A. Samal, and J. Jost, in International Conference on Complex Networks and their Applications (Springer, 2019) pp. 943–954.

- Haantjes (1947) J. Haantjes, Proc. Kon. Ned. Akad. v. Wetenseh., Amsterdam 50, 302 (1947).

- (70) “Yahoo finance database,” https://finance.yahoo.co.jp/, accessed on 7th July, 2017.

- Prim (1957) R. C. Prim, The Bell System Technical Journal 36, 1389 (1957).

- Latora and Marchiori (2001) V. Latora and M. Marchiori, Physical Review Letters 87, 198701 (2001).

- Girvan and Newman (2002) M. Girvan and M. E. J. Newman, Proceedings of the National Academy of Sciences USA 99, 7821 (2002).

- Blondel et al. (2008) V. D. Blondel, J.-L. Guillaume, R. Lambiotte, and E. Lefebvre, Journal of Statistical Mechanics: Theory and Experiment 2008, P10008 (2008).

- Solé and Valverde (2004) R. V. Solé and S. Valverde, in Complex Networks (Springer, 2004) pp. 189–207.

- Hagberg et al. (2008) A. Hagberg, P. Swart, and D. S. Chult, Exploring network structure, dynamics, and function using NetworkX, Tech. Rep. (Los Alamos National Laboratory (LANL), Los Alamos, NM (United States), 2008).

- Bollerslev (1986) T. Bollerslev, Journal of Econometrics 31, 307 (1986).

- Cra (a) “List of stock market crashes and bear markets,” https://en.wikipedia.org/wiki/List_of_stock_market_crashes_and_bear_markets (a), accessed on 7th July, 2019.

- (79) “Bull markets,” https://bullmarkets.co/u-s-stock-market-in-1996/, accessed on 7th July, 2019.

- (80) “United states housing bubble,” https://en.wikipedia.org/wiki/United_States_housing_bubble, accessed on 7th July, 2019.

- Cra (b) “A short history of stock market crashes,” https://www.cnbc.com/2016/08/24/a-short-history-of-stock-market-crashes.html (b), accessed on 7th July, 2019.

- (82) “Stock market selloff,” https://en.wikipedia.org/wiki/2015-16_stock_market_selloff, accessed on 7th July, 2019.

- (83) “August 2011 stock markets fall,” https://en.wikipedia.org/wiki/August_2011_stock_markets_fall, accessed on 13th August, 2020.

- Kenett et al. (2010) D. Y. Kenett, M. Tumminello, A. Madi, G. Gur-Gershgoren, R. N. Mantegna, and E. Ben-Jacob, PloS One 5, e15032 (2010).

- San Miguel et al. (2012) M. San Miguel, J. H. Johnson, J. Kertesz, K. Kaski, A. Díaz-Guilera, R. S. MacKay, V. Loreto, P. Érdi, and D. Helbing, The European Physical Journal Special Topics 214, 245 (2012).

- Millington and Niranjan (2020) T. Millington and M. Niranjan, Applied Network Science 5, 1 (2020).

- Sharma et al. (2017) K. Sharma, S. Shah, A. S. Chakrabarti, and A. Chakraborti, in Economic Foundations for Social Complexity Science (Springer, 2017) pp. 211–238.

Electronic Supplementary Material (ESM)

(a)

(b)

(a)

(b)

(a)

(b)

(a)

(b)

(b)

| S.No. | Code | Company Name | Sector | Abbreviation |

| 1 | CMCSA | Comcast Corp. | Consumer Discretionary | CD |

| 2 | DIS | The Walt Disney Company | Consumer Discretionary | CD |

| 3 | F | Ford Motor | Consumer Discretionary | CD |

| 4 | GPC | Genuine Parts | Consumer Discretionary | CD |

| 5 | GPS | Gap Inc. | Consumer Discretionary | CD |

| 6 | GT | Goodyear Tire & Rubber | Consumer Discretionary | CD |

| 7 | HAS | Hasbro Inc. | Consumer Discretionary | CD |

| 8 | HD | Home Depot | Consumer Discretionary | CD |

| 9 | HRB | Block H&R | Consumer Discretionary | CD |

| 10 | IPG | Interpublic Group | Consumer Discretionary | CD |

| 11 | JCP | J. C. Penney Company, Inc. | Consumer Discretionary | CD |

| 12 | JWN | Nordstrom | Consumer Discretionary | CD |

| 13 | LEG | Leggett & Platt | Consumer Discretionary | CD |

| 14 | LEN | Lennar Corp. | Consumer Discretionary | CD |

| 15 | LOW | Lowe’s Cos. | Consumer Discretionary | CD |

| 16 | MAT | Mattel Inc. | Consumer Discretionary | CD |

| 17 | MCD | McDonald’s Corp. | Consumer Discretionary | CD |

| 18 | NKE | Nike | Consumer Discretionary | CD |

| 19 | SHW | Sherwin-Williams | Consumer Discretionary | CD |

| 20 | TGT | Target Corp. | Consumer Discretionary | CD |

| 21 | VFC | V.F. Corp. | Consumer Discretionary | CD |

| 22 | WHR | Whirlpool Corp. | Consumer Discretionary | CD |

| 23 | ADM | Archer-Daniels-Midland Co | Consumer Staples | CS |

| 24 | AVP | Avon Products, Inc. | Consumer Staples | CS |

| 25 | CAG | Conagra Brands | Consumer Staples | CS |

| 26 | CL | Colgate-Palmolive | Consumer Staples | CS |

| 27 | CPB | Campbell Soup | Consumer Staples | CS |

| 28 | CVS | CVS Health | Consumer Staples | CS |

| 29 | GIS | General Mills | Consumer Staples | CS |

| 30 | HRL | Hormel Foods Corp. | Consumer Staples | CS |

| 31 | HSY | The Hershey Company | Consumer Staples | CS |

| 32 | K | Kellogg Co. | Consumer Staples | CS |

| 33 | KMB | Kimberly-Clark | Consumer Staples | CS |

| 34 | KO | Coca-Cola Company (The) | Consumer Staples | CS |

| 35 | KR | Kroger Co. | Consumer Staples | CS |

| 36 | MKC | McCormick & Co. | Consumer Staples | CS |

| 37 | MO | Altria Group Inc | Consumer Staples | CS |

| 38 | SYY | Sysco Corp. | Consumer Staples | CS |

| 39 | TAP | Molson Coors Brewing Company | Consumer Staples | CS |

| 40 | TSN | Tyson Foods | Consumer Staples | CS |

| 41 | WMT | Wal-Mart Stores | Consumer Staples | CS |

| 42 | APA | Apache Corporation | Energy | EG |

| 43 | COP | ConocoPhillips | Energy | EG |

| 44 | CVX | Chevron Corp. | Energy | EG |

| 45 | ESV | Ensco plc | Energy | EG |

| 46 | HAL | Halliburton Co. | Energy | EG |

| 47 | HES | Hess Corporation | Energy | EG |

| 48 | HP | Helmerich & Payne | Energy | EG |

| 49 | MRO | Marathon Oil Corp. | Energy | EG |

| 50 | MUR | Murphy Oil Corporation | Energy | EG |

| 51 | NBL | Noble Energy Inc | Energy | EG |

| 52 | NBR | Nabors Industries Ltd. | Energy | EG |

| 53 | SLB | Schlumberger Ltd. | Energy | EG |

| 54 | TSO | Tesoro Corp | Energy | EG |

| 55 | VLO | Valero Energy | Energy | EG |

| 56 | WMB | Williams Cos. | Energy | EG |

| 57 | XOM | Exxon Mobil Corp. | Energy | EG |

| 58 | AFL | AFLAC Inc | Financials | FN |

| 59 | AIG | American International Group, Inc. | Financials | FN |

| 60 | AON | Aon plc | Financials | FN |

| 61 | AXP | American Express Co | Financials | FN |

| 62 | BAC | Bank of America Corp | Financials | FN |

| 63 | BBT | BB&T Corporation | Financials | FN |

| 64 | BEN | Franklin Resources | Financials | FN |

| 65 | BK | The Bank of New York Mellon Corp. | Financials | FN |

| 66 | C | Citigroup Inc. | Financials | FN |

| 67 | CB | Chubb Limited | Financials | FN |

| 68 | CINF | Cincinnati Financial | Financials | FN |

| 69 | CMA | Comerica Inc. | Financials | FN |

| 70 | EFX | Equifax Inc. | Financials | FN |

| 71 | FHN | First Horizon National Corporation | Financials | FN |

| 72 | HBAN | Huntington Bancshares | Financials | FN |

| 73 | HCN | Welltower Inc. | Financials | FN |

| 74 | HST | Host Hotels & Resorts, Inc. | Financials | FN |

| 75 | JPM | JPMorgan Chase & Co. | Financials | FN |

| 76 | L | Loews Corp. | Financials | FN |

| 77 | LM | Legg Mason, Inc. | Financials | FN |

| 78 | LNC | Lincoln National | Financials | FN |

| 79 | LUK | Leucadia National Corp. | Financials | FN |

| 80 | MMC | Marsh & McLennan | Financials | FN |

| 81 | MTB | M&T Bank Corp. | Financials | FN |

| 82 | PSA | Public Storage | Financials | FN |

| 83 | SLM | SLM Corporation | Financials | FN |

| 84 | TMK | Torchmark Corp. | Financials | FN |

| 85 | TRV | The Travelers Companies Inc. | Financials | FN |

| 86 | USB | U.S. Bancorp | Financials | FN |

| 87 | VNO | Vornado Realty Trust | Financials | FN |

| 88 | WFC | Wells Fargo | Financials | FN |

| 89 | WY | Weyerhaeuser Corp. | Financials | FN |

| 90 | ZION | Zions Bancorp | Financials | FN |

| 91 | ABT | Abbott Laboratories | Health Care | HC |

| 92 | AET | Aetna Inc | Health Care | HC |

| 93 | AMGN | Amgen Inc | Health Care | HC |

| 94 | BAX | Baxter International Inc. | Health Care | HC |

| 95 | BCR | Bard (C.R.) Inc. | Health Care | HC |

| 96 | BDX | Becton Dickinson | Health Care | HC |

| 97 | BMY | Bristol-Myers Squibb | Health Care | HC |

| 98 | CAH | Cardinal Health Inc. | Health Care | HC |

| 99 | CI | CIGNA Corp. | Health Care | HC |

| 100 | HUM | Humana Inc. | Health Care | HC |

| 101 | JNJ | Johnson & Johnson | Health Care | HC |

| 102 | LLY | Lilly (Eli) & Co. | Health Care | HC |

| 103 | MDT | Medtronic plc | Health Care | HC |

| 104 | MRK | Merck & Co. | Health Care | HC |

| 105 | MYL | Mylan N.V. | Health Care | HC |

| 106 | SYK | Stryker Corp. | Health Care | HC |

| 107 | THC | Tenet Healthcare Corp | Health Care | HC |

| 108 | TMO | Thermo Fisher Scientific | Health Care | HC |

| 109 | UNH | United Health Group Inc. | Health Care | HC |

| 110 | VAR | Varian Medical Systems | Health Care | HC |

| 111 | AVY | Avery Dennison Corp | Industrials | ID |

| 112 | BA | Boeing Company | Industrials | ID |

| 113 | CAT | Caterpillar Inc. | Industrials | ID |

| 114 | CMI | Cummins Inc. | Industrials | ID |

| 115 | CSX | CSX Corp. | Industrials | ID |

| 116 | CTAS | Cintas Corporation | Industrials | ID |

| 117 | DE | Deere & Co. | Industrials | ID |

| 118 | DHR | Danaher Corp. | Industrials | ID |

| 119 | DNB | The Dun & Bradstreet Corporation | Industrials | ID |

| 120 | DOV | Dover Corp. | Industrials | ID |

| 121 | EMR | Emerson Electric Company | Industrials | ID |

| 122 | ETN | Eaton Corporation | Industrials | ID |

| 123 | EXPD | Expeditors International | Industrials | ID |

| 124 | FDX | FedEx Corporation | Industrials | ID |

| 125 | FLS | Flowserve Corporation | Industrials | ID |

| 126 | GD | General Dynamics | Industrials | ID |

| 127 | GE | General Electric | Industrials | ID |

| 128 | GLW | Corning Inc. | Industrials | ID |

| 129 | GWW | Grainger (W.W.) Inc. | Industrials | ID |

| 130 | HON | Honeywell Int’l Inc. | Industrials | ID |

| 131 | IR | Ingersoll-Rand PLC | Industrials | ID |

| 132 | ITW | Illinois Tool Works | Industrials | ID |

| 133 | JEC | Jacobs Engineering Group | Industrials | ID |

| 134 | LMT | Lockheed Martin Corp. | Industrials | ID |

| 135 | LUV | Southwest Airlines | Industrials | ID |

| 136 | MAS | Masco Corp. | Industrials | ID |

| 137 | MMM | 3M Company | Industrials | ID |

| 138 | ROK | Rockwell Automation Inc. | Industrials | ID |

| 139 | RTN | Raytheon Co. | Industrials | ID |

| 140 | TXT | Textron Inc. | Industrials | ID |

| 141 | UNP | Union Pacific | Industrials | ID |

| 142 | UTX | United Technologies | Industrials | ID |

| 143 | AAPL | Apple Inc. | Information Technology | IT |

| 144 | ADI | Analog Devices, Inc. | Information Technology | IT |

| 145 | ADP | Automatic Data Processing | Information Technology | IT |

| 146 | AMAT | Applied Materials Inc | Information Technology | IT |

| 147 | AMD | Advanced Micro Devices Inc | Information Technology | IT |

| 148 | CA | CA, Inc. | Information Technology | IT |

| 149 | HPQ | HP Inc. | Information Technology | IT |

| 150 | HRS | Harris Corporation | Information Technology | IT |

| 151 | IBM | International Business Machines | Information Technology | IT |

| 152 | INTC | Intel Corp. | Information Technology | IT |

| 153 | KLAC | KLA-Tencor Corp. | Information Technology | IT |

| 154 | LRCX | Lam Research | Information Technology | IT |

| 155 | MSI | Motorola Solutions Inc. | Information Technology | IT |

| 156 | MU | Micron Technology | Information Technology | IT |

| 157 | TSS | Total System Services, Inc. | Information Technology | IT |

| 158 | TXN | Texas Instruments | Information Technology | IT |

| 159 | WDC | Western Digital | Information Technology | IT |

| 160 | XRX | Xerox Corp. | Information Technology | IT |

| 161 | AA | Alcoa Corporation | Materials | MT |

| 162 | APD | Air Products & Chemicals Inc | Materials | MT |

| 163 | BLL | Ball Corp | Materials | MT |

| 164 | BMS | Bemis Company, Inc. | Materials | MT |

| 165 | CLF | Cleveland-Cliffs Inc. | Materials | MT |

| 166 | DD | DuPont | Materials | MT |

| 167 | ECL | Ecolab Inc. | Materials | MT |

| 168 | FMC | FMC Corporation | Materials | MT |

| 169 | IFF | Intl Flavors & Fragrances | Materials | MT |

| 170 | IP | International Paper | Materials | MT |

| 171 | NEM | Newmont Mining Corporation | Materials | MT |

| 172 | PPG | PPG Industries | Materials | MT |

| 173 | VMC | Vulcan Materials | Materials | MT |

| 174 | CTL | CenturyLink Inc | Telecommunication Services | TC |

| 175 | FTR | Frontier Communications Corporation | Telecommunication Services | TC |

| 176 | S | Sprint Nextel Corp. | Telecommunication Services | TC |

| 177 | T | AT&T Inc | Telecommunication Services | TC |

| 178 | VZ | Verizon Communications | Telecommunication Services | TC |

| 179 | AEP | American Electric Power | Utilities | UT |

| 180 | CMS | CMS Energy | Utilities | UT |

| 181 | CNP | CenterPoint Energy | Utilities | UT |

| 182 | D | Dominion Energy | Utilities | UT |

| 183 | DTE | DTE Energy Co. | Utilities | UT |

| 184 | ED | Consolidated Edison | Utilities | UT |

| 185 | EIX | Edison Int’l | Utilities | UT |

| 186 | EQT | EQT Corporation | Utilities | UT |

| 187 | ETR | Entergy Corp. | Utilities | UT |

| 188 | EXC | Exelon Corp. | Utilities | UT |

| 189 | NEE | NextEra Energy | Utilities | UT |

| 190 | NI | NiSource Inc. | Utilities | UT |

| 191 | PNW | Pinnacle West Capital | Utilities | UT |

| 192 | SO | Southern Co. | Utilities | UT |

| 193 | WEC | Wec Energy Group Inc | Utilities | UT |

| 194 | XEL | Xcel Energy Inc | Utilities | UT |

| S.No. | Code | Company Name | Sector | Abbreviation |

| 1 | S-8801 | MITSUI FUDOSAN CO., LTD. | Capital Goods | CG |

| 2 | S-8802 | MITSUBISHI ESTATE CO., LTD. | Capital Goods | CG |

| 3 | S-8804 | TOKYO TATEMONO CO., LTD. | Capital Goods | CG |

| 4 | S-8830 | SUMITOMO REALTY & DEVELOPMENT CO., LTD. | Capital Goods | CG |

| 5 | S-7003 | MITSUI ENG. & SHIPBUILD. CO., LTD. | Capital Goods | CG |

| 6 | S-7012 | KAWASAKI HEAVY IND., LTD. | Capital Goods | CG |

| 7 | S-9202 | ANA HOLDINGS INC. | Capital Goods | CG |

| 8 | S-1801 | TAISEI CORP. | Capital Goods | CG |

| 9 | S-1802 | OBAYASHI CORP. | Capital Goods | CG |

| 10 | S-1803 | SHIMIZU CORP. | Capital Goods | CG |

| 11 | S-1808 | HASEKO CORP. | Capital Goods | CG |

| 12 | S-1812 | KAJIMA CORP. | Capital Goods | CG |

| 13 | S-1925 | DAIWA HOUSE IND. CO., LTD. | Capital Goods | CG |

| 14 | S-1928 | SEKISUI HOUSE, LTD. | Capital Goods | CG |

| 15 | S-1963 | JGC CORP. | Capital Goods | CG |

| 16 | S-5631 | THE JAPAN STEEL WORKS, LTD. | Capital Goods | CG |

| 17 | S-6103 | OKUMA CORP. | Capital Goods | CG |

| 18 | S-6113 | AMADA HOLDINGS CO., LTD. | Capital Goods | CG |

| 19 | S-6301 | KOMATSU LTD. | Capital Goods | CG |

| 20 | S-6302 | SUMITOMO HEAVY IND., LTD. | Capital Goods | CG |

| 21 | S-6305 | HITACHI CONST. MACH. CO., LTD. | Capital Goods | CG |

| 22 | S-6326 | KUBOTA CORP. | Capital Goods | CG |

| 23 | S-6361 | EBARA CORP. | Capital Goods | CG |

| 24 | S-6366 | CHIYODA CORP. | Capital Goods | CG |

| 25 | S-6367 | DAIKIN INDUSTRIES, LTD. | Capital Goods | CG |

| 26 | S-6471 | NSK LTD. | Capital Goods | CG |

| 27 | S-6472 | NTN CORP. | Capital Goods | CG |

| 28 | S-6473 | JTEKT CORP. | Capital Goods | CG |

| 29 | S-7004 | HITACHI ZOSEN CORP. | Capital Goods | CG |

| 30 | S-7011 | MITSUBISHI HEAVY IND., LTD. | Capital Goods | CG |

| 31 | S-7013 | IHI CORP. | Capital Goods | CG |

| 32 | S-7911 | TOPPAN PRINTING CO., LTD. | Capital Goods | CG |

| 33 | S-7912 | DAI NIPPON PRINTING CO., LTD. | Capital Goods | CG |

| 34 | S-7951 | YAMAHA CORP. | Capital Goods | CG |

| 35 | S-1332 | NIPPON SUISAN KAISHA, LTD. | Consumer Goods | CN |

| 36 | S-2002 | NISSHIN SEIFUN GROUP INC. | Consumer Goods | CN |

| 37 | S-2282 | NH FOODS LTD. | Consumer Goods | CN |

| 38 | S-2501 | SAPPORO HOLDINGS LTD. | Consumer Goods | CN |

| 39 | S-2502 | ASAHI GROUP HOLDINGS, LTD. | Consumer Goods | CN |

| 40 | S-2503 | KIRIN HOLDINGS CO., LTD. | Consumer Goods | CN |

| 41 | S-2531 | TAKARA HOLDINGS INC. | Consumer Goods | CN |

| 42 | S-2801 | KIKKOMAN CORP. | Consumer Goods | CN |

| 43 | S-2802 | AJINOMOTO CO., INC. | Consumer Goods | CN |

| 44 | S-2871 | NICHIREI CORP. | Consumer Goods | CN |

| 45 | S-8233 | TAKASHIMAYA CO., LTD. | Consumer Goods | CN |

| 46 | S-8252 | MARUI GROUP CO., LTD. | Consumer Goods | CN |

| 47 | S-8267 | AEON CO., LTD. | Consumer Goods | CN |

| 48 | S-9602 | TOHO CO., LTD | Consumer Goods | CN |

| 49 | S-9681 | TOKYO DOME CORP. | Consumer Goods | CN |

| 50 | S-9735 | SECOM CO., LTD. | Consumer Goods | CN |

| 51 | S-8331 | THE CHIBA BANK, LTD. | Financials | FN |

| 52 | S-8355 | THE SHIZUOKA BANK, LTD. | Financials | FN |

| 53 | S-8253 | CREDIT SAISON CO., LTD. | Financials | FN |

| 54 | S-8601 | DAIWA SECURITIES GROUP INC. | Financials | FN |

| 55 | S-8604 | NOMURA HOLDINGS, INC. | Financials | FN |

| 56 | S-3405 | KURARAY CO., LTD. | Materials | MT |

| 57 | S-3407 | ASAHI KASEI CORP. | Materials | MT |

| 58 | S-4004 | SHOWA DENKO K.K. | Materials | MT |

| 59 | S-4005 | SUMITOMO CHEMICAL CO., LTD. | Materials | MT |

| 60 | S-4021 | NISSAN CHEMICAL IND., LTD. | Materials | MT |

| 61 | S-4042 | TOSOH CORP. | Materials | MT |

| 62 | S-4043 | TOKUYAMA CORP. | Materials | MT |

| 63 | S-4061 | DENKA CO., LTD. | Materials | MT |

| 64 | S-4063 | SHIN-ETSU CHEMICAL CO., LTD. | Materials | MT |

| 65 | S-4183 | MITSUI CHEMICALS, INC. | Materials | MT |

| 66 | S-4208 | UBE INDUSTRIES, LTD. | Materials | MT |

| 67 | S-4272 | NIPPON KAYAKU CO., LTD. | Materials | MT |

| 68 | S-4452 | KAO CORP. | Materials | MT |

| 69 | S-4901 | FUJIFILM HOLDINGS CORP. | Materials | MT |

| 70 | S-4911 | SHISEIDO CO., LTD. | Materials | MT |

| 71 | S-6988 | NITTO DENKO CORP. | Materials | MT |

| 72 | S-5002 | SHOWA SHELL SEKIYU K.K. | Materials | MT |

| 73 | S-5201 | ASAHI GLASS CO., LTD. | Materials | MT |

| 74 | S-5202 | NIPPON SHEET GLASS CO., LTD. | Materials | MT |

| 75 | S-5214 | NIPPON ELECTRIC GLASS CO., LTD. | Materials | MT |

| 76 | S-5232 | SUMITOMO OSAKA CEMENT CO., LTD. | Materials | MT |

| 77 | S-5233 | TAIHEIYO CEMENT CORP. | Materials | MT |

| 78 | S-5301 | TOKAI CARBON CO., LTD. | Materials | MT |

| 79 | S-5332 | TOTO LTD. | Materials | MT |

| 80 | S-5333 | NGK INSULATORS, LTD. | Materials | MT |

| 81 | S-5706 | MITSUI MINING & SMELTING CO. | Materials | MT |

| 82 | S-5707 | TOHO ZINC CO., LTD. | Materials | MT |

| 83 | S-5711 | MITSUBISHI MATERIALS CORP. | Materials | MT |

| 84 | S-5713 | SUMITOMO METAL MINING CO., LTD. | Materials | MT |

| 85 | S-5714 | DOWA HOLDINGS CO., LTD. | Materials | MT |

| 86 | S-5715 | FURUKAWA CO., LTD. | Materials | MT |

| 87 | S-5801 | FURUKAWA ELECTRIC CO., LTD. | Materials | MT |

| 88 | S-5802 | SUMITOMO ELECTRIC IND., LTD. | Materials | MT |

| 89 | S-5803 | FUJIKURA LTD. | Materials | MT |

| 90 | S-5901 | TOYO SEIKAN GROUP HOLDINGS, LTD. | Materials | MT |

| 91 | S-3865 | HOKUETSU KISHU PAPER CO., LTD. | Materials | MT |

| 92 | S-3861 | OJI HOLDINGS CORP. | Materials | MT |