Pareto efficient combinatorial auctions:

dichotomous preferences without quasilinearity††thanks: We thank two anonymous referees and the associate editor for their detailed comments. We are grateful to

Krishnendu Ghosh Dastidar, Tomoya Kazumura, Dilip Mookherjee, Kolagani Paramahamsa, Arunava Sen, Shigehiro Serizawa and seminar participants

at ISI Delhi for useful comments.

Abstract

We consider a combinatorial auction model where preferences of agents over bundles of objects and payments need not be quasilinear.

However, we restrict the preferences of agents to be dichotomous.

An agent with dichotomous preference partitions the set of bundles of objects as acceptable and unacceptable, and at the same

payment level, she is indifferent between bundles in each class but strictly prefers acceptable to unacceptable bundles.

We show that there is no Pareto efficient,

dominant strategy incentive compatible (DSIC), individually rational (IR) mechanism satisfying no subsidy if the domain of preferences

includes all dichotomous preferences.

However, a generalization of the VCG mechanism is Pareto efficient, DSIC, IR and satisfies no subsidy

if the domain of preferences contains only positive income effect dichotomous preferences.

We show tightness of this result: adding any non-dichotomous

preference (satisfying some natural properties) to the domain of quasilinear dichotomous preferences brings back the impossibility result.

JEL Codes: D82, D90

Keywords: combinatorial auctions; non-quasilinear preferences; dichotomous preferences; single-minded bidders

1 Introduction

The Vickrey-Clarke-Groves (VCG) mechanism (Vickrey, 1961; Clarke, 1971; Groves, 1973) occupies a central role in mechanism design theory (specially, with private values). It satisfies two fundamental desiderata: it is dominant strategy incentive compatible (DSIC) and Pareto efficient. We study a model of combinatorial auctions, where multiple objects are sold to agents simultaneously, who may buy any bundle of objects. For such combinatorial auction models, the VCG mechanism and its indirect implementations (like ascending price auctions) have been popular. The VCG mechanism is also individually rational (IR) and satisfies no subsidy (i.e., does not subsidize any agent) in these models.

Unfortunately, these desirable properties of the VCG mechanism critically rely on the fact that agents have quasilinear preferences. While analytically convenient and a good approximation of actual preferences when payments involved are low, quasilinearity is a debatable assumption in practice. For instance, consider an agent participating in a combinatorial auction for spectrum licenses, where agents often borrow from various investors at non-negligible interest rates. Such borrowing naturally leads to a preference which is not quasilinear. Further, income effects are ubiquitous in settings with non-negligible payments. For instance, a bidder in a spectrum auction often needs to invest in telecom infrastrastructure to realize the full value of spectrum. Higher payment in the auction will lead to lower investments in infrastructure, and hence, a lower value for the spectrum.

This has initiated a small literature in mechanism design theory (discussed later in this section and again in Section 4), where the quasilinearity assumption is relaxed to allow any classical preference of the agent over consumption bundles: (bundle of objects, payment) pairs.111 Classical preferences assume mild continuity and monotonicity (in money and bundles of objects) properties of preferences. The main research question addressed in this literature is the following:

In combinatorial auction models, if agents have classical preferences, is it possible to construct a “desirable" mechanism: a mechanism which inherits the DSIC, Pareto efficiency, IR, and no subsidy properties of the VCG mechanism?

1.1 Dichotomous preferences

This paper contributes to this literature, focusing on the particular case in which agents’ preferences belong to a class of preferences, which we call dichotomous. If an agent has a dichotomous preference, she partitions the set of bundles of objects into acceptable and unacceptable. If the payments for all the bundles of objects are the same, then an agent is indifferent between her acceptable bundles of objects; she is also indifferent between unacceptable bundles of objects; but she prefers every acceptable bundle to every unacceptable bundle.

Such preferences, though restrictive, are found in many settings of interest. For instance, consider the recent “incentive auction" done by the US Government (Leyton-Brown et al., 2017). It involved a “reverse auction" phase where the broadcast licenses from existing broadcasters were bought; a “forward auction" phase where buyers bought broadcast licenses; and a clearing phase. The auction resulted in billions of dollars in revenue for US treasury (Leyton-Brown et al., 2017). The theoretical analysis of the reverse auction phase was done by Milgrom and Segal (2020), where they assume quasilinear preferences with “single-minded" bidders, a specific kind of dichotomous preference where the bidder has a unique acceptable bundle (a broadcast band in this case). In these auctions, a broadcaster had some feasible frequency bands in which it can operate. Any of those feasible frequency bands were “acceptable” and it was indifferent between them (since any of these frequencies allowed the broadcaster to realize its full value of broadcast). This resulted in dichotomous preferences of agents.222Quoting Milgrom and Segal (2017), “Milgrom and Segal (2015) (hereafter MS) offer a theoretical analysis which assumes that all bidders are single-station owners who know their station values and are “single-minded”, that is, willing to bid only for a single option. This assumption is reasonable for commercial UHF broadcasters that view VHF bands as ill-suited for their operations and for non-profit broadcasters that are willing to move for compensation to a particular VHF band but that view going off-air as incompatible with their mission.” Milgrom and Segal (2020) argue that the VCG mechanism is computationally challenging in this setting and propose a simpler mechanism.

The assumption of dichotomous preferences seems natural in settings where a bidder is acquiring some resources, and finds any bundle acceptable if it satisfies some requirements. For instance, consider the following examples.

-

•

Consider a scheduling problem, where a certain set of jobs (say, flights at the take-off slots of an airport) need to be scheduled on a server. There are certain intervals where each job is available and can be processed and other intervals are not acceptable. For instance, a supplier bidding to supply to a firm’s production schedule can do so only on some fixed interval of dates. So, certain dates are acceptable to it and others are not acceptable. A traveller is buying tickets between a pair of cities but find certain dates acceptable for travel and realize value only on those dates.

-

•

Consider a seller who is selling land to different buyers. The lands differ in size but are homogeneous otherwise. Each buyer only demands a land of a fixed size. For instance, suppose the Government is allocating land to firms to set up factories in a region, and each firm needs a land of a fixed size to set up its factory. This means all the bundles of land exceeding the size requirement are acceptable to a firm.

-

•

Consider firms (data providers) buying paths on (data) networks (Babaioff et al., 2009) - a firm is interested in sending data from node to node on a directed graph whose edges are up for sale, and as long as a bundle of edges contain a path from to , it is acceptable to the firm.

In all the examples above, if the payment involved are high, we can expect income effects, which will mean that agents do not have quasilinear preferences. One may also consider the dichotomous preference restriction as a behavioural assumption, where the agent does not consider computing values for each of the exponential number of bundles but classifies the bundles as acceptable and unacceptable. Hence, they are easy to elicit even in combinatorial auction setting. Even with quasilinear preferences, the dichotomous restriction poses interesting combinatorial challenges for computing the VCG outcome. This has led to a large literature in computer science for looking at approximately desirable VCG-style mechanisms (Babaioff et al., 2005, 2009; Lehmann et al., 2002; Ledyard, 2007; Milgrom and Segal, 2014). Also related is the literature in matching and social choice theory (models without payments), where dichotomous preferences have been widely studied (Bogomolnaia and Moulin, 2004; Bogomolnaia et al., 2005; Bade, 2015).

1.2 Summary and intuition of results

We show that if the domain of preferences contains all dichotomous classical preferences, there is no desirable mechanism. However, a natural generalization of the VCG mechanism to classical preferences, which we call the generalized VCG (GVCG) mechanism, is desirable if the domain contains only positive income effect dichotomous preferences. In other words, when normal goods are sold, the GVCG mechanism is desirable. Further, the GVCG mechanism is the unique desirable mechanism in any domain of positive income effect dichotomous preferences if it contains the quasilinear dichotomous preferences. The GVCG mechanism allocates the goods in a way such that the collective willingness to pay of all the bidders is maximized. Classical preferences imply that willingness to pay for a bundle of objects depends on the payment level. Thus, it is not clear what the counterpart of “valuation" of a bundle of objects is in this setting. Our generalized VCG is defined by treating the willingness to pay at zero payment as the “valuation" of a bundle and then defining the VCG outcome with respect to these valuations, i.e., the allocation maximizes the sum of agents’ valuations and each agent pays her externality.

The intuition for these results is the following. The GVCG mechanism allocates the goods in a way that maximizes the collective willingness to pay of all the bidders. In fact, with enough richness in the domain, every desirable mechanism must allocate objects like the GVCG mechanism at certain profiles. Individual rationality implies that winning bidders pay an amount less than their willingness to pay. So, winning makes a winning bidder wealthier. With dichotomous preferences, the payments in the GVCG mechanism can be quite low. If bidders have negative income effect, then their willingness to sell (i.e., the compensating amount needed to make a winning bidder lose her bundle of objects) is lower than their willingness to pay. This creates ex-post trading opportunities and the GVCG mechanism is no longer efficient. On the other hand, with positive income effect, the willingness to sell of winning bidders is higher than their willingness to pay and the GVCG mechanism is efficient.

Our positive result is tight: we get back impossibility in any domain containing quasilinear dichotomous preferences and at least one more positive income effect non-dichotomous preference (satisfying some extra reasonable conditions). Such an additional preference may be a unit-demand preference, where the agent is interested in at most one object (Demange and Gale, 1985). To get an intuition for this result, suppose we consider a domain which contains all quasilinear dichotomous preferences and one unit-demand positive income effect preference. We know that the GVCG mechanism may not be strategy-proof in the domain of unit-demand preferences if agents have income effects (Morimoto and Serizawa, 2015). But, we know that in the quasilinear domain with dichotomous preferences, the GVCG mechanism is the unique desirable mechanism. With two agents having positive income effect unit-demand preference and others having quasilinear dichotomous preference, we show that the outcome in a desirable mechanism, if it existed, would still have to be the outcome of the GVCG mechanism. As a result, the agents with positive income effect unit-demand preferences could manipulate at such preference profiles. This negative result not only establishes the tightness of our positive result, but also helps to illuminate the bigger picture of possibility and impossibility domains without quasilinearity.

We briefly connect our results to some relevant results from the literature. A detailed literature survey is given in Section 4. Saitoh and Serizawa (2008) was the first paper to define the generalized VCG mechanism for the single object auction model. They show that the generalized VCG mechanism is desirable in their model even if preferences have negative income effect. This is in contrast to our model, where we get impossibility with negative income effect preferences but the generalized VCG mechanism is desirable with positive income effect.

When we go from single object to multiple object combinatorial auctions, the generalized VCG may fail to be DSIC without quasilinear preferences. For instance, Demange and Gale (1985) consider a combinatorial auction model where multiple heterogenous objects are sold but each agent demands at most one object. In this model, the generalized VCG is no longer DSIC. However, Demange and Gale (1985) propose a different mechanism (based on the idea of market-clearing prices), which is desirable.

When agents can demand more than one object in a combinatorial auction model with multiple heterogeneous objects, Kazumura and Serizawa (2016) show that a desirable mechanism may not exist - this result requires certain richness of the domain of preferences which is violated by our dichotomous preference model. Similarly, Baisa (2020) shows that in the homogeneous objects sale case, if agents demand multiple units, then a desirable mechanism may not exist – he requires slightly different axioms than our desirability axioms.

These results point to a conjecture that when agents demand multiple objects in a combinatorial auction model, a desirable mechanism may not exist. Since ours is a combinatorial auction model where agents can consume multiple objects, an impossibility result might not seem surprising. However, dichotomous preferences are somewhat close to the single object model preference. So, it is not clear which intuition dominates. Our impossibility result with dichotomous preferences complement the earlier impossibility results, showing that the multi-demand intuition goes through if we include all possible dichotomous preferences. However, what is surprising is that we recover the desirability of the generalized VCG mechanism with positive income effect dichotomous preferences. This shows that not all multi-demand combinatorial auction models without quasilinearity are impossibility domains.

2 Preliminaries

Let be the set of agents and be a set of objects. Let be the set of all subsets of . We will refer to elements in as bundles (of objects). A seller (or a planner) is selling/allocating bundles from to agents in using payments. We introduce the notion of classical preferences and type spaces corresponding to them below.

2.1 Classical Preferences

Each agent has preference over possible outcomes, which are pairs of the form , where is a bundle and is the amount paid by the agent. Let denote the set of all outcomes. A preference of agent over is a complete transitive preference relation with strict part denoted by and indifference part denoted by . This formulation of preference is very general and can capture wealth effects. For instance, varying levels of transfers will correspond to varying levels of wealth and this can be captured by our preference over .

We restrict attention to the following class of preferences.

Definition 1

Preference of agent over is classical if it satisfies

-

1.

Monotonicity. for each with and for each with , the following hold: (i) and (ii) .

-

2.

Continuity. for each , the upper contour set and the lower contour set are closed.

-

3.

Finiteness. for each and for each , there exist such that and .

Restricting attention to such classical preferences is standard in mechanism design literature without quasilinearity (Demange and Gale, 1985; Baisa, 2020; Morimoto and Serizawa, 2015). The monotonicity conditions mentioned above are quite natural. The continuity and finiteness are technical conditions needed to ensure nice structure of the indifference vectors. A quasilinear preference is always classical, where indifference vectors are “parallel". Notice that the monotonicity condition requires a free-disposal property: at a fixed payment level, every bundle is weakly preferred to every other bundle which is a subset of it. All our results continue to hold even if we relax this free-disposal property to require that at a fixed payment level, every bundle be weakly preferred to the empty bundle only.

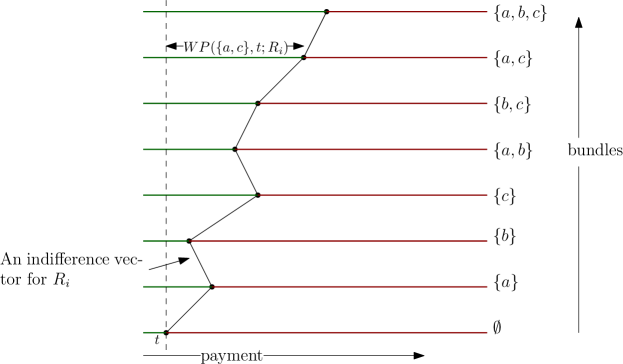

Given a classical preference , the willingness to pay (WP) of agent at for bundle is defined as the unique solution to the following equation:

We denote this solution as . The following fact is immediate from monotonicity, continuity, and finiteness.

Fact 1

For every classical preference , for every and for every , is a unique non-negative real number.

For quasilinear preference, is independent of and represents the valuation for bundle .

Another way to represent a classical preference is by a collection of indifference vectors. Fix a classical preference . Then, by definition, for every and for every , agent with classical preference will be indifferent between the following outcomes:

Figure 1 shows a representation of classical preference for three objects .

The horizontal lines correspond to payment levels for each of the bundles. Hence, these lines are

the set of all outcomes – the space between these eight lines have no meaning and are

kept only for ease of illustration. As we go to the right along any of these lines, the outcomes become worse

since the payment (payment made by the agent) increases. Figure 1 shows eight points, each

corresponding to a unique bundle and a payment level for that bundle. These points are joined

to show that the agent is indifferent between these outcomes for a classical preference. Classical preference

implies that all the points to the left of this indifference vector are better than these outcomes and all the points

to the right of this indifference vector are worse than these outcomes. Indeed, every classical preference can be represented

by a collection of an infinite number of such indifference vectors.

2.2 Domains and mechanisms

A bundle allocation is an ordered sequence of objects , where denotes the bundle allocated to agent , such that for each , we have - note that can be equal to for any in an object allocation. Let denote the set of all bundle allocations.

An outcome profile is a collection of outcomes such that is the bundle allocation and denotes the payment made by agent . An outcome profile is Pareto efficient at , if there does not exist another outcome profile such that

-

1.

for each ,

-

2.

,

with one of the inequalities strictly satisfied. The first relation says that each agent prefers to . The second relation requires that the seller is not spending money to make everyone better off. Without the second relation, we can always improve any outcome profile by subsidizing the agents.333Our efficiency definition says that the agents and the designer cannot improve using an outcome profile, which may involve negative payments. Later, we impose no-subsidy as an axiom for our mechanism. The way to think about this is that Pareto efficient improvements are outside the mechanism and may involve one agent or the designer “buying” a bundle of objects from another agent by compensating (negative payment) her.

A domain or type space is any subset of classical preferences. A typical domain of preferences will be denoted by . A mechanism is a pair , where and is a collection of payment rules with each . Here, is the bundle allocation rule and is the payment rule of agent . We denote the bundle allocated to agent at type profile by in the bundle allocation rule .

We require the following properties from a mechanism, which we term desirable.

Definition 2 (Desirable mechanisms)

A mechanism is desirable if

-

1.

it is dominant strategy incentive compatible (DSIC): for all , for all , and for all , we have

-

2.

it is Pareto efficient: is Pareto efficient at , for all .

-

3.

it is individually rational (IR): for all and for all ,

-

4.

satisfies no subsidy: for all and for all ,

We will explore domains where a desirable mechanism exists. DSIC, Pareto efficiency, and IR are standard constraints in mechanism design. No subsidy is debatable. Our motivation for considering it as desirable stems from the fact that most auction formats in practice and the VCG mechanism satisfy it. It also discourages fake buyers from participating in the mechanism.

2.3 A motivating example

In this section, we provide an example to give some intuition for one of our main results.

Example 1

Consider a setting with three agents , and two objects . We are interested in a preference profile where agents 2 and 3 have identical preference: . In particular, all non-empty bundles have the same willingness to pay according to and satisfy

for . We are silent about the willingness to pay below , but it can be taken to be . We will only consider payments for this example. At preference , we have

for all . Hence, as increases, bundle (or or ) will require more payment to be indifferent to . We term this negative income effect.

Agent has quasilinear preference with a value of for bundle ; value zero (or, arbitrarily close to zero) for bundle and bundle , and value of bundle is normalized to zero. We denote this preference as . The willingness to pay at zero payment for these preferences are shown in Table 1.

Suppose is a desirable mechanism defined on a (rich enough) type space containing the preference profile . Notice that the value of for agent is 3.9 but . Hence, a consequence of Pareto efficiency, individual rationality, and no subsidy is that .444This follows from the following reasoning. Individual rationality and no subsidy imply that agents who are not allocated any object pay zero. Hence, any outcome where agent is given both the objects can be Pareto improved. Then, without loss of generality, agent gets bundle and agent gets bundle due to Pareto efficiency.

Next, we can pin down the payments of agents at . Since agent gets , her payment must be zero by IR and no subsidy. Now, pretend as if agents and have quasilinear preference with valuations equal to their willingness to pay at zero payment (see Table 1). Then, the VCG mechanism would charge them their externalities, which is equal to for both the agents. If the type space is sufficiently rich (in a sense, we make precise later), DSIC will still require that (a precise argument is given in the proof of Theorem 1).

The negative income effect of makes the Pareto improvement possible in this example. The maximum payment we can extract from agent is . Hence, to collect more payment than the VCG outcome, we can pay a maximum of to agents 2 and 3. If the preference was quasilinear, agents 2 and 3 would have required a compensation of each to be indifferent between not getting any objects and the VCG outcome. Due to negative income effect, agents 2 and 3 can be made to improve from their VCG outcome by paying them much lower amounts. This in turn enables us to Pareto dominate the VCG outcome.

To be precise, the following outcome vector Pareto dominates the outcome of the mechanism at :

To see why, note that (a) sum of payments in is ; (b) agent is indifferent between and ; (c) agents 2 and 3 are also indifferent between their outcomes in the mechanism and since (because for all ).

It is important to note that having high value on and (almost) zero value on all other bundles played a crucial role in determining payments of agents, and hence, in the impossibility. Indeed, if agent also had equal willingness to pay on some smaller bundle, then the example will not work.555 If the willingness to pay of agent is on or , then her preference will satisfy the unit demand property (for a formal definition, see Section 3.3). Preference also satisfies the unit demand property. It is known that if agents have unit demand preferences, a desirable mechanism exists, even if such preferences have negative income effect (Demange and Gale, 1985). This motivates the class of preferences we study in the next section.

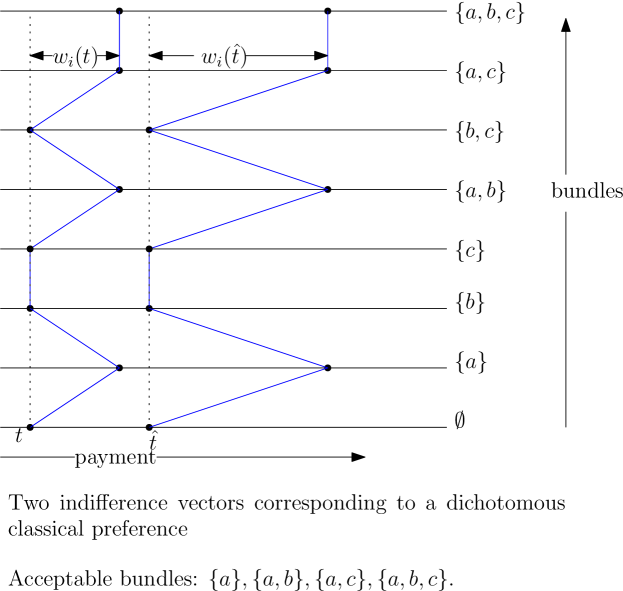

2.4 Dichotomous preferences

We turn our focus on a subset of classical preferences which we call dichotomous. The dichotomous preferences can be described by: (a) a collection of bundles, which we call the acceptable bundles, and (b) a willingness to pay function, which only depends on the payment level. Formally, it is defined as follows.

Definition 3

A classical preference of agent is dichotomous if there exists a non-empty set of bundles and a willingness to pay (WP) map such that for every ,

In this case, we refer to as the collection of acceptable bundles.

The interpretation of the dichotomous preference is that, given same price (payment) for all the bundles, the agent is indifferent between the bundles in . Similarly, she is indifferent between the bundles in , but it strictly prefers a bundle in to a bundle outside it. Hence, a dichotomous preference can be succinctly represented by a pair , where is a WP map and is the set of acceptable bundles.

By our monotonicity requirement (free-disposal) of classical preference, for every , we have

Hence, a dichotomous preference can be described by and a minimal set of bundles such that

Figure 2

shows two indifference vectors of a dichotomous preference. The figure shows that

the bundles and are acceptable but others are not.

We will denote the domain of all dichotomous preferences as , where each preference in for agent is described by a map and a collection of minimal bundles . A dichotomous domain is any subset of dichotomous preferences.

For some of our results, we will need a particular type of dichotomous preference.

Definition 4

A dichotmous preference is called a single-minded preference if .

An agent having a single-minded dichotomous preference has a unique bundle of objects and all its supersets as acceptable bundles. Let denote the set of all single-minded preferences. Single-minded preferences are well-studied in the algorithmic game theory literature (Lehmann et al., 2002; Babaioff et al., 2005, 2009). They were also central in the recent analysis of US incentive auction (Milgrom and Segal, 2020). Our main negative result will be for domains containing . Establishing a negative result on domains containing implies a negative result on domains containing since .

Before concluding this section, we briefly discuss how dichotomous preferences are similar to some other kinds of preferences in the literature. In the single object model, the preferences are clearly dichotomous, where there is no uncertainty about the acceptable bundles. Similarly, consider the unit demand preferences studied in Demange and Gale (1985); Morimoto and Serizawa (2015). A preference is a unit demand preference if for every and every , we have . Now, suppose the objects are homogeneous in the following sense: for all and for all . It is clear that a unit demand preference over homogeneous objects is a dichotomous preference, where consists of singleton bundles. If the objects are not homogeneous, the unit demand preferences are not dichotmous since the willingness to pay of different objects may be different.

3 The results

We describe our main results in this section.

3.1 An impossibility result

We start with our main negative result: if the domain consists of all single-minded preferences, then there is no desirable mechanism. This generalizes the intuition we demonstrated in the example in Section 2.3.

Theorem 1 (Impossibility)

Suppose (i.e., the domain contains all single-minded preferences), , and . Then, no desirable mechanism exists in .

The proof of this theorem and all other proofs are relegated to an appendix at the end. The proof formalizes the sketch given in the example in Section 2.3. The main idea of the proof is that if a desirable mechanism exists in , it has to define outcomes at all single-minded preference profiles, which includes an -agent and -object version of the preference profile discussed in Section 2.3. The challenge is to show that any desirable mechanism at that profile must coincide with the outcome of a generalized VCG mechanism (where agents pay their “externalities"). Once this is shown, the rest of the proof is similar to the discussion in Section 2.3.

As discussed in the introduction, Theorem 1 adds to a small list of papers that have established such negative results in other combinatorial auction problems. Notice that the domain may contain preferences that are not dichotomous or it may be equal to , the set of all dichotomous preferences.

The conditions and are both necessary: if , we know that a desirable mechanism exists (Saitoh and Serizawa, 2008); if , the mechanism that we propose next is desirable – see Proposition 1 and discussions after it.

Definition 5

The generalized Vickrey-Clarke-Groves mechanism with loser’s payment (GVCG-), denoted as , is defined as follows: for every profile of preferences ,

We refer to the GVCG- mechanism as the GVCG mechanism.

The GVCG class of mechanisms is a natural generalization of the VCG mechanism to our setting without quasilinearity. Note that the current definition does not use anything about dichotomous preferences. It computes the “externality” of every agent with respect to a reference transfer level . This transfer level corresponds to the payment by any agent who does not win any non-empty bundle of objects in the mechanism (such an agent has zero externality). The additional term in the payment expression ensures that when we use as the reference transfer level to compute externalities, we maintain incentive compatibility in the dichotomous domain. In the quasilinear domain, the reference transfer level does not matter as the willingness to pay does not change with reference transfer: for each , if is a quasilinear preference.

Theorem 1 implies that the GVCG mechanism is not desirable. Indeed, no GVCG mechanism can be DSIC in an arbitrary combinatorial auction domain without quasilinearity. For instance, Morimoto and Serizawa (2015) show that there is a unique desirable mechanism in the domain of “unit-demand" (where agents have demand for at most one object) preferences, and it is not a GVCG mechanism. We show that the GVCG mechanism is DSIC, individually rational, and satisfies no subsidy in any dichotomous preference domain.

Proposition 1

Consider the GVCG- mechanism for some , defined on an arbitrary dichotomous domain . Then, the following are true.

-

1.

The GVCG- mechanism is DSIC.

-

2.

The GVCG- mechanism is individually rational if .

-

3.

The GVCG- mechanism satisfies individual rationality and no subsidy if .

-

4.

The GVCG- mechanism is Pareto efficient if .

-

5.

The GVCG- mechanism is not Pareto efficient if , and .

We explain below why the GVCG class of mechanisms are compatible with Pareto efficiency when but

not compatible when . For simplicity, we assume that preferences of agents are single-minded, i.e., the domain

is . We consider various cases.

One object (). It is well known that the GVCG mechanism is Pareto efficient if (Saitoh and

Serizawa, 2008).

Note that for , every preference is single-minded.

The GVCG mechanism allocates the object

to an agent with the highest WP at , i.e., . All agents except agent

pay zero and agent pays . This outcome is always Pareto efficient. The main reason for this is

that there is only one object, and any new outcome can only give this object to one agent (may be the same or another agent).

Take any such outcome and assume for contradiction that it Pareto dominates the GVCG outcome.

If agent continues to get the object in also, her payment cannot be more than .

Further, payments of other agents cannot be more than zero. As a result, total payment cannot be more than .

Similarly, if any other agent receives the object in , then her payment cannot be more than (else,

she will prefer the GVCG outcome of getting nothing and paying zero). Further, in this case, since agent does not receive the object

in , her payment will be non-positive. As a result, the total payment cannot be more than .

In fact, the total payment in in both the cases will be strictly less than the GVCG

payments if any agent strictly improves, which is a contradiction.

Two agents () but arbitrary . Since preferences of agents are

single-minded, at every preference profile the acceptable bundles of each agent are supersets of some . Since

there are two agents, we have only two cases to consider: (i)

and (ii) . Intuitively, in the first case, the two agents are not competing against each other.

Pareto efficiency requires us to allocate each agent her acceptable bundle . The GVCG mechanism charges zero payment to the agents. Clearly, this cannot be Pareto dominated.

In the second case, the two agents compete against each other like the single object case. This is because means

exactly one agent can be assigned an acceptable bundle. In fact the allocation and payment in the GVCG mechanism for this case

mirrors the single object case: the agent with the

higher WP at gets her acceptable bundle and pays the willingness to pay of the other agent.

The fact that this outcome cannot be Pareto dominated follows an argument similar to the case.

Summarizing, if there are two agents, independent

of the number of objects, the Pareto efficiency requirement is very similar to the single object case. Hence, the GVCG mechanism remains compatible

with Pareto efficiency.

More than two agents and more than one object (). With more than two agents and more than one object, the Pareto efficiency requirement is no longer like the single object case. To understand, let us consider Example 1 (see Table 1). The GVCG mechanism allocates objects and to agents and but charges them low payments ( each). This is akin to low payments in the VCG mechanism as documented in Ausubel and Milgrom (2006).666They point out that when there are at least two objects and at least three agents, the VCG mechanism outcome may not lie in the “core” of the associated game if objects are complements. This in turn results in low payments. The dichotomous preferences exhibit extreme form of complementarity. In our example, even though agent is not allocated any object, she has high enough willingness to pay for the bundle of objects – with one object, if the payment of the winning agent is low, then the willingness to pay of all losing agents is also low. With negative income effect, agents and feel “wealthier" after getting the objects at low payments. So, their “willingness to sell" amount is low. Hence, it is easier to compensate them. With agent having a high enough willingness to pay (), a Pareto improving trade is thus possible. Such a Pareto improving trade is not possible if agents and have positive income effect preferences. This is because with positive income effect, the “willingness to sell" amount is higher than the willingness to pay.

3.2 Positive income effect and possibility

Proposition 1 and Theorem 1 point out that the GVCG is not Pareto efficient in the entire dichotomous domain. A closer look at the proof of Theorem 1 (and Example 1) reveals that the impossibility is driven by a particular kind of dichotomous preferences: the ones where the willingness to pay of an agent increases with payment. We term such preferences negative income effect.

A standard definition of positive income effect will say that as income rises, a preferred bundle becomes “more preferred". We do not model income explicitly, but our preferences implicitly account for income. So, if payment decreases from to , the income level of the agent increases implicitly. As a result, she is willing to pay more for his acceptable bundles at than at . Thus, positive income effect captures a reasonable (and standard) restriction on preferences of the agents.

Definition 6

A dichotomous preference satisfies positive income effect if for all , we have

A dichotomous domain of preferences satisfies positive income effect if every preference in satisfies positive income effect.

As an illustration, the indifference vectors shown in Figure 2 cannot be part of a dichotomous preference satisfying positive income effect – we see that but . The preference in Example 1 also violated positive income effect. A quasilinear preference (where for all ) always satisfies positive income effect, and the GVCG mechanism is known to be a desirable mechanism in this domain. We show below that the GVCG mechanism is Pareto efficient if the domain contains preferences that satisfy positive income effect. Before stating the result, let us reconsider Example 1 and see why the GVCG mechanism becomes desirable with positive income effect.

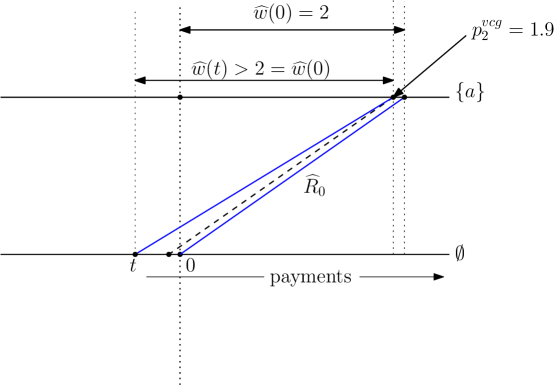

Example 2

We revisit Example 1 but with an important difference: the preferences of agents 2 and 3 now satisfy positive income effect. So, we have three agents and two objects . As in Example 1, agent has single-minded quasilinear preference with valuation on the unique acceptable bundle . All the bundles are acceptable bundles for agents 2 and 3. But their preference is now which satisfies positive income effect. However, similar to Example 1, we have . Figure 3 shows two indifference vectors of . Since satisfies positive income effect, we have , where .

The GVCG outcome does not change from Example 1 at this profile: agent gets object and agent gets object with payments . To Pareto dominate this outcome, we need to give both the objects to agent .

Now, the GVCG outcome to agent is and, by Table 2 (see Figure 3 also), . If , then by positive income effect . A pictorial description of the indifference vectors of for these transfer amounts are shown in Figure 3. This means that if agent is not given any object, the total compensation required for her alone will be more than . Since agent needs to be compensated too and the total revenue collected in the VCG outcome is , we need to charge more than to agent to Pareto dominate the VCG outcome. This is impossible since the value of agent for both the objects is only .

The intuition in this example generalizes. The main idea is that the GVCG mechanism allocates goods in a way that maximizes the collective willingness to pays (at zero) of the winning bidders. IR implies that the winning bidders pay a price less than their willingness to pay for their winning bundles. Thus, winning essentially makes the bidders feel “wealthier". Positive income effect then implies that their “willingness to sell" after the auction exceeds the willingness to pay before the auction. This rules out any Pareto improving trades777We are grateful to an anonymous referee for this intuition. Baisa and Burkett (2019) give similar intuition in a single object auction model to establish a mapping between non-quasilinear and quasilinear economies..

Our next result says that the impossibility in Theorem 1 is overturned in any domain of dichotomous preferences satisfying positive income effect.

Theorem 2 (Possibility)

The GVCG mechanism is desirable on any dichotomous domain satisfying positive income effect.

Theorem 2 can be interpreted to be a generalization of the well-known result that the VCG mechanism is desirable in the quasilinear domain. Indeed, we know that if the domain of preferences is the set of all quasilinear preferences, then standard revenue equivalence result (which holds in the quasilinear domain) implies that the VCG mechanism is the only desirable mechanism. Though we do not have a revenue equivalence result, we show below a similar uniqueness result of the GVCG mechanism. For this, we first remind ourselves of the definition of a quasilinear preference. A dichotomous preference is quasilinear if for every , we have . We denote by the set of all dichotomous quasilinear preferences. This leads to a characterization of the GVCG mechanism.

Theorem 3 (Uniqueness)

Suppose the domain of preferences is a dichotomous domain satisfying positive income effect and contains . Let be a mechanism defined on . Then, the following statements are equivalent.

-

1.

is a desirable mechanism.

-

2.

is the GVCG mechanism.

3.3 Tightness of results

In this section, we investigate if the positive results in the previous sections continue to hold if the domain includes (positive income effect) non-dichotomous preferences. In particular, we investigate the consequences of adding a non-dichotomous preference satisfying positive income effect and some other reasonable properties (we precisely define them later in the section). Both these conditions are natural properties to impose on preferences. Our results below can be summarized as follows: if we take the set of all quasilinear dichotomous preferences and add any non-dichotomous preference satisfying the above two conditions, then no desirable mechanism can exist in such a type space. As corollaries, we uncover new type spaces where no desirable mechanism can exist with non-quasilinear preferences, and establish the role of dichotomous preferences in such type spaces. Before we formally state the result, we give an example to show why we should expect such an impossibility result.

Example 3

We consider an example with two object and three agents . We will require the following preferences of the agents. The preference of agent is quasilinear and the corresponding values for bundles of objects is shown in Table 3. It is clear that is a single-minded preference. We have two preferences of agent : and . Preference is not quasilinear, but it satisfies positive income effect (decreasing prices by the same amount of two indifferent consumption bundles lead the agents to strictly prefer the costlier object): and . This is shown in Figure 4, where we show some indifference vectors of . Note that the other indifference vectors of can be constructed such that it satisfies the unit demand property and positive income effect. Preference is a quasilinear single-minded preference with and as acceptable bundles and value . Finally, preference of agent is also .

We argue that the GVCG mechanism containing all quasilinear dichotomous preferences and is not DSIC. So, our domain is . We will look at two preference profiles: and . At the preference profile , agents 2 and 3 should get objects from according to GVCG. Since they have identical preferences, we break the tie by giving object to agent and object to agent : .888 The example can be modified to work if the tie is broken by giving object to agent and object to agent . The payment of agent is .

Now, consider the preference profile . Here, since agent has only and in her acceptable bundle, her GVCG outcome changes: and . In other words, the externality of agent changes from at preference profile to at .

If was a quasilinear preference, then agent would have been indifferent between and . But since satisfies positive income effect (see Figure 4), . This shows that with positive income effect, agent can manipulate in the GVCG mechanism in this domain.

This is a general problem. We formalize this in Theorem 4. We show in the proof of Theorem 4 that any desirable mechanism in such a domain must have the GVCG outcomes at these profiles, and this will lead to manipulation by the agent having positive income effect.

It is crucial that for this manipulation to happen in this example. If , then can be a dichotomous preference (i.e., besides the indifference vector shown in Table 3, we can construct other indifference vectors such that it is a dichotomous preference). We know that the GVCG mechanism is DSIC in such domains. Indeed, in that case, the externality of agent remains unchanged across profiles and . In other words, we have . So, no manipulation is possible by agent across these two preference profiles.999This is true even if this preference does not satisfy positive income effect.

We formalize the intuition in Example 3 now. We consider a preference where an agent can demand multiple heterogeneous objects. We require that at least two objects are heterogeneous in the following sense.

Definition 7

A preference satisfies heterogenous demand if there exists ,

Heterogeneous demand requires that for some pair of objects, the WP at must be different for them. If objects are not the same (i.e., not homogeneous), then we should expect this condition to hold. We can provide an analogous tightness result if objects are homogeneous.101010The result is available on request.

Besides the heterogeneous demand, we will impose two natural conditions on preferences. The first condition is a mild form of substitutability condition.

Definition 8

A preference satisfies strict decreasing marginal WP if for every ,

Strict decreasing marginal WP requires a minimal degree of submodularity: the marginal increase in WP (at ) by adding to is less than adding to . Notice that this substitutability requirement is only for bundles of size two. Hence, larger bundles may exhibit complementarity or substitutability. Because of free disposal, for every , we have

Hence, strict decreasing marginal WP implies that and , i.e., each object is a good in a weak sense (getting an object is preferred to getting nothing at payment ).

We point out that unit demand preferences (studied in (Demange and Gale, 1985; Morimoto and Serizawa, 2015)) satisfy strict decreasing marginal WP. A preference is called a unit demand preference if for every ,

If is a unit demand preference and objects are goods, then it satisfies strict decreasing marginal WP. To see this, call every object a real good if at every . If every object is a real good, then for every , we see that

Besides the strict decreasing marginal WP condition, we will also be requiring strict positive income effect, but only for singleton bundles.

Definition 9

A classical preference satisfies strict positive income effect if for every and for every with , the following holds for every :

This definition of strict positive income effect requires that if two objects are indifferent then decreasing their prices by the same amount makes the higher priced (lower income) object better. This is a generalization of the definition of positive income effect we had introduced for dichotomous preferences in Definition 6, but only restricted to singleton bundles.111111An alternate definition along the lines of Definition 6 using willingness to pay map is also possible. It will require decreasing differences of willingness to pay. Formally, a preference satisfies strict positive income effect if for every and for every , we have implies . This means that for larger bundles, we do not require positive income effect to hold.

We are ready to state the main tightness result with heterogeneous objects.

Theorem 4

Suppose . Let be a heterogeneous demand preference satisfying strict positive income effect and strict decreasing marginal WP. Consider any domain containing . Then, no desirable mechanism exists in .

We make a quick remark about the statement of Theorem 4.

Remark 1. Though Theorem 4 requires , a careful look at its proof reveals that we only need if . If there are only two objects, the impossibility result in Theorem 4 holds with . This was shown in Example 3 also.

The basic idea of the proof of Theorem 4 is similar to Example 3. With more than two object (), we will need at least four agents. The reason is slightly delicate. Notice that in the statement of Theorem 4 is an arbitrary preference. As in Example 3, the proof ensures that three agents compete for two objects, say , out of which two agents have as their preference. With more than two objects, we need a way to ensure that are allocated among these three agents. In the absence of a fourth agent, it is not possible to ensure that the two agents having preference are not assigned objects outside of . A fourth agent having arbitrarily large willingness to pay for the bundle ensures that.

We do not know if the impossibility result holds for or when , but we conjecture that it does not.

Unlike the negative result in Theorem 1, Theorem 4 does not require the existence of negative income effect dichotomous preferences. It requires the domain to contain the set of quasilinear dichotomous preferences and one heterogeneous demand preference satisfying some reasonable conditions. This negative result parallels a result of Kazumura and Serizawa (2016) who show that adding any multi-demand preference to a class of rich unit demand preference gives rise to a similar impossibility. As was explained in Example 3, our proof exploits the fact that any desirable mechanism must coincide with the GVCG mechanism in the positive income effect dichotomous domain, and adding any strictly positive income effect preference to the domain leads to manipulation. In the case of Kazumura and Serizawa (2016), they add an arbitrary multi-demand preference (which may or may not satisfy positive income effect) to a domain of unit demand preferences, where the GVCG mechanism is not desirable. So, neither of the results imply the other and the proof strategies are different.

We now spell out an exact implication of Theorem 4 in a corollary below. Let be the set of all positive income effect dichotomous preferences (note that ) and be the set of all heterogeneous unit demand preferences satisfying positive income effect (as argued earlier, unit demand preferences satisfy strict decreasing marginal WP). Then, the following corollary is immediate from Theorem 4.

Corollary 1

Suppose . Then, no desirable mechanism exists on .

Theorem 3 shows that the GVCG mechanism is the unique desirable mechanism on . Similarly, Demange and Gale (1985) have shown that a desirable mechanism exists in . This mechanism is called the minimum Walrasian equilibrium price mechanism and collapses to the VCG mechanism if preferences are quasilinear. Corollary 1 says that we lose these possibility results if we consider the unions of these two type spaces.

4 Related Literature

The quasilinearity assumption is at the heart of mechanism design literature with payments. Our formulation of classical preferences was studied in the context of single object auction by Saitoh and Serizawa (2008), who proposed the generalized VCG mechanism and axiomatized it for that setting. Other such axiomatizations include Sakai (2008, 2013). As discussed, Demange and Gale (1985) had shown that a mechanism different from the generalized VCG mechanism is desirable when multiple heterogeneous objects are sold to agents with unit demand. Characterizations of this mechanism have been given in Morimoto and Serizawa (2015), Zhou and Serizawa (2018) and Kazumura et al. (2020b). However, impossibility results for the existence of a desirable mechanism were shown (a) by Kazumura and Serizawa (2016) for multi-object auctions with multi-demand agents and (b) by Baisa (2020) for multiple homogeneous object model with multi-demand agents. Social choice problems with payments are studied with particular form of non-quasilinear preferences in Ma et al. (2016, 2018). These papers establish dictatorship results in this setting with non-quasilinear preferences.

Baisa (2016) considers non-quasilinear preferences with randomization in a single object auction environment. He proposes a randomized mechanism and establishes strategic properties of this mechanism. Dastidar (2015) considers a model where agents have same utility function but models income explicitly to allow for different incomes. He considers equilibria of standard auctions. Samuelson and Noldeke (2018) discuss an implementation duality without quasilinear preferences and apply it to matching and adverse selection problems. Kazumura et al. (2020a) discuss monotonicity based characterization of DSIC mechanisms in domains which admit non-quasilinear preferences. Baisa and Burkett (2019) discuss a model of single object allocation when bidders have interdependent values and non-quasilinear preferences with positive income effects. They give necessary and sufficient conditions for the existence of an ex-post implementable and Pareto efficient mechanism in two settings: (i) where the auctioneer is the seller; and (ii) the procurement setting, where the auctioneer is the buyer. In the former setting, their condition requires existence of an ex-post implementable and Pareto efficient mechanism in a corresponding quasilinear economy. In the latter setting, they show an impossibility result if the level of interdependence is strong.

The literature on auction design with budget constrained bidders models budget constraint such that if an agent has to pay more than budget, then his utility is minus infinity. This introduces non-quasilinear utility functions but it does not fit our model because of the hard budget constraint. For the multi-unit auction with such budget-constrained agents, Lavi and May (2012) establish that no desirable mechanism can exist – see an extension of this result in Dobzinski et al. (2012). They prove this result by considering two bidders each with publicly known budgets and two units. Their result shows an impossibility similar to ours as long as the public budgets of the bidders are not equal. Their paper also allows complementary preferences but not of the extreme form seen with dichotomous preferences.

For combinatorial auctions with single-minded and quasilinear preferences, Le (2018) shows that these impossibilities with budget-constrained agents can be overcome in a generic sense – he defines a “truncated" VCG mechanism and shows that it is desirable almost everywhere.

There is a literature in algorithmic mechanism design on combinatorial auctions with quasilinear but “single-minded" preferences. Apart from practical significance, the problem is of interest because computing a VCG outcome is computationally challenging but various “approximately" desirable mechanisms which are computationally tractable can be constructed (Babaioff et al., 2005, 2009; Lehmann et al., 2002; Milgrom and Segal, 2020). Rastegari et al. (2011) show that in this model, the revenue from the VCG mechanism (and any DSIC mechanism) may not satisfy monotonicity, i.e., adding an agent may decrease revenue. Our paper adds to this literature by illustrating the implications of non-quasilinear preferences.

Appendix A Proofs

A.1 Proof of Theorem 1

The proof extends the intuition in Example 1.

Proof: We start by providing two useful lemmas.

Lemma 1

Suppose is an individually rational mechanism satisfying no subsidy. Then for every agent and every , we have if .

Proof: Suppose is a profile such that for agent . By individual rationality, . But implies that . Hence, . But no subsidy implies that .

Lemma 2

Suppose is an individually rational mechanism satisfying no subsidy. Then for every agent and every , we have

Proof: If , then the claim follows from Lemma 1. Suppose . By individual rationality, . This implies that . No subsidy implies that .

Consider any three non-empty bundles such that and . Consider a profile of single-minded preferences as follows. Since all the agents have dichotomous preferences, to describe any agent ’s preference, we describe the minimal acceptable bundles (i.e., the set of acceptable bundles are derived by taking supersets of each element in ) and the willingness to pay map . Preference of agent is quasilinear:

Preference of agent is:

Preference of agent is:

Preference of each agent is quasilinear:

where but very close to zero.

Assume for contradiction that there exists a DSIC, Pareto efficient, individually rational

mechanism satisfying no subsidy.

We now do the proof in several steps.

Step 1. In this step, we show that at every preference profile with for all , we must have if . We know that for all . Assume for contradiction for some . Then, . By Lemma 1, . Consider the following outcome:

Since preferences of agent and agent are quasilinear (note that and ) and is very close to zero, we have

Also, the sum of payments in the outcome vector is

This contradicts Pareto efficiency of .

Step 2. Fix a preference of agent 2 such that and . We show that at preference profile , . Suppose . Then, and . By Lemma 1, . Consider a new outcome vector:

By quasilinearity of , we get . By definition,

Similarly, . Further, the sum of payments in the outcome vector is

where the inequality used the fact that and .

This contradicts Pareto efficiency of .

Step 3. Fix any quasilinear preference of agent such that and , where . We show that at preference profile , we must have . If not, then by Step 1 and by Pareto efficiency, and . Now, consider the following outcome :

Note that by Lemma 1, . Hence, using quasilinearity of , we get . Similarly, by quasilinearity of , we get . Also, the sum of payments in outcome is

where we used the fact that .

We now prove that . For this, let . Note that follows from the definition of and the fact that by Lemma 2. This implies i.e.

Hence, we get a contradiction to Pareto efficiency.

Step 4. In this step, we show that at preference profile ,

and

Since in preference , by Step 2, . By Step 1, for all . By Pareto efficiency, it must be

Now, assume for contradiction . Fix a preference of agent 2 such that and . By Step 2, . By DSIC, . Hence, . This is a contradiction to Lemma 2.

Finally, assume for contradiction . Then, consider any quasilinear preference of agent such that and . By Step 3, and by Lemma 1, . But by reporting , agent gets at a payment less than . By quasilinearity of and the fact that , she prefers this outcome to outcome , which is a contradiction to DSIC.

This concludes the proof that . A similar argument establishes (with Steps 2 and 3 applied to agent 3)

that .

Step 5. We now complete the proof. By Step 4, we know that the outcome at preference profile satisfies:

Note that by Lemma 1, for all .

Now, consider the following outcome: for all and

Note that sum of payments in is .

Agent is indifferent between and . Agents 2 and 3 are also indifferent between and . This follows from the fact

that

This contradicts Pareto efficiency.

A.2 Proof of Proposition 1

Proof: Fix a dichotomous domain . For some , consider the GVCG- mechanism and denote it as . We prove the following claim first.

Claim 1

For every agent and for every profile of preferences , the following hold:

| (1) | ||||

| (2) |

where is the acceptable set of bundles of agent at .

Proof: The following inequalities follow straightforwardly.

But this implies that

where the second relation comes from the definition of .

Suppose is not an acceptable bundle at , then . Then, the relation (1) implies that . But by construction, . Hence, if .

Using Claim 1, we prove each assertion of the proposition.

Proof of (1). We prove that the GVCG- is DSIC. Fix agent , , and . Let and . We start with a simple lemma.

Lemma 3

If and belong to the acceptable bundle set at , then

Proof: Note that

where the third equality follows from the fact that belong to the acceptable bundle set at and the last inequality follows from the fact that .

Let be the acceptable bundle set of agent according to . We consider two cases.

Case 1. . If , then Lemma 3 implies that

If , then Equation (2) implies that . But, then Inequality (1) implies that

where the first inequality followed from the definition of . This implies that

This further implies that

Hence, in both cases, we see that agent prefers his outcome in the GVCG mechanism to

the outcome obtained by reporting . This concludes the proof that the GVCG- is strategy-proof.

Proofs of (2) and (3). By Inequality (1), for every and for every , we have

. If , we get that , which

is individual rationality. (3) follows from (2).

Proof of (4). We now show that for , the GVCG- mechanism (for any )

is Pareto efficient in any dichotomous domain. Let

and consider a preference profile with and as

the collection of acceptable bundles of agents 1 and 2 respectively. We consider two cases. As before, denote

by .

Case 1. There exists

and such that . Then,

and and .

Denote and .

Assume for contradiction that there is an outcome profile such that

, , and with strict inequality

holding for one of them. By the last two relations, it must be that and with strict

inequality holding whenever these relations are strict, which

means that . But this means since we assumed .

Hence, none of the relations can hold strict, a contradiction.

Case 2. For every and for every , we have . Then, one of the agents in will be assigned an acceptable bundle in . Let this agent be . Hence, and . Further, , where is the willingness to pay of agent at , and .

Denote and assume for contradiction that there is an

outcome profile such that

, , and with strict inequality

holding for one of them. Consider the following two subcases - by our assumption that

for every and for every ,

we have , only the following two subcases may happen.

-

•

Case 2a. Suppose and . Since and , we have and . Hence, we have .

- •

Both the cases imply that with strict inequality holding if

But we are given that or

or . This is a contradiction.

Proof of (5). We show the impossibility for and . The impossibility can be extended easily to the case when and by (i) considering preference profiles where each agent has minimal acceptable bundle set and (ii) every agent has arbitrarily small willingness to pay (at every transfer level) on acceptable bundles. This is similar as in the proof of Theorem 1.

Fix the GVCG- mechanism for some and denote it as . Consider the following single-minded preference profile such that

The WP values at transfer level are as follows:

such that . Further, we require and to satisfy the following:

Such dichotomous preferences are possible to construct. Figure 5 illustrates the some indifference vectors of , and .

Hence, the GVCG- mechanism produces the following outcome:

Consider the following outcome profile

By construction (see Figure 5), each agent is indifferent between and . Total transfers in the outcome profile is: . Total transfers in the GVCG- mechanism: , where the inequality follows since and is arbitrarily close to zero. Hence, the GVCG- mechanism is not Pareto efficient.

A.3 Proof of Theorem 2

Proof: By Proposition 1, the GVCG mechanism is DSIC, individually rational, and satisfies no subsidy. Now, we prove Pareto efficiency. Let be a dichotomous domain satisfying positive income effect. Assume for contradiction that there exists a profile such that is not Pareto efficient. As before, let denote the dichotomous preference of any agent . Let and . Then there exists, an outcome profile which Pareto dominates .

We consider various cases to derive relationship between and for each .

Case 1. Pick such that or . Dichotomous preference implies that . But implies that . Hence, we get

| (3) |

Case 2. Pick such that but . This implies that (by Lemma 1). Hence, Thus,

| (4) |

Case 3. Pick such that but . Since , we can write . But implies that

Also, , where the last inequality is due to individual rationality of the GVCG mechanism. Hence, . But then, positive income effect implies that . This gives us

| (5) |

A.4 Proof of Theorem 3

Proof:

Let be a Pareto efficient, DSIC, IR mechanism satisfying no subsidy.

The proof proceeds in two steps. We assume without loss of generality that

at every preference profile , if an agent is assigned an acceptable

bundle , then is a minimal acceptable bundle at , i.e., there

does not exist another acceptable bundle at . 121212This is without loss of

generality for the following reason. For every Pareto efficient, DSIC, IR mechanism satisfying

no subsidy, we can construct another mechanism such that: for all and for all ,

and is a minimal acceptable bundle at whenever is an acceptable bundle

at and otherwise. Further, . It is routine to verify that

is DSIC, IR, Pareto efficient and satisfies no subsidy. Finally, by construction, if is a generalized VCG mechanism, then

is also a generalized VCG mechanism. We now proceed with the proof in two Steps.

Allocation is GVCG allocation. In this step, we argue that must satisfy:

Assume for contradiction that for some , we have

Before proceeding with the rest of the proof, we fix a generalized VCG mechanism and introduce a notation. For every , denote by

We now construct a sequence of preference profiles, starting with preference profile , as follows.

Let . Also, we will maintain a sequence of subsets of agents, which is initialized as .

We will denote the preference profile constructed in step of the sequence as and the

willingness to pay map at preference as for each .

-

S1.

If , then stop. Else, go to the next step.

-

S2.

Choose and consider to be a quasilinear dichotomous preference with valuation and a unique minimal acceptable bundle - such a quasilinear preference exists because . Let for all .

-

S3.

Set and . Repeat from Step S1.

Because of finiteness of number of agents, this process will terminate finitely in some steps. We establish some claims about the preference profiles generated in this procedure.

Claim 2

For every , and .

Proof: Fix and assume for contradiction . Since is the unique minimal acceptable bundle at and only assigns a minimal acceptable bundle whenever it assigns acceptable bundles, it must be that is not an acceptable bundle at . Then, by Lemma 1, we get . Since and is an acceptable bundle at , we get

This contradicts DSIC. Finally, if , we must have due to DSIC since acceptable bundle at is and is also an acceptable bundle at .

The next claim establishes a useful inequality.

Claim 3

For every , the following holds:

Proof:

Pick some and suppose the above inequality does not hold. We complete the proof in two steps.

Step 1. In this step, we argue that must be an acceptable bundle for agent at preference . If this is not true, then we must have

where the last inequality follows from our assumption that the claimed inequality does not hold and the last equality

follows from the fact that is an acceptable bundle of agent at . But, then the resulting inequality contradicts

the definition of .

Step 2. We complete the proof in this step. Notice that the payment of agent in is defined as follows.

where the strict inequality followed from our assumption and the last equality follows from the fact both and are acceptable bundles for agent at (Step 1). But, this implies that

This is a contradiction to the fact that . This completes the proof.

We now establish an important claim regarding an inequality satisfied by the sequence of preferences generated.

Claim 4

For every ,

Proof: The inequality holds for by assumption. We now use induction. Suppose the inequality holds for . We show that it holds for . To see this, denote . By Claim 2, we know that . Further, by definition, belongs to the acceptable bundle of at and . Now, observe the following:

| (using the fact that for all ) | |||

We now complete our claim that the allocation is the same as in a GVCG mechanism. Let . Let and . Partition the set of agents as follows.

Now, consider the following consumption bundle :

Notice that for each , we have . For each , we know that - this implies that is not an acceptable bundle at . Hence, for all , we have , where the last relation follows from Lemma 1. Finally, for all , implies that . Then, for every , either we have or we have (i.e., is a quasilinear preference). In the first case, implies

In the second case, quasilinearity of implies . This completes the argument that for every .

Now, observe the sum of payments across all agents in is:

| (since is not acceptable, Lemma 1 implies for all ) | ||

where the last inequality follows from Claim 4.

Hence, Pareto dominates the outcome , contradicting Pareto efficiency. We now proceed to the next step

to show that the payment in must also coincide with the generalized VCG outcome.

Payment is GVCG payment. Fix a preference profile . We now know that

By Lemma 1, for every , if is not acceptable

for agent , then - here, we assume, without loss of generality,

that for all .131313Depending on how we break ties

for choosing a maximum in the maximization of sum of willingness to pay, we have a different generalized

VCG mechanism. This assumption ensures that we pick the generalized VCG mechanism

that breaks the ties the same way as . We now consider two cases.

Case 1. Assume for contradiction that there exists such that is an acceptable bundle of agent and

| (6) |

Now consider with the set of acceptable bundles the same in and but but arbitrarily close to . Let . We argue that is an acceptable bundle (at ). If not, then

where we used the fact that is not an acceptable bundle for . But then, by construction of and Inequality (6), we get

which is a contradiction to our earlier step that is the same allocation as in the GVCG mechanism.

Hence, is an acceptable bundle at . But, then by DSIC (since

is also an acceptable bundle at and the set of acceptable bundles at and are the same).

Since , we get a contradiction to individual rationality.

Case 2. Assume for contradiction that there exists such that is an acceptable bundle of agent and

Pick such that the set of acceptable bundles at and are the same but . Notice that if is not an acceptable bundle at , then his payment is zero (Lemma 1). In that case, implies that

contradicting DSIC. Hence, is an acceptable bundle at . This implies that is an acceptable bundle at . Since the generalized VCG is DSIC, we get that . But is a contradiction to IR of the generalized VCG. This completes the proof.

A.5 Proof of Theorem 4

Proof: Assume for contradiction that is a desirable mechanism on . By heterogeneous demand, there exist objects and such that . Consider a preference profile as follows:

-

1.

Agent has quasilinear dichotomous preference with and value that satisfies

(7) -

2.

for all .

-

3.

If , agent has quasilinear dichotomous preference with acceptable bundle and value very high. If , agent has quasilinear dichotomous preference with acceptable bundle and value equals to , which is very close to zero.

-

4.

For all , let be a quasilinear dichotomous preference with and value equals to , which is very close to zero.

We begin by a useful claim.

Claim 5

Pick and . Let be a preference profile such that for all . Suppose is such that

| (8) |

Then, the following are true:

-

1.

-

2.

-

3.

and .

Proof:

It is without loss of generality (due to Pareto efficiency) that or for all

who has dichotomous preference. Since is very close to zero, Pareto efficiency implies that (a) if , for all ;

and (b) if , since agent has very high value for , and

for all . Hence, agents and will be

allocated at . Denote and .

Proof of (1) and (2). Assume for contradiction . Pareto efficiency implies that and . Lemma 1 implies that . Then, consider the following outcome:

By definition of willingness to pay, for all . Since agent has quasilinear preferences, she is also indifferent between and . Thus, the difference in total payment between the outcome and the payment in at is

where the inequality follows from Inequality (8). This is a contradiction to Pareto efficiency of . Hence, .

By Pareto efficiency, .

Proof of (3). Now, we show that and . Suppose . Then, and Lemma 1 implies that . We first argue that . To see this, consider a quasilinear dichotomous preference with acceptable bundle and value equal to . Notice that - if , then this is true by Inequality (8) and if , then satisfies by Inequality (7). Since agents and have the same acceptable bundle at but , this implies that (due to Pareto efficiency), and (Lemma 1). By DSIC, This implies that . IR of agent at implies .

Next, consider the following outcome

By definition, for every agent , . The difference between the sum of payments of agents in and at is:

where the first inequality follows from Inequality (8) and the second inequality follows from Inequality (8) if and from Inequality (7) if . This contradicts Pareto efficiency of . A similar proof shows that .

Now, pick any and set in Claim 5. By Inequality (7), Inequality (8)

holds for . As a result, we get that , and .

Hence, without loss of generality, assume that and .141414Since we have assumed , this

may appear to be with loss of generality. However, if we have and , then

we will swap and in the entire argument following this.

We now complete the proof in two steps.

Step 1. We argue that and . Suppose . Then, consider the quasilinear dichotomous preference such that the minimum acceptable bundle of agent is and his value satisfies

| (9) |

Now, note that by IR of agent at , we have

where the strict inequality followed from Inequality (7). Hence, and by Inequality (9). Hence, choosing and , we can apply Claim 5 to conclude that and , . Since is a dichotomous preference with acceptable bundle , Pareto efficiency implies that . By DSIC, . But Inequality (9) gives , and this contradicts individual rationality.

Next, suppose . Then, consider the quasilinear dichotomous preference such that the minimal acceptable bundle of agent is and his value satisfies

| (10) |

Now, consider the preference profile such that and for all . We first argue that . Suppose not, then by Pareto efficiency, . By Pareto efficiency, we have and . By Lemma 1, . We argue that . To see this, consider a profile where for all and is a quasilinear dichotomous preferences with minimum acceptable bundle and value equal to - notice that every agent in has quasilinear preference. As a result, Theorem 3 implies that the outcome of at must coincide with the GVCG mechanism. But implies that and . Then, DSIC implies that (incentive constraint of agent from to ) . By individual rationality of agent at we get, , and combining these we get .

Now, consider the following allocation vector :

By definition of , we get that . Also, since is quasilinear with value , we get For agent , notice that and by the definition of willingness to pay, we get . For , each agent gets the same outcome in and . Finally, the sum of payments of agents , and (payments of other agents remain unchanged) in is

where the strict inequality follows from Inequality (10) and the fact that . This contradicts the fact that is Pareto efficient.

Hence, we must have . By Lemma 1, we have . But since , we get . Hence, . This contradicts DSIC.

An identical argument establishes that .

Step 2. In this step, we show that agent can manipulate at , thus contradicting DSIC and completing the proof. Consider a quasilinear dichotomous preference where the minimum acceptable bundle of agent is (note that ) and his value is . Consider the preference profile where and for all . Notice that if we let , and , Inequality (8) holds, and hence, Claim 5 implies that and but . Hence, Pareto efficiency implies that and . Then, we can mimic the argument in Step 1 to conclude that

Now, by the definition of willingness to pay,

and by our assumption, . By subtracting (which is positive by Inequality (7)) from payments on both sides, and using the fact that satisfies strict positive income effect, we get

Hence, . This contradicts DSIC.

References

- Ausubel and Milgrom (2006) Ausubel, L. and P. Milgrom (2006): “The loverly but lonely Vickrey auction,” in Combinatorial Auctions, ed. by P. Cramton, Y. Shoham, and R. Steinberg, Cambridge, MA: MIT Press, chap. 1, 17–40.

- Babaioff et al. (2005) Babaioff, M., R. Lavi, and E. Pavlov (2005): “Mechanism design for single-value domains,” in AAAI, vol. 5, 241–247.

- Babaioff et al. (2009) ——— (2009): “Single-Value Combinatorial Auctions and Algorithmic Implementation in Undominated Strategies,” J. ACM, 56.

- Bade (2015) Bade, S. (2015): “Multilateral matching under dichotomous preferences,” Working Paper, University of London.

- Baisa (2016) Baisa, B. (2016): “Auction design without quasilinear preferences,” Theoretical Economics, 12, 53–78.

- Baisa (2020) ——— (2020): “Efficient multi-unit auctions for normal goods,” Theoretical Economics, 15, 361–413.

- Baisa and Burkett (2019) Baisa, B. and J. Burkett (2019): “Efficient ex post implementable auctions and English auctions for bidders with non-quasilinear preferences,” Journal of Mathematical Economics, 82, 227–246.

- Bogomolnaia and Moulin (2004) Bogomolnaia, A. and H. Moulin (2004): “Random matching under dichotomous preferences,” Econometrica, 72, 257–279.

- Bogomolnaia et al. (2005) Bogomolnaia, A., H. Moulin, and R. Stong (2005): “Collective choice under dichotomous preferences,” Journal of Economic Theory, 122, 165–184.